Brown & Brown: The Story of America's Relentless Insurance Consolidator

I. Introduction & Episode Roadmap

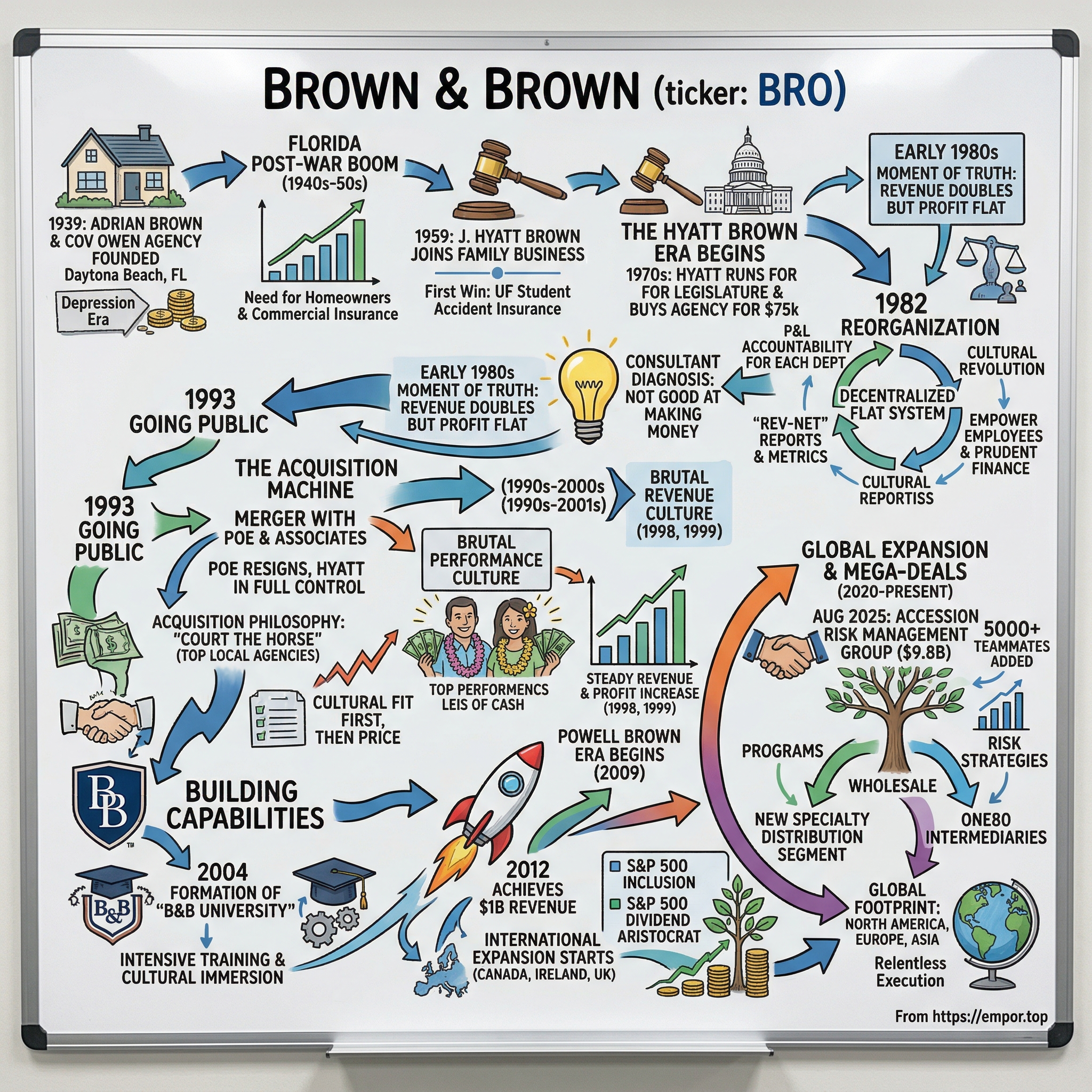

Picture this: A father-son insurance agency in Daytona Beach, Florida, 1939. Two desks, a filing cabinet, maybe a dozen clients. Fast forward to 2025, and that same company commands a $34.74 billion market capitalization, operates from 450+ locations worldwide, and just closed a $9.8 billion acquisition that shook the entire insurance industry. This is Brown & Brown—the 618th most valuable company globally, yet somehow still flying under most investors' radars. The numbers tell just part of the story. Brown & Brown reported GAAP revenues of $4.8 billion for the full year ending December 31, 2024, representing a 12.9% increase from 2023, with organic revenue increased by 10.4%. What's more fascinating is how they got here—through a relentless, disciplined acquisition strategy that has seen them complete over 500 deals since going public in 1993.

Here's what makes Brown & Brown different: While the insurance brokerage industry has become a private equity feeding frenzy, with flashy rollups and leveraged buyouts dominating headlines, Brown & Brown has quietly built an empire the old-fashioned way—with patience, cultural obsession, and three generations of family leadership. They don't just buy companies; they absorb entrepreneurs into a decentralized federation where local heroes keep running their fiefdoms.

This is the story of how a Depression-era insurance agency transformed into a $34 billion behemoth, why the insurance brokerage model might be one of the best businesses nobody talks about, and what the recent $9.8 billion Accession acquisition means for the future of insurance distribution. It's a masterclass in compounding, culture, and the power of thinking in decades rather than quarters.

II. The Founding Years: Adrian Brown's Insurance Agency (1939–1959)

The year was 1939. Hitler had just invaded Poland. The Great Depression was finally loosening its grip on America. And in Daytona Beach, Florida—a town better known for bootleggers racing on its hard-packed sand than for financial services—J. Adrian Brown was about to make a career move that would echo through generations.

Adrian Brown wasn't starting from scratch. He'd been an agent for Metropolitan Life Insurance Company, learning the trade during the lean years when a life insurance policy was as much about dignity in death as protection in life. But Adrian saw something others missed: Florida was about to boom. The state had no income tax, endless sunshine, and increasingly, retirees with assets to protect. He convinced his cousin, Charles "Cov" Owen, to partner with him, and together they hung out a shingle: Brown & Owen Insurance Agency. The timing couldn't have been worse—or better, depending on your perspective. J. Adrian Brown, an agent for Metropolitan Life Insurance Company, partnered with his cousin, Charles "Cov" Owen to open an insurance agency in Daytona Beach, Florida. The firm was then known as Brown & Owen. The world was descending into chaos, but Florida's insurance market was about to experience something extraordinary. The state's population would double between 1940 and 1960, from 1.9 million to 4.9 million residents. Every new arrival needed homeowners insurance, auto coverage, and increasingly, commercial policies for the businesses they were starting.

Adrian Brown understood something fundamental about insurance: it's a relationship business disguised as a financial service. While the big carriers focused on standardized products and mass marketing, Brown & Owen carved out a niche as the local experts who knew their clients' names, their businesses, their families. They weren't selling policies; they were selling peace of mind with a handshake.

The business grew steadily through the 1940s and 1950s, riding Florida's post-war boom. Veterans returning from World War II were using GI Bill benefits to buy homes and start businesses. The space program was bringing aerospace engineers to the coast. Tourism was exploding. By the late 1950s, Brown & Owen had established itself as a fixture in Daytona Beach's business community. But Adrian Brown was getting older, and the agency needed fresh energy. In 1959, the agency was generating approximately $45,000 in annual revenue. This wasn't much—barely enough to support two families—but it was honest work in a growing market. That year would prove pivotal. Adrian's son, J. Hyatt Brown, fresh from completing a double major in real estate and insurance at the University of Florida, came home to join the family business.

The transition from father to son would define not just Brown & Brown's future, but the entire trajectory of insurance brokerage consolidation in America.

III. The Hyatt Brown Era Begins: From Local to Regional (1959–1980s)

Adrian Brown's son, Hyatt, completed his double major in real estate and insurance at the University of Florida. He returned to help run the family business in 1959, immediately demonstrating his understanding of the interaction between relationships and sales. Using his college connections, Hyatt helped Brown & Brown land the contract for the University of Florida's student accident insurance.

That first win—the University of Florida student insurance contract—was vintage Hyatt Brown. He didn't just cold-call the university. He leveraged his fraternity connections, his professors' recommendations, his reputation as a former student leader. It was a masterclass in using social capital to build financial capital, and it became the template for everything that followed.

Hyatt Brown buys the agency for $75,000 and his vision for the company begins to take shape. To grow the agency, Hyatt knew that he had to sell one account at a time, service it well, then build on that good reputation. In 1961, BRO generated ~$61k in revenue and $1.4k in profit. The math was brutal: a 2.3% profit margin on tiny revenues. Most people would have seen a lifestyle business, maybe good for a comfortable middle-class existence. Hyatt saw something else entirely.

But Hyatt's ambitions extended beyond insurance. Someone apparently dared him to run for the legislature and he accepted the challenge in 30 seconds. He won by a whisker and sat in the Florida House of Representatives, as a Democrat, from 1972 to 1980. He served as Speaker of the House from 1978 to 1980, becoming one of the most powerful politicians in Florida while simultaneously running his insurance agency.

The political years were formative. Hyatt learned how to build coalitions, negotiate complex deals, and most importantly, how to think systematically about large organizations. When he returned full-time to Brown & Brown in 1980, he brought with him a network that spanned the entire state of Florida and a sophisticated understanding of how to wield influence.

Hyatt then returned to Brown and outlined a plan to double the revenue organically by 1982 from $2 mn to $4 mn. Brown was indeed able to meet the revenue target, but operating margin declined from 16% to 8% leading to pretty much similar profit despite doubling the revenue.

This was the moment of truth. For the first time, Hyatt decided to call a consultant to take a look at his operating plan. The consultant carefully looked at Brown's business and spoke with them three days later. He suggested while they were all great salespeople, they are not good at making money.

The consultant's diagnosis was devastating but accurate. Brown & Brown had grown like kudzu—wild, uncontrolled, without discipline. Hyatt's response would define the company's future: he didn't just tweak the model; he revolutionized it.

[In 1982] Brown & Brown reorganized to create a highly decentralized, flat system. Each office was divided into departments of business focus, such as small, middle and large commercial; personal; employee benefits; and bonds. Each department had accountability for profit and loss, and all direct and indirect costs. The Company measured everything and used the metrics to rank every office, department and salesperson. Those with the best rankings were recognized and honored. A monthly Revenue and Net Income – or Rev-Net – report was distributed to all profit centers to provide a snapshot of operating results and keep everyone focused.

This wasn't just organizational restructuring; it was cultural revolution. Every producer became a profit center. Every office became a business. The company started measuring everything—close ratios, revenue per producer, profit margins by department. The famous Brown & Brown "Rev-Net" reports became legendary in the industry, turning insurance brokerage from a relationship business into a science of optimization.

In 1990, BRO posted $25.5 Mn revenue (~26% CAGR) with 24.5% operating margin. The transformation was complete. Brown & Brown had become a profit machine, growing at venture-capital rates with private-equity margins, all while remaining essentially a family business.

His leadership style, built on unwavering integrity, employee empowerment, prudent financial management, and a relentless drive for performance and discipline, established the core values that became the foundation of Brown & Brown's distinctive culture and sustainable growth.

But Hyatt knew that organic growth alone wouldn't be enough. The insurance brokerage industry was fragmented—thousands of small, local agencies run by aging entrepreneurs. Many were profitable, well-run businesses with deep community roots. They just lacked scale, succession planning, and access to capital. Hyatt saw an opportunity: What if Brown & Brown could become the acquirer of choice for these agencies?

The strategy crystallized in the early 1990s. Brown & Brown would need to go public to access acquisition currency. But more importantly, it would need to develop a unique value proposition for sellers—one that went beyond just price.

IV. Going Public & The Acquisition Machine (1993–2000s)

The insurance industry in 1992 was at an inflection point. Hurricane Andrew had just devastated South Florida, causing $27 billion in damages and bankrupting eleven insurance companies. The hard market that followed meant soaring premiums and desperate clients looking for coverage. For brokers who could navigate the chaos, it was a goldmine.

It was against this backdrop that William Poe approached Hyatt Brown with a merger proposition. It was Poe who approached Brown about a possible merger in September 1992. Both he and his partner, Jordan, were looking to cut down on their responsibilities in order to spend more time with their families. For Brown, whose business was limited almost entirely to retail insurance in Florida, the merger was an opportunity to expand his product offerings and extend his reach to new regions. Taking advantage of being a public company he would also have greater potential for making acquisitions by issuing stock. Poe and Brown met secretly in a small hotel between Tampa and Daytona to work out the details of what would become Poe & Brown. They agreed that Brown would serve as president and CEO and make the day-to-day business decisions.

In April 1993, the US Securities and Exchange Commission approved the firm's merger with Poe & Associates, which ultimately became Brown & Brown, Inc. The ability to use public stock for acquisitions fueled a methodical expansion strategy based on buying middle-market insurance brokers throughout the country.

The merger was transformative. Revenues had jumped from $83 million combined for the two separate companies in 1992 to $95.6 million after the merger, making Poe & Brown the 19th largest insurance broker in the world. But the cultural integration proved challenging. 'He's a decentralist and I'm a centralist,' Poe told the St. Petersburg Times in the paper's August 4, 1994 edition. 'He's more of a bottom-line-oriented manager, I'm more of a people-oriented manager. He's the hardest worker you've ever seen. He works about 70 hours a week.'

Within a year, Poe resigned as chairman. Hyatt Brown now had full control of a public company with acquisition currency. The real growth was about to begin. The acquisition philosophy that emerged was quintessentially Brown & Brown, and it centered on what they called "the horse." "Our biggest competitor is not a large, publicly traded broker; it's the best local agency in each town," says Powell. Such an agency, with 20 to 500 employees, is usually run by a guy Hyatt calls "the horse" because he pulls the whole town along. He's been head of the Chamber of Commerce, everyone knows him, and his social connections make it impossible to take away his business. But even horses tire, and many smaller brokerages are run by the middle-aged men and women who started them.

This insight—that the best agencies were also the hardest to compete against but potentially willing to sell—became the cornerstone of Brown & Brown's acquisition strategy. They didn't want distressed assets or turnaround situations. They wanted winners.

Brown & Brown's top executives start a courtship process, meeting with these brokers several times at conferences or individually, to see if the prospect fits into the B&B culture. Brown & Brown opens up its own financials to show the prospect how it functions. "It's like marriage," says Downs, who as a regional executive vice president negotiated several deals. "We date until we're sure. We have no secrets. We share how our model works. Some will take what we say and implement it and that makes them more valuable when they do sell. That's OK with us."

The process was deliberately slow, often taking years. "Cultural fit comes first, the way they relate to fellow brokers, insurance carriers and clients," says Powell. "Then we talk about how much we can pay." This reversed the typical M&A playbook where price negotiations dominate. Brown & Brown would rather lose a deal on price than compromise on culture.

J. Hyatt Brown was a man who expected results, and who made it clear that only employees who could thrive would survive at Brown & Brown. At annual sales meetings, each of the company's sales managers were made to stand before an audience in excess of 1,000 and detail their results for the year. The lowest earners were spotlighted by going first, accompanied by somber music. The top performers were given the coveted final slots in the program, where they are rewarded with applause and gifts, as well as cold hard cash. The fittest of the fit received Hawaiian leis made of $100 bills instead of flowers.

The performance culture was brutal but effective. 'You are either producing revenue for the company or you are overhead. It's that simple.' This Darwinian approach extended to acquisitions. Underperforming offices could be shut down. Producers who didn't meet targets were counseled out. But those who thrived were given extraordinary autonomy and compensation.

By 1998, the machine was humming. In 1998 the company brought 26 agencies and three new product lines into its fold. One of the largest acquisitions that year, of the Daniel James Insurance Group, significantly enhanced Poe & Brown's Midwest presence—adding offices in Toledo, Ohio, and Indianapolis, Indiana.

The results spoke for themselves. Bolstered by contributions from its acquisitions, Poe & Brown saw its revenues increase to $153.8 million in 1998 and its profits soar by 23.5 percent, reaching $23.1 million. In 1999, the shareholders voted to change the company name from Poe & Brown back to Brown & Brown, acknowledging the reality of who was running the show.

He noted that the company's expansion over the past two decades – from approximately $300 million in 2000 to nearly $5 billion last year – has been driven by strategic acquisitions. But what made Brown & Brown different wasn't just the volume of deals—it was the integration model.

With Brown & Brown, no one finds out they've been acquired by email. The regional manager is involved in negotiating the purchase, since he or she will ultimately be responsible for the operation going forward. "We want the day after the acquisition to be like the day before," says Downs.

This philosophy—maintain the entrepreneurial spirit while providing the resources of scale—became the secret sauce. Acquired agencies kept their names, their offices, their local relationships. What changed was access to Brown & Brown's carrier relationships, technology platforms, and most importantly, its performance culture.

The company had become, in essence, a federation of entrepreneurs united by common metrics, shared values, and an unrelenting focus on profitable growth. By the early 2000s, Brown & Brown had completed over 100 acquisitions and was ready for its next evolution.

V. Building Capabilities: Education, Culture & Expansion (2000–2010)

The insurance industry in 2004 faced a talent crisis. The average age of an insurance agent was 59. Young people saw insurance as boring, a career for their parents' generation. Meanwhile, the products were becoming increasingly complex—cyber liability, environmental impairment, employment practices liability. The industry needed sophisticated advisors, not order-takers.

Powell Brown and Tom Finwall saw an opportunity. If Brown & Brown could build its own talent pipeline, it could solve two problems simultaneously: reduce dependence on acquisitions for growth and create a competitive advantage in human capital. In order to continue to better serve our customer base, Powell Brown and Tom Finwall formed 'B&B University,' our in-house insurance training program, in early 2004. The program was designed to arm our producers with a broad base of technical knowledge. In addition to its emphasis on technical coverage issues and premium calculations, the school inculcates the discipline that is so important to long-term success in our business. The results have been exceptional. 'Brown & Brown University' continues to be a very important part of the acculturation of the new people who join us through acquisitions and who come to us from other industries, as well as a centre for reinforcement and improvement of our technical knowledge and sales training. We teach everything from basic property and casualty insurance to complex health care solutions.

Brown & Brown University wasn't just a training program—it was a cultural immersion. New hires and acquired producers spent six months in intensive training, learning not just insurance products but the Brown & Brown way. Tom Finwall, who became the program's legendary instructor, was known for his brutal honesty and encyclopedic knowledge. Students emerged either as true believers or they washed out.

The program solved a critical integration challenge. When Brown & Brown acquired an agency, the producers could attend B&B University to learn the company's systems, metrics, and culture. It transformed potentially resistant acquired employees into evangelists. As one graduate noted, "Tom Finwall is a legend. To sit under him for 6 months was an honor. The growth we have had in 6 months in all lines of insurance is unreal."

Meanwhile, the acquisition machine continued to accelerate. Between 2000 and 2010, Brown & Brown completed over 200 acquisitions, expanding from approximately $300 million in revenue to over $1 billion. Each deal followed the same playbook: identify "the horse" in each market, court them for years, pay a fair price, maintain local autonomy, integrate through culture rather than systems. In 2009, after 48 years at the helm, Hyatt Brown stepped down as CEO. He retired as CEO of his insurance agency, Brown & Brown, though he remained as Chairman. The transition had been carefully orchestrated. At 42, Powell replaced his 72-year-old father, Hyatt, as CEO in July 2009.

The timing was terrible—or perhaps perfect for proving Powell's mettle. "Two thousand nine was a year in hell," CFO Cory Walker told analysts after the company's fourth-quarter earnings fell nearly 30% from a year earlier. In 2009, Brown & Brown acquired less than a quarter of the new brokerage revenue it did the previous year.

But the foundation was solid. Achieving $1 billion in revenues and growing, Chairman Hyatt Brown rings the opening bell. The company had reached a scale where it could compete with anyone, yet maintained the entrepreneurial spirit that made it special.

International expansion began in earnest during this period. The company established beachheads in Canada and began exploring opportunities in Europe. But unlike competitors who rushed into foreign markets, Brown & Brown was patient, looking for the same cultural fit abroad that it demanded domestically.

The decentralization philosophy reached its zenith. With corporate operating expenses comprising just 3% of total revenues, we're the leanest in our industry. Purely administrative positions are virtually nonexistent within our organization. From the executive office to customer service, everyone is responsible for sales and profitability.

This wasn't just cost-cutting; it was cultural reinforcement. Every employee, from the CEO to the receptionist, understood they were in the revenue business. There was no bureaucratic middle layer, no empire-building, no politics. You either produced or you were out.

By 2010, Brown & Brown had transformed from a regional Florida broker into a national powerhouse. The pieces were in place for the next phase of growth. Powell Brown had proven himself worthy of the family legacy. The acquisition machine was humming. And the insurance market was about to enter one of the most favorable cycles in decades.

VI. The Powell Brown Era: Scale & Sophistication (2009–2020)

Powell Brown's first day as CEO began with a ritual that would define his leadership style. Instead of heading to the executive suite, he spent the morning calling clients—not the CEOs or CFOs, but the risk managers and insurance buyers who actually worked with Brown & Brown daily. The message was clear: this was still a sales organization, regardless of size.

The inheritance Powell received was both blessing and burden. Powell's father, Hyatt, did him no favors by putting him in charge just when things are toughest. The financial crisis had decimated commercial insurance demand. Clients were laying off employees, closing locations, reducing coverage. Organic growth—the lifeblood of any broker—had turned negative.

But Powell saw opportunity where others saw crisis. "At Brown & Brown, we think long term and not merely quarter-to-quarter. We think about next year, three years from now, five years from now, and beyond, with our focus on cash flows and how to invest them wisely," he would tell investors.

His first major strategic decision was counterintuitive: instead of cutting costs and hunkering down, Brown & Brown accelerated hiring of young producers. The logic was simple—competitors were laying off talent, training programs were being cut, and Brown & Brown could cherry-pick the best people at reasonable prices. Brown & Brown University expanded its enrollment, betting that the investment in human capital would pay off when the market turned.

The acquisition strategy evolved under Powell. While Hyatt had focused on small, local agencies, Powell began targeting larger, more specialized brokers. The deals got bigger, more complex, more transformative. But the core philosophy remained: cultural fit first, financial terms second.

In 2012, Brown & Brown achieved $1 billion in revenue. This wasn't just a financial milestone; it was a psychological barrier. The company could now compete for the largest accounts, access the best talent, and command respect from global carriers.

The technology investments during this period were substantial but characteristically pragmatic. While competitors spent hundreds of millions on digital transformation initiatives, Brown & Brown focused on tools that directly improved producer productivity: CRM systems that actually got used, comparative rating platforms that saved time, and data analytics that identified cross-selling opportunities.

The company's expansion over the past two decades – from approximately $300 million in 2000 to nearly $5 billion last year – has been driven by strategic acquisitions. But what made this growth sustainable was the discipline. Bad deals were walked away from. Overpriced assets were ignored. The focus remained on quality over quantity.

The international expansion accelerated dramatically. Brown & Brown creates flagship operations in the Irish insurance market by acquiring O'Leary Insurances, a family-owned company headquartered in Cork that grew to become Ireland's largest independently owned brokerage. The pattern was familiar: find the best local player, pay a fair price, maintain the entrepreneurial culture.

Brown & Brown achieves the honor of being included on the prestigious S&P 500 index, composed of the top 500 companies in leading industries of the U.S. economy. This distinction further demonstrates our long-standing history of proven success and company growth, both organically and through strategic acquisitions.

The S&P 500 inclusion in 2021 was more than symbolic. It meant index funds had to buy the stock. It meant institutional credibility. It meant access to cheaper capital. But most importantly, it validated the model—that a family-controlled, decentralized, acquisition-focused insurance broker could compete with anyone.

S&P Dow Jones Indices adds Brown & Brown to the S&P 500 Dividend Aristocrats Index that recognizes longtime dividend payers who have raised their dividend payments for at least 25 consecutive years. Brown & Brown has increased its dividend for 28 straight years (as of 2022).

The dividend aristocrat status highlighted another aspect of the Brown & Brown model: consistent cash generation. Insurance brokerage is a beautiful business—minimal capital requirements, recurring revenues, negative working capital. The company could fund growth, make acquisitions, and still return cash to shareholders.

Under Powell's leadership, the company culture evolved but didn't fundamentally change. The brutal performance reviews continued. The $100 bill leis for top performers remained. But there was more sophistication—better training, more specialization, deeper carrier relationships.

The organizational structure became more complex but remained fundamentally decentralized. Regional presidents had P&L responsibility. Local offices maintained autonomy. The corporate overhead remained minimal. "We don't think of ourselves as a large organization. We think of ourselves as a bunch of very highly competitive teams that operate under this umbrella called Brown & Brown," Powell would say.

By 2020, Brown & Brown had become the sixth-largest insurance broker globally. Powell had successfully navigated the transition from founder-led to professional management while maintaining the entrepreneurial spirit. The company was generating over $2.5 billion in revenue, had completed hundreds more acquisitions, and was positioned for its most ambitious move yet.

VII. Global Expansion & Mega-Deals (2020–Present)

The boardroom at Brown & Brown's Daytona Beach headquarters was unusually crowded on a humid June morning in 2024. Investment bankers from J.P. Morgan filled one side of the table. Lawyers from Simpson Thacher lined the other. At the head sat Powell Brown, about to sign the largest deal in the company's 85-year history.

The target was Accession Risk Management Group, and the price tag was staggering: $9.825 billion. Accession, which has more than 5,000 insurance professionals throughout the U.S. and Canada, operates mainly in the middle-market segment and has completed over 190 acquisitions. The group reported pro forma adjusted revenue of $1.7 billion and placed $15.7 billion in premiums in 2024.

This wasn't just about scale. Accession, established in 1997 and currently the ninth largest privately held insurance brokerage in the United States, is the parent to Risk Strategies, a dynamic specialty brokerage firm, and One80 Intermediaries, a leading insurance wholesaler and program manager. Composed of over 5,000 insurance professionals throughout the U.S. and Canada and with 2024 pro forma adjusted revenues of approximately $1.7 billion, Accession is known for its specialization, deep customer relationships and high-performing culture.

The strategic logic was compelling. Risk Strategies brought expertise in complex risks—healthcare, private equity, construction. One80 Intermediaries added wholesale distribution capabilities. Together, they transformed Brown & Brown from a retail-focused broker into a full-service insurance platform.

But the real story was how the deal came together. This wasn't a hostile takeover or a distressed sale. Mike Christian, who founded Risk Strategies in 1997, had built his company using the same playbook as Brown & Brown—entrepreneurial culture, decentralized operations, acquisition-driven growth. The companies had been competing and admiring each other for years.

The negotiations took months. Cultural fit sessions where leadership teams spent days together. Deep dives into compensation structures, ensuring producers wouldn't flee. Integration planning that respected both companies' entrepreneurial DNA. The two companies, according to Brown, do not have a "significant" amount of concentration or overlap in any single area.

The financing structure was characteristically conservative. Funding for the acquisition will be secured through a combination of a $4 billion equity raise and $4 billion in bonds issued across various maturities. No excessive leverage. No financial engineering. Just a straightforward deal that preserved Brown & Brown's financial flexibility.

Brown & Brown CEO Powell Brown told analysts that the acquisition would be a "major" step in its journey to the next intermediate goal of $8 billion and beyond in revenue. In August 2025, Brown & Brown completes the acquisition of Accession Risk Management Group, Inc; adding 5,000+ talented teammates to the team. This acquisition brings additional specialties and broader carrier relationships, combining two high-performing cultures to provide the best solutions to our customers.

The integration approach was vintage Brown & Brown. Following the close of this transaction, the Risk Strategies team will become part of Brown & Brown's Retail segment, and John Mina will join the Retail senior leadership team. The business will remain aligned with Brown & Brown's decentralized sales and service model, while gaining access to Brown & Brown's global resources, specialty capabilities and collaborative network.

Meanwhile, the international expansion continued. In March 2022, it was announced Brown & Brown had completed the acquisition two property-focused insurance companies - Florida-based Orchid Underwriters Agency and Texas-based CrossCover Insurance Services. Brown & Brown extended their reach in the United Kingdom when they acquired Global Risk Partners in 2022.

The Global Risk Partners acquisition was particularly significant. GRP was the UK's largest independent insurance intermediary, with over 150 locations. It gave Brown & Brown instant scale in the world's second-largest insurance market. More importantly, it came with a management team that understood the Brown & Brown model of decentralized growth.

The company also pushed into specialty markets. Orchid Underwriters focused on catastrophe-exposed property. CrossCover specialized in Texas windstorm coverage. These weren't just acquisitions; they were capability additions that made Brown & Brown more valuable to carriers and clients.

The broader industry context made these moves even more impressive. Last year, Aon acquired NFP for $13 billion, while Marsh McLennan bought McGriff Insurance Services for $7.75 billion. Arthur J. Gallagher's $13.45 billion deal for AssuredPartners is expected to close later this year.

The consolidation wave reflected a fundamental truth: scale matters more than ever in insurance brokerage. Carriers want to work with fewer, larger partners. Clients demand global capabilities and specialized expertise. Technology investments require size to amortize costs. The mid-sized broker is becoming extinct.

But Brown & Brown's approach remained different. While competitors pursued transformational mergers that required massive integration efforts, Brown & Brown continued its strategy of disciplined, accretive acquisitions that preserved entrepreneurial culture. The Accession deal was large, but it followed the same playbook used for hundreds of smaller deals.

The results spoke for themselves. For the full year ending December 31, 2024, Brown & Brown reported GAAP revenues of $4.8 billion, representing a 12.9% increase from 2023. Commissions and fees rose by 12.1%, and organic revenue increased by 10.4%.

The company's global footprint now spans North America, Europe, and Asia. The employee count exceeds 16,000. The market capitalization has reached $34 billion. Yet the culture remains remarkably consistent with what Hyatt Brown built decades ago—decentralized, entrepreneurial, performance-driven.

VIII. Business Model Deep Dive: The Four Segments

To understand Brown & Brown's economics, you need to understand how insurance brokerage actually works. It's deceptively simple: brokers connect insurance buyers with insurance carriers, taking a commission (typically 10-20% of premiums) for their trouble. No inventory, no manufacturing, no massive capital requirements. Just relationships, expertise, and execution.

Brown & Brown has organized this simple model into four distinct segments, each with different economics, growth profiles, and strategic roles:

The Retail Segment: The Core Engine

The Retail segment provides property and casualty, employee benefits insurance products, personal insurance products, specialties insurance products, risk management strategies, loss control survey and analysis, consultancy, and claims processing services. It serves commercial, public and quasi-public entities, professional, and individual customers.

This is the heritage business—what Adrian Brown started in 1939. Today, it represents about 60% of revenues and the majority of profits. The Retail segment is thousands of producers sitting across from business owners, solving problems, placing coverage. Average account size: $50,000 in premiums. Sweet spot: middle-market companies with $10-500 million in revenue.

The economics are attractive. Gross margins run 35-40%. Client retention exceeds 93% annually. The recurring nature of the revenue—most commercial insurance renews annually—provides tremendous visibility. Organic growth tracks GDP plus a few points, with pricing cycles adding volatility.

But here's the secret sauce: cross-selling. A typical middle-market client needs property coverage, general liability, workers' compensation, auto fleet, employee benefits, cyber liability, directors & officers coverage. Brown & Brown might start with one line and eventually write them all. The lifetime value of a client can be 10-20x the first year's commission.

The Programs Segment: The Profitable Niche

The Programs segment offers professional liability and related package insurance products for dentistry, legal, eyecare, insurance, financial, physicians, real estate title professionals, as well as supplementary insurance products related to weddings, events, medical facilities, and cyber liabilities. This segment also provides public entity-related and specialty programs through a network of independent agents; and program management services for insurance carrier partners.

Programs is where Brown & Brown gets creative. Instead of being a generalist, they become the specialist for specific niches. Take dentists: Brown & Brown understands their professional liability needs, their equipment coverage requirements, their employee practices exposures. They package it all together, negotiate preferred terms with carriers, and become the go-to broker for dental practices nationwide.

The margins here are spectacular—often 40-45%. Why? Specialization creates value. Carriers love the consistent, predictable risk. Clients appreciate the tailored coverage. Competitors can't easily replicate decades of expertise and relationships. It's a moat built on knowledge.

The Programs segment also includes managing general agents (MGAs) and managing general underwriters (MGUs), where Brown & Brown actually underwrites on behalf of carriers. This moves them up the value chain, capturing underwriting profit in addition to commissions.

The Wholesale Brokerage Segment: The Connector

The Wholesale Brokerage segment markets and sells excess and surplus commercial and personal lines insurance through independent agents and brokers.

Wholesale is the business behind the business. When a retail broker—maybe even a Brown & Brown retail office—has a client with unusual or high-risk needs that standard markets won't touch, they turn to wholesalers. Think cannabis dispensaries, haunted houses, extreme sports operators.

This segment serves 15,000+ retail agents, acting as their gateway to specialty markets. Margins are lower—20-25%—because Brown & Brown splits commissions with the retail broker. But there's no client acquisition cost and minimal service requirements. It's almost pure profit after the commission split.

The wholesale business is also countercyclical. In soft markets, when standard carriers write anything, wholesale struggles. In hard markets, when carriers tighten standards, wholesale booms. This provides natural hedging for the retail business.

The Services Segment: The Fee Generator

The Services segment offers third-party claims administration and medical utilization management services in the workers' compensation and all-lines liability arenas, Medicare Set-aside, Social Security disability, Medicare benefits advocacy, and claims adjusting services.

Services is the outlier—fee-based rather than commission-based. Companies outsource claims management to Brown & Brown, paying hourly or per-claim fees. It's lower margin—15-20%—but provides diversification from commission income and deepens client relationships.

This segment also includes innovative services like Medicare Set-aside arrangements for workers' compensation settlements, Social Security disability advocacy, and medical bill review. These aren't huge revenue generators individually, but they make Brown & Brown stickier with clients and create cross-selling opportunities.

The Integrated Model

What makes Brown & Brown's four-segment model powerful is the interplay:

- A Retail client with hard-to-place risks gets served by Wholesale

- A Programs relationship introduces new retail opportunities

- Services work leads to benefits consulting

- Every segment reinforces the others

This isn't visible in the reported financials, but it's crucial to understanding the durability of the model. A client might show up in multiple segments, making Brown & Brown increasingly indispensable.

The segment reporting also obscures the real profitability drivers. Corporate overhead is minimal—remember, just 3% of revenue. Most costs sit in the segments, close to revenue generation. This radical decentralization means each segment, each region, each office must justify its existence through profitability.

The capital allocation across segments is equally disciplined. Retail gets the most acquisition investment because of its predictable returns. Programs receives growth capital for new niche development. Wholesale and Services grow more organically, requiring minimal investment.

Post-Accession, the company is reorganizing. In connection with the closing of the acquisition, Brown & Brown will combine its Programs and Wholesale Brokerage segments into a new Specialty Distribution segment, which will be led by Steve Boyd and Chris Walker. One80 Intermediaries will join the operations of our new Specialty Distribution segment, with Matt Power joining the segment's senior leadership team.

This restructuring makes strategic sense. The distinction between Programs and Wholesale has blurred as distribution strategies converge. The new Specialty Distribution segment will house all non-retail distribution, simplifying the story for investors and operations for management.

IX. Financial Performance & Capital Allocation

The numbers tell a story of relentless execution. In 2024 the company made a revenue of $4.66 Billion USD an increase over the revenue in the year 2023 that were of $4.18 Billion USD. But revenue is just the beginning. The real story is how Brown & Brown turns that revenue into cash, and what it does with that cash.

Let's start with the revenue build. For the full year ending December 31, 2024, Brown & Brown reported GAAP revenues of $4.8 billion, representing a 12.9% increase from 2023. Commissions and fees rose by 12.1%, and organic revenue increased by 10.4%.

That 10.4% organic growth number is remarkable. In a mature industry, growing at GDP plus a few points, Brown & Brown is taking share. The drivers are straightforward: - New business from increased sales productivity - Retention rates exceeding 93% - Cross-selling into existing accounts - Exposure growth as clients expand - Rate increases in hard market conditions

But here's where it gets interesting: the margin expansion. Adjusted EBITDAC increased by 17.0% to $1.7 billion, while the adjusted EBITDAC margin improved to 35.2% from 33.9%.

This isn't financial engineering. It's operational leverage. The business model has enormous fixed-cost coverage. Once you have an office, a producer, and carrier appointments, the incremental revenue drops straight to the bottom line. Every additional dollar of commission costs maybe 20-30 cents to service.

The cash generation is even more impressive. Cash from Operations: Nearly $1.2 billion generated for the full year 2024. Insurance brokerage is a negative working capital business—commissions are collected before expenses are paid. Growth actually generates cash rather than consuming it.

The Capital Allocation Framework

With over a billion in annual free cash flow, capital allocation becomes paramount. Brown & Brown follows a clear hierarchy:

1. Organic Investment (10-15% of cash flow) - Hiring and training new producers - Technology infrastructure - Office expansion in growth markets

The returns here are exceptional—often 30-40% IRR—but limited by talent availability and market opportunity.

2. Acquisitions (60-70% of cash flow) The acquisition math is compelling. Brown & Brown typically pays 8-10x EBITDA for quality brokers. Post-synergies (cost saves, revenue enhancement, tax optimization), the effective multiple drops to 6-8x. With organic growth and margin expansion, these deals generate 15-20% IRRs consistently.

The discipline is crucial. "Acquisitions must be high quality and fit culturally. If we build relationships with acquiring companies over time we find the financials work out".

3. Dividends (15-20% of cash flow) The dividend policy is conservative but consistent. We're really proud that we've increased our dividends for 29 years, but we don't have a very high dividend yield, because we think we can invest the money more in a better way and drive more value than actually paying it out in dividends.

The current yield is modest—around 0.7%—but the growth is reliable. This isn't an income stock; it's a compounder that happens to pay a growing dividend.

4. Share Buybacks (Opportunistic) We'll buy stock back sometimes, if the stock's not appropriately valued. But buybacks are the last priority, used only when the stock is clearly undervalued and no better opportunities exist.

The Accession Financing

The Accession deal required Brown & Brown to access capital markets at scale. The solution was elegant: Funding for the acquisition will be secured through a combination of a $4 billion equity raise and $4 billion in bonds issued across various maturities.

The equity raise was priced efficiently, with minimal dilution to existing shareholders. The debt was structured across maturities to match cash flow generation. Even post-deal, leverage remains conservative at around 2.5x EBITDA—well below the 4-5x typical in the industry.

Unit Economics That Matter

Beyond the reported financials, several unit economics drive the business:

Revenue per Producer: ~$1.2 million annually Top quartile producers generate $3-5 million. Bottom quartile often below $500k. The spread drives the performance culture.

Customer Acquisition Cost: ~$15,000 Mostly sales compensation for the first year. With average account life exceeding 10 years and growing revenue per account, the lifetime value to CAC exceeds 20:1.

Margin by Vintage: - Year 1: 5-10% (investment phase) - Year 3: 20-25% (breaking even) - Year 5+: 35-40% (mature margins)

This J-curve dynamic means growth temporarily depresses margins, but creates enormous value over time.

Acquisition Integration Costs: 2-3% of deal value Remarkably low because of the decentralized model. No massive system integration. No headquarters relocation. Just cultural alignment and best practice sharing.

The Economic Moat

The financial performance reflects deep competitive advantages:

-

Scale Economics: Larger brokers get better terms from carriers, access to exclusive programs, and can amortize technology costs

-

Switching Costs: Moving brokers is painful for clients—new relationships, different systems, potential coverage gaps

-

Network Effects: More clients attract more carriers attract more clients

-

Intangible Assets: Decades of data, relationships, and expertise that can't be replicated

-

Culture: The performance-driven, entrepreneurial culture acts as both an attraction and retention tool

The result is a business with predictable growth, expanding margins, and tremendous cash generation. It's not exciting, but it's extraordinarily profitable.

X. Playbook: Lessons in Building a Serial Acquirer

If you wanted to build Brown & Brown from scratch today, you couldn't. Not because the opportunity doesn't exist—insurance brokerage remains highly fragmented with 35,000+ independent agencies in the U.S. alone. You couldn't replicate it because Brown & Brown's success isn't about strategy; it's about execution accumulated over decades.

But the playbook itself is surprisingly simple and universally applicable:

Lesson 1: Culture Eats Strategy (And Everything Else)

"Cultural fit comes first, the way they relate to fellow brokers, insurance carriers and clients. Then we talk about how much we can pay". This isn't corporate speak. Brown & Brown has walked away from dozens of deals over cultural misalignment, even when the financial metrics were compelling.

The culture itself is brutal but transparent: performance-based, radically decentralized, entrepreneurial. The annual sales meetings where underperformers are publicly shamed and top performers get $100 bill leis? That's not theater—it's cultural reinforcement.

This culture acts as both filter and accelerant. People who thrive in ambiguous, competitive, results-oriented environments flourish. Everyone else leaves quickly. There's no middle ground, no place to hide, no excuses.

Lesson 2: Decentralization as Competitive Advantage

"For us, decentralization means operating with little overhead. In fact, with corporate operating expenses comprising just 3% of total revenues, we're the leanest in our industry. Purely administrative positions are virtually nonexistent within our organization".

Every office operates as its own P&L. Every producer knows their numbers. Every region competes against every other region. This isn't just about cost control—it's about ownership mentality. When you're responsible for your own results, you act like an owner.

The decentralization extends to acquisitions. With Brown & Brown, no one finds out they've been acquired by email. The regional manager is involved in negotiating the purchase, since he or she will ultimately be responsible for the operation going forward. "We want the day after the acquisition to be like the day before".

Lesson 3: Patient Capital Wins

Brown & Brown's acquisition process often takes years. They'll court a target, compete against them, learn their business, build relationships. When the owner is finally ready to sell—often for personal reasons like retirement or estate planning—Brown & Brown is the natural buyer.

This patience extends to integration. No forced system migrations. No immediate headcount reductions. No rebranding mandates. The acquired company continues operating largely as before, just with better resources and metrics.

"At Brown & Brown, we think long term and not merely quarter-to-quarter. We think about next year, three years from now, five years from now, and beyond, with our focus on cash flows and how to invest them wisely".

Lesson 4: Build Internal Capabilities

Brown & Brown University isn't just training—it's indoctrination. Six months of intensive education that covers technical knowledge, sales skills, and cultural values. It's expensive, time-consuming, and absolutely essential.

This investment in human capital creates multiple advantages: - Consistent service quality across offices - Common language and metrics - Cultural transmission to acquired companies - Pipeline of future leaders

The internal promotion statistics are telling: the vast majority of senior leadership came up through the ranks. This isn't nepotism (despite the family involvement); it's the natural result of developing talent internally.

Lesson 5: The Power of No

What Brown & Brown doesn't do is as important as what it does: - No transformational mergers that require massive integration - No ventures outside core insurance brokerage - No aggressive financial engineering - No centralized command-and-control - No tolerance for underperformance

This discipline seems obvious but is incredibly difficult to maintain. The temptation to pursue the big deal, to diversify into adjacent markets, to juice returns with leverage—Brown & Brown has resisted them all.

Lesson 6: Align Incentives Ruthlessly

Brown & Brown is unique for a firm of its caliber, with 25% of the company owned by the employees and 50% publicly traded. This ownership structure aligns everyone's interests. Producers think like owners because they are owners.

The compensation structure reinforces this. Low base salaries, high commission rates, and equity participation for top performers. You eat what you kill, but if you're successful, you get rich.

Even acquired company owners often retain equity stakes in Brown & Brown, aligning their interests with the company's long-term success. They're not just selling out; they're buying in.

Lesson 7: Embrace Creative Destruction

Brown & Brown's willingness to fire underperformers, shut down unsuccessful offices, and walk away from bad business is remarkable. In an industry built on relationships, they're unsentimental about performance.

This extends to acquisitions. If an acquired office underperforms, it gets fixed or closed. No sacred cows, no protected territories, no excuses. The discipline maintains the culture and the margins.

The Meta-Lesson: Compound Learning

Every acquisition teaches something. Every integration reveals opportunities. Every mistake becomes institutional knowledge. After 500+ deals, Brown & Brown has seen every scenario, every problem, every opportunity.

This accumulated learning creates an insurmountable advantage. Competitors can copy the strategy, but they can't replicate decades of pattern recognition. They can hire bankers and consultants, but they can't buy institutional memory.

The playbook looks simple because it is simple. The difficulty is in the execution, maintained consistently over decades, through multiple cycles, across hundreds of acquisitions. It's not about being smarter; it's about being more disciplined for longer.

XI. Industry Analysis & Competitive Positioning

The insurance brokerage industry is experiencing its golden age. After decades of sleepy, fragmented competition among mom-and-pop agencies, the industry is consolidating rapidly into a handful of global giants. The math is compelling: there are still ~35,000 independent insurance agencies in the U.S., most with under $5 million in revenue. The top 10 brokers control less than 35% of the market. In most industries, that screams opportunity.

In 2021 the company ranked as the fifth largest independent insurance brokerage in the U.S. and sixth largest in the world by Business Insurance magazine. But rankings don't tell the full story. The industry is segmented into distinct competitive groups:

The Global Giants: Marsh, Aon, Willis Towers Watson

These firms, with $15-20 billion in annual revenue, dominate Fortune 500 accounts. They're consultants as much as brokers, providing risk management, actuarial services, human capital consulting. Their sweet spot: multinational corporations with complex, global risks.

Brown & Brown doesn't compete here, and that's by design. The investment required to serve global accounts—offices in 100+ countries, sophisticated modeling capabilities, armies of consultants—destroys returns. Let the giants fight over the Fortune 500; Brown & Brown will take the Fortune 50,000.

The National Players: Gallagher, Brown & Brown, Hub International

This is Brown & Brown's peer group—companies with $4-10 billion in revenue, national presence, and middle-market focus. The competition is intense but rational. Everyone's rolling up smaller brokers, expanding capabilities, and pushing into new geographies.

What distinguishes Brown & Brown is the execution. While Gallagher pursues massive transformational deals and Hub leverages private equity financial engineering, Brown & Brown sticks to its disciplined, cultural-fit-first approach. It's tortoise and hare, and Brown & Brown is comfortable being the tortoise.

The PE-Backed Consolidators: Acrisure, AssuredPartners, NFP

Private equity discovered insurance brokerage around 2010 and fell in love. Predictable cash flows, fragmented market, rollup opportunity—it checked every box. Firms like Acrisure have gone from nothing to $4+ billion in revenue in less than a decade.

But PE-backed consolidators face challenges. They're often leveraged 6-8x EBITDA, limiting flexibility. They need exits in 5-7 years, creating pressure for unsustainable growth. Most importantly, they struggle with culture—financial engineering doesn't inspire insurance producers.

Brown & Brown benefits from this competition. PE firms often overpay for assets, inflating valuations. But they also create opportunity—when PE firms need to exit or overleveraged platforms struggle, Brown & Brown is ready with patient capital and a permanent home.

The Technology Disruptors: InsurTech

Every few years, Silicon Valley discovers insurance and declares the industry ripe for disruption. Digital brokers, AI-powered underwriting, blockchain-enabled contracts—the promises are grand. The results, so far, are modest.

The reality is that commercial insurance is complex, relationship-driven, and regulated. A small business owner whose factory just burned down doesn't want to chat with an AI; they want their broker's cell phone number. Technology enhances the brokerage model; it doesn't replace it.

Brown & Brown embraces useful technology—comparative rating platforms, CRM systems, data analytics—while avoiding the hype. They're fast followers, not bleeding-edge innovators, and that's perfectly fine for their clients.

Industry Dynamics Favoring Consolidation

Several structural forces are driving consolidation:

1. Carrier Consolidation: As insurance carriers merge, they prefer working with fewer, larger brokers. Scale begets scale.

2. Regulatory Complexity: Increasing compliance requirements favor larger firms that can amortize costs.

3. Technology Investment: Modern systems require scale to justify investment.

4. Succession Crisis: The average agency owner is 58 years old. Many have no succession plan except selling.

5. Specialization Premium: Clients increasingly want specialists, not generalists. Only large firms can afford deep specialization.

These dynamics are accelerating. While small buyouts are typical in the highly fragmented industry, the deal highlights that companies are willing to pay top dollar for acquisitions that significantly enhance their market presence or strengthen their competitive edge.

Brown & Brown's Unique Position

Brown & Brown occupies an enviable position: large enough to compete with anyone, focused enough to avoid costly distractions, disciplined enough to maintain returns. The company's specific advantages include:

Middle-Market Dominance: The U.S. has ~600,000 businesses with $10-500 million in revenue. They're too small for global brokers, too complex for local agents. It's Brown & Brown's sweet spot.

Cultural Coherence: Unlike PE rollups or transformational mergers, Brown & Brown's 500+ acquisitions share common culture and systems. This coherence enables efficiency without centralization.

Permanent Capital: As a public company controlled by the Brown family, Brown & Brown can think in decades. No exit pressure, no refinancing cliffs, no forced sales.

Acquisition Reputation: After decades of fair dealing, Brown & Brown is the buyer of choice for quality agencies. Sellers know their employees will be treated well, their cultures respected, their legacies preserved.

Competitive Threats and Responses

The biggest threat isn't a competitor; it's complacency. Brown & Brown's model has worked for so long that adaptation could be delayed. Specific risks include:

Direct Distribution: Carriers going direct to customers, cutting out brokers. Response: Focus on complex risks where advice adds value.

Technology Disruption: Digital brokers capturing simple, transactional business. Response: Let them have it; focus on relationship-driven accounts.

Talent War: Competition for young producers intensifying. Response: Brown & Brown University and ownership culture.

Valuation Inflation: PE firms driving acquisition prices to unsustainable levels. Response: Patience and discipline; wait for the cycle to turn.

The insurance brokerage industry structure increasingly resembles other professional services—accounting, law, consulting—where a handful of global firms dominate large accounts while regional and specialist firms thrive in niches. Brown & Brown is positioned perfectly in this structure: too focused to compete globally, too large to be niche, just right for the vast American middle market.

XII. Bear vs. Bull Case & Future Outlook

The Bull Case: Compounding Machine with Decades of Runway

The optimists see Brown & Brown as Warren Buffett would—a compounding machine disguised as a boring insurance broker. Their arguments are compelling:

Proven Acquisition Platform: With 500+ successful integrations, Brown & Brown has de-risked the rollup model. They've seen every problem, solved every integration challenge, avoided every pitfall. The Accession deal, despite its size, is just another rep in a well-practiced routine. The pipeline remains robust with 35,000 independent agencies in the U.S., most run by aging owners without succession plans.

Organic Growth Excellence: That 10.4% organic growth in 2024 wasn't a fluke. Brown & Brown is taking share through superior execution—better producers, deeper specialization, stronger carrier relationships. The flywheel is accelerating: scale attracts talent, talent drives growth, growth enables investment, investment builds scale.

Margin Expansion Opportunity: At 35% EBITDAC margins, Brown & Brown is already best-in-class. But there's room to run. Technology investments are starting to pay off. The mix shift toward higher-margin specialty business continues. The Accession synergies could add 200+ basis points. Getting to 40% margins would add $400 million to EBITDA.

Dividend Aristocrat Status: Brown & Brown has increased its dividend for 28 straight years (as of 2022). This isn't just about income; it's about discipline. Companies that can grow dividends for decades have sustainable competitive advantages, strong cultures, and aligned management.

Valuation Support: Trading at ~22x forward earnings, Brown & Brown isn't cheap, but it's reasonable for a business growing revenue at 12%, expanding margins, and generating 20%+ returns on equity. If the company hits its $8 billion revenue target with 37% margins, the stock could double.

The Bear Case: Peak Multiples Meet Structural Headwinds

The skeptics see a different picture—a mature industry consolidator trading at peak multiples just as the tailwinds reverse:

Integration Risk: The Accession deal is massive—$9.8 billion is 10x larger than any previous Brown & Brown acquisition. The integration complexity is exponential, not linear. Cultural alignment with 5,000 new employees is harder than with 50. One integration stumble could destroy billions in value.

Technology Disruption: InsurTech isn't a joke anymore. Embedded insurance, parametric products, AI-powered underwriting—these innovations are moving from experiment to execution. Brown & Brown's relationship-based model works today, but what about when digital natives become business owners?

Cycle Risk: Insurance brokerage is cyclical, despite the recurring revenue. We're in year five of a hard market with strong pricing. When the cycle turns—and it always does—organic growth could go negative. The last soft market (2015-2017) saw industry organic growth near zero.

Competition Intensifying: Gallagher's AssuredPartners deal, Aon's NFP acquisition—everyone's going big. The easy rollup targets are gone. What's left is expensive, competed, or broken. Brown & Brown's disciplined approach is admirable, but it might mean slower growth in a world where scale increasingly matters.

Economic Sensitivity: Middle-market commercial insurance is economically sensitive. In recessions, businesses fail, employees get laid off, coverage gets cut. Brown & Brown weathered 2008-2009, but that was a smaller, simpler company. The next recession hits a leveraged, complex, global enterprise.

Valuation Risk: At 22x earnings and 7x revenue, Brown & Brown is priced for perfection. Any disappointment—integration delays, organic growth slowdown, margin compression—could trigger multiple compression. If the stock rerates to 15x earnings (the historical average), that's a 30% decline.

The Realistic Case: Steady Execution in a Volatile World

The truth likely lies between extremes. Brown & Brown is an exceptional business with a proven model, but it operates in a competitive, evolving industry. The most probable outcome:

Revenue Growth: 8-10% annually—5-6% organic plus 3-4% from acquisitions. The $8 billion target is achievable by 2027-2028, though it might require another large deal.

Margin Trajectory: Gradual expansion to 36-37%, with technology and mix shift offsetting wage inflation and competition.

Capital Deployment: Continued disciplined acquisitions, growing dividends, opportunistic buybacks. No transformational deals beyond Accession, no aggressive leverage, no strategic pivots.

Competitive Position: Maintain #5-6 global ranking, strengthen middle-market leadership, selective international expansion. Let others fight for Fortune 500 accounts or unprofitable InsurTech experiments.

Stock Performance: High single-digit annual returns—6% earnings growth plus 1% dividend plus modest multiple expansion if execution continues. Not spectacular, but solid in a world of zero interest rates and volatile markets.

Key Monitorables for Investors

Organic Growth Rate: The canary in the coal mine. If organic growth drops below 3-4%, something's wrong—either execution, competition, or cycle.

Accession Integration: Watch employee retention, revenue synergies, and margin progression. Success here validates the model; failure questions everything.

Acquisition Pace and Pricing: If deal volume slows or multiples paid increase significantly, growth could disappoint.

Technology Investments: Brown & Brown needs to balance automation with relationship focus. Too little risks obsolescence; too much destroys the culture.

Succession Planning: Powell Brown is 54—plenty of runway—but who's next? The fourth generation? Professional management? The answer matters for culture and strategy.

The bear case isn't catastrophic—this isn't a buggy whip manufacturer facing automobiles. The bull case isn't fantasy—the execution track record is real. The most likely outcome is continued steady execution, which in a world of disruption and volatility, might be exactly what investors want.

XIII. Epilogue & "If We Were CEOs"

Standing in Brown & Brown's Daytona Beach headquarters, you can still see the original office building where Adrian Brown and Cov Owen started in 1939. It's been preserved, like a shrine to persistence. The juxtaposition with the gleaming modern campus tells the entire story—respect for heritage, ambition for growth, patience in execution.

What makes Brown & Brown different isn't any single brilliant insight. It's the accumulation of thousands of good decisions over decades. The discipline to walk away from bad deals. The patience to court acquisition targets for years. The courage to fire underperformers. The wisdom to stay decentralized despite the temptation to control.

The three-generation family leadership story is remarkable but not unique—Walmart, Ford, Cargill all have family through-lines. What's unique is maintaining entrepreneurial culture at scale. Most companies lose their soul around $1 billion in revenue. Brown & Brown at nearly $5 billion still feels like a collection of entrepreneurs who happen to share a parent company.

If We Were CEOs: Three Strategic Imperatives

1. Double Down on Technology, But Stay Human

Brown & Brown has been a thoughtful technology adopter, but the pace is accelerating. If we ran the company, we'd create Brown & Brown Ventures—a $100 million fund to invest in InsurTech startups. Not to compete with the core business, but to learn, experiment, and occasionally acquire.

The key is maintaining the human touch. Technology should enable producers to spend more time with clients, not replace them. Automate the mundane—data entry, quote comparison, renewal processing. Preserve the strategic—risk assessment, claims advocacy, trusted advisor relationships.

Specific initiatives: - AI-powered cross-sell identification - Automated renewal processing for simple accounts - Predictive analytics for client retention - Digital self-service for basic transactions - Blockchain for placement documentation

But every technology investment would face a simple test: does it help our producers sell more insurance more profitably? If not, pass.

2. Build the Fourth Pillar: Alternative Risk

Brown & Brown has mastered traditional brokerage, but the future includes alternative risk transfer. Captives, parametric insurance, insurance-linked securities—these aren't mainstream yet, but they will be.

We'd acquire or build expertise in: - Captive insurance company formation and management - Parametric products for weather and catastrophe risk - Insurance-linked securities for capital markets access - Risk retention groups for homogeneous risks - Blockchain-based peer-to-peer insurance models

This isn't abandoning the core model; it's extending it. As risks become more complex and traditional insurance more expensive, clients need alternatives. Brown & Brown should provide them.

3. Go Global, But Stay Local

International expansion has been opportunistic—UK, Ireland, Canada. We'd be more systematic. The playbook that works in the U.S.—rolling up fragmented markets with disciplined cultural integration—translates globally.

Target markets: - Australia: Similar market structure, common language, compatible culture - Germany: Europe's largest economy, fragmented brokerage market - Japan: Aging demographics creating succession opportunities - Brazil: Large, growing, underserved middle market

But—and this is crucial—each market would operate locally. No American executives parachuting in. No forced standardization. Find the best local operators, give them capital and culture, let them build.

The goal isn't global domination. It's selective expansion into markets where Brown & Brown's model creates value. Stay focused, stay disciplined, stay local even while going global.

The Eternal Questions

Some questions don't have answers, only trade-offs:

Scale vs. Entrepreneurship: How big can Brown & Brown get while maintaining its entrepreneurial culture? Is there a natural limit where bureaucracy inevitably emerges?

Family vs. Professional: Should the fourth generation lead Brown & Brown? Or is it time for purely professional management? The family connection provides continuity and long-term thinking, but risks insularity.

Specialization vs. Diversification: Should Brown & Brown stick to pure brokerage or expand into adjacent services? The focused strategy has worked, but leaves money on the table.

Technology vs. Tradition: How aggressively should Brown & Brown embrace digital transformation? Too slow risks obsolescence; too fast risks destroying the relationship model that built the company.

Final Reflections: The Power of Compound Culture

Brown & Brown's story isn't about insurance. It's about the power of culture to compound over time. Every acquisition adds to the culture. Every producer trained reinforces it. Every underperformer fired strengthens it.

This cultural compounding is more powerful than financial compounding. Money can be lost in a bad year. Market share can evaporate. Technology can disrupt. But culture, once embedded, endures.

The lesson for other industries seeking consolidation plays isn't about tactics—how to value acquisitions or structure deals. It's about patience and principles. Build a culture worth joining. Maintain standards worth meeting. Create ownership worth having.

Brown & Brown proves that in an age of disruption, execution beats innovation. In a world of financial engineering, operations beat optimization. In a time of constant change, culture beats everything.

The company motto, unofficially, might as well be: "We're not the smartest, fastest, or flashiest. We just show up every day, sell insurance, treat people fairly, and let the results compound."

Eighty-five years in, the formula still works.

XIV. Recent News

The Accession deal closed on August 1, 2025, marking a new chapter in Brown & Brown's history. In August 2025, Brown & Brown completes the acquisition of Accession Risk Management Group, Inc; adding 5,000+ talented teammates to the team. This acquisition brings additional specialties and broader carrier relationships, combining two high-performing cultures to provide the best solutions to our customers.

The market reaction has been positive but measured. The stock trades around $105, up modestly from pre-announcement levels. Investors appreciate the strategic logic but await integration proof points. The consensus view: if Brown & Brown can integrate Accession as smoothly as its hundreds of smaller deals, this transforms the company. If not, it's an expensive lesson in scaling limits.

Q2 2025 earnings provided confidence. Total GAAP revenue rising to $1.3 billion, an increase of $107 million, or 9.1%, compared to the same period in 2024. The growth was led by an 8.2% rise in commissions and fees and a 3.6% increase in organic revenue.

The organic growth momentum continues despite a softening rate environment. Commercial property rates are declining after years of increases. Cyber insurance, after explosive growth, is moderating. But exposure growth—clients adding employees, locations, and assets—more than compensates.

Looking ahead to Q4 2024 results and full-year 2025 guidance, analysts expect: - Revenue approaching $5.5 billion including partial Accession contribution - Organic growth moderating to 6-8% as comparisons toughen - Margins expanding 50-100 basis points from mix and synergies - EPS growth of 15-20% despite acquisition dilution

The key questions for 2025 and beyond: - Can Brown & Brown maintain cultural coherence at unprecedented scale? - Will the specialty distribution reorganization unlock revenue synergies? - How quickly can Accession's systems and processes be integrated? - What's the next acquisition target after digesting Accession?

The insurance brokerage consolidation wave continues. Gallagher's AssuredPartners deal should close in late 2025. PE firms are raising new funds targeting insurance distribution. The remaining independent brokers face increasing pressure to pick a partner.

For Brown & Brown, the challenge is execution, not strategy. The playbook remains unchanged: identify great brokers, pay fair prices, maintain entrepreneurial culture, measure everything, fire underperformers, let results compound.

The story that began with Adrian Brown and Cov Owen in 1939 continues. Three generations, 500+ acquisitions, and $34 billion in market value later, the formula endures: disciplined growth, decentralized execution, and relentless focus on performance.

In an industry measuring relationships in decades and policies in centuries, Brown & Brown thinks in generations. The Accession deal isn't an endpoint; it's another milestone on an journey that, if history is any guide, has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube