Commercial Metals Company: From Dallas Scrap Yard to America's Rebar King

I. Introduction & Episode Roadmap

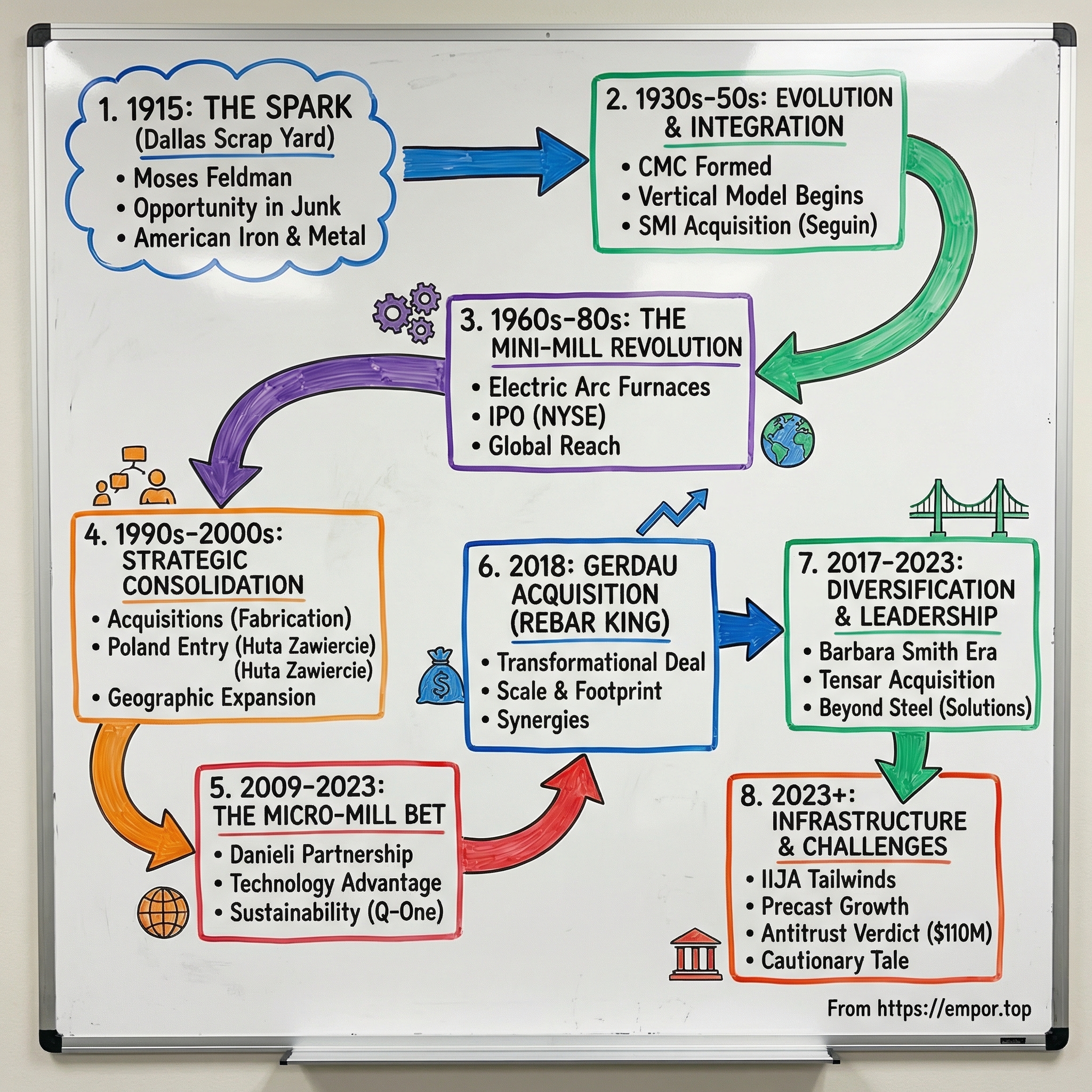

Picture a hot Texas summer day in 1915. Moses Feldman, a Russian immigrant who had arrived in Galveston just nine years earlier, stands in a dusty lot on the outskirts of Dallas, surrounded by twisted metal, rusted pipes, and the detritus of industrial America. He sees what others dismiss as junk. He sees opportunity.

More than a century later, that single scrap yard has transformed into Commercial Metals Company (CMC), a company that produces rebar and related construction materials headquartered in Irving, Texas. Along with Nucor, it is one of two primary suppliers of steel used to reinforce concrete in buildings, bridges, roads, and infrastructure in the U.S.

The numbers tell a story of remarkable scale: In its fiscal 2023 year, it shipped 6.1 million short tons of steel to external customers; 84% of its sales were in the United States and 16% of its sales were from its facilities in Poland. With over 13,000 employees across 213 facilities in the United States, United Kingdom, Central Europe, and Asia, the company recycled 8.87 million metric tons of metal and produced 5.33 million metric tons of raw steel in fiscal year 2024.

The central question of this story is profound yet often overlooked: How did a Russian immigrant's scrap yard in Dallas become a Fortune 500 company that quietly builds the hidden backbone of American infrastructure?

The answer lies in understanding several interconnected themes that run through CMC's 110-year history: the power of vertical integration, the mini-mill revolution that upended the steel industry, disciplined M&A execution, and the unglamorous but essential business of concrete reinforcement. This is a company that doesn't seek headlines—you won't find CMC sponsoring stadiums or running Super Bowl ads. Yet when you drive across a bridge, enter a high-rise, or walk into a sports arena, there's a good chance CMC steel is silently holding everything together.

What makes CMC particularly fascinating for investors is its ability to continuously reinvent itself through technology and strategic acquisitions while maintaining the family-instilled culture of thrift that defined its earliest days. From pioneering the world's first micro-mill to executing the transformational Gerdau acquisition, CMC has demonstrated that "boring" infrastructure plays can generate exceptional returns when managed with operational excellence and strategic clarity.

But this story also carries warnings. The company's November 2024 antitrust verdict—a $110 million judgment that will treble to $330 million plus attorney fees—reveals the thin line between aggressive competition and anticompetitive behavior in concentrated markets. It's a cautionary tale for any company that dominates its niche.

The backdrop for CMC's current opportunity couldn't be more favorable. Three years into the 5-year $1.2 trillion Infrastructure Investment and Jobs Act, only 40% of funds from the infrastructure law have been allocated to projects. White House data analyzed by CNBC unveiled that the biggest chunk of IIJA money was flowing to road and bridge construction. For a company whose products literally reinforce American infrastructure, the timing couldn't be better.

Let's trace the journey from that Dallas scrap yard to America's rebar kingdom.

II. Founding & The Feldman Family Legacy (1915–1950s)

The story of Commercial Metals Company begins not with steel mills or construction sites, but with the timeless immigrant narrative of America—a man arriving at America's shores with little more than ambition and an eye for opportunity.

The company's historical roots stretch back to 1915, when Moses Feldman started a scrap metals company named American Iron & Metal Company. Feldman, who emigrated from Russia and settled in Houston ten years before he founded American Iron & Metal, superintended his company's growth during its early years.

Moses Feldman establishes his first scrap operation in Dallas. The business was simple: buy scrap metal from local sources, process it, and sell it to manufacturers who could transform it into new products. In an era before environmental consciousness made recycling fashionable, Feldman recognized the economic logic of giving metal a second life.

The early years were about survival and slow accumulation. American Iron & Metals lists $51,000 of materials in its inventory—a modest sum that represented the entirety of the family's commercial enterprise. But Moses Feldman was building something more valuable than inventory: he was establishing relationships, learning the rhythms of the scrap metal trade, and training the next generation.

Moses Feldman's eldest son David is sent to oversee a rail salvage job in Florida, leading to CMC's first international shipment of scrap metal out of the Port of Miami. This early foray beyond Texas borders would prove prophetic—CMC's story would eventually span continents.

Moses Feldman signs control of American Iron & Metals over to his son Jacob. The generational handoff marked a pivotal moment. Jacob Feldman had absorbed his father's business instincts but brought a more formal approach after graduating from Southern Methodist University. The younger Feldman joined the family business after he graduated from Southern Methodist University and in 1932, with the help of family members, formed a brokerage house in Dallas named Commercial Metals Company to buttress the family's scrap operations.

The timing of this incorporation—1932, the depths of the Great Depression—might seem inauspicious. Yet it revealed something essential about the Feldman approach: they saw opportunity when others saw only despair. The company is formed by Jacob Feldman as a scrap trading brokerage, capitalized at $100,000, with Jake owning 98%. His high school friend Tom Kleinman came on as co-director to handle the company's finances—a partnership that would last decades.

For the next two decades, Commercial Metals remained a scrappy (pun intended) Texas operation. But Jacob Feldman harbored larger ambitions. The scrap business had taught him the cyclical nature of metal markets, the importance of logistics, and crucially, the value that could be captured by controlling more of the supply chain.

In 1949, CMC made a move that would reshape its destiny: CMC purchases assets of Southern Iron & Metal in Beaumont, Texas. This acquisition marked CMC's first tentative step toward steel manufacturing. But the real breakthrough came when an entrepreneur named Marvin Selig entered the picture.

Marvin Selig buys a cornfield in Seguin, Texas, for $300, and officially establishes Structural Metals, Incorporated (SMI). The SMI mill will become the first Commercial Metals Company mill in 1963. That $300 cornfield purchase would prove to be one of the most consequential real estate transactions in American steel history.

First rebar for commercial sale is produced at SMI. In its first year the company is profitable and produces 2,300 tons of rebar. Customers include fabricators, supply companies, contractors and the Texas Highway Department.

The strategic insight embedded in this evolution deserves emphasis: As the first steel manufacturer in the United States to adopt a vertical integration business model, we understood the importance of connecting our businesses, both up and downstream, to facilitate operations. This wasn't just about diversification—it was about capturing value at multiple points along the chain while reducing dependency on external suppliers and customers.

By combining the recycling and processing of scrap metals with the blending of processed scrap into new steel and the fabrication of finished steel products, CMC revolutionized the way the steel industry operates.

The family business DNA established in these early decades continues to define CMC today. The culture of thrift—buying a cornfield for $300 rather than premium industrial land, starting with scrap rather than virgin ore, building relationships over generations—became embedded in the company's operating philosophy. It's a culture that still manifests in CMC's conservative balance sheets, disciplined capital allocation, and willingness to be patient in building competitive advantages.

III. The Mini-Mill Revolution & Going Public (1960s–1980s)

The 1960s brought transformation to CMC—not merely growth, but a fundamental reimagining of how steel could be made. While integrated steel giants like U.S. Steel and Bethlehem Steel operated massive blast furnaces fed by iron ore and coal, a new paradigm was emerging: the electric arc furnace mini-mill.

In the 1950's, CMC began thinking about how to make steel differently. And by 1962, had built its first electric arc furnace using electric energy and recycled scrap metal. This important event in CMC history meant that we would not run our mills with coal and iron ore. Every CMC mill uses electric energy and 100% recycled scrap to produce our products.

This wasn't just an operational choice—it was a strategic bet that would prove visionary. Traditional integrated steel mills required billions in capital, massive workforces, and proximity to iron ore deposits and ports. Mini-mills, by contrast, could be built for a fraction of the cost, located near customer markets, and fed by locally sourced scrap metal. The environmental profile was radically different too: Since our first heat of steel in 1962, we have manufactured steel using recycled scrap metal and Electric Arc Furnace (EAF) technology, which is far more efficient and environmentally friendly than traditional blast furnace technology, using 82% less energy than the industry average and producing 63% less CO2 per ton of steel we melt.

The broadening of the company's interests began in 1963, when Commercial Metals acquired a 74 percent interest in Structural Metals, Inc. Located in Seguin, Texas, near San Antonio, Structural Metals operated an electric furnace steel mill that provided Commercial Metals with a new source of sales and increased the company's market for its own processed raw materials.

The acquisition of SMI created a powerful flywheel. CMC's recycling operations generated scrap metal. The scrap fed the mini-mill. The mini-mill produced rebar and merchant bar products. Those products served construction customers. The integration reduced costs, improved margins, and created strategic optionality.

In 1960, CMC took another transformational step: ownership of Commercial Metals changed from private to public hands when the company became the first independent metals firm to be listed on the American Stock Exchange (the company would eventually move to the New York Stock Exchange). The switch to public ownership ushered in a period of diversification and expansion, touching off the first definitive surge of growth recorded by the company.

Being first matters. As the first secondary metals company listed on a major exchange, CMC established credibility and gained access to capital markets that would fund its expansion. By the beginning of the 1960s, nearly five decades of operation had built a roughly $50 million company.

The growth accelerated throughout the decade. In total, the growing Commercial Metals empire comprised 32 plants and offices in the United States and abroad by the late 1960s, positioning it as a major competitor in what was becoming an increasingly important and lucrative global industry. Its sixth international office was opened at the end of 1967 in Zug, Switzerland, complementing the company's other trading offices in Amsterdam, Tokyo, Taipei, Montreal, and Mexico City.

Annual sales eclipsed $320 million in 1973, then nearly doubled the following year, reaching $643 million, while earnings nearly quadrupled, soaring to more than $19 million.

But success brought challenges. By virtue of its success as a broker, manufacturer, and processor of scrap metals, Commercial Metals soared to the top of its industry, ranking as one of the largest independent companies in the country, but after the encouraging results of 1970, Jacob Feldman suffered a heart attack a year later and the company's financial health likewise deteriorated. Though Feldman remained titular head of the company, Charlie Merritt, who joined Commercial Metals in 1937 as a stenographer, essentially assumed control of the company's day-to-day operations. Under Merritt's stewardship, Commercial Metals' financial growth came to an abrupt halt, but the blame did not rest on Merritt's shoulders. A nationwide recession and laggard demand overseas combined to hamper Commercial Metals' growth, curtailing production volume at its 22 scrap processing plants and diminishing its scrap metals trading activities.

The 1970s recession revealed the cyclicality inherent in steel and construction. But it also demonstrated CMC's resilience—the company survived while many competitors did not. The lesson was clear: in a cyclical business, conservative financial management during good times provides the cushion to survive bad times.

In 1979, Stanley Rabin, age 40, is appointed CMC president and chief executive officer. Rabin's appointment marked the transition from family leadership to professional management—a critical evolution for any company seeking to scale beyond its founder's capabilities.

The 1980s brought renewed expansion. CMC acquires the Connors minimill in Birmingham, Alabama. In 1984, the company acquired Connors Steel Co.'s mini-mill in Birmingham, Alabama.

In 1986, CMC reported a 33% increase in cash flow compared to the prior year, as well as record earnings and shipments at the SMI, Seguin minimill. The Seguin facility had evolved from that $300 cornfield into a world-class operation. As the company's history notes, CMC's minimill in Seguin, Texas completed its transformation from a regional operation to a world-class steel mill due to the impact from a new electric arc furnace and caster.

The following year, 1985, marked Commercial Metals' 70th year of business, a milestone that marked the passing of two world wars and numerous economic hills and valleys since Moses Feldman had arrived in Galveston and founded American Iron & Metals Company. Over the course of seven decades, Commercial Metals had evolved into an internationally recognized firm, involved in three main metals-related businesses through the manufacturing and fabrication of steel products and copper tubing, the recycling of ferrous and nonferrous scrap metals, and the marketing and trading of metals products and raw materials.

Why does the mini-mill model matter for investors? It creates structural cost advantages that compound over time. Lower capital intensity means higher returns on invested capital. Regional focus reduces logistics costs and strengthens customer relationships. The scrap-based model provides natural inflation protection, as both input costs and output prices tend to move together. And the smaller scale allows nimble response to market conditions—easier to adjust production at a mini-mill than to slow a blast furnace.

IV. Strategic Consolidation & Geographic Expansion (1990s–2000s)

The 1990s marked CMC's emergence as a consolidator—a company with the financial strength and operational expertise to roll up fragmented industry segments while maintaining disciplined pricing.

During the first nine months of 1993, the company's revenues increased 44 percent, while its profits exploded exponentially, jumping a prodigious 135 percent.

As these financial records were being achieved, the company strengthened its processing capabilities further, acquiring the assets of three Texas scrap processing facilities, Atlas Iron & Metal, Federal Iron & Metal, and Laredo Scrap Metals, in September 1995.

The logic was simple but powerful: each additional scrap processing facility fed more raw material into CMC's mills, reducing external purchasing while building density in core markets. The Texas focus wasn't accidental—it reflected a strategy of being dominant in specific regions rather than spreading thin across the country.

A CMC press release on May 2, 2000 announced the company's acquisitions of two southern California rebar fabrication companies. The expansion into fabrication added another link to the value chain. Raw scrap became steel billets, billets became rebar, and now CMC could bend and shape that rebar into custom configurations for construction projects.

The 1990s saw major expansions in recycling and fabrication, culminating in the 1995 acquisitions of Atlas Iron & Metal, Federal Iron & Metal, and Laredo Scrap Metals, which bolstered CMC's scrap processing network across Texas. By 1993, further acquisitions like Shepler's Equipment Co. and Construction Materials Inc. extended the product line into concrete-related items, solidifying a vertical integration model that combined scrap recycling, steel melting in minimills, and fabrication into a cohesive operation with a capacity exceeding 1.7 million tons annually by 1994.

But the most transformative move of this era took CMC international for the first time as a manufacturer.

Commercial Metals AG has been selected as the preferred bidder to purchase all the shares of Poland's Huta Zawiercie SA. Impexmetal SA located in Warsaw, Poland owns 71.1% of the outstanding shares of Huta Zawiercie and these are controlled by Polish treasury. US' longs producer CMC has competed with Arcelor, LMN Holdings and two local Polish companies during the negotiations of purchasing stakes of Huta Zawiercie.

On December 3, 2003 the mill began a new chapter in its history. After the period of intensive negotiations, Commercial Metals Company (International) AG in Switzerland acquired the outstanding shares from the Polish company Impexmetal and became the majority shareholder of Huta Zawiercie. As of this day the mill became the part of CMC capital group and changed its name into CMC Zawiercie SA. The mill took advantage of dynamic development and improvement process and just one year after the acquisition reported record production and sales volumes which allowed planning new investments and modernizations.

Huta Zawiercie operates a steel minimill similar to those operated domestically by CMC. Furthermore, the company's foreseen capacity is 1 million tons with two electric arc furnaces (EAF). The company produces mainly rebar and wire rod at two separate rolling mills. CMC's authorities made a statement that Huta Zawiercie provided a unique opportunity for investment in an updated facility with producing products which are familiar for the growing Polish and European markets.

CMC Poland Sp. z o.o. operates a state-of-the-art steel mill in Zawiercie, Poland, and has grown its position as a leading domestic and foreign supplier with over 120 years of mill operations experience.

The Poland acquisition reflected several strategic considerations. First, Poland's EU accession in 2004 promised strong construction demand as the country invested in infrastructure to European standards. Second, the facility's mini-mill model matched CMC's operational expertise. Third, the price was attractive relative to building greenfield capacity. And fourth, geographic diversification reduced dependence on U.S. construction cycles.

CMC Poland is one of the largest steel manufacturers in EAF process and metals recyclers in Poland, and we take seriously our responsibility for protecting the environment. We value the communities in which we operate and live. Steel scrap makes up more than 92% of charge material; 98% of charge material is supplied from locations situated within 800 kilometers distance.

Throughout this expansion period, CMC maintained its conservative financial approach. Acquisitions were funded primarily with cash flow rather than aggressive leverage. Integration focused on operational improvement rather than financial engineering. And the company continued investing in its existing facilities while expanding its footprint.

Commercial Metals Company reported sales of $2.7 billion and net earnings of $46.3 million for its fiscal year ending August 31, 2000.

By the early 2000s, CMC had built a business model that would prove remarkably durable: scrap recycling fed mills, mills fed fabrication facilities, fabrication facilities served construction customers. Each link in the chain added value while reducing vulnerability to external suppliers or customers. The vertical integration that Jacob Feldman had intuited in the 1960s had matured into a systematic competitive advantage.

V. The Micro-Mill Innovation: CMC's Technology Bet (2009–2023)

If the mini-mill revolution distinguished CMC from integrated steel producers, the micro-mill innovation would distinguish CMC from other mini-mill operators. This is where the company placed a technology bet that would prove both brilliant and legally contentious.

Commercial Metals Co. (CMC), an Irving, Texas-based manufacturer and recycler of steel and metal products, recently started up the first in a "new generation of Danieli continuous casting-rolling, compact micromills," in Mesa, Ariz. The CMC micromill has a rated capacity of 300,000 shtpy of 12- to 36-mm rebar and Y sections, although it's capable of producing bigger sizes up to 57-mm bar, according to Danieli. The mill makes use mainly of local scrap and supplies CMC's local fabrication shops as well as the Southwest market. "CMC plant startup, which occurred slightly over one year from groundbreaking, is a remarkable technology milestone in production of commercial steel long products."

CMC was the first in the world to successfully operate a micro mill – and now we have two. These plants have smaller footprints and are just the right size for their markets. They connect the two main steps in rebar production – melting recycled scrap into molten steel and forming that steel into a finished product in a single uninterrupted strand.

The technology partnership with Italian equipment maker Danieli proved transformative. Danieli micro mill technology is a continuous casting and rolling process with a single uninterrupted billet strand from melting to finished product. Danieli micro mills are driven by Danieli Automation advanced 3Q process control systems, including full data analysis and reporting. Due to compact layout, energy savings and advanced process control system, it offers the best CapEx and OpEx.

MIDA-Micromill Danieli concept is a low-capacity steel plant for regional markets that, thanks to its innovative technological solutions, can compete in term of CapEx and OpEx with steel plants with much higher capacity.

Why does micro-mill technology matter? Consider the economics:

The "endless casting-rolling" process eliminates the need to reheat billets before rolling—a step that consumes significant energy in traditional mini-mills. By maintaining a continuous strand from molten steel to finished product, the micro-mill achieves substantial yield, energy cost, and productivity benefits compared to traditional rebar production methods.

Lower capital expenditure means faster payback periods and higher returns on investment. Lower operating expenditure means better margins throughout the cycle. And the smaller scale allows CMC to locate facilities closer to customer markets, reducing freight costs while improving service levels.

Commercial Metals Company (NYSE: CMC) and the State of Oklahoma today announced that CMC has selected Durant, Oklahoma, as the location for construction of its second technologically advanced micro mill. This new investment in Oklahoma will mirror CMC's existing micro mill in Mesa, Arizona and will be built with improved technology developed from CMC's operating experience with the world's first micro mill, which CMC successfully commissioned in Mesa in 2009. The addition of a second micro mill to CMC's portfolio of highly efficient, customer focused and cost effective steel production facilities will enhance CMC's position as a leading supplier of long products in the U.S. market.

The Oklahoma micro mill, utilizing Danieli technology and equipment, is expected to be commissioned in the fall of 2017 and to create approximately 300 jobs in the Durant area. The direct and indirect investment exceeded approximately $250 million—substantial, but far less than traditional mill construction.

"The location of the mill in Durant, Oklahoma, 80 miles north of Dallas, Texas, will allow us to better serve a growing North Texas market as well as expand into markets in Oklahoma, Kansas, Nebraska, Arkansas and Missouri."

The pattern continued with a third micro-mill. Supplied by Danieli, this MIDA QLP micro mill will be the first in the world capable of producing both steel rebar and merchant products with high yield strengths and maximum uptime.

On August 13, 2020, CMC announced plans to build its third micro mill, AZ2, adjacent to CMC Steel Arizona. The mill will be the first in the world to produce merchant bar quality (MBQ) products through a continuous-continuous production process. AZ2 will feature Danieli's "Q-One" technology which will allow CMC to have a direct connection between the EAF and Ladle Furnace to renewable energy sources. This technology reduces electricity transmission losses as compared to traditional methods and associated operating costs.

The Arizona 2 facility added another innovation: renewable energy integration. The Q-One technology allows direct connection to renewable energy sources, making it the first mill ready to operate in hybrid mode in North America. This positions CMC advantageously as construction customers increasingly demand low-carbon materials for LEED-certified and environmentally conscious projects.

Pioneer in endless rolling since 2009, the American steelmaker Commercial Metals Company (CMC) has awarded Danieli the order to supply a fourth Hybrid-ready, MIDA QLP plant for the production of 500,000 shtpy of various sizes of both straight length and spooled rebar. The selected location for CMC's new minimill is Berkeley County, West Virginia.

"CMC Steel West Virginia is a core component of CMC's strategic growth plan and will help ensure our long-term competitiveness in critical geographical markets. We believe this new micro mill, among the most environmentally friendly steelmaking operations in the world, will strengthen our operational network throughout the Eastern U.S. by achieving synergies with our existing mill and downstream facilities."

By 2023, CMC had established clear technological leadership in micro-mill production. CMC, a pioneer in endless casting-rolling, has been operating two Danieli MIDA micro mills, in Mesa (Arizona) and Durant (Oklahoma), USA. This is the 25th order received by Danieli for this unique, patented, endless casting rolling technology in operation worldwide.

The micro-mill bet exemplified CMC's approach to innovation: partner with world-class technology providers, be first to market with new processes, learn from operational experience, and incrementally improve each successive installation. The strategy created lasting cost advantages that competitors couldn't easily replicate without similar capital investment and learning curve traversal.

However, as we'll see, the close partnership with Danieli would become the center of serious antitrust allegations.

VI. The Gerdau Acquisition: Becoming the Rebar King (2018)

If the micro-mill innovation demonstrated CMC's technology prowess, the Gerdau acquisition showcased its M&A capabilities. This was the deal that transformed CMC from a significant player to the undisputed rebar king.

The transaction, which combined two of the three largest domestic rebar producers in the United States, was announced on January 2, 2018, and closed on November 5, 2018.

Commercial Metals Company (NYSE: CMC), today announced it has completed the acquisition of 33 rebar fabrication facilities in the United States, as well as steel mills located in Knoxville, Tennessee; Jacksonville, Florida; Sayreville, New Jersey and Rancho Cucamonga, California from Gerdau S.A. (NYSE: GGB), a producer of long and specialty steel products in the Americas for a cash purchase price of $600 million, subject to customary purchase price adjustments.

The acquisition includes 33 rebar fabrication facilities in the U.S., as well as steel mills located in Knoxville, Tenn.; Jacksonville, Fla; Sayreville, N.J.; and Rancho Cucamonga, Calif., with annual mill rolling capacity of 2.5 million tons.

After adding the incremental 2.7 million tons of melt capacity, CMC will have approximately 7.2 million tons of global melt capacity at the close of the transaction.

The strategic rationale was compelling. The four mills filled critical geographic gaps in CMC's network—the East Coast and California had been underserved by CMC's Texas-centric footprint. The 33 fabrication facilities created a nationwide presence that could serve construction customers wherever they built. And the scale economics of combining two of the three largest rebar producers promised meaningful synergies.

"I am thrilled to welcome the approximately 3,200 employees of these operations to Commercial Metals Company," said Barbara Smith, Chairman of the Board, President, and Chief Executive Officer of Commercial Metals. "The successful completion of the transaction represents an important step in our strategy to be the leading concrete reinforcing specialist as well as a significant provider of merchant and wire rod products. With our expanded geographic footprint and added operational flexibility, this transaction supports our vertically integrated steel making model and will leverage our existing rebar manufacturing technology and customer service core competencies."

CMC announced the acquisition in January 2018, and the transaction closed in November 2018 after the DOJ granted approval. The parties completed the $600 million transaction after regulatory review by the U.S. Department of Justice.

The regulatory scrutiny deserved close attention. When two of the three largest players in a market combine, antitrust authorities pay attention. CMC's successful navigation of DOJ review reflected careful deal structuring and, presumably, some asset divestitures to address competitive concerns. The fact that the deal closed demonstrated the regulators' view that sufficient competition would remain.

Excluding non-recurring integration related costs related to the four steel mills and rebar fabrication assets purchased from Gerdau S.A., that closed on November 5, 2018, the acquired assets contributed revenue of $453.5 million and operating income of $56.6 million to the consolidated results of CMC in the third quarter of fiscal 2019.

The rapid contribution from acquired assets validated the deal thesis. Integration proceeded smoothly, with CMC applying its operational playbook to optimize the acquired facilities. The acquisition was expected to be accretive to earnings and cash flow within the first year after the transaction closed. Once fully integrated, the combined operations were expected to generate approximately $40 million in pre-tax operational synergies annually.

Barbara R. Smith, Chairman of the Board, President and Chief Executive Officer, said, "The strong results for the quarter reflect the strength of construction activity, as well as solid industrial production levels and the resilient U.S. and Polish economies. Our recent acquisition, our greenfield Oklahoma facility, and introduction of hot spooled rebar were all meaningful contributors to top and bottom line financial results."

The Gerdau acquisition exemplified disciplined M&A. The price—$600 million plus working capital adjustment—was attractive relative to the capacity acquired. The assets fit CMC's existing business model. The integration leveraged proven operational capabilities. And the financing remained conservative, avoiding the over-leveraging that has destroyed value in so many acquisitions.

VII. The Barbara Smith Era & Strategic Diversification (2017–2023)

The Gerdau acquisition occurred under the leadership of Barbara Smith, whose tenure marked a new chapter in CMC's evolution from regional operator to diversified construction solutions provider.

Barbara Smith, who started with CMC in 2011 as SVP & CFO, is appointed CMC president and chief executive officer on September 1, 2017.

Smith served as CMC's President and Chief Operating Officer ("COO") from January 2017 to September 2017, COO from January 2016 to January 2017, and Senior Vice President and Chief Financial Officer from May 2011 to January 2016.

Prior to joining CMC, Ms. Smith served as Vice President and Chief Financial Officer of Gerdau Ameristeel Corporation, a mini mill steel producer, from July 2007 to May 2011, after joining Gerdau Ameristeel as Treasurer in July 2006. From February 2005 to July 2006, she served as Senior Vice President and Chief Financial Officer of FARO Technologies, Inc., a developer and manufacturer of 3-D measurement and imaging systems. From 1981 to 2005, Ms. Smith was employed by Alcoa Inc., a producer of primary aluminum, fabricated aluminum and alumina, where she held a variety of financial leadership positions.

Smith's background is notable: she came to CMC from Gerdau Ameristeel, the very company whose assets CMC would later acquire. Her deep understanding of both organizations undoubtedly facilitated the smooth integration. Her Alcoa experience provided perspective on running large-scale metals operations. And her financial background—she's a CPA—informed disciplined capital allocation.

Barbara led CMC through a period of unprecedented transformation, growth and innovation. The Board is looking forward to continuing this strong trajectory under the leadership of Peter Matt, who is a strategic thinker, strong collaborator and proven leader.

Under Smith's leadership, CMC expanded beyond its steel roots with the transformative Tensar acquisition.

Commercial Metals Company (NYSE: CMC) ("CMC") today announced that it has successfully completed the acquisition of TAC Acquisition Corp. ("Tensar") from Castle Harlan, a New York-based private equity firm, for a cash purchase price of $550 million, subject to customary purchase price adjustments. Tensar is a leading global provider of innovative ground stabilization and soil reinforcement solutions, selling into more than 80 national markets through its two major product lines: Tensar® geogrids and Geopier® foundation systems.

Geogrids are polymer-based products used for ground stabilization, soil reinforcement, and asphalt optimization in construction applications including roadways, public infrastructure, and industrial facilities. Geopier systems are ground improvement solutions that increase the load-bearing characteristics of ground structures and working surfaces.

"I am thrilled to welcome Tensar's 650 worldwide employees to Commercial Metals," said Barbara Smith, Chairman of the Board, President, and Chief Executive Officer. "This acquisition marks another important milestone in CMC's growth strategy, expanding the scope of products and services we can provide to our customers."

The $550 million purchase price for Tensar is equal to 9.2x the company's 2021 EBITDA of $60 million. Including $5 million of cost synergies estimated by CMC, the EBITDA multiple drops to 8.5x. Over the past five years, Tensar's average EBITDA margin is just over 25%.

The Tensar acquisition represented strategic expansion of CMC's total addressable market. While rebar remains the core business, Tensar positions CMC to participate in the broader infrastructure story—every road, bridge, and building foundation benefits from ground stabilization solutions. The cross-selling opportunity is significant: CMC's fabrication relationships provide access to the same contractors who specify geogrids and foundation systems.

"I'm enthusiastic about the opportunity for Tensar to join with CMC for expanded reach in the civil infrastructure market," said Mike Lawrence, CEO of Tensar. "Both companies have a rich history of innovation, service and commitment to our customers' success. Together we will be well-positioned to grow into key markets, leveraging forthcoming infrastructure spending as well as growing requirements for more sustainable solutions globally."

The branding evolution reflected CMC's expanding scope. In October 2023, they launched an updated logo designed to express CMC's growth and strength as a company, capturing the core purpose of CMC's diverse construction products and solutions. The new logo and updated branding also reflects their growth strategy to expand the scope of products and solutions beyond metals.

Recent acquisitions of Tendon Systems LLC, Tensar, and EDSCO Fasteners LLC are "critical examples of CMC's move beyond its roots in steel production to new opportunities across the construction industry."

Retiring CEO Smith capped off a strong year in 2022 as one of ten Entrepreneur Of The Year National Award winners last November. Smith also was highlighted in the "first-ever" Women CEOs in America Report, released in 2020 by C200, Catalyst, and the Women Business Collaborative, further exemplifying her impact and influence as a female CEO.

VIII. Infrastructure Tailwinds & The Current Era (2023–Present)

Barbara R. Smith, the Company's Chief Executive Officer and Chairman, has chosen to retire as Chief Executive Officer and has been appointed Executive Chairman of the Board, effective September 1, 2023. The board unanimously voted to appoint Peter R. Matt, the Company's President, to the role of Chief Executive Officer and President of the Company effective September 1, 2023. Mr. Matt will also continue as a member of the Company's Board of Directors, which he joined in June 2020.

Mr. Matt is a seasoned global business leader with significant experience across a range of industrial companies including metals and metals-related industries.

Prior to his appointment as President of the company on April 9, 2023, Matt served as the Executive Vice President and Chief Financial Officer of Constellium SE, a leading global aluminum fabrication company, from January 2017 to April 2023. Before joining Constellium, Matt worked as a Managing Partner for Tumpline Capital, LLC from 2015 to 2016. Notably, he held various leadership positions with Credit Suisse from 1985 to 2015.

Matt's appointment represents continuity with evolution. His metals industry experience (at Constellium) provides operational context, while his investment banking background (Credit Suisse) brings capital markets sophistication. The smooth succession planning—Matt joined the board in 2020, became President in April 2023, and CEO in September 2023—reflects the deliberate approach that has characterized CMC leadership transitions.

The macro environment presents significant opportunity. Analysts at UBS have initiated coverage on Commercial Metals Company (NYSE:CMC) with a 'Buy' rating on their belief that the steel and reinforcing bar (rebar) producer is well positioned to benefit from infrastructure investment growth. "Infrastructure projects will have a material impact on rebar consumption on the back of US$550 billion in new Federal investment from the Infrastructure Investment and Jobs Act (IIJA) in 2021 and about US$800 billion from the Inflation Reduction Act (IRA) and CHIPS in 2022."

They forecast 2 to 2.5 million tons per annum of US rebar consumption growth by 2026, representing a more than 20% potential upside for rebar and a 7% potential upside for long steel. They estimated that up to 2.5 million tons per annum of demand growth would come from 1.5 million tons per annum IIJA spending on highways and transportation, 0.5 million tons per annum from accelerating wind turbine installments and other clean energy benefits.

The company estimates that federal funding through the Infrastructure Law and other legislation will increase by 65% compared to funds through the Fixing America's Surface Transportation Act, a law that allocates long-term funds toward surface transportation infrastructure planning and investment. Smith said those funds would also create 1.5 million tons of incremental rebar demand.

"All of these facilities include multiple phases, are massive in size and consume large amounts of rebar," Smith said on the call. "They also require extreme structural rigidity and extensive site logistics development."

CMC has continued its acquisition momentum under new leadership. Commercial Metals Company (NYSE: CMC) ("CMC") today announced it has entered into a definitive agreement to acquire Foley Products Company ("Foley"), the largest regional supplier of precast concrete solutions in the United States and leader within the Southeastern U.S., for a cash purchase price of $1.84 billion, subject to customary purchase price adjustments.

The purchase price represents a multiple of 10.3x Foley's forecasted 2025 EBITDA.

The latest move for CMC comes on the heels of the company's September 2025 acquisition of Virginia-based Concrete Pipe & Precast for $675 million.

Enhances CMC's business with combined precast platform that will transform financial profile: The proposed acquisitions of Foley and CP&P, creating one of the largest precast businesses in the U.S., will add a complementary new earnings driver that substantially enhances CMC's financial profile, increasing our core EBITDA margin by 210 basis points on a pro forma basis, and driving meaningful improvement in our free cash flow. Following the completion of the transactions, approximately 32% of CMC's total pro forma segment adjusted EBITDA will be generated by the Emerging Businesses Group and the precast platform, representing a significant increase from the 15% contributed by the Emerging Businesses Group in FY 2025.

With a 17% share of the U.S. concrete market that continues to grow, precast is a strong strategic fit for CMC, and its success will be supported by leveraging existing leadership positions in early-stage construction and deep knowledge of customers, market applications, and geographies. Following the proposed acquisitions of Foley and CP&P, CMC will operate 35 facilities across 14 states, creating the #3 precast platform in the United States and a leader in the Mid-Atlantic and Southeast.

Recent financial performance shows the company navigating cyclical headwinds. Net earnings were $103.9 million, or $0.90 per diluted share, on net sales of $2.0 billion, compared to prior year period net earnings of $184.2 million, or $1.56 per diluted share, on net sales of $2.2 billion. For the full year fiscal 2024, CMC reported net earnings of $485.5 million, or $4.14 per diluted share, on net sales of $7.9 billion compared to prior year net earnings of $859.8 million, or $7.25 per diluted share, on net sales of $8.8 billion.

The Company's balance sheet and liquidity position remained strong. As of August 31, 2024, cash and cash equivalents totaled $857.9 million, with available liquidity of nearly $1.7 billion.

The strategic initiative called "Transform, Advance, Grow" (TAG) aims to enhance operational excellence. Matt added, "During 2024, we made significant progress on the development of a key component of our long-term strategic plan – Transform, Advance, Grow (TAG), an enterprise wide operational and commercial excellence initiative – which we expect will support substantial value creation in the years ahead. The improvement program, which seeks to leverage our leading positions in most of our core markets, touches nearly every aspect of our business and aims to achieve higher through-the-cycle margins by lowering costs, increasing efficiency, and better capturing commercial opportunities across our business. We believe the execution of several early initiatives will begin yielding financial benefits in fiscal 2025."

IX. The Pacific Steel Antitrust Lawsuit: A Cautionary Tale (2024)

Every business story has shadows, and CMC's involves a significant legal setback that reveals the risks inherent in market leadership positions.

On November 5, 2024, after two-week jury trial, a federal jury issued a $110 million verdict against Commercial Metals Company, a multi-national steel conglomerate and the nation's largest manufacturer and fabricator of steel rebar, for conspiring to block the entry of Pacific Steel Group from entering the Southern California rebar market. The lawsuit, brought on behalf of Pacific Steel Group, a steel rebar fabricator located in San Diego, California, sought damages and injunctive relief against Commercial Metals Company for violations of federal and state antitrust laws.

Pacific Steel Group (PSG) was founded in 2014 as a fabricator and installer of rebar in California. On October 30, 2020, PSG filed an antitrust lawsuit against Commercial Metals Company (CMC), a multi-national steel conglomerate and the nation's largest manufacturer and fabricator of steel rebar, in Northern California federal court.

In 2020, PSG filed a complaint against Commercial Metals Co (CMC) and Danieli Corp in US District court in California, where PSG alleged that CMC attempted to monopolize the California rebar market. PSG accused CMC of suppressing competition by pushing Danieli Corporation, a maker of rebar micro-mills, into an exclusivity contract for the next three years, effectively barring Danieli Corp from developing any rival mills within a 500-mile radius from CMC's now-defunct Rancho Cucamonga California mill.

The complaint further alleged that when CMC learned of PSG's plans, it had been planning to build a new Danieli micro mill in Mesa, Arizona, and secured Danieli's agreement not to build another micro mill for any CMC competitor within a 500-mile radius of Rancho Cucamonga, California for 69 months. This agreement effectively blocked PSG and other potential competitors from manufacturing rebar for years.

On November 5, jurors found that PSG had proven "by a preponderance of the evidence" that there is a relevant steel rebar market 500 miles around the mill, and that CMC's exclusivity contract with Danieli was an unreasonable restraint of trade in that market. Jurors concluded that CMC made a move to monopolize the market, and that its subsequent conduct harmed PSG, who acquired land north of Los Angeles for developing a new, technologically cutting-edge micro mill.

In light of CMC's purported misconduct, jurors awarded PSG $74 million in lost profits from its mill operations; $12.9 million in lost rebar transportation savings; $10.8 million in lost fabrication cost savings and $12.28 million in increased costs to purchase the mill due to inflation, according to the verdict form. This verdict brings PSG's total damages award to $110 million, which is the full amount PSG's counsel had sought during trial closings.

A trial on Pacific Steel's claims began on October 21st and concluded today with a verdict in favor of Pacific Steel in the amount of $110 million, which will be trebled as a matter of law, plus attorneys' fees. We are very disappointed by the outcome, and plan to appeal the verdict. CMC stands by the strong integrity of its business practices and will vigorously defend its position.

A unanimous nine-member jury handed down the verdict in favor of San Diego-based steel fabricator PSG after less than 3 hours of jury deliberations in the high-stakes jury trial that began Oct. 22 in Oakland, California, according to court documents. During trial, PSG accused Texas-based CMC of suppressing competition by pushing micromill-maker Danieli Corp. into a three-year exclusivity contract barring Danieli from developing most rival mills within 500 miles around CMC's since-shuttered Rancho Cucamonga, California mill.

The financial impact is substantial. First quarter net loss was ($175.7) million, or ($1.54) per diluted share, on net sales of $1.9 billion, compared to prior year period net earnings of $176.3 million, or $1.49 per diluted share, on net sales of $2.0 billion. This reflected the litigation expense charge related to the verdict.

The case raises important questions about competitive behavior in concentrated markets. CMC's micro-mill technology partnership with Danieli was a legitimate business relationship that created real competitive advantages. But when that relationship allegedly included provisions preventing Danieli from serving competitors, it crossed into potentially anticompetitive territory.

The lesson for investors: market leadership brings regulatory and legal scrutiny. Companies that dominate their niches must be vigilant about the line between aggressive competition and antitrust violation. CMC's appeal may succeed, but the verdict underscores the risks inherent in concentrated market positions.

X. Playbook: Business & Investing Lessons

CMC's 110-year journey offers several enduring lessons for business leaders and investors:

1. Vertical Integration as Competitive Advantage From Moses Feldman's first scrap yard to today's integrated operation, CMC demonstrates how controlling the value chain creates defensible positions. CMC's recycling facilities and use of scrap as the primary feedstock for our mills, recycling 13.6 billion pounds of metal each year. CMC operates six electric arc furnace (EAF) minimills, two EAF micromills and one rerolling mill strategically located throughout the United States. The scrap taken in at our recycling facilities is processed and used as the primary source of ferrous material for our steel mills. In total, CMC has the capacity to produce more than five million tons of finished long steel products, including rebar (both traditional and threaded), t-post stock for fence posts and merchant bar products (including angles, channels, flats, squares and rounds), in addition to wire rod and semi-finished billets. Drawing on both their strategic locations and CMC's extensive logistics network, customers can rely on CMC to deliver their steel quickly and efficiently wherever they need it, when they need it.

2. Regional Density vs. National Spread CMC's strategy has consistently emphasized being dominant in specific regions rather than spreading thin nationally. The Gerdau acquisition filled geographic gaps; it didn't create scattered outposts. This density creates logistics advantages, customer intimacy, and operating leverage.

3. Technology Bets Being first-mover on micro-mill technology created lasting cost advantages. CMC was the first in the world to successfully operate a micro mill – and now we have two. These plants have smaller footprints and are just the right size for their markets. The key was partnering with world-class technology providers (Danieli) while maintaining operational ownership of the learning curve.

4. Disciplined M&A The Gerdau acquisition doubled capacity at attractive valuations. The Tensar acquisition expanded TAM without losing focus. Recent precast acquisitions build new growth platforms. Each deal fit the strategic framework, was priced reasonably, and was integrated effectively.

5. Platform Expansion The Tensar and precast acquisitions show how to expand addressable market without losing strategic coherence. All serve construction customers, leverage existing relationships, and create cross-selling opportunities.

6. Sustainability as Strategy CMC's recycling roots and EAF technology position it well for increasing ESG scrutiny. Since our first heat of steel in 1962, we have manufactured steel using recycled scrap metal and Electric Arc Furnace (EAF) technology, which is far more efficient and environmentally friendly than traditional blast furnace technology, using 82% less energy than the industry average and producing 63% less CO2 per ton of steel we melt.

7. Leadership Succession CMC has navigated multiple leadership transitions—from family to professional management, from one professional CEO to another—without disruption. The deliberate succession planning deserves emulation.

XI. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

| Force | Assessment | CMC's Position |

|---|---|---|

| Threat of New Entrants | LOW | High capital requirements create significant barriers. Direct and indirect investment for a micro-mill exceeds approximately $250 million. Technical expertise, regional logistics networks, and customer relationships take years to develop. CMC's scale and vertical integration make entry difficult. |

| Supplier Power | LOW-MODERATE | CMC controls its own scrap supply through recycling operations. The scrap taken in at our recycling facilities is processed and used as the primary source of ferrous material for our steel mills. This reduces dependency on external suppliers. |

| Buyer Power | MODERATE | Construction contractors have some leverage, but CMC's fabrication capabilities and regional presence create switching costs. The fragmented buyer base limits any single customer's power. |

| Threat of Substitutes | LOW | Steel rebar has no viable substitute for concrete reinforcement in major construction. Wood, composite materials, and fiber-reinforced polymers have limited applications for structural purposes. |

| Competitive Rivalry | MODERATE-HIGH | Along with Nucor, it is one of two primary suppliers of steel used to reinforce concrete in buildings, bridges, roads, and infrastructure in the U.S. The duopoly dynamics in rebar create rational competition, but imports and regional players add competitive pressure. |

Hamilton's 7 Powers

| Power | Assessment | Evidence |

|---|---|---|

| Scale Economies | STRONG | After adding the incremental 2.7 million tons of melt capacity, CMC will have approximately 7.2 million tons of global melt capacity. Unit costs decline with volume across mills and fabrication. |

| Network Economies | MODERATE | Our rebar fabrication business has more than 60 years of industry leadership. With more than 60 state-of-the-art fabrication facilities located all across the United States, CMC offers everything from rebar, rebar accessories, fence posts, wire mesh and more. Our fabricating facilities have a total of nearly 2.5 million tons of fabricating capacity annually. This creates network effects for customer service and logistics. |

| Counter-Positioning | STRONG | Micro-mill technology allows CMC to serve regional markets more efficiently than traditional integrated mills. Incumbents can't easily replicate without cannibalizing existing operations. |

| Switching Costs | MODERATE | Fabrication relationships, technical specifications, and reliability create customer stickiness. Construction contractors value consistent quality and on-time delivery—changing suppliers introduces project risk. |

| Branding | WEAK | This is a commodity business with limited brand differentiation. Customers care about price, quality, and delivery—not brand image. |

| Cornered Resource | MODERATE | CMC's early partnership with Danieli provided technology advantages—it was first to operate micro-mills globally. However, as the Pacific Steel case showed, exclusivity agreements carry legal risk. |

| Process Power | STRONG | MIDA-Micromill Danieli concept is a low-capacity steel plant for regional markets that, thanks to its innovative technological solutions, can compete in term of CapEx and OpEx with steel plants with much higher capacity. Operational excellence in mini-mill and micro-mill production creates sustainable cost advantages. |

Key Strategic Takeaways

CMC's competitive moat is built on Scale Economies + Process Power + Counter-Positioning. The vertical integration model amplifies these advantages by capturing margin at multiple points in the value chain while reducing vulnerability to external parties.

The Tensar and precast acquisitions add Network Economies potential through cross-selling construction solutions to existing customer relationships.

The primary vulnerability remains regulatory and antitrust risk inherent in market leadership. The Pacific Steel verdict demonstrates that aggressive competitive behavior can cross legal lines, with substantial financial consequences.

Key Performance Indicators to Monitor

For investors tracking CMC's ongoing performance, three KPIs merit particular attention:

-

Metal Margin per Ton (Steel Segment): The spread between selling prices and raw material costs drives profitability more than volume. Watch for compression during industry downturns or expansion during strong markets.

-

Downstream Backlog (Fabrication): This leading indicator reveals future revenue visibility. Stable or growing backlog suggests healthy construction activity; declining backlog signals potential volume weakness ahead.

-

Core EBITDA Margin: This encompasses both steel and emerging businesses, capturing the company's ability to maintain profitability through cycles. The TAG initiative targets improvement here; watch for execution.

XII. Looking Forward: Bull Case, Bear Case, and Key Questions

The Bull Case

CMC is positioned at the intersection of several powerful secular trends. The Infrastructure Investment and Jobs Act (IIJA) which was signed into law in November 2021 is still in action. Considering the fact that significant funding to the asphalt and road paving industry comes from the US government, the beneficiaries in this scenario are construction materials companies. Three years into the 5-year $1.2 trillion act, only 40% of funds from the infrastructure law have been allocated to projects. White House data analyzed by CNBC unveiled that the biggest chunk of IIJA money was flowing to road and bridge construction.

The West Virginia micro-mill, when operational, will serve East Coast markets currently dependent on imports or distant mills. The precast acquisitions diversify earnings into higher-margin, less cyclical businesses. And the TAG initiative promises operational improvement through the cycle.

Nucor is the U.S. market leader in merchant bar and rebar products. CMC's position as the #2 player in a rational duopoly suggests pricing discipline will persist.

The Bear Case

Cyclicality remains inherent in construction materials. Interest rate sensitivity affects both residential and commercial construction. The Pacific Steel verdict—potentially $330 million plus attorney fees—represents a material charge that could recur if the appeal fails and other competitors pursue similar claims.

First quarter net loss was ($175.7) million, or ($1.54) per diluted share—the litigation charge demonstrates how legal risk can dominate quarterly results.

Additionally, the precast acquisitions (totaling approximately $2.5 billion for Foley and CP&P combined) add leverage at a time of economic uncertainty. Integration risk exists with any acquisition of this scale.

Key Questions for Investors

-

Pacific Steel Appeal: Will CMC prevail on appeal, or will the $330+ million judgment stand? Precedent implications could invite additional litigation.

-

West Virginia Timing: The micro-mill was initially expected in late 2025 but now targets spring 2026. Further delays would postpone capacity and earnings contribution.

-

Precast Integration: Can CMC execute on $25-30 million in synergies while maintaining Foley's industry-leading margins?

-

Cycle Position: With construction activity showing mixed signals, is CMC expanding at the top of a cycle or positioning for long-term structural growth?

Conclusion: The Hidden Backbone of American Infrastructure

The next time you drive across a bridge, enter a building, or walk into a stadium, consider what holds everything together. Hidden within the concrete—invisible but essential—is steel rebar, and there's a good chance it came from Commercial Metals Company.

From Moses Feldman's Dallas scrap yard in 1915 to today's Fortune 500 enterprise with operations spanning continents, CMC exemplifies the patient building of competitive advantage through vertical integration, technology leadership, and disciplined execution. The story encompasses immigrant ambition, family succession, professional management, transformative acquisitions, and yes, legal setbacks that remind us that market dominance brings both rewards and responsibilities.

From a single scrap yard in Dallas, Texas, CMC has grown into a Fortune 500 company with hundreds of facilities and more than 10,000 employees serving our valued customers around the world.

For long-term investors, CMC offers exposure to American infrastructure development through a company with demonstrated ability to compound value over decades. The micro-mill technology advantage, vertical integration model, and expanding construction solutions portfolio create multiple avenues for growth. The balance sheet remains conservative. The dividend has been paid for 55 consecutive years.

But this is no sleepy utility. The antitrust verdict reminds us that CMC operates in a concentrated industry where competitive tactics receive regulatory scrutiny. The cyclicality of construction markets means earnings will fluctuate. And execution risk exists with any company pursuing billion-dollar acquisitions.

What distinguishes CMC is a culture—traceable to those early Feldman family values—that prioritizes long-term positioning over short-term maximization. In an era of quarterly thinking, CMC thinks in decades. In an industry of commodity pricing pressure, CMC builds structural cost advantages. In a market of generalist industrial companies, CMC maintains laser focus on early-stage construction.

The story continues. Infrastructure bills provide tailwinds. Precast acquisitions diversify the earnings base. Micro-mills advance toward completion. And somewhere in Texas, scrap metal continues its transformation into the hidden backbone of American infrastructure—much as it has for more than a century.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube