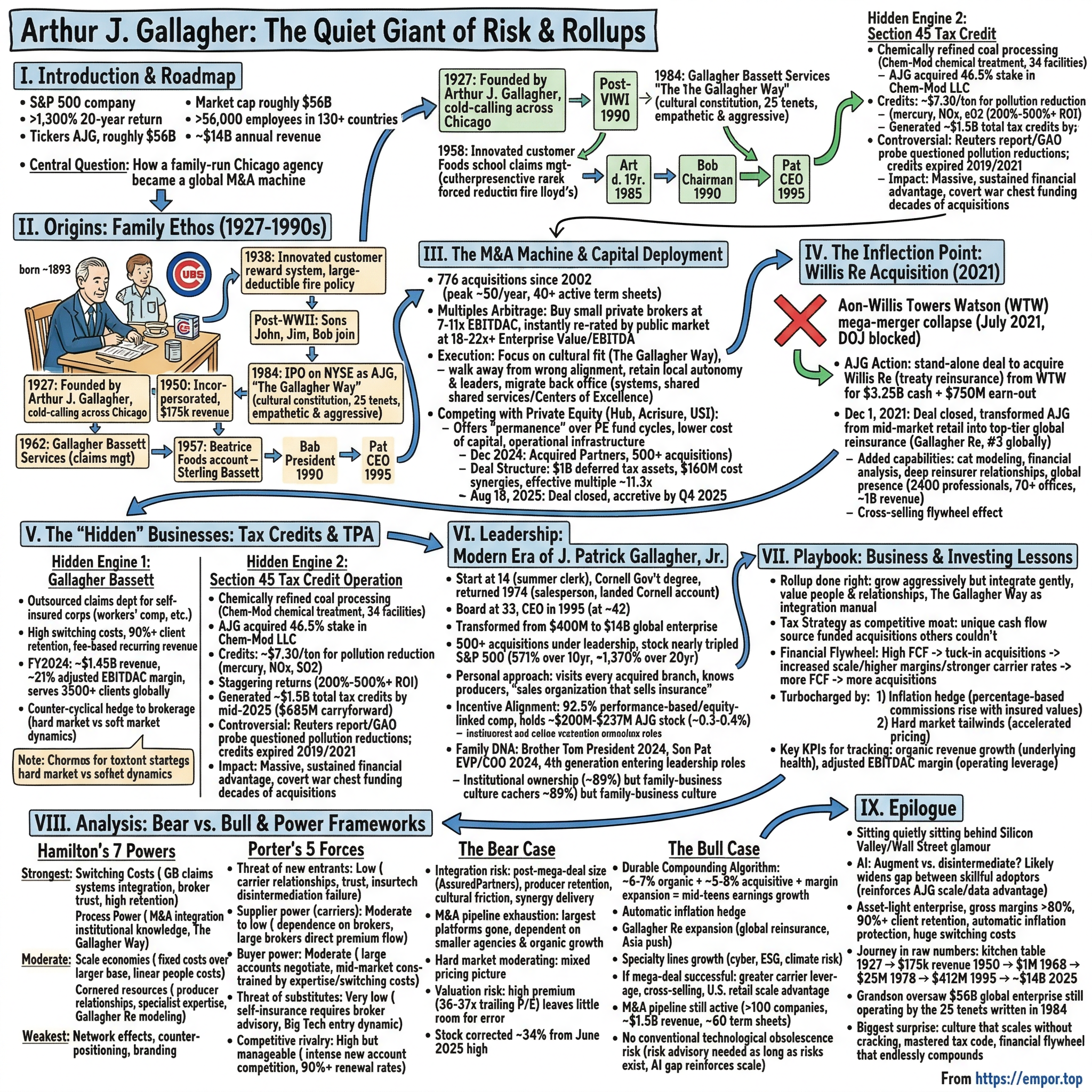

Arthur J. Gallagher: The Quiet Giant of Risk & Rollups

I. Introduction & Episode Roadmap

There is a company in the S&P 500 that has returned over 1,300% in the last twenty years, quietly compounding wealth while almost nobody outside the insurance industry talked about it. It does not make a product you can hold in your hand. It does not have a consumer-facing brand you would recognize at the grocery store. It operates in the decidedly unsexy world of insurance brokerage, and yet its financial track record makes most Silicon Valley darlings look like lottery tickets by comparison.

Arthur J. Gallagher & Co. trades under the ticker AJG on the New York Stock Exchange. As of early 2026, the company commands a market capitalization of roughly fifty-six billion dollars, employs over fifty-six thousand people across more than one hundred thirty countries, and generates nearly fourteen billion dollars in annual revenue. It is the third-largest insurance brokerage on the planet, behind only Marsh McLennan and Aon. And the way it got there is one of the most remarkable stories in modern American business.

The central question is deceptively simple: how did a family-run Chicago insurance agency, founded by the son of Irish immigrants using his kitchen table as an office, transform itself into a global mergers-and-acquisitions machine that absorbs dozens of smaller brokerages every single year, while simultaneously running one of the most lucrative tax credit operations in corporate America?

The answer involves a unique corporate culture written by hand in 1984, a breathtaking arbitrage between private and public market valuations, a controversial foray into chemically refined coal, and one of the most opportunistic acquisitions in recent memory when a thirty-billion-dollar mega-merger between two rivals collapsed at the finish line.

This is not just an insurance story. It is a masterclass in capital allocation, cultural integration, and the quiet power of compounding. The business model underlying insurance brokerage may, in fact, be one of the greatest business models ever invented: asset-light, high-margin, inflation-protected, and blessed with enormous switching costs. Arthur J. Gallagher understood this better than almost anyone and built an empire on that understanding, one tuck-in acquisition at a time.

Before diving in, it helps to understand what an insurance broker actually does, because the simplicity of the model is exactly what makes it so powerful. An insurance broker does not take risk. It does not underwrite policies or pay claims. It sits between the buyer of insurance — a corporation, a municipality, a nonprofit — and the sellers of insurance, the carriers like AIG, Chubb, or Hartford.

The broker advises the client on what coverage it needs, shops that coverage across multiple carriers, negotiates the best terms and pricing, and earns a commission — typically ten to twenty percent of the premium — paid by the carrier. The client does not pay the broker directly. The carrier does, as a distribution cost.

This means the broker earns a percentage of every premium dollar that flows through its hands, year after year, as policies renew. No factories. No inventory. No underwriting losses. Just recurring, percentage-based fees on someone else's risk. It is an extraordinary business model, and the story of how Arthur J. Gallagher exploited its full potential begins in the Irish neighborhoods of Chicago's West Side nearly a century ago.

II. Origins: The Family Ethos (1927–1990s)

Picture Chicago's West Side in the early 1900s. The neighborhood around St. Columbkille Parish is thick with Irish immigrant families, and among them are Jack Gallagher and Mary Fitzpatrick, a schoolteacher whose ancestors had traced a long arc from Virginia to Kentucky to Illinois. Their son, Arthur James Gallagher, was born around 1893 — a gangly, thin, wiry kid with what people described as "big Irish hands." He was an excellent pool player and harbored dreams of signing a professional contract with the Chicago Cubs. His parents had different plans. They sent him to DePaul University to study bookkeeping.

After college, young Art took a job at an insurance firm called Moore Case. It was clerical work — tedious, repetitive — but Gallagher quickly recognized something that would shape his entire career: the real money in insurance came not from processing paperwork, but from selling it.

He struck a deal with his employers. He would complete his clerical duties early in the morning or late in the evening, freeing his days to pound the pavement. He became a relentless cold-caller, ringing doorbells across Chicago, and soon emerged as Moore Case's top producer.

On October 1, 1927, Arthur J. Gallagher walked away from his employer and launched his own independent insurance brokerage. Company lore holds that his first office was his family's kitchen table. He started with two employees and a single carrier relationship with Hartford Accident & Indemnity.

The timing was, on its face, terrible — the stock market crash of 1929 and the Great Depression were just around the corner. But in a counterintuitive twist that foreshadowed the company's future, economic calamity actually elevated demand for risk management and insurance. Banks demanded more collateral protection from borrowers. Businesses that survived the downturn needed to insure their remaining assets more carefully. Gallagher's business grew through the Depression while other enterprises crumbled — an early lesson that insurance brokerage possesses counter-cyclical qualities that would serve the company well across every subsequent economic crisis.

By the late 1930s, Gallagher was innovating in ways that his competitors were not. In 1938, he partnered with The Hartford Group to develop one of the industry's first customer reward systems for loss minimization — essentially incentivizing clients to reduce their own risk, which lowered premiums and strengthened the broker-client relationship simultaneously. He wrote a large-deductible fire policy for a Chicago dairy — a groundbreaking structure at the time that shifted some of the risk back to the client in exchange for significantly lower premiums. These were small moves in a small firm, but they revealed a pattern: Gallagher did not just sell insurance policies. He helped clients think differently about risk itself.

After World War II, the founder's three sons — John, Jim, and Bob — returned from service and joined the family business. The company was formally incorporated in 1950, at which point annual revenues stood at a modest one hundred seventy-five thousand dollars.

Then came the account that changed everything. In 1957, Beatrice Foods Company approached Gallagher with a radical proposal: a self-insurance program covering multiple lines of coverage simultaneously. This was revolutionary for its era — most companies simply bought separate policies for each risk category and hoped for the best. Beatrice wanted a holistic, integrated approach. Winning this account vaulted the firm past competitors, and it directly led to the recruiting of Sterling Bassett, a top claims adjuster whose expertise in managing self-insured programs would become the foundation of an entirely new business line.

The 1960s brought a moment of genuine tragedy that paradoxically created one of Gallagher's most significant innovations. In December 1958, a devastating fire at Our Lady of the Angels school on Chicago's West Side killed ninety-two children and three nuns. The disaster horrified the city and the Gallagher family, who had deep roots in the same West Side Catholic community.

In response, the company developed what became known as the Bishop's Plan for Self-Insurance — a comprehensive risk management program for Catholic dioceses, underwritten through Lloyd's of London. Rather than simply selling policies, Gallagher designed an entire risk management framework: loss prevention programs, safety inspections, centralized claims handling, and coordinated coverage across every diocese that participated. The plan achieved national adoption and dramatically elevated Gallagher's profile beyond the Midwest.

In 1962, Gallagher Bassett Services was formally established to handle claims management for self-insured clients — a pioneering move into third-party administration. Revenue crossed one million dollars for the first time in 1968. International expansion began in 1972 with an office in Bermuda, followed by a Lloyd's broker partnership in London in 1974. By the late 1970s, revenue was growing rapidly — from ten million dollars in 1976 to twenty-five million just two years later, a pace that reflected both organic growth and the increasing sophistication of the firm's service offerings.

Through the 1970s and early 1980s, the company steadily expanded its geographic footprint across the American Midwest and into the Sun Belt, adding offices in cities where commercial real estate, manufacturing, and energy industries were booming. Each new office brought new client relationships, and each new client relationship reinforced the firm's reputation as a broker that thought holistically about risk rather than simply shopping for the cheapest policy.

The pivotal year was 1984. On June 20, Arthur J. Gallagher & Co. conducted its initial public offering and joined the New York Stock Exchange under the ticker AJG. That same year, Bob Gallagher — then chairman and CEO — sat down and wrote, in his own hand, a document that would become the company's cultural constitution: The Gallagher Way.

It contained twenty-five tenets that read less like corporate platitudes and more like the personal philosophy of a man who believed deeply that how you treat people determines how well you do business. "Empathy for the other guy is not a weakness," reads one tenet. "Fear is a turn-off," states another. "We are a warm, close Company. This is a strength — not a weakness," declares a third.

But sandwiched between these humanistic principles was a stark declaration: "We're a very competitive and aggressive Company." That tension — between warmth and aggression, between family values and relentless ambition — is the defining paradox of Arthur J. Gallagher. And it explains, perhaps better than any financial analysis, how a company with a family business ethos could execute the most prolific rollup strategy in insurance history without destroying itself in the process. The Gallagher Way was not just a set of values. It was an integration manual — written before the integration era had even begun.

The founder died on July 22, 1985, at age ninety-two. His Chicago Tribune obituary described him as the chairman of the tenth-largest insurance brokerage in the country, with more than eleven hundred employees across seventy-six U.S. cities. That same year, the company formally launched its acquisition strategy — the engine that would drive the next four decades of growth.

The late 1980s and early 1990s were a period of steady, methodical expansion. The company made its first forays into international markets beyond Bermuda and London, began building specialty practices in niche industries like construction, energy, and public entities, and continued to invest in Gallagher Bassett's claims management infrastructure. Revenue crossed one hundred million dollars. The firm was no longer a scrappy Midwestern agency; it was becoming a national platform with global ambitions.

In 1990, Bob Gallagher was elected Chairman of the Board, and his nephew J. Patrick Gallagher Jr. — the founder's grandson — was named President and Chief Operating Officer. Five years later, upon Bob's death, Pat Gallagher assumed the role of CEO at approximately forty-two years old. The company had revenues of roughly four hundred twelve million dollars and ranked eighth among global brokerages. By 1998, under Pat's early leadership, the firm had climbed to fourth globally — a remarkable ascent driven by both organic growth and the first wave of systematic acquisitions that would soon accelerate into the relentless M&A machine the company is known for today.

III. The M&A Machine & Capital Deployment Masterclass

To understand Arthur J. Gallagher's growth over the past three decades, you need to understand one number: seven hundred seventy-six. That is approximately how many acquisitions the company completed since 2002 alone. Not seven hundred seventy-six over a century. Seven hundred seventy-six in roughly twenty-three years. In peak years, AJG closed more than fifty transactions — approximately one per week. At any given moment, the company typically has forty or more term sheets active simultaneously.

This is not occasional deal-making. This is an industrial-scale acquisition machine, and understanding how it works — and why it works when most rollups eventually collapse — is the key to understanding Arthur J. Gallagher.

The strategy rests on what finance professionals call "multiples arbitrage," but it is easier to think of it as a kind of alchemy. The insurance brokerage industry is extraordinarily fragmented. There are thousands of independent agencies and brokerages scattered across the United States, many of them family-owned businesses with ten to one hundred employees generating anywhere from five to fifty million dollars in annual revenue. These businesses are profitable, well-run, and sticky — their clients renew year after year.

But because they are private, small, and illiquid, they trade at relatively modest valuations when their owners decide to sell. Historically, AJG acquired these firms at seven to eleven times their earnings before interest, taxes, depreciation, amortization, and commissions — a metric the insurance industry calls EBITDAC. The "C" stands for commissions, acknowledging that the primary revenue stream of an insurance broker is commission income.

Here is where the alchemy happens. Once those earnings are absorbed into Arthur J. Gallagher's publicly traded entity, they are instantly re-rated by the public market at a dramatically higher multiple. AJG's stock has historically traded at eighteen to twenty-two times enterprise value to EBITDA — and sometimes considerably higher, approaching thirty-eight times price-to-earnings in recent years.

The spread between what AJG pays for a dollar of earnings and what the market values that same dollar at within the AJG umbrella is enormous. Every dollar of acquired earnings creates two to three dollars of shareholder value before a single synergy is captured. It is, in essence, a legal and repeatable money machine — as long as the acquired businesses perform as expected after integration.

To put this in concrete terms: if AJG acquires a small brokerage generating one hundred million dollars in EBITDAC at ten times that figure, it pays one billion dollars. The market, valuing AJG at twenty times EBITDA, immediately ascribes two billion dollars of value to those same earnings. That is one billion dollars of shareholder value created from the act of closing the deal alone.

Now add in the operational synergies — migrating the acquired firm's back office to AJG's shared services platform, giving it access to AJG's carrier relationships and specialty expertise, eliminating redundant IT and compliance costs — and the returns become even more compelling. AJG has historically generated returns exceeding twenty percent on its acquisition capital, a figure that puts most private equity firms to shame.

But the real genius is not in the math. The real genius is in the execution. Most industry rollups eventually fail because of what practitioners call "integration indigestion" — the acquired companies lose their culture, their best people leave, clients defect, and what looked like a brilliant deal on paper turns into an operational nightmare. The graveyard of failed rollups stretches across industries from funeral homes to veterinary clinics to dental practices.

Arthur J. Gallagher largely avoided this fate, and the reason is The Gallagher Way.

When Pat Gallagher describes his acquisition philosophy, he says something that sounds almost naive: "Let's go out and find people that run really good businesses in our industry and, if we like them, let's try to convince them to sell to us and nobody else." But behind that folksy language is a rigorous and distinctive process. The company reportedly spends the vast majority of its due diligence time not on financial modeling but on cultural fit.

Will the acquired firm's leaders embrace The Gallagher Way? Will they stay and continue running their business? Do they share the same values around client service and ethical behavior? AJG has walked away from financially attractive acquisitions because the cultural alignment was wrong — a discipline that most serial acquirers abandon under the pressure to hit quarterly deal-count targets.

When a deal closes, AJG does not gut the acquired firm with layoffs. The acquired firm's leaders typically stay. They retain significant autonomy over their local operations. Their clients keep dealing with the same people they have always dealt with.

What changes is the back office: technology systems are migrated to AJG's platform, administrative functions are consolidated through global Centers of Excellence in India and other low-cost geographies, and the acquired firm gains access to AJG's vast carrier relationships, specialty expertise, and reinsurance capabilities. The front end stays local and personal. The back end becomes global and efficient.

It is a model that Pat Gallagher personally reinforces by visiting every single acquired branch and meeting with key leaders — a practice he has maintained for decades, even as the company grew to fifty-six thousand employees across one hundred thirty countries. The personal touch is not ceremonial. Gallagher reportedly asks acquired leaders two questions above all others: "Are your clients happy?" and "Are your people staying?" If the answers are yes, the integration is working. If not, he wants to know why immediately.

This combination of cultural discipline and operational efficiency has allowed AJG to maintain remarkably high retention rates among acquired producers — the salespeople who carry client relationships and whose departure would undermine the entire acquisition rationale. The two hundred million dollars in retention awards built into the AssuredPartners integration budget reflects how seriously the company takes this issue at every deal scale.

Throughout the 2010s and into the 2020s, AJG faced an escalating challenge: private equity. Firms like GTCR, KKR, and Hellman & Friedman poured billions into the insurance distribution space, creating PE-backed platforms like Hub International, Acrisure, USI Insurance Services, and AssuredPartners.

These platforms ran their own aggressive acquisition strategies, competing directly with AJG for the same targets and driving entry multiples from the historical eight to ten times range up to twelve to fifteen times. By 2024, PE-sponsored brokers accounted for approximately eighty-seven percent of total brokerage M&A deal volume. The insurance brokerage M&A market had become a feeding frenzy, with over three thousand transactions completed in just five years.

AJG competed by offering something private equity could not: permanence. PE firms operate on fund cycles — they buy, grow, and sell within five to seven years. Agency owners who sold to PE knew that their firm would be flipped again, with all the disruption that entails.

AJG offered a forever home. The pitch was straightforward: sell to Gallagher, and your name may change but your people will stay, your clients will stay, and you will never go through another ownership transition. Combined with its lower cost of capital — investment-grade credit versus PE's leveraged financing — and the genuine operational infrastructure of a sixty-thousand-person global enterprise, AJG remained competitive for the best acquisition targets even as multiples rose across the industry.

And then, in December 2024, AJG made the move that stunned the industry: it announced the acquisition of AssuredPartners for thirteen billion four hundred fifty million dollars in cash. AssuredPartners was itself one of the largest PE-backed insurance distribution platforms in the country, with approximately two billion nine hundred million dollars in annual revenue, ten thousand nine hundred employees across four hundred offices, and a history of completing more than five hundred acquisitions of its own over thirteen years. The seller was GTCR, a Chicago-based private equity firm.

The deal represented, in effect, AJG buying out an entire rival rollup in a single transaction — absorbing the accumulated output of AssuredPartners' thirteen-year acquisition spree in one stroke. It was the largest sale of a U.S. insurance broker to a strategic acquirer in the history of the industry.

The headline multiple was 14.3 times EBITDAC — a number that raised eyebrows given AJG's historically disciplined approach. But a closer look at the deal structure revealed something far more sophisticated. AJG identified approximately one billion dollars in deferred tax assets embedded within AssuredPartners' structure — tax shields that would reduce AJG's future tax obligations as it integrated the business.

Additionally, the company projected one hundred sixty million dollars in expected cost synergies as operations were consolidated. When these adjustments were factored in, the effective acquisition multiple dropped to approximately 11.3 times — well within AJG's historical range and far below the multiple at which AJG's own stock traded.

In one transaction, AJG effectively consolidated an entire rival rollup platform at a price that was immediately ten to twelve percent accretive to earnings. The deal closed on August 18, 2025, after a longer-than-expected regulatory review.

By the fourth quarter of 2025, the combined entity was already showing sixty basis points of EBITDAC margin expansion despite the early-stage integration costs. The integration budget of five hundred million dollars over three years — including two hundred million dollars in non-cash retention awards specifically designed to keep AssuredPartners' key producers — was significant but manageable for a company generating over two billion dollars in annual free cash flow.

AJG was not alone in making this kind of move. Within a twelve-month window, all three of the largest global brokers executed massive mid-market acquisitions: Aon acquired NFP for thirteen billion dollars in April 2024, Marsh McLennan acquired McGriff Insurance Services for seven billion seven hundred fifty million dollars in November 2024, and AJG's AssuredPartners deal followed weeks later.

This synchronized land-grab signaled that the global brokers had collectively concluded that buying PE-built platforms was strategically superior to building their own mid-market presence organically — and that the window to do so was closing as the best platforms were being spoken for. But none of those rival deals matched the financial engineering brilliance of AJG's tax-asset structuring, which effectively bought one of the industry's most aggressive rollup strategies at a meaningful discount to the headline price.

IV. The Inflection Point: The Willis Re Acquisition (2021)

To understand the single most transformative deal in Arthur J. Gallagher's history, you have to start with a deal that never happened — and the spectacular circumstances of its collapse.

In March 2020, Aon plc announced it would acquire Willis Towers Watson in an all-stock transaction valued at approximately thirty billion dollars. Had it closed, the deal would have created the world's largest insurance brokerage, surpassing Marsh McLennan and reshaping the competitive landscape of the industry for a generation. It was the kind of transaction that gets called "transformational" in press releases, and for once, the word would have been accurate.

The U.S. Department of Justice disagreed. In June 2021, the DOJ filed a civil antitrust lawsuit to block the merger, arguing it would eliminate competition in multiple insurance brokerage markets and harm American businesses and consumers. The DOJ's case was aggressive and, crucially, it signaled that even proposed divestitures — Aon and WTW had offered to sell off certain business units to appease regulators — were insufficient to address the competitive concerns.

On July 26, 2021, Aon and WTW abandoned the merger, with Aon paying a one-billion-dollar termination fee. It was a dramatic and unexpected outcome. The two companies had spent over a year planning their integration, relocating staff, and briefing clients on the combined entity. All of it unwound overnight.

Arthur J. Gallagher had been watching this drama with keen strategic interest — and had done far more than watch. Back in May 2021, when the merger still seemed likely to proceed, AJG struck a contingent agreement to acquire Willis Re — the treaty reinsurance brokerage arm of Willis Towers Watson — as part of the divestitures that Aon and WTW had proposed to satisfy antitrust requirements. The original package was priced at approximately three billion five hundred seventy million dollars and included Willis Re along with certain other WTW operations.

When the mega-merger collapsed on July 26, that contingent deal fell apart too — the divestitures were only happening because of the merger, and without the merger, there was nothing to divest.

AJG moved fast. On August 13, 2021 — less than three weeks after the merger collapse — AJG announced a new, standalone agreement to acquire Willis Re's treaty reinsurance brokerage operations directly from WTW. The renegotiated price was three billion two hundred fifty million dollars in cash, plus up to seven hundred fifty million dollars in additional consideration tied to certain third-year revenue targets.

The speed of the renegotiation reflected both AJG's preparedness — it had already done extensive due diligence during the contingent agreement period — and WTW's motivation to monetize a business unit it no longer needed as a standalone entity. The deal closed on December 1, 2021, and it fundamentally altered what Arthur J. Gallagher was.

Before Willis Re, AJG was primarily known as a middle-market retail insurance broker — enormously successful in that segment, but largely absent from the elite world of global treaty reinsurance. To understand why this mattered, consider how the reinsurance market works.

When a hurricane devastates a coastline and an insurance company faces billions in claims, that insurer often does not bear the full cost itself. It has purchased its own insurance — called reinsurance — from specialist firms like Munich Re, Swiss Re, and Hannover Re. The brokers who arrange these complex, high-stakes transactions operate in a rarefied world that demands capabilities far beyond standard commercial insurance placement.

You need advanced catastrophe modeling — sophisticated computer simulations that estimate the probability and severity of natural disasters across every geography on earth. You need dynamic financial analysis — the ability to model how different reinsurance structures affect an insurance company's capital adequacy under various stress scenarios. You need deep relationships with a small number of extremely large reinsurers who deploy billions of dollars in capacity. And you need a global presence, because reinsurance is an inherently international market where a hurricane in Florida generates claims payments flowing from London, Zurich, Munich, and Bermuda simultaneously.

Willis Re brought all of this and more. The acquisition added approximately twenty-four hundred reinsurance broking professionals operating from more than seventy offices across thirty-one countries, with roughly one billion dollars in annualized reinsurance revenue.

Overnight, the newly christened Gallagher Re leaped from fifth to third among global reinsurance brokers, behind only Guy Carpenter (a Marsh McLennan subsidiary) and Aon Reinsurance Solutions. The specialized expertise that came with Willis Re — in catastrophe modeling, aviation risk, cyber reinsurance, mortgage reinsurance, and life reinsurance — gave AJG technical capabilities it had never possessed.

The strategic implications extended far beyond the revenue contribution. These new capabilities opened doors to client relationships that had previously been inaccessible. A large multinational corporation might now use AJG for its primary insurance program and Gallagher Re for its captive reinsurance placement, creating cross-selling opportunities that deepened relationships and dramatically increased switching costs.

An insurance carrier that placed reinsurance through Gallagher Re was also more likely to offer favorable terms when AJG's retail brokers placed primary insurance business with that same carrier. The flywheel effect was powerful and multidirectional.

Before Willis Re, conversations about the "Big Three" global brokers meant Marsh McLennan, Aon, and WTW. After Willis Re — and especially after the subsequent mega-deal discussed earlier — those conversations increasingly included Arthur J. Gallagher. The company graduated from being a very large U.S. broker to being an undeniable global superpower.

AJG's stock roughly doubled in the years following the Willis Re acquisition, as the market recognized the transformative potential of the deal. Gallagher Re expanded aggressively into Asia, opening or strengthening offices in Japan, China, Vietnam, and South Korea — markets where reinsurance demand was growing rapidly due to increasing natural catastrophe exposure and the maturation of local insurance markets.

In 2025 alone, global natural catastrophe losses reached approximately one hundred five billion dollars, driving intense demand for exactly the kind of sophisticated reinsurance solutions that Gallagher Re provided.

The Willis Re acquisition was, in retrospect, one of the great opportunistic deals in modern corporate history. It only became available because of a regulatory intervention that few anticipated. AJG was positioned to act because of the contingent agreement it had already negotiated, and it had the financial capacity and strategic vision to close a multi-billion-dollar deal in a matter of months.

Luck played a role — you cannot plan for a thirty-billion-dollar merger to collapse — but preparation and decisiveness made the luck matter.

The deal also illustrates a broader truth about AJG's strategic opportunism. The company does not initiate industry-shaping events. It does not lobby for regulatory change or engineer competitive disruptions. Instead, it positions itself to move rapidly when others stumble — a doctrine of patient aggression that has served it extraordinarily well across multiple deal cycles. The Willis Re acquisition was the purest expression of that doctrine, and it was this deal, more than any other, that turned the quiet Midwestern rollup into a global reinsurance powerhouse, paving the way for the even bolder move that followed three years later.

V. The "Hidden" Businesses: Tax Credits & Third-Party Administration

Every great company has a business that outsiders overlook. Arthur J. Gallagher has two of them, and together they quietly underwrote the company's growth for decades.

Hidden Engine 1: Gallagher Bassett

When most people think about Arthur J. Gallagher, they think about the brokerage business — the deal-making, the acquisitions, the carrier relationships. What they often overlook is Gallagher Bassett, the company's risk management segment and one of the largest third-party administrators in the United States.

To understand what Gallagher Bassett does, imagine you are the CFO of a large corporation — say, a national restaurant chain with thirty thousand employees across five hundred locations. Workers' compensation claims are a constant reality: slips, burns, strains, and the occasional serious injury.

You could buy a traditional workers' compensation insurance policy from a carrier, paying a premium and letting the carrier handle everything. But you would be paying the carrier's profit margin, its overhead, and its loss reserves — and you would have limited visibility into how claims are actually managed.

The alternative is to self-insure: set aside your own reserves to pay claims directly, saving the carrier's profit margin and gaining granular control over the claims process. But self-insuring means you need someone to actually manage the claims — investigate incidents, negotiate settlements, coordinate medical treatment, manage return-to-work programs, handle litigation, and maintain compliance with state-by-state regulatory requirements.

Building that capability in-house is prohibitively expensive for most companies. You would need adjusters, nurses, attorneys, and compliance specialists — all specialized in workers' compensation — plus the technology infrastructure to manage claims across fifty different state regulatory frameworks.

That is where Gallagher Bassett steps in. It is the outsourced claims department for self-insured corporations.

This might sound like mundane back-office work. But the business characteristics are extraordinary. Once a corporation integrates Gallagher Bassett's claims management systems into its operations — connecting incident reporting workflows, compliance tracking, employee benefits administration, return-to-work protocols, and legal coordination — the cost and disruption of switching to a competitor is enormous.

Every client-specific protocol, every state-specific compliance workflow, every relationship between Gallagher Bassett's adjusters and the client's managers has to be rebuilt from scratch if they switch. Client relationships in the TPA business last for decades. Retention rates regularly exceed ninety percent. The revenue is fee-based and recurring, largely insulated from insurance pricing cycles.

In fiscal year 2024, the risk management segment generated approximately one billion four hundred fifty million dollars in revenue with an adjusted EBITDAC margin of roughly twenty-one percent. Gallagher Bassett handles more than nine billion dollars in claims annually, serves over thirty-five hundred clients globally, and operates through more than one hundred branches. It has won the Business Insurance Buyers Choice Award for Overall Commercial TPA six times.

Perhaps most importantly, Gallagher Bassett provides a natural counter-cyclical hedge to the brokerage business. When insurance prices are high — a "hard market" — brokerage commissions surge, but some corporations respond by self-insuring more aggressively to avoid those elevated premiums, which drives TPA volumes higher. When prices soften in a "soft market," brokerage commissions may decelerate, but fewer companies feel the urgency to self-insure. The two businesses do not move in perfect opposition, but their partial offset provides AJG with more stable earnings across market cycles than a pure-play brokerage would have.

The risk management segment represents roughly thirteen to fourteen percent of total company revenue — not dominant, but significant enough to provide meaningful diversification and a recurring revenue floor that makes the overall business more resilient.

Hidden Engine 2: The Section 45 Tax Credit Operation

And then there is the other hidden business — the one that generated the most extraordinary returns in the company's history, provoked a congressional investigation, attracted scrutiny from Reuters investigative reporters, and provided a covert war chest to fund decades of acquisitions. It is the story of chemically refined coal, and it is one of the strangest chapters in the history of any Fortune 500 company.

Under Section 45 of the Internal Revenue Code, companies that produced "refined coal" — coal treated with chemical additives to reduce emissions of mercury, nitrogen oxides, and sulfur dioxide by specified percentages — could claim a federal tax credit of approximately seven dollars and thirty cents per ton, adjusted for inflation. The provision was created by the American Jobs Creation Act of 2004, ostensibly to incentivize cleaner-burning coal at a time when coal-fired power generation still accounted for a significant share of America's electricity supply.

Arthur J. Gallagher saw an opportunity that had nothing to do with insurance.

The company built or invested in thirty-four refined coal facilities across the United States, strategically locating them adjacent to major coal-burning power plants to maximize throughput. The process itself was remarkably straightforward — almost comically so, given the scale of the financial returns it generated.

Raw coal traveled along a conveyor belt from the power plant's existing coal supply. As it moved along the belt, chemical additives — manufactured by a company called Chem-Mod LLC — were sprayed onto the coal. The chemically treated coal then continued along the belt into the power plant's existing boilers, where it was burned to generate electricity. The facility operator collected tax credits based on the volume of coal processed. There was no separate plant. There was no meaningful change to the power plant's operations. There was, in many cases, just a conveyor belt and a spray system.

To deepen its position, AJG acquired a 46.5 percent controlling stake in Chem-Mod LLC itself, becoming both the operator of the facilities and the supplier of the chemicals used in them. This vertical integration meant AJG was earning returns on both the tax credits and the chemical supply chain — a clever piece of structuring that maximized the economic return from every ton of coal processed.

The financial results were, to use the company's own word, staggering. On a March 2018 earnings call, AJG's Chief Financial Officer Douglas Howell told analysts: "Our return on investment is staggering. Oh, 200 percent, 300 percent, 400 percent, 500 percent."

These were not hypothetical projections. The capital required to build a refined coal facility — essentially a conveyor-belt-mounted spray system — was relatively modest, perhaps a few million dollars per installation. The chemical treatment process was simple. And the tax credits were volume-based, meaning high-throughput facilities near major power plants processing millions of tons of coal per year generated enormous credits relative to the invested capital.

By 2018, AJG had accumulated approximately eight hundred fifty million dollars in tax credits from refined coal activities. The company also recruited outside investors — including Fidelity Investments — into the facilities, earning management fees on top of its own credit generation.

At its peak, refined coal activities accounted for a significant share of AJG's total revenue and earnings. By the time the core credits wound down, the company had generated approximately one billion five hundred million dollars in total tax credits, of which roughly six hundred eighty-five million dollars remained as a carryforward on the balance sheet as of mid-2025.

The strategic impact of this tax windfall cannot be overstated. The credits dramatically reduced AJG's effective tax rate for years, freeing up enormous amounts of cash flow that would otherwise have gone to the IRS. Clean energy investments generated over one hundred eighty million dollars in annual after-tax cash flow in 2025, growing toward two hundred million dollars by 2026.

This cash flowed directly into the acquisition machine, funding tuck-in deals without requiring AJG to issue dilutive equity or take on excessive debt. In a very real sense, the Section 45 tax credits were the hidden fuel propelling AJG's entire M&A strategy — a war chest that competitors in the insurance brokerage industry simply did not possess.

But the program was not without controversy, and the controversy eventually became significant. In December 2018, Reuters published an investigative report that cast serious doubt on whether refined coal was actually achieving the pollution reductions that the tax credits were supposed to incentivize.

An independent study by Resources for the Future — a nonpartisan environmental research organization — found that at twenty-two of fifty-six power plants burning refined coal, nitrogen oxide emission rates had actually risen rather than fallen. The environmental promise of the program appeared to be failing even as the tax benefits continued to flow.

The revelations triggered a political backlash. Senators Sheldon Whitehouse, Elizabeth Warren, and Sherrod Brown called on the Government Accountability Office to investigate. The GAO launched a formal probe. Critics described the Section 45 refined coal credit as a "boondoggle" — a program that cost taxpayers approximately one billion dollars per year across all participants while failing to deliver the environmental benefits that justified its existence.

AJG weathered the controversy without suffering material financial harm. The credits for its "2009 era" plants expired after 2019, and those for its "2011 era" plants expired at the end of 2021. Legislative efforts to extend the program did not advance in Congress.

The company has since explored broader clean energy tax credit opportunities, including Section 45Q credits for carbon capture and sequestration, though these have not yet approached the scale of the refined coal program. Whether one views the Section 45 story as brilliant tax planning or exploitation of a flawed government program depends largely on one's perspective. What is undeniable is that it provided AJG with a massive, sustained financial advantage that its brokerage competitors simply did not have — a hidden engine that powered the M&A machine for years while the rest of the industry barely noticed.

VI. Leadership: The Modern Era of J. Patrick Gallagher, Jr.

He started working in the family business at age fourteen, filing documents as a summer clerk at company headquarters. He went to Cornell University, where he studied government — not business, not finance, not actuarial science — and joined the Psi Upsilon fraternity. He returned to the family firm in 1974 as a production account executive, essentially a salesperson, and one of his early accomplishments was landing the Cornell University insurance account, turning his alma mater into a long-term client. He was elected to the board of directors at age thirty-three.

And in January 1995, at approximately forty-two years old, J. Patrick Gallagher Jr. became the chief executive officer of Arthur J. Gallagher & Co.

Over the next three decades, he transformed the company from a four-hundred-million-dollar Midwestern brokerage into a fourteen-billion-dollar global enterprise. The stock delivered total returns that nearly tripled the S&P 500 over any meaningful time horizon — approximately 571 percent over ten years and over 1,370 percent over twenty years.

Under his leadership, the company completed more than five hundred acquisitions, expanded from thirty-seven hundred employees to over fifty-six thousand, and climbed from eighth to third in the global brokerage rankings. The revenue compounded at a rate that turned every ten thousand dollars invested in AJG stock at the time of his appointment into well over one hundred thousand dollars by 2026.

How does someone manage a conglomerate of that scale while retaining the intimacy and loyalty of a mid-sized family agency? Part of the answer lies in Pat Gallagher's personal approach. He describes the firm not as an insurance brokerage but as "a sales organization that happens to sell insurance."

He personally visits every acquired branch. He knows producers by name. On earnings calls, he speaks with the informality and confidence of a man who genuinely enjoys the business he runs — peppering financial presentations with references to individual client wins, specific producer achievements, and detailed commentary on local market conditions that most CEOs of his stature would delegate to divisional heads.

He has cultivated a reputation for warmth and accessibility that seems impossible given the size of the organization, and yet employee surveys and industry recognition suggest it is genuine. He received a Business Insurance Lifetime Achievement Award in 2022 and was inducted into the Chicago Business Hall of Fame in 2025.

People who have worked with him describe a leader who remembers names, follows up on personal details, and creates an environment where employees feel they are part of something more meaningful than a corporation. In an industry where the largest firms often feel impersonal and bureaucratic, this personal touch is a genuine differentiator — and it starts at the top.

The other part of the answer lies in incentive alignment — and here, the numbers tell a compelling story. Pat Gallagher's total compensation in 2024 was approximately seventeen million four hundred fifty thousand dollars. His base salary was one million three hundred thousand dollars — just 7.5 percent of total compensation.

The remaining 92.5 percent was performance-based and equity-linked: a cash bonus tied to adjusted revenue growth and adjusted EBITDAC growth, stock options that vest over three to five years, and performance stock units tied to three-year adjusted EBITDAC per share growth. In 2024, the compensation committee increased his annual incentive target from 225 percent to 265 percent of salary, and his long-term incentive target from 435 percent to 500 percent of salary. The message embedded in that structure is unambiguous: the CEO's wealth is overwhelmingly determined by whether the company performs for shareholders.

Beyond annual compensation, Pat Gallagher holds approximately nine hundred eight thousand shares of AJG stock, worth roughly two hundred million to two hundred thirty-seven million dollars at recent prices. This represents about 0.3 to 0.4 percent of shares outstanding — a seemingly small percentage for a founding family member, but an enormous absolute dollar amount that ensures the CEO's personal wealth rises and falls with the stock price. He also maintains significant deferred compensation balances totaling over seventy million dollars.

The broader Gallagher family's stake is approximately one percent of shares outstanding. Though this is modest in percentage terms — inevitable after four decades as a public company — the family's continued presence in the top leadership positions provides a cultural anchor that transcends ownership percentages.

Pat's brother, Thomas J. Gallagher, was named President of the company in January 2024. Pat's son, Patrick M. Gallagher, was simultaneously appointed Executive Vice President and Chief Operating Officer. Two additional sons work as producers in the brokerage division. The fourth generation is entering leadership roles, and the succession framework is unmistakably a family affair.

This creates an unusual dynamic for a company of AJG's size. It is overwhelmingly institutionally owned — nearly eighty-nine percent of shares are held by institutional investors including Vanguard, BlackRock, and State Street — and yet it operates with the cultural DNA of a family business. The Gallagher Way still physically sits on the desks of employees across the organization.

Pat Gallagher has been the guardian of this culture for three decades. His most important legacy may not be the financial returns — extraordinary as they are — but the proof that a sixty-thousand-person global enterprise can scale without losing its soul.

The leadership transition that lies ahead is the most important non-financial question the company faces. Whether the next generation can maintain the cultural intensity that Pat has embodied — while simultaneously navigating the largest integration in company history and an increasingly complex competitive landscape — will determine whether AJG's next three decades look like the last three.

VII. Playbook: Business & Investing Lessons

The Arthur J. Gallagher story is rich with lessons that extend far beyond insurance. Three stand out as particularly instructive for anyone thinking about business models, capital allocation, and competitive advantage.

The Rollup Done Right

The word "rollup" carries baggage in investing circles, and for good reason. Most industry consolidation strategies eventually buckle under integration debt — the accumulated cultural friction, operational complexity, and talent attrition that come from absorbing too many companies too quickly. The history of healthcare staffing, dental practices, veterinary clinics, and even funeral homes is littered with rollups that looked brilliant on a spreadsheet and disastrous in execution.

The pattern is depressingly predictable: aggressive acquisition, superficial integration, key talent departure, client defection, margin compression, and eventual value destruction. Anyone who has studied Valeant Pharmaceuticals, Quorum Health, or the serial acquirer playbook of the early 2000s knows the script. The question with every rollup is always the same: at what point does the acquisition pace outrun the organization's ability to integrate?

AJG avoided this fate through an approach that is almost paradoxical: it grows aggressively while integrating gently. The key insight — and this is the single most important takeaway for anyone studying the company — is that in a people-intensive, relationship-driven business like insurance brokerage, the value being acquired is not a product, a patent, or a piece of real estate. The value is the people and their client relationships.

Destroy the culture that keeps those people engaged, and you destroy the asset you just paid for. This sounds obvious. It is not obvious in practice. The gravitational pull of every large acquiring organization is toward standardization, centralization, and control — forces that tend to crush the entrepreneurial culture of acquired firms.

AJG's rigid adherence to The Gallagher Way — its insistence on cultural fit during due diligence, its willingness to let acquired leaders retain autonomy, its centralized-backbone-but-decentralized-frontline operating model — represents a genuine innovation in how rollups can be executed at scale. The lesson is not that all rollups are good or bad, but that the integration methodology is the variable that determines the outcome.

Tax Strategy as a Competitive Moat

The Section 45 clean coal story is frequently dismissed as an accounting curiosity or a regulatory loophole. It was far more consequential than that. By mastering a specific provision of the tax code and investing aggressively in its exploitation, AJG created a source of cash flow that its insurance brokerage competitors simply did not have. That cash flow funded acquisitions that created operating scale, which generated more cash flow, which funded more acquisitions.

The lesson for business strategists is that tax optimization — deployed with the same rigor and creativity that most companies reserve for product development or sales strategy — can be a genuine competitive advantage. The fact that the advantage was ultimately controversial and time-limited does not diminish its impact during the decades it was active. AJG's competitors were playing checkers — focused entirely on the brokerage business. AJG was playing chess, using the tax code as a source of fuel for a strategy that its rivals had no way to replicate.

The Financial Flywheel

Arthur J. Gallagher's business model embodies one of the most powerful flywheels in corporate America. High free cash flow — over two billion four hundred million dollars in fiscal year 2024 — funds tuck-in acquisitions. Those acquisitions increase the company's scale, which commands higher margins through operating leverage and stronger carrier commission rates. The higher margins generate more free cash flow, which funds more acquisitions. And the cycle repeats, year after year, with the consistency of a metronome.

This flywheel is turbocharged by two structural tailwinds that most other industries lack.

First, insurance brokerage commissions are percentage-based, meaning they rise automatically with inflation. Consider a building insured for fifty million dollars at a 0.5 percent rate — the premium is two hundred fifty thousand dollars, and the broker's fifteen percent commission is thirty-seven thousand five hundred dollars. If inflation pushes the building's replacement cost to sixty million dollars, the premium rises to three hundred thousand dollars and the commission to forty-five thousand dollars — a twenty percent revenue increase with zero additional effort.

This mechanism operates across every insured asset class: buildings, equipment, vehicles, payrolls, medical costs. When the world gets more expensive, AJG's revenue grows automatically.

Second, the hard insurance market that prevailed from 2020 through 2024 layered additional pricing tailwinds on top of the inflationary effect, creating a period where AJG's organic growth doubled its historical pace. The combination of organic growth, acquisitive growth, and margin expansion produced mid-teens earnings growth compounding year after year — the kind of consistent, predictable value creation that makes long-term shareholders wealthy.

For anyone tracking this company going forward, two KPIs matter above all else.

First, organic revenue growth: this strips out the effect of acquisitions and currency fluctuations, revealing the underlying health of the business. AJG delivered six percent organic growth for full-year 2025, with quarterly figures ranging from nine percent in the first quarter to about five percent in the third quarter. Any sustained move below four percent would signal that the hard market tailwind has reversed and the organic engine is slowing.

Second, adjusted EBITDAC margin: this measures operating profitability and shows whether the company is achieving operating leverage as it scales. The fourth-quarter 2025 margin of 30.8 percent represented meaningful expansion even while absorbing the substantial integration costs of the mega-deal. These two numbers — organic growth and margin — tell investors whether the flywheel is spinning faster or slower.

VIII. Analysis: Bear vs. Bull & Power Frameworks

Hamilton's 7 Powers

Hamilton Helmer's framework identifies seven sources of durable competitive advantage that allow a business to sustain superior returns over long periods. Applied to Arthur J. Gallagher, the analysis reveals formidable but uneven strategic positioning.

Switching costs represent AJG's strongest power. When a mid-market corporation has embedded Gallagher Bassett's claims management systems into its operations, connected its compliance reporting, integrated employee benefits administration, and built personal trust between its risk managers and their Gallagher broker team over years of collaboration, the cost of switching to a competitor is immense.

The friction is not just financial — it is operational, informational, and personal. The incumbent broker holds years of claims history, loss data, coverage structures, and institutional knowledge about the client's risk profile. A new broker would need months to rebuild that understanding.

Industry data suggests it costs seven to nine times more to acquire a new insurance client than to retain an existing one — the highest acquisition cost asymmetry of any industry. This friction drives retention rates above ninety percent at large brokers and creates a recurring revenue base that is extraordinarily durable.

Process power is AJG's second-strongest competitive advantage. The Gallagher Way is not a marketing slogan; it is a genuine operating system refined through more than seven hundred acquisitions over two decades. The ability to evaluate a target for cultural fit, close a transaction, migrate technology systems, consolidate back-office functions through Centers of Excellence, and retain the acquired firm's producers and client relationships — all while doing this forty to fifty times a year — represents deep institutional knowledge that competitors find extraordinarily difficult to replicate.

Marsh McLennan and Aon are larger, but neither has demonstrated the same volume and consistency of successful tuck-in integrations. This process power compounds over time: each successful integration teaches the organization something that makes the next integration slightly more efficient.

Scale economies matter but are less dominant than in technology businesses. AJG spreads fixed costs — IT infrastructure, compliance systems, InsurTech investments, global analytics platforms — across an expanding base of acquired brokers. The marginal cost of adding a new tuck-in acquisition decreases as the platform grows. But insurance brokerage remains fundamentally a people business, and people costs scale roughly linearly with revenue. The scale advantage is real but moderate compared to, say, a software company where marginal costs approach zero.

Cornered resources are present in the form of talent and institutional expertise. Experienced producers carry deep client relationships that are difficult to replicate — a top producer at AJG might personally manage fifty to one hundred client relationships generating tens of millions of dollars in annual commission revenue, and those relationships are often personal enough that the client would follow the producer if they left. AJG's M&A team represents institutional capital that cannot be hired away in bulk. And the catastrophe modeling and capital modeling capabilities acquired through Willis Re give Gallagher Re technical resources that few competitors possess.

Network effects, counter-positioning, and branding are the weakest powers in AJG's arsenal. Insurance brokerage does not exhibit true network effects where each additional participant makes the platform more valuable for others. AJG's approach is distinctive but does not represent classic counter-positioning where incumbents cannot respond without damaging their existing model. Branding matters for large multinational accounts but is secondary to relationships in the mid-market.

Porter's Five Forces

The insurance brokerage industry is structurally one of the most attractive in financial services, and a Five Forces analysis explains why.

Threat of new entrants: Low. Building carrier relationships takes years. Licensing requirements vary across jurisdictions. Trust-based corporate relationships cannot be replicated quickly. The InsurTech movement's attempt to disintermediate brokers largely failed — poster children like Lemonade, Hippo, and Root either struggled toward profitability or pivoted to using traditional agents after initially trying to bypass them. The surviving insurtechs repositioned as technology enablers for brokers rather than replacements — a validation, not a threat, to the incumbent model.

Supplier power (carriers): Moderate to low. Carriers depend on brokers for distribution, and large brokers like AJG can direct billions in premium toward or away from specific carriers. With hundreds of carriers competing in most lines, no individual carrier has significant leverage over a broker of AJG's scale. The exception is in specialty or distressed lines where carrier capacity becomes scarce, temporarily shifting power to suppliers.

Buyer power: Moderate. Large multinational corporations can run competitive broker reviews and negotiate fee-based arrangements, but mid-market and small-business clients — AJG's traditional sweet spot — lack the expertise to go direct to carriers. Switching costs further constrain buyer power even among the largest accounts.

Threat of substitutes: Very low. Self-insurance is a partial alternative but still requires broker advisory services. The more credible long-term threat is Big Tech entering insurance distribution, but commercial insurance complexity and regulatory barriers provide significant protection for years to come.

Competitive rivalry: High but manageable. Marsh McLennan, Aon, WTW, Brown & Brown, and AJG compete intensely for large accounts, but the market is large enough — roughly one hundred forty billion dollars in the U.S. alone — that all major players grow simultaneously. Ninety-plus percent renewal rates mean most competitive battles occur for new accounts, not the existing book of business.

The net assessment across all five forces is that insurance brokerage is one of the most structurally attractive industries in financial services — which explains why the top brokers consistently generate returns on capital that exceed their cost of capital by wide margins, and why private equity has poured billions into the space over the past decade.

The Bear Case

The most compelling bear argument centers on what happens after the mega-deal. AJG absorbed the largest acquisition in its history, and the integration is still in its early stages. AssuredPartners was built through rapid, PE-style inorganic growth with a decentralized structure. Integrating ten thousand nine hundred employees across four hundred offices into The Gallagher Way is qualitatively different from absorbing a small agency.

Key producer retention, client defection, and cultural friction are all elevated risks. The projected synergies must be delivered; failure would weigh on the stock.

Beyond integration risk, there is the question of M&A pipeline exhaustion. With the largest independent platforms now spoken for — AssuredPartners, NFP, and McGriff all acquired within twelve months — the remaining pipeline consists of smaller agencies. The era of transformative deal-making may be over, leaving AJG dependent on organic growth in an environment where the hard insurance market appears to be moderating.

Property rates declined approximately five percent in 2025 while casualty rates rose about six percent — a mixed picture that could compress organic growth from the six-to-nine percent range toward three to four percent if the pricing cycle turns more broadly.

The valuation carries its own risk. AJG trades at roughly thirty-six to thirty-seven times trailing earnings — a premium that reflects the market's confidence in the compounding algorithm but also leaves little room for execution missteps.

The stock already corrected approximately thirty-four percent from its all-time high of three hundred forty-six dollars reached in June 2025. If growth decelerates further, multiple compression could amplify downside from current levels.

The Bull Case

The bull case rests on the extraordinary durability of the compounding algorithm. AJG delivered roughly seven hundred twenty-seven percent total returns over ten years versus the S&P 500's two hundred sixty percent — nearly three times the benchmark.

The formula — approximately six to seven percent organic growth plus five to eight percent acquisitive growth plus margin expansion — has produced mid-teens earnings growth with remarkable consistency. Sixteen consecutive quarters of double-digit revenue growth speak to an engine that shows no sign of stalling.

The inflation hedge is perhaps the most underappreciated element. Commission-based revenue is percentage-linked to premiums, which are linked to insured values, which are linked to replacement costs. This three-layer compounding means AJG's revenue grows automatically in inflationary environments — with zero additional effort required.

Gallagher Re's expansion into global reinsurance represents a significant and still-maturing growth opportunity. Natural catastrophe losses reached one hundred five billion dollars in 2025, and the geographic push into Asia targets markets where reinsurance penetration is growing rapidly.

Specialty lines — cyber insurance, ESG-linked products, climate risk coverage — are growing at thirty percent or more annually, representing high-margin growth where AJG's specialist teams are well-positioned.

If the mega-deal integration executes successfully, the combined entity will possess significantly more carrier leverage, deeper cross-selling opportunities, and a scale advantage in U.S. retail that few competitors can match. The current M&A pipeline still contains more than one hundred companies representing approximately one billion five hundred million dollars in annualized revenues, with approximately sixty term sheets either signed or in preparation — the tuck-in machine has not stopped.

And there is one final point that the bulls emphasize: insurance brokerage has no technological obsolescence risk in any conventional sense. The product — risk advisory and placement — does not get disrupted the way physical goods or media distribution does. As long as businesses face risks, they will need brokers. And as long as the world grows more complex, litigious, and climate-exposed, the demand for sophisticated risk management will only increase.

IX. Epilogue

The insurance brokerage industry is not the kind of business that inspires breathless magazine covers or viral social media threads. It does not lend itself to dramatic narratives about visionary founders disrupting staid industries with breakthrough technologies. And yet, sitting quietly behind the glamour of Silicon Valley and the spectacle of Wall Street, companies like Arthur J. Gallagher have compounded wealth for shareholders with a consistency that most technology companies can only dream of.

The future holds genuine uncertainties. Artificial intelligence is beginning to reshape insurance underwriting, with AI adoption in the sector expected to jump from fourteen percent to seventy percent within the next few years. The early applications are already visible: commercial property and casualty models with predictive win rates now deliver quotes in one to two hours instead of two to three days, and specialty risk engineering tools generate initial risk assessments in days instead of months.

Whether AI augments the broker's role — making human advisors more productive and their analysis more sophisticated — or ultimately disintermediates them remains an open question. OpenAI's recent moves into insurance distribution have raised eyebrows, though for now the complexity of commercial insurance appears to resist the kind of simple automation that transformed consumer financial services. The more likely near-term outcome is that AI widens the gap between brokers who adopt it skillfully and those who do not — which, given AJG's scale and data advantages, could actually reinforce rather than erode its competitive position.

The sunsetting of Section 45 clean coal credits removes a significant, if controversial, financial advantage, though the remaining carryforward balance of roughly six hundred eighty-five million dollars continues to benefit the bottom line for years to come. And the private equity landscape continues to evolve, with new platforms emerging to replace those that the global brokers have absorbed.

What is not uncertain is the quality of the underlying business model. An asset-light enterprise with gross margins north of eighty percent, ninety-plus percent client retention, automatic inflation protection, enormous switching costs, and a recurring revenue base that compounds year after year is, by almost any analytical framework, one of the finest business models in existence.

Consider the journey in raw numbers: from a kitchen table in 1927 to one hundred seventy-five thousand dollars in revenue at incorporation in 1950, to one million dollars in 1968, to twenty-five million dollars by 1978, to four hundred twelve million dollars when Pat Gallagher took over as CEO in 1995, to nearly fourteen billion dollars in 2025. Each stage of that growth built on the one before it, and the flywheel spun a little faster with each revolution.

Arthur J. Gallagher understood the power of this model nearly a century ago when he started ringing doorbells across Chicago. His grandson understands it today as he oversees a fifty-six-billion-dollar global enterprise that still operates by the twenty-five tenets written by hand in 1984.

The biggest surprise from studying this company is not any single deal or financial metric. It is the realization that the most powerful competitive advantages in business are often the least visible: a culture that scales without cracking, a tax code mastered with the same creativity others apply to product innovation, and a financial flywheel that spins faster with each revolution — converting free cash flow into acquisitions, acquisitions into scale, and scale into higher margins and more free cash flow, endlessly compounding.

Arthur J. Gallagher did not build a quiet giant by making noise. It did it by making the same disciplined moves, decade after decade, while the world looked elsewhere.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube