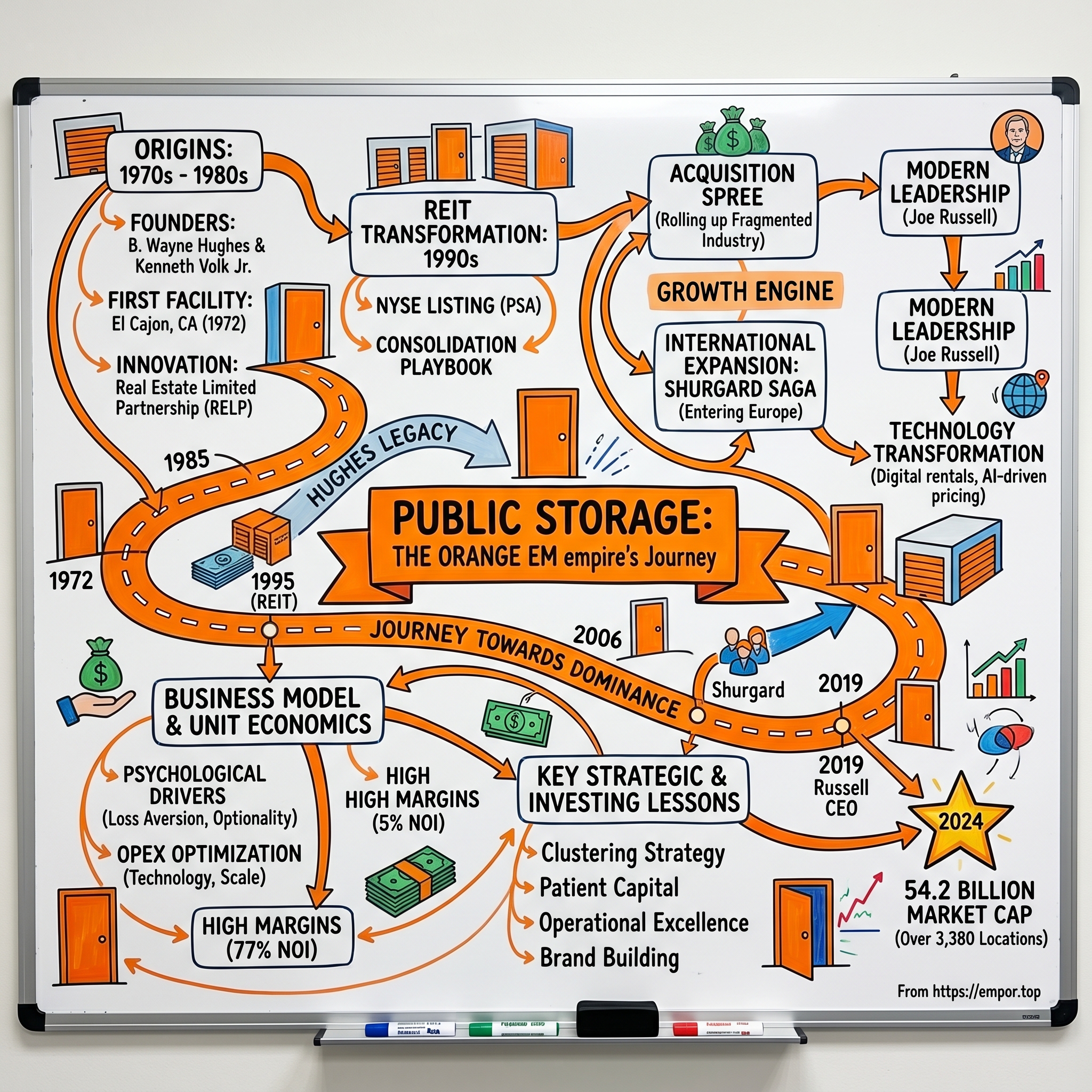

Public Storage: The Orange Empire

I. Introduction & Episode Roadmap

Picture this: August 1972, El Cajon, California. A mariachi band plays under the scorching sun as curious drivers slow down on the highway, drawn by impossibly bright orange doors gleaming in the distance. Two friends, B. Wayne Hughes and Kenneth Volk Jr., stand watching their first customer—an STP Motor Oil distributor—drive up to rent a unit. They'd scraped together $50,000 to build this single facility, a simple bet that Californians needed somewhere to store their stuff while waiting for land values to appreciate.

Fast forward five decades. That single facility has multiplied into an empire of 3,380+ locations spanning 247 million square feet—roughly the size of Manhattan. Public Storage commands a $54.2 billion market capitalization, making it larger than Ford Motor Company and nearly as valuable as FedEx. The temporary land-holding strategy? It became permanent infrastructure for American life.

How does a company built on the premise of renting empty boxes become one of the most successful real estate stories in American history? How did two guys with a mariachi band create a business model so powerful that Warren Buffett would later call self-storage "a terrific business"?

This is the story of Public Storage—a company that turned life's transitions into a predictable revenue stream, transformed tax law changes into competitive advantages, and built a brand so dominant that its orange doors became synonymous with an entire industry. It's a tale of patient capital meeting perfect timing, of seeing opportunity where others saw empty space, and of a Depression-era newspaper boy who would build one of America's great fortunes by betting on a simple truth: Americans accumulate stuff, and they need somewhere to put it.

We'll trace the journey from that first facility to today's real estate juggernaut, examining the financial engineering that funded expansion when competitors couldn't borrow, the consolidation playbook that rolled up a fragmented industry, and the operational excellence that generates 77% NOI margins—higher than luxury hotels or Class A office buildings. Along the way, we'll uncover how Public Storage didn't just build storage units; they built a new asset class.

II. Origins: The Dust Bowl to Orange Doors (1930s–1972)

The dust storms that ravaged Oklahoma in 1933 sent thousands of families west, searching for opportunity in California's promised land. Among them was the Hughes family, carrying their young son B. Wayne, born that same year in the heart of the Depression. This migration—from America's devastated heartland to its golden coast—would shape not just one boy's ambition but eventually transform how Americans think about space, stuff, and storage.

Young Wayne Hughes learned capitalism through newspaper routes. Every morning before dawn, he'd bike through Los Angeles neighborhoods, tossing papers onto porches to fund his education at USC. The work ethic was relentless: Hughes would later tell employees that success came from "getting up earlier and working harder than the next guy." That philosophy, forged in predawn darkness, would drive him from newspaper delivery to building a real estate empire worth billions.

After USC and a stint in the Navy, Hughes entered real estate in the 1960s—not as a developer but as a deal-maker, putting together limited partnerships for apartment buildings. The business was good but conventional. Then came the Texas trip that changed everything.

In 1971, Hughes traveled to Texas on unrelated business and noticed something peculiar: rows of small, garage-like units with roll-up doors, each rented monthly like apartments but without the headaches of toilets, tenant complaints, or midnight maintenance calls. The facilities were primitive—basically converted warehouses divided into smaller spaces—but they were full. And profitable. Incredibly profitable.

The math was seductive. These "mini-warehouses" (as they were called then) cost 35-40% less to build than apartments but rented for similar prices per square foot. No plumbing meant no plumbers. No kitchens meant no appliance repairs. No bedrooms meant no eviction nightmares. Just concrete, steel, and a lock. The operating expenses were minimal, the management simple, and the demand—surprisingly—was everywhere.

Hughes returned to California energized. He found his friend Kenneth Volk Jr., a fellow real estate investor, and pitched the concept over drinks. Volk was skeptical—who would pay to store old furniture and Christmas decorations? But Hughes had done his homework. Post-war prosperity meant Americans were accumulating possessions faster than ever. California's housing boom meant people were constantly moving, downsizing, upsizing, divorcing, marrying. Life transitions created storage needs, and life transitions were constant.

They pooled $50,000—$25,000 each—and bought a piece of land in El Cajon, just outside San Diego. The location was strategic: visible from the highway, accessible to growing suburbs, cheap enough to make the numbers work. But Hughes knew they needed something to catch drivers' attention at 65 miles per hour.

The orange doors were Hughes' masterstroke. Not just any orange—a blazing, unmistakable, almost offensive shade that scorched retinas from a quarter-mile away. "You couldn't not look," recalled an early employee. The color would become so iconic that decades later, customers would simply ask for directions to "the orange place."

August 1972: Opening day arrived with deliberate fanfare. Hughes hired a mariachi band—a celebration that acknowledged California's Mexican heritage while creating spectacle. Local news covered the odd event: a grand opening for empty rooms? The publicity was perfect. Within hours, that STP Motor Oil distributor became their first customer, needing space for excess inventory. By week's end, they had a dozen renters.

The original business thesis was almost comically different from what Public Storage would become. Hughes and Volk viewed self-storage as a placeholder—a way to generate cash flow from land while waiting for real estate values to appreciate enough to justify redevelopment into apartments or offices. Storage was supposed to be temporary. The land was the real investment.

But something unexpected happened in those first months. The facility filled up faster than any apartment complex Hughes had ever seen. They hit 35% occupancy—their break-even point—within three months. By month six, they were at 60%. The cash flow was immediate, predictable, and required almost no ongoing investment. Why would you ever redevelop?

III. The RELP Innovation & Early Growth (1972–1989)

Three months. That's all it took for Hughes and Volk to realize they'd stumbled onto something extraordinary. Their El Cajon facility hit 35% occupancy—the break-even point—in ninety days. No apartment building filled that fast. No office complex generated positive cash flow that quickly. By comparison, a typical apartment complex took 18-24 months to stabilize. The velocity of cash generation was unprecedented in real estate.

The unit economics were almost too good to be true. Construction costs ran 35-40% less than apartments, yet monthly rents per square foot were comparable. A 10x10 storage unit might rent for $30 per month—the same $0.30 per square foot as a studio apartment, but without renovations between tenants, without habitability warranties, without fair housing regulations. The gross margins approached 70% from day one.

Hughes became obsessed with expansion. If one facility could generate these returns, what about ten? Or a hundred? But real estate development requires capital—lots of it—and traditional bank financing was expensive. Interest rates in the mid-1970s climbed toward double digits. Most developers pulled back. Hughes pushed forward with an innovation that would fund an empire: the Real Estate Limited Partnership (RELP).

The RELP structure was elegant financial engineering. Hughes would identify sites, design facilities, and manage operations. Limited partners—dentists, doctors, small business owners—would provide capital in exchange for tax benefits and cash distributions. The 1976 Tax Reform Act had created massive tax incentives for real estate investment, allowing investors to shelter ordinary income through depreciation and interest deductions. A dentist earning $200,000 could invest $50,000 in a Hughes RELP and potentially save $30,000 in taxes while earning 12-15% annual returns.

The first RELP launched in 1975 raised $2 million. By 1980, Hughes was raising $200-300 million annually. While competitors begged banks for loans at 18% interest, Hughes had doctors writing checks at country club dinners. The capital advantage was insurmountable.

Twenty locations by 1974 became fifty by 1976, then one hundred by 1978. Hughes developed a expansion playbook that would define Public Storage's growth for decades:

The Clustering Strategy: Rather than scatter facilities randomly, Hughes concentrated them in specific metros. Los Angeles might have twenty locations before he'd build one in Phoenix. This clustering created operational leverage—one manager could oversee multiple sites, one maintenance crew could service a dozen facilities, one local TV ad campaign could drive traffic to all locations.

Local television advertising became Hughes' secret weapon. While national chains ignored TV (too expensive) and mom-and-pop operators relied on Yellow Pages, Hughes bought late-night local TV spots cheap. The ads were deliberately low-budget, featuring the orange doors and a simple message: "Public Storage—Clean, Secure, Convenient." The ROI was extraordinary—a $5,000 monthly TV spend in Los Angeles might drive $50,000 in new rentals.

By the mid-1980s, success created tension between the founders. Kenneth Volk Jr. wanted to slow down, take profits, maybe diversify into other real estate. Hughes wanted to accelerate, to dominate, to build something unprecedented. The philosophical divide was unbridgeable. Volk, nearing retirement age and satisfied with his millions, agreed to sell his stake to Hughes.

The buyout terms remain private, but industry insiders suggest Hughes paid roughly $100 million for Volk's 50% stake—a fortune in 1985, but a fraction of what it would be worth just five years later. Volk retired to enjoy his wealth. Hughes, now sole captain, pushed the throttle forward.

The late 1980s brought explosive growth. Hughes perfected the development formula: Find sites near highways but not on expensive corners. Build identical facilities to minimize architectural costs. Paint everything the same shade of orange. Hire managers from retail, not real estate—people who understood customer service, not property management. Keep operations lean—one manager per 300 units versus one per 100 in apartments.

By 1989, Public Storage reached a milestone: 1,000 locations. The company that started as a land-holding play now owned more self-storage facilities than anyone in history. Annual revenues approached $500 million. The RELP funds had raised over $2 billion in capital. Hughes was worth an estimated $400 million.

But storm clouds gathered. The 1986 Tax Reform Act had eliminated many real estate tax shelters. The RELP market—Hughes' money machine—was dying. Savings and loan associations were failing. Real estate values were collapsing. The company that had thrived on financial engineering would need new fuel for growth.

The answer would transform not just Public Storage but the entire real estate industry: the Real Estate Investment Trust.

IV. REIT Transformation & Consolidation (1990–2002)

The 1986 Tax Reform Act hit like a sledgehammer. With one signature, President Reagan eliminated the tax shelters that had fueled Public Storage's growth. Overnight, the RELP market evaporated. Doctors and dentists no longer needed real estate investments to shelter income. The capital spigot that had funded Hughes' empire shut off completely.

By 1990, Hughes controlled over 1,000 facilities through a byzantine structure of 38 different limited partnerships, each with hundreds of investors, different fee structures, and competing interests. The complexity was becoming unmanageable. Some partnerships wanted to sell. Others wanted to hold. Many investors just wanted out—the tax benefits were gone, and real estate was crashing nationwide.

Hughes saw crisis as opportunity. If he could consolidate these partnerships into a single entity, he'd create the largest self-storage company in history. But how do you convince thousands of limited partners to exchange their partnership interests for something else?

The answer was a REIT—a Real Estate Investment Trust. REITs had existed since 1960 but were sleepy, forgotten vehicles. The structure offered unique advantages: no corporate taxes if you distributed 90% of income as dividends, liquid shares tradeable on public markets, and the ability to raise capital through stock offerings. Hughes would merge the partnerships into a unified REIT, giving investors liquid shares instead of illiquid partnership units.

The consolidation took five years of negotiations, lawsuits, and financial gymnastics. Hughes personally visited hundreds of investors, selling the vision: "You own 0.5% of a single facility in Fresno. Wouldn't you rather own 0.0001% of a thousand facilities nationwide?" The pitch worked, mostly.

The pivotal moment came in 1995 with the Storage Equities merger. Storage Equities, another large operator, had been pursuing a similar REIT conversion. Rather than compete, Hughes engineered a merger that created the unified Public Storage REIT. The combined entity went public on the NYSE under the ticker PSA, with a market cap of $1.5 billion.

Wall Street initially didn't understand the business. Analysts covering REITs focused on apartments, offices, and malls—"real" real estate. Storage was an oddity, a niche. The first earnings calls were educational seminars, with Hughes patiently explaining why Americans needed storage (divorce, death, dislocation, and downsizing—the "four Ds") and how 5x5 concrete boxes could generate 70% margins.

The public markets provided rocket fuel. Between 1995 and 2000, Public Storage issued $3 billion in equity and debt, funding an acquisition spree that rolled up the fragmented industry. Mom-and-pop operators who'd built single facilities in the 1970s sold to Hughes at 6-8x cash flow. He'd integrate them into the Public Storage network, repaint the doors orange, implement revenue management systems, and watch cash flow double within 18 months.

The operational playbook during this period became legendary in real estate circles:

Revenue Management Revolution: Public Storage pioneered dynamic pricing in storage, similar to airlines and hotels. Prices changed daily based on occupancy, seasonality, and local competition. A 10x10 unit might cost $50/month in January but $150/month in August when college students scrambled for space. This yield management added 20-30% to revenues without adding a single new unit.

Brand Building: The orange doors became a national symbol. Public Storage spent millions on TV advertising—unheard of for REITs. The tagline "It's Your Space" resonated with customers who saw storage as an extension of their homes. By 2000, Public Storage had higher brand recognition than Marriott Hotels in many markets.

Technology Adoption: While competitors still used paper ledgers, Public Storage invested heavily in technology. Centralized call centers replaced on-site leasing. Automated payment systems reduced labor costs. Digital locks eliminated key management. The company that rented concrete boxes ran like a Silicon Valley startup.

Hughes' leadership style during this period was paradoxical. He drove a 20-year-old Volvo and ate lunch at Denny's, yet deployed billions with aggressive precision. He'd personally visit facilities, checking cleanliness and counting cars in the parking lot. Employees described him as simultaneously frugal and fearless—he'd haggle over a $10,000 maintenance contract then write a $100 million check for an acquisition.

By November 2002, Hughes decided to step back. At 69, he'd built Public Storage from one facility to over 1,500, from $50,000 in capital to a $5 billion market cap. He announced his retirement as CEO, though he'd remain chairman and largest shareholder. The company was professionally managed, publicly traded, and positioned for its next phase of growth.

The boy who delivered newspapers in Depression-era Los Angeles had built one of America's great companies. But Public Storage's biggest acquisition—and greatest challenge—still lay ahead.

V. The Shurgard Saga & International Expansion (2000–2010)

February 2000: While dot-com millionaires bid up San Francisco lofts and day traders flipped tech stocks, Wayne Hughes quietly wrote a check that would reshape global self-storage. Public Storage acquired a 24% stake in Shurgard Storage Centers—not just another competitor, but a company with ambitions beyond America's borders. Shurgard operated 440 facilities in the US, but more intriguingly, had planted flags across Europe with 41 locations in seven countries.

Chuck Barbo, Shurgard's CEO, was everything Hughes wasn't—flashy, internationally minded, eager to spread American-style storage to Europeans who still stuffed belongings in damp basements and dusty attics. The European operations were bleeding money, but Barbo insisted the continent was "five years behind America" in storage adoption. Hughes, typically skeptical of overseas adventures, saw something different: a chance to buy American assets cheap while getting a free option on European growth.

The relationship started cordially. Public Storage increased its stake to 30% by 2001, becoming Shurgard's largest shareholder. Hughes joined the board, offering advice while learning about European markets. But tensions emerged. Shurgard's management wanted to grow aggressively in Europe, burning cash to establish market position. Hughes wanted profitability first, expansion second.

2003 brought the first takeover attempt. Public Storage offered $23 per share—a 20% premium. Shurgard's board rejected it as "opportunistic." Hughes increased to $26. Rejected again. The dance continued for two years, offers and rejections, with Shurgard management insisting their European bet would eventually pay off while hemorrhaging $20 million annually overseas.

By 2005, Shurgard's resistance was weakening. European losses were mounting, American competitors were getting aggressive, and the stock market was losing patience. Public Storage made another offer: $40.50 per share. Shurgard countered at $45. They settled at $44—a total value of $5.5 billion, the largest self-storage acquisition in history.

The deal brought Public Storage 624 premium locations, including 141 in Europe across Belgium, France, Sweden, Denmark, the Netherlands, Germany, and the UK. Hughes now owned storage facilities in Paris, Stockholm, and London—cities where a closet-sized apartment rented for $2,000 per month and basement storage was a luxury.

The European operations were a puzzle wrapped in a regulatory nightmare. Each country had different rules about construction permits, rental agreements, and tax structures. In France, storage contracts required 30-day notice periods. In Germany, Sunday operations were illegal. In Sweden, facilities needed heating systems to prevent customer goods from freezing.

Hughes appointed his lieutenant, John Reyes, to figure out Europe. Reyes discovered that European storage customers were fundamentally different from Americans. Europeans rented smaller units (25 square feet versus 75 in America) but kept them longer (24 months versus 12). They stored different items—wine collections, seasonal sporting equipment, business archives—reflecting smaller living spaces and different lifestyles.

The operational playbook needed complete revision. American-style drive-up facilities didn't work in dense European cities. Instead, Public Storage built vertical facilities—six-story storage buildings in urban cores with elevator access and climate control. Construction costs were triple the US, but rental rates were double. A 50-square-foot unit in central London commanded £200 per month—$4 per square foot versus $1 in Los Angeles.

Marketing required cultural translation. The orange doors stayed, but messaging changed. Americans responded to "convenience" and "space." Europeans preferred "security" and "flexibility." TV advertising, so effective in America, flopped in Europe where regulations limited commercial messaging. Instead, Public Storage pioneered digital marketing, becoming the largest Google AdWords buyer in several European markets.

By 2008, the European experiment faced its first real test: the global financial crisis. European economies crashed harder than America. Spain's real estate bubble burst. UK banks failed. The euro seemed fragile. Public Storage's European occupancy dropped from 85% to 75% in six months.

Hughes made a crucial decision: rather than retreat, he doubled down. While competitors froze expansion, Public Storage acquired distressed facilities across Europe at 50 cents on the dollar. They bought a 12-property portfolio in France from a bankrupt developer. They acquired Sweden's largest independent operator. They consolidated the fragmented UK market, becoming London's dominant storage provider.

The strategy paid off magnificently. By 2010, European operations had turned profitable, generating €100 million in annual revenue. But regulatory complexity and management challenges led to a strategic shift. Public Storage spun off the European operations into a separate entity—Shurgard Self Storage Limited—retaining 35% ownership but removing operational headaches.

Today, that 35% stake in Shurgard Europe (318 facilities across seven countries) is worth approximately $2 billion. The "free option" Hughes saw in 2000 became a massive value creator. More importantly, the Shurgard acquisition proved Public Storage could execute transformational deals, integrate massive portfolios, and compete globally.

The boy from Oklahoma had built an international empire, but the next decade would require a different kind of growth—one driven not by geographic expansion but by technological transformation and financial engineering.

VI. Modern Growth Engine (2010–Present)

December 2010: While America crawled out of the Great Recession, Public Storage did something audacious—it spent $281 million acquiring A-American Self Storage's 31 properties. Competitors thought Hughes had lost it. Credit markets were frozen, consumers were deleveraging, and storage occupancies had dropped to 80%. But Hughes, now 77 and officially retired but still pulling strings as chairman, saw what others missed: a once-in-a-generation opportunity to consolidate an industry in distress.

The A-American deal became the template for a decade-long acquisition binge that would redefine scale in self-storage. Public Storage had survived 2008-2009 with minimal leverage while competitors had gorged on debt during the boom years. Now those chickens were coming home to roost. Overleveraged operators needed to sell. Banks holding foreclosed facilities wanted out. Public Storage had $500 million in cash and untapped credit lines—it was shopping season.

2013: Stor-All's 21 facilities for $241 million. The portfolio included prime California locations that competitors had been circling for years. Public Storage won by offering all-cash, no-financing contingencies, closing in 30 days. Speed became a weapon.

But the real transformation began in 2019 when Joe Russell took over as CEO. Russell, a Public Storage lifer who'd started as a district manager in 1989, brought operational intensity to what had been primarily a deal-making culture. His mandate from the board (still influenced by Hughes until his death in 2021) was clear: deploy capital aggressively while rates were low, consolidate while the market was fragmented, and build a platform for the next generation.

Russell unleashed a stunning acquisition spree. Between 2019 and 2024, Public Storage deployed $7.1 billion in acquisitions—more than it had spent in the previous decade combined:

ezStorage Acquisition (2021): $1.8 billion for 48 properties concentrated in the Mid-Atlantic. What made ezStorage attractive wasn't just its facilities but its technology platform—a proprietary revenue management system that beat Public Storage's own algorithms. Russell didn't just buy boxes; he bought capabilities.

All Storage Portfolio (2021): $1.5 billion for 56 properties across Texas and Georgia. The timing was perfect—Sun Belt migration was accelerating, remote work was reshaping housing patterns, and these facilities sat in the path of growth. Within 18 months, occupancies increased from 87% to 94% just through Public Storage's operational improvements.

Beyond Self Storage (2020): This acquisition was different—a property management company operating 80 third-party facilities. Russell recognized that Public Storage's operational expertise was itself valuable. Why not manage facilities for others, earning fees while gaining market intelligence?

The expansion numbers are staggering: 36 million square feet added since 2019, a 22% increase in rentable space. For context, that's equivalent to adding 650 football fields of storage in five years. The company now operates 3,380+ facilities with 247 million square feet—roughly 10% of all self-storage space in America.

But Russell's real innovation was the development pipeline. While acquisitions grabbed headlines, Public Storage quietly ramped up ground-up development. As of 2024, there's 3.7 million square feet under construction at a cost of $665.5 million. These aren't your grandfather's storage facilities—they're climate-controlled, technology-enabled, urban-infill properties designed for e-commerce fulfillment as much as personal storage.

The technology transformation under Russell has been profound:

Digital Customer Journey: 70% of rentals now start online. Customers can tour facilities virtually, sign leases digitally, and move in without meeting a human. The cost to acquire a customer dropped from $150 to $75.

Automated Revenue Management: AI-driven pricing algorithms adjust rates hourly based on occupancy, competitor pricing, weather patterns, and local events. A facility near a university might automatically raise prices 40% during move-in week.

Predictive Maintenance: IoT sensors monitor HVAC systems, detecting failures before they happen. Maintenance costs dropped 12.4% even as the portfolio expanded 22%.

Third-Party Management Platform: Public Storage now manages 80+ facilities it doesn't own, earning $50 million in annual fees while gathering competitive intelligence. It's the AWS of self-storage—monetizing infrastructure expertise.

The competitive landscape has shifted dramatically. Extra Space Storage, once a distant second, merged with Life Storage in 2023 for $12.7 billion, creating a rival with 3,500+ facilities. CubeSmart has grown aggressively through technology and customer experience investments. The big four (Public Storage, Extra Space, CubeSmart, and U-Haul) now control 25% of the market, up from 15% a decade ago.

Yet Public Storage maintains crucial advantages. Its average facility is 73,000 square feet versus 55,000 for competitors—scale that provides operational leverage. Its locations skew toward high-barrier coastal markets where new supply is virtually impossible. Its balance sheet remains fortress-like with just 25% debt-to-capital versus 40-50% for peers.

Current performance metrics tell the story: 91.5% occupancy (industry average: 88%), $18.92 per square foot rental rates (industry: $15.50), and 77.1% NOI margins (industry: 65%). Every metric leads the industry, usually by wide margins.

The development pipeline promises continued growth. Public Storage is building in markets where supply has been constrained for years—San Francisco, Boston, Seattle. These facilities will cost $200 per square foot to build but generate $30+ per square foot in annual rent. The math is compelling: 15% unlevered returns in a 5% interest rate world.

As 2024 ends, Public Storage stands at an inflection point. The massive acquisition spree is largely complete—there simply aren't many large portfolios left to buy. New supply is declining as developers struggle with higher construction costs and financing rates. Demographics favor continued demand as millennials form households and baby boomers downsize.

The question isn't whether Public Storage will grow, but how. The answer may lie not in adding more orange doors, but in reimagining what those doors represent.

VII. The Hughes Legacy & Leadership Transition

August 21, 2021: B. Wayne Hughes died at his mansion in Malibu, overlooking the Pacific Ocean he'd first glimpsed as a dust bowl refugee. He was 87, worth an estimated $4.1 billion, and had never quite gotten comfortable with the wealth. Until the end, he drove used cars, flew commercial when possible, and insisted Public Storage executives eat at Denny's during business trips. "Why pay $50 for a steak when $10 gets you a good meal?" he'd ask, genuinely puzzled by the extravagance around him.

Hughes' philosophy was deceptively simple: work harder than everyone else, spend less than everyone else, and compound the difference over decades. He arrived at Public Storage facilities before dawn, counting cars to estimate occupancy. He negotiated personally with contractors, saving thousands on million-dollar projects. He answered his own phone, returning calls from small investors who owned a handful of shares. This wasn't affectation—it was conviction that business was personal, that every dollar mattered, that success came from accumulation of small advantages.

The work ethic bordered on obsession. Hughes routinely worked 80-hour weeks into his eighties. Executives received emails at 3 AM with ideas about pricing strategies or maintenance protocols. He memorized occupancy rates for hundreds of facilities, challenging managers who reported numbers that didn't match his mental models. One manager recalled Hughes visiting a Los Angeles facility and immediately noting that three lights were out in the parking lot: "If we can't keep the lights on, why should customers trust us with their belongings?"

But Hughes was more than a micromanager with a calculator. He understood capital allocation with rare clarity. While competitors leveraged up during booms, Hughes maintained conservative debt levels, keeping powder dry for downturns. This patience paid off repeatedly—in 1991, 2001, 2008, and 2020, Public Storage emerged from each crisis stronger, having acquired distressed assets at discounts while competitors struggled to survive.

His greatest insight was that self-storage wasn't really about real estate—it was about solving life's transitions. "People don't want storage," he'd say. "They want to preserve memories, maintain options, navigate change. We're selling time and space for people to figure out their lives." This empathy, surprising from such a hardened businessman, informed every decision from facility design to customer service training.

The succession plan was characteristic Hughes—thorough, unemotional, and focused on continuity. He'd groomed internal candidates for years, promoting from within rather than hiring flashy outsiders. Joe Russell, who became CEO in 2019, had started as a district manager three decades earlier. Ron Havner, who preceded Russell as CEO, had joined in 1986. This internal promotion philosophy created deep institutional knowledge and cultural consistency.

Hughes' daughter, Tamara Hughes Gustavson, emerged as the family standard-bearer. Currently Public Storage's largest individual shareholder with an 11% stake worth $7.3 billion, she serves on the board while maintaining her father's low profile. Unlike many heirs who coast on inherited wealth, Gustavson earned a business degree and worked in Public Storage operations, learning the business from the ground up.

Her approach differs from her father's while honoring his principles. Where Hughes was frugal to the point of asceticism, Gustavson balances cost discipline with strategic investment. She's pushed for technology upgrades Hughes resisted, arguing that customer experience drives long-term value. She's also expanded Public Storage's environmental initiatives, installing solar panels on hundreds of facilities—investments Hughes would have questioned but that now generate 15% IRRs through energy savings.

B. Wayne Hughes Jr., the founder's son, took a different path. After serving as VP of Acquisitions from 1985 to 1998, he left to pursue his own ventures, including founding American Homes 4 Rent, now America's largest single-family rental REIT. The parallel is striking—both father and son built billion-dollar businesses by institutionalizing previously fragmented real estate sectors. The younger Hughes' success validates the father's core insight: operational excellence and scale advantages can transform sleepy asset classes into institutional investments.

The philanthropic legacy reflects Hughes' practical bent. Rather than flashy naming gifts, he focused on impact. The Parker Hughes Cancer Center in Minnesota, named after a friend who died from the disease, conducts cutting-edge research with minimal fanfare. He donated millions to USC but insisted on funding scholarships for working-class students rather than buildings. Even in charity, ROI mattered—he wanted maximum societal benefit per dollar donated.

Current leadership under Joe Russell maintains Hughes' operational intensity while adapting to modern realities. Russell instituted "founder's principles" training for all employees, codifying Hughes' philosophy: "Take care of customers, take care of properties, take care of costs—in that order." But he's also embraced changes Hughes resisted, like work-from-home policies and diversity initiatives that broaden Public Storage's talent pool.

The cultural transmission extends beyond family and executives. Public Storage's 5,000+ employees often describe an almost cultish devotion to Hughes' principles. Store managers compete to achieve the highest occupancy rates, not for bonuses but for bragging rights. Maintenance crews take pride in facility cleanliness ratings. The company that rents empty boxes has somehow created emotional engagement around operational excellence.

The ultimate testament to Hughes' legacy is Public Storage's continued dominance after his death. Many founder-led companies struggle with succession, losing their edge when the visionary departs. Public Storage has actually accelerated, deploying more capital and generating higher returns post-Hughes than during his final years. The machine he built runs without him—the ultimate entrepreneurial achievement.

Yet questions remain about long-term stewardship. As ownership disperses beyond the Hughes family, will Public Storage maintain its disciplined culture? Can professional managers replicate founder's intuition about market cycles and capital allocation? Will the company that revolutionized self-storage be able to reinvent itself for whatever comes next?

VIII. Business Model & Unit Economics

Walk into any Public Storage facility at 9 AM on a Saturday and you'll witness a peculiar economic phenomenon: people cheerfully paying $200 per month to store $500 worth of belongings. The behavioral economics are irrational—customers could buy new items for less than five years of storage fees—yet the business model is bulletproof. Understanding why requires examining the deepest drivers of human behavior and the elegant simplicity of Public Storage's economic engine.

The self-storage value proposition rests on four powerful psychological and practical foundations:

Loss Aversion: Humans value things they own twice as much as identical items they don't own—the endowment effect. That $50 lamp becomes priceless when it was grandmother's. Public Storage monetizes emotional attachment at $2 per square foot per month.

Optionality Preservation: Storage provides flexibility during uncertainty. The divorcing couple who can't decide who gets the dining set. The consultant who might return from Singapore in six months or six years. The entrepreneur keeping equipment for a business that might restart. Customers pay premium prices to defer decisions.

Transaction Cost Avoidance: Moving, selling, and storing belongings involves tremendous hassle. Storage eliminates immediate transaction costs even if long-term costs exceed asset values. It's economically irrational but behaviorally optimal.

Identity Maintenance: Possessions define identity. The golf clubs represent who you were. The wedding dress represents who you hoped to be. Storage allows people to maintain aspirational and nostalgic identities without cluttering current reality.

These psychological drivers create pricing power that defies traditional economic logic. Public Storage raises rates 5-8% annually on existing customers, who rarely leave despite cheaper alternatives. The switching costs aren't financial—moving requires physical effort, emotional energy, and confronting delayed decisions. Result: 92% annual customer retention despite consistent price increases.

The operational metrics are stunning:

NOI Margins: 77.1%—Higher than luxury hotels (60%), Class A offices (65%), or high-end retail (70%). Only parking garages approach similar margins, and they require prime locations. Public Storage achieves these margins in secondary locations with minimal services.

Occupancy: 91.5%—Compare to apartments (95%), hotels (70%), or office buildings (85%). Storage occupancy remains remarkably stable through economic cycles. Even during 2008-2009, occupancy only dropped to 85%. People stop traveling and delay home purchases, but they keep storing.

Revenue per Square Foot: $18.92 annually—A 150,000 square foot facility generates $2.8 million in revenue, $2.2 million in NOI. The same land developed as apartments might generate $3.5 million revenue but only $1.5 million NOI after maintenance, management, and tenant issues.

The cost structure is elegantly simple:

| Cost Category | % of Revenue | Notes |

|---|---|---|

| Property Taxes | 11.2% | Rising 4-5% annually, the biggest headache |

| Payroll | 8.3% | One manager per 300 units vs 100 for apartments |

| Marketing | 3.1% | Mostly digital, highly measurable ROI |

| Utilities | 2.2% | Climate control only in premium units |

| Maintenance | 2.8% | No plumbing, minimal mechanical systems |

| Insurance | 1.5% | Low liability, no habitability issues |

| Other Operating | 4.3% | Software, corporate overhead, misc |

| Total Operating Expenses | 33.4% | Industry average: 40-45% |

| NOI Margin | 66.6% | Before corporate G&A |

Labor optimization drives margin expansion. Through technology, Public Storage reduced payroll costs 12.4% over five years while growing revenue 35%. Automated gates eliminated security guards. Digital leasing eliminated leasing agents. Centralized call centers eliminated on-site sales staff. A typical facility operates with 1.5 full-time equivalent employees versus 3-4 a decade ago.

The capital allocation framework is disciplined:

Development Returns: 15-20% unlevered—New facilities in supply-constrained markets generate exceptional returns. A $20 million development producing $3-4 million NOI beats any alternative real estate investment.

Acquisition Returns: 8-12% unlevered—Lower than development but faster and less risky. Public Storage typically improves acquired facilities' performance by 20-30% through operational improvements.

Share Buybacks: Minimal—REITs must distribute 90% of taxable income, limiting buyback capacity. Public Storage occasionally repurchases shares but prefers growth investments.

Dividends: 90% of AFFO—Currently yielding 3.8%, growing 5-7% annually. The dividend is sacred—Public Storage has never cut it, even during 2008-2009.

The REIT structure provides advantages and constraints:

Advantages: - No corporate taxes if distributing 90% of income - Access to liquid capital markets - Currency (stock) for acquisitions - Forced discipline on capital allocation

Constraints: - Limited retained earnings for growth - Constant need for external capital - Dividend obligations during downturns - Regulatory compliance costs

Technology increasingly drives operational leverage. Public Storage's proprietary systems manage:

Dynamic Pricing: Algorithms adjust rates based on unit size, facility occupancy, local competition, seasonality, and demand signals. A 10x10 unit's price might change daily, optimizing revenue per square foot.

Customer Acquisition: 70% of customers start online. SEO, SEM, and social media targeting reduce acquisition costs while improving customer quality. Lifetime values increased 23% through better targeting.

Operational Efficiency: Predictive maintenance, automated climate control, and remote monitoring reduce operational costs while improving customer experience. One operations manager now oversees 10 facilities versus 3 a decade ago.

The combination of psychological pricing power, operational simplicity, and technology leverage creates a business model that's nearly impossible to disrupt. New entrants face massive scale disadvantages. Technology platforms can't replicate physical presence. Economic downturns actually increase demand as people downsize.

The result is a perpetual cash machine: predictable revenue, expanding margins, minimal capital needs, and tremendous pricing power. It's Warren Buffett's dream business hidden inside orange doors.

IX. Playbook: Strategic & Investing Lessons

Study Public Storage's five-decade journey and you'll extract strategic lessons that transcend self-storage—principles for building dominant businesses in fragmented industries, creating value through operational excellence, and compounding advantages over time. These aren't theoretical frameworks but battle-tested strategies that transformed a $50,000 investment into a $54 billion empire.

Lesson 1: Boring is Beautiful

Wayne Hughes didn't chase sexy. While contemporaries built shopping malls and office towers—prestigious projects with ribbon cuttings and press releases—Hughes built boxes. Concrete boxes. In secondary locations. With roll-up doors.

The insight: boring businesses often have better economics than exciting ones. Nobody dreams of disrupting self-storage. Business schools don't write cases about storage innovation. Venture capitalists don't fund storage startups. This lack of attention creates opportunity. While brilliant minds chase the next big thing, boring businesses compound quietly.

Public Storage generated 18% annual returns over 40 years—better than Amazon, Apple, or Google over equivalent periods. The lesson isn't to avoid innovation but to recognize that operational excellence in mundane industries often beats innovation in competitive ones.

Lesson 2: Fragmentation is Opportunity

In 1972, self-storage was impossibly fragmented—thousands of mom-and-pop operators running single facilities. Traditional thinking suggested this was a bad industry: no barriers to entry, commodity product, price-based competition. Hughes saw differently.

Fragmented industries offer consolidation opportunities. Small operators can't achieve scale economies, lack capital for growth, and struggle with professional management. The consolidator who achieves scale first gains insurmountable advantages: purchasing power, operational leverage, brand recognition, and capital access.

Public Storage's consolidation playbook: - Buy at 6-8x EBITDA when mom-and-pops have no alternatives - Improve operations immediately (raise occupancy 10%, cut costs 20%) - Use scale to negotiate better insurance, maintenance, and marketing rates - Reinvest savings into more acquisitions, creating a virtuous cycle

This playbook works across industries—waste management (Waste Management), funeral homes (Service Corporation), collision repair (Boyd Group)—wherever fragmentation meets consolidation opportunity.

Lesson 3: Patient Capital Wins

Hughes' greatest edge wasn't intelligence or connections—it was patience. He maintained low leverage when competitors levered up. He accumulated cash during booms to deploy during busts. He waited years for the right acquisitions rather than forcing bad deals.

The 2008 financial crisis exemplified this patience. While competitors struggled with debt, Public Storage had capacity to invest. They acquired $2 billion in assets at distressed prices, permanently expanding their competitive advantage. The companies that survived 2008 emerged weakened; Public Storage emerged dominant.

Patient capital requires psychological strength. Watching competitors grow faster during booms tests conviction. Shareholders pressure for aggressive growth. But cycles are inevitable, and patient capital becomes predatory capital when cycles turn.

Lesson 4: Operational Excellence Compounds

Public Storage's moat isn't technology or patents—it's thousands of small operational advantages that compound over decades: - 2% better occupancy through superior revenue management - 3% lower costs through scale purchasing - 1% better locations through clustering strategies - 2% higher rates through brand recognition - 4% better margins through labor optimization

Individually, these advantages seem trivial. Collectively, they create 77% NOI margins versus 60% for competitors—a 28% EBITDA advantage on every dollar of revenue. Over decades, this operational edge compounds into market dominance.

The lesson: sustainable competitive advantages rarely come from single breakthrough innovations but from accumulation of marginal gains. The British cycling team won Tour de France by optimizing hundreds of tiny factors—Public Storage dominated self-storage the same way.

Lesson 5: Clustering Creates Leverage

Hughes' clustering strategy—concentrating facilities within specific metros—contradicted conventional wisdom about geographic diversification. But clustering created three powerful advantages:

Operational Leverage: One district manager oversees 15 facilities instead of 5. Maintenance crews service multiple locations daily. Training programs achieve scale. Clustering reduces operating costs by 20-30%.

Marketing Efficiency: A single TV campaign or billboard reaches multiple facilities. Brand recognition compounds faster. Word-of-mouth accelerates. Customer acquisition costs drop 40% in clustered markets.

Competitive Deterrence: Dense market presence deters new entrants. Why build next to 20 Public Storage facilities with established customer bases? Clustering creates local monopolies within competitive markets.

Lesson 6: Use Capital Structure as Strategy

Public Storage's evolution from partnerships to REIT wasn't just financial engineering—it was strategic transformation. Each structure served specific purposes:

- RELPs (1975-1990): Accessed tax-advantaged capital when traditional financing was expensive

- REIT (1995-present): Provided permanent capital, public currency for acquisitions, and tax efficiency

The lesson: capital structure should align with business strategy. High-growth phases might require venture capital. Mature businesses benefit from debt leverage. Asset-heavy industries need patient capital. Public Storage matched structure to strategy at each phase.

Lesson 7: Build for Downturns

Hughes built Public Storage to survive catastrophe. Low leverage meant survival during credit crunches. Geographic diversity meant resilience against regional recessions. The boring nature of storage meant steady demand during downturns.

This conservatism looked foolish during booms—competitors grew faster using leverage. But downturns revealed the wisdom. Public Storage survived every recession since 1972, emerging stronger each time. Competitors disappeared or weakened, ceding market share permanently.

Building for downturns requires accepting lower returns during good times. It means maintaining flexibility when others optimize for efficiency. But businesses built for downturns become dynasties; those built for booms become casualties.

Lesson 8: Brand Matters in Commodities

Storage units are commodities—identical concrete boxes. Yet Public Storage commands 20% price premiums through brand power. How?

- Consistency: Every facility looks identical—same orange doors, same signage, same experience

- Ubiquity: 3,380 locations means customers see Public Storage everywhere

- Trust: Storing valuable possessions requires trust that Public Storage delivers

- Mind Share: When people think storage, they think Public Storage

The lesson: even commodities can achieve pricing power through brand. Coca-Cola sells flavored sugar water at premium prices. Public Storage rents empty boxes at premium prices. Brand transforms commodities into differentiated products.

These lessons explain Public Storage's dominance but apply broadly. Whether building a business, analyzing investments, or crafting strategy, these principles endure: boring can be beautiful, patience pays, operations matter, and competitive advantages compound from marginal gains rather than breakthrough innovations.

X. Analysis & Investment Case

Standing at a $54.2 billion market capitalization in late 2024, Public Storage trades at a crossroads. The stock has underperformed the broader REIT index by 15% over the past year as investors worry about oversupply, slowing demand, and peak margins. But is the market missing the forest for the trees? Let's examine both the bear and bull cases with the rigor this business deserves.

Current Position: The Undisputed Leader

Public Storage's market position is formidable: - 16.96% market share of U.S. self-storage - 3,380+ facilities versus Extra Space's 3,500 (post-Life Storage merger) - Average facility size 73,000 sq ft versus industry average 45,000 sq ft - Coastal market concentration where new supply is virtually impossible - 77.1% NOI margins versus 65% industry average - 91.5% occupancy versus 88% for competitors

The company generates $5 billion in annual revenue, $2.5 billion in NOI, and $1.9 billion in funds from operations (FFO). At current trading levels, PSA yields 3.8% with a payout ratio of 90% of FFO—sustainable but with limited room for increases beyond organic growth.

The Bear Case: Multiple Headwinds Converging

Skeptics point to several concerning trends:

Oversupply in Sunbelt Markets: Development surged 2021-2023 as cheap capital met COVID-driven demand. Markets like Austin, Phoenix, and Tampa saw supply grow 20-30%. Public Storage has heavy exposure to these markets, with 40% of NOI from Sunbelt states. New supply typically takes 3-4 years to absorb—pressure will persist through 2026.

Demand Normalization: The COVID boom is over. Remote work reshuffling has stabilized. Urban exodus reversed. Household formation is slowing. The "four Ds" (death, divorce, downsizing, dislocation) that drive storage demand are returning to historical norms after pandemic acceleration.

Competition Intensifying: Extra Space's merger with Life Storage creates a peer nearly Public Storage's size. Institutional capital is flooding the sector—Blackstone, KKR, and Carlyle all launched storage platforms. Mom-and-pops are professionalizing with third-party management. Public Storage's advantages are eroding.

Peak Margins: At 77% NOI margins, where can they go? Property taxes are rising 5-7% annually. Insurance costs exploded 20% in 2023. Labor shortages push wages higher. The margin expansion story that drove returns for two decades has likely ended.

Valuation Concerns: At 22x FFO, Public Storage trades at premium multiples despite slowing growth. The dividend yield of 3.8% barely beats treasuries. Why accept equity risk for bond-like returns?

The Bull Case: Misunderstood Moat

Yet optimists see opportunity where others see obstacles:

Supply Declining Sharply: New construction starts dropped 70% in 2024 as financing costs soared and banks pulled back. Projects started today won't deliver until 2026. By 2025, net supply growth will turn negative for the first time since 2011. The oversupply narrative is backward-looking.

Structural Demand Tailwinds: Americans accumulate 3% more stuff annually. Living spaces are shrinking—new apartments average 850 sq ft versus 1,050 in 2000. Millennials are finally forming households at scale. Baby boomers are downsizing from 4,000 sq ft houses to 1,500 sq ft condos. E-commerce requires storage for inventory. These aren't cyclical trends but structural shifts.

Consolidation Acceleration: Rising rates and tighter credit will force small operators to sell. Public Storage has $2 billion in liquidity to acquire distressed assets. They bought $7 billion of properties in the last cycle—the next downturn could see $10+ billion deployed at attractive returns.

Technology Moat Widening: Public Storage's technology investments are paying off. Customer acquisition costs dropped 40%. Revenue management systems add 2-3% annual rate growth. Operational efficiency improvements save $100 million annually. Small operators can't match these capabilities.

Hidden Asset Value: The real estate is carried at historical cost but worth far more. Manhattan facilities built for $50/sq ft in 1990 are worth $500/sq ft today. The replacement cost of Public Storage's portfolio exceeds $35 billion versus $18 billion book value. NAV per share could be $400 versus today's $312 stock price.

Interest Rate Relief Coming: The Fed will cut rates as inflation moderates. Lower rates reduce financing costs, increase acquisition activity, and compress cap rates. REITs historically outperform when rates fall. A 100 basis point decline in rates could drive 20% stock appreciation.

Macro Environment Increasingly Favorable

Several macro trends support Public Storage:

Housing Unaffordability: With mortgage rates at 7% and home prices at records, Americans are renting longer. Renters use storage 30% more than homeowners. Every year of delayed homeownership increases storage demand.

Geographic Mobility: Remote work made Americans more mobile. The average American moves 11 times—each move creates storage demand. Interstate migration reached record levels and remains elevated.

Demographic Destiny: 73 million millennials are entering prime storage years (30-50 age range). 76 million baby boomers are downsizing. Gen X is managing estates from deceased parents. Three generations simultaneously driving demand is unprecedented.

Financial Projections: The Path to $400

Analyst consensus projects: - 2025: Revenue $5.15B (+3%), FFO $2.05B (+5%), FFO/share $14.75 - 2026: Revenue $5.35B (+4%), FFO $2.18B (+6%), FFO/share $15.65 - 2027: Revenue $5.60B (+5%), FFO $2.32B (+6%), FFO/share $16.60 - 2028: Revenue $5.90B (+5%), FFO $2.45B (+6%), FFO/share $17.50

At historical average multiples of 23x FFO, 2028 earnings support a $400+ stock price—28% upside plus 15% cumulative dividends equals 43% total return over four years, or 10% annually.

Risk Factors to Monitor

- Sustained oversupply beyond 2026 in key markets

- Recession reducing discretionary storage demand

- Technology disruption (though unclear what replaces physical storage)

- Management missteps in capital allocation

- Regulatory changes to REIT taxation

- Climate change increasing insurance costs and property damage

The Verdict: Quality at a Reasonable Price

Public Storage isn't cheap at 22x earnings, but quality rarely is. The company offers: - Defensive characteristics during uncertainty - Offensive capability during distress - Technological advantages widening - Balance sheet strength for opportunistic growth - Management aligned with shareholders

For long-term investors seeking steady returns with downside protection, Public Storage merits consideration. It won't double overnight, but it could compound wealth steadily for decades—just as it has since 1972.

XI. Epilogue & Reflections

What would B. Wayne Hughes think of Public Storage today? Standing in one of the company's newest facilities—a gleaming six-story urban storage complex in downtown Seattle with facial recognition entry, climate-controlled units, and package acceptance services—would he recognize the business he founded with mariachi music and orange doors?

The founder who insisted on Denny's lunches might blanch at the $200 per square foot construction costs. The man who personally negotiated $10,000 maintenance contracts might puzzle over artificial intelligence algorithms adjusting prices every hour. The entrepreneur who saw storage as temporary land holding might marvel that those temporary orange boxes became permanent infrastructure for American life.

Yet beneath the technology and scale, Hughes would recognize the core truth he discovered in 1972: life's transitions create predictable demand for space and time. People still divorce, still die, still downsize, still dislocate. They still pay irrational prices to preserve memories, maintain options, and defer decisions. The business model remains elegantly simple—rent empty space to people navigating life's complexity.

The evolution from temporary to permanent infrastructure reflects a broader lesson about business building. Hughes thought he was in the land development business using storage for cash flow. He discovered he was in the business of solving human problems that never go away. The best businesses often emerge from such misunderstandings—Amazon thought it was selling books, Google thought it was organizing information, Facebook thought it was connecting college students. The founders who recognize the deeper truth and adapt their vision build enduring enterprises.

Public Storage's journey also illustrates how category-defining businesses emerge from confluence of factors no single actor controls. Hughes didn't create American materialism, suburban sprawl, or life transitions. He simply recognized these forces and built infrastructure to serve them. The lesson for modern founders: look for massive behavioral shifts that lack supporting infrastructure, then build the bridges, platforms, or in this case, storage units that emerging behaviors require.

The operational excellence that defines Public Storage offers timeless lessons. In an era obsessed with disruption, Public Storage dominated through execution. No patents, no network effects, no switching costs—just thousands of small operational improvements compounded over decades. While entrepreneurs chase breakthrough innovation, Public Storage proves that perfect execution of a simple idea often beats imperfect execution of a complex one.

The capital allocation story provides a masterclass in patient opportunism. Hughes waited years for the right deals, maintained conservative leverage when others binged on debt, and deployed capital aggressively during distress. This counter-cyclical philosophy—cautious during booms, aggressive during busts—requires psychological strength that few possess. But those who master it build dynasties.

Looking forward, self-storage faces evolution, not revolution. Automation will reduce labor costs further—imagine facilities with no human employees, just apps and robots. Urban density will drive vertical facilities that look more like warehouses than traditional storage. E-commerce will blur lines between personal storage and commercial fulfillment. Climate change will require resilient facilities that protect belongings from increasing natural disasters.

Yet the fundamental value proposition endures. Humans accumulate possessions that define identity. Life transitions create dislocation between current needs and future possibilities. Storage provides the buffer, the option, the peace of mind that precious things remain safe even as life changes. This psychological truth won't change even if the physical form evolves.

The competitive dynamics will intensify. Extra Space has scale nearly matching Public Storage. Institutional capital seeks storage's stable returns. Technology enables new entrants. International expansion beckons. But Public Storage's advantages compound daily—every customer served, every facility optimized, every market clustered adds to a moat that took fifty years to dig.

For investors, Public Storage represents a philosophical choice. It's not a lottery ticket or a moonshot. It won't make anyone rich overnight. But it exemplifies the boring compounders that build wealth over decades—businesses with predictable demand, rational competition, pricing power, and operational leverage. In a market obsessed with the next big thing, Public Storage is the last big thing, executed perfectly.

The broader lesson transcends storage. In every industry, fragmented markets await consolidation. Operational excellence beats innovation in most sectors. Patient capital eventually defeats impatient capital. Boring businesses often generate exciting returns. The principles Hughes applied to storage work in waste management, funeral homes, car washes, veterinary clinics—anywhere that fragmentation meets consolidation opportunity.

Perhaps the greatest lesson from Public Storage's journey is the power of focus. For fifty years, the company has done one thing: rent storage units. No diversification into apartments, offices, or hotels. No ventures into unrelated businesses. No transformation into a "platform" or "ecosystem." Just storage, executed better than anyone else, scaled beyond what anyone imagined possible.

In our age of endless pivots and constant disruption, Public Storage stands as a monument to the power of picking one thing and perfecting it over decades. Wayne Hughes found a simple business with attractive economics and never let go. He ignored fads, rejected diversification, and focused relentlessly on operational excellence. The result is a $54 billion testament to the power of patient concentration.

As Public Storage enters its sixth decade, it faces challenges—oversupply, competition, technological change. But it also possesses advantages that compound daily—scale, brand, operational excellence, balance sheet strength. The company that began as a temporary land play became permanent infrastructure. The boy who delivered newspapers in Depression-era Los Angeles built one of America's great businesses. The orange doors that caught drivers' attention in 1972 became symbols of an entire industry.

What would Wayne Hughes think of Public Storage today? He'd probably complain about construction costs, question marketing spend, and insist executives fly coach. But watching customers stream through those orange doors, solving life's transitions with storage units, generating 77% margins from concrete boxes—he'd recognize his creation. And perhaps, allowing himself a rare moment of satisfaction, he'd admit that building boring businesses beautifully might be the greatest innovation of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube