Regentis Biomaterials: The 20-Year Journey to Solve Orthopedic Medicine's Most Stubborn Problem

I. Introduction & Episode Roadmap

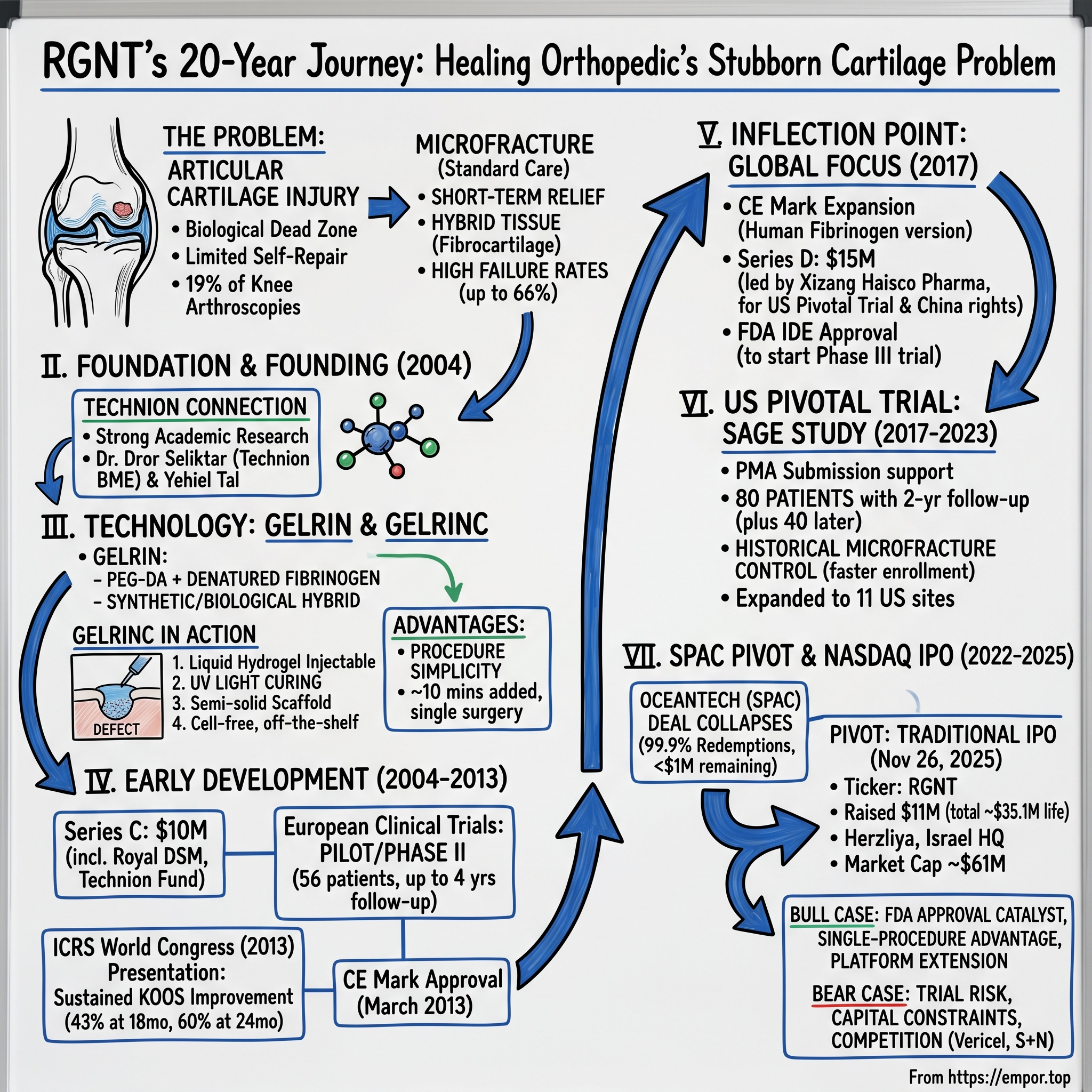

Picture the operating room. A surgeon pauses, scalpel in hand, staring at a divot in the gleaming white surface of a patient's knee cartilage. The injury looks innocuous—perhaps the size of a fingernail—but the surgeon knows the truth that orthopedics has confronted for a century: this tissue will never heal on its own. Not today, not in a year, possibly not ever. Articular cartilage, the smooth coating that allows our bones to glide painlessly against each other, lacks blood vessels and nerve endings. It is, in essence, a biological dead zone where regeneration goes to die.

"The cartilage repair market is the largest unmet need in orthopedic sports medicine today, and represents an estimated market opportunity of more than US $1 billion." These words from a company press release could sound like typical biotech hyperbole. But this time, the market size isn't the remarkable part—it's the word "unmet." Despite decades of surgical innovation, despite a $6 billion global orthopedic industry, the current standard of care is called microfracture, which involves drilling small holes in the underlying bone to allow a blood clot to form within the defect. However, microfracture often provides only short-term relief and may require repeat surgeries.

This is the story of Regentis Biomaterials, an Israeli company that emerged from the Technion—Israel's legendary engineering university—with an audacious premise: what if you could fill that cartilage defect with a liquid, cure it with ultraviolet light, and watch as the body's own stem cells transformed it into something resembling natural tissue?

OceanTech Acquisitions I Corp., a publicly-traded special purpose acquisition company, announced the execution of a definitive Agreement and Plan of Merger with Regentis Biomaterials Ltd, an Israeli company, "a regenerative medicine company dedicated to developing innovative tissue repair solutions that seek to restore the health and enhance the quality of life of patients."

That SPAC deal collapsed. Most companies would have folded. Instead, Regentis Biomaterials Ltd IPO took place November 26 on the NASDAQ exchange under the ticker RGNT. The company persevered, pivoting to a traditional IPO and finally reaching the public markets after a journey that spanned two decades, multiple funding rounds, failed merger attempts, and an approval pathway that would test the patience of even the most committed investors.

This episode covers the arc of regenerative medicine ambition: from a professor's lab bench at the Technion to the operating tables of Europe and America, through the brutal economics of medical device development, and into a competitive landscape dominated by multi-billion-dollar incumbents. Along the way, we'll explore the Israeli medtech ecosystem that nurtured this company, the science behind the product, and what it takes to survive—and potentially thrive—in the "valley of death" that claims most biotech startups.

II. The Science Foundation & Founding Story (2004)

The Problem: Cartilage's Stubborn Refusal to Heal

To understand why Regentis matters, one must first appreciate the biological tragedy that is articular cartilage injury. Articular cartilage is the smooth, white tissue covering the ends of bones where they come together to form joints. Cartilage has limited ability to repair itself, which means that surgical intervention is often required. Focal defects typically occur as a result of trauma and are extremely painful to the patient.

The numbers are sobering. Cartilage defects appear in roughly 19% of patients undergoing knee arthroscopies—a staggering prevalence for a condition with no reliable cure. The long-term failure rate of microfracture, the standard treatment, was 66%, compared with 51% for alternative osteochondral autograft transfer. Furthermore, the mean time to failure was significantly shorter in the microfracture group—4.0 years compared with 8.4 years for the alternative.

For young athletes, the calculus is particularly cruel. Failure rates for microfracture increased with increasing years of follow-up: 9% within 1 year, 18% within 3 years, and 32% within 5 years. Failure rates defined by total knee replacement after microfracture surgery were 5% within 1 year, 12% within 3 years, and 22% within 5 years. Although the gold standard, knee microfracture surgeries have high failure rates as defined by repeat procedures within five years.

The core problem is biological. The surface of joints is covered with articular cartilage—a smooth bearing surface with a dense matrix, few cells, and no blood vessels. When injured by a fall or a sports injury, the dent in the articular cartilage never heals. If the injury is large enough to both expose the underlying bone and cause bleeding, a degree of healing can occur. But the repair tissue is usually not the same as the normal cartilage.

What microfracture produces isn't even true cartilage. The new tissue is a "hybrid" of articular-like cartilage plus fibrocartilage. Experience shows that this hybrid tissue is durable and functions similarly to articular cartilage—at least initially. But as the years pass, that patch begins to fail.

The Technion Connection: Where Innovation Meets Necessity

In Haifa, on the slopes of Mount Carmel, sits the Technion—Israel Institute of Technology. Strong academic and research institutions – top-tier universities such as Technion, Hebrew University, and Weizmann Institute produce cutting-edge research and a steady pipeline of talent. These institutions are deeply integrated into the innovation ecosystem, often spinning off technologies and companies through tech transfer offices.

Dr. Dror Seliktar is an associate professor on the Technion's Faculty of Biomedical Engineering. Dr. Seliktar earned his master's and PhD degrees in mechanical engineering and biomedical engineering, respectively, from Georgia Tech. He previously received his bachelor's degree in mechanical engineering from Drexel University in 1994. After earning his PhD, he was awarded a two-year post-doctoral appointment at the Swiss Federal Institute of Technology in Zurich sponsored by the United States National Science Foundation.

This international pedigree matters. Seliktar returned to Israel carrying the scientific rigor of American and Swiss academia, but he landed in an ecosystem that transformed research into commercial reality with unusual velocity. It was during his first year there that he established the technology that would form the basis of Gelrin, a unique hydrogel matrix of polyethylene glycol diacrylate (PEG-DA) and denatured fibrinogen.

Seliktar's applied research in tissue regeneration led to the discovery of a new biomaterial, Gelrin™, which has been licensed to a company called Regentis Biomaterials Ltd., of which he is a founder. The technology transfer of the patented Gelrin biomaterial technology from the Technion into human clinical trials became an integral part of his academic tenure—an unusual arrangement that speaks to the deep integration between Israeli universities and commercial ventures.

In December 2017, Regentis Biomaterials announced that company co-founder and chief scientific officer Prof. Dror Seliktar was awarded the Rita Levi Montalcini Award for his regenerative medicine research over the past 15 years at the Technion. Prof. Seliktar was in Rome for a special award ceremony held at the Italian Ministry of Foreign Affairs to receive the €40,000 prize.

Company Formation: The Founding Team

Regentis Biomaterials was founded in 2004. The company was founded by Dror Seliktar and Tal Yehiel (also written as Yehiel Tal in some sources).

Yehiel Tal is a seasoned executive in the biomedical field and brings over two decades of management experience in both high-tech and biotech companies. Prior to joining CollPlant, Yehiel served as CEO and co-founder of Regentis Biomaterials Ltd.; Vice-President of Business Development at ProChon BioTech Ltd.; Vice President of Marketing and Business Development at OrthoScan Technologies Ltd. Tal held a BSc and an MSc degree in Mechanical Engineering from the Technion—another Technion connection.

Yehiel Tal founded Regentis in 2004 and served as the Chief Executive Officer from 2004 to 2010. He is currently the Chief Executive Officer of CollPlant Ltd.—itself a regenerative medicine company working with plant-derived collagen for tissue engineering.

The founding story illustrates a pattern common in Israeli medtech: Haifa-based Regentis employs 12 and was founded in 2004 by Tal and Dr. Dror Seliktar from the Department of Biomedical Engineering at the Technion-Israel Institute of Technology. A scientist with a breakthrough, partnered with a commercially-minded executive, both drawing on Technion networks for talent, funding, and credibility.

The company established offices in Or Akiva, Israel and Princeton, NJ—a dual headquarters reflecting the reality that while innovation might begin in Israel, the largest market for medical devices is the United States.

For investors tracking medtech stories, the founding pattern here is textbook: university IP transfer, founder-scientist maintaining scientific direction while professional management handles commercialization, and immediate dual presence in Israel (R&D) and the US (market access). The question, as always in medtech, was whether the science would translate into products, and whether the products would generate returns before the money ran out.

III. The Technology: Understanding Gelrin and GelrinC

How It Works: The Marriage of Synthetic and Biological

The company's core technology is a biodegradable hydrogel called Gelrin™. It is based on polyethylene glycol diacrylate and denatured fibrinogen originally developed at the Technion - Israel Institute of Technology by Dr. Dror Seliktar. The Gelrin hydrogel platform combines the stability and versatility of a synthetic material with the bio-functionality of a natural substance for a range of clinical applications.

That description contains the essence of what makes Gelrin different. Polyethylene glycol (PEG) is a workhorse of medical materials—found in everything from laxatives to injectable drugs. It's synthetic, stable, and well-understood. PEG and native human fibrinogen have been used individually in medical products for many years with excellent results.

Fibrinogen, meanwhile, is the protein that forms the scaffolding of blood clots—nature's original wound-healing material. Gelrin is a synthetic biodegradable, bioactive polymer, composed of PEG that is cross-linked with fibrinogen produced from human plasma. Fibrinogen, a natural protein, the main component of blood clots—the body's unique healing mechanism—is called into action whenever tissue is damaged. It serves as a scaffold in the Gelrin implant, and enables the controlled degradation process of the implant.

The innovation lies in combining these materials. It is a family of hydrogels that derive their unique physical and chemical properties from polymer chains crosslinked with trace quantities of denatured protein. In the body, Gelrin is eroded and resorbed over time. The body of this receding mass acts to stimulate the body's natural healing process, by guiding the migration and organization of cells involved in tissue repair doing so in a gradual process over time.

The Product: GelrinC in Action

GelrinC is the company's specific application of this platform technology for cartilage repair. The company's first commercial product is GelrinC, a cell-free, off-the-shelf hydrogel implant for the treatment of painful injuries to articular knee cartilage. After standard microfracture, the hydrogel is injected as a liquid and conforms to the lesion's size, shape, and depth, with no cutting or press fitting required to fill the lesion. After brief exposure to UV light, the hydrogel becomes a semisolid implant tightly integrated with the surrounding tissue and bone with no fibrin glue necessary to secure it in place. The implant acts as a scaffold, gradually eroding over time as new cartilage takes its place.

The procedural simplicity is a key selling point. GelrinC's unique mode of action relies upon its ability to be implanted as a liquid so that it completely fills the defect, and then be cured into a gel that enables the body's own stem cells to settle on its surface. Over a period of six to 12 months, the GelrinC is gradually resorbed by the body and replaced by new cartilage tissue.

"Unlike other polymers, in the body GelrinC degrades from the outside in and it is this feature which makes it an ideal cartilage repair material," says Alastair Clemow, Ph.D. "We inject the GelrinC into the cartilage defect as a liquid and then solidify it using ultraviolet light. It then becomes a soft, slippery, clear hydrogel. Over time, the hydrogel allows the repair of new cartilage into the defect."

Competitive Advantages: Why GelrinC Is Different

The medical device industry is littered with products that work in theory but fail in practice because they're too difficult for surgeons to adopt. GelrinC's design addresses this directly.

"GelrinC is an off-the-shelf product that can be used at any time during surgery when a lesion is identified without the need for pre-planning or additional surgeries," said Dr. Clemow. "This makes GelrinC an attractive treatment option that is as simple to perform as microfracture with superior clinical outcomes."

The off-the-shelf nature is crucial. Competing cellular products require harvesting cells from the patient, culturing them in a lab, and scheduling a second surgery for implantation. That process takes weeks, costs more, and requires significant infrastructure.

By GelrinC creating such impenetrable barrier and thereby preventing the migration of the cells, the cells are forced to take a different route of creating aggregate and contiguous tissue. Unlike GelrinC, cellular products used by competing companies require a plug of two layers of which the lower layer is a mineral scaffold, which is a foreign body material that has been engineered to be inserted into the bone tissue even though the bone is often healthy.

The manufacturing process of GelrinC meets strict international safety, quality and biocompatibility standards, including GMP and ISO 13485.

For surgeons, what matters most is the practical reality. "We are entering our next evolution in the field of joint preservation. While many current techniques involve transplanting cartilage from a donor, the GelrinC implant allows us to harness the benefits of our patient's own mesenchymal stem cells," said Dr. Jason Scopp from Peninsula Orthopaedic Clinic. "The technique was extremely quick, adding a mere 10 minutes to a standard practice procedure. Product application to the lesion was easy with the assistance of Regentis's proprietary delivery device. It completely filled the defect and after a short exposure to UV light, an optimal implant was formed."

Ten minutes. That's the surgical adoption story in a nutshell. When a new technology requires hours of additional training or fundamentally changes operative workflow, adoption stalls. When it adds ten minutes to an existing procedure, surgeons will try it.

IV. The Long Road: Early Development & Funding (2004-2013)

The Funding Gauntlet Begins

Medical device development is capital-intensive and slow. Unlike software startups that can iterate weekly, medical companies must invest years and tens of millions before generating a dollar of revenue. Regentis's funding journey illustrates this reality.

Regentis Biomaterials's Series B round was from August 06, 2007—three years after founding, with no product on the market and human trials still ahead.

Series C: Royal DSM and European Expansion (2012)

By 2012, the company had progressed far enough to attract strategic interest. Regentis Biomaterials Ltd., a privately held company focused on developing proprietary hydrogels for tissue regeneration, announced that it raised $10 million in its latest round of funding from new investors Royal DSM through its venturing subsidiary and from Crossroad Fund, as well as from existing investors Medica Venture Partners, SCPVitalife and the Technion Investment Opportunities Fund. The Series C round of financing will be used to establish Regentis's European presence and expand its ongoing clinical efforts of GelrinC.

Royal DSM's participation was noteworthy—a global materials science company with $8 billion in revenue joining an early-stage Israeli startup. It signaled validation of the underlying polymer chemistry. The Technion Investment Opportunities Fund's continued participation demonstrated the university's ongoing stake in seeing its spin-offs succeed.

Investors include Medica Venture Partners, SCPVitalife, Royal DSM through its venturing subsidiary, the Crossroad Fund, Haisco Pharmaceutical Group Co. Ltd., Technion Investment Opportunities Fund, ProSeed and Shalom Equity Fund.

European Clinical Trials: The Road to CE Mark

While US FDA approval remained years away, the European pathway offered a faster route to market. Regentis carried out a Pilot/Phase II study of 56 patients that were treated with GelrinC and followed up for up to four years in multiple sites in Northern Europe and Israel. The primary efficacy endpoints were superior changes from baseline for overall KOOS scores and KOOS pain subscale. The primary efficacy end points were met; the improvements observed in the KOOS and VAS pain measurement scores taken over two years were superior (100% greater improvement) to those seen with the traditional microfracture procedure. Additionally, patients continued to report further improvement and greater pain reduction of their knee and associated problems using GelrinC for four years. No serious adverse events were observed for the product in the completed Pilot study.

The results were striking: 100% greater improvement than microfracture at two years, with continued improvement through year four. In a field where treatment effects often fade, sustained improvement was significant.

GelrinC gained CE mark approval in March 18, 2013. This approval, under European regulations, permitted commercial sale in the EU and other countries recognizing the CE mark.

Key Milestone: ICRS Presentation (2013)

Regentis Biomaterials announced new clinical data demonstrating the efficacy and safety of its GelrinC implant for treating articular cartilage in injured knees. As presented at the International Cartilage Repair Society World Congress in Izmir, Turkey, the clinical results demonstrated sustained knee function improvement over 24 months after implantation and significant pain reduction. In addition, the clinical safety data showed that adverse effects were limited and comparable to those reported in similar studies with no serious adverse events related to the implant.

"These results show that GelrinC is safe and that the treatment effectively regenerates high quality cartilage," said Regentis Biomaterials president and CEO Alastair Clemow. "While recovery rates for knees treated with standard procedures plateau and even decrease over time, GelrinC patients showed constant improvement over the course of the study."

The data showed a substantial improvement of the KOOS score of 23.6 points at 18 months, representing a 43% improvement, and 32.9 points at 24 months, representing a 60% improvement.

For investors watching this journey, the 2012-2013 period represented a critical validation point. The technology worked in humans. It was better than standard care. It was safe. The question now became: could they reach the US market, where the real money was?

V. Inflection Point #1: European Approval & Strategic Pivot (2017)

CE Mark Expansion: Human Fibrinogen Version

GelrinC was approved as a device, with a Conformité Européene, or CE, mark in Europe, in 2017. This represented an expansion from the earlier 2013 approval. Regentis Biomaterials Ltd. received European CE mark approval for its GelrinC® biodegradable implant. The approval covers GelrinC manufactured using denatured human fibrinogen and expands upon the existing CE mark for a version containing denatured bovine-sourced fibrinogen. This latest approval enables Regentis to begin accessing new global markets, and helping more patients suffering from damaged articular knee cartilage.

"Since a CE mark is recognized internationally, this key approval opens the door to making the product available in many other territories," said Regentis Biomaterial CEO Alastair Clemow, Ph.D.

Series D: The China Pivot (2016-2017)

The most significant funding development came from an unexpected direction: China. Xizang Haisco Pharma led a $15 million Series D funding for Regentis Biomaterials, an Israeli medical device company. As part of its investment, Haisco will own China rights to Regentis' lead product, GelrinC®.

Regentis Biomaterials raised a $15 million Series D round from investors led by Chinese biopharma Haisco Pharmaceutical Group. The Israeli cartilage repair company will use the financing to conduct a U.S. pivotal trial of its GelrinC.

"We are delighted to enter the Israeli market with a significant investment in Regentis Biomaterial. We see great potential for GelrinC in China and look forward to applying our know-how and experience in bringing this exciting surgical technology to the China market for the benefit of patients, surgeons and hospitals alike," Haisco CEO Wang Junmin said.

As part of the funding round, Haisco will serve as the exclusive distributor of GelrinC in China.

This deal structure—funding in exchange for regional distribution rights—is common in medtech. It solves two problems simultaneously: Regentis gained the capital needed for US trials without excessive dilution, while Haisco secured exclusive access to a potentially transformative product for the world's second-largest healthcare market.

FDA IDE Approval: The US Market Opens

Regentis Biomaterials, a developer of hydrogels for tissue regeneration, announced it received U.S. Food and Drug Administration (FDA) Investigational Device Exemption (IDE) approval to initiate a pivotal Phase III clinical study of GelrinC, a novel treatment for focal cartilage defects in the knee. This clinical study will be used to support a Premarket Approval Application (PMA) which will allow Regentis to market GelrinC in the U.S.

"Gaining IDE approval is a significant step forward for Regentis and brings us that much closer to helping US patients recover from damaged articular knee cartilage," said Regentis President and CEO Alastair Clemow. "GelrinC has been shown to effectively regenerate high quality cartilage, a key challenge in treating these kinds of knee injuries. GelrinC has already demonstrated excellent clinical outcomes in our European study, and we look forward to substantiating these results in the U.S."

The IDE approval was the critical gate to the US market. Without it, there could be no US clinical trial; without the trial, no PMA; without the PMA, no US sales. Each step took years, each step cost millions, and each step could fail.

VI. Inflection Point #2: US Pivotal Trial Launch (2017-2023)

Phase III Begins: First US Patients

Regentis Biomaterials announced the start of its Phase III pivotal clinical trial of GelrinC for the treatment of focal knee cartilage defects with successful surgery on three patients in the U.S. and Denmark. These procedures are part of a Food and Drug Administration (FDA) approved Investigational Device Exemption (IDE) clinical study to compare GelrinC to microfracture, the current standard of care treatment. The clinical study will be used to support a Pre-market Approval Application (PMA) which will allow Regentis to market GelrinC in the U.S. The US procedures were performed by Dr. Jason Scopp at the Peninsula Orthopaedic Clinic in Salisbury, Maryland and by Dr. Bryan Huber at Mansfield Orthopaedics at Copley Hospital in Morrisville, Vermont.

"The success of these three clinical procedures is a significant milestone for Regentis and represents a big step to helping US and European patients recover from damaged articular knee cartilage," said Regentis President and CEO Alastair Clemow, Ph.D.

Trial Design Innovation

The FDA trial will appraise the safety and efficacy of GelrinC compared to the raw level data of a historical microfracture control arm. This study design overcomes the limitation of randomized control studies in this field, and is expected to generate faster patient enrollment and significantly reduce the time for product approval. With an estimated market opportunity in excess of $1 billion, cartilage repair is the largest unmet need in orthopedic sports medicine today.

The trial design deserves attention. Rather than randomizing patients—assigning some to GelrinC and others to microfracture—the FDA agreed to allow comparison against historical data. This approach dramatically speeds enrollment (patients prefer guaranteed access to experimental treatment over a coin-flip) but requires rigorous documentation of the control arm data.

No serious adverse events were observed for the product in the completed Pilot study. Based on these results, the FDA granted Regentis an investigational device exemption, or IDE, for our pivotal trial, permitting PMA submission with two-year follow-up data of 80 patients, with an additional 40 patients to be treated thereafter. The pivotal trial is currently being conducted in the United States and Europe, under the FDA's sanctioned protocol, as an open label study, with one arm only (treatment), using the historical control (microfracture).

SAGE Study Expansion

Regentis Biomaterials today announced it has expanded the SAGE clinical trial of GelrinC™ for the treatment of articular cartilage damage in the knee to 11 U.S. sites. GelrinC is an investigational device being evaluated as a treatment to help the body regrow cartilage in the knee.

The SAGE study is a Food and Drug Administration (FDA) Investigational Device Exemption (IDE) clinical study comparing GelrinC to microfracture, the current standard of care treatment for damaged knee cartilage. The multi-center Phase III pivotal study will enroll 120 patients. All patients who meet study requirements and agree to enter the trial are provided GelrinC as treatment, and their results will be compared to raw level historical data of a microfracture control arm. To be eligible for the study, participants must be between the ages of 18 and 50 and have pain caused by cartilage damage in only one knee.

"This makes GelrinC an attractive treatment option that is as simple to perform as microfracture with superior clinical outcomes. With a potential yearly market of more than 150,000 procedures in the U.S. alone, the opportunities for GelrinC as the primary treatment for articular knee cartilage repair are very exciting."

The 150,000 US procedures annually represents a significant commercial opportunity if even a fraction could be converted to GelrinC.

VII. Inflection Point #3: The SPAC Pivot & Direct IPO (2022-2025)

The SPAC Deal That Wasn't

By 2023, Regentis needed capital. The pivotal trial was ongoing, commercialization required investment, and private funding was getting harder to secure. The SPAC market, which had exploded in 2020-2021, seemed to offer a solution.

OceanTech Acquisitions I Corp., a publicly-traded special purpose acquisition company, announced the execution of a definitive Agreement and Plan of Merger with Regentis Biomaterials Ltd. The all-stock deal contemplates that Regentis' shareholders will receive, in the aggregate, $95 million of OceanTech common stock (subject to certain adjustments), with each such OceanTech common share valued for the transaction at $10.00. Certain outstanding options and warrants to acquire capital stock of Regentis would be assumed by OceanTech.

The pro forma equity valuation of the combined company at deal announcement was estimated to be approximately $133.6 million, which assumed no redemptions.

But the SPAC market that had seemed so promising in 2021 had turned hostile by 2023. Redemptions ahead of an extension vote in May removed 66% of the SPAC's remaining cash in trust, leaving about $8.8 million. In March, the SPAC's original management sold the sponsor holdings to a new team, which signed the definitive merger agreement in May with Regentis.

The deal deteriorated rapidly. OceanTech I shareholders approved the deal in February, although final redemptions reached 99.9% and there is a $6 million minimum cash condition to close the deal. Following the merger vote, the SPAC had about $143,000 remaining in trust.

From nearly $9 million to $143,000—that's what happens when SPAC investors decide to redeem rather than stay in a deal.

OceanTech Acquisitions I in an 8-K said it was calling off its shareholder-approved merger with Regentis, after the Nasdaq confirmed the initial listing application for the post-closing company would not be approved.

The SPAC era produced many casualties. What distinguished Regentis was its response: rather than folding, management pivoted.

Pivoting to Traditional IPO (2025)

The company filed confidentially on January 24, 2025.

(Note: Regentis Biomaterials, Ltd. increased its IPO's size to 1.0 million shares – up from 909,090 shares – and kept the price range at $10.00 to $12.00 to raise $11.0 million, according to its S-1/A filing in May 2025.

The company has a market-cap of $61 million. ThinkEquity acted as the underwriter for the IPO.

The Herzliya, Israel-based company plans to raise $10 million by offering 0.9 million shares at a price range of $10 to $12. At the midpoint of the proposed range, Regentis Biomaterials would command a fully diluted market value of $61 million.

IPO Execution

Regentis Biomaterials Ltd IPO took place November 26 on the NASDAQ exchange under the ticker RGNT. The company is offering shares at an expected price between $10.00 and $12.00 per share.

Regentis Biomaterials has raised $35.1M over its life as a company—remarkably capital-efficient for a medical device company that has conducted clinical trials on multiple continents.

The trial was initiated in late 2017, and the company expects to complete patient recruitment by the end of 2025. Regentis Biomaterials was founded in 2004 and plans to list on the Nasdaq under the symbol RGNT.

Twenty-one years from founding to IPO. That timeline puts the medtech "valley of death" in perspective. Software companies can go from inception to unicorn status in five years. Medical device companies measure progress in decades.

VIII. Market Analysis: The Cartilage Repair Landscape

Market Size and Growth

Estimates of the cartilage repair market vary significantly depending on how the boundaries are drawn. The global orthopedic cartilage repair market was valued at $405 million in 2024 and is expected to grow at a CAGR of 9.2%, reaching $750 million by 2031.

Broader definitions yield larger numbers. The global cartilage repair market size was estimated at USD 5.98 billion in 2024 and is expected to grow at a CAGR of 5.1% from 2025 to 2030.

The cartilage repair market is valued at USD 1.73 billion in 2025 and is on course to reach USD 3.28 billion by 2030, translating into a 13.7% CAGR. Demographic aging, rising obesity, and sports injury volumes expand the patient pool, while technological advances in cell-based implants and tissue-engineered scaffolds improve clinical outcomes. Outpatient arthroscopic procedures shorten recovery times and lower costs, reinforcing payer and provider adoption.

Competitive Landscape

The competitive landscape of the cartilage repair market is witnessing active product development, technological upgrades, and strategic partnerships among leading players such as Vericel Corporation, Zimmer Biomet, Smith & Nephew, and Stryker.

Vericel was the leader in the cartilage repair market due to its offering of MACI®, an autologous cartilage repair therapy for knee defects. The treatment involves expanding a patient's own cartilage cells on a collagen membrane for implantation. In August 2024, the FDA approved an arthroscopic delivery method, allowing for less invasive procedures and faster recovery.

Premium products such as MACI generated USD 46.3 million in Q1 2025 sales, reflecting commercial traction in the United States.

In January 2024, Smith+Nephew acquired CartiHeal, a company focused on innovative cartilage regeneration technologies in sports medicine-Agili-C. This acquisition is intended to bolster Smith+Nephew's offerings in knee cartilage repair and broaden its market reach.

As previously revealed, Smith+Nephew paid $180 million upon completion, with an additional $150 million depending on future financial success. Agili-C has the potential to revolutionize cartilage repair results due to its demonstrated superiority over the existing standard of care.

Treatment Modality Trends

The cell-based modalities segment held the largest market share of 60.5% in 2024 and is expected to grow at the fastest rate during the forecast period. This growth is attributable to the growing preference for autologous chondrocyte transplants as a surgical treatment for damaged articular cartilage.

This is where GelrinC's positioning becomes strategically interesting. It's cell-free—not relying on cultured cells—yet it aims to match or exceed outcomes of cell-based approaches. Cell-based solutions captured 62.39% revenue in 2024 through clinical superiority in pain reduction and tissue restoration. However, cell-free implants should post 14.69% CAGR through 2030 on the strength of off-the-shelf availability and lower cost.

IX. Strategic Frameworks Analysis

Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-HIGH

The cartilage repair market presents a paradox for new entrants. On one hand, In April 2025, Queen Mary University of London developed a new, noninvasive regeneration therapy, marking a significant breakthrough in the treatment of osteochondral defects. The invention uses tiny, soluble polypeptides derived from Agrin to control the cellular repair pathway within the joint. This tailored technique efficiently prevents cartilage degeneration while encouraging the regeneration of new cartilage tissue.

Academic innovation continues to produce novel approaches, suggesting the pipeline of potential entrants remains active. However, FDA/CE regulatory requirements impose 8-10+ year timelines and tens of millions in capital requirements before any revenue can be generated. This protects incumbents but also means that today's research could emerge as competition a decade hence.

2. Bargaining Power of Suppliers: LOW

GelrinC uses commodity materials—synthetic PEG and fibrinogen derived from human plasma. Neither component is proprietary or scarce. The manufacturing challenge lies in combining them correctly and meeting regulatory standards, not in sourcing.

3. Bargaining Power of Buyers: HIGH

Hospital systems and health insurers wield significant negotiating power. The high cost of procedures remains a significant barrier for patients, even for those with private insurance. This cost is not expected to decline significantly over the forecast period, limiting unit sales.

Reimbursement is critical for adoption. A product can be clinically superior but fail commercially if payers refuse to cover it at prices that sustain the business.

4. Threat of Substitutes: MODERATE-HIGH

Multiple alternatives exist. Microfracture remains standard despite limitations because it's cheap and universally available. Total knee replacement is the last resort for severe cases. Newer cell-based therapies (MACI, ACI) compete for the same patients.

5. Competitive Rivalry: HIGH

The key players operating in the global Cartilage Repair industry are Johnson & Johnson Services, Inc., Smith & Nephew plc, Zimmer Biomet, CONMED Corporation, Stryker, Collagen Solutions (US) LLC, Arthrex, Inc., Anika Therapeutics, Inc., B. Braun SE and Vericel Corporation.

Regentis faces competitors with market capitalizations in the tens of billions and established surgeon relationships spanning decades.

Hamilton Helmer's 7 Powers Analysis

1. Scale Economies: WEAK (Currently)

With only 7 employees and no commercial US revenue, Regentis cannot yet exploit scale advantages. This is a future opportunity rather than a current strength.

2. Network Effects: WEAK

Medical devices don't exhibit traditional network effects. Surgeon training and familiarity create some stickiness, but no platform dynamics exist.

3. Counter-Positioning: STRONG ✓

This is Regentis's most powerful position. By GelrinC creating an impenetrable barrier and thereby preventing the migration of cells, the cells are forced to take a different route of creating aggregate and contiguous tissue. Unlike GelrinC, cellular products used by competing companies require a plug of two layers of which the lower layer is a mineral scaffold, which is a foreign body material.

Incumbents like Vericel have built businesses around cell-based approaches. To match GelrinC's simplicity, they would need to cannibalize their existing revenue streams—an incumbent's dilemma.

4. Switching Costs: MODERATE

Surgeon training and hospital protocol investments create switching costs. Once a surgeon learns a procedure and a hospital stocks the materials, changing requires effort. But these costs are surmountable with demonstrated clinical superiority.

5. Branding: DEVELOPING

Regentis has begun building reputation through clinical presentations and surgeon relationships but lacks the brand equity of established orthopedic giants.

6. Cornered Resource: STRONG ✓

Seliktar's applied research in tissue regeneration led to the discovery of a new biomaterial, Gelrin™, which has been licensed to a company called Regentis Biomaterials Ltd. The technology transfer of the patented Gelrin biomaterial technology from the Technion into human clinical trials has been an integral part of the development.

The Technion-licensed patents protect the unique PEG-fibrinogen hydrogel formulation. Dr. Seliktar's continued involvement as CSO ensures ongoing scientific direction.

7. Process Power: MODERATE-STRONG

"The technique was extremely quick, adding a mere 10 minutes to a standard practice procedure." This process simplicity—the ability to integrate GelrinC into existing surgical workflows with minimal disruption—represents genuine process power that competitors would struggle to replicate without fundamentally redesigning their products.

X. Playbook: Business & Investing Lessons

University Tech Transfer Done Right

The Technion-to-startup model exemplifies best practices in academic commercialization. Strong academic and research institutions produce cutting-edge research and a steady pipeline of talent. These institutions are deeply integrated into the innovation ecosystem, often spinning off technologies and companies through tech transfer offices.

Key success factors include: - Founder-scientist maintaining involvement (Dr. Seliktar as CSO) - Professional management for commercialization (Yehiel Tal as initial CEO, Alastair Clemow subsequently) - University investment arm participation (Technion Investment Opportunities Fund) - Clear IP licensing arrangements

Surviving the Medtech Valley of Death

Twenty-one years from founding to IPO. Multiple pivot points in financing strategy (VC → SPAC → traditional IPO). Total of $35.1M raised over the life of the company.

That capital efficiency is remarkable. Many medical device companies burn through $100M+ before reaching commercialization. Regentis's frugality was born of necessity—Israeli companies often lack access to the deep capital pools available in Boston or San Francisco—but it became a competitive advantage when market conditions turned hostile in 2022-2023.

Regulatory Strategy as Competitive Moat

The study design overcomes the limitation of randomized control studies in this field, which is expected to result in faster patient enrollment and significantly reducing the time for product approval.

The decision to pursue CE Mark first, then FDA PMA, reflects standard medtech strategy: prove the concept in Europe's faster regulatory environment, then use that data to support the longer US pathway. Each regulatory approval adds to the moat—competitors must replicate not just the technology but the expensive, time-consuming approval process.

The CEO Who Made It Work

Dr. Clemow has more than 25 years of experience in the development and management of orthopaedic devices. He has served in numerous senior management positions including President & CEO of Gelifex, Inc.; Vice President of Worldwide New Business Development at Ethicon Endo-Surgery (a division of Johnson & Johnson); Vice President of New Business Development, Johnson and Johnson Professional Inc.; and Director of R&D, Johnson and Johnson Orthopaedics. Dr. Clemow holds B.Sc. and Ph.D. degrees in Metallurgy from the University of Surrey, and an MBA in Finance from Columbia University. Dr. Clemow is a Fellow of the American Institute for Medical and Biological Engineering and a Past President of the Society for Biomaterials.

Clemow's background—J&J experience, technical depth, financial training—represents the ideal profile for taking a startup through clinical development and commercialization. He knows the regulatory pathway intimately, understands surgeon adoption dynamics, and has the credibility to negotiate with large potential partners.

XI. Bull vs. Bear Case & Future Outlook

Bull Case

The FDA Approval Catalyst The trial was initiated in late 2017, and the company expects to complete patient recruitment by the end of 2025. If enrollment completes on schedule, two-year follow-up data would be available in late 2027, potentially leading to PMA submission and FDA approval in 2027-2028.

FDA approval would unlock the largest orthopedic market in the world. With a potential yearly market of more than 150,000 procedures in the U.S. alone, the opportunities for GelrinC as the primary treatment for articular knee cartilage repair are very exciting.

Off-the-Shelf Advantage Cell-based competitors require two surgeries: one to harvest cells, another to implant them after weeks of culture. GelrinC's single-procedure approach reduces cost, complexity, and patient burden. This operational simplicity could drive adoption among surgeons and health systems focused on efficiency.

Platform Extension This technology serves as the foundation for future clinical indications in osteoarthritis. Knee cartilage repair is the initial application; the Gelrin platform could potentially address other orthopedic indications, expanding the addressable market.

M&A Target Strategic mergers and acquisitions continue to influence the market dynamics in the cartilage repair industry. In January 2024, Smith+Nephew acquired CartiHeal. At a $61 million market cap, Regentis is an affordable acquisition target for large orthopedic players seeking innovative technology.

Bear Case

Clinical Trial Risk The pivotal trial must succeed. Failure to meet endpoints would devastate the company's prospects. While European data is encouraging, US regulatory standards differ, and the historical control design, while efficient for enrollment, creates analytical challenges.

Capital Constraints Raising $11.0 million at IPO provides runway but not abundance. Commercialization—building a sales force, establishing reimbursement, managing inventory—requires significant additional capital. Further dilution seems likely before profitability.

Competitive Pressure Vericel's arthroscopic MACI launch creates a short-term edge, whereas Smith & Nephew integrates CartiHeal with its robotics suite for comprehensive knee solutions. Well-capitalized competitors are actively strengthening their positions.

Reimbursement Uncertainty Even with FDA approval, commercial success depends on payer acceptance. New technologies often face reimbursement challenges that limit adoption regardless of clinical merit.

Key KPIs to Track

For investors monitoring Regentis, three metrics matter most:

-

Trial Enrollment Progress: Monthly updates on patient recruitment. The company expects completion by end of 2025. Delays signal execution problems or site recruitment challenges.

-

European Commercial Traction: GelrinC has CE Mark approval. Any European commercial activity—partnership announcements, procedure volumes, surgeon feedback—provides real-world validation independent of US trials.

-

Cash Runway: Burn rate versus available capital. Medical device companies without revenue live and die by cash management. Investors should track quarterly cash positions and projections.

XII. Conclusion: What It Takes

Regentis Biomaterials embodies the brutal arithmetic of medical device innovation. A genuine scientific breakthrough at a world-class university. Twenty years of development. Multiple funding rounds. A failed SPAC merger. A successful traditional IPO against odds. And still, the critical question—FDA approval—remains unanswered.

The Israeli tech ecosystem exemplifies how a small nation can become a global innovation leader by cultivating a culture of bold thinking, embracing failure, and building bridges across sectors and disciplines. It is not only a hub of startups but a robust, scale-up-oriented, globally integrated economy.

Whether Regentis ultimately succeeds will depend on clinical data yet to be generated, regulatory decisions yet to be made, and commercial execution yet to be proven. But the company's survival to this point—through the valley of death, through a collapsed SPAC market, to a public listing at a $61 million valuation—demonstrates something about the resilience required to bring regenerative medicine from laboratory concept to operating room reality.

For investors, Regentis represents a binary bet: FDA approval could transform a micro-cap into a substantial orthopedic player; failure would likely eliminate most of the equity value. The technology is promising. The management is experienced. The market opportunity is real. The execution risk is significant.

That's the story of every medical device company. What distinguishes them is who makes it through—and Regentis, against considerable odds, is still in the game.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube