Primerica: The MLM That Became a Financial Services Powerhouse

I. Introduction: A Football Coach's Unlikely Empire

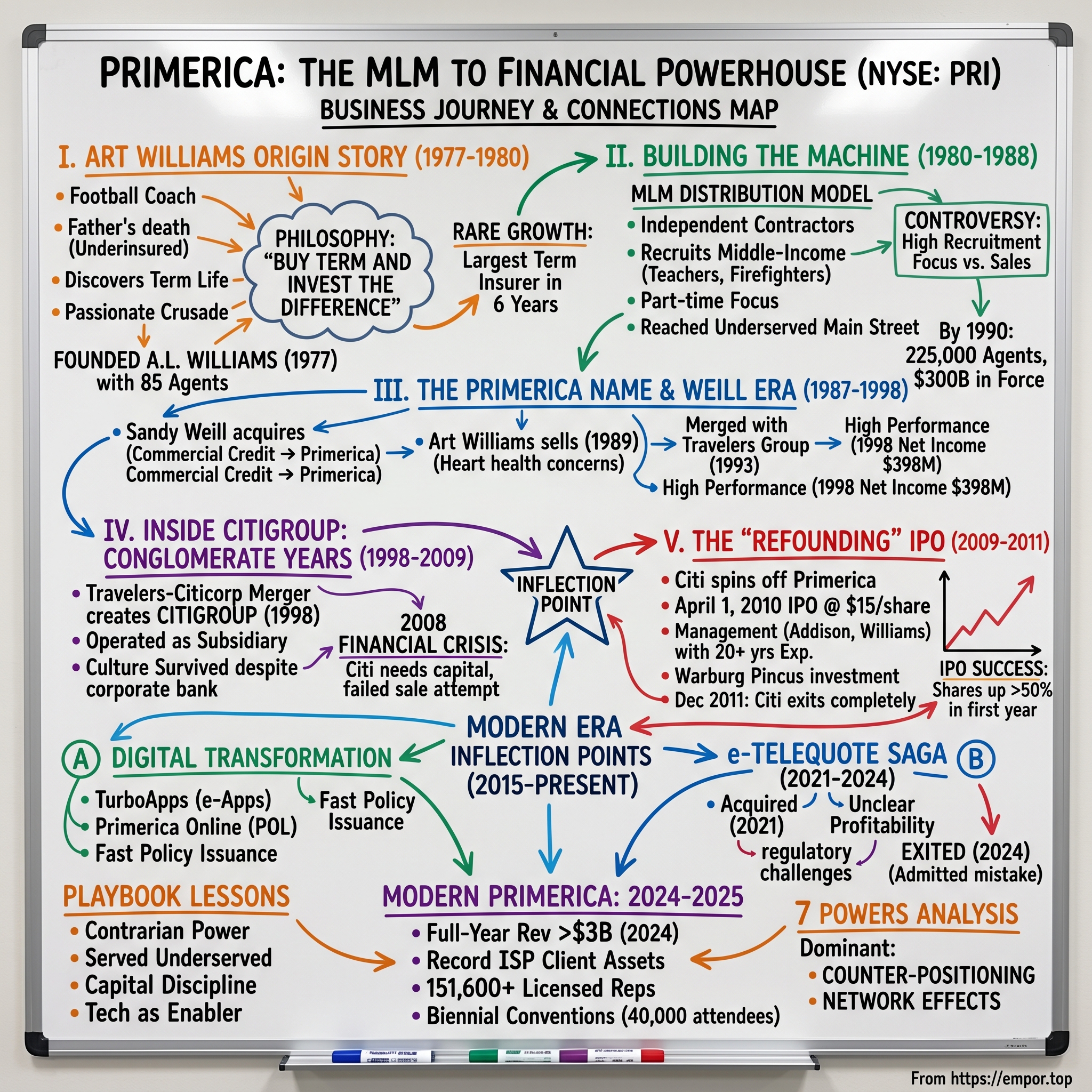

Imagine standing at the edge of a football field in Columbus, Georgia, in the early 1970s. The man pacing the sidelines—clipboard in hand, whistle around his neck—earns $10,700 a year coaching high school athletes. He has won two "State Coach of the Year" awards. His players adore him. By every conventional measure, Art Williams has achieved his dream.

Then imagine that same man, less than two decades later, commanding a sales force of 225,000 people, having built a company that sells more individual life insurance than Prudential and New York Life combined. The firm he founded from nothing now controls $300 billion in life insurance face value.

Art Williams is the founder of A.L. Williams & Associates, known as Primerica Financial Services since 1991. Today, that company—Primerica, Inc. (NYSE: PRI)—trades on the New York Stock Exchange with a market capitalization approaching $9 billion, with a sales force that grew to 152,200 life-licensed representatives as of September 30, 2025.

This is the story of how a crusade against the life insurance establishment, powered by a controversial multi-level marketing structure, survived multiple corporate owners, emerged from the wreckage of Citigroup, and rebuilt itself into one of North America's dominant term life insurance providers.

The central question worth investigating: How did a high school football coach's contrarian philosophy—"Buy Term and Invest the Difference"—create a company that now ranks as the #1 term life insurance issuer by new annualized premium in the first quarter of 2024, leading even State Farm?

Primerica, Inc. completed its initial public offering on April 1, 2010, with shares initially priced at $15. Since then, the stock has delivered extraordinary long-term appreciation. The all-time high Primerica stock closing price was $301.45 on November 26, 2024. That represents roughly a 20-fold return for investors who bought at the IPO price—not including dividends.

The story weaves together several powerful themes: the power of a contrarian philosophy, the mechanics of multi-level marketing at massive scale, the art of maintaining culture through decades of corporate conglomerate ownership, and ultimately, what the company calls its "Refounding"—the remarkable 2010-2011 transition from Citigroup subsidiary to independent public company.

Let's go back to where it all began.

II. The Art Williams Origin Story: A Football Coach's Crusade (1977–1980)

The Primerica story doesn't begin in a boardroom. It begins with a heart attack.

In 1965, Williams's father suddenly died of a heart attack. He had a whole life insurance policy that left their family underinsured. Art was in college at the time, watching helplessly as his mother struggled to raise his two younger brothers and pay the bills alone.

For years afterward, Art Williams didn't think much about insurance. A high school football coach, Art Williams didn't know anything about insurance or investments. Most people he knew—including himself—bought just enough "whole life" to cover burial expenses. Life insurance was expensive. That was simply the way things were.

Five years later, Art Williams' cousin Ted Harrison introduced him to the concept of term life insurance, a simpler alternative to whole life. The conversation was a revelation. Term life—pure death protection without the cash value component—cost a fraction of whole life premiums for the same coverage amount. Art was shocked to learn he could provide $150,000 in coverage for his family at a price far lower than the whole life policies his father had owned.

The more Art learned, the angrier he became. Williams was taken aback by the idea of not knowing that there was a choice when buying life insurance and described the whole conversation as "disturbing," recalling his father's death. Believing that families were paying too much for whole life policies that left them poor in the wallet and deeply underinsured, Williams joined his cousin at ITT Financial Services in 1970.

For the next several years, Art sold term insurance part-time while continuing to coach football. He began to sell term insurance part-time, and quickly found that his commissions surpassed his coach's salary. The products were selling themselves—families who understood the comparison between term and whole life often converted on the spot.

In June 1973, six months before ITT went out of business, he left and went on board with Waddell & Reed, another "Buy term and invest the difference" company. Williams gained momentum at W&R and became regional vice-president the same year, with a sales force that covered six states.

But Williams grew frustrated with the corporate structure at Waddell & Reed. Despite the numerous benefits of working at W&R in comparison to ITT, it became clear to Williams that with a corporate structure in which the executives, not the sales force, owned the company, financial decisions would always have priorities that conflicted with his agents' interests.

So he did what entrepreneurs do: he walked away from security and bet on himself.

On February 10, 1977, with no business education or corporate management experience, he formed A.L. Williams & Associates in Atlanta, Georgia, with just 85 agents.

The early days were chaotic, exhilarating, and frequently absurd. Art Williams brought a coach's mentality to building a financial services company. He talked about "crushing" the competition. He held meetings that felt more like football team huddles than corporate gatherings. His agents called themselves "termites"—a play on the term insurance they sold and their intention to eat away at the traditional insurance establishment.

A.L. Williams became one of the fastest-growing companies in modern business history. After six years in the industry, it was the largest term life insurance company. In ten years, it was a billion-dollar company.

The philosophy was simple enough to fit on a bumper sticker: "Buy Term and Invest the Difference." The logic was equally straightforward. Whole life insurance combined death protection with a forced savings component (the "cash value"). But the returns on that cash value were typically poor compared to what families could earn by simply buying cheaper term insurance and investing the premium savings in mutual funds or other vehicles.

By stripping away the cash value component and selling pure protection, A.L. Williams could offer families far more coverage for the same premium—or the same coverage for far less money. The difference could then go into retirement accounts, education savings, or other investments.

The traditional insurance industry hated this message. Art did something no one else before him had done—he challenged a stagnant industry with a better product...and a revolutionary way of selling to families who needed help. "Buy Term and Invest the Difference" became his passionate crusade—and battle cry for a little "no name" company that single-handedly tackled the scheming political world of life insurance.

By 1984—just seven years after the company's founding—the results were staggering. The company placed $38 billion of life insurance in force, leading the entire industry. By 1990, the company had a sales force of 225,000 people and ranked as the largest seller of individual life insurance in the United States, selling $93.5 billion in face value of individual life insurance. In just 12 years, the company became the first in the entire industry to have more than $300 billion of life insurance in force.

The raw numbers don't capture the cultural intensity of what Art Williams built. His speeches became legendary—particularly the "Just Do It" talk (delivered years before Nike adopted a similar phrase) that became required listening for his agents. The conventions, the recognition programs, the emphasis on promoting from within—all of it created a sense of mission that transcended simple product sales.

In a story rich with the details and anecdotes, heroes and villains, Art Williams chronicles how A.L. Williams and its "ragtag army of part-timers" took on a Goliath-sized insurance industry.

The investment thesis that would later attract conglomerate acquirers was already visible: a motivated, self-replicating sales force that could reach customers traditional insurance agents never touched.

III. Building the Machine: MLM Model & Early Scaling (1980–1988)

The growth of A.L. Williams was powered by a distinctive distribution model that would become both the company's greatest strength and its most persistent source of controversy.

In 1980, A.L. Williams (founded in 1977) entered into a contract with Boston-based Massachusetts Indemnity and Life Insurance Company (MILICO), an underwriter of life insurance and a subsidiary of Santa Monica–based PennCorp Financial Services. This partnership solved a critical problem: A.L. Williams could sell insurance, but it needed an established carrier to actually underwrite the policies.

The MILICO relationship provided the institutional backbone that allowed Art Williams to focus on what he did best: recruiting, training, and motivating a massive field force.

Primerica uses a multi-level marketing strategy, with eleven tiers of representatives and recruiters selling financial products and services for commission. This structure remains the foundation of Primerica's business model today.

How does the MLM model work in practice? New representatives join the company as independent contractors—not employees. They receive training and licensing support, but their income depends entirely on their sales and the sales of representatives they recruit. Successful agents who build "downlines" (teams of other agents) earn override commissions on their team's production, creating income that compounds with scale.

Primerica's key differentiator was a unique distribution model consisting of part-time agents organized in a multi-level marketing structure, which efficiently reached the underserved lower-to-middle income consumer.

The part-time nature of the sales force was intentional and strategic. Rather than recruiting career insurance agents who might bring preconceptions about how the business should work, A.L. Williams recruited school teachers, firefighters, police officers, and factory workers—people who could relate to middle-income families because they were middle-income families. These representatives often knew their customers personally. They sold insurance across kitchen tables in living rooms, not in sterile office buildings.

Over the next 13 years, the "peanut" company grew into an industry phenomenon—a licensed sales force of 225,000 agents, $300 billion in cumulative sales, thousands of offices across the United States and Canada.

By 1986, the company had expanded into Canada, and by 1987, through its underwriter MILICO (which would later become Primerica Life), it had over one million life insurance policies in force, providing millions of families with over $200 billion in term life protection.

The culture Art Williams cultivated resembled a religious revival as much as a corporate enterprise. Conventions were massive events—tens of thousands of agents gathering to celebrate top performers, hear inspirational speakers, and recommit to the mission. Recognition was lavish and public. The message was consistent: ordinary people could achieve extraordinary results if they believed in the cause and worked hard enough.

This culture had genuine believers. Many agents built substantial incomes and achieved financial independence they never imagined possible as teachers or firefighters. Some became millionaires. The "crusade" language wasn't just marketing—for true believers, replacing whole life policies with term insurance felt like a moral mission.

But the model also had critics. The MLM structure meant that many recruits earned little or nothing, while those at the top of successful hierarchies captured the lion's share of the economics. The emphasis on recruitment alongside sales created what some viewed as pyramid-like incentives. And the passion of true believers sometimes crossed into aggressive sales tactics that alienated prospects.

One of the most common criticisms of Primerica is how much it focuses on recruitment rather than actual sales. Critics argue that Primerica's reps are incentivized to bring in new agents more than they are to sell financial products.

These tensions have followed Primerica throughout its history and remain relevant today. The company operates as a legitimate, regulated financial services business—it is not a pyramid scheme in any legal sense. But the multi-level marketing structure continues to generate skepticism among industry observers and consumer advocates who question whether the model truly serves representatives' interests.

While recruitment drives the MLM model, Primerica focuses on financial education and products, distinguishing it from pure pyramid schemes.

What cannot be disputed is the sheer effectiveness of the distribution machine Art Williams built. By the late 1980s, A.L. Williams had fundamentally disrupted the life insurance industry, forcing established carriers to offer their own term products and acknowledge that cash value wasn't the only legitimate approach to life insurance.

IV. The Primerica Name & Sandy Weill Era (1987–1998)

The late 1980s brought transformative changes that would shape the company's corporate identity for decades to come.

The name "Primerica" first appeared in 1987—not attached to Art Williams' company, but to a completely different entity. In 1987, American Can changed its name to Primerica Corporation, with Gerald Tsai as CEO, the first Chinese American to lead a member of the Dow Jones Industrials.

This Primerica Corporation was a diversified conglomerate that had evolved far from its origins as a container manufacturer. Among its holdings was Smith Barney, the venerable Wall Street brokerage firm, and PennCorp Financial Services—the parent company of MILICO, which underwrote A.L. Williams' policies.

Then came Sandy Weill.

Sanford I. Weill was already a legendary figure on Wall Street. He had built Shearson into one of the largest brokerage firms in America, sold it to American Express, and then—after losing a power struggle with American Express leadership—walked away and started over.

After an attempt to become the CEO of BankAmerica Corp., he persuaded Minneapolis-based Control Data Corporation to spin off a troubled subsidiary, Commercial Credit, a consumer finance company. In 1986, Weill bought Commercial Credit for $7 million.

From this modest base, Weill began executing one of the most ambitious acquisition strategies in financial services history. In December 1988, Sanford Weill's Commercial Credit acquired Primerica Corporation for $1.54 billion, retaining the Primerica name.

The deal structure was unusual. The total purchase price was $1.54 billion. Weill insisted on keeping operating control, so although Primerica owned 54% of the new company, they held only four of 15 seats on the board of directors.

Although Commercial Credit is acquiring Primerica, it is anticipated that the merged entities would operate under the Primerica name. Weill, who would serve as chairman, is acquiring a company many times the size of Commercial Credit.

What did Weill see in the A.L. Williams sales force that came with the Primerica acquisition? Primerica's A.L. Williams sales force, which sells individual term life insurance, has 195,000 independent agents. These will be part of a company with massive channels of distribution once they are combined with Commercial Credit's 425 branch lending offices. "We love human sales forces," said Commercial Credit Executive Vice President F. Gregory Fitzgerald.

November 1989 marked another milestone: Art Williams sold his company to New York-based Primerica Corporation, a diversified financial services company—a decision that has been one of his biggest regrets. Williams had a family history of bad heart conditions and had a pacemaker in his own heart. He felt that in case anything happened to him and for the future stability of the company, it would be wise to sell it.

The sale made Art Williams extraordinarily wealthy—by 2007, he owned 21 million shares of Citigroup stock. But personally, the transition was difficult. He lost his passion for his business and questioned everything, even his faith. The Lord took him to the lowest of the low when he lost his company. Through that two-year trial after he sold his company, he learned he had his priorities wrong.

Sandy Weill, meanwhile, was just getting started. The acquisition machine continued to roll. Weill's next big move came in 1992 when he oversaw Primerica's purchase of a 27 percent share in Travelers Corporation. This was followed in 1993 by the realization of a dream for Weill. He regained control of Shearson, the massive brokerage firm he had struggled to build, when Primerica acquired the company's retail-brokerage and asset-management operations from American Express for $1.2 billion.

In December 1993, Primerica fully acquired Travelers Insurance Corporation and adopted the name Travelers Inc., which was changed to Travelers Group the following year. By this point, the corporate structure included Primerica Financial Services (the former A.L. Williams), Smith Barney, Travelers Insurance, and a constellation of other financial services businesses.

By 1998, Primerica (operating within Travelers Group) was performing remarkably well. Net income reached $398 million on net sales of $1.65 billion—a testament to the durability of the business model Art Williams had created.

V. Inside Citigroup: The Conglomerate Years (1998–2009)

Then came the mega-merger that redefined American finance.

In 1998, Travelers Group and Citicorp merged creating Citigroup (NYSE: C). Primerica and its affiliates continued to operate as subsidiaries of Citigroup, although the Travelers insurance business was spun off in 2002.

The Citicorp-Travelers merger created the largest financial services company in the world—a "financial supermarket" that could offer everything from checking accounts to life insurance to investment banking under one corporate umbrella. Sandy Weill had achieved the impossible: returning from exile to create a financial colossus.

For Primerica, the Citigroup years presented both opportunities and challenges. On one hand, the company had access to the resources of a global financial giant. On the other hand, it was a relatively small piece of an enormous conglomerate with very different priorities.

From 1998 to 2010, under Citigroup's ownership, Primerica sustained growth amid varying economic conditions, focusing on financial education seminars and mutual fund distribution through its PFS Investments arm.

The company expanded internationally, continued building its sales force, and maintained its distinctive culture despite operating within a behemoth institution. Remarkably, the "Buy Term and Invest the Difference" philosophy survived intact—even though it sometimes clashed with the financial engineering mentality that characterized other parts of Citigroup.

But maintaining an entrepreneurial, mission-driven culture within a massive banking conglomerate was never easy. Primerica's management had to navigate corporate politics while preserving the elements that made the distribution model work.

Then came 2008.

The global financial crisis devastated Citigroup. The bank that Sandy Weill had built required multiple government bailouts to survive. In the aftermath, Citigroup's new leadership—facing regulatory pressure and desperate to raise capital—began divesting non-core assets.

Citigroup attempted to sell Primerica in 2008, having received several bids from life insurance companies and private equity firms interested in buying. At the time the market value of the company was estimated to be $7 billion. JC Flowers & Co. LLC and Protective Life Corp began to purchase the company but the deal was canceled for undisclosed reasons.

The failed sale attempt left Primerica in limbo. Citigroup clearly wanted to divest the business, but market conditions had made a traditional sale impossible. A different path would be necessary.

VI. INFLECTION POINT #1: The "Refounding" IPO (2009–2011)

What emerged was one of the most successful "refoundings" in American corporate history.

Citigroup closed a chapter in its troubled history with the spin-off of Primerica, its door-to-door insurance unit, in a move that raised about $250 million and enabled the US bank to move more than $2 billion in assets off its balance sheet.

On November 5, 2009, Citi announced that it intended to spin off Primerica through an initial public offering. The first trading occurred on April 1, 2010, priced at $15 a share the day before trading. Citi raised $320 million through the IPO.

The IPO exceeded expectations. It was a strong start, opening with 21.36 million shares at $15.00—over three million shares more than anticipated and at least a dollar above the expected $12.00–$14.00 price per share.

In 2010, Warburg Pincus acquired a minority stake in Primerica to facilitate the company's IPO spin-out from Citigroup. Warburg Pincus' investment thesis was predicated on backing a strong, experienced management team with a unique and attractive franchise. Primerica also fit well within two notable Warburg Pincus investment themes: growing power of distributors versus manufacturers of financial products and finding cost-effective means to service underpenetrated lower-to-middle income consumers.

The management team that led Primerica through this transition had deep roots in the company. Co-Chief Executive Officers John Addison and Rick Williams (no relation to founder Art Williams) had both joined the company more than 20 years earlier and were appointed co-CEOs in late 1999. The 14 members of the senior management team had an average of 23 years of experience at Primerica.

This continuity was critical. Unlike many spin-offs that struggle with cultural disruption and management turnover, Primerica's leadership had spent decades in the trenches, building relationships with the independent sales force. They understood the culture and were trusted by the field.

The process began when Primerica was spun off in a 2010 IPO, after which Citigroup beneficially owned approximately 40% of Primerica common stock. In April 2011, Citigroup publicly sold 12 million shares of Primerica common stock, reducing its ownership stake to 23.1%. Primerica repurchased $200 million in shares in November 2011, reducing Citigroup's ownership to 12.5%.

On December 19, 2011, Citigroup sold its remaining equity stake in Primerica.

John Addison, Chairman of Primerica Distribution and Co-Chief Executive Officer, said, "This announcement marks the culmination of our 'Refounding'. It is an exciting and historic day for our company and we wish to thank our 2,000 employees in North America, as well as our more than 90,000 independent representatives, without whom this day would not be possible."

The term "Refounding" was deliberate and meaningful. For the first time since the 1989 sale to Sandy Weill's Primerica Corporation, the company's management and sales force were truly in control of their own destiny. No longer a subsidiary of a giant bank with conflicting priorities, Primerica could focus entirely on its mission of serving middle-income families.

In May 2013, Warburg Pincus fully exited its position in Primerica. The private equity firm's relatively quick exit—at a healthy profit—validated both the investment thesis and Primerica's ability to execute as an independent company.

The IPO proved to be one of the best performing of 2010. Primerica shares are among the best performing IPOs of the year and are ahead in excess of +50% from the offering price of $15 a share on March 31st.

VII. INFLECTION POINT #2: Digital Transformation & Technology Investment (2015–Present)

Independence unlocked something else: the freedom to invest aggressively in technology without navigating corporate bureaucracy.

Primerica has always recognized that its competitive advantage depends on empowering a massive field force of part-time and full-time representatives. Technology that makes those representatives more efficient—and more effective at serving clients—directly translates to competitive advantage.

The company offers independent sales representatives an electronic life insurance application that supports term life insurance products. Almost all of the life insurance applications received in 2024 were submitted electronically via TurboApps.

TurboApps represents the centerpiece of Primerica's digital strategy. Primerica's point-of-sale technology, TurboApps, streamlines the application process for insurance and investment products. These applications automatically populate client information from the Financial Needs Analysis and other external sources to eliminate redundant data collection and provide real-time feedback to eliminate incomplete and illegible applications. Integrated with the paperless field office management system and home office systems, TurboApps allows RVPs and the company to realize the efficiencies of straight-through-processing of application data.

The technology investment goes beyond simple application processing. Primerica uses its award-winning technology to simplify the business for representatives with a complete arsenal of cutting-edge tools. With a laptop, netbook, or tablet device like the iPad, and a high-speed internet connection, TurboApps web-based applications let representatives submit applications in real-time. This allows the company to process the business faster and representatives to get paid quickly!

Primerica Online ("POL"), delivered through a secure intranet website and a cross-platform mobile application ("Primerica App"), serves as the primary tool designed to support independent sales representatives and assist them in building their own businesses.

The company has allocated approximately $45 million annually to digital enhancements, ensuring that its platform remains competitive in a rapidly evolving financial landscape. For a company whose representatives often work part-time from their homes, having robust mobile-first tools is not a luxury—it's a competitive necessity.

In October 2022, Primerica introduced new term life insurance products, PowerTerm and PrecisionTerm, which offer rapid issue and traditional underwriting options, respectively. These products leverage the company's technology infrastructure to dramatically accelerate policy issuance.

The technology strategy reflects a broader understanding: in the 21st century, even a relationship-based "kitchen table" sales model must be digitally enabled. Representatives who can complete applications, access training materials, track their business metrics, and communicate with their teams through mobile devices are more productive than those relying on paper processes.

VIII. INFLECTION POINT #3: The e-TeleQuote Saga—An Acquisition Lesson (2021–2024)

Not every strategic initiative succeeds. The e-TeleQuote acquisition represents a cautionary tale in diversification gone wrong—and, to Primerica's credit, a case study in cutting losses quickly.

In July 2021, Primerica announced it had closed its previously announced acquisition of 80% of Etelequote Limited's operating subsidiaries. Pursuant to the terms of the acquisition agreement dated April 18, 2021, the transaction had an enterprise value of $600 million and an implied equity value of approximately $450 million.

The thesis made strategic sense on paper. e-TeleQuote is a senior health insurance distributor of Medicare-related insurance policies and offers products from a wide array of carriers (including United Healthcare, Humana, and Anthem) with over 2,700 Medicare Advantage plans available.

The synergies created by this acquisition will allow Primerica's life insurance-licensed independent sales representatives to serve clients' financial needs more fully throughout their lifecycle," said Glenn Williams, Primerica Chief Executive Officer. "e-TeleQuote's specialized technology platform and dynamic sales centers align perfectly with Primerica's powerful distribution capabilities."

As Primerica clients aged, they would eventually need Medicare guidance. Owning a Medicare distribution business could extend the customer relationship and create cross-selling opportunities. The aging of the U.S. population provided a demographic tailwind.

Then reality set in.

Primerica announced that after carefully considering various options, the Board of Directors opted to exit its senior health business by relinquishing ownership of e-TeleQuote Insurance, Inc. The senior health subsidiary, acquired in July 2021, does not have a clear path toward anticipated profitability within an acceptable timeframe in the increasingly challenging senior health distribution market. Further, the industry is facing an uncertain regulatory environment that could adversely impact the business.

"Various options for exiting the senior health market were carefully considered and, among other things, the significant structural changes the sector has undergone since e-TeleQuote's acquisition drove the decision," said Glenn Williams, CEO of Primerica. "We will continue to support client relationships with no plans to decrease staffing levels at e-TeleQuote during the transition."

Primerica determined that relinquishing its ownership of e-TeleQuote is the most expeditious way to exit its senior health business while maximizing Primerica's residual stockholder value. Primerica expects to terminate its rights to e-TeleQuote no later than September 30, 2024.

Medicare broker GoHealth announced that it entered into a purchase and subscription agreement which will ultimately lead to the acquisition of e-TeleQuote Insurance. Primerica had acquired e-TeleQuote in 2021 for $515 million. Primerica stated that e-TeleQuote does not have a clear path toward anticipated profitability within an acceptable timeframe in the "increasingly challenging senior health distribution market."

The e-TeleQuote episode illustrates several important lessons:

Know your core competency. Primerica's strength lies in its multi-level marketing distribution model for term life insurance and investment products. The senior health market operates differently—with different economics, different regulatory dynamics, and different customer acquisition strategies.

Regulatory risk in healthcare is real. Medicare distribution is subject to rapidly evolving CMS regulations that can fundamentally alter the economics of customer acquisition. What looked like an attractive market in 2021 became far less attractive as regulatory tightening increased compliance costs and reduced margins.

Admit mistakes quickly. Rather than throwing good money after bad, Primerica's management made the difficult decision to exit within three years of the acquisition. Taking a loss on e-TeleQuote was painful, but continuing to invest in a business without a clear path to profitability would have been worse.

The willingness to acknowledge failure and act decisively actually reinforced confidence in management. As an investor, you want leadership that recognizes when a thesis isn't working rather than stubbornly defending a sunk cost.

IX. The COVID-19 Stress Test & Emergence Stronger (2020–2021)

The pandemic represented the ultimate stress test for a life insurance company—and Primerica passed with flying colors.

During the COVID-19 pandemic, in 2020, Primerica paid out $1.7 billion in death claims. This was a 15.8% increase over 2019. The financial services company ended 2021 with $900 billion in active term life insurance.

That 15.8% increase in death claims during 2020 represented the grim reality of the pandemic. But it also demonstrated the fundamental value proposition of life insurance—when tragedy strikes, families need the protection they purchased. Primerica was there to pay claims.

Operationally, the pandemic forced rapid adaptation. A sales model built around in-person "kitchen table" meetings suddenly had to function virtually. Representatives who had never conducted video calls had to learn new skills overnight.

The company's investment in technology paid dividends. Tools like TurboApps and Primerica Online enabled representatives to continue working—conducting virtual meetings, submitting applications electronically, and communicating with their teams remotely.

Rather than retreating during the crisis, Primerica's sales force actually grew. The disruption to traditional employment—layoffs, remote work, flexible schedules—created an opportunity for the company's entrepreneurial pitch. People who suddenly had more time, less job security, or both became receptive to Primerica's message about building an independent business.

The pandemic also reinforced awareness of mortality and the importance of life insurance. Sales of term life insurance industrywide increased during 2020 and 2021, and Primerica captured its share of that demand.

By year-end 2021, the company had nearly $900 billion of active term life insurance in force—a testament to decades of steady accumulation and strong persistency.

X. Modern Primerica: 2024–2025 Performance & Scale

Today's Primerica is firing on all cylinders.

Primerica, Inc. reported strong financial performance for the year 2024, with total revenues of $3,089 million, a 12% increase from 2023, driven by higher commissions and fees, net premiums, and net investment income. Income from continuing operations reached $720 million, a 22% increase from 2023.

Full-year revenue exceeded $3 billion for the first time in company history.

For Q1 2025, total revenues were $804.8 million, an increase of 9% from the first quarter of 2024. Net income of $169.1 million increased 14%.

For Q3 2025, total revenues were $839.9 million, an increase of 8% from the third quarter of 2024. Net income of $206.8 million increased 6%.

The sales force continues to expand. Primerica provides financial products and services to middle-income households in the United States and Canada with 151,611 life insurance-licensed sales representatives as of December 31, 2024.

Primerica grew its licensed sales force by 7% in 2024, surpassing 151,600 life-licensed reps. Life-licensed representatives exceeded 150,000, marking a milestone.

Primerica insured over 5.5 million lives and had approximately 3.0 million client investment accounts as of December 31, 2024.

Investment and Savings Products have become an increasingly important segment. Record Investment and Savings Products sales of $3.7 billion were achieved in Q3 2025, up 28%, with record ISP client asset values ending the quarter at $126.8 billion.

"With more than $967 billion of Term Life face amount in force as of September 30, 2025, together with our fee-based investment business, we have a solid foundation for capital generation," said Glenn Williams, Chief Executive Officer.

Capital allocation remains shareholder-friendly. During the fourth quarter of 2024, the Company repurchased $44.4 million of its common stock, completing the Board of Directors' authorization to repurchase $425 million of common stock during 2024, and authorized a new $450 million share repurchase program through December 31, 2025. The Board of Directors approved a 16% dividend increase to $1.04 per share.

As of December 31, 2024, Primerica reported insuring over 5.5 million lives and managing approximately 3.0 million client investment accounts.

The company's capital position is exceptionally robust. Primerica Life Insurance Company's statutory risk-based capital (RBC) ratio was estimated to be about 515% as of September 30, 2025. This is well above regulatory minimums and provides substantial cushion for adverse scenarios.

The 2024 Primerica International Convention, Atlanta's largest corporate meeting with attendees from across the U.S. and Canada, was estimated to draw as many as 40,000 members of its sales force with a projected economic impact of $46 million on the local economy.

Primerica's biennial convention was held at the Mercedes-Benz Stadium in Atlanta, GA in July 2024. With nearly 40,000 attendees, this event was the ideal platform from which to cast a vision for the future.

The Primerica International Convention will return to Atlanta in 2027, when the Company celebrates its 50th anniversary.

XI. Playbook: Business & Investing Lessons

What can investors and business builders learn from the Primerica story?

The Power of a Contrarian Philosophy

"Buy Term and Invest the Difference" wasn't just a tagline—it was a genuine insight that the traditional insurance industry had ignored for a century. By articulating a simple, compelling alternative to the status quo, Art Williams created a movement rather than just a company.

The most powerful businesses often emerge from challenging established orthodoxies. When an entire industry is structured around a particular approach, there's usually an opportunity for someone willing to question fundamental assumptions.

Multi-Level Marketing Done Right

Primerica represents MLM at its most successful and least pyramid-like. The company sells legitimate, regulated financial products to actual customers. Representatives earn income primarily from product sales, not from recruitment fees. The field force has produced genuine wealth for thousands of individuals.

The business structure is one like a real estate brokerage. They recruit people and pay for them to get their state license to transact business as a life insurance agent. And just like a real estate broker who has agents within his business, anytime a licensed agent transacts business within your organization, you receive an override.

That said, the MLM model has inherent tensions. Critics rightly point out that many representatives earn little or nothing, that the emphasis on recruitment can distort incentives, and that the culture can become cult-like. Primerica navigates these tensions better than most MLM companies, but they never fully disappear.

Serving the Underserved

Primerica's key differentiator was a unique distribution model consisting of part-time agents organized in a multi-level marketing structure, which efficiently reached the underserved lower-to-middle income consumer.

Middle-income families—the "Main Street" households that Primerica targets—are often underserved by traditional financial services. They're not wealthy enough to attract attention from private bankers but have genuine needs for life insurance and retirement savings. Primerica's model creates an efficient way to reach these customers through representatives who are themselves part of the middle-income community.

Surviving Corporate Ownership

Primerica maintained its culture through 12 years of Citigroup ownership—no small feat. The keys were management continuity, field force loyalty, and a mission-driven identity that transcended corporate ownership structures.

The Value of Independence

The 2010 "Refounding" unlocked shareholder value by removing the constraints of conglomerate ownership. An independent Primerica could allocate capital according to its own priorities, invest in technology without navigating corporate bureaucracy, and focus entirely on serving its core customer base.

Capital Allocation Discipline

Since independence, Primerica has returned substantial capital to shareholders through consistent buybacks and dividend growth. The company generates strong free cash flow and has limited needs for retained capital, making it an effective capital return machine.

Knowing When to Exit

The e-TeleQuote write-off was painful but demonstrated management's willingness to acknowledge mistakes quickly. Cutting losses on a failed acquisition is far better than stubbornly defending a sunk cost.

Technology as Enabler

Even a relationship-based sales model must embrace technology. Primerica's investment in TurboApps, mobile applications, and digital tools has made representatives more productive and the business more scalable.

XII. Porter's Five Forces Analysis

| Force | Assessment |

|---|---|

| Threat of New Entrants | MODERATE - Low capital requirements for individual agents, but building a 150,000+ licensed sales force takes decades. Regulatory licensing creates barriers. The culture and training infrastructure are difficult to replicate. |

| Supplier Power | LOW - Primerica underwrites its own term life insurance, reducing dependence on external carriers. For distributed products (mutual funds, annuities), many providers compete for access to Primerica's distribution network. |

| Buyer Power | LOW-MODERATE - Middle-income families have limited alternatives for in-home financial education. The relationship-based sales model creates switching costs. However, informed consumers can comparison shop for term life insurance online. |

| Threat of Substitutes | MODERATE-HIGH - Online insurance comparison sites, robo-advisors, and direct-to-consumer insurance represent alternatives. However, the human touch and education model differentiates Primerica for customers who value personal relationships. |

| Competitive Rivalry | MODERATE - Primerica Life Insurance ranked #1 in new annualized premium in Q1 2024, ahead of State Farm. Major competitors include traditional insurers and other distributors, but few focus exclusively on middle-income families with Primerica's model. |

XIII. Hamilton's 7 Powers Framework Analysis

| Power | Assessment |

|---|---|

| Scale Economies | MODERATE - A large in-force book provides operating leverage. Fixed costs (technology, compliance, home office) are spread across a massive distribution network. |

| Network Effects | STRONG - The MLM structure creates natural network effects. Each successful agent recruits others; convention culture reinforces growth. The 2024 Primerica International Convention drew as many as 40,000 members of its sales force. |

| Counter-Positioning | VERY STRONG - This is Primerica's core power. Traditional insurers cannot adopt the "buy term" message without cannibalizing profitable whole-life products. The MLM model is antithetical to career agent forces at legacy insurers. Incumbents would destroy existing revenue streams by following Primerica's playbook. |

| Switching Costs | MODERATE - Term life policies are technically portable, but client relationships and trust built through personal meetings create stickiness. Licensed representatives have invested in training and hierarchy position. |

| Branding | MODERATE - Primerica was listed by Forbes as one of "America's 50 Most Trustworthy Financial Companies" in 2015. Strong brand recognition within target demographic, but MLM stigma affects perception among some observers. |

| Cornered Resource | MODERATE - Experienced sales representatives have significant longevity. Of sales representatives, approximately 21,000 have been with the company for at least ten years, and approximately 7,000 have been with the company for at least 20 years. This tenure is difficult to replicate. |

| Process Power | STRONG - Nearly 50 years of refining the "kitchen table" sales process, compensation structures, training programs, and digital tools creates institutional knowledge that competitors cannot easily duplicate. |

Dominant Powers: Counter-Positioning and Network Effects are Primerica's strongest moats. The Counter-Positioning power is particularly important—traditional insurers cannot follow Primerica's playbook without destroying their existing businesses.

XIV. Bear vs. Bull Case

Bull Case

Industry Tailwinds: The financial services industry continues to expand, and direct sales models enable efficient customer acquisition. Primerica's focus on underserved middle-income families positions it well for demographic growth.

Flywheel Effect: Success breeds success in the MLM model. As the sales force grows, more representatives are recruited and trained, expanding the distribution network. The convention culture and recognition programs create positive reinforcement.

Technology Investment: Continued digital enhancement improves representative productivity and customer experience. Almost all of the life insurance applications received in 2024 were submitted electronically via TurboApps.

Capital Return: The company's robust free cash flow generation and disciplined capital allocation provide consistent shareholder returns. The company's Board of Directors authorized a $450 million share repurchase program through December 31, 2025.

Management Quality: Long-tenured leadership with deep company experience navigates challenges effectively, as demonstrated by the quick e-TeleQuote exit.

Counter-Positioning Moat: Traditional insurers cannot easily replicate Primerica's model without cannibalizing their existing businesses.

Bear Case

MLM Stigma: The multi-level marketing structure creates persistent reputational risk. Regulatory scrutiny of MLM models could increase. Critics argue that Primerica's reps are incentivized to bring in new agents more than they are to sell financial products.

Representative Turnover: High attrition among new representatives creates continuous recruiting requirements. Many recruits earn little or nothing before leaving.

Online Competition: Direct-to-consumer insurance platforms and comparison sites enable informed consumers to bypass Primerica's higher-touch (and higher-cost) model.

Interest Rate Sensitivity: Investment returns on the company's portfolio are affected by interest rate movements, though this is partially offset by higher investment income in rising rate environments.

Customer Pricing: Primerica's core pitch is "Buy Term and Invest the Difference," a sound idea in theory. But that only works if the term policy is competitively priced, and some critics argue Primerica isn't always the cheapest option.

Concentration Risk: Heavy dependence on the U.S. and Canadian middle-income market limits geographic diversification.

XV. Key Metrics to Watch

For investors tracking Primerica's ongoing performance, three metrics matter most:

1. Life-Licensed Sales Force Growth

The sales force is the engine of the business. Growth in the number of licensed representatives—particularly those who remain active and productive—directly drives premium growth and recruiting momentum. Look for year-over-year comparisons of licensed representatives and recruit-to-license conversion rates.

2. Investment and Savings Products (ISP) Client Asset Values

As Primerica has diversified beyond pure term life insurance, the ISP segment has become increasingly important. Client asset values (which generate recurring fee income) represent a growing portion of the business. By year-end 2024, client asset values stood at $112.1 billion, reflecting a 16% growth from December 31, 2023.

3. Term Life Insurance In-Force

The accumulated book of in-force policies represents a durable asset. Persistency rates (the percentage of policies that remain in force rather than lapsing) and the growth of total face value in force indicate the health of the core business.

XVI. Myth vs. Reality

| Myth | Reality |

|---|---|

| Primerica is a pyramid scheme | Legally and structurally, Primerica is not a pyramid scheme. Representatives earn income from selling legitimate, regulated financial products—not from recruitment fees. However, the MLM structure does create pyramid-like dynamics where those at the top of successful hierarchies earn disproportionately. |

| Term life insurance is always cheaper | Term life is cheaper than whole life for equivalent death benefit, but Primerica's term policies aren't always the cheapest available. Comparison shopping can find lower rates from other carriers. The value proposition is partly about convenience and the educational relationship, not just price. |

| Anyone can succeed at Primerica | While the opportunity is technically open to anyone, success requires substantial effort, sales ability, and often an existing social network. Many representatives earn little or nothing. In 2010, Primerica was reported to have over 100,000 representatives selling the company's financial products, with individual earnings averaging $5,156 per year. |

| Primerica's products are inferior | AM Best has affirmed the Financial Strength Rating of A+ (Superior) for Primerica Life Insurance Company. The products are legitimate and backed by a financially sound company, but critics argue they may not always represent the best value compared to alternatives. |

XVII. Regulatory and Legal Considerations

Several regulatory and legal factors warrant investor attention:

Independent Contractor Status: Primerica representatives are classified as independent contractors, not employees. Changes to labor regulations regarding gig workers or contractor classification could impact the business model, though the financial services industry has historically maintained contractor relationships.

State Insurance Regulation: Life insurance is regulated at the state level, with varying requirements across jurisdictions. Maintaining licenses and compliance in all 50 states plus Canadian provinces requires substantial infrastructure.

Securities Regulation: The Investment and Savings Products segment involves distribution of mutual funds and other securities, subject to SEC and FINRA oversight. In 1998, the SEC censured and fined PFS Investments Inc. for failure to properly supervise registered representatives in Dearborn, Michigan. While this was resolved, securities distribution requires ongoing compliance vigilance.

MLM Scrutiny: Multi-level marketing companies face periodic regulatory scrutiny from the FTC and state attorneys general. Primerica's focus on selling actual products (rather than primarily recruiting) provides protection, but the regulatory environment could shift.

XVIII. Conclusion: A Crusade That Became a Business

Nearly fifty years after Art Williams walked away from his coaching career to challenge the life insurance establishment, the company he founded continues to thrive. Primerica has survived multiple corporate owners, emerged stronger from the 2008 financial crisis, achieved independence through a successful IPO, and grown into a multi-billion-dollar enterprise serving millions of families.

The foundation remains the same: a contrarian philosophy about term life insurance, a motivated sales force organized in a multi-level marketing structure, and a mission-driven culture that creates genuine believers.

Primerica's business model uniquely positions it to reach underserved middle-income consumers in a cost-effective manner and has proven itself in both favorable and challenging economic environments. Its purpose is to create financially independent families.

The company is not without critics, and the MLM model will always generate skepticism. But the financial results speak for themselves: consistent revenue growth, strong profitability, disciplined capital allocation, and a sales force that continues to expand.

As 2026 approaches, Primerica is laying the foundation for strong momentum by launching a series of major regional field events in the spring. The company's goal is to build excitement and field engagement as it moves toward its 50th anniversary convention in 2027.

Fifty years since a Georgia football coach decided that ordinary families deserved a better deal on life insurance. Fifty years since a "ragtag army of part-timers" set out to challenge an entrenched industry. Fifty years of buying term and investing the difference.

Art Williams was right about one thing: All you can do is all you can do. But all you can do is enough.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube