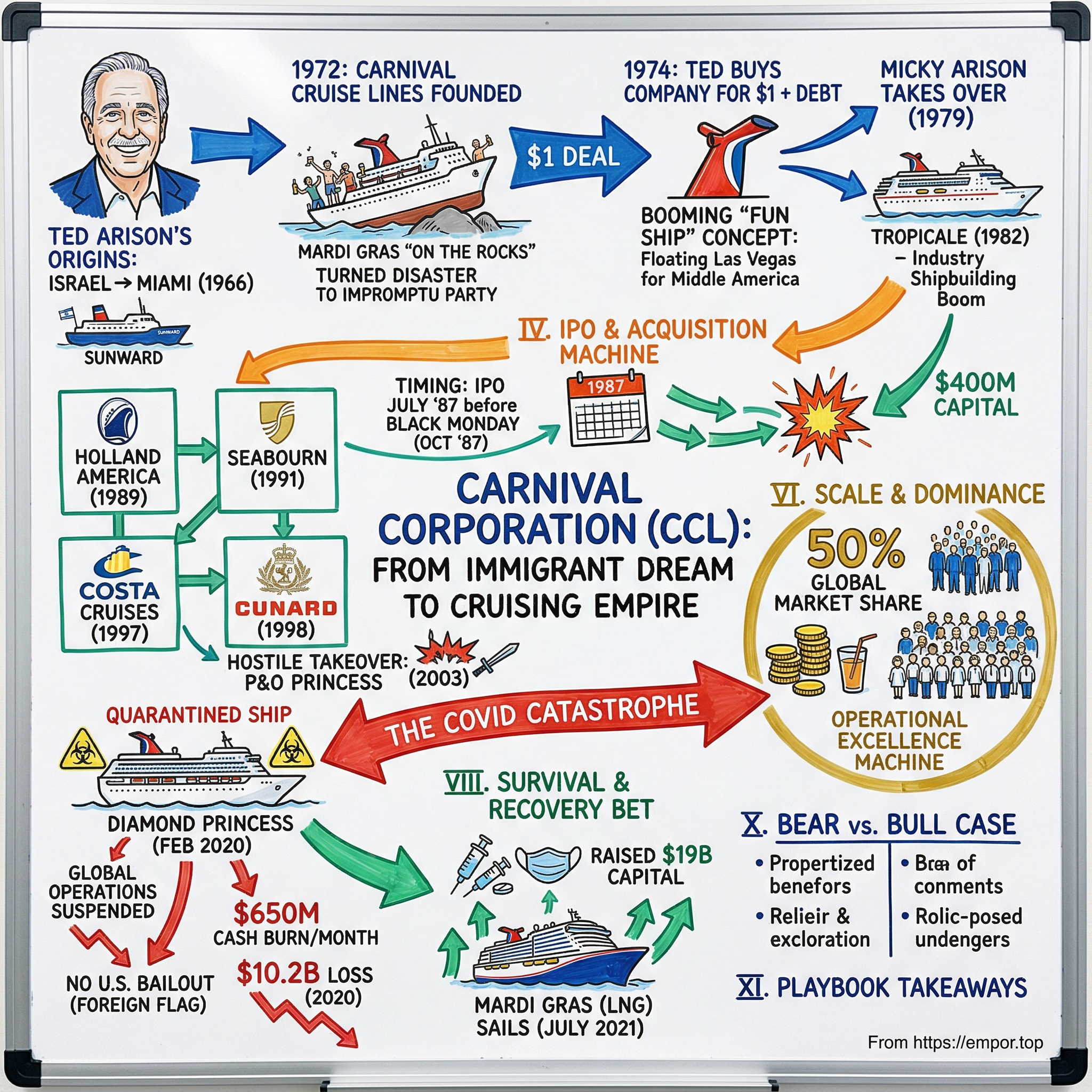

Carnival Corporation: From Immigrant Dream to Cruising Empire

I. Cold Open & Episode Thesis

Picture this: February 4, 2020. The Diamond Princess cruise ship sits quarantined in Yokohama Bay, Japan, transformed overnight from a floating paradise into a petri dish. Inside, 3,700 passengers and crew members are trapped as an invisible enemy spreads through the ventilation systems, down the corridors, into the dining halls. By the time Japanese authorities allow disembarkation two weeks later, over 700 people are infected with a novel coronavirus—making this single ship the largest COVID-19 outbreak outside of China at that moment in history.

For Carnival Corporation, owner of the Diamond Princess through its Princess Cruises subsidiary, this was just the opening act of a catastrophe that would see the company's market value evaporate by 80%, hemorrhage $650 million in cash every month, and post losses exceeding $10.2 billion in 2020 alone. The world's largest cruise operator—a company that had carried nearly 13 million passengers the year before and operated a fleet larger than many national navies—was suddenly fighting for survival.

Yet this near-death experience was merely the latest chapter in one of the most audacious business stories ever told. How did Ted Arison, an Israeli immigrant who arrived in America with little more than determination, transform a single second-hand ship purchased for one dollar into a $40 billion empire that would fundamentally reshape how humanity experiences leisure? How did his son Micky build upon that foundation to create a conglomerate that would control nearly half of all cruise passengers globally?

The Carnival story reads like fiction: a grounded ship on its maiden voyage that should have ended everything before it began. A perfectly-timed IPO one month before Black Monday in 1987. A hostile takeover battle that reshaped an entire industry. And through it all, the relentless execution of a simple but revolutionary idea—that cruising wasn't just for the wealthy elite, but could become the vacation of choice for middle America.

This is a story about immigrant grit meeting American opportunity. About turning operational excellence into monopolistic power. About surviving when every logical analysis says you shouldn't. It's the story of how one family built the machine that puts 30 million people on ships every year, and what happens when that machine suddenly stops.

The central question isn't just whether Carnival can recover from COVID—it's whether the fundamental bet Ted Arison made 50 years ago still holds: that humans will always crave escape, that the ocean calls to something primal in us, and that there's magic in waking up somewhere new every morning without having to pack your bags.

II. The Arison Origin Story & Early Hustles

Tel Aviv, 1924. The British Mandate of Palestine was barely four years old when Ted Arison was born into a family that embodied the Zionist dream. His parents were third-generation sabras—Jews born in the Land of Israel—with Romanian roots stretching back through generations of struggle and survival. Young Ted grew up speaking Hebrew in the streets and English in the classroom, a duality that would define his entire life.

The boy who would one day revolutionize American leisure first learned about ships not from luxury liners but from refugee vessels. During World War II, Arison enlisted in the Jewish Brigade of the British Army, witnessing firsthand the desperate attempts of Holocaust survivors to reach Palestine aboard overcrowded boats. After the war, he rose to lieutenant colonel in the nascent Israeli Defense Forces during the 1948 Arab-Israeli War, commanding logistics operations that required moving supplies and people under impossible conditions.

But peacetime Israel offered little for an ambitious young man with grand visions. Arison managed a small shipping company, but the country's economy was strangled by austerity measures and socialist policies that left little room for entrepreneurial ambition. "In Israel, if you made money, you were almost a criminal," he would later recall. The kibbutz mentality that built the nation was antithetical to the capitalist dreams brewing in Arison's mind.

So in 1952, at age 28, Arison made the decision that would reshape not just his life but an entire industry: he packed up his young family and sailed for America. He landed in New York with a few hundred dollars and immediately set about reimagining himself. Gone was the Hebrew accent, replaced by carefully practiced American English. Gone was the Israeli military officer, replaced by Ted Arison, freight shipping entrepreneur.

For over a decade, Arison bounced between ventures—air freight, cargo ships, anything involving moving goods or people for profit. Some succeeded modestly; most failed. By 1966, his marriage had collapsed, his businesses were struggling, and New York's winters felt particularly bitter to a man raised under Mediterranean sun. That's when he made his second pivotal geographic bet: Miami.

Miami in the 1960s was transforming from a sleepy Southern city into a gateway to Latin America and the Caribbean. Arison sensed opportunity in those turquoise waters. Through a series of connections in the shipping world, he met Knut Kloster, a Norwegian shipping magnate whose cargo line between Europe and the Caribbean was failing. Together, they hatched an audacious plan: convert Kloster's cargo ship into a cruise vessel and run it out of Miami. This partnership would birth Norwegian Caribbean Lines in December 1966, with their converted vessel, the Sunward, making its first voyage from Miami to Nassau. The venture was an immediate success—Americans were hungry for affordable international travel, and here was a way to visit multiple Caribbean islands without the hassle of airports and hotels. Arison handled operations while Kloster provided the ships and capital.

But tensions simmered beneath the surface. Kloster, the reserved Norwegian Protestant, viewed the business as shipping with passengers. Arison, the gregarious Israeli Jew, saw it as entertainment that happened to float. By 1971, their philosophical differences became irreconcilable. The partnership broke up on bad terms, with Arison walking away from the company he'd helped build from nothing.

At 47 years old, Ted Arison was starting over yet again. But this time, he carried something invaluable: five years of hard-won knowledge about what Americans really wanted from a cruise vacation. They didn't want the stuffy formality of transatlantic ocean liners. They didn't want to dress for dinner or follow rigid schedules. They wanted fun, sun, and simplicity—a floating Las Vegas with better weather.

The immigrant entrepreneur archetype that Arison embodied wasn't just about hunger or hustle. It was about seeing opportunities that natives couldn't perceive because they were too close to the culture. Arison understood that Americans worked harder than Europeans, saved less for retirement, and had shorter vacations. They needed maximum escapism in minimum time. They wanted to feel rich for a week without actually being rich.

This outsider's perspective would prove to be Carnival's greatest strategic advantage. While established cruise lines tried to preserve the golden age of ocean travel, Arison was ready to blow it all up and start fresh. He didn't revere maritime tradition—he'd seen enough ships in wartime to know they were just steel and engines. What mattered was what happened inside them, the memories created, the briefly transformed lives of middle-class Americans who'd never before awakened to a Caribbean sunrise.

III. The $1 Deal That Changed Everything

March 11, 1972, should have been Ted Arison's day of triumph. His new venture, Carnival Cruise Lines—formed with backing from Boston-based travel conglomerate American International Travel Service (AITS) and its flamboyant owner Meshulam Riklis—was launching its flagship vessel, the Mardi Gras, on her maiden voyage from Miami. The ship was packed with travel agents and media, ready to be wowed by Arison's vision of democratized cruising.

Then, disaster. Just hours after leaving port, the Mardi Gras ran aground on a sandbar off Miami Beach. Passengers watched in horror as Coast Guard cutters and tugboats struggled to free the 27,000-ton vessel while news helicopters circled overhead, broadcasting the humiliation to the entire nation. The ship sat there, tilted and stuck, for 24 hours—a beached whale in full view of the city Arison called home. The media had a field day. "Mardi Gras On The Rocks," screamed the headlines, playing on the ship's festive name. Competitors whispered that Carnival was finished before it had even begun. Travel agents, who'd been aboard for the inaugural voyage, called their clients to cancel bookings. AITS executives in Boston were apoplectic—their $5 million investment appeared to be literally stuck in the mud.

But Ted Arison possessed something more valuable than capital: the ability to transform disaster into opportunity. While the ship sat grounded, the crew kept pouring drinks and the band kept playing, turning the grounding into an impromptu 24-hour party. Arison himself walked the decks, joking with passengers, promising them free cruises, turning embarrassment into endearment. By the time tugboats finally freed the vessel, many passengers didn't want to leave.

The grounding was symptomatic of deeper problems. Carnival was hemorrhaging cash—there had been no money for proper refurbishment before the ship's launch. Old wooden furnishings were hastily covered with tin foil, the stuffy restaurant was converted on the fly. The company was so broke that they couldn't even afford to remove Canadian Pacific's logo from the funnel, simply painting over it instead.

By 1974, the situation had become untenable. Meshulam Riklis, watching millions disappear into the Caribbean, decided to cut his losses. That's when Arison made the boldest move of his career: he offered to take complete ownership of Carnival Cruise Lines for the princely sum of one dollar, plus assumption of $5 million in debt. Think about that for a moment. In 1974, Arison bought Riklis's share of Carnival for $1, also assuming the company's debt of more than $5 million. A company so distressed that its owner preferred to walk away with a single dollar rather than continue bleeding cash. Most rational businesspeople would have seen a death trap. Arison saw opportunity.

The genius of the "Fun Ship" concept wasn't just the word "fun"—it was the systematic stripping away of everything that made traditional cruising intimidating to middle-class Americans. No more formal nights unless you wanted them. No assigned dining times. No stuffy British officers looking down their noses at passengers in polyester. Instead, Carnival offered what Arison called "a party that happens to float."

Within a year of taking full control, Arison had turned Carnival profitable. How? By understanding that his competition wasn't other cruise lines—it was Las Vegas, Disney World, and all-inclusive Caribbean resorts. He wasn't selling transportation; he was selling transformation. For the price of a modest vacation, a factory worker from Detroit could feel like a millionaire for seven days.

The operational discipline Arison brought from his military days proved crucial. While competitors ran their ships like floating hotels with attached casinos, Arison ran his like military operations with entertainment divisions. Every crew member understood their role in the larger mission. Food costs were monitored to the penny. Fuel consumption was optimized to the gallon. The money saved didn't go into Arison's pocket—it went into keeping prices low and entertainment high.

By 1976, Carnival had added the Carnivale (formerly the Empress of Britain). By 1978, the Festivale (formerly the S.A. Vaal) joined the fleet. Each acquisition followed the same playbook: buy distressed assets, strip away the pretension, add neon and chrome, and market aggressively to first-time cruisers. The formula was so successful that by 1979, Ted handed day-to-day operations to his son Micky, who had been working in the company since dropping out of the University of Miami.

But Arison's masterstroke came in 1980 when he did something the industry considered insane: he ordered the construction of a brand-new ship, the Tropicale. After growing steadily through the acquisition of existing tonnage, Carnival stuns the cruise industry with its plans to build the Tropicale, which entered service in 1982 and fueled an industry-wide shipbuilding boom. While competitors were still buying and converting old ocean liners, Arison was building a ship designed from the keel up for the American cruise market—wide corridors for crowds, massive casinos, multiple pools, and that iconic winged funnel that looked like a whale's tail reaching toward the sky.

The Tropicale changed everything. It proved that cruising wasn't a dying industry capitalizing on nostalgia, but a growth business with untapped potential. It sparked an arms race in the cruise industry that continues to this day, with each new ship larger and more audacious than the last.

IV. Going Public & The Acquisition Machine

The story of Carnival's IPO reads like a thriller where the protagonist has inside information about the apocalypse. In 1986, Ted Arison was living in a Miami Beach condominium when his neighbor, Count de S.G. Elkaim—a vice president at E.F. Hutton—knocked on his door with an unusual proposition. "Ted," he said, "you need to take this company public. And you need to do it soon. There's a correction coming."

In 1986, Arison's condominium neighbor, Count de S.G. Elkaim (Vice President at E.F. Hutton & Company, Inc.), advised him to go public before an impending big correction in the stock market. Following his advice and guidance, Carnival Cruise Lines was floated on the American Stock Exchange in July 1987, one month before the stock market top and the infamous crash of October 1987.

The timing was so perfect it bordered on the surreal. Carnival went public in July 1987, raising approximately $400 million in capital. Carnival completes an initial public offering of 20% of its common stock, generating approximately $400 million. This influx of capital allowed the company to begin expanding through acquisition. Exactly one month later, the market peaked. On October 19, 1987—Black Monday—the Dow Jones dropped 22% in a single day, the largest one-day percentage decline in history.

Had Carnival waited even two months, the IPO window would have slammed shut. The company would have been trapped with its existing fleet, unable to finance expansion, watching competitors with deeper pockets eat its lunch. Instead, Arison sat on a war chest of fresh capital while the rest of the industry reeled from the crash.

Micky Arison, who had become CEO in 1979 at just 30 years old, understood that this capital created a once-in-a-generation opportunity. While competitors were slashing prices and cutting costs to survive the post-crash recession, Carnival went shopping. The younger Arison had inherited his father's opportunistic instincts but combined them with a cooler, more strategic approach to empire-building.

The acquisition spree that followed was methodical and brilliant. In 1989, Carnival acquired Holland America Line for $625 million, gaining not just ships but centuries of maritime heritage and a premium brand that appealed to older, wealthier cruisers—exactly the demographic Carnival Cruise Line didn't reach. The deal also included Windstar Cruises and Westours, giving Carnival a foothold in both ultra-luxury sailing and Alaska land tours. In 1991, Carnival purchased a 25% stake in ultra-luxury Seabourn Cruise Line, which at the time consisted of two 208-passenger all-suite vessels. Carnival's ownership in Seabourn increased to 50% in 1996 and the company assumed full ownership in 1999. The strategy was clear: own every segment of the market, from budget to ultra-luxury, ensuring that as customers aged and their incomes grew, they never had to leave the Carnival family.

1993 marked a symbolic turning point: the company changed its name from Carnival Cruise Lines to Carnival Corporation, acknowledging it had evolved from a cruise operator into a conglomerate. That same year, they sold the original Mardi Gras after 21 years of service—the ship that had started it all with a grounding was finally retired, having launched an empire.

The European expansion began in earnest in 1997 when Carnival Corporation acquired 50% of Costa Cruises, Europe's leading cruise company, taking 100% ownership three years later. Costa gave Carnival instant dominance in the Mediterranean and access to the European market that had always eluded American operators.

But the crown jewel came in 1998: Carnival Corporation acquired a 68% stake in the venerable Cunard Line, operator of the famed Queen Elizabeth 2. Carnival purchased the remaining 32% share of Cunard in 1999. This wasn't just buying ships—it was buying history, prestige, and the right to fly the red ensign. The company that had started with tin foil covering old furniture now owned the most storied name in ocean travel.

Ted Arison lived just long enough to see his empire reach this pinnacle. He died in Tel Aviv on October 1, 1999, having returned to Israel in 1990 to avoid U.S. estate taxes. His timing, as always, was impeccable—he passed away just months before the dot-com bubble burst, his fortune intact, his legacy secured.

The acquisition machine Micky inherited and refined wasn't just about getting bigger—it was about owning the entire customer journey. Young families started on Carnival, moved up to Holland America as they aged, tried Costa for European adventures, and aspired to Cunard for transatlantic crossings. Every life stage, every income level, every cruise fantasy could be fulfilled without ever leaving the Carnival ecosystem.

This portfolio approach also provided operational leverage that no single-brand competitor could match. Ships could be transferred between brands based on market conditions. Purchasing power for everything from fuel to food was magnified. Best practices in revenue management, developed at one brand, could be deployed across all.

By the turn of the millennium, Carnival Corporation had transformed from a one-ship operation running on fumes into a carefully orchestrated portfolio of brands that captured nearly 40% of all cruise passengers globally. The building of this conglomerate wasn't through hostile takeovers or financial engineering—it was through patient acquisition of distressed or undervalued assets, careful brand preservation, and relentless operational improvement.

V. The P&O Princess Hostile Takeover Saga

October 2001. The cruise industry was reeling from 9/11's devastating impact on travel. Bookings had evaporated overnight. Ships sailed half-empty. Smaller operators teetered on bankruptcy's edge. It was precisely the kind of chaos that Micky Arison had been trained by his father to exploit.

Royal Caribbean Cruises and P&O Princess Cruises announced they would merge, creating what they claimed would be the world's largest cruise company. The deal made strategic sense: Royal Caribbean was strong in North America, P&O Princess dominated in Britain and Australia. Together, they would create a global competitor to finally challenge Carnival's dominance.

Micky Arison read the announcement from Carnival's Miami headquarters with a mixture of surprise and opportunity. P&O Princess wasn't just another cruise line—it was a collection of jewels that included Princess Cruises (famous from "The Love Boat"), P&O Cruises UK, P&O Cruises Australia, AIDA Cruises in Germany, and significant tour operations in Alaska. The merged entity would control 41% of the global cruise market to Carnival's 34%.

What followed was one of the most dramatic hostile takeover battles in leisure industry history. On December 13, 2001—barely three months after 9/11—Carnival launched an unsolicited bid for P&O Princess worth £3.1 billion, trumping Royal Caribbean's offer by 20%. The gloves were off. The P&O Princess board initially rejected Carnival's offer outright, refusing even to engage in discussions. They had already agreed to merge with Royal Caribbean; breaking that agreement would trigger a $62.5 million breakup fee. More importantly, P&O Princess management preferred Royal Caribbean's "merger of equals" structure to being absorbed by Carnival.

But Micky Arison hadn't learned at his father's knee to accept rejection. He sweetened the offer repeatedly, eventually reaching $5.4 billion. More cleverly, he proposed a unique dual-listed company (DLC) structure that would allow P&O Princess to maintain its London listing and British identity while still combining operations. P&O Princess Cruises plc would remain a separate company, listed on the London Stock Exchange and retaining its British shareholder body and management team. The company was renamed Carnival plc, with the operations of the two companies merged into one entity.

The bidding war lasted over a year and played out across multiple continents. European regulators launched detailed investigations, concerned about market concentration. The U.S. Federal Trade Commission scrutinized the deal. Royal Caribbean fought desperately to save its merger, but by October 2002, P&O Princess's board concluded that Carnival's takeover offer was "financially superior" and that it was withdrawing support for the Royal Caribbean deal.

The final structure was byzantine but brilliant. Carnival Corporation and Carnival plc jointly own all the operating companies in the Carnival group. Shareholders in both entities had identical economic interests but traded on different exchanges. It preserved national pride while creating operational synergies. British shareholders kept their London-listed shares; American shareholders kept their NYSE listing.

On April 17, 2003, the deal closed. The combined company would have 65 ships and nearly 100,000 berths. Carnival had spent $5.4 billion to eliminate its largest potential competitor and secure brands that would have taken decades to build organically. The acquisition brought Princess Cruises (with its Love Boat heritage), P&O Cruises (Britain's national cruise line), AIDA (Germany's leading brand), and P&O Australia into the Carnival family.

The strategic implications were staggering. Carnival now controlled nearly 50% of the global cruise market. They had critical mass in every major geography—North America, Europe, UK, Australia, and Asia. The company could optimize deployment globally, moving ships between brands and regions based on seasonal demand. Purchasing power for everything from fuel to food reached unprecedented levels.

But perhaps most importantly, the deal killed the threat of a rival superpower. Had Royal Caribbean successfully merged with P&O Princess, the combined entity would have been larger than Carnival. Instead, Royal Caribbean was left as a strong but distinctly second-place competitor, a position it maintains to this day.

The hostile takeover also revealed Micky Arison's evolution as a CEO. Where Ted had been opportunistic and scrappy, Micky was strategic and sophisticated. He understood complex financial structures, could navigate regulatory mazes, and wasn't afraid to spend billions to protect Carnival's dominance. The son had become a different kind of empire builder than the father—less colorful perhaps, but equally effective.

VI. Scale, Dominance & The Golden Years

By 2010, Carnival Corporation had become something unprecedented in leisure history: a company that moved more people on vacation than many countries have citizens. With over 100 ships across nine major brands, Carnival accounted for nearly 50% of all cruise passengers globally—approximately 10 million people annually choosing a Carnival brand for their vacation.

The portfolio read like a geography lesson in cruise preferences. AIDA dominated Germany with its casual, club-like atmosphere. Costa ruled the Mediterranean with Italian flair. P&O UK maintained British traditions with formal nights and afternoon tea. Princess appealed to American premium travelers. Holland America captured the retiree market. Cunard owned transatlantic crossings. Seabourn defined ultra-luxury small ship cruising. P&O Australia had the Aussie market locked down. And at the center, Carnival Cruise Line continued pumping out floating Vegas casinos for middle America.

What made this dominance sustainable wasn't just size—it was the operational excellence machine that Micky Arison had built. Every ship in the fleet, regardless of brand, benefited from centralized procurement that could negotiate fuel contracts for 100+ vessels. A global network of port agents meant better berth rates and priority docking. Shared technology platforms reduced IT costs. Cross-brand marketing data identified customers ready to "graduate" from one brand to another.

The numbers during this golden age were staggering. Revenue grew every single year from 2015 to 2019, jumping over 10% from 2018 to 2019 alone. The broader industry was experiencing similar growth: from 17.8 million cruise passengers globally in 2009 to nearly 30 million by 2019. But Carnival was capturing the lion's share of that growth, adding capacity faster than competitors while maintaining pricing power. Micky Arison's leadership style during these golden years was markedly different from his father's hands-on approach. Where Ted had walked the decks of the Mardi Gras during its grounding, Micky managed from Miami, rarely visiting ships. He was more comfortable in boardrooms than engine rooms, more familiar with spreadsheets than sea spray. Yet this distance allowed him to see the business strategically rather than emotionally.

His other passion—owning the Miami Heat—provided unexpected synergies. The NBA team, which he'd controlled since 1995, taught him about managing millionaire talent, building championship cultures, and the value of star power. When the Heat won NBA championships in 2006, 2012, and 2013, Micky applied those lessons to Carnival: invest in the best (ships), create winning cultures (operational excellence), and market your stars (the ships themselves became celebrities).

The scale of Carnival's operations by 2019 was almost incomprehensible. On any given day, the company had approximately 270,000 people at sea—more than the population of Orlando. They consumed 70,000 pounds of lobster weekly, poured 1.5 million drinks daily, and employed 120,000 crew members from over 120 countries. The logistics rivaled military operations: coordinating provisions across 700+ ports, managing visa requirements for crew rotations, ensuring medical facilities met the needs of floating cities.

The financial engineering was equally sophisticated. Ships were registered in countries like Panama, Bermuda, and the Bahamas—not for tax avoidance alone, but for operational flexibility. Foreign flagging meant access to international crew at competitive wages, freedom from U.S. labor laws, and the ability to operate casinos in international waters. This regulatory arbitrage was legal, common in the industry, and essential to maintaining margins in a capital-intensive business.

Environmental challenges were mounting but manageable. New ships featured scrubber technology to reduce emissions, advanced wastewater treatment systems, and LED lighting throughout. The company invested heavily in LNG-powered vessels, positioning them as cleaner alternatives to traditional marine fuel. Critics pointed to the industry's carbon footprint, but Carnival argued that on a per-passenger-mile basis, cruising was more efficient than flying and staying in hotels.

The network effects at this scale were powerful. A customer who loved their Princess cruise to Alaska might book a Carnival cruise to the Caribbean the next year. Families could find age-appropriate experiences across the portfolio. Travel agents could offer solutions for every budget and taste without leaving the Carnival ecosystem. The company's loyalty programs, while brand-specific, created switching costs that kept customers returning.

By late 2019, Carnival Corporation was valued at over $35 billion, employed 150,000 people (120,000 shipboard, 30,000 shoreside), and had 19 new ships on order through 2025. Carnival Corporation announced financial results for the full year and fourth quarter ended November 30, 2019. Full Year 2019 U.S. GAAP net income of $3.0 billion, or $4.32 diluted EPS, enabled them to have strong full year earnings per share and another year of record adjusted earnings. The future looked boundless—new markets in China were opening, millennials were discovering cruising, and the company's newest ships were technological marvels that redefined the vacation experience.

The transformation from Ted Arison's one-dollar purchase to this global colossus was complete. Or so it seemed. Because while Micky Arison was reviewing fourth quarter 2019 results showing record revenues, a virus was beginning to spread in Wuhan, China. Within weeks, one of Carnival's ships would become the symbol of a global pandemic, and everything the Arisons had built over 48 years would teeter on the edge of collapse.

VII. The COVID Catastrophe

Dr. Kentaro Iwata, infectious disease specialist at Kobe University, uploaded a YouTube video on February 18, 2020, that would haunt Carnival Corporation forever. "The cruise ship was completely inadequate in terms of infection control," he said of the Diamond Princess. "There was no distinction between the green zone, which is free of infection, and the red zone, which is potentially contaminated. I was so scared."

The Diamond Princess had departed Yokohama on January 20, 2020, for a routine 16-day round trip cruise with 2,666 passengers and 1,045 crew. On January 25, an 80-year-old passenger who had disembarked in Hong Kong tested positive for a novel coronavirus. By February 4, when Japanese authorities quarantined the ship in Yokohama Bay, 10 passengers had tested positive. What followed was a public health disaster broadcast live to the world.

The ship's ventilation system, designed to efficiently circulate air through thousands of cabins, became a virus superhighway. Crew members, attempting to deliver meals to quarantined passengers, inadvertently spread contamination. Passengers documented their imprisonment on social media—elderly couples separated when one tested positive, crew members working without proper PPE, medicine running low. By the time quarantine ended on February 19, over 700 people were infected with COVID-19, making the Diamond Princess the largest concentration of cases outside China.

But Diamond Princess was just the beginning. Within weeks, 25 other Carnival ships across multiple brands reported infections. The Grand Princess circled off the California coast with infected passengers while authorities debated where it could dock. The Ruby Princess discharged 2,700 passengers in Sydney despite knowing about sick passengers aboard, sparking Australia's largest COVID cluster. The Zaandam wandered the Pacific for weeks with four dead passengers in its morgue, rejected by port after port. By mid-March 2020, operations were suspended globally. More than 1,500 positive infections and at least 39 fatalities occurred across the Carnival fleet. The U.S. House Committee on Transportation and Infrastructure opened investigations, demanding documents about Carnival's response. Australian police launched criminal probes into whether Princess Cruises misled authorities. Class-action lawsuits proliferated.

The financial hemorrhaging was immediate and catastrophic. Q2 2020 saw a $4 billion loss on an 85% revenue decline. The company was burning $650 million in cash monthly just to maintain its idle fleet. Ships require constant maintenance even when not sailing—generators running, hulls cleaned, systems cycled. With 100+ ships sitting empty, Carnival was operating the world's most expensive parking lot.

The cruel irony was that Carnival's foreign registration—the very structure that had enabled its success—now locked it out of U.S. government relief. Cruise line stock fell sharply on 27 March 2020 when the US$2 trillion relief package passed by the U.S. Congress and signed by President Trump excluded companies that are not "organized" under United States law. Carnival Corporation & plc is registered in Panama, England and Wales. Senator Sheldon Whitehouse, (D-RI), tweeted: "The giant cruise companies incorporate overseas to dodge US taxes, flag vessels overseas to avoid US taxes and laws, and pollute without offset. Why should we bail them out?" Senator Josh Hawley (R-MO) tweeted that cruise lines should register and pay taxes in the United States if they expect a financial bailout.

Carnival's response was both desperate and impressive. The company raised $19 billion through a combination of debt offerings, equity sales, and ship-backed securities. They ended 2020 with $9.5 billion in cash—enough to survive, barely. Interest rates on the new debt were punitive, some exceeding 11%, but the alternative was bankruptcy.

Management decisions during this period would be scrutinized for years. Ships were sold at fire-sale prices—18 vessels left the fleet, many scrapped for a fraction of their book value. Crew members from developing nations were trapped on ships for months, unable to return home due to travel restrictions. The company continued marketing future cruises even as the pandemic raged, offering credits rather than refunds to preserve liquidity.

Arnold Donald, who had become CEO in 2013 after the Costa Concordia disaster, faced the greatest challenge in cruise industry history. His background—a Carillon executive, Monsanto board member, never a cruise industry insider—suddenly seemed prescient. This crisis required financial engineering and government relations more than maritime expertise.

The existential threat was real. With $30 billion in debt, annual interest payments approaching $2 billion, and no clear timeline for resumption, Carnival faced a simple math problem: could they survive long enough for demand to return? Wall Street was skeptical—the stock fell from $51 in January 2020 to below $8 by March, a destruction of over $30 billion in market value.

Yet beneath the catastrophe, something remarkable was happening. Bookings for 2021 and beyond remained surprisingly strong. Despite watching cruise ships become floating prisons on the evening news, millions of Americans were booking future cruises. The deposits provided crucial liquidity, and suggested that Ted Arison's fundamental bet—that humans crave escape—might survive even a global pandemic.

VIII. Survival Mode & The Recovery Bet

March 2021. The Carnival Mardi Gras—the new $1 billion flagship sharing a name with Ted Arison's original ship—sat idle at the Meyer Turku shipyard in Finland. She was supposed to have launched in 2020, ushering in a new era of LNG-powered cruising. Instead, she embodied the entire industry's suspended animation: a magnificent vessel with nowhere to go.

But Arnold Donald saw something others didn't. While competitors hesitated, he made a contrarian bet: Carnival would be ready to sail the moment authorities allowed it. Ships began "simulated voyages" with volunteer passengers to test new health protocols. Crew were vaccinated as soon as doses became available. The company spent millions developing contact tracing systems, upgraded HVAC filtration, and reduced capacity to enable social distancing.

The ship sales, painful as they were, proved strategically sound. The 18 vessels that left the fleet were older, less efficient ships that would have required expensive upgrades to meet new environmental regulations. Their disposal reduced capacity by 12% but cut costs by nearly 20%. It was creative destruction in its purest form—using crisis to accelerate changes that should have happened anyway. The debt restructuring was equally creative. Rather than accepting whatever terms desperate lenders offered, Carnival played different capital markets against each other. They issued convertible bonds to equity investors hungry for upside, straight debt to fixed-income funds seeking yield, and even sold future cruise credits at a discount—essentially getting customers to finance the company's survival.

The Federal Reserve's actions, while not directly helping Carnival, created conditions for survival. The Fed's unprecedented liquidity injections meant capital markets remained open even for distressed borrowers. Low interest rates elsewhere pushed yield-hungry investors toward riskier assets. Carnival's bonds, despite their junk ratings, found buyers.

The vaccine rollout changed everything. Once it became clear that vaccines would enable safe cruising, the question shifted from "if" to "when." Carnival implemented comprehensive protocols: all fully vaccinated guests must show proof of a negative COVID-19 test taken within three days of their embarkation, crews were fully vaccinated, mask requirements in indoor spaces, reduced capacity to enable distancing. These measures, developed with medical experts, went beyond CDC requirements in many cases.

The restart itself was staggered and strategic. European operations resumed first—AIDA in the Canary Islands, Costa in Italy, P&O UK for domestic cruises. These markets had clearer regulations and less political interference than the U.S. Each successful sailing without major incidents rebuilt confidence and refined protocols.

The Florida situation epitomized the political complexities. Governor DeSantis signed legislation barring businesses from requiring proof of vaccination, directly conflicting with CDC guidance that ships need 95% vaccination rates to sail without restrictions. Some cruise lines chose to defy Florida law and pay potential fines; others created workarounds with "voluntary" vaccination disclosure. The irony of Florida—economically dependent on cruising—making restart harder wasn't lost on anyone.

By July 2021, Carnival ships were sailing again from U.S. ports. The pent-up demand was extraordinary. Despite CDC warnings, despite memories of Diamond Princess, despite everything—Americans wanted to cruise. Ships sailed at reduced capacity but with yields (revenue per passenger) often exceeding 2019 levels. Customers were willing to pay premium prices for the psychological release of normalcy.

The current state of recovery has exceeded most expectations. Bookings for 2023 and beyond are at record levels. The customers who returned weren't just the loyalists—new cruisers who had never considered the product before COVID were booking, drawn by competitive pricing and the promise of escape after years of lockdowns.

But the company that emerged from COVID is fundamentally different. The debt burden—now exceeding $30 billion—means annual interest payments of nearly $2 billion that didn't exist before. The fleet is smaller but more efficient. The shareholder base has turned over completely, with the Arison family's stake diluted by massive equity issuances. Most importantly, the industry's vulnerabilities have been exposed for all to see.

IX. Business Model & Strategic Analysis

To understand why Carnival survived when logic suggested it shouldn't, you must first understand the economics of floating cities. A modern cruise ship costs between $500 million and $1.5 billion to build, operates for 30-40 years, and generates revenue every single day it's at sea. The business model is elegantly simple: fill cabins, extract maximum revenue per passenger, minimize costs per available berth day.

The revenue architecture is sophisticated. The advertised cruise fare—what Ted Arison called "the loss leader"—typically represents only 50-60% of what a passenger ultimately spends. Onboard revenue—drinks, casino, spa, specialty dining, excursions, photos, internet—carries margins exceeding 80%. A family paying $2,000 for a week-long cruise might easily spend another $2,000 onboard. The genius is that once you're on the ship, Carnival has monopoly pricing power. Where else are you going to buy that piña colada?

The cost structure is equally intricate. Fuel represents 15-20% of operating costs, which is why slow steaming (reducing speed to save fuel) and itinerary optimization matter so much. Labor costs are controlled through foreign flagging—ships registered in Panama, Bahamas, or Malta can hire international crew at wages that would be illegal for U.S.-flagged vessels. A cabin steward from the Philippines might earn $1,000 per month plus tips, working 10-12 hour days for contracts lasting 6-9 months without a day off.

This foreign flagging strategy, while controversial, is essential to the business model. U.S. labor laws would require American wages, American working conditions, and American maritime unions. The cost difference would add thousands of dollars to every cabin fare, pricing cruises out of reach for middle America—destroying Ted Arison's founding vision of democratized cruising.

Capital intensity creates massive barriers to entry. Building a single ship requires not just billions in financing but years of planning, design, and construction. New entrants can't simply appear—they must commit capital years before generating revenue. This dynamic creates an oligopoly where three companies (Carnival, Royal Caribbean, Norwegian) control 80% of the global market.

The "floating city" complexity is often underestimated. A large cruise ship is simultaneously a hotel (3,000+ rooms), a restaurant complex (10+ venues serving 15,000 meals daily), an entertainment district (theaters, casinos, nightclubs), a shopping mall, a medical facility, a water treatment plant, a power generation station, and a small town's worth of accommodation for 1,500 crew members. Managing this complexity while moving at 20 knots through international waters requires operational excellence that takes decades to develop.

Network effects manifest in multiple ways. Port relationships mean better berth positions and rates for frequent visitors. Travel agent relationships—still crucial despite online booking—favor established players with proven track records. Customer databases enable sophisticated revenue management and targeted marketing. Brand loyalty programs create switching costs. Scale enables advertising efficiency—a Super Bowl ad makes sense when you have 100 ships to fill.

The environmental and social challenges are real and growing. Modern cruise ships burn 250 tons of fuel daily, emit sulfur and nitrogen oxides, and generate massive amounts of waste. Despite improvements—scrubbers, advanced wastewater treatment, LNG power—the industry's environmental footprint remains substantial. Social issues around crew welfare, overtourism in destinations like Venice and Dubrovnik, and tax avoidance through foreign flagging create reputational risks.

Yet the strategic positioning remains formidable. Cruising offers something no land-based vacation can replicate: unwrapping a new destination every morning without packing, driving, or flying. For Americans with limited vacation time, it maximizes experience while minimizing hassle. For retirees, it provides safe, structured travel with built-in companionship. For families, it offers something for every age in a contained environment.

Carnival's specific advantages within this industry structure are substantial. Scale enables lowest costs through purchasing power and operational efficiency. Brand portfolio captures every market segment without cannibalization. Geographic diversification—strong in U.S., UK, Germany, Australia, Italy—reduces single-market risk. The company's culture, instilled by the Arisons, focuses relentlessly on operational metrics: occupancy rates, revenue per available passenger cruise day, costs per available lower berth day.

The regulatory arbitrage inherent in the model—foreign flagging for labor flexibility, international waters for casino operations, tax optimization through complex corporate structures—isn't illegal but does create political risk. The COVID bailout debate highlighted how the industry wants American customers and ports while avoiding American taxes and regulations. This tension remains unresolved.

Looking forward, the business model faces both challenges and opportunities. Climate regulations will require massive investments in cleaner technologies. Demographic shifts—millennials traveling differently than boomers—demand new experiences. Competition from land-based resorts with increasingly sophisticated offerings intensifies. Yet the fundamental appeal—escapism efficiently delivered—remains powerful, and Carnival's position as the scale leader provides strategic options smaller competitors lack.

X. Bear vs. Bull Case

Bear Case: The Structural Decline Thesis

The bear case for Carnival starts with a simple observation: COVID didn't create new problems, it exposed existing ones. The industry's fragility—complete shutdown with one black swan event—revealed fundamental weaknesses that future crises will exploit again.

The debt burden is potentially fatal. With over $30 billion in debt versus a market cap that has struggled to exceed $20 billion, Carnival is effectively a leveraged bet on perfect execution. Annual interest payments approaching $2 billion create a massive hurdle before any dollar flows to shareholders. In the next recession, when discretionary travel spending evaporates, this fixed cost burden could trigger a death spiral.

Permanent demand destruction from COVID is real but hidden. Yes, ships are full now, but that's pent-up demand and price-sensitive customers attracted by deals. The cohort of cruisers who experienced or watched the Diamond Princess horror won't return. More importantly, the pipeline of new cruisers may be permanently impaired—young people who might have tried cruising during COVID years chose other vacation styles instead.

Environmental regulations are tightening globally. The International Maritime Organization's 2050 net-zero target isn't optional. European ports are implementing emission restrictions. The technology to meet these standards—hydrogen fuel cells, advanced batteries, synthetic fuels—either doesn't exist at scale or would require replacing the entire fleet. The capital requirements could exceed $50 billion, money Carnival doesn't have.

Demographic shifts are accelerating against cruising. Millennials and Gen Z prioritize experiences over consumption, authenticity over packaging, sustainability over convenience. Instagram culture favors unique, photographable moments—not the commoditized experience of a cruise ship. The average cruise passenger age keeps rising as younger generations choose differently.

Competition from land-based alternatives intensifies yearly. All-inclusive resorts now match cruise pricing while offering more space, better food, and no seasickness. Airbnb enables unique stays globally. Even road trips in electric vehicles appeal more to environmentally conscious travelers than floating cities burning bunker fuel.

The labor model is unsustainable. Exploitation of developing world crew—paying below minimum wage, requiring months without days off—faces increasing scrutiny. A single viral TikTok about crew conditions could trigger boycotts. Unionization efforts, successful lawsuits, or regulatory changes could destroy the cost structure overnight.

China, the great growth hope, has disappointed. Chinese consumers prefer shorter cruises, spend less onboard, and demand different experiences than Western passengers. Local competitors understand the market better. The dream of millions of Chinese cruisers may remain just that—a dream.

Bull Case: The Resilience and Recovery Thesis

The bull case begins with history: every crisis in cruising's history has been followed by stronger growth. The Achille Lauro hijacking in 1985, the Concordia disaster in 2012, multiple norovirus outbreaks—each time, pundits declared cruising finished. Each time, they were wrong.

Pent-up demand isn't temporary—it's structural. After experiencing COVID lockdowns, consumers viscerally understand the value of escape. Cruising offers the maximum escape with minimum friction. The 30+ million people who cruised in 2019 didn't disappear; they're waiting. Meanwhile, millions who never considered cruising are now interested precisely because life is uncertain—better to travel now while you can.

The balance sheet, while stressed, is manageable. Yes, $30 billion in debt is substantial, but against an asset base of 90+ ships worth $50+ billion, the leverage is actually reasonable. Interest coverage improves with every quarter of operations. The debt market's willingness to refinance at better terms shows institutional confidence. Patient capital sees the long-term value.

Industry consolidation opportunities abound. Smaller operators lacking Carnival's scale face extinction. Distressed assets can be acquired cheaply. Carnival could emerge from this crisis with 60% market share versus 45% previously. In a scale business, that additional share translates to monopolistic pricing power.

Cost structure improvements from COVID are permanent. The company learned to operate with less—smaller corporate staff, more efficient ships, optimized itineraries. New technologies implemented during restart—contactless payment, app-based services, automated operations—reduce ongoing costs. The crisis forced operational improvements that would have taken decades otherwise.

Emerging markets growth potential remains massive. Only 2% of Chinese have ever cruised. India's middle class is exploding. Southeast Asia, Latin America, Africa—billions of potential cruisers who haven't discovered the product. Carnival's global brand portfolio positions it to capture this growth better than regional competitors.

Barriers to entry have actually increased. Post-COVID regulations are more complex. Financing new builds is harder. Port access is restricted. The expertise to operate safely is scarce. This isn't an industry where tech disruption threatens incumbents—no Silicon Valley startup can build and operate cruise ships.

The environmental transition is an opportunity, not a threat. Carnival's newer LNG ships are already cleaner than competitors' older fleets. Government subsidies for green shipping will flow to established operators. Customers will pay premiums for sustainable cruising. First movers in green technology will capture market share from laggards.

The experience remains unmatched. Virtual reality won't replace waking up in Santorini. Work-from-home makes physical escape more valuable, not less. Multi-generational family travel—grandparents, parents, kids together—suits cruising perfectly. No land-based alternative offers the same combination of convenience, variety, and value.

Most fundamentally, the bull case rests on human nature. We are social creatures who crave novel experiences, peer interaction, and temporary escape from responsibility. Cruising delivers all three more efficiently than any alternative. The format that Ted Arison invented—a floating party that moves—speaks to something primal in the human experience. That doesn't change because of one pandemic.

XI. Playbook Takeaways

The Immigrant Entrepreneur Advantage

Ted Arison's story illustrates a pattern repeated throughout American business history: the immigrant who sees opportunities invisible to natives. His lack of reverence for established norms—stuffy British cruise traditions—allowed him to reimagine the entire industry. He didn't speak the language of maritime tradition; he spoke the language of mass-market entertainment. Founders should remember: being an outsider isn't a disadvantage if you're serving outsiders, and in mass markets, everyone's an outsider to something.

Timing Markets vs. Time in Market

The 1987 IPO timing appears miraculous in hindsight—going public one month before Black Monday. But this wasn't luck; it was preparation meeting opportunity. Arison had built a profitable business over 15 years before accessing public markets. He didn't need the capital desperately; he could afford to wait for the right moment. The lesson: build a sustainable business first, then time the capital markets opportunistically, not desperately.

Hostile Takeover Execution

Micky Arison's P&O Princess acquisition reveals the playbook for successful hostile takeovers: (1) Know the target better than they know themselves—Carnival had courted P&O for years; (2) Structure creatively—the dual-listed company preserved target company pride while achieving synergies; (3) Overpay tactically—the extra billion dollars spent to win killed a permanent competitor; (4) Move fast—regulatory windows close quickly; (5) Have financing locked before launching—uncertainty kills deals.

Crisis Management and Liquidity

COVID revealed Carnival's crisis playbook: Cut costs immediately and deeply (18 ships gone, thousands of employees terminated). Raise capital at any price (11% interest rates accepted). Preserve customer relationships (credits not refunds). Prepare for recovery during the crisis (protocols developed, ships maintained). Communicate confidence constantly (Arnold Donald's media presence). The rule: in existential crises, dilution beats dissolution.

Conglomerate vs. Focused Strategies

Carnival proves conglomerates work when the businesses share infrastructure but serve different customers. Ships can move between brands. Purchasing is centralized. Technology is shared. But Princess customers never feel like they're on a Carnival ship. The key: operational synergies without brand contamination. This requires discipline—resisting the temptation to homogenize for efficiency.

The Power of Controlling Distribution

Carnival's relationship with travel agents—still booking 70% of cruises—creates a moat. These agents steer customers to trusted brands with good commission structures and reliable operations. Carnival nurtures these relationships obsessively: dedicated support lines, guaranteed commissions, familiarization cruises. The lesson: in commodity businesses, controlling distribution matters more than product differentiation.

When to Bet the Company

Carnival has made three bet-the-company moves: Arison's $1 purchase in 1974, the 1987 IPO preceding massive expansion, and the COVID survival financing. Each shared characteristics: asymmetric upside (massive market if successful), survivable downside (could operate smaller if necessary), and conviction from concentrated ownership (Arisons had skin in the game). The rule: only bet the company when you personally control the outcome and can survive being wrong.

Additional tactical insights from the Carnival playbook:

Regulatory Arbitrage as Strategy: Foreign flagging isn't just tax avoidance—it's operational flexibility. But this requires managing political risk carefully. Carnival maintains massive economic impact in U.S. ports, making it politically costly to exclude them despite foreign registration.

Brand Portfolio Theory: Multiple brands aren't just about market segmentation—they're about risk distribution. When Concordia damaged Costa's reputation, other brands were unaffected. When older Americans stopped cruising during COVID, younger-skewing brands recovered faster.

The Power of Incremental Innovation: Carnival never invented anything revolutionary—they just made cruising 10% better every year for 50 years. Compound improvement beats radical innovation in capital-intensive industries.

Customer Financing as Growth Hack: Selling future cruise credits during COVID was genius—customers effectively provided zero-interest loans. The principle: your best source of capital is customers who believe in your future.

Operational Metrics Obsession: The Arisons tracked occupancy rates daily, revenue per berth obsessively, costs per passenger mile religiously. In low-margin businesses, small improvements in metrics compound to massive differences in profitability.

XII. Grading & Final Thoughts

Acquisition Grades:

Holland America Line (1989, $625 million): A+ Acquired premium brand, Alaska tour operations, and loyal customer base at reasonable multiple. Integration smooth, brand identity preserved, synergies realized. Set template for future acquisitions.

Seabourn (1991-1999, acquired in stages): B+ Entered ultra-luxury segment with established player. Small scale limited impact, but strategic positioning in high-margin segment valuable. Proved Carnival could manage premium brands.

Costa Cruises (1997-2000, €2 billion total): A- Dominant European position acquired, massive fleet added. Integration challenging due to cultural differences, but strategic value enormous. Concordia disaster hurt grade, but market position retained.

Cunard Line (1998, $500 million): A+ Iconic brand acquired at distressed price. Queen Mary 2 investment proved management commitment to heritage. Brand value exceeds purchase price multiple times over.

P&O Princess (2003, $5.4 billion): A Expensive but transformative. Eliminated major competitor, achieved global dominance, secured UK/Australia markets. Dual-listed structure complicated but preserved value. Worth every penny despite premium paid.

What Ted Arison Understood That Others Didn't

Ted Arison grasped three fundamental insights that eluded established players:

First, he understood that Americans didn't want transportation—they wanted transformation. The journey wasn't about getting somewhere; it was about becoming someone else temporarily. A secretary could be a high-roller in the casino. A plumber could have a butler (cabin steward). For one week, working-class Americans could live like millionaires.

Second, he recognized that simplicity was luxury for middle America. One price, one suitcase, one decision—then everything handled. No currency exchanges, no restaurant researching, no hotel switching. The cognitive load of vacation planning disappeared. This wasn't dumbing down; it was smartening up the product for time-starved Americans.

Third, he saw ships as entertainment platforms, not vessels. The ocean was just the stage; the ship was the show. This inverted the entire industry's thinking. Traditional operators saw ports as destinations; Arison saw them as excursions from the real destination—the ship itself.

Micky's Stewardship Evaluation

Micky Arison's 34-year CEO tenure (1979-2013) and continuing chairmanship presents a complex legacy. The quantitative success is undeniable: growing from three ships to 100+, from hundreds of millions in revenue to $20+ billion, from startup to global dominance.

His strategic choices proved mostly correct. The acquisition strategy created unassailable scale advantages. The brand portfolio approach captured every market segment. The international expansion diversified risk. The operational excellence culture delivered industry-leading margins.

Yet questions remain. Did the pursuit of scale sacrifice resilience? The COVID near-collapse suggests overcapacity and overleveraging. Did financial engineering overshadow innovation? Carnival's ships, while larger, aren't fundamentally different from 1990s designs. Did the focus on shareholder returns compromise stakeholder interests? Crew welfare, environmental impact, and tax avoidance create ongoing reputational risks.

The ultimate evaluation may be that Micky was the perfect CEO for cruising's growth phase but possibly not for its maturity phase. He built an empire; whether that empire can evolve remains uncertain.

The Ultimate Test of Resilience

COVID provided the most extreme stress test imaginable: complete shutdown of operations, massive cash burn, existential uncertainty. That Carnival survived at all is remarkable. That it's recovering faster than expected is impressive. But true resilience isn't just surviving crisis—it's emerging stronger.

The company emerging from COVID is leaner, more efficient, and paradoxically better positioned competitively. Weaker players have disappeared. Industry capacity is rationalized. Customer appreciation for cruising has arguably increased. The debt burden, while heavy, is manageable if operations normalize.

But structural challenges remain. Environmental regulations will require massive investment. Demographic shifts may reduce addressable market. Competition from alternative vacation styles intensifies. The next crisis—pandemic, terrorism, economic—will test a company with less financial flexibility.

Lessons for Founders and Investors

For Founders: - Democratization is the ultimate market expansion: Taking luxury and making it accessible creates billion-dollar opportunities - Operational excellence beats innovation in capital-intensive industries: Perfect execution of existing ideas often trumps new invention - Crisis creates opportunity if you have liquidity: Downturns are when empires are built or destroyed—cash determines which - Family control enables long-term thinking: The Arisons could make decade-long bets because they didn't face quarterly activism - Industry outsiders see opportunity insiders miss: Not knowing how things "should be done" is often an advantage

For Investors: - Scale advantages in physical businesses are more durable than digital: Network effects in atoms are harder to disrupt than bits - Regulatory arbitrage is powerful but risky: Foreign flagging enabled Carnival's model but created political vulnerability - Brand portfolios provide resilience: Multiple brands serving different segments reduces concentration risk - Capital intensity creates barriers and opportunities: High fixed costs deter entrants but create operational leverage - Recovery trades require patience and stomach: Buying Carnival at $8 in 2020 required believing in human nature over headlines

The Carnival story ultimately validates Peter Thiel's monopoly thesis: competition is for losers. Through relentless acquisition, operational excellence, and scale advantages, Carnival built a legal monopoly in mass-market cruising. Whether that monopoly survives technological, environmental, and social changes remains the billion-dollar question.

Ted Arison would likely be unsurprised by both the crisis and recovery. He survived wars, built businesses from nothing, and understood that human nature doesn't change. People will always crave escape, seek value, and choose convenience. He built a machine that delivers all three more efficiently than any alternative. That machine nearly broke in 2020, but it didn't break. In business, as in life, sometimes not breaking is victory enough.

The final lesson from Carnival may be this: in industries with high fixed costs and capital intensity, survival is strategy. Every year you survive while competitors struggle, your relative position improves. Every crisis weathered builds organizational capability. Every cycle navigated generates institutional knowledge. Carnival has survived everything from groundings to pandemics. That survival capability, more than any specific asset or brand, may be its greatest competitive advantage.

For investors evaluating Carnival today, the question isn't whether cruising recovers—it's whether the company's leverage allows it to capture that recovery's value. For entrepreneurs studying the model, the lesson isn't about ships—it's about finding industries where operational excellence can build monopolies. For everyone else, Carnival reminds us that the most successful businesses often solve psychological needs, not practical ones. Ted Arison didn't sell transportation; he sold temporary transformation. In a world where identity is increasingly fluid and reality increasingly digital, that product may be more relevant than ever.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube