PNB Housing Finance: The Rise of India's Housing Finance Powerhouse

I. Introduction & Episode Hook

Picture this: It's May 2025, and in the gleaming towers of Mumbai's financial district, a block deal worth hundreds of millions of dollars is being executed. The seller? Carlyle Group, one of the world's most sophisticated private equity firms. The asset? Their remaining 10.44% stake in PNB Housing Finance. The return? A staggering 367% over a decade—the kind of return that makes even seasoned PE partners pause and smile.

But this isn't just another private equity exit story. This is the tale of how a sleepy subsidiary of a state-owned bank transformed into one of India's most intriguing housing finance companies, navigating the treacherous waters between government control and private capital, between regulatory scrutiny and market ambition. Today, with a market capitalization hovering around ₹20,000 crore, PNB Housing Finance stands as India's third-largest housing finance company by loan assets. Yet behind this seemingly straightforward success story lies a complex narrative of transformation, regulatory battles, and the delicate dance between public sector heritage and private capital ambitions.

The central question we're exploring today isn't just how a housing finance company grew—it's how a sleepy government subsidiary became a test case for India's evolving financial sector, where state-owned enterprises meet global private equity, where regulatory conservatism clashes with market innovation, and where the promise of India's massive housing deficit creates both extraordinary opportunities and unexpected challenges.

What makes this story particularly fascinating is the timing. As India undergoes its most ambitious urbanization in history, with millions moving from villages to cities, the demand for housing finance has never been more acute. Yet PNB Housing's journey shows us that capturing this opportunity requires more than just capital—it demands navigating the intricate web of Indian regulation, managing the expectations of both government and private stakeholders, and building a retail franchise in one of the world's most competitive financial markets.

This is a story about transformation at multiple levels: a company transforming from government subsidiary to market-oriented player, a sector transforming from state-dominated to increasingly private, and a country transforming its approach to housing finance. Let's dive in.

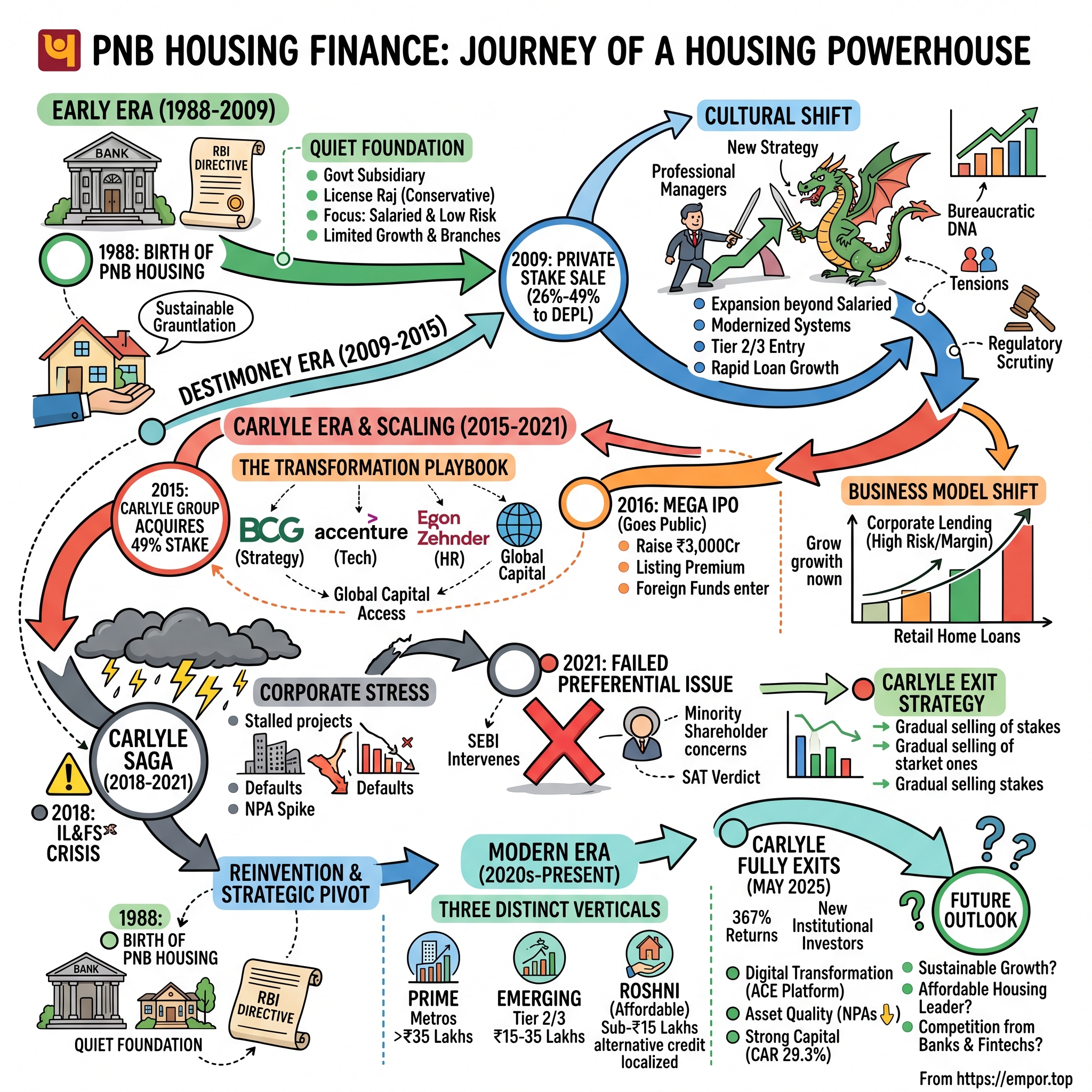

II. Punjab National Bank & The Birth of PNB Housing (1988–2000s)

The year was 1988. India was still a closed economy, the Berlin Wall was still standing, and the country's banking sector operated under the heavy hand of government control. It was in this environment that Punjab National Bank, one of India's oldest and most prestigious public sector banks, made a decision that would seem unremarkable at the time but would set in motion a three-decade transformation story.

On November 11, 1988, PNB Housing Finance commenced operations as a wholly owned subsidiary of Punjab National Bank, incorporated under the Companies Act of 1956. The birth of this entity wasn't driven by entrepreneurial vision or market opportunity—it was a response to government directive. The Reserve Bank of India, concerned about the growing housing deficit and the banking sector's inability to adequately address it, had been encouraging major banks to set up specialized housing finance subsidiaries.

Think about the India of 1988 for a moment. The License Raj was in full force—you needed government permission for everything from starting a business to expanding production capacity. The economy was growing at what would later be mockingly called the "Hindu rate of growth"—around 3-4% annually. Home ownership was a distant dream for most Indians, with mortgage penetration at less than 2% of GDP compared to over 50% in developed economies.

For Punjab National Bank, setting up a housing finance subsidiary was both a compliance exercise and a strategic hedge. The parent bank, established in 1894, had survived partition, nationalization, and multiple economic crises. Its leadership understood that specialized lending required specialized expertise, and housing finance—with its long tenures, different risk profiles, and unique regulatory requirements—was sufficiently different from traditional banking to warrant a separate entity.

The early years of PNB Housing were characterized by extreme conservatism. Loan-to-value ratios rarely exceeded 50%, documentation requirements were stringent to the point of being prohibitive, and the customer base was limited to government employees and professionals with impeccable credentials. The company's first office in Delhi operated more like a government department than a financial services firm—complete with the stereotypical lethargy and red tape that plagued public sector enterprises of that era.

What's fascinating about this period is how unremarkable PNB Housing was. Annual loan disbursements in the early 1990s were measured in tens of crores, not thousands. The company had fewer than 100 employees, operated from a handful of branches, and its growth trajectory was essentially flat. This wasn't a company trying to capture market share or revolutionize housing finance—it was a dutiful subsidiary fulfilling a mandate.

The regulatory environment added another layer of complexity. While incorporated in 1988, PNB Housing only received its registration with the National Housing Bank (NHB) in 2001—thirteen years after commencing operations. This delay wasn't unusual in the bureaucratic maze of Indian financial regulation, but it meant the company operated in a regulatory grey zone for over a decade, limiting its ability to expand or innovate.

During this period, India's housing finance sector was dominated by three players: HDFC (the private sector pioneer), LIC Housing Finance (backed by the insurance behemoth), and a collection of small, regional players. PNB Housing was barely a blip on the radar—neither fully private nor aggressively public sector, caught in an institutional no-man's land.

The conservative approach had its merits. Non-performing assets were virtually non-existent, capital adequacy was never a concern given the parent bank's backing, and the company weathered the various economic storms of the 1990s—including the 1991 balance of payments crisis and the Asian financial crisis of 1997—without breaking a sweat. But this stability came at the cost of relevance. By the early 2000s, as India's economy began to liberalize and the housing finance sector started to boom, PNB Housing found itself increasingly marginalized.

The irony was palpable. Here was a company backed by one of India's largest banks, operating in one of the economy's fastest-growing sectors, in a country with massive housing shortage—and yet it was barely growing. The company's loan book in 2005 was smaller than what HDFC would disburse in a single quarter. Something had to change.

The first signs of transformation came in the mid-2000s. India's economy was booming, real estate prices were soaring, and the banking sector was undergoing rapid modernization. Punjab National Bank's leadership began to recognize that PNB Housing's conservative approach was leaving money on the table. The subsidiary needed capital, expertise, and most importantly, a new strategic direction.

But transforming a public sector enterprise is never simple. The company's culture, shaped by two decades of government ownership, was resistant to change. Employees were comfortable with the status quo, processes were ossified, and the very idea of competing aggressively for market share was alien to the organizational DNA. The stage was set for what would become one of the most interesting public-private partnerships in Indian financial services.

III. The Destimoney Partnership Era (2009–2015)

December 9, 2009 marked a watershed moment in PNB Housing's history. On this day, Punjab National Bank made a decision that would have been unthinkable just a few years earlier—it sold a 26% stake in its housing finance subsidiary to Destimoney Enterprises Private Limited (DEPL), a then-unknown real estate and financial services player. This wasn't just a financial transaction; it was PNB's admission that government ownership alone couldn't unlock the company's potential.

To understand why this partnership mattered, you need to understand Destimoney. Founded by Ravindra Kishore Sinha, DEPL was the kind of aggressive, entrepreneurial firm that thrived in India's newly liberalized economy. Sinha, who would later become infamous for other ventures, saw in PNB Housing what the parent bank couldn't—a sleeping giant with a pristine loan book, minimal competition in the mid-market segment, and the backing of a major public sector bank.

The initial 26% stake sale was just the beginning. Over the next few years, DEPL would increase its stake to 49%, effectively becoming an equal partner with PNB in running the housing finance company. This created an unusual dynamic—a public sector bank sharing control of its subsidiary with a private entity that had very different ideas about risk, growth, and market positioning.

Under the Destimoney partnership, PNB Housing underwent its first real transformation. The company began expanding beyond its traditional customer base of government employees. New products were launched targeting self-employed individuals and small business owners. The branch network, which had remained largely static for two decades, began expanding into Tier-2 and Tier-3 cities. Loan disbursements, which had been growing at single digits, suddenly jumped to 20-30% annually.

But the most significant change was cultural. Destimoney brought in professional managers from the private sector, introduced performance-based incentives, and began modernizing the company's technology infrastructure. For the first time, PNB Housing started thinking like a business rather than a government department. Sales teams were given targets, branches were evaluated on profitability, and customer service—long an afterthought—became a priority.

The numbers tell the story. Between 2009 and 2014, PNB Housing's loan book grew from under ₹5,000 crore to over ₹20,000 crore. The company's market share, while still small compared to giants like HDFC, had quadrupled. More importantly, the company had proven it could grow without compromising asset quality—NPAs remained under 0.5%, among the lowest in the industry.

Yet beneath this success story, tensions were brewing. DEPL's aggressive growth strategy sometimes clashed with PNB's conservative approach. The parent bank was concerned about reputation risk, regulatory scrutiny, and the possibility of asset quality deterioration. Destimoney, on the other hand, wanted to push harder into developer financing and land loans—higher margin but riskier segments that made PNB uncomfortable.

The broader context is important here. This was the period when India's real estate sector was booming but also becoming increasingly controversial. Stories of builder defaults, incomplete projects, and buyer grievances were making headlines. The Reserve Bank of India was tightening regulations on real estate lending. In this environment, having a real estate-connected shareholder like Destimoney was becoming more liability than asset.

By 2014, it was clear that the Destimoney partnership had run its course. The company had been transformed from a sleepy subsidiary to a growing financial services firm, but it needed a different kind of partner for the next phase of growth. DEPL, facing its own challenges and seeking to monetize its investments, was ready to exit. The question was: who would be the buyer?

Enter Carlyle Group. One of the world's largest private equity firms, Carlyle had been watching India's financial services sector closely. They saw in PNB Housing exactly what they were looking for—a platform with clean assets, strong parentage, growth potential, and most importantly, a seller motivated to exit. In February 2015, Carlyle acquired DEPL's entire 49% stake through its entity Quality Investment Holdings.

The Destimoney era had ended, but its impact was lasting. The company that Carlyle inherited in 2015 was fundamentally different from the one DEPL had invested in six years earlier. It had scale, momentum, and most importantly, it had proven that a public sector subsidiary could be transformed into a competitive market player. The stage was now set for an even more ambitious transformation—one that would take PNB Housing to the public markets.

IV. Enter Carlyle: The Private Equity Play (2015–2016)

When Carlyle Group acquired its 49% stake in PNB Housing Finance in 2015 for ₹1,600 crore, the global private equity firm wasn't just buying into another Indian financial services company. They were making a calculated bet on India's housing finance sector, armed with a playbook they'd successfully executed across emerging markets from China to Brazil.

The timing was deliberate. India's real estate sector had just emerged from a painful correction, interest rates were beginning to decline, and the newly elected Modi government was pushing affordable housing as a national priority. Carlyle's team, led by Shankar Narayanan, saw an opportunity to apply institutional private equity discipline to what was essentially a sub-scale player with enormous potential.

The first hundred days under Carlyle ownership were transformational. The PE firm brought in Sanjaya Gupta, a veteran banker with stints at State Bank of India and Yes Bank, as Managing Director. Gupta's mandate was clear: professionalize operations, accelerate growth, and prepare the company for an IPO within 18-24 months. This wasn't just about financial engineering—it was about building an institution.

Carlyle's approach was methodical. They commissioned Boston Consulting Group to review the company's strategy, brought in Accenture to overhaul technology systems, and hired executive search firm Egon Zehnder to strengthen the leadership team. Within six months, PNB Housing had a new CFO, a new head of retail banking, and a new chief risk officer—all recruited from leading private sector banks.

The transformation went deep into the organization's DNA. Carlyle introduced sophisticated risk management systems, implementing credit scoring models and portfolio analytics that were standard in global banks but revolutionary for a company that had relied on manual underwriting for decades. They pushed for geographic diversification—by end of 2015, PNB Housing was present in 65 cities compared to just 23 two years earlier.

But perhaps the most significant change was in the company's approach to capital and funding. Under government ownership, PNB Housing had relied heavily on its parent bank for funding. Carlyle pushed for diversification—within a year, the company had raised money through commercial paper, non-convertible debentures, and external commercial borrowings. The cost of funds dropped by 150 basis points, directly improving margins.

The PE firm also brought sophistication to product development. They introduced loan products for non-resident Indians, launched loan against property as a major business line, and most controversially, expanded aggressively into construction finance and lease rental discounting. These higher-margin products would later become a source of both profits and problems.

What's remarkable about this period is the speed of execution. In just 18 months, Carlyle transformed PNB Housing from a regional player to a national presence. The loan book grew from ₹24,000 crore to over ₹38,000 crore. The number of branches increased from 38 to 67. Employee count doubled. This wasn't organic growth—this was a force-fed expansion funded by Carlyle's reputation and PNB's balance sheet.

The IPO preparation was a military operation. Carlyle brought in investment banks Kotak Mahindra, Citigroup, and JM Financial as lead managers. The company's financials were scrutinized and cleaned up—every non-performing asset was provided for, every contingent liability was disclosed. The prospectus, running over 500 pages, was a masterclass in transparency, designed to appeal to both retail and institutional investors.

Behind the scenes, there was intense negotiation between Carlyle and PNB about the IPO structure. Carlyle wanted to partially exit through the IPO, while PNB was reluctant to dilute below 51% to maintain control. The final structure—a pure primary issue with no secondary sale—was a compromise that satisfied both parties while raising capital for growth.

The roadshows were revealing. In meetings with international investors in Singapore, Hong Kong, and London, the Carlyle brand opened doors that would have been closed to a standalone Indian housing finance company. Fund managers who had invested in Carlyle's previous exits in India—from HDFC to SBI Cards—were predisposed to trust the PE firm's judgment.

Yet there were skeptics. Some investors questioned the sustainability of the growth trajectory. Others worried about asset quality, particularly in the construction finance book that had grown from almost nothing to 20% of loans in just two years. The concentration risk—with PNB still owning 51% and Carlyle 49%—also raised governance concerns.

Carlyle's response was to double down on the India story. In investor presentations, they painted a picture of a country with a housing shortage of 20 million units, mortgage penetration at just 9% of GDP versus 25% in China and 80% in the US, and a government committed to "Housing for All by 2022." PNB Housing wasn't just a company—it was a play on India's demographic dividend.

The PE firm's influence extended beyond financial metrics. They instituted quarterly board meetings with detailed presentations, introduced independent directors with global experience, and implemented employee stock option plans to align management incentives. The company that approached the public markets in October 2016 was unrecognizable from the entity Carlyle had acquired just 18 months earlier.

As the IPO date approached, one thing was clear: Carlyle had executed one of the fastest and most comprehensive transformations in Indian financial services history. Whether this transformation was sustainable—and whether public market investors would validate Carlyle's vision—would soon be tested.

V. The 2016 IPO: Going Public

The last week of October 2016 was a defining moment for India's capital markets. As PNB Housing Finance's IPO opened for subscription on October 25, the country was still reeling from the surprise announcement of a new central bank governor just months earlier. The real estate sector was under pressure, interest rates were elevated, and global markets were jittery ahead of the U.S. presidential election. It was, to put it mildly, not ideal timing for India's largest housing finance IPO.

The numbers were ambitious: ₹3,000 crore to be raised entirely through fresh equity, with no secondary sale by existing shareholders. The price band was set at ₹750-775 per share, valuing the company at nearly ₹13,000 crore—a bold ask for a company that had been valued at less than ₹4,000 crore when Carlyle invested just 18 months earlier.

The first day of bidding revealed the market's appetite. Institutional investors, particularly foreign funds, came in strong. By noon, the qualified institutional buyer portion was oversubscribed. But it was the retail response that surprised everyone—small investors, attracted by the PNB parentage and the Carlyle pedigree, flooded the issue with applications.

Behind the scenes, the book-building process was a sophisticated operation. The lead managers—Kotak, Citi, and JM Financial—had divided global investors among themselves. Kotak focused on domestic mutual funds and insurance companies, Citi handled global long-only funds, while JM Financial targeted high-net-worth individuals and family offices. The coordination was precise, with hourly updates on subscription levels and investor feedback.

What made this IPO particularly interesting was the investor composition. Unlike typical Indian IPOs dominated by domestic institutions, PNB Housing attracted significant foreign interest. Funds like Government of Singapore Investment Corporation, Fidelity, and Aberdeen Asset Management saw in PNB Housing a proxy for India's consumer finance story—a bet on rising incomes, urbanization, and formalization of the economy.

The pricing discussion on October 27, the last day of bidding, was intense. The issue was oversubscribed 5.7 times overall, with the institutional portion oversubscribed 11 times. Carlyle pushed for pricing at the top of the band, arguing that the strong demand justified maximum valuation. PNB, more conservative, worried about listing performance and long-term investor relationships. The final price—₹775, at the top of the band—was a victory for Carlyle's aggressive approach.

November 7, 2016—listing day. The stock opened at ₹778, barely above the issue price, disappointing those expecting a strong pop. But as the day progressed, buying emerged. Foreign funds that had missed the IPO allocation began building positions. The stock closed at ₹818, a 5.5% premium to the issue price—respectable if not spectacular.

The post-IPO shareholding structure revealed the new reality. PNB's stake had diluted to 51% (maintaining control), Carlyle held 32%, and public shareholders owned 17%. For the first time in its history, PNB Housing had genuine public market scrutiny. Quarterly earnings calls, analyst coverage, and share price movements would now drive management decisions as much as board directives.

The immediate impact was cultural. The employee stock options issued during the IPO created a cohort of middle managers with skin in the game. The company's senior leadership, accustomed to the relative anonymity of being a subsidiary, now found themselves presenting to analysts and investors. The transformation from a government-owned entity to a public company was complete—or so it seemed.

But the IPO also created new tensions. Public market investors expected consistent growth and margin expansion. They were less patient with the company's exposure to construction finance and developer loans, segments that offered high returns but carried reputation risk. The stock's performance—range-bound for the first few months—reflected this uncertainty.

The use of IPO proceeds became a closely watched metric. The company had promised to deploy the ₹3,000 crore for growth, but investors wanted details. How much would go to retail versus corporate? What geographies would be prioritized? How would the company compete with established players like HDFC and new entrants like fintech-backed NBFCs?

Management's response was measured. In the first earnings call post-IPO, they outlined a strategy of "profitable growth"—expanding the retail book while gradually reducing corporate exposure, investing in technology while maintaining cost discipline, growing the balance sheet while improving asset quality. It was a delicate balance, designed to appeal to multiple stakeholders with different priorities.

The IPO had another unintended consequence—it put PNB Housing firmly on the regulatory radar. The National Housing Bank, the Reserve Bank of India, and the Securities and Exchange Board of India all had oversight roles. The company's every move would now be scrutinized not just for business merit but for regulatory compliance. This would become particularly relevant in the years ahead.

As 2016 drew to a close, PNB Housing's IPO was deemed a success. The company had raised significant capital, achieved a reasonable valuation, and attracted quality investors. But the real test lay ahead. Could a company with government parentage, private equity ownership, and public market scrutiny navigate the competing demands of all three? The answer would unfold over the next several years in ways no one could have predicted.

VI. Business Model & Product Portfolio Evolution

To understand PNB Housing Finance's evolution, you need to think of it as three distinct businesses operating under one roof: the traditional home loan business inherited from its government days, the high-margin corporate lending business built during the PE era, and the emerging affordable housing franchise that represents its future. Each tells a different story about India's financial services landscape.

The retail housing business—what management calls the "prime" segment—remains the company's bread and butter. In FY24, retail segment contributed to 97% of the total AUM, whereas corporate segment contributed to 3%. This dramatic shift from just five years ago, when corporate loans comprised nearly 40% of the book, represents one of the most aggressive portfolio transformations in Indian financial services.

The retail products themselves are unremarkable—standard home loans, loans against property, top-up loans. What's interesting is how the company segments its customers. The prime segment targets salaried employees and self-employed professionals in metros and Tier-1 cities with ticket sizes above ₹35 lakhs. The emerging markets segment, carved out as a separate vertical in FY25, focuses on Tier-2 and Tier-3 cities with ticket sizes between ₹15-35 lakhs. And then there's Roshni, the affordable housing brand targeting sub-₹15 lakh loans.

The company's focused strategy for the affordable segment led it to expand its Roshni branches to 160 during the year, up from 82 at the end of FY23. This isn't just branch expansion—it's a completely different business model. Roshni branches operate with different underwriting standards, employ local staff who understand the informal economy, and use alternative credit assessment methods including field visits and community references.

The corporate lending story is more complex. At its peak in 2018, PNB Housing had over ₹25,000 crore in corporate loans—construction finance, lease rental discounting, and developer funding. These were high-margin products, often yielding 200-300 basis points more than retail loans. But they were also high-risk, particularly in India's troubled real estate sector.

The IL&FS crisis of 2018 changed everything. As liquidity dried up and real estate projects stalled across India, PNB Housing's corporate book came under severe stress. NPAs spiked, provisions ballooned, and the stock price crashed. Management made a strategic decision—run down the corporate book and transform into a pure-play retail lender.

The transformation was painful but decisive. By FY24, the corporate segment had shrunk to just 3% of AUM from nearly 40% five years earlier. Billions in corporate loans were either repaid, sold, or written off. Entire teams were disbanded. Relationships with developers, carefully cultivated over years, were abandoned.

But here's where the story gets interesting. After a three-year hiatus, PNB Housing Finance is looking to grow its corporate loan book from Q3 of FY25, though the mortgage lender's focus would continue to be the emerging and affordable housing segment. The company previously had a substantial corporate loan portfolio, but due to stress in the segment, it reduced its exposure to corporate loans.

This return to corporate lending, albeit cautiously, reflects both the cleaned-up real estate sector and management's confidence in their risk management capabilities. But it also highlights a fundamental tension—retail lending is safe but low-margin, while corporate lending is profitable but risky. Finding the right balance has been PNB Housing's perpetual challenge.

The technology transformation deserves special mention. When Carlyle took over, PNB Housing's technology infrastructure was archaic—loan applications were processed manually, customer data was stored in silos, and digital channels were non-existent. Today, the company claims to process loans in three minutes, offers end-to-end digital journeys, and uses artificial intelligence for credit underwriting.

Yet the digital transformation remains incomplete. Unlike new-age fintech lenders who are digital-native, PNB Housing is retrofitting technology onto legacy processes. The company's cost-to-income ratio, while improved, still lags best-in-class players. Customer acquisition costs remain high, and the branch network—while extensive—is expensive to maintain.

The funding side reveals another evolution. Historically dependent on its parent bank, PNB Housing has diversified its liability franchise significantly. The company now raises funds through multiple channels—bank loans, bonds, commercial paper, external commercial borrowings, and retail deposits. This diversification has reduced funding costs but also increased complexity.

The competitive landscape has shifted dramatically. When PNB Housing went public in 2016, its main competitors were traditional housing finance companies like HDFC, LIC Housing, and Indiabulls. Today, it faces competition from multiple fronts—banks flush with liquidity and aggressive on mortgages, fintech players offering instant loans, and even non-financial companies entering housing finance through partnerships.

The numbers tell a sobering story. The company has delivered a poor sales growth of -2.03% over past five years. This isn't just about market share loss—it's about a fundamental challenge in finding profitable growth in an increasingly competitive market.

Product innovation has been limited. While peers have launched innovative products like step-up loans, flexi-hybrid loans, and integrated home buying solutions, PNB Housing's product suite remains conventional. The company's attempts at differentiation—like faster processing, doorstep service, and relationship managers—are easily replicable and provide limited competitive advantage.

The margin trajectory is equally concerning. Net interest margins have compressed from over 4.5% in 2018 to around 4.1% in FY24, reflecting both competitive pressure and changing mix. As the company shifts toward affordable housing—a strategically important but lower-margin segment—this pressure will likely intensify.

Yet there are bright spots. Asset quality has improved dramatically, with gross NPAs at just 1.5% in FY24 compared to nearly 4% during the crisis years. The capital position is robust, with capital adequacy ratio at 29.3%, providing ample buffer for growth. And the retail transformation, while painful, has de-risked the business model significantly.

What emerges from this analysis is a company in transition—from corporate to retail, from traditional to digital, from government-influenced to market-oriented. Whether this transformation will create sustainable competitive advantage remains an open question.

VII. The Carlyle Saga: Control Attempts & Exit (2021–2025)

The summer of 2021 should have been Carlyle's moment of triumph. After six years of patient value creation, with PNB Housing's stock trading at all-time highs and the Indian housing market booming, the PE firm was ready to execute one of the most audacious moves in Indian private equity history—taking control of a public sector-linked company through a ₹4,000 crore preferential issue.

In early 2021, Punjab National Bank Housing Finance announced plans to raise Rs 4,000 crore through the allotment of preferential shares and convertible bonds. PNB Housing Finance would alot these shares to private equity firm Carlyle Group-led investment vehicles, Aditya Puri's family investment arm, and a bunch of other shareholders. The structure was elegant: Pluto Investments S.a.r.l., an affiliated entity of Carlyle Asia Partners IV, L.P. and Carlyle Asia Partners V, L.P., agreed to invest up to ₹3,185 crore through a preferential allotment of equity shares and warrants, at a price of ₹390 per share.

What made this deal extraordinary wasn't just its size but its implications. This would mean that the Carlyle Group would gain greater control over a Public Sector Undertaking (PSU) due to a greater shareholding in the company. After the deal, the total shareholding of Punjab National Bank (PNB) would eventually reduce from ~32% to ~20%. For the first time in Indian corporate history, a global PE firm would control a company with public sector DNA.

The pricing became the flashpoint. However, the market price of the shares of the PNB housing was Rs. 525 per share. The proposed issue price of ₹390 represented a significant discount to market price, raising questions about fairness to minority shareholders. This wasn't just a technical issue—it was about corporate governance in the age of activist regulators. Enter SEBI—the market regulator that had been watching this transaction with increasing concern. SES, a proxy advisory firm, raised concerns with SEBI, which eventually led to the deal being stalled. The regulator's objection wasn't just technical—it was fundamental. The company received a letter from the capital market regulator on June 18 calling it to comply with the legal provisions in the matter. "The current resolution bearing item no. 1 (Issue of Securities of the company and matters related therewith) of EGM notice dated May, 31, 2021 is ultra-vires of AOA (articles of association) and shall not be acted upon until the company undertakes the valuation of shares as prescribed under 19(2) of AOA, for purpose of preferential allotment, from an independent registered valuer as per the provisions of applicable laws," a regulatory filing by PNB Housing Finance quoted the letter as saying.

What followed was a regulatory and legal drama that would drag on for months. PNB Housing filed an appeal with the Securities Appellate Tribunal (SAT), arguing that it had complied with all applicable laws. The company's board, dominated by Carlyle nominees, believed the preferential allotment was in the best interests of all stakeholders. But the parent bank, Punjab National Bank, found itself in an impossible position—caught between its subsidiary's ambitions and the regulator's concerns.

The SAT hearings revealed the deeper tensions. The Securities Appellate Tribunal (SAT) in a hearing on Tuesday said market watchdog Securities and Exchange Board of India (Sebi) tried to pre-empt the outcome of PNB Housing Finance's extraordinary general meeting (EGM) that was called to decide on the allotment of preferential shares to the Carlyle Group and other investors. The tribunal gave a split verdict—allowing the EGM to proceed but preventing the company from acting on its results.

By October 2021, the writing was on the wall. In October 2021, PNB Housing finance announced that it had terminated the preferential stake sale to Carlyle. The ₹4,000 crore that would have transformed the company's capital structure and ownership would never materialize. Carlyle's dream of controlling a quasi-public sector company had been thwarted by regulatory intervention.

The failure of the preferential issue forced Carlyle to pivot. If they couldn't increase their stake, they would monetize what they had. The exit strategy that followed was methodical and patient. In July last year, the US-based Carlyle divested a 12.8 per cent stake in PNB Housing Finance for Rs 2,578 crore. In November 2024, Carlyle Group offloaded 2.45 crore shares, or 9.43 per cent, stake in PNB Housing Finance for Rs 2,301.58 crore.

The final act came in May 2025. Global investment firm The Carlyle Group has fully exited its position in PNB Housing Finance, offloading its entire 10.44% stake via a block trade, according to a report by Reuters citing Moneycontrol. The sale was executed with military precision—The deal involved approximately 17.3 million shares of PNB Housing, accounting for roughly 60% of the total block deal, which was launched at a floor price of 960 rupees per share. In early trading, shares were sold at 1,000.20 rupees each, which represented a small discount of nearly 1% compared to the previous day's closing price.

The buyers list read like a who's who of global finance. The stake was snapped up by a mix of global and domestic institutional investors, including Société Générale, Goldman Sachs, and the Saudi Arabia Public Investment Fund. Notably, Norway's Government Pension Fund Global and Aurigin Capital also entered the fray, signaling confidence in PNB Housing's post-exit prospects.

The numbers tell a remarkable story. The $2.7 billion divestment not only crystallizes a staggering 367% return on Carlyle's original investment but also underscores the complexities and rewards of long-term investing in emerging markets. After initially acquiring a 49% stake in 2015 for ₹1,600 crore, the firm gradually reduced its holdings. Despite the regulatory setbacks, despite missing the opportunity to take control, Carlyle had generated returns that would make any PE partner proud.

What's fascinating about Carlyle's exit is what it reveals about the evolution of Indian capital markets. A decade ago, a PE firm exiting through gradual block deals would have been seen as a failure. Today, with deep institutional participation and sophisticated market mechanisms, it's a viable and profitable strategy. The fact that sovereign wealth funds and global asset managers were willing to buy Carlyle's stake at minimal discount shows the maturity of both the market and the asset.

The impact on PNB Housing was immediate and positive. PNB Housing Finance share price hit a seven-month high of ₹1,087.95 today, as it rallied 8 per cent on the BSE in Friday's intraday amid heavy volumes, after a huge block deal was executed on the counter. The market, it seemed, was relieved to see the back of the ownership uncertainty that had plagued the company for years.

But Carlyle's exit also raises questions about PNB Housing's future. The exit leaves PNB Housing's largest private equity backer behind, but Punjab National Bank retains a 28.1% stake, ensuring continuity. Without a strong anchor investor pushing for growth and transformation, will the company revert to its conservative, public sector ways? Or will the new institutional investors provide the governance and strategic direction needed for the next phase of growth?

The Carlyle saga ultimately is a story about the limits of private equity in India's quasi-public sector. Despite their sophistication, despite their capital, despite their strategic vision, Carlyle couldn't overcome the fundamental tension between private ambition and public oversight. The regulatory intervention in 2021 wasn't just about protecting minority shareholders—it was about preserving the delicate balance between state control and market forces that characterizes much of India's financial sector.

Yet Carlyle's 367% return proves that even within these constraints, value can be created and monetized. The PE firm may not have achieved its goal of control, but it transformed PNB Housing from a sleepy subsidiary to a viable public company, created thousands of crores in market value, and ultimately, delivered exceptional returns to its limited partners. In the complex world of emerging market private equity, that counts as a win.

VIII. Modern Era: Strategic Shifts & Market Position (2020s–Present)

The post-Carlyle era at PNB Housing Finance began not with a whimper but with reinvention. With market capitalization hovering around ₹20,000 crore and the ownership overhang finally resolved, management could focus on what had been neglected during years of capital structure drama—building a sustainable, competitive business model for the 2020s.

The strategic pivot was clear from day one: We shifted our focus to the retail sector, reduced our corporate exposure, invested in digitalisation to enhance our internal processes and created a superior customer journey. This wasn't just rhetoric—the numbers backed it up. Retail segment contributed to 99% of the total loan disbursement in FY24 and Retail segment contributed to 97% of the total AUM in FY24, whereas corporate segment contributed to 3%.

But the real innovation came in how PNB Housing segmented its retail business. Management carved out three distinct verticals, each with its own strategy, risk profile, and growth trajectory. The prime segment continued to serve traditional customers in metros and Tier-1 cities. Further, from the beginning of FY25, we also carved out separate segment termed emerging markets to cater to tier 2 and 3 cities. And then there was Roshni, the affordable housing brand that represented both the company's biggest opportunity and its greatest challenge.

The Roshni story deserves special attention. To cater to diverse customer segments, we introduced Roshni, a dedicated offering for the affordable housing finance sector, providing specialised services to meet the unique needs of this important and growing market. Our focused strategy for the affordable segment led us to expand our Roshni branches to 160 during the year, up from 82 at the end of FY23. This wasn't just branch expansion—it was building an entirely new business from scratch.

The revamped Unnati portfolio under Roshni revealed the depth of transformation. According to MD & CEO Hardayal Prasad, PNB Housing Finance is redesigning its "Unnati" loan portfolio to expand into the affordable housing market and target consumers who require loans between Rs 9 to 12 lakh. A minor vertical under Unnati that will be distinct from the current Rs 18–19 lakh affordable home loans has been formed by PNB Housing. This represented a fundamental shift—from serving the lower middle class to truly addressing the affordable housing deficit.

The geographic expansion was equally ambitious. Promoted by Punjab National Bank (PNB), the housing finance company (HFC) has identified and mapped almost 140 districts where it will offer products under this vertical of Unnati. "We are going to enter about 10-12 states. Whether it is Uttar Pradesh, Uttarakhand, Madhya Pradesh, Rajasthan, Chhattisgarh, Gujarat, Tamil Nadu, Andhra Pradesh, Telangana, we are going to be pan-India. We will have branches in these states," Prasad said.

The target customer for Unnati was radically different from PNB Housing's traditional base. So, whether you are a salaried individual of stable or local business entity or a self-employed individual like kirana shop owner, garment shop or other business set ups who may or may not have formal income proof but have sufficient income to serve obligations, your search ends here and Unnati home loan is a right product for you. This required not just new products but a complete reimagination of underwriting, collections, and customer service.

The technology transformation accelerated post-2021. The company's claim of processing loans in three minutes wasn't just marketing—it represented a fundamental shift from manual, paper-based processes to digital-first operations. The ACE technology platform, which won the Business Transformation Awards 2021, enabled end-to-end digital journeys, from application to disbursement.

Yet the digital transformation wasn't without challenges. Unlike fintech startups building from scratch, PNB Housing was retrofitting technology onto decades-old processes. Legacy systems had to be integrated, employees retrained, and customers educated. The cost-to-income ratio, while improving, still lagged best-in-class players, reflecting the ongoing investment required.

The competitive landscape in the 2020s presented both opportunities and threats. On one hand, India's housing deficit remained massive—estimated at over 20 million units. Government initiatives like Pradhan Mantri Awas Yojana created tailwinds for affordable housing. Interest rates, after years of increases, were beginning to stabilize.

On the other hand, competition had never been fiercer. Banks, flush with liquidity and under pressure to grow their retail books, were aggressively pricing home loans. New-age fintech players were using technology to dramatically reduce customer acquisition costs. Even non-financial companies were entering housing finance through partnerships and co-lending arrangements.

The company has delivered a poor sales growth of -2.03% over past five years. This sobering statistic reflected not just competitive pressure but fundamental questions about PNB Housing's positioning. Was it a mass-market lender competing on price? A niche player focused on underserved segments? Or something in between?

Management's answer was to pursue a barbell strategy—maintain the profitable prime segment while aggressively growing in affordable housing. But executing this strategy required different capabilities. The prime segment demanded superior service and competitive pricing. The affordable segment required local presence, alternative underwriting, and intensive customer engagement.

The asset quality improvement provided some breathing room. Gross NPAs had declined from nearly 4% during the crisis years to just 1.5% in FY24. The provision coverage ratio was healthy, and the company had a substantial written-off pool from which recoveries could boost profitability. Capital adequacy at 29.3% provided ample buffer for growth.

But structural challenges remained. Company has a low return on equity of 11.6% over last 3 years. For a financial services company, this was concerning—it suggested either excessive capital, insufficient leverage, or margin pressure. Probably all three.

The ownership structure post-Carlyle exit created its own dynamics. Promoter Holding: 28.1% While PNB remained the largest shareholder, it no longer had majority control. The new institutional investors—including sovereign wealth funds and global asset managers—brought sophistication but also demanding return expectations.

The cultural transformation was perhaps the most challenging. For decades, PNB Housing had operated with a public sector mindset—conservative, process-oriented, hierarchical. The Carlyle years had begun shifting this culture, but old habits died hard. Creating a performance-driven, customer-centric organization required not just new systems but fundamental behavioral change.

The brand positioning remained confused. Was PNB Housing leveraging its government parentage for trust and stability? Or positioning itself as a modern, technology-enabled lender? The company seemed to want both, but in a market increasingly segmented between traditional and digital players, sitting in the middle was dangerous.

Recent developments suggested management recognized these challenges. After a three-year hiatus, PNB Housing Finance is looking to grow its corporate loan book from the current quarter (Q3) of FY25, Girish Kousgi, MD & CEO of the housing finance firm, told Business Standard. Having said that, the mortgage lender's focus would continue to be the emerging and affordable housing segment. This return to corporate lending, while risky, acknowledged that pure retail play might not generate adequate returns.

The modern era of PNB Housing Finance is thus one of contradictions. A company with government heritage trying to compete with private players. A traditional lender attempting digital transformation. A prime-focused franchise pivoting to affordable housing. Whether these contradictions can be resolved into a coherent strategy remains the central question for investors and stakeholders.

IX. Playbook: Investment & Business Lessons

The PNB Housing Finance story offers a masterclass in value creation, value destruction, and value recovery—all within a single decade. For investors, operators, and policymakers, the lessons are profound and often counterintuitive. This isn't just about one company's journey; it's about how financial services evolve in emerging markets.

Lesson 1: The State-Owned Enterprise Transformation Playbook

The transformation of sleepy government subsidiaries into dynamic market players follows a predictable pattern. First comes the realization that government ownership alone cannot unlock value. Then comes the search for a strategic partner—usually private equity—who brings not just capital but operational expertise. The partnership phase is characterized by rapid growth, cultural change, and inevitable tensions between public and private stakeholders.

PNB Housing's journey from 1988 to 2015 exemplifies this pattern. The company languished for decades under pure government ownership, transformed rapidly under the Destimoney partnership, and achieved escape velocity under Carlyle. But here's the critical insight: the transformation only works when the government parent is willing to cede control, even if gradually. PNB's willingness to dilute from 100% to 51% to eventually 28% was essential for unlocking value.

Lesson 2: Private Equity Value Creation in Regulated Industries

The $2.7 billion divestment not only crystallizes a staggering 367% return on Carlyle's original investment but also underscores the complexities and rewards of long-term investing in emerging markets. Carlyle's playbook was textbook PE: professionalize management, accelerate growth, improve operations, access capital markets, and exit at a multiple. But executing this playbook in India's heavily regulated financial sector required adaptations.

The key was patience. After initially acquiring a 49% stake in 2015 for ₹1,600 crore, the firm gradually reduced its holdings. Rather than pushing for a quick flip, Carlyle invested in genuine operational improvements. They brought in professional management, upgraded technology, expanded distribution, and most importantly, navigated the complex relationship with the government parent. The 367% return wasn't just financial engineering—it was value creation through transformation.

Lesson 3: Regulatory Risk Can Trump Business Fundamentals

The failed 2021 preferential issue was a watershed moment. Despite board approval, shareholder support, and business logic, regulatory intervention killed a ₹4,000 crore transaction. The lesson? In emerging markets, regulatory risk isn't just another risk factor—it can be the dominant risk factor.

Smart investors don't just analyze the regulatory environment; they anticipate how it might evolve. The SEBI intervention wasn't random—it reflected growing concern about governance in quasi-public companies and protection of minority shareholders. Investors who saw this trend could have anticipated regulatory pushback against the Carlyle control attempt.

Lesson 4: The Housing Finance Opportunity in Emerging Markets

India's housing finance sector presents a paradox: massive demand meets structural impediments. The demand side is compelling—housing shortage of 20 million units, mortgage penetration at 9% of GDP versus 80% in developed markets, government support through subsidies and tax breaks. Yet the supply side faces challenges—land acquisition issues, lengthy approval processes, informal income documentation, and limited credit history.

PNB Housing's evolution shows that capturing this opportunity requires segmentation and specialization. The prime segment is increasingly commoditized, with banks offering comparable products at competitive rates. The real opportunity lies in affordable housing and emerging markets, but these require different capabilities—local presence, alternative underwriting, and patient capital.

Lesson 5: Timing the Exit—Why Carlyle Left Money on the Table

Carlyle's 367% return over a decade is a testament to PNB Housing's strong fundamentals and India's growing housing market. The company's shares rose 516% over five years, driven by robust demand for affordable housing loans and PNB's backing as a state-owned entity. Yet Carlyle chose to exit when the company was seemingly well-positioned for future growth. Why?

The answer reveals sophisticated portfolio management. PE firms don't just maximize individual returns; they optimize portfolio returns. After a decade, with most value creation captured and regulatory uncertainties persisting, redeploying capital into new opportunities made sense. The discipline to exit when others are buying, to take profits when the story still sounds good, separates great investors from merely good ones.

Lesson 6: Capital Allocation in Cyclical Businesses

Housing finance is inherently cyclical, tied to interest rates, real estate prices, and economic growth. PNB Housing's journey shows that successful capital allocation in cyclical businesses requires counter-cyclical thinking. Expand distribution during downturns when competitors retreat. Build provisions during good times when credit costs are low. Raise capital when markets are receptive, not when you desperately need it.

The company's failure to raise capital in 2021, when markets were buoyant, forced it to navigate subsequent challenges with limited flexibility. Contrast this with the successful 2016 IPO, timed perfectly to capture market optimism. The lesson? In cyclical businesses, timing of capital raises matters as much as the amount raised.

Lesson 7: The Retail Transformation Trade-off

PNB Housing's shift from corporate to retail lending exemplifies a broader trend in emerging market finance. Retail segment contributed to 97% of the total AUM in FY24, whereas corporate segment contributed to 3%. This transformation reduced risk but also compressed returns. Retail lending is safer but more expensive to originate and service. It requires extensive distribution, sophisticated technology, and intensive customer engagement.

The trade-off is stark: corporate lending offers higher margins but concentration risk and potential NPAs. Retail lending provides diversification and stability but requires scale for profitability. PNB Housing's experience suggests that pure-play strategies in either direction may be sub-optimal. The sweet spot might be a carefully managed mix, with retail providing stability and selective corporate lending driving returns.

Lesson 8: Technology as Enabler, Not Differentiator

PNB Housing's digital transformation illustrates a crucial distinction. Technology can enable better customer experience and operational efficiency, but in financial services, it rarely provides sustainable differentiation. The company's three-minute loan processing is impressive, but competitors can and will match it.

The real differentiation comes from how technology is deployed—to serve segments others can't, to underwrite risks others won't, to create experiences others haven't imagined. PNB Housing's investment in technology for affordable housing, where documentation is minimal and credit histories sparse, represents genuine innovation. The lesson? Don't invest in technology for its own sake; invest in technology that enables unique business models.

Lesson 9: The Governance Premium in Emerging Markets

The stock price reaction to Carlyle's exit—an 8% jump—reveals the market's view on ownership structure. Despite Carlyle's operational improvements and strategic guidance, the market valued clarity and simplicity over PE expertise. This governance premium is particularly pronounced in emerging markets, where ownership disputes and related-party transactions are common concerns.

For investors, this creates opportunity. Companies with clean, simple ownership structures trade at premiums to those with complex, opaque structures. The transition from complex PE ownership to distributed institutional ownership can itself create value, independent of operational improvements.

Lesson 10: Building Sustainable Competitive Advantage

After all the transformation, what sustainable competitive advantage does PNB Housing possess? The government parentage provides some trust benefit but decreasing relevance. The branch network offers distribution but at high cost. The technology platform enables efficiency but is replicable.

Perhaps the real competitive advantage lies in the affordable housing franchise being built through Roshni. Our focused strategy for the affordable segment led us to expand our Roshni branches to 160 during the year, up from 82 at the end of FY23. This requires local knowledge, specialized underwriting, and patient capital—capabilities not easily replicated. If PNB Housing can crack the affordable housing code, it could build a genuinely differentiated position.

The meta-lesson from PNB Housing's journey is that value creation in emerging markets requires navigating multiple, often conflicting stakeholders—government parents, private investors, regulators, public markets. Success comes not from optimizing for any single stakeholder but from finding dynamic balance among all. This is messy, complex, and often frustrating. It's also where the greatest opportunities lie.

X. Analysis & Investment Case

Standing at the crossroads of its evolution, PNB Housing Finance presents a complex investment thesis that defies simple categorization. With Mkt Cap: 20,201 Crore, it's neither a small-cap growth story nor a large-cap stability play. It's a mid-cap transformation story with both significant upside potential and meaningful downside risks.

Current Valuation Metrics and Peer Comparison

The valuation picture is mixed. Trading at approximately 1.1 times book value, PNB Housing appears cheap relative to peers like HDFC (trading at 3-4x book) or even other housing finance companies like LIC Housing Finance (1.5-2x book). But this discount exists for reasons that go beyond simple metrics.

Company has a low return on equity of 11.6% over last 3 years. For context, well-run housing finance companies generate ROEs of 15-18%, while best-in-class players like HDFC historically delivered 20%+. This ROE gap explains much of the valuation discount. Investors aren't just buying current earnings; they're buying future earning power, and PNB Housing's track record raises questions.

The efficiency metrics are equally concerning. Despite years of digital investment and cost optimization, the cost-to-income ratio remains elevated compared to peers. While exact figures aren't disclosed, industry analysis suggests PNB Housing operates at 35-40% cost-to-income versus 25-30% for efficient players. This structural cost disadvantage limits profitability even in good times.

The Bull Case: India's Housing Deficit and Government Support

The macro opportunity remains compelling. India needs 20 million additional housing units, and mortgage penetration at 9% of GDP has substantial room to grow toward the 25% seen in China or 50%+ in developed markets. Simple math suggests the mortgage market could triple over the next decade.

Government support provides additional tailwinds. The Pradhan Mantri Awas Yojana subsidy program directly benefits affordable housing players. Tax deductions on home loan interest make mortgages attractive for middle-class buyers. Infrastructure development in Tier-2 and Tier-3 cities opens new markets. These aren't temporary phenomena—they represent structural shifts in India's political economy.

PNB Housing's strategic positioning could capture disproportionate growth. Our focused strategy for the affordable segment led us to expand our Roshni branches to 160 during the year, up from 82 at the end of FY23. If the company can successfully scale affordable housing while maintaining asset quality, the ROE expansion could be dramatic. Affordable housing typically generates NIMs of 5-6% versus 3-4% for prime mortgages.

The clean balance sheet provides room for growth. With gross NPAs at just 1.5% and capital adequacy at 29.3%, PNB Housing has both the asset quality and capital buffer to expand aggressively. The written-off pool of ₹1,400 crore represents potential upside through recoveries, providing a cushion for future credit costs.

The Bear Case: Structural Challenges and Competitive Pressure

Yet the bear case is equally compelling. The company has delivered a poor sales growth of -2.03% over past five years. This isn't just a rough patch—it's five years of shrinkage in a growing market. While management attributes this to strategic repositioning, investors might reasonably wonder if it reflects deeper competitive disadvantages.

The competitive landscape is brutal and getting worse. Banks with lower funding costs are aggressively entering housing finance. Fintech players are using technology to dramatically reduce customer acquisition costs. Even within affordable housing, specialized players like Aavas Financiers have first-mover advantages. PNB Housing risks being stuck in the middle—not cheap enough to compete with banks, not specialized enough to compete with niche players.

Company has low interest coverage ratio. This suggests margin pressure that could worsen if interest rates rise or competition intensifies. Housing finance is increasingly commoditized, and PNB Housing lacks clear differentiators to maintain pricing power.

The ownership overhang, while reduced post-Carlyle exit, persists. With PNB holding just 28.1%, questions remain about strategic direction and governance. Will PNB support the company during downturns? Can management make bold decisions without a strong anchor shareholder? These uncertainties create a governance discount that may persist.

New Institutional Investors: Smart Money or Greater Fools?

The stake was snapped up by a mix of global and domestic institutional investors, including Société Générale, Goldman Sachs, and the Saudi Arabia Public Investment Fund. Notably, Norway's Government Pension Fund Global and Aurigin Capital also entered the fray, signaling confidence in PNB Housing's post-exit prospects.

The entry of sophisticated institutional investors post-Carlyle exit is intriguing. These aren't momentum traders but patient capital with multi-year horizons. Their investment suggests confidence in India's structural housing story and PNB Housing's positioning within it. But it's worth noting they're buying at prices significantly below Carlyle's average exit price, suggesting more cautious optimism than enthusiasm.

Future Catalysts and Key Monitorables

Several catalysts could reshape the investment thesis:

-

Corporate Lending Revival: After a three-year hiatus, PNB Housing Finance is looking to grow its corporate loan book from the current quarter (Q3) of FY25. "We are starting with our corporate loan book this quarter. In the retail segment, we are expecting a growth of 17 per cent year-on-year (YoY) in FY25. If executed well, selective corporate lending could boost ROEs without excessive risk.

-

Affordable Housing Scale: The Roshni expansion is at an inflection point. If the company can scale from 160 to 300+ branches while maintaining asset quality, the earnings impact would be substantial.

-

Digital Transformation Payoff: Years of technology investment should eventually translate to lower costs and better customer acquisition. The key metric to watch is cost-to-income ratio—if it doesn't decline meaningfully, the digital strategy isn't working.

-

Interest Rate Cycle: PNB Housing is particularly sensitive to rate cycles given its funding mix and customer segment. Rate cuts could provide a significant tailwind, while sustained increases could pressure both demand and margins.

-

Regulatory Changes: Any shifts in affordable housing subsidies, tax benefits, or regulatory requirements could materially impact the business model.

The Verdict: Contrarian Value or Value Trap?

PNB Housing Finance presents a classic contrarian opportunity—unloved, misunderstood, but potentially mispriced. The stock trades at a significant discount to book value and peers, despite operating in a structurally growing market with improving operational metrics.

For patient, risk-tolerant investors, the asymmetry is attractive. If management executes its retail transformation while selectively returning to corporate lending, ROEs could expand to 15%+, driving a re-rating to 1.5-2x book value. That's a potential doubling from current levels.

But this isn't a slam dunk. The company faces structural challenges that won't disappear overnight. The competitive landscape is intensifying, not easing. And without a clear competitive advantage, PNB Housing might remain a perpetual laggard, generating sub-par returns that justify its discount valuation.

The investment case ultimately depends on your view of management's ability to execute a complex transformation while navigating an increasingly difficult market. The pieces are in place—clean balance sheet, government parentage, expanding distribution, growing market. But assembling these pieces into a coherent, profitable whole requires execution excellence that PNB Housing hasn't consistently demonstrated.

For most investors, PNB Housing remains a "watch and wait" story. Let management prove they can grow profitably in retail while managing corporate exposure. Let the affordable housing expansion demonstrate sustainable unit economics. Let the digital investments translate to measurable efficiency gains. If these proof points emerge, the stock could re-rate significantly. If they don't, there are better opportunities elsewhere in India's financial services sector.

The meta-lesson for investors? In emerging markets, transformation stories are common but successful transformations are rare. The difference usually comes down to execution, and execution is hard to evaluate from outside. When in doubt, wait for evidence. In PNB Housing's case, that evidence is still being written.

XI. Epilogue & Future Outlook

As monsoon clouds gather over Mumbai in 2025, PNB Housing Finance finds itself at a defining moment. The Carlyle era has ended, the ownership structure has stabilized, and management has articulated a clear strategy. Yet the fundamental question remains: Can a company born in the License Raj, transformed by private equity, and now navigating as a quasi-independent entity, create sustainable value in India's hypercompetitive financial services landscape?

India's housing finance sector poised to grow as urbanization accelerates and affordable housing initiatives gain traction. The macro story remains intact. By 2030, India will add 200 million urban residents. The government's "Housing for All" mission, while ambitious, has created irreversible momentum toward formalization and financial inclusion. Interest rates, after a painful hiking cycle, are expected to moderate. These aren't just cyclical tailwinds—they're structural transformations that will play out over decades.

PNB Housing's strategic positioning for this future is both logical and risky. The three-pronged approach—prime lending for stability, emerging markets for growth, affordable housing for differentiation—makes sense on paper. But execution requires capabilities the company is still building. Can a traditionally conservative lender develop the risk appetite for truly affordable housing? Can a cost-heavy organization achieve the efficiency needed for competitive pricing? Can a company without a clear technological edge compete with digital-native players?

The management transitions ahead will be crucial. The current leadership, brought in during the Carlyle era, has successfully navigated the ownership transition and strategic repositioning. But the next phase requires different skills—not just managing transformation but driving growth, not just reducing risk but taking calculated bets, not just satisfying stakeholders but delighting customers.

The competitive dynamics are evolving rapidly. The traditional boundaries between banks, NBFCs, and housing finance companies are blurring. Co-lending partnerships allow small fintechs to access bank funding while banks access origination capabilities. Technology platforms enable instant credit decisions and seamless customer experiences. In this environment, being a traditional housing finance company may no longer be enough.

Yet PNB Housing has underappreciated strengths. The trust associated with the PNB brand, while diminished among urban millennials, remains strong in Tier-2 and Tier-3 cities where the company is expanding. The physical distribution network, expensive to maintain, provides touchpoints that purely digital players can't match. The experience in navigating Indian bureaucracy and regulation, hard-won over decades, creates barriers that new entrants struggle to overcome.

The next chapter will likely see consolidation in India's housing finance sector. Subscale players will struggle to compete on technology and funding costs. Over-leveraged players will face asset quality pressure in the next downturn. PNB Housing, with its clean balance sheet and stable funding, could emerge as a consolidator rather than a target. Strategic acquisitions in affordable housing or specific geographies could accelerate growth and provide economies of scale.

The technology roadmap deserves special attention. While PNB Housing has invested in digital capabilities, the next frontier is artificial intelligence and machine learning for credit underwriting, particularly in affordable housing where traditional metrics don't work. The company that cracks alternative data—from mobile phone usage to social media behavior to utility payment patterns—will have a sustainable advantage in serving India's informal economy.

Environmental, social, and governance (ESG) considerations are becoming increasingly important. PNB Housing's affordable housing focus naturally aligns with social impact, but the company needs to articulate this story better. International investors, particularly the sovereign wealth funds now on the shareholder register, increasingly evaluate investments through an ESG lens. A clear sustainability strategy could reduce the cost of capital and attract patient, long-term investors.

The regulatory environment will continue evolving. The Reserve Bank of India's scale-based regulation for NBFCs, while not directly applicable to housing finance companies, signals increasing scrutiny of systemic risk. The National Housing Bank's guidelines on affordable housing could become more prescriptive. The government's push for financial inclusion might come with directed lending requirements. Navigating this evolving landscape requires not just compliance but anticipation and influence.

For all stakeholders—employees, customers, investors, regulators—PNB Housing represents something larger than a single company. It's a test case for whether India's traditional financial institutions can transform themselves for the digital age. It's an experiment in whether public sector heritage and private sector efficiency can coexist. It's a bet on whether serving India's underserved millions can be both profitable and impactful.

The lessons from PNB Housing's journey apply broadly to emerging market financial services. First, transformation is possible but takes longer and costs more than expected. Second, regulatory risk can trump business fundamentals, making stakeholder management as important as strategy. Third, competitive advantage in financial services increasingly comes from serving segments others can't or won't, not from doing the same things better.

As we look toward 2030, several scenarios are possible. In the optimistic case, PNB Housing successfully scales affordable housing, achieves operating leverage through technology, and emerges as a leading player in India's formalized mortgage market. The stock re-rates to 2x book value, generating substantial returns for patient investors.

In the pessimistic case, competition intensifies, margins compress, and PNB Housing remains subscale in all segments. The company muddles through, generating returns below the cost of capital, until it's eventually acquired or merged with a stronger player.

The most likely scenario lies between these extremes. PNB Housing will probably succeed in building a profitable affordable housing franchise while maintaining a stable prime lending business. Returns will improve but not dramatically. The company will remain a solid, if unspectacular, player in India's housing finance sector—no longer transforming but sustainably growing.

What's certain is that India's housing finance story is still being written. The demand is real, the need is urgent, and the opportunity is massive. Whether PNB Housing captures its fair share of this opportunity depends on decisions being made today in boardrooms and branches, in technology labs and training centers, in regulatory offices and customer homes.

The company that started as a sleepy government subsidiary, transformed into a private equity play, and emerged as a public market story, now faces its greatest challenge: becoming a sustainable, profitable, customer-centric financial institution. It's a challenge that many attempt but few achieve. The next five years will determine whether PNB Housing joins the few or remains among the many.

For India's millions still dreaming of owning a home, the stakes couldn't be higher. PNB Housing's success or failure won't just affect shareholders and employees—it will impact whether the promise of "Housing for All" becomes reality or remains aspiration. In that sense, this isn't just a business story. It's a story about development, inclusion, and the kind of country India is becoming.

The journey continues, and the destination remains uncertain. But one thing is clear: PNB Housing Finance's story, like India's, is far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube