AU Small Finance Bank: From Rajasthan Vehicle Financier to India's Banking Disruptor

I. Introduction & Episode Roadmap

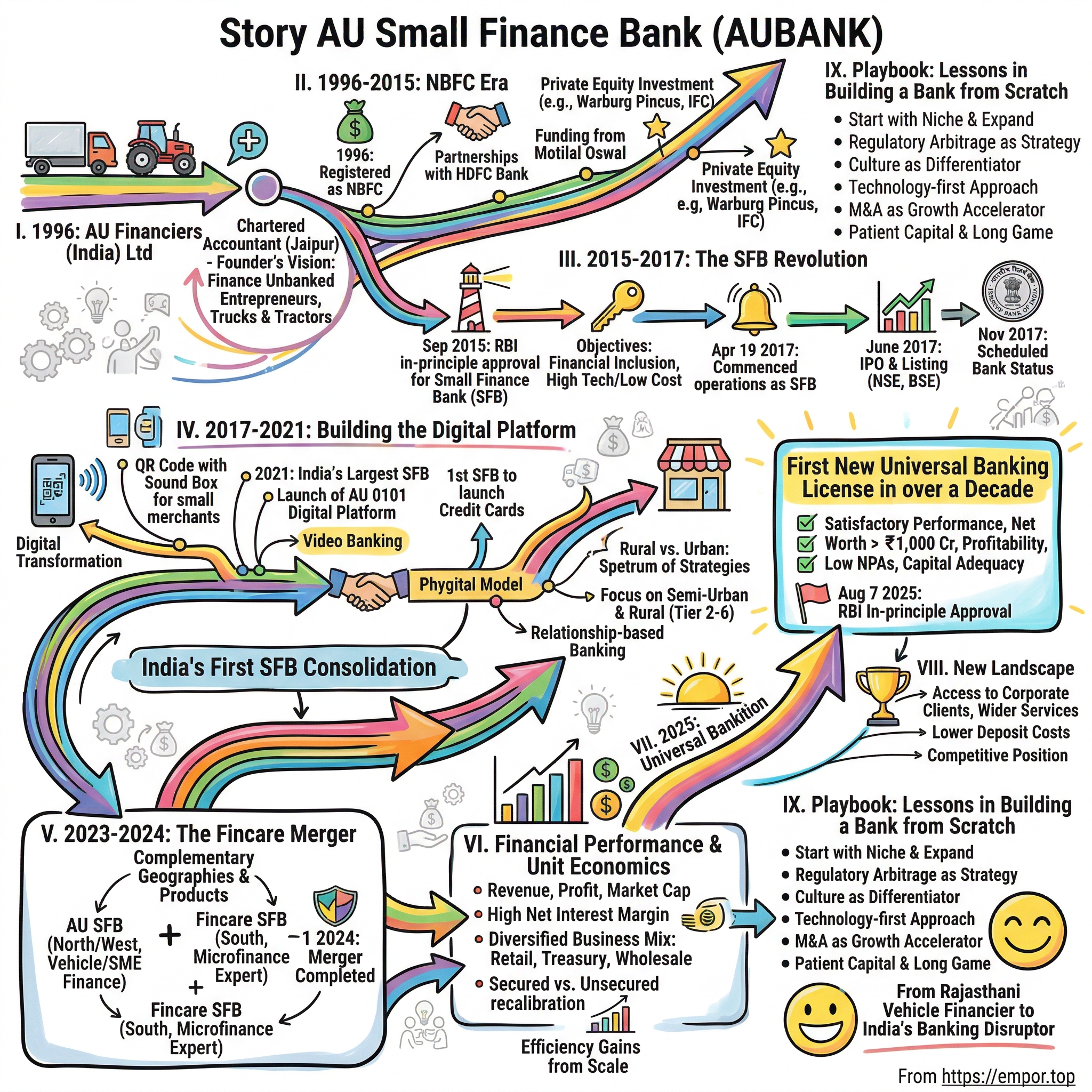

Picture this: A chartered accountant in Jaipur, 1996, sitting in a modest office, sketching out plans to finance trucks and tractors for local entrepreneurs. Fast forward to 2025—that same company has become India's largest small finance bank with a market capitalization exceeding ₹54,000 crores, and just received the nation's first new universal banking license in over a decade.

The audacious question at the heart of this story isn't just how Sanjay Agarwal built a bank without any banking background—it's how a vehicle finance company from Rajasthan became the template for India's financial inclusion revolution. This August, when the Reserve Bank of India granted AU Small Finance Bank its in-principle approval to become a universal bank, it wasn't just validating one company's journey. It was acknowledging that the future of Indian banking might look nothing like its past. Indeed, on August 7, 2025, AU Small Finance Bank became the first SFB to receive RBI's in-principle approval to transition into a universal bank—a moment that marks not just a regulatory milestone, but the culmination of a three-decade entrepreneurial odyssey that began with financing trucks and tractors in the dusty outskirts of Jaipur.

This story is fundamentally about three transformations. First, how India's financial landscape shifted from a state-dominated banking oligopoly to a vibrant ecosystem where a non-banking finance company could evolve into a full-fledged bank. Second, how technology enabled a lender focused on vehicle finance to serve millions of India's unbanked. And third, how regulatory frameworks designed for financial inclusion accidentally created pathways for some of India's most innovative financial institutions.

The arc we'll trace begins with a chartered accountant's conviction that India's economic miracle couldn't happen without bringing credit to its smallest entrepreneurs. It follows AU through its metamorphosis from NBFC to small finance bank, through India's first-ever merger between two SFBs, and ultimately to the nation's first new universal banking license issued by RBI in 11 years. Along the way, we'll examine the economics of serving India's underbanked, the regulatory chess game of moving up the banking hierarchy, and what AU's journey tells us about the future of Indian finance.

But perhaps most importantly, this is a story about timing. AU didn't just ride India's financial inclusion wave—it helped create it. And now, as it prepares to shed its "small finance bank" label and compete with the HDFCs and ICICIs of the world, we're witnessing the birth of what might be India's next major private sector bank. The question isn't whether AU can make this transition—the regulatory approval validates AU's robust business model and sound governance, and will enable it to lower deposit costs and operate in less risky asset classes. The question is whether a bank built to serve India's forgotten millions can maintain its soul while chasing universal banking ambitions.

II. The Founder's Story & Pre-Banking Origins (1996–2015)

In the mid-1990s, Rajasthan's economy ran on wheels—literally. Trucks carried marble from Makrana, tractors tilled fields in Shekhawati, and three-wheelers ferried goods through the narrow lanes of Jaipur's old city. Yet for most small transporters and farmers, buying a vehicle meant navigating a maze of moneylenders charging usurious rates or banks that demanded collateral worth twice the loan amount. This was the India that Sanjay Agarwal saw when he decided to leave his comfortable chartered accountancy practice in 1996.

Agarwal wasn't your typical financier. A merit-holder chartered accountant and first-generation entrepreneur, he carried none of the baggage of traditional banking families. What he did carry was an almost missionary zeal about financial inclusion before the term became fashionable. His founding vision, articulated in early company documents, spoke of "contributing to nation-building" by financing the "entrepreneurship aspirations of the unreached and unbanked masses." This wasn't corporate speak—it was personal conviction born from watching small entrepreneurs struggle for capital in one of India's most entrepreneurial states.

The name he chose for his venture revealed both ambition and pragmatism. "AU" derived from Aurum, the Latin word for gold, with its chemical symbol considered auspicious in Indian business culture. In 1996, AU Financiers (India) Ltd was established as a vehicle finance company and registered as a non-banking financial company (NBFC). The initial capital was modest, the office in Jaipur even more so, but the opportunity was enormous. What made Rajasthan perfect for AU's model was precisely what made it unattractive to established banks. The lack of institutions to cater to the financial needs of people in rural and semi-urban Rajasthan created a vacuum that AU rushed to fill. The state's entrepreneurial culture—from marble traders to transport operators—meant there was genuine credit demand, just no supply at reasonable rates.

Headquartered in Jaipur, Rajasthan, the retail-focused Non-Banking Finance Company for two decades provided speedy and customised financial solutions to rural and urban population. The NBFC model offered AU crucial advantages: lighter regulation compared to banks, freedom to price loans based on risk, and the ability to move fast. But it also came with limitations—no ability to take deposits, higher cost of funds, and a ceiling on how large the business could grow.

The early years were about building trust, one loan at a time. AU's approach was radically different from traditional lenders. Where banks demanded collateral and extensive documentation, AU focused on cash flows and character assessment. A truck driver with steady contracts but no property to mortgage could get financing. A small trader expanding into neighboring districts could access working capital. This wasn't charity—it was smart risk assessment based on understanding local businesses.

By the mid-2000s, AU had caught the attention of sophisticated investors. Private equity companies that provided venture capital, including Warburg Pincus and International Finance Corporation, recognized what Agarwal was building. These weren't just financial investors—they brought credibility, governance standards, and ambitions for scale. The International Finance Corporation's involvement was particularly significant, signaling that AU's model of financial inclusion had global relevance.

Agarwal's entrepreneurial spirit led him to get a partnership with HDFC Bank and funding from Motilal Oswal, which helped his company expand. These partnerships weren't just about capital—they were about learning from India's best-run financial institutions while maintaining AU's unique culture and focus.

By 2015, AU Financiers had built an impressive track record: nearly two decades of profitable growth, a deep understanding of India's underbanked segments, and operational excellence in vehicle finance. But Agarwal knew that to truly fulfill his vision of financial inclusion, AU needed something more fundamental—the ability to mobilize deposits. The company had proven it could lend responsibly to India's masses. Now it needed to become their banker.

The timing couldn't have been better. The Reserve Bank of India, under Governor Raghuram Rajan, was about to launch one of the most ambitious experiments in Indian banking history—small finance banks. For AU, this wasn't just an opportunity to grow. It was validation that their model of serving the unbanked wasn't just viable—it was essential for India's economic future.

III. The Small Finance Bank Revolution (2015–2017)

The auditorium at the Reserve Bank of India's Mumbai headquarters was packed on the morning of September 16, 2015. Banking executives, journalists, and analysts had gathered to witness history—the announcement of India's first small finance bank licenses in over a decade. When RBI Deputy Governor S.S. Mundra read out AU Financiers' name among the ten successful applicants, Sanjay Agarwal, watching the livestream from Jaipur, knew everything was about to change. The RBI's framework for small finance banks was revolutionary in its simplicity and ambition. The objectives were clear: extending banking to unserved and underserved sections of the population, addressing the credit needs of marginal farmers, small businesses, and micro industries using a "high technology-low cost operation approach." The objectives of setting up of small finance banks will be for furthering financial inclusion by provision of savings vehicles primarily to unserved and underserved sections of the population.

For AU, the requirements read like a validation of their existing model. Small finance banks would be required to extend 75 per cent of its Adjusted Net Bank Credit (ANBC) to the sectors eligible for classification as priority sector—a mandate AU was already exceeding in practice. The minimum capital requirement, the technology infrastructure, the rural focus—AU had been building these capabilities for two decades.

The competition was fierce. There were 72 applicants vying for licenses, including established microfinance institutions, local area banks, and other NBFCs. An external advisory committee headed by Usha Thorat would evaluate the license applications. What set AU apart wasn't just its track record but its vision alignment with RBI's objectives.

When the results were announced on September 17, 2015, AU Financiers was among the ten successful applicants granted in-principle approval. The process of licensing culminated in granting in-principle approval to ten applicants and they have since established the banks. This wasn't just a license—it was a transformation. AU would now be able to accept deposits, issue debit cards, offer internet banking, and most importantly, access low-cost funds through savings and current accounts.

The eighteen months between receiving the license and commencing operations as a bank were perhaps the most intense in AU's history. Converting an NBFC into a bank meant rebuilding almost everything—technology systems, compliance frameworks, product portfolios, even the organizational culture. Every process had to be reimagined through the lens of banking regulations.

On April 19, 2017, AU Small Finance Bank officially commenced operations. The transformation was immediate and dramatic. From 403 touchpoints in 8 states and 2 union territories, AU was now a bank—able to offer the full spectrum of financial services. Two months later, on June 29, 2017, came another milestone: the IPO and public listing on NSE and BSE.The IPO was a defining moment. The AU Financiers IPO was subscribed 53.6 times by June 30, 2017, with the retail portion oversubscribed 3.52 times and institutional investors showing overwhelming interest. The offering raised Rs 1,912.51 crores at a price of Rs 358 per share. For a company that started as a small NBFC in Jaipur, this level of investor enthusiasm validated everything AU had been building.

By November 1, 2017, AU achieved another milestone—scheduled bank status from the Reserve Bank of India, becoming a Fortune India 500 Company. This wasn't merely ceremonial. Scheduled bank status meant AU could now participate in the RBI's liquidity operations, access refinance from the central bank, and most importantly, signal to depositors that it was now part of India's formal banking system.

The regulatory trade-offs of becoming a small finance bank were significant but manageable. The requirement to extend 75 per cent of its Adjusted Net Bank Credit to priority sectors actually aligned with AU's existing business model. The mandate that 25% of branches be located in unbanked areas wasn't a burden—it was an opportunity to expand into markets AU understood better than most traditional banks.

What made AU's transition unique wasn't just the speed of execution but the cultural transformation. The company that had operated for two decades as an NBFC—with its entrepreneurial culture, quick decision-making, and deep customer relationships—now had to embrace the discipline, compliance requirements, and public scrutiny that came with being a bank. Every loan officer who had built relationships over chai and conversations now had to master core banking systems. Every branch that had operated with the flexibility of a finance company now had to meet the exacting standards of banking regulation.

The transformation from NBFC to SFB wasn't just about getting a banking license—it was about proving that India's financial inclusion agenda could be profitable, scalable, and sustainable. As AU prepared to expand its footprint across India, it carried with it the lessons learned from two decades of serving India's underbanked. The vehicle finance company from Jaipur had become a bank, but its next challenge would be even greater: competing with established players while maintaining the soul of what made AU special.

IV. Building the Digital Banking Platform (2017–2021)

The WhatsApp message arrived at 11:47 PM on March 24, 2020—the first night of India's nationwide COVID-19 lockdown. A vegetable vendor in Bhilwara, one of AU Bank's earliest vehicle loan customers, was asking if he could access his savings through his phone. His branch was 40 kilometers away, public transport had stopped, and he needed money for supplies. This single message would accelerate AU's digital transformation by years.

When AU commenced operations as a small finance bank in April 2017, its technology infrastructure was adequate for an NBFC but primitive by banking standards. After bagging the Small Finance Bank license in 2015, Au Financiers commenced its journey as an SFB on 19th April 2017. The initial footprint of 403 touchpoints in 8 states and 2 union territories represented decades of relationship building, but in the digital age, physical presence alone wouldn't suffice.

The first phase of AU's digital journey focused on basics—core banking implementation, internet banking, mobile apps. But AU's leadership understood something crucial: their customers weren't the urban millennials that most digital banking platforms targeted. They were truck drivers checking loan balances between hauls, small shop owners reconciling accounts after closing time, farmers transferring money to input suppliers. The technology had to work on basic smartphones, with patchy internet, in multiple languages.

By 2019, AU had launched its first major digital initiative with a distinctly Indian flavor. The QR Code with Sound Box wasn't just another payment solution—it addressed a specific pain point. Small merchants couldn't always check their phones during busy periods, but the sound box would announce payments in their local language, building trust in digital transactions. Within months, thousands of small retailers who had never used POS machines were accepting digital payments through AU's solution. The launch of AU 0101 in 2021 marked AU's digital coming of age. AU Small Finance Bank, India's largest SFB, launched a massive advertising strategy dubbed "BADLAAV Humse Hai" and unveiled its cutting-edge digital banking platform AU 0101 during the event, marking the advent of 'nextgen' banking by allowing customers to access a complete complement of financial services online, featuring face-to-face interaction with a banker via video chat.

In 2021, the Bank became the Largest Small Finance Bank of the country and evolved its positioning from 'Chalo Aage Badhein' to 'Badlaav Humse Hai'. The new tagline, which is also the Bank's first integrated brand campaign, resonates well with its spirit of challenging the status quo. Along with the launch of the brand campaign, digital platform AU 0101, Credit Card and QR Code with Sound Box were also unveiled.

The name AU 0101 itself was clever—binary code for the digital age, yet simple enough for non-technical users to remember. But what made it revolutionary wasn't the technology—it was the understanding that India needed both digital and human touch. One of the most distinctive features of AU 0101 is Video Banking, wherein customers can directly connect with AU's video bankers from the comfort of their homes.

The credit card launch was equally significant. AU Bank is the first among SFBs to launch its own credit card. AU Bank Credit Card comes in four variants - Altura, Altura Plus, Vetta, and Zenith, to match the changing needs of the first-timer, new age, digitally savvy customers. This wasn't just about product expansion—it signaled that AU could now compete with universal banks in lucrative fee-generating businesses.

Then came COVID-19, and everything accelerated. Branch visits plummeted, digital adoption soared, and AU's investments in technology suddenly looked prescient. The bank that had built its reputation on personal relationships now had to maintain those connections through screens. Video banking, which might have taken years to gain acceptance, became essential overnight.

The pandemic also revealed AU's operational resilience. While many lenders struggled with collections and asset quality, AU's deep customer relationships—built over decades—paid dividends. Borrowers who had multiple loans prioritized repaying AU because of the trust built over years. The bank's rural and semi-urban focus, initially seen as a weakness during lockdowns, proved to be a strength as these markets recovered faster than metros.

By 2021, AU had transformed from a traditional lender with digital capabilities to a digital-first bank with a human touch. The numbers validated the strategy—digital transactions grew exponentially, cost-to-income ratios improved, and customer acquisition accelerated. But more importantly, AU had proven that financial inclusion and digital innovation weren't contradictory—they were complementary.

The stage was set for AU's next big move. With a robust digital platform, expanding product suite, and proven execution capabilities, AU was ready to pursue growth through acquisition—a strategy that would culminate in India's first-ever merger between two small finance banks.

V. The Fincare Merger: India's First SFB Consolidation (2023–2024)

The conference room at AU's Mumbai office was unusually crowded on the evening of October 28, 2023. Investment bankers, lawyers, and AU's senior leadership had been negotiating for 72 straight hours. At stake was a deal that would reshape India's small finance banking landscape—the merger with Fincare Small Finance Bank. When the final signatures were affixed at 11:47 PM, AU had just orchestrated India's first-ever consolidation between two small finance banks. The announcement on October 29, 2023, created market cap of US$6.3 billion. The strategic rationale was compelling: leveraging "complementary geographic footprints and product offerings." AU, strong in North and West India with vehicle and SME finance, would gain Fincare's microfinance expertise and South Indian presence. Fincare, which had been preparing for its own IPO, would get access to AU's technology platform and listed status.

The numbers told the story of complementarity. As of December 31, 2023, Fincare Small Finance Bank's Gross Loan Portfolio amounted to ₹13,352 Crore, while Deposits reached ₹9,734 Crore. The Bank efficiently caters to a customer base exceeding 59 Lakhs+, supported by a robust team of over 14,800 dedicated employees. Fincare's portfolio was largely concentrated in the microfinance segment—54% microfinance, 19% micro-business loans, 14% affordable housing, and 10% gold loans.

The deal structure was elegant in its simplicity: an all-stock merger with 579 AU shares for every 2,000 Fincare shares held. This valued Fincare at around Rs 4,416 crore—a premium that reflected both Fincare's growth potential and the strategic value of consolidation. For Fincare's investors, including LeapFrog Investments and TA Associates, the merger offered liquidity and upside through AU's listed shares.

But mergers in banking are never just about numbers—they're about culture, systems, and people. Fincare had started as a microfinance institution serving the bottom of the pyramid, with 93.6% of its microfinance loans serving rural areas. AU had built its reputation on vehicle finance and SME lending. These weren't just different business models—they were different philosophies of banking.

The integration planning revealed the complexity ahead. Fincare operated 1,292 banking outlets across nearly two dozen states, with different core banking systems, product offerings, and customer profiles. The merger would require harmonizing interest rates, integrating technology platforms, training thousands of employees, and most critically, maintaining service continuity for millions of customers.

Leadership structure became crucial for success. Rajeev Yadav, former MD & CEO of Fincare SFB, was designated as Deputy CEO of AU SFB and would continue to lead all key asset businesses of Fincare SFB, now housed within the Fincare Unit at AU SFB. Meanwhile, Uttam Tibrewal was promoted to Deputy CEO and Executive Director, ensuring continuity in AU's existing operations.

On April 1, 2024, India witnessed its first merger between two small finance banks completed. The combined entity now boasted a balance sheet exceeding ₹1.2 lakh crores, over 1 crore customers, 2,350 touchpoints, and nine states with 100+ locations each. Post-merger, all 5.9 million customers of Fincare SFB would be able to experience and enjoy the best-in-class digital services and flagship products of AU SFB including its offerings like credit cards, QR code and video banking.

The market's initial reaction was mixed—AU's shares declined 8% on announcement as investors digested dilution and integration risks. But the strategic logic was undeniable. In a cut-throat deposit market where SFBs had been offering higher rates to attract depositors, scale mattered. The merged entity could optimize branch networks, cross-sell products, and most importantly, compete more effectively for the universal banking license that AU coveted.

The Fincare merger wasn't just about getting bigger—it was about becoming complete. AU's micro loan book, even after the acquisition, was less than 10% of the total book—a relatively conservative exposure at a time when the microfinance sector faced multiple headwinds. Yet it gave AU credibility in financial inclusion, a critical requirement for regulatory approvals.

For the Indian banking sector, the merger set a precedent. It proved that consolidation among small finance banks was not only possible but potentially value-creating. As other SFBs struggled with scale and profitability, AU had shown a path forward—not through organic growth alone, but through strategic combinations that created synergies while maintaining focus on financial inclusion.

VI. Financial Performance & Unit Economics

The numbers on AU's Q3 FY25 earnings call could have been from an entirely different institution than the vehicle finance company that went public in 2017. Market cap: ₹54,149 crores. Revenue: ₹16,673 crores. Profit: ₹2,184 crores. But what made these numbers remarkable wasn't their size—it was the transformation they represented in AU's fundamental economics. The business mix evolution tells the story of transformation: Retail Banking now comprises 76% of revenue (9M FY25), Treasury 13%, Wholesale Banking 9%, and Others 2%. This distribution reflects AU's evolution from a monoline vehicle financier to a diversified financial institution. Each segment tells its own story of strategic choices and economic realities.

The headline number that catches every analyst's attention is the Net Interest Margin at 5.9% (Q3FY25)—among the highest in Indian banking. This isn't just about charging high rates; it's about AU's unique positioning. While universal banks with CASA ratios above 40% struggle to maintain NIMs above 3.5%, AU achieves nearly double that despite a CASA ratio of just 31%. The secret lies in the asset side—AU's deep understanding of credit risk in underserved segments allows it to price loans appropriately while maintaining asset quality.

The Q3FY25 results showcased this balance: PAT growth of 41% YoY to ₹528 crores, driven by controlled credit costs and operational efficiency improvements. The Cost to Income ratio at 54.4% had declined by 886 basis points YoY—a dramatic improvement that reflected both scale benefits from the Fincare merger and technology investments paying off.

But the most revealing metrics are in the details. Gross NPA ratio at 1.7% (March 2024) rising slightly to 2.31% by Q3FY25 reflects the integration of Fincare's microfinance portfolio and broader sectoral stress. Yet the Provision Coverage Ratio at 80% and net NPA at just 0.91% show conservative provisioning. AU carries additional contingency provisions of ₹17 crore and floating provisions of ₹41 crore specifically for the MFI portfolio—belt and suspenders approach to risk management.

The secured vs. unsecured mix reveals strategic recalibration. Secured businesses (Retail Commercial) grew by 22% YoY whereas Unsecured businesses (primarily MFI and Credit Card) de-grew by 23% YoY driven by cyclical slowdown in MFI and calibration in credit card book. This isn't retreat—it's prudent risk management in a challenging credit environment.

The deposit franchise metrics tell another story. Total deposits of ₹1,12,260 crore with CASA at 31% might seem weak compared to established private banks. But dig deeper: CASA plus Retail term deposits constitute 65%, and including non-callable bulk deposits, it reaches 80%. This granular deposit base, built customer by customer in rural and semi-urban markets, provides stable, albeit higher-cost, funding.

The efficiency gains from scale are evident. Despite expanding to 2,400 touchpoints across 21 states and 4 union territories with 49,000 employees, the cost-to-income ratio has consistently declined. Digital channels now handle routine transactions, branches focus on relationship building and complex products, and the cost per transaction has plummeted.

Return metrics validate the model: ROA at 1.5% and ROE at 13.1% might seem modest compared to some peers, but they're achieved with a Capital Adequacy Ratio of 20.1%—nearly double the regulatory requirement. This fortress balance sheet positions AU for growth without dilution, a luxury most fast-growing banks don't have.

The comparison with peers reveals AU's unique position. Trading at 3.17x book value, AU commands a premium to most other SFBs but trades at a discount to established private banks. The market is essentially pricing AU somewhere between a small finance bank and a universal bank—exactly where it sits in its evolution journey. The priority sector lending economics deserve special attention. As noted earlier, AU's PSL loans were 80 per cent—well above the 75% requirement for SFBs. While this might seem like regulatory burden, AU has turned it into competitive advantage. These loans, properly underwritten and priced, generate NIMs exceeding 7% while fulfilling social obligations. The upcoming transition to universal banking will reduce this requirement to 40%, freeing up capital for higher-margin corporate lending.

The treasury operations, contributing 13% of revenue, reveal sophisticated asset-liability management. In a rising rate environment, AU has managed its ALM profile to benefit from repricing while maintaining stable funding costs. The bank maintains a Liquidity Coverage Ratio of 116%, well above requirements, with additional buffers in high-quality liquid assets.

What's most impressive about AU's financials isn't any single metric—it's the consistency. Quarter after quarter, AU delivers predictable earnings growth, stable asset quality, and improving efficiency. In a sector known for volatility, this predictability commands a premium.

The unit economics tell the real story: AU has cracked the code of making money while serving India's underbanked. Every rural branch that breaks even in 18 months, every microfinance loan that generates 15% returns with 2% credit costs, every small business loan that creates a 20-year customer relationship—these aren't just transactions, they're proof points that financial inclusion can be profitable at scale.

VII. The Universal Banking Ambition & Regulatory Navigation

The text message from the Reserve Bank of India arrived at 4:47 PM on August 7, 2025, but Sanjay Agarwal had been preparing for this moment for three decades. "In-principle approval granted for transition to universal bank"—fifteen words that represented not just regulatory approval, but validation of AU's entire journey from vehicle financier to India's newest full-service bank.

AU Small Finance Bank becomes the first SFB to receive RBI's in-principle approval to transition into a universal bank. This wasn't just another license—it was the first full-fledged banking license issued by RBI in 11 years, making AU's achievement even more remarkable.

The path to universal banking had been carefully orchestrated. In April 2024, RBI laid out norms on the voluntary transition path for small finance banks into universal banks. The criteria were stringent: minimum five years of satisfactory performance, net worth exceeding ₹1,000 crore, profitability in the previous two financial years, low NPAs, and robust capital adequacy. AU didn't just meet these criteria—it exceeded them comprehensively.

What universal banking means for AU is transformational. The removal of the 'Small Finance Bank' tag will enable AU to lower its deposit costs—no longer will they need to offer premium rates to overcome the perception disadvantage. The priority sector lending requirement drops from 75% to 40%, freeing up funds for deployment in the mid-corporate lending segment, earning attractive yields in the range of around 12 per cent.

Most significantly, AU will now be able to service corporate clients and offer a wider bouquet of financial services. The corporate banking opportunity alone could double AU's addressable market. Large corporations that wouldn't consider banking with an SFB will now evaluate AU alongside established private banks.

The regulatory hurdles AU overcame read like a checklist of Indian banking's highest standards. Gross and Net NPA thresholds, capital adequacy requirements, corporate governance standards—each requirement validated AU's operational excellence. AU met all the eligibility criteria and applied for the conversion in September last year, demonstrating confidence in their readiness.

But the real story is how AU navigated the unwritten rules of Indian banking. Building relationships with regulators through transparency, maintaining conservative accounting practices when aggressive growth was tempting, investing in compliance infrastructure before it was mandatory—these decisions, invisible to outsiders, paved the way for regulatory approval.

"This in-principle approval acknowledges not just our ability to grow, but to grow responsibly," said Sanjay Agarwal, MD & CEO, AU SFB. "It is a testament to AU's strength in reaching widely, integrity in serving wisely, and resilience to shine across economic cycles."

The competitive dynamics shift dramatically with universal banking status. AU no longer competes just with other SFBs for deposits—it goes head-to-head with HDFC Bank, ICICI Bank, and Axis Bank. But it also means AU can now compete for corporate relationships, international banking services, and complex financial products that generate high fees.

The technology advantage becomes even more critical in this new landscape. While established private banks struggle with legacy systems—some still running on mainframes from the 1990s—AU's modern technology stack built over the last seven years provides incredible flexibility. API-first architecture, cloud-native applications, real-time data analytics—these aren't buzzwords at AU, they're operational reality.

Yet challenges remain. Two more SFBs have also applied for such conversion—Ujjivan SFB and Jana SFB—with applications still pending with the regulator. The race to scale and establish market position before others receive approval adds urgency to AU's expansion plans.

The talent war intensifies too. Universal banking requires capabilities AU hasn't needed before—corporate treasury specialists, investment bankers, forex dealers. Attracting this talent while maintaining AU's entrepreneurial culture presents a delicate balance.

Regulatory navigation doesn't end with the universal banking license. AU must now manage a more complex compliance landscape—Basel III norms, exposure limits, international banking regulations. The in-principle approval is just the beginning; AU still needs to fulfill operational and regulatory conditions for full universal banking rollout.

What has worked in AU SFB's favour is its scale and the relatively low share of unsecured loans in its portfolio. This conservative approach, sometimes criticized by growth-focused analysts, now looks prescient as the microfinance sector faces headwinds.

The timing of the approval is particularly significant. As India pushes toward a $5 trillion economy, the need for banks that can serve both ends of the economic spectrum—from microfinance to corporate banking—has never been greater. AU's unique positioning, with roots in financial inclusion and ambitions in universal banking, makes it a template for 21st-century Indian banking.

VIII. Geographic & Digital Expansion Strategy

The map on the wall of AU's strategy room tells a story of calculated expansion. Red pins mark AU's original strongholds in Rajasthan and Gujarat. Blue pins show Fincare's southern footprint. Green pins indicate the next frontiers. By December 2024, AU's reach had expanded to 2,400 touchpoints in 21 states and 4 union territories—but the real transformation wasn't in the pin count, it was in how each location connected to AU's digital backbone.

The phygital model—physical plus digital—sounds like consultant-speak until you see it in action. In Udaipur's old city, an AU branch occupies just 800 square feet, but serves 5,000 customers. The secret: most transactions happen on phones, the branch is for relationships. The branch manager knows every small business owner by name, but their loan applications are processed by AI models running in Mumbai data centers.

Rural versus urban isn't a binary choice for AU—it's a spectrum of strategies. In villages, AU's banking correspondents use biometric devices to serve customers who've never entered a bank. In metros, AU's video banking serves young professionals who never want to enter one. Different products for different Indias, united by a common technology platform.

The post-merger integration revealed the power of complementary geographies. AU's strength in vehicle finance in North India perfectly complemented Fincare's microfinance expertise in the South. Rather than forcing standardization, AU maintained distinct approaches—Fincare units continue operating with their proven models while gradually adopting AU's technology infrastructure. The footprints expanded from 403 Touchpoints in 8 States and 2 Union Territories in 2017 to 2400 Touchpoints in 21 States and 4 Union Territories as on 31st December 2024. But raw expansion isn't the strategy—intelligent clustering is. AU focuses on achieving critical mass in specific geographies before expanding further. Nine states now have over 100 locations each, providing economies of scale in operations, marketing, and risk management.

The digital expansion runs parallel to physical growth. Post-merger digital services include credit cards, QR codes, and video banking—capabilities that turn every smartphone into a potential banking touchpoint. The AU 0101 platform now serves as the backbone for all digital interactions, processing millions of transactions daily.

Competition from fintechs and payment banks has forced AU to innovate constantly. Where Paytm Payments Bank offers convenience, AU offers trust. Where Pine Labs provides payment solutions, AU provides credit. The strategy isn't to out-fintech the fintechs but to combine their innovation with banking's stability.

The southern expansion, accelerated by the Fincare merger, reveals AU's ambition. As of December 2023, the Southern region surpassed Rs 3,000 crore in deposits. Bangalore alone contributes to around Rs 9 lakh crores of deposits of the State and remains a key city in AU SFB's expansion plan. The bank aimed to reach approximately 37 branches in South India by March 2024—a target exceeded through the Fincare integration.

We have established a well-entrenched contiguous distribution franchise with 61% of our branches in rural and semi-urban areas (Tier 2 to Tier 6). This isn't corporate social responsibility—it's core strategy. These markets, ignored by larger banks focused on metros, offer higher margins, lower competition, and deeper customer loyalty.

The technology investments enable this distributed model to work efficiently. Every branch, regardless of size or location, connects to the same core banking platform. A customer opening an account in rural Bihar can access services in urban Bangalore seamlessly. This interoperability, taken for granted in developed markets, is revolutionary in India's fragmented banking landscape.

The expansion strategy also reflects changing customer behaviors. The post-COVID world accelerated digital adoption by a decade. Customers who would never have tried digital banking before 2020 now prefer it. AU's video banking, which might have seemed gimmicky pre-pandemic, now processes thousands of interactions daily.

What's most impressive about AU's expansion isn't its speed but its discipline. Every new geography is entered with clear metrics for success. Every digital feature is launched with specific adoption targets. Every branch opening is evaluated not just on immediate returns but on strategic value to the network.

The next phase of expansion, enabled by universal banking status, will test AU's model at new scales. Can the culture that worked with 1,000 branches work with 5,000? Can the technology platform that serves 10 million customers scale to 50 million? Can AU maintain its community banking ethos while competing nationally? These questions will define AU's next decade.

IX. Playbook: Lessons in Building a Bank from Scratch

If you were to distill AU's journey into a playbook for building a financial institution in the 21st century, it wouldn't read like a traditional banking manual. Instead, it would be a guide to patient capital deployment, regulatory arbitrage, and most importantly, understanding that banking is ultimately about trust, not transactions.

Lesson 1: Start with a niche and expand concentrically. AU didn't try to be everything to everyone from day one. It started with vehicle finance—a business Sanjay Agarwal understood deeply. Only after dominating this niche did AU expand into adjacent areas: SME loans, then microfinance, then retail banking. Each expansion built on existing capabilities while adding new ones. This concentric growth model reduced execution risk while building institutional knowledge.

Lesson 2: Regulatory arbitrage as strategy. AU's progression from NBFC to SFB to universal bank wasn't opportunistic—it was architected. Each regulatory level brought new capabilities (deposits, payments, forex) while imposing new obligations (priority sector lending, CRR/SLR). AU turned these obligations into advantages, using priority sector requirements to build deep rural relationships that became competitive moats.

Lesson 3: Culture as competitive advantage. In an industry where products are commodities and pricing is transparent, culture becomes the differentiator. AU's values of "Inclusivity, progress for all, simplicity, and action & urgency" aren't just wall posters—they're embedded in every process. The banker who stays late to help a first-time borrower fill forms, the credit officer who visits a defaulter's home to understand their situation rather than sending legal notices—these behaviors, multiplied across thousands of employees, create a culture that competitors can't replicate.

Lesson 4: Technology-first approach in a traditionally physical business. AU didn't digitize existing processes—it reimagined them. Video banking isn't just a Zoom call with a banker; it's a completely redesigned customer journey that combines the convenience of digital with the trust of human interaction. The QR code with sound box isn't just a payment device; it's a trust-building tool for merchants skeptical of digital payments.

Lesson 5: M&A as growth accelerator in a fragmented market. The Fincare merger wasn't just about scale—it was about capability acquisition. AU got microfinance expertise, southern presence, and most importantly, regulatory credibility in financial inclusion. The all-stock structure aligned interests, while maintaining separate units for different business models prevented culture clash.

Lesson 6: Patient capital and the long game. AU's investors—from early PE backers to public market shareholders—understood they were funding a decades-long transformation, not quarterly earnings. Promoter holding at 22.8% shows skin in the game while allowing institutional ownership to provide governance and growth capital. This balance between entrepreneurial drive and institutional discipline is rare in Indian banking.

Lesson 7: Managing multiple stakeholders. Banking is perhaps the most stakeholder-complex business. Regulators want safety, investors want returns, customers want service, employees want growth. AU's ability to balance these often conflicting demands—maintaining 20% capital adequacy for regulators while delivering 13% ROE for investors—demonstrates sophisticated stakeholder management.

The playbook also reveals what AU didn't do. It didn't chase every trend—no cryptocurrency ventures, no Buy Now Pay Later experiments during the hype cycle. It didn't expand internationally prematurely. It didn't diversify into non-banking businesses like insurance manufacturing or mutual funds. This discipline of saying no protected capital and management bandwidth for core banking growth.

The deeper lesson is about timing and patience. AU spent 20 years as an NBFC building capabilities before becoming a bank. It spent 7 years as an SFB proving its model before seeking universal banking license. This patient building of capabilities before seeking the next level of growth is antithetical to the "growth at all costs" mentality prevalent in startup culture.

The technology strategy deserves special attention. Rather than building everything in-house or outsourcing everything, AU chose a hybrid approach. Core banking from established vendors, customer-facing applications built internally, and cutting-edge capabilities through partnerships. This pragmatic approach balanced control with speed-to-market.

Risk management philosophy permeates the playbook. AU's approach isn't about avoiding risk—it's about understanding and pricing it correctly. The higher NIMs aren't just about charging more; they're about knowing your customer well enough to price risk accurately. The conservative provisioning isn't pessimism; it's preparedness for cycles.

What makes this playbook valuable isn't just what worked for AU—it's the framework for thinking about building financial institutions in emerging markets. The combination of financial inclusion with profitability, technology with human touch, growth with prudence provides a template that transcends geography and time.

X. Bear vs. Bull Case Analysis

The investment case for AU Small Finance Bank presents a fascinating study in contrasts. At 3.17x book value, the market is pricing in significant growth, but also significant risks. Let's examine both sides with the rigor they deserve.

The Bear Case:

The bears' primary concern is competition—and it's intensifying from every direction. Established private banks like HDFC and ICICI are moving down-market with digital offerings targeting AU's customer base. Fintechs are unbundling banking, offering specific products with better user experience and lower costs. New SFBs are emerging, and existing ones are scaling rapidly. In this environment, AU's margins face inevitable compression.

The regulatory risks are real and mounting. Priority sector lending constraints, even at the reduced 40% for universal banks, limit flexibility in asset allocation. Any regulatory tightening on microfinance or unsecured lending—both growing segments for AU—could impact growth and profitability. The integration of Fincare's microfinance portfolio comes just as the sector faces stress, with industry-wide credit costs rising.

Asset quality concerns keep bears awake at night. While AU's current NPAs seem manageable, the unsecured lending book is seasoning during an economic slowdown. The vehicle finance portfolio, AU's historical strength, faces headwinds from electric vehicle transition and shared mobility trends. Rural and semi-urban markets, AU's core, are more vulnerable to economic shocks and climate events.

Integration risks from the Fincare merger shouldn't be minimized. Merging two banks with different cultures, systems, and customer bases is complex. Technology integration, employee retention, and maintaining service quality during transition all present execution challenges. History is littered with financial mergers that destroyed value despite strategic logic.

The valuation at 3.17x book value prices in perfect execution. Any disappointment—a quarter of elevated credit costs, slower than expected loan growth, or regulatory surprises—could trigger significant multiple compression. With interest rates potentially peaking, the tailwind of rising NIMs may reverse.

The management key person risk is significant. AU's culture and strategy are deeply intertwined with founder Sanjay Agarwal's vision. While succession planning exists, the transition from founder-led to professionally managed institution is always challenging in Indian companies.

The Bull Case:

Bulls see AU's universal banking approval as a game-changer. AU Small Finance Bank becomes the first SFB to receive RBI's in-principle approval to transition into a universal bank, expanding its product reach and lending base. The removal of lending restrictions and access to corporate banking could double AU's addressable market. Going forward, the most significant change will be the removal of the 'Small Finance Bank' (SFB) tag, which will enable AU to lower its deposit costs. This, in turn, will allow the bank to operate in less risky asset classes, contributing to more stable profitability.

The massive underpenetrated market for financial services in India provides decades of growth runway. With 400 million+ underbanked Indians and credit-to-GDP ratio at just 55% compared to 150%+ in developed markets, the opportunity is generational. AU's proven ability to serve these segments profitably gives it first-mover advantage as these markets formalize.

The execution track record speaks for itself. From NBFC to SFB to universal bank, AU has successfully navigated every transition. The management team has consistently delivered on guidance, managed credit cycles, and integrated acquisitions. This isn't a story of potential—it's a demonstration of capability.

Technology platform advantages over legacy banks are structural and widening. While established banks struggle with decades-old core banking systems, AU's modern architecture enables rapid product launches, better risk management, and superior customer experience. This advantage compounds over time as technology becomes more central to banking.

The post-merger scale benefits are just beginning to materialize. Cost synergies from branch optimization, technology consolidation, and procurement scale will improve efficiency ratios. Revenue synergies from cross-selling products across expanded customer base will drive growth without additional customer acquisition costs.

In 2014, RBI had granted in-principle approval to Bandhan and IDFC (now IDFC First Bank) to operate as a universal bank. Both have created significant shareholder value since then. AU's universal banking license positions it to follow a similar trajectory, but from a stronger starting position.

The India macro story supports AU's growth. Financial inclusion is a government priority with programs like JAM (Jan Dhan-Aadhaar-Mobile) creating infrastructure for formal financial services. GST implementation is formalizing the economy, expanding AU's addressable market. Rising per capita income is driving credit demand across retail and SME segments.

The Synthesis:

The truth, as always, lies somewhere between extreme optimism and pessimism. AU is neither the next HDFC Bank nor a value trap. It's a well-executed financial institution in transition, facing real challenges but possessing genuine advantages.

The key variables to watch are execution on universal banking transition, asset quality through the credit cycle, and ability to maintain margins while scaling. The company trading at premium valuations suggests the market believes in the bull case, but any execution missteps will be punished severely.

For long-term fundamental investors, AU represents a play on India's financial inclusion with proven execution capability. The risks are real but manageable, the opportunity is large but competitive. The next 24 months, as AU transitions to universal banking while integrating Fincare, will likely determine whether the bulls or bears are right.

XI. Power & The Future of Indian Banking

Standing at the intersection of India's financial past and future, AU Small Finance Bank represents more than just another banking institution—it embodies the transformation of Indian finance from exclusion to inclusion, from physical to digital, from local to national.

India's financial inclusion imperative isn't just moral—it's economic. With 400 million+ underbanked Indians representing untapped economic potential, financial inclusion isn't charity but the unlocking of human capital. Every small business that gets working capital, every farmer who accesses formal credit, every family that builds savings represents economic activity that compounds through the economy.

The role of SFBs in India's $5 trillion economy ambition is critical but evolving. As institutions like AU graduate to universal banking, they carry with them the DNA of inclusion. Unlike traditional banks that might view priority sector lending as obligation, these institutions see it as opportunity. They've proven that serving the underserved isn't just socially responsible—it's profitable.

Can AU become India's JPMorgan Chase, or will it remain a regional champion? The answer depends on execution over the next decade. The universal banking license provides the regulatory framework, the Fincare merger provides scale, and the technology platform provides capability. What remains to be proven is whether AU can maintain its cultural differentiation while operating at national scale.

The competitive landscape will reshape dramatically. We're likely to see more consolidation among SFBs, with subscale players either merging or failing. The lines between banks, NBFCs, and fintechs will continue to blur. Digital public infrastructure like UPI and Account Aggregator will commoditize basic banking, forcing differentiation through service and risk management rather than product features.

Potential acquisition targets for AU could include other SFBs seeking scale, regional NBFCs with complementary portfolios, or fintech platforms with technology capabilities. Conversely, AU itself could become an acquisition target for larger private banks seeking to quickly build presence in underserved markets. The promoter holding at 22.8% makes hostile takeover unlikely but doesn't preclude friendly combination.

The next decade will bring challenges AU hasn't faced before. Digital currencies—whether crypto or central bank digital currency—could fundamentally alter banking economics. Embedded finance could make traditional banking touchpoints obsolete. Climate change could impact rural loan portfolios in unprecedented ways. Artificial intelligence could automate much of traditional banking, forcing redefinition of human roles.

Yet AU's journey from a Jaipur vehicle financier to India's newest universal bank provides confidence in its adaptability. The same pragmatism that led AU to focus on vehicle finance in 1996, to apply for SFB license in 2015, and to merge with Fincare in 2024 will guide future strategic choices.

The broader implications for Indian banking are profound. AU has proven that you don't need centuries of history or government backing to build a significant banking franchise. It's shown that financial inclusion and shareholder returns aren't mutually exclusive. Most importantly, it's demonstrated that in a rapidly digitizing economy, the advantages of legacy—branch networks, brand recognition, government relationships—matter less than execution, technology, and customer focus. The World Bank data underscores the opportunity and challenge: 79% of adults globally now have an account, but meaningful financial inclusion—active usage of a broader range of financial services—remains elusive for many. As of March 2024, India's Financial Inclusion Index (FI-Index) surged to 64.2, up from 60.1 in the previous year, reflecting substantial progress. India's journey from 53% to nearly 80% of the population now having bank accounts demonstrates what's possible with focused policy and execution.

AU's role in this transformation extends beyond its direct customer base. Every successful loan to a first-time borrower creates demonstration effects in communities. Every digital transaction in a rural market normalizes electronic payments. Every woman entrepreneur who builds a business with AU's credit inspires others. These ripple effects, unmeasurable in quarterly earnings, represent AU's true impact.

The future of Indian banking will be shaped by institutions that can bridge multiple divides—urban and rural, digital and physical, wholesale and retail, profit and purpose. AU's journey from vehicle financier to universal bank provides a template, but not a guarantee. Execution, culture, and adaptability will determine whether AU becomes a footnote or a case study in India's financial history.

As we reflect on AU's transformation, the larger question emerges: Is this the future of emerging market finance? Can the AU model—patient capital deployment, regulatory progression, technology adoption, and relentless focus on underserved segments—work in Indonesia, Nigeria, or Brazil? The answer will shape not just banking but economic development across the developing world.

For investors, AU represents a clear choice. You're either betting on India's formal economy expanding to include hundreds of millions more participants, with AU as a primary beneficiary. Or you believe that incumbents and new entrants will squeeze AU's niche, that technology will commoditize its advantages, and that premium valuations will compress. There's little middle ground.

The power in AU's story isn't just financial—it's inspirational. A chartered accountant from Jaipur, with no banking background, built one of India's most valuable financial institutions by serving customers that established banks ignored. In an era of increasing inequality and financial exclusion globally, AU proves that doing good and doing well aren't mutually exclusive—they're mutually reinforcing.

As AU embarks on its universal banking journey, it carries the hopes of millions of Indians seeking their first loan, opening their first account, or building their first business. The responsibility is immense, the opportunity historic. Whether AU succeeds or fails, its impact on Indian banking is already indelible—it proved that banking's future belongs not to those with the biggest balance sheets, but to those who best understand and serve their customers.

The next chapter of AU's story remains unwritten. But if the past three decades are any indication, it will be shaped by the same principles that guided a young chartered accountant in 1996: that finance should be inclusive, that technology should serve humanity, and that banking, at its best, is about enabling dreams—one customer, one loan, one account at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube