Regions Financial: The Unlikely Super-Regional Banking Champion

I. Introduction & Episode Roadmap

Picture this: Birmingham, Alabama, 1971. Three bankers from three different Alabama cities gather to sign documents that would create the state's first bank holding company. None of them could have imagined that their modest merger would eventually produce one of the nation's largest full-service providers of consumer and commercial banking, wealth management and mortgage products and services, serving customers across the South, Midwest and Texas.

The story of Regions Financial isn't just another tale of banking consolidation. It's the unlikely journey of how three Alabama banks—one that stored Frank James's rifle as collateral, another that survived the Civil War, and a third born during the Jazz Age—became a $140 billion super-regional powerhouse that would survive the 2008 financial crisis, weather regulatory storms, and emerge as one of America's most significant regional banks.

Today, we're diving deep into how Regions transformed from a collection of small-town Alabama banks into 428th on the Fortune 500, becoming the largest deposit holder in Alabama and Tennessee along the way. We'll explore the aggressive consolidation strategy that built an empire, the mega-merger with AmSouth that nearly broke it, the TARP bailout that saved it, and the regulatory challenges that continue to shape it.

This is a story of Southern banking ambition, regulatory chess moves, survival instincts, and the perpetual challenge of being a super-regional bank caught between community banking roots and Wall Street expectations. Let's begin where it all started: in the aftermath of America's most divisive conflict.

II. The Deep Roots: Three Banks, Three Cities, One Vision (1850s–1971)

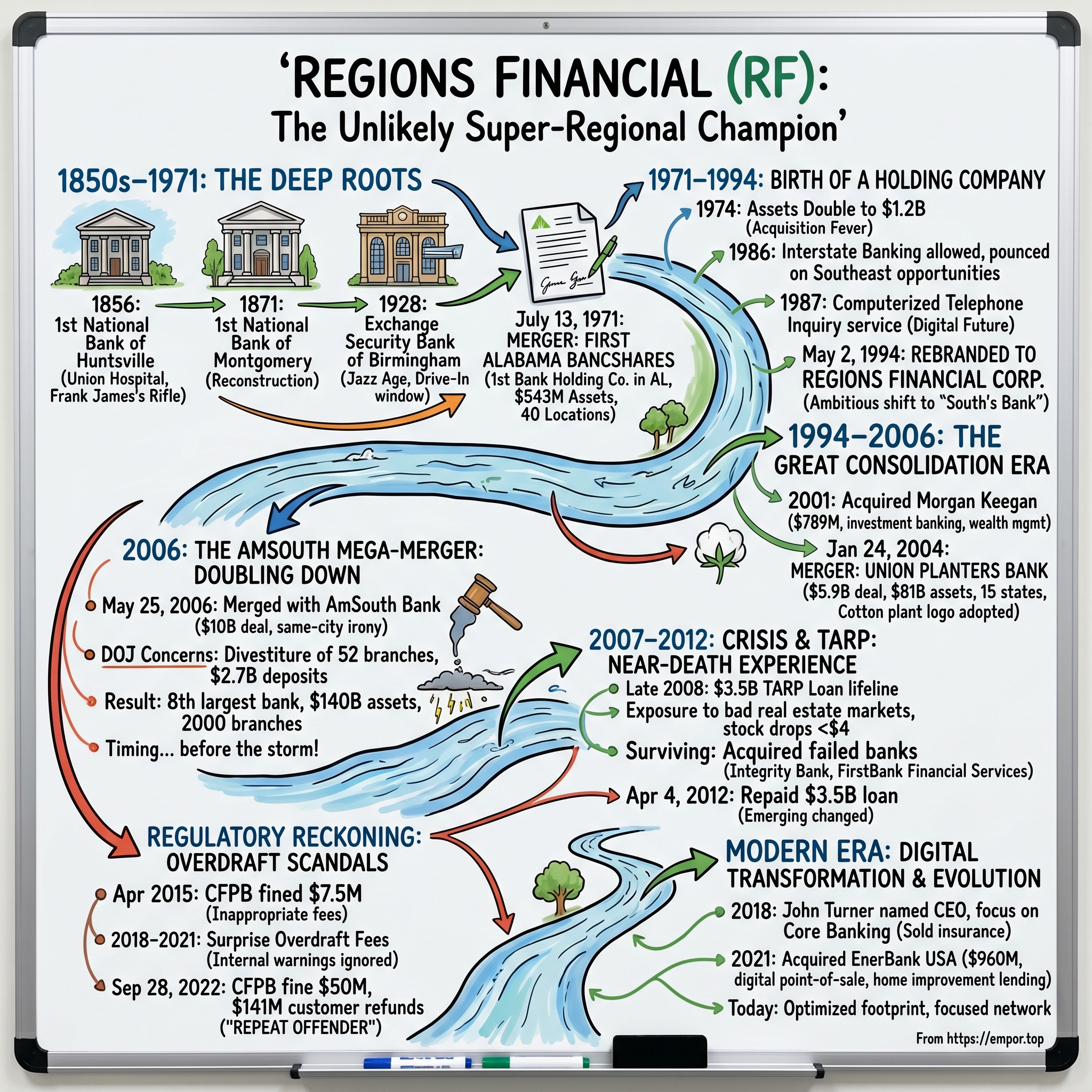

The rain was coming down hard in Huntsville on that April morning in 1865 when Union soldiers carried their wounded into the limestone building at the corner of the town square. The structure, a historic building built in 1835, had been many things—but on this day, it became a field hospital. Nobody knew then that this building would one day house the headquarters of First National Bank of Huntsville, one of the three pillars that would form Regions Financial.

First National Bank of Huntsville opened in 1856, making it the oldest of the three founding institutions. The bank had character from the start—it served as a hospital for Union soldiers during the American Civil War, and once held a rifle owned by Frank James as collateral for bail money when he was incarcerated across the street in the Madison County Jail. Imagine that conversation: "What collateral do you have, Mr. James?" "Well, I've got this rifle..."

Meanwhile, down in Montgomery, the state capital was rebuilding from the ashes of war. First National Bank of Montgomery opened in 1871, just six years after the Civil War ended. Montgomery bankers had to navigate Reconstruction, carpetbaggers, and the complete restructuring of the Southern economy. They learned early that survival meant adaptability.

The third member of this banking trinity came much later. Exchange Security Bank of Birmingham opened in 1928, just in time for the Great Depression. But Birmingham was different—it was the "Pittsburgh of the South," powered by iron, coal, and steel. The Exchange Bank started with capital totaling $35,000 and in 1947 moved to Tenth Avenue and 20th Street South. The new building was the most modern bank structure in the city and brought Birmingham the first drive-in teller window and the first bank parking lot.

These three banks operated independently for decades, each serving their local communities, each developing their own culture and expertise. Huntsville had the aerospace boom with NASA. Montgomery had state government and agriculture. Birmingham had heavy industry and commerce. But by the late 1960s, the banking landscape was shifting.

The Bank Holding Company Act was being liberalized. Interstate banking was on the horizon. Local banks across the South were realizing they needed scale to compete with the money center banks from New York and Charlotte. In 1970, a small group of Alabama bankers and businessmen got together to form the first multi-banking holding company in Alabama. Their proposal was grounded in one idea: sound banking principles and new growth opportunities could be combined to create a stronger financial institution for the state. These banking pioneers overcame legal and regulatory hurdles as well as opposition from the banking industry in the state.

On July 13, 1971, the three Alabama banks merged to form First Alabama Bancshares, Alabama's first multibank holding company. The holding company began operations with a total of $543 million in assets and 40 locations in Birmingham, Huntsville and Montgomery.

But here's the fascinating part: Until their formal merger in March 1985, under revised banking regulations, the banks continued to operate independently. For fourteen years, they were technically one company but operated as three separate banks. It was a structure that would seem bizarre today, but it preserved local relationships while building scale—a balance Regions would struggle with for the next five decades.

III. Birth of a Holding Company: First Alabama Bancshares (1971–1994)

If you walked into any of the three First Alabama banks in 1972, you wouldn't have known they were part of the same company. The tellers in Huntsville didn't wear the same uniforms as those in Montgomery. The loan officers in Birmingham used different forms than their counterparts in other cities. This was intentional—First Alabama Bancshares was feeling its way through uncharted territory.

The 1970s were a transformative decade for Southern banking. Deregulation was opening doors that had been locked since the Great Depression. In less than four years, First Alabama's assets doubled – from $543 million in 1971 to $1.2 billion at the end of 1974. This wasn't organic growth—this was acquisition fever.

The real game-changer came in 1986, when changes in the Interstate Banking Bill allowed bank holding companies to purchase bank branches outside the state in which they were chartered. Suddenly, the playing field expanded from Alabama to the entire Southeast. First Alabama's executives saw the opportunity and pounced.

In 1987, Regions became the first bank in Alabama to provide customers with direct access to their account information via a computerized telephone inquiry service. Today, this seems quaint, but imagine the revolution: customers could check their balance without driving to a branch or waiting for a monthly statement. It was a glimpse of the digital future.

The company was growing so fast and expanding so far beyond Alabama's borders that "First Alabama Bancshares" no longer made sense. The name "Regions" was purchased from First Commercial Corporation, the Arkansas Bank that Regions subsequently purchased in 1998. On May 2, 1994, the company became Regions Financial Corporation to better reflect its growing presence throughout the South.

The rebranding was more than cosmetic. It signaled a shift in ambition. Regions wasn't content to be Alabama's bank—it wanted to be the South's bank. The next decade would test whether that ambition was achievable or hubris.

IV. The Great Consolidation Era (1994–2006)

Carl Jones stood before the board in 2001 with an audacious proposal: buy Morgan Keegan, the Memphis-based investment bank, for $789 million. Some board members shifted uncomfortably. Regions was a commercial bank. What did they know about investment banking?

"Gentlemen," Jones said, "the future of banking isn't just about taking deposits and making loans. It's about being a full-service financial partner."

In 2001, Regions acquired Morgan Keegan & Company for $789 million. It was a bold move that would give Regions capabilities in wealth management, capital markets, and investment banking—services that would differentiate it from other regional players.

But the real transformation came in 2004. On January 24, 2004, Regions merged with Memphis, Tennessee–based Union Planters Bank in a $5.9 billion transaction. This wasn't just another acquisition—it was a merger of equals that would fundamentally reshape the company.

Jackson Moore, who had succeeded Benjamin Rawlins as the CEO of Union Planters Bank after Rawlins died of a heart attack in September 2000, took the helm of the largest bank in Tennessee. Moore was a cost-cutter, a efficiency expert who had closed over two hundred of the bank's under-performing branches, eliminated unnecessary salaries and expenditures, and streamlined operations during his tenure at Union Planters.

The integration was complex. The combined bank would have $81 billion of assets and $56 billion of deposits, with roughly 1,400 banking offices in 15 states. Jackson W. Moore, the former CEO of Union Planters, became CEO of the merged company. He suffered a stroke after the merger closed, but was still able to assume his new post upon recovery.

After the merger, Regions adopted Union Planters' former logo of a young cotton plant—a symbol that would soon become iconic across the South. The merger significantly increased Regions' footprint in Tennessee; Union Planters had been the largest Tennessee-based bank.

By 2006, Regions had transformed from a three-bank Alabama holding company into one of the South's banking giants. It had the scale, the footprint, and the product suite to compete with anyone. But the biggest test—and the biggest opportunity—was about to present itself in the form of another Birmingham bank.

V. The AmSouth Mega-Merger: Doubling Down (2006)

The conference room on the 30th floor of the AmSouth-Sonat Tower in downtown Birmingham had witnessed many deals, but nothing like this. On a humid May morning in 2006, executives from two Birmingham banking giants were about to announce a merger that would shake the foundations of Southern banking.

AmSouth was previously known as First National Bank of Birmingham, which was first organized by Charles Linn in 1872. Like Regions, AmSouth had grown through decades of acquisitions. AmSouth's size more than doubled in 2000 when it absorbed Nashville, Tennessee-based First American National Bank. With the merger came hundreds of branches primarily in Tennessee but also in Kentucky, Virginia, and Mississippi. This is cited as a rare example of one bank absorbing another bank larger than itself.

On May 25, 2006, AmSouth announced it would merge with Regions Financial Corporation, another Birmingham-based bank, in a $10 billion deal. The irony wasn't lost on anyone—two banks headquartered in the same city, whose executives probably ran into each other at the same country clubs and charity events, were now combining forces.

But this wasn't a friendly neighborhood merger. The Department of Justice had concerns. 52 AmSouth Bank Branches with $2.7 Billion in Deposits to be Divested in Alabama, Mississippi and Tennessee. The regulatory scrutiny was intense. In Alabama alone, 39 branches divested were sold to RBC Centura Bank and converted in Spring 2007.

While Regions was the surviving company, the merged entity adopted AmSouth's corporate structure—a unusual arrangement that spoke to the complexity of melding two large, proud institutions. Upon completion of the merger, Regions Financial became the nation's 8th largest bank with total assets of nearly $140 billion and approximately 2,000 branches.

The timing couldn't have been worse—or so it seemed. The merger closed just as storm clouds were gathering over the American financial system. Subprime mortgages were starting to default. Credit markets were beginning to tighten. What looked like the deal of the decade in May 2006 would soon look like a death wish.

VI. Crisis and TARP: The Near-Death Experience (2007–2012)

Grayson Hall's hands were steady as he signed the documents, but everyone in the room knew what this meant. It was late 2008, and Regions was accepting a lifeline from the federal government. In 2008, Regions Bank received a $3.5 billion loan as part of the Troubled Asset Relief Program.

The financial crisis had exposed every weakness in the AmSouth merger. The combined entity had too many branches, too much commercial real estate exposure, and too much debt from financing the deal. What had looked like geographic diversification now looked like exposure to every failing real estate market in the South.

The numbers were staggering. Credit losses mounted quarter after quarter. The stock price, which had been above $35 before the crisis, plummeted to under $4. There were days when employees wondered if they'd have jobs the next morning.

But Regions did what Southern banks have always done—it survived. It raised capital, cut costs, and worked through problem loans one by one. The bank also found opportunities in the crisis. On August 29, 2008, Regions paid $9 million to acquire $900 million in deposits and $33.4 million for five branch offices and other assets from the failed Alpharetta, Georgia-based Integrity Bank. Later, in February 2009, Regions acquired $285 million in deposits and $17 million in assets from the failed Georgia-based FirstBank Financial Services.

The road back was long and painful. But on April 4, 2012, Regions repaid the $3.5 billion loan. The bank had survived its near-death experience, but it emerged changed. The freewheeling acquisition days were over. Now came the hard work of building a sustainable, compliant, profitable regional bank.

VII. The Regulatory Reckoning: Overdraft Scandals & Consequences

The CFPB's letter arrived on a Tuesday morning in 2015. For a bank that had just emerged from the financial crisis, it was another blow. In April 2015, Regions was fined $7.5 million by the Consumer Financial Protection Bureau (CFPB) for charging consumers with inappropriate or illegal overdraft fees. Regions did not obtain affirmative opt-ins from charging overdraft fees on ATM and point of sale transactions. The CFPB also found that Regions misrepresented overdraft and non-sufficient fund fees related to the bank's short-term loan program.

But that was just the beginning. Inside Regions, a more serious problem was brewing. The bank's overdraft practices were generating enormous fees—and enormous problems. Between 2018 and 2021, Regions was charging what the CFPB would later call "surprise overdraft fees."

Here's how it worked: A customer would check their balance at an ATM, see they had sufficient funds, make a purchase, and then get hit with an overdraft fee. From August 2018 through July 2021, Regions charged customers surprise overdraft fees on certain ATM withdrawals and debit card purchases. The bank charged overdraft fees even after telling consumers they had sufficient funds at the time of the transactions.

The most damning part? Leadership knew. Internal emails and documents would later reveal that executives understood the practice was problematic but delayed fixing it while they figured out how to replace the lost revenue. It was exactly the kind of short-term thinking that gives banking a bad name.

On September 28, 2022, the CFPB again ordered Regions Bank to pay $50 million into the CFPB's victims relief fund and to refund at least $141 million to customers harmed by its illegal surprise overdraft fees, labeling the bank a "repeat offender".

The financial hit was significant, but the reputational damage was worse. Regions had positioned itself as a relationship bank, a trusted financial partner for the South. Now it was a "repeat offender" in regulatory documents. CFPB Director Rohit Chopra said in a statement: "Regions Bank raked in tens of millions of dollars in surprise overdraft fees every year, even after its own staff warned that the bank's practices were illegal".

The overdraft scandal forced a reckoning at Regions. It wasn't just about compliance—it was about culture. Could a super-regional bank maintain its community banking values while meeting Wall Street's demands for profits?

VIII. Modern Era: Digital Transformation & Strategic Evolution (2012–Today)

John Turner had been with Regions for just seven years when he was named CEO in 2018, but he understood the bank's challenges intimately. Turner joined Regions in 2011 as the regional president of the South Region and led banking operations in Alabama, Mississippi, South Louisiana, and the Florida Panhandle. He was named head of Regions' Corporate Bank in 2014 and President in 2017.

Turner replaced Grayson Hall, who had been CEO of the $123 billion-asset company since April 2010. Hall had successfully navigated the bank through the aftermath of the financial crisis, but Turner faced different challenges: digital disruption, fintech competition, and changing customer expectations.

The strategy was clear but execution was complex. Regions needed to modernize without losing its relationship banking soul. In 2018, Regions sold its insurance operations to BB&T, deciding to focus on core banking rather than trying to be all things to all people.

But the boldest move came in 2021. On June 8th, Regions Bank announced its plans to acquire the Salt Lake City-based EnerBank USA for a whopping $960 million. EnerBank has worked with hundreds of loan program sponsors, inclusive of thousands of home improvement contractors, serving over a million homeowners and funding over $12 billion in home improvement projects.

The EnerBank acquisition was strategic on multiple levels. It gave Regions a digital-first platform for point-of-sale lending. It provided exposure to the booming home improvement market. And perhaps most importantly, it showed that Regions could still innovate and grow without traditional branch-based acquisitions.

Today, Regions operates about 2,000 automated teller machines and 1,300 branches in 15 states in the Southern and Midwestern United States. The footprint has been optimized—no longer the 2,000-branch behemoth from the AmSouth merger days, but a more focused, more profitable network.

IX. Playbook: Lessons from Southern Banking Consolidation

After five decades of growth, crisis, and transformation, what can we learn from Regions' journey? The playbook that emerges is both cautionary tale and roadmap.

First, timing is everything in bank M&A. The Union Planters deal in 2004 was perfectly timed—completed before the crisis, with enough time to integrate before the storm hit. The AmSouth merger in 2006? The timing couldn't have been worse, closing just as the financial crisis was beginning. Same strategy, different outcomes.

Second, cultural integration matters more than synergies. Regions struggled for years to integrate three different banking cultures—its own traditional Alabama roots, Union Planters' Tennessee efficiency focus, and AmSouth's aggressive growth culture. The companies achieved the promised cost synergies, but cultural conflicts persisted for years.

Third, regulatory compliance isn't optional—it's existential. The overdraft scandals cost Regions not just hundreds of millions in fines and restitution, but immeasurable reputational damage. In today's environment, a single compliance failure can undo years of relationship building.

Fourth, scale provides resilience but not immunity. Regions' size helped it survive the financial crisis—it was big enough to matter, big enough to get TARP funds, big enough to absorb losses. But size also made it a target for regulators and a symbol of "too big to fail" banks that many Americans resented.

Fifth, technology is the new frontier for competition. The EnerBank acquisition shows Regions understands that future growth won't come from buying more branches but from digital capabilities. The challenge is building tech-forward capabilities while maintaining the relationship banking that differentiates regionals from both megabanks and fintechs.

X. Analysis & Investment Case

Looking at Regions today requires viewing it through multiple lenses. As of March 2025 it was the 26th largest U.S. chartered bank holding corporation, with $158.4 billion in consolidated assets and a market capitalization of $18.98 billion, and is part of the S&P 500 index.

The Bear Case: Regions faces structural headwinds that won't disappear. Net interest margins remain under pressure in a competitive deposit environment. Credit losses are normalizing from unsustainably low pandemic levels. Regulatory scrutiny remains high given the bank's history of compliance issues. Most concerning: Regions operates in a strategic no-man's land—too small to compete with JPMorgan or Bank of America on scale, too large to be a nimble community bank.

The efficiency challenges are real. Despite years of cost-cutting, Regions still operates with higher expense ratios than top-performing regionals. The branch network, while optimized from its peak, still represents significant fixed costs in an increasingly digital world.

The Bull Case: But there's another story here. Regions dominates attractive markets across the fast-growing Southeast. It is the largest deposit holder in Alabama and Tennessee. It is also one of the largest deposit holders in Arkansas, Louisiana, Mississippi, and Florida. These markets benefit from population growth, business migration, and economic dynamism that outpaces the national average.

The digital investments are starting to pay off. The EnerBank platform provides a blueprint for growth beyond traditional banking. Customer satisfaction scores have improved. Credit quality remains strong with disciplined underwriting standards learned through crisis.

Most importantly, Regions trades at a meaningful discount to tangible book value compared to regional banking peers. If management can execute on operational improvements while avoiding regulatory missteps, the valuation gap should close.

The Verdict: Regions is neither a growth story nor a value trap—it's a "show me" story. The pieces are in place for success: dominant market position, improving technology, experienced management. But execution risk remains high. For patient investors who believe in the long-term growth of the American Southeast and trust management to avoid another regulatory disaster, Regions offers interesting risk-reward. For those seeking either rapid growth or sleep-well-at-night stability, better options exist elsewhere.

XI. Epilogue & Future Outlook

As John Turner looks out from the executive floor of the Regions Center in Birmingham, he sees a city transformed. The steel mills are gone, replaced by medical centers and university research parks. The banking landscape has transformed too. The community banks that once dotted every small Southern town have been absorbed or disappeared. The fintech disruptors that seemed so threatening five years ago are now potential partners or acquisition targets.

What's next for Regions? The crystal ball is cloudy, but certain trends seem clear.

Consolidation isn't over. Despite predictions of its demise, regional bank consolidation will continue. But the next wave won't look like the last one. Instead of large-scale mergers of equals, expect targeted acquisitions of digital capabilities, fee-based businesses, and specialized lending platforms. Regions could be either buyer or seller, depending on valuations and strategic options.

Digital transformation will accelerate. The EnerBank acquisition was just the beginning. Regions needs to build or buy more digital capabilities to remain relevant. This isn't just about mobile apps—it's about embedded finance, banking-as-a-service, and meeting customers where they are rather than expecting them to come to branches.

Regulatory pressure will intensify, not ease. The political pendulum swings, but the direction of travel is clear: more scrutiny of bank fees, more focus on financial inclusion, more examination of systemic risks. Regions' history as a "repeat offender" means it will face extra scrutiny. One more major compliance failure could trigger dramatic consequences.

The Southeast advantage will persist. Demographics are destiny in banking, and the Southeast's demographics remain favorable. Population growth, business formation, and economic dynamism in Regions' core markets provide tailwinds that many Northeastern and Midwestern banks lack.

The story of Regions Financial isn't finished. From three Alabama banks to a super-regional powerhouse, from near-death in 2008 to digital transformation in the 2020s, this unlikely champion of Southern banking continues to evolve. Whether it thrives, merely survives, or becomes part of something larger remains to be written.

But one thing is certain: the next chapter will look nothing like the last. The days of growth through traditional bank acquisitions are over. The future belongs to those who can blend relationship banking with digital innovation, community roots with scalable technology, regulatory compliance with profitable growth.

For Regions, the challenge is clear: honor the past while building the future. It's a challenge every 150-year-old institution faces. Some succeed. Some fail. Some transform into something entirely new.

Which path will Regions take? Check back in another decade. The answer, like the bank itself, is still being written in the humid air and red clay soil of the American South.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube