Construction Partners: The Asphalt Empire of the Sunbelt

How a Private Equity Roll-Up from Dothan, Alabama Became a $5+ Billion Infrastructure Compounder

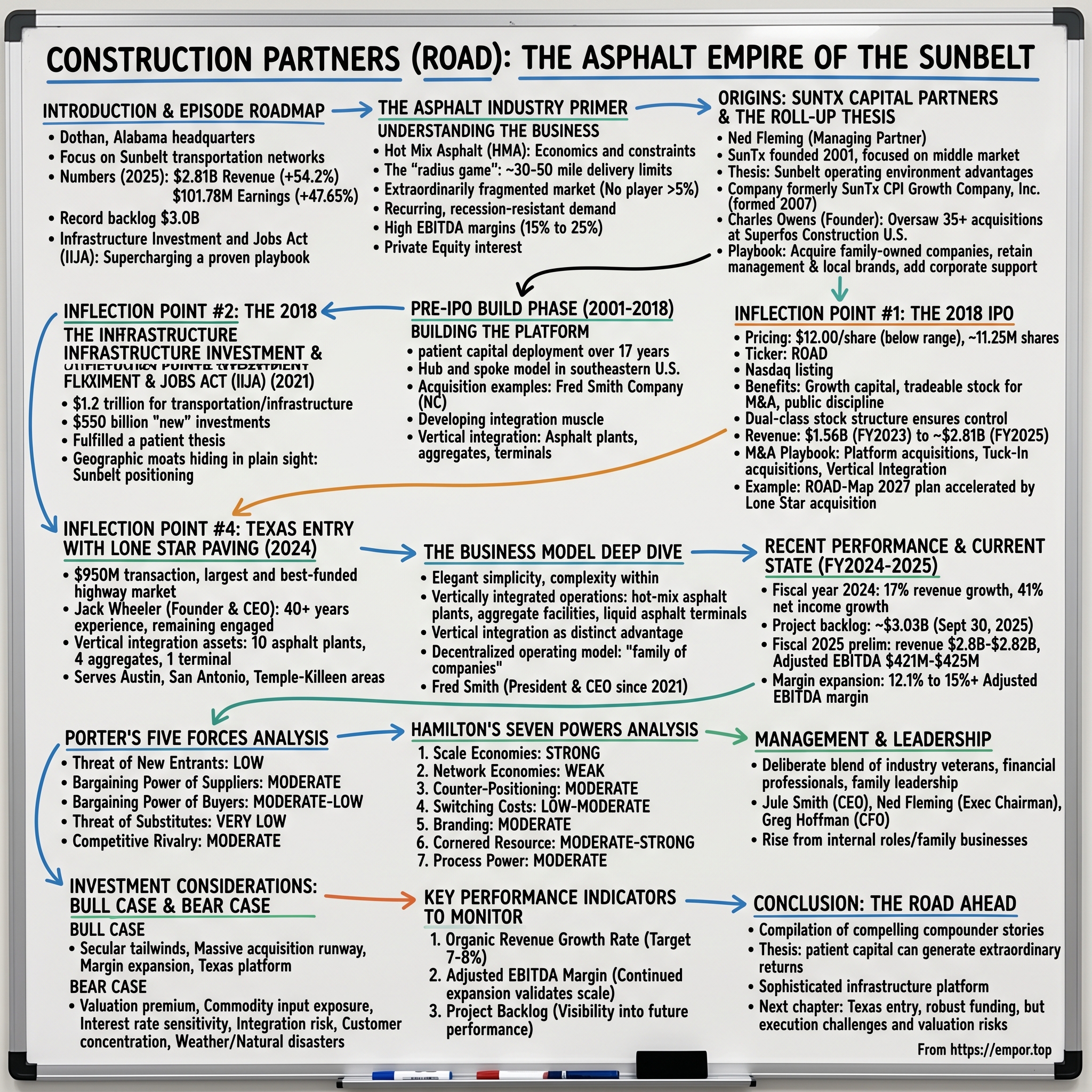

I. Introduction & Episode Roadmap

Picture a family of four driving down Interstate 85 through Alabama on a scorching July afternoon. The asphalt beneath them—that dark, resilient ribbon stretching toward the horizon—seems almost alive in the shimmering heat. It's doing its job silently, absorbing the punishment of eighteen-wheelers, absorbing the summer sun, absorbing the weight of American commerce. Most drivers never think twice about who laid that road, who maintains it, who profits from its very existence.

But in Dothan, Alabama—a city of about 70,000 souls nestled in the southeast corner of the state—a company has been thinking about little else for over two decades. Construction Partners is an asphalt-centered infrastructure company dedicated to building and maintaining the transportation networks that keep the Sunbelt moving. Their vertically integrated operations include hot-mix asphalt plants, aggregate facilities, and liquid asphalt terminals, allowing them to ensure quality, efficiency, and timely project delivery.

The numbers tell a story of relentless compounding. In 2025, Construction Partners' revenue was $2.81 billion, an increase of 54.20% compared to the previous year's $1.82 billion. Earnings were $101.78 million, an increase of 47.65%. From a $12 IPO price in May 2018 to a stock trading near $100 in late 2025, the company has delivered roughly a 10x return to early investors—in an industry most would dismiss as boring, commoditized, and low-margin.

This is the story of how a private equity thesis from Dallas, a collection of family-owned paving businesses, and a once-in-a-generation infrastructure spending bill combined to create one of the most compelling compounder stories in American industrials. It's a tale about the power of vertical integration, the art of acquiring family businesses, and the geographic moats hiding in plain sight beneath our feet.

The company ended fiscal year 2025 with revenue up 54% compared to FY24, net income up 48%, Adjusted EBITDA up 92%, and a record backlog of $3.0 billion. These aren't the numbers of a sleepy regional contractor—they're the numbers of a company executing on a decades-long strategy at precisely the right moment in American infrastructure history.

The Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Law, was signed into law by President Biden on November 15, 2021. The law authorizes $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward "new" investments and programs. This legislative moment didn't create Construction Partners' opportunity—it supercharged an already-proven playbook.

To understand why this company matters, we need to understand the peculiar economics of asphalt, the genius of the roll-up thesis, and why the Sunbelt isn't just growing—it's being rebuilt.

II. The Asphalt Industry Primer: Understanding the Business

Before we can appreciate Construction Partners' strategy, we need to understand why hot mix asphalt is perhaps the most underappreciated industrial material in America.

Due to the relatively higher predicted temperatures (150–180 °C), the latest research on pavement energy consumption and carbon dioxide emission assessment mentioned contributing to higher environmental burdens such as air pollution and global warming. However, warm-mix asphalt was introduced by pavement researchers and the road construction industry instead of hot-mix asphalt to reduce these environmental problems.

Hot mix asphalt (HMA) is exactly what it sounds like—a mixture of aggregates (crushed stone, sand, and gravel) bound together by asphalt cement (a petroleum byproduct), heated to temperatures exceeding 300 degrees Fahrenheit, and then applied to road surfaces while still hot and workable. The "hot" part is crucial: The production cost of asphalt mixtures includes the materials, processing, trucking, and lay down cost, of which the materials cost is the most expensive, accounting for about 70% of the total cost.

Here's where the economics get interesting. HMA begins cooling the moment it leaves the plant. Within approximately one to two hours, it hardens to the point where it can no longer be properly compacted and laid. This creates what industry insiders call the "radius game"—a natural geographic moat that limits delivery distance from any single plant to roughly 30-50 miles under optimal conditions. Go farther, and the product literally becomes unusable.

This physical constraint has profound implications for industry structure. There are no companies that hold a market share exceeding 5% in the Paving Contractors in the US industry. The industry remains extraordinarily fragmented precisely because of this radius limitation—no single plant can serve a wide geographic area, requiring either a network of facilities or a focus on hyper-local markets.

The highway and road construction industry generated approximately $165.0 billion of revenues in 2014. Federal, state and local DOT budgets drive industry performance, with the public sector generating 95% of total industry revenues in 2016. This government-dominated customer base creates another distinctive characteristic: demand is remarkably stable and visible. Politicians may disagree on many things, but they rarely vote against fixing potholes.

According to the National Asphalt Pavement Association, about 65% of the bitumen pavement market is publicly funded mainly for highway projects, where non-residential and residential construction accounts for 35%. Roads require constant maintenance regardless of economic conditions—in fact, recession can actually increase maintenance funding as governments pursue countercyclical stimulus.

"If you look at the demographic of the folks that own these types of businesses, they're definitely an aging ownership group collectively, and it's still very, very fragmented," said Greg Hogan, managing director at SC&H Capital. "Even the sponsors that are coming in now more recently still have a tremendous amount of targets and a lot of whitespace."

The industry's fragmentation isn't accidental—it reflects its history. Asphalt contractors don't just accidentally become asphalt contractors. If you closely follow the lineage of families and individuals involved in the paving business in the Northeast you won't be surprised to find out that a lot of the larger, more prominent, and in some cases less prominent, asphalt contractors are somehow related. These are multi-generational family businesses, passed from fathers to sons to grandsons, rooted in specific communities and relationships built over decades.

According to National Asphalt Pavement Association, approximately 3,500 asphalt mix production sites are operated in the U.S. where the production of asphalt pavement material is over 350 million tons per year. That's 3,500 potential acquisition targets—many run by aging founders whose children have chosen other careers, creating a generational succession crisis that presents both opportunity and obligation for consolidators.

Recurring revenue, diversified customer base, recession resistance and high EBITDA margins of 15% to 25% have private equity knocking on the door of asphalt pavers. Meanwhile, barriers to entry due to capital requirements for equipment and skilled worker training haven't stopped new investors as federal infrastructure funding and an abundance of dry powder have led PE into new investment categories.

For investors, the asphalt industry represents a rare combination: visible recurring demand (roads always need maintenance), local monopoly characteristics (the radius game), stable government customers, and a fragmented acquisition landscape. The question was never whether this industry could be consolidated—it was who would do it, and how.

III. Origins: SunTx Capital Partners & The Roll-Up Thesis

The story of Construction Partners begins not in Alabama, but in Dallas, Texas, in the minds of a group of private equity investors who saw what others missed.

SunTx was founded in 2001 and currently has over $600 million of assets under management. SunTx Capital Partners, LP, is a Dallas, TX-based private equity firm that invests in middle market manufacturing, distribution and service companies. SunTx specializes in supporting talented management teams in industries where SunTx can apply its operational experience and financial expertise to build leading middle-market companies with operations typically in the Sun Belt region of the United States.

The firm's founding thesis was both simple and contrarian: the Sunbelt region of the United States—stretching from the Carolinas through Florida, along the Gulf Coast, and into Texas—represented a fundamentally different operating environment than the rest of America. Business-friendly regulations, right-to-work labor laws, rapid population growth, and a culture of entrepreneurship created fertile ground for building companies that could achieve scale advantages while competitors elsewhere struggled with unionization, regulation, and demographic decline.

Ned Fleming is a Founding Partner and the Managing Partner of SunTx Capital Partners. He serves on the board of multiple portfolio companies including his role as Executive Chairman of Construction Partners, Inc.

Ned N. Fleming III's background shaped SunTx's distinctive approach. Before co-founding the firm, Fleming served as President and Chief Operating Officer of Spinnaker Industries, a publicly traded materials manufacturing company, until its sale in 1999. With an MBA from Harvard Business School and a BA in Political Science from Stanford University, Fleming brought both operational rigor and strategic sophistication to the firm's investment thesis.

"We are honored to receive this recognition and humbled by the group of excellent firms who join us on the list for 2021," said Ned Fleming, Founding Partner of SunTx. "Over the course of our 20 year history, we have built highly successful and enduring partnerships with business owners."

Construction Partners emerged from SunTx's observation that the asphalt and paving industry exhibited all the characteristics they sought: fragmented ownership, aging operators, stable cash flows, and the potential for operational improvement through scale. The company was formerly known as SunTx CPI Growth Company, Inc. and changed its name to Construction Partners, Inc. in September 2017. The company was incorporated in 2007 and is headquartered in Dothan, Alabama.

Why Dothan? The city sits at the intersection of U.S. Routes 231 and 84, placing it within striking distance of significant portions of Alabama, Georgia, and Florida. More importantly, southeastern Alabama was home to several established paving companies whose founders had built strong reputations over decades but lacked clear succession plans. SunTx recognized that these weren't distressed assets—they were healthy businesses whose owners simply needed an exit strategy that honored what they'd built.

Charles Owens is a founder of Construction Partners. He has been a member of the board of directors since 2001. From 1990 to its sale in 1999, Mr. Owens was President and Chief Executive Officer of Superfos Construction U.S., Inc., the North American operation of Superfos a/s, a publicly held Danish company. During his tenure as President and Chief Executive Officer at Superfos Construction U.S., he oversaw the successful acquisition and integration of more than 35 companies towards becoming one of the largest highway construction companies in the United States.

Charles Owens brought precisely the operational experience the thesis required. Having already rolled up 35+ companies at Superfos, he knew how to integrate family businesses without destroying what made them successful. Prior to that, he was President of Couch Construction, a subsidiary of Superfos Construction U.S. headquartered in Dothan, Alabama. His local roots and industry relationships made Dothan not just a logical headquarters, but the only possible one.

"This transformational acquisition exemplifies the growth strategy that we have executed since our founding – partnering with experienced local operators who know how to build and operate great companies that we can further support within our larger organization," said Fleming.

The SunTx playbook for Construction Partners would prove remarkably consistent over the next two decades: identify family-owned paving companies with strong local reputations, acquire them at reasonable valuations, retain the management teams and local brands, and layer on corporate support in areas like finance, safety, legal, and procurement. Never strip out what made the businesses successful; instead, amplify their strengths with scale advantages.

IV. The Pre-IPO Build Phase (2001-2018): Building the Platform

The foundation of Construction Partners wasn't laid overnight—it was built brick by brick, acquisition by acquisition, over seventeen years of patient capital deployment.

The company's initial strategy focused on creating a "hub and spoke" model across the southeastern United States. Each acquired company retained its local identity and management team, but gained access to shared services, bulk purchasing power, and capital for equipment and plant upgrades. Many of the senior executives have over 30 years of construction management experience. Prior to joining Construction Partners, several came from companies like Ashland Paving and Construction, Inc., Oldcastle Materials, Inc., and various regional paving operations, bringing deep operational expertise.

The integration playbook developed during these years would prove crucial to later success. Unlike some roll-ups that immediately centralize operations and impose standardized processes, Construction Partners took a more nuanced approach. Local management teams kept their decision-making authority on day-to-day operations, project bidding, and customer relationships. Corporate headquarters provided support in areas where scale genuinely helped: safety programs, equipment financing, insurance procurement, and financial reporting.

Fred Smith Company in North Carolina represented a particularly important acquisition. Jule Smith began his career in highway construction with Fred Smith Company in 1992, and served as President from 2009 to 2020. The Fred Smith family business traced its roots back generations in Johnston County, North Carolina, and brought both geographic expansion and, crucially, the future CEO into the Construction Partners organization.

By the time the company was preparing for its IPO in 2018, it had assembled a portfolio of operations across Alabama, Florida, Georgia, North Carolina, South Carolina, and Tennessee. More importantly, it had developed the institutional muscle for integration—the ability to acquire a family business on Friday and have it fully operational within the CPI system by Monday, without disrupting customers or employees.

The vertical integration strategy was already taking shape. Rather than simply acquiring paving companies, Construction Partners systematically added upstream assets: hot mix asphalt plants that could supply multiple paving crews, aggregate facilities (quarries and sand pits) that controlled key raw materials, and liquid asphalt terminals that reduced dependence on third-party suppliers. Each layer of vertical integration improved margins, reduced supply chain risk, and created barriers to competition.

"In a highly fragmented industry with an extremely long runway for continued growth, we believe CPI will continue to enhance value for all of our stakeholders." This conviction, expressed consistently by leadership over the years, reflected a clear-eyed understanding of both the opportunity and the competitive advantages being built.

V. Inflection Point #1: The 2018 IPO

The decision to go public in 2018 represented a calculated bet—one that would transform Construction Partners from a regional private equity portfolio company into a nationally-significant infrastructure compounder.

DOTHAN, Ala., May 3, 2018—Construction Partners, Inc., specializing in the construction and maintenance of roadways across five southeastern states, announced the pricing of its initial public offering of 11,250,000 shares of its Class A common stock at $12.00 per share. Construction Partners sold 9,000,000 shares, and certain selling stockholders sold 2,250,000 shares.

The pricing told an interesting story. The initial public offering price was expected to be between $15.00 and $17.00 per share. Coming in at $12—well below the range—suggested skepticism from public market investors about a regional paving company from Alabama. The skeptics would be proven spectacularly wrong.

Construction Partners received net proceeds of approximately $100 million after deducting underwriting discounts and commissions. Construction Partners intended to use the net proceeds to provide growth capital, to fund acquisitions and for general corporate purposes, which may include the repayment of debt from time to time.

The shares began trading on The Nasdaq Global Select Market on May 4, 2018 under the ticker symbol "ROAD." The ticker symbol itself—ROAD—captured the company's focused identity. This wasn't a diversified construction conglomerate; this was a company that built and maintained roads, period.

The IPO provided far more than just capital. Public company currency—tradeable stock—became a powerful tool for acquisitions. Family business owners who might prefer equity to cash now had a liquid option. The public listing also imposed discipline: quarterly reporting, analyst coverage, and institutional investor scrutiny forced continuous operational improvement.

The dual-class stock structure ensured that SunTx and management maintained control while accessing public capital. Class B shares, held primarily by the founders and SunTx affiliates, carried enhanced voting rights, insulating long-term strategic decisions from the pressures of activist investors or short-term traders.

From that $12 IPO price, the stock would climb steadily over the following years. By late 2025, with shares trading near $100, early investors had achieved returns that rivaled some of the most celebrated technology companies. The "boring" paving company from Alabama had outperformed most of the glamorous IPOs of its era.

VI. Inflection Point #2: The Infrastructure Investment & Jobs Act (2021)

If the IPO provided the financial foundation for growth, the Infrastructure Investment and Jobs Act provided the demand foundation.

The Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Law, was signed into law by President Biden on November 15, 2021. The law represents the largest long-term investment in our infrastructure and economy in our Nation's history, authorizing $1.2 trillion for transportation and infrastructure spending over five years from FY 2022 through FY 2026. Of the total authorized funding, approximately $550 billion is new infrastructure spending above current "baseline" levels.

At the core of the new law is a five-year reauthorization of the federal surface transportation program and $284 billion for highway, bridge, public transportation, and transportation safety improvements – more than half of the IIJA's total new investment.

For Construction Partners, the IIJA represented the fulfillment of a patient thesis. 17% of the 4-million-mile US public roads are in "poor" condition; road and bridge repair backlogs exceed $560 Billion. The recently signed Infrastructure Investment & Jobs Act and its ancillary Acts of $1.2 Trillion allocates $359 Billion for highway infrastructure over 5 years. This legislation should spur a "super cycle" in the asphalt paving industry.

The IIJA authorizes $477 billion in new funding over five years for surface transportation programs, including $351 billion for highways — a 38% boost above the baseline levels set in the last highway reauthorization bill, the FAST Act.

The Sunbelt positioning proved prescient. Not only did the region benefit from federal formula allocations, but state governments in CPI's footprint had simultaneously been increasing their own infrastructure investments. While other states struggle to fund major transportation projects, Texas' 10-year transportation spending plan has surpassed $100 billion for the third year in a row.

"From a macro perspective, continued increasing funding for public projects at the federal, state and local levels coupled with a steady commercial project environment in the southeastern United States continue to drive growth at CPI. At the micro level of the business, the entire CPI team continues to effectively execute our strategic goals throughout our footprint."

The IIJA didn't just increase demand—it increased visibility. State departments of transportation could now plan multi-year programs with confidence about federal funding. This visibility cascaded down to contractors like Construction Partners, who could bid on larger projects, commit to equipment purchases, and hire workers with confidence about future workloads.

The third macro trend is related to funding. Both the federal and state governments are investing in infrastructure, and that's going to continue. We see strong public contract bidding throughout our eight states and over 100 local markets and expect contract awards in FY2026 to increase approximately 15% over FY2025.

VII. Inflection Point #3: The Accelerated M&A Engine Post-IPO

With public currency and a supportive funding environment, Construction Partners shifted its acquisition strategy into high gear.

Revenue Growth and Market Expansion: Construction Partners has demonstrated a remarkable ability to grow its revenue streams, with a 68.5% increase from 2023 to 2025. This growth is not only a testament to the company's strong operational capabilities but also to its strategic expansion through acquisitions.

The post-IPO acquisition pace accelerated dramatically. The company reported 8.4% organic revenue growth, entry into two new states and five acquisitions in FY2025. The company developed a sophisticated playbook for identifying, evaluating, and integrating targets:

Platform Acquisitions: When entering a new state, CPI looked for a "platform" company—a well-established operator with strong management, multiple locations, and growth potential. This platform then became the foundation for smaller "tuck-in" acquisitions in adjacent markets.

Tuck-In Acquisitions: Smaller deals within existing states added market share, hot mix plants, and aggregate facilities. These deals often came at lower multiples because sellers valued the integration support CPI provided.

Vertical Integration: Some acquisitions focused specifically on upstream assets—aggregate quarries, liquid asphalt terminals—that reduced costs and supply chain risk across the entire portfolio.

Fiscal 2023 revenues were $1.56 billion, an increase of 20% compared to $1.30 billion in fiscal 2022. Gross profit was $196.4 million in fiscal 2023, an increase of 41% compared to $139.3 million in fiscal 2022.

The integration benefits became increasingly apparent in margins. As CPI added scale, it could negotiate better prices on equipment, insurance, and raw materials. Shared safety programs reduced incident rates and workers' compensation costs. Corporate overhead got spread across a larger revenue base.

In October 2023, the company announced ROAD-Map 2027, a strategic business plan aiming for revenues exceeding $3 billion by fiscal year 2027. With the announcement of the transformational acquisition of Lone Star Paving as the Texas platform company, the anticipated timeline to achieve those ROAD-Map 2027 goals was accelerated by almost two years.

VIII. Inflection Point #4: Texas Entry with Lone Star Paving (2024)

The Lone Star Paving acquisition represented Construction Partners' most ambitious and transformative deal—a bet on Texas that would reshape the company's geographic footprint and growth trajectory.

Construction Partners announced that it had entered into a definitive agreement to acquire Asphalt Inc., LLC d/b/a Lone Star Paving, headquartered in Austin, Texas. Lone Star is a vertically integrated asphalt manufacturing and paving company operating in attractive high-growth markets in central Texas, with 10 hot-mix asphalt plants, four aggregate facilities, and one liquid asphalt terminal supporting its operations. This value-enhancing acquisition will be immediately accretive to earnings upon closing and is anticipated to generate an annualized run-rate contribution of $530 million of revenue and $120 million of Adjusted EBITDA in fiscal 2025.

Under the terms of the definitive agreement, CPI acquired all of the outstanding membership units of Lone Star for $654 million in cash and 3 million shares of CPI's Class A common stock. In addition, CPI paid cash to the sellers of Lone Star in an amount equal to the working capital remaining in Lone Star at the closing in four quarterly installments following the closing and purchased from the sellers an entity holding certain real property for $30 million in cash.

The $950 million transaction includes consideration from CPI of $654 million in cash, 3 million shares of CPI stock, reimbursement of working capital, and a future purchase commitment for assets retained by the members of Lone Star Paving.

Lone Star's talented team created a well-established and respected brand in Texas under the leadership of its founder and Chief Executive Officer, Jack Wheeler, an industry veteran with more than 40 years of experience in the asphalt business.

Jack Wheeler embodied the type of founder CPI sought: experienced, respected, and willing to remain engaged during the transition. His four decades in the asphalt business provided institutional knowledge that couldn't be replicated—relationships with TxDOT officials, understanding of local competitive dynamics, and credibility with employees and customers.

Lone Star primarily serves the Austin, San Antonio and Temple-Killeen metropolitan areas. Through this acquisition, CPI added three of the fastest growing markets in the country to its geographic footprint.

The Texas opportunity couldn't be overstated. Texas features more than 700,000 lane miles supported by the largest state transportation funding program in the United States. This program provides stable funding sources and the highest allocation from the Infrastructure Investment and Jobs Act.

While many state transportation budgets are pegged to dwindling gas tax revenue, Texas has increased funding from other sources over the last decade. In 2014 Texas voters approved Proposition 1, which allocates tax revenue from oil and gas production—a key industry in the state—to the state highway fund. The next year they approved Proposition 7, which directed more state sales tax revenue to transportation. Together, these measures have generated more than $40 billion for the State Highway Fund to date.

In 2014 and 2015, Texas voters overwhelmingly supported Propositions 1 and 7 which fund 47% of the record $104 billion UTP investment.

The acquisition of Lone Star closed in November 2024, allowing CPI to include Lone Star's expected operations in its outlook earlier than previously anticipated.

ROAD's shares rose 13.4% during the trading session on October 21, 2024 when the acquisition was announced. The market immediately understood what CPI was accomplishing: entering the largest and best-funded highway market in America with a platform perfectly positioned for expansion.

IX. The Business Model Deep Dive

Understanding Construction Partners requires understanding the elegant simplicity of its business model—and the complexity hidden within that simplicity.

Construction Partners is an asphalt-centered infrastructure company dedicated to building and maintaining the transportation networks that keep the Sunbelt moving. Their vertically integrated operations include hot-mix asphalt plants, aggregate facilities, and liquid asphalt terminals, allowing them to ensure quality, efficiency, and timely project delivery. They operate across eight states, serving both public and private clients on roads, highways, runways, bridges, and commercial projects.

The Revenue Mix

Publicly funded projects make up the majority of its business and include local and state roadways, interstate highways, airport runways and bridges. The company also performs private sector projects that include paving and sitework for office and industrial parks, shopping centers, local businesses and residential developments.

Public projects, representing approximately 63% of fiscal 2024 revenues, provide stability and visibility. The Florida DOT alone represented 13.6% of fiscal 2024 revenues—a concentration risk on one hand, but a testament to the company's competitive position on the other. Government customers are demanding but predictable; they pay their bills and award contracts through transparent competitive processes.

Private sector work—site development for warehouses, parking lots for shopping centers, paving for residential developments—provides margin enhancement and fills capacity gaps between public projects. This work tends to be smaller, shorter-duration, and higher-margin than public highway jobs.

The Vertical Integration Advantage

The true genius of Construction Partners' model lies in its vertical integration. Rather than simply being a paving contractor that buys materials from third parties, CPI controls significant portions of its supply chain.

Their vertically integrated operations include hot-mix asphalt plants, aggregate facilities, and liquid asphalt terminals.

Each hot mix asphalt plant serves as a profit center in its own right. CPI uses the asphalt internally for its construction projects, but also sells to third parties—smaller contractors who lack their own plants. This creates a competitive dynamic where CPI benefits whether it wins a particular project or a competitor does.

Aggregate facilities (quarries and sand operations) provide the stone, gravel, and sand that constitute the bulk of asphalt's weight. Owning these facilities locks in a critical input and generates additional revenue from sales to third parties.

Liquid asphalt terminals store the petroleum-derived binding agent that holds asphalt together. Controlling terminal capacity provides flexibility in purchasing—CPI can buy when prices are favorable rather than paying spot rates.

The Decentralized Operating Model

Fred Smith has served as President and Chief Executive Officer of Construction Partners since April 2021. Before that, he served in other senior management roles within the company, including as its Chief Operating Officer and Senior Vice President. Mr. Smith also served in various management roles for the Company's North Carolina subsidiary, including as its President from 2009 to 2020.

Construction Partners operates as a "family of companies"—each acquired business retains its local brand, management team, and community identity. This isn't just sentiment; it's strategy. Local managers know their markets, their customers, and their competitors in ways that distant corporate executives never could.

Corporate headquarters in Dothan provides shared services: safety programs, legal support, financial reporting, insurance procurement, and capital allocation. Local operations make day-to-day decisions about bidding, staffing, and execution.

Our people and the culture they create and maintain are the key to our business and the primary differentiator for CPI in our more than 100 local markets and as a buyer of choice for new acquisitions. As a family of companies, we strive to live out our core values of family and respect, which create an incredible place to work together each day.

X. Recent Performance & Current State (FY2024-2025)

The fiscal years 2024 and 2025 demonstrated Construction Partners' execution capabilities at an unprecedented scale.

DOTHAN, Ala., Nov. 21, 2024—Construction Partners reported financial and operating results for the fiscal quarter and year ended September 30, 2024. We are proud of the contributions from our more than 5,000 employees that helped deliver a record fiscal year and generated revenue growth of 17%, net income growth of 41%, and Adjusted EBITDA growth of 28% compared to fiscal 2023.

Project backlog was approximately $3.03 billion at September 30, 2025, compared to $2.94 billion at June 30, 2025 and $1.96 billion at September 30, 2024.

That backlog growth—from $1.96 billion to $3.03 billion in a single year—tells the story of a company successfully integrating a major acquisition while continuing to win new business organically. The company has approximately 80%-85% of the next 12 months' contract revenue covered in backlog.

Construction Partners reported preliminary fiscal 2025 results with key ranges: revenue $2.800B–$2.820B (vs $1.824B in FY2024), net income $101.0M–$101.8M (vs $68.9M), Adjusted EBITDA $421.0M–$425.0M (vs $220.6M) and Adjusted EBITDA margin 15.0%–15.1% (vs 12.1%).

The margin expansion is particularly noteworthy. Moving Adjusted EBITDA margin from 12.1% to 15.0%+ demonstrates the operating leverage inherent in the business model—scale drives efficiency, vertical integration captures value, and shared corporate costs get spread across a larger revenue base.

FY2026 outlook: revenue $3.4B–$3.5B, net income $150M–$155M, Adjusted EBITDA $520M–$540M and margin 15.3%–15.4%.

The fourth quarter represented revenue of $900 million, an increase of 67% compared to the same quarter last year, of which 10.4% was organic growth.

XI. Porter's Five Forces Analysis

Threat of New Entrants: LOW

The asphalt paving industry presents formidable barriers to new entrants. The capital requirements for hot mix asphalt plants can exceed tens of millions of dollars per facility. Environmental permitting for aggregate quarries and asphalt plants takes years and faces significant community opposition. Established relationships with state DOTs—built over decades—cannot be easily replicated.

Most critically, the "radius game" means a new entrant must establish facilities in specific geographic areas to compete. CPI's network of plants across eight states creates overlapping competitive moats that would require massive capital deployment to challenge.

Bargaining Power of Suppliers: MODERATE

Liquid asphalt cement, derived from petroleum refining, represents a meaningful input cost subject to commodity price volatility. However, The company's vertical integration strategy, which includes manufacturing and distributing hot mix asphalt, paving, site development, and mining aggregates, creates operational efficiencies and a competitive edge.

CPI's ownership of aggregate facilities and liquid asphalt terminals substantially reduces supplier power for its most significant inputs. For other supplies—equipment, fuel, consumables—CPI's scale enables favorable procurement terms.

Bargaining Power of Buyers: MODERATE-LOW

Federal, state and local DOT budgets drive industry performance, with the public sector generating 95% of total industry revenues in 2016.

Public customers award contracts through competitive bidding, creating price pressure. However, CPI's geographic diversification means no single customer dominates the revenue base, and the company's reputation for quality and reliability commands some pricing power. The Florida DOT at 13.6% of revenues represents the largest single customer—significant but not dominant.

Threat of Substitutes: VERY LOW

Approximately 94% of America's paved roads use asphalt surfaces. Concrete alternatives exist but cost significantly more and prove less suitable for many applications. More importantly, roads require ongoing maintenance regardless of the surface material—creating perpetual demand for repair and resurfacing services.

Competitive Rivalry: MODERATE

There are no companies that hold a market share exceeding 5% in the Paving Contractors in the US industry.

Competition remains local/regional rather than national. Within each geographic market, CPI faces competition from other vertically integrated players, regional contractors, and smaller family-owned operators. However, CPI's advantages—scale, vertical integration, financial strength—create meaningful differentiation that limits purely price-based competition.

XII. Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

Construction Partners exhibits classic scale economies across multiple dimensions:

- Fleet utilization improves with size, spreading fixed costs across more projects

- Centralized procurement leverages combined purchasing power

- Corporate overhead (legal, finance, safety, HR) distributes across larger revenue base

- Hot mix plants can serve multiple paving crews, improving asset utilization

Consistent with historical seasonality, the company anticipates the first half of the fiscal year to contribute approximately 40%-42% of annual revenue and 30%-34% of adjusted EBITDA. In the second half of the year, during peak construction season, they expect to deliver the remaining 58%-60% of revenue and 66%-68% of the adjusted EBITDA.

This seasonality creates operating leverage that rewards scale—fixed costs are covered in the slower months, allowing strong incremental margins during peak season.

2. Network Economies: WEAK

Traditional network effects are limited in infrastructure construction. Unlike software platforms where each additional user increases value for others, CPI's competitive advantage doesn't fundamentally improve as it adds customers or projects.

However, the company does benefit from "network-adjacent" effects: a larger footprint creates more opportunities for equipment and personnel redeployment, more attractive career paths for employees, and a broader reputation that facilitates acquisitions.

3. Counter-Positioning: MODERATE

CPI's strategy creates a classic counter-positioning challenge for small family operators. These competitors cannot easily replicate CPI's access to public capital markets, corporate support functions, or multi-state geographic footprint. Attempting to do so would require fundamental changes to their business models—changes that most family operators are unwilling or unable to make.

Meanwhile, large national construction companies typically view the Sunbelt paving market as too local, too fragmented, and too relationship-dependent to warrant strategic focus. CPI occupies a "Goldilocks zone" between these two competitor types.

4. Switching Costs: LOW-MODERATE

For end customers (DOTs, private developers), switching between contractors involves limited costs. Projects are typically awarded through competitive bidding, and contractors must earn each job on its merits.

However, CPI's vertical integration creates implicit switching costs. Smaller contractors who purchase asphalt from CPI plants face switching costs if CPI's plants are the most convenient option—and those contractors may think twice before aggressively competing against their supplier.

5. Branding: MODERATE

In a government contracting environment, brand matters less than in consumer markets—but it doesn't disappear entirely. CPI's family of companies maintains strong local reputations built over decades. These reputations influence private sector customer decisions and create preference in situations where non-price factors affect contract awards.

The "family of companies" approach preserves these local brands rather than subsuming them under a corporate identity, protecting this accumulated brand equity.

6. Cornered Resource: MODERATE-STRONG

CPI's aggregate facilities represent a potentially cornered resource. Quarries and sand operations require specific geology, large land parcels, and environmental permits that are increasingly difficult to obtain. Once permitted, these facilities can operate for decades, providing secure access to critical inputs.

Additionally, the management talent that CPI has assembled—executives with decades of industry experience and local relationships—represents an intangible cornered resource that competitors cannot easily replicate.

7. Process Power: MODERATE

The company's acquisition integration playbook represents accumulated process knowledge that improves execution of each successive deal. The ability to acquire a family business, integrate it operationally, and retain key personnel while capturing synergies is a learned capability that CPI has refined over two decades.

XIII. Management & Leadership

The management team at Construction Partners reflects a deliberate blend of industry veterans, financial professionals, and multi-generational family business leadership.

Jule Smith is CEO of Construction Partners Inc. Fred Julius "Jule" Smith, III grew up in Johnston County, North Carolina. After graduating from Clayton High School, he earned a Bachelor of Arts in History from Wake Forest University, followed by a Master's in Business Administration from Wake Forest University's Babcock Graduate School of Management. Jule began his career in highway construction with Fred Smith Company in 1992, and served as President from 2009 to 2020. In 2020, he began working for Construction Partners, Inc. as its Chief Operating Officer and was named Chief Executive Officer on March 31st, 2021. He served in the United States Navy from 2004 to 2012 as a Supply Corps Officer.

Smith's trajectory—from family business to acquired subsidiary to corporate CEO—embodies the Construction Partners model. His operational credibility with the family companies comes from having lived their experience; his strategic perspective comes from watching the roll-up strategy execute over years.

Jule Smith, age 51, has served as the Company's Chief Operating Officer since October 2020. Before that, he was a Senior Vice President of the Company since 2017 and also served in various management roles for the Company's North Carolina subsidiary since 2005, including as its President from 2009 to 2020. Prior to that, he held various other positions within Fred Smith Construction, Inc. and also served in the Supply Corps of the U.S. Navy.

Ned Fleming is a Founding Partner and the Managing Partner of SunTx Capital Partners. He serves on the board of multiple portfolio companies including his role as Executive Chairman of Construction Partners, Inc.

Ned Fleming's continued involvement as Executive Chairman provides strategic continuity and access to SunTx's deal-making capabilities. Fleming's dual role—managing partner at SunTx, executive chairman at CPI—ensures alignment between the company's largest shareholder and its strategic direction.

Mr. Hoffman has served as Chief Financial Officer since April 2023. Prior to that, Mr. Hoffman served as Senior Vice President, Finance from April 2021 to March 2023 and as Chief Financial Officer of Wiregrass Construction Company, our Alabama subsidiary, from 2009 to 2021.

CFO Greg Hoffman's path mirrors the company's grow-from-within culture. Rising from a subsidiary CFO role to corporate CFO, Hoffman brings deep understanding of local operations alongside the financial sophistication required for a public company executing major acquisitions.

XIV. Investment Considerations: Bull Case & Bear Case

The Bull Case

-

Secular Tailwinds Persist: Federal infrastructure funding through IIJA continues through 2026, and state programs in Texas, Florida, and other Sunbelt states show no signs of diminishing. The fundamental need to maintain and expand American road infrastructure creates durable multi-decade demand.

-

Acquisition Runway Remains Massive: "Even the sponsors that are coming in now more recently still have a tremendous amount of targets and a lot of whitespace." With 3,500+ asphalt plants nationally and ongoing generational succession challenges among family owners, CPI's acquisition pipeline extends well into the future.

-

Margin Expansion Continues: As the company scales, operating leverage should continue driving margin improvement. The fiscal 2025 demonstration of 15%+ EBITDA margins suggests further expansion potential as integration benefits compound.

-

Texas Platform Unlocks New Growth: The Lone Star Paving acquisition positions CPI in the nation's largest highway market, with clear paths for both organic growth and acquisitive expansion across the state.

-

Management Execution Track Record: The team has demonstrated ability to execute on its stated strategy over 20+ years, integrating acquisitions successfully while maintaining operational excellence.

The Bear Case

-

Valuation Premium Embedded: Construction Partners trades at a premium compared with the Zacks Building Products - Miscellaneous industry on a forward 12-month price-to-earnings ratio basis. With a forward 12-month P/E ratio of 40.7, the company stands above the broader Construction sector and the S&P 500 index. The stock's premium valuation leaves limited margin for error.

-

Commodity Input Exposure: Liquid asphalt cement prices correlate with petroleum markets. Significant oil price spikes could pressure margins, particularly if competitive dynamics limit the ability to pass through cost increases.

-

Interest Rate Sensitivity: The acquisition strategy requires substantial debt financing. Higher-for-longer interest rates increase the cost of capital for deals and could slow acquisition pace or compress returns.

-

Integration Risk at Scale: As acquisitions grow larger (Lone Star at $950M total value), integration complexity increases. A stumble on a major deal could damage the company's reputation as a preferred acquirer.

-

Customer Concentration: Florida DOT represents 13.6% of revenues. Political shifts, budget constraints, or relationship deterioration could create meaningful revenue volatility.

-

Weather and Natural Disasters: Hurricane Debby, Francine, and Helene impacted August and September 2024. Climate-related disruptions affect construction schedules and can impact quarterly results unpredictably.

XV. Key Performance Indicators to Monitor

For investors tracking Construction Partners' ongoing performance, three KPIs warrant particular attention:

1. Organic Revenue Growth Rate

Management has targeted 7-8% annual organic growth from fiscal 2026 through 2030. This metric isolates underlying market share gains and pricing power from acquisition-driven growth. Consistent organic growth above the target range signals strong competitive positioning; growth below target may indicate market share erosion or pricing pressure.

The company achieved 8.4% organic growth in fiscal 2025, above the stated target. Monitoring quarterly organic growth trends provides early indication of market dynamics.

2. Adjusted EBITDA Margin

This metric captures the operating efficiency of the combined business, reflecting both scale benefits and integration success. Adjusted EBITDA margin expanded from 12.1% in FY2024 to 15.0%–15.1% in FY2025.

Continued margin expansion validates the thesis that scale drives efficiency. Margin compression would signal competitive pressure, integration challenges, or cost inflation that cannot be passed through to customers.

3. Project Backlog

The company has approximately 80%-85% of the next 12 months' contract revenue covered in backlog.

Backlog provides forward visibility into revenue and capacity utilization. Growing backlog indicates strong demand and competitive win rates; shrinking backlog could signal market weakness or competitive pressure. The composition of backlog—public vs. private, geographic distribution, project duration—provides additional insight into business quality.

XVI. Conclusion: The Road Ahead

Construction Partners' journey from a collection of family-owned Alabama paving companies to a nearly $6 billion market cap infrastructure compounder represents one of the most compelling roll-up success stories of the past two decades.

The thesis proved out: fragmented industries with high-quality local operators, stable recurring demand, and opportunities for operational improvement through scale can generate extraordinary returns for patient capital. The execution proved consistent: acquire with respect for what founders built, retain local management, integrate back-office functions, and deploy capital for vertical integration and growth.

"The fundamentals in our core markets remain strong, supported by ongoing transportation investment, population growth, and healthy commercial demand. With these tailwinds, our fiscal 2026 outlook reflects another year of meaningful growth. We are confident in CPI's ability to build on its momentum and continue creating long-term value for our employees, partners, and shareholders."

The next chapter presents both opportunity and challenge. The opportunity: Texas entry opens the largest highway market in America; federal and state funding remains robust; the acquisition pipeline remains full; and the organization has never been better positioned to execute. The challenge: maintaining discipline at scale, integrating larger deals successfully, and delivering growth that justifies an above-market valuation.

What began with a simple observation—that roads in the Sunbelt needed building and maintaining, and that family businesses doing this work needed an exit path—has evolved into a sophisticated infrastructure platform. The asphalt beneath our tires may still seem mundane, but the company laying it has proven anything but ordinary.

For investors evaluating Construction Partners, the fundamental question isn't whether the business model works—that's been demonstrated conclusively over two decades. The question is whether the current valuation adequately reflects the growth ahead versus the risks of execution at scale. The road stretches forward; the question is how far it runs.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube