Old Dominion Freight Line: The Story of America's LTL Excellence

I. Cold Open & The Puzzle

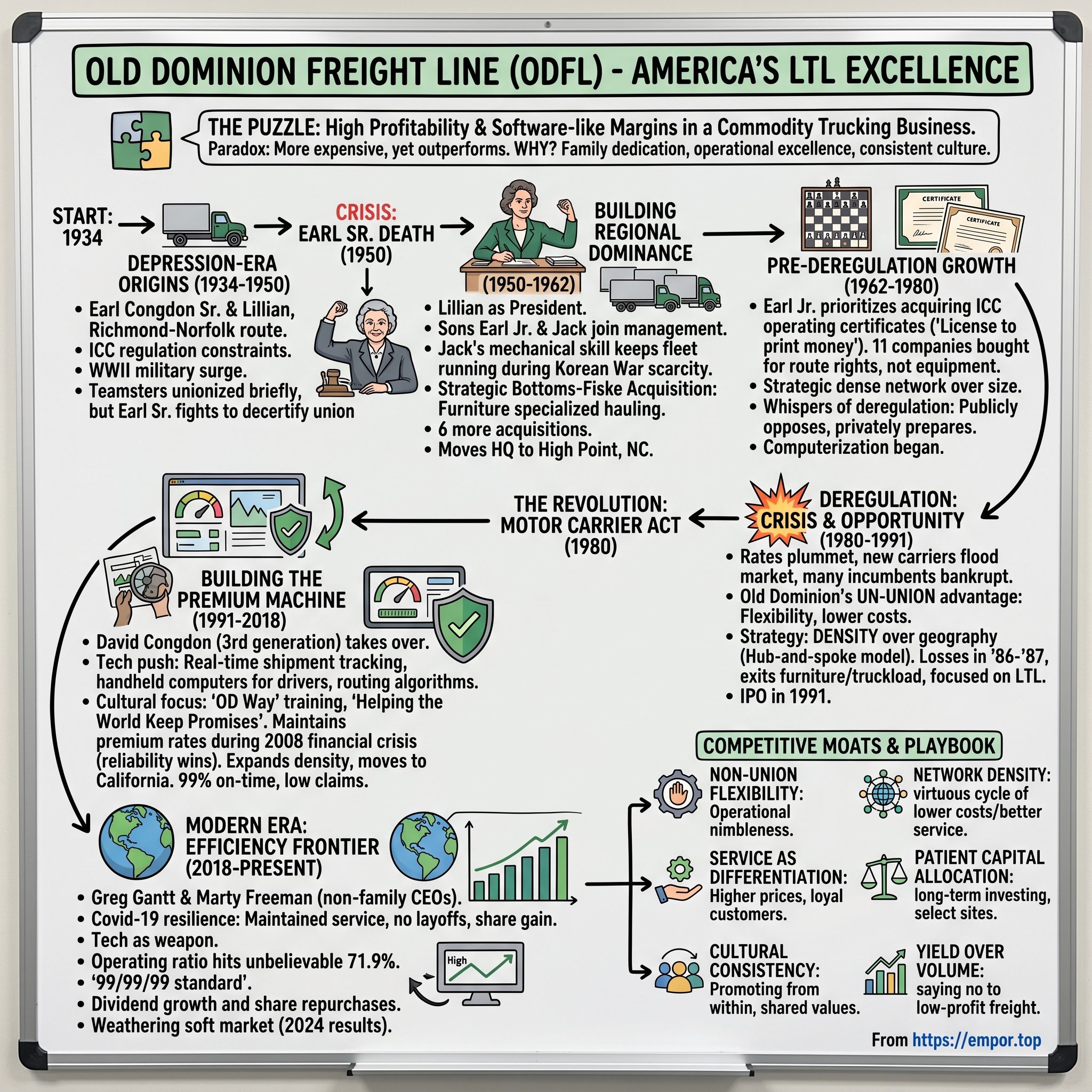

Picture this: It's July 2024, and Wall Street analysts are poring over quarterly earnings reports from the trucking industry. Most less-than-truckload (LTL) carriers are reporting operating ratios in the high 80s or low 90s—respectable numbers in a notoriously tough business. Then Old Dominion Freight Line drops its Q2 results: an operating ratio of 71.9%. In an industry where moving boxes from point A to point B is supposed to be a commodity, one company is generating software-like margins.

How does a trucking company—a trucking company—achieve operating efficiency that would make most tech companies envious? How did a single-truck operation started during the Great Depression in Richmond, Virginia, transform into North America's most profitable freight carrier, commanding premium prices in a business where customers supposedly only care about the lowest bid?

The paradox deepens when you realize that Old Dominion doesn't win on price—they're often 10-15% more expensive than competitors. They don't have proprietary technology that others can't replicate. They don't own exclusive routes or have regulatory monopolies. Yet their stock has outperformed the S&P 500 by nearly 10x over the past two decades, turning patient shareholders into multimillionaires.

This is the story of how three generations of the Congdon family built an operational excellence machine in the most unlikely of industries. It's a masterclass in compound advantages, cultural consistency, and the power of saying no. It's about winning through reliability in a world that usually rewards the cheapest option. And it holds lessons for any business trying to create differentiation in commoditized markets.

We'll trace Old Dominion's journey from Depression-era Virginia through trucking deregulation, family succession crises, technological transformation, and emergence as the envy of the logistics world. Along the way, we'll uncover the counterintuitive strategies that turned hauling freight into a premium business—and why, despite everyone knowing their playbook, no competitor has successfully replicated it.

II. Depression-Era Origins & The Congdon Foundation (1934-1950)

The year was 1934. Franklin Roosevelt was in his second year as president, the Dust Bowl was ravaging the Midwest, and a gallon of gas cost 10 cents. In Richmond, Virginia, Earl Congdon Sr. and his wife Lillian scraped together enough money to buy a single straight truck. Their business plan was simple: haul freight between Richmond and Norfolk, a 94-mile stretch of Virginia highway that connected the state capital to its largest port.

Earl named his company Old Dominion Freight Line, a nod to Virginia's colonial-era nickname. The name carried weight in the region—"Old Dominion" evoked tradition, reliability, and deep local roots. In those early days, Earl would drive the truck himself while Lillian handled the books from their kitchen table. Their first "terminal" was quite literally their front yard.

The timing seemed terrible for starting a trucking company. The Interstate Commerce Commission (ICC), created in 1887 to regulate railroads, had recently expanded its authority to cover motor carriers. Every route required government approval. Every rate needed filing. Every acquisition demanded regulatory blessing. These operating certificates weren't just paperwork—they were golden tickets, mini-monopolies that could make or break a trucking operation. Earl quickly learned that success meant playing a complex regulatory chess game while simultaneously keeping trucks running and customers happy.

By 1935, the Congdons had outgrown their house and moved operations to a rented grocery store space. A year later, they relocated again to a two-bay facility they shared with Overnite Transportation—a competitor that would, decades later, become part of the UPS empire. By the end of 1936, Old Dominion operated six tractor-trailers and twelve straight trucks. The company was growing, but slowly, constrained by both capital and ICC regulations.

Then came Pearl Harbor. The transformation of southeastern Virginia into a military logistics hub changed everything. The Norfolk Naval Base exploded in size. Camp Lee (later Fort Lee) became a quartermaster training center. Langley Field expanded into a major Army Air Forces installation. Suddenly, the Richmond-Norfolk corridor wasn't just a sleepy state route—it was a critical military supply line. Old Dominion's trucks ran around the clock, hauling everything from uniforms to ammunition. Revenue quadrupled between 1941 and 1945.

But wartime prosperity brought unexpected complications. In 1940, at the insistence of a major customer who preferred dealing with unionized carriers, Earl agreed to let the Teamsters organize his drivers. It seemed like a small concession at the time—the customer's freight paid well, and Earl genuinely wanted good wages for his men. The decision would echo through the company's history in ways no one could have predicted.

The war's end brought both opportunity and crisis. The military contracts dried up, but civilian demand surged as returning veterans started families and bought homes. Old Dominion had grown to 35 trucks and was generating steady profits. Then, in 1947, the Teamsters called a strike. The work stoppage lasted three weeks and nearly broke the company. Earl, watching his competitors steal customers while his unionized drivers walked picket lines, made a decision that would define Old Dominion's next seven decades: when the strike ended, he began planning the company's exit from union representation.

By 1950, Old Dominion had successfully decertified the union through a employee vote—a rarity in the trucking industry where the Teamsters wielded enormous power. The company now operated 50 trucks and had expanded its network throughout eastern Virginia. Earl had built something substantial, something that could survive without him.

He would need to. That same year, Earl Congdon Sr. died suddenly of a heart attack at age 57, leaving behind a thriving regional trucking company and a question: could a business this dependent on one man's relationships and reputation survive his loss?

III. The Lillian Era: Building Regional Dominance (1950-1962)

When Lillian Congdon walked into Old Dominion's Richmond office the morning after her husband's funeral, the room fell silent. In 1950, women didn't run trucking companies. They certainly didn't manage dozens of rough-edged drivers and negotiate with industrial customers. The betting money along the Richmond docks was that Old Dominion would be sold within six months.

They didn't know Lillian Congdon.

She had been keeping the company's books since day one, knew every customer by name, and understood the ICC's byzantine regulations better than most lawyers. More importantly, she had two sons—Earl Jr. and Jack—who had grown up in the business. Earl Jr., just 23, had been driving trucks since he was 16. Jack, 21, knew the maintenance shop inside and out. Lillian's first executive decision was to name herself president and bring her boys into management. Earl Jr. would handle operations; Jack would run maintenance and equipment.

The early 1950s tested this unconventional leadership team immediately. The Korean War created another military shipping boom, but also fuel shortages and equipment scarcities. While competitors struggled to keep trucks running, Jack Congdon's mechanical genius shined. He rebuilt engines other shops declared dead, fabricated parts that couldn't be bought, and kept Old Dominion's aging fleet operational through sheer ingenuity. The company's on-time delivery rate during the Korean conflict exceeded 95%—unheard of when parts shortages sidelined a third of the industry's trucks.

But Lillian's real genius emerged in 1957 with the acquisition of Bottoms-Fiske Trucking. Bottoms-Fiske wasn't just any carrier—they specialized in furniture hauling from High Point, North Carolina, the "Furniture Capital of the World." The company held ICC certificates for routes throughout the Carolinas and into Tennessee. More importantly, they had relationships with every major furniture manufacturer in the region.

The acquisition negotiations revealed Lillian's steel spine. When Bottoms-Fiske's owners tried to renegotiate terms at the last minute, assuming a woman would fold under pressure, she walked away from the table. Three days later, they called back and accepted her original offer. The $400,000 deal—financed through a combination of profits and Old Dominion's first bank loan—doubled the company's size overnight.

High Point became Old Dominion's new center of gravity. The furniture industry's unique shipping needs—careful handling, white-glove delivery service, complex multi-stop routes—demanded operational excellence that commodity freight haulers couldn't match. Old Dominion developed specialized equipment: air-ride suspensions to prevent damage, furniture pads and straps, drivers trained in residential delivery. The company charged premium rates and customers gladly paid.

Between 1957 and 1962, Old Dominion executed six more acquisitions, each carefully chosen for their route authorities and customer relationships. Barnes Trucking brought Virginia-to-Florida certificates. Nilson Motor Express opened up routes to Atlanta. Henderson Trucking provided access to Charleston and Savannah ports. Lillian orchestrated each deal, often negotiating directly with owners who underestimated the small woman in conservative dress—until they saw her command of financial details and regulatory requirements.

By 1962, Old Dominion operated 200 trucks and generated $8 million in annual revenue. The company had terminals in five states and employed over 400 people. The Congdon family had built something remarkable: a dense regional network with minimal competition on most routes, premium pricing power from specialized services, and a non-union workforce that provided flexibility unionized competitors couldn't match.

That year, recognizing that High Point had become the company's operational heart, Lillian made it official: Old Dominion relocated its headquarters from Richmond to a new 15-acre complex in High Point. The move symbolized a generational transition. At the dedication ceremony, Lillian announced that Earl Jr. would become president, with her remaining as chairman.

As Earl Jr. took the podium, he looked out at a company his parents built from nothing—and ahead to a trucking industry about to undergo revolutionary change.

IV. Pre-Deregulation Growth & The Chess Game (1962-1980)

Earl Congdon Jr. understood something his competitors missed: in the regulated trucking world of the 1960s and 70s, you weren't really in the transportation business—you were in the certificate accumulation business. Every ICC operating certificate was a license to print money on specific routes. The game wasn't about operational efficiency; it was about acquiring the right to serve profitable lanes before someone else did.

"We bought companies for their birthrights, not their trucks," Earl Jr. would later tell investors. Between 1969 and 1979, Old Dominion acquired eleven trucking companies, spending nearly $20 million on what amounted to pieces of paper granting permission to haul freight between specific cities. Each acquisition was a chess move in a complex geographic puzzle.

The 1969 purchase of Star Transport illustrates the strategy perfectly. Star was bleeding money, their equipment was junk, and their terminal was a converted barn. But they held certificates for Memphis-to-Birmingham and Birmingham-to-Atlanta—routes that connected Old Dominion's Carolina network to the booming Southeast corridor. Earl paid $800,000 for a company with $300,000 in assets. Wall Street would have called him crazy; the ICC's route protection made it genius.

The regulated environment created bizarre inefficiencies that Old Dominion exploited. A manufacturer in Greensboro shipping to Nashville might need three different carriers to complete a 400-mile journey, each handling their ICC-approved segment. Old Dominion methodically acquired certificates to eliminate these handoffs, offering single-carrier service at premium prices. Customers paid extra to avoid the hassle of coordinating multiple trucking companies and the damage that came from multiple loading/unloading cycles.

The 1979 Deaton Trucking acquisition marked a strategic departure. Deaton operated truckload and flatbed services—a different business model from Old Dominion's LTL network. Truckload meant one customer's freight filling an entire trailer, point-to-point. LTL meant consolidating multiple customers' partial loads, requiring terminals, sorting, and complex routing. Earl Jr. saw Deaton as a hedge: if deregulation came and destroyed LTL margins, perhaps truckload would survive.

Throughout the 1970s, whispers of deregulation grew louder. The Teamsters and established carriers lobbied frantically to preserve the status quo, warning of chaos, bankruptcies, and highway safety disasters. But economists and consumer advocates pushed back: regulation was costing Americans billions in inflated shipping costs. The ICC's route restrictions meant trucks often ran empty on return trips because they lacked authority to carry freight in both directions.

Earl Jr. played both sides masterfully. Publicly, Old Dominion joined industry associations opposing deregulation. Privately, he prepared for a radically different world. The company invested in technology—early computer systems for routing and billing. They expanded terminal capacity in anticipation of volume growth. Most importantly, they maintained the non-union status Earl Sr. had fought for, knowing labor flexibility would be crucial in a deregulated market.

The chess game accelerated in 1978-79 as deregulation became inevitable. Acquisition prices for operating certificates collapsed as sellers realized their monopolies were ending. Old Dominion went on a buying spree, acquiring six companies in eighteen months. They paid pennies on the dollar for route authorities that would still have value during the transition period.

By early 1980, Old Dominion operated 500 trucks, served eight southeastern states, and generated $45 million in revenue. The company ran 27 terminals and employed 1,200 people. They had built a regional powerhouse under the old rules—but Earl Jr. knew the old rules were about to be torched.

President Carter signed the Motor Carrier Act on July 1, 1980. The regulated trucking world—where profits came from government protection rather than operational excellence—officially ended. Within five years, 15,000 new carriers would flood the market. Rates would plummet 25%. A third of established trucking companies would disappear.

The revolution everyone feared had arrived. Earl Jr. saw it differently: "Deregulation didn't destroy the trucking industry," he'd say later. "It revealed who could actually run a trucking company."

V. Deregulation Revolution: Crisis & Opportunity (1980-1991)

The morning after President Carter signed the Motor Carrier Act, Earl Congdon Jr. called an all-hands meeting at Old Dominion's High Point headquarters. "Gentlemen," he began, looking at his terminal managers, "as of today, every two-bit operator with a truck and a phone can compete with us on any route. The government gravy train just ended. From now on, we win on service or we die."

The numbers were staggering. Within six months of deregulation, 5,000 new trucking companies entered the market. Shipping rates plummeted 20% in the first year alone. Established carriers, bloated by decades of protected profits, began hemorrhaging cash. Consolidated Freightways, once the industry titan, saw its stock price collapse 60%. McLean Trucking, a century-old company, began its death spiral.

But Earl Jr. had spotted opportunity in the chaos: the unionized carriers couldn't adapt. Their labor contracts, negotiated during the fat regulated years, mandated rigid work rules. A unionized dock worker couldn't drive a forklift without a grievance filing. A driver couldn't help unload freight without violating job classifications. The Teamsters had built a fortress of workplace protections that became a prison when flexibility meant survival.

Old Dominion's non-union workforce became a lethal competitive weapon. When a customer needed emergency pickup at 2 AM, Old Dominion's terminal manager could drive the truck himself. When freight patterns shifted, workers moved seamlessly between driving, dock work, and customer service. The company's labor costs ran 15-20% below unionized competitors—a massive advantage when every penny counted.

The Motor Carrier Act didn't just eliminate route restrictions; it allowed instant expansion. Old Dominion could now serve Florida, Tennessee, California, Dallas, and Chicago without seeking ICC approval. But Earl Jr. resisted the temptation to chase growth everywhere. Instead, he deployed a counter-intuitive strategy: density over geography.

While competitors rushed to offer coast-to-coast service, Old Dominion doubled down on the Southeast. They opened 27 new terminals between 1980 and 1985, but all within their existing footprint. The goal was shipment density—more freight per mile, more stops per route, more revenue per terminal. A dense network meant trucks ran fuller, fixed costs spread wider, and service times shortened. Customers in Charlotte might have five daily pickup options from Old Dominion versus two from a stretched-thin national competitor.

The company also pioneered hub-and-spoke operations in LTL. Freight would flow from local terminals to regional breakbulk facilities where shipments were sorted and reconsolidated for final delivery. It required massive capital investment—construction costs for a single breakbulk facility could exceed $10 million—but created network effects. Each new terminal made existing terminals more valuable by expanding destination options.

The strategy extracted a price. Old Dominion lost money in 1986 and 1987, the only unprofitable years in company history. Wall Street questioned whether a regional player could survive against emerging national giants. Employee morale wavered as competitors declared bankruptcy weekly. Earl Jr. mortgaged company properties to fund operations, betting everything on the network investment paying off.

The furniture division, once Old Dominion's crown jewel, became an albatross. Furniture manufacturing was shifting overseas, devastating High Point's factories. Specialized furniture hauling required expensive equipment that couldn't be repurposed for general freight. In 1989, Earl Jr. made the painful decision to exit the business his mother had built through the Bottoms-Fiske acquisition.

The Deaton subsidiary faced similar challenges. Truckload and flatbed operations required different equipment, different drivers, different customers. The operational complexity of running two distinct business models overwhelmed management bandwidth. In 1991, Old Dominion sold Deaton's general commodities and flatbed divisions, completing the transformation to a pure-play LTL carrier.

By 1991, the trucking industry bloodbath was ending. Of the top 50 LTL carriers in 1980, only 12 survived as independent companies. Old Dominion wasn't just among the survivors—they were thriving. Revenue had grown to $180 million. The terminal network had expanded to 47 facilities. Most importantly, the company had developed operational capabilities their union-constrained competitors couldn't match.

That year, Earl Jr. made another pivotal decision: Old Dominion would go public. The IPO would raise capital for expansion, provide liquidity for family members, and impose market discipline on operations. But it also meant quarterly earnings calls, activist investors, and pressure for growth that might compromise the company's careful strategy.

As Old Dominion prepared its IPO documents, a 26-year-old named David Congdon was working his way through the company's management training program. Earl Jr.'s son had started at the bottom—loading trucks on the night shift, learning every job in the terminal. The third generation was preparing to take the wheel, though nobody yet imagined how far David would drive the company his grandfather started with one truck.

VI. Going Public & The Super-Regional Strategy (1991-2000)

The Old Dominion team gathered in a conference room at Goldman Sachs on October 22, 1991, watching ODFL ticker symbols scroll across the screen for the first time. The IPO priced at $13 per share, raising $23 million. Earl Congdon Jr., now 64, had transformed his father's trucking company into a public corporation worth $115 million. But the real story wasn't the money—it was what Earl planned to do with it.

"We're not trying to be everything to everyone," Earl told the Wall Street analysts who questioned Old Dominion's regional focus. While FedEx was building a global empire and Consolidated Freightways chased transcontinental routes, Old Dominion pursued something different: super-regional dominance. They would own the Southeast and Mid-Atlantic so thoroughly that no competitor could match their service levels, creating what Earl called "density economics."

The math was compelling. In LTL trucking, profit margins expanded exponentially with route density. A truck stopping at three customers per hour instead of two didn't increase driver costs but added 50% more revenue. A terminal handling 100 shipments daily had the same overhead as one handling 50, but twice the gross profit to cover it. Every additional shipment in a geographic cluster made every existing shipment more profitable.

Wall Street didn't get it. Analysts wanted growth stories, national expansion, sexy acquisitions. Old Dominion's stock languished, trading between $11 and $15 for most of 1992-1994. But Earl Jr. and his team stayed disciplined, methodically filling in their regional network like a pointillist painting—each new terminal a dot that made the whole picture clearer.

The 1995 acquisition of Goggin Truck Line demonstrated the strategy perfectly. Goggin was tiny—just $12 million in revenue—but operated in precisely the Virginia and Maryland markets where Old Dominion needed density. Rather than buying a large carrier with overlapping routes, they acquired small, strategic pieces that enhanced network efficiency. The integration took six weeks; most customers never noticed the change except their service improved.

Then came the succession question nobody wanted to discuss. Earl Jr. was approaching 70, and while he remained sharp, the board pressed for transition planning. Jack Congdon had left the company years earlier to pursue other interests. That left David Congdon, Earl's son, who had spent six years rotating through every department, learning the business from the ground up.

In 1997, the board named David Congdon president at age 32. The promotion raised eyebrows—nepotism concerns, worries about his youth, questions about whether the third generation had the hunger of the first two. David's first all-company meeting addressed the elephant directly: "I know what you're thinking—the boss's kid got handed the keys. But I've loaded trucks at 3 AM in January. I've dealt with irate customers. I've driven routes when drivers called in sick. I'm not here because of my last name. I'm here because I believe we can build something special."

David brought something his father and grandmother hadn't possessed: technological vision. While Earl Jr. perfected operational blocking and tackling, David saw how technology could transform a fundamentally analog industry. His first major initiative was implementing a company-wide information system that tracked every shipment in real-time. The $8 million investment—massive for a company generating $300 million in revenue—put scanners in every driver's hands and computers in every terminal.

The technology push accelerated in 1999 when Old Dominion moved to new headquarters in Thomasville, North Carolina. The facility wasn't just offices—it was a command center with network monitoring, centralized dispatch, and customer service operations that could see every truck, every shipment, every delay across the entire system. Customers could track shipments online, revolutionary for an industry where "it's on the truck somewhere" had been standard for decades.

The Frederickson Motor Express acquisition in 1998 expanded Old Dominion into Texas and the Southwest, carefully extending the network while maintaining density discipline. The $23 million deal brought 12 terminals and Dallas-area coverage that connected Old Dominion's southeastern network to growing Texas markets. Unlike previous acquisitions focused on certificates and rights, Frederickson was about physical network—terminals in the right locations with room for expansion.

By 2000, Old Dominion's super-regional strategy was vindicated. Revenue reached $458 million. The operating ratio improved to 89.2%, approaching best-in-class territory. The stock, finally discovered by growth investors, quintupled from its IPO price. The company operated 82 terminals across 20 states—not the biggest footprint, but the densest, most efficiently run network in those markets.

As the new millennium began, three generations of Congdons had built something remarkable: a trucking company that competed on service, not price. But the real transformation was just beginning. David Congdon was about to demonstrate that operational excellence, pushed to its logical extreme, could turn a commodity business into a premium brand.

The dot-com boom was creating e-commerce giants that would reshape supply chains. September 11th would transform transportation security. The Great Recession would test every assumption about freight markets. Through it all, David would pursue a simple but radical strategy: what if a trucking company operated with the reliability of FedEx, the technology of a software company, and the customer service of Nordstrom?

VII. The David Congdon Era: Building the Premium Machine (2000-2018)

David Congdon stood before 500 terminal managers at Old Dominion's 2003 annual meeting and wrote three numbers on a whiteboard: 99, 0.1, and 85. "Ninety-nine percent on-time delivery," he said. "Zero-point-one percent claims ratio. Eighty-five percent operating ratio. These aren't aspirational targets. These are minimum acceptable standards. Any terminal that can't hit these numbers needs to explain why—or find new leadership."

The room went quiet. In LTL trucking, 95% on-time was considered excellent. A 0.5% claims ratio was industry-leading. An 85% operating ratio would make Old Dominion the most efficient carrier in America. David was demanding perfection in an industry that had accepted "good enough" for decades.

The transformation started with technology. In 2004, Old Dominion deployed handheld computers to every driver—a $12 million investment that competitors mocked as overkill. But the devices did more than track packages. They captured signature proof of delivery, photographed damaged freight, updated customers in real-time, and fed data to route optimization algorithms. A missed delivery wasn't discovered at day's end anymore; dispatch knew within minutes and could redirect another driver.

The routing algorithms themselves became a competitive weapon. Old Dominion hired PhDs from MIT and Stanford, paying Silicon Valley salaries to operations researchers who developed proprietary optimization models. The system considered traffic patterns, customer delivery windows, driver hours-of-service regulations, and fuel costs to create routes that shaved minutes off each stop. Minutes multiplied by thousands of daily stops meant millions in savings.

But technology was just an enabler. The real revolution was cultural—the institutionalization of what David called "the OD Way." Every employee, from dock workers to senior executives, attended quarterly training on service standards. Mystery shoppers called terminals posing as customers, scoring response times and problem resolution. Terminal managers' bonuses depended more on service metrics than profitability—a radical departure from industry norms.

The company's tagline, "Helping the World Keep Promises," wasn't marketing fluff—it was operational doctrine. When Hurricane Katrina devastated the Gulf Coast in 2005, Old Dominion kept terminals open using generators, sleeping bags for drivers, and helicopters to deliver critical supplies. Competitors shut down for a week; Old Dominion missed zero service days. Customers remembered.

The 2008 financial crisis tested every assumption. Freight volumes collapsed 30% in six months. Competitors slashed prices desperately, offering 40% discounts to fill empty trucks. The Old Dominion board pressed David to match pricing, warning that maintaining premium rates during a depression was suicide.

David refused. "We're not in the cheap freight business," he told the board. "We're in the reliability business. Customers who only care about price aren't our customers anyway." Old Dominion did lose volume—revenue dropped 15% in 2009—but maintained margins while competitors bled red ink. When the recovery came, customers who had switched to cheaper carriers came flooding back, frustrated by missed deliveries and damaged freight.

The discipline extended to capacity expansion. While competitors built terminals wherever they could find cheap land, Old Dominion spent millions extra to locate facilities optimally for network efficiency. A terminal might cost $2 million more to build five miles closer to customer clusters, but those five miles, multiplied by hundreds of daily routes over decades, justified the premium. The company maintained a five-year land bank, acquiring parcels years before needed, ensuring perfect positioning.

Network expansion accelerated after 2010, but always following the density playbook. Old Dominion entered California not with a splash but with surgical precision—first Los Angeles, then gradually expanding along logical freight lanes. By 2015, they served all 48 continental states, but the expansion took 15 years of methodical growth, never sacrificing service quality for geographic reach.

The numbers validated the strategy spectacularly. The operating ratio improved from 89% in 2000 to 81% by 2015—a 900 basis point improvement in an industry where 100 basis points was considered meaningful. On-time delivery reached 99.2%. Claims ratio dropped to 0.08%. Revenue per hundredweight—the industry's key pricing metric—exceeded competitors by 15-20%.

Family control enabled this long-term focus. While public company CEOs obsessed over quarterly earnings, David could make investments with five-year payoffs. When activists pushed for share buybacks or dividend increases, the Congdon family's 15% ownership stake provided insulation. The board included independent directors who understood trucking, not financial engineers seeking quick returns.

The cultural consistency across three generations was remarkable. Earl Sr.'s emphasis on reliability, Lillian's strategic thinking, Earl Jr.'s operational discipline—David synthesized them all while adding technological sophistication. Old Dominion promoted exclusively from within, ensuring cultural continuity. The average senior executive had 20+ years with the company. Terminal managers started as dock workers. This wasn't just employee retention; it was institutional memory preservation.

By 2018, Old Dominion had become the anomaly that proved the rule. In a commodity industry, they commanded premium prices. In a unionized sector, they remained union-free through superior treatment of employees. In a fragmented market with 50,000 competitors, they consistently gained share. Revenue reached $3.8 billion. The operating ratio touched 80%. The stock price had increased 50-fold since David became president.

But succession loomed again. David, now 53, had no children in the business. The board began considering external candidates for the first time in company history. The question wasn't just who could run operations—Old Dominion had plenty of capable executives. The question was who could maintain the cultural DNA that made Old Dominion different while adapting to whatever came next: autonomous trucks, Amazon's logistics ambitions, the next recession.

As 2018 ended, Old Dominion announced Greg Gantt, a 25-year company veteran who started as a regional manager, would become CEO. David would remain executive chairman. The fourth era of leadership—the first outside the Congdon direct line—was about to begin.

VIII. Modern Era: The Efficiency Frontier (2018-Present)

Greg Gantt stepped into the CEO role in May 2018 with a deceptively simple observation: "We've built the best LTL network in America. Now we need to prove it's recession-proof." The timing seemed odd—the economy was booming, freight volumes hitting records, and Old Dominion's stock touching all-time highs. But Gantt, who'd joined the company as a regional vice president in 1994 and worked his way up through operations, understood something his Wall Street analysts missed: Old Dominion's excellence hadn't been truly tested since becoming a premium carrier.

The first test came faster than anyone expected. In March 2020, as COVID-19 shutdowns froze the economy, Old Dominion faced an existential question: How does a premium-priced carrier survive when customers are desperately cutting costs? Competitors slashed prices 30-40%, offering pandemic discounts to fill empty trucks. The board pressed Gantt to match pricing, warning that maintaining premium rates during a depression was suicide.

Gantt's response defined his leadership: "We recognize the vital role we play in linking together the supply chain and delivery services for many of our customers that are manufacturing and distributing critically-needed items". Rather than cut prices, Old Dominion doubled down on service. When competitors closed terminals, Old Dominion kept all 237 service centers operational. The company spent $10.1 million on special employee bonus payments in March to non-executive employees "in appreciation for their extraordinary effort in responding to the COVID-19 pandemic".

The operational response was remarkable. Revenue per day fell 19.3% year-over-year in April 2020, but improved to only an 11.4% decline by June and just a 3% dip by July as manufacturers resumed operations. While volumes dropped, Old Dominion maintained its 99% on-time delivery standard when competitors were missing 20-30% of commitments due to staffing shortages and terminal closures.

The pandemic accelerated a trend Gantt had been pushing since 2018: operational automation not to replace workers but to multiply their effectiveness. Dock workers received tablets showing optimal loading patterns. Drivers got real-time rerouting based on delivery window changes. The dispatch system automatically adjusted for COVID closures, redirecting shipments before they became service failures. The technology investments, mocked as excessive in 2019, became competitive weapons in 2020.

But Gantt's real genius was recognizing that COVID created a once-in-a-generation market share opportunity. As struggling competitors retrenched, Old Dominion expanded its network by nine service centers in 2020, adding nearly 500 doors in Montana, Iowa, Texas, Arkansas, Indiana, Georgia, New York, and two in Illinois. Each facility was built with pandemic learnings: touchless entry systems, enhanced ventilation, space for social distancing, and excess capacity for volume surges.

The financial discipline during crisis was extraordinary. Despite pandemic challenges and a slight decrease in annual revenue, Old Dominion achieved a company-record operating ratio of 77.4% in 2020, contributing to double-digit growth in earnings per diluted share. While competitors burned cash, Old Dominion generated it, continuing share buybacks when most corporations suspended them entirely.

The January 24, 2022 addition to the Nasdaq-100 index validated the transformation—Old Dominion had evolved from a regional trucker to a technology-enabled logistics platform worthy of inclusion alongside America's most innovative companies. The index inclusion brought institutional ownership, analyst coverage, and a valuation multiple that finally reflected operational excellence.

Then came the ultimate leadership test. In January 2023, Gantt announced his retirement effective June 30, 2023, with Kevin "Marty" Freeman succeeding him as President and CEO on July 1, 2023. The transition exemplified Old Dominion's succession planning: Freeman had served as Executive Vice President and Chief Operating Officer since May 2018, with 45 years in the transportation industry and various positions in operations and sales since joining Old Dominion in February 1992.

Freeman inherited a different challenge than his predecessors. Not how to build excellence, but how to maintain it when everyone knew the playbook. Every competitor had studied Old Dominion's model. Private equity firms were consolidating smaller carriers to replicate the network density strategy. Amazon was building its own logistics network. Autonomous trucks threatened to eliminate driver cost advantages.

Freeman's response was subtle but profound: if operational excellence had become table stakes, cultural excellence would be the differentiator. He institutionalized what he called "the 99/99/99 standard"—99% on-time delivery, 99% damage-free, 99% accurate billing. But the real innovation was making these metrics personal. Every employee could see, in real-time, how their actions affected company-wide service levels. A dock worker in Charlotte could track how their loading efficiency impacted on-time delivery in Dallas.

The yield management discipline reached new sophistication under Freeman. LTL revenue per hundredweight, excluding fuel surcharges, increased 4.6% in Q3 2024 as the company maintained its long-term and disciplined approach to pricing. But this wasn't just rate increases—it was surgical pricing based on lane density, customer profitability, and capacity utilization. Some customers paid 30% premiums; others got discounts. The algorithm knew the difference.

The first quarter 2024 operating ratio of 73.5% improved direct operating costs as a percent of revenue through yield increases and ongoing operational efficiencies. By Q2 2024, the company achieved something remarkable: an operating ratio of 71.9%, best-in-class for the LTL industry. For context, this meant Old Dominion spent 72 cents to generate a dollar of revenue in one of the most capital-intensive industries in America—efficiency that would make software companies envious.

The numbers validated the strategy spectacularly. The company maintained its debt-to-equity ratio at just 0.04—essentially debt-free in an industry that typically leverages heavily. Return on equity hit 26.25%, return on invested capital reached 20.88%. The trailing P/E ratio of 29.52 might seem expensive, but for a trucking company generating tech-like returns with utility-like consistency, the premium was justified.

Throughout 2024, as recession fears mounted and freight volumes softened, Old Dominion demonstrated the resilience Gantt had built and Freeman had refined. While Q3 2024 financial results reflected ongoing economic softness and the first year-over-year quarterly revenue decrease, market share and volume trends remained consistent with the first half of the year while yield continued to improve. Even in a down market, Old Dominion gained share.

The modern Old Dominion operates 256 service centers across all 50 states, Canada, and Puerto Rico, employing over 23,000 people. But the real asset isn't the terminal network or the truck fleet—it's the institutional knowledge accumulated over 90 years, refined through three generations of leadership, and encoded in systems that make excellence repeatable.

As 2025 begins, Old Dominion faces new challenges: nearshoring driving different freight patterns, e-commerce demanding faster delivery times, environmental regulations requiring fleet electrification. But the company has proven something remarkable: in a commodity business, operational excellence pushed to its logical extreme becomes a moat. When everyone knows your strategy but no one can execute it, transparency becomes the ultimate competitive advantage.

IX. The Playbook: How to Win in Commoditized Industries

The Old Dominion story reads like a business school paradox: How does a company in the most commoditized industry imaginable—moving boxes from point A to point B—command premium prices, generate software-like margins, and create a competitive moat that deepens with transparency? The answer isn't one brilliant strategy but seven interconnected advantages that compound over decades.

The Non-Union Advantage: Flexibility as Strategy

Old Dominion's non-union status isn't just about labor costs—though paying 15-20% less than unionized competitors certainly helps. The real advantage is operational flexibility that union work rules prevent. When a shipment needs emergency redelivery at 10 PM, an Old Dominion terminal manager can drive the truck themselves. When freight patterns shift suddenly, workers move seamlessly between dock, driving, and customer service roles. During COVID, this flexibility meant the difference between maintaining 99% service levels and complete operational breakdown.

But here's the counterintuitive part: Old Dominion often pays more than union carriers. Drivers can earn $100,000+ annually. Benefits exceed industry standards. The company promotes exclusively from within, creating career paths from dock to C-suite. The result? Turnover rates half the industry average. When your competitive advantage depends on thousands of daily human decisions, employee stability becomes strategic.

Network Density Economics: The Compound Advantage

LTL trucking exhibits powerful network effects that most investors miss. Every additional shipment in a geographic cluster doesn't just generate incremental revenue—it makes every existing shipment more profitable. A truck serving five customers per route has the same driver cost as one serving three, but 67% more revenue. A terminal handling 200 shipments daily has similar overhead to one handling 100, but double the gross profit to cover it.

Old Dominion understood this mathematics before competitors. While others chased geographic coverage, Old Dominion built density. They'd rather own 30% market share in North Carolina than 5% share nationally. This density creates a virtuous cycle: more shipments per route → lower cost per shipment → ability to reinvest in service → win more shipments → increase density further.

The density advantage compounds. In markets where Old Dominion has 25%+ share, their operating ratio approaches 65%—margins that shouldn't exist in trucking. Competitors can't replicate this without massive capital investment and years of patient share building. By the time they achieve density in one market, Old Dominion has moved to the next.

Service as Differentiation: The 99/0.1 Standard

Old Dominion's service metrics seem impossible: 99% on-time delivery, 0.1% claims ratio. Industry averages run 94% and 0.5% respectively. But those five percentage points of service difference justify 15-20% price premiums. For a manufacturer shipping $50,000 of products, paying $500 extra to ensure arrival is cheap insurance.

The service standard creates selection effects. Price-sensitive customers who'll switch carriers for 5% savings self-select away from Old Dominion. Quality-conscious customers who value reliability concentrate with them. Over time, Old Dominion's customer base becomes less price-sensitive, more stable, and more profitable—allowing further service investments.

Technology amplifies service advantages. Every shipment is tracked in real-time. Delays are communicated proactively. Delivery windows are guaranteed. But technology isn't the differentiator—every carrier has tracking systems. The differentiator is 23,000 employees culturally programmed to prioritize service over efficiency. That's not teachable in a training program; it's built over generations.

Capital Allocation Excellence: Patient Capital, Explosive Returns

Old Dominion's capital allocation seems boring: build terminals, buy trucks, upgrade technology. No flashy acquisitions, no diversification adventures, no financial engineering. But the discipline is the strategy. Every dollar invested must clear a 20% ROIC hurdle. Projects are evaluated over 10-year horizons. Short-term earnings are sacrificed for long-term competitive position.

Consider terminal placement. Old Dominion pays 20-30% premiums for locations five miles closer to customer clusters. Over a 20-year terminal life, those five miles, multiplied by hundreds of daily routes, generate millions in fuel and time savings. Competitors locate terminals wherever land is cheap. The difference compounds annually.

The company maintains a five-year land bank, acquiring parcels years before needed. They'll hold empty land for a decade waiting for the right moment. When expansion time comes, the terminal is perfectly positioned. Competitors scramble for available sites, accepting suboptimal locations that handicap operations forever.

Family Control with Public Market Discipline

The Congdon family's 15% ownership stake provides insulation from short-term market pressures while public listing enforces discipline. This balance enables strategies that purely public or private companies couldn't execute. Investing through recessions, maintaining premium pricing during downturns, accepting lower growth for higher quality—these decisions require patient capital.

But family control doesn't mean nepotism. David Congdon worked night shifts loading trucks before becoming CEO. Greg Gantt and Marty Freeman rose through operations over decades. The board includes independent directors with deep industry knowledge. Family ownership aligns with long-term value creation, not family employment.

Cultural Consistency Across Three Generations

Culture is Old Dominion's most powerful and least replicable advantage. Three generations of leadership have maintained consistent values: reliability, employee respect, operational excellence, financial discipline. These aren't poster slogans but daily operating principles embedded in every process.

New employees undergo weeks of training—not just on procedures but on why things are done the Old Dominion way. Veterans tell stories of deliveries made during hurricanes, of employees buying parts with personal credit cards to keep trucks running, of terminal managers working Christmas Eve to ensure shipments arrive. These stories become organizational mythology that shapes behavior.

The culture is reinforced through measurement. Every employee knows their terminal's on-time percentage, claims ratio, and operating ratio. Performance reviews weight service metrics equally with financial results. Bonuses depend more on customer satisfaction than profitability. Over time, employees who prioritize service over shortcuts self-select into Old Dominion; those who don't self-select out.

The Power of Saying No: Yield Over Volume

Old Dominion's most controversial strategy is rejecting business. They'll turn away million-dollar accounts that demand unsustainable pricing. They'll refuse shipments that compromise network efficiency. They'll exit customer relationships that create operational complexity. In trucking, where filling empty capacity seems logical, saying no seems insane.

But selectivity creates virtuous cycles. Premium pricing attracts premium customers. Stable customers enable better planning. Better planning improves service. Better service justifies premium pricing. The cycle continues. Meanwhile, competitors accepting any freight at any price create operational chaos that degrades service, forcing them to discount further.

The discipline extends to growth. Old Dominion could double revenue tomorrow by cutting prices 20%. They could acquire struggling competitors for pennies on the dollar. They could expand internationally. They don't. Growth must enhance the network, not dilute it. Revenue that weakens density or service is revenue not worth having.

The Synthesis: Compound Advantages

Each advantage reinforces others. Non-union flexibility enables superior service. Superior service justifies premium pricing. Premium pricing funds network investment. Network density reduces costs. Lower costs enable service investment. The flywheel accelerates.

Competitors can copy pieces but not the system. They can build terminals but not density. They can buy technology but not culture. They can cut prices but not achieve costs. They can promise service but not deliver it consistently. By the time they replicate one advantage, Old Dominion has strengthened others.

The ultimate proof is transparency. Old Dominion publishes detailed operational metrics. Executives explain strategies on earnings calls. The playbook is public. Yet no competitor has successfully replicated it. When everyone knows your strategy but can't execute it, you've built something special.

This is the Old Dominion paradox resolved: In commoditized industries, operational excellence isn't just an advantage—it's the only sustainable advantage. Everything else can be copied, acquired, or engineered. But excellence, built over generations and embedded in culture, becomes a moat that widens with time.

X. Competition & Industry Dynamics

The LTL industry looks deceptively simple from the outside: dozens of carriers moving partial truckloads between cities, competing primarily on price and transit time. But underneath this commodity surface lies one of the most complex competitive dynamics in American business—a game where scale advantages battle network effects, where regional density trumps national reach, and where Old Dominion has somehow figured out how to win consistently against larger, better-capitalized competitors.

The Competitive Landscape: David Among Goliaths

FedEx Freight, with $9.4 billion in revenue, towers over Old Dominion's $5.9 billion. XPO Logistics leverages sophisticated technology and Wall Street financial engineering. UPS's logistics network spans the globe. Yet Old Dominion generates superior margins, commands premium pricing, and consistently wins market share from these giants. Understanding why requires examining each competitor's structural disadvantages.

FedEx Freight emerged from the 2001 acquisition of American Freightways and Viking Freight, bolted onto FedEx's express delivery network. The promise was synergy—shared terminals, integrated systems, customer cross-selling. The reality was complexity. FedEx Freight operates as a division within a conglomerate, competing for capital with express delivery, ground services, and international operations. When FedEx needs quarterly earnings, Freight faces pressure to cut costs or push volume—decisions that compromise long-term positioning.

XPO represents modern trucking: algorithm-driven, acquisition-assembled, financially optimized. Since 2011, XPO has acquired 17 companies, creating the second-largest LTL network through consolidation. But cultural integration takes decades, not quarters. XPO operates with dozen different legacy systems, conflicting operational procedures, and varying service standards across regions. While XPO talks about technology transformation, drivers still struggle with basic routing inconsistencies from incompatible platforms.

The unionization divide creates the industry's starkest competitive boundary. ABF Freight, once Old Dominion's superior, remains shackled by Teamster work rules negotiated in the regulated era. Yellow Corporation (formerly YRC), despite multiple restructurings and concessions, couldn't escape union constraints and declared bankruptcy in 2023—eliminating the industry's third-largest player and creating a generational market share opportunity.

Why Consolidation Creates Opportunity

Traditional economics suggests industry consolidation advantages incumbents. Fewer competitors means rational pricing. Scale economies favor the largest players. But LTL trucking inverts this logic. Every consolidation creates integration challenges, service disruptions, and customer defection opportunities. Old Dominion has built its modern network largely by capturing share from consolidating competitors.

When XPO acquired Con-way Freight in 2015 for $3 billion, the integration took three years. Systems didn't communicate. Terminals had different procedures. Customers experienced service failures. Old Dominion quietly captured $200 million in revenue from defecting Con-way customers—growth that required zero acquisition cost, came with premium pricing, and enhanced network density.

Yellow's 2023 bankruptcy created the largest disruption in LTL history. $5 billion in freight needed new carriers overnight. While competitors scrambled to absorb volume, Old Dominion cherry-picked profitable lanes that enhanced network density. They rejected 70% of available Yellow freight, accepting only shipments that fit their network design and service standards. The selectivity seemed irrational—until Q3 2024 results showed margin expansion despite industry overcapacity.

The Amazon Threat That Never Materialized

For a decade, industry observers warned that Amazon would disrupt LTL trucking like it disrupted retail. The company had capital, technology, and logistics expertise. Amazon's delivery network already rivaled UPS and FedEx for last-mile service. Expanding into middle-mile LTL seemed inevitable.

But LTL trucking proved resistant to Amazon's playbook. Unlike parcel delivery, where standard boxes move through centralized hubs, LTL requires handling heterogeneous freight—pallets of chemicals, crates of machinery, rolls of carpet. Each shipment needs different equipment, handling procedures, and expertise. Amazon's technology advantages evaporated when facing the physical complexity of mixed freight.

More importantly, LTL economics don't fit Amazon's model. Building a competitive network requires thousands of terminals, tens of thousands of trucks, and decades of density building. Amazon could lose billions subsidizing market entry—but for what? LTL margins, even at Old Dominion levels, pale compared to cloud computing or advertising. The return on invested capital doesn't justify the investment, especially when organic growth opportunities exist elsewhere.

Amazon's retreat validated Old Dominion's strategy. In 2022, Amazon quietly shut down its LTL pilot program after two years of testing. The company that disrupted everything from bookstores to cloud computing couldn't crack regional trucking. Physical networks, it turns out, are harder to disrupt than digital ones.

Regulatory Advantages and Challenges

Deregulation created the modern LTL industry, but remnants of regulation still shape competition. The Federal Motor Carrier Safety Administration's Compliance, Safety, Accountability (CSA) program scores carriers on safety metrics. Hours-of-service rules limit driver time. Environmental regulations mandate equipment upgrades. These rules create barriers to entry that protect incumbents.

Old Dominion turns regulatory compliance into competitive advantage. Their CSA scores rank in the top decile, enabling better insurance rates and customer confidence. Investment in new equipment ahead of environmental mandates avoids disruption when regulations take effect. Electronic logging devices, mandated in 2017, were installed years earlier, allowing operational optimization while competitors scrambled for compliance.

But regulations also create challenges. California's AB5 law, attempting to reclassify independent contractors as employees, threatens the owner-operator model many competitors rely on. While Old Dominion uses company drivers, reducing flexibility for competitors potentially reduces industry capacity, creating upward pricing pressure that benefits all carriers.

Technology Disruption: Autonomous Trucks and Digital Freight

Autonomous trucks promise to revolutionize trucking by eliminating driver costs—typically 30-40% of operating expenses. Companies like TuSimple, Waymo, and Aurora are testing self-driving trucks on highways. The technology works for long-haul truckload—point-to-point highway driving. But LTL trucking presents unique challenges.

LTL requires complex urban navigation, multiple daily stops, and customer interaction. Drivers don't just drive; they manage freight, handle documentation, solve delivery problems. A robot can drive a truck on a highway. It can't navigate a congested loading dock, negotiate with receiving clerks, or reconfigure loads when customers change requirements. The last mile—where LTL complexity concentrates—remains stubbornly human.

Digital freight brokers like Convoy and Uber Freight promised to eliminate inefficiency through algorithmic matching. But they focus on truckload, where standardized point-to-point moves fit algorithmic optimization. LTL's complexity—partial loads, multiple stops, specialized handling—resists commoditization. Old Dominion's service differentiation becomes more valuable as digital platforms commoditize basic trucking.

The Moat: Why It's So Hard to Replicate ODFL

Every strategic consultant can diagram Old Dominion's model: network density, service excellence, operational efficiency, cultural consistency. The playbook is public. The metrics are published. The strategy is transparent. Yet no competitor has successfully replicated it. Why?

Time is the crucial ingredient. Network density takes decades to build. Culture develops over generations. Operational excellence requires millions of small improvements compounded daily. Customer relationships deepen through thousands of successful deliveries. These advantages can't be acquired, only earned.

Capital isn't enough. XPO spent billions on acquisitions without achieving Old Dominion's margins. Technology isn't sufficient. Every carrier has routing software and tracking systems. Scale doesn't guarantee success. FedEx Freight's larger network generates lower returns.

The real moat is systematic execution. Old Dominion makes fewer mistakes. Their trucks break down less frequently. Freight gets damaged less often. Deliveries arrive more predictably. Bills are more accurate. Each advantage seems minor—1% better here, 2% improvement there. But compound these advantages across millions of annual shipments, and the gap becomes insurmountable.

Competition in LTL trucking isn't about grand strategy or brilliant innovation. It's about doing ordinary things extraordinarily well, consistently, at scale, forever. Old Dominion has institutionalized this discipline. Competitors know what to do. They just can't do it.

XI. Bear vs. Bull Case

The Bear Case: Why Old Dominion Might Stumble

Economic Sensitivity: The Achilles' Heel

LTL trucking is ultimately a derived demand business—when factories produce less, retailers stock less, and shipments decline. Old Dominion's premium model amplifies this sensitivity. In recessions, customers switch from premium reliability to cheap capacity. The company's Q2 2009 revenue dropped 22% during the Great Recession, and while margins held better than competitors, the volume decline was brutal.

The next recession could be worse. Old Dominion now trades at 29.5x earnings versus 15x in 2009. Investor expectations have shifted from "cyclical trucker" to "quality compounder." A 20% revenue decline—normal in trucking downturns—would shatter the narrative. The stock wouldn't just decline with earnings; the multiple would compress simultaneously. A 40-50% stock price decline is conceivable even if operations remain sound.

Valuation Premium: Priced for Perfection

At 29.5x trailing earnings, Old Dominion trades at twice the S&P 500 multiple and five times typical trucking valuations. The market prices Old Dominion like a software company with 90% gross margins and zero capital requirements. But this is still trucking: capital-intensive, labor-dependent, economically sensitive. Even best-in-class execution can't repeal industry physics.

The valuation assumes continuous market share gains, perpetual margin expansion, and seamless succession planning. Any disappointment—a quarter of margin compression, share loss to a competitor, integration challenges from an acquisition—could trigger multiple compression. When a stock trades at perfection pricing, even minor imperfection creates major drawdowns.

Succession Risk: The Fourth Generation Question

David Congdon built the modern Old Dominion. Greg Gantt institutionalized excellence. Marty Freeman maintains momentum. But Freeman is 63, and the fourth generation of leadership remains undefined. The company promotes from within, but internal candidates lack the founder DNA that drove previous transitions. For the first time, Old Dominion might need external leadership.

Culture is fragile. One bad CEO hiring, one quarter of prioritizing earnings over service, one strategic acquisition that doesn't integrate—and decades of accumulated advantages begin eroding. Walmart struggled for years after Sam Walton. IBM never recovered its dominance post-Watson. Family businesses face unique succession challenges when family involvement ends.

Competitive Dynamics: The Replication Risk

Every Old Dominion innovation eventually gets copied. Electronic logging? Industry standard. Route optimization? Everyone has it. Premium pricing for premium service? XPO and FedEx are attempting the same strategy. As competitors close operational gaps, Old Dominion's differentiation narrows.

Private equity is consolidating regional carriers to build Old Dominion replicas. With Yellow's bankruptcy, billions in capital are chasing LTL opportunities. A well-funded competitor could build density in specific regions, cherry-pick Old Dominion's best lanes, and compete directly on service. It would take years and billions in losses, but Amazon proved that patient capital can disrupt seemingly impregnable positions.

The Bull Case: Why Old Dominion Keeps Winning

Best Operator in a Growing Industry

E-commerce fundamentally changed freight patterns. Instead of full truckloads to stores, retailers need partial loads to fulfillment centers. Manufacturing reshoring increases domestic freight. Just-in-time inventory requires reliable LTL service. These secular trends favor LTL over truckload and premium service over basic capacity.

Old Dominion captures disproportionate growth. In expanding markets, they win share through superior service. In declining markets, weaker competitors fail first. The company has gained share for 20 consecutive years across multiple economic cycles. Market share increased from 3% in 2000 to 12% today, with runway to 20%+ given service advantages.

Inflation Hedge with Pricing Power

Old Dominion's premium positioning enables price increases that exceed cost inflation. When driver wages rise 5%, Old Dominion raises rates 6-7% and customers accept it. When fuel spikes, surcharges pass through immediately. When capacity tightens, premium service commands premium pricing. The company essentially indexes revenue to inflation while controlling cost growth through efficiency.

This pricing power creates operating leverage. A 3% price increase on 80% incremental margins drops straight to the bottom line. In inflationary environments, Old Dominion's earnings grow faster than inflation. The 71.9% operating ratio has room for improvement—best-in-class rail operates at 60%. Even 200 basis points of margin expansion would increase earnings 30%.

Market Share Runway

Yellow's bankruptcy removed $5 billion in capacity. Customer freight needs rebidding. Service requirements are rising. Old Dominion could double market share and still have room for growth. At 12% share in a $90 billion market, the company generates $5.9 billion in revenue. At 20% share—achievable given competitive dynamics—revenue reaches $18 billion without market growth.

The share gain math is compelling. Every 100 basis points of share equals $900 million in revenue. At 28% incremental margins, that's $250 million in operating profit. The company needs just 2% annual share gains to drive double-digit earnings growth regardless of economic conditions.

Financial Analysis: The Numbers That Matter

ROIC: The Ultimate Scorecard

Old Dominion's 20.88% return on invested capital seems impossible for trucking. Competitors generate 5-10%. The spread reflects operational excellence converting to financial excellence. Every dollar invested generates 21 cents of annual profit—in perpetuity. At these returns, growth creates enormous value.

The ROIC remains stable across cycles. During 2020's pandemic disruption, ROIC stayed above 18%. In 2009's recession, it exceeded 15%. This stability suggests structural advantages, not cyclical luck. When a capital-intensive business generates consistent 20% returns, the market appropriately awards premium valuations.

Margins: Room for Expansion

The 71.9% operating ratio represents the industry's best margins, but improvement remains possible. Driver utilization could increase through better routing. Terminal automation could reduce handling costs. Network density in newer markets will improve. Management targets a 70% operating ratio—achievable given current trajectory.

Each 100 basis points of margin improvement increases earnings 8-10%. The path from 72% to 70% operating ratio would grow earnings 20% without any revenue growth. Combined with market share gains, earnings could compound at 15%+ annually for years.

Growth Algorithm

Old Dominion's growth formula is straightforward:

- GDP growth: 2-3%

- Market share gain: 2-3%

- Yield improvement: 3-4%

- Operating leverage: 2-3%

- Total earnings growth: 10-15%

This algorithm has worked for two decades. Nothing suggests it stops working. As long as the economy grows, freight moves, and service matters, Old Dominion compounds value.

Why the Premium Multiple Might Be Justified

Trucking companies typically trade at 10-15x earnings because they're cyclical, capital-intensive, and undifferentiated. Old Dominion has proven it's different. The company generates ROIC comparable to software companies. Margins expand continuously. Market share grows regardless of economic conditions. The business is essentially a subscription model—customers rarely leave.

At 29.5x earnings, Old Dominion isn't expensive if earnings compound at 12-15% annually. The multiple seems high versus trucking but reasonable versus quality compounders. Costco trades at 35x. Copart at 40x. Best-in-class operators in mundane industries command premium multiples.

The debt-free balance sheet provides downside protection. Book value exceeds $40 per share. Replacement cost of the terminal network approaches $100 per share. In severe recession, the stock has fundamental support. The upside remains multiples of current price if execution continues.

The bear case is real—recession risk, valuation concerns, succession challenges. But the bull case is compelling—best operator, growing industry, expanding margins, massive runway. For long-term investors who understand the power of compound operational advantages, Old Dominion represents a rare opportunity: buying the Berkshire Hathaway of trucking before everyone realizes that's what it is.

XII. Lessons & Looking Forward

What Founders Can Learn from Three Generations of Congdons

The Old Dominion story offers a masterclass in multi-generational business building, but not in the way most founder hagiographies unfold. There was no lightning-bolt moment of invention, no venture capital rocket ship, no overnight transformation. Instead, three generations of Congdons built wealth through something unfashionable in Silicon Valley: patient operational excellence in an unsexy industry.

Earl Sr. started with desperation, not vision. He needed to feed his family during the Depression, and hauling freight between Richmond and Norfolk was marginally better than unemployment. But he understood something profound: in commoditized industries, reliability is the only differentiator that matters. When your truck absolutely will deliver on time, customers pay premiums. That insight, discovered through necessity in 1934, drives billions in value today.

Lillian Congdon demonstrated that succession doesn't require a male heir or an MBA. When Earl Sr. died, she could have sold to competitors offering quick cash. Instead, she ran operations while training her sons, executed strategic acquisitions that doubled the company's size, and relocated headquarters to capture better opportunities. Her 12-year tenure proved that pragmatic execution beats grand strategy.

Earl Jr. mastered the metagame. While competitors focused on operations, he understood that regulated trucking was actually about accumulating certificates—government-granted monopolies. He spent millions buying worthless companies with valuable route rights. When deregulation arrived, he'd assembled a network that would cost billions to replicate. The lesson: sometimes the real game isn't the obvious game.

David Congdon's contribution was synthesis. He combined his grandfather's operational focus, grandmother's strategic thinking, and father's network building with modern technology. But his real innovation was cultural institutionalization—making excellence systematic rather than dependent on individual heroics. Great founders build great companies; generational founders build systems that outlast them.

The Paradox of Winning Through Operational Excellence

Old Dominion violates modern business strategy. They don't disrupt. They don't innovate business models. They don't platform, network effect, or winner-take-all. They just execute basic trucking better than anyone else, every day, forever. In a world obsessed with differentiation, they prove that operational excellence is differentiation.

The paradox deepens: their strategy is completely transparent. Every earnings call details their approach. Competitors can visit terminals, hire employees, copy processes. Yet the gap widens. Why? Because operational excellence isn't a strategy you implement; it's a capability you build over decades through millions of small decisions that compound.

Consider Old Dominion's IT system. It's not revolutionary—tracking packages, optimizing routes, managing billing. Every competitor has similar software. But Old Dominion's system reflects 30 years of incremental refinements. Each edge case handled, every exception coded, all processes integrated. A competitor can buy the same software platform but not the institutional knowledge embedded in configuration.

This creates a profound moat: advantages visible to everyone but replicable by no one. It's like publishing your chess strategy while playing at grandmaster level—knowing the moves doesn't mean you can execute them. Old Dominion has institutionalized grandmaster-level execution in trucking.

Future Scenarios: Recession, Automation, New Competition

The Next Recession: Stress Test or Breaking Point?

The next recession will test whether Old Dominion has truly transcended trucking cycles. Bears expect 30% volume declines and margin collapse. Bulls believe the company will gain share as weak competitors fail. History suggests both are partially right—volumes will decline, margins will compress, but Old Dominion will emerge stronger.

The company's response playbook is proven: maintain service standards, avoid desperation pricing, invest counter-cyclically. When competitors cut driver pay, Old Dominion maintains wages to retain talent. When others defer maintenance, Old Dominion keeps trucks pristine. Short-term earnings suffer, but competitive position strengthens. The stock will tank—perhaps 40-50%—creating generational buying opportunity for those who understand the strategy.

Automation: Threat or Opportunity?

Autonomous trucks are coming, but not how futurists imagine. Highway autopilot will arrive first, allowing drivers to rest during long segments. This helps truckload carriers more than LTL. Urban delivery automation remains decades away—too many variables, too much liability, too little economic incentive.

Old Dominion will adopt automation pragmatically. They'll test autonomous yard vehicles moving trailers between dock doors. They'll deploy routing algorithms that approach theoretical efficiency. They'll use predictive maintenance to prevent breakdowns. But humans will remain central because LTL trucking is ultimately a service business requiring judgment, flexibility, and customer interaction that robots can't provide.

New Competition: The Threat From Where?

The next competitive threat won't come from traditional truckers or tech giants but from an unexpected angle. Perhaps a Chinese logistics company expanding globally. Maybe a private equity roll-up achieving critical mass. Possibly a customer like Amazon insourcing their LTL needs and selling excess capacity.

But Old Dominion has survived every previous competitive wave: regulation, deregulation, consolidation, technology disruption, pandemic chaos. Their response remains consistent—focus on service, maintain discipline, let competitors make mistakes. It's boring. It's predictable. It works.

The Next Decade for ODFL

By 2035, Old Dominion will likely be a radically different company operating the same basic business. Revenue should reach $12-15 billion through market share gains. The operating ratio might touch 70%, generating 30% margins in trucking. International expansion seems inevitable—Canada and Mexico first, then following customers globally.

The terminal network will densify rather than expand. Instead of 250 terminals serving 50 states, expect 400 terminals creating unprecedented route density. Service standards will tighten—99.5% on-time, 0.05% claims. Price premiums will widen as service gaps grow. The company might acquire selectively—buying terminals and route density, not competitors.

Technology will embed deeper but remain invisible. Customers won't know their shipment was routed by AI, loaded by algorithm, delivered via optimized sequence. They'll just know it arrived on time, undamaged, as promised. The technology will be table stakes; the execution will remain differentiated.

Leadership transition remains the wildcard. Will the fourth generation maintain culture? Can external executives preserve what makes Old Dominion special? The company's history suggests they'll navigate succession successfully—they've done it three times before.

The stock will be volatile. Multiple compression during recessions, expansion during growth. Bears will perpetually warn about valuation. Bulls will point to execution. Long-term owners will compound wealth. The story continues.

The Lesson That Matters

Old Dominion proves something profound: in business, execution beats strategy. Not the execution of launching products or closing deals, but the daily execution of basic operations, repeated millions of times, improved continuously, forever. It's not sexy. It won't get Harvard Business School case studies. But it builds generational wealth.

In a world racing toward disruption, Old Dominion succeeds through consistency. While competitors chase the next big thing, they perfect the current thing. When everyone zigs toward technology, they zag toward service. As industries digitize and virtualize, they prosper through physical network effects.

The ultimate lesson isn't about trucking. It's about finding an essential service, executing it exceptionally, and compounding advantages over time. Whether you're building software or hauling freight, the principles remain: operational excellence, cultural consistency, patient capital, and the discipline to say no to good opportunities that compromise great ones.

Old Dominion will never be Apple or Amazon. They won't revolutionize industries or change how we live. They'll just keep delivering packages on time, every time, better than anyone else. In a world of moonshots and unicorns, sometimes the biggest opportunity is doing ordinary things extraordinarily well. That's the Old Dominion way. After 90 years, it's still working.

XIII. Recent News**

Q4 2024 Results: Weathering the Storm**

Old Dominion's fourth quarter 2024 results reflected ongoing economic softness, with revenue declining 7.3%. However, market share remained relatively consistent, and the company continued operating efficiently while maintaining best-in-class service, achieving 99% on-time performance and a cargo claims ratio below 0.1%.

The operating ratio deteriorated to 75.9%, up 410 basis points year-over-year, as revenue declines created deleveraging effects on operating expenses. Miscellaneous expenses increased 110 basis points due primarily to lower gains on property and equipment disposal.

Despite challenges, Old Dominion returned substantial capital to shareholders, utilizing $967.3 million for share repurchases in 2024, including a $200 million accelerated share repurchase settled in Q4, and paying $223.6 million in cash dividends.

2025 Capital Investment Strategy: Strategic Restraint

Looking ahead to 2025, the company initially planned capital expenditures of $575 million, including $300 million for real estate and service center expansion, $225 million for tractors and trailers, and $50 million for information technology.

However, by Q1 2025, the company reduced its aggregate capital expenditure plan to $450 million—a $125 million reduction—now including $210 million for real estate projects, $190 million for equipment, and $50 million for technology and other assets.

Management explained the capex deferral noting their real estate portfolio operates at 30% capacity following the downturn. Growth could rebound later in the year, which would increase capacity utilization.

Q1-Q2 2025: Persistent Headwinds