ResMed: The Story of Sleep Medicine Innovation

I. Introduction & Episode Roadmap

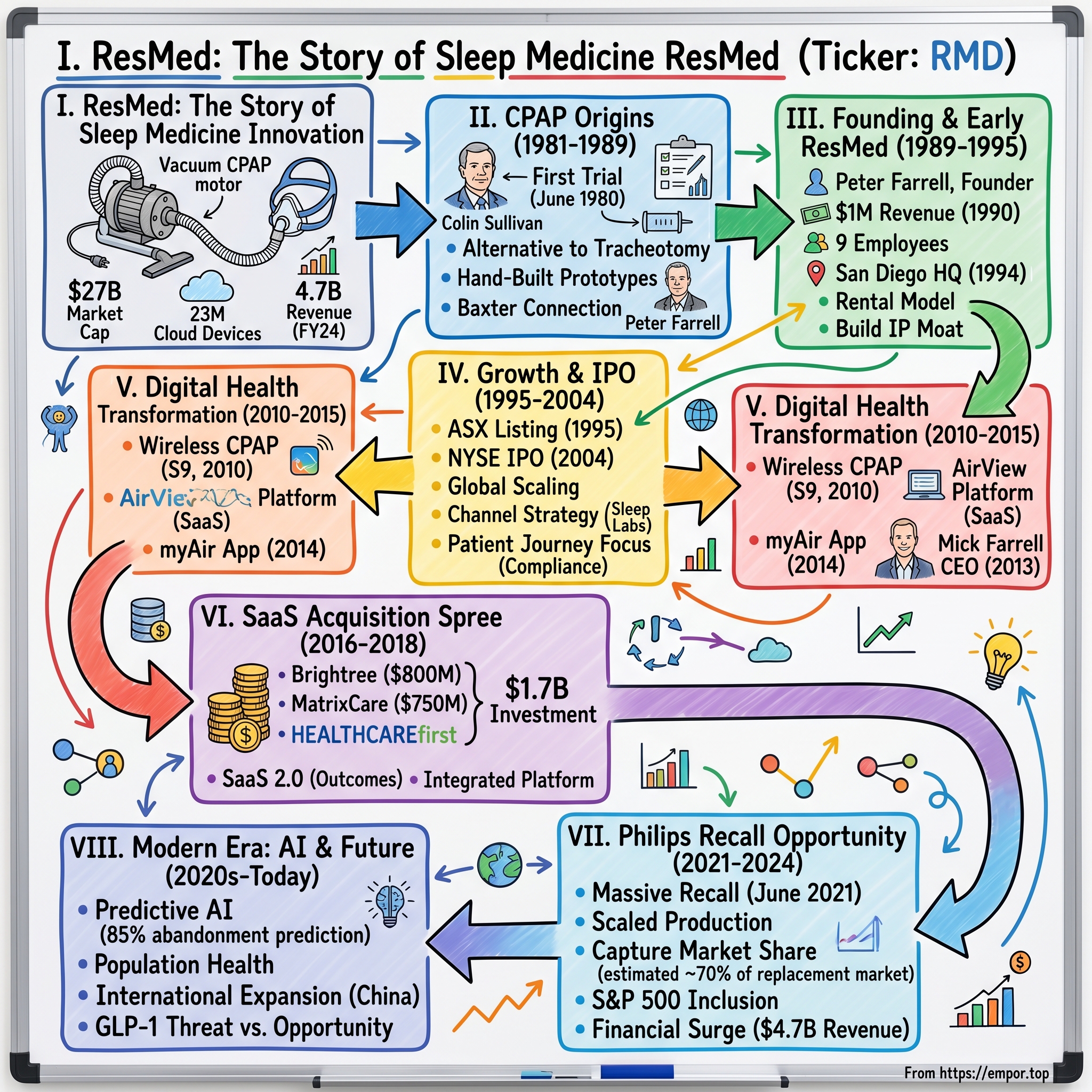

Picture this: It's 2 AM in a sleep lab at Sydney's Royal Prince Alfred Hospital, circa 1980. A desperate patient with severe sleep apnea faces two choices—undergo a tracheotomy, literally cutting a hole in their throat to breathe at night, or continue risking death with every sleep. In the corner of that lab, a young Australian researcher named Colin Sullivan is tinkering with vacuum cleaner motors and plastic tubes, convinced there must be a better way. That makeshift contraption would become the foundation of what is today ResMed—a $27 billion market cap medical device giant that generated $4.7 billion in revenue in fiscal 2024 and has 23 million cloud-connected devices monitoring sleep patterns across the globe.

How did a hand-built prototype assembled in a hospital workshop evolve into the backbone of modern sleep medicine? How did an Australian startup founded by an American executive become the dominant force in a market that barely existed forty years ago? And perhaps most intriguingly—how did a company built on clunky bedside machines transform itself into a software-powered, AI-driven healthcare platform that's reshaping out-of-hospital care?

This is the story of ResMed—a company that not only created an industry but has consistently reinvented itself through multiple technological waves. It's a tale of academic innovation meeting commercial ambition, of patent battles and strategic acquisitions, of navigating regulatory mazes while building recurring revenue streams that would make any SaaS company envious. Along the way, we'll explore how ResMed capitalized on a competitor's catastrophic recall to cement market dominance, why they spent nearly $2 billion acquiring seemingly unrelated software companies, and what their journey reveals about building enduring healthcare franchises in an era of rapid technological change.

The ResMed story offers profound lessons about founder-driven innovation, the power of platform economics in healthcare, and the delicate dance between medical device manufacturing and software services. It's a masterclass in capital allocation, competitive positioning, and long-term value creation that every investor and entrepreneur should understand. Let's dive into how a vacuum cleaner motor in a Sydney hospital became the foundation of a global medtech empire.

II. The Colin Sullivan Innovation & CPAP Origins (1981–1989)

The eureka moment came not in a pristine research facility but in Colin Sullivan's cramped workshop at Royal Prince Alfred Hospital. Sullivan, a respiratory physician and researcher, had been obsessing over a seemingly intractable problem: how to keep airways open during sleep without invasive surgery. His patients were suffocating dozens of times per hour, their soft throat tissues collapsing and blocking airflow—a condition called obstructive sleep apnea that affected millions but had no good treatment options.

Sullivan's breakthrough was elegantly simple yet revolutionary: use continuous positive air pressure delivered through the nose to create a "pneumatic splint" that would keep the airway open. Think of it like inflating a balloon inside a collapsing tunnel—the pressure keeps the walls from caving in. But the execution was anything but elegant. Sullivan's first prototype involved a reversed vacuum cleaner motor (to blow rather than suck), plastic tubing, and a fiberglass mask molded to fit a patient's face. He literally glued the mask to a patient's nose with medical-grade silicone sealant for the first trial in June 1980.

That first night was transformative. The patient, who had been experiencing severe apnea events throughout the night, slept peacefully for the first time in years. Sullivan watched the polysomnography readings in amazement—the apnea events had completely disappeared. When Sullivan published his findings in The Lancet in 1981, he described the nasal continuous positive airway pressure (CPAP) machine as a treatment for sleep apnea, fundamentally changing how medicine approached the condition.

Prior to the invention of the nasal CPAP machine, sleep apnea was often treated with radical measures such as tracheotomy—a procedure where surgeons would cut a hole in the patient's throat and insert a tube that could be opened at night to bypass the collapsing upper airway. Imagine telling patients their choice was between suffocating in their sleep or living with a permanent hole in their throat. Sullivan's CPAP offered a third way—non-invasive, reversible, and remarkably effective.

What happened next was perhaps even more remarkable than the invention itself. Rather than immediately commercializing his discovery, Sullivan turned his hospital workshop into a proto-manufacturing facility. Sullivan helped make CPAP machines and masks by hand in a workshop at the Royal Prince Alfred Hospital for the treatment of patients at the world's first sleep apnea clinic at the university. Each device was custom-built, with Sullivan and his small team crafting masks from dental impression materials and assembling pumps from industrial components.

The demand was overwhelming. Over 100 patients were being treated there by 1985, and over 1000 patients by 1989—all with machines built by hand in what was essentially a hospital basement. Sullivan wasn't just treating patients; he was proving market demand and refining the technology through thousands of real-world iterations. Every mask that didn't seal properly, every motor that was too loud, every patient complaint became data for the next version.

But Sullivan's journey from inventor to entrepreneur would hit a devastating roadblock. In 1993 a setback occurred when three judges of the Australian Federal Court revoked Sullivan's original Australian patent for a CPAP machine. The court ruled that the invention lacked sufficient novelty—a crushing blow that would have profound implications for how the technology would be commercialized. This patent drama would shape the industry's competitive dynamics for decades, forcing companies to innovate around the core CPAP concept rather than relying on fundamental patent protection.

Enter the business minds who would transform Sullivan's workshop operation into a global enterprise. The Baxter Centre connection brought Chris Lynch and Peter Farrell's involvement, with Baxter's investment in Sullivan's technology. Baxter International, the medical device giant, had established the Baxter Centre for Medical Research at the University of Sydney, where Sullivan worked. They saw the potential in CPAP technology and initially planned to commercialize it themselves.

Peter Farrell, an American chemical engineer who had joined Baxter in 1984 to lead their R&D efforts in Asia-Pacific, became fascinated with Sullivan's work. Farrell wasn't a typical medical device executive—he had a PhD from the University of Washington and had spent years in industrial R&D. He understood both the science and the business potential of what Sullivan had created. When Baxter decided not to enter the sleep apnea market, Farrell saw his opportunity and founded ResMed.

The decision by Baxter to walk away from sleep apnea—a market that would grow to be worth tens of billions—ranks among the great corporate blunders in medical device history. They saw it as too niche, too uncertain, requiring too much patient education. Farrell saw it differently: an enormous undiagnosed population, a technology with proven efficacy, and the opportunity to build an entirely new medical specialty around sleep disorders. That divergence in vision would create one of the most successful medical device companies of the next three decades.

III. Peter Farrell's Founding & Early ResMed (1989–1995)

ResMed was established in June 1989 by Peter Farrell in Australia, but the founding story reads more like a startup thriller than a typical medical device launch. Farrell had mortgaged his house, convinced a handful of investors to back him, and negotiated a complex licensing deal with Baxter for Sullivan's technology—all while Baxter executives probably thought he was making a career-ending mistake. The name itself, ResMed (Respiratory Medicine), signaled ambition beyond just sleep apnea; Farrell envisioned addressing all respiratory disorders that could be managed outside the hospital.

The early days were brutal. Revenues for ResMed's first fiscal year in 1990 were less than $1 million, and there were only 9 employees. Farrell operated out of a small office in Sydney, personally assembling devices, training clinicians, and even delivering machines to patients' homes. He would later recall working 18-hour days, switching between roles as CEO, engineer, salesperson, and delivery driver—sometimes all in the same afternoon.

The founding vision centered on commercializing Sullivan's CPAP technology, but Farrell understood that success required more than just manufacturing devices. He needed to build an entire ecosystem: educate physicians about sleep disorders, establish reimbursement pathways with insurers, create distribution networks, and most critically, design products that patients would actually use. The original hospital-built CPAPs worked, but they were loud, uncomfortable, and looked like medieval torture devices. Farrell's team set out to transform them into consumer-friendly medical products.

The geographic expansion strategy was counterintuitive but brilliant. Rather than focusing solely on the Australian market, the company opened an office in San Diego in 1992, and made that its headquarters two years later when it incorporated in the US. Why San Diego? It wasn't just the weather—though Farrell, an American expat, probably appreciated returning to California. San Diego offered proximity to the UC San Diego medical complex, access to engineering talent, and most importantly, a gateway to the massive U.S. healthcare market where sleep medicine was just beginning to gain recognition.

The dual-headquarters structure—R&D and manufacturing in Australia, corporate and commercial operations in the U.S.—would become a defining characteristic of ResMed's operational model. It allowed them to leverage Australian research grants and Sullivan's continued innovations while attacking the lucrative American market where reimbursement rates for CPAP therapy were being established.

Building the business model required solving a fundamental challenge: CPAP machines were expensive (initially $3,000-5,000), but patients wouldn't know if they could tolerate the therapy until they tried it. Farrell pioneered the rental model—patients could rent devices monthly, with insurance covering the cost if they demonstrated compliance. This transformed CPAP from a risky upfront purchase into an ongoing service, creating predictable recurring revenue streams that would later make ResMed's financial model the envy of the medical device industry.

The patent landscape remained treacherous following the Australian court's decision to revoke Sullivan's original patent. Farrell's response was to build an innovation machine that would generate hundreds of patents around specific improvements: quieter motors, better mask seals, data recording capabilities, comfort features. If they couldn't own the fundamental CPAP concept, they would own everything that made CPAP actually work in the real world. This IP strategy would prove prescient as competitors emerged.

By 1995, ResMed had grown to roughly $25 million in revenue—a 25x increase from their first year but still tiny by medical device standards. Yet Farrell was laying foundations that would support exponential growth: physician education programs that treated sleep specialists as partners rather than customers, reimbursement strategies that made CPAP accessible to middle-class patients, and most importantly, a culture of continuous innovation that turned patient complaints into product improvements. The scrappy startup was ready to scale, setting the stage for a public offering and global expansion that would transform sleep medicine forever.

IV. Growth, Scale & Going Public (1995–2004)

The late 1990s marked ResMed's transformation from startup to scale-up, but the journey to IPO was anything but smooth. Farrell faced a classic founder's dilemma: the company needed capital to fund international expansion and R&D, but venture capitalists wanted control and a quick exit. His solution was audacious—bypass traditional Silicon Valley VCs entirely and go straight to public markets, but do it in a way that had never been tried before.

In 1995, ResMed became the first medical device company to list on the Australian Securities Exchange (ASX) through a public offering that raised AUD $15 million. But Farrell wasn't done. Nine years later, in 2004, the company completed an initial public offering (IPO) on the New York Stock Exchange, creating a dual-listed structure that gave them access to both Australian and U.S. capital markets. This wasn't just financial engineering—it was a strategic masterstroke that provided currency for acquisitions while maintaining Farrell's control and long-term vision.

The product innovation during this period was relentless. ResMed introduced the AutoSet in 1997, the industry's first auto-titrating CPAP that could automatically adjust pressure based on the patient's needs throughout the night. Think of it as cruise control for breathing—the device would increase pressure when detecting apnea events and decrease it when the airway was stable, dramatically improving comfort. Competitors were still selling fixed-pressure "dumb" devices; ResMed was building intelligent machines that learned from each night's sleep.

The competitive landscape was heating up. Fisher & Paykel, the New Zealand appliance manufacturer, had pivoted into medical devices and was attacking ResMed's mask business with heated humidification technology. Respironics, backed by deep pockets and U.S. market knowledge, was emerging as the primary rival. The battle wasn't just about technology—it was about controlling the channel. Sleep labs were the gatekeepers, diagnosing patients and recommending specific devices. ResMed's strategy was to make sleep specialists partners in innovation, regularly visiting labs, incorporating feedback, and even funding sleep research.

The company's manufacturing footprint expanded globally, with facilities established in Australia, Singapore, France, and the United States. This wasn't just about cost optimization—though Singapore certainly offered advantages there. Each facility specialized in different components: motors in Australia, electronics in Singapore, masks in France, final assembly in the U.S. This distributed model provided supply chain resilience that would prove invaluable during future disruptions.

By 2004, at the time of the NYSE listing, ResMed had grown to approximately $340 million in annual revenue. The company was operating in more than 140 countries worldwide, with particularly strong positions in the U.S., Australia, and emerging European markets. The German and French healthcare systems had begun recognizing and reimbursing for sleep apnea treatment, opening massive new markets for growth.

The distribution strategy evolved from direct sales to a hybrid model. In major markets, ResMed maintained direct relationships with sleep labs and specialists. In smaller markets, they partnered with durable medical equipment (DME) providers who handled patient setup and ongoing support. This created leverage—ResMed could focus on innovation and manufacturing while partners managed the last-mile delivery and patient compliance.

But the real innovation wasn't in the devices themselves—it was in understanding the patient journey. ResMed discovered that nearly 50% of patients abandoned CPAP therapy within the first year, usually due to discomfort or perceived lack of benefit. Rather than accepting this as inevitable, they attacked the problem systematically: lighter masks, quieter motors, better humidification, and crucially, data systems that could track usage and alert providers when patients were struggling. This focus on compliance would become the foundation for their next transformation into digital health.

The IPO proceeds funded an acquisition spree that consolidated the fragmented mask and accessories market. Rather than competing head-to-head with Respironics on core CPAP devices, ResMed bought complementary technologies that improved the overall therapy experience. Each acquisition brought patents, manufacturing expertise, and customer relationships that strengthened their competitive moat. By 2004, ResMed wasn't just a CPAP company—they were building a respiratory therapy platform that would be difficult for any single competitor to replicate.

V. Digital Health Transformation & Cloud Connectivity (2010–2015)

The transformation began with a simple observation: ResMed's CPAP machines were generating gigabytes of sleep data every night—breathing patterns, pressure changes, mask leaks—but most of it was trapped on SD cards that patients rarely brought to appointments. It was like having a goldmine of medical insights locked in millions of bedside tables around the world. The company's next chapter would be about liberating that data and turning it into actionable intelligence.

In 2010, ResMed launched its first wireless-enabled CPAP device, the S9 with wireless connectivity. This wasn't just a feature upgrade—it represented a fundamental reimagining of the business model. Instead of selling machines and hoping patients used them, ResMed could now monitor therapy in real-time, alert providers to compliance issues, and intervene before patients gave up on treatment. The devices became nodes in a vast respiratory health network, streaming data to the cloud every morning.

The development of the AirView platform marked ResMed's entry into software-as-a-service. Clinicians could log into a dashboard and see all their patients' therapy data: who was using their device regularly, who was struggling with mask fit, who might need pressure adjustments. For sleep centers managing thousands of patients, this was revolutionary. Instead of waiting for quarterly appointments to check compliance, they could practice proactive medicine, reaching out to struggling patients within days of detecting problems.

The myAir patient app, launched in 2014, completed the ecosystem. Patients could see their own sleep data, track improvement over time, and receive coaching tips to improve therapy adherence. The app gamified CPAP usage with scores and achievements—seemingly trivial features that actually moved the needle on compliance rates. ResMed discovered that patients who engaged with myAir used their devices an average of one hour more per night than those who didn't.

On March 1, 2013, Peter's son Mick Farrell became the company's new CEO, marking a crucial generational transition. Mick wasn't a typical nepotism hire—he had joined ResMed in 2000, earned his stripes running the Americas business, and had been instrumental in driving the digital transformation. Where Peter was the visionary founder who built the hardware business, Mick saw the future in software and services. His appointment signaled to investors that ResMed was serious about becoming a healthcare technology company, not just a device manufacturer.

The cultural shift under Mick's leadership was profound. ResMed started hiring software engineers and data scientists alongside mechanical engineers. They established innovation labs in San Francisco and Boston to be closer to tech talent. The company that had been built on manufacturing excellence was learning to operate like a Silicon Valley software company—agile development, continuous deployment, A/B testing of features. Old-timers grumbled about "losing their manufacturing DNA," but Mick understood that software was eating the medical device world just as it had eaten every other industry.

The business model implications were staggering. Connected devices created switching costs—once a patient's data was in AirView, moving to a competitor meant losing that history. Providers became locked into ResMed's ecosystem because their workflows were built around the platform. The recurring software revenue streams had 90%+ gross margins compared to 55-60% for devices. Wall Street started to revalue ResMed not as a medical device company trading at 2-3x revenue, but as a connected health platform that deserved SaaS multiples.

By 2015, ResMed had over 5 million cloud-connected devices in the field, generating 3 billion nights of sleep data. They were running one of the largest IoT deployments in healthcare, processing more data than most hospitals. The infrastructure investments were massive—data centers, cybersecurity, HIPAA compliance—but the payoff was clear. ResMed could now prove with hard data that their therapy worked, that connected patients had better outcomes, and that digital engagement improved adherence. Insurance companies loved it because better compliance meant fewer hospitalizations. Providers loved it because it made their practices more efficient. Patients loved it because they could finally see that therapy was working.

The foundation was set for an even bolder transformation. If ResMed could build a platform for managing sleep apnea remotely, why couldn't they do the same for other chronic conditions? Why stop at devices when the real opportunity was in managing population health? The next phase would see ResMed venture far beyond sleep, acquiring software companies that had never built a medical device but understood how to manage complex patient populations at scale.

VI. The SaaS Acquisition Spree: Brightree, HEALTHCAREfirst & MatrixCare (2016–2018)

The Brightree acquisition in April 2016 shocked industry observers. ResMed acquired Brightree for $800 million in cash, with Brightree having net sales of approximately $113 million and EBITDA of about $43 million in calendar year 2015. On paper, paying 7x revenue for a software company that served durable medical equipment providers seemed insane for a device manufacturer. But Mick Farrell saw something others missed: Brightree's software was the operating system for the very DME providers who distributed ResMed's devices. By owning the software layer, ResMed could influence how thousands of providers managed their businesses—and subtly advantage ResMed products in the process.

Brightree wasn't making CPAP machines or masks. They built cloud-based business management software for post-acute care providers—billing systems, inventory management, patient documentation. Boring, essential infrastructure that every DME needed but no one got excited about. Yet this software controlled the entire workflow of how respiratory devices moved from manufacturer to patient. By acquiring Brightree, ResMed wasn't just buying revenue; they were buying strategic position in the value chain.

The MatrixCare deal in 2018 took the strategy even further. ResMed completed its $750 million acquisition of Minnesota-based MatrixCare, a company that provided software to skilled nursing facilities and senior living communities. Again, observers scratched their heads—what did nursing home software have to do with sleep apnea? But Farrell understood that chronic respiratory conditions didn't exist in isolation. The same patients using CPAP devices often cycled through hospitals, skilled nursing facilities, and home care. By stitching together software across these settings, ResMed could follow patients through their entire care journey.

HEALTHCAREfirst, acquired for an undisclosed sum that industry sources pegged around $150 million, added home health and hospice agencies to the portfolio. The acquisitions of Brightree, MatrixCare and HEALTHCAREfirst cost ResMed almost $1.7 billion—a staggering sum for a company that had spent decades carefully shepherding capital. This wasn't incremental evolution; it was a bold bet that the future of medical devices lay not in the devices themselves but in the software ecosystems surrounding them.

The strategic logic was elegant once you understood it. ResMed was building what Farrell called "Software as a Service 2.0"—not just software for software's sake, but software that improved medical outcomes. Each acquisition brought different pieces of the puzzle: Brightree managed equipment and supplies, MatrixCare handled clinical documentation and care coordination, HEALTHCAREfirst dealt with home health billing and compliance. Together, they formed an integrated platform for out-of-hospital care.

The financial engineering was equally sophisticated. These software businesses had 70-80% gross margins versus ResMed's device margins in the 50s. They generated predictable recurring revenue with net retention rates above 100%. Most importantly, they created network effects—the more providers using the platform, the more valuable it became for payers and health systems seeking to coordinate care across settings. ResMed was transitioning from selling products to selling outcomes.

Integration challenges were massive. ResMed had to merge different technology stacks, reconcile competing product roadmaps, and retain engineering talent that had better-paying options at pure software companies. They established a separate Software as a Service division, gave it P&L autonomy, and crucially, kept the acquired management teams in place. Rather than forcing everything into the ResMed way, they let each business maintain its identity while gradually building bridges between platforms.

The market response was initially skeptical. ResMed's stock fell nearly 20% in the months following the Brightree announcement as investors worried about integration risk and dilution to margins. Analysts questioned whether a medical device company had the DNA to run software businesses. The multiple paid for MatrixCare—roughly 6x revenue—seemed rich for a company growing in the mid-teens. Short sellers circled, betting that ResMed was desperately diversifying away from a declining device business.

But the numbers told a different story. By 2018, ResMed's SaaS business was generating over $350 million in annual recurring revenue, growing at 25%+ annually. More importantly, the software was making the device business stronger. Providers using Brightree were more likely to prescribe ResMed devices. MatrixCare facilities had better protocols for managing residents with sleep apnea. The ecosystem was creating competitive advantages that no single-product competitor could match.

The billion-dollar question was whether this would translate to better patient outcomes and sustainable competitive advantages, or whether ResMed had just paid premium prices for mediocre software businesses. The answer would come sooner than anyone expected, when a competitor's catastrophic failure would test whether ResMed's platform strategy could handle unprecedented demand.

VII. The Philips Recall Opportunity & Market Dominance (2021–2024)

On June 14, 2021, Philips Respironics—ResMed's largest competitor with roughly 35% market share—announced one of the most catastrophic recalls in medical device history. The polyester-based polyurethane foam used for sound dampening in millions of CPAP devices was degrading, potentially releasing toxic particles and gases that patients could inhale. The initial recall covered 3.5 million devices; it would eventually expand to over 5 million units globally. For patients dependent on these machines to breathe at night, it was a nightmare. For ResMed, it was an unprecedented opportunity that would test every aspect of their platform strategy.

The significant Philips recall starting in 2021 saw ResMed scaling production and leveraging its robust supply chain to effectively capture substantial market share. But "scaling production" understates the herculean effort required. ResMed had to essentially double their manufacturing capacity in months, not years. Their distributed manufacturing footprint—built for supply chain resilience rather than efficiency—suddenly became their greatest strategic asset.

The Singapore facility went to 24/7 production. The French mask facility added entire new production lines. Most remarkably, ResMed's Sydney operation, which many had written off as an expensive legacy of their Australian origins, proved invaluable. While competitors scrambled to find manufacturing capacity, ResMed could surge production across four time zones, keeping factories running around the clock.

The software infrastructure proved even more crucial. Through AirView, ResMed could identify Philips patients whose devices had been recalled and proactively reach out with replacement options. The Brightree platform allowed DME providers to manage the massive logistics challenge of swapping out millions of devices. MatrixCare helped skilled nursing facilities ensure no resident went without therapy. What could have been chaos became a coordinated response that showcased the power of ResMed's integrated ecosystem.

The financial impact was staggering. ResMed's device revenue grew 35% year-over-year in fiscal 2022, adding over $700 million in incremental revenue. But the real victory was in market share—ResMed captured an estimated 70% of the replacement market, converting millions of Philips users who might never have tried their products otherwise. The switching costs created by their connected ecosystem meant many of these customers would likely stay for life.

The competitive dynamics shifted permanently. Philips, once a formidable rival with the resources of a $40 billion conglomerate behind it, was crippled. They stopped selling new devices in the U.S., faced billions in litigation costs, and saw their sleep and respiratory division's revenue collapse by 40%. Other competitors like Fisher & Paykel and Löwenstein picked up some share, but none had the manufacturing capacity or software infrastructure to capitalize like ResMed did.

ResMed's current market position as the largest CPAP manufacturer globally understates their dominance. Industry estimates suggest they now control 60-70% of the U.S. flow generator market and similar shares in other developed markets. In masks and accessories, where competition remains more fragmented, ResMed still commands 40%+ share. The company that started with hand-built devices in a hospital workshop now produces over 7 million devices annually.

Financial performance reached new heights with growth to $4.7 billion in revenue and S&P 500 inclusion. The S&P 500 inclusion in January 2024 marked ResMed's arrival as a blue-chip healthcare company, triggering billions in passive index buying and cementing their status among institutional investors. The stock price more than doubled from pre-recall levels, pushing market capitalization above $30 billion at its peak.

But success brought new challenges. Regulators scrutinized whether ResMed was exploiting the recall for anti-competitive advantage. Some insurance companies, alarmed by the surge in CPAP prescriptions, tightened reimbursement criteria. Most concerning, the massive influx of new patients strained ResMed's customer service and support infrastructure. Social media filled with complaints about long wait times and device shortages, threatening to tarnish the reputation they'd built over decades.

Management's response revealed the maturity of their operation. Rather than maximize short-term profits, they invested heavily in customer support, hiring thousands of representatives and expanding training programs. They maintained disciplined pricing, resisting the temptation to gouge despite overwhelming demand. Most strategically, they used the windfall profits to accelerate R&D and software development rather than return it all to shareholders. The message was clear: ResMed was playing for permanent market leadership, not quarterly earnings beats.

By 2024, the acute phase of the recall opportunity had passed, but the structural changes appeared permanent. ResMed had converted a one-time crisis into lasting competitive advantage through superior execution, integrated platform capabilities, and strategic restraint. The question now was what to do with their commanding position—coast on their dominance or continue pushing into new frontiers of digital health and artificial intelligence.

VIII. Modern Era: AI, Digital Health & The Future (2020s–Today)

The COVID-19 pandemic initially looked like a nightmare for ResMed. Elective sleep studies stopped, new diagnoses plummeted, and hospitals commandeered every ventilator they could find. But ResMed's response showcased organizational agility that few 30-year-old companies possess. Within weeks, they had redesigned their bilevel devices to function as emergency ventilators, scaled production of their AirCurve devices for non-invasive ventilation, and deployed cloud monitoring to help overwhelmed hospitals manage respiratory patients remotely.

The pandemic accelerated digital health adoption by years. Suddenly, remote patient monitoring wasn't a nice-to-have—it was essential. ResMed's cloud-connected devices allowed physicians to manage CPAP patients without in-person visits. The myAir app became a lifeline for isolated patients seeking to understand their therapy. Insurance companies, desperate to avoid hospital admissions, embraced home sleep testing and remote titration protocols that ResMed had been advocating for years.

The evolution of ResMed's software business during this period was remarkable. The SaaS division grew to over $600 million in annual recurring revenue by 2024, with margins approaching 80%. But more interesting than the financials was the strategic evolution. ResMed began positioning itself not as a sleep company that happened to have software, but as a digital health platform that happened to start with sleep.

The AI and machine learning capabilities being deployed were genuinely innovative. ResMed's algorithms could now predict with 85% accuracy which patients would abandon therapy within 30 days, allowing preemptive interventions. The AirView platform incorporated natural language processing to analyze clinical notes and identify undiagnosed sleep apnea patients in electronic health records. Most ambitiously, they were developing predictive models that could forecast cardiovascular events based on CPAP usage patterns—moving from treating sleep apnea to preventing its deadly complications.

Competition emerged from unexpected directions. Apple Watch's sleep tracking and blood oxygen monitoring capabilities raised questions about whether consumer wearables would eventually diagnose sleep disorders. Startup companies like Eight Sleep and Dreem promised to solve sleep problems without prescriptions or insurance. Amazon's acquisition of One Medical and push into healthcare suggested that Big Tech saw opportunity in the fragmented sleep medicine market.

ResMed's response was nuanced. Rather than dismiss consumer devices as toys, they launched a venture fund to invest in digital health startups. They partnered with consumer wearable companies to create referral pathways from detection to diagnosis to treatment. The strategy acknowledged that the future of sleep medicine wouldn't be controlled by any single company but would require an ecosystem approach.

The out-of-hospital care strategy expanded beyond sleep and respiratory. ResMed's software platforms now managed patients with congestive heart failure, COPD, and diabetes—chronic conditions that often coexisted with sleep apnea. The MatrixCare acquisition looked prescient as the senior living industry embraced value-based care models that rewarded providers for keeping residents healthy rather than treating them when sick.

Population health management became the organizing principle. ResMed wasn't just selling devices or software; they were selling the capability to manage complex chronic conditions at scale. Health systems could use ResMed's platforms to identify at-risk patients, coordinate care across settings, optimize resource allocation, and demonstrate value to payers. The business model was evolving from fee-for-service to risk-sharing arrangements where ResMed's compensation was tied to patient outcomes.

The international expansion accelerated, particularly in Asia where sleep apnea was massively underdiagnosed. China alone represented a potential market of 100 million untreated patients. ResMed established local manufacturing, partnered with regional distributors, and critically, developed lower-cost devices specifically for emerging markets. The AirMini, a travel-sized CPAP that connected to smartphones, became a breakthrough product in markets where traditional devices were too expensive or cumbersome.

By 2024, ResMed's transformation was complete. They had evolved from a medical device manufacturer to a connected health platform, from selling products to managing populations, from treating sleep apnea to preventing its complications. The company that started with a vacuum cleaner motor in a Sydney hospital had become one of the most sophisticated digital health companies in the world, processing billions of hours of sleep data and managing millions of patients across the care continuum.

IX. Playbook: Business & Investing Lessons

The power of founder-led innovation shines through ResMed's history, but it's not the typical Silicon Valley story of disruption. Peter Farrell didn't break things—he built them methodically over decades. His 24-year tenure as CEO (1989-2013) provided consistency that allowed long-term bets to pay off. When developing the first AutoSet device took five years and nearly bankrupted the company, Farrell persisted. When investors pushed for quick returns, he invested in R&D. This patient capital approach—enabled by dual-class shares that gave Farrell supervoting rights—created compound advantages that growth-at-all-costs competitors couldn't match.

Building a patent moat with over 6,000 granted patents represents one of the most successful IP strategies in medical devices. But the brilliance wasn't in patenting the big idea—remember, Sullivan's original CPAP patent was invalidated. Instead, ResMed patented thousands of incremental innovations: mask cushion geometries, motor control algorithms, data transmission protocols. Each patent was individually minor but collectively impregnable. Competitors could copy the concept of CPAP, but they couldn't copy the accumulated decades of refinements that made ResMed's devices superior.

The platform economics of devices plus software plus services created multiple reinforcing moats. Hardware sales drove software adoption which improved patient outcomes which increased device prescriptions. The $1.7 billion spent on software acquisitions looked expensive initially but created switching costs worth far more. Once a provider's entire workflow ran on ResMed software, changing device suppliers meant disrupting operations. Once a patient's years of sleep data lived in myAir, switching meant losing their history. Once payers integrated with AirView for compliance monitoring, they demanded other manufacturers match ResMed's capabilities.

Managing through competitive disruptions—particularly the Philips recall—revealed organizational capabilities that financial statements don't capture. ResMed could have extracted maximum value during the shortage, raising prices and prioritizing high-margin markets. Instead, they maintained price discipline, served all markets equally, and invested windfall profits in long-term capabilities. This restraint built trust with customers and regulators that will pay dividends for decades. When the next crisis hits—and in medical devices, there's always a next crisis—ResMed will be the partner of choice.

The recurring revenue model in medical devices deserves special attention. Most device companies face lumpy capital purchase cycles and commodity pricing pressure. ResMed transformed one-time device sales into ongoing service relationships. Between rental programs, software subscriptions, mask replacements, and value-based contracts, over 70% of revenue is now recurring or consumable. This predictability allows higher R&D investment, better manufacturing planning, and most importantly, premium valuations from investors who prize stable cash flows.

Capital allocation evolved from pure organic investment to strategic M&A, but always with clear strategic logic. Early acquisitions were technology tuck-ins—buying mask designs or motor technologies. The middle period focused on geographic expansion—acquiring distributors to enter new markets. The recent SaaS buying spree targeted platform capabilities. Notably absent: diversification for its own sake, financial engineering, or empire building. Every dollar spent—whether on R&D, acquisitions, or dividends—aligned with strengthening the core respiratory franchise.

The lesson on market creation versus market capture is subtle but crucial. ResMed didn't invent CPAP, but they created the market for home sleep therapy. They funded sleep labs, trained physicians, lobbied for insurance coverage, and educated patients. This market development took decades and billions in investment. But once established, the barriers to entry became enormous. New entrants faced not just ResMed's technology but an entire ecosystem built around their standards. The investment in market creation became the ultimate competitive moat.

X. Analysis & Bear vs. Bull Case

The Bull Case: Structural Growth for Decades

The undiagnosed sleep apnea opportunity remains massive. Of the estimated 1 billion people globally with sleep apnea, fewer than 20% are diagnosed, and fewer than 10% are treated. In the U.S., despite decades of market development, penetration remains under 30%. Every percentage point of increased diagnosis rates represents hundreds of millions in revenue opportunity. Demographics are a powerful tailwind—sleep apnea prevalence increases with age and obesity, both rising globally.

The software transformation is still early. At $600 million in annual recurring revenue, ResMed's SaaS business could triple as healthcare digitization accelerates. The 80% gross margins and 100%+ net retention rates create a compounding machine that could be worth more than the device business within a decade. As value-based care models proliferate, ResMed's ability to manage populations and demonstrate outcomes becomes increasingly valuable.

Geographic expansion, particularly in Asia, could surprise to the upside. China's middle class is developing Western health conditions—and healthcare expectations. India's insurance coverage is expanding rapidly. Japan's aging population desperately needs home care solutions. ResMed's early investments in these markets position them to capture disproportionate share as awareness and reimbursement improve.

The Bear Case: Disruption from Multiple Angles

GLP-1 drugs like Ozempic and Wegovy represent an existential threat that's hard to quantify. These medications cause significant weight loss, and obesity is the primary driver of sleep apnea. Early studies suggest 40-50% of patients on GLP-1s no longer need CPAP therapy. If these drugs become first-line therapy for obesity—which seems likely given their cardiovascular benefits—ResMed's addressable market could shrink dramatically. Management argues that increased diagnosis will offset therapy discontinuation, but that assumes GLP-1 adoption remains limited.

Philips is wounded but not dead. They're settling lawsuits, redesigning products, and will eventually return to market with a vengeance. Their parent company has deep pockets and strong hospital relationships. When they return—likely in 2025-2026—pricing pressure will intensify. ResMed's 60%+ market share is unsustainably high; mean reversion is inevitable.

Consumer technology disruption looms larger each year. Apple, Google, and Amazon are circling healthcare. The Apple Watch can already detect sleep apnea indicators. What happens when iPhone can diagnose sleep disorders and recommend treatment? When Amazon starts shipping generic CPAP devices with next-day delivery? ResMed's moat is regulatory and reimbursement complexity, but those barriers are eroding as digital health companies mature.

Reimbursement pressure never stops. Insurance companies are tightening criteria, demanding more documentation, and pushing lower-cost alternatives. Medicare Advantage plans are gaining share with narrower networks that exclude premium products. International markets are adopting reference pricing that caps ResMed's pricing power. The golden age of 5-7% annual price increases is ending.

Financial Metrics Analysis

Trading at 25x forward earnings and 5.5x revenue, ResMed commands premium multiples reflecting market dominance and growth potential. The 55% gross margins and 24% EBITDA margins are exceptional for medical devices but below pure software comparables. Return on invested capital consistently exceeds 15%, validating the acquisition strategy. Free cash flow conversion approaches 100% of net income, funding both growth investments and shareholder returns.

The balance sheet is conservative with net debt/EBITDA under 1x despite the acquisition spree. This provides flexibility for opportunistic M&A or aggressive share buybacks if the stock weakens. The dividend yield of 1% seems low, but the payout ratio under 30% preserves capital for growth investments.

The Verdict

ResMed sits at a fascinating inflection point. The bear case centers on disruption—from drugs, technology, and competition. The bull case rests on execution—continued penetration of underpenetrated markets, successful software scaling, and platform advantages. History suggests betting against ResMed is dangerous. They've navigated technology transitions, competitive threats, and regulatory changes for 35 years. But history also suggests that dominant market positions attract disruption. The next five years will determine whether ResMed's platform strategy creates insurmountable advantages or merely delays inevitable disruption.

XI. Epilogue & "If We Were CEOs"

If we were running ResMed, the strategic priorities would be clear but the execution would be complex. First, we'd accelerate the shift to artificial intelligence and predictive diagnostics. ResMed sits on one of the world's largest databases of sleep information—billions of nights of physiological data linked to clinical outcomes. This data moat could enable AI models that predict not just sleep apnea but cardiovascular disease, diabetes complications, even neurodegenerative disorders. The company that can tell a 45-year-old that their sleep patterns indicate 70% probability of heart disease within five years owns the future of preventive medicine.

The consumer versus medical device strategy needs resolution. ResMed has watched from the sidelines as Eight Sleep raised venture capital at unicorn valuations, as Oura rings became status symbols, as Apple pushed into health tracking. The traditional response would be to launch a consumer brand, but that risks channel conflict and regulatory complications. Instead, we'd create a "powered by ResMed" white-label platform that lets consumer brands handle marketing while ResMed provides the medical-grade backend. Imagine Peloton sleep coaches powered by ResMed algorithms, or Hilton hotels offering ResMed-certified sleep optimization suites.

International expansion, particularly in Asia, deserves more aggressive investment. The current strategy of premium products for wealthy markets misses the massive middle-market opportunity. We'd develop a $200 "good enough" CPAP specifically for emerging markets—basic functionality, smartphone-based controls, cloud connectivity for remote monitoring. Partner with local manufacturers for production, governments for distribution, and telecommunications companies for connectivity. The profit margins would be lower, but the volume opportunity and first-mover advantages in markets with 2 billion potential patients justify the investment.

The software platform needs to expand beyond healthcare providers to include patients as direct customers. Currently, ResMed gives away the myAir app to drive device compliance. We'd create a premium subscription tier—$20/month for advanced analytics, personalized coaching, integration with other health devices, and telehealth consultations with sleep specialists. With 10 million active device users, even 20% conversion would generate $500 million in high-margin recurring revenue while improving patient outcomes.

The biggest surprise from studying ResMed's history is how many times they could have settled for being a very good niche company. After Sullivan's invention, they could have remained an Australian medical device manufacturer. After the IPO, they could have focused solely on sleep apnea. After establishing market leadership, they could have harvested profits rather than investing in software. At each junction, they chose the harder path of expansion and innovation.

The second surprise is how much of ResMed's success came from focusing on the entire patient journey rather than just the device. Most medical device companies obsess over features and specifications. ResMed obsessed over why patients stopped therapy and how providers managed care. This systems thinking—understanding that a CPAP machine is useless if patients won't wear it—drove innovations that competitors dismissed as marginal but patients found essential.

Looking forward, ResMed faces the classic innovator's dilemma. They've built a dominant position in traditional CPAP therapy, but that very success makes it harder to embrace potentially cannibalizing innovations. Will they be the ones to develop an implantable device that makes CPAP obsolete? Will they pivot aggressively if pharmaceutical solutions prove superior? Will they recognize if consumer devices become good enough for most patients? The answer to these questions will determine whether ResMed's next 35 years match the success of its first 35.

The Colin Sullivan story that began this journey—a desperate researcher hand-building devices to save patients from tracheotomies—feels almost quaint now. Today's ResMed operates at a scale Sullivan probably never imagined: billions in revenue, millions of patients, terabytes of data. But the core mission remains unchanged: helping people breathe so they can sleep so they can live. In a world of apps and algorithms, that physical, fundamental human need grounds the company in a way that pure software never could. The challenge and opportunity for ResMed is to leverage their digital capabilities while never forgetting that at the end of every data stream is a person trying to get a good night's sleep.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube