EQT Corporation: The American Natural Gas Giant's Evolution

I. Introduction & Episode Roadmap

Picture this: Deep beneath the rolling hills of Pennsylvania and West Virginia lies an ancient ocean of energy, trapped in microscopic pores of shale rock for millions of years. Above ground, in a gleaming Pittsburgh headquarters, executives at EQT Corporation orchestrate the most sophisticated natural gas extraction operation in America. This is a company that pumps out 6% of the entire nation's natural gas supply—enough energy to heat 20 million homes through brutal winters. If EQT were a country, it would rank as the world's 12th largest natural gas producer, ahead of nations like Qatar and Algeria.

Yet just fifteen years ago, EQT was a regional utility company most Americans had never heard of. The transformation from local gas distributor to energy colossus didn't happen through luck or timing alone—it required betting the company on unproven technology, surviving a hostile takeover by the very executives they'd acquired, and revolutionizing how natural gas is extracted from rock formations two miles underground.

This is the story of how a 136-year-old company founded by George Westinghouse to light Pittsburgh's street lamps became the most efficient natural gas producer in America. It's a tale of three distinct eras: the century-long foundation as a regional utility, the dramatic pivot into shale production that nearly destroyed the company, and the operational renaissance under new leadership that transformed EQT into what Morgan Stanley calls "the Saudi Aramco of natural gas."

The narrative arc bends through deregulation battles, technological breakthroughs in horizontal drilling, multi-billion dollar acquisitions that went sideways, and one of the most dramatic proxy fights in corporate history. Along the way, we'll explore how commodity businesses create lasting value, why vertical integration matters in cyclical industries, and what happens when operational excellence becomes a genuine competitive moat.

What makes EQT particularly fascinating isn't just its scale—it's the company's ability to repeatedly reinvent itself. From Westinghouse's 19th-century utility to today's algorithmic drilling operations, EQT has navigated every major energy transition while somehow emerging stronger. The question isn't whether natural gas has a future in America's energy mix—it's whether anyone can challenge EQT's dominance in providing it.

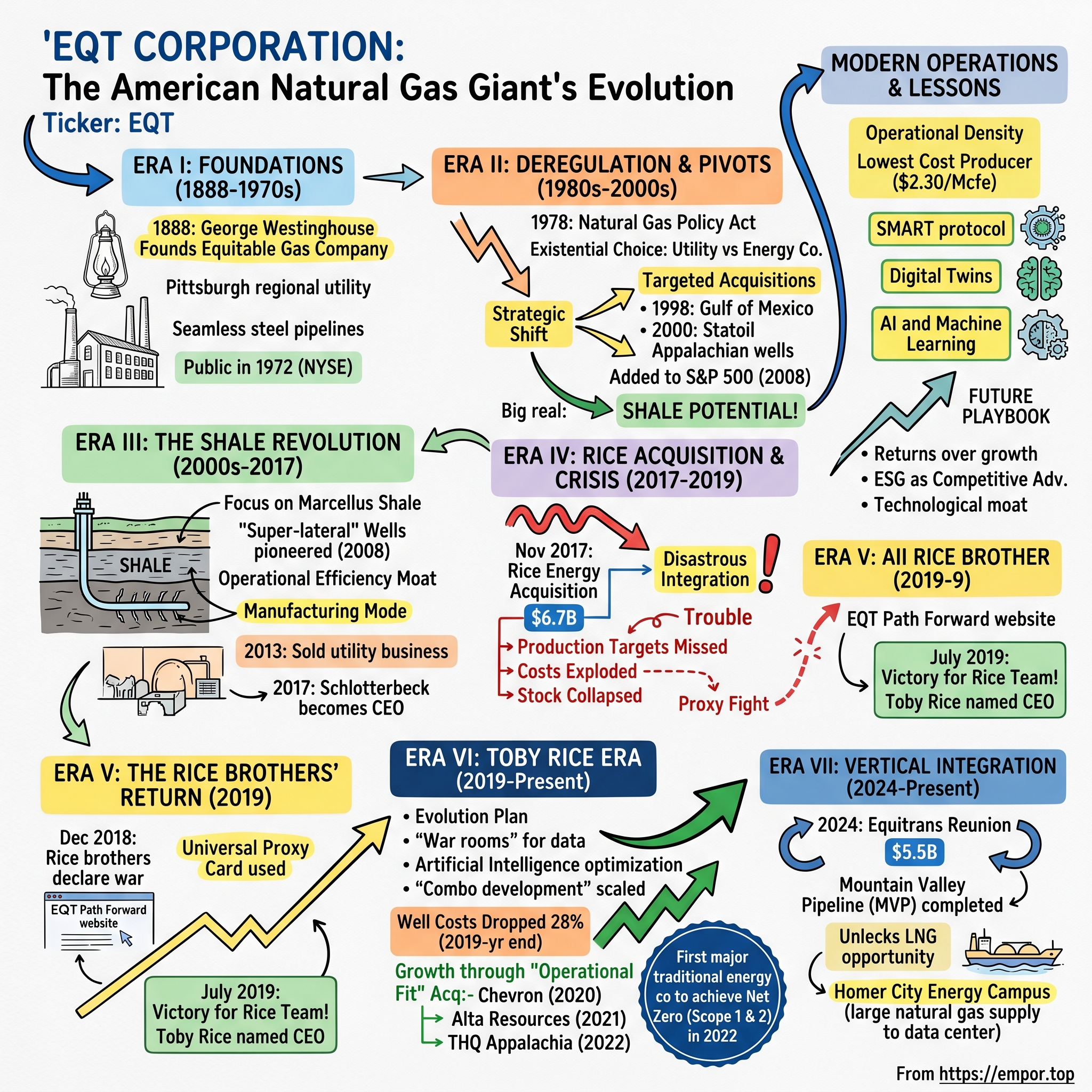

II. Origins: The Westinghouse Legacy & Early Years (1888–1970s)

The year was 1888, and George Westinghouse had a problem. The inventor who'd revolutionized railroad safety with the air brake and would soon wage the "War of Currents" against Thomas Edison needed fuel for his industrial ambitions in Pittsburgh. Coal smoke already choked the city's air, earning it the nickname "Hell with the lid off." Natural gas—clean-burning and efficient—offered an elegant solution, but only if someone could reliably extract and distribute it.

So Westinghouse did what titans of industry do: he created his own solution. On a humid July day, he founded the Equitable Gas Company with $5 million in capital, an astronomical sum for the era. The company's charter was simple yet ambitious—to "mine for, produce, deal in, transport and distribute natural gas." Within months, Equitable's crews were laying cast-iron pipes beneath Pittsburgh's cobblestone streets, connecting businesses and homes to gas wells dotting the countryside.

Westinghouse brought his inventor's mindset to the natural gas business. While competitors used primitive wooden pipes that leaked constantly, Equitable pioneered seamless steel pipelines that could handle higher pressures. The company developed early pressure regulators—descendants of Westinghouse's railroad brake technology—that prevented explosions in customers' homes. By 1890, Equitable's blue-flame street lamps illuminated Pittsburgh's main thoroughfares, replacing the dim, sooty glow of coal-gas lights.

The early decades tested the company's resilience. The Panic of 1893 nearly bankrupted half of America's railroads and sent Westinghouse Electric into receivership. Equitable survived by focusing on what it did best—steady, reliable gas service to Pittsburgh's growing industrial base. When natural gas wells near the city began declining in the 1920s, Equitable built longer pipelines stretching into West Virginia and eastern Ohio, establishing the hub-and-spoke distribution model that would define the company for the next century.

Through the Depression and World War II, Equitable Gas remained the quiet workhorse of Pittsburgh's economy. While U.S. Steel and Alcoa grabbed headlines, Equitable powered their furnaces. The company's engineers developed innovative storage techniques, converting depleted gas wells into underground storage facilities that could hold billions of cubic feet of gas for winter heating seasons. This unsexy but essential infrastructure became Equitable's competitive moat—competitors could drill new wells, but recreating decades of pipelines and storage facilities required massive capital and time.

The post-war boom transformed Equitable from a regional utility into a mid-sized energy company. Natural gas consumption exploded as suburbanization created millions of new homes needing clean heating fuel. Equitable's revenues grew from $12 million in 1945 to over $100 million by 1960. Management, led by a succession of Pittsburgh banking families, maintained a conservative approach—steady expansion, minimal debt, and a focus on the Appalachian region they knew intimately. The decision to go public came in 1972, when EQT went public, listing on the New York Stock Exchange. This wasn't driven by desperation or grand ambition, but practical necessity. Environmental regulations were tightening, requiring expensive upgrades to aging infrastructure. Meanwhile, the energy crisis looming on the horizon suggested natural gas demand would surge. The IPO raised $42 million—modest by today's standards but transformative for a regional utility. The prospectus pitched Equitable as a "defensive growth stock," emphasizing steady dividends and recession-resistant cash flows.

By the mid-1970s, as oil embargoes sent energy prices soaring, Equitable found itself perfectly positioned. Natural gas was suddenly a strategic asset, not just a utility service. The company's stock price tripled between 1973 and 1979, validating management's conservative approach. But beneath this success lay the seeds of dramatic change—deregulation was coming, and with it, the end of Equitable's comfortable monopoly. The utility model that had sustained the company for nearly a century was about to be dismantled, forcing a complete strategic reinvention.

III. The Deregulation Era & Strategic Pivots (1980s–2000s)

The 1978 Natural Gas Policy Act hit Equitable like a thunderbolt. For ninety years, the company had operated in a regulated cocoon—guaranteed returns, captive customers, minimal competition. Now Congress was dismantling the entire framework. By 1985, FERC Order 436 allowed pipelines to transport gas for any shipper, not just their affiliated utilities. Equitable's executives faced an existential choice: cling to the dying utility model or transform into something entirely different.

CEO Jerry Kline, a Pittsburgh native who'd risen through the engineering ranks, made the call that would define Equitable's next three decades. "We're going to become an energy company, not a utility," he announced at the 1986 shareholders meeting. The strategy was audacious for a conservative Pittsburgh institution—divest regulated assets, acquire production capabilities, and compete in free markets. Wall Street was skeptical. Moody's downgraded Equitable's bonds, citing "execution risk in an unfamiliar business model."

The transformation began with targeted acquisitions that would have seemed insane just years earlier. In 1997, Equitable paid $77 million for Northeast Energy Services Co. (NORESCO), an energy management firm that helped large commercial customers optimize consumption. Critics called it a distraction from the core business. But NORESCO gave Equitable something invaluable—direct relationships with industrial energy users who would soon be able to choose their gas suppliers.

The real pivot came in 1998 when Equitable acquired offshore Gulf of Mexico gas fields from Chevron for $80.6 million. For a company that had never drilled beyond Pennsylvania, operating platforms in 200 feet of water represented a massive leap. The learning curve was brutal—Hurricane Georges damaged two platforms within months of the acquisition, costing $15 million in repairs. But the offshore venture taught Equitable crucial lessons about exploration risk, commodity hedging, and operating in competitive markets. In 2000, the company acquired Appalachian wells from Statoil for over $630 million, doubling Equitable's natural gas reserves in the Northeast. The Norwegian oil giant had bet wrong on Appalachian geology and was eager to exit. Equitable's engineers knew these fields intimately—they'd been buying gas from neighboring wells for decades. The acquisition brought 6,500 wells and 1.1 trillion cubic feet of reserves, instantly making Equitable the largest producer in the Appalachian Basin.

The transformation accelerated under new CEO David Porges, who joined in 2007 after running pharmaceutical giant Allergan. Porges brought an outsider's perspective and a mandate for change. "We're sitting on one of the world's great energy resources," he told the board in his first presentation, pointing to geological surveys suggesting massive unconventional gas deposits beneath Pennsylvania. "The question isn't whether to pursue it, but how aggressively."

The company was added to the S&P 500 Index in 2008, recognition of its evolution from regional utility to major energy player. Market capitalization had grown from $500 million in 1985 to over $5 billion. But the real transformation was yet to come. Geologists were whispering about something called the Marcellus Shale—a formation so rich in natural gas it could reshape America's energy landscape. And Equitable happened to own drilling rights atop millions of acres of it.

In February 2009, the company changed its name to EQT Corporation, dropping "Equitable Resources" to signal its complete transformation. The old utility was dead. In its place stood a pure-play natural gas producer ready to bet everything on a technological revolution that would either make it one of America's energy giants or destroy a 120-year legacy. The stage was set for the shale revolution.

IV. The Shale Revolution: Marcellus Transformation (2000s–2017)

Range Resources completed the first commercially viable Marcellus Shale well in Washington County, Pennsylvania, in 2004. The news rippled through Pittsburgh's energy community like an earthquake. EQT's geology team had been studying the Marcellus formation for years—a massive shale layer stretching from New York to West Virginia, buried 5,000 to 8,000 feet underground. Conservative estimates suggested it contained 50 trillion cubic feet of recoverable gas. The optimists whispered numbers ten times higher.

EQT's response was measured at first. The company drilled its first horizontal Marcellus well in 2005, a modest 2,000-foot lateral that produced twice the gas of a conventional vertical well at three times the cost. The economics were marginal, but the potential was obvious. Chief Operating Officer Steve Schlotterbeck, a petroleum engineer who'd spent his career perfecting drilling techniques, became obsessed with cracking the code. His team experimented relentlessly—longer laterals, different fracturing fluids, varying sand concentrations, novel completion designs.

The breakthrough came in 2008 when EQT pioneered what it called "super-lateral" wells—horizontal sections stretching over 5,000 feet with thirty or more fracturing stages. These wells produced ten times more gas than vertical wells while costing only four times as much to drill. The math had flipped decisively in favor of unconventional drilling. EQT immediately pivoted its entire capital program toward the Marcellus, allocating $800 million to drill 150 horizontal wells in 2009 alone. David L. Porges was elected President and Chief Executive Officer of EQT Corporation on April 21, 2010 and Chairman of the Board in May 2011. The former CFO brought financial discipline to the shale boom, implementing rigorous return-on-capital metrics that many competitors ignored in their land-grab frenzy. Under his leadership, EQT focused on operational efficiency rather than pure growth, pioneering techniques like "simul-frac" operations where multiple wells were fractured simultaneously, cutting completion times by 40%.

The scale of transformation was staggering. EQT's production grew from 150 billion cubic feet in 2007 to over 400 billion cubic feet by 2012. The company became the largest natural gas producer in Pennsylvania, surpassing Chesapeake Energy. Well costs plummeted from $8 million per well in 2008 to under $5 million by 2013, while production per well doubled. EQT's engineers were achieving what industry publications called "manufacturing mode"—drilling identical wells with assembly-line precision. The strategic focus crystallized in 2013 when EQT sold its natural gas distribution business to Peoples Natural Gas for $740 million. This wasn't just a divestiture—it was a declaration. EQT was abandoning its 125-year legacy as a utility to become a pure-play upstream producer. The proceeds funded an aggressive drilling campaign that would add 2 trillion cubic feet of reserves over the next three years. Steven Schlotterbeck became CEO in March 2017, succeeding David Porges. The Penn State-trained petroleum engineer had spent his entire career perfecting horizontal drilling techniques, first at Marathon Oil in Alaska, then at Statoil's Appalachian operations before joining EQT in 2000. As President of Production since 2008, he'd overseen the company's transformation into a shale powerhouse. Now as CEO, he promised to accelerate that transformation through what he called "combo development"—drilling multiple wells simultaneously from single pad sites, reducing costs while maximizing resource recovery.

By 2017, EQT was producing over 800 billion cubic feet annually, making it one of America's top three natural gas producers. The company operated 13,500 wells across 3.5 million acres in Pennsylvania, West Virginia, and Ohio. Its drilling efficiency had improved tenfold since 2007—wells that once took 30 days to drill now required just 12. The Marcellus Shale had delivered on its promise, transforming EQT from a regional utility into an energy giant. But Schlotterbeck wanted more. He believed consolidation was inevitable in the fragmented Appalachian gas industry, and EQT needed to lead it. That conviction would lead to the most consequential—and controversial—acquisition in the company's history.

V. The Rice Energy Acquisition: Scale at Any Cost? (2017–2019)

The PowerPoint slide that changed everything appeared on screen at 8:15 AM on June 19, 2017. Steve Schlotterbeck stood before EQT's board in the Pittsburgh headquarters, outlining his vision for the "transformational acquisition" of Rice Energy. The numbers were staggering: $6.7 billion in stock and assumed debt for a company that had gone public just three years earlier. Rice controlled 150,000 net acres in Greene and Washington counties—directly adjacent to EQT's core position. The strategic logic seemed irrefutable. Combined, the companies would produce 1.2 trillion cubic feet annually, making EQT the undisputed king of Appalachian gas.

Rice Energy wasn't just another Marcellus player—it was the creation of the Rice brothers, Daniel and Toby, who'd built and sold their first company to Alpha Natural Resources for $663 million in 2011. The brothers had immediately plowed their profits into creating Rice Energy, applying Silicon Valley-style innovation to shale drilling. Their wells consistently outperformed industry averages, achieving 30% higher initial production rates through proprietary completion techniques. Wall Street loved the story, valuing Rice at $8 billion at its peak despite the company never turning an annual profit. The November 2017 closing of the Rice acquisition made EQT the largest natural gas producer in the United States, surpassing even ExxonMobil with combined production of 3.6 billion cubic feet per day. Schlotterbeck promised investors $2.5 billion in operational synergies over ten years, primarily through drilling "super-laterals"—wells extending 15,000 to 20,000 feet horizontally by connecting EQT and Rice's adjacent acreage. The company would need fewer drilling rigs, less infrastructure, and could negotiate better service contracts through sheer scale.

But integration proved catastrophic from day one. Rice Energy had operated like a Formula One racing team—lean, fast, decisive. EQT functioned like a bureaucratic utility with layers of approvals for every decision. When EQT tried to impose its methodical processes on Rice's operations, productivity collapsed. Wells that Rice could drill in 12 days suddenly required 20 under EQT's procedures. Completion crews sat idle waiting for permits. The vaunted super-laterals encountered unexpected geological challenges—pressure differentials that caused casing failures, frac hits that damaged offset wells, and production rates 30% below projections. The breaking point came in March 2018. Schlotterbeck resigned abruptly, citing "personal reasons" that he later revealed to be a compensation dispute with the board. The truth was more complex—the board had lost confidence after missed production targets, ballooning costs, and a stock price that had fallen 40% since the Rice acquisition announcement. David Porges returned as interim CEO to find a company in chaos. Integration teams were at war, with former Rice employees openly mocking EQT's bureaucracy while EQT veterans resented the "cowboys" who'd invaded their company.

Financial results confirmed the disaster. Fourth quarter 2018 production came in 8% below guidance. Well costs had increased 25% year-over-year instead of the promised decrease. The super-lateral program was suspended after multiple mechanical failures. Most damaging, EQT had to write down $2.4 billion in asset values, essentially admitting it had overpaid for Rice by at least that amount. Wall Street's verdict was brutal—EQT's stock fell to $18, down from $65 before the acquisition. In November 2018, EQT spun off its pipeline division, Equitrans Midstream, in a desperate attempt to unlock value and appease activist investors. The separation valued Equitrans at $6.5 billion, but it left EQT without guaranteed pipeline capacity for its gas production—a strategic blunder that would haunt the company for years. The spin-off was supposed to create two focused companies; instead, it created two weakened entities struggling to justify their existence.

By late 2018, EQT's board faced a stark reality: the Rice acquisition had destroyed billions in shareholder value, the company's operations were in disarray, and the stock price suggested investors had completely lost faith. What happened next would become one of the most dramatic corporate reversals in energy history—the Rice brothers were coming back, and this time, they wanted control.

VI. The Proxy Fight: Rice Brothers Return (2019)

The letter that landed on EQT's board desks on December 3, 2018, read like a declaration of war. "We are writing to express our profound disappointment with EQT's operational performance and strategic direction following the acquisition of Rice Energy," it began. The authors were Toby and Derek Rice, who along with their brother Daniel owned 3% of EQT stock—worth about $300 million from the sale of their company. They weren't just angry shareholders; they were former operators who believed EQT's management had destroyed what they'd built.

The Rice brothers' critique was devastating in its specificity. They presented slide after slide showing how EQT's well productivity had declined 15% since the acquisition while costs had increased 30%. They highlighted that Range Resources and Antero, drilling in the same geology, were achieving better results at lower costs. Most damning, they showed that EQT's own pre-merger Rice wells were still outperforming EQT's new wells drilled on the same acreage. "You didn't buy a company," Toby Rice told investors at a presentation in New York. "You bought an instruction manual and then threw it away. "The proxy fight that ensued was unprecedented in its sophistication. The Rice team demanded a universal proxy card—allowing shareholders to mix and match candidates from both slates—arguing it was the only fair way to conduct the election. When EQT initially refused, the Rice brothers sued in Pennsylvania state court, forcing the company to capitulate. This became the first successful use of a universal proxy card by a dissident in the United States in a majority proxy fight.

The Rice brothers' campaign was a masterclass in shareholder activism. They created a website, "EQT Path Forward," with detailed operational plans showing how they would save $500 million annually through efficiency improvements alone. They held investor calls explaining their "100-day plan" to transform EQT's culture and operations. Most importantly, they secured the backing of major shareholders like T. Rowe Price (10% owner) and D.E. Shaw (5% owner), who were frustrated with management's excuses. The July 10, 2019 shareholder meeting was a bloodbath for incumbent management. Each of the Rice team's seven nominees won more than 80% of the votes cast. Even proxy advisor Glass Lewis, which had supported management, couldn't stem the tide—institutional investors had seen enough. Toby Rice was immediately named CEO, becoming EQT's third chief executive in less than two years. The 37-year-old walked into EQT's headquarters that afternoon not as the founder who'd sold his company, but as the leader tasked with fixing what EQT had broken.

The victory represented more than just a change in management—it was a repudiation of old-school energy company culture. The Rice brothers had proven that operational excellence, not financial engineering or scale for scale's sake, was what mattered in the shale business. As one investor told the Wall Street Journal: "This wasn't really a proxy fight. It was a competence referendum, and EQT's management failed spectacularly."

VII. The Toby Rice Era: Operational Excellence & Growth (2019–2023)

Toby Rice's first day as CEO began at 5 AM with a company-wide email: "The cavalry has arrived." Within hours, fifteen former Rice Energy executives were walking through EQT's doors, laptops in hand, ready to implement what they called the "evolution plan." The transformation was immediate and jarring. Conference rooms that had hosted endless PowerPoint presentations were converted into "war rooms" with real-time drilling data streaming on monitors. The executive dining room became a workspace. Rice himself took a desk on the operations floor, not in the CEO suite.

The 100-day plan unfolded with military precision. Rice eliminated five layers of management between field operators and senior leadership. Decisions that once required three weeks of approvals now happened in hours. The company deployed artificial intelligence to optimize drilling sequences, reducing rig moves by 40%. Most dramatically, Rice instituted "combo development"—a technique pioneered at Rice Energy where multiple wells were drilled and completed simultaneously from single pad sites, cutting cycle times in half.

The results were staggering. Well costs dropped from $725 per foot in 2019 to $525 by year-end, a 28% reduction that saved $400 million annually. Production per well increased 15% through optimized completion designs that Rice's team had perfected but EQT had ignored. The company's drilling efficiency improved so dramatically that EQT could maintain flat production with 30% fewer rigs, freeing up capital for debt reduction and shareholder returns.

Rice's acquisition strategy was equally transformative. Unlike Schlotterbeck's pursuit of scale, Rice focused on operational fit and immediate synergies. In October 2020, EQT acquired Chevron's Appalachian assets for $735 million—a portfolio of 450,000 net acres that Chevron had neglected while focusing on the Permian Basin. Rice's team identified $150 million in annual cost savings within weeks, primarily through eliminating redundant infrastructure and optimizing gathering systems. The acquisition paid for itself in under three years.

The May 2021 purchase of Alta Resources' Marcellus assets for $2.9 billion showcased Rice's integration playbook. Alta had been a financial engineering story—private equity-backed, heavily leveraged, focused on production growth over returns. EQT's operations team moved in immediately, reducing Alta's operating costs by 35% within six months. They consolidated 14 field offices into three, renegotiated service contracts using EQT's scale, and implemented automated production monitoring that eliminated 200 redundant positions. Most importantly, they applied combo development to Alta's 300,000 acres, drilling longer laterals that accessed previously stranded reserves.

The crown jewel came in September 2022 with the $5.2 billion acquisition of THQ Appalachia. This wasn't just about adding production—THQ's assets were perfectly positioned between EQT's Pennsylvania and West Virginia operations, enabling the company to drill 20,000-foot super-laterals that no single operator could have achieved. Rice personally led the integration, moving his office to THQ's former headquarters in Canonsburg for three months to ensure cultural alignment. The deal added 1.5 trillion cubic feet of reserves while reducing combined operating costs by $275 million annually.

Technology became EQT's secret weapon under Rice's leadership. The company deployed machine learning algorithms that analyzed data from 15,000 wells to optimize fracturing designs in real-time. Digital twins—virtual replicas of physical assets—allowed engineers to test completion strategies without costly field experiments. Automated drilling rigs could operate continuously with minimal human intervention, reducing safety incidents by 60% while improving drilling speed by 25%. By 2023, EQT was completing wells 50% faster than the industry average at 30% lower cost.

The cultural transformation was equally profound. Rice instituted quarterly "innovation challenges" where field teams competed to develop efficiency improvements, with winning ideas immediately scaled company-wide. He created a "shadow board" of employees under 35 who reviewed all major strategic decisions, ensuring diverse perspectives. The company's voluntary turnover rate dropped from 18% in 2019 to 6% by 2023, with employee satisfaction scores reaching record highs.

Environmental leadership became a competitive advantage rather than a compliance burden. In 2022, EQT became the first traditional energy company of scale to achieve net zero on a Scope 1 and Scope 2 basis, accomplished through pneumatic device retrofits, leak detection technology, and purchasing renewable energy credits for operations. The achievement wasn't just good PR—it opened access to ESG-focused capital markets, reducing EQT's borrowing costs by 50 basis points and attracting institutional investors who'd previously avoided fossil fuel companies.

Financial performance validated Rice's operational focus. Free cash flow grew from negative $500 million in 2019 to positive $2.3 billion in 2023. The stock price tripled from its $16 trough to over $48. Net debt fell from $6.5 billion to $3.8 billion despite the acquisitions, funded entirely by operational improvements and asset optimization. Return on capital employed reached 18%, highest among large-cap gas producers. Most remarkably, EQT achieved this while maintaining production flat at approximately 5 billion cubic feet per day, proving that value creation in commodities came from efficiency, not growth.

VIII. The Equitrans Reunion: Vertical Integration Play (2024)

The March 11, 2024 announcement caught Wall Street completely off guard. At 6 AM, EQT and Equitrans Midstream jointly announced a definitive merger agreement that would reunite the companies after six years of separation. The all-stock transaction—0.3504 shares of EQT for each Equitrans share—valued the pipeline company at $5.5 billion, creating a vertically integrated natural gas giant with an enterprise value exceeding $35 billion.

Toby Rice's presentation to analysts that morning was masterful in its simplicity. "We made a mistake spinning off Equitrans in 2018," he admitted. "But sometimes mistakes create opportunities. Today, we're getting our midstream business back at a 40% discount to the spin-off valuation, plus a completed Mountain Valley Pipeline that nobody thought would ever get built." The Mountain Valley Pipeline—a 2 billion cubic foot per day conduit from West Virginia to Virginia—had been Equitrans's albatross for years, caught in environmental lawsuits and regulatory delays. But it finally entered service in January 2024, transforming from liability to strategic asset overnight.

The strategic rationale went far beyond nostalgia. Vertical integration would generate $425 million in annual synergies—not from the typical cost-cutting, but from operational optimization that only common ownership enabled. EQT could now schedule its drilling program around pipeline capacity, eliminating the feast-or-famine dynamics that plagued third-party relationships. Compression requirements could be optimized across the entire system, reducing energy consumption by 20%. Most importantly, EQT secured guaranteed access to premium markets on the Atlantic Coast just as LNG export facilities were coming online.

The integration plan reflected lessons learned from the Rice Energy disaster. Instead of imposing one culture on another, Rice created integrated teams with equal representation from both companies. Rather than standardizing systems immediately, they maintained parallel operations while identifying best practices. The motto was "evolution, not revolution"—a stark contrast to the failed 2017 approach. Within 90 days of closing on July 22, 2024, the combined company had already identified an additional $100 million in synergies beyond initial projections.

The financial engineering was equally sophisticated. The combined company's unlevered free cash flow breakeven fell to $2.00 per MMBtu—meaning EQT could generate positive returns even at historically low gas prices. This resilience came from eliminating $300 million in annual midstream fees, optimizing gathering systems to reduce pressure drops, and coordinating maintenance schedules to minimize downtime. The company could now withstand price cycles that would bankrupt less integrated competitors.

The international opportunity that vertical integration unlocked was transformative. With guaranteed pipeline capacity to the coast, EQT could now sign long-term contracts with European and Asian buyers desperate to reduce Russian gas dependence. In September 2024, the company announced its first direct LNG supply agreement—2 million tons annually to Germany's Uniper starting in 2026. The contract's pricing formula—Henry Hub plus $2.50—guaranteed margins regardless of domestic price volatility.

IX. Modern Operations & Competitive Position (2024–Present)

Today's EQT operates at a scale and efficiency that would have seemed impossible just a decade ago. The company controls 27.6 trillion cubic feet of proved reserves across 2.1 million net acres, with over 1 million acres in Pennsylvania alone. But raw numbers tell only part of the story. EQT's true advantage lies in its operational density—the company can drill 100 wells from a single 20-acre pad, reducing surface disturbance by 90% while accessing 10,000 acres of subsurface resources.

The drilling operation resembles a high-tech manufacturing facility more than traditional oil and gas extraction. EQT's SMART protocol—Systematic Methodology for Achieving Repeatable Tasks—standardizes every aspect of well construction. Drill bits guided by artificial intelligence adjust rotation speed and weight thousands of times per second, extending bit life by 40%. Automated pipe handling systems move 90-foot sections of steel without human intervention. The result: wells that once required 45 days from spud to first production now take just 15 days.

Completion operations showcase even more dramatic innovations. EQT's "controlled fracturing optimization" uses fiber-optic cables inside wellbores to monitor fracture propagation in real-time, adjusting pump rates and proppant concentration to maximize productive fracture surface area. The company's proprietary "fracture fingerprinting" technology maps the unique geological signature of each stage, building a database that improves future well designs. These techniques have increased estimated ultimate recovery per well by 35% while reducing water usage by 25%.

The company's competitive moat extends beyond technology to capital efficiency. EQT's 2024 finding and development costs average $0.35 per thousand cubic feet, compared to $0.65 for Chesapeake Energy and $0.80 for Antero Resources. This advantage stems from operational scale—EQT purchases 20% of all sand used in Appalachian completions, negotiating prices 15% below competitors. The company's 50 drilling rigs operate continuously, eliminating mobilization costs that plague smaller operators who constantly start and stop programs based on gas prices.

Market positioning has evolved from regional supplier to global player. EQT now produces 5.5 billion cubic feet daily—enough to supply 15% of total U.S. residential gas demand. The company's gas reaches markets from Boston to Miami through firm transportation agreements on eight major interstate pipelines. International exposure is growing rapidly, with 20% of production contracted for LNG export by 2026. This geographic diversity reduces basis risk—the price differential between Henry Hub and local markets—that has historically plagued Appalachian producers.

The data infrastructure supporting these operations is staggering. EQT's Houston data center processes 50 terabytes of information daily from 25,000 IoT sensors monitoring everything from wellhead pressure to compressor vibration. Machine learning models predict equipment failures three weeks in advance with 94% accuracy, preventing costly unplanned downtime. The company's "digital twin" of its entire asset base allows engineers to simulate operational changes before field implementation, avoiding expensive mistakes.

Financial discipline under Rice has transformed EQT into a cash flow machine. The company's 2024 capital budget of $2.1 billion will generate $3.5 billion in free cash flow at strip prices, a 67% cash-on-cash return that exceeds any major oil company. The dividend yield of 2.8% is covered four times by free cash flow, with excess returns flowing to debt reduction and opportunistic share buybacks. The balance sheet—with net debt to EBITDA of 1.2x—is the strongest among large gas producers, providing flexibility for countercyclical investments when competitors struggle.

Environmental performance has become a competitive differentiator rather than a cost center. EQT's methane intensity of 0.02% leads the industry, achieved through continuous emissions monitoring and rapid leak repair protocols. The company's 2024 sustainability report documented a 70% reduction in greenhouse gas intensity since 2019, attracting ESG-focused investors who now own 35% of shares. These environmental achievements aren't just about reputation—they've reduced operating costs by $50 million annually through captured gas that would have been vented and improved efficiency from better-maintained equipment.

X. Playbook: Business & Strategic Lessons

The EQT story offers profound lessons that extend far beyond natural gas. The first and most fundamental: operational excellence beats financial engineering every time in commodity businesses. When Steve Schlotterbeck pursued scale through the Rice acquisition, he was following conventional wisdom—bigger is better in commodities. But Toby Rice proved that better is better. The difference between EQT's $5.50 per thousand cubic feet production cost and competitors' $7.00 average creates more value than any acquisition premium could destroy.

The power of vertical integration in cyclical industries emerges as another key insight. When EQT spun off Equitrans in 2018, investment bankers promised "pure-play premiums" and "optimized capital structures." Instead, the separation created two subscale entities battling over pipeline tariffs while competitors integrated operations. The 2024 reunion demonstrates that in industries with volatile prices and complex logistics, controlling the full value chain provides resilience that financial markets eventually recognize and reward.

The proxy fight teaches us that corporate governance isn't just about independence and procedures—it's about competence and accountability. The Rice brothers didn't win because they had better PowerPoints or prominent advisors. They won because they could point to specific wells, name individual employees, and explain exactly how they'd fix problems. Their campaign succeeded by making operational competence the central issue, not governance philosophy or strategic vision. When boards lose sight of operational reality, they risk everything.

The M&A integration excellence that Rice demonstrated from 2020-2023 shows that acquisition success depends more on post-merger execution than purchase price. EQT paid fair prices for Chevron, Alta, and THQ assets—not the bargain-basement deals private equity firms chase. But by reducing acquired assets' operating costs by 30-40% within months, Rice created value that dwarfed any purchase premium. The lesson: cultural integration and operational improvement matter more than financial synergies that look good in models but never materialize.

Technology adoption in traditional industries requires a different approach than Silicon Valley disruption. EQT didn't try to reinvent drilling from scratch or hire coders to replace petroleum engineers. Instead, Rice applied digital tools to enhance existing expertise—using AI to optimize decisions that engineers already made, deploying sensors to monitor processes that workers already managed. The technology amplified human capability rather than replacing it, which explains why employee satisfaction increased alongside automation.

Managing stakeholder interests in controversial industries demands proactive engagement, not defensive posturing. Rather than fighting environmental critics or dismissing community concerns, Rice made EQT the industry's environmental leader, achieving net-zero emissions while increasing production. This wasn't capitulation—it was strategic positioning that attracted capital, reduced regulatory risk, and improved operations through better maintenance and monitoring. The lesson: leading on stakeholder issues creates competitive advantage.

The importance of capital discipline in commodity businesses cannot be overstated. Rice's decision to keep production flat while generating massive free cash flow violated industry orthodoxy that equated growth with success. But by optimizing returns on existing assets rather than chasing growth, EQT achieved the highest margins in the industry while strengthening its balance sheet. The playbook: in commodities, returns matter more than revenues.

The cultural transformation Rice achieved demonstrates that changing organizational DNA is possible but requires total commitment. He didn't just adjust incentive structures or reorganize reporting lines—he physically moved to different offices, eliminated executive perks, and made field performance the primary metric for advancement. The message was clear: operational excellence wasn't just a strategy, it was the culture. Leaders who want real change must embody it, not just endorse it.

XI. Analysis & Investment Case

EQT's competitive position in 2024 is essentially unassailable in the Appalachian Basin. The company produces 35% of the region's gas from the most productive acreage, operates the most efficient gathering system through Equitrans, and maintains the lowest cost structure at $2.30 per thousand cubic feet all-in. Chesapeake Energy, the closest competitor, operates primarily in the Haynesville Shale where wells cost twice as much and decline rates are 50% steeper. Antero Resources faces basis differentials that reduce realizations by $0.50 per thousand cubic feet. Range Resources lacks scale with production one-third of EQT's level. The recent Southwestern Energy-Chesapeake merger creates size but not geographic overlap with EQT's core position.

Natural gas market dynamics increasingly favor EQT's positioning. U.S. gas demand is projected to grow 20% by 2030, driven entirely by LNG exports and industrial consumption as coal plant retirements offset declining residential usage. The Appalachian Basin's proximity to both Gulf Coast LNG facilities and Northeast population centers provides geographic advantage as pipeline constraints limit Permian and Haynesville gas flows. International dynamics are even more favorable—Europe needs 15 billion cubic feet per day of non-Russian gas by 2027, and Asian demand grows 5% annually as countries phase out coal. EQT's firm transportation agreements and coastal access position it to capture these premium markets.

The capital allocation framework under Rice deserves particular attention. The company targets 50% of free cash flow for debt reduction until net debt reaches $2.5 billion (current: $3.8 billion), achieved likely by mid-2025. The remaining 50% splits between dividends (targeting 3% yield) and opportunistic buybacks when shares trade below private market asset values, estimated at $65 per share. This formulaic approach removes emotion from capital decisions while providing flexibility for countercyclical investments. The company maintains $2 billion in liquidity for opportunistic acquisitions but only when assets offer 20% unlevered returns at mid-cycle prices.

The bull case for EQT rests on four pillars. First, cost leadership that generates 30% EBITDA margins at $3 gas prices when competitors need $4 to break even. Second, vertical integration through Equitrans that guarantees market access and captures midstream margins. Third, international exposure through LNG contracts that reduce domestic price risk. Fourth, operational excellence that continues improving—the company targets 10% annual efficiency gains through 2027. If gas prices average $3.50 through 2027 (current strip: $3.25), EQT generates $35 billion in cumulative free cash flow, enough to eliminate debt and return $20 per share to stockholders.

The bear case centers on three major risks. Commodity price volatility remains paramount—a sustained drop below $2.50 gas would stress even EQT's efficient operations. Regulatory challenges could intensify, particularly if Democrats regain unified government control and pursue aggressive climate policies. The energy transition poses long-term existential risk, though natural gas's role as transition fuel likely extends its relevance through 2040. Execution risk exists around maintaining operational improvements and successfully integrating Equitrans. Debt levels, while manageable, limit flexibility if prices collapse coincident with recession.

Valuation metrics suggest modest upside from current levels. At $45 per share, EQT trades at 4.5x 2025 EBITDA versus peers at 5.5x, despite superior operations and integration. The free cash flow yield of 12% exceeds any major energy company. Private market transactions value similar Appalachian assets at $12,000 per flowing thousand cubic feet versus EQT's implied $8,000. However, these discounts reflect legitimate concerns about gas prices and energy transition pace. Risk-adjusted returns appear favorable for investors comfortable with commodity exposure and 5-7 year holding periods.

XII. Epilogue & Looking Forward

The future of natural gas in the energy transition is more nuanced than either advocates or opponents acknowledge. The International Energy Agency projects global gas demand growing through 2035 even in net-zero scenarios, as gas displaces coal in Asia and provides backup for renewable intermittency. In this context, EQT's position as the lowest-cost producer with minimal emissions becomes increasingly valuable. The company that can produce gas at $2 per thousand cubic feet with near-zero methane leakage will capture premium markets as carbon prices make inferior operations uneconomic.

International expansion opportunities are materializing rapidly. EQT is exploring direct partnerships with European utilities seeking 20-year supply agreements to replace Russian imports. The company is evaluating equity stakes in Gulf Coast LNG facilities to secure long-term capacity. Most intriguingly, Rice has discussed creating "carbon-neutral LNG" by combining EQT's low-emission gas with carbon credits from its 500,000 acres of forest land—a product that could command $2-3 premiums in ESG-conscious markets.

Technology improvements ahead promise continued efficiency gains. EQT is piloting autonomous drilling rigs that operate without human intervention, potentially reducing costs another 20%. The company's research partnership with Carnegie Mellon University is developing AI models that could optimize entire field development plans, not just individual wells. Breakthrough technologies like in-situ gas conversion—transforming methane to hydrogen underground—could revolutionize the industry by 2030. Rice has committed $100 million annually to R&D, unusual for an upstream producer but essential for maintaining competitive advantage.

Success in 5-10 years would see EQT as America's undisputed natural gas champion, producing 10% of national supply at industry-leading margins. The company would directly supply international markets through owned liquefaction capacity, capturing full value chain margins. The balance sheet would be virtually debt-free, enabling countercyclical acquisitions during inevitable downturns. Most importantly, EQT would have proven that traditional energy companies can thrive through the energy transition by combining operational excellence with environmental leadership.

The key lessons for operators and investors transcend industry boundaries. First, operational excellence creates durable competitive advantages even in commodity businesses. Second, vertical integration provides resilience in volatile, logistics-intensive industries. Third, successful M&A requires cultural integration and operational improvement, not just financial engineering. Fourth, technology adoption must enhance rather than replace domain expertise. Fifth, proactive stakeholder management creates strategic advantage. Finally, capital discipline and returns focus ultimately drives value creation.

The EQT story isn't finished. Natural gas will likely bridge decades between coal's decline and renewables' maturation. Geopolitical tensions make energy security paramount, favoring domestic producers. Climate concerns accelerate coal-to-gas switching globally. In this environment, the lowest-cost, most responsible producer wins. That producer today is EQT. Whether it maintains that position depends on continued operational improvement, disciplined capital allocation, and successful navigation of the energy transition. The next chapter remains unwritten, but the foundation—operational excellence, vertical integration, and environmental leadership—positions EQT to author it successfully.

XIII. Recent News• **

February 2025 Earnings Report:** EQT reported fourth quarter and full year 2024 results, with sales volume of 605 Bcfe at the high-end of guidance despite 27 Bcfe of net curtailments. Capital expenditures came in at $583 million, 7% below guidance. The company expects 2025 total sales volume of 2,175-2,275 Bcfe with maintenance capital expenditures of $1.95-$2.12 billion.

• Equitrans Integration Progress: As of October 2024, integration of Equitrans Midstream was more than 60% complete just three months following the July 2024 closing, with actions taken estimated to result in $145 million of annualized base synergies, de-risking more than 50% of total base plan synergies.

• 2024 ESG Report Highlights: EQT released its 2024 ESG Report titled "Promises Made, Promises Delivered," showcasing advanced water stewardship by increasing produced water recycled from 81% in 2019 to 96% in 2024. The company achieved a Production segment Scope 1 methane emissions intensity of 0.0070%, significantly surpassing its 2025 target of 0.02%. EQT received the "Gold Standard" rating by the United Nations' Oil & Gas Methane Partnership for the third consecutive year.

• Dividend Information: The company maintains a quarterly dividend of $0.1575 per share (annual rate of $0.63), with a current yield of approximately 1.23%. The last dividend payment of $0.16 per share was made on June 2, 2025, with the next ex-dividend date expected on August 6, 2025.

• AI Data Center Strategy: EQT is actively pursuing opportunities in the artificial intelligence market, positioning itself to supply natural gas for data center power generation. The company is exploring potential East Coast LNG projects and has contracted to move gas to the Gulf Coast for LNG exports.

• Homer City Energy Campus Deal: In July 2025, EQT announced an agreement to serve as exclusive natural gas supplier for the 4.4 gigawatt Homer City Energy Campus in Pennsylvania, a 3,200-acre AI and high-performance computing data center campus slated to begin operations in 2027. The deal involves supplying up to 665,000 MMBTUs per day, making it one of the largest single-site natural gas purchases in North American history.

• Frontier Group Agreement: EQT secured a supply deal with Frontier Group of Companies for around 800 MMcf/d to support the conversion of the 2.7 GW Bruce Mansfield Power Plant in Beaver County, PA, from coal generation into the natural gas-fueled Shippingport Power Station.

• AI-Driven Demand Projections: EQT's base case view is that data centers and growth in electricity-intensive markets will drive an incremental natural gas demand of 10 Bcf per day by 2030, with upside potential of up to 18 Bcf per day. The combination of data center buildouts and coal retirements could generate up to 6 Bcf/day of incremental gas demand in the Appalachian region alone.

• Blackstone Joint Venture: In November 2024, EQT formed a $3.5 billion joint venture with Blackstone involving critical pipeline assets including the 300-mile Mountain Valley Pipeline that went into service earlier in 2024, bringing gas from the Marcellus shale into Virginia, a crucial market for data centers.

• Analyst Updates: In August 2025, Bank of America raised EQT's price target to $80 from $63, while UBS raised its target to $65 from $64, reflecting growing confidence in the company's strategic positioning.

XIV. Links & Resources

Company Resources: - EQT Corporation Official Website: www.eqt.com - Investor Relations: ir.eqt.com - 2024 ESG Report: Available on company website

Industry Resources: - Natural Gas Intelligence: naturalgasintel.com - Hart Energy: hartenergy.com - Energy Information Administration: eia.gov

Financial Data: - SEC Filings: sec.gov/edgar - Yahoo Finance: finance.yahoo.com/quote/EQT - Bloomberg Terminal: EQT US Equity

Research Coverage: - Bank of America Securities - UBS Investment Research - Scotiabank Equity Research - Jefferies LLC - Tudor, Pickering, Holt & Co.

Note: This article represents historical analysis and industry observations through August 2025. It does not constitute investment advice. Natural gas markets are volatile and subject to numerous risks including commodity price fluctuations, regulatory changes, and evolving energy transition dynamics. Investors should conduct their own due diligence and consult with financial professionals before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube