Royal Gold: The "Royalty on Gold" Business Model That Changed Mining Finance

I. Introduction & Episode Roadmap

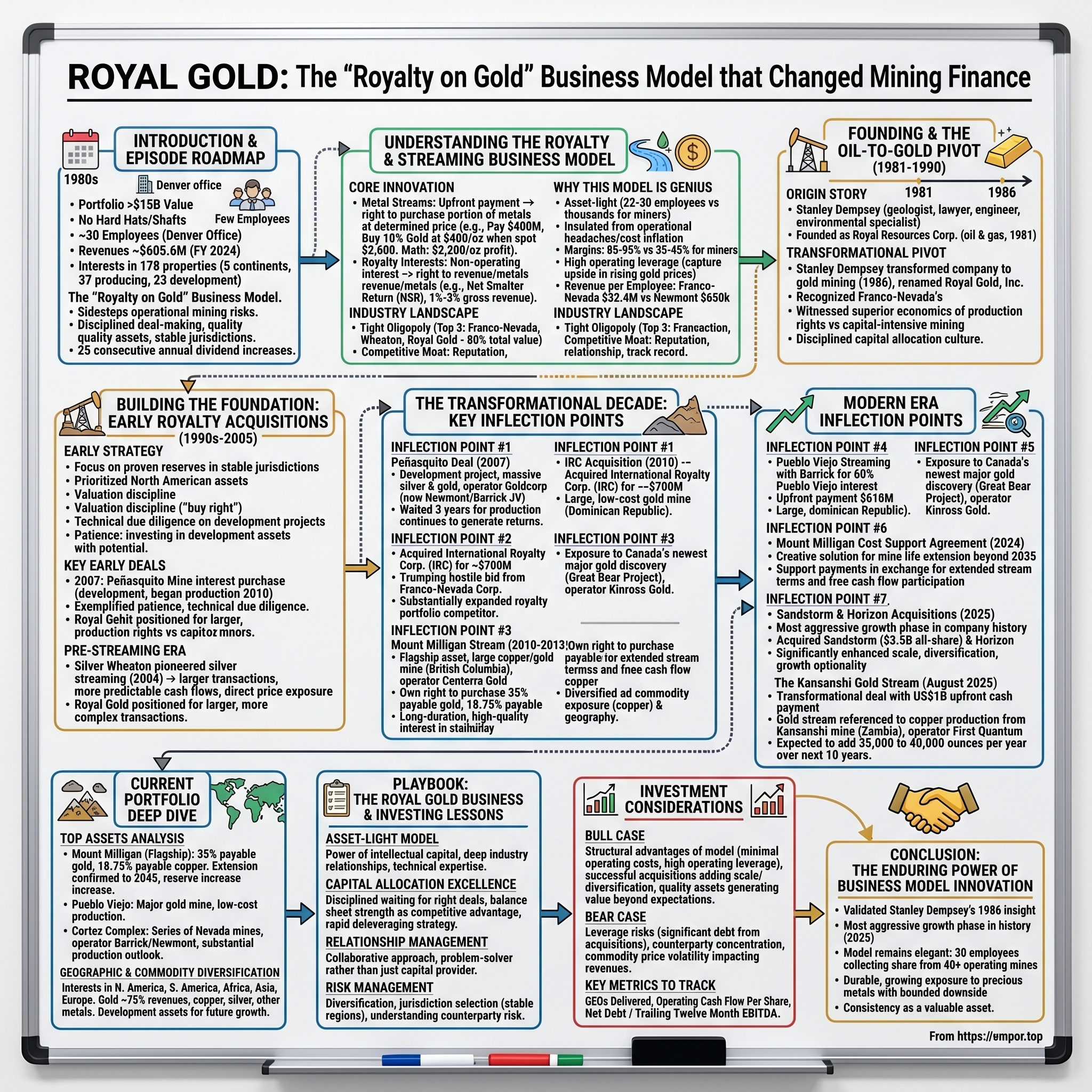

Picture a Denver office building where roughly 30 employees manage a portfolio worth over $15 billion. No hard hats. No mine shafts. No unions to negotiate with. Just a small team of dealmakers, analysts, and relationship managers quietly collecting checks from gold mines scattered across five continents.

This is Royal Gold, a company that has mastered perhaps the most elegant business model in the entire commodities sector—and yet remains remarkably unknown outside professional mining investment circles.

The company achieved revenues of approximately $605.6 million for the fiscal year ended June 30, 2024, operating primarily through a specialized royalty and streaming model that sidesteps many direct operational mining risks. Their global footprint includes interests in 178 properties on five continents, including 37 producing mines and 23 development stage projects.

The central puzzle of Royal Gold is deceptively simple: How do you build a $15+ billion enterprise with a workforce smaller than most restaurants? The answer lies in one of the most brilliant applications of financial engineering to natural resources ever devised.

The industry remains very consolidated, with the top three players—Wheaton Precious Metals, Franco-Nevada Corporation, and Royal Gold—representing approximately 80 percent of the total value of streaming-and-royalty contracts as defined by gold equivalent ounces. Royal Gold has carved out its position as the third member of this exclusive triumvirate through four decades of disciplined deal-making, strategic acquisitions, and a relentless focus on quality assets in stable jurisdictions.

"Royal Gold's consistent history of returning capital to shareholders is unmatched in the precious metals sector, and paying a growing and sustainable dividend has remained a core strategic objective since we declared our first dividend in 2000," noted Bill Heissenbuttel, President and CEO. The company recently announced its 25th consecutive annual dividend increase—raising the annual payout to $1.90 per share for 2026.

The themes that make Royal Gold a compelling study extend far beyond precious metals. This is a story about business model innovation—taking a concept from oil and gas and applying it to gold with transformative results. It's about capital allocation mastery—the discipline to say "no" to hundreds of deals in order to say "yes" to the right ones. It's about the investor's dilemma in commodities—how to capture the upside of rising gold prices without being crushed by operational complexity. And ultimately, it's about creating asymmetric returns with bounded downside.

II. Understanding the Royalty & Streaming Business Model

The Core Innovation

Before understanding Royal Gold's story, investors must first grasp the mechanics of an industry that remains opaque to most market participants.

Metal streams are purchase agreements that provide, in exchange for an upfront deposit payment, the right to purchase all or a portion of one or more metals produced, at a price determined for the life of the transaction. In practice, a streaming company might pay $400 million upfront to a mining company, then purchase 10% of gold production at $400 per ounce when the spot price trades at $2,600. The math is devastatingly simple: every ounce yields $2,200 in immediate profit.

Royalty interests involve non-operating interests in mining projects that provide the right to revenue or metals produced from the project. The most common structure is a Net Smelter Return (NSR) royalty, typically ranging from 1% to 3% of a mine's gross revenue. While royalties usually apply to a very small portion of production, generally only up to 3% of all extracted minerals, streams routinely apply to 10-30% of a mine's production.

Consider the difference through concrete examples. A streaming company provides capital and then specifies a price relative to the spot price to purchase the gold that the mining company produces. If the deal was for 50% of the spot price, then the streaming company can realize quite a nice profit margin by paying $600 per ounce for gold when the spot price is $1,200 per ounce.

Why This Model is Genius

The royalty business model represents a fundamental improvement over traditional mining operations. While miners grapple with operational risks, labor disputes, permitting delays, and relentless cost inflation, royalty companies operate with remarkable simplicity and efficiency. Franco-Nevada employs roughly 50 people compared to Newmont's 25,000+ workforce, yet generates comparable returns with far less complexity. This asset-light structure translates into gross margins of 85-95% versus the 35-45% margins typical of traditional miners.

The operating leverage in a rising gold price environment is particularly striking. When gold increases by $100/oz, traditional miners might see margin improvements of 5-10% as their fixed costs are diluted by higher revenues. Royalty companies, with their minimal operating expenses and fixed-price purchasing agreements, can experience margin expansion of 15-25% or more from the same price movement. They capture the full upside of commodity price appreciation while remaining insulated from the operational headaches that consistently plague mining companies.

Perhaps the most distinctive feature of royalty companies is their extraordinary margin structure. At scale, royalty businesses can achieve operating margins of approximately 90% compared to around 30% for traditional miners.

The revenue-per-employee metric tells the story most vividly. For example, the world's biggest R&S company, Franco-Nevada, had only 40 employees as of the end of 2021, while its revenue was nearly USD 1.3 billion. This amounts to USD 32.4 million per employee. For comparison, the world's biggest gold miner, Newmont Corporation, had 14,400 employees and revenues of USD 12.2 billion, or roughly USD 850,000 per employee.

Royal Gold operates with even greater efficiency—approximately 30 employees managing hundreds of millions in annual revenue.

The Industry Landscape

Royalty ownership in the mining industry is generally agreed to have originated with Franco-Nevada in the mid-1980s. The mining company's first royalty investment in 1986 involved spending half the corporate treasury to acquire 4 percent of the revenues from a mine in Nevada owned by Western State Minerals. Following this initial transaction, Franco-Nevada went on to purchase royalties in various other commodities, further developing the mining sector's royalty business model.

The arrival of the precious-metals streaming business model is often attributed to Wheaton River: while seeking to raise funds in 2004 to expand its core business of gold mining, the company conceived the idea of streaming silver by-product from the San Dimas gold mine in Mexico to a new subsidiary company, Silver Wheaton. In the world's first streaming agreement, Silver Wheaton purchased yet-to-be-produced silver in return for an up-front payment and additional payments.

Since the inception in the 1980s and early 2000s of the mining royalty and streaming sectors, respectively, these alternative forms of financing have grown steadily from $2.1 billion in 2010 to more than $15 billion in 2019. Indeed, the acceleration over the past half-decade has taken place in an environment in which raising capital has been challenging within both the public-debt and public-equity markets.

The industry today remains a tight oligopoly. New players have emerged in the past decade in the streaming-and-royalty sector, including Triple Flag in 2016, Nomad Royalty in 2019, and Deterra Royalties in 2020. Yet breaking into the top tier requires not just capital, but decades of relationship-building and execution track record that cannot be easily replicated.

For investors, understanding this landscape reveals why Royal Gold's position—built over 40 years—represents genuine competitive advantage. The moat isn't patents or technology. It's institutional knowledge, operator relationships, and a reputation for being a reliable partner when mining companies need capital.

III. Founding & The Oil-to-Gold Pivot (1981-1990)

The Origin Story

Stanley Dempsey was not an obvious candidate to revolutionize mining finance. Born in La Porte, Indiana in 1939, raised in Indianapolis, he found his calling through an unexpected path—the Indianapolis Public Library, where his mother would leave him while she worked as a telephone operator during World War II.

Dempsey came to the Colorado School of Mines in the fall of 1956, beginning a career that would span decades of mining industry evolution. He began his career as an independent mining operator and went to work as an engineer for Climax Molybdenum Company in 1960. He then took time off to attend law school.

The combination proved transformative. Dempsey became a geologist, lawyer, executive, and entrepreneur. He was at the forefront of developing the mining industry's legal and policy responses to environmental regulation during the early period, and became Director of Environmental Affairs for AMAX, Inc., the first position of its kind in the industry.

In the early 1980s, he served as Vice President for the worldwide operations of AMAX. After a brief stint at a law firm, Dempsey co-founded a merchant bank called the Denver Mining Finance Company. In later years, he founded one of the first and most successful mineral royalty firms, Royal Gold, Inc.

The story began in 1981, as Royal Resources Corporation, an oil and gas exploration and production company. The company was founded by Stanley Dempsey on January 5, 1981 and is headquartered in Denver, CO.

The Transformational Pivot

The mid-1980s represented a pivotal moment for the nascent company. Dempsey practiced law in the Denver office of the Washington-based law firm Arnold and Porter in the mid-1980s. He then founded the gold mining firm, Royal Gold, Inc.

In the 1980s, the company was named Royal Resources, Inc., and was an oil-exploration company. In 1986, H. Stanley Dempsey, a board member of the public company, transformed the company into a gold mining company and renamed the company Royal Gold, Inc.

What drove this transformation? Dempsey witnessed Franco-Nevada's groundbreaking 1986 royalty deal and recognized something profound: the fundamental economics of owning production rights were far superior to the capital-intensive, operationally risky business of actual mining.

Dempsey served as Royal Gold's chief executive officer through 2006, as its executive chairman through 2008, and its non-executive chairman through 2014. Dempsey was inducted into the National Mining Hall of Fame in 2016.

His tenure of over three decades shaped Royal Gold's culture of disciplined capital allocation and relationship-focused dealmaking. Unlike many founders who resist adapting their approach, Dempsey proved willing to evolve the business model as opportunities emerged—from pure royalties to hybrid stream structures to corporate acquisitions.

Context: The Birth of the Royalty Model

The mid-1980s gold environment created unique opportunities. Following the end of the gold standard in 1971 and the subsequent price spikes of 1980, gold markets entered a volatile period. Traditional mining companies struggled with the boom-bust nature of commodity cycles, and innovative financing structures began emerging as alternatives.

The most fundamental transformation was the move away from the capital-intensive and risky business of mineral exploration and production in the mid-1980s. Embracing the royalty model, starting with the Sleeper Mine, allowed the company to gain exposure to gold production with significantly lower overhead and operational risk. This strategic pivot defined its future success.

Dempsey's unique background—engineer, lawyer, environmental specialist, and corporate executive—gave him the multidisciplinary perspective needed to structure royalty deals that worked for both parties. He understood mining operations from the inside, could draft complex legal agreements, and had spent years navigating the regulatory environment. Few founders could match this combination of technical, legal, and business expertise.

The early years required patience and persistence. Building a royalty portfolio from scratch meant negotiating one deal at a time, often with skeptical mining companies unfamiliar with the concept. But each successful deal created a reference point for the next, and Royal Gold's reputation gradually accumulated.

IV. Building the Foundation: Early Royalty Acquisitions (1990s-2005)

The Early Strategy

The 1990s represented Royal Gold's formative period—a time of patient portfolio construction that would lay the groundwork for exponential growth in the following decade.

The company's strategy centered on several principles that remain core to its approach today. First, focus on proven reserves in stable jurisdictions. Political risk in mining can be catastrophic—a nationalization, regulatory change, or community conflict can render a royalty worthless overnight. Royal Gold prioritized North American assets and carefully vetted international opportunities.

Second, the discipline of "buying right" in royalty deals. Unlike streams, which require significant upfront capital, royalties could often be acquired through smaller investments or as part of property transactions. The key was valuation discipline—ensuring that the price paid would generate attractive returns even under conservative assumptions about production and metal prices.

Third, building credibility with mining operators. The royalty business is fundamentally relationship-driven. Mining companies have options when they need capital—equity, debt, joint ventures, asset sales. Royalty and streaming companies win deals through reputation, speed of execution, and flexibility in structuring arrangements. Every deal completed successfully created another reference customer.

Fourth, embracing the advantages of being small and nimble. Major streaming companies like Franco-Nevada could compete for billion-dollar deals, but smaller transactions weren't worth their attention. Royal Gold found opportunities in this middle market—deals too large for individuals but too small for giants.

Key Early Deals

In 2007, Royal Gold purchased an interest in the Peñasquito mine which did not begin producing until 2010. This deal exemplified a crucial strategic principle: patience. Development-stage projects carry higher risk—mines can be delayed, underperform expectations, or fail entirely. But they also offer more attractive valuations than producing assets.

The Peñasquito investment demonstrated Royal Gold's ability to conduct technical due diligence on complex projects and structure deals that compensated for development risk. When the mine finally reached production three years later, Royal Gold began receiving royalty payments that would continue for decades.

This pattern—investing in quality development assets with patient capital—would become a hallmark of Royal Gold's approach. The company wasn't just buying income streams; it was buying optionality on world-class deposits operated by capable mining companies.

The Pre-Streaming Era

While Royal Gold built its royalty portfolio, the streaming concept was evolving elsewhere in the industry. The arrival of the precious-metals streaming business model is often attributed to Wheaton River: while seeking to raise funds in 2004 to expand its core business of gold mining, the company conceived the idea of streaming silver by-product from the San Dimas gold mine in Mexico to a new subsidiary company, Silver Wheaton. In the world's first streaming agreement, Silver Wheaton purchased yet-to-be-produced silver in return for an up-front payment and additional payments on delivery.

This innovation would prove transformative for the entire sector. Streaming offered several advantages over traditional royalties: larger transaction sizes, more predictable cash flows, and direct exposure to metal price appreciation. Royal Gold observed this evolution and began positioning itself to participate.

The company's early 2000s represented a period of strategic preparation. The royalty portfolio was generating steady income, the balance sheet was strengthening, and management was building the technical and financial capabilities needed for larger, more complex transactions.

What Royal Gold recognized—and what would drive its explosive growth in the next decade—was that the streaming and royalty market was about to enter a new phase. Mining companies emerging from the post-2000 commodity downturn would need significant capital to develop massive new projects. Traditional financing sources were becoming more constrained. And the success of Franco-Nevada and Silver Wheaton was creating institutional investor demand for royalty/streaming exposure.

The table was set for Royal Gold's transformational decade.

V. The Transformational Decade: Key Inflection Points (2007-2015)

Inflection Point #1: The Peñasquito Deal (2007)

In 2007, Royal Gold purchased an interest in the Peñasquito mine which did not begin producing until 2010.

The Peñasquito deal exemplified everything Royal Gold had learned in its first two decades. Located in Mexico's Zacatecas state, Peñasquito would become one of the world's largest silver mines and a major gold producer. But in 2007, it was still a development project—massive, complex, and requiring billions in capital to bring to production.

Royal Gold's investment thesis was straightforward: Goldcorp (the operator) had the technical capability and financial resources to execute. The geology was exceptional. The jurisdictional risk was manageable. And the valuation—a development-stage asset trading at a significant discount to its potential production value—was attractive.

The art of buying into development-stage projects requires a different skill set than acquiring producing royalties. Technical due diligence must assess not just what exists underground, but what will actually be extracted and processed. Management capability matters more—a great deposit can fail with poor execution. And patience is essential—development timelines regularly extend beyond initial projections.

Royal Gold waited three years for Peñasquito to reach production. When it did, the company began receiving royalty payments on one of the world's premier precious metals assets. The initial investment generated returns for over a decade, demonstrating how patience combined with rigorous analysis creates asymmetric outcomes.

Inflection Point #2: The IRC Acquisition & Franco-Nevada Bidding War (2010)

2010 was the year the company experienced the most growth with over a billion of the $1.86 billion in assets added during the year.

The transformational moment came in early 2010 with the acquisition of International Royalty Corporation (IRC). In February 2010, Royal Gold completed the acquisition of another royalty company, IRC, which has claims in Chile (Pascua Lama) and Canada (Voisey's Bay). International Royalty Company was quick to accept the $702 million deal from Royal Gold after Franco-Nevada attempted a hostile $640 million takeover.

The IRC saga revealed the intensifying competition within the streaming and royalty sector. Franco-Nevada Corporation had commenced an unsolicited offer on December 14, 2009 to purchase all of the outstanding common shares of IRC for $6.75 in cash. Following Franco-Nevada's offer, Royal Gold and its wholly owned subsidiary entered into an arrangement agreement with IRC on December 17, 2009.

Royal Gold Inc. said it had signed an arrangement agreement to acquire International Royalty Corp., trumping a rival bid from gold-focused royalty company Franco-Nevada Corp. Under terms of the agreement, Royal Gold offered either $7.45 cash or 0.1385 of a share for IRC, valuing the company at about $749 million. IRC said it had determined the Royal Gold offer to be a "superior proposal" and one that was fair to shareholders.

Royal Gold completed its acquisition on February 22, 2010 of all of the outstanding common shares of IRC, a global mineral royalty company, for a combination of cash and share consideration valued at approximately $700 million.

The strategic importance of IRC extended beyond its asset portfolio. IRC held 85 royalties including an effective 2.7% NSR on the Voisey's Bay mine, a sliding scale NSR on the Chilean portion of the Pascua-Lama project, a 1.5% NSR on the Las Cruces project and a 1.5% NSR on approximately 3.0 million acres of gold lands in Western Australia.

The 2010 acquisition of International Royalty Corporation substantially expanded the royalty portfolio, adding diversification and scale, including the Voisey's Bay royalty. The cost was approximately $700 million.

This deal transformed Royal Gold from a mid-sized player into a legitimate competitor in the premier league of streaming and royalty companies. More importantly, it demonstrated management's willingness to compete aggressively when the right opportunity emerged—and their ability to win against larger rivals.

Inflection Point #3: Mount Milligan Stream (2010-2013)

The most consequential transaction of the era was the Mount Milligan stream, which would become Royal Gold's flagship asset.

Mount Milligan is a large-scale, open-pit copper and gold mine in north-central British Columbia operated by Centerra Gold. Royal Gold assembled its interest through multiple transactions, ultimately securing a position that would generate value for decades.

Royal Gold, through its wholly-owned subsidiary RGLD Gold AG, owns the right to purchase 35% of the payable gold and 18.75% of the payable copper produced from Mount Milligan.

The structure of the Mount Milligan stream exemplified sophisticated deal-making. For Mount Milligan, the cash payments under the stream agreement are the lesser of $435 per ounce or the prevailing market price of gold when purchased and 15% of the spot price for copper near the date of metal delivery.

What made Mount Milligan exceptional was the scale of Royal Gold's interest combined with the quality of the asset. Located in mining-friendly Canada, operated by a capable company, with decades of reserve life—the stream represented exactly the kind of long-duration, high-quality interest that defines successful royalty portfolios.

The Post-2010 Scaling Strategy

While gold remains central, deliberate steps were taken to diversify by commodity and geography. Adding copper streams (like Mount Milligan) and royalties on base metals (like Voisey's Bay—nickel, copper, cobalt) reduced dependency on gold price fluctuations. Expanding globally mitigated geopolitical risks associated with any single region. This diversification strategy enhanced the resilience of its revenue streams.

The transformation was remarkable. In just a few years, Royal Gold evolved from a pure royalty company focused primarily on precious metals in North America to a diversified streaming and royalty enterprise with global exposure across multiple commodities. The strategic positioning proved prescient—when gold prices corrected in subsequent years, the copper and base metal exposure provided stabilization.

VI. Modern Era Inflection Points (2015-2025)

Inflection Point #4: Pueblo Viejo Stream (2015)

In August 2015, Royal Gold announced a transaction that would become one of its most valuable interests.

Barrick has signed a gold and silver streaming agreement with RGLD Gold AG, a wholly-owned subsidiary of Royal Gold, for production linked to Barrick's 60 percent interest in the Pueblo Viejo mine. In return, Royal Gold has agreed to make an upfront cash payment of $610 million plus continuing cash payments for gold and silver delivered under the agreement.

Pueblo Viejo is an open-pit mining operation located 100 kilometers northwest of Santo Domingo. It is managed by a joint venture between two of the world's largest gold producers, with Barrick owning 60% and responsible for operations and Goldcorp Inc. owning the remaining 40%. The mine began production in 2013, and is the only primary gold mine in the world with annual production of more than one million ounces of gold (100% basis), at all-in sustaining costs below $700 per ounce.

Under the terms of the agreement, Barrick will sell gold and silver to Royal Gold equivalent to: 7.5 percent of Barrick's interest in the gold produced at Pueblo Viejo until 990,000 ounces of gold have been delivered, and 3.75 percent thereafter. 75 percent of Barrick's interest in the silver produced at Pueblo Viejo until 50 million ounces have been delivered, and 37.5 percent thereafter.

Inflection Point #5: The Great Bear Royalties Acquisition (2022)

"I am pleased to announce the closing of this friendly transaction with Great Bear Royalties Corp.," commented Bill Heissenbuttel, President and CEO of Royal Gold. "The acquisition provides Royal Gold exposure to Canada's newest major gold discovery, the Great Bear Project, and furthers our strategic objective of acquiring quality, long lived assets with excellent operators in favorable jurisdictions."

Under the terms of the Arrangement, Newco paid cash consideration of C$6.65 for each GBR common share for aggregate consideration of approximately C$199.5 million (approximately US$152.2 million).

GBR's sole material asset is a 2.0% net smelter return royalty that covers the entirety of the Great Bear Project in the Red Lake district of Ontario, Canada, indirectly owned and operated by Kinross Gold Corporation. The Royalty includes all metals produced from contiguous claims covering 9,140 hectares and will be registered on title to the relevant claims. Royalty payments will be made quarterly with applicable standard deductions.

The Great Bear acquisition represented strategic optionality—positioning Royal Gold to benefit from what could become a world-class gold district while the project was still in early development stages.

Inflection Point #6: The Mount Milligan Cost Support Agreement (2024)

In February 2024, Royal Gold announced an additional agreement with Centerra to provide cost support to allow an extension of the Mount Milligan mine life beyond 2035 and offer the potential for a future mine life increase.

"We are pleased to see the results of this PFS, which confirms a significant extension to the mine life at Mount Milligan," commented Bill Heissenbuttel, President and CEO of Royal Gold. "Our Cost Support Agreement with Centerra, entered into in early 2024, was designed to help Centerra unlock the potential of the large resource at Mount Milligan and add long term value for each company's stakeholders, which is clearly demonstrated with the results of this study."

Centerra has announced the results of a pre-feasibility study for the Mount Milligan mine in British Columbia that confirms a life of mine extension of approximately 10 years, to 2045, with the potential to increase the process plant throughput by approximately 10% in 2029.

The study reports a substantial 56% increase in gold reserves to 4.4 million ounces and a 52% increase in copper reserves to 1.7 billion pounds, compared to year-end 2024 figures.

Mount Milligan is Royal Gold's largest stream interest and they have recovered over 150% of their advance stream deposit to date. With the mine life expected to continue for another 20 years and the potential for further extensions, Royal Gold has another significant interest on a long-life mine in a stable and mining-friendly jurisdiction.

Royal Gold also holds a life of mine free cash flow interest, payable annually, of 5% of the cumulative free cash flow generated from Mount Milligan after certain thresholds. The FCF Interest will increase to 10% after reaching additional delivery thresholds.

Inflection Point #7: The Transformational Sandstorm & Horizon Acquisitions (2025)

The year 2025 marked Royal Gold's most aggressive growth phase in company history.

Sandstorm Gold Ltd. has entered into a definitive arrangement agreement with Royal Gold Inc., pursuant to which Royal Gold will acquire all of the issued and outstanding common shares of Sandstorm in an all-share transaction with an implied value of approximately $3.5 billion. Sandstorm shareholders will receive 0.0625 of a share of common stock of Royal Gold for each Sandstorm Share held, implying a 21% premium to the 20-day volume-weighted average price.

Concurrent with the Sandstorm Transaction, Royal Gold has entered into a definitive arrangement agreement with Horizon Copper Corp., pursuant to which Royal Gold will acquire all of the issued and outstanding common shares of Horizon Copper in an all-cash transaction valued at approximately $196 million. Horizon Copper shareholders will receive C$2.00 for each Horizon Share held, implying an 85% premium.

Royal Gold announced the closing of the previously announced acquisitions of Sandstorm Gold Ltd. and Horizon Copper Corp., which add significantly to Royal Gold's world-class diversified portfolio of precious metal stream and royalty interests.

The arrangement received overwhelming support, with 98.68% of all shareholder votes and 98.66% of minority shareholder votes in favor, meeting necessary Canadian regulatory requirements.

The Kansanshi Gold Stream (August 2025)

Following the Sandstorm and Horizon announcements, Royal Gold demonstrated its enhanced firepower with another transformational deal.

The effective date of the transaction is August 5, 2025 and Royal Gold expects to receive approximately 12,500 ounces of gold in 2025.

Sandstorm Gold Ltd. acknowledges and supports Royal Gold Inc.'s acquisition of a gold stream on the Kansanshi copper-gold mine for US$1 billion. Royal Gold announced earlier today that the company has entered into a precious metals purchase agreement for gold deliveries referenced to copper production from the Kansanshi copper-gold mine in the North Western Province of Zambia, operated and 80% owned by a subsidiary of First Quantum Minerals Ltd.

Royal Gold is funding the Advance using cash on hand and a draw of $825 million on its $1 billion revolving credit facility. Separately, Royal Gold has notified the members of the credit syndication group of its exercise of the $400 million accordion feature and has received commitments from them for the full $400 million of increased capacity. We anticipate closing on the accordion feature on August 5, 2025, following which $1.4 billion will be available under the revolving credit facility.

"The Kansanshi transaction is an excellent example of a cash-flowing stream on a large, long-life mine with current reserves supporting a 20-year mine life from a first-tier operator. The gold stream is expected to add approximately 35,000 to 40,000 ounces per year over the next 10 years, further enhancing the combined portfolio."

VII. The Current Portfolio Deep Dive

Top Assets Analysis

Mount Milligan (Flagship Asset)

Mount Milligan represents the crown jewel of Royal Gold's portfolio—a large-scale, producing asset in a stable jurisdiction with decades of remaining life.

Royal Gold, through its wholly-owned subsidiary RGLD Gold AG, owns the right to purchase 35% of the payable gold and 18.75% of the payable copper produced from Mount Milligan.

Centerra Gold Inc. reported that the site-wide optimization program continues to progress and it is maintaining 2025 production guidance at the Mount Milligan mine in British Columbia. Centerra expects 2025 gold production to range between 165,000 and 185,000 ounces, and copper production to range between 50 and 60 million pounds.

Material assumptions for 2025 include an average realized gold price at Mount Milligan of $1,712 per ounce after reflecting the streaming arrangement with Royal Gold (35% of Mount Milligan's gold at $435 per ounce). A market copper price of $4.00 per pound and an average realized copper price at Mount Milligan of $3.36 per pound after reflecting the streaming arrangement with Royal Gold (18.75% of Mount Milligan's copper at 15% of the spot price per metric tonne).

The September 2025 pre-feasibility study confirmed the strategic value of Royal Gold's Cost Support Agreement. The pre-feasibility study for the Mount Milligan mine details a significant 10-year mine life extension to 2045. This extends the revenue stream from this key asset for a considerable period. Furthermore, the study reports a substantial 56% increase in gold reserves to 4.4 million ounces and a 52% increase in copper reserves to 1.7 billion pounds.

Pueblo Viejo

Located in the Dominican Republic, Pueblo Viejo is an open-pit gold mine owned by a joint venture between Barrick Gold and Newmont. The mine began production in 2013, and is the only primary gold mine in the world with annual production of more than one million ounces of gold (100% basis), at all-in sustaining costs below $700 per ounce.

According to Barrick, process plant construction has been completed with the focus now on increasing production from the crushing and milling circuits and operational stability and recovery improvements in the flotation circuit.

Cortez Complex

The Cortez Complex, operated by Barrick Gold Corporation and held within the Nevada Gold Mines joint venture, is a series of large, open-pit and underground mines with oxide milling and heap leach processing facilities situated on the Cortez-Battle Mountain trend of Nevada. The operator's 2025 production guidance is 680,000–765,000 ounces of gold with a longer-term outlook of between 750,000–1.1 million ounces annually over the next five years.

Royal Gold owns various royalty interests on the Cortez Complex across producing operations, development projects, and several exploration targets on a large land package. Several of these royalty interests overlap in certain areas, creating multiple effective royalty rates across the Cortez Complex. Royal Gold will hold an additional sliding scale net smelter returns royalty of 2.25% at current metal prices on the Robertson development project acquired through the Sandstorm Transaction.

Geographic & Commodity Diversification

The post-acquisition Royal Gold portfolio represents remarkable diversification. The company now holds interests across North America, South America, Africa, and select operations in Asia and Europe. Gold contributes approximately 75% of revenues, with copper, silver, and other metals providing additional diversification.

Development assets including MARA in Argentina, Hod Maden in Turkey, Platreef in South Africa, and Warintza in Ecuador provide optionality for future growth without requiring additional capital deployment.

VIII. Playbook: The Royal Gold Business & Investing Lessons

The Asset-Light Model

Royal Gold's operating model represents the ultimate expression of asset-light business principles in the natural resources sector.

Royal Gold has only approximately 22-30 employees. This tiny team manages a portfolio generating hundreds of millions in annual revenue and commanding a market capitalization exceeding $15 billion.

The royalty and streaming companies are tremendously efficient, with among the highest revenue-per-employee ratios out of all companies in the world.

The power of intellectual capital over physical capital manifests in every aspect of the business. Deal sourcing requires deep industry relationships and technical expertise. Due diligence demands rigorous geological, engineering, and financial analysis. Structuring transactions requires legal sophistication and creative problem-solving. But once a deal closes, the ongoing work is minimal—monitoring operator performance and collecting payments.

Capital Allocation Excellence

The discipline of waiting for the right deals at the right prices defines Royal Gold's culture. Management has consistently walked away from transactions that didn't meet return thresholds, even when under pressure from investors seeking growth.

As of October 2025, Royal Gold has $1.225 billion drawn on the revolving credit facility, leaving $175 million undrawn and available. We estimate repayment of the outstanding borrowings could occur within two years assuming current metal prices.

Balance sheet strength serves as competitive advantage. When opportunities emerge—whether from distressed mining companies needing capital or corporate transactions creating divestitures—Royal Gold can move quickly and decisively. The Kansanshi acquisition demonstrated this capability: $1 billion deployed within months of announcing the Sandstorm and Horizon deals.

Relationship Management

The streaming and royalty business is fundamentally about relationships. Mining companies have alternatives when seeking capital. They choose partners based on reputation, reliability, and flexibility.

The Mount Milligan Cost Support Agreement exemplifies relationship-driven dealmaking. When Centerra faced challenges extending mine life, Royal Gold structured a creative solution that benefited both parties—additional support payments in exchange for extended stream terms and free cash flow participation.

"Our Cost Support Agreement with Centerra, entered into in early 2024, was designed to help Centerra unlock the potential of the large resource at Mount Milligan and add long term value for each company's stakeholders."

This collaborative approach—being a problem-solver rather than just a capital provider—creates competitive advantage that pure financial engineering cannot replicate.

Risk Management

Diversification across assets, geography, commodity, and operator represents the primary risk management framework. No single mine failure, political disruption, or operator problem can materially impair the overall portfolio.

Jurisdiction selection receives particular attention. Mining operations face complex regulatory environments, and political risk can emerge suddenly. Royal Gold's preference for stable, mining-friendly regions reflects decades of industry experience with the consequences of jurisdictional risk.

Understanding counterparty risk is essential in the streaming model. Even with the benefits of higher margins and consistent earnings, there are still risks with investing in royalties and streams. One of the main risks relates to the structure of the business. To invest in mines, royalties and streaming companies need a large amount of capital. Stream agreements are only as good as the operator's ability to perform—if a mine shuts down, stream revenue stops regardless of contract terms.

IX. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces Analysis

1. Threat of New Entrants: LOW

The streaming and royalty sector presents formidable barriers to entry. Capital requirements are substantial—meaningful portfolios require hundreds of millions in deployment. But capital alone is insufficient; relationship networks built over decades cannot be quickly replicated.

New players have emerged in the past decade in the streaming-and-royalty sector, including Triple Flag in 2016, Nomad Royalty in 2019, and Deterra Royalties in 2020. Yet breaking into the top tier remains extremely difficult—the gap between the "Big Three" and newer entrants is measured in billions of dollars of portfolio value.

Scale economies in due diligence, deal sourcing, and corporate operations favor larger players. A $100 million transaction requires nearly the same analytical effort as a $500 million deal, making larger companies more efficient deployers of capital.

2. Bargaining Power of Suppliers (Mining Companies): MODERATE

Mining companies have alternative financing options: equity issuance, traditional debt, project finance, joint ventures, and asset sales. However, streaming and royalty financing offers unique advantages: non-dilutive (compared to equity), doesn't require collateral (compared to debt), and provides flexible terms suited to mining project economics.

These deals are especially attractive for mining companies for which the streamed product is noncore or a by-product. Different reasons exist for sellers to enter into streaming and royalty contracts, but these are usually related to market capitalization and project development status. In the case of large and midcap miners, the decision to enter into streaming-and-royalty contracts has historically been driven by the need to improve balance-sheet leverage.

Quality miners are selective about partners, but Royal Gold's reputation—built over 40 years—provides access to the best opportunities.

3. Bargaining Power of Buyers: LOW

Royal Gold sells into commodity markets at prevailing prices. No single buyer has negotiating leverage. Gold and precious metals have deep, liquid global markets with transparent pricing.

4. Threat of Substitutes: LOW-MODERATE

Traditional debt and equity financing represent alternatives for miners. However, streaming and royalty offers unique benefits that are difficult to replicate—non-dilutive, asset-specific, and aligned with production rather than fixed payment schedules.

Royalties and streams limit the holder's exposure, in most instances, to exploration, development, operating, sustaining or reclamation expenditures typically associated with an operating interest in a mine. While they have limited operating exposure, royalty and stream holders do however benefit from any resource expansion or upside generated by exploration success, mine life extensions and operational expansions.

5. Industry Rivalry: MODERATE-HIGH

Competition for premium deals is intense among the top players. The top three players—Wheaton Precious Metals, Franco-Nevada Corporation, and Royal Gold—represent approximately 80 percent of the total value of streaming-and-royalty contracts.

However, the growing capital needs of the mining industry create expanding opportunity. Global gold production requires continual replacement of depleting reserves, generating ongoing demand for development capital that streaming and royalty companies can supply.

Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

Fixed costs spread across a massive royalty/stream portfolio create extraordinary operating leverage. Franco-Nevada employs roughly 50 people compared to Newmont's 25,000+ workforce, yet generates comparable returns with far less complexity. Royal Gold's 30 employees managing $15B+ in market value demonstrates extreme capital efficiency.

2. Network Economies: MODERATE

Reputation and relationships create a virtuous cycle: more deals completed successfully → better reputation → access to better deals. Information advantages from an extensive portfolio—understanding which operators perform well, which jurisdictions are truly mining-friendly—compound over time.

3. Counter-Positioning: STRONG

Traditional miners cannot easily replicate the royalty/streaming model. Mining companies are operationally focused; the financing business requires different organizational DNA, different risk frameworks, and different skill sets. Attempting to compete would dilute miner focus on core competencies.

4. Switching Costs: STRONG

Streaming and royalty agreements are perpetual—they last for the life of the mine. Once established, these interests cannot be terminated by the operator. This creates extraordinarily durable revenue streams that compound value over decades.

5. Branding: MODERATE

In a relationship-driven business, reputation functions as brand. Royal Gold's 40-year track record, consistent dividend increases, and collaborative approach with operators create preference among mining company management teams seeking financing partners.

6. Cornered Resource: MODERATE

The best royalty and streaming opportunities are finite. World-class gold deposits in stable jurisdictions with capable operators represent scarce resources. Early movers who secured interests on these assets enjoy advantages that cannot be replicated.

7. Process Power: MODERATE

Deal origination, due diligence, structuring, and relationship management represent accumulated process expertise. While individual capabilities can be hired, the institutional knowledge embedded in Royal Gold's organization—understanding of hundreds of mining assets, relationships across the industry—constitutes difficult-to-replicate process power.

X. Investment Considerations

Bull Case

The streaming and royalty model offers structural advantages that compound over time. Rising gold prices flow almost entirely to the bottom line given minimal operating costs. Royalty companies provide nearly direct exposure to gold price movements through percentage-based royalties on production revenue. When gold prices rise 10%, royalty revenue typically increases by a similar percentage, creating a high correlation to the underlying commodity. This direct correlation contrasts with traditional miners, who often see margin compression from rising input costs during gold bull markets.

The Sandstorm and Horizon acquisitions significantly enhance Royal Gold's scale, diversification, and growth optionality. High-quality, long-life stream and royalty assets, with built-in optionality, increasing proven and probable attributable gold equivalent ounces to 18 times the expected 2025 GEO sales, and remaining accretive to consensus NAV on a per share basis.

"We grew our business significantly in 2025 and our dividend increase for 2026 reflects a prudent balance between our commitment to increasing the dividend, executing on new investment opportunities and allocating capital towards debt repayment. Royal Gold's dividend history is unique amongst our peers, and we remain the only precious metals company in the S&P High Yield Dividend Aristocrats Index."

The Mount Milligan pre-feasibility study validation—a 10-year mine life extension with significant reserve increases—demonstrates how quality assets can generate value far beyond initial expectations.

Bear Case

As of October 2025, Royal Gold has $1.225 billion drawn on its revolving credit facility—the most leveraged the company has been in its history. While management expresses confidence in rapid deleveraging, integration risks and potential commodity price volatility create near-term uncertainty.

Counterparty concentration represents structural risk. Mount Milligan, Pueblo Viejo, and Cortez together represent significant portfolio exposure. Operational challenges at any of these assets could materially impact financial results.

Spot prices and mine production obviously impact the profitability of royalty and streaming companies. If the spot prices fall, royalty companies will receive less revenue, and streaming companies can only sell their metals at a lower price. In the case of mine delays, both types of companies will be impacted by a delay of gold flow.

The Franco-Nevada Cobre Panama situation serves as a cautionary example for the entire sector. Franco-Nevada had more than US$1 billion invested in First Quantum's Cobre Panama mine before it was shuttered by the Panamanian government following protests at the end of 2023. The mine brought in US$223.3 million for Franco-Nevada in 2022 and represented nearly a quarter of its precious metal income. While it fared better than First Quantum, the royalty company's share price took a significant hit.

Valuation multiples in the streaming and royalty sector have expanded significantly. Competition for quality deals has intensified, potentially compressing returns on new deployments.

Key Metrics to Track

For long-term fundamental investors monitoring Royal Gold, three KPIs matter most:

1. Gold Equivalent Ounces (GEOs) Delivered The fundamental driver of revenue. Track quarterly sales volumes against guidance, watching for production disruptions at key assets and portfolio additions from new deals.

2. Operating Cash Flow Per Share The purest measure of value creation. Unlike earnings, which can be distorted by non-cash charges, operating cash flow reflects actual capital available for dividends, debt repayment, and new investments.

3. Net Debt / Trailing Twelve Month EBITDA Given the significant leverage taken on through the 2025 acquisitions, the pace of deleveraging will be critical. Management's credibility depends on demonstrating the "two-year repayment" thesis through actual debt reduction.

XI. Conclusion: The Enduring Power of Business Model Innovation

Stanley Dempsey's 1986 pivot from oil exploration to gold royalties wasn't just a strategic repositioning—it was the recognition that the best way to profit from mining isn't always to do the mining yourself.

Four decades later, Royal Gold stands as validation of that insight. "We paid our first dividend in 2000 and have increased it every year since 2001, and to date we have paid out total dividends of approximately $1 billion."

The company's transformation in 2025—absorbing Sandstorm and Horizon while deploying $1 billion for the Kansanshi stream—represents the most aggressive growth phase in its history. Whether this expansion creates or destroys value will depend on execution, gold prices, and the performance of newly acquired assets.

What remains constant is the fundamental elegance of the business model. While traditional miners battle geological surprises, labor disputes, equipment failures, and cost inflation, Royal Gold's 30 employees simply collect their share of production from 40+ operating mines worldwide.

The streaming and royalty model won't make investors rich overnight—it lacks the volatility and potential for explosive gains that speculative mining investments offer. But for those seeking durable, growing exposure to precious metals with bounded downside risk, Royal Gold's four-decade track record speaks for itself.

"Royal Gold's consistent history of returning capital to shareholders is unmatched in the precious metals sector."

In a sector defined by boom-bust cycles, operational chaos, and shareholder value destruction, that consistency may be the most valuable asset of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube