CECO Environmental: The Hidden Champion of Industrial Air & Water

I. Introduction: The Quiet Giant You've Never Heard Of

Picture this: somewhere in the Texas hill country, a massive petrochemical refinery churns out products that power everything from vehicles to plastic bottles. The air around it should be a toxic soup of particulates, volatile organic compounds, and nitrogen oxides. Instead, the sky remains blue, the nearby community breathes easily, and the plant operator sleeps soundly knowing that regulators won't come knocking. The reason? Somewhere inside that facility, equipment designed and manufactured by a company most investors have never heard of is quietly capturing billions of pounds of pollutants.

CECO Environmental is a leading environmentally focused, diversified industrial company whose solutions protect people, the environment, and industrial equipment across the globe, serving a broad landscape of industrial air, industrial water and energy transition markets. It's the kind of business that operates in plain sight yet remains invisible to the average observer—deeply embedded in the industrial fabric of modern civilization, mission-critical to its customers, yet unknown to Wall Street's spotlight chasers.

The numbers tell an increasingly compelling story. For full-year 2024, CECO reported orders of $667.3 million (up 14%), revenue of $557.9 million (up 2%), and gross profit of $196.1 million (up 15%). But the more striking figures lie ahead: the company has guided for 2025 revenues in the range of $700-750 million, representing approximately 30% growth, with Adjusted EBITDA expected to expand by roughly 50% year-over-year.

What transformed a modest air pollution control company into a billion-dollar enterprise positioned at the intersection of regulatory compliance, environmental consciousness, and the energy transition? The answer involves a shrewd M&A playbook, a CEO succession that changed everything, and timing that would make even the luckiest investor jealous.

The central question this analysis will explore: Can programmatic M&A create durable competitive advantage in industrial environmental solutions? Or has CECO simply assembled a hodgepodge of niche businesses whose whole is worth less than the sum of its parts? The answer reveals much about where industrial investing is headed in an era of decarbonization, reshoring, and environmental accountability.

II. Heritage & Founding Context: Two Origin Stories

The Deep Roots (1869): When America Built the Machines

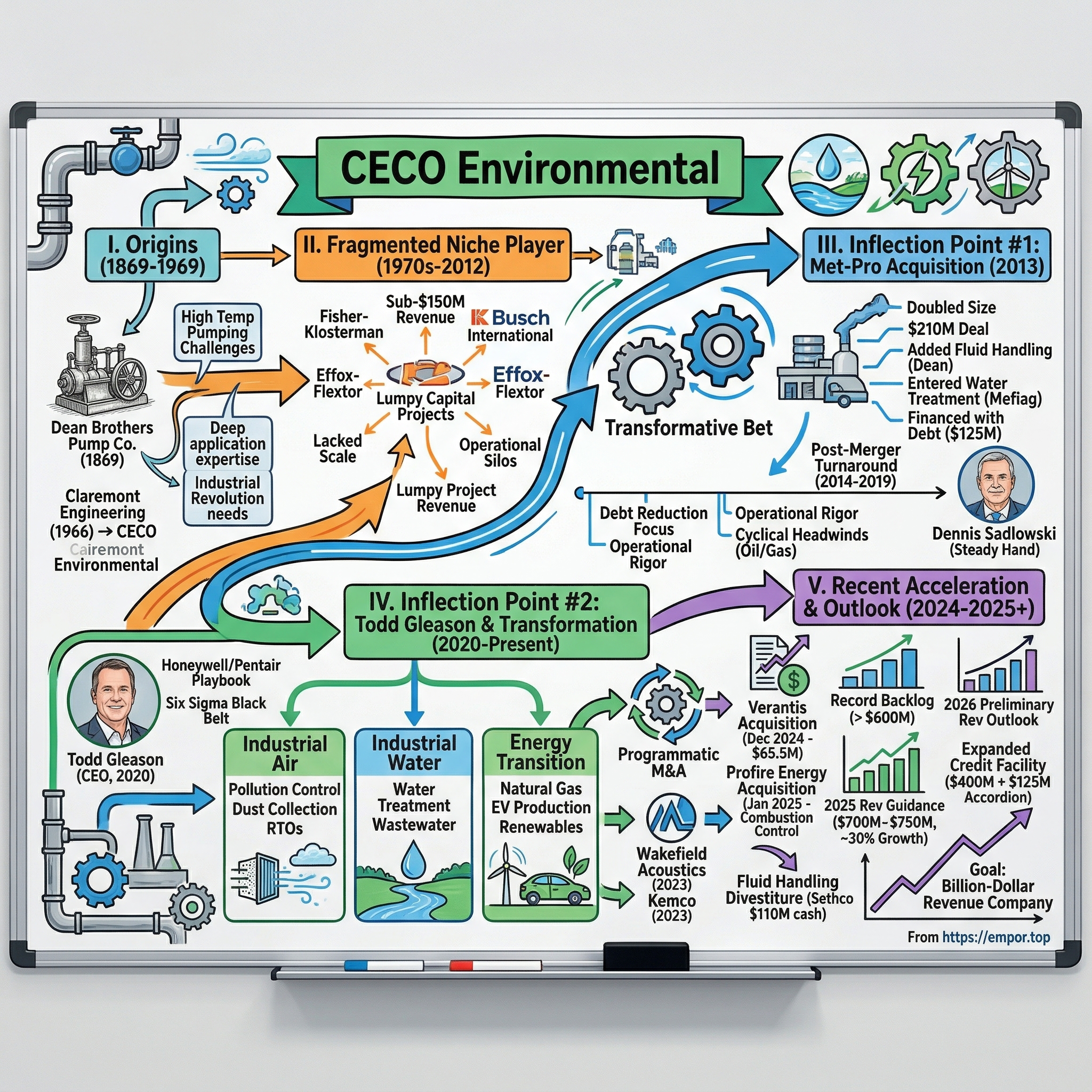

The story of CECO Environmental begins not in the environmental movement of the 1960s, but in the smoke-belching, ambition-fueled industrial expansion following the American Civil War. Our heritage dates back to 1869, when the Dean Brothers Pump Company was established to solve the world's high temperature pumping challenges.

Consider the context: 1869 America was a nation transformed. The transcontinental railroad had just been completed, binding east to west with iron and steam. The Industrial Revolution was reshaping the landscape—literally—as factories, foundries, and refineries sprouted across the Northeast and Midwest. These operations faced a fundamental challenge: how do you move superheated liquids, corrosive chemicals, and scalding water without destroying your equipment?

The Dean Brothers answered that question with specialized pump technology. Their innovations became the backbone of industrial operations that most Americans took for granted: steel mills needed to cool molten metal, refineries needed to move hydrocarbons at extreme temperatures, and chemical plants needed to handle substances that would eat through conventional equipment.

This heritage matters because it explains something essential about CECO's modern business: the company's DNA includes deep application expertise in solving mission-critical problems for heavy industry. When a refinery operator needs equipment that will function flawlessly in conditions that would destroy ordinary machinery, they turn to companies with century-plus track records.

The Modern Founding (1966-1969): The Environmental Era Dawns

One hundred years later, the Claremont Engineering company was founded and has since become known as CECO Environmental. CECO Environmental Corp. is a company founded in 1966 and now is based in Dallas, TX. The company provides air pollution control technology, products and services for various industries, including aerospace, brick, cement, steel, printing, food, foundries, utilities, woodworking, chemical processing.

The timing was not coincidental. The 1960s represented a watershed moment in American consciousness about environmental degradation. Rachel Carson's Silent Spring had awakened the public to the hidden costs of industrial progress. Smog choked major cities—Los Angeles became infamous for air so thick you could taste it. Rivers caught fire. The Cuyahoga River burning in 1969 became a symbol of environmental neglect.

Congress responded. The Clean Air Act of 1963 was followed by more muscular amendments in 1967 and 1970. The Environmental Protection Agency was established in 1970. For the first time, American industry faced binding requirements to control what came out of their smokestacks and waste pipes.

This created an entirely new industry from scratch. Companies like the newly-formed CECO Environmental suddenly found themselves selling not just equipment, but compliance—the ability to meet regulatory requirements that carried criminal penalties for violation. Trusted customer partnerships are built over decades of delivering quality engineering and technology solutions that help improve operating efficiency and safety while helping them reduce toxic emissions.

The environmental regulations of this era established a pattern that would prove crucial to CECO's long-term prospects: regulatory requirements tend to ratchet upward, never backward. Once a standard is set, it typically becomes stricter over time. This creates a perpetual demand driver for companies that help industrial facilities stay on the right side of the law.

For investors examining CECO today, understanding this dual heritage illuminates the company's competitive positioning. The Dean Brothers legacy provides deep expertise in fluid handling and high-temperature applications. The Claremont/CECO origin established the company's identity as an environmental solutions provider. The 2013 merger of these lineages—through the Met-Pro acquisition—created the foundation for the modern company.

III. The Pre-Transformation Era: A Fragmented Niche Player (1970s-2012)

For four decades following its modern founding, CECO Environmental operated as what industry analysts might charitably describe as a "small-cap orphan"—a company too small to attract meaningful institutional attention, too niche to benefit from thematic investment flows, and too fragmented to achieve meaningful scale economies.

CECO Environmental is a leading global provider of air pollution control technology. Through its subsidiaries – Aarding, Adwest Technologies, Busch International, CECO Filters, CECO Abatement Systems, Kirk & Blum, Effox-Flextor, Fisher-Klosterman/Buell, CECO China and A.V.C. Specialists – CECO provides a wide spectrum of air quality products and services including engineered equipment, cyclones, scrubbers, dampers, diverters, RTOs, component parts and monitoring and management services.

The subsidiary structure reveals both strength and weakness. Each brand carried deep expertise in specific niches—Fisher-Klosterman in cyclones and industrial dust collection, Kirk & Blum in air handling systems, Effox-Flextor in dampers and expansion joints. But fragmentation meant duplicated overhead, inconsistent pricing power, and limited ability to cross-sell solutions to customers with multiple needs.

The Structural Challenge of Environmental Equipment

Understanding CECO's pre-transformation limitations requires grasping the economics of the industrial environmental equipment business:

Project-Based Revenue: Unlike software companies with recurring subscription revenue, environmental equipment manufacturers traditionally generated revenue through lumpy capital projects. A refinery might order a $2 million scrubber system, providing a burst of revenue, followed by years of minimal business until the next major capital expenditure cycle.

Industrial Cyclicality: Demand for pollution control equipment correlates strongly with industrial capital expenditure, which itself tracks commodity prices, economic growth, and regulatory enforcement intensity. This created significant revenue volatility that made planning difficult and valuation challenging.

Technical Complexity Without Scale: Each installation required custom engineering to meet specific customer requirements. This prevented the standardization that might have allowed for manufacturing efficiency and margin expansion.

Regional Fragmentation: The market featured dozens of regional players, many family-owned, with limited geographic reach. No dominant player had emerged to consolidate the industry.

By 2012, CECO remained a sub-$150 million revenue company—respectable, profitable, but lacking the scale to compete effectively against diversified industrials like Honeywell or GE that offered environmental solutions as part of broader portfolios. The company needed a transformative move, and management knew it.

For long-term investors, this era illustrates a crucial principle: niche leadership alone does not guarantee sustainable competitive advantage. Without scale, pricing power, or recurring revenue, even mission-critical suppliers can remain stuck in value-investing purgatory—cheap on paper, but with limited catalysts for multiple expansion.

IV. Inflection Point #1: The Met-Pro Acquisition – A Transformative Bet (2013)

The Deal That Changed Everything

In August 2013, CECO Environmental Corp., a global leader in air pollution control systems, product recovery and filtration technology, announced today that it has completed the previously announced acquisition of Met-Pro Corporation. With pro forma revenues of approximately $300 million, the transaction creates a clear global market leader in air pollution control, product recovery and fluid handling technology.

CECO acquired all of the outstanding shares of Met-Pro common stock in a cash and stock transaction valued at a total of approximately $210 million, or $13.75 per share, which represents a 43% premium to Met-Pro's share price as of the close on April 19, 2013. The consideration includes $7.25 per share in cash and $6.50 per share in CECO common stock.

To appreciate the boldness of this move, consider the context: CECO was effectively doubling its size overnight by acquiring a company nearly equal to itself. Currently (2013.12) the company owns twelve subsidiaries. The integration challenge was enormous—two different corporate cultures, overlapping product lines, duplicated back-office functions, and the typical friction that accompanies mergers of equals.

Bank of America provided CECO committed debt financing of $125 million to support the cash portion of the transaction. This meant CECO was leveraging up significantly to fund the acquisition, a calculated risk that would either establish the company as a diversified leader or saddle it with potentially crushing debt.

The Strategic Rationale

Jason DeZwirek, CECO's Chairman stated, "The acquisition of Met-Pro is a transformative step in CECO's history and key to our future success. The ability to bring these two great companies and management teams together represents a unique opportunity to create value for our customers and shareholders."

Beyond the press release language, the strategic logic was compelling:

Fluid Handling Addition: Met-Pro brought the Dean pump brands—the very heritage stretching back to 1869—adding fluid handling capabilities to CECO's air pollution control portfolio. This created a more complete solution set for industrial customers.

Water Treatment Entry: Met-Pro's Mefiag Filtration Technologies segment designs, manufactures, and sells filtration systems that are used in corrosive applications in the plating, metal finishing, and printing industries. Its Filtration/Purification Technologies segment offers chemicals for the treatment of municipal drinking water systems, and boiler and cooling tower systems; cartridges and filter housings; filtration products for industrial air and liquid applications.

Geographic Expansion: Met-Pro's Pennsylvania headquarters and established distribution networks complemented CECO's existing footprint.

End Market Diversification: The combined businesses will be uniquely positioned to capitalize on fast growing end markets and secular trends supported by increasingly stringent levels of pollution control regulation, increasing global energy demand, emerging market dynamics, most notably in China and India, and a low cost natural gas environment, driving new plant construction in the U.S.

The Integration Reality

Mergers are announced in press releases but executed in spreadsheets and factory floors. The Met-Pro integration consumed the next several years of management attention. Revenue synergies that looked obvious on paper—cross-selling air and water solutions to the same customers—required building new sales processes, training technical staff on unfamiliar products, and overcoming the natural territorial instincts of formerly independent business units.

The debt load from the acquisition required careful management. While the company eventually proved it could service the debt, the leverage constrained strategic flexibility and made CECO vulnerable to any cyclical downturn in industrial spending.

For investors evaluating serial acquirers, the Met-Pro deal offers important lessons. First, transformative acquisitions that change a company's scale and capabilities are qualitatively different from tuck-in deals that simply add revenue. Second, the post-merger period often involves years of digestion before the benefits fully materialize. Third, leverage magnifies both success and failure—CECO's bet paid off, but only because execution proved adequate and end markets cooperated.

V. The Post-Merger Years: Debt Reduction & Operational Turnaround (2014-2019)

The five years following the Met-Pro acquisition represented a period of unglamorous but essential work. CEO Dennis Sadlowski's tenure focused not on dramatic strategic moves, but on the blocking and tackling that determines whether acquisitions create or destroy value.

CECO is much stronger and in a better financial position due to Dennis' steady hand and operational leadership. Dennis was instrumental in CECO significantly reducing its debt, strengthening its leadership team and implementing strong processes and overall operational rigor.

The Discipline of Debt Reduction

Post-acquisition, CECO faced a familiar challenge: the debt used to fund the Met-Pro deal now competed for cash flow that might otherwise fund growth investments. Every dollar paid to lenders was a dollar not invested in new products, geographic expansion, or additional acquisitions.

Sadlowski's approach prioritized balance sheet health over aggressive growth. This meant:

- Cash Flow Focus: Operational improvements to generate free cash flow for debt paydown

- Cost Discipline: Eliminating redundancies from the merged organization without destroying capabilities

- Selective Reinvestment: Investing only in projects with clear payback periods rather than speculative initiatives

- Leadership Development: Building a management bench capable of running a larger, more complex organization

Navigating Cyclical Headwinds

The 2014-2019 period included significant headwinds for industrial equipment suppliers:

Oil & Gas Volatility: The shale revolution initially drove capital spending, but the oil price collapse in 2014-2015 devastated energy-sector customers who represented a significant portion of CECO's end markets.

Industrial Capex Cycles: Global manufacturing investment ebbed and flowed with trade tensions, currency movements, and regulatory uncertainty.

Chinese Slowdown: The emerging market growth story that had supported Met-Pro's investment thesis cooled considerably as China's economy decelerated.

Through these challenges, CECO maintained profitability while steadily reducing leverage. The company proved its business model could withstand cyclical pressure—essential validation for a potential serial acquirer that would need access to debt markets for future deals.

The Foundation for What Came Next

By the time Sadlowski departed, CECO had accomplished something crucial: it had demonstrated that the combined company worked. Revenue had stabilized, margins had expanded, and debt had declined to manageable levels. The company had established the operational infrastructure—financial controls, management processes, IT systems—necessary to absorb additional acquisitions.

This often-overlooked phase of corporate development deserves attention from investors. The companies that eventually emerge as successful roll-up platforms rarely do so through continuous acquisition. Instead, periods of intense deal-making alternate with periods of digestion and capability building. CECO's 2014-2019 period represented exactly this kind of necessary pause—unglamorous, unremarkable from a headline perspective, but essential to what followed.

VI. Inflection Point #2: Todd Gleason & The Transformation Strategy (2020-Present)

The CEO Who Brought the Playbook

CECO Environmental Corp. announced today that Todd Gleason has been appointed to succeed Dennis Sadlowski as Chief Executive Officer of the Company. The appointment concludes a comprehensive search that began in early 2020, in which CECO's Board of Directors, together with a leading executive search firm, worked to identify the right leader for CECO's next phase of growth.

The choice of Gleason revealed much about the board's ambitions. Todd joined CECO in July 2020 after over 20 years in executive positions at leading diversified industrial companies including Honeywell International, Trane Technologies and most recently Pentair. He also held Chief Executive Officer and Board Director positions at DARI Motion, a private equity-backed, predictive analytics technologies and services company.

This background matters enormously. Honeywell, under David Cote, had pioneered the "Honeywell Operating System"—a rigorous approach to operational excellence borrowed from Toyota's manufacturing principles. Trane (now Trane Technologies) and Pentair both operated as diversified industrials pursuing programmatic M&A strategies. Gleason had spent two decades learning how elite industrial companies operate, grow through acquisition, and integrate acquired businesses.

He holds a master's degree in management and public policy from Carnegie Mellon University and an undergraduate degree in history and international relations from Wesleyan. He also has his Six Sigma Black Belt and has completed numerous process improvement programs in LEAN Enterprise.

The Six Sigma Black Belt certification signals something specific: Gleason is a systems thinker who approaches operations through data-driven process improvement. This methodology, originally developed at Motorola and popularized by GE, has become standard among diversified industrials seeking to drive margin expansion through operational excellence.

The Strategic Vision: Air, Water & Energy Transition

Gleason wasted little time articulating a clear strategic direction. CEO Gleason stated: "While our Fluid Handling business is very well positioned in its markets, we are laser focused on businesses that more closely align with our strategic investments and leadership positions in Air, Water and Energy Transition."

This framework established three pillars for capital allocation:

Industrial Air: CECO's legacy business, including pollution control systems, dust collection, thermal oxidizers, and related technologies Industrial Water: Water treatment, wastewater handling, and water recycling solutions for industrial applications Energy Transition: Technologies serving the shift toward cleaner energy sources, including solutions for natural gas infrastructure, EV production, and renewable energy installations

The thesis underlying this focus is straightforward: environmental regulation and energy transition create secular demand drivers that transcend economic cycles. As regulations tighten and companies pursue decarbonization commitments, demand for CECO's solutions should grow regardless of near-term GDP fluctuations.

The Programmatic M&A Strategy

Gleason implemented what he explicitly termed "programmatic M&A"—a systematic approach to acquisition-driven growth that contrasts with the opportunistic deal-making that characterizes many acquirers.

Transcend is the second acquisition for CECO in 2023, following the previously announced deal for U.K.-based Wakefield Acoustics Ltd. in January 2023 and four transactions in 2022, continuing CECO's steady execution of its programmatic M&A strategy launched in early 2022.

The approach involves several distinctive elements:

Clear Criteria: Targets must operate in air, water, or energy transition markets with defensible niche positions and margin profiles at or above company averages Manageable Size: Deals small enough to digest without overwhelming integration capacity but large enough to move the needle Cultural Fit: Target management teams typically stay with the business, incentivized to drive continued growth Synergy Realization: Systematic approach to achieving cost synergies without damaging operational capabilities

Kemco, founded in 1969, marks the third acquisition for CECO during 2023, and a continuation of CECO's steady execution of its programmatic M&A strategy. CEO Gleason described the Kemco acquisition as "another important and strategic step to build upon our already strong and diversified industrial water capabilities, which we have been building with tremendous organic growth execution and the acquisitions of Compass Water, Index Water, DS21, and General Rubber."

The Impact Installed Base

The environmental impact CECO claims for its installed base is striking: CECO Environmental has installed more than 32,000 air pollution control systems with the capability to eliminate more than 4.4 billion pounds of pollutants per year, equivalent to removing more than 50 million passenger vehicles from the road.

While such figures should be evaluated carefully—they represent theoretical capacity rather than verified emissions reductions—they illustrate the scale of CECO's relevance to industrial environmental compliance. CECO technologies and products reduce or eliminate harmful pollutants, including CO, VOCs, NOx, HAPs, Acid Gases, and Particulate Matter.

For ESG-focused investors, this positions CECO as a "picks and shovels" play on corporate environmental commitments. Rather than betting on which company will successfully decarbonize, investors can own the equipment supplier serving all of them.

VII. The 2024-2025 Acceleration: Major Deals & Portfolio Reshaping

The past twelve months have witnessed CECO's transformation accelerate dramatically, with major acquisitions, a significant divestiture, and expanded financial capacity signaling management's conviction that the company's moment has arrived.

Profire Energy Acquisition (January 2025)

CECO Environmental Corp. announced the closing of its acquisition of Profire Energy, Inc., as of January 3, 2025, (formerly NASDAQ: PFIE) ("Profire"), a technology company and industry-leading provider of intelligent control solutions that enhance the efficiency, safety, and reliability of industrial combustion appliances while mitigating potential environmental impacts related to the operation of these devices with its primary operations in Lindon, Utah and Acheson, Alberta.

The aggregate consideration paid by CECO to acquire the shares of PFIE was approximately $122.7M, which CECO financed through a combination of cash on hand and borrowings under its existing credit facility.

Profire represents a strategic expansion into burner management and combustion control—technologies that reduce emissions while improving operational efficiency for industrial combustion applications. Profire expects to generate approximately $60 million in revenues with adjusted EBITDA margins of approximately 20 percent in the full year 2024.

CEO Gleason stated: "I am excited to welcome the Profire team to CECO as we advance our strategic portfolio of leading environmental solution businesses in niche energy and industrial markets. Together, I believe that we will accelerate Profire's growth by accelerating expansion in new energy, industrial and international markets."

Verantis Acquisition & Strategic Divestiture

CECO Environmental Corp. acquired Verantis Corporation on December 17, 2024. CECO Environmental Corp. completed the acquisition of Verantis Corporation for $65.5 million on December 17, 2024.

In late December 2024, the company completed its acquisition of Verantis Environmental Solutions Group. Verantis had annualized sales of approximately $45M and operating margins which are expected to be accretive to the company.

The strategic narrative crystallized with the simultaneous announcement of a divestiture. CECO Environmental Corp. announced it has completed the previously announced divestiture of its Fluid Handling business (also known as its Global Pump Solutions, or GPS, business) contained in its Industrial Process Solutions segment to May River Capital, effective March 31, 2025. The enterprise value of the transaction is approximately $110 million, paid in cash at closing.

The GPS business consists of three niche leadership severe service industrial metallic, fiberglass and thermoplastic centrifugal pump brands - Dean, Fybroc and Sethco - which joined the CECO family through an acquisition in 2013.

This divestiture is significant: the Dean, Fybroc, and Sethco pump brands represent the heritage tracing back to 1869. Selling them signals that Gleason prioritizes strategic fit over historical attachment. CEO Gleason stated: "I am pleased to have completed our previously announced divesture of GPS, which enables greater alignment of our portfolio of leading environmental solution businesses against our high growth opportunities in energy and industrial markets. We believe that the GPS business is well positioned as a niche leader in its respective end markets and applications, and we also believe that we have found the right buyer and future home to ensure its continued success and development of the GPS team. This sale will – after our recent acquisitions of Verantis Environmental and Profire Energy - create additional capacity for further investment in CECO's growth and business expansion, and execution of our strategies in Industrial Air, Industrial Water, and the Energy Transition."

Financial Firepower

The M&A acceleration required expanded financial capacity. CECO Environmental Corp. has announced a significant upsize in the form of an amendment and restatement of its credit facility, increasing it to a $400 million senior secured revolving credit facility. This expansion from the existing $246 million aggregate capacity underscores CECO's strategic commitment to strengthening its financial resources in pursuit of both organic and inorganic growth.

The expanded credit facility comes with a five-year term and an option to increase the facility by $125 million. This move enables CECO with additional resources to efficiently fund potential opportunities and expand its footprint in global markets.

The $400 million facility, with an additional $125 million accordion feature, provides CECO with significant acquisition capacity. Management has demonstrated willingness to deploy this firepower rapidly when opportunities align with strategic priorities.

VIII. Business Model Deep Dive

Two Operating Segments

CECO operates through two reportable segments that reflect the diverse nature of its solution portfolio:

Serving the power generation, refinery, water/wastewater and midstream oil and gas markets, we are a key part of helping meet the global demand for environmental and equipment protection through our highly engineered emissions management, product recovery, and water and gas separation solutions. Serving the broad industrial air pollution control, beverage can, fluid handling, electric vehicle production, food and beverage, semi-conductor, process filtration, pharmaceutical, petrochemical, wastewater treatment, wood manufacturing, desalination and aquaculture markets.

Engineered Systems serves large capital projects for power generation, refineries, midstream oil & gas, and water/wastewater markets. This segment typically involves higher project values, longer sales cycles, and more significant engineering content.

Industrial Process Solutions addresses the broader industrial landscape with solutions for air pollution control, beverage can production, EV manufacturing, semiconductors, food & beverage processing, and similar applications. This segment trends toward shorter cycle times and more standardized products.

Product Portfolio

The breadth of CECO's product offering reflects both its acquisition history and the diverse environmental challenges facing industrial facilities:

Air Quality Systems: Cyclones, dust collectors, thermal oxidizers (RTOs), scrubbers (wet and dry), selective catalytic reduction systems

Thermal Acoustics: Industrial silencers, noise attenuation systems (expanded through the Wakefield Acoustics acquisition)

Separation & Filtration: Separators, coalescers, filtration systems for process applications

Water Treatment: Water treatment packages, wastewater handling, water recycling systems

Dampers & Expansion Joints: Critical components for managing airflow and accommodating thermal expansion in industrial systems

Energy Controls: Burner management systems, combustion controls (added through Profire acquisition)

Geographic Footprint

We have a multinational presence of 25 principal operating facilities across 11 U.S. states and eight countries · Globally diverse, broad reaching organization: serving customers in >40 countries.

This geographic diversity provides several advantages: proximity to customers in key industrial regions, localized manufacturing that reduces logistics costs and tariff exposure, and cultural familiarity with regulatory requirements in different markets.

Revenue Model & Customer Relationships

Understanding CECO's revenue model requires distinguishing between project-based and aftermarket revenue streams:

Project Revenue: Large capital installations typically involve competitive bidding, extended engineering and manufacturing periods, and revenue recognition over project duration. These projects carry execution risk and can produce lumpy quarterly results.

Aftermarket Revenue: Replacement parts, consumables, maintenance services, and upgrades to installed equipment generate more predictable, higher-margin revenue. CECO has strategically emphasized growing this component of its mix.

A typical customer relationship might involve a refinery seeking to reduce harmful emissions. CECO's engineers work with the customer to design a customized scrubber system capturing specific pollutants. Once installed, the customer relies on CECO for replacement components, filter media, and periodic upgrades as regulations tighten. This installed base relationship provides switching costs—customers hesitate to change suppliers for mission-critical equipment where CECO understands their specific operating environment.

IX. Industry Context & Market Dynamics

The Air Pollution Control Market

The market CECO serves is substantial and growing. Air Pollution Control Systems Market size was valued at USD 87.97 Billion in 2023 and is poised to grow from USD 91.66 Billion in 2024 to USD 127.38 Billion by 2032, growing at a CAGR of 4.2% during the forecast period (2025-2032).

Leading companies such as ABB Ltd., Mitsubishi Hitachi Power Systems, Babcock & Wilcox Enterprises, and DuPont Clean Technologies dominate the market due to their extensive product portfolios and technological innovations. Emerging players like CECO Environmental Corp and Thermax Group are also gaining traction by focusing on sustainable and cost-effective solutions.

Several factors drive market growth:

Regulatory Stringency: Environmental regulations globally trend toward stricter requirements. This creates perpetual demand as facilities must upgrade equipment to comply with tightening standards.

Industrial Growth in Emerging Markets: As developing nations industrialize, they simultaneously develop environmental regulatory frameworks requiring pollution control equipment.

Energy Transition: The shift toward cleaner energy creates both challenges (reduced demand from coal-fired power plants) and opportunities (new requirements for natural gas infrastructure, EV manufacturing, battery production).

ESG Commitments: Corporate environmental, social, and governance commitments increasingly drive voluntary environmental investments beyond regulatory minimums.

Regulatory Tailwinds

The regulatory environment constitutes CECO's most important demand driver. Unlike discretionary industrial spending that can be deferred during downturns, environmental compliance is non-negotiable. Facilities that fail to meet air quality standards face operational shutdowns, criminal penalties, and reputational damage.

Key regulatory frameworks affecting CECO's markets include:

- Clean Air Act (US): National Ambient Air Quality Standards, New Source Performance Standards, Maximum Achievable Control Technology requirements

- European Industrial Emissions Directive: Best Available Techniques requirements for European installations

- China's Air Pollution Prevention Law: Increasingly stringent requirements driving demand in the world's largest manufacturing economy

- Various National Standards: Country-specific regulations in India, Southeast Asia, Middle East, and Latin America

The trajectory of these regulations remains consistently toward tightening. Political shifts may affect enforcement intensity, but outright regulatory rollback remains rare once standards are established.

End Market Diversification

CECO's strategy emphasizes serving diverse end markets to reduce concentration risk:

Traditional Industrial: Oil & gas, petrochemicals, power generation, steel and metals—these mature markets generate steady demand but may face long-term headwinds from energy transition Growth Markets: EV production, battery manufacturing, semiconductor fabrication, data centers—these emerging applications benefit from powerful secular trends Infrastructure: Water/wastewater treatment, natural gas infrastructure—essential services with stable demand profiles

X. Competitive Landscape

Key Competitors

CECO Environmental competes with other environmental technology and industrial solutions providers including Donaldson Company (NYSE:DCI), Evoqua Water Technologies (now part of Xylem, NYSE:XYL), Fuel Tech (NASDAQ:FTEK), and privately-held companies like Dürr Environmental and Babcock & Wilcox Environmental.

The competitive landscape varies significantly across CECO's different product lines:

Diversified Industrials (Honeywell, Dürr, GE): These companies offer environmental solutions as part of broader portfolios. They bring scale, brand recognition, and bundling capabilities but may lack the specialized focus that smaller pure-plays provide.

Pure-Play Environmental (Donaldson, Fuel Tech): These competitors focus exclusively on environmental solutions, competing directly with CECO across various product lines. Donaldson, in particular, is substantially larger and benefits from greater scale in filtration products.

Water Specialists (now Xylem/Evoqua): Following Xylem's acquisition of Evoqua, the combined entity represents a formidable competitor in industrial water markets.

Regional Specialists: Numerous smaller companies compete in specific geographies or product niches, often acquired by consolidators like CECO.

CECO's Competitive Position

With $608.3 million in revenue over the past 12 months, CECO Environmental is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale. On the bright side, it can grow faster because it has more room to expand. CECO's 12.6% annualized revenue growth over the last five years was excellent.

CECO occupies an interesting competitive position: large enough to serve major industrial customers with confidence, yet small enough to remain focused and nimble. The company lacks the scale of Donaldson or the diversification of Honeywell, but compensates through application expertise, customer relationships, and the ability to provide comprehensive solutions across air, water, and energy transition markets.

The programmatic M&A strategy aims to address the scale disadvantage over time. Each acquisition adds capabilities, customer relationships, and revenue, gradually building the critical mass necessary to compete more effectively with larger players.

XI. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MODERATE

The environmental equipment market presents meaningful barriers to entry that protect incumbents like CECO:

Engineering Expertise: Designing effective pollution control systems requires deep understanding of thermodynamics, fluid dynamics, chemical engineering, and process integration. This expertise accumulates over decades and cannot be easily replicated.

Regulatory Knowledge: Understanding how regulatory requirements translate into equipment specifications requires specialized knowledge that takes years to develop.

Customer Relationships: Trusted customer partnerships are built over decades of delivering quality engineering and technology solutions. Industrial customers prefer proven suppliers for mission-critical equipment.

Capital Requirements: Manufacturing facilities, engineering teams, and service infrastructure require significant investment.

Installed Base: Existing installations create ongoing aftermarket revenue opportunities that new entrants cannot access.

However, the barrier-lowering factors include potential technology commoditization in simpler product categories and the ability of well-funded competitors to acquire rather than build capabilities.

2. Bargaining Power of Suppliers: LOW-MODERATE

CECO maintains diversified supplier relationships across multiple geographies, limiting any single supplier's leverage. While certain specialized components may come from limited sources, the company's scale provides negotiating leverage and the ability to qualify alternative suppliers.

3. Bargaining Power of Buyers: MODERATE

Large industrial customers—refineries, utilities, major manufacturers—possess significant negotiating leverage due to their purchasing volume and the competitive nature of bidding processes. However, several factors limit this power:

- Regulatory compliance requirements are non-negotiable, reducing pure price sensitivity

- Custom-engineered solutions create switching costs once specifications are established

- CECO's application expertise and installed base knowledge provide value beyond equipment pricing

4. Threat of Substitutes: LOW

Environmental compliance is fundamentally mandatory. Industrial facilities cannot simply choose not to control emissions—they must either comply or cease operations. While alternative technologies exist, switching typically requires significant investment in new equipment and permitting, creating substantial barriers to substitution.

We protect the air we collectively breathe, maintain clean and safe operations for employees, lower energy consumption and minimize waste for customers. These functions are mission-critical without practical substitutes.

5. Competitive Rivalry: MODERATE-HIGH

The environmental equipment market features significant competitive intensity:

- Multiple capable competitors across various product categories

- Project-based competition that often comes down to price and delivery

- Ongoing R&D efforts aimed at improving efficiency and capturing market share

- Strategic M&A activity as competitors consolidate regional players

XII. Hamilton's 7 Powers Analysis

1. Scale Economies: EMERGING

With pro forma revenues of approximately $300 million, the transaction creates a clear global market leader in air pollution control, product recovery and fluid handling technology.

CECO's scale has grown substantially through acquisition, but the company remains significantly smaller than diversified industrials. Scale benefits are emerging in areas like shared services, procurement leverage, and R&D amortization across broader product lines, but have not yet reached the level that creates decisive competitive advantage.

2. Network Effects: WEAK

Limited network effects exist in industrial equipment. Some benefit accrues from the installed base (aftermarket revenue, customer relationships), but equipment performance does not improve as more customers adopt CECO solutions.

3. Counter-Positioning: MODERATE

CECO's pure-play environmental focus allows it to move faster on energy transition opportunities than diversified industrials burdened by legacy businesses. The company can allocate all capital to environmental solutions while competitors must balance investments across multiple priorities.

4. Switching Costs: MODERATE-HIGH

Custom-engineered solutions create meaningful switching costs. When CECO designs a scrubber system for a specific application, the customer becomes dependent on CECO's understanding of that installation for maintenance, upgrades, and replacement components. Regulatory compliance documentation is tied to specific equipment configurations, making changes costly and time-consuming.

5. Branding: MODERATE

CECO operates multiple brands with established reputations in their niches: "Wakefield is an industry-recognized brand, with more than 40 years of engineering leadership in the industrial acoustics market. With our complementary suite of products and solutions, CECO will be well-positioned to expand in the high growth energy and green markets in Europe and beyond."

While not consumer-facing brands, these industrial brands carry significant weight with purchasing engineers who value proven track records in mission-critical applications.

6. Cornered Resource: MODERATE

CECO's expertise in air pollution control represents a form of cornered resource—the accumulated knowledge of thousands of installations across diverse industries. This institutional expertise cannot be easily replicated and provides competitive advantage in understanding customer needs and designing effective solutions.

7. Process Power: EMERGING

Our programmatic M&A program added tremendous businesses to our mix in the second half of 2024 and early 2025, and we expect each of these acquisitions will deliver solid growth and accretive margins to the Company.

Gleason's Six Sigma and Lean Enterprise background suggests systematic approaches to operational improvement. The acquisition integration playbook—developed over multiple deals—represents emerging process power that could accelerate value creation from future transactions.

XIII. Current Performance & Outlook

Recent Results: Strong Momentum Despite Challenges

Todd Gleason, CECO's Chief Executive Officer commented, "While we acknowledge mixed results in 2024 driven by customer project and market related order delays, we are energized by our fourth quarter record orders bookings of $219 million, which provides incredible momentum moving into 2025."

CECO Environmental reported record Q4 2024 bookings of $218.9 million (up 71%) and elevated year-end backlog to a record $540.9 million (up 46%).

Full year 2024 results reflected the tension between strong demand indicators and execution challenges: For the full year ended 2024, the Company expects to report revenues in the range of $555 to $558 million, when compared to the previous guidance of $575 to $600 million, and Adjusted EBITDA between $62 to $63 million.

Q1 2025: Record Performance

The first quarter of 2025 demonstrated the power of CECO's transformed portfolio:

CECO Environmental reported strong Q1 2025 results with multiple financial records. Orders reached $227.9 million, up 57%, while backlog hit a historic $602.0 million, increasing 55%. Revenue grew 40% to $176.7 million.

CEO Todd Gleason commented: "We started 2025 with outstanding first quarter record orders of $228 million, which helped drive new record levels of backlog and revenue for the company. This is a powerful statement on the strength of our well-positioned portfolio, which is closely aligned to key long-term growth themes of industrial manufacturing reshoring, electrification, power generation, natural gas infrastructure, and industrial water investments."

2025 Outlook

For the full year 2025 outlook, the Company maintains its expectation to deliver Revenue of $700 to $750 million, up approximately 30 percent at the midpoint year and maintains its expected range for Adjusted EBITDA of $90 to $100 million, up approximately 50 percent at the midpoint versus 2024.

The growth trajectory is compelling: from roughly $560 million in 2024 to a $725 million midpoint in 2025 represents transformative acceleration, driven by both acquisitions and organic growth in favorable end markets.

2026 Preliminary Outlook

Full year 2026 revenue outlook is projected to be between $850 million and $950 million, which is up between 15% to 25% year over year when compared to 2025's midpoint. Our estimated 2025 year-end backlog of approximately $750 million or greater gives us significant visibility as we start 2026.

Management is openly discussing a path toward becoming "a billion-dollar revenue company on our way to much more"—a striking statement of ambition from leadership.

XIV. Investment Considerations: Bull vs. Bear Case

The Bull Case

Secular Tailwinds: Environmental regulation and energy transition create demand drivers that transcend economic cycles. As global regulatory frameworks tighten and corporations pursue decarbonization, CECO's solutions become increasingly essential.

Programmatic M&A Execution: Management has demonstrated ability to identify, acquire, and integrate businesses that enhance strategic positioning. The expanded credit facility provides firepower for continued acquisition-driven growth.

Backlog Visibility: Backlog hit a historic $602.0 million in Q1 2025, increasing 55%. This provides unusual revenue visibility for an industrial company and suggests demand strength that transcends quarterly noise.

Margin Expansion Potential: As scale increases and integration synergies materialize, operating margins have room to expand toward levels achieved by best-in-class industrial companies.

Leadership Quality: Gleason's background at Honeywell, Trane, and Pentair—combined with the operational discipline he's brought to CECO—provides confidence in management execution.

The Bear Case

Acquisition Integration Risk: Rapid deal-making increases execution risk. The simultaneous integration of Profire, Verantis, and earlier acquisitions strains management bandwidth and organizational capacity.

Leverage Exposure: The expanded credit facility enables growth but also increases financial risk. Any significant downturn in end markets could stress the balance sheet.

Customer Concentration: Large projects with major industrial customers create potential for revenue volatility if key customers delay or cancel projects.

Regulatory Uncertainty: While regulations generally trend stricter, enforcement intensity can vary with political changes. A deregulatory environment could reduce demand urgency.

Project Execution: Large engineered systems carry execution risk. Cost overruns, delays, or customer disputes could impact profitability on specific projects.

XV. Key Performance Indicators to Monitor

For investors following CECO Environmental, three metrics deserve particular attention:

1. Orders-to-Revenue Ratio (Book-to-Bill)

This metric measures new orders received relative to revenue recognized. A book-to-bill ratio consistently above 1.0 indicates growing backlog and future revenue visibility. CECO's recent quarters have shown exceptional book-to-bill performance: - Q4 2024: Orders of $219M vs. revenue of $159M (1.38x) - Q1 2025: Orders of $228M vs. revenue of $177M (1.29x)

Sustained book-to-bill above 1.2x suggests demand exceeding current execution capacity—a positive signal for growth but potentially a constraint on near-term revenue recognition.

2. Adjusted EBITDA Margin

This metric captures operating profitability before the impact of acquisition-related amortization and integration costs. Management targets margin expansion as scale increases and integration synergies materialize. The trajectory from approximately 11% in 2024 toward the 13% implied by 2025 guidance demonstrates progress toward the margin profile of best-in-class industrial companies (typically 15-20%).

3. Backlog Composition and Duration

Understanding the composition of CECO's $600+ million backlog provides insight into revenue quality and visibility. Key questions include: - What portion is contracted vs. expected but not yet booked? - What is the typical conversion timeline from backlog to revenue? - How much relates to large multi-year projects vs. shorter-cycle business? - What is the margin profile of current backlog relative to historical norms?

XVI. Conclusion: The Hidden Champion Emerging

CECO Environmental's story is one of patient transformation—from a fragmented collection of niche industrial businesses into a focused environmental solutions provider positioned at the intersection of regulatory compliance, industrial efficiency, and the energy transition.

The company's competitive position benefits from meaningful barriers to entry (engineering expertise, customer relationships, installed base), moderate switching costs, and emerging scale advantages from programmatic M&A. The strategic focus on Air, Water, and Energy Transition aligns capital allocation with secular growth drivers that should persist regardless of near-term economic fluctuations.

Management quality represents a key differentiator. Todd Gleason's pedigree from elite industrial companies like Honeywell and Pentair, combined with his demonstrated execution at CECO, provides confidence that the company can navigate the challenges inherent in acquisition-driven growth.

The bear case centers on execution risk—integrating multiple acquisitions while maintaining service quality for demanding industrial customers requires exceptional organizational capability. The leverage taken on to fund growth amplifies both the upside and downside scenarios.

For investors seeking exposure to environmental compliance and industrial decarbonization trends, CECO offers a differentiated vehicle: a pure-play provider of mission-critical solutions with demonstrated growth momentum, improving margins, and a management team executing a clear strategic vision.

The company that traces its heritage to 1869's Dean Brothers Pump Company has reinvented itself for the environmental and energy challenges of the 21st century. Whether it can successfully navigate the transition from small-cap specialist to billion-dollar industrial platform represents the investment question that will define shareholder returns in the years ahead.

The hidden champion is emerging into the light. The question is whether it can sustain the momentum that has brought it this far.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube