Regal Rexnord: The Quiet Industrial Compounder That Became a Motion Control Powerhouse

I. Introduction & Episode Roadmap

Picture this: a global manufacturing colossus with approximately $6 billion in annual sales, 30,000 employees scattered across five continents, and products humming inside virtually every variable-speed HVAC system in American homes. Regal Rexnord Corporation, with approximately $6 billion in sales and 30,000 employees, is a global leader focused on creating a better tomorrow with sustainable solutions that power, transmit, and control motion.

The company's business purpose sounds almost poetic for an industrial manufacturer: "Creating a better tomorrow by energy-efficiently converting power into motion." But behind that polished mission statement lies one of the most remarkable industrial transformation stories in American manufacturing history.

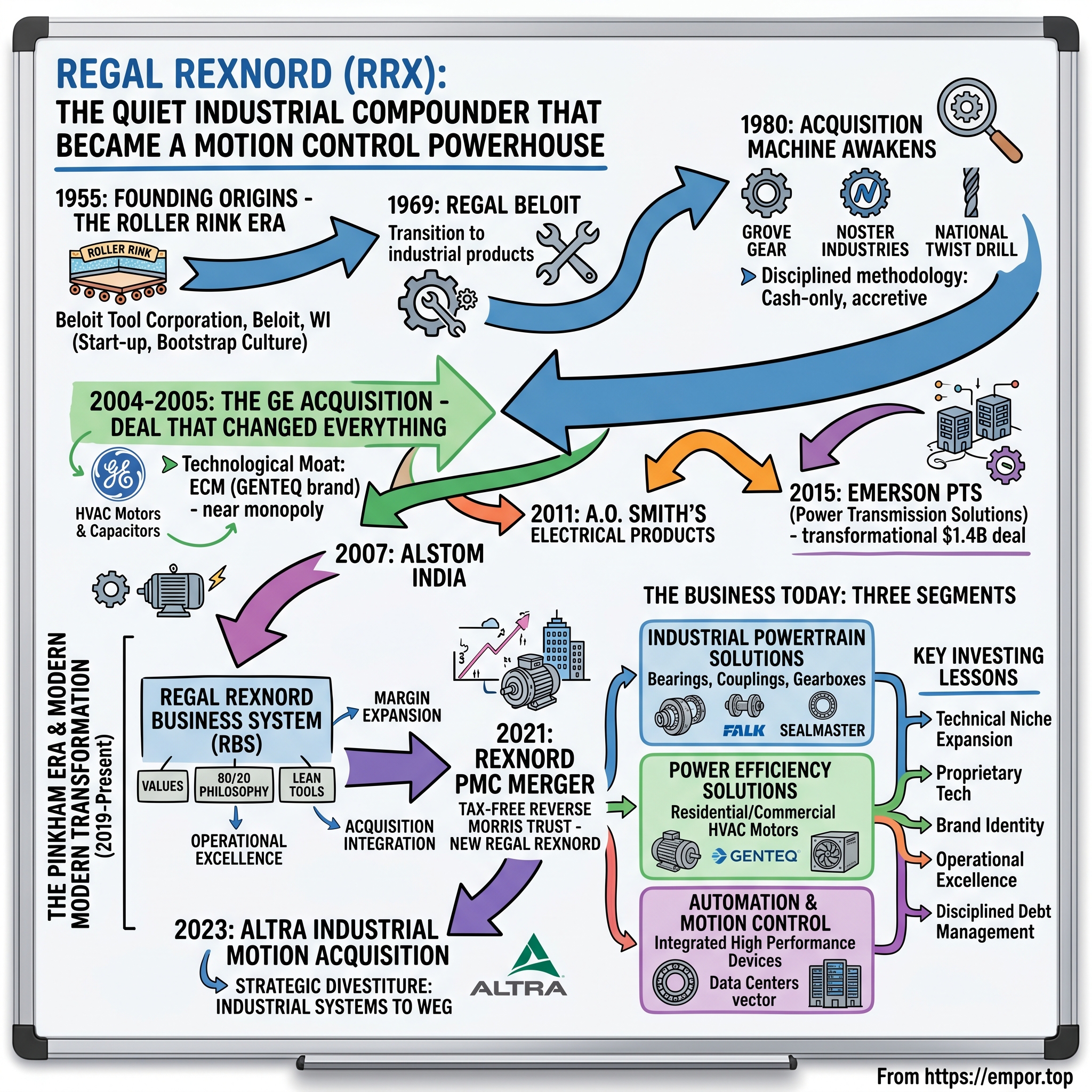

The company was founded in 1955 as Beloit Tool Corporation, and began operations in a converted roller rink. From those humble origins making cutting tools in small-town Wisconsin, Regal Rexnord has executed what might be the most disciplined industrial roll-up strategy of the past half-century.

A key part of the company's growth can be attributed to the 69 acquisitions it successfully completed since 1955, including multiple acquisitions that catapulted the company into the power transmission, electric motor, electric generator and customer electronic controls businesses.

This is not a story of a single brilliant acquisition or one visionary founder. Instead, it represents a masterclass in what professional investors call "compounding"—the patient accumulation of businesses, capabilities, and competitive advantages over decades, executed with financial discipline that would make Warren Buffett nod approvingly.

The central thesis here is that Regal Rexnord demonstrates how a disciplined industrial roll-up strategy, combined with rigorous 80/20 execution and strategic portfolio transformation, can create enduring shareholder value in businesses most people never think about. The motors inside your air conditioner, the bearings in your car's engine, the conveyor belts moving your Amazon packages—Regal Rexnord likely made something inside all of them.

II. Founding Origins: The Roller Rink Era (1955–1980)

Beloit, Wisconsin in 1955 was a quintessential Midwestern manufacturing town—population around 30,000, situated along the Rock River, about 90 miles from both Chicago and Milwaukee. The region had long been a hub for machinery and tool manufacturing, benefiting from access to Great Lakes shipping routes and a skilled workforce shaped by decades of industrial tradition.

The company's roots, established more than half a century ago, originated in the domestic manufacture of metal cutting tools and gear boxes. In 1955 it was known as Beloit Tool and set up shop in a roller rink in Beloit, Wisconsin.

The roller rink detail is not mere corporate mythology—it speaks to the bootstrapped origins of so many successful industrial enterprises. Initially operating from a garage with a small team, the company quickly relocated to an abandoned roller-skating rink due to rapid demand for its products. The founders found a building with high ceilings and adequate floor space at a bargain price, repurposing it for manufacturing. It was the kind of practical, no-nonsense decision that would characterize the company for decades.

In 1961, it moved to facilities in South Beloit, Illinois, and in 1969 it changed its name to Regal Beloit. The name change signified the company's transition beyond its original toolmaking roots toward a wider array of industrial products.

In 1973 Taylor officially changed Beloit Tool's name to Regal-Beloit (after, some said, a type of flower) and continued his strategy of expanding its market share and diversifying its business niche by acquiring promising companies in its basic power transmission and cutting tools lines.

This period represented the company's first foray into the acquisition strategy that would define its future. The U.S. power transmission market had traditionally been fragmented among dozens of smaller manufacturers, and the pickings for an acquisition-minded, cash-heavy firm like Regal-Beloit seemed ripe. In its cutting tool segment alone, Regal-Beloit had already absorbed such small players as Empire Gage, Walter T. Cole, Waukegan Quality Tool Works, and others.

Turning to the power transmission segment, in mid-1978, Taylor purchased Orbmark Company, the developer of a high-torque, low-speed hydraulic motor. This acquisition marked a crucial pivot point—the company was no longer just making static cutting tools but was entering the business of motion, of moving parts, of power transmission.

In 1980, sales were about $40 million—impressive at the time—however, the company had bigger aspirations. That $40 million in sales may seem modest by today's standards, but for a regional manufacturer that had started in a roller rink just 25 years earlier, it represented remarkable progress. More importantly, the company had developed both the manufacturing expertise and the acquisition muscle to pursue far more ambitious growth.

What made this early era significant was not just the financial performance but the DNA it established: a culture of operational excellence, acquisition discipline, and relentless focus on industrial markets where quality and reliability mattered more than brand marketing or consumer whimsy. These foundations would prove essential as the company entered its most aggressive growth phase.

III. The Acquisition Machine Awakens (1980–2003)

The early 1980s brought new leadership and a dramatically accelerated acquisition strategy that would transform the regional tool maker into a national industrial powerhouse.

James L. Packard and Henry W. Knueppel joined the company and initiated an aggressive acquisition strategy to expand our business. Packard's background was unusual for an industrial CEO—he was a seasoned corporate manager from PepsiCo's Frito-Lay division. He joined Regal-Beloit Corporation in 1979 and was elected President in 1980.

This consumer packaged goods background proved oddly beneficial. Packard understood brands, distribution, and the importance of scale—lessons he brought from snack foods into industrial manufacturing. He was elected Chief Executive Officer in 1984 and took on the additional responsibilities as Chairman of the Board in April 1986.

Taylor's ambitious acquisition program continued in the 1980s. Twelve firms were purchased and absorbed during the decade, substantially expanding the firm's market share, manufacturing capability, and profitability.

What distinguished Regal-Beloit's acquisition approach was its disciplined methodology. As James Packard later commented, "by quickly instituting effective cost controls, more efficient manufacturing methods and our strong customer service philosophy, these new divisions became strong contributors to the company's overall performance." Moreover, by holding out for a reasonable selling price, paying only cash (rather than stock), and considering only firms that could generate earnings in the first year following acquisition, Regal-Beloit recuperated its acquisition costs quickly.

This cash-only, immediate-accretion discipline was remarkably sophisticated for the era. While many industrial roll-ups of the 1980s loaded up on debt and issued dilutive stock, Regal-Beloit maintained financial discipline that would allow it to weather multiple economic cycles without existential crises.

Regal-Beloit's 1980s buying spree commenced in 1981 with the acquisition of Grove Gear of Union Grove, Wisconsin, a manufacturer of standard and special worm gear speed-reducing gear boxes, adaptors, and accessories, founded in 1947.

The company systematically built capabilities across both cutting tools and power transmission. Packard returned to the acquisition waters again in 1985 with the purchase of Noster Industries Inc. of Michigan and National Twist Drill of Columbia, South Carolina, a producer of large-volume drills, taps, end mills, gages, and reamers.

By its 30th anniversary year, Regal-Beloit was employing 1,250 people working out of 18 manufacturing and customer service facilities nationwide. Packard led its large facilities through a major improvement program, incorporated new products and related manufacturing equipment into the company's plants, and began a systematic workforce flexibility program in which nearly a third of Regal-Beloit's employees were training for new positions at any given time.

This investment in workforce flexibility foreshadowed what would later become the company's embrace of lean manufacturing principles. Rather than treating workers as interchangeable cogs, the company invested in cross-training that made facilities more adaptable and employees more valuable.

The 1990s continued the acquisition cadence. With sales arcing past $152 million, two more acquisitions—hydraulic pump drive manufacturers Hub City, Inc. of Aberdeen, South Dakota, in April 1992 and Terrell Gear Drives, Inc. of Charlotte, North Carolina, in November—boosted Regal-Beloit's sales to $199.8 million by year-end.

By this point, Regal-Beloit had established a distinctive multi-brand, multi-channel distribution model. Rather than consolidating acquisitions under a single brand, the company maintained individual brand identities—Marathon Electric, Leeson, Hub City, Grove Gear, and others—each with established customer relationships and distribution networks. This approach preserved customer loyalty while extracting back-office synergies.

By the end of 2004, approaching the company's 50th year of operation, annual sales reached $756 million. From $40 million in 1980 to $756 million in 2004 represented nearly 20-fold growth over 24 years—a compound annual growth rate of approximately 13%, sustained through multiple economic cycles.

The company entered its 50th year having transformed from a regional cutting tool manufacturer into one of the largest motor and power transmission manufacturers in North America. But management recognized that the next phase of growth would require a different magnitude of transaction.

IV. The GE Acquisition: The Deal That Changed Everything (2004–2005)

If the first five decades of Regal-Beloit's history could be characterized as patient accumulation, 2004 marked the moment of transformation. In that single year, the company executed an acquisition that didn't just accelerate growth—it fundamentally redefined what the company was.

Regal acquired General Electric's Commercial and HVACR Motors and Capacitors businesses in 2004. These acquisitions from General Electric effectively doubled Regal's size.

The strategic logic was compelling. GE, in the midst of its own portfolio transformation under CEO Jeffrey Immelt, was shedding industrial businesses that no longer fit its vision. Motors, while essential products, didn't carry the profit margins or growth potential that GE sought. For Regal-Beloit, these same businesses represented transformational opportunities.

On December 31, 2004, REGAL-BELOIT Corporation acquired from several subsidiaries of General Electric Company selected assets and assumed certain liabilities of GE's Heating, Ventilation and Air Conditioning/Refrigeration (HVAC) motors and capacitors businesses.

The transaction structure was notable. As consideration for the Acquisition, the Company paid to GE at closing approximately $400 million, consisting of $270 million in cash and the issuance of 4,559,048 shares of common stock. This was Regal-Beloit's first major use of equity in an acquisition—a departure from its cash-only tradition, but justified by the transformational nature of the deal.

On December 31, 2004, the company issued 4,559,048 shares of common stock to GE in connection with the acquisition of its HVAC motors and capacitors businesses. As of August 10, 2005, GE's ownership of the common stock represented approximately 15.7% of shares outstanding.

What made this acquisition particularly valuable was the proprietary technology it included. General Electric developed an Electronically Commutated Motor (also called Electronically Controlled Motor), or ECM, technology for use in residential and light commercial heating and air conditioning systems in North America in the mid-1980s. The GE ECM motor was the first ultra-high efficiency motor for home heating and air conditioning systems, providing greater home comfort and energy efficiency.

This ECM technology represented a genuine technological moat. The newly acquired, patented ECM technology utilizes a brushless DC electric motor with integrated speed control made possible through sophisticated electronic and sensing technology. ECM motors provide many attractive performance characteristics versus competitive variable speed solutions, including motor life, noise and energy efficiency.

James L. Packard, CEO and chairman of Regal-Beloit, stated, "We are tremendously excited to announce this acquisition. The acquisition of GE's HVAC/Refrigeration motor and capacitor operations is another significant step in our strategy to expand our end markets and product offering."

"Additionally, the acquisition adds four outstanding facilities to our manufacturing footprint and continues our strategy to expand our manufacturing capabilities on a global basis. We are also excited about the potential for the leading edge ECM technology that is a part of this transaction."

"It's not often that a company can make an acquisition that will double its size," Packard acknowledged. The acquisition was indeed rare in its impact, not just doubling revenues but fundamentally changing the company's competitive position in the HVAC motor market.

As part of that acquisition, Regal acquired the rights to use the GE brand through 2009. Nearing the end of that licensing period, Regal rebranded these divisions as Genteq in February 2009.

The Genteq rebranding was a critical strategic decision. Rather than losing the brand equity associated with GE motors, the company invested in building Genteq as a standalone brand with its own identity. Genteq is the leading brand in Electronically Commutated Motor (ECM) technology used by all major HVAC system manufacturers for over 30 years.

One of the largest electric motor manufacturers in the world, its Genteq brand brushless DC electric motors are found in almost all variable-speed residential HVAC equipment in the United States today.

That phrase—"almost all"—captures the extraordinary market position the company achieved. The GE acquisition didn't just add revenues; it created near-monopoly positioning in a critical segment of the HVAC industry. When virtually every major HVAC manufacturer uses your motors, you've achieved the kind of market position that compounds value for decades.

V. Building Scale: The 2007–2015 Acquisition Spree

Following the transformational GE acquisition, Regal-Beloit entered a sustained period of bolt-on acquisitions that extended its global reach while deepening its capabilities in both motors and power transmission.

In 2007, Regal Beloit corporation USA acquired Alstom India Motors and Fans business and named it Marathon Electric Motors India Limited. This established the company's manufacturing presence in one of the world's largest industrial markets.

In October 2008, Regal acquired the Dutchi Motors B.V. for $34 million in cash and $3.2 million in net liabilities. Dutchi expanded Regal's European motor manufacturing capabilities, providing a local production base to serve Continental customers.

In April 2010, the company acquired CMG Engineering Group, a manufacturer of industrial motors, blowers and metal products headquartered in Melbourne, Australia, for $75 million in cash. The Australian acquisition extended reach into Asia-Pacific markets.

But the most significant transaction of this period came in 2011. In 2011, the company completed the largest acquisition in its history by purchasing A.O. Smith's Electrical Products Company. This acquisition added about $700 million in sales revenues, and further expanded the company in Mexico and China, while adding new products to its production lines.

The A.O. Smith deal was another transformational transaction. A.O. Smith was shedding its electrical products business to focus on water heating, where it had stronger competitive positioning. For Regal-Beloit, the acquisition reinforced its position as the dominant player in fractional horsepower motors while significantly expanding its manufacturing footprint in low-cost regions.

Then came 2015, and another company-defining acquisition. Regal Beloit Corporation announced it had entered into a definitive agreement to acquire the Power Transmission Solutions business ("PTS") of Emerson Electric Co. for approximately $1.4 billion comprised of $1.4 billion in cash plus $40 million of assumed liabilities. "This acquisition will be transformational for Regal. PTS will broaden our portfolio, diversify our end market exposure and strengthen our global footprint," commented Chairman and CEO Mark Gliebe.

Mark Gliebe had succeeded Packard as CEO, maintaining the acquisition-led growth strategy while bringing his own operational focus to the enterprise.

PTS is a global leader in highly engineered power transmission products and solutions. The business manufactures, sells and services bearings, couplings, gearing, drive components, and conveyer systems under industry leading brands including Browning, Jaure, Kop-Flex, McGill, Morse, Rollway, Sealmaster and System Plast. With annual revenues of approximately $600 million, PTS has over 3,000 employees around the world.

Regal management estimated 2015 accretion between $0.40 and $0.60 per share including purchase accounting adjustments and closing costs, and 2016 accretion between $0.95 and $1.15 per share. Transaction synergies were estimated to be $30 million within a four-year period.

The Emerson PTS acquisition was strategically brilliant. Emerson, like GE before it, was reshaping its portfolio and shedding businesses that didn't fit its long-term vision. "While the Power Transmission Solutions business no longer aligns with the strategic direction of our portfolio, it is a strong business with an outstanding management team that has created significant value while part of Emerson," said Chairman and Chief Executive Officer David Farr. "This transaction allows us to better focus on our value creation priorities and provides Regal Beloit with a unique opportunity to strengthen and grow its mechanical power transmission segment."

By the end of 2015, the company's total sales were $3.5 billion. In a decade, the company had more than quadrupled its revenues through disciplined acquisition.

The portfolio now spanned electric motors, generators, power transmission components, and a growing array of controls and automation products. Regal-Beloit was no longer just a motor company or just a power transmission company—it was becoming a comprehensive industrial powertrain solutions provider.

VI. The Pinkham Era & Modern Transformation (2019–Present)

Louis Pinkham arrived at Regal Beloit in April 2019 with a mandate for change. The company had grown substantially through acquisitions but needed operational transformation to realize the full potential of its assembled portfolio.

Louis Pinkham joined Regal Rexnord Corporation (formerly Regal Beloit Corp.) on April 1, 2019, as the Chief Executive Officer, and joined the Board of Directors on May 1, 2019.

Pinkham's background was perfectly suited for the task ahead. Prior to Regal Rexnord, Louis joined Crane Co., a manufacturer of highly engineered industrial products, in October 2012 as Group President, Fluid Handling. From 2016 to 2019, Louis held the position of Senior Vice President with responsibility for three of Crane's four reporting segments. Prior to joining Crane Co., Louis was Senior Vice President and General Manager of the Critical Power Solutions Division, Electrical Group at Eaton Corporation. From 2000 to 2012, he held successive and increasing roles of global responsibility at Eaton, including General Manager, Electrical Group for North Asia based in China; and Managing Director of the Electrical Group based in Switzerland.

Louis is a graduate of Duke University with a Bachelor of Science in Engineering. He also holds a Master of Engineering Management from Northwestern University's McCormick School of Engineering and a Master of Business Administration from the Kellogg Graduate School of Management.

The combination of engineering expertise, global operating experience at major industrial companies, and top-tier business education positioned Pinkham to both understand the technical details of Regal's products and drive the operational transformation needed to improve margins.

Pinkham quickly set ambitious goals. The company had historically operated with margins below industry leaders, and Pinkham saw substantial opportunity for improvement through what the company called the "300-in-3" margin expansion program.

Then came the transformational merger that would create Regal Rexnord. In February 2021, Regal Beloit Corporation announced a definitive agreement to merge with Rexnord Corporation's Process & Motion Control (PMC) business in a tax-free Reverse Morris Trust transaction valued at $3.69 billion, comprising $3.32 billion in Regal stock and the assumption of $370 million in net debt.

The merger closed on October 4, 2021, forming Regal Rexnord Corporation as the combined entity.

Regal shareholders will own 61.4% and Rexnord shareholders will own 38.6% of the combined entity ("New Regal"), before a potential dividend to Regal shareholders and a corresponding ownership adjustment to Rexnord shareholders.

CEO Louis Pinkham commented, "The addition of PMC is a tremendous positive step forward in Regal's ongoing transformation, positioning our company – the new Regal Rexnord – better than ever before, to create significant value for all our key stakeholders. We will provide the industry's most complete Industrial Powertrain solutions – comprised of our high-efficiency motors and critical power transmission components – to enable a range of efficiency and productivity gains for our customers. Our shareholders will benefit from a business that we expect will be faster-growing, higher-margin and more cash generative."

The Rexnord PMC merger had profound strategic logic. The combination with PMC fills gaps in Regal's PTS portfolio, creates a more compelling partner for distributors, and enables Regal to provide complete drive train solutions across all major applications for customers.

In addition to the significant, ongoing restructuring that has been underway at legacy Regal, which has resulted in material margin expansion over the last two years, including hitting the Company's "300-in-3" margin expansion program goal over a year ahead of schedule, the new Regal Rexnord expects to realize $120 million of cost synergies over the next three years related to the merger with PMC. The merger synergies are expected to drive over 500 basis points of adjusted EBITDA margin expansion by 2024.

Less than two years later, Regal Rexnord executed an even larger deal. On March 27, 2023, Regal Rexnord Corporation announced it had completed the acquisition of Altra Industrial Motion Corp. (Nasdaq: AIMC), closing the deal that was signed on October 26, 2022.

Regal Rexnord acquired 100% of Altra shares in an all cash transaction for US$62.00 per share. The transaction, which was signed on October 26, 2022, closed on March 27, 2023. Sidley represented Regal Rexnord Corporation in its US$4.95 billion acquisition of Altra Industrial Motion Corp.

"The addition of Altra will mark an important milestone in Regal Rexnord's ongoing journey to become a higher-performing enterprise, and one with a more balanced portfolio of differentiated products and solutions that solve our customers' challenges by 'energy-efficiently converting power into motion,'" said Regal Rexnord CEO Louis Pinkham. "The automation business has highly attractive growth prospects and margins, serving many markets that have anticipated secular growth tailwinds, including factory automation, medical, aerospace, and warehouse & logistics. The transaction also significantly enhances our power transmission portfolio, in particular our industrial powertrain offering, by adding complementary products in brakes, gears, and clutches."

Based in Braintree, Massachusetts, Altra has more than 9,000 associates and 47 production facilities in 17 countries around the world and generates $1.9 billion in sales.

Altra is the parent company of several power transmission industry brands, including: Ameridrives, Boston Gear, Warner Electric, TB Wood's, Stieber Clutch, Twiflex, Matrix International and Wichita Clutch.

But Pinkham's transformation wasn't just about acquiring. In September 2023, the company made a strategic divestiture that reshaped its portfolio. In September 2023, the company sold its industrial electric motors and generators business of the Marathon, Cemp, and Rotor brands to rival WEG S.A. for $400M.

This divestiture was counterintuitive on the surface—why would a motor company sell motor businesses? The answer lay in portfolio optimization. "I am proud of what our Industrial team has accomplished in the last few years. Through their disciplined deployment of 80/20 and rigorous use of lean tools, adjusted EBITDA margins for the business have improved by roughly 700 basis points. The business is also growing nicely, aided by share gains, which is evident in recent revenue and orders performance."

Since the merger of Regal Beloit and Rexnord in 2021, Regal Rexnord has struggled to maintain its competitiveness in the low voltage motor market, losing market share every year since the merger's announcement. To Regal's competition, it quickly became clear that the new company was not interested in expanding its industrial motors business and was instead focused on building capabilities more aligned with segments such as HVAC/R and material handling.

The Industrial Systems divestiture allowed Regal Rexnord to focus resources on higher-margin, higher-growth segments while WEG—a Brazilian motor manufacturer with global ambitions—could better invest in the industrial motor business.

Then came the most surprising news. On October 29, 2025, Regal Rexnord Corporation announced the planned departure of CEO Louis Pinkham as part of a CEO succession process. Pinkham, who has led the company since April 2019, will remain in his role until March 31, 2026, or until a successor is appointed, ensuring a smooth transition.

Louis Pinkham, CEO since April 2019, will remain in place until a successor is named and will resign from the Board upon appointment. During Pinkham's tenure the company says enterprise value rose to $15 billion from about $4.5 billion and total shareholder return was nearly 100% (inclusive of reinvested dividends).

"It has been an immense honor to lead the Company for the past six plus years. I believe the Company's business and team are strong and that now is a good time for a new leader to drive the next chapter for Regal Rexnord. I look forward to continuing to lead the Company until the Board identifies my successor," said Louis Pinkham, Chief Executive Officer.

The Pinkham era transformed Regal from a collection of acquired businesses into a cohesive industrial powerhouse. The question now is whether his successor can maintain the momentum.

VII. The Business Today: Understanding the Three Segments

Regal Rexnord is comprised of three operating segments: Industrial Powertrain Solutions, Power Efficiency Solutions, and Automation & Motion Control.

Regal Rexnord, with 2024 sales of $6.0 billion, and 30,000 associates around the world, helps create a better tomorrow by providing sustainable solutions that power, transmit and control motion.

Industrial Powertrain Solutions (~37% of sales)

Industrial Powertrain Solutions is expected to consist of the majority of the current Motion Control Solutions segment, excluding the conveying and aerospace business units, plus Altra's Power Transmission Technologies segment. The segment is led by Jerry Morton, Executive Vice President and President, Industrial Powertrain Solutions, who most recently served as President - Integration for MCS. Morton's prior experience includes four years leading the legacy Regal PTS business prior to the 2021 merger with Rexnord PMC, and 28 years in various management and leadership roles at Emerson.

This segment represents the heart of Regal Rexnord's industrial offerings—the bearings, couplings, gearboxes, and drive components that keep industrial machinery running. The Industrial Powertrain Solutions segment provides mounted and unmounted bearings, couplings, mechanical power transmission drives and components, gearboxes, gear motors, clutches, brakes, special, and industrial powertrain components and solutions for metals and mining, general industrial, energy, alternative energy, machinery/off-highway, discrete automation, and other markets.

The merger will create a company that serves industrial-powertrain customers, and it will market brands from Regal and Rexnord PMC, including Regal's Browning, Grove Gear, Hub City, Jaure, Kop-Flex, McGill, ModSort, Sealmaster and System Plast brands, as well as PMC's Berg, Cambridge, Centa, Falk, Rexnord and Stearns brands.

Power Efficiency Solutions (~31%)

Power Efficiency Solutions is expected to consist of the current Climate Solutions and Commercial Systems businesses.

Products enable the fans in HVAC systems that keep us comfortable; the power source that keeps smart buildings running; agricultural and food service equipment that keeps us fed; and conveyor systems that keep e-commerce flowing.

This segment contains the crown jewel Genteq brand and serves the residential and commercial HVAC markets. It also includes commercial motors for refrigeration, pumps, and other applications.

Automation & Motion Control (~24%)

Producers of industry-leading integrated high performance precision motion control devices including miniature motors, linear systems, and precision automation systems. Additionally, this business provides end-to-end conveying systems, aerospace components, and remote condition monitoring solutions.

In particular, the pro forma Automation & Motion Control business, with 2022 sales of ~$1.7 billion, is anticipated to have at least 70% of its sales generated in end markets with secular growth characteristics. It is anticipated that a significant share of new product development investments will be directed to support the needs of customers in these markets.

This segment represents Regal Rexnord's highest-growth opportunity, benefiting from secular tailwinds in factory automation, medical devices, aerospace, and data centers.

The Brand Portfolio

Together, we offer a comprehensive product portfolio that enables Regal Rexnord to provide more complete power transmission capabilities and automation solutions. Our brands are better together. And together, we're creating a better tomorrow. Explore our family of brands below.

The multi-brand strategy remains central to Regal Rexnord's approach. Rather than consolidating everything under a single brand, the company maintains distinct brand identities for different product categories and end markets.

VIII. The Regal Rexnord Business System & 80/20 Philosophy

At the core of Regal Rexnord's operational approach is the Regal Rexnord Business System (RBS), an enterprise-wide framework that combines 80/20 principles with lean manufacturing tools.

With the Regal Rexnord Values at its core, the Regal Rexnord Business System enables leadership and engagement from each Regal Rexnord associate to progress 80/20 focused growth and performance excellence. The Regal Rexnord Business System, together with our management cadence, drives the achievement of our company-wide goals through facilitated and effective goal alignment, collaborative problem-solving, and sharing of best practices, tools, skills and expertise.

The 80/20 principle—the idea that 80% of results come from 20% of inputs—is not just a slogan at Regal Rexnord but a systematic approach to prioritization. Leaders lead and drive the Regal Rexnord Business System which includes 80/20, lean principles, and Continuous Improvement. They must be skilled and experienced in decomposing a strategic vision into actionable strategies and tactics, that can be cascaded to every manufacturing facility.

We call it the Regal Rexnord Business System (RBS), and it drives every aspect of our culture and performance. We use RBS to guide what we do, measure how well we execute, and create options for doing even better - including improving RBS itself. Fueled by Regal Rexnord's core values, the RBS engine drives the company through a never-ending cycle of change and improvement: exceptional people develop outstanding plans and execute them using world-class tools to construct sustainable processes, resulting in superior performance.

What makes the RBS particularly powerful is its role in acquisition integration. Unites aligned cultures with deep commitment to 80/20 and Lean principles. The businesses share cultures focused on serving customers and driving operating efficiencies. Leveraging Regal Rexnord's competencies in 80/20 and lean, and building on its successful integration of Rexnord PMC, the acquisition presents an opportunity to further optimize the combined company's global operating model, which in turn can support greater investment in the business to drive profitable growth.

The results speak for themselves. CEO Louis Pinkham commented, "Our team's controllable execution was strong in the third quarter, most evident in healthy adjusted gross and EBITDA margin gains, and clear signs of market outgrowth in our largest and highest-margin segment, Industrial Powertrain Solutions. As a Company, we delivered record adjusted gross margins of 38.4%, providing clear line of sight to our goal of 40% exiting 2025. A record high adjusted EBITDA margin of 22.8% was up 110 basis points versus prior year and aligned with our goal of 25% exiting 2025."

Regarding 2024, it continued to be a year of transformation, as we further evolved the portfolio through the divestiture of the Industrial Systems business, which along with our synergies helped us achieve a record adjusted gross margin of 37.8%, a year-over-year improvement of 210 basis points.

IX. Playbook: Business & Investing Lessons

Regal Rexnord's seven-decade journey offers a masterclass in industrial roll-up execution. Several key lessons emerge:

1. Start with Technical Niche, Then Expand Adjacently

The company began with cutting tools and gearboxes—products requiring precision manufacturing and engineering expertise. These capabilities transferred naturally to motors, then to power transmission, then to automation. Each step built on existing competencies rather than leaping into unfamiliar territory.

2. Buy Proprietary Technology From Giants Exiting Markets

The GE ECM acquisition remains the defining example. When major conglomerates divest non-core businesses, they often undervalue specialized technologies that don't fit their strategic vision. Regal capitalized on this dynamic repeatedly with GE, A.O. Smith, Emerson, and Rexnord.

3. Maintain Brand Identity Through Multi-Brand Strategy

Unlike many roll-ups that consolidate brands, Regal Rexnord maintains individual brand identities. Customers who have specified Marathon motors for decades don't want to switch to an unfamiliar brand. Preserving these relationships while extracting back-office synergies is a delicate but valuable balance.

4. Apply Operational Excellence Consistently

"We see tremendous upside from bringing Regal Rexnord's 80/20 skillset, partnered with both companies' continuous improvement mindset, and a disciplined plan-do-check-act (PDCA) management approach — producing a broader offering and higher service levels for our customers, growth opportunities for our associates, and compelling expected financial returns for our shareholders."

5. Disciplined Debt Management Post-Acquisition

The company paid down $205 Million of gross debt in Q4. Net Debt/Adjusted EBITDA (Including Synergies) of ~3.6x.

"I am also extremely pleased that we were able to pay down $938 million of gross debt in the year. Mr. Pinkham concluded, 'We are starting the year managing a number of uncertainties, with some of our key markets still under pressure, headwinds around currency, and unknowns related to potential tariffs and other regulatory changes.'"

6. Know When to Divest

The Industrial Systems sale to WEG demonstrated that successful compounders aren't just buyers—they recognize when assets would be worth more to others. Selling a growing, profitable business might seem counterintuitive, but it freed resources for higher-return opportunities.

Capital Allocation and Financial Targets

The company maintained its 2024 guidance with sales of $6.2 billion and adjusted diluted EPS of $9.40 to $9.80, but now expects results in the lower half of the range. For 2024-2027, RRX targets: organic net sales growth at 2% to 5% CAGR, adjusted gross margins rising to ~40% by 2025, adjusted EBITDA margins increasing to ~25% by 2025, adjusted diluted EPS growth at low double-digit CAGR, adjusted free cash flow margins in low- to mid-teens by 2027, and net leverage declining to ~2.5x in 2025 and 1.5-2.0x by 2027.

X. Porter's Five Forces & Hamilton's 7 Powers Analysis

Understanding Regal Rexnord's competitive position requires examining both the industry structure and the sources of sustainable advantage.

Porter's Five Forces Analysis

Threat of New Entrants: LOW

The barriers to entry in industrial motors and power transmission are formidable. Capital intensity for precision manufacturing facilities runs into hundreds of millions of dollars. One of the largest electric motor manufacturers in the world, its Genteq brand brushless DC electric motors are found in almost all variable-speed residential HVAC equipment in the United States today. This near-monopoly position in key segments would take decades for a new entrant to challenge.

Moreover, OEM qualification cycles often span years. A motor or bearing specified into an industrial machine becomes effectively locked in for the product's lifetime. New entrants would need to invest heavily in R&D to develop proprietary technologies like ECM, then spend years qualifying with major OEMs—all while competing against an entrenched incumbent with established relationships.

Bargaining Power of Suppliers: MODERATE

Raw material inputs—copper, steel, aluminum, rare earth magnets—are commodity-like and sourced from multiple suppliers globally. The company's global manufacturing footprint provides sourcing flexibility, and scale provides negotiating leverage.

However, rare earth magnets used in high-efficiency motors present a potential vulnerability. These materials are primarily sourced from China, creating geopolitical supply risk. Tariff cost neutrality is targeted by mid-next year, with margin neutrality by year-end.

Bargaining Power of Buyers: MODERATE

Regal Rexnord's customers include major OEMs who have considerable purchasing power. However, switching costs are significant due to product specifications, certifications, and long qualification cycles. Today, only about 20% of our customers buy more than one of our products. If you're buying one of our products, you're likely buying all of them. The cross-sell opportunity here is significant. To date, 2025, we'll see about $175 million of cross-sell with Regal and Rexnord and Altra on path to close to $250 million by the end of next year.

Threat of Substitutes: LOW TO MODERATE

Electric motors and mechanical power transmission have no readily available substitutes for most applications. The ongoing electrification trend actually benefits Regal Rexnord, as more applications require electric motors. However, in some applications, hydraulic or pneumatic systems can substitute for electric motors, and some power transmission can be replaced by direct-drive systems.

Competitive Rivalry: MODERATE

Key direct competitors include SKF, Siemens, ABB, and Timken. These companies offer similar products and services, directly competing with Regal Rexnord in various industrial applications.

WEG and Nidec are significant competitors in the electric motors market. They directly challenge Regal Rexnord's Power Efficiency Solutions segment. Their competitive strategies focus on efficiency, cost-effectiveness, and global distribution networks.

Regal Rexnord and WEG have historically been each other's most significant competition, overlapping heavily in many of their target verticals.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Significant scale advantages in manufacturing, purchasing, and R&D amortization. With 30,000 employees and $6 billion in sales, Regal Rexnord can spread development costs across a large revenue base.

Network Effects: Limited direct network effects, but the company's broad distribution network creates value for distributors who prefer to source multiple products from a single supplier.

Counter-Positioning: The company's 80/20-focused operating model and willingness to divest low-margin businesses represents counter-positioning versus conglomerates that prioritize revenue over returns.

Switching Costs: High switching costs in many applications. Motors and bearings specified into OEM products remain for the life of that product line. Changing suppliers requires requalification, testing, and regulatory approvals.

Branding: For more than 100 years, the Regal electric motor brands have kept the residential, commercial, and industrial marketplace in motion. Regal is a leading designer and manufacturer of single and three phase AC motors including NEMA and IEC enclosures, DC motors, gearmotors, low and medium voltage motors, and variable-speed control solutions.

Cornered Resource: The ECM technology acquired from GE represents a cornered resource—proprietary technology that competitors cannot easily replicate.

Process Power: The Regal Rexnord Business System guides our manufacturing, engineering, operations and sales business processes to provide the foundation for efficiency and innovation.

XI. Key Performance Indicators to Watch

For investors tracking Regal Rexnord's ongoing performance, three metrics deserve particular attention:

1. Adjusted Gross Margin

This metric captures the company's success in both pricing power and operational efficiency. The trajectory from 33% in 2022 toward the 40% target by year-end 2025 represents the clearest measure of portfolio transformation success. The company remains on track to achieve a 40% adjusted gross margin exiting 2025.

2. Net Leverage Ratio (Net Debt/Adjusted EBITDA)

With significant debt taken on through acquisitions, the pace of deleveraging indicates both cash flow generation capability and balance sheet health. Net leverage is targeted to decline to ~2.5x in 2025 and 1.5-2.0x by 2027.

3. Organic Sales Growth

While acquisitions have driven historical growth, organic growth demonstrates the health of the underlying businesses and the success of cross-selling initiatives. Organic net sales growth is targeted at 2% to 5% CAGR for 2024-2027.

XII. Bull Case vs. Bear Case

Bull Case

Secular Tailwinds: The Company's end markets benefit from meaningful secular demand tailwinds, and include factory automation, food & beverage, aerospace, medical, data center, warehouse, alternative energy, residential and commercial buildings, general industrial, construction, metals and mining, and agriculture.

Data centers represent a particularly compelling growth vector. Data center business is projected to double in the next two years, supported by a nearly billion-dollar pipeline. The electrification of everything—from vehicles to buildings to industrial processes—creates sustained demand for the motors and power transmission products that Regal Rexnord manufactures.

Margin Expansion: The path to 40% gross margins and 25% EBITDA margins is visible and largely under management control through 80/20 implementation and synergy capture.

Portfolio Quality: The divestiture of Industrial Systems and acquisition of Altra has reshaped the portfolio toward higher-margin, higher-growth businesses.

Deleveraging Capacity: Strong free cash flow generation supports rapid debt reduction, which will free up capital for share repurchases or additional acquisitions.

Bear Case

Leadership Transition Risk: Mr. Pinkham will remain as CEO until a successor is identified to facilitate an orderly leadership transition. Mr. Pinkham will resign from the Board at the time of the appointment of the new CEO. CEO transitions always introduce uncertainty, particularly for companies with acquisition-led growth strategies where personal relationships matter.

Cyclical Exposure: Despite diversification, Regal Rexnord remains exposed to industrial cycles. A manufacturing recession would pressure volumes across most segments.

Integration Risk: The Altra acquisition added complexity and debt. Full synergy realization takes years, and integration always carries execution risk.

China/Tariff Exposure: "We are starting the year managing a number of uncertainties, with some of our key markets still under pressure, headwinds around currency, and unknowns related to potential tariffs and other regulatory changes."

Rare Earth Dependency: High-efficiency motors require rare earth magnets, which are primarily sourced from China. Supply disruptions could impact production.

Competitive Dynamics

The Regal Rexnord industry faces competition from various companies. These include established players like Siemens, WEG, and The Timken Company.

The competitive environment is intensifying, particularly from WEG, which acquired Regal Rexnord's divested industrial motors business. WEG's $400 million acquisition of Regal Rexnord's industrial electric motors and generators business diversifies and strengthens its market position. WEG's handling post-pandemic supply chain constraints has led to a 2.5% growth in its low voltage ac motor market share since 2020, positioning it for potential market leadership.

XIII. Regulatory and Accounting Considerations

Energy Efficiency Regulations: Increasingly stringent energy efficiency standards for motors and HVAC equipment generally benefit Regal Rexnord, as higher standards require more sophisticated products where the company has technological advantages.

Tariffs: The company manufactures globally and faces potential tariff impacts on cross-border component flows. Management is actively working on tariff mitigation strategies.

Goodwill and Intangibles: With significant acquisition activity, the balance sheet carries substantial goodwill and intangible assets. Investors should monitor for impairment risk, particularly if acquired businesses underperform expectations.

Debt Covenants: Synergies expected to be realized in the future are included in the calculation of EBITDA that serves as the basis for financial covenant compliance for certain of the Company's debt. Covenant calculations include expected synergies, providing some cushion but also requiring continued synergy realization.

XIV. The Road Ahead

Regal Rexnord stands at an interesting inflection point. The Pinkham era transformed a collection of acquired businesses into a cohesive industrial powerhouse with clear strategic direction and improving financial performance. During his tenure, Mr. Pinkham led the transformation of the Company to become a global leader in automation and motion control, power transmission, and power efficiency solutions. As a result, and during his tenure, the enterprise value of the Company has increased to $15 billion from ~$4.5 billion, with a total shareholder return of nearly 100% (inclusive of reinvested dividends).

CEO Louis Pinkham said: "We see many opportunities to create significant value for shareholders by capitalizing on the strengths of our enterprise, which over the last five years we have dramatically transformed, through organic and inorganic actions, to be increasingly durable, high-margin, and cash generative. As we will discuss in some detail at our investor meeting today, our teams are working on a wide range of compelling initiatives to accelerate organic growth. We also see a clear path to top quartile gross, EBITDA and cash flow margins, ROIC expansion, and meaningful opportunities to create value through de-levering and, over time, inorganic growth. In short, we believe Regal Rexnord presents a highly compelling value creation opportunity, underpinned by lots of controllable execution."

The next chapter will be written by a new CEO inheriting a company with substantial competitive advantages, a transformed portfolio, and a proven operating system. The roller rink origins could not be further from where Regal Rexnord stands today—but the same Midwestern manufacturing values that characterized those early years remain embedded in the company's DNA.

For investors, Regal Rexnord represents a case study in how disciplined industrial compounding can create substantial shareholder value over time. The company may not make headlines like technology darlings, but the motors, bearings, and power transmission components it manufactures are the unglamorous guts of modern civilization—and that's precisely what makes the business so durable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube