Insulet Corporation: The Tubeless Revolution in Diabetes Management

I. Introduction & Episode Roadmap

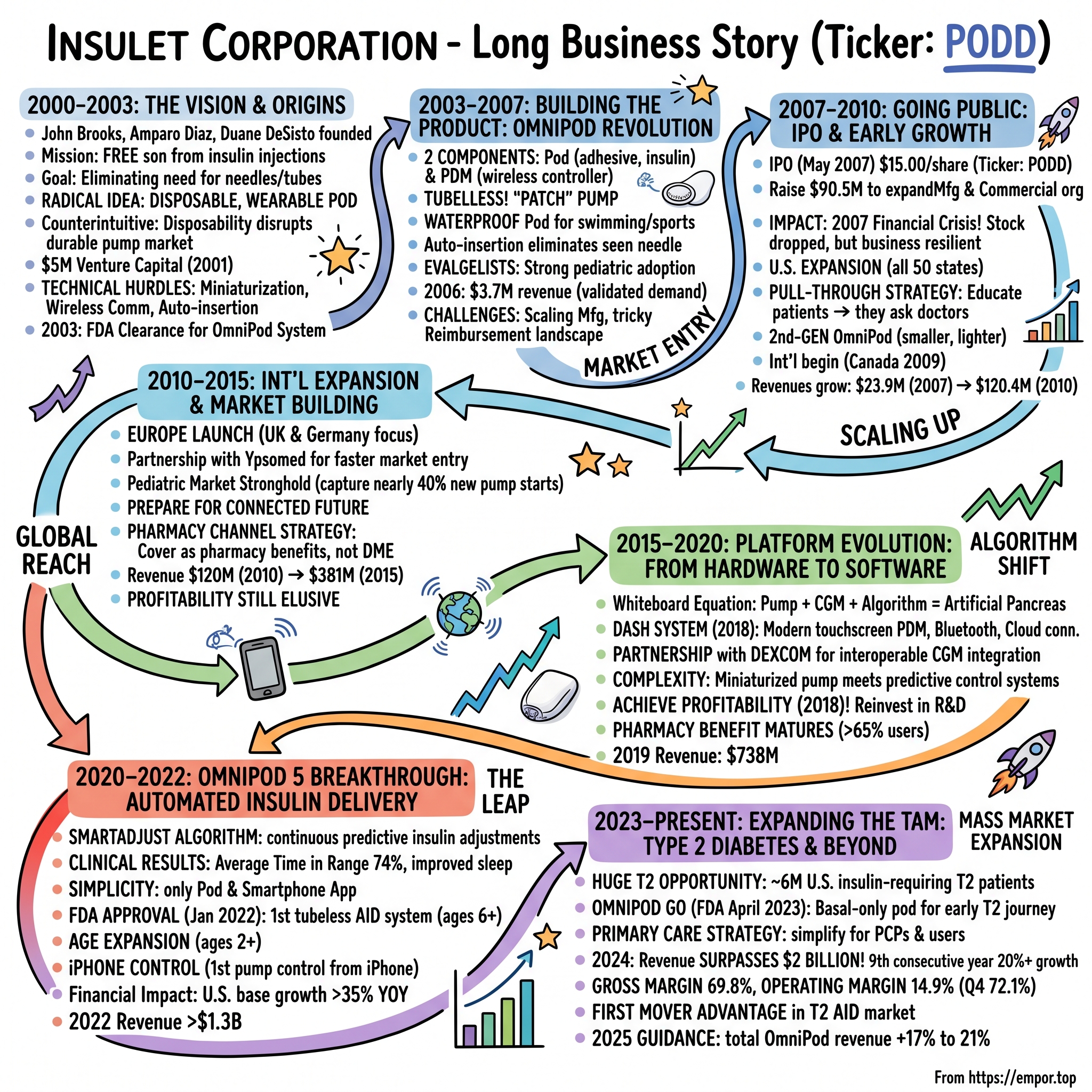

Picture this: A father watches his young son grimace as he prepares for yet another insulin injection—the fourth that day. The year is 2000, and for millions of families touched by Type 1 diabetes, this scene plays out multiple times daily, a relentless routine of needles, calculations, and worry. John Brooks wasn't just any father watching this struggle; he was an entrepreneur with a radical idea. What if insulin delivery could be as simple as wearing a Band-Aid?

Fast forward to 2024, and that father's vision has transformed into Insulet Corporation, a company that just crossed $2 billion in annual revenue for the first time. The journey from a parent's determination to a NASDAQ-listed powerhouse reveals one of medtech's most compelling David-versus-Goliath stories. While giants like Medtronic dominated with complex, tubed insulin pumps that resembled pagers tethered to patients, Insulet dared to imagine something fundamentally different: a tubeless, wearable pod that would revolutionize how millions manage diabetes. The core question driving today's exploration is deceptively simple yet profound: How did a company founded by a father's determination to free his son from daily insulin injections become the leader in tubeless insulin pump technology? The answer reveals crucial lessons about patient-centric innovation, the power of focusing on unmet needs, and the delicate art of disrupting entrenched medical device markets.

Today's journey will trace three interwoven themes. First, we'll explore innovation in medical devices—not the incremental improvements that dominate the space, but the radical reimagining of what insulin delivery could be. Second, we'll examine the power of patient-centric design, where every engineering decision was filtered through the lens of "would a child want to wear this?" And third, we'll navigate the complex diabetes market, where clinical excellence alone doesn't guarantee success; you need to master reimbursement codes, distribution channels, and the conservative nature of endocrinologists who've been prescribing the same devices for decades.

What makes Insulet's story particularly compelling for investors and founders alike is how it challenged every assumption about what a successful medical device company should look like. While competitors focused on adding features to existing pump designs—more buttons, more settings, more complexity—Insulet took the opposite approach. They removed the tubes. They eliminated the belt clips. They made the device disposable. In an industry obsessed with durability and longevity, they built something meant to be thrown away every three days. The result? A company that surpassed $2 billion in annual revenue for the first time in 2024, marking its ninth consecutive year of 20% or more constant currency revenue growth.

This episode will unfold in distinct acts, each revealing how strategic decisions compound over decades. We'll begin with the origin story—a father's mission that sparked a revolution. We'll then dive into the engineering challenges of creating the OmniPod, navigate the treacherous waters of going public during the 2007 financial crisis, and examine the international expansion that established Insulet as a global force. The narrative accelerates as we explore the platform evolution from hardware to software, the breakthrough of automated insulin delivery with Omnipod 5, and the massive market expansion into Type 2 diabetes. Finally, we'll dissect the business model that turned a simple pod into a recurring revenue machine and extract the playbook lessons that make this story essential reading for anyone building in regulated markets.

Buckle up. This is the story of how a tubeless patch forever changed the lives of millions living with diabetes, and how a father's love built a multi-billion dollar business that even Medtronic couldn't ignore.

II. The Origin Story: A Father's Mission (2000–2003)

The conference room at Duane DeSisto's house in 2000 didn't look like the birthplace of a medical revolution. Three people sat around a table, united by frustration with the status quo of diabetes management. John Brooks, whose young son lived with Type 1 diabetes, had watched him struggle with the daily burden of multiple insulin injections. Amparo Diaz brought deep medical device expertise. And DeSisto, a successful entrepreneur, understood how to build companies from impossible ideas. Together, they weren't trying to build a better insulin pump—they were trying to eliminate everything people hated about them.

To understand the audacity of their vision, you need to understand the diabetes landscape in 2000. For the 1.25 million Americans with Type 1 diabetes, life revolved around a relentless routine. Multiple daily injections—typically four or more—punctuated every meal, every snack, every correction for blood sugar swings. The lucky few who could afford insulin pumps (and convince their insurance to cover them) wore devices that looked like pagers from the 1980s, complete with long tubes snaking under clothing to injection sites. These pumps cost upward of $6,000, plus hundreds more monthly for supplies. Medtronic's MiniMed dominated with over 60% market share, while companies like Animas and Disetronic fought for the remainder.

Brooks' vision was radical in its simplicity: What if there were no tubes? No belt clips? No visible medical device announcing to the world that you had diabetes? His son's experience had taught him that the psychological burden of diabetes often matched the physical one. Traditional pumps required users to thread tubing through clothing, find places to clip bulky devices during sleep, and navigate the awkwardness of intimacy while tethered to a machine. Swimming meant disconnecting entirely. Sports became a challenge of securing tubes and devices. For children and teenagers—already navigating the social complexities of growing up—traditional pumps added another layer of difference, another reason to feel isolated. The founding team brought complementary skills that would prove essential. The founders were John Brooks, Amparo Diaz, and Duane DeSisto. Brooks' personal connection to diabetes came from his three-year-old son was diagnosed with type 1 diabetes, driving his determination to revolutionize insulin delivery. In a revealing interview years later, Brooks described the exact moment of inspiration: "That was born out of a flight that he and I took in 2000 back from the West Coast. I was describing all the challenges of insulin initiation and administration for our son, and we came up with this idea of a disposable insulin delivery system" based on technology they'd seen in disposable hearing aids.

The early vision crystallized around a counterintuitive insight: disposability could be disruptive. While the entire insulin pump industry focused on building durable, long-lasting devices that justified their high price tags, the Insulet founders saw opportunity in the opposite direction. A disposable, adhesive pod worn directly on the skin would eliminate tubes, simplify manufacturing, and reduce the psychological burden of wearing a medical device. The wireless handheld controller would give users discrete control without advertising their condition to the world.

In 2001, the company secured $5 million in venture capital, giving them the runway to transform their radical idea into a functioning prototype. But money was just the beginning of their challenges. The technical hurdles were immense: How do you miniaturize an insulin pump to fit in a small pod? How do you ensure reliable wireless communication between pod and controller? How do you automate cannula insertion so users never have to see or handle a needle? Each question spawned dozens more, and the team spent two years in intensive development. By mid-2003, after three years of intensive development and testing, Insulet achieved its first major milestone: the company received its first clearance from the Federal Drug Administration (FDA). This 510(k) clearance for the OmniPod System represented more than regulatory approval—it validated that a tubeless insulin pump was not only possible but safe and effective. The engineering team had solved seemingly impossible challenges: creating a waterproof pod that could deliver precise insulin doses, developing automated cannula insertion that eliminated the fear factor of needles, and ensuring wireless communication reliability between pod and controller.

The technical challenges they overcame were staggering. Traditional insulin pumps used long tubes because separating the pump mechanism from the infusion site seemed impossible—the precision required for insulin delivery demanded mechanical linkages. Insulet's team had to miniaturize everything: the pump motor, the insulin reservoir, the electronics, and the power supply, all while making it light enough to wear comfortably and cheap enough to throw away. They developed a proprietary automated insertion mechanism that deployed a soft cannula with the push of a button, eliminating one of the most anxiety-inducing aspects of pump therapy. The wireless communication protocol had to be bulletproof—a missed insulin dose due to signal interference could be life-threatening.

What made their approach revolutionary wasn't just the technology, but the philosophy behind it. While competitors added features—more alarms, more settings, more complexity—Insulet removed friction at every turn. The pod would arrive pre-filled or easy to fill. No maintenance. No cleaning. When it was done after three days, you simply removed it and applied a new one. This disposable model flew in the face of medical device orthodoxy, where durability and longevity justified premium pricing. But Brooks and his team understood something fundamental: for patients, especially children, simplicity trumped sophistication.

The funding trajectory tells its own story of skepticism transforming into belief. After the initial $5 million in 2001, investors began to see the potential. The FDA clearance in 2003 opened the floodgates for additional capital as the company prepared for commercial launch. But money alone wouldn't guarantee success. Insulet needed to build manufacturing capabilities, establish distribution channels, and most critically, convince a conservative medical establishment that their radical new approach was better than the status quo.

As 2003 drew to a close, Insulet stood at the precipice of commercialization. They had proven the technology worked, secured regulatory approval, and built a team capable of bringing their vision to market. The next phase would test whether patients and physicians were ready for a tubeless revolution—and whether a father's determination to improve his son's life could transform an entire industry.

III. Building the Product: The OmniPod Revolution (2003–2007)

The conference room at Insulet's Bedford, Massachusetts headquarters buzzed with nervous energy in early 2005. After years of development and refinement following their initial FDA clearance, the team was about to ship the first commercial OmniPod to a real patient. This wasn't a clinical trial participant or a test subject—this was someone's child, someone's parent, someone whose life would either be transformed or disappointed by what they'd built. In 2005, Insulet Corp. released the Omnipod Insulin Pump system commercially, marking the birth of the world's first tubeless insulin pump.

The OmniPod System that launched in 2005 was elegantly simple in concept yet remarkably sophisticated in execution. Two components comprised the entire system: a small, lightweight pod that adhered directly to the skin, and a Personal Diabetes Manager (PDM) that looked like an early smartphone. The pod containing insulin is attached to the body for insulin delivery. It is a compact and lightweight device that comes with an adhesive base. It features a soft cannula that is inserted into the subcutaneous tissue upon application. No tubes. No belts. No constant reminder tethered to your body that you have a chronic disease.

The revolutionary design addressed every pain point of traditional pump therapy. PDM and the Pod are connected wirelessly allowing for bi-directional communication. This technology eliminated the need for a tube for insulin delivery. Therefore, the Omnipod was referred to as a "Patch" or a "Tubeless" Insulin Pump. Users could wear the waterproof pod while swimming, showering, or playing sports—activities that required traditional pump users to disconnect entirely, disrupting their insulin delivery and blood sugar control.

The automated cannula insertion was perhaps the most psychologically important innovation. Traditional pump users had to manually insert their infusion sets using spring-loaded insertion devices that many found intimidating. With OmniPod, users simply pressed a button on the PDM, and the pod automatically inserted a soft cannula—they never saw the needle, never had to steel themselves for the insertion. Parents reported their children actually looked forward to "pod change day" rather than dreading it.

Early adopters became evangelists. One mother from Texas wrote to the company describing how her 7-year-old daughter, previously resistant to pump therapy because of the tubing, had embraced the OmniPod completely. She could wear dresses without figuring out where to clip a pump. She could play on the monkey bars without tubes getting caught. She could have sleepovers without explaining complicated medical equipment to her friends' parents. These weren't just quality-of-life improvements—they were fundamental changes to how young people with diabetes saw themselves.

The company's first full year of sales in 2006 generated $3.7 million in revenue—modest by pharmaceutical standards but remarkable for a company challenging entrenched competitors with 20-year head starts. Each sale represented not just revenue but validation. Endocrinologists who had been skeptical began requesting samples. Diabetes educators who had dismissed tubeless pumps as a gimmick started recommending them to patients who had rejected traditional pumps.

Manufacturing presented unique challenges. Unlike traditional durable medical equipment that might last 4-7 years, each OmniPod lasted just 72 hours. This meant Insulet needed to produce millions of units annually, each one as reliable as a device costing ten times more. They developed automated assembly lines that could produce pods at scale while maintaining medical device quality standards. The adhesive alone required months of testing—it needed to stick reliably for three days through showers, sweat, and daily life, yet remove painlessly without skin damage.

The reimbursement landscape proved treacherous. Insurance companies had established codes and coverage policies for traditional insulin pumps, but OmniPod didn't fit neatly into existing categories. Was it a pump? A supply? Durable medical equipment or disposable? Insulet's reimbursement team worked tirelessly with insurers, making the case that the pod system's benefits—improved adherence, better glycemic control, higher patient satisfaction—justified coverage. They pioneered a new model where the upfront PDM cost was minimal, with ongoing pod supplies covered like diabetes testing supplies rather than durable equipment.

Clinical validation came through real-world evidence. While established pump makers could point to decades of studies, Insulet had to prove their novel approach was not just different but better. Early studies showed comparable glycemic control to traditional pumps, but with significantly higher satisfaction scores and lower discontinuation rates. Pediatric endocrinologists particularly embraced the system, noting that children who had refused traditional pumps readily adopted OmniPod.

Competition watched with a mixture of skepticism and concern. Medtronic, commanding over 60% of the insulin pump market, initially dismissed the tubeless concept as a niche product for pump-resistant patients. Animas and other traditional pump makers focused on adding features to their existing platforms rather than reimagining the form factor. This dismissal gave Insulet crucial time to establish their foothold and refine their technology.

By the end of 2006, patterns were emerging that would define Insulet's growth trajectory. Users weren't switching from other pumps—they were new to pump therapy entirely. The OmniPod was expanding the market, reaching patients who had rejected traditional pumps due to the tubing, visibility, or lifestyle limitations. Pediatric adoption was particularly strong, with parents appreciating the simplicity and children embracing the freedom from tubes.

The challenges were equally clear. Manufacturing yields needed improvement to achieve profitability. Reimbursement remained a battle with each insurer. Market education was expensive and slow—many endocrinologists remained loyal to established pump brands. International expansion would require navigating different regulatory environments and reimbursement systems. And always lurking was the question: would Medtronic or another giant simply copy the tubeless concept and crush the startup?

As 2007 approached, Insulet faced a critical decision. They had proven product-market fit and shown sustainable demand. But scaling would require capital—lots of it. The venture funding that had sustained them through development wouldn't suffice for the manufacturing expansion, sales force build-out, and international expansion needed to compete with billion-dollar competitors. The path forward led to only one destination: the public markets.

The OmniPod revolution was real, but revolutions require resources. The next chapter would test whether public market investors shared the vision of a tubeless future that had driven Insulet from a father's sketch to a commercial reality.

IV. Going Public: The IPO and Early Growth (2007–2010)

The roadshow presentations in the spring of 2007 had an unusual prop: a traditional insulin pump with its long tubing next to the sleek, tubeless OmniPod. Investment bankers from JP Morgan, Lehman Brothers, and Thomas Weisel Partners watched as Insulet's management team demonstrated the stark difference. "This," CEO Duane DeSisto would say, holding up the tubed pump, "is what patients have endured for twenty years." Then, applying an OmniPod to his arm with one smooth motion: "This is the future we're building."

The timing seemed perfect. The company had momentum from successful commercial launch, growing revenues, and expanding insurance coverage. The IPO prospectus told a compelling story: a revolutionary product addressing a massive market, with only 11% of Type 1 diabetes patients using insulin pumps due to the limitations of existing devices. The initial plan targeted raising $90.5 million through the sale of 6.7 million shares priced between $14 and $16.

On May 15, 2007, Insulet Corporation began trading on the NASDAQ Global Market under the symbol PODD, with shares priced at $15.00—right in the middle of the expected range. The first day of trading saw shares climb to $16.40, a modest but encouraging start. The capital raised would fund three critical initiatives: expanding manufacturing capacity at their Bedford facility, building out the commercial organization to reach more endocrinologists and diabetes educators, and continuing research and development on the next generation of OmniPod technology.

What nobody could foresee was the financial hurricane brewing on the horizon. By late 2007, the subprime mortgage crisis was metastasizing into a full-blown financial meltdown. Lehman Brothers, one of Insulet's IPO underwriters, would collapse within a year. Credit markets froze. Healthcare companies saw their valuations crater as investors fled to safety. Insulet's stock price, which had reached $19 in late 2007, plummeted below $5 by March 2009.

Yet paradoxically, the financial crisis created unexpected opportunities. While Insulet's stock price suffered, the underlying business showed remarkable resilience. Patients didn't stop needing insulin pumps because of a recession. Insurance coverage, once approved, rarely reversed. And as larger competitors like Medtronic focused on protecting their core businesses and maintaining margins, Insulet doubled down on growth, using their public company status to access capital markets even in turbulent times.

By the end of 2008, the OmniPod System was available and supported in all 50 U.S. states—a remarkable achievement for a company just three years into commercialization. The state-by-state expansion required navigating a byzantine maze of insurance regulations, Medicaid policies, and regional distributor relationships. California and Texas, with their large populations and favorable reimbursement environments, became strongholds. But even small states mattered—every endocrinologist won over, every diabetes educator trained, every insurance plan approved expanded the addressable market.

The competitive landscape during this period revealed the innovator's dilemma in action. Medtronic, with its MiniMed division generating over $1 billion annually, focused on incremental improvements to its existing pumps—smaller size, better displays, integration with continuous glucose monitors. But they didn't embrace the tubeless concept, viewing it as cannibalizing their profitable pump and supplies business. Animas, acquired by Johnson & Johnson in 2006, similarly focused on enhancing their traditional pump platform. This left Insulet to define and dominate the tubeless category.

Sales execution became the company's religion. The diabetes sales model differed fundamentally from pharmaceuticals or even other medical devices. Endocrinologists didn't prescribe insulin pumps casually—pump therapy required extensive patient education, insurance verification, and ongoing support. Insulet built a high-touch sales model where representatives didn't just call on physicians but embedded themselves in diabetes clinics, training nurses, working with billing departments, and even meeting directly with interested patients.

The "pull-through" strategy proved particularly effective. Rather than just convincing doctors to prescribe OmniPod, Insulet educated patients directly through diabetes conferences, online communities, and peer support programs. Patients would then ask their endocrinologists about OmniPod specifically. This consumer-pull approach, unusual in medical devices, leveraged the unique appeal of tubeless technology to those living with diabetes daily.

Product iteration during this period focused on reliability and user experience rather than radical changes. The second-generation OmniPod, introduced in 2009, was 34% smaller and 25% lighter than the original, with improved adhesive and more intuitive PDM software. These might seem like minor improvements, but for a device worn 24/7, every gram mattered, every millimeter counted. Users celebrated the smaller pod with the enthusiasm typically reserved for new iPhone releases.

International expansion began cautiously but strategically. Canada, with its single-payer system and cultural similarity to the U.S., became the first international market in 2009. The lessons learned about government reimbursement, bilingual requirements, and cross-border logistics would prove invaluable for future expansion. Europe loomed as the next frontier, but the regulatory requirements of CE marking and country-by-country reimbursement negotiations demanded patience and capital.

Financial performance during these early public years painted a picture of a company in aggressive growth mode. Revenues grew from $23.9 million in 2007 to $120.4 million by 2010—a five-fold increase. But losses mounted as well, with the company burning cash to fund expansion. Critics questioned whether Insulet could ever achieve profitability given the high cost of producing disposable pods versus the recurring revenue from supplies. The bear case was simple: they were selling dollar bills for ninety cents.

Management's response was to focus on the long game. Every new patient represented not just an initial sale but potentially decades of recurring pod purchases. The lifetime value of a patient could exceed $100,000. The key was achieving scale—spreading fixed costs across a growing base of users while improving manufacturing efficiency. They pointed to their growing gross margins, from negative in 2007 to 30% by 2010, as evidence the model could work.

The organizational culture that emerged during these formative public years would define Insulet for decades. Unlike traditional medical device companies staffed with engineers and regulatory experts, Insulet hired people passionate about diabetes. Many employees were patients themselves or had family members with diabetes. The company's Bedford headquarters featured a "Wall of Fame" with photos and letters from OmniPod users. This wasn't just corporate decoration—it was daily reminder of the mission.

By 2010, Insulet had survived the crucible of going public during a financial crisis, expanded nationwide, and proven sustainable demand for tubeless pump technology. Revenue run rate exceeded $100 million annually. Over 20,000 patients relied on OmniPod for their daily insulin delivery. The infrastructure was in place for international expansion. Most importantly, they had maintained their innovation edge while larger competitors remained wedded to traditional designs.

The question was no longer whether tubeless pumps were viable—that had been definitively answered. The question now was whether Insulet could expand beyond their beachhead of pump-resistant patients to challenge Medtronic's dominance directly. The answer would require thinking beyond hardware to software, beyond domestic to international, and beyond Type 1 to the much larger Type 2 diabetes market. The foundation was built; now it was time to scale the revolution globally.

V. International Expansion & Market Building (2010–2015)

The customs office at Heathrow Airport in July 2010 held a shipment that represented years of preparation: the first commercial OmniPods bound for patients in the United Kingdom. As Insulet's European team waited anxiously for clearance, they knew this moment marked more than geographic expansion—it was a test of whether American medical device innovation could navigate the complex tapestry of European healthcare systems. Launching the OmniPod in Europe and other international markets broadened the company's customer base and established it as a global player in diabetes technology.

The European launch strategy reflected hard-learned lessons from the U.S. market. Rather than attempting to conquer all of Europe simultaneously, Insulet focused on the UK and Germany first—two markets with sophisticated diabetes care infrastructure, favorable reimbursement potential, and combined population exceeding 140 million. The UK's National Health Service presented a centralized decision-making structure, while Germany's insurance system offered higher reimbursement rates for innovative medical technology.

The CE mark obtained in 2009 had given Insulet the regulatory green light for European sales, but regulatory approval was just the beginning. Each country required separate reimbursement negotiations, distribution partnerships, and clinical education programs. In the UK, NICE (National Institute for Health and Care Excellence) guidelines influenced adoption. In Germany, the G-BA (Federal Joint Committee) determined coverage. France, Italy, and the Netherlands each had their own Byzantine approval processes waiting in the wings.

Cultural adaptation proved as important as regulatory navigation. European diabetes management differed subtly but significantly from American approaches. MDI (multiple daily injection) therapy was more prevalent, with many European endocrinologists viewing insulin pumps as a last resort rather than optimal therapy. The OmniPod's positioning had to shift from "better than traditional pumps" to "the bridge between MDI and pump therapy." Marketing materials emphasized discretion and normalcy—values that resonated particularly strongly in European markets where medical privacy was paramount.

The partnership strategy in Europe diverged from the direct sales model used in the United States. Insulet partnered with Ypsomed, a Swiss medical device company with established distribution channels across Europe. This decision traded control for speed and capital efficiency. Ypsomed's sales force already called on endocrinologists, had relationships with pharmacy chains, and understood local reimbursement intricacies. The partnership allowed Insulet to enter multiple European markets simultaneously without the massive upfront investment of building their own infrastructure.

Back in the United States, the period from 2010 to 2015 saw Insulet evolve from insurgent to established player. The installed base grew from 20,000 to over 70,000 active users. This growth came not from converting existing pump users—market research showed less than 15% of new OmniPod users switched from other pumps. Instead, Insulet was expanding the entire pump market, reaching patients who had previously rejected pump therapy entirely.

The pediatric market became Insulet's stronghold. By 2013, OmniPod had captured nearly 40% of new pump starts in patients under 18. Parents drove this adoption, attracted by the simplicity and the elimination of tubes that could get caught during play. Pediatric endocrinologists appreciated the lower training burden and higher adherence rates. Summer diabetes camps became crucial marketing venues, where children could see peers wearing OmniPods and experience the freedom from tubes firsthand.

Product development during this period focused on building toward a more connected future. The OmniPod DASH system, in development since 2012, reimagined the user experience around modern smartphone interfaces. The new PDM featured a color touchscreen, Bluetooth connectivity, and intuitive menu systems that resembled consumer electronics rather than medical devices. This wasn't just cosmetic improvement—it was preparation for the connected health ecosystem that everyone knew was coming.

The competitive dynamics shifted dramatically in 2013 when Medtronic acquired insulin pump maker MiniMed's remaining assets for $3.7 billion, consolidating their dominant position. Rather than discourage Insulet, this move validated the insulin pump market's value and highlighted the opportunity for differentiated offerings. Medtronic's focus on sensor-augmented pumps and eventual artificial pancreas systems left room for Insulet to own the simplicity and lifestyle positioning.

Financial performance during this period reflected the challenges of international expansion and product development. Revenues grew from $120 million in 2010 to $381 million in 2015, but profitability remained elusive. International sales, while growing, carried lower margins due to distributor partnerships and price pressures from government payers. R&D spending increased as the company developed DASH and began early work on automated insulin delivery algorithms.

The Affordable Care Act's implementation in 2014 created both opportunities and challenges. Expanded insurance coverage meant more Americans had access to insulin pumps, growing the addressable market. But the ACA also increased pressure on medical device makers through new taxes and emphasis on value-based care. Insulet had to demonstrate not just that OmniPod was different, but that it delivered better outcomes at reasonable cost.

Manufacturing evolution during this period was crucial but unglamorous. The company's Billerica, Massachusetts facility (relocated from Bedford in 2012) became increasingly automated, with robotic assembly lines and sophisticated quality control systems. Manufacturing yields improved from 70% to over 90%, directly impacting gross margins. The company also established backup manufacturing capabilities in China, both for cost efficiency and supply chain resilience.

The pharmacy channel strategy emerged as one of Insulet's most important innovations during this period. While traditional insulin pumps went through durable medical equipment (DME) channels—requiring prior authorizations, lengthy approval processes, and specialized suppliers—Insulet pioneered getting OmniPods covered as pharmacy benefits. Patients could pick up their pods at CVS or Walgreens just like insulin or test strips. This seemingly minor change dramatically reduced friction in the acquisition process and improved medication adherence.

Market education remained an enormous challenge and expense. Despite growing adoption, many endocrinologists remained unfamiliar with OmniPod's benefits. Insulet invested heavily in medical education, sponsoring continuing education programs, publishing clinical studies, and maintaining a robust presence at diabetes conferences. The sales force grew from 50 representatives in 2010 to over 200 by 2015, each requiring extensive training not just on OmniPod but on diabetes management generally.

The international expansion beyond Europe began cautiously. Canada had proven successful, with OmniPod capturing significant market share despite competition from Medtronic's Canadian operations. Australia and select Middle Eastern markets followed. Each new country required regulatory approval, reimbursement negotiation, distribution setup, and clinical education—a two-to-three-year process that consumed capital and management attention.

By the end of 2015, Insulet had transformed from an American startup to a global medical device company. Operations spanned three continents. The installed base exceeded 70,000 users. Annual revenue run rate approached $400 million. The company had survived the transition from founder-led startup to professionally managed public company. Most importantly, the technological foundation was in place for the next leap forward: automated insulin delivery.

The challenges were equally clear. Profitability remained elusive despite scale. International operations were subscale in most markets. The competitive landscape was evolving rapidly, with continuous glucose monitors (CGMs) becoming mainstream and artificial pancreas systems moving from research to reality. The next phase would require Insulet to evolve from hardware manufacturer to algorithm developer, from standalone device to integrated system, from following the market to defining it.

VI. The Platform Evolution: From Hardware to Software (2015–2020)

The whiteboard in Insulet's advanced development lab in late 2015 contained a simple but profound equation: "Pump + CGM + Algorithm = Artificial Pancreas." Below it, someone had added: "But first, make it simple." This tension—between technological sophistication and user simplicity—would define Insulet's transformation from a hardware company to a platform company over the next five years.

The strategic shift began with a recognition that the insulin pump industry was approaching an inflection point. Continuous glucose monitors (CGMs) were becoming accurate enough for insulin dosing decisions. Smartphones were ubiquitous, powerful, and always connected. Machine learning algorithms could predict glucose trends and adjust insulin delivery. The companies that could integrate these technologies seamlessly would win; those that couldn't would become commoditized hardware suppliers.

The DASH system, officially launched in 2018 after years of development, represented Insulet's first major step toward platform thinking. On the surface, DASH looked like an evolutionary upgrade: a modern touchscreen PDM with Bluetooth connectivity replacing the older button-based interface. But underneath, DASH was revolutionary. The Bluetooth Low Energy connectivity enabled smartphone control—a first for insulin pumps. The cloud connectivity allowed remote monitoring by caregivers. The modular architecture made future CGM integration possible without hardware changes.

The development of DASH revealed the complexity of modernizing medical devices. The FDA required extensive cybersecurity testing—what if hackers could control insulin delivery? The Bluetooth protocol needed to be rock-solid reliable—a dropped connection could be life-threatening. The user interface had to be intuitive enough for elderly Type 2 patients yet sophisticated enough for tech-savvy Type 1 users. Every design decision carried regulatory, safety, and usability implications.

The partnership with Dexcom for CGM integration proved pivotal. While Medtronic pursued a vertically integrated strategy with their own CGM sensors, Insulet chose interoperability. This decision reflected both pragmatism and principle. Pragmatically, Dexcom's G6 sensor was widely regarded as the most accurate and user-friendly CGM available. Principally, Insulet believed patients should have choice—they shouldn't be locked into one company's entire ecosystem.

The technical integration between OmniPod and Dexcom CGM was complex but elegant. The systems needed to communicate reliably every five minutes, sharing glucose readings and trend data. The OmniPod's algorithm had to interpret this data and adjust insulin delivery accordingly. But critically, the system needed to fail gracefully—if CGM communication was lost, the pump had to continue delivering basal insulin safely. This redundancy and safety-first design would prove crucial for FDA approval.

Building toward automated insulin delivery (AID) required Insulet to develop competencies far from their hardware roots. They hired algorithm developers from aerospace and defense industries, where predictive control systems managed complex dynamic processes. They recruited endocrinologists and diabetes researchers to inform algorithm design. They partnered with academic institutions conducting artificial pancreas research. The company that had started as a mechanical engineering shop was becoming a software and data science organization.

The smartphone control vision faced unexpected regulatory headwinds. The FDA initially resisted allowing smartphones to control medical devices directly, citing cybersecurity and reliability concerns. What if the phone battery died? What if a software update broke compatibility? What if users accidentally bolused insulin while trying to send a text? Insulet had to pioneer new regulatory pathways, working with FDA to establish standards for mobile medical device control that balanced innovation with safety.

The competitive landscape during this period underwent tectonic shifts. Tandem Diabetes emerged as a formidable competitor with their t:slim pump and eventual Control-IQ algorithm. Bigfoot Biomedical and other startups raised hundreds of millions to develop next-generation systems. Even consumer tech companies like Apple and Google showed interest in diabetes management. The race was on to deliver the first truly automated insulin delivery system.

Financial performance during the platform transition reflected the dual challenges of maintaining growth while investing heavily in R&D. Revenues grew from $381 million in 2015 to $738 million in 2019, but R&D spending nearly doubled. The company finally achieved profitability in 2018—a milestone eighteen years in the making—but immediately reinvested profits into algorithm development and clinical trials. Wall Street questioned whether Insulet could compete in software against larger, better-resourced competitors.

The international expansion continued during this period but with a platform-first mentality. Rather than just selling pods in new countries, Insulet focused on markets ready for connected diabetes management. The UK and Germany became testing grounds for new features. Canada served as a preview market for U.S. regulatory submissions. This coordinated global approach replaced the country-by-country tactics of earlier years.

Clinical validation for automated insulin delivery required unprecedented investment. The pivotal trial for what would become Omnipod 5 enrolled over 300 patients across multiple sites, generating thousands of hours of glucose and insulin data. The trial had to prove not just that the algorithm worked, but that it was safe across diverse populations—children, adolescents, adults, those with hypoglycemia unawareness, those with varying insulin sensitivity. Every edge case had to be considered, tested, and validated.

The organizational transformation during this period was profound. Software engineers became as important as mechanical engineers. Data scientists joined clinical researchers. User experience designers worked alongside regulatory experts. The company's Acton headquarters (moved from Billerica in 2016) resembled a Silicon Valley tech company more than a traditional medical device manufacturer, with open floor plans, agile development teams, and rapid prototyping labs.

Manufacturing evolution continued with the introduction of U.S.-based fully automated production lines. While some components were still sourced globally, final assembly moved entirely to Massachusetts. This wasn't just about patriotic marketing—it was about quality control, supply chain security, and rapid iteration. When the COVID-19 pandemic struck in early 2020, this domestic manufacturing capability would prove prescient.

The pharmacy benefit strategy matured during this period, with over 65% of U.S. OmniPod users accessing their supplies through pharmacy channels by 2019. This seemingly mundane achievement had profound implications. Pharmacy benefits typically had lower co-pays than DME. Prior authorization was simpler. Patients could pick up pods with their monthly insulin, improving adherence. The strategy that had seemed risky in 2010 was now Insulet's key competitive advantage.

By early 2020, as the world entered pandemic lockdown, Insulet stood on the cusp of launching Omnipod 5—their automated insulin delivery system. Years of algorithm development, clinical trials, and regulatory preparation were complete. The platform transformation was about to be tested in the market. The company that had started with a father's desire to eliminate insulin injections was now positioned to eliminate the constant calculations and decisions that defined life with diabetes.

The challenges ahead were clear but different from those of the past. Success would no longer be measured just by pod sales but by time in range—the percentage of time users maintained healthy glucose levels. Competition would come not just from other pump makers but from smart pens, connected glucose monitors, and digital therapeutics. The platform game required continuous innovation, regular software updates, and ecosystem thinking.

VII. The Omnipod 5 Breakthrough: Automated Insulin Delivery (2020–2022)

The FDA review meeting in January 2022 had an unusual atmosphere. Typically, regulatory reviews for medical devices were tense affairs with company executives defending their data against skeptical regulators. But as Insulet's team presented the Omnipod 5 clinical results, even the FDA reviewers seemed impressed. The time-in-range improvements were dramatic. The hypoglycemia reduction was significant. And remarkably, these benefits came with no increase in user burden—the system just worked.

The journey to this moment had taken nearly a decade. The automated insulin delivery (AID) algorithm at Omnipod 5's heart—called SmartAdjust—represented thousands of person-years of development. The algorithm had to predict where glucose would be in 60 minutes based on current levels, trend, insulin on board, and historical patterns. It then had to adjust insulin delivery every five minutes, increasing, decreasing, or suspending delivery to keep glucose in target range. All of this had to happen automatically, safely, and reliably for users as young as two years old.

The clinical trial results exceeded even internal expectations. Users achieved an average time in range of 74%—meaning nearly three-quarters of the day spent with healthy glucose levels, compared to 64% with standard pump therapy. Overnight control was even better, with time in range exceeding 80%. For parents of children with diabetes, this meant actually sleeping through the night instead of waking for glucose checks and corrections. One trial participant called it "the first full night's sleep I've had in five years."

The technological achievement was remarkable, but what set Omnipod 5 apart was its simplicity. While competitors' systems required multiple devices, cables, and complex setup procedures, Omnipod 5 worked with just the pod and a smartphone. Users could onboard themselves in under an hour. The system learned and adapted to individual patterns without requiring constant user input. This was automated insulin delivery for the real world, not just for the highly motivated patients who participated in clinical trials.

The FDA approval came on January 28, 2022, for Type 1 diabetes patients aged six and above—making Omnipod 5 the first tubeless automated insulin delivery system. The approval timing was fortuitous. The diabetes community, exhausted from managing blood sugars during COVID-19 lockdowns and stress, was desperate for technology that reduced burden. Endocrinologists, who had seen diabetes control worsen during the pandemic, were eager for tools that could help patients achieve better outcomes with less effort.

The market launch strategy reflected lessons learned over two decades. Rather than rushing to maximize volume, Insulet pursued a limited market release to ensure quality and support. The first Omnipod 5 systems shipped in February 2022 to selected clinics and patients. Each launch was treated as a learning opportunity—how was the training working? What questions did users have? What features did they want? This measured approach built confidence among providers and patients while allowing rapid iteration.

The age expansion approvals came faster than anyone expected. By August 2022, FDA cleared Omnipod 5 for ages 2 and up—making it the only automated insulin delivery system approved for toddlers. This wasn't just a label expansion; it was acknowledgment that the system was safe and effective for the most vulnerable patients. Parents of young children with diabetes, who lived in constant fear of overnight hypoglycemia, finally had a tool that could protect their children while they slept.

The smartphone integration represented a paradigm shift in medical device control. Through 2022, Insulet worked to expand compatible devices, starting with specific Android phones and working toward iPhone compatibility. FDA 510(k) clearance for the Omnipod 5 App for iPhone would come in 2023, making Insulet the first company to offer full insulin pump control from an iPhone. This wasn't just about convenience—it was about meeting users where they were, on the devices they already carried.

The competitive response was swift but struggled to match Omnipod 5's simplicity. Medtronic's 780G system, while technologically sophisticated, still required tubes and separate devices. Tandem's Control-IQ, though effective, couldn't match the freedom of tubeless delivery. Beta Bionics' iLet Bionic Pancreas, approved later in 2022, offered innovation but lacked Insulet's established user base and distribution infrastructure. The market was validating what Insulet had believed all along: simplicity and effectiveness weren't mutually exclusive.

Real-world evidence quickly validated the clinical trial results. Early adopters reported life-changing improvements. A teacher from Ohio described being able to focus on her students instead of constantly monitoring her glucose. A teenager from California talked about playing soccer without fear of going low. A parent from Texas simply said, "We have our life back." These weren't just medical outcomes—they were human outcomes, the realization of John Brooks' original vision of freeing people from the burden of diabetes management.

The manufacturing and supply chain excellence required for Omnipod 5's launch cannot be overstated. Each pod now contained sophisticated electronics capable of complex calculations and wireless communication. The quality standards were extraordinary—a failure rate of even 0.1% would affect hundreds of users. Insulet's Massachusetts facility, upgraded with new automated lines, could produce over 400,000 Omnipod 5 pods monthly by late 2022, with capacity for expansion.

Financial impact was immediate and substantial. Omnipod 5 drove new user additions to record levels, with the U.S. installed base growing over 35% year-over-year. Average revenue per user increased as Omnipod 5 commanded premium pricing. Gross margins expanded as manufacturing efficiency improved. By the end of 2022, Insulet's annual revenue exceeded $1.3 billion, with Omnipod 5 accounting for the majority of new starts.

The international rollout strategy for Omnipod 5 was deliberately sequenced. Rather than launching globally simultaneously, Insulet focused on markets with established CGM adoption and favorable reimbursement. The UK and Germany were prioritized for European launch. Canada's approval process was accelerated based on FDA clearance. Each market launch incorporated learnings from previous ones, refining training materials, support processes, and marketing messages.

Clinical evidence continued to accumulate through 2022. Studies showed Omnipod 5 reduced diabetes distress—the psychological burden of constant glucose management. Data demonstrated improved sleep quality for both users and caregivers. Research revealed that even users with poor baseline control showed dramatic improvements. This wasn't just an incremental advance; it was a step-change in diabetes management.

The ecosystem strategy became clearer as Omnipod 5 matured. Integration with additional CGM platforms was planned. Digital health partnerships were explored. Data analytics capabilities were enhanced. Insulet was building not just a pump but a platform for comprehensive diabetes management. The vision extended beyond insulin delivery to include predictive analytics, personalized insights, and eventually, prevention of complications.

Organizational culture during the Omnipod 5 launch reflected the mission-driven nature of the company. Employees worked overtime not because they were required to but because they knew every day of delay meant patients suffering unnecessarily. Customer service representatives, many with diabetes themselves, provided support with empathy born from experience. The entire organization aligned around a singular goal: getting this life-changing technology to as many people as possible.

The challenges weren't entirely solved. Insurance coverage for Omnipod 5 required new prior authorization processes. Training thousands of healthcare providers took time and resources. Manufacturing capacity, while substantial, still constrained growth. International regulatory approvals moved slowly. Competition continued to invest heavily in their own AID systems. But these were scaling challenges, not existential ones.

As 2022 drew to a close, Insulet had achieved what many thought impossible: they had built a truly automated insulin delivery system that was both sophisticated and simple, both powerful and accessible. The father's dream that started the company—freeing his son from the burden of diabetes management—was now reality for hundreds of thousands of users. But the biggest opportunity still lay ahead: bringing this technology to the millions of Type 2 diabetes patients who required insulin.

VIII. Expanding the TAM: Type 2 Diabetes & Beyond (2023–Present)

The endocrinology conference in San Diego in June 2023 had an unusual energy. Word had spread that Insulet was about to present data that could fundamentally change diabetes management. As Dr. Sarah Chen took the stage to present the SECURE-T2D trial results, the auditorium was packed. The data she revealed would reshape how the medical community thought about insulin delivery for Type 2 diabetes: Omnipod 5 was able to lower HbA1c by 0.8 percentage points overall and by 2.1 points among adults with Type 2 diabetes who started the study at 9% or higher.

The Type 2 diabetes opportunity had always been tantalizing but elusive. More than 30 million people live with type 2 diabetes in the U.S. and about 6 million require insulin. Of those, 2.5 million use multiple daily injections (MDI). Yet historically, less than 5% of Type 2 patients used insulin pumps. The barriers were numerous: cost, complexity, stigma, and the perception that pumps were only for Type 1 diabetes. Insulet's strategy to crack this market required rethinking everything from product design to distribution.

The FDA clearance in August 2024 was momentous: The FDA has cleared its first automated insulin pump for adults with Type 2 diabetes, with Insulet's Omnipod 5 delivery system opening the door to a population of more than 6 million people. This wasn't just a label expansion—it was validation that automated insulin delivery could benefit a much broader population than previously imagined. The clearance made Omnipod 5 the first and only such system cleared for type 1 and type 2 diabetes.

The clinical evidence was compelling beyond the headline HbA1c improvements. The system also reduced total daily insulin doses, with a 20% increase in the daily amount of time spent in a healthy blood sugar range compared to manual injections. This efficiency mattered enormously for Type 2 patients, who often struggled with weight gain from insulin therapy. Less insulin achieving better control meant improved outcomes with fewer side effects.

But Insulet recognized that one size wouldn't fit all in the Type 2 market. Enter Omnipod GO, cleared by the FDA in April 2023: An insulin delivery device cleared for use for people with type 2 diabetes age 18 or older who would typically take daily injections of long-acting insulin. This basal-only pod represented radical simplification—no PDM, no smartphone app, just preset basal rates delivering steady insulin. "Omnipod GO was designed to serve the more than three million people using basal insulin or transitioning to insulin therapy" said CEO Jim Hollingshead.

The Omnipod GO strategy was brilliant in its simplicity. Type 2 patients starting insulin typically began with once-daily basal insulin. Omnipod GO replaced that daily injection with a pod changed every three days. No calculations, no carb counting, no boluses—just steady background insulin. The product was developed to serve people with type 2 diabetes earlier in their treatment journey by starting them on Pod therapy for their insulin delivery, rather than daily injections. If a patient becomes insulin-intensive, meaning they require both basal and bolus insulin, the transition to another Omnipod product would be seamless.

The commercial strategy for Type 2 required fundamental changes. Primary care physicians, not endocrinologists, managed most Type 2 patients. These doctors had neither the time nor inclination for complex device training. Insulet's response was to make initiation dead simple: Insulet developed Omnipod GO with convenience in mind for both the primary care physician and the user, including prescribing, getting started, training and using the product. Customers may start Omnipod GO in their physician's office and will be able to access ongoing supplies through their pharmacy benefit.

The sales force expansion announced in early 2024 reflected the magnitude of the opportunity. Insulet added over 100 representatives focused specifically on primary care, doubling their field presence. These weren't traditional device reps but diabetes educators who could train office staff, simplify insurance processing, and support patients directly. The investment was substantial but necessary—primary care doctors saw dozens of patients daily and had minutes, not hours, for new technology adoption.

Financial performance in 2024 validated the Type 2 strategy dramatically. Annual revenue surpassed $2 billion for the first time in Insulet's history, representing the ninth consecutive year of 20% or more constant currency revenue growth. The company achieved this milestone faster than analysts predicted, driven by accelerating adoption in both Type 1 and Type 2 populations.

The margin expansion story was equally impressive. Gross margin reached 69.8% (an increase of 210 basis points year-over-year) and operating margin expanded to 14.9% (up 260 basis points year-over-year). The fourth quarter of 2024 was particularly strong: gross margin reaching 72.1%, an increase of 120 basis points from the previous year. This wasn't just growth—it was profitable growth, proving the business model could scale efficiently.

International expansion accelerated with the Type 2 indication providing new momentum. European health systems, struggling with diabetes costs, were receptive to technology that could improve outcomes while potentially reducing long-term complications. The UK's NHS began pilot programs for Type 2 patients. Germany's insurance system created new reimbursement codes. Even emerging markets showed interest, recognizing that diabetes was becoming a global epidemic requiring innovative solutions.

The competitive landscape in Type 2 was surprisingly sparse. Medtronic and Tandem had focused primarily on Type 1, viewing Type 2 as too price-sensitive and complex to serve profitably. This left Insulet with an enormous first-mover advantage. By the time competitors pivoted to address Type 2, Insulet would have thousands of patients, refined protocols, and established reimbursement—classic network effects in a medical device market.

The technology roadmap revealed at investor meetings showed ambitious plans. Integration with GLP-1 medications like Ozempic and Mounjaro was being explored—could the pod deliver these drugs too? Predictive analytics using AI could identify patients likely to benefit from pod therapy. Digital therapeutics partnerships could provide behavioral support alongside insulin delivery. The vision extended beyond insulin to become a comprehensive metabolic health platform.

Real-world evidence from early Type 2 adopters was encouraging. Patients reported feeling "more normal" with a discrete pod versus multiple daily injections. Adherence rates exceeded 90%, compared to less than 60% for injection therapy. Healthcare providers noted improved patient satisfaction and reduced diabetes-related hospitalizations. These soft metrics mattered as much as clinical outcomes in driving adoption.

The reimbursement landscape for Type 2 required careful navigation. While Type 1 pump coverage was well-established, Type 2 coverage varied widely. Insulet's market access team worked with payers to demonstrate cost-effectiveness—showing that improved control reduced expensive complications. The pharmacy channel strategy proved particularly valuable, as pharmacy benefits typically had fewer restrictions than medical benefits for Type 2 treatments.

Manufacturing capacity expansion announced in late 2024 reflected confidence in continued growth. A new highly automated facility in Massachusetts would triple production capacity by 2026. Advanced robotics and AI-powered quality control would improve yields while reducing costs. The investment exceeded $500 million but was essential to meet projected demand as Type 2 adoption accelerated.

Looking ahead to 2025, Insulet's guidance reflected continued confidence: Total Omnipod revenue expected to increase between 17% and 21%. The company anticipates U.S. sales to rise by 16% to 20% and international sales by 22% to 26%, with a projected gross margin of 70.5% and operating margin of 16.5%. These weren't startup growth rates—they were exceptional for a $2 billion revenue company.

The organizational transformation to serve Type 2 was profound. The company hired endocrinologists specializing in Type 2 diabetes. They brought in experts from primary care. They invested in patient support programs tailored to older adults who might be less tech-savvy. The culture evolved from "pump company" to "diabetes solution company," a subtle but critical shift in identity.

As 2024 ended, Insulet stood at an inflection point. The Type 2 market was opening rapidly. International expansion was accelerating. The technology platform was extending beyond insulin. Competition was struggling to keep pace. The company that had started with a father's dream of simplifying his son's Type 1 diabetes management was now poised to transform treatment for millions with Type 2 diabetes globally.

IX. Business Model & Competitive Moat

The spreadsheet on the CFO's screen in late 2024 told a story that would make any subscription software executive envious. Customer lifetime value exceeding $40,000. Gross margins approaching 70%. Revenue retention rates above 90%. Annual recurring revenue surpassing $2 billion. But this wasn't a SaaS company—it was Insulet, and they had cracked the code on turning disposable medical supplies into a predictable, high-margin revenue stream.

The brilliance of Insulet's business model lies in its simplicity: sell the PDM (Personal Diabetes Manager) at or near cost, then generate recurring revenue from pod sales every month for potentially decades. Each pod lasts 72 hours, meaning users need approximately 10 pods monthly, or 120+ annually. At roughly $350-400 per month in revenue per patient, the math becomes compelling quickly. This razor/razorblade model, perfected by Gillette a century ago, found new life in diabetes management.

But unlike razors, insulin pumps have extraordinary switching costs. Changing pump systems requires new insurance approvals, extensive retraining, learning new interfaces, and adjusting life routines built around specific device characteristics. Patients invest emotionally in their devices—they're not just tools but lifelines. This creates powerful lock-in effects that subscription software companies can only dream of. Insulet's annual patient attrition rate of less than 10% reflects this stickiness.

The pharmacy channel strategy emerged as perhaps Insulet's most underappreciated competitive advantage. While competitors' pumps required DME (Durable Medical Equipment) billing with complex prior authorizations and specialized suppliers, Insulet pioneered pharmacy benefit coverage. By 2024, over 70% of U.S. Omnipod users obtained pods through their local pharmacy. This seemingly mundane distribution innovation had profound implications: lower patient co-pays, simplified reimbursement, improved adherence, and reduced administrative burden for providers.

The patent portfolio provided crucial protection but wasn't the primary moat. Insulet held over 500 patents covering everything from automated insertion mechanisms to wireless communication protocols. But more important than individual patents was the integrated system—the complex interplay of miniaturized pumping mechanisms, adhesive technology, wireless communication, and software algorithms. Competitors could potentially design around individual patents but replicating the entire system would take years and hundreds of millions in investment.

Network effects, often discussed in technology but rare in medical devices, emerged strongly in Insulet's model. Each endocrinologist trained on Omnipod became more likely to prescribe it. Each diabetes educator familiar with the system became an advocate. Each patient successfully using Omnipod became a reference for others. Online communities formed around Omnipod, sharing tips, decorating ideas, and troubleshooting. This organic ecosystem was impossible to replicate with marketing dollars alone.

The manufacturing scale advantages compounded over time. Producing millions of pods annually allowed Insulet to negotiate better component prices, invest in automation, and spread fixed costs across a larger base. A new entrant would face the chicken-and-egg problem: needing scale to achieve competitive costs but needing competitive costs to achieve scale. Insulet's gross margins expanding from 30% in 2010 to nearly 70% in 2024 demonstrated these scale economics in action.

Competition analysis revealed why Insulet's position was so defensible. Medtronic, despite being 10x larger, struggled to compete in the patch pump segment. Their attempted patch pump, developed with Calibra Medical, never reached market. Their focus on sensor-integrated systems and closed-loop algorithms, while technologically impressive, added complexity that many patients didn't want. Medtronic's business model, built on high-margin durable pumps lasting 4-7 years, made it structurally difficult to embrace disposable models.

Tandem Diabetes represented a more direct threat with their t:slim X2 pump gaining share among tech-savvy Type 1 patients. But Tandem's traditional tubed design limited their addressable market to patients willing to accept tubes. Their Control-IQ algorithm was excellent, but Omnipod 5 had caught up technologically while maintaining the tubeless advantage. Tandem's attempts to develop a patch pump (t:sport) had been delayed multiple times, suggesting the technical challenges were harder than anticipated.

Emerging competitors like Beta Bionics (iLet Bionic Pancreas) and Bigfoot Biomedical offered innovation but lacked Insulet's scale and infrastructure. These companies faced the brutal reality of medical device commercialization: even with superior technology, building distribution, training thousands of providers, navigating reimbursement, and scaling manufacturing took years and hundreds of millions of dollars. Many would likely become acquisition targets rather than standalone competitors.

The continuous glucose monitor (CGM) companies—Dexcom and Abbott—represented both partners and potential threats. While currently partnering with Insulet for integrated systems, these companies had the technology and capital to potentially enter insulin delivery. However, their business models and core competencies in sensors differed significantly from insulin delivery. More likely, they would continue partnering with pump makers rather than competing directly.

The data and software layer emerging in Insulet's model created new value and defensibility. Every Omnipod 5 generated continuous data on insulin delivery, glucose patterns, and user behaviors. This data, properly analyzed, could improve algorithms, personalize therapy, and predict complications. While regulations limited how this data could be monetized directly, it created a learning advantage that compounded over time. Insulet's algorithms would improve faster than competitors' simply because they had more real-world data.

The international expansion strategy leveraged the business model globally. In markets with single-payer systems, the economic argument was compelling: better control reduced expensive complications. The subscription model aligned with how health systems preferred to budget—predictable monthly costs rather than large upfront expenditures. Country-by-country reimbursement approval created additional barriers to entry, as each market required years of negotiation and relationship building.

Capital efficiency had improved dramatically as the model matured. In the early years, Insulet burned cash acquiring customers and building infrastructure. By 2024, the company generated substantial free cash flow, with established customers funding new customer acquisition. This self-funding growth model meant Insulet could expand without dilutive equity raises or expensive debt, a luxury most medical device companies never achieved.

The platform extensibility into adjacent markets showcased the model's potential. The same pod technology delivering insulin could potentially deliver other medications—GLP-1 agonists for weight loss, glucagon for severe hypoglycemia, or even non-diabetes drugs requiring continuous subcutaneous delivery. Each new application leveraged existing manufacturing, distribution, and regulatory expertise. Insulet wasn't just building a pump business but a drug delivery platform.

Risk factors remained real despite the strong moat. Technological disruption from smart insulin pens or ultra-long-acting insulins could reduce pump demand. Reimbursement pressure from government payers could compress margins. Manufacturing problems or recalls could damage reputation. New entrants with deep pockets—imagine Apple or Google entering diabetes—could change competitive dynamics. But these risks affected all pump makers, and Insulet's model provided more resilience than traditional approaches.

The financial metrics by late 2024 validated the model's strength. Return on invested capital exceeded 15%. Free cash flow margins approached 20%. Revenue per employee surpassed $500,000. These weren't medical device metrics—they were software company metrics achieved with hardware. The market recognized this, awarding Insulet a valuation multiple premium to traditional medical device companies.

Looking forward, the business model's evolution seemed clear. Higher-margin software and services would complement hardware revenue. International expansion would improve scale economics further. New therapeutic areas would leverage the platform. Data analytics would enable value-based contracting. The subscription model that had started with simple pod sales was evolving into a comprehensive diabetes management platform with multiple revenue streams and compounding competitive advantages.

X. Playbook: Lessons for Founders & Investors

The conference room at a prominent Boston venture capital firm in early 2024 was packed with associates and analysts, all leaning in as John Brooks, Insulet's co-founder, shared hard-won wisdom from building a $2 billion revenue medical device company. "Everyone asks about the technology," he began, "but the real lessons are about persistence, focus, and understanding that in healthcare, being right isn't enough—you have to change entire systems of behavior."

Lesson 1: Start with genuine personal mission, not market analysis. Brooks' drive came from watching his son struggle with diabetes, not from McKinsey reports about TAM. This authentic motivation sustained him through the brutal early years when everyone—investors, doctors, insurers—said tubeless pumps were unnecessary. Founders solving their own problems have an emotional reservoir that founders chasing market opportunities lack. When Insulet nearly ran out of cash in 2008, it was mission, not financial upside, that kept the team together.

Lesson 2: Patient-centric design beats feature wars. While Medtronic added features—more alarms, more settings, more complexity—Insulet subtracted. They removed tubes, eliminated maintenance, simplified training. Every design decision was filtered through "Would a seven-year-old want to wear this?" This discipline is hard because engineers love complexity and sales teams always want more features to sell. But in medical devices, less is often more. The winning products are those patients actually use, not those with the most impressive spec sheets.

Lesson 3: Navigate FDA strategically, not fearfully. Many founders view FDA as an adversary to overcome. Insulet treated them as partners to educate. They brought FDA reviewers to patient focus groups. They shared real stories of children afraid of tubes. They positioned Omnipod not as replacing existing pumps but expanding the market to pump-resistant patients. This collaborative approach led to faster approvals and even FDA support for novel regulatory pathways like smartphone control.

Lesson 4: Build distribution before demand. Insulet spent years getting insurance coverage before having significant sales. They trained diabetes educators before doctors were prescribing. They established pharmacy relationships before patients were asking. This seemed backwards—why build infrastructure without revenue? But in healthcare, distribution is destiny. When demand finally inflected, Insulet could fulfill it while competitors scrambled to build infrastructure.

Lesson 5: Choose business model innovation over technical innovation. The pharmacy channel strategy wasn't technologically innovative but was transformational for the business. Moving from DME to pharmacy benefits reduced friction, improved margins, and created competitive advantage. Too many medtech founders focus on technical differentiation while ignoring business model innovation. How you sell, distribute, and get paid matters as much as what you build.

Lesson 6: Go deep before going broad. Insulet could have launched internationally immediately or expanded into Type 2 diabetes earlier. Instead, they spent a decade perfecting the Type 1 pediatric market in the U.S. This focus allowed them to refine the product, build evidence, and establish reimbursement. Only after dominating their beachhead did they expand. Premature scaling is the number one killer of medical device startups.

Lesson 7: Platform transitions require conviction and capital. The shift from hardware to software (Omnipod to Omnipod 5) took seven years and hundreds of millions in investment. Wall Street questioned it. Competitors mocked it. But Insulet's leadership understood that standalone devices were becoming commoditized. The future belonged to connected, intelligent systems. This transition required not just technical investment but organizational transformation—hiring software engineers, building cloud infrastructure, creating data science capabilities.

Lesson 8: Capital efficiency comes from model innovation, not cost cutting. Insulet achieved profitability not by reducing R&D or cutting sales force but by innovating the business model. The subscription revenue model, pharmacy distribution, and disposable design all improved unit economics. Too many medtech companies try to cut their way to profitability rather than innovating their way there.

Lesson 9: Timing matters more than being first. Insulet wasn't the first patch pump—that was Insulon's D-Tron in the 1990s. But earlier attempts failed because the ecosystem wasn't ready—CGMs weren't accurate, smartphones didn't exist, patients weren't frustrated enough with existing options. Insulet succeeded because they arrived when technology, market readiness, and patient dissatisfaction converged. Being too early is often worse than being too late.

Lesson 10: Competition validates markets. When Tandem went public and Bigfoot raised $100 million, Insulet celebrated. Competition validated that tubeless/automated delivery was the future, expanding the entire category. Too many founders fear competition when they should welcome it. In nascent markets, the enemy isn't competitors but the status quo. Multiple players educating the market accelerates adoption for everyone.

For Investors: Evaluating medical device opportunities requires different frameworks than software or biotech. Look for authentic founder motivation—personal connection to the problem predicts persistence. Evaluate distribution strategy as carefully as technology—great products fail without market access. Understand reimbursement dynamics—who pays, how much, and why determines everything. Assess regulatory strategy—companies that partner with FDA succeed; those that fight it struggle.

The capital requirements in medtech are often misunderstood. Yes, the initial capital needs are high—Insulet raised over $500 million before achieving sustained profitability. But unlike biotech with binary outcomes, medical devices can show progressive clinical and commercial validation. Revenue comes earlier than drug development. And once achieved, the moats are often stronger than software because of regulatory barriers, switching costs, and manufacturing complexity.

The time horizons are longer than software but shorter than biotech. Insulet took 18 years to reach profitability, but they had revenue by year 5 and went public by year 7. This middle ground—longer than typical venture horizons but with intermediate milestones—requires patient capital and staged funding strategies. The winners are investors who understand these dynamics and structure investments accordingly.

Market size can be deceptive in medical devices. The insulin pump market was supposedly $3 billion when Insulet started—tiny by venture standards. But Insulet expanded the market by reaching new patients. They turned non-consumers into consumers. The lesson: don't just analyze existing markets; consider how innovation might expand categories entirely.

The role of strategic acquirers is complex. Throughout Insulet's history, acquisition rumors swirled—would Medtronic, Johnson & Johnson, or Abbott buy them? But Insulet's success came from independence, allowing them to partner with multiple CGM companies and maintain innovation speed. The playbook lesson: build for independence while maintaining strategic option value.

Culture matters enormously in medical devices. Insulet's employee base included many with personal diabetes connections. This created authentic passion that no amount of equity compensation could replicate. When evaluating medtech investments, spend time understanding culture and mission alignment. The companies that change healthcare have employees who genuinely care about patients, not just exit valuations.

The session concluded with Brooks reflecting on what he'd do differently: "I'd trust our instincts more and conventional wisdom less. Every breakthrough decision we made—going tubeless, choosing disposable, using pharmacy channels—was contrarian. The experts said we were wrong. The incumbents said it wouldn't work. But patients said 'finally, someone understands.' In healthcare, patient pull beats expert push every time."

XI. Bear vs. Bull Case Analysis

The investment committee meeting at a major healthcare fund in December 2024 was reaching its climax. Two analysts had spent months evaluating Insulet, and now they presented opposing views. The bear analyst opened with a stark warning: "Insulet is priced for perfection in a market about to undergo fundamental disruption." The bull analyst countered: "This is a rare opportunity to own the dominant player in a massive, underpenetrated market with decades of growth ahead." Both made compelling cases.

The Bull Case: A Generational Growth Story