Marubeni Corporation: The Ohmi Merchant's 165-Year Journey from Linen to Global Sōgō Shōsha

I. Introduction & Episode Roadmap

The year was 2019, and in the hushed offices of Berkshire Hathaway in Omaha, Nebraska, Warren Buffett was quietly doing something he rarely did: shopping in Japan. Over the course of twelve months, without fanfare or announcement, the Oracle of Omaha accumulated stakes in five Japanese trading companies—conglomerates so unusual, so fundamentally different from anything in the Western business lexicon, that they remain largely unknown to most American investors. When Buffett finally revealed his positions on his 90th birthday in August 2020, the investment world paused.

Berkshire Hathaway raised its holdings in five Japanese trading houses—Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo—to stakes ranging from 8.5% to 9.8%. "We simply looked at their financial records and were amazed at the low prices of their stocks," Buffett later explained. What confounded him wasn't the complexity of these businesses—it was that anyone could pass on such obvious value.

Among the five, Marubeni Corporation stands out as a case study in transformation, resilience, and the unique power of Japanese business philosophy. Marubeni Corporation is a sōgō shōsha (general trading company) headquartered in Otemachi, Chiyoda, Tokyo, Japan. It is one of the largest sogo shosha and has leading market shares in cereal and paper pulp trading as well as a strong electrical and industrial plant business.

The question this deep dive seeks to answer: How did a 15-year-old boy selling linen cloth in rural Japan in 1858 create a company that now spans everything from grain to power plants to aerospace—and why did Warren Buffett bet billions on it?

In the last 12 months, Marubeni had revenue of 54.75 billion and earned 3.85 billion in profits. The current market capitalization of Marubeni is $42.1B. From humble origins as a linen peddler to a global conglomerate with operations in over 60 countries, Marubeni's story encompasses Japanese modernization, wartime consolidation, post-war reconstruction, scandal, near-death experiences, and ultimately, transformation into a company that Warren Buffett considers worthy of holding for the next fifty years.

What follows is that story—from Ohmi merchants to the Buffett stamp of approval.

II. The Sōgō Shōsha Model: Understanding Japan's Unique Trading Houses

Before diving into Marubeni's specific history, understanding what makes Japanese trading houses so fundamentally different from Western companies is essential. The term itself—sōgō shōsha—literally translates to "general trading company," but this translation dramatically undersells the concept.

Sogo shosha (総合商社, sōgō shōsha; or general trading companies) are Japanese wholesale companies that trade in a wide range of products and materials. In addition to acting as intermediaries, sōgō shōsha also engage in logistics, plant development and other services, as well as international resource exploration. Unlike trading companies in other countries, which are generally specialized in certain types of products, sōgō shōsha have extremely diversified business lines, in which respect the business model is unique to Japan.

The phrase "from ramen to rockets" captures the absurd breadth of these companies. A single sōgō shōsha might simultaneously be involved in importing iron ore from Australia, financing a power plant in Southeast Asia, operating convenience stores in Japan, trading grain from the American Midwest, leasing aircraft to airlines, and developing real estate—all while maintaining a textile division dating back a century.

A sogo shosha may control about 10% of Japan's trade, handle a range of 10000 to 20000 products including food, clothing, automobiles and appliances, and have a network of over 200 offices throughout the world.

Why Japan—and Nowhere Else?

Its closure from the outside world for over 200 years meant that trade had to be developed in a very short period of time relative to Europe, where networks could naturally develop over a longer period of time. Japan also lacked effective capital markets to fund companies, and its industrial base was largely composed of cottage industry enterprises that could not market on their own, in contrast to the larger firms prevalent in the West.

When Japan rapidly modernized after the Meiji Restoration of 1868, it needed institutional intermediaries that could do everything: source raw materials, provide financing, coordinate logistics, and navigate foreign markets. The existing family conglomerates known as zaibatsu developed trading arms to serve exactly this purpose.

As Japan modernized, a number of existing family-run conglomerates known as zaibatsu (most notably Mitsubishi and Mitsui) developed captive trading companies to coordinate production, transportation and financing between the various enterprises within the group. A number of smaller and more specialized Japanese firms, particularly in the cotton supply industry, also took on a larger role in acting as intermediaries for foreign trade, initially in importing raw cotton and later in exporting finished products.

The Competitive Moat

The structure of sōgō shōsha can give them advantages in international trade. First, they have extensive risk management capabilities in that they trade in many markets, keep balances in many foreign currencies and can generate captive supply and demand for their own operations. They also have large-scale in-house market information systems which give them economies of scale in pursuing new business opportunities.

This isn't just about trading—it's about owning positions across entire value chains. Utilizing these strengths, general trading companies typically develop businesses centered on two pillars, trade and business investment. Recently, the ratio of business investment has been increasing. Trade is a traditional and basic business for general trading companies. General trading companies build relationships with customers and partners through the sale and mediation of products, as we seek to globally expand sales channels and information networks for diverse products. We also contribute to various transactions around the world by creating added value, such as providing logistics or financial functions.

Relative to these global players, where the Shoshas are really strong is in their relationship with the Japanese buyers. They move large volumes in Japan, and are able to provide better service to Japanese buyers with assets and supply chain that are optimized to serving a single geography. For example, they are highly flexible and responsive to meet the very precise delivery schedules of Japanese manufacturers. Another advantage of Shoshas is their access to low-cost borrowings through strong relationships with their Keiretsu banks. This is often passed down to customers in the form of favorable credit terms - extended payment terms or lower rates than what the customers could obtain on their own.

All five are the biggest "sogo shosha," or trading houses, in Japan that invest across diverse sectors domestically and abroad—"in a manner somewhat similar to Berkshire itself," Buffett said. This comparison is not accidental—like Berkshire, the sōgō shōsha are diversified conglomerates with a focus on cash generation, long-term thinking, and disciplined capital allocation.

For investors, the question becomes: what's the moat? The answer lies in accumulated relationships, information networks, and the institutional role these companies play in Japan's trade-dependent economy. The sogo shosha's responsibilities extend beyond trading because they take active measures to ensure stable levels of supply and demand over long periods. In addition to their ability to make the greatest use of the marketing intelligence network, the sogo shosha work on extremely thin margins, commonly little more than 1.5%. It is therefore necessary for these companies to maintain very high sales volumes and remain focused on longterm business development.

III. The Ohmi Merchant Origins (1858–1918)

Founding & The Itoh Family Legacy

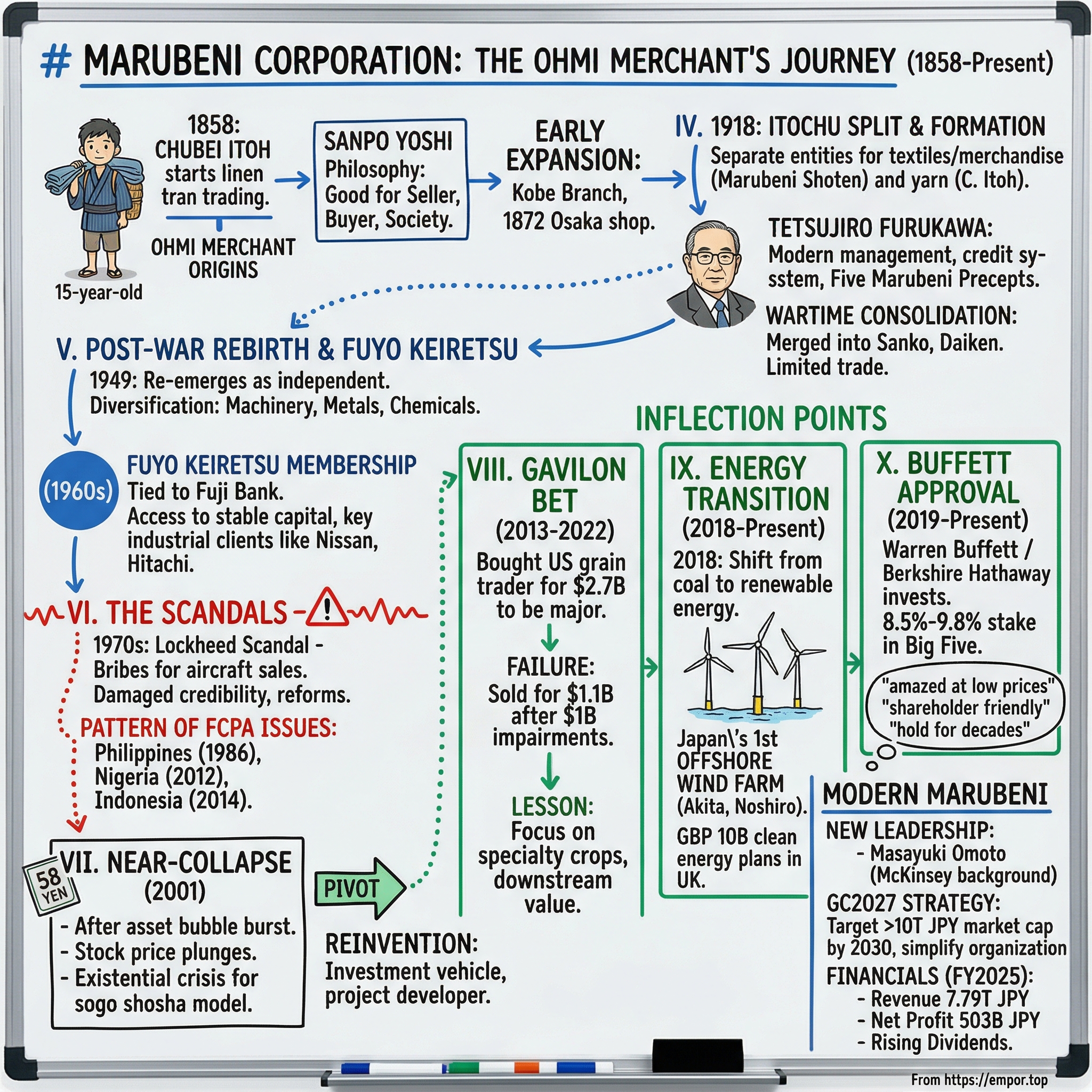

In the spring of 1858, a 15-year-old boy from a small village near Lake Biwa made a decision that would ultimately create two of Japan's largest corporations. Marubeni Corporation traces its origins to May 1858, when Chubei Itoh, born in 1842 in Shiga Prefecture, began an independent linen trading business after leaving his family's operations at age 15.

From an early age he was involved in the family trading business, making his first business trip when he was eleven years old with his brother Manjiro, to sell goods in the town of Goso in Houzuki Village. This was not simply commerce—it was apprenticeship in a centuries-old tradition.

Marubeni considers itself to have been founded in 1858, when Chubei began peddling Ohmi linen, following the mochikudari system. Chubei traveled a regular circuit of market towns, taking orders with a sample book and having the goods delivered by express messenger to a designated inn. The following year he observed the foreign trade activity in Nagasaki and determined to open his own trading business at the earliest opportunity.

The young Itoh's ambition was shaped by witnessing foreign trade in Nagasaki—Japan's sole window to the outside world during the Edo period. While other merchants were content to peddle goods domestically, Itoh understood that Japan's eventual opening to the world would create unprecedented opportunities.

The company's symbolic "Marubeni" name, meaning "full circle" or "red seal," derived from the red circular mark Itoh used on commercial documents to signify completeness and reliability in transactions. The name itself—combining "maru" (circle) and "beni" (red)—would become synonymous with Japanese trading excellence.

The Ohmi Merchant Philosophy

What set Chubei Itoh apart wasn't just business acumen—it was philosophy. He came from the Ohmi region (modern-day Shiga Prefecture), home to a merchant tradition that had developed over centuries a fundamentally different approach to commerce.

The Omi Shonin's principle of Sanpo Yoshi (三方よし), means 'Three-Way Satisfaction'. The word sanpo means "three-way", and the word yoshi means "good". The sanpo-yoshi principle that guided the activities of the Omi merchants was a way of expressing their commitment to simultaneously doing good for themselves (the sellers), the buyers, and the wider community.

One differentiating factor about the merchants was that they travelled far and wide to do business. This meant that being accepted by communities was an integral part of their success. The Omi Shonin had to build long-term, trusting relationships and ensure that they were liked and respected by the communities in which they operated. This may have been one major driver behind the emergence of their unique business philosophy — Sanpo Yoshi.

This wasn't mere moral posturing—it was survival strategy. Ohmi merchants operated far from home, in communities where they had no family connections. Their reputation was their only capital.

One of their most important principles was to think in terms of long-term business, with an emphasis on how the business would continue perpetually. They always kept in mind the concept of "Sow loss and reap gain." But the most famous expression created by the Ohmi merchants, which brought one into touch with the roots of their management philosophy, was "Good seller, good buyer, good society" epitomizing the so-called "Sampo-yoshi," that provided benefits to a company, its customers and to society at large.

Chubei Itoh, a feudal era trader who founded Itochu Corporation, divided his profits three ways: between the store owner, the store's reserve fund, and employees. Merchants of the Ohmi region, where the founder was from, popularized this radical approach in the late-1800s.

Early Expansion

This is regarded as Marubeni's founding year. In 1872, Chubei opened Benchu, a drapery store in Senba, Osaka, and established a management foundation. He began exporting general goods to the U.S. in 1890.

Itoh's business continued to prosper in spite of the civil war. In 1872 he opened a small shop in Osaka and within five years was one of the largest textile wholesaler-retailers in the city.

Basically, Chubei Itoh liked new things and never got bogged down by old traditions and customs. While he adopted a council and the "tripartite division of profits principle" and other such management systems that were employed by other Ohmi Merchants, Chubei also believed in frequent power changes, giving promotions based on skill rather than seniority. Chubei placed young and talented individuals in positions of responsibility, only giving advice when it was requested and otherwise allowing his employees to operate freely.

The second generation brought international sophistication. In 1909–1910, Chubei Itoh II went abroad to study in England, visiting the U.S.A. on his way. While in England, he gained experience as a businessman and formulated new trading methods that became the basis of Marubeni today, such as trading directly with businesses in the U.K. rather than through the foreign trading houses to gain more profit for Japan, and making use of low interest rates in the U.K. to finance importing. Chubei Itoh II's international outlook and practical approach to business were the key to Marubeni's growth into a major international corporation.

This insight—bypassing intermediaries and leveraging international capital markets—would become foundational to the sōgō shōsha model.

IV. Corporate Formation & The Itochu Split (1918–1945)

The family business that Chubei Itoh built would eventually split into two corporate giants. Understanding this split is essential to understanding Marubeni's identity.

It was established in 1918 as Itochu Shoten, Ltd. in a spin-off of certain sales divisions of C. Itoh & Co. (Itochu) into a separate entity. Itochu Shoten merged with Itoh Chobei Shoten in 1921 to form Marubeni Shoten, Ltd. under the leadership of Chobei Itoh IX. Marubeni started out as a textile trading firm and expanded to trade in other consumer and industrial goods during the 1920s.

In 1914, the Company was reorganized from a proprietorship into C. Itoh & Co. In 1918, the limited partnership was divided into Itochu Shoten Ltd. with the Main store and Kyoto store at its center, and C. Itoh & Co., Ltd. with the yarn store and the Kobe Branch at its center. These two companies were the forerunners to Marubeni Corporation and Itochu Corporation, respectively.

This 1918 division matters because it established Marubeni's distinct identity—initially focused on textiles and general merchandise, while C. Itoh (later Itochu) emphasized yarn and export trading. The sibling rivalry between these two companies would continue for over a century.

Tetsujiro Furukawa and Modern Management

A pivotal figure emerged in the 1920s: Tetsujiro Furukawa, Chubei Itoh's nephew. Chubei Itoh's nephew Tetsujiro Furukawa became Marubeni Shoten's Senior Managing Director. He introduced modern management methods such as the credit system and the budget system, while also helping to create a mutually beneficial and creative company culture by establishing the Five Marubeni Precepts.

Chubei Itoh's nephew Tetsujiro Furukawa became Marubeni Shoten's Senior Managing Director. He introduced modern management methods such as the credit system and the budget system, while also helping to create a mutually beneficial and creative company culture by establishing the Five Marubeni Precepts. He went on an overseas inspection tour in 1928, which prompted him to focus on strengthening elementary education in Toyosato. He made a number of donations including the construction of Toyosato Elementary School in 1937, the renovation of the teachers' residence and the construction of the school's lunch room.

Furukawa's contributions were transformational. He took a family trading business and professionalized it—introducing credit management, budget systems, and formalized governance that would prove essential for Marubeni's survival through the turbulent decades ahead.

Wartime Consolidation

The 1930s and 1940s brought forced consolidation. In September 1941, the three companies of Kishimoto Shoten Ltd., a steel trading company for which Chubei Itoh served as an officer, Marubeni Shoten and C. Itoh & Co., Ltd., were merged to form Sanko Kabusiki Kaisha Ltd. Soon after, however, World War II erupted in the Pacific, resulting in strong economic regulation, which made conducting company activities difficult and limited trading to China and Southeast Asia. In September 1944, the three companies of Sanko, Daido Boeki, and Kureha Cotton Spinning Co., Ltd. were merged to form Daiken Co., Ltd.

The wartime period erased the carefully constructed corporate identities. Marubeni, Itochu, and several other companies were forcibly merged under government direction into conglomerates like Sanko and Daiken—entities created not for commercial logic but for national mobilization.

V. Post-War Rebirth & The Fuyo Keiretsu (1949–1972)

Re-emergence as Independent Entity

Japan's defeat in 1945 led to American occupation and the dissolution of the zaibatsu conglomerates. For Marubeni, this meant liberation.

This conglomerate was dismantled in the wake of the war and Marubeni again emerged as a separate trading company in 1949. Post-war Marubeni was predominantly a textile trading firm at its outset, but diversified into machinery, metals and chemicals, with textiles barely forming a majority of its business by the end of the decade.

The first president of Marubeni Co., Ltd. He made Marubeni survive the difficult times just after the foundation, and led the company to the general trading company by establishing a global network, entering various business fields and merging with Iida & Co., Ltd.

The post-war reinvention was remarkably swift. Within a decade, Marubeni had transformed from a textile specialist into a diversified trading company with exposure to machinery, metals, and chemicals—the sectors that would power Japan's economic miracle.

The Fuji Bank Marriage & Keiretsu Formation

The most consequential post-war development was Marubeni's integration into the Fuyo keiretsu—a network of companies centered on Fuji Bank.

Marubeni merged with Takashimaya-Iida, a trading company that owned the Takashimaya department store chain, in 1955, changing its name to Marubeni-Iida from 1955 to 1972. The merger was orchestrated by Fuji Bank in order to create a stronger trading company partner for the bank's corporate customers. Marubeni and Fuji Bank developed a network of corporate clients which was formalized as the Fuyo Group keiretsu in the 1960s, paralleling the development of the DKB Group and Sanwa Group. The Fuyo Group included Hitachi, Nissan, Canon, Showa Denko, Kubota and Nippon Steel.

This keiretsu membership proved invaluable. The cross-shareholding and preferential banking relationships gave Marubeni stable capital, patient investors, and a built-in customer base of Japan's largest industrial companies. Marubeni is a member of the Fuyo keiretsu.

The Fuyo keiretsu structure meant that Marubeni wasn't just a trading company—it was the commercial arm of an industrial network that included electronics (Hitachi), automobiles (Nissan), cameras (Canon), chemicals (Showa Denko), and farm machinery (Kubota). When these companies needed to source raw materials, arrange financing, or enter new markets, Marubeni was their natural partner.

VI. The Scandals: Lockheed & Beyond (1970s–2014)

The Nixon Shock & Corporate Restructuring

The early 1970s brought disruption. President Nixon's decision to remove the U.S. dollar from the gold standard in August 1971 disrupted currency values worldwide. For export-dependent Japanese companies like Marubeni-Iida, the resulting yen appreciation made American sales dramatically less profitable.

The company responded by dropping the "Iida" name in 1972, becoming simply Marubeni Corporation—a fresh start that would prove tragically premature.

The Lockheed Scandal

In February 1976, testimony before a U.S. Senate subcommittee revealed that American aircraft manufacturer Lockheed had systematically bribed foreign officials to secure aircraft sales. Japan was at the center of the scandal, and Marubeni was implicated as Lockheed's local agent.

In February 1976, Marubeni's credibility was damaged when it was implicated in a scandal involving the sale of Lockheed's wide-bodied Tri-Star passenger plane to Japan's largest domestic carrier, ANA. Lockheed contracted Marubeni to act as its representative in the multi-million dollar negotiations. The former vice-chairman of Lockheed, Carl Kotchian, testified that a Marubeni official made arrangements for Lockheed to pay US$300,000 (US$50,000 for each of six planes originally ordered) to the president of the airline, as well as US$100,000 to six government officials, in accordance with "Japanese business practices," to secure the contract. By July 1976, prosecutors had arrested nearly 20 officials of Marubeni and All Nippon Airways. The scandal nearly brought down the Japanese government.

At hearings of the Church committee, Lockheed's vice chairman A. Carl Kotchian testified that a total of approximately $2 million (nearly 600 million yen) had been distributed to Japanese government officials through Marubeni.

The scandal involved the Marubeni Corporation and several high-ranking members of Japanese political, business, and underworld circles, including Finance Minister Eisaku Satō and the JASDF Chief of Staff Minoru Genda.

The scandal engulfed Japan's political establishment. The question of who had accepted the money set off a storm in Japan, which on July 27 culminated with the Tokyo District Public Prosecutors Office arresting Tanaka on suspicion of violating the Foreign Exchange and Foreign Trade Act. It was the first time in Japan's history for a prime minister to be arrested for a crime committed during his tenure.

In Wednesday's ruling, the high court upheld a 21/2-year prison sentence given by lower courts to former Marubeni Corp. chairman Hiro Hiyama, 85. Marubeni, a major Japanese trading company, was acting as Lockheed's agent in Japan when the case arose.

The case directly contributed to passage of the Foreign Corrupt Practices Act (1977) in the United States. Marubeni was seriously damaged by the public image resulting from the scandal; more than 40 municipalities canceled contracts, and several international ventures were terminated. The company implemented a reform of its management structure, distributing many of the president's administrative responsibilities to a board of senior executives and adding checks and balances at the executive level.

The Lockheed scandal forced the first of several governance reforms at Marubeni. But it wouldn't be the last corruption issue.

Pattern of FCPA Issues

The corruption problems persisted across decades. In 1986, Marubeni was found to have bribed Filipino President Ferdinand Marcos in connection with Japanese ODA work. In 2012, Marubeni agreed to pay $54.6 million to settle FCPA charges related to LNG facilities in Nigeria. Foreign Corrupt Practices Act violation related to power plant contracts in Indonesia. Despite such incidents, which led to fines exceeding $200 million, Marubeni maintains a focus on compliance enhancements and diversified revenue streams to support long-term value creation.

This pattern—significant bribery charges across different regions and decades—represents a material risk factor that investors must weigh against the company's commercial strengths. The sōgō shōsha model, with its extensive government relationships and infrastructure project involvement, creates structural corruption risk that requires ongoing vigilance.

VII. The Lost Decade & Near-Collapse (1990s–2001)

The collapse of Japan's asset bubble in the early 1990s brought existential crisis. The speculative excesses of the 1980s—when Japanese companies bought everything from Rockefeller Center to Pebble Beach—gave way to a prolonged deflation that nearly destroyed the sōgō shōsha model.

Marubeni, like other sogo shosha, was hit hard by the collapse of the Japanese asset price bubble in the early 1990s and recorded its first annual net loss in 1998. The company again booked massive losses as part of a restructuring in 2001, with its stock price plummeting to 58 yen per share in December 2001.

A stock price of 58 yen—that's not a typo. For context, shares recently traded around 2,500 yen. The company had lost nearly all its market value.

The late 1990s saw widespread questioning of whether sōgō shōsha had become obsolete. Japan's manufacturers had grown sophisticated enough to handle their own trading. The information advantages that trading companies once possessed seemed less valuable in an age of telecommunications. Cross-shareholding was being unwound. The entire model appeared anachronistic.

What saved Marubeni—and its peers—was their ability to pivot. The trading companies reinvented themselves as investment vehicles and project developers, moving from transaction fees to equity ownership across value chains. This transformation laid the groundwork for the Buffett investment two decades later.

VIII. KEY INFLECTION POINT #1: The Gavilon Bet (2012–2022)

The Grand Vision: Becoming a Global Grain Major

By 2012, Marubeni had rebuilt from its near-death experience and was ready for bold moves. The company identified grain trading as a strategic priority—Japan imports virtually all its grains, and controlling supply chains from origin to destination offered compelling logic.

The target was Gavilon Holdings, the third-largest grain trader in the United States. Marubeni paid $2.7 billion to buy grains merchant Gavilon in 2013.

The vision was audacious: Marubeni would become a global grain major, doubling its handling volume and challenging incumbents like ADM, Cargill, and Louis Dreyfus. With Chinese demand for corn seemingly insatiable, the timing appeared perfect.

The Painful Unraveling

What followed was one of the most spectacular acquisition failures in Japanese corporate history.

According to the Reuters report, for Marubeni, the sale marks the end of a painful journey as it booked a series of impairment losses, totaling 120 billion yen, since buying Gavilon for $2.7 billion in 2013, due to weaker grain prices and market volatility.

"We have struggled also as our acquisition price was too high," he said, adding that the Gavilon grain business was not easily controlled by the Japanese managers.

The problems were multiple. Grain prices collapsed. Chinese demand disappointed. The business proved far more volatile than anticipated. Cultural differences made integration difficult. And Marubeni discovered that volume-based strategies in commodity trading exposed them to enormous market risk.

Marubeni first announced it would sell Gavilon to Glencore-owned Viterra on January 26, 2022, with the transaction expected to complete by end of March 2023.

The purchase price for the acquisition is US $1.125 billion, plus working capital, and is subject to certain price adjustments.

The math is brutal: Marubeni paid $2.7 billion in 2013, booked $1 billion in impairments, and sold for roughly $1.1 billion in 2022. Add opportunity cost and management attention, and Gavilon represents a multi-billion dollar lesson.

The Pivot: From Volume to Value

Marubeni says the Gavilon divestment follows a re-evaluation of its grain business strategy. While selling most of the US grain assets, it seeks to grow its Asian grain activities – especially in Japan – as well as its fertiliser operations. Accordingly, it will keep eight of the Gavilon grain elevators in the northern US together with Gavilon's equity in a joint venture grain export terminal business on the Pacific north-west coast, to service Asian customers. These assets will be operated by Marubeni subsidiary Columbia Grain International (CGI).

Despite the sale, Marubeni is looking to further strengthen its grain business to meet demand for grain in Asia, especially Japan, while reinforcing the handling of speciality crops and developing its processing and downstream businesses, it said.

The Gavilon experience forced strategic clarity. Rather than chasing volume in commodity trading, Marubeni would focus on specialty crops, Asian markets where relationships matter, and downstream processing where margins are more defensible. The retained fertilizer business—with its closer ties to Marubeni's agri-input subsidiary Helena—represented this new approach.

For investors, Gavilon offers critical lessons: even well-capitalized sōgō shōsha can make catastrophic acquisition errors, integration of Western businesses by Japanese management presents real challenges, and volume-based commodity strategies are treacherous for companies without incumbent advantages.

IX. KEY INFLECTION POINT #2: The Energy Transition & ESG Pivot (2018–Present)

The September 2018 Announcement

In September 2018, Marubeni announced to shift from coal to renewable energy resources.

This seemingly simple announcement marked a profound strategic shift. Marubeni had been one of the world's largest developers of coal-fired power plants—a business that generated strong returns but faced growing opposition from investors, regulators, and society.

In September 2018, Marubeni issued the Notification Regarding Business Policies Pertaining to Sustainability in Relation to Coal-Fired Power Generation Business and Renewable Energy Generation Business and, in March 2021, formulated the Marubeni Long-Term Vision on Climate Change, as initiatives to contribute to efforts to address global climate change.

Japan's First Offshore Wind Farm

Marubeni positioned itself as a leader in Japan's nascent offshore wind industry. Marubeni is pleased to announce that it started commercial operation based on the feed-in tariff program for renewable energy (hereinafter, "FIT") at Akita Port Offshore Wind Farm on January 31, 2023.

At the helm of this project is Marubeni, the largest shareholder of the 13 companies with equity participation in the project. Marubeni has been leading this project since being selected by Akita prefecture in a bidding process conducted in 2014 and is responsible for assembling and executing all construction, operation, maintenance, and financing of all facilities related to power generation and transmission. A total of 33 wind turbine units with an output of 4.2 megawatts (MW) each will operate off the coast of Akita port and Noshiro port. The total output will reach about 140 MW, which is enough electricity for approximately 130,000 households.

"We were able to launch this project because we have been taking the lead in the industry," says Mr. Hisafumi Manabe, President & CEO of Marubeni Offshore Wind Development. Marubeni was one of the first Japanese companies to enter the offshore wind power generation industry. The first (2011) and second (2014) projects Marubeni worked on were wind farms in the UK, both of which were acquired from the Danish company that originally owned them. Furthermore, in 2012, Marubeni acquired Seajacks, a leading UK-based offshore wind power installation provider, and was able to build up knowledge and contacts in the offshore wind industry.

Global Ambitions

According to Marubeni, the MoU affirms the partnership between the UK Government and the company, indicating the UK Government's commitment to supporting Marubeni's plans, with its partners, to invest approximately GBP 10 billion (about EUR 11.5 billion) in clean energy projects over the next ten years.

In October 2021, Marubeni invested in B2U Storage Solutions, a Santa Monica-based startup that reuses EV batteries to a battery storage system. In January 2022, Marubeni won the sea bed rights of Scotland to construct an offshore wind farm. They have partnered with SSE Renewables and Copenhagen Infrastructure Partners. In addition, Marubeni is working on Japan's first offshore wind farm as well as floating turbine demonstrations.

Yamagata Yuza Offshore Wind LLC, a special purpose company (SPC) established through a joint investment by Marubeni Corporation, The Kansai Electric Power Co., Inc., BP IOTA Holdings Limited, Tokyo Gas Co., Ltd., and Marutaka Corporation, has been appointed to operate an offshore wind farm off the coast of Yuza Town in Yamagata Prefecture, Japan as of December 24. The Project involves the construction, maintenance, and operation of a 450,000 kW bottom-fixed offshore wind farm. Through this Project, the parties aim to contribute to the development of local communities, the vitalization of the domestic offshore wind industry, and the realization of a zero-carbon society.

The energy transition creates both opportunity and risk for Marubeni. On the opportunity side, the company's project development expertise—honed through decades of power plant construction globally—translates directly to renewable energy projects. On the risk side, the transition involves exiting profitable legacy assets and betting heavily on technologies still evolving.

X. KEY INFLECTION POINT #3: The Buffett Stamp of Approval (2019–Present)

The Initial Investment

Buffett first unveiled the Japanese positions on his 90th birthday in August 2020 after making regular purchases on the Tokyo Stock Exchange, saying he was "confounded" by the opportunity and was attracted to the trading houses' dividend growth.

The five "very successfully operate in a manner somewhat similar to Berkshire itself." The first investments were made in July 2019, and they seem destined to continue for years.

Buffett's approach was characteristically patient. Rather than announcing a position and moving the market, he accumulated stakes over twelve months before disclosure. The total initial investment across all five trading houses was roughly $6.3 billion.

The Buffett Thesis

What attracted Buffett to these seemingly complex businesses? Several factors:

Valuation: "We simply looked at their financial records and were amazed at the low prices of their stocks." Japanese trading houses had traded at persistent discounts to book value, reflecting both market pessimism about Japan and the inherent complexity of these businesses.

Shareholder Friendliness: Buffett continued: "As the years have passed, our admiration for these companies has consistently grown. Greg [Abel, Buffett's designated successor] has met many times with them, and I regularly follow their progress. Both of us like their capital deployment, their managements and their attitude in respect to their investors. Each of the five companies increase dividends when appropriate, they repurchase their shares when it is sensible to do so, and their top managers are far less aggressive in their compensation programs than their U.S. counterparts."

Currency Arbitrage: Part of the investment strategy involves Buffett hedging currency risk by selling Japanese debt and then pocketing the difference between dividends from the investments and the bond coupon payments he has to make to service the debt. At the end of 2024, the market value of Berkshire's Japanese holdings came to $23.5 billion, at an aggregate cost of $13.8 billion.

The annual dividend income expected from the Japanese investments in 2025 will total about $812 million and the interest cost of Berkshire's yen-denominated debt will be about $135 million, according to Berkshire's earnings report.

This is financial engineering at its finest: borrow in yen at near-zero rates, buy dividend-paying stocks, pocket the spread, and let appreciation compound.

Growing Conviction

Berkshire grew its stake in Mitsui to 9.82% from 8.09%, in Mitsubishi to 9.67% from 8.31%, in Marubeni to 9.3% from 8.3%, in Sumitomu to 9.29% from 8.23%, and in Itochu to 8.53% from 7.47%.

"In the next 50 years ... we won't give a thought to selling those," Buffett said in May. "We will not be selling any stock. That will not happen in decades, if then," he continued. "The Japan investment has just been right up our alley."

"I expect that Greg [Abel] and his eventual successors will be holding this Japanese position for many decades and that Berkshire will find other ways to work productively with the five companies in the future," Buffett added, referring to his designated replacement as CEO.

The Buffett endorsement matters beyond capital flows. It validated the sōgō shōsha model for international investors, drew attention to Japanese corporate governance improvements, and created a template for value investing in complex businesses.

XI. Modern Marubeni: Leadership, Strategy & Financial Position

New Leadership

TOKYO -- Japanese trading company Marubeni announced on Wednesday that Masayuki Omoto will become its new president and CEO from April, stepping up from his current position as managing executive officer.

Omoto began his career with Marubeni, but left for consulting firm McKinsey before returning in 2007. The 55-year-old started out in the company's Power Division and has experience in its foreign operations in places such as Costa Rica and China.

Masayuki Omoto has served as President and Chief Executive Officer of Marubeni Corporation since April 1, 2025, succeeding Masumi Kakinoki in the role. Born on September 9, 1969, Omoto joined Marubeni in April 1992 after graduating from Waseda University's School of Commerce. He gained experience in the company's Power Division and international operations, including postings in Costa Rica and China, and briefly worked at McKinsey & Company from 2006 before returning to Marubeni. Prior to his appointment as CEO, Omoto held positions as Managing Executive Officer and Chief Operating Officer, focusing on digital innovation and next-generation business development.

Omoto's McKinsey background and digital focus signal a modernizing trajectory. His appointment reflects Marubeni's recognition that future competitiveness requires operational excellence and technological capability alongside traditional relationship management.

GC2027: The New Mid-Term Strategy

In its Mid-Term Management Strategy GC2027, Marubeni aims to achieve a market capitalization exceeding 10 trillion yen by fiscal year 2030. Through the establishment of MCPJ, Marubeni will continue to capture growth in consumer related businesses to enhance its corporate value.

In its Mid-Term Management Strategy (GC2027), Marubeni is focusing on Strategic Platform Investments (businesses with "Growth Domains x High Added Value x Scalability"). In this investment, Marubeni will establish and strengthen a new platform.

Regarding what I want to change, we've set a goal of achieving a market capitalization exceeding 10 trillion yen. I want to strongly promote initiatives to increase Marubeni's overall value. I aim to strengthen the organizational capabilities of the entire company. After consulting with President and CEO Kakinoki, we've decided to reorganize our 16 business divisions into 10.

The strategy emphasizes: - Strategic Platform Investments: Focusing on high-growth, high-margin businesses with scalability - Organizational Simplification: Consolidating from 16 to 10 business divisions - Capital Discipline: Maintaining ROIC hurdles of 10%+ for new investments

Financial Position

Year ended Mar 31, 2025: Revenues 7.79 trln, Net 502.97 billion, EPS 302.78 yen, Annual Dividend 95.00 yen.

Marubeni's dividend policy signals confidence in its strategy: dividends rose to ¥95 per share for FY2025 and are targeted to reach ¥100 by FY2026, with a 40% payout ratio.

Japan Credit Rating Agency (JCR) raised Marubeni's Rating to "AA (Stable)" from "AA- (Stable)".

Key financial metrics as of fiscal year 2025: - Revenue: ¥7.79 trillion (~$51 billion) - Net Profit: ¥503 billion (~$3.4 billion) - Dividend per Share: ¥95 (forecasted to rise to ¥100) - Credit Rating: AA (Stable) from JCR

Return on equity (ROE) is 14.05% and return on invested capital (ROIC) is 2.71%.

XII. Competitive Position & Strategic Analysis

The Five Major Competitors

Key competitors that directly challenge Marubeni's market position include Mitsubishi Corporation, Mitsui & Co., Itochu Corporation, Sumitomo Corporation, Sojitz Corporation, and Toyota Tsusho.

Among the "Big Five" trading houses where Berkshire holds positions, Marubeni occupies a distinctive niche: - Mitsubishi Corporation: Largest by market cap, strongest in metals and machinery - Mitsui & Co.: Leading in LNG and iron ore, most resource-focused - Itochu Corporation: Consumer-goods focused, strongest balance sheet - Sumitomo Corporation: Balanced portfolio, strong in infrastructure - Marubeni: Leading in grains, agricultural inputs, and power generation

Marubeni controls global grain resources and has a trading network for commodities such as corn, wheat, and soybeans, ranking first among Japan's trading companies.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The sōgō shōsha business requires decades of accumulated relationships, global infrastructure, and financial scale that present formidable barriers. Shoshas have the backings of the Japanese government, and will continue to have a seat at the most important resources and energy projects of its allies and partners around the world.

Bargaining Power of Suppliers: MODERATE Marubeni operates across thousands of supply relationships, reducing dependence on any single supplier. However, in resource businesses, major mining and energy companies hold significant power.

Bargaining Power of Buyers: MODERATE Japanese industrial customers have long-standing relationships with their trading partners. Another reason that Shoshas can't be disintermediated easily is because they deal with lots of SMEs and not just big customers. Due to capital constraints smaller customers don't have the resources to build out their own direct sale network, and will continue to rely on the trading companies for distribution.

Threat of Substitutes: MODERATE TO HIGH The historical threat has been disintermediation—manufacturers handling trade directly. This has been ongoing for decades but appears largely played out. In Part 1, we discussed the "Shosha winter" period of the 1980's, where disintermediation was one of the troubles to hit the trading companies. Since then, the threat of disintermediation has always been present. But what's also true is that disintermediation has played out over four decades, having largely run its course, leaving the trading companies today with entrenched businesses that have generally proved to be stickier.

Competitive Rivalry: HIGH Competition among the Big Five is intense but disciplined. Historical cross-shareholding and informal coordination have prevented destructive price wars, though this structure is weakening under governance reforms.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Present in trading volume and infrastructure, though less defensible than in manufacturing.

Network Effects: Limited direct network effects, but extensive relationship networks create switching costs.

Counter-Positioning: The sōgō shōsha model itself represents counter-positioning versus Western trading companies and private equity firms—competitors cannot easily replicate the combination of trading relationships, long-term capital, and cross-industry expertise.

Switching Costs: Moderate to high for Japanese industrial customers with decades-long relationships and integrated supply chains.

Branding: Limited consumer branding, but strong B2B reputation for reliability and relationship management.

Cornered Resource: Access to Japanese government-backed infrastructure projects, preferential bank financing through keiretsu relationships.

Process Power: Accumulated expertise in project development, risk management across diverse sectors, and navigating Japanese business relationships.

XIII. Bull & Bear Cases

The Bull Case

-

Buffett Validation: When the world's greatest value investor commits to holding for 50+ years, that's a powerful signal. With $23.5 billion invested as of late 2024, his bet on Japan's trading houses signals confidence in their ability to thrive for decades.

-

Energy Transition Upside: Marubeni's early positioning in offshore wind and renewable energy could generate substantial returns as Japan and global markets decarbonize. The MOU affirms the partnership between the UK Government and Marubeni, indicating the UK Government's commitment to supporting Marubeni's plans, with its partners, to invest approximately £10 billion in clean energy projects over the next 10 years.

-

Japanese Corporate Governance Reform: Ongoing pressure from the Tokyo Stock Exchange is improving capital efficiency across Japanese companies. Aggregate return on equity (ROE) for TOPIX constituents has doubled over the past decade; net cash balances are falling as boards shrink share counts.

-

Valuation: Trading at 15.5% below its 52-week high and a P/E of 12.8x vs. a five-year average of 14.5x, it offers a margin of safety.

-

Dividend Growth: Projected trajectory: 75 (2020) → 80 (2022) → 95 (2025) → 100 (2026E).

The Bear Case

-

Commodity Volatility: The Gavilon disaster demonstrated how commodity price movements can devastate even well-managed trading businesses.

-

Corruption Risk: The company's pattern of FCPA violations raises ongoing compliance concerns. Despite such incidents, which led to fines exceeding $200 million, Marubeni maintains a focus on compliance enhancements.

-

Currency Risk: While Buffett has hedged, most international investors face yen exposure. A strengthening yen would hurt export-dependent Japanese companies.

-

Complexity Discount: The inherent difficulty of understanding sōgō shōsha may result in persistent valuation discounts.

-

Geopolitical Risk: Geopolitical Tensions: Trade wars or regulatory shifts (e.g., U.S. tax policies) could disrupt supply chains. Commodity Price Volatility: While GC2027 assumes stable prices, sudden spikes (e.g., copper) could pressure margins.

Myth vs. Reality

| Common Belief | Reality |

|---|---|

| "Trading houses are obsolete" | The sōgō shōsha have reinvented themselves as investment vehicles and project developers. Berkshire's investment validates the model. |

| "Japanese companies don't return capital" | Marubeni has consistently increased dividends and executes buybacks. Shareholder returns are now a strategic priority. |

| "Too complicated to understand" | The business model—trade + investment across value chains—is analogous to Berkshire Hathaway, which Buffett explicitly acknowledged. |

| "Japan is in permanent decline" | Japanese corporate governance reforms and ROE improvements suggest structural change, not stagnation. |

XIV. Key Performance Indicators for Investors

For ongoing monitoring of Marubeni, focus on these critical metrics:

1. Core Operating Cash Flow (Most Important)

This measures cash generation from business operations excluding working capital swings. For a trading company with volatile working capital, this reveals true earnings power. Core operating cash flow growth: Historically double-digit growth rates provide a solid base.

Investors should track whether core operating cash flow grows consistently, as this funds dividends, buybacks, and strategic investments.

2. Return on Invested Capital (ROIC)

GC2027 targets 10%+ ROIC on new investments. This metric reveals whether capital allocation is creating value. The agri-inputs business in Brazil and copper projects in South America are expected to deliver ROIC of 10%+, a key metric under GC2027. These initiatives are part of ¥90 billion of profit growth from existing operations through operational efficiency and divestments.

3. Resource vs. Non-Resource Profit Mix

Currently, Marubeni's financial condition has improved with the sale of Gavilon's grain business. Based on the management's environmental strategy and initiatives to optimize capital allocation through growth investments, more attention should be paid to the core operating profit generated by the main business in the future.

Tracking the balance between volatile commodity businesses and more stable non-resource operations reveals strategic progress.

XV. Conclusion: The Circle Complete

The red circle—Marubeni's corporate symbol—traces back to Chubei Itoh's commercial seal in 1858. The "maru" (circle) represents completeness; the "beni" (red) signifies reliability and prosperity. That a 15-year-old linen peddler's mark now appears on aircraft leases, wind turbines, and grain terminals across the world speaks to both the continuity and transformation that defines this company.

Marubeni was established in 1858 when Ohmi merchant Chubei Itoh from the eastern side of Lake Biwa (now Toyosato in Shiga Prefecture) began business trips to deal in linen cloth.

Today, Marubeni stands at an inflection point. The painful lessons of Gavilon have been absorbed. The energy transition is creating new opportunities. Corporate governance reforms are improving capital discipline. And Warren Buffett's imprimatur has validated the sōgō shōsha model for international investors.

In its Mid-Term Management Strategy GC2027, Marubeni aims to achieve a market capitalization exceeding 10 trillion yen by fiscal year 2030. Through the establishment of MCPJ, Marubeni will continue to capture growth in consumer related businesses to enhance its corporate value.

The Sanpo Yoshi philosophy—benefit for seller, buyer, and society—has guided this company through Meiji modernization, wartime destruction, post-war reconstruction, scandal, near-bankruptcy, and reinvention. The 'three-way satisfaction' it refers to means that what benefits you, should ultimately also benefit your partners and society at large. It is our hope that more and more people will embrace the sanpo-yoshi spirit – to make the world a much brighter and happier place.

Whether Marubeni can achieve its ¥10 trillion market cap ambition depends on execution—on disciplined capital allocation, successful energy transition, and continued shareholder focus. The ingredients are present. The track record, while imperfect, demonstrates resilience.

"I expect that Greg [Abel] and his eventual successors will be holding this Japanese position for many decades and that Berkshire will find other ways to work productively with the five companies in the future."

When the world's most celebrated long-term investor commits to holding a position for decades, that's not just an investment thesis—it's an endorsement of institutional durability. For 165 years, Marubeni has evolved with Japan and the global economy. The next chapter—renewable energy, digital transformation, strategic platform businesses—is being written now.

The circle continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube