PSEG: From Trolleys to Terawatts—The Transformation of America's First Utility Conglomerate

I. Introduction & Episode Roadmap

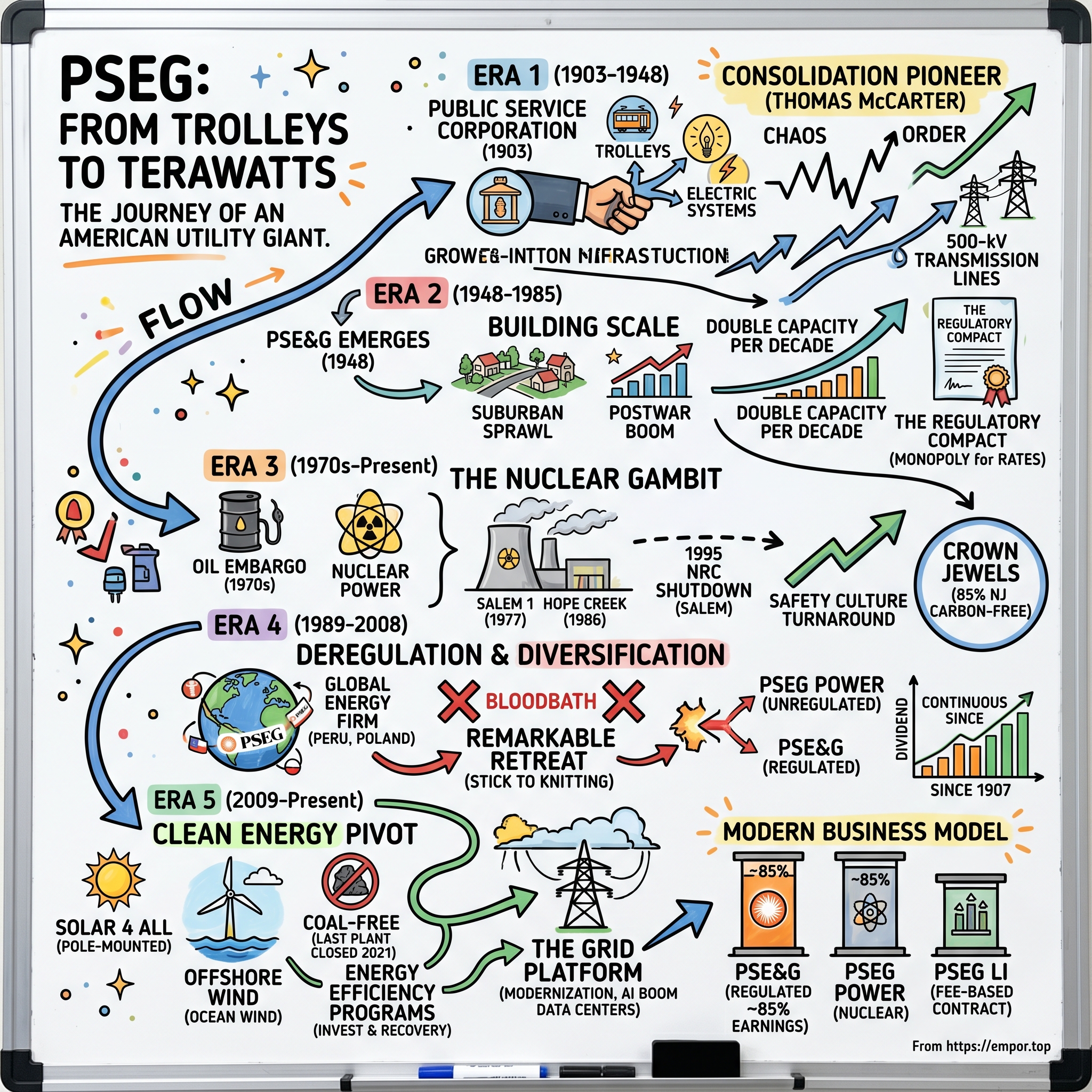

Picture this: It's 1903, and more than 400 separate companies are operating trolleys, gas lights, and primitive electric systems across New Jersey. Horse-drawn carriages share the streets with newfangled electric streetcars. Gas lamps flicker alongside experimental electric bulbs. Into this chaos steps Thomas McCarter, a lawyer with a vision to consolidate this patchwork into something extraordinary—what would become the Public Service Electric and Gas Company, today's PSEG.

Fast forward 121 years. That trolley operator is now one of America's ten largest electric companies, generating $10.29 billion in revenue in 2024, running nuclear reactors that provide 85% of New Jersey's carbon-free power, and managing electric infrastructure for 3.5 million customers from Newark to Long Island. The company that once debated whether electricity or gas would win now operates at the frontier of the clean energy transition, courting data centers hungry for reliable power while managing a $40.72 billion market cap that makes it larger than most tech unicorns.

How does a company survive—and thrive—through two world wars, the Great Depression, the atomic age, deregulation, climate change, and now the AI boom? How did a New Jersey trolley operator become a nuclear powerhouse and regulated utility giant?

This is a story about adaptation without losing your core. It's about betting the company on nuclear when everyone said you were crazy, then watching those bets become your crown jewels. It's about navigating the treacherous waters between public service and shareholder returns, between political masters and market forces. And ultimately, it's about building infrastructure that outlives its builders by centuries.

We'll trace PSEG's journey through five distinct eras: the consolidation pioneer phase under McCarter's four-decade reign, the regulated utility golden age of suburban expansion, the nuclear gambit that nearly broke the company but now defines it, the deregulation adventure that taught painful lessons about straying from your knitting, and finally today's clean energy pivot that has the company dismantling its coal plants while doubling down on atoms.

Along the way, we'll unpack the regulated utility model—that peculiar American invention where private companies get monopolies in exchange for serving everyone at regulated rates. We'll explore how PSEG has played this game for over a century, turning boring into beautiful for investors who've collected dividends every single year since 1907.

II. Origins: The Public Service Corporation Era (1903–1948)

The meeting took place in a Newark boardroom thick with cigar smoke. It was May 6, 1903, and representatives from over 400 companies had gathered to sign papers that would fundamentally reshape New Jersey's infrastructure landscape. Gas companies that competed block by block, electric firms with incompatible systems, trolley lines that refused to connect—all would merge into the Public Service Corporation of New Jersey. At the head of the table sat Thomas McCarter, the 35-year-old lawyer who'd orchestrated this unprecedented consolidation.

McCarter wasn't your typical utility executive. A Princeton graduate who'd served as New Jersey's Attorney General at just 29, he understood that the chaos of competing utilities was holding back the state's industrial development. Factories couldn't rely on consistent power. Commuters faced a byzantine system of disconnected transit lines. Gas and electric companies duplicated infrastructure while leaving whole neighborhoods in the dark. McCarter saw opportunity where others saw only complexity.

The Public Service Corporation he created was revolutionary for its time—a holding company that would standardize, interconnect, and rationalize New Jersey's entire utility infrastructure. This wasn't just about economies of scale; it was about building the backbone for an industrial powerhouse. New Jersey sat between New York and Philadelphia, perfectly positioned to capture the manufacturing boom if only it had reliable power and transport.

McCarter's management style was hands-on to the point of obsession. He personally inspected trolley tracks, reviewed equipment purchases, and even rode the lines incognito to observe operations. Employees told stories of the president appearing at 2 AM to check on emergency repairs. His 36-year presidency—followed by six more years as chairman until 1945—gave the company extraordinary continuity through tumultuous times.

The Progressive Era context is crucial here. Across America, reformers were battling the "trusts"—monopolistic combinations that controlled everything from oil to steel. Municipal ownership of utilities was gaining ground as cities argued that essential services shouldn't be in private hands. McCarter had to navigate this minefield carefully, positioning Public Service as a responsible monopoly that served the public interest better than either competition or government ownership could.

His masterstroke came in 1928 with a major restructuring. McCarter merged all electric and gas operations into a single entity—Public Service Electric and Gas Company (PSE&G)—while spinning transportation into Public Service Coordinated Transport. This wasn't just corporate housekeeping; it recognized that energy and transport were fundamentally different businesses requiring different regulatory approaches and capital structures.

The company's innovation extended beyond corporate structure. In 1937, Public Service pioneered the diesel-electric bus fleet, replacing aging trolleys with modern buses that could adapt to suburban sprawl. This seemingly mundane decision reflected deep strategic thinking: trolleys required expensive fixed infrastructure, while buses could follow customers wherever development led.

But storm clouds were gathering. The utility holding company model that enabled Public Service's creation was increasingly under attack. The 1935 Public Utility Holding Company Act aimed to break up the sprawling utility empires that had emerged in the 1920s. Public Service, with its relatively compact New Jersey focus, survived better than most, but the writing was on the wall.

By 1948, the original Public Service Corporation was dissolved, with PSE&G emerging as an independent company. The transportation business would struggle on until 1971 when it was renamed Transport of New Jersey, finally being sold to the state's NJ Transit in 1980. The grand consolidation era was over, but McCarter's vision of integrated infrastructure serving New Jersey would endure, setting the stage for PSE&G's next chapter as a regulated utility in the booming postwar economy.

III. The Regulated Utility Years: Building Scale (1948–1985)

The Levittown model home opened to the public on a crisp October morning in 1958. As young families toured the three-bedroom ranch—complete with modern electric appliances, central heating, and enough power outlets to run a television in every room—PSE&G engineers were doing their own calculations. Each new subdivision meant miles of distribution lines, transformers on every block, and generating capacity that had to stay ahead of demand that was doubling every decade.

This was the golden age of the regulated utility, and PSE&G was perfectly positioned to capture it. The postwar suburban boom transformed New Jersey from garden state to bedroom community for New York and Philadelphia. Between 1950 and 1970, the state's population grew by 50%, but electricity consumption grew by 400%. Every new house needed power. Every new factory demanded reliable service. Every new shopping mall required massive feeds.

The regulatory compact that governed this expansion was elegantly simple: PSE&G would serve everyone in its territory—no cherry-picking profitable customers—and in return, state regulators would guarantee the company a fair return on its investments. Build a power plant? Earn 10-12% on that capital. String transmission lines? Same deal. This wasn't charity; it was a business model that aligned private capital with public need.

The company's president during much of this period, Robert Blake (1959-1970), was an engineer's engineer who understood that reliability was everything. Under his leadership, PSE&G pioneered the use of 500-kilovolt transmission lines, among the highest voltages in the country at the time. These superhighways of electricity could move massive amounts of power from generating plants to load centers with minimal losses. The company's grid became a marvel of redundancy and resilience—any single failure could be routed around without customers losing power.

But the 1970s brought a harsh awakening. The 1973 oil embargo sent fuel costs soaring—oil that PSE&G relied on for much of its generation. Electricity rates, stable for decades, suddenly spiked. Regulatory hearings became battlegrounds as consumer advocates accused the company of profiteering while PSE&G argued it was barely covering costs. The social contract of the regulated utility was being tested.

Meanwhile, the transportation business was hemorrhaging money. Those diesel buses that seemed so smart in 1937 were now competing with private automobiles on highways built with federal dollars. The renamed Transport of New Jersey was carrying fewer passengers each year while costs relentlessly climbed. When the state finally took it over in 1980, creating NJ Transit, it was almost a relief—PSE&G could focus on its core energy business.

The solution to the oil crisis seemed obvious: nuclear power. Atoms don't care about OPEC embargoes. But as we'll see in the next chapter, this bet would nearly break the company before ultimately becoming its salvation. For now, in the early 1980s, PSE&G's leadership recognized that the old utility model needed a new structure for a new era.

Thus, in 1985, the Public Service Enterprise Group (PSEG) was born—a holding company that would own PSE&G as a subsidiary while allowing for other ventures. This wasn't just corporate restructuring; it was preparation for a world where utilities might compete, where generation might separate from distribution, where the cozy regulated monopoly might not last forever. The company that McCarter built was preparing for its next transformation.

IV. The Nuclear Gambit: Building New Jersey's Clean Baseload

The control room at Salem Unit 1 was dead silent except for the hum of monitoring equipment. It was June 30, 1977, and after years of delays, cost overruns, and regulatory battles, operators were finally initiating the chain reaction that would bring New Jersey's first commercial nuclear reactor online. Outside, protesters held vigil. Inside, engineers who'd staked their careers on this moment watched nervously as power levels climbed toward criticality.

PSEG's nuclear journey actually began much earlier, in the optimistic days of "Atoms for Peace" when nuclear electricity was supposed to be "too cheap to meter." The company's decision to build on Artificial Island—740 acres of manmade land in Salem County along the Delaware River—was both practical and symbolic. This wasn't just a power plant; it was a statement about New Jersey's energy future.

The numbers were staggering even by utility standards. Salem's two units would generate 2,275 megawatts—enough to power 2 million homes. PSEG owned 57% with Philadelphia Electric (later Exelon, now Constellation) owning the rest. When Hope Creek came online in 1986, adding another 1,174 megawatts, the site became the third-largest nuclear facility in America. Combined with PSEG's 50% stake in Pennsylvania's Peach Bottom plant, the company had bet everything on fission.

But nuclear power in America was never just about engineering; it was about politics, fear, and public trust. Three Mile Island's partial meltdown in 1979—just two years after Salem Unit 1 started—transformed the regulatory landscape overnight. Suddenly, every valve, every procedure, every training program was under scrutiny. Costs that were already ballooning exploded higher.

The real crisis came in the mid-1990s. Years of deferred maintenance and operational shortcuts caught up with Salem. In 1995, the Nuclear Regulatory Commission shut down both Salem units—an extraordinary action that put PSEG on the nuclear industry's wall of shame. For two years, the reactors sat idle while the company rebuilt not just equipment but its entire safety culture. The financial hit was brutal: hundreds of millions in lost revenue, plus over a billion in repairs and upgrades.

E. James Ferland, who became CEO during this crisis, made a decision that would define PSEG's future: instead of abandoning nuclear like many utilities, double down and do it right. He brought in Navy nuclear veterans, implemented military-grade operational discipline, and most importantly, changed the culture from one that prioritized production to one obsessed with safety.

The transformation was remarkable. By 2000, Salem and Hope Creek were operating at capacity factors above 90%—world-class performance. The plants that nearly killed the company became its most valuable assets. When natural gas prices spiked in the 2000s, when carbon pricing entered the conversation, when reliability became paramount, PSEG's nuclear fleet looked prescient rather than problematic.

Today, these reactors provide 85% of New Jersey's carbon-free electricity and support 6,000 direct and indirect jobs. The state, recognizing their irreplaceable value, approved Zero-Emission Certificates worth $300 million annually from 2019 to 2025—essentially a subsidy for keeping the plants open. License extensions have been approved through the 2040s, with plans to operate until 2056, 2060, and even 2066.

The nuclear gambit that almost destroyed PSEG has become its moat. No one is building new nuclear plants in New Jersey. The regulatory barriers, capital requirements, and public opposition make it essentially impossible. Yet as the grid strains under data center demands and clean energy mandates, these 40-year-old reactors are more valuable than ever. Sometimes the best investments are the ones that nearly kill you first—if you survive to tell the tale.

V. Deregulation and Diversification Era (1989–2008)

The PowerPoint slide looked compelling: a map of the world with PSEG logos dotting multiple continents. It was 2001, and CEO E. James Ferland was presenting his vision to transform PSEG from a New Jersey utility into a "global energy firm." Within five years, the company would own power plants in Peru, operate distribution systems in Poland, and trade electricity from Texas to Maine. What could go wrong?

Everything, as it turned out.

The story begins in 1989 when PSEG created Enterprise Diversified Holdings (later PSEG Energy Holdings), a subsidiary designed to house everything that didn't fit in the regulated utility box. The timing seemed perfect. Deregulation was sweeping through industries from airlines to telecommunications, and electricity was next. The old model—vertically integrated utilities with geographic monopolies—was supposedly dead. The future belonged to nimble competitors who could generate, trade, and market power across open markets.

PSEG's first moves were cautious and logical. In 1997, it formed Energis Resources to market energy products to commercial customers who could now choose their electricity supplier. When full deregulation hit New Jersey in 2000, the company split its unregulated generation assets into PSEG Power, separate from the still-regulated transmission and distribution business of PSE&G. This wasn't voluntary; it was the price of admission to the deregulated world.

But then ambition took over. PSEG started buying independent power plants across the country—gas-fired facilities in Texas, peaking plants in California, combined-cycle units in Pennsylvania. The thesis was straightforward: electricity was becoming a commodity, and PSEG's operational expertise would give it an edge in running these plants efficiently.

International ventures followed the same logic with even more hubris. Peru's privatizing electricity system? PSEG was there. Poland's post-communist energy reforms? Sign them up. The company even explored opportunities in India and China. Each deal came with consultants' reports showing inevitable growth, promising returns, and synergies with existing operations.

The 2005 merger attempt with Exelon was supposed to be the crowning achievement—creating America's largest utility with combined market value over $20 billion. The Federal Energy Regulatory Commission approved it. Shareholders blessed it. But New Jersey regulators, worried about market concentration and job losses, killed it after 18 months of negotiations. The collapse cost PSEG millions in fees and, more importantly, strategic momentum.

Meanwhile, the merchant power market was turning into a bloodbath. The California energy crisis of 2000-2001 had initially sent power prices soaring, making every megawatt look like gold. But by 2002, overbuilding led to a capacity glut. Spark spreads—the difference between electricity prices and fuel costs—collapsed. Independent power plants that looked brilliant at $60/MWh electricity prices were disasters at $30.

The international adventures fared even worse. Peru's government changed regulations retroactively. Poland's promised reforms stalled. By 2003, PSEG was writing down hundreds of millions in foreign investments. The global energy firm was retreating to New Jersey with its tail between its legs.

Ralph Izzo, who became CEO in 2007, inherited this mess and made a crucial decision: PSEG would return to its roots as a regional utility with a strong nuclear base. The merchant plants were sold or shut down. International ventures were unwound. Trading operations were dramatically scaled back. The company that had tried to be Enron without the fraud would instead be boring, predictable PSE&G with better returns.

The lesson was expensive but clear: in the utility business, the grass isn't greener on the unregulated side—it's just more volatile. The deregulation era taught PSEG that its competitive advantage wasn't operational excellence that could be exported anywhere, but deep relationships with regulators, understanding of local markets, and ownership of irreplaceable assets like nuclear plants and transmission lines. Sometimes the best strategy is to stick to your knitting, even when everyone else is learning to weave.

VI. The Clean Energy Pivot (2009–Present)

The utility poles stretched for miles along Route 1, each one topped with something unprecedented: a solar panel tilted toward the southern sky. It was 2009, and PSEG was installing what would become the world's largest pole-mounted solar project—200,000 panels attached to the infrastructure it already owned. The $773 million Solar 4 All program was audacious in scale and clever in execution. Why fight rooftop solar when you could own utility-scale solar using assets you already had?

This was Ralph Izzo's PSEG—not trying to be something it wasn't, but reimagining what a utility could be in the clean energy era. Izzo, an MIT-trained engineer who'd run the nuclear fleet during its turnaround, understood that the energy transition wasn't optional. The question was whether PSEG would lead or follow.

The transformation started with subtraction. In 2021, PSEG sold its entire 6,750-megawatt fossil fuel portfolio to ArcLight Capital for $1.92 billion. These weren't struggling assets—many were profitable gas plants—but Izzo saw the writing on the wall. Carbon regulations were coming. Natural gas, despite being cleaner than coal, wouldn't be clean enough. Better to sell at the peak than hold assets that would become stranded.

That same year, Hudson Generating Station, PSEG's last coal plant, shut down permanently. The company that once burned millions of tons of coal annually was now 100% coal-free. The symbolism mattered as much as the economics. PSEG was positioning itself as New Jersey's clean energy infrastructure company.

But the boldest move came with offshore wind. In 2021, PSEG bought a 25% equity stake in the Ocean Wind project from Danish developer Ørsted. The planned 1,100-megawatt wind farm off Atlantic City would be New Jersey's first utility-scale offshore project. This wasn't just another power plant; it was a bet on New Jersey's energy future and PSEG's role in building it.

The 2014 contract to manage Long Island Power Authority's system after Hurricane Sandy exposed massive failures showed another evolution: PSEG as emergency infrastructure expert. The 10-year deal to operate LIPA's grid for 1.1 million customers wasn't about ownership but operational excellence—exactly the kind of boring, steady business that generated predictable fees without capital risk.

The Clean Energy Future program launched in 2018 represented perhaps the biggest strategic shift. Instead of just selling electrons, PSEG would help customers use less of them—investing $1.9 billion in energy efficiency programs from 2025-2027. This seems counterintuitive—why would a utility want customers to buy less of its product? Because under New Jersey's regulations, PSEG could earn returns on efficiency investments just like traditional infrastructure. Helping a factory reduce consumption by 30% could be as profitable as building a power plant.

The nuclear fleet, once nearly abandoned, became the crown jewel of the clean energy strategy. License extensions to 2056, 2060, and 2066 mean these plants could operate for literally a century. The Zero-Emission Certificates—$300 million annually—explicitly recognized nuclear's role in meeting climate goals. PSEG's reactors went from regulatory burden to policy solution.

Even the emerging data center opportunity fits this framework. PSEG is in talks for 50-100 megawatt deals, with potential for co-location near nuclear plants. AI companies need three things: massive amounts of power, absolute reliability, and increasingly, clean energy credentials. PSEG's nuclear plants offer all three. The same reactors that protesters tried to shut down in the 1970s might power the AI revolution of the 2020s.

The company's 2025-2029 capital plan—$22.5 to $26 billion, almost entirely in regulated investments—shows where this is heading. Grid modernization, renewable integration, resilience upgrades—all the unsexy infrastructure that makes the energy transition actually work. PSEG isn't trying to be Tesla or NextEra. It's content being the company that keeps the lights on while the world figures out how to decarbonize.

VII. Modern Business Model & Operations

The control center in Newark operates 24/7, a NASA-style mission control where engineers monitor every substation, every major transmission line, every generating unit across PSEG's territory. On the massive display board, New Jersey's electric grid pulses with real-time data: 2.4 million electric customers drawing power through 25,000 circuit miles suspended from 869,000 poles. Below the streets, 18,000 miles of gas mains serve another 1.9 million customers. This is infrastructure at a scale that's almost incomprehensible—and it all has to work, every second of every day.

PSEG's modern structure reflects hard-learned lessons about focus and competitive advantage. Three main subsidiaries do three distinct things. PSE&G, the regulated utility, owns and operates the poles, wires, substations, and gas pipes in New Jersey. PSEG Power owns the nuclear plants and remaining generation assets. PSEG Long Island manages (but doesn't own) LIPA's system for 1.1 million customers. Clean, simple, boring—exactly how investors like it.

The regulated utility model that governs PSE&G is a masterpiece of aligned incentives, though it takes some explaining. Here's how it works: PSEG proposes investments in infrastructure—say, $500 million to upgrade aging transmission lines. The New Jersey Board of Public Utilities reviews the proposal, examining whether it's necessary and cost-effective. If approved, PSEG builds the infrastructure and adds it to its "rate base"—the total value of assets serving customers.

Now comes the magic: regulators allow PSEG to earn a specified return (currently around 9.6%) on that rate base. So that $500 million investment generates about $48 million in annual allowed earnings. Customers pay rates calculated to cover PSEG's costs plus this allowed return. The company doesn't profit from selling more electricity; it profits from investing in infrastructure.

This model explains seemingly paradoxical behavior. Why does PSEG promote energy efficiency? Because efficiency programs get added to the rate base. Why replace equipment before it breaks? Because new assets earn returns while fully depreciated ones don't. The incentive is to invest, not to sell.

The 2024 rate case illustrates this dance. PSEG requested $505 million in additional annual revenues to cover infrastructure investments and rising costs. After months of testimony, analysis, and negotiation, regulators approved most of it. This wasn't a windfall—it was the systematic process of adjusting rates to reflect invested capital and earned returns.

The numbers are staggering. PSEG's 2025-2029 capital plan allocates $22.5-26 billion, with 90% going to regulated investments. That's $5 billion per year in infrastructure spending, all of which (if approved) earns that ~9.6% return. No wonder the company guides to 9% earnings growth—it's mathematically baked into the model.

But there's a catch: execution risk. Every dollar of capital must be deployed efficiently. Every project must come in on budget. Every regulatory filing must be bulletproof. The New Jersey Board of Public Utilities can disallow costs if PSEG screws up. The infamous Salem nuclear shutdown in the 1990s led to hundreds of millions in disallowed costs—investments PSEG made but couldn't recover through rates.

The data center opportunity represents an evolution of this model. Large customers wanting dedicated power sources can negotiate special arrangements. A data center co-located with a nuclear plant might pay premium rates for guaranteed 24/7 clean power. These deals don't require regulatory approval if structured correctly, offering PSEG market-based returns alongside its regulated earnings.

PSEG Long Island operates differently—it's a fee-for-service contract where PSEG manages but doesn't own the assets. The company earns about $80 million annually for operating LIPA's system, with bonuses for meeting performance metrics and penalties for failures. It's the utility equivalent of property management—steady fees without capital risk.

The beauty of this business model is its predictability. PSEG knows its allowed returns, can forecast its capital investments, and faces limited commodity risk since fuel costs pass through to customers. In a world of volatile markets and disrupted business models, PSEG offers something invaluable: boring, predictable, growing earnings backed by essential infrastructure that society literally cannot function without.

VIII. Financial Performance & Market Position

The dividend check arrived like clockwork, as it had every year since 1907. Through two world wars, the Great Depression, stagflation, the financial crisis—PSEG had never missed an annual payment. For 118 consecutive years, shareholders have received their cut of earnings, making PSEG not just a dividend aristocrat but practically dividend royalty. The 2025 dividend of $2.52 per share, growing for 12 straight years, tells you everything about this business: steady, predictable, relentless.

The market values this consistency at $40.72 billion as of Q3 2024, making PSEG larger than most flashy tech companies you've heard of. But the financial story is more nuanced than just big numbers. Revenue actually declined from $11.23 billion in 2023 to $10.29 billion in 2024—not because the business is shrinking, but because PSEG is shedding volatile merchant power operations to focus on regulated returns.

Q3 2024 results show this strategy working: net income of $1.04 per share, with non-GAAP operating earnings at $0.90 per share. Full-year 2024 guidance of $3.64-3.68 per share might seem modest, but look at 2025: $3.94-4.06 per share, representing ~9% growth. This isn't hypergrowth; it's compound growth, the kind that turns modest annual gains into spectacular long-term returns.

The capital allocation strategy deserves special attention. PSEG plans to fund its entire $22.5-26 billion capital program through 2029 without issuing equity. How? By reinvesting earnings and issuing debt at the subsidiary level. This might seem like financial engineering, but it's actually profound: existing shareholders won't be diluted, meaning per-share growth equals absolute growth.

The company's presence in the S&P 500 and its 17 consecutive years on the Dow Jones Sustainability Index reflect institutional recognition of PSEG's quality. ESG investors particularly love utilities like PSEG—essential services, clean energy transition, unionized workforce with good jobs. The company that once burned coal now scores higher on sustainability metrics than most tech companies.

Breaking down the earnings sources reveals the model's elegance. PSE&G (the regulated utility) generates about 85% of earnings—stable, growing with rate base additions. PSEG Power (mainly nuclear) contributes most of the rest—volatile year-to-year but valuable long-term. The Long Island contract and other ventures add marginal but steady contributions.

The balance sheet strength enables this entire strategy. With investment-grade credit ratings and modest leverage relative to regulatory asset value, PSEG can borrow cheaply to fund infrastructure investments that earn higher regulated returns. It's the utility equivalent of a carry trade, but with regulatory protection instead of currency risk.

What's remarkable is how countercyclical this business can be. During recessions, regulators often become more accommodative, understanding that infrastructure investment creates jobs. During booms, growing electricity demand justifies system expansion. Climate change and extreme weather, perversely, support the investment case—every storm demonstrates the need for grid hardening.

The 9% earnings growth guidance isn't pulled from thin air—it's mathematically derived from rate base growth plus modest efficiency improvements. If PSEG invests $5 billion annually and earns 9.6% returns, that's $480 million in incremental earnings. Divide by share count, adjust for taxes and financing costs, and you get to that 9% growth. It's formulaic in the best way.

Comparing PSEG to pure-play renewables developers or merchant generators misses the point. This isn't a growth story or a turnaround story—it's a compound returns story. Like a REIT or pipeline company, PSEG monetizes essential infrastructure through predictable cash flows. The $2.52 dividend yields about 3.5% at current prices. Add 9% growth and you get to low-teens total returns with minimal volatility. In a world of zero interest rates and inflated valuations, that's increasingly attractive.

The financial performance ultimately reflects the business model: converting massive infrastructure investments into regulated returns, year after year, decade after decade. It's not exciting, but over long periods, boring tends to beat exciting in the wealth creation game.

IX. Playbook: Business & Investing Lessons

Survival across 120 years requires more than luck—it demands systematic adaptation while maintaining core competencies. PSEG's playbook offers lessons that extend far beyond utilities, speaking to fundamental questions about corporate longevity, regulatory strategy, and the value of boring businesses in a world obsessed with disruption.

Lesson 1: The Moat of Essential Infrastructure PSEG doesn't sell products; it sells civilization's prerequisites. You can choose not to buy an iPhone or Tesla, but you cannot choose to live without electricity. This isn't just about demand inelasticity—it's about social necessity creating regulatory protection. When your service is essential, society won't let you fail but also won't let you gouge. The regulated utility model is this bargain made explicit.

Lesson 2: Regulatory Relationships as Competitive Advantage Most businesses fear regulation; PSEG embraces it. Over 120 years, the company has built institutional knowledge about working with regulators that no competitor can replicate. They know how to structure rate cases, when to push and when to compromise, how to frame investments as public benefits. This isn't lobbying—it's a specialized competency as valuable as any technology patent.

Lesson 3: The Conglomerate Discount Is Sometimes Worth Paying Modern finance theory hates conglomerates, preferring pure-plays that investors can mix themselves. But PSEG's integration of generation, transmission, and distribution creates value that separation would destroy. Nuclear plants need guaranteed transmission access. Distribution systems need reliable generation. The integration others see as inefficient is actually risk reduction.

Lesson 4: Nuclear as the Ultimate Moat Nobody is building new nuclear plants in New Jersey—the regulatory hurdles, capital requirements, and public opposition make it impossible. Yet these plants are essential for clean, reliable baseload power. PSEG's nuclear fleet is like owning the only bridges across a river that can't be forded. The same assets that nearly bankrupted the company in the 1990s are now irreplaceable.

Lesson 5: Patient Capital Wins Infrastructure Games PSEG thinks in decades, not quarters. A transmission line might take 10 years from planning to energization. A nuclear plant operates for 60-80 years. This temporal mismatch with Wall Street's quarterly focus creates opportunity. While markets obsess over next quarter's earnings, PSEG quietly builds assets that will generate returns for generations.

Lesson 6: Failed Diversification as Valuable Education The merchant power disasters of the 2000s taught PSEG what not to do. The company learned that operational excellence in New Jersey doesn't translate to Peru, that unregulated markets are winner-take-all games, that financial engineering can't overcome fundamental business model flaws. These expensive lessons created institutional memory that prevents repeat mistakes.

Lesson 7: ESG Before It Had a Name PSEG has practiced stakeholder capitalism since 1903—not from altruism but necessity. A utility that angers its community loses its social license. One that mistreats workers faces strikes that black out cities. One that ignores environmental concerns faces regulatory punishment. The ESG framework modern investors love is just formalization of what utilities always knew: sustainable business requires balancing all stakeholders.

Lesson 8: The Value of Boring in a Volatile World PSEG will never be a meme stock. It won't 10x in a year. But it also won't go to zero. In a portfolio context, this negative correlation with market volatility is invaluable. When tech stocks crater, utilities hold steady. When inflation spikes, regulated returns adjust. Boring becomes beautiful when everything else is chaos.

Lesson 9: Adaptation Without Transformation PSEG has survived by evolving within its core competency rather than abandoning it. From trolleys to nuclear power, the company has adopted new technologies while maintaining its essential function: providing energy infrastructure. This is different from transformation—it's systematic adaptation that preserves institutional knowledge while embracing change.

Lesson 10: The Compound Returns of Compound Returns A utility earning 9.6% regulated returns that reinvests at those same returns creates a mathematical flywheel. Each year's earnings fund next year's growth, which generates more earnings, which fund more growth. Over decades, this compounds into extraordinary wealth creation. PSEG's 118-year dividend history is this principle made tangible.

The meta-lesson is that sustainable competitive advantages often come from structural factors rather than operational excellence. PSEG isn't necessarily better at running power plants than competitors. But it owns irreplaceable assets, operates under favorable regulations, and serves captive customers. In business, being positioned correctly often matters more than executing perfectly.

X. Analysis & Bear vs. Bull Case

The investment case for PSEG ultimately comes down to a fundamental question: In an era of technological disruption and energy transition, is a 120-year-old regulated utility a dinosaur awaiting extinction or a toll booth on the bridge to the future?

The Bull Case: Infrastructure for the Inevitable

Bulls see PSEG as perfectly positioned for multiple megatrends. Start with electrification: every Tesla sold, every heat pump installed, every data center built increases electricity demand. After decades of flat consumption, power demand is inflecting upward. PSEG's infrastructure becomes more valuable, not less, in an electrified economy.

The nuclear fleet transforms from liability to crown jewel in this narrative. While others scramble to build renewable capacity, PSEG already owns carbon-free baseload that runs 24/7. The Zero-Emission Certificates are just the beginning—expect nuclear's value to soar as intermittent renewables create grid stability challenges. Those 40-year-old reactors with licenses extending to the 2060s look impossibly cheap versus any alternative.

Data center demand could be transformational. AI training requires massive, stable power that solar and wind can't reliably provide. PSEG's discussions for 50-100 MW dedicated supplies could mushroom into gigawatt-scale partnerships. Co-location at nuclear sites solves transmission constraints while providing the clean energy that tech companies need for ESG credentials. This isn't priced into the stock.

The regulated utility model itself is the biggest bull argument. That 9.6% allowed return is locked in regardless of interest rates, inflation, or market volatility. The $22.5-26 billion capital plan through 2029 mathematically drives 9% earnings growth. No execution risk, no competitive threats, no technology disruption—just formulaic returns on essential infrastructure.

Climate change, perversely, strengthens the investment case. Every hurricane, heat wave, and polar vortex demonstrates the grid's vulnerability and justifies massive resilience investments. Regulators can't say no to storm hardening after watching customers lose power for weeks. PSEG's capital opportunities expand with climate chaos.

Finally, valuation remains reasonable. At roughly 16x forward earnings, PSEG trades at a discount to the S&P 500 despite more predictable earnings. The 3.5% dividend yield exceeds 10-year Treasuries. For income investors, this is a bond substitute with growth.

The Bear Case: Disruption Comes for Everyone

Bears see existential threats lurking behind regulatory protection. Distributed generation is the nightmare scenario: solar panels and batteries getting so cheap that customers disconnect from the grid entirely. Every rooftop solar installation reduces PSEG's revenue while leaving infrastructure costs unchanged. The utility death spiral—fewer customers bearing higher costs driving more defection—is already visible in places like Hawaii.

Nuclear operational risk can't be ignored. Three Mile Island, Chernobyl, Fukushima—one accident at Salem or Hope Creek would be catastrophic. Even minor incidents trigger costly shutdowns. The plants are 40+ years old; mechanical failures increase with age. License extensions to 2066 assume nothing goes wrong for four more decades. That's a massive bet on perfect execution.

Regulatory risk cuts both ways. New Jersey's politics lean progressive, and utilities make convenient targets for populist anger. Rate increase requests face growing opposition. Allowed returns could be cut. Stranded asset risk from forced early retirements isn't theoretical—look at PG&E's bankruptcy. Political winds can shift rapidly against investor-owned utilities.

The growth algorithm has limits. You can't raise rates forever without political backlash. At some point, industrial customers flee high-cost New Jersey for cheaper power elsewhere. The capital investment opportunities might dry up once basic reliability is achieved. That 9% growth could decelerate to GDP-plus quickly.

Technology disruption comes in unexpected forms. Microgrids, fuel cells, industrial-scale batteries—all threaten the centralized utility model. PSEG's massive infrastructure could become stranded assets if power generation and consumption localize. The company investing billions in transmission lines might be like Blockbuster building more stores in 2005.

Climate change is a double-edged sword. Yes, storms drive investment, but they also destroy returns. Hurricane Sandy cost billions in emergency response and repairs that weren't fully recovered through rates. Flooding at shore substations, heat stress on equipment, wildfire risk—climate change could overwhelm adaptation efforts.

The Verdict: Asymmetric Risk-Reward

The bear case requires multiple disruptions happening simultaneously and quickly. Distributed generation needs breakthrough cost reductions. Regulators must turn hostile. Nuclear plants must fail catastrophically. Technology must enable grid defection at scale. While possible, this convergence seems unlikely in the investment horizon that matters.

The bull case requires nothing changing—just PSEG executing its stated plan with regulatory approval it's received for decades. The asymmetry favors bulls: limited downside with steady upside. PSEG won't make anyone rich quickly, but it probably won't make anyone poor either. In a portfolio context, that's increasingly valuable as correlation approaches one across most assets.

XI. Epilogue & "If We Were CEOs"

Standing in PSEG's Newark headquarters, looking out at the industrial landscape that electricity helped build, you can't help but wonder: What would Thomas McCarter make of his company today? The trolleys are gone, replaced by nuclear reactors. The gas lamps have given way to smart meters. But the essential mission—providing the energy infrastructure that makes modern life possible—remains unchanged.

If we were running PSEG today, the strategic priorities would write themselves, though execution would be anything but simple.

First, we'd go all-in on the data center opportunity, but not in the way most expect. Rather than just selling power, we'd create "Energy Development Zones" around our nuclear plants—pre-permitted sites with guaranteed power, fiber connectivity, and cooling water access. Partner with real estate developers to build the facilities, keeping PSEG as the utility rather than landlord. The goal: capture the economic development benefits for New Jersey while maintaining our regulated utility model.

Second, we'd future-proof the nuclear fleet through aggressive life extension and uprating. Every megawatt of additional capacity from existing plants is worth its weight in gold—no new permitting, minimal opposition, immediate revenue. Spend whatever it takes to keep these plants running until fusion makes them obsolete (so basically forever).

Third, we'd reframe the entire regulatory conversation around resilience rather than rates. Climate change gives utilities social license to invest massively in grid hardening. Instead of fighting over allowed returns, we'd propose a "Resilience Compact" with regulators: pre-approved investment categories for storm hardening, cybersecurity, and redundancy. Take the politics out of necessary infrastructure.

Fourth, we'd embrace distributed resources rather than fight them. Create a subsidiary that installs and operates battery storage at commercial sites, sharing savings with customers while maintaining grid control. Turn the threat of grid defection into an opportunity for new regulated investment.

The long-term vision would be positioning PSEG as the platform layer for the energy transition. We don't need to own every solar panel or wind turbine—we need to own the irreplaceable infrastructure that connects, balances, and backs up everything else. Think of it as the AWS of energy: boring, essential, impossibly profitable.

But here's the deeper insight: PSEG's next century won't be about electricity per se, but about what electricity enables. The company that once powered factories now powers server farms. The grid that enabled suburbanization will enable vehicle electrification. The infrastructure that supported the industrial age must adapt for the information age.

The fundamental question facing PSEG—and all utilities—is whether they can evolve from commodity providers to enablers of economic transformation. Can a company structured for 20th-century regulation thrive in 21st-century markets? Can patient capital compete with venture velocity? Can public service and shareholder returns align when society's needs are changing faster than rate cases can adjust?

We think yes, but with caveats. PSEG will survive another century, but it might look as different from today as today looks from McCarter's trolley empire. The core competency isn't generating or distributing electricity—it's managing complex infrastructure that society depends on. That need isn't disappearing; it's intensifying.

The recipe for continued success is paradoxical: change everything while changing nothing. Adopt every new technology that makes sense. Restructure whenever necessary. Enter and exit businesses as economics dictate. But never forget that PSEG's ultimate product isn't kilowatt-hours—it's reliability, resilience, and the invisible infrastructure that makes visible progress possible.

Looking forward, PSEG's story will be written by forces beyond any CEO's control: climate change, technology disruption, political upheaval, economic transformation. But if history is any guide, the company will adapt, survive, and somehow keep paying dividends through it all. The trolleys are gone, but the tracks they laid—metaphorically speaking—still guide PSEG's journey from the industrial age through the information age and into whatever comes next.

That's the thing about essential infrastructure: it has to evolve, but it can never disappear. PSEG bet its existence on that principle 120 years ago. So far, it's been a winning wager.

XII. Recent News* **

February 2025:** PSEG announced 2024 results with $3.54 per share net income and $3.68 per share non-GAAP operating earnings. The company initiated 2025 guidance of $3.94-$4.06 per share, representing ~9% growth over 2024 results

-

Capital Plan Expansion: Raised 2025-2029 capital spending plan to $22.5-26 billion (up $3.5 billion from prior plan), consisting of $21-24 billion of regulated investment. The increase is driven by incremental investments for PSE&G to meet growing customer demand, modernize infrastructure and CEF-EE II programs

-

October 2024 Rate Case Settlement: The New Jersey Board of Public Utilities approved a settlement agreement for PSE&G's electric and gas distribution base rate case filed in December 2023. New rates went into effect October 15, 2024, advancing PSE&G's ability to provide affordable service while maintaining financial strength for grid reliability

-

Rate Impact: This base rate increase was PSE&G's first since 2018 and represents less than half the rate of inflation during that time. The settlement results in a typical combined residential electric and gas customer bill increase of 7%, or $15 per month

-

Clean Energy Future II Approval: In October 2024, the BPU approved PSE&G's CEF-EE II filing totaling approximately $2.9 billion, which includes direct investments and on-bill repayment financing. This new cycle comprises 10 energy efficiency programs supporting economic growth and clean energy jobs in New Jersey

-

Data Center Opportunities: PSEG is in talks to sell power to data centers from its Hope Creek and Salem nuclear plants in southern New Jersey, where it owns 2,486 MW. Power demand from each of the mid-sized data centers ranges from about 50 MW to 100 MW, with inquiries also including requests for behind-the-meter, co-located facilities seeking highly reliable carbon-free baseload power

-

Nuclear for AI: CEO Ralph LaRossa stated in 2024: "We have had discussions related to both sides of the meter in recent months ... for mid-sized data center construction of approximately 50MW to 100MW, and behind-the-meter inquiries for colocated facilities that prioritize highly reliable carbon-free baseload power from existing facilities"

-

S&P Global Assessment: Public Service Enterprise Group is in talks to supply data centers with capacity from the Hope Creek and Salem nuclear power plants. S&P noted: "We think that nuclear complexes such as the Salem and Hope Creek generation stations are potential candidates. They have adequate interconnection, significant generation redundancies, and are ideally located to provide edge computing near load centers"

-

Nuclear Expansion Plans: PSEG Power is planning to increase capacity at the Salem nuclear station by up to 200 MW, which would qualify for clean hydrogen tax credits. PSEG Power has notified the Nuclear Regulatory Commission that it plans to seek 20-year license renewals for the three units at Hope Creek and Salem, extending their lives to 2056, 2060 and 2066, respectively

-

ESG Recognition: PSEG has appeared on the Dow Jones Sustainability North America Index for 16 consecutive years. PSEG is included on the 2023-2024 list of U.S. News' Best Companies to Work For

XIII. Links & Resources

While this analysis provides comprehensive coverage of PSEG's 120-year journey from trolley operator to nuclear powerhouse, readers seeking deeper insights into specific aspects of the company's history, operations, and market position may find the following resources valuable:

Regulatory & Financial Resources: - New Jersey Board of Public Utilities website for current rate cases and regulatory proceedings - PSEG Investor Relations portal (investor.pseg.com) for quarterly earnings, presentations, and SEC filings - PJM Interconnection for regional transmission planning and market data - Nuclear Regulatory Commission database for plant performance metrics and license information

Historical & Industry Context: - "The Prize: The Epic Quest for Oil, Money & Power" by Daniel Yergin - Essential context on energy industry evolution - "Confessions of a Radical Industrialist" by Ray Anderson - Perspective on sustainable business practices in traditional industries - Electric Power Research Institute (EPRI) reports on grid modernization and nuclear operations - Edison Electric Institute publications on utility industry trends and benchmarking

Energy Transition & Market Analysis: - International Energy Agency reports on global energy transitions and nuclear power's role - S&P Global Market Intelligence for utility sector analysis and peer comparisons - BloombergNEF for renewable energy economics and grid integration studies - Wood Mackenzie research on data center power demand and infrastructure requirements

Books on Utility History & Regulation: - "Power Loss: The Origins of Deregulation and Restructuring in the American Electric Utility System" by Richard F. Hirsh - "The Grid: Biography of an American Technology" by Julie A. Cohn - "Networks of Power: Electrification in Western Society, 1880-1930" by Thomas P. Hughes

Nuclear Industry Resources: - World Nuclear Association for global nuclear industry data and analysis - Nuclear Energy Institute for U.S. nuclear policy and economic analysis - "Atomic Awakening: A New Look at the History and Future of Nuclear Power" by James Mahaffey

Climate & Resilience Planning: - NOAA Climate Resilience Toolkit for extreme weather projections - Department of Energy Grid Modernization Initiative reports - Resources for the Future analysis on carbon pricing and clean energy subsidies

Data Center & AI Infrastructure: - Uptime Institute for data center industry standards and trends - Data Center Dynamics for emerging markets and co-location strategies - NVIDIA and major cloud providers' white papers on power requirements for AI training

New Jersey Specific Resources: - New Jersey Economic Development Authority for state energy initiatives - Rutgers Energy Institute for regional energy research - New Jersey Business & Industry Association for business perspective on energy costs

Note: As financial markets and regulatory environments evolve rapidly, readers should verify current information through primary sources and recent filings. This article represents analysis as of the publication date and should not be considered investment advice.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube