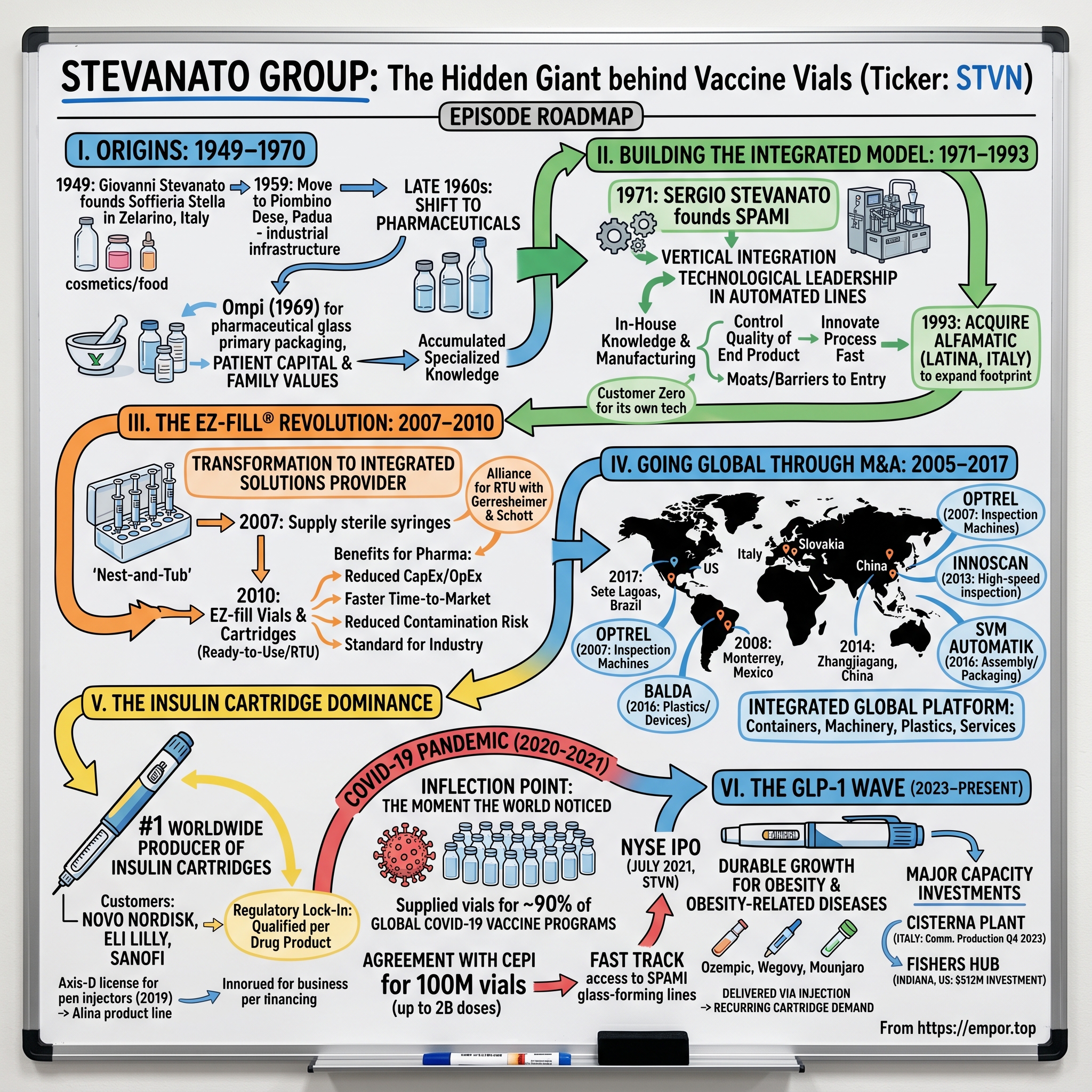

Stevanato Group: The Hidden Giant Behind Every Vaccine Vial

I. Introduction & Episode Roadmap

Somewhere in the misty industrial sprawl between Venice and Padua, a factory churns out a product so mundane that most people have never given it a second thought. Glass vials. Syringes. Cartridges. The humble containers that hold the medicines keeping billions of people alive.

Yet inside that factory in Piombino Dese, Italy, sits one of the most strategically important companies in global healthcare—one that supplied vials to approximately 90% of COVID-19 vaccine programs worldwide, making it indispensable to the largest vaccination campaign in human history.

The company reported net sales of €1,104 million for fiscal year 2024, a figure that barely hints at the company's outsized influence. When the world scrambled for vaccines in 2020, Stevanato Group emerged as the quiet backbone of the global response. Stevanato Group and CEPI signed an agreement for the supply of 100 million Type 1 Borosilicate glass vials to hold up to 2 billion doses of a vaccine against the COVID-19 virus.

This is the story of how a family-owned Italian glassblower transformed itself over seven decades into an indispensable partner to 41 of the top 50 pharmaceutical companies globally. It's a masterclass in vertical integration, patient capital, and the strategic patience that only family ownership can provide. The company has secured a reputation for reliability, positioning itself as a partner to over 700 clients worldwide, including 41 of the top 50 pharmaceutical companies and 15 of the top 20 biotechnology companies.

The themes of this deep dive will be familiar to students of durable competitive advantage: vertical integration so deep it creates moats, switching costs so high they become regulatory barriers, and a business model that positions the company at the intersection of every major healthcare megatrend—from GLP-1 obesity drugs to mRNA vaccines to the biologics revolution.

In the third quarter of 2025, revenue increased 9% to €303.2 million, with high-value solutions representing a record 49% of total revenue—a testament to the company's ongoing transformation from commodity glass supplier to integrated solutions provider.

The question isn't whether Stevanato matters. It's whether the market fully appreciates the durability of its competitive position and the magnitude of the secular tailwinds at its back.

II. Origins: From Venetian Glassblowing to Pharmaceutical Pioneer (1949–1970)

Picture post-war Italy in 1949. The country lay in ruins, yet the ancient tradition of Venetian glassmaking persisted. In Zelarino, a small town near Venice, a craftsman named Giovanni Stevanato opened a modest operation called "Soffieria Stella"—literally "Star Glassblowing."

Stevanato Group was founded in 1949 by Giovanni Stevanato as Soffieria Stella, a glass bottle manufacturer based in Zelarino near Venice, Italy. The company's early focus was pedestrian: glass bottles for the cosmetic and food industries. Giovanni developed machinery capable of automating glass production—a hint of the engineering DNA that would later define the company.

Initially operating in the post-World War II economic recovery period, the company capitalized on Italy's longstanding tradition of glass craftsmanship to meet demand for everyday packaging solutions. The Veneto region had been home to glassmakers for centuries, with Murano's artisans world-famous for their craft. But Giovanni Stevanato wasn't making chandeliers—he was industrializing glass production for commercial applications.

In 1959 the company moved to its current location: Piombino Dese, Padua – Italy. This relocation proved pivotal. The move to Piombino Dese in the Padua province gave access to better industrial infrastructure and proximity to raw materials, marking an early step toward operational efficiency.

The real strategic inflection came in the late 1960s. By the late 1960s, the Stevanato family recognized the growing potential in the pharmaceutical sector, leading to the establishment of Ompi in 1969 in Piombino Dese. Ompi represented a pivotal transition, redirecting the group's expertise toward the manufacture of glass primary packaging specifically designed for pharmaceuticals.

Why pharmaceuticals? The answer lies in margin and moat. Cosmetic bottles were commodity products—any glassmaker could produce them. But pharmaceutical containers required specialized glass formulations, tighter tolerances, and regulatory approvals that took years to obtain. Giovanni Stevanato saw a market where quality commanded pricing power and switching costs created customer stickiness.

Giovanni's vision and values became the compass guiding the company through decades of growth and transformation. Giovanni always believed in the power of innovation and the importance of investing in people and emerging technologies. This dedication to quality and precision laid the foundation for the creation of Ompi in 1969.

By 1969, Stevanato had evolved from a generic glassmaker into a focused pharmaceutical packaging company. The decision to concentrate on a single vertical—drug containment—would prove transformational. It allowed the company to accumulate specialized knowledge, develop proprietary processes, and build regulatory relationships that competitors would struggle to replicate.

The Venetian glass tradition provided more than just technical heritage. It instilled a culture of craftsmanship and patient, generational thinking. Northern Italy's ecosystem of precision manufacturers—from automotive components to medical devices—created a supplier network and talent pool that would support Stevanato's growth for decades to come.

For investors, the origin story reveals two critical elements: the family's willingness to make concentrated bets on high-quality market segments, and the early recognition that vertical integration into machinery would become the company's defining advantage.

III. Building the Integrated Model: The SPAMI Masterstroke (1971–1993)

The year was 1971, and Sergio Stevanato—Giovanni's son, who had taken leadership of the company after graduating from law school at the University of Ferrara in 1969—made a decision that would fundamentally reshape the company's competitive position.

A second company (SPAMI) was established in 1971, specialized in the design and construction of high-speed precision machines and complete lines for the production and control of glass tube containers for pharmaceutical use.

This was a masterstroke of strategic thinking. Most pharmaceutical glass manufacturers purchased their production equipment from third-party suppliers. Stevanato chose to build its own.

The most important milestone for the company took place in 1971 when the Stevanato family founded Spami. Spami would manufacture the glass-forming technology that allows Stevanato to manufacture its high-quality containers even today.

The logic was elegant. If you build your own machines, you control the quality of your end product. You can innovate on process technology faster than competitors who must wait for equipment suppliers. You create barriers to entry because competitors cannot simply buy the same machines. And you generate an additional profit stream by selling equipment to other glass converters.

Glass converting is the first step in the value chain. It's the technology that allows Stevanato (and its customers) to transform glass into vials, ampoules, cartridges, etc. The company has been doing this since 1971, and it constitutes one of its primary advantages as other companies don't own their technology.

This vertical integration philosophy ran deep. Stevanato Group produces fully automated, high-speed, precision glass forming lines through its brand Spami. The equipment provides the most accurate processing of ampoules, vials, cartridges and syringes found in the industry.

Spami's main strengths are its technological leadership in automated lines, combined with its in-house knowledge and manufacturing capabilities. Because it is part of the wider Stevanato Group, Spami not only supplies automated lines, it has also gained in-depth understanding of the pharmaceutical glass primary packaging market.

The company became what strategists call "customer zero" for its own technology. Every improvement in glass-forming equipment could be tested and refined on Stevanato's own production lines before being offered to external customers. This created a virtuous cycle of innovation and competitive intelligence—Stevanato understood what glass converters needed because it was the world's most sophisticated glass converter itself.

In 1993 Stevanato Group purchased Alfamatic (Latina, Italy). This acquisition expanded the company's Italian footprint and added manufacturing capacity in the Lazio pharmaceutical district south of Rome.

Franco Stevanato, Sergio's son and the current CEO, would later reflect on these formative years. Franco tells the story of how he used to attend his grandfather's factory on Saturday mornings as a child: "I was always very excited for this. I remember I used to visit the production floor and then go to the engineering department where we used to develop a new idea for the glass forming technology. These were the two things he used to love the most."

The image is striking: three generations gathered on the factory floor, discussing glass-forming innovations. This wasn't just nostalgia—it was the transmission of institutional knowledge that would become impossible for competitors to replicate.

Spami is the number one choice when it comes to forming lines. The company not only has 50 years of experience, but also draws on 70+ years of experience in pharmaceutical glass primary packaging and a wide range of related capabilities within Stevanato Group.

For investors, the SPAMI strategy reveals the depth of Stevanato's moat. This isn't a company that can be easily disrupted by a well-funded competitor. The integration of engineering and manufacturing creates compounding advantages that strengthen with each decade of accumulated learning.

IV. Inflection Point #1: The Ready-to-Use Revolution – EZ-fill® (2007–2010)

The year 2007 marked the beginning of what would become Stevanato's defining innovation—a product platform that transformed the company from a component supplier into an integrated solutions provider.

The company started supplying sterile syringes (EZ-fill Syringes) in 2007 and then it extended the ready-to-fill concept to vials and cartridges in 2010 (EZ-fill Vials & Cartridges).

To understand why EZ-fill® matters, you need to understand the traditional pharmaceutical manufacturing process. When a drug company receives bulk glass vials from a supplier, it must wash them, sterilize them, siliconize them (to allow smooth drug extraction), and depyrogenate them (to remove bacterial endotoxins) before filling them with medicine. Each step requires specialized equipment, cleanroom space, trained personnel, and regulatory validation.

Stevanato's insight was that pharmaceutical companies didn't want to be in the glass-processing business. They wanted to focus on what they did best: developing and manufacturing drugs. An easy, flexible and streamlined production process means pharmaceutical and biotech companies can immediately fill our EZ-fill® pre-sterilized vials containment solution, as well as cartridges and syringes systems, consistently shortening time to market. It's the perfect solution for both clinical trials and during the industrialization phase.

The EZ-fill® platform delivered glass containers that arrived at customer facilities ready to fill—washed, sterilized, and packaged in nest-and-tub configurations that eliminated glass-to-glass contact during transport. Stevanato Group EZ-fill® Vials are offered in pre-sterilized RTU nest & tub and tray configurations eliminating glass-to-glass contact to assure pristine cosmetic quality. The pre-sterilized formats are designed for direct entry into aseptic fill operations.

The economics were compelling. Traditional fill & finish processes present several operational risks and require increased efficiency. By adopting an industrial ready-to-use (RTU) setup, pharmaceutical companies and Contract Manufacturing Organizations (CMOs) can benefit from reduced operational risks, enhanced flexibility and efficiency, and lower waste. RTU technology can help streamline processes, increase productivity, and thus lower total cost of ownership (TCO) while reducing contamination risks.

For pharmaceutical companies, EZ-fill® meant: - Reduced capital expenditure: No need to build washing and sterilization lines - Lower operating costs: Fewer personnel, less energy, reduced quality control burden - Faster time-to-market: Especially critical for clinical trials where speed matters - Reduced contamination risk: Stevanato's industrial-scale processes produced more consistent results than in-house operations

When it comes to RTU containment solutions for biopharmaceutical products, no solution matches EZ-fill® platform, whose proven advantages have turned its processing technology into an industry standard. Over the last years, more than 300 lines have been installed using EZ-fill® packaging technology.

The EZ-fill® platform exemplified Stevanato's broader strategy: take non-core activities away from pharmaceutical customers and perform them at industrial scale with superior quality. This approach deepened customer relationships, increased revenue per unit, and created switching costs that extended far beyond simple product preferences.

The new EZ-fill Smart™ is an evolution of Stevanato Group's groundbreaking EZ-fill® platform, and it brings new advancements that can create significant enhancements to customer product offerings amid growing demand for RTU vials.

By 2022, Stevanato had partnered with competitor Gerresheimer to launch EZ-fill Smart™, an enhanced version of the platform. The EZ-fill Smart™ platform leverages increased automation throughout the manufacturing process to increase productivity and reduce human errors. The optimized platform features no glass-to-glass and no glass-to-metal contact, which improves quality and integrity of the vials throughout the product life cycle.

The willingness to partner with a competitor on EZ-fill Smart™ reveals strategic sophistication. Rather than competing on proprietary platform standards, Stevanato recognized that industry-wide RTU adoption would grow the total addressable market. Better to have a larger share of a much bigger pie.

For investors, EZ-fill® demonstrates Stevanato's ability to identify value migration opportunities and capture them before competitors. The platform transformed commodity glass containers into high-margin integrated solutions—exactly the kind of product evolution that creates durable competitive advantage.

V. Inflection Point #2: Going Global Through M&A (2005–2017)

The early 2000s found Stevanato at a strategic crossroads. The company had built formidable capabilities in glass manufacturing and machinery design, but its footprint remained largely European. Major pharmaceutical customers were globalizing their supply chains, establishing manufacturing facilities in emerging markets. Stevanato needed to follow.

With the acquisition of Medical Glass (Bratislava) in 2005, the Group opened to the internationalization.

Medical Glass was based in Slovakia, and its manufacturing plant is still in operation. The latter was quite relevant because it marked Stevanato's first foray into international markets.

Slovakia offered several advantages: lower labor costs than Italy, proximity to growing Eastern European pharmaceutical markets, and access to EU regulatory frameworks. The acquisition signaled Stevanato's intent to compete globally.

The next major move came in Mexico. In 2008 a new production plant called "Ompi of America" was built in Monterrey, Mexico. The rationale was clear: several large US pharmaceutical companies had moved manufacturing operations to northern Mexico, and Stevanato wanted supply contracts with these customers.

The Mexico plant was built in 2008 and doubled in 2012 in order to serve the American market. The expansion demonstrated both growing demand and Stevanato's confidence in its North American strategy.

China came next. In 2014, Stevanato officially inaugurated a new production plant in Zhangjiagang, China. The construction of the new production plant, for which Stevanato already invested 27 million Euro, represented an important step in the growth and internationalisation strategy that the Group pursued for several years.

Stevanato Group is currently the world's leading manufacturer of cartridges for insulin used in diabetes treatment. China represented both a manufacturing base and a massive end market—the country's diabetic population exceeded 100 million, creating enormous demand for insulin cartridges.

Alongside geographic expansion, Stevanato assembled capabilities through strategic acquisitions:

In 2007 the Group acquired Optrel (Vicenza), an Italian company specialized in the design and the construction of inspection machines for the pharmaceutical industry.

Stevanato Group acquired InnoScan, a Danish company who specializes in the production of high-speed inspection systems for complex drugs. The InnoScan series, acquired in 2013, provides automated visual inspection for injectable products including ampoules, vials, cartridges, and syringes, capable of handling clear liquids, emulsions, viscous or turbid products, and lyophilized drugs with throughputs reaching up to 48,000 units per hour.

The Danish company SVM Automatik was acquired by Stevanato Group in 2016. SVM Automatik is a company specialized in assembly, packaging and serialization solutions for the pharmaceutical industry.

Stevanato Group acquired Balda, a company with manufacturing facilities in Germany and California, specializing in plastic development and manufacturing for diagnostic consumables, drug delivery systems, and medical components.

The Balda acquisition was particularly strategic. With the acquisition of the operative units of Balda, the division is also specialized now in high quality and high precision plastic solutions. Balda's healthcare segment is active in diagnostic, pharmaceutical and medical device applications.

By 2017, Stevanato had constructed a truly integrated global platform: - Glass containers: Vials, cartridges, syringes, ampoules - Machinery: Glass-forming lines, inspection systems, assembly equipment - Plastics: Diagnostic consumables, medical device components - Services: Analytical testing, consulting, after-sales support

As of July 2021, the company operated nine production plants for manufacturing and assembling pharmaceutical and healthcare products in Italy, Germany, Slovakia, Brazil, China, Mexico and the US; five plants for machinery and equipment production in Italy and Denmark.

Brazil rounded out the footprint. The plant is situated in Sete Lagoas, Minas Gerais, Brazil. The greenfield facility construction started at the beginning of 2016 and the plant started production in June 2017.

For investors, this acquisition-driven expansion demonstrates capital allocation discipline. Stevanato didn't chase revenues in unrelated markets. Every acquisition strengthened its core pharmaceutical packaging and delivery franchise, deepening vertical integration and extending geographic reach.

VI. The Insulin Cartridge Dominance

Before COVID-19 vaccines made Stevanato famous, the company had already achieved quiet dominance in one of healthcare's most important markets: diabetes treatment.

The Group is the first worldwide producer of insulin cartridges for diabetes treatment and design and production of machinery for glass tubing converting.

We're the largest supplier of cartridges to the pen injector market for insulin in the world today.

Today, Stevanato Group is the market leader in manufacturing glass cartridges for insulin pen injectors and is the world's second-largest manufacturer of glass vials.

The diabetes market represents one of healthcare's most powerful secular trends. Diabetes is a severe and chronic disease that has been steadily increasing over the past few decades. Globally, an estimated 422 million adults were living with diabetes in 2014, compared to 108 million in 1980.

Insulin therapy requires patients to inject themselves multiple times daily—a reality that creates extraordinary demand for delivery devices and the glass cartridges that hold the insulin. Pen injectors, which allow diabetics to self-administer precise doses, have become the dominant delivery format globally.

Stevanato's position in this market was no accident. The company had spent decades refining glass cartridge manufacturing to meet the exacting tolerances required for pen injectors. With over 70 years of experience in glass production, Stevanato Group is currently the market leader in cartridge systems manufacturing. Our knowledge ensures high quality glass cartridges for parenteral applications, designed for hand-held or wearable injection devices.

The customer base reads like a who's who of diabetes care: Novo Nordisk, Eli Lilly, Sanofi—companies whose insulin products generate tens of billions of dollars annually. When these pharmaceutical giants develop new diabetes treatments, they design their delivery devices around Stevanato's cartridge specifications.

Stevanato Group and Haselmeier announced an exclusive agreement to license the Axis-D pen-injector technology. The Axis-D pen-injector was designed and developed by Haselmeier, and a version is currently on the market having been approved by the European Medical Agency and the US FDA. Stevanato Group plans to utilize this technology to provide a new pen injector to support diabetes patients worldwide.

The licensing of pen injector technology from Haselmeier in 2019 extended Stevanato's capabilities from cartridges into complete delivery devices. Italy-based Stevanato secured an exclusive license to the Axis-D pen injector technology for use in the delivery of diabetes medicines in 2019, leading to the production of its Alina line of products. The revised deal positions Stevanato to offer the technology for delivery of treatments including obesity, cardiovascular disease, gastrointestinal and neurological disorders.

The strategic logic was compelling: if Stevanato supplied both the glass cartridges and the plastic pen injector devices, it could offer customers truly integrated solutions while capturing more value per unit.

For investors, the insulin cartridge position demonstrates customer stickiness in action. Pharmaceutical companies don't casually switch glass suppliers. The regulatory qualification process takes years, requires extensive stability studies, and introduces risk that no quality assurance director wants to accept. Once Stevanato earns a spot in a drug product's regulatory filing, it tends to keep that position for the product's entire commercial life.

VII. Inflection Point #3: COVID-19 – The Moment the World Noticed (2020–2021)

In early 2020, as SARS-CoV-2 began its deadly global spread, attention focused on vaccine development. Moderna, Pfizer-BioNTech, AstraZeneca, Johnson & Johnson—dozens of companies raced to create immunity against the novel coronavirus.

Almost no one was thinking about glass vials.

As international efforts to find a vaccine to combat COVID-19 intensified, the most crucial element in global vaccination programs, once a successful vaccine candidate moved into the manufacturing phase, was the worldwide supply of medical-grade glass vials.

The world produces approximately 15 to 20 billion medical vials annually. Based on a Reuters report, the current annual global production is 15 billion to 20 billion glass vials. With potentially 8 billion people needing two doses of vaccine, the math was terrifying. Each person getting the vaccine would likely require two doses, creating a potential immediate need for up to 15.6 billion glass vials.

Enter CEPI—the Coalition for Epidemic Preparedness Innovations—which began frantically securing vaccine manufacturing capacity. When CEPI's advisors surveyed the pharmaceutical glass industry, they made a discovery. Italy-based Stevanato Group, a leading producer of pharmaceutical glass containers, and CEPI signed an agreement for the supply of 100 million Type 1 Borosilicate glass vials to hold up to 2 billion doses of a vaccine against the COVID-19 virus.

Through this agreement, Stevanato Group, which produces annually 10 billion units among drug delivery systems, sterile and bulk glass containers, plastic diagnostic and medical components, became a key supplier to CEPI's COVID-19 vaccine programmes.

The high-quality glass vials that CEPI secured from Stevanato Group were to store 20 doses per vial (2 billion doses in total). Besides the provision of these 100 million vials, the Group also granted a "fast track" access to its glass vial forming lines provided by its company Spami.

That last detail is crucial. Stevanato didn't just supply vials—it supplied the machinery that other manufacturers needed to ramp up their own vial production. The vertical integration strategy that began in 1971 with SPAMI was now accelerating global vaccine supply.

Italy's Stevanato estimated it supplied glass vials and syringes to around 90% of currently marketed COVID-19 vaccine programs.

The pandemic created unprecedented demand. Franco Stevanato said: "Since the pandemic outbreak, we have activated a taskforce acting on two fronts. On one side, we have been implementing all the health and safety measures to protect our staff in all our global operations. On the other hand, we have proactively increased our global capacity to sustain the industry's scale-up industrialisation need."

The company hired aggressively to meet demand while the world locked down. The vials produced were technological marvels in their own right—capable of withstanding temperature ranges from minus 80 to plus 30 degrees Celsius, a requirement for mRNA vaccines that needed ultra-cold storage.

Medical vials are made of Type I borosilicate glass. Type I glass has better pH stability, releases less alkali and chemicals, and is more resistant to drastic temperature changes than other glass types, making it the gold standard in vial making.

The pandemic also accelerated Stevanato's IPO plans. On July 16, 2021, Stevanato Group celebrated its debut on the New York Stock Exchange under the ticker symbol "STVN."

Stevanato Group, an Italian supplier of glass vials, syringes, and other pharmaceutical containers, raised $672 million by offering 32 million shares at $21, the low end of the range.

"IPO is the best way to further finance the business...most of the proceeds of the IPO, we are going to invest in the new greenfield plants, one in Indiana, and one in China," said Franco Stevanato.

The timing was impeccable. The pandemic had demonstrated to investors exactly how critical pharmaceutical glass infrastructure was—and how few companies could provide it at scale. Controlled by the founding Stevanato family, the profitable company is a leading provider of glass and plastic drug containment, drug delivery, and diagnostic solutions to pharma, biotech, and life sciences companies, supplying more than 700 customers globally, including 41 of the top 50 pharmaceuticals.

For investors, COVID-19 proved the real-world resilience of Stevanato's business model. When global health hung in the balance, pharmaceutical companies didn't shop around for new glass suppliers. They turned to the established players they trusted—and Stevanato was first among them.

VIII. Inflection Point #4: The GLP-1 Wave (2023–Present)

Just as COVID-19 vaccine demand began normalizing, another healthcare revolution emerged—one that promises even more durable growth than the pandemic response.

GLP-1 agonists—drugs like Ozempic, Wegovy, Mounjaro, and Zepbound—have become the most talked-about medications in healthcare. Originally developed for Type 2 diabetes, these drugs produced dramatic weight loss in clinical trials, creating a market opportunity that analysts estimate could exceed $100 billion annually by 2030.

The approval and widespread adoption of GLP-1 drugs like Ozempic, Wegovy and Zepbound have revolutionized the healthcare and biopharmaceutical landscapes over the last few years. The efficacy of these drugs in treating obesity and obesity-related diseases stands as a turning point in drug development and patient treatments and outcomes.

Companies like Novo Nordisk and Eli Lilly are at the forefront of producing these drugs, with products like Wegovy, Ozempic, Zepbound, and Mounjaro gaining significant traction in the market.

For Stevanato, the GLP-1 boom represents a perfect alignment of product capabilities and market demand. Two examples in this category are West Pharmaceutical and Stevanato Group. These companies provide critical components on their highest margin products and may see demand and positive mix shift with exposure to more GLP-1 drugs. As a result, improving rates of return are anticipated for both companies.

GLP-1 drugs are delivered via injection—typically using pen injectors with glass cartridges. Stevanato's market leadership in insulin cartridges translates directly to GLP-1 applications because the delivery mechanisms are nearly identical.

Small-volume RTU cartridges are designed to cope with the demands of delivering precise, small amounts of drugs such as GLP-1 for the treatment of diabetes and obesity, insulin, and hormones.

The company has responded with major capacity investments. Cisterna's site is the first to implement premium solutions outside the Group's headquarters in Piombino Dese to meet the growing demand for biopharmaceuticals, such as GLP-1s in Europe.

Located just a few kilometers from the Group's first historic plant in Latina, the new Cisterna site covers an area of 65,000 square meters and employs around 200 people. The facility started commercial production in Q4 2023 and houses advanced production lines for the production of EZ-fill® pre-sterilized syringes with the aim of responding to the modern challenges of the European market, constantly growing in biopharmaceuticals, such as GLP-1s.

The plant in Cisterna di Latina represents one of Stevanato Group's most significant investments in the last five years.

In the United States, Stevanato is building an even larger facility. Stevanato Group announced in June 2021 their intent to build a facility in the Fishers Life Science and Innovation Park with a $140 million investment. Stevanato updated its total investment to $512 million with a plan to hire 515 employees by 2031.

The new U.S. hub solutions and services support operations in the GLP-1 & Peptides, mAbs, Vaccines and RNA-based drugs markets. The new hub in Indiana hosts the production of drug containment solutions, including the EZ-fill® pre-sterilized platform, device manufacturing, and an after-sales support center for equipment.

The Fishers plant is "being positioned as the company's comprehensive North American manufacturing hub for high value solutions, including the production of prefilled syringes and vials," with Stevanato looking to "capitalize on the strong and growing underlying trends in biologics"—such as antibody-drug conjugates, GLP-1s, and monoclonal antibodies.

Fast forward to 2025 and Stevanato's €500 million investment in Fishers is boosting its production capabilities. Commercial production launched in 2024 at the site with the goal of bringing together Stevanato's drug containment solutions and device manufacturing capabilities.

The Fishers investment timeline reveals management's confidence in GLP-1 demand. William Blair analysts highlighted that the first commercial revenue at Fishers was generated in the third quarter of 2024, with the facility expected to "flip to a positive gross margin" in the second half of 2025. The company's prior timeline to reach 100% capacity utilization with €500 million in annual revenues in 2028 "remains on track."

For investors, GLP-1 represents a multi-decade tailwind. Unlike COVID-19 vaccines—which surged and then declined—obesity treatment is a chronic condition requiring ongoing medication. Patients who start Wegovy or Zepbound typically continue for years. Every new patient added creates recurring cartridge and syringe demand.

IX. The Business Model Deep Dive

Stevanato operates through two synergistic business segments that together create an unusually integrated offering.

Stevanato Group comprises two operational divisions: Pharmaceutical Systems with Ompi specialized in glass primary packaging and Balda, focused on specialty plastics and delivery devices; Engineering Systems with Spami, Optrel, InnoScan and SVM, specialized in glass processing, inspection systems, assembly, and packaging solutions.

Biopharmaceutical and Diagnostic Solutions (BDS) generates the vast majority of revenue—around 85%—through the manufacture of glass vials, syringes, cartridges, and plastic components. This segment sells directly to pharmaceutical and biotech companies.

Engineering provides the machinery that makes pharmaceutical glass manufacturing possible: glass-forming lines, inspection systems, assembly equipment, and packaging solutions. This segment sells both to Stevanato's own manufacturing operations and to external customers.

Revenue for the third quarter of 2025 grew 9% to €303.2 million, driven by a 14% increase in the BDS segment, which offset a 19% decline in the engineering segment.

The two divisions maintain a symbiotic relationship. An important thing to note is that Stevanato is customer zero for most of these technologies. So, for example, now that the company is conducting a capacity expansion plan, most of the machines used to fill new plants are coming from the engineering division.

This integration creates competitive advantages at multiple levels:

Quality Control: When problems emerge on production lines, Stevanato's engineers can diagnose whether issues stem from equipment, raw materials, or process parameters. Competitors relying on third-party machinery lack this diagnostic capability.

Speed to Market: New manufacturing technologies can be tested and refined on Stevanato's own lines before being sold externally. The company learns faster than competitors.

Customer Intelligence: Selling equipment to other glass converters provides insight into industry trends and competitor capabilities.

Revenue Diversification: Engineering provides a secondary revenue stream that partially offsets cyclicality in the BDS segment.

The customer base reflects Stevanato's strategic positioning. The company has secured a reputation for reliability, positioning itself as a partner to over 700 clients worldwide, including 41 of the top 50 pharmaceutical companies and 15 of the top 20 biotechnology companies.

Global manufacturing presence ensures supply chain resilience. With locations throughout the world (Italy, Slovakia, Germany, Mexico, USA, China, Brazil), the Pharmaceutical Systems Division produces both traditional products such as vials and ampoules, and strong growth products such as syringes and cartridges for autoinjection systems.

Franco Stevanato stated: "We delivered a solid third quarter with 9% revenue growth and a record 47% increase in high-value solutions, driven primarily by demand for high-performance Nexa® syringes. Our strategic investments in capacity expansion and innovation position us to meet rising demand for injectable biologics, biosimilars, and ready-to-use platforms."

The shift toward "high-value solutions"—RTU products, premium syringes, integrated containment systems—represents the ongoing transformation of Stevanato's revenue mix. As this proportion grows, margins expand because high-value products command premium pricing.

In Q3 2025, revenue increased 9% to €303.2 million. High-value solutions represented a record 49% of total revenue.

For investors, the business model's elegance lies in its self-reinforcing nature. Engineering capabilities enable manufacturing excellence, which builds customer relationships, which drives equipment sales to third parties, which funds R&D for the next generation of technology.

X. Family Ownership & Governance

Three generations of Stevanatos have led this company, creating institutional continuity that publicly-traded competitors cannot replicate.

Son of Giovanni Stevanato, founder of the Stevanato Group, Sergio Stevanato has been actively involved in the family business since high school. He graduated in law from the University of Ferrara in 1969, to then take the leadership of the Company.

With a 68% voting interest in Stevanato Holding, Sergio Stevanato is estimated by Forbes to have a net worth of approximately $5 billion. His sons, Franco Stevanato and Marco Stevanato, hold 16% voting stakes each, ensuring family control over the business.

Stevanato Group S.p.A. operates as a subsidiary of Stevanato Holding S.R.L.—the family-controlled entity that maintains voting control even after the NYSE listing.

Franco Stevanato, currently Chairman and CEO, has been central to the company's transformation. Franco Stevanato resumed his role as Chief Executive Officer of Stevanato Group in May 2024. He previously served as Executive Chairman of the Board and led the Group as CEO from 2010 to 2020. Franco is responsible for leading the company's global expansion and transformation of its core strategic objectives.

Born in Mestre (Venice) in 1973, Franco Stevanato graduated in Political Science in 1998 at University of Trieste. During university he gained work experience in the sales department of Saint Gobain in France and in Stevanato Group. After graduation he officially started to work in the sales area of the Group.

Franco's return to the CEO role in 2024 came after a brief period (2021-2024) when professional manager Franco Moro held the position. Franco Moro was appointed Chief Executive Officer, replacing Franco Stevanato who had held the position since 2010. Franco Stevanato assumed the role of Executive Chairman of the Board of Directors. Sergio Stevanato was appointed Chairman Emeritus, while Marco Stevanato remained as Vice-Chairman.

Under Franco's guidance, he led the Group to consistent growth underscored by its primary business pillars—biopharmaceutical and diagnostic solutions, engineering equipment, and analytical services—driving growth from €143 million in revenue in 2010 to over €1.1 billion in 2024.

Marco Stevanato, the Vice Chairman, focuses on strategic development projects and international expansion—the same role his father Sergio played in earlier decades.

The family governance structure creates both advantages and risks for investors:

Advantages: - Long-term orientation: No pressure for quarterly earnings optimization at the expense of strategic investments - Strategic patience: Willingness to accept near-term margin dilution for capacity expansion - Cultural continuity: Values and operating philosophy transmitted across generations - Alignment: Family wealth tied directly to company performance

Risks: - Key person dependence: Company direction closely tied to family members - Governance concentration: Minority shareholders have limited influence on strategic decisions - Succession uncertainty: Each generational transition introduces execution risk

Italian family capitalism has produced some of the world's most enduring companies—Luxottica, Ferrero, Barilla, Benetton. Stevanato fits this tradition: patient capital deployed over decades in focused industrial niches, with ownership and management closely aligned.

For investors, family control provides assurance that Stevanato won't be managed for short-term financial engineering. The €500 million Fishers investment—which will dilute margins before reaching full utilization—reflects exactly the kind of long-term thinking that family ownership enables.

XI. Porter's Five Forces Analysis

Threat of New Entrants: LOW

The current shortage is due to slow growth of the vials manufacturing industry combined with an unexpected surge in demand. These dynamics help explain why there are only a few major medical glass vial manufacturers in the world.

Pharmaceutical glass manufacturing presents formidable barriers: - Capital intensity: Building a pharmaceutical-grade glass facility requires hundreds of millions of dollars - Regulatory qualification: FDA and EMA approval processes take 3-5 years - Customer validation: Each drug product requires stability studies with specific container suppliers - Technical expertise: Glass-forming precision accumulated over decades cannot be purchased

Spami is the number one choice when it comes to forming lines. The company not only has 50 years of experience, but also draws on 70+ years of experience in pharmaceutical glass primary packaging.

Bargaining Power of Suppliers: MODERATE

Medical vials are made of Type I borosilicate glass. Another type—soda-lime glass which is used for windows and house decor—cannot be used for vaccine vials due to its chemical reactivity and lack of resistance to thermal shock.

Schott AG is the biggest supplier of borosilicate glass for medical bottles and syringes. The supply of pharmaceutical-grade glass tubing is concentrated among few players—Schott, Nippon Electric Glass, Corning—creating some supplier concentration risk.

However, Stevanato's vertical integration into machinery development reduces dependency on equipment suppliers. The company makes its own production lines.

Bargaining Power of Buyers: MODERATE-LOW

Large pharmaceutical companies like Pfizer, Novo Nordisk, and Eli Lilly represent significant purchasing power. However, buyer power is constrained by: - FDA qualification: Switching suppliers requires regulatory filings and stability studies - Quality criticality: A contaminated vial can destroy a billion-dollar drug product - Supply assurance: Pharma companies prioritize reliability over price - Limited alternatives: Few suppliers can match Stevanato's integrated capabilities

Threat of Substitutes: LOW (but watch closely)

BARDA invested $143 million in SiO2 Materials Science to scale up production capacity for the company's glass-coded plastic containers.

Plastic alternatives exist but face significant hurdles: - Glass remains the gold standard for biologics and sensitive formulations - Regulatory agencies prefer proven materials - Plastic-glass hybrids are not yet validated at commercial scale

An industry report notes plastics and polymers led the material market in 2024 due to scalability. Glass is essential for injectables but is a smaller overall share. Trends include substitution of plastic where possible—though these technical shifts are gradual.

Competitive Rivalry: MODERATE-HIGH

The top 5 players in the global pharmaceutical glass packaging market are Schott AG, Gerresheimer AG, Corning Incorporated, Stevanato Group S.p.A., and Nipro Corporation, collectively accounting for over 26% market share.

With 35 production sites in 16 countries, Gerresheimer has a global presence. With around 12,000 employees, the company generated revenues of around €2bn in 2023.

Competition is real but tempered by: - Market growth absorbing capacity expansion - Customer lock-in through regulatory approvals - Industry cooperation on standards

Stevanato Group, together with Gerresheimer AG and SCHOTT Pharma AG, announced that they have entered into a strategic industry alliance ("Alliance for RTU") to support market adoption of Ready-to-Use (RTU) vials and cartridges.

The "Alliance for RTU" demonstrates that competitors sometimes cooperate to grow the overall market—a sign of rational competitive dynamics.

XII. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

Stevanato Group produces annually 10 billion units among drug delivery systems, sterile and bulk glass containers, plastic diagnostic and medical components.

Massive fixed costs in glass furnaces, cleanrooms, and inspection systems spread across enormous production volumes. Each incremental unit carries lower average fixed cost, creating pricing power against smaller competitors.

2. Network Effects: WEAK

Limited direct network effects exist in manufacturing. However, indirect effects emerge through industry standard-setting: as more customers adopt EZ-fill® platforms, fill-finish equipment manufacturers optimize for EZ-fill® specifications, making the platform more attractive.

3. Counter-Positioning: STRONG (historically)

Stevanato's integrated model—glass manufacturing plus machinery development plus inspection systems—proved difficult for pure-play competitors to replicate. Equipment manufacturers like IMA Group would have to enter glass production; glass converters like SGD Pharma would have to acquire machinery capabilities.

The vertical integration creates organizational complexity that incumbents avoid. Gerresheimer and Schott have partially followed, but none match Stevanato's depth.

4. Switching Costs: VERY STRONG

This is Stevanato's most powerful advantage.

FDA Drug Master Files create regulatory lock-in. When a pharmaceutical company files for drug approval, it specifies the container supplier. Changing suppliers later requires supplemental filings, stability studies, and regulatory review. The process takes years and introduces risk.

For biologics—which represent the fastest-growing drug category—container switching is even more challenging because proteins interact with glass surfaces in complex ways.

Support from primary container experts to final assembly and packing solutions is offered. 3mL glass cartridge available in EZ-fill® or bulk configuration.

The depth of integration (containers + devices + analytical services) increases switching costs further. Customers would need to replace multiple suppliers simultaneously.

5. Branding: MODERATE

When it comes to RTU containment solutions for biopharmaceutical products, no solution matches EZ-fill® platform, whose proven advantages have turned its processing technology into an industry standard.

EZ-fill® has achieved brand recognition within pharmaceutical manufacturing. When procurement managers specify "RTU containers," they often mean "EZ-fill® or equivalent"—similar to how "Kleenex" became synonymous with tissues.

6. Cornered Resource: MODERATE-STRONG

Under Franco's guidance, he led the Group to consistent growth—driving growth from €143 million in revenue in 2010 to over €1.1 billion in 2024.

Family ownership provides strategic patience unavailable to publicly-traded competitors. The willingness to accept near-term dilution for long-term capacity expansion represents a resource that competitors cannot easily obtain.

Decades of accumulated know-how in glass forming and machine building create institutional knowledge that cannot be purchased.

7. Process Power: STRONG

These systems employ advanced camera technologies and testing methods to ensure compliance with pharmacopeial standards, reducing false rejects through precise defect classification. Post-2013 acquisition, InnoScan advancements have enhanced inspection speed and accuracy, incorporating AI-driven deep learning models.

Proprietary manufacturing processes refined over 75 years create continuous improvement cycles. Each year of operation generates process learning that competitors must spend time and money to replicate.

XIII. Competitive Benchmarking & Financial Analysis

The Competitive Landscape

Companies like Schott, Gerresheimer, and Corning are among the top players in the market, providing cutting-edge packaging solutions that help ensure the safety and reliability of medical products.

Gerresheimer AG (Germany) Gerresheimer AG, founded in 1864, is a global leader in pharmaceutical packaging and medical technology. Headquartered in Düsseldorf, Germany, the company specializes in the production of glass and plastic packaging solutions for pharmaceutical and healthcare industries.

With 35 production sites in 16 countries, Gerresheimer has around 12,000 employees and generated revenues of around €2bn in 2023.

Schott Pharma AG (Germany) Schott AG, founded in 1884 by Otto Schott, is a leading multinational glass manufacturing company specializing in glass and glass-ceramics. Headquartered in Mainz, Germany, Schott is known for its innovation in pharmaceutical glass packaging.

With over 1,000 patents and technologies developed in-house, SCHOTT Pharma AG & Co. KGaA is headquartered in Mainz, Germany and listed on the Frankfurt Stock Exchange. It generated revenue of EUR 899 million in fiscal year 2023.

West Pharmaceutical Services (USA) West Pharmaceutical Services, Inc., founded in 1923, is a global leader in innovative solutions for injectable drug administration. The company specializes in designing and manufacturing packaging components and systems for pharmaceuticals. Its headquarters are located in Exton, Pennsylvania.

West focuses more on elastomeric components (rubber stoppers, seals) rather than glass containers, making it complementary rather than directly competitive.

Financial Positioning

Stevanato reported 9% revenue growth, record revenue from high-value solutions, expanded margins, and maintained fiscal year 2025 guidance.

For the third quarter of 2025, adjusted EBITDA increased to €77.8 million and the adjusted EBITDA margin improved 280 basis points to 25.7%, compared with the same period last year.

The margin expansion reflects the ongoing product mix shift toward high-value solutions. Revenue from high-value solutions grew 47% and represented 49% of total company revenue. Strong performance in the BDS segment led to a 240 basis point increase in consolidated gross profit margin, reaching 29.2% in the third quarter of 2025.

Capital expenditure remains elevated due to the Fishers and Cisterna expansions. Strong operational cash flow and reduced capital expenditures resulted in €0.3 million in free cash flow for the third quarter of 2025, and €16.9 million for the nine-months ended September 30, 2025. The Company believes it has adequate liquidity to fund its strategic priorities.

FY25 revenue guidance of €1.160–€1.190 billion was maintained.

The financial profile reveals a company investing heavily for future growth. Near-term free cash flow is constrained by capacity expansion, but the underlying business generates healthy operating margins that will compound as new facilities reach full utilization.

XIV. Bull vs. Bear Case

The Bull Case

GLP-1 Drugs Represent a Multi-Decade Tailwind

The efficacy of GLP-1 drugs in treating obesity and obesity-related diseases stands as a turning point in drug development and patient treatments and outcomes.

Unlike COVID-19 vaccines—which surged and declined—obesity treatment is chronic. Patients start Wegovy and continue for years. Every new GLP-1 patient creates recurring demand for glass cartridges and syringes.

Market estimates suggest GLP-1 could exceed $100 billion annually by 2030. Stevanato supplies cartridges to both Novo Nordisk and Eli Lilly—the duopoly controlling this market.

Biologics Growth Drives Demand for Premium Containment

Biologics (large-molecule drugs derived from living cells) represent the fastest-growing pharmaceutical category. These sensitive proteins require premium glass containers that minimize particle shedding and chemical interaction.

"Our strategic investments in capacity expansion and innovation position us to meet rising demand for injectable biologics, biosimilars, and ready-to-use platforms."

Capacity Expansion Positions for Volume Growth

The Fishers and Cisterna facilities represent major bets on future demand. The company's prior timeline to reach 100% capacity utilization with €500 million in annual revenues at Fishers in 2028 "remains on track."

As these facilities ramp, operating leverage will drive margin expansion.

RTU Industry Transition Favors Stevanato

By adopting an industrial RTU setup, pharmaceutical companies can benefit from reduced operational risks, enhanced flexibility and efficiency, and lower waste. RTU technology can help streamline processes, increase productivity, and lower total cost of ownership.

The "Alliance for RTU" with Gerresheimer and Schott suggests industry-wide momentum toward RTU adoption. Stevanato's EZ-fill® platform is the established standard.

Family Control Enables Long-Term Thinking

The Stevanato family's majority ownership allows strategic patience unavailable to competitors pressured by quarterly earnings expectations.

The Bear Case

Customer Concentration Risk

While Stevanato serves 41 of the top 50 pharma companies, GLP-1 demand is concentrated among Novo Nordisk and Eli Lilly. If either company faces supply disruption, pricing pressure, or competitive setback, Stevanato's growth trajectory could suffer.

Capacity Utilization Risk

The company has made substantial capital commitments—€500 million at Fishers alone. If GLP-1 demand disappoints or competition intensifies, these facilities could face underutilization, compressing margins.

Competition from Larger Rivals

Gerresheimer has 35 production sites in 16 countries with around 12,000 employees and generated revenues of around €2bn in 2023.

Gerresheimer and Schott Pharma are formidable competitors with larger scale and deeper resources. The RTU alliance suggests cooperation, but competitive dynamics could shift.

Glass Substitution Risk

BARDA invested $143 million in SiO2 Materials Science to scale up production capacity for glass-coded plastic containers.

While glass remains the gold standard, technological innovation could eventually enable plastic alternatives for sensitive biologics.

Currency and Trade Policy Exposure

As a European company with growing U.S. operations, Stevanato faces currency translation effects and potential trade policy disruption. Foreign currency translation was a headwind, and on a constant currency basis, revenue grew 11%. Certain tariff costs that were not mitigated tempered margins in the third quarter.

Engineering Segment Volatility

A 19% decline in the engineering segment offset growth in BDS. Engineering revenues can be lumpy depending on customer capital expenditure cycles.

Key Performance Indicators for Investors

For ongoing monitoring, three KPIs stand out:

-

High-Value Solutions as % of Revenue: Currently 49% in Q3 2025. This measures the product mix shift toward premium products with better margins. Target: continued expansion toward 50%+ sustainably.

-

BDS Segment Revenue Growth Rate: The core business indicator. Q3 2025 showed 14% growth—investors should watch for sustained double-digit growth.

-

Fishers/Cisterna Utilization Ramp: These capacity investments determine future earnings power. Watch for management commentary on line installations and capacity utilization targets.

XV. Conclusion: The Hidden Infrastructure of Modern Medicine

In the pharmaceutical supply chain, certain nodes are so critical that their failure would cascade throughout the system. Stevanato Group occupies exactly such a position.

As international efforts to find a vaccine to combat COVID-19 intensified, the most crucial element in global vaccination programs was the worldwide supply of medical-grade glass vials. Without medical glass vials, vaccines cannot be stored or delivered, and patients cannot be vaccinated.

This understated Italian company has spent 75 years building capabilities that competitors cannot easily replicate. The vertical integration into machinery development, begun in 1971 with SPAMI, created compounding advantages that strengthen with each decade of accumulated learning.

The EZ-fill® platform transformed Stevanato from a commodity supplier into a solutions provider, deepening customer relationships and raising switching costs. The global manufacturing footprint—Italy, Germany, Slovakia, Mexico, Brazil, China, USA—ensures supply chain resilience for customers with worldwide operations.

Family ownership provides the strategic patience that long-term capacity investments require. The €500 million Fishers facility and the Cisterna expansion represent bets on GLP-1 demand and biologics growth that a quarterly-focused management team might have hesitated to make.

The competitive position reflects multiple moats: scale economies in capital-intensive manufacturing, regulatory switching costs measured in years rather than months, process power accumulated over seven decades, and counter-positioning that competitors have struggled to replicate.

Yet the company remains relatively unknown to investors outside the pharmaceutical industry. COVID-19 provided a brief moment of visibility—but attention quickly shifted to vaccine makers themselves, leaving Stevanato to return to the background where it had always operated.

For long-term investors, this obscurity may represent opportunity. Stevanato sits at the intersection of multiple secular healthcare trends: GLP-1 obesity drugs, biologics manufacturing, vaccine preparedness, and the ongoing shift toward ready-to-use containers. Each trend requires more glass containers, not fewer.

The question isn't whether pharmaceutical glass will remain essential—it will. The question is whether Stevanato can maintain its competitive position while converting market growth into shareholder value. Based on 75 years of evidence, the odds appear favorable.

As Franco Stevanato noted, echoing lessons learned on Saturday mornings at his grandfather's factory: the human relationships with people remain the key driver for the success of the company. In an industry where trust and reliability matter more than price, that philosophy has proven remarkably durable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube