Pentair: From Hot Air Balloons to Global Water Empire

I. Introduction: The Unlikely Water Champion

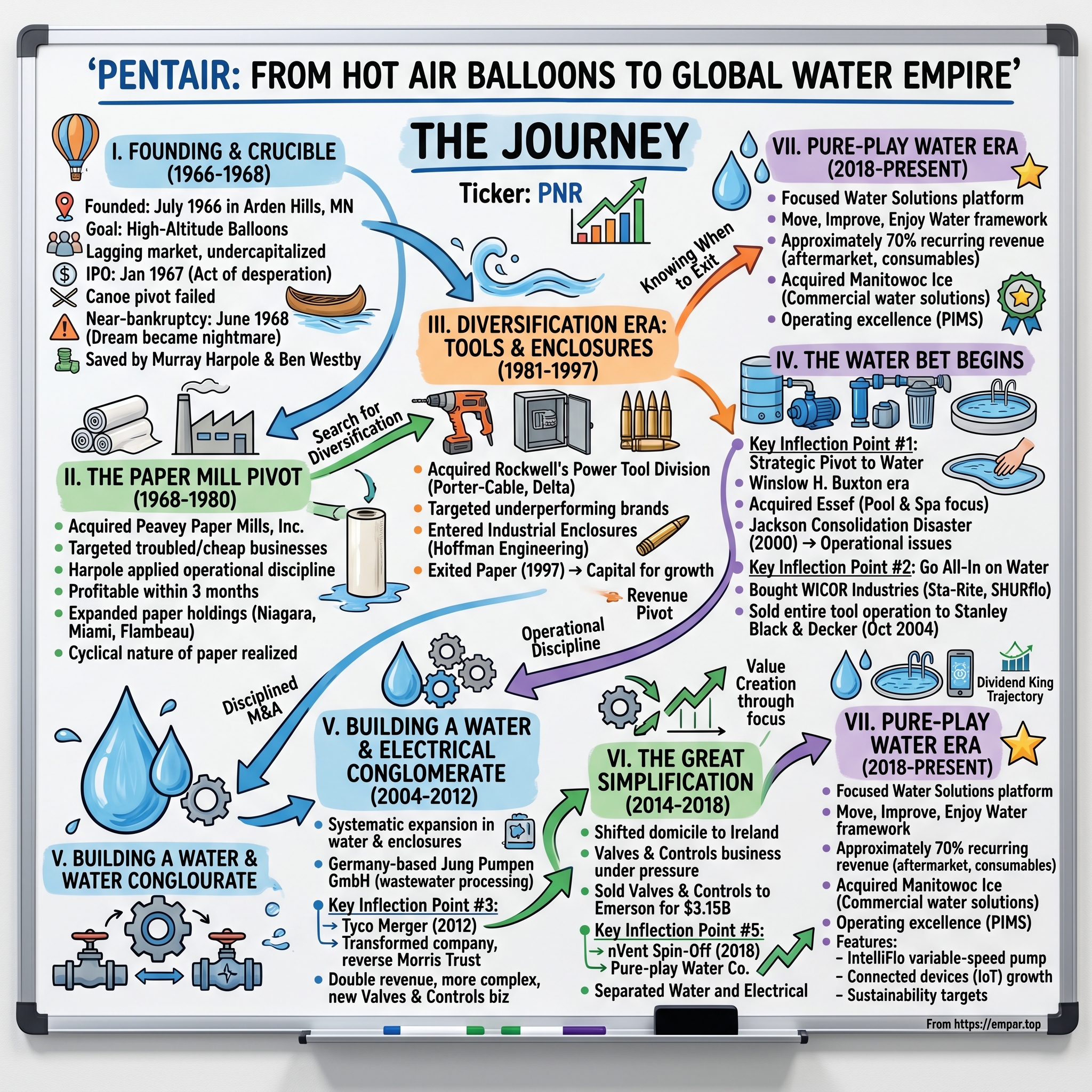

Picture a mid-1960s Minnesota winter: five former Litton Industries employees—three engineers, a foreman, and a salesman—gathered in Arden Hills, pooling their modest savings to chase an unusual dream. They wanted to build high-altitude research balloons. The name they chose, Pentair, was almost comically literal: "penta" for the five founders, "air" for their product. Pentair was founded in July 1966 in Arden Hills, Minnesota, as a five-person partnership with the purpose of manufacturing high-altitude research balloons. The company founders—three engineers, a foreman, and a salesman—were all former employees of a local branch of Litton Industries.

Nearly six decades later, Pentair had revenue in 2024 of approximately $4.1 billion with approximately 9,750 global employees serving customers in more than 150 countries. The company that once dreamed of filling the sky with balloons now helps the world move, improve, and enjoy its most essential resource: water.

How did a company that started with hot air balloons, pivoted to paper mills, dabbled in power tools, flirted with ammunition, and experimented with industrial enclosures become a pure-play water solutions powerhouse? The answer lies in one of the most remarkable examples of corporate reinvention through strategic M&A in American industrial history.

Pentair plc (PNR) is an American water treatment company incorporated in Ireland with tax residency in UK, with its main U.S. office in Golden Valley, Minnesota. This unusual corporate structure—American operations, Irish incorporation, British tax residency—is itself a testament to the company's decades of strategic maneuvering. Its current market cap is $18.2B with 164M shares. As of 30-Sep-2025, Pentair has a trailing 12-month revenue of $4.13B.

The themes that define Pentair's journey read like a masterclass in industrial transformation: - Disciplined M&A: Buying underperforming businesses at bargain prices and executing turnarounds - Knowing when to exit: Selling paper at peak, divesting tools to fund water, spinning off electrical when focus demanded - The power of secular trends: Betting big on water at a time when most investors dismissed it as too boring - The recurring revenue pivot: Transforming from a cyclical industrial conglomerate to a business model where roughly 70% of revenue comes from aftermarket and consumables

What follows is the story of how a company defied near-bankruptcy within two years of its founding, built and shed multiple identities, and ultimately emerged as a focused global leader in one of the 21st century's most critical sectors.

II. The Unlikely Origin Story (1966-1968): When Hot Air Became Fiscal Reality

The founding of Pentair reads less like a corporate origin story and more like a cautionary tale that somehow ended well. The partners incorporated as Pentair Industries, Inc. in August and completed an initial public offering in January 1967 to sustain their seriously undercapitalized business. Further complicating matters at the time was the lagging market for inflatables.

Going public within months of incorporating wasn't a sign of confidence—it was an act of desperation. The five founders had pooled their modest savings but lacked the capital to actually build a sustainable business. The market for high-altitude research balloons, it turned out, was considerably smaller than they had hoped.

Harpole, one of Pentair's five founding partners, started the company in 1966 to manufacture research balloons. Harpole was named Pentair's first Chairman and CEO that year and remained in this position for 15 years and served another 5 years as Chairman, ultimately retiring from the board in 1991.

Murray Harpole emerged as the pivotal figure in these early years. An Iowa State engineering graduate, Harpole had the practical sensibility to recognize when a business model wasn't working—and the stubbornness to refuse to give up on the company itself.

Following the guidance of cofounder and acting manager Murray Harpole, the company decided to purchase a neighboring, virtually bankrupt business for the small sum of $14,500. With some modest engineering applications this new venture, the American Thermo-Vac Company, promised at least one saleable product: vacuum-formed, high-quality canoes.

From research balloons to canoes. The pivot seems almost comical in retrospect, but it illustrates a trait that would define Pentair for decades: pragmatic opportunism. If one product didn't work, find another. The $14,500 acquisition of American Thermo-Vac represented Pentair's first foray into the M&A strategy that would ultimately define its corporate identity.

But the canoe business proved no more successful than balloons. "By June, 1968, before Pentair was two years old, the corporate dream had become a nightmare. The company had no product to speak of, it was nearly out of money, one cofounder had died and three others had abandoned the venture." What sustained the company was Harpole's pledge to commit himself entirely to the business for at least five years—this and the entry of high-risk investor Ben Westby.

This moment—June 1968—represents the true crucible of Pentair's corporate character. Four of the five founders were gone. The company had burned through its IPO proceeds chasing failed ventures. Most companies in this position simply disappear, their brief existence relegated to footnotes in SEC archives.

What saved Pentair was Harpole's personal commitment and the arrival of Ben Westby, a high-risk investor willing to bet on turnarounds. Although Westby did not formally join the company until May 1968, he had been in close contact with Harpole for some time and had accompanied the founder on a business trip to Wisconsin, to consider the purchase of then debt-ridden, privately owned Peavey Paper Mills, Inc.

The Wisconsin trip would change everything. Harpole and Westby weren't looking at paper mills because they had expertise in the paper industry. They were looking because Peavey was cheap, troubled, and available—the same characteristics that would define Pentair's acquisition targets for decades to come.

III. The Paper Mill Pivot & Building the Acquisition Playbook (1968-1980)

Although Westby did not formally join the company until May 1968, he had been in close contact with Harpole for some time and had accompanied the founder on a business trip to Wisconsin, to consider the purchase of then debt-ridden, privately owned Peavey Paper Mills, Inc. A manufacturer of absorbent tissue paper, Peavey was acquired in June and became Pentair's first wholly owned subsidiary.

The terms of the Peavey deal were extraordinary. First was the low cost: $10,000 down, $20,000 due in one year, and an additional five percent of after-tax profits for the first five years. Second, and most importantly, was the paper mill's potential: annual sales of $4 million even in its current state of disrepair and mismanagement. Of course, with this ostensibly one-of-a-kind deal came a particularly painful and hidden price: Peavey's $1.5 million in debt.

The hidden debt was a brutal lesson in due diligence that Harpole would never forget. But it also illustrated something important: even a troubled business with $1.5 million in debt could be worth acquiring if the underlying operations had potential. Despite this preventable surprise, a lesson in cautious and thorough research, the acquisition was made profitable within three months due primarily to Harpole's management and labor-negotiation skills.

Three months to profitability. This wasn't financial engineering or creative accounting—it was operational excellence. Harpole brought discipline to a business that had been poorly managed, and the results were immediate.

The Peavey acquisition established what would become Pentair's distinctive acquisition playbook: 1. Target troubled businesses available at bargain prices 2. Look for operational upside that previous management had failed to capture 3. Implement management and capital improvements rapidly 4. Use cash flow from stabilized acquisitions to fund additional growth

The company expanded its paper holdings systematically. Company shifts focus to paper industry through purchase of Peavey Paper Mills, Inc. 1972 Niagara of Wisconsin Paper Corporation is acquired. Miami Paper followed in 1974, and Flambeau Paper Corporation in 1978.

According to Harpole, whose Living the American Dream recounts the corporation's history, he and Nugent "had to be successful on their first venture because the investment community was skeptical of our ability to expand beyond paper." The initial goal was for a company with annual sales of $25 to $100 million, preferably floundering and consequently available at a bargain price.

By the late 1970s, Pentair had successfully transformed itself from a failed balloon manufacturer into a profitable regional paper company. But Harpole and his team recognized a fundamental problem: the paper industry was capital-intensive and cyclical. Every time the economy softened, paper prices collapsed, and maintaining aging manufacturing facilities required continuous reinvestment.

The search for diversification had begun—not to escape paper entirely, but to create a portfolio that would smooth out the earnings volatility. Unfortunately, the realization of the goal was postponed, largely due to a time-consuming battle against a takeover threat by Steak and Ale founder Peter Wray, an attempt that ended only after Pentair agreed to a $4.5 million settlement in early 1981. By the middle of that year Pentair had researched and considered more than 125 manufacturers before deciding in October to acquire Porter-Cable Corporation.

The Peter Wray takeover attempt is a fascinating footnote—the founder of Steak and Ale restaurants attempting a hostile acquisition of a Minnesota paper company. The $4.5 million settlement was painful for a company of Pentair's size, but it bought time for the management team to execute their diversification strategy.

Reviewing 125 potential acquisitions before selecting one demonstrates the discipline that Harpole had instilled. This wasn't opportunistic deal-making; it was systematic portfolio construction.

IV. The Diversification Era: Tools, Enclosures, & More (1981-1997)

The Tools Play

In 1981, Pentair acquired Rockwell International's power hand tool factory from its Power Tool Division. Rockwell had purchased Porter-Cable in 1960 and merged it into the Power Tool Division but kept manufacturing in a separate facility. The Porter-Cable name had been retired in 1965 but Pentair had not licensed the Rockwell name, so the Porter-Cable name was revived.

The Porter-Cable acquisition represented a significant strategic departure. Power tools operated in entirely different markets from tissue paper—different customers, different distribution channels, different competitive dynamics. But the fundamental playbook remained the same: buy an underperforming asset, apply management discipline, and execute a turnaround.

Porter-Cable had a storied history dating to 1906 Syracuse, New York, where the company pioneered innovations like the portable belt sander and helical-drive circular saw. Under Rockwell's ownership, the brand had been diluted through lower-quality products and lost its premium positioning. Pentair saw an opportunity to restore the brand to its professional roots.

In 1984 Pentair purchased the remains of the Power Tool Division from Rockwell. This consisted chiefly of the Delta line of shop tools and marked Rockwell's exit from the tool business.

The Delta acquisition gave Pentair a dominant position in professional woodworking equipment—table saws, drill presses, jointers, and planers. Combined with Porter-Cable's hand tools, Pentair now controlled two of the most respected names in the professional tool market.

The Enclosures Entry

In 1988, Pentair agreed to acquire FC Holdings Inc., the holding company for Federal Cartridge and Hoffman Engineering, for $175 million in cash and the assumption of debt. Pentair would not hold Federal Cartridge for a long time, but the purchase of Hoffman Engineering was the start of a prosperous era of enclosures manufacturing for Pentair.

The FC Holdings deal illustrates another key element of the Pentair playbook: acquiring holding companies with multiple businesses, retaining what fits the long-term strategy, and divesting what doesn't. Federal Cartridge made ammunition—a business with little strategic connection to Pentair's other operations. Hoffman Engineering made industrial enclosures—metal boxes and cabinets that protect electrical and electronic equipment.

It's easy to underestimate the enclosures business. Metal boxes don't generate headlines. But they're essential to every industrial operation, every data center, every telecommunications installation. And critically, they generate recurring revenue through accessories, modifications, and replacement.

Exiting Paper

In August 1997, Pentair acquired the General Signal Pump Group. Pentair sold off its papermaking business to Consolidated Papers Inc. in 1997. While paper had been the backbone of Pentair's business it only amounted to about 10% of their revenue at the time of the sale.

The 1997 paper divestiture marked a profound strategic shift. Paper had been Pentair's original turnaround success, the business that saved the company from its failed balloon and canoe ventures. For three decades, paper mills had provided the cash flow that funded diversification.

But by 1997, paper had become a drag on growth. Capital requirements remained high, commodity price volatility created earnings unpredictability, and environmental regulations increased compliance costs. Most importantly, paper contributed only 10% of revenue but consumed disproportionate management attention.

The sale to Consolidated Papers freed capital and management bandwidth for higher-growth opportunities. It also sent a signal to investors: Pentair was willing to exit legacy businesses when the strategic logic demanded it.

V. The Water Bet Begins: The Buxton Era (1997-2004)

Key Inflection Point #1: The Strategic Pivot to Water

In 1999 under chairman, president, and chief executive officer, Winslow H. Buxton, Pentair made a series of acquisitions. In April 1999, PNR purchased Essef, the global leader in the manufacture of composite water tanks, pumps, filters, and other water equipment used in pools and spas, for the cash-equivalent price of approximately $312 million.

Winslow Buxton's tenure as CEO marked the decisive pivot toward water. The Essef acquisition wasn't Pentair's first foray into water-related products—the General Signal Pump Group acquisition in 1997 had already established a beachhead. But Essef represented a commitment to scale.

Essef brought expertise in pool and spa equipment, composite pressure vessels, and residential water filtration. The deal gave Pentair access to markets that were growing steadily, driven by demographic trends (suburban sprawl, rising homeownership) and increasing consumer attention to water quality.

In August 1999, Pentair bought the DeVilbiss Air Power Company for $460 million in cash. DeVilbiss makes air compressors, pressure washers and generators, which complemented Pentair's professional Pneumatics tools that were powered by air compressors such as DeWalt and Porter-Cable.

The DeVilbiss acquisition demonstrated that Pentair hadn't yet fully committed to water. Air compressors and generators complemented the tools business, suggesting management still saw professional equipment as a core growth vector.

The Jackson Disaster

The new facility came online in February 2000 and was an immediate disaster. The decade started extremely poorly for Pentair. The botched opening of its new corporate office and distribution center in Jackson caused an immediate drop in revenue as the shipping facility encountered numerous issues.

In 2000, Porter-Cable consolidated with sister company Delta Machinery, the latter moving its headquarters and distribution center from Pittsburgh, Pennsylvania to Jackson, Tennessee. The same year, Pentair acquired DeVilbiss Air Power Company.

The Jackson consolidation was supposed to generate synergies by combining Porter-Cable and Delta operations under one roof. Instead, it nearly destroyed both brands. Orders shipped late, arrived with incorrect products, or failed to arrive at all. Customer complaints surged. Returns overwhelmed the system.

It took almost three years to sort out the mess and return the Delta and Porter-Cable lines to profitability. This caused Pentair to further review its holdings and look at ways to cut costs. It expanded its production in Taiwan and started to negotiate with the union of its Delta manufacturing facility to reduce payroll.

The Jackson disaster serves as a cautionary tale about integration execution. Strategic logic—consolidating operations to reduce overhead—collided with operational reality: complex supply chains, different product lines, and systems that couldn't communicate effectively.

The episode forced a reckoning. If Pentair couldn't efficiently manage a tools consolidation, should tools remain a core business?

Key Inflection Point #2: Exiting Tools, Going All-In on Water

In July 2004, Pentair bought WICOR Industries, the former water systems subsidiary of Wisconsin Energy, for $850 million. WICOR made water pumps, filters, and pool equipment components under the Sta-Rite, SHURflo, and Hypro brands.

The WICOR acquisition was transformative. "The WICOR acquisition will transform Pentair into a diversified company defined largely by a $2 billion Water Technologies business," said Pentair Chairman and Chief Executive Officer, Randall J. Hogan. "Not only do we anticipate creating a significant water and wastewater systems business having some $900 million in sales, but we will also be operating a global pool and spa equipment business with revenues of roughly $600 million."

Sta-Rite, the crown jewel of WICOR, traced its history to 1934 Wisconsin—a legacy brand with deep distribution relationships and recognized quality. Combined with Essef's products, Pentair now controlled a comprehensive portfolio spanning residential wells, pool equipment, water filtration, and agricultural pumps.

To help offset this purchase it sold its entire tool operation to Stanley Black & Decker that October. This marked Pentair's exit from the tool business.

The tools sale to Black & Decker for approximately $775 million freed capital to absorb the WICOR debt and signaled the definitive end of Pentair's diversified industrial era. Porter-Cable, Delta, DeVilbiss—brands that had defined Pentair for two decades—were gone.

The logic was clear: water markets offered better growth characteristics than tools. Residential water treatment benefited from increasing concerns about water quality. Pool equipment served an installed base of millions of American homes with pools requiring ongoing maintenance. Agricultural and industrial water applications were growing globally.

VI. Building a Water & Electrical Conglomerate (2004-2012)

With tools divested and water established as the growth engine, Pentair entered an era of systematic expansion in both water and its remaining industrial business—enclosures and thermal management.

In 2005, Pentair bought some of the assets of APW for $144 million, including McLean Thermal Management, Aspen Motion Technologies, and Electronic Solutions, all of which provide thermal management products and integration services to the telecom, medical, and security industries. This broadened Pentair's technical products line to include markets outside of the traditional electrical and electronics businesses.

In 2006, Pentair purchased Germany-based Jung Pumpen GmbH, which makes pumps and other products for wastewater processing.

The dual-track strategy made sense on paper: water and technical products operated in different cycles, served different customers, and provided diversification. But investors increasingly questioned whether the conglomerate structure created or destroyed value.

Key Inflection Point #3: The Tyco Merger (2012)

Pentair, Inc. and Tyco International Ltd. announced a definitive agreement to combine Tyco's Flow Control business with Pentair in a tax-free, all-stock merger. The transaction values Tyco Flow at approximately $4.9 billion, including assumed net debt and minority interest.

This was Pentair's largest deal by far—a "reverse Morris Trust" transaction that would more than double the company's revenue. Upon completion of the transaction, which has been unanimously approved by the boards of both companies, Tyco shareholders will own approximately 52.5% of the combined company and Pentair shareholders will own approximately 47.5%. The combination will bring together complementary leaders in water and fluid solutions, valves and controls, and equipment protection products to create a premier industrial growth company.

The estimated $10-billion merger of Pentair Inc. and the Flow Control business of Tyco International Ltd. is completed, now forming Pentair Ltd. The new company is described as a global manufacturer of "water and fluid solutions, valves and controls, equipment protection and thermal management products."

The combined company will be incorporated in Switzerland, where Tyco is currently incorporated, with main U.S. offices remaining in Minneapolis, Minn. where Pentair is based. Following completion of the transaction, the new Pentair is expected to have approximately 30,000 employees worldwide.

The Tyco merger transformed Pentair into a very different company—larger, more global, and significantly more complex. The Valves & Controls business brought exposure to oil and gas, petrochemical, and power generation markets. These were cyclical industries with different dynamics than residential water or pool equipment.

CEO Randall Hogan, who had led Pentair since 2001, championed the deal as creating scale in attractive end markets. The combined company would have diversified revenue streams and cross-selling opportunities.

But the marriage of water solutions with industrial valves created inherent tensions. The businesses served different customers, operated at different margin structures, and faced different competitive dynamics.

VII. The Great Simplification: Divestitures & the nVent Spin-Off (2014-2018)

Tax Inversion & Valves Sale

PNR was reorganized in 2014, shifting the corporate domicile from Switzerland to Ireland.

The Switzerland-to-Ireland redomiciliation was part of a broader corporate restructuring driven by tax efficiency considerations. Ireland offered advantageous tax treatment while maintaining European Union membership and treaty access.

But the bigger strategic question remained: did the post-Tyco portfolio make sense?

Emerson (NYSE: EMR) today announced it has signed an agreement to purchase the Valves & Controls business of Pentair (NYSE: PNR) for $3.15 billion.

The Valves & Controls divestiture acknowledged what had become apparent: the business didn't fit. Oil and gas exposure created earnings volatility that investors punished. The integration synergies that justified the Tyco merger had proven elusive.

Headquartered in Switzerland, the Pentair Valves & Controls business had sales of $1.8 billion in 2015 and almost 7,500 employees worldwide. Pentair acquired the Valves & Control business in 2012 through its all-stock merger with the flow control business of Tyco International Ltd. The divestiture will allow Pentair to focus on its priorities in water quality and availability, equipment and building protection, industrial and process efficiency, and food and beverage processing.

Sales in Pentair's valves and controls business fell 23% last year to $1.8 billion as the price of oil declined.

The timing was brutal. Pentair had acquired Valves & Controls near peak oil prices and sold it during a collapse. But sometimes selling at the wrong price is better than holding the wrong asset.

Key Inflection Point #5: The nVent Spin-Off (2018)

With Valves & Controls gone, Pentair still operated two distinct businesses: water solutions and electrical (enclosures, thermal management, and electrical infrastructure). The question became whether these belonged together.

Pentair plc (NYSE: PNR) ("Pentair") today announced its board of directors has approved the previously announced spin-off of its Electrical business. The transaction will result in two independent, publicly traded companies: Pentair plc and nVent Electric plc ("nVent").

"We have built two strong, high-performing businesses with the operating acumen and culture to thrive as two independent companies," said Randall J. Hogan, Pentair Chairman and Chief Executive Officer. "Separating Water and Electrical to create two pure-play companies is the next logical step in the evolution of Pentair and is consistent with our strategy to continually enhance shareholder value."

On April 30, 2018, Pentair plc completed the separation and distribution of its Electrical business to nVent Electric plc. In connection with this separation and distribution, Pentair's shareholders received nVent ordinary shares on a pro rata basis.

Pentair plc (NYSE:PNR) completed the spin-off of nVent Electric plc (NYSE:NVT) for $3.8 billion on April 30, 2018.

"And there is no common [sales] channel and no common customers" between the two, said Hogan, who will retire as CEO Monday and become chairman of nVent. When Pentair and nVent officially split Monday, Pentair will become a company with annual revenue of $2.8 billion.

The nVent spin-off completed Pentair's transformation from diversified conglomerate to focused water company. Randall Hogan, who had led the company through its most aggressive acquisition phase, departed to chair nVent. The new CEO would be John Stauch, the CFO who had helped orchestrate the portfolio transformation.

Beth Wozniak said she is excited to lead Pentair's spinoff of its electrical unit, to be called nVent, which will be completed this week. A year ago, Beth Wozniak was only four months into her new job as the head of Pentair's $2.1 billion electrical division when the CEO suggested they talk.

VIII. The Pure-Play Water Era & COVID Boom (2018-Present)

The Post-Spin Thesis

The nVent spin-off crystallized Pentair's investment thesis. Gone was the conglomerate complexity. Gone was the oil and gas exposure. Gone was the need to explain how enclosures and pool pumps belonged in the same portfolio.

What remained was a focused water company with compelling characteristics: - Recurring revenue: Approximately 70% of revenue from aftermarket, consumables, and replacement parts - Installed base: Millions of pools, wells, and filtration systems requiring ongoing maintenance - Secular growth drivers: Water quality concerns, aging infrastructure, sustainability mandates - Pricing power: Brand strength and distribution relationships supporting premium positioning

"We delivered another transformative year in 2024 and drove strong margin expansion across our entire portfolio despite a challenging global macroeconomic and geopolitical environment. By leveraging our Transformation initiatives and 80/20, our teams produced another solid year of operational and financial performance which mitigated risk to the topline while expanding profitability. This was a direct reflection of the power of our balanced and resilient water portfolio, our focused growth strategy and strong execution," said John L. Stauch, Pentair's President and Chief Executive Officer.

"Each of our Move, Improve and Enjoy Water segments drove record margins for another consecutive year post the nVent separation in 2018. In Flow, we continued to grow our Commercial business while evolving our go-to-market strategy within Industrial. In Water Solutions, our filtration sales delivered another year of growth, and in Pool, we returned to sales growth driven by a strong aftermarket."

Recent Acquisitions

Pentair plc, a leading provider of water treatment and sustainable solutions, today announced that it has entered into a definitive agreement to acquire Manitowoc Ice, a leading provider of commercial ice makers, for $1.6 billion, subject to customary adjustments. When adjusted for approximately $220 million of expected tax benefits, the net transaction value is approximately $1.38 billion.

Manitowoc Ice, a portfolio brand of Welbilt, Inc. (NYSE: WBT), is a leading designer, manufacturer, and distributor of commercial ice machines in the United States and globally. With a global installed base of approximately 1 million units and more than 200 models of commercial ice machines worldwide, Manitowoc Ice has excelled at delivering differentiated product innovation, food safety and sustainability in icemaking.

The Manitowoc Ice acquisition in July 2022 demonstrated Pentair's continued acquisition discipline. Highly complementary offering to expand Water Solutions platform, enhance value proposition for customers and provide an additional springboard for growth. Strategically expands Pentair's commercial water solutions platform and will accelerate growth within the foodservice industry space.

Commercial ice machines require high-quality water to produce crystal-clear ice. By combining ice machines with Everpure filtration systems, Pentair created an integrated solution for restaurants, hotels, and foodservice operations.

Current Business Model

Pentair is a global provider of smart and sustainable water solutions to homes, business, and industry around the world. Pentair is comprised of two reportable business segments: Consumer Solutions and Industrial & Flow Technologies. The Consumer Solutions segment designs, manufactures and sells energy-efficient residential and commercial pool equipment and accessories, and commercial and residential water treatment products and systems.

The brand names under Consumer Solutions include Everpure, Kens Beverage, Kreepy Krauly, Pentair Water Solutions, Pleatco, RainSoft and Sta-Rite. The Industrial & Flow Technologies segment manufactures and sells a variety of fluid treatment products, pumps, valves, and spray nozzles as well as systems combining these products.

IX. Business Deep Dive: Understanding Pentair Today

Products & Segments

Pentair organizes its operations around a simple framework: Move Water, Improve Water, Enjoy Water.

Pool (Enjoy Water): This segment includes pumps, filters, heaters, lights, automatic cleaners, and pool automation systems. The Pool business benefits from a large installed base of approximately 10 million in-ground residential pools in the United States alone, each requiring ongoing maintenance and periodic equipment replacement.

"Roughly 20 years ago, Pentair brought the variable speed and flow technology to the U.S. — a transformative innovation that remains the cornerstone of the pool industry. And that innovation continues today with the IntelliFlo3 pump."

The IntelliFlo variable-speed pump franchise represents Pentair's most successful product innovation. IntelliFlo VS Variable Speed pump is the next generation of Pentair's variable-speed pump technology. With energy savings up to 90%* versus conventional pumps, near-silent operation and advanced programming capabilities.

Water Solutions (Improve Water): Residential and commercial filtration, water softeners, and the Everpure commercial foodservice line. Pentair acquired Everpure in 2006 for $287 million, strengthening its position in commercial water filtration.

Flow (Move Water): Industrial pumps, agricultural irrigation equipment, and wastewater systems. Legacy brands include Fairbanks, Aurora, Myers, and Hydromatic—some with histories spanning over 100 years.

The PIMS Operating System

The Pentair Integrated Management System (PIMS) is the foundation of our success at Pentair. PIMS provides the language and tools to ensure we are building sustainable performance across our entire global enterprise.

PIMS has four key components (1) the Rapid Growth Process (RGP) for accelerating organic growth; (2) new product development process for accelerating innovation, referred to as 3D; (3) Pentair Talent System for attracting and developing top talent; and (4) Lean Enterprise methodology for eliminating waste across the Pentair enterprise.

Lean is described as Pentair's competitive advantage and focuses on eliminating waste to improve customer value and business velocity. Priorities for 2013 include deploying strategy to drive breakthrough objectives, transformation planning, and focusing talent and resources on largest opportunities.

PIMS represents the operational discipline that enables Pentair to execute acquisitions successfully. When Pentair acquires a business, it implements PIMS methodology—standardizing processes, eliminating waste, and driving productivity improvements.

Sustainability Strategy

Pentair has committed to ambitious environmental targets that align with its water-focused mission. The company targets a 60% reduction in Scope 1 and 2 greenhouse gas emissions by 2030 from its 2019 baseline—an increase from an already achieved 50% reduction target.

This sustainability focus creates commercial advantages. Energy-efficient products like IntelliFlo command premium prices while helping customers reduce operating costs. Municipal and commercial customers increasingly require sustainability credentials from suppliers.

X. Competitive Landscape & Market Position

Pool Equipment Market

The swimming pool equipment market is highly competitive, with key players including Pentair, Hayward Pool Products, and Fluidra leading in innovation and market share. These companies dominate with a wide range of products and advanced technologies, such as energy-efficient pumps and smart automation systems.

The U.S. robotic pool cleaner market is consolidated, with approximately 60% of the market share held by four key players: Pentair, Hayward Industries, Fluidra, and Maytronics. These companies maintain a dominant presence through extensive distribution networks, a broad product portfolio, and consistent technological innovation.

Swimming pool filter systems have seen three dominant players in the market for decades: Pentair, Jandy, and Hayward. Pentair leads the pack with a 35% market share, and Jandy follows closely with 25%.

The pool equipment market exhibits classic oligopoly characteristics. High distribution costs, brand loyalty among pool professionals, and regulatory barriers (energy efficiency requirements, safety standards) create meaningful moats. New entrants must build distribution networks, earn professional contractor trust, and navigate complex certification requirements.

Water Solutions Fragmentation

The broader water treatment market presents a different competitive picture. Top equipment suppliers such as Fluidra and Pentair control just under half of global pump, filter, and heater sales, benefiting from extensive distributor networks and R&D pipelines focused on sensor-embedded devices.

In residential water filtration, Pentair competes with hundreds of local and regional players. The market remains highly fragmented, presenting both challenge and opportunity. Fragmentation limits pricing power but creates acquisition targets for roll-up strategies.

Key Competitive Advantages

Distribution Network: Pentair's relationships with pool builders, contractors, and distributors create switching costs. Pool professionals learn Pentair systems, stock Pentair parts, and recommend Pentair products.

Installed Base: Millions of Pentair pumps, filters, and automation systems require replacement parts and service. This installed base generates recurring revenue regardless of new construction activity.

Innovation Leadership: Patent filings show Pentair targeting solar harvesting, winterization automation, and secure cloud connectivity, underscoring a pivot toward integrated ecosystems that lock in aftermarket parts demand.

Connected Products: The expansion of the Internet of Things (IoT) also presents a big growth opportunity for Pentair. The company already has around 500,000 connected devices deployed. It's targeting to more than double that number next year.

XI. Playbook: Business & Investing Lessons

The Acquisition Playbook

Pentair's M&A strategy offers several transferable lessons:

Buy at distress, sell at strength: From Peavey Paper Mills to Porter-Cable to Tyco Valves, Pentair repeatedly acquired troubled businesses at attractive valuations. When businesses reached peak value or no longer fit the portfolio, management demonstrated willingness to sell—even at apparent losses.

Operational excellence as integration strategy: PIMS provided a repeatable methodology for post-acquisition integration. Rather than relying on financial engineering, Pentair created value through manufacturing efficiency, procurement optimization, and operational discipline.

Know when to exit: Selling paper, divesting tools, spinning off nVent—each major divestiture freed capital and management attention for higher-return opportunities.

The Power of Focus

The nVent spin-off illustrated how conglomerate discounts can destroy value. Both Pentair (water-focused) and nVent (electrical-focused) achieved higher valuations as independent companies than they commanded together.

The lesson: investors reward clarity. A water company can be evaluated against water peers. An electrical company can be measured against electrical competitors. A conglomerate containing both gets valued at a discount because investors can't easily categorize it.

Capital Allocation Excellence

$0.23 per share per quarter in 2024 and marks the 49th consecutive year that Pentair has increased its dividend. During the fourth quarter, the company repurchased 0.4 million shares.

The water solutions company has increased its dividend for 49 consecutive years. Unless that impressive streak is broken next year, Pentair is on track to become the next Dividend King.

Forty-nine consecutive years of dividend increases spans recessions, inflation, oil shocks, financial crises, and pandemics. Maintaining this streak requires disciplined capital allocation, conservative balance sheet management, and sustainable earnings power.

Financial Performance Post-Transformation

Full year 2024 operating income was $804 million, up 9 percent compared to operating income in 2023, and ROS was 19.7 percent, an increase of 170 basis points. On an adjusted basis, the Company reported adjusted operating income of $959 million, up 12 percent in 2024, and ROS was 23.5 percent, an increase of 270 basis points.

Pentair's earnings are growing. The company expects adjusted earnings per share to jump 10% to 12% in full-year 2025.

XII. Bull Case vs. Bear Case

Bull Case

Secular Water Tailwinds: Global water scarcity, aging infrastructure, and increasing quality concerns drive demand for Pentair's products. The UN estimates that by 2025, two-thirds of the world's population may face water shortages.

Recurring Revenue Model: With ~70% of revenue from aftermarket and consumables, Pentair has reduced cyclicality relative to its industrial conglomerate past. Pool maintenance happens regardless of new construction activity.

Margin Expansion Runway: The 80/20 initiative and transformation programs continue driving operating margin improvement. Management guides to continued triple-digit basis point expansion.

Connected Products Moat: IoT-enabled pumps and automation systems create data advantages and deepen customer relationships. Connected devices drive recurring software revenue and enable predictive maintenance services.

Dividend King Trajectory: Unless that impressive streak is broken next year, Pentair is on track to become the next Dividend King. What are the chances that Pentair will be able to raise its dividend again in 2026? Very good.

Bear Case

Pool Market Cyclicality: Despite recurring revenue emphasis, new pool construction remains cyclical and sensitive to housing market conditions. High interest rates pressure discretionary spending on pool installation.

Competition from Asian Manufacturers: Lower-cost competitors from Asia increasingly target the U.S. pool equipment market. Brand loyalty may not persist if price differentials widen.

Integration Risk: Acquisitions remain central to the growth strategy. Integration failures like the Jackson disaster of 2000 could repeat.

Valuation: Its shares trade at around 20.5 times forward earnings. That's not terribly expensive, but the multiple doesn't make the stock a bargain, either.

Climate Volatility: Unseasonable weather affects pool season length and maintenance activity. Climate-driven demand patterns may become more volatile.

Porter's Five Forces Analysis

Supplier Power (Low-Medium): Pentair sources components globally, limiting individual supplier leverage. Raw materials like copper and resins can create cost pressure during commodity price spikes.

Buyer Power (Medium): Distribution through Pool Corp and other major wholesalers creates buyer concentration. However, contractor loyalty and brand strength limit pure price competition.

Threat of New Entrants (Low): Distribution relationships, regulatory certifications, brand equity, and manufacturing scale create meaningful barriers.

Threat of Substitutes (Low): Pools require filtration and pumping. Water requires treatment. The core functions Pentair serves have limited substitutes.

Competitive Rivalry (Medium-High): Three players dominate pool equipment. Competition on features, energy efficiency, and connected capabilities intensifies.

Hamilton Helmer's 7 Powers Framework

Switching Costs: Pool professionals trained on Pentair systems create switching costs. Installed base of Pentair equipment requires Pentair parts.

Network Effects: Limited direct network effects, though connected devices create data advantages that improve over time.

Counter-Positioning: Not applicable—competitors offer similar products.

Scale Economies: Meaningful in manufacturing and distribution. Larger scale enables lower unit costs and broader product portfolios.

Brand: Strong professional and consumer brand recognition, particularly in pool equipment.

Cornered Resource: Proprietary technologies like sensorless flow control provide temporary advantages.

Process Power: PIMS methodology represents institutionalized operational excellence that competitors may struggle to replicate.

XIII. Key Metrics to Track

For long-term investors monitoring Pentair, three KPIs matter most:

1. Aftermarket Revenue as Percentage of Total Sales

Currently approximately 70%, this metric indicates business model resilience. Higher aftermarket percentage means more recurring revenue, better visibility, and reduced cyclicality. Track whether this ratio holds or improves with each acquisition.

2. Return on Sales (ROS) / Operating Margin

Management has delivered consistent margin expansion post-nVent spin-off. ROS was 23.8 percent, an increase of 370 basis points when compared to the fourth quarter of 2023. Continued expansion validates the transformation strategy and 80/20 initiatives. Compression would signal competitive pressure or operational issues.

3. Free Cash Flow Conversion

In the first half of 2025 alone, the company produced $540 million in free cash flow, representing a 178% conversion of its net income. Strong FCF conversion enables dividends, buybacks, debt reduction, and acquisitions simultaneously. Deteriorating conversion could signal working capital issues or earnings quality concerns.

XIV. Leadership Profile: John Stauch

John Stauch currently serves as Pentair President and Chief Executive Officer. Prior to joining Pentair as chief financial officer in 2007, Stauch served as chief financial officer of the automation and control systems unit of Honeywell International Inc. Previously, he held a series of executive, investor relations and managerial finance roles with Honeywell International Inc. and its predecessor AlliedSignal Inc.

Stauch's background is notable for two reasons. First, his Honeywell tenure provided exposure to industrial transformation at scale—AlliedSignal and Honeywell executed legendary operational improvement under Larry Bossidy and Dave Cote. Second, his CFO-to-CEO progression means he deeply understands the financial implications of strategic decisions.

Mr. Stauch assumed the role of President and Chief Executive Officer of Pentair plc in May 2018. From 2007 until his CEO appointment, Mr. Stauch served as the Executive Vice President and Chief Financial Officer of Pentair plc.

John L. Stauch is President and Chief Executive Officer of Pentair plc and a director since 2018; age 60 as of the 2025 proxy. Prior roles include Pentair CFO (2007–2018), Honeywell International's Automation and Control Systems CFO (2005–2007), and PerkinElmer Optoelectronics CFO & IT Director.

The timing of Stauch's CEO appointment—May 2018, immediately following the nVent spin-off—positioned him as the leader of the newly focused water company. He wasn't inheriting a conglomerate; he was building a pure-play.

Pentair's "pay versus performance" shows rising TSR and earnings under his tenure: 2024 TSR value of an initial $100 investment reached $236.25 vs S&P 500 Industrials peers at $207.55.

XV. Final Thoughts: The Long Road to Focus

Pentair's journey from hot air balloons to global water empire defies easy categorization. It's not a story of visionary founders who saw the future of water. It's not a tale of technological breakthrough creating a market-leading position. It's something more pragmatic: five decades of disciplined capital allocation, operational excellence, and willingness to change.

Murray Harpole couldn't have imagined pool pumps when he was negotiating to buy Peavey Paper Mills in 1968. Randall Hogan couldn't have predicted the nVent spin-off when he completed the Tyco merger in 2012. John Stauch likely didn't foresee acquiring ice machines when he became CEO in 2018.

What connects these moments is institutional capability: the ability to buy underperforming assets, fix them, and either integrate them into a coherent portfolio or sell them when they no longer fit. This capability—embodied in PIMS, in financial discipline, in operational culture—represents Pentair's true competitive advantage.

The company that exists today bears almost no resemblance to its founding vision. But that's precisely the point. Pentair succeeded not by executing a predetermined strategy but by adapting relentlessly to market opportunities. Paper when paper made sense. Tools when tools made sense. Water when water became the clear strategic focus.

For investors, Pentair offers exposure to water infrastructure megatrends through a management team with demonstrated ability to create shareholder value. The valuation asks whether transformation gains are fully reflected in the stock price or whether further margin expansion justifies current multiples.

The answer depends on whether you believe Pentair's operational playbook—proven across fifty years and dozens of acquisitions—can continue delivering results in a focused water portfolio. If the past is prologue, the next chapter of Pentair's story may prove as surprising as its origin.

After all, few balloon companies become paper companies become tool companies become water companies. But then again, few companies survive their first two years the way Pentair did—through sheer determination, opportunistic acquisition, and unwillingness to accept failure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube