Abivax: The Serendipitous Pivot from HIV to IBD

I. Introduction & Episode Roadmap

On a grey morning in July 2025, the Nasdaq opened to scenes reminiscent of a biotech fairy tale. Abivax SA's stocks had been trading up by 554.8% following the announcement that would transform this once-struggling French biotech from near-bankruptcy to one of the year's most remarkable success stories. In August 2025, the stock price of Abivax surged by around 580% following dual Phase III success in ulcerative colitis.

The central question of the Abivax story is this: How did a small French biotech, founded to cure HIV, stumble upon a potentially transformative treatment for inflammatory bowel disease—and nearly run out of cash multiple times doing it?

Abivax is a clinical-stage biotechnology company driven to advance human health by regulating the immune response through the power of microRNA. But this elegant description belies a decade of pivots, near-death financing experiences, and the kind of scientific serendipity that makes drug development one of the most unpredictable industries on Earth.

The 50 mg once-daily dose of obefazimod led to a compelling pooled 16.4% (p<0.0001) placebo-adjusted clinical remission rate at Week 8 in the ABTECT-1 and ABTECT-2 trials. Individually, the 50 mg dose demonstrated a placebo-adjusted remission rate of 19.3% (p<0.0001) in ABTECT-1 and a placebo-adjusted remission rate of 13.4% (p=0.0001) in ABTECT-2.

These numbers, while technical, represent something far more significant: validation that a molecule originally designed to fight HIV could become a first-in-class treatment for millions suffering from a devastating autoimmune disease. The journey from HIV target to IBD breakthrough involves strategic pivots, the infamous "biotech valley of death," novel microRNA biology, and a market opportunity that could reshape treatment paradigms for millions of patients worldwide.

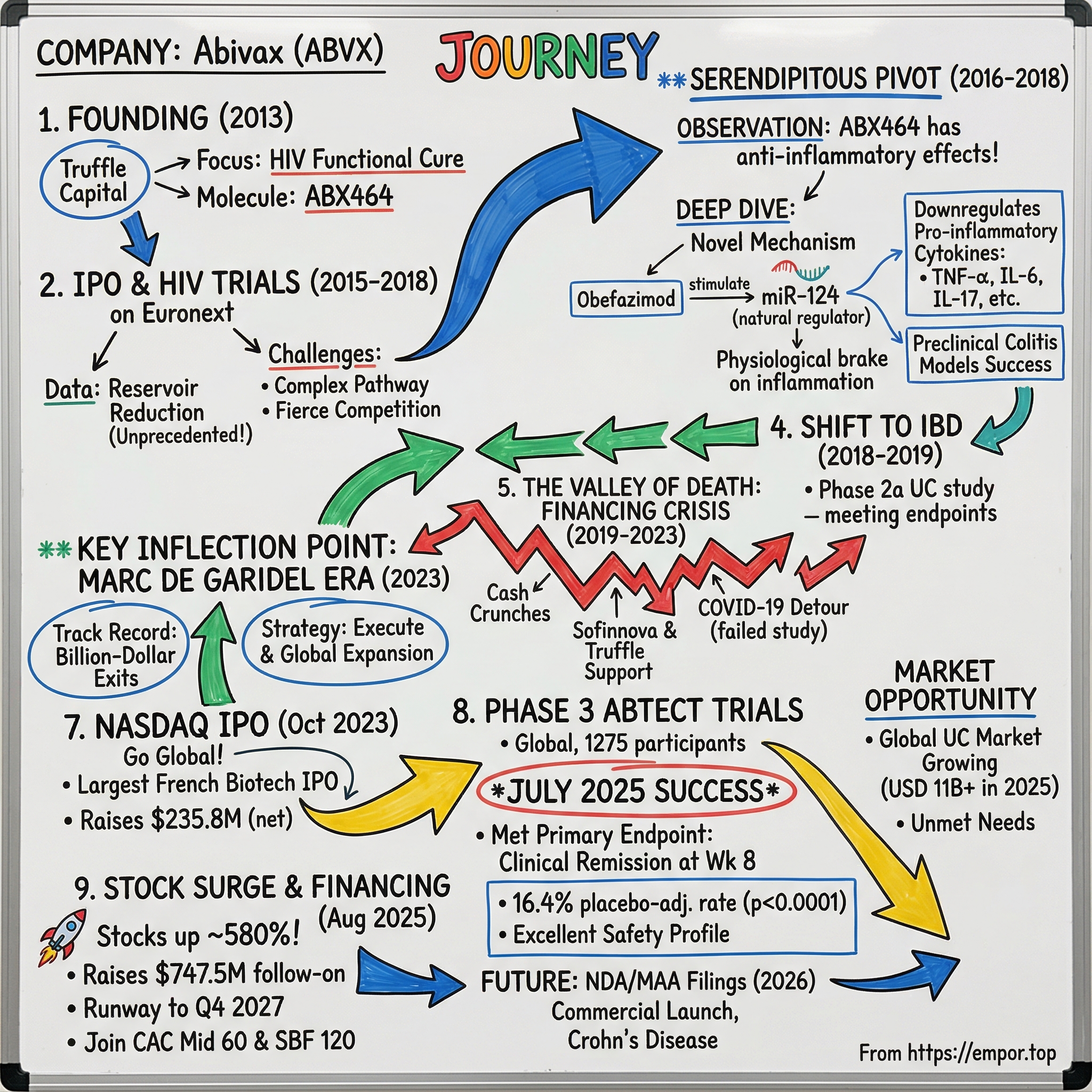

II. Founding Origins: Truffle Capital & the Merger of Three Biotechs (2013)

The story of Abivax begins not in a gleaming research laboratory, but in the venture capital offices of one of France's most prolific biotech pioneers. Founded in 2013 in Paris, by the French immunologist Philippe Pouletty.

Philippe Pouletty is no ordinary venture capitalist. Philippe Pouletty is the founder and CEO of Truffle Capital, one of Europe's leading Venture Capital firms. He is a pioneer in the biotech and medical device industries, with over 30 years' experience in France and in the Silicon Valley. His credentials read like a master class in academic-to-commercial translation: He is the inventor of 39 patents, including the second-highest revenue-generating patent in Life Sciences for Stanford University, which earned him induction into the University's prestigious Hall of Fame of Inventors in 2012.

Pouletty's approach to company creation differed fundamentally from the traditional model of scientists spinning out university research. His philosophy centered on identifying promising academic science, licensing the intellectual property, and building commercial enterprises around it while maintaining close collaboration with the original inventors.

Abivax's origins trace back to Montpellier, where researchers from the CNRS (France's National Centre for Scientific Research) and the Institut Curie in Paris were collaborating with Splicos, a private company, on a molecule designed to inhibit HIV replication. This collaboration represented the collision of world-class French immunology research with the commercial infrastructure needed to transform laboratory discoveries into therapeutic candidates.

The original vision was ambitious and focused: become a leader in immuno-virology. The company would leverage cutting-edge RNA biology to tackle some of the most challenging viral diseases, starting with HIV—a market that, despite decades of therapeutic advances, still lacked a functional cure.

Pouletty was the Founder of SangStat (1988, organ transplantation therapeutics, IPO on NASDAQ in 1993, sold to Genzyme for $600M in 2002). This track record of building and exiting biotech companies successfully positioned Truffle Capital as a cornerstone investor capable of the patient capital and strategic guidance that early-stage biotechs desperately need.

Dr. Pouletty, who served as Chairman of the Board from the company's inception in December 2013 until August 2022, stepped down due to his recent appointment as Chairman and acting CEO of a French listed biotechnology company in plastics recycling. As CEO of Truffle Capital, he was instrumental in founding Abivax and developing obefazimod, the company's lead drug candidate.

The genesis of ABX464, Abivax's lead molecule, emerged from this academic-commercial partnership. The compound represented a novel approach to HIV—rather than targeting the virus directly as existing antiretrovirals did, it worked by modulating RNA biogenesis, potentially offering a pathway to a functional cure by addressing viral reservoirs that existing treatments couldn't touch.

For investors considering clinical-stage biotechs, the Abivax origin story illustrates a critical pattern: the most transformative discoveries often emerge not from targeted drug development but from following the science wherever it leads. Truffle Capital's willingness to fund exploration rather than rigid milestone achievement would prove essential in the company's eventual pivot.

III. The Initial Public Offering & HIV Focus (2015-2018)

By 2015, Abivax had accumulated enough preclinical data and early clinical evidence to warrant a public market debut. In 2015, Abivax launched its initial public offering on the stock market Euronext in Paris, raising EUR 57.7m, a record amount for a French biotechnology company on the Euronext in Paris.

EnterNext, the Euronext subsidiary dedicated to promoting and growing the market for SMEs, celebrated the listing of Abivax, a biotech company specialising in the clinical development and commercialisation of anti-viral therapies. The company positioned itself squarely in the immuno-virology space, with HIV as its lead indication.

Prof Hartmut Ehrlich, CEO of Abivax, stated: "We are proud to join the biotechnology companies listed on Euronext in Paris, with strong demand from institutional investors and European family offices that showed their support very early on in our listing process, as well as retail investors."

The HIV thesis was compelling. Despite decades of antiretroviral therapy (ART) advancement that had transformed HIV from a death sentence to a manageable chronic condition, no treatment could eliminate viral reservoirs—the hidden pockets of infected cells where HIV DNA integrated into the host genome, ready to reactivate if treatment stopped.

ABX464's mechanism offered tantalizing potential. Rev inhibitor. ABX464 is a small molecule ARV compound that acts through a novel mode of action to prevent HIV replication after proviral DNA integration. ABX464 blocks the formation of viral structural proteins that are essential for HIV replication.

Early clinical results generated genuine excitement in the HIV research community. The results show a statistically significant reduction (p<0.01) of the HIV viral reservoir in the blood of study participants with HIV. These data confirm the human HIV reservoir reduction by ABX464 seen in ABIVAX's previous Phase IIa trial, ABX464-004.

ABIVAX announced that the company's lead therapeutic candidate ABX464 demonstrated the first reduction in HIV reservoirs ever observed in chronically infected HIV patients as measured by total HIV DNA detected in peripheral blood mononuclear cells (PBMCs).

This was unprecedented. Amongst evaluable patients (4 placebo and 14 ABX464-treated patients), a reduction in viral DNA copies/mPBMCs was observed in 7/14 treated patients (mean change of -40%, ranging from -27% to -67%) and no responders were observed in the placebo group.

However, the HIV drug development landscape presented formidable challenges. The regulatory pathway was extraordinarily complex, requiring demonstration not just of reservoir reduction but of clinical benefit—and the gold standard would be treatment interruption studies that could take years to complete. Competition was fierce, with dozens of well-funded programs pursuing similar goals. And the commercial dynamics were challenging: existing ART regimens worked well enough that payers might not reimburse premium prices for incremental improvements.

An efficacy signal with respect to a reduction of the viral load by ABX464 was detected, mainly in subjects treated at the highest dose. Further studies will be required to demonstrate antiviral effects in HIV-infected subjects in combination with other antiretroviral therapies.

The results, while scientifically significant, proved commercially "mixed"—sufficient to suggest the compound had biological activity but insufficient to justify the massive investment required to reach regulatory approval in HIV alone.

For fundamental investors, the 2015-2018 period illustrates the gap between scientific novelty and commercial viability. ABX464's HIV data were genuinely groundbreaking from a research perspective but fell short of the clear-cut efficacy signals that would justify late-stage development costs in a crowded market.

IV. The Serendipitous Discovery: From HIV to Inflammation (2016-2018)

⭐ KEY INFLECTION POINT #1: The Anti-Inflammatory Discovery

The pivot that would ultimately define Abivax's future emerged not from strategic planning but from careful observation of what the science was revealing. As researchers conducted HIV trials and analyzed patient samples, they noticed something unexpected: ABX464 appeared to have profound effects on inflammation.

Dr. Jean-Marc Steens, M.D., chief medical officer of ABIVAX, commented: "Our new data on the anti-inflammatory effects of ABX464 on rectal tissue are highly encouraging, and support the continued development of ABX464 for treatment of HIV, and inflammatory diseases like ulcerative colitis."

This observation triggered deeper investigation into ABX464's mechanism. Moreover, ABX464 has been shown to stimulate the expression of anti-inflammatory molecules (IL-22 and miR-124) in immune cells in preclinical testing.

The science behind this dual effect proved fascinating. Obefazimod, an investigational oral therapy, is the first and only molecule that enhances the expression of miR-124, a natural regulator of the inflammatory response. Enhancing the expression of miR-124 results in decreases in cytokines and immune cells, helping to reduce inflammation.

MicroRNAs (miRNAs) are small non-coding RNA molecules that regulate gene expression at the post-transcriptional level. miR-124 had been identified in academic research as a natural "brake" on inflammatory responses—it was found at reduced levels in patients with inflammatory conditions, suggesting that enhancing its expression might restore immune homeostasis.

Specifically, obefazimod enhances the selective splicing of a single long non-coding RNA to generate the anti-inflammatory microRNA, miR-124, which downregulates the translation of pro-inflammatory cytokines and chemokines like TNF-α, IL-6, CCL2/MCP-1 and IL-17, as well as Th17+ cells.

What made this mechanism particularly elegant was its physiological nature. ABX464 acts as "a physiological brake" of inflammation and does not blunt the immune response. Unlike immunosuppressants that broadly dampen immune function—increasing infection risk—obefazimod's mechanism appeared to restore balance rather than impose suppression.

Enhanced expression of miR-124 stabilizes the inflammatory response only in the presence of dysregulation, with no effect in its absence, potentially indicating preservation of immune competence.

Advanced therapies have transformed the treatment of inflammatory bowel disease; however, many patients fail to respond, highlighting the need for therapies tailored to the underlying cell and molecular disease drivers. The first-in-class oral molecule ABX464 (obefazimod), which selectively upregulates miR-124, has demonstrated its ability to be a well-tolerated treatment with rapid and sustained efficacy in patients with ulcerative colitis (UC).

The transition from HIV to inflammation wasn't a complete abandonment but rather a portfolio rebalancing driven by commercial reality and scientific opportunity. The inflammatory diseases market offered several advantages: clearer regulatory pathways with established endpoints, unmet medical need despite existing therapies, and a mechanism of action—oral, once-daily, immune-modulating—that could differentiate meaningfully from biologics that required injections and carried immunosuppressive risks.

For example, ABX464 was recently shown to protect mice from the lethal effects of DSS (Dextrane Sulfate Sodium), a substance inducing severe colitis.

The preclinical evidence was compelling enough to justify a Phase 2a proof-of-concept study in ulcerative colitis—a disease that affects millions worldwide and where existing treatments leave substantial room for improvement.

V. The Pivot to Inflammatory Bowel Disease (2018-2019)

⭐ KEY INFLECTION POINT #2: Strategic Pivot to IBD

As the molecule showed a strong anti-inflammatory effect in preclinical models, Abivax decided to conduct a Phase 2a clinical study in ulcerative colitis, an inflammatory bowel disease (IBD). Based on the promising results of this clinical study in ulcerative colitis, the company decided to shift its focus towards the treatment of chronic inflammatory diseases.

This wasn't an abandonment of HIV—the company continued to pursue investigator-initiated studies with third-party funding—but rather a recognition that the inflammatory disease opportunity offered a more viable commercial path.

The Phase 2a results validated the pivot. ABX464 has completed a Phase 2a proof-of-concept study, ABX464-101, aimed at evaluating the safety and efficacy of ABX464 50 mg given once daily versus placebo for two months in subjects with moderate-to-severe active ulcerative colitis (UC) who have failed or are intolerant to immunomodulators, anti-TNFα, vedolizumab and/or corticosteroids. This study revealed a statistically significant difference.

The encouraging Phase 2a data led directly to a larger, more definitive Phase 2b trial. Obefazimod is an oral small-molecule drug candidate in clinical development for the treatment of moderately to severely active ulcerative colitis (UC) and has demonstrated anti-inflammatory activity in preclinical studies and in both Phase 2a and Phase 2b clinical trials. In April 2021, Abivax completed its randomized, double-blind and placebo-controlled Phase 2b trial which was conducted in 15 European countries, the United States and Canada in 252 patients. The primary endpoint (statistically significant reduction of Modified Mayo Score) was met with once-daily administration of obefazimod (25 mg, 50 mg, 100 mg) at week 8. Further, all key secondary endpoints, including endoscopic improvement, clinical remission, clinical response and the reduction of fecal calprotectin showed significant difference in patients dosed with obefazimod as compared to placebo.

The market opportunity Abivax was targeting was substantial. The global ulcerative colitis market size was valued at USD 8 billion in 2024 and is estimated to grow at a CAGR of 5.6% from 2025 to 2034. One of the major factors contributing to the growth of this market is the rising prevalence of the disease.

The ulcerative colitis treatment market is anticipated to grow from USD 11.01 billion in 2025 to USD 15.81 billion by 2034, with a compound annual growth rate (CAGR) of 4.1% during the forecast period from 2025 to 2034.

More importantly, the data revealed obefazimod's durability. In addition to the induction results, the analysis of the open-label maintenance trial after two years of treatment demonstrated clinical remission rates of 53% in 217 ulcerative colitis patients treated with once-daily oral 50 mg obefazimod.

The Phase 2b results positioned Abivax for what should have been a straightforward path to Phase 3 trials and partnership discussions. But the biotech industry rarely follows straight lines, and Abivax was about to enter its darkest period—the valley of death that claims so many promising clinical-stage companies.

VI. The Valley of Death: Financing Crisis (2019-2023)

⭐ KEY INFLECTION POINT #3: Near-Death Financial Experience

The period from 2019 to 2023 represents one of the most harrowing chapters in modern European biotech history—a case study in how promising science can nearly perish for lack of capital.

Sofinnova first invested €12 million ($14 million) in Abivax in 2019. At the time, the French biotech was facing a cash crunch with its share price having fallen more than 60% since its 2015 Paris listing. However, Kinam Hong, partner at Sofinnova, told BioXconomy the firm saw beyond the immediate financial distress to the underlying scientific potential.

The investment extends Abivax's cash runway out to the middle of 2020, buying the biotech time to fund ABX464 to milestones while seeking a partner for the asset. Abivax ended 2018 with €13 million in cash after burning through about €1.5 million a month that year. A loan agreement with Kreos Capital and equity line with Kepler Cheuvreux gave Abivax access to €17 million more.

The challenge was stark: Phase 2b results were promising, but Phase 3 trials would cost far more than the company could fund from existing resources or European capital markets alone.

"Sofinnova Partners is globally recognized as a leading specialist investor and their investment, combined with the continued support of our founding shareholder, Truffle Capital, not only validates our science and strategy but also extends our cash runway."

The 2019 Sofinnova investment bought time but didn't solve the fundamental problem. Abivax needed to finance a Phase 3 program that would ultimately involve over 1,200 patients across 36 countries—a commitment requiring hundreds of millions of dollars that the company simply didn't have.

Then came the COVID-19 detour. The randomized, double-blind, placebo-controlled miR-AGE study investigates the effect of early treatment (at point of diagnosis) in 1,034 COVID-19 elderly or high-risk patients.

The German regulatory authority for drugs and medical products, BfArM, has approved its Phase 2b/3 study of ABX464 in COVID-19 patients. The randomized, double-blind, placebo-controlled study is investigating early treatment (at diagnosis) in 1,034 COVID-19 elderly or high-risk patients (miR-AGE trial).

The COVID-19 pivot was scientifically rational—ABX464's anti-inflammatory properties could theoretically address the cytokine storm that killed many COVID patients—and it brought non-dilutive funding. Financing is being provided by the French investment bank Bpifrance, with €36 million in non-dilutive funding (€20.1 million grant, and €15.9 million loan refundable upon success) for this Phase 2b/3 trial, as well as manufacturing scale-up, additional clinical and other development costs.

Abivax SA has rejected an acquisition offer in order to pursue a phase IIb/III trial of its lead anti-inflammatory drug ABX-464 in 1,034 COVID-19 patients.

But the COVID trial ultimately failed. The Data Safety and Monitoring Board (DSMB) confirmed ABX464 was safe and well tolerated in 383 high-risk Covid-19 patients but recommended stopping due to lower than expected rate (10.1%) of progression to severe disease or death with no difference between ABX464 and placebo groups.

While the COVID setback was disappointing, it didn't derail the core UC program. ABX464 has been shown to be highly efficacious in treating "chronic" inflammation according to clinical, endoscopic and histological endpoints in ulcerative colitis, as confirmed by the phase 2a data. Therefore, this outcome in "hyper-acute" Covid-19 disease has no impact on ABX464 potential to be successful in chronic inflammatory disease.

The financing struggle continued through 2022. This financing was subscribed by new and existing US and European biotech investors, led by TCGX, with the participation from Venrock Healthcare Capital Partners, Deep Track Capital, Sofinnova Partners, Invus and Truffle Capital. The subscription price of the New Shares was set at EUR 8.36, with a 9.6% premium to the last closing price. Funds managed by Truffle Capital, which held a 30.5% stake in the Company, subscribed to the Capital Increase for an amount of EUR 1.6M.

The total costs of the phase 3 UC program until the end of 2024, which is the expected date of the results of the two phase 3 induction studies, is estimated by the Company to amount to EUR 200M.

By early 2023, Abivax had promising Phase 2 data, a differentiated mechanism of action, and a clear regulatory pathway—but was running out of cash. The company needed transformational leadership and transformational capital.

VII. Leadership Transition: The Marc de Garidel Era (2023)

⭐ KEY INFLECTION POINT #4: New CEO & Nasdaq IPO

In April 2023, Abivax announced the appointment that would change everything. Abivax SA announced the appointment of Marc de Garidel as Chief Executive Officer (CEO) and Interim Board Chair, effective May 5, 2023. Prof. Hartmut J. Ehrlich, M.D., will retire from the CEO position, which he has held since the Company's founding in 2013.

Marc de Garidel was no ordinary CEO candidate. His track record was extraordinary, featuring two billion-dollar exits in rapid succession:

Marc also sold Corvidia Therapeutics in August 2020 to Novo Nordisk for $2.1B in total consideration after having joined the company in April 2018. He was the CEO of Ipsen between November 2010 and July 2016, overseeing the development of its U.S. presence.

From July 2021 through February 2023, de Garidel served as CEO of CinCor Pharma where he led the successful sale of the company for up to $1.8B, subject to the achievement of certain milestones, to AstraZeneca in February 2023.

The pattern was unmistakable: de Garidel specialized in taking clinical-stage assets, executing flawlessly, and delivering premium exits. But his interest in Abivax went beyond the usual turnaround playbook.

Having recently guided CinCor Pharma through its successful acquisition by AstraZeneca, I was drawn to the clarity of the science and the conviction of the team. After attending the ECCO (European Crohn's and Colitis Organisation) congress in Copenhagen and immersing myself in the IBD field, I became convinced that obefazimod's profile was truly unique. I therefore accepted both the CEO and chairman roles to steer Abivax through its pivotal Phase 3 programme and the next stage of its global expansion.

De Garidel's background equipped him uniquely for this challenge. Marc de Garidel has 40+ years of experience in the pharmaceutical and biotechnology sectors, with the last 12 years as a CEO. Marc joined Abivax in May 2023.

Marc has a degree in Civil Engineering from the Ecole des Travaux Publics in Paris, has a Master's in International Management (MIM) from Thunderbird Global School Management and an executive MBA from Harvard Business School.

His educational pedigree combined engineering rigor with global business sophistication, while his career trajectory—starting at Eli Lilly, progressing through Amgen to Ipsen leadership—gave him deep understanding of both European and U.S. pharmaceutical markets.

There is very little time for this company for a turnaround, given the fact that the company is not well financed. Phase 3 has started, but it's not really going fast enough. So, you need someone to execute.

De Garidel's assessment of Abivax's situation was clear-eyed: great science, inadequate capital, need for urgent action. His prescription would prove equally direct.

As a CEO, I cannot rely on the prospect of an acquisition; that assumption during Phase 2 proved costly when no deal materialised. This time, our focus is firmly on building a sustainable business capable of standing on its own, while remaining open to collaboration if the opportunity arises.

This philosophy represented a fundamental shift from the previous approach. Rather than developing the asset to a partnership-ready stage and seeking a deal, de Garidel would build commercial infrastructure for independent U.S. launch while maintaining partnership optionality for ex-U.S. markets.

VIII. The Nasdaq IPO: Going Global (October 2023)

⭐ KEY INFLECTION POINT #5: U.S. Market Access

Within months of joining, de Garidel executed the financing transformation Abivax desperately needed. Abivax announced the pricing of its initial public offering on the Nasdaq Global Market by way of a capital increase of 20,325,500 new ordinary shares, consisting of a public offering of 18,699,460 ordinary shares in the form of American Depositary Shares, in the United States and a concurrent offering of 1,626,040 ordinary shares in certain jurisdictions outside of the United States.

The aggregate gross proceeds are expected to be approximately $235.8 million, equivalent to approximately €223.3 million, before deduction of underwriting commissions and estimated expenses payable by the Company. The Global Offering is expected to close on October 24, 2023.

The ADSs began trading on the Nasdaq Global Market on October 20, 2023.

Abivax successfully completed its initial public offering on the Nasdaq Global Market in October 2023, raising USD 235.8 million in gross proceeds (app. USD 212.2 million in net proceeds) under challenging market conditions: Abivax's offering is the largest ever US IPO of a French-listed biotech company.

The timing was notable. October 2023 represented one of the more challenging periods for biotech IPOs, with rising interest rates and sector-wide skepticism dampening investor appetite. Yet Abivax attracted substantial institutional interest.

Truffle Capital is pleased with Abivax's highly successful Nasdaq IPO, despite a challenging stock market environment. Abivax is a clinical-stage biotechnology company focused on the development of drugs that exploit the body's natural regulatory mechanisms to modulate the immune response of patients suffering from chronic inflammatory diseases.

"If you want to raise, say, $100-plus million or $200 million, there's only one way to go: it's Nasdaq," de Garidel said. Nasdaq's 3,490 listed securities is more than quadruple the 800+ listings in Paris and nearly twice the approximately 1,900 listings across all Euronext markets. Euronext's roughly €6.5 trillion in market capitalization is just over 30% of Nasdaq's approximately $22 trillion in market cap. "You have a depth of investors with bigger pockets in the U.S. You have also more expertise in the U.S.," de Garidel said.

Didier Blondel, Chief Financial Officer of Abivax, added: "The past year was also very successful looking at the trust that our existing and new U.S. and European investors placed in us, reflected in the significant capital raises in 2023. With the successful Nasdaq IPO last year, the largest Nasdaq IPO of a French-listed biotech company, we continue to implement our multi-pronged financial strategy to fund our projects in 2024 and beyond."

The Nasdaq listing accomplished several strategic objectives simultaneously: it provided the capital needed to complete Phase 3 trials, it gave Abivax access to U.S. specialist investors who understood IBD therapeutics, and it positioned the company for an eventual U.S. commercial launch with American Depositary Shares already trading.

Abivax SA has been listed on Euronext Paris since 26 June 2015 and on the Nasdaq Global Market since October 20, 2023.

The dual listing also created a unique position: Abivax could tap European research tax credits and support mechanisms while accessing U.S. growth capital. This hybrid model would prove essential as the company scaled its Phase 3 program.

IX. Phase 3 ABTECT Trials: The Make-or-Break Moment (2022-2025)

⭐ KEY INFLECTION POINT #6: Phase 3 Success

The ABTECT program represented the definitive test of everything Abivax had built over a decade. The ABTECT program is one of the largest Phase 3 ulcerative colitis trials ever conducted.

Enrollment Completion: 1,275 participants successfully enrolled into two Phase 3 pivotal studies across multiple clinical sites.

ABTECT-1 and ABTECT-2 are global, multicenter, randomized, double-blind, placebo-controlled trials assessing once-daily oral administration of obefazimod at 25 mg or 50 mg doses in adult patients with moderately to severely active UC. Eligible participants had inadequate response, loss of response, or intolerance to conventional and/or advanced therapies. The trials were conducted simultaneously and have enrolled 1275 patients from > 600 participating clinical trial sites in 36 countries.

The patient population was notably challenging—nearly half had already failed advanced therapies, representing some of the hardest-to-treat UC patients. ABTECT included a well-balanced distribution of advanced therapy naïve and advanced therapy experienced participants, with 47.3% of participants having had inadequate response to prior advanced therapy, including the largest population of patients with inadequate response to JAK inhibitor therapy.

On July 22, 2025, the results arrived. Abivax announced positive topline results from its Phase 3 ABTECT-1 (Study 105) and ABTECT-2 (Study 106) 8-week induction trials evaluating its oral, first-in-class miR-124 enhancer, obefazimod (ABX464), in adult patients with moderately to severely active ulcerative colitis.

Results from ABTECT-1 and ABTECT-2 showed obefazimod met its FDA primary endpoint of clinical remission at week 8 in the 50 mg once-daily dose regimens for both trials.

The pooled 50 mg once-daily dose produced a 16.4% placebo-adjusted clinical remission rate at Week 8 (p<0.0001) and both ABTECT 1 and 2 met the FDA primary endpoint and all key secondary endpoints at 50 mg.

The results were particularly impressive in patients who had failed JAK inhibitors—a population where treatment options are severely limited. The trials enrolled 1,272 patients with a refractory population (47% with prior inadequate response to advanced therapy; 21% with prior JAK inhibitor inadequate response).

50 mg once-daily dose of obefazimod met all key secondary endpoints demonstrating highly statistically significant and clinically meaningful benefits.

Fabio Cataldi, M.D., Chief Medical Officer, stated: "The exemplary results from the ABTECT induction trials reflect our dedication to scientific rigor and disciplined execution. We are thrilled to report outcomes that not only met but exceeded the bar set by our Phase 2b trial, a remarkable achievement that speaks volumes about the quality of our development program."

Safety data reinforced the positive picture. No signal for serious, severe, or opportunistic infections or malignancies was reported.

The safety profile of obefazimod remained consistent with prior clinical experience. No new safety signals were observed in either trial and the treatment was generally well tolerated across both dose groups.

With induction data in hand, the path to regulatory submission became clear. Contingent on positive 44-week maintenance results, Abivax intends to submit a New Drug Application (NDA) to the U.S. Food and Drug Administration (FDA) and a Marketing Authorization Application (MAA) to the European Medicines Agency (EMA) in the second half of 2026.

X. The Stock Surge & Follow-On Financing (August 2025)

The market's response to the Phase 3 results was extraordinary. French biotechnology company Abivax SA experienced an extraordinary surge in premarket trading on July 23, 2025, with shares skyrocketing over 400% following the announcement of positive Phase 3 clinical trial results for its ulcerative colitis treatment. The company reported compelling results from its ABTECT trials, which evaluated obefazimod, a first-in-class oral miR-124 enhancer, in patients with moderate to severely active ulcerative colitis. This breakthrough announcement represents a significant milestone for the clinical-stage biotechnology company and offers new hope for patients suffering from this chronic inflammatory bowel disease.

ABVX shares opened the premarket session at $49.88, representing a staggering 398.80% increase from the previous close of $10.00. The dramatic surge was triggered by the company's announcement of successful Phase 3 trial results released after market hours on July 22, 2025.

Abivax shares surged 500% after positive phase 3 results for obefazimod in moderate-to-severe ulcerative colitis, achieving significant clinical remission at 8 weeks induction period.

The company moved quickly to capitalize on this validation. Abivax successfully closed its public offering of 11,679,400 American Depositary Shares (ADSs), including the full exercise of the underwriters' option. The offering generated gross proceeds of $747.5 million (€637.5 million), with estimated net proceeds of $700.3 million (€597.2 million) after deducting costs. The company expects these proceeds, combined with existing cash, will extend its operational runway into Q4 2027, providing 12 months of cash following the planned NDA submission for Ulcerative Colitis.

Abivax announced the full exercise of underwriters' option to purchase 1,523,400 additional American Depositary Shares (ADSs) at $64.00 per ADS. The additional shares bring the total offering to 11,679,400 ADSs, resulting in gross proceeds of $747.5 million. The offering price represents a 21.0% premium over the volume-weighted average price of Ordinary Shares on Euronext Paris over the last three trading sessions.

The dramatic stock movement can be attributed in part to pivotal events this quarter, including the completion of a substantial $650 million follow-on equity offering, which bolstered market confidence and investor interest.

The financing represented one of the largest biotech follow-on offerings in European history. The current stock price of Abivax S.A. (ABVX) is $125.71 as of November 24, 2025. The market cap of Abivax S.A. (ABVX) is approximately 9.3B.

Abivax has been selected to join the CAC Mid 60 and SBF 120 indices following Euronext Paris's annual review. The inclusion will become effective on September 19, 2025. The company expects this inclusion to enhance its visibility and broaden its investor base, particularly among institutional investors and index-linked funds. CEO Marc de Garidel highlighted this achievement as a validation of the company's strategic vision and execution capabilities.

The transformation was complete: from near-bankruptcy to multi-billion dollar market capitalization in just over two years.

XI. The Science Deep Dive: Understanding Obefazimod's Mechanism

Understanding why obefazimod represents a potentially paradigm-shifting therapy requires diving into its unique mechanism of action.

Abivax is exploring the ability to treat chronic inflammatory diseases like ulcerative colitis in a new way. Obefazimod, Abivax's lead drug candidate, is the first and only molecule that enhances the expression of microRNA-124 (miR-124), a natural regulator of the inflammatory response.

MicroRNAs are small non-coding RNA molecules, typically 21-23 nucleotides in length, that regulate gene expression post-transcriptionally. They don't code for proteins themselves but instead fine-tune the expression of genes by binding to messenger RNAs and either degrading them or preventing their translation.

miR-124 was identified in research as downregulated in inflammatory conditions, including UC. When inflammation occurs, miR-124 levels drop, removing a natural brake on the inflammatory cascade. Obefazimod works by restoring this brake.

The long-term efficacy of obefazimod 50 mg QD in patients with moderate-to-severe UC is associated with a sustained increase in miR-124 expression in blood and rectal tissue. The sustained enhanced expression of miR-124 for 2 years may be associated with the durability of clinical response observed with obefazimod.

ABX464 treatment upregulated miR-124 and led to decreases in proinflammatory cytokines including interleukin (IL) 17 and IL6, and in the chemokine CCL2. Consistently, miR-124 expression was upregulated in the rectal biopsies and blood samples of patients with UC, and a parallel reduction in Th17 cells and IL17a levels was observed in serum samples.

What distinguishes this mechanism from existing therapies is its physiological nature. Under dysregulated inflammatory conditions in preclinical studies, enhanced expression of miR-124 resulted in stabilized levels of multiple cytokines and chemokines, bringing them back to homeostatic levels. Simultaneously restoring multiple pathways to homeostatic levels may lower the potential for compensatory immune escape mechanisms, which may result in more durable, long-term efficacy.

Traditional biologics like anti-TNF agents target single inflammatory mediators. JAK inhibitors are broader but still work through defined signaling pathways. Obefazimod, by contrast, restores a natural regulatory mechanism that modulates multiple pathways simultaneously—potentially explaining its observed durability and favorable safety profile.

Because of obefazimod's ability to enhance the expression of miR-124, the mechanism of action of obefazimod is novel and has shown potential in clinical trials in its ability to bring patients into remission and achieve clinical response.

The oral delivery provides additional differentiation. Most advanced UC therapies require injection or infusion, creating burden for patients and healthcare systems. A once-daily oral pill with comparable or superior efficacy would represent a significant advancement.

What was once perceived as a limitation has become a key differentiator. Unlike anti-TNFs, anti-IL-23s, or the newer anti-TL1A antibodies, all of which target single inflammatory pathways, obefazimod enhances miR-124, a natural regulator of immune balance that modulates several cytokines simultaneously, including IL-6, IL-17, and TNF-α.

XII. Market Landscape & Competitive Analysis

The ulcerative colitis market represents a substantial and growing opportunity. National Library of Medicine estimates that ulcerative colitis impacts between 9 and 20 individuals per 100,000 annually, with an overall prevalence of 156 to 291 cases per 100,000.

Despite the expanding range of therapies, 10–20% of patients with ulcerative colitis still require proctocolectomy due to refractory disease. This surgical removal of the colon represents the treatment of last resort—and the fact that such a significant proportion of patients still require it underscores the unmet need.

The current treatment paradigm follows a step-up approach. The rising prevalence of ulcerative colitis has expanded the global patient pool, driving higher demand for effective treatments. Patients with mild to moderate disease benefit from oral therapies like aminosalicylates, while those with severe cases increasingly rely on biologics and JAK inhibitors.

By drug class, the TNF inhibitors segment has recorded more than 38% of revenue share in 2024. By drug class, the JAK inhibitors segment is expected to grow at the fastest rate in the market during the forecast period.

Key competitors dominate different segments:

Anti-TNF Biologics: AbbVie's Humira (adalimumab) and Janssen's Remicade (infliximab) established the biologics paradigm but face biosimilar competition. Anti-TNF biologics lead treatment options with a 30% share.

Integrin Inhibitors: Takeda's Entyvio (vedolizumab) has become a preferred option for many gastroenterologists due to its gut-selective mechanism and favorable safety profile.

JAK Inhibitors: Pfizer's Xeljanz (tofacitinib) and AbbVie's Rinvoq (upadacitinib) offer oral convenience but carry boxed warnings for cardiovascular and malignancy risks.

S1P Modulators: Pfizer's Velsipity (etrasimod) and Bristol Myers Squibb's Zeposia (ozanimod) represent the newest oral class with differentiated mechanisms.

IL-23 Inhibitors: Johnson & Johnson's Tremfya (guselkumab) and Eli Lilly's Omvoh (mirikizumab) target the IL-23 pathway with promising efficacy.

Obefazimod's positioning appears differentiated on several dimensions:

- Mechanism: First-in-class miR-124 enhancer with multi-cytokine modulation

- Administration: Once-daily oral, like JAK inhibitors and S1P modulators

- Safety: Favorable profile without the cardiovascular/malignancy signals of JAK inhibitors

- Durability: Long-term maintenance data suggesting sustained response

By route of administration, the oral route of administration of drugs segment is expected to grow at the fastest rate during the projected period.

The patient preference shift toward oral therapies creates tailwinds for obefazimod if it achieves approval with competitive efficacy data.

XIII. Porter's Five Forces & Strategic Analysis

1. Threat of New Entrants: MODERATE-HIGH

The IBD therapeutic space attracts substantial R&D investment due to the market size and unmet need. Barriers exist—clinical trials are expensive and lengthy, regulatory pathways demanding—but well-capitalized biotechs and large pharma continue entering.

2. Bargaining Power of Buyers: HIGH

Payers (insurance companies, PBMs) wield significant leverage in specialty drug pricing. Hospital systems and integrated delivery networks increasingly influence prescribing through formulary decisions. Real-world evidence demonstrating value over existing options will be essential for premium pricing.

3. Bargaining Power of Suppliers: LOW-MODERATE

As an oral small molecule, obefazimod benefits from relatively commoditized manufacturing. Contract manufacturing organizations (CMOs) for small molecules are numerous, reducing supplier power. However, scaling production for potential blockbuster demand requires careful supply chain management.

4. Rivalry Among Existing Competitors: HIGH

The UC market features aggressive competition from established players with substantial resources. AbbVie, Takeda, Pfizer, J&J, and Bristol Myers Squibb all have major franchises and extensive commercial infrastructure. Differentiation on efficacy, safety, and convenience will determine market share capture.

5. Threat of Substitutes: MODERATE

For mild disease, 5-ASA therapies remain first-line and adequate for many patients. For severe disease, surgery (proctocolectomy) represents the ultimate alternative—eliminating the disease at the cost of the colon. Neither creates direct competitive pressure on advanced therapies for moderate-to-severe disease.

Hamilton Helmer's 7 Powers Analysis:

- Counter-Positioning: Obefazimod's novel mechanism may be difficult for incumbents to replicate quickly without abandoning existing franchises

- Scale Economies: Not yet applicable for a pre-commercial company

- Switching Costs: Patient inertia and physician familiarity could benefit first-movers in the miR-124 space

- Network Economies: Limited applicability in pharmaceuticals

- Process Power: Manufacturing know-how for obefazimod represents modest barrier

- Branding: To be established through commercial launch

- Cornered Resource: The first-in-class mechanism and clinical data package represent intellectual property barriers

XIV. Bull and Bear Case Analysis

The Bull Case

First-Mover Advantage in Novel Mechanism: As the first and only miR-124 enhancer, obefazimod creates a potentially defensible niche. If the mechanism delivers differentiated long-term outcomes, Abivax could establish standard-of-care status.

Oral Convenience with Biologic-Like Efficacy: The combination of once-daily oral administration with efficacy comparable to biologics addresses a key patient preference gap in the market.

Favorable Safety Profile: Unlike JAK inhibitors, obefazimod hasn't shown cardiovascular or malignancy signals in clinical trials. If this profile holds post-marketing, it could become preferred for certain patient populations.

Expansion Potential: Success in UC creates a platform for Crohn's disease (Phase 2b initiated), with potential for other inflammatory conditions where miR-124 dysregulation plays a role.

In July 2025, we announced positive top-line results from the 8-week induction trials of obefazimod in UC, marking a key milestone in our clinical development program. Patient enrollment for ENHANCE-CD in Crohn's disease was initiated in Q3 2024.

Financial Position: With the recent financing, the company expects to fund operations into Q4 2027, providing 12 months of cash following the planned NDA submission.

The Bear Case

Clinical Risk: Maintenance data from the 44-week study (expected Q2 2026) remains outstanding. Induction success doesn't guarantee maintenance efficacy—some drugs have faltered at this stage.

Commercial Execution: Abivax has never launched a commercial product. Building U.S. sales and marketing infrastructure from scratch is challenging, expensive, and fraught with execution risk.

Outside the United States, we plan to commercialise obefazimod through partnerships, but in the US, our objective is to launch independently.

Competitive Dynamics: The UC market is intensely competitive with well-resourced incumbents. AbbVie, Pfizer, and others have substantial resources to defend market share through pricing, contracting, and physician relationships.

Regulatory Risk: While Phase 3 results were positive, FDA and EMA review processes can identify issues not apparent from trial data. Labeling restrictions could limit commercial potential.

Reimbursement Uncertainty: Premium pricing for a first-in-class oral therapy requires payers to accept differentiation claims. In an increasingly cost-conscious environment, this isn't guaranteed.

XV. Key Performance Indicators for Ongoing Monitoring

For investors tracking Abivax's ongoing performance, three KPIs merit close attention:

1. 44-Week Maintenance Trial Data Quality

The Q2 2026 maintenance data readout represents the single most important near-term catalyst. Metrics to watch:

- Clinical remission rate durability vs. placebo

- Endoscopic improvement sustainability

- Safety profile consistency over extended treatment

- Comparison to historical maintenance results for approved therapies

Strong maintenance data supports the NDA filing thesis; weak data could substantially impair commercial potential.

2. NDA/MAA Filing and Regulatory Milestones

Following maintenance data, the regulatory trajectory becomes paramount:

- NDA submission timing (planned H2 2026)

- FDA acceptance and review designation (priority review would signal regulatory enthusiasm)

- Advisory committee recommendation if required

- Approval decision and label contents

Label breadth—particularly for refractory patients and use without prior biologic failure—will influence commercial positioning.

3. Commercial Launch Execution Metrics

Post-approval, standard pharmaceutical launch metrics apply:

- Prescriber adoption rates among target gastroenterologists

- Gross-to-net pricing dynamics (rebates, contracting)

- Payer coverage breadth and tier positioning

- Market share capture trajectory

XVI. Regulatory and Accounting Considerations

Regulatory Overhangs:

The primary regulatory risk centers on FDA and EMA review of the complete data package. While Phase 3 induction results were positive, regulators examine:

- Long-term safety across the entire clinical program

- Manufacturing quality and supply chain reliability

- Proposed labeling claims vs. supporting data

- Risk-benefit profile in context of approved alternatives

No current FDA communications have raised concerns, but the review process can surface issues not anticipated from clinical results alone.

Accounting Considerations:

As a clinical-stage company, Abivax's financial statements require particular attention:

- R&D Expenses: Continue to dominate P&L; expect elevated spending through NDA filing and commercial preparation

- Revenue Recognition: Currently minimal; will become significant only post-approval

- Cash Burn Rate: With ~$700M+ in net proceeds from 2025 offering, runway extends into Q4 2027; monitor burn relative to milestones

- Stock-Based Compensation: Common in biotech; affects GAAP operating results but represents non-cash expense

The company recorded an operating loss of EUR 93.7M in H1 2025, up from EUR 80.0M in H1 2024, primarily due to expanded R&D expenses of EUR 77.9M.

XVII. Myth vs. Reality: Fact-Checking the Consensus Narrative

MYTH: "Obefazimod is just another oral drug for UC"

REALITY: Obefazimod works through a first-in-class mechanism (miR-124 enhancement) distinct from JAK inhibitors or S1P modulators. This isn't just a formulation difference—it's a fundamentally different approach to immune modulation that restores physiological balance rather than suppressing specific pathways.

MYTH: "The HIV pivot was a failure"

REALITY: The HIV program demonstrated proof-of-concept for a novel mechanism and generated safety data across hundreds of patients. The "failure" was commercial viability in a crowded market, not scientific validity. The anti-inflammatory properties discovered through HIV research enabled the UC pivot that now defines the company.

MYTH: "European biotechs can't compete with U.S. companies"

REALITY: Abivax's dual listing strategy, combined with de Garidel's U.S. commercial expertise, positions the company to compete effectively. The 2025 follow-on offering—one of the largest European biotech financings ever—demonstrates U.S. investor appetite for the story.

MYTH: "Phase 3 success guarantees commercial success"

REALITY: The maintenance data, regulatory review, and commercial execution phases all present distinct challenges. Many drugs with positive Phase 3 induction data have stumbled on maintenance, labeling, or launch execution.

XVIII. Conclusion: From Serendipity to Strategy

The Abivax story encapsulates both the promise and peril of biotech development. A molecule designed to cure HIV discovered unexpected anti-inflammatory properties. A company that nearly ran out of cash multiple times executed one of the largest European biotech financings in history. A French biotech competing in a market dominated by American and Japanese giants now stands on the threshold of U.S. commercial launch.

"There were moments when resources were stretched and setbacks hit, but we believed in the science and worked with management to keep the company on track. That resilience has turned into one of Europe's great biotech success stories."

Several lessons emerge for investors evaluating clinical-stage biotechs:

Follow the science, not the original thesis: Abivax's pivot from HIV to IBD wasn't a failure—it was adaptation to what the data revealed. Companies that rigidly pursue original hypotheses despite contradictory evidence often fare worse than those willing to pivot.

Capital structure determines fate: Abivax survived the valley of death because patient investors—Truffle Capital, Sofinnova—continued to support the company through difficult periods. Without that support, promising Phase 2 data would have died on the vine.

Leadership transitions can be transformational: Marc de Garidel's arrival coincided with the company's transformation from struggling European biotech to globally funded late-stage player. Execution matters, and experienced leadership can unlock value that promising science alone cannot.

First-in-class mechanisms carry premium risk and reward: Obefazimod's novel mechanism means no precedent for regulatory success or commercial performance in the miR-124 space. This cuts both ways—differentiation supports premium positioning, but lack of precedent increases uncertainty.

As Abivax awaits its 44-week maintenance data and prepares for regulatory submissions, the company stands at an inflection point. The science has been validated through Phase 3 success. The capital is in place. The leadership team has the track record. What remains is execution—the translation of clinical promise into commercial reality.

Philippe Pouletty said: "It is a great pride for me and Truffle Capital to have founded Abivax and to have contributed to the development of obefazimod for over a decade. I am convinced that Abivax, led by a strong CEO, management team, and board of directors, has the potential to help hundreds of thousands of patients suffering from severe inflammatory diseases."

Whether that potential is realized depends on decisions yet to be made and data yet to be generated. But for investors seeking exposure to novel mechanism of action drugs with platform potential, Abivax represents one of the more compelling stories in contemporary biotech—a decade-long journey from serendipitous discovery to potential market leadership, with all the attendant risks and rewards that such journeys entail.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube