Air Products and Chemicals (APD): The Industrial Gas Giant's Transformation Story

I. Introduction & Episode Roadmap

Picture this: A $65 billion market cap industrial giant that most people have never heard of, yet touches nearly every aspect of modern life—from the oxygen in hospital rooms to the hydrogen fueling rockets to space. Air Products and Chemicals isn't just another industrial conglomerate; it's the world's largest supplier of hydrogen and helium, and it's betting $15 billion that it knows something about the future of energy that others don't.

But here's the fascinating question that drives our story today: How did a Depression-era entrepreneur with only a high school education, who sold his life insurance policy for $6,000 in startup capital, lay the foundation for what would become the clean hydrogen leader of the 21st century? And perhaps more importantly—is the company's massive bet on green hydrogen genius or hubris?

This is a story about innovation born from necessity, about how changing a business model can topple industry giants, and about the audacity of betting an entire company's future on a technology that barely exists at commercial scale today. It's about Leonard Pool's "tiger pack" of aggressive engineers who revolutionized industrial gases, about mobile oxygen generators that helped win World War II, and about a company that's writing off $3.1 billion in projects while simultaneously doubling down on hydrogen infrastructure.

Today we'll explore three transformative themes that define Air Products: First, the power of on-site production—a simple idea that disrupted an entire industry. Second, how wartime necessity created peacetime opportunity. And third, why a company that spent decades diversifying into chemicals is now laser-focused on becoming the backbone of the hydrogen economy.

By the end of this episode, you'll understand why activist investors are circling, why the board is searching for a new CEO, and whether Air Products' bet on hydrogen represents the trade of the century or a cautionary tale about first-mover disadvantage. Let's dive in.

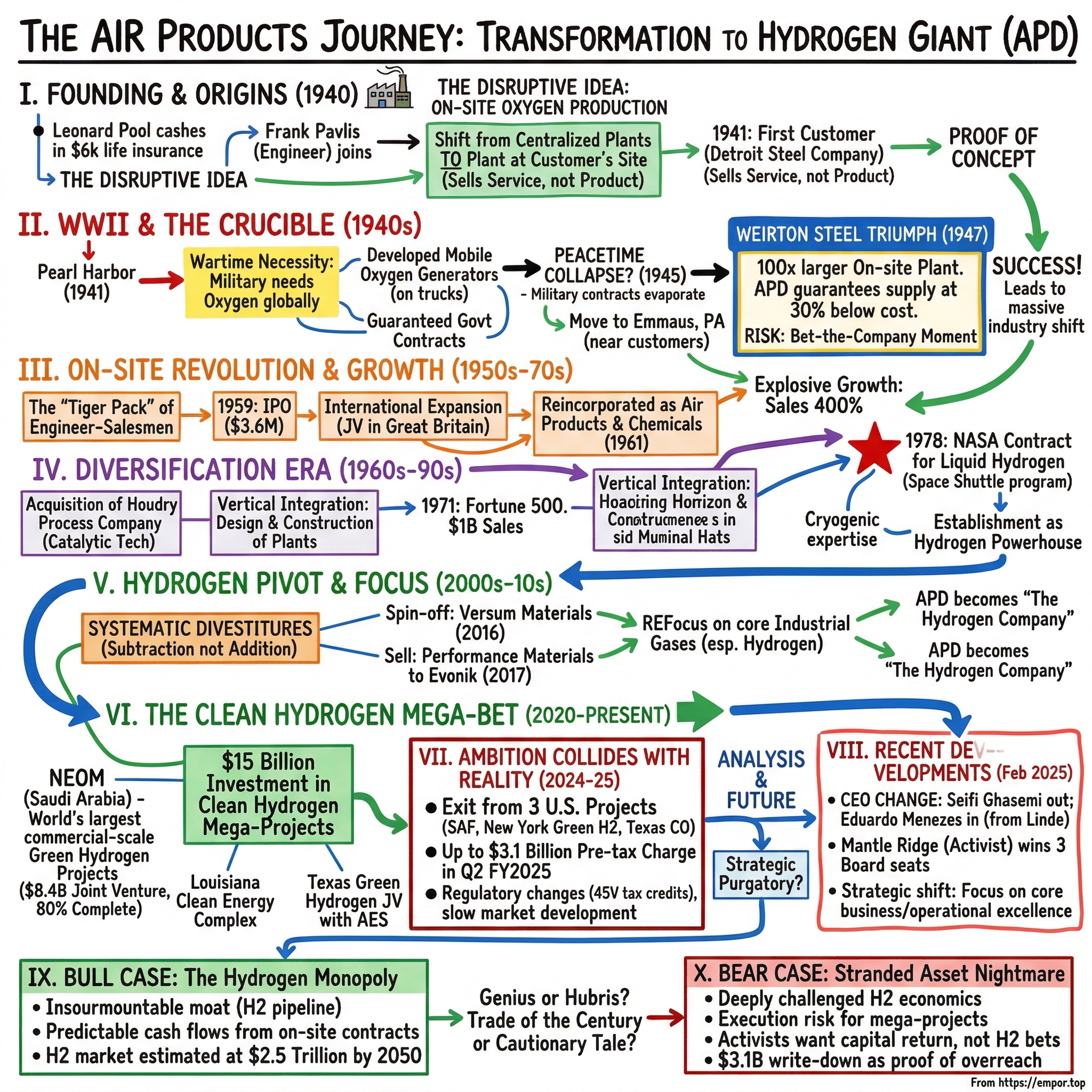

II. The Leonard Pool Origin Story & Founding Context

Detroit, 1940. The country is still climbing out of the Great Depression, and Leonard Parker Pool—a man with only a high school diploma but an engineer's mind—makes a decision that would seem insane to most people. He quits his stable job as district manager at Compressed Industrial Gases, one of the established players in the oxygen business. But Pool doesn't just quit; he cashes out his life insurance policy for $6,000 and convinces a young engineer named Frank Pavlis to join him in what must have seemed like a quixotic venture.

To understand the audacity of Pool's move, you need to understand the oxygen industry of 1940. The market was dominated by behemoths who had perfected a seemingly unassailable business model: they produced oxygen at massive centralized plants, compressed it into heavy steel cylinders that weighed five times more than the gas they contained, and shipped these cylinders across the country on trucks and trains. It was capital-intensive, logistically complex, and riddled with inefficiency—but it worked, and the incumbents liked it that way.

Pool saw something different. While working at Compressed Industrial Gases, he'd noticed a fundamental absurdity: steel companies and other heavy users of oxygen were paying enormous sums not for the gas itself, but for the privilege of shipping heavy cylinders back and forth. What if, he wondered, you could eliminate the cylinders entirely? What if you built the oxygen plant right next to the customer?

This wasn't just a logistics optimization—it was a complete reimagining of the industrial gas business model. Instead of selling a product, Pool would sell a service. Instead of managing thousands of cylinders, he'd manage a handful of on-site plants. Instead of competing on distribution networks, he'd compete on engineering excellence and customer relationships.

The idea was revolutionary, but Pool faced a chicken-and-egg problem that would have defeated most entrepreneurs: no customer wanted to be first to try an unproven technology from an unknown company, and Pool couldn't build a demonstration plant without a customer. This is where Pool's background as a salesman became crucial. He didn't just pitch the cost savings; he sold a vision of partnership, of shared risk and reward, of a new way of doing business.

In 1941, Pool found his first believer: a small Detroit steel company willing to take a chance on his leased oxygen generator. The contract wasn't massive—this wasn't U.S. Steel or Bethlehem—but it proved the concept. The on-site generator worked, costs dropped dramatically, and suddenly Pool had something more valuable than capital: he had proof.

What's remarkable about this founding story isn't just Pool's vision or determination—it's his timing. Within months of securing that first customer, the United States would enter World War II, and suddenly the ability to produce oxygen anywhere, anytime, wouldn't just be convenient—it would be critical to the war effort. Pool couldn't have known Pearl Harbor was coming, but his innovation was about to intersect with history in a way that would transform his tiny startup into an industrial powerhouse.

III. World War II: The Crucible Moment

December 7, 1941. As the smoke cleared from Pearl Harbor, America's industrial machine shifted into overdrive. For Leonard Pool and his fledgling Air Products, the timing was extraordinary—and existential. The military didn't just need oxygen; they needed it in places where no industrial gas company had ever delivered it before: on remote Pacific islands, in mobile field hospitals, aboard aircraft carriers, at high-altitude bomber bases.

Pool's response would define not just his company but an entire approach to innovation under pressure. Working around the clock with Frank Pavlis and a small team of engineers, he developed something that seemed impossible: a mobile oxygen generator that could be loaded onto a truck, shipped anywhere, and produce medical-grade oxygen on demand. Think about the engineering challenge here—these machines had to survive ocean transport, operate in jungle humidity and desert heat, and be simple enough for military personnel to maintain without specialized training.

The mobile generators were an engineering marvel, but they were also a business education for Pool. The military contracts brought in revenue that dwarfed anything from the commercial sector—Air Products went from a startup struggling to make payroll to a company with guaranteed government contracts and steady cash flow. Pool used this windfall wisely, plowing profits back into R&D and hiring what he would later call his "tiger pack"—aggressive young engineers who combined technical brilliance with evangelical sales fervor.

But here's where the story takes a turn that would have destroyed most companies. When Japan surrendered in August 1945, Air Products' military contracts evaporated almost overnight. The company went from boom to potential bust in a matter of weeks. Pool later recalled this as the darkest period in the company's history—darker even than the startup days, because now he had employees to pay, leases to honor, and creditors to satisfy.

Pool's response revealed the kind of leader he was. Instead of retreating or downsizing, he went on offense. He packed up the company—literally—and moved from Detroit to Emmaus, Pennsylvania, positioning Air Products closer to the industrial heart of the Northeast. The Lehigh Valley location wasn't chosen randomly; it put Pool within driving distance of the steel mills of Pittsburgh, the chemical plants of New Jersey, and the refineries of Philadelphia.

Then came the masterstroke: Pool's "door-stepping" technique. In an era when industrial sales meant scheduled appointments and formal presentations, Pool would simply show up at a potential customer's plant and refuse to leave until he got a meeting. His most famous door-stepping campaign targeted Weirton Steel in West Virginia. Pool checked into a local motel and visited the plant every single day for weeks. Security knew him by name. Secretaries felt sorry for him. Engineers thought he was crazy.

But Pool understood something fundamental about industrial sales: the person who says no today might say yes tomorrow if you can just stay in the conversation. After three weeks of daily visits, Weirton's management finally agreed to meet with him—partly out of admiration for his persistence, partly to make him go away. Pool walked into that meeting with blueprints for an on-site oxygen plant 100 times larger than anything Air Products had built before.

The Weirton executives were skeptical. This wasn't just a big generator—it was a fundamental bet on a new way of producing oxygen. If it failed, Weirton's steel production would grind to a halt. Pool's response was brilliant in its simplicity: he offered to build the plant at Air Products' expense and guarantee supply at a price 30% below what Weirton was currently paying. If the plant failed, Air Products would eat the cost and supply cylinder oxygen at the contracted price.

It was a bet-the-company moment. The Weirton plant would cost more than Air Products' entire net worth. A failure wouldn't just mean losing money; it would mean bankruptcy. But Pool understood that without a signature win, Air Products would remain a marginal player forever. He needed a reference customer that would make the entire industry take notice.

The Weirton plant came online in 1947 and exceeded every performance metric. The success reverberated through the steel industry—if Weirton could cut oxygen costs by 30%, every steel company needed to evaluate on-site generation. Within 18 months, Air Products had signed contracts with three more major steel producers. The company that had nearly collapsed when the war ended was now the fastest-growing player in industrial gases, and Pool's tiger pack of engineer-salesmen became legends in the industry for their technical knowledge and relentless pursuit of deals.

IV. The On-Site Revolution & Early Growth (1945-1970s)

The Weirton triumph wasn't just a big contract—it was a proof of concept that would reshape an entire industry. By 1950, Air Products had perfected what would become its signature move: approaching massive industrial gas users with a simple proposition—why pay to ship heavy cylinders when we can build the plant in your backyard?

But scaling this model required more than just engineering prowess. Pool needed capital, talent, and a systematic approach to growth. This is where his concept of the "tiger pack" became central to Air Products' culture. These weren't your typical industrial salesmen in gray flannel suits. Pool recruited young engineers, often straight from college, and taught them to sell by understanding the customer's process better than the customer did. A tiger pack member visiting a steel mill wouldn't just quote prices; they'd analyze the entire oxygen consumption pattern, identify inefficiencies, and design solutions that saved money in ways the customer hadn't even considered.

The tiger pack operated with an almost missionary zeal. One legendary story involves a young engineer who camped outside a chemical plant in Louisiana for two weeks, studying their hydrogen consumption patterns by counting delivery trucks and timing production cycles. When he finally got his meeting, he presented an analysis so detailed that the plant manager accused him of industrial espionage. The engineer's response? "I didn't need to spy. Your inefficiencies are visible from the parking lot."

By the late 1950s, Air Products had grown large enough to build a proper headquarters, choosing Trexlertown, Pennsylvania—a location that reflected Pool's philosophy of being close to customers but not too comfortable. The building itself was designed to embody the company's engineering culture: functional, efficient, with laboratories and meeting rooms where customers could see innovations being developed in real-time.

The international expansion began almost by accident. In 1957, a British steel company, frustrated with their local oxygen suppliers, reached out to Air Products after hearing about the Weirton success. Pool's response was characteristic: instead of trying to export from America, he partnered with the Butterley Company to create Air Products (Great Britain), Ltd. This joint venture model—combining Air Products' technology with local knowledge and relationships—would become the template for international growth.

Going public in 1959 marked a turning point. Pool had resisted outside capital for years, preferring to maintain control and reinvest profits. But the opportunity pipeline had grown beyond what internal funding could support. The IPO raised $3.6 million—not a huge sum even by 1959 standards, but enough to fund simultaneous expansion into multiple markets.

The reincorporation as Air Products & Chemicals in 1961 signaled a strategic shift that would define the next four decades. Pool recognized that many of their industrial gas customers also needed specialty chemicals, and the same on-site production model could work for other materials. But more importantly, he saw that understanding chemical processes made Air Products better at gas separation and purification—capabilities that would prove invaluable as industries demanded higher purity gases.

Through the 1960s, the numbers told a story of explosive growth: sales rose 400% while earnings grew 500%. But behind these numbers was a more important transformation. Air Products had evolved from a disruptor to an institution. The company that had started by challenging the establishment had become the establishment—or at least part of it. By 1970, no major steel mill or chemical plant would make oxygen procurement decisions without considering on-site generation, and Air Products had fundamentally changed how industrial gases were bought and sold.

Yet Pool, now in his 60s, remained restless. He'd conquered industrial gases, but he saw bigger opportunities in chemicals, in new markets, and in technologies that didn't yet exist. The scrappy startup had grown up, but it hadn't lost its appetite for risk. The next phase would test whether Air Products could maintain its entrepreneurial edge while operating at industrial scale.

V. The Chemical Diversification Era (1960s-1990s)

The acquisition of Houdry Process Company in 1962 marked Air Products' bold entry into chemicals, but to understand why this mattered, you need to understand what Houdry represented. This wasn't just buying a chemical company—it was acquiring one of the most innovative catalytic technology platforms in the world. Eugene Houdry had invented the catalytic cracking process that revolutionized petroleum refining, and his company's expertise in catalysis would prove synergistic with Air Products' gas separation technologies in ways that wouldn't be fully apparent for years.

The Houdry acquisition came with an unexpected bonus: Catalytic Construction Company, a subsidiary that designed and built chemical plants. Suddenly, Air Products wasn't just supplying gases and chemicals; they could design and construct entire production facilities. This vertical integration gave them a unique competitive advantage—they could offer customers complete solutions, from plant design to ongoing supply.

Pool's strategy in chemicals mirrored his approach to gases: find inefficiencies in how things were bought and sold, then restructure the entire business model. When Air Products acquired Escambia Chemical Corporation in Florida in 1969, they didn't just buy a commodity chemical producer. They transformed it into a specialty chemical powerhouse by applying their on-site model to polymer emulsions—materials critical for paints, coatings, and adhesives.

The 1970s brought a massive strategic coup with the acquisition of Airco's chemicals and plastics business. This wasn't a distressed asset purchase—Airco was divesting to focus on other areas, and Air Products paid a fair price. But what they got was remarkable: overnight, they became a major player in polymer emulsions, with established customer relationships and proven technology. Over the next four decades, this business would quietly generate nearly $1 billion in annual revenues, providing the steady cash flow that would fund more ambitious ventures.

By 1978, Air Products had crossed a symbolic threshold: inclusion in the Fortune 500, with $1 billion in sales. But Pool, now approaching 80, faced a succession challenge. He'd built a company culture around his personal dynamism and relationship-driven dealmaking. The question was whether Air Products could maintain its entrepreneurial edge as it transitioned to professional management.

The answer came from an unexpected source: NASA. In 1978, Air Products won a 12-year, $287 million contract to supply liquid hydrogen for the Space Shuttle program. This wasn't their first hydrogen project, but the scale and precision required were unprecedented. NASA didn't just need hydrogen; they needed it at purities measured in parts per billion, in quantities that could fuel rockets, delivered with 100% reliability. The Space Shuttle program transformed Air Products from a chemical conglomerate into a hydrogen powerhouse. The company's relationship with NASA began in 1957 and continued through the Apollo 11 moon landing and Mars missions, but the Shuttle program represented something entirely different in scale and precision. The engineering challenges were staggering—delivering hydrogen at temperatures of minus 423 degrees Fahrenheit, maintaining purities that made semiconductor-grade materials look dirty by comparison, and doing it all with zero tolerance for failure.

The success with NASA had ripple effects throughout Air Products' business. The cryogenic expertise developed for rocket fuel found applications in semiconductor manufacturing, medical gases, and food freezing. The quality systems demanded by NASA became the standard across all operations. Most importantly, Air Products established itself as the go-to supplier for anyone needing large-scale hydrogen infrastructure—a reputation that would prove invaluable decades later.

By 1992, the transformation was complete: revenues reached $3 billion, the company employed 14,600 people across twenty-nine countries, and Air Products had successfully evolved from Pool's scrappy startup into a diversified industrial giant. The chemical businesses provided steady cash flow, the gas business continued to grow through on-site installations, and the hydrogen expertise gained from NASA positioned them for opportunities that didn't yet exist.

But success bred complexity. Air Products was now competing on multiple fronts—against focused gas companies like Praxair and Air Liquide, against chemical specialists like Dow and BASF, and against emerging players in specialty materials. The question for the 1990s would be whether this diversification was a strength or a distraction.

VI. The Hydrogen Pivot & Strategic Focus (2000s-2010s)

The late 1990s marked a crucial inflection point for Air Products—one that would define its trajectory for the next quarter-century. After decades of empire-building through acquisitions, the company made a counterintuitive decision in 1996: it would systematically divest most of its environmental and energy systems businesses and refocus on its core competencies in industrial gases and select chemicals. This wasn't retreat; it was strategic concentration.

By fiscal year 2001, this refocusing had pushed revenues to $5.7 billion with 17,800 employees—impressive growth, but the real story was happening beneath the surface. Air Products was quietly becoming the hydrogen company, though few outside the industry recognized it at the time. While competitors diversified into healthcare gases or specialty chemicals, Air Products doubled down on hydrogen infrastructure, seeing what others missed: the coming transformation of energy markets.

The strategic masterstroke came through a series of hydrogen acquisitions that seemed expensive at the time but would prove prescient. In 2020, Air Products paid $530 million to PBF Energy for five steam methane reformer (SMR) hydrogen plants with a combined capacity of nearly 300 million standard cubic feet per day. The plants—located in Torrance and Martinez, California, and Delaware City, Delaware—weren't just production assets; they were beachheads in key refining markets where hydrogen demand was set to explode as environmental regulations tightened.

But the real transformation came through subtraction, not addition. In September 2015, Air Products announced it would spin off its Materials Technologies business into a standalone company called Versum Materials. This wasn't a fire sale of an underperforming asset—Materials Technologies was profitable and growing. But CEO Seifi Ghasemi understood something fundamental: in the coming energy transition, focus would matter more than scale.

The Versum spinoff, completed in October 2016, was executed flawlessly. Shareholders received one share of Versum for every five shares of Air Products they owned, and the new company immediately commanded a $3 billion market cap. Within two years, Merck would acquire Versum for $5.8 billion—a validation of both the business's value and Air Products' timing in separating it.

The divestiture momentum continued in January 2017 when Air Products sold its Performance Materials division to Evonik. This business had generated nearly $1 billion in annual revenues and was the U.S. market leader in polymer emulsions—exactly the kind of steady, profitable business that most companies would never sell. But Ghasemi saw it as a distraction from the main event: the hydrogen economy.

With these divestitures, Air Products had transformed from a diversified industrial conglomerate into a focused industrial gas company with an overwhelming emphasis on hydrogen. The company now operated the world's longest hydrogen pipeline system along the U.S. Gulf Coast, had hands-on experience with over 250 hydrogen fueling station projects in 20 countries, and its technologies were being used in over 1.5 million fueling operations annually.

The strategic logic was compelling: hydrogen was the only molecule that could serve both today's industrial markets and tomorrow's clean energy needs. While producing hydrogen from natural gas (gray hydrogen) wasn't environmentally revolutionary, the infrastructure, expertise, and customer relationships built around gray hydrogen would be invaluable when green hydrogen—produced from renewable electricity and water—became economically viable.

By 2019, Air Products wasn't just talking about the hydrogen economy; they were building it. The company had methodically positioned itself at the intersection of industrial necessity and environmental ambition. Traditional customers in refining and chemicals still needed hydrogen for their operations, but new markets were emerging: fuel cell vehicles, clean steel production, sustainable aviation fuels, and green ammonia for fertilizer and shipping.

The financial markets initially punished this focus. Diversified competitors like Linde (formed from the merger of Praxair and Linde AG) commanded higher multiples, and activists questioned why Air Products was shrinking rather than growing through acquisition. But Ghasemi held firm, arguing that the company's deep expertise in hydrogen would ultimately be more valuable than broad exposure to commodity industrial gases.

As the 2010s drew to a close, Air Products had completed its transformation from Leonard Pool's on-site production innovator to the world's largest hydrogen supplier. The company had shed billions in non-core assets, concentrated its engineering talent on hydrogen technologies, and built relationships with every major hydrogen consumer on the planet. The stage was set for the biggest bet in the company's history—one that would either establish Air Products as the infrastructure backbone of the clean energy transition or serve as a cautionary tale about the dangers of being too early to a market that might never materialize.

VII. The Clean Hydrogen Mega-Bet (2020-Present)

In 2020, as the world grappled with a pandemic and energy markets crashed, Seifi Ghasemi made a declaration that sent shockwaves through the industrial gas industry: Air Products would invest at least $15 billion in clean hydrogen mega-projects by 2027. This wasn't incremental investment or optionality hedging—it was an all-in bet that hydrogen would become the backbone of the global energy transition, with Air Products positioned as its primary infrastructure provider.

The crown jewel of this strategy is the NEOM Green Hydrogen Project in Saudi Arabia—an $8.4 billion venture that represents the world's largest commercial-scale green hydrogen production facility. The numbers are staggering: 4 gigawatts of renewable power from solar and wind, producing 600 tonnes of green hydrogen per day through electrolysis, converted into 1.2 million tonnes of green ammonia annually for global export. Construction has reached 80% completion across the green hydrogen facility, wind garden, solar farm and transmission grid, with milestone equipment being received and installed.

The NEOM project exemplifies Air Products' approach to the hydrogen economy: go big, partner strategically, and lock in the entire value chain. NEOM Green Hydrogen Company achieved financial close with 23 local, regional, and international banks at a total investment value of USD 8.4 billion. Air Products isn't just a technology provider here—they're an equal joint venture partner alongside NEOM and ACWA Power, they're the exclusive off-taker for all the hydrogen produced, and they'll handle global distribution and marketing.

But NEOM is just one piece of a much larger puzzle. In Texas, Air Products announced a $4 billion joint venture with AES to build what would be the largest green hydrogen production facility in the United States, featuring approximately 1.4 gigawatts of wind and solar power generation capable of producing over 200 metric tons per day of green hydrogen. The Louisiana Clean Energy Complex represents another multi-billion dollar commitment, positioning Air Products at the heart of America's industrial hydrogen infrastructure.

The scale of these investments has no precedent in the industrial gas industry. To put it in perspective, $15 billion is more than Air Products' entire annual revenue. It's a bet that would make even the most aggressive venture capitalists pause. And it's happening at a time when the economics of green hydrogen remain challenging—production costs are still multiples higher than gray hydrogen from natural gas, and the end-use markets for clean hydrogen are still developing. Yet cracks in the strategy emerged in 2024 and crystallized in early 2025. Following a review by its newly-elected Board and CEO, Air Products announced its exit from three U.S. projects and expects to record a pre-tax charge up to $3.1 billion in Q2 fiscal 2025 for asset write-downs and contract terminations. The cancelled projects tell a story of ambition colliding with reality:

The World Energy Sustainable Aviation Fuel expansion in California—a $2 billion investment—was terminated due to challenging commercial aspects. The Massena green hydrogen facility in New York, planned to produce 35 metric tons per day, was cancelled due to regulatory changes affecting hydroelectric power eligibility for tax credits and slow market development. A Texas carbon monoxide project was terminated due to unfavorable economics.

These aren't just project cancellations; they're admissions that the hydrogen economy isn't developing as quickly or predictably as Air Products anticipated. The Massena cancellation is particularly telling—the project depended on qualifying for the Clean Hydrogen Production Tax Credit (45V), but regulatory interpretations made the hydroelectric power source ineligible. This highlights a fundamental risk in the clean hydrogen strategy: dependence on government subsidies and regulations that can change with political winds.

Despite these setbacks, Air Products isn't abandoning its hydrogen vision—it's recalibrating. The NEOM project has reached 80% completion across the green hydrogen facility, wind garden, solar farm and transmission grid, with milestone equipment being received and installed. The company maintains that green ammonia production will commence by the end of 2026, and CEO Seifi Ghasemi has indicated that demand exceeds the facility's production capacity.

The Louisiana Clean Energy Complex continues to progress toward a 2028 startup, though Air Products is now seeking equity partners for the ammonia loop and carbon dioxide sequestration components—a sign that even the company's flagship U.S. project needs risk-sharing to proceed.

What we're witnessing is a company caught between two worlds. The traditional industrial gas business remains profitable and growing, but it's not exciting enough to justify premium valuations. The hydrogen economy promises transformational growth, but it's arriving slower than expected, with more complexity and risk than initially modeled. Air Products has committed too much to retreat, but the path forward is narrower and more treacherous than the broad hydrogen highway they envisioned just a few years ago.

The $3.1 billion write-down represents more than just financial pain—it's a recalibration of expectations, a tacit acknowledgment that being first in clean hydrogen might mean being too early. Yet with $15 billion committed and projects like NEOM nearing completion, Air Products has crossed the Rubicon. The question now isn't whether they believe in the hydrogen economy, but whether they can survive long enough to see it materialize.

VIII. Modern Operations & Financial Profile

Today's Air Products operates at a scale that would have been unimaginable to Leonard Pool: fiscal 2024 sales of $12.1 billion from operations in approximately 50 countries and has a current market capitalization of over $65 billion. The company employs approximately 23,000 passionate, talented and committed employees across a global footprint that spans from Pennsylvania to Saudi Arabia, from Louisiana to Singapore.

The business model has evolved but retains Pool's core insight about customer intimacy. Air Products operates through three primary mechanisms: on-site plants built adjacent to major customers with long-term contracts, merchant liquid and gas delivery to smaller customers, and equipment sales for customers who prefer to own their gas generation assets. Each model serves different customer needs, but all are built on the foundation of technical excellence and reliability that Pool established.

The product portfolio reads like a periodic table of industrial necessity. Atmospheric gases—oxygen, nitrogen, and argon—form the bread and butter of the business, separated from air using massive cryogenic distillation columns that can cost hundreds of millions of dollars each. Hydrogen, increasingly the company's strategic focus, is produced through steam methane reforming for traditional applications and, soon, through electrolysis for green applications. Specialty gases for semiconductor manufacturing, where impurities are measured in parts per trillion, command premium prices and require extraordinary quality control.

Financial performance in fiscal 2024 reflected both the strength of the core business and the challenges of transition. GAAP EPS from continuing operations of $17.24, up 67 percent from the prior year, though this included a one-time gain from the LNG business divestiture. GAAP net income of $3.9 billion was up 65 percent, demonstrating the cash-generative nature of the industrial gas business even as the company pours billions into hydrogen infrastructure.

The adjusted numbers tell a more nuanced story. In fiscal 2024, Air Products reported adjusted EPS of $12.43, up 8%, and adjusted EBITDA of $5.0 billion, a 7% increase. These are solid results, but not spectacular—reflecting the mature nature of the traditional industrial gas business and the drag from investments that haven't yet begun generating returns.

The geographic breakdown reveals interesting dynamics. The Americas remain the largest contributor, generating roughly 45% of sales, with strong positions in refining, chemicals, and metals. Asia, representing about 30% of sales, offers the highest growth potential, particularly in electronics and emerging hydrogen applications. Europe, about 25% of sales, faces the most interesting near-term opportunities as the continent aggressively pursues decarbonization.

But the most telling aspect of Air Products' modern operations is what's not visible in current financials: the massive capital deployment underway. The company spent approximately $5 billion in capital expenditures in fiscal 2024, with the vast majority going toward hydrogen infrastructure that won't generate meaningful revenue for years. This is either visionary investment or dangerous overreach, depending on your view of the hydrogen economy's timeline.

The operational excellence metrics are impressive—Air Products maintains industry-leading safety performance, with recordable incident rates well below industrial averages. Plant reliability exceeds 99% for most facilities, critical when a shutdown can halt a customer's entire production. The company operates the world's longest hydrogen pipeline system along the U.S. Gulf Coast, over 600 miles of infrastructure that connects refineries and chemical plants in a network effect that would be nearly impossible for competitors to replicate.

Yet beneath these operational achievements lies a fundamental tension. Air Products is simultaneously trying to be the most efficient operator of traditional industrial gas assets while pioneering unproven green hydrogen technologies. It's maintaining focus on cost reduction and margin improvement while making the largest capital investments in its history. It's serving customers who need reliable, low-cost industrial gases today while betting those same customers will pay premium prices for green hydrogen tomorrow.

The recent divestiture of the LNG business for $1.6 billion exemplifies this strategic focus. LNG was profitable and growing, but it didn't fit the hydrogen-centric vision. Similarly, the Materials Technologies spinoff as Versum wasn't about jettisoning underperformers—it was about concentrating resources and management attention on what Air Products believes is a generational opportunity in hydrogen.

The company's modern operations represent a fascinating dichotomy: a business that generates tremendous cash flow from mature, stable operations, using that cash to fund speculative investments in technologies that may revolutionize energy markets—or may prove to be ahead of their time. It's a high-stakes transformation that will either position Air Products as the critical infrastructure provider for the clean energy transition or leave it overinvested in assets the market doesn't yet need.

IX. Playbook: Business & Investing Lessons

The Air Products story offers a masterclass in industrial strategy, revealing timeless principles about disruption, capital allocation, and the challenges of technological transition. These lessons resonate far beyond industrial gases, offering insights for any business facing fundamental market shifts.

The Power of Business Model Innovation Over Product Innovation

Leonard Pool didn't invent a better way to make oxygen—he invented a better way to sell it. The on-site production model was a business model innovation that trumped any technological advantage the incumbents possessed. This mirrors what Amazon did to retail or what Netflix did to video rental: the disruption came not from a superior product but from a fundamentally different approach to delivering value. For investors, this highlights an crucial insight: look for companies that are rethinking the entire value chain, not just improving individual components.

The on-site model created multiple competitive advantages that compound over time. First, it locked in customers with 15-20 year contracts, providing predictable cash flows that could support further investment. Second, it raised switching costs to prohibitive levels—once a steel mill reconfigured its operations around on-site oxygen, changing suppliers meant rebuilding infrastructure. Third, it transformed Air Products from a vendor into a partner, embedding them in customers' operational decisions. This is the industrial equivalent of software's SaaS model, decades before Silicon Valley coined the term.

Capital Intensity as Both Moat and Trap

Air Products' business requires enormous capital investment—a single air separation unit can cost $100-500 million. This creates a powerful moat once assets are deployed, but it also creates a trap. The company must commit capital years before generating returns, making bet-the-company decisions based on uncertain future demand. The current hydrogen investments exemplify this dynamic: $15 billion committed based on a vision of the hydrogen economy that may take decades to fully materialize.

The lesson for investors is nuanced. Capital intensity can create unassailable competitive positions—try competing with Air Products' Gulf Coast hydrogen pipeline network—but it also amplifies the cost of strategic mistakes. Unlike software companies that can pivot quickly, Air Products' mistakes are literally set in concrete and steel. The $3.1 billion write-down on cancelled projects isn't just an accounting entry; it represents years of misdirected effort and capital that could have been deployed elsewhere.

The Innovator's Dilemma in Reverse

Clay Christensen's famous framework describes how incumbents fail to respond to disruptive technologies. Air Products presents the opposite challenge: an incumbent trying to disrupt itself by moving into adjacent markets with uncertain economics. The company is essentially betting that its expertise in gray hydrogen (produced from natural gas) will translate into dominance in green hydrogen (produced from renewable electricity). But these are fundamentally different businesses with different economics, customers, and competitive dynamics. The parallel to Kodak is instructive. Kodak invented digital photography but couldn't cannibalize its film business fast enough. Air Products faces the inverse challenge: it's trying to cannibalize its gray hydrogen business before green hydrogen economics make sense, betting that being early will translate into lasting advantage. This requires not just vision but exceptional execution and deep pockets to survive the valley of death between investment and returns.

The Activist Investor Paradox

The Mantle Ridge situation perfectly illustrates the tensions in Air Products' strategy. Mantle Ridge LP, holding approximately $1.3 billion stake (about 1.8% ownership), successfully won three board seats at Air Products in January 2025, with shareholders voting to elect Paul Hilal, Dennis Reilley and Andrew Evans to the company's board. This victory came despite Mantle Ridge's relatively small stake, suggesting broader shareholder frustration with the hydrogen strategy.

The activist's critique is straightforward: Air Products has strayed from its core competency, making speculative bets on unproven technologies while the traditional business underperforms. They're not wrong—the stock has lagged the S&P 500, and the $3.1 billion write-down validates concerns about capital allocation. But Mantle Ridge's alternative vision—essentially, run the traditional business for cash and return capital to shareholders—ignores the existential question: what happens to Air Products if the hydrogen economy does materialize and they're not positioned to capture it?

This creates a fascinating governance dilemma. The activists want predictable returns from a mature business. Management wants transformational growth from emerging technologies. Both are rational positions, but they lead to fundamentally different strategies. The board must now navigate between harvesting today's cash flows and investing in tomorrow's opportunities—a balance that has defeated many industrial companies facing technological transitions.

First-Mover Advantage vs. First-Mover Disadvantage

Air Products' hydrogen strategy assumes first-mover advantage, but history suggests the relationship between timing and success is more complex. Consider wind power: the early movers in the 1980s mostly failed, while companies that entered in the 2000s with better technology and economics dominated. Or solar panels: First Solar and SunPower were early leaders but have been eclipsed by Chinese manufacturers who entered later with massive scale.

The NEOM project exemplifies both the promise and peril of being first. At 80% completion, it's too late to abandon without massive losses, but it's still unclear whether there will be sufficient demand for green ammonia at prices that justify the investment. Air Products is essentially building infrastructure for a market that doesn't fully exist, hoping that "if you build it, they will come."

The Capital Allocation Masterclass (or Cautionary Tale)

Air Products' capital allocation over the past decade reads like a case study in strategic focus—or strategic tunnel vision, depending on your perspective. The systematic divestiture of non-core businesses (Versum, Performance Materials, LNG) freed up capital and management attention for hydrogen. This is textbook portfolio management: exit businesses where you lack competitive advantage to fund areas where you can dominate.

But the magnitude of the hydrogen bet raises questions about prudent capital allocation. Investing $15 billion when your entire company generates $12 billion in annual revenue is extraordinarily aggressive. It's the industrial equivalent of betting the company on a single product launch—except the product (green hydrogen at scale) doesn't yet exist commercially.

Leadership Transitions and Strategic Continuity

The ongoing CEO succession, with the board expecting to announce a new President by March 31, 2025, adds another layer of complexity. Seifi Ghasemi, at 80 years old, has been both architect and evangelist for the hydrogen strategy. His successor will inherit massive ongoing projects that can't easily be abandoned but may not align with their vision for the company.

This succession challenge is common in companies undergoing fundamental transitions. The leader who conceives the bold strategy rarely sees it through to completion. The question for Air Products is whether the next CEO will have the conviction to continue the hydrogen bet or the courage to acknowledge sunk costs and pivot. Either path requires exceptional leadership, but they demand different skills and temperaments.

The playbook Air Products is writing—whether ultimately successful or cautionary—offers timeless lessons about industrial strategy, capital allocation, and the challenges of technological transition. The company is attempting something genuinely difficult: transforming from a mature, profitable industrial gas company into the infrastructure backbone of a new energy economy. Success would validate everything from Pool's original entrepreneurial vision to Ghasemi's hydrogen bet. Failure would serve as a warning about the perils of betting too much, too soon, on technologies that may arrive too late.

X. Analysis & Bear vs. Bull Case

The Air Products investment thesis presents one of the most fascinating dichotomies in industrial markets today. It's simultaneously a stable, cash-generative industrial gas leader and a speculative bet on the hydrogen economy—a Schrödinger's cat of industrial investing where the company exists in two states until the hydrogen market either materializes or doesn't.

Bull Case: The Hydrogen Infrastructure Monopoly

The bulls see Air Products as criminally undervalued, trading at a discount to inferior competitors while positioned to dominate the next great energy transition. Start with the fundamentals: this is the world's largest supplier of hydrogen and helium, with infrastructure that would cost tens of billions to replicate. The Gulf Coast hydrogen pipeline network alone represents an insurmountable moat—you literally cannot compete in Gulf Coast hydrogen without either using Air Products' infrastructure or spending decades building your own.

The industrial gas business model remains exceptional. On-site contracts typically run 15-20 years with take-or-pay provisions and price escalators. Customer switching costs are astronomical—retooling a refinery or chemical plant to work with a different gas supplier can cost hundreds of millions and require months of downtime. This creates predictable, inflation-protected cash flows that can support aggressive investment in new technologies.

The hydrogen opportunity is measured in trillions, not billions. McKinsey estimates the hydrogen economy could be worth $2.5 trillion by 2050. Even capturing a small fraction of this market would transform Air Products into one of the world's most valuable industrial companies. And unlike speculative hydrogen startups, Air Products has real assets, real customers, and real expertise in handling hydrogen at scale.

The NEOM project, despite its massive scale, is substantially de-risked. At 80% completion with green ammonia production expected to commence at the end of 2026, the project has already secured offtake interest that exceeds production capacity. This isn't speculative development—it's infrastructure with committed customers in a region desperately seeking to diversify from oil.

The valuation disconnect is striking. Air Products trades at roughly 20x forward earnings while pure-play renewable energy companies with no profits trade at astronomical valuations. If the market valued Air Products' hydrogen option value appropriately, the stock could easily trade 50% higher. The recent board additions from Mantle Ridge, despite the acrimony, bring fresh perspectives and may accelerate value realization.

Bear Case: The Stranded Asset Nightmare

The bears see a company destroying shareholder value by abandoning a perfectly good business to chase hydrogen dreams that may never materialize. The $3.1 billion write-down isn't just an accounting entry—it's proof that management has been making bad bets with shareholder capital. And this may be just the beginning; the remaining hydrogen projects could face similar fates if the market doesn't develop as expected.

The hydrogen economics remain deeply challenged. Green hydrogen costs 3-5x more than gray hydrogen from natural gas. Yes, costs will decline with scale, but so will natural gas prices as fracking technology improves. The economic crossover point keeps moving further into the future. Meanwhile, Air Products is spending billions on infrastructure for a product that customers can't afford to buy.

Competition is intensifying from every direction. Linde, the industry leader with a $220 billion market cap, has the scale to outinvest Air Products. Regional players in Asia and the Middle East are building their own hydrogen infrastructure with government support. Tech companies and startups are developing alternative technologies that could obsolete traditional hydrogen production. Air Products risks being the Blockbuster of industrial gases—dominant in the old model but irrelevant in the new one.

The execution risk is enormous. Air Products is simultaneously building the world's largest green hydrogen facilities, attempting to commercialize unproven technologies, and navigating complex international partnerships. One major project failure—a technology problem at NEOM, a partner dispute, a regulatory change—could cascade through the entire portfolio. The company has minimal experience managing projects of this scale and complexity.

The governance turmoil suggests deeper problems. The abrupt departure of COO Samir Serhan, the CEO succession uncertainty, and the activist battle all point to a company in strategic disarray. Mantle Ridge's critique—that management is making "large-scale speculative non-core investments" that have "increased shareholder risk and destroyed value"—resonates with many shareholders who've watched the stock underperform while management pursues grand visions.

The Synthesis: Path Dependency and Optionality

The truth likely lies between these extremes. Air Products has made an irreversible strategic choice that will define its next decade. The hydrogen investments are too large to abandon but too uncertain to justify further acceleration. The company finds itself in a strategic purgatory—committed but not yet vindicated.

The key variables to watch are concrete and measurable. First, the NEOM project's commercial performance when it comes online in late 2026 will provide the first real data point on green hydrogen economics at scale. Second, the development of hydrogen tax credits and carbon prices will determine whether green hydrogen can compete with gray. Third, the pace of industrial decarbonization—particularly in steel, chemicals, and refining—will drive demand growth.

The investment case ultimately depends on your time horizon and risk tolerance. For value investors seeking predictable cash flows, Air Products offers a decent but unspectacular opportunity—a quality industrial company trading at a reasonable multiple with sustainable competitive advantages. For growth investors willing to underwrite the hydrogen transition, it's potentially the infrastructure play of the next decade, available at a fraction of the valuation of pure-play hydrogen stocks.

The activist involvement adds another dimension. Mantle Ridge's board seats create pressure for near-term performance improvement, which could mean slower hydrogen investment, higher dividends, or asset sales. This might boost the stock short-term but could sacrifice long-term positioning. The tension between quarterly earnings and decadal transformation will define the investment narrative going forward.

What's clear is that Air Products can't return to its pre-hydrogen strategy. The die is cast, the capital is committed, and the company's future is intertwined with the hydrogen economy's development. Whether that's visionary or foolish won't be clear for years, but the answer will determine whether Air Products becomes the Standard Oil of hydrogen or a cautionary tale about industrial companies trying to be technology pioneers.

XI. Epilogue & "If We Were CEOs"

The boardroom at Air Products' Trexlertown headquarters must feel like a pressure cooker these days. A new CEO will soon inherit a company at the most consequential inflection point in its 85-year history—billions committed to hydrogen infrastructure, activists demanding strategic change, and a workforce wondering whether they're building the future or chasing mirages.

If we were taking the CEO chair at Air Products today, the path forward would require threading an impossibly small needle: maintaining strategic conviction while acknowledging market realities, pushing forward on hydrogen while protecting the core business, and satisfying both growth investors betting on transformation and value investors demanding returns today.

First Priority: Define What Victory Looks Like

The hydrogen strategy lacks clear success metrics. Is Air Products trying to be the largest green hydrogen producer? The most profitable? The technology leader? Without clear goals, every decision becomes a debate. We'd establish concrete milestones: NEOM must achieve 50% capacity utilization within 18 months of startup, with positive EBITDA within 24 months. Louisiana must secure firm offtake agreements for 70% of capacity before breaking ground on phase two. These aren't arbitrary targets—they're proof points that the hydrogen economy is real, not theoretical.

Second Priority: Create Options, Not Obligations

The current strategy is too binary—either the hydrogen economy explodes and Air Products wins big, or it doesn't and shareholders lose billions. We'd restructure projects to create more optionality. Instead of building massive facilities hoping demand materializes, we'd design modular expansions that can scale with demand. Partner with customers to share development risk—if they truly believe in hydrogen, they should co-invest. Create joint ventures for the riskiest projects, maintaining upside while limiting downside.

Third Priority: Bridge the Present and Future

The core industrial gas business funds the hydrogen dreams, but it's being neglected in the strategic narrative. We'd reinvest in the traditional business, particularly in Asia where industrial growth remains robust. Every dollar of improved efficiency in the core business is a dollar available for hydrogen investment. More importantly, industrial gas customers will be the first adopters of clean hydrogen—strengthening these relationships today creates hydrogen customers tomorrow.

The Geographic Opportunity

Air Products is underexposed to Asia relative to competitors. While Linde generates nearly 30% of revenue from Asia-Pacific, Air Products is closer to 20%. Yet Asia represents both the fastest-growing industrial gas markets and the most aggressive hydrogen adoption targets. We'd accelerate Asian expansion through targeted acquisitions and partnerships, particularly in South Korea and Japan where hydrogen strategies are most advanced.

The Technology Question

Air Products is betting primarily on alkaline electrolysis for green hydrogen, but competing technologies like PEM (Proton Exchange Membrane) and SOEC (Solid Oxide Electrolysis) may prove superior. We'd hedge technology bets by partnering with multiple electrolyzer manufacturers, treating Air Products as the systems integrator rather than technology developer. This reduces risk while maintaining flexibility to adopt winning technologies.

The Activist Reality

With Mantle Ridge now holding board seats, confrontation is counterproductive. We'd embrace their push for operational excellence while educating them on hydrogen's long-term potential. Create a hydrogen subsidiary with separate reporting to provide transparency on investments and returns. Establish clear hurdle rates for new projects and commitment to return capital if opportunities don't meet these thresholds. This isn't capitulation—it's pragmatic governance that maintains strategic flexibility while respecting shareholder concerns.

The Succession Solution

The next CEO needs to be a "ambidextrous" leader—someone who can operate today's business while building tomorrow's. This probably means an external hire with experience managing industrial transitions. Think of someone like Jim Fitterling at Dow, who's successfully balanced commodity chemicals with specialty products, or Murray Auchincloss at BP, who's navigating the oil-to-energy transition. The leader needs credibility with both industrial customers and clean energy visionaries.

The Ultimate Question: Is the Bet Too Big?

Leonard Pool bet his life insurance on on-site production. Seifi Ghasemi is betting the company on hydrogen. The difference is timing—Pool's innovation addressed an immediate customer pain point with clear economics. The hydrogen bet assumes customer pain points that don't yet fully exist and economics that require government support.

If we were CEO, we'd acknowledge this reality without abandoning the vision. Slow the pace of investment to match market development. Focus on "no-regret" investments that make sense even if the hydrogen economy develops slowly—like hydrogen for existing industrial uses where green premiums are acceptable. Build the infrastructure backbone but wait for clear demand signals before massive capacity additions.

The Final Reflection

Air Products stands at a crossroads that many industrial companies will face: how to transform for a sustainable future while maintaining current profitability. The company's choices—whether ultimately successful or cautionary—will influence how industrial companies approach the energy transition.

The tragedy would be abandoning the hydrogen vision just before it materializes. The equal tragedy would be destroying a great industrial gas company chasing dreams that never materialize. The path between these outcomes is narrow, requiring exceptional leadership, disciplined capital allocation, and a bit of luck.

In 10 years, Air Products will either be case-studied as the industrial company that successfully navigated the energy transition, or as a warning about the perils of moving too fast into uncertain markets. The next CEO's decisions will determine which case study gets written. The stakes couldn't be higher—not just for Air Products, but for the industrial companies watching and learning from their journey.

XII. Recent News & Developments### **

Leadership Transition Accelerates (February 2025)**

In a dramatic turn of events, Air Products' Board announced the appointment of Eduardo F. Menezes as CEO effective February 7, 2025, succeeding Seifollah ("Seifi") Ghasemi, who is leaving the Company after more than 10 years of dedicated service. This change came less than two weeks after the contentious annual meeting where Mantle Ridge won three board seats.

At his last position, Menezes was the executive vice president (EVP) of Linde plc for Europe, Middle East and Africa, with responsibility for operations in more than 40 countries with over $8 billion in sales and 18,000 employees. Prior to that, Mr. Menezes worked for Praxair in a variety of senior roles, including as EVP accountable for North America. His appointment represents a homecoming of sorts—Menezes brings deep industrial gas expertise from Air Products' main competitor, potentially signaling a return to operational excellence over transformational bets.

The board restructuring continues with Wayne T. Smith named Chairman and Dennis H. Reilley as Vice Chairman. Notably, Reilley was one of Mantle Ridge's nominees, suggesting the activist's influence extends beyond just board seats to strategic direction.

Strategic Pivot Signals New Direction

The $3.1 billion project cancellation announced in February 2025 wasn't just housecleaning—it was a statement about Air Products' future direction under new leadership. The cancelled projects included some of Ghasemi's most ambitious clean energy initiatives, suggesting a more cautious approach to the hydrogen transition.

The company's messaging has notably shifted from "first-mover advantage in clean hydrogen" to "back to basics" and focus on the core industrial gas business. While NEOM and Louisiana continue, the pace of new hydrogen investments will likely slow dramatically under Menezes, who must balance activist demands for near-term returns with the long-term hydrogen opportunity.

Market Reaction and Forward Outlook

Initial market reaction has been positive but cautious. The stock has recovered from its late-2024 lows, but remains well below the peaks reached during peak hydrogen enthusiasm. Investors seem relieved to have clarity on leadership but remain uncertain about strategic direction.

The key questions facing Menezes and the reconstituted board: - How to optimize the traditional industrial gas business while competitors have gained share during Air Products' hydrogen focus - Whether to seek partners or buyers for the massive hydrogen projects already underway - How to rebuild employee morale and customer relationships after months of uncertainty - Whether to accelerate capital returns to shareholders or maintain investment for future growth

The next earnings call will be crucial in setting expectations and outlining the strategic vision under new leadership. Will Air Products double down on operational excellence in traditional markets, or maintain its hydrogen ambitions with better execution? The answer will determine whether this leadership transition marks a return to Air Products' industrial roots or merely a pause in its energy transition journey.

XIII. Resources for Further Learning

Essential Long-Form Reads

-

"The Alchemy of Air" by Thomas Hager - While focused on the Haber-Bosch process for ammonia synthesis, this book provides crucial context for understanding industrial gas technology and its impact on civilization.

-

"The Hydrogen Economy" by Jeremy Rifkin - A visionary but controversial take on hydrogen's potential to reshape global energy systems. Essential reading to understand the bull case for Air Products' strategy.

-

McKinsey's "The Clean Hydrogen Opportunity" (2023 Report) - Comprehensive analysis of hydrogen economics, technology pathways, and market development scenarios through 2050.

-

Harvard Business Review: "The Hard Truth About Innovative Cultures" (2019) - Explains the cultural challenges companies like Air Products face when pivoting from operational excellence to innovation-driven growth.

-

MIT Energy Initiative's "The Future of Hydrogen" (2019) - Technical deep-dive into hydrogen production, storage, and use cases, with realistic assessments of economic viability.

Industry & Historical Context

-

"Good to Great" by Jim Collins - The chapter on Level 5 Leadership provides a framework for understanding the CEO transition challenges at Air Products.

-

Linde plc Annual Reports (2019-2024) - Essential competitive intelligence to understand how the industry leader approaches similar challenges without the same hydrogen concentration.

-

"The Innovator's Dilemma" by Clayton Christensen - The canonical text on why successful companies fail at transitions, directly applicable to Air Products' current situation.

-

IEA's "Global Hydrogen Review 2024" - The definitive source for hydrogen market data, policy developments, and demand projections.

-

Air Products' own "A History of Growth and Innovation" (Company Archives) - The company's official history provides valuable context on past pivots and cultural DNA.

Financial & Investment Analysis

-

Morningstar's Industrial Gas Industry Reports - Excellent comparative analysis of Air Products versus peers, with focus on competitive advantages and moats.

-

"Value Investing: From Graham to Buffett and Beyond" by Bruce Greenwald - Chapter on capital-intensive businesses provides framework for evaluating Air Products' investment strategy.

The story of Air Products is far from over. As Leonard Pool proved with on-site production and Seifi Ghasemi demonstrated with the hydrogen pivot, industrial gas companies can reinvent themselves when technology and markets shift. Whether Eduardo Menezes will write the next transformative chapter or manage a strategic retreat remains to be seen. What's certain is that Air Products will remain a fascinating case study in industrial transformation, capital allocation, and the eternal tension between current profits and future possibilities.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube