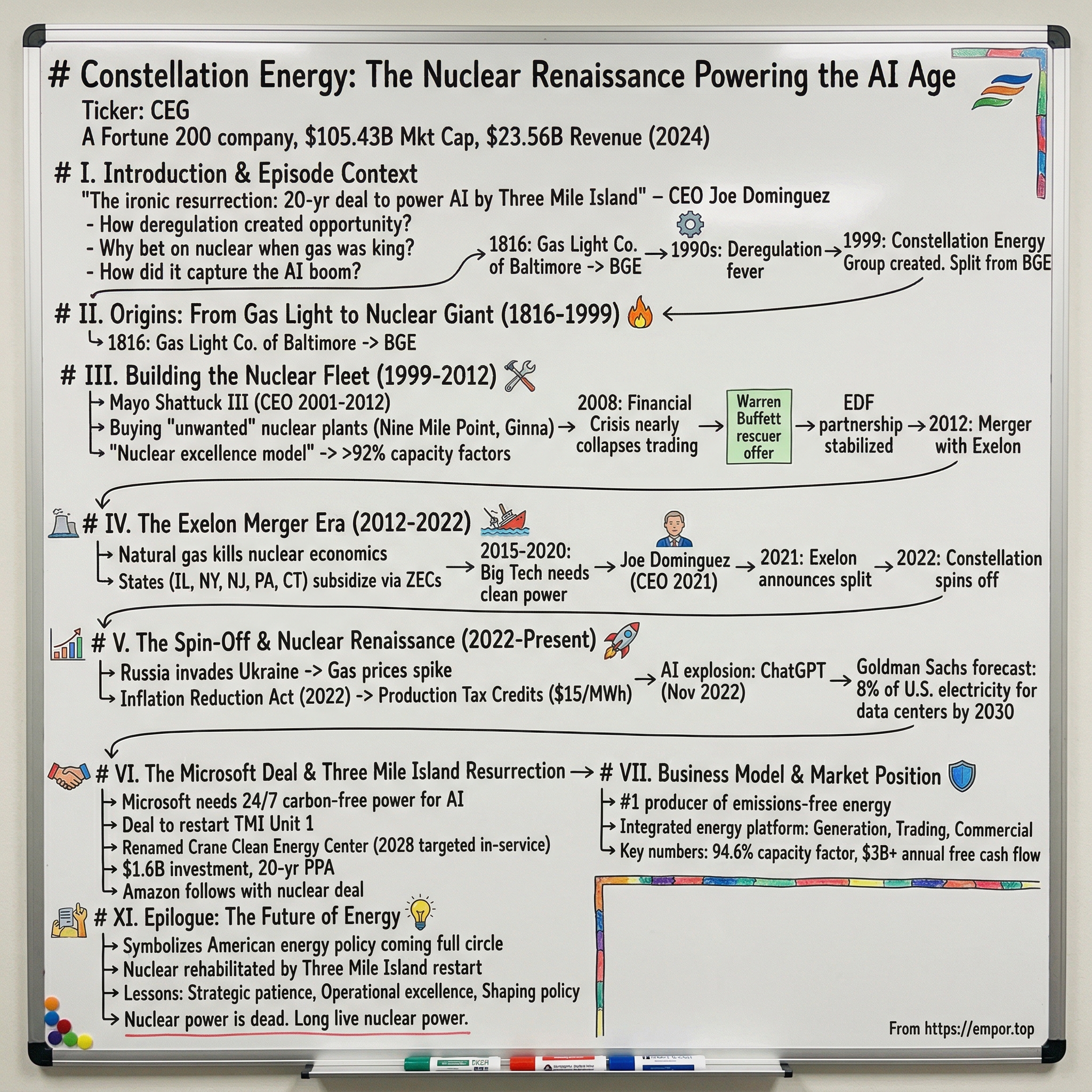

Constellation Energy: The Nuclear Renaissance Powering the AI Age

I. Introduction & Episode Context

Picture this: September 20, 2024. Joe Dominguez, CEO of Constellation Energy, stands before a room of stunned journalists and announces something that would have been unthinkable just five years earlier. Microsoft, the tech giant worth over $3 trillion, has just signed a 20-year deal to resurrect Three Mile Island—yes, that Three Mile Island, site of America's worst commercial nuclear accident. The plant that became synonymous with nuclear fear in 1979 will now power the artificial intelligence revolution.

The irony is almost too perfect. The facility that nearly killed the American nuclear industry will be reborn as the Crane Clean Energy Center, fueling ChatGPT queries and cloud computing operations. But this isn't just a story about one deal or one plant. It's about how a Baltimore gas lighting company founded when James Madison was president became America's nuclear powerhouse, worth $99 billion and generating nearly a quarter of the nation's carbon-free electricity. Today, Constellation Energy stands as a Fortune 200 company with a market cap of $105.43 billion and revenue of $23.56 billion in 2024. It operates the nation's largest fleet of nuclear reactors—21 units across 12 plants—and produces more carbon-free electricity than any other American company. But to understand how we got here, how a regional utility became the backbone of America's clean energy future, we need to go back to when cities were still lit by whale oil and the electric grid was a science fiction dream.

The big questions driving this story: How did deregulation create the opportunity for a nuclear pure-play? Why did Constellation bet everything on nuclear when natural gas was killing the industry? And most intriguingly, how did the company position itself to capture the AI boom before anyone knew ChatGPT would exist?

This is a story of three transformations. First, the shift from regulated monopoly to competitive market player. Second, the near-death and resurrection of American nuclear power. And third, the convergence of climate policy, grid reliability, and artificial intelligence that has made nuclear energy suddenly indispensable. It's about timing, operational excellence, and the willingness to make contrarian bets when everyone else is running for the exits.

II. Origins: From Gas Light to Nuclear Giant (1816-1999)

In 1816, while America was still recovering from the War of 1812, a group of Baltimore businessmen received a charter to bring gas lighting to their city. The Gas Light Company of Baltimore—Constellation's earliest ancestor—laid pipes beneath cobblestone streets to fuel streetlamps that would replace whale oil and candles. It was cutting-edge technology for its time, as revolutionary as any Silicon Valley startup today.

For over a century, this company and its successors—eventually becoming Baltimore Gas and Electric (BGE)—operated as a classic regulated utility. They built infrastructure, served customers, and earned a guaranteed return on investment. It was stable, predictable, and thoroughly boring to anyone who wasn't collecting dividends. BGE powered Baltimore through the Civil War, two World Wars, and the rise of suburbia. By the 1960s, they'd even entered the nuclear age, breaking ground on the Calvert Cliffs plant on the western shore of the Chesapeake Bay.

But in the 1990s, everything changed. Deregulation fever swept through American utilities like wildfire. The theory was elegant: separate power generation from distribution, create competitive markets, and let consumers choose their electricity supplier like they choose their long-distance carrier. California led the charge (and would spectacularly implode with Enron's help), but Maryland followed close behind.

Christian Poindexter, BGE's CEO in the late 1990s, saw deregulation coming and made a fateful decision. Rather than fight it or simply comply, BGE would use it as an opportunity to transform. In 1999, the company created Constellation Energy Group as a holding company, splitting its regulated utility operations from its power generation business. The utility would continue as BGE, serving Baltimore customers under regulatory oversight. But the generation assets—including those nuclear plants—would compete in open markets.

"We're not going to be your grandfather's utility anymore," Poindexter told investors at the time. The company began acquiring power plants across the country, building a generation portfolio that stretched from New England to Texas. They weren't just producing power; they were trading it, optimizing it, building sophisticated risk management systems that looked more like Wall Street than Main Street.

The crown jewels were nuclear. While other companies saw nuclear plants as regulatory nightmares with massive fixed costs, Constellation saw something else: assets that could run 24/7, producing massive amounts of carbon-free power with minimal fuel costs. In deregulated markets where power prices could spike during heat waves or cold snaps, nuclear plants were money printing machines—if you could operate them well.

By 1999, Constellation had transformed from a sleepy Baltimore utility into an aggressive energy merchant with national ambitions. They owned 9,000 megawatts of generation capacity and were trading power like commodity futures. Revenue grew from $3 billion to over $4 billion in just two years. Wall Street loved the story—here was a utility acting like a growth company.

But this was just the appetizer. The main course would come in the 2000s, as Constellation embarked on one of the most aggressive nuclear acquisition sprees in American history. They were about to bet the company on a technology that most considered dying, if not already dead.

III. Building the Nuclear Fleet (1999-2012)

Mayo Shattuck III took the helm as CEO of Constellation in 2001, and he wasn't your typical utility executive. A former investment banker from Alex. Brown & Sons (Baltimore's legendary investment house), Shattuck brought a dealmaker's mentality to what had been an engineering culture. His timing seemed terrible—Enron had just imploded, taking the shine off energy trading, and the California power crisis had made "deregulation" a dirty word.

But Shattuck saw opportunity in chaos. While others retreated, Constellation went shopping. Their target: nuclear plants that utilities were desperate to unload. In the early 2000s, nuclear was the unwanted stepchild of American energy. Three Mile Island's shadow still loomed, natural gas was cheap, and the plants required massive capital investments with uncertain returns.

"Everyone thought we were insane," recalled Michael Wallace, Constellation's nuclear chief at the time. "We were buying plants that others were practically giving away."

The buying spree was breathtaking. In 2001, they acquired Nine Mile Point Units 1 and 2 in upstate New York from Niagara Mohawk. In 2003, they bought the R.E. Ginna plant, also in New York. Each deal was structured creatively—often involving long-term power purchase agreements that provided revenue certainty while Constellation took on operational risk.

The secret sauce wasn't just buying cheap assets. It was Constellation's ability to operate them at world-class efficiency. Under Wallace's leadership, they implemented the "nuclear excellence model"—standardized procedures, shared best practices, and rigorous maintenance schedules. Plant capacity factors—the percentage of time reactors actually produced power—rose from industry average 85% to over 92%. That extra 7% was pure profit.

By 2007, Constellation operated 16,750 megawatts of generation, with nuclear comprising the backbone. They were the nation's largest competitive nuclear operator, controlling about 7% of America's nuclear capacity. The company's market cap exceeded $20 billion. Shattuck was featured on magazine covers as the utility executive who cracked the code.

Then came 2008, and everything nearly collapsed.

The financial crisis hit Constellation like a nuclear meltdown. The company had built a massive energy trading operation, using its generation assets as collateral for complex derivatives positions. When Lehman Brothers collapsed in September 2008, credit markets froze. Constellation faced margin calls it couldn't meet. The stock price plummeted from $107 to $13 in a matter of days.

On September 17, 2008—just two days after Lehman's bankruptcy—Warren Buffett's MidAmerican Energy swooped in with a rescue offer: $4.7 billion for the entire company, or about $26.50 per share. It was a fire sale price, but Constellation's board saw no alternative. They accepted.

But Buffett's deal had conditions. He wanted regulatory approvals, time for due diligence, and most importantly, he wanted Constellation to stop the bleeding at its trading operation. As the weeks passed, French utility EDF emerged with a competing offer—$4.5 billion for just a 50% stake in the nuclear business, valuing it far higher than Buffett's bid for the whole company.

The boardroom drama was intense. Shattuck favored the EDF deal, seeing it as preserving shareholder value and company independence. Others worried about reneging on Buffett—never a wise move. In December 2008, Constellation chose EDF, paying Buffett a $175 million breakup fee that the Oracle of Omaha called "the easiest money I ever made."

The EDF partnership stabilized Constellation but fundamentally changed its character. The French had deep nuclear expertise but different ideas about risk and trading. Tensions emerged almost immediately. Meanwhile, the competitive power market was entering its darkest period. The shale revolution had begun, flooding America with cheap natural gas. Power prices collapsed from $80 per megawatt-hour to $30. Nuclear plants that had been profit centers became money pits.

By 2010, Constellation faced an existential choice. They could double down on nuclear, hoping for a market recovery that might never come. Or they could find a partner with deeper pockets and a longer time horizon. They chose the latter, entering merger talks with Exelon, Chicago's utility giant that owned the nation's largest nuclear fleet.

The marriage made strategic sense. Combined, Exelon and Constellation would own 20% of America's nuclear capacity, creating unprecedented economies of scale. But it also meant the end of Constellation as an independent company. After months of negotiations and regulatory reviews, the deal closed in March 2012. Constellation's wild ride as a standalone company was over. Or so everyone thought.

IV. The Exelon Merger Era (2012-2022)

When Exelon absorbed Constellation in 2012, creating America's largest competitive energy company, the nuclear industry was in free fall. Natural gas prices had plummeted to $2 per million BTUs. Wind and solar, backed by federal tax credits, were undercutting nuclear on price. The "nuclear renaissance" that industry advocates had promised after Three Mile Island had turned into a death march.

Chris Crane, Exelon's CEO (no relation to Three Mile Island, despite the unfortunate name coincidence), inherited a portfolio of 23 nuclear plants that were hemorrhaging cash. Wall Street analysts openly questioned whether these plants were stranded assets. "We're watching the slow-motion destruction of America's nuclear fleet," one analyst wrote in 2013.

The numbers were brutal. Clinton, Quad Cities, and Three Mile Island—plants that had operated profitably for decades—were now losing hundreds of millions annually. Chris Crane, who would later be honored when Three Mile Island was renamed, faced an impossible choice: shut down reactors that provided carbon-free power to millions, or find a way to change the game entirely.

Crane chose to fight, but not in the market—in state capitals. If competitive markets wouldn't value nuclear's unique attributes (24/7 reliability, zero carbon emissions, thousands of high-paying jobs), then maybe politicians would. The strategy was audacious: convince state governments to essentially subsidize nuclear plants through Zero Emission Credits (ZECs).

Illinois moved first. In 2016, after intense lobbying and grassroots campaigns featuring nuclear workers pleading for their jobs, the state passed the Future Energy Jobs Act. It provided $235 million annually to keep Quad Cities and Clinton running. New York followed suit, saving Nine Mile Point and Ginna. New Jersey, Connecticut, Pennsylvania—one by one, states created programs to prevent nuclear closures.

The environmental movement, historically nuclear's greatest enemy, became an unlikely ally. Climate activists realized that closing nuclear plants meant burning more natural gas, increasing emissions. The Sierra Club remained opposed, but newer groups like Environmental Progress actively campaigned to save reactors. The politics had shifted—nuclear went from environmental villain to climate hero.

But subsidies were band-aids, not cures. The real game-changer came from an unexpected source: Big Tech's insatiable appetite for electricity. By 2015, data centers consumed 2% of U.S. electricity. By 2020, it was approaching 3%. More importantly, tech companies had made carbon-neutral commitments. They needed clean power, lots of it, available 24/7. Solar and wind couldn't deliver that. Nuclear could.

Inside Exelon, a quiet transformation was underway. The company had split into two cultures: the traditional regulated utility business, steady but slow-growing, and Constellation, the competitive generation and retail supply operation that still operated as a distinct brand. The businesses had different economics, different strategies, different futures.

Joe Dominguez, who became Constellation's CEO within Exelon in 2021, saw the mismatch clearly. A chemical engineer by training who'd spent his career in nuclear operations, Dominguez understood something Wall Street didn't: nuclear plants were about to become incredibly valuable again. Not because of subsidies or regulations, but because of fundamental supply and demand.

"We could see the demand curve shifting," Dominguez would later explain. "Electrification of transportation, data center growth, reshoring of manufacturing—everything pointed to massive electricity demand growth. And we had the only large-scale, carbon-free, reliable supply."

In late 2021, Exelon announced it would split in two. The regulated utility business would keep the Exelon name. The competitive business—the nuclear fleet, the retail operation, the trading desk—would spin off as a standalone company called Constellation Energy. Wall Street was skeptical. Why separate now, just when nuclear was stabilizing?

The answer would become clear soon enough. As an independent company, Constellation could move faster, take bigger risks, and capture opportunities that a regulated utility never could. Like, say, restarting Three Mile Island to power Microsoft's AI ambitions. But first, they had to prove nuclear's renaissance was real, not just another false dawn.

V. The Spin-Off and Nuclear Renaissance (2022-Present)

January 19, 2022. Constellation Energy began trading on the NASDAQ as an independent company, valued at just $14 billion. The timing seemed inauspicious—markets were jittery about inflation, the Fed was hiking rates, and tech stocks were beginning their long slide. But for those paying attention, the stars were aligning for nuclear power in ways not seen since the 1970s.

Two forces converged to transform Constellation's fortunes. First, Russia's invasion of Ukraine in February 2022 sent energy markets into chaos. Natural gas prices spiked from $3 to $9 per million BTUs. Suddenly, nuclear plants that had been marginal were printing money. Second, the Inflation Reduction Act, passed in August 2022, included something the nuclear industry had sought for decades: production tax credits for existing reactors.

The nuclear production tax credit in the IRA provided a stable foundation for consistent and growing earnings, worth $15 per megawatt-hour through 2032. For Constellation's fleet, producing 180 million megawatt-hours annually, that translated to $2.7 billion per year in essentially free cash flow. The stock market did the math quickly—shares doubled within six months.

But Dominguez wasn't content to simply collect government checks. He launched "Generation Growth," an ambitious program to squeeze more power from existing plants. Through turbine upgrades, efficiency improvements, and better fuel management, Constellation added 400 megawatts of capacity—equivalent to building a new natural gas plant—for a fraction of the cost.

The company operates approximately 31,676 megawatts of generating capacity consisting of nuclear, wind, solar, natural gas, and hydroelectric assets. The nuclear fleet achieved a 94.6% capacity factor from 2022-2023, approximately 4% above industry average—equivalent to having another reactor's worth of power or $335 million in additional annual revenue.

The operational excellence showed in the numbers. While the industry average capacity factor hovered around 90%, Constellation's fleet consistently exceeded 94%. Every percentage point of improvement meant $100 million in additional revenue. It was the compound effect of thousands of small improvements: shorter refueling outages, better preventive maintenance, optimized fuel cycles.

The retail business, often overlooked, became a strategic weapon. Constellation served three-quarters of the Fortune 100, selling them not just electricity but carbon-free credentials. As companies made net-zero commitments, they needed clean power purchase agreements. Constellation could offer what others couldn't: genuine, additional carbon-free electricity, not just renewable energy certificates or offsets.

Then came the AI explosion. ChatGPT launched in November 2022, triggering a data center building boom unlike anything in tech history. Goldman Sachs forecast data centers would consume 8% of total U.S. electricity demand by 2030, compared with 3% currently. Every query to an large language model, every image generated by AI, required servers running 24/7. The power demand was staggering and growing exponentially.

Tech companies faced a trilemma: they needed massive amounts of power, they'd committed to carbon neutrality, and they needed absolute reliability. Solar and wind, even with batteries, couldn't guarantee 24/7 availability. Natural gas worked but produced emissions. Nuclear was the only solution, but there weren't enough reactors and building new ones took decades.

Unless, of course, you could restart a shuttered plant.

Three Mile Island Unit 1 had closed in 2019, a victim of low power prices and expiring subsidies. Unit 2, site of the 1979 accident, had been shut since then. But Unit 1 was mechanically sound, its license valid until 2034. It just needed a customer willing to pay for its resurrection. In Microsoft, desperately seeking power for its data centers in the PJM grid, Constellation found that customer.

The negotiations were complex, conducted in secret for months. Microsoft wanted certainty—fixed prices, guaranteed delivery, no regulatory surprises. Constellation wanted returns that justified a $1.6 billion investment. The project would require approximately $1.6 billion for capital expenditures necessary to restart the plant, with an in-service date targeted for 2028.

On September 20, 2024, they announced the deal that shocked the energy world. Microsoft would buy 100% of the plant's output for 20 years. The plant would be renamed the Crane Clean Energy Center, honoring Chris Crane who passed away in April 2024. The symbolism was perfect: America's most notorious nuclear accident site reborn to power the AI age.

Wall Street's reaction was explosive. Constellation's stock jumped 20% in a week. The deal didn't just validate the nuclear renaissance thesis—it supercharged it. If Three Mile Island could be restarted, what about other shuttered plants? The land rush was on.

VI. The Microsoft Deal & Three Mile Island Resurrection

Inside Microsoft's Redmond headquarters in early 2024, a crisis was brewing. The company's AI ambitions—pouring billions into OpenAI, integrating Copilot across its entire suite, competing with Google and Amazon in the AI arms race—had created an infrastructure problem no one had fully anticipated. Data centers in Northern Virginia, the world's largest concentration, were already consuming more electricity than entire countries. Microsoft alone needed thousands of additional megawatts, and they needed it yesterday.

Brad Smith, Microsoft's president, had made carbon negativity by 2030 a cornerstone commitment. But every new data center made that promise harder to keep. Solar and wind projects took years to develop and couldn't guarantee round-the-clock power. The math was simple and brutal: without nuclear, Microsoft couldn't be both AI leader and climate champion.

Bobby Hollis, Microsoft's vice president of energy, approached Constellation with an audacious proposal in March 2024. What would it take to restart Three Mile Island Unit 1? The initial response was skepticism. The plant had been shuttered for five years. Systems were mothballed. The workforce dispersed. The regulatory approvals alone could take years.

But Dominguez saw opportunity where others saw obstacles. Constellation had retained the plant's licenses, kept critical systems maintained, even preserved the institutional knowledge through former operators now working at other facilities. They'd run the numbers quietly for years, waiting for the right moment and the right partner.

The technical challenges were formidable. The reactor vessel and containment structure were sound—nuclear plants are essentially overbuilt bunkers designed to last centuries. But auxiliary systems needed complete overhauls: cooling towers rebuilt, turbines refurbished, control systems digitized. The steam generators, each the size of a school bus and critical to plant operation, required extensive inspection and repair.

More challenging was reassembling the human infrastructure. A nuclear plant requires 600-700 highly skilled operators, engineers, and technicians. The original Three Mile Island workforce had scattered to other plants or retired. Constellation launched a recruitment campaign, offering bonuses to lure talent back, partnering with local community colleges to train new operators.

The regulatory gauntlet was byzantine. The Nuclear Regulatory Commission needed to approve the restart—unprecedented for a plant closed this long. The Pennsylvania Department of Environmental Protection required new permits. PJM, the regional grid operator, had to validate the plant could reliably deliver power. The Federal Energy Regulatory Commission had to approve the transmission arrangements.

But the biggest challenge was public perception. Three Mile Island remained America's nuclear boogeyman, its very name shorthand for atomic disaster. Local communities near Middletown, Pennsylvania, had mixed feelings. Some welcomed the jobs and tax revenue. Others remembered the fear of 1979, the evacuation preparations, the decades of stigma.

Constellation launched a charm offensive. Town halls, community meetings, local newspaper op-eds. They emphasized what had changed: modern safety systems, multiple backup generators, real-time monitoring technology that didn't exist in 1979. They promised local hiring, community investment, transparent operations. They even involved Microsoft, having executives explain why this project mattered for American competitiveness in AI.

The September 20, 2024 announcement was orchestrated perfectly. Constellation executed a 20-year power purchase agreement with Microsoft that would support the restart of Three Mile Island Unit 1, with Microsoft purchasing the output to help power its data centers in PJM with clean energy. The financial terms, while not fully disclosed, were reported to guarantee Constellation returns well above typical power contracts—industry sources suggested $100+ per megawatt-hour versus market prices around $40.

The renaming to Crane Clean Energy Center was strategic beyond honoring the late CEO. It signaled a break from the past, a new chapter. The investment required was massive—approximately $1.6 billion in capital expenditures—but the returns justified it. With Microsoft's guaranteed payments plus federal production tax credits, the plant would generate over $800 million in annual revenue once operational.

The ripple effects were immediate. Amazon, not to be outdone, announced its own nuclear deal weeks later, purchasing a data center campus powered by Talen Energy's Susquehanna plant. Oracle declared plans for data centers powered by small modular reactors. Google began negotiations with multiple nuclear operators. The tech industry's embrace of nuclear was complete.

For Constellation, the Microsoft deal was transformative beyond the immediate economics. It validated their entire strategy, proved the value of maintaining optionality on shuttered assets, and positioned them as the partner of choice for tech giants needing clean, reliable power. The stock price reflected this new reality, climbing toward $200 per share, valuing the company at over $80 billion by year-end 2024.

But perhaps the most profound impact was psychological. Three Mile Island, the disaster that had haunted the nuclear industry for 45 years, was being resurrected to power humanity's next technological leap. If that transformation was possible, anything was.

VII. Business Model & Market Position

Understanding Constellation's business model requires thinking beyond traditional utility frameworks. This isn't a company that simply generates electricity and sends bills. It's an integrated energy platform that monetizes nuclear expertise across generation, trading, retail supply, and increasingly, bespoke infrastructure solutions for hyperscale customers.

Constellation ranked as the No. 1 producer of emissions-free energy with the lowest carbon dioxide emissions rate for the 11th consecutive year. The nuclear fleet, producing 180 million megawatt-hours annually, forms the foundation. But the real value creation happens in how that power flows through the rest of the business.

Start with the generation portfolio. The company operates approximately 31,676 megawatts of generating capacity, but not all megawatts are created equal. The nuclear plants run at 94%+ capacity factors, meaning they're essentially always on. The natural gas plants fire up during peak demand when prices spike. The renewables provide diversity and green credentials. This portfolio approach allows Constellation to optimize across different market conditions.

The trading operation, inherited from the old Constellation and refined under Exelon, is Wall Street-caliber. They don't just sell power—they optimize it across time, location, and market conditions. When polar vortex conditions send spot prices to $1,000 per megawatt-hour, Constellation's traders have already positioned the portfolio to capture those spikes while maintaining customer obligations.

But the real sophistication lies in the commercial business. Constellation serves 16 million customers, from residential homes to Fortune 100 headquarters. For large commercial and industrial customers, they're not just providing electrons but comprehensive energy management: demand response programs, efficiency solutions, on-site generation, and crucially, carbon-free energy certificates that allow companies to meet sustainability goals.

The integration between these businesses creates competitive moats. A Fortune 500 company might buy baseline power from Constellation's retail arm, carbon-free energy certificates from the nuclear fleet, demand response services from the trading desk, and backup generation from the distributed energy business. No other competitor can offer this full stack.

The numbers tell the story. Gross margins in the generation business exceed 30%, remarkable for what many consider a commodity business. The retail operation, typically low-margin, generates 15%+ margins through sophisticated pricing and risk management. The trading operation adds another $500-800 million in annual earnings, pure optimization value.

Customer concentration, often seen as risk, is actually strategic. Three-quarters of the Fortune 100 work with Constellation—these aren't price-sensitive buyers but sophisticated energy consumers who value reliability, sustainability, and partnership. Microsoft isn't just buying power; they're buying certainty, carbon credits, and grid priority during constrained conditions.

The operational excellence that underpins everything can't be overstated. The nuclear fleet achieved a 94.6% capacity factor, compared to industry average of 90%. That 4.6% difference equals an extra 8 million megawatt-hours of production—at $50 per megawatt-hour, that's $400 million in additional revenue with essentially no incremental cost.

The balance sheet reflects this operational strength. Despite capital intensity, Constellation generates over $3 billion in annual free cash flow. Debt is manageable at 2.5x EBITDA. The company grew its dividend by 25% in 2024, bringing total dividend increase to 150% in two years, while completing a $1 billion share buyback and authorizing another $1 billion program.

Looking ahead, the growth algorithm is compelling. Base earnings grow with inflation-adjusted power prices. The nuclear production tax credits add $15 per megawatt-hour through 2032. Capacity payments from grid operators are rising as reliability becomes scarce. New long-term contracts with tech companies provide step-changes in profitability. And the Crane Clean Energy Center restart adds $800 million in high-margin revenue starting in 2028.

The competitive position is nearly unassailable. Building new nuclear plants takes 10-15 years and $10+ billion. The regulatory expertise, operational knowledge, and workforce training create barriers that money alone can't overcome. Constellation controls scarce assets in an environment where scarcity is increasing.

This isn't disruption risk like utilities face from rooftop solar or batteries. This is selling the one thing that modern economy can't function without: reliable, clean, baseload power. As one analyst put it: "Constellation isn't in the electricity business. They're in the physics business. And physics always wins."

VIII. The AI Power Boom & Nuclear's Moment

The email that changed everything arrived at Constellation's headquarters in February 2023, months before ChatGPT mania peaked. It was from a data center developer in Northern Virginia, asking a simple question: "Can you deliver 500 megawatts of firm, carbon-free power by 2025?" The request was unprecedented—that's enough electricity to power 400,000 homes, needed at a single location, with 99.999% reliability.

This was the hidden crisis of the AI revolution. Every large language model query, every image generation, every autonomous vehicle simulation required massive computational power running 24/7 in temperature-controlled data centers. The infrastructure demands were staggering and accelerating exponentially. OpenAI's GPT-4 training alone reportedly consumed 50 gigawatt-hours—enough to power 5,000 homes for a year. The numbers were staggering. Goldman Sachs Research forecasts global power demand from data centers will increase by as much as 165% by the end of the decade (compared with 2023), while the IEA projects global electricity demand from data centres will more than double over the next five years, consuming as much electricity by 2030 as the whole of Japan does today. In the U.S. alone, data centers could consume 9% of the United States' electricity generation by 2030, with AI queries requiring approximately ten times the electricity of traditional internet searches.

The geography of this demand was highly concentrated. Virginia's "Data Center Alley" already consumed more power than many small countries. But the new AI facilities were different—instead of distributed clusters of 10-50 megawatt facilities, companies wanted single campuses consuming 500+ megawatts. That's nuclear plant scale. Amazon made the first move, buying a 960-megawatt data center campus from Talen Energy for $650 million that would be powered directly by the Susquehanna nuclear plant. The arrangement, called "behind the meter," essentially plugged the data center directly into the reactor, bypassing the grid entirely. It was nuclear power as a service—reliable, carbon-free, and massive in scale. Oracle went even further. Larry Ellison announced in September 2024 that the company was designing a data center that would be powered by three small modular reactors, calling the electricity demand from AI "crazy." "The electricity demand from artificial intelligence is becoming so 'crazy' that Oracle is looking to secure power from next-generation nuclear technology," Ellison told investors. The data center would require more than a gigawatt of electricity and would be powered by three small nuclear reactors.

The rush was on. Every major tech company needed nuclear partnerships yesterday. For Constellation, positioned with the largest fleet of operational reactors and deep expertise in nuclear operations, it was like being the only water vendor in a desert. They could name their price, structure deals to their advantage, and fundamentally reshape the economics of nuclear power.

The company's fleet powers more than 16 million homes and businesses, providing 10% of all clean power on the grid in the U.S., with annual output that is nearly 90% carbon-free. But the real value wasn't in serving traditional utility customers anymore—it was in becoming the critical infrastructure provider for the AI age.

The economics were transformative. Traditional power purchase agreements might fetch $40-60 per megawatt-hour. But tech companies, desperate for reliable, carbon-free power and facing the alternative of building their own generation (impossible in any reasonable timeframe), were willing to pay $80-100 or more. With federal production tax credits adding another $15 per megawatt-hour, nuclear plants that had struggled to break even were suddenly gold mines.

But perhaps the most profound shift was psychological. For decades, nuclear had been the energy source everyone loved to hate—too dangerous, too expensive, too complicated. Now, it was the only solution to power humanity's next technological leap. The industry that Three Mile Island nearly killed was being resurrected by the very site of that disaster. The AI revolution didn't just need nuclear power—it was making nuclear power cool again.

IX. Playbook: Business & Investing Lessons

Timing Matters: Surviving the Dark Years to Catch the Wave

Constellation's story is fundamentally about timing—not lucky timing, but strategic patience. The company and its predecessors held onto nuclear assets through the worst decade in the industry's history (2008-2018) when natural gas prices made nuclear plants money-losers. Many competitors sold or shuttered their reactors. Exelon/Constellation kept them running, often at losses, betting that the economics would eventually shift.

The lesson: In capital-intensive industries with long asset lives, the ability to survive downturns is often more important than optimizing for short-term returns. Constellation's balance sheet strength and operational excellence allowed them to weather the storm. When the tide turned—through climate policy, AI demand, and natural gas price recovery—they owned irreplaceable assets that competitors couldn't quickly replicate.

The Value of Operational Excellence in Commodity Businesses

Nuclear plants are essentially identical—they split atoms to boil water to spin turbines. Yet Constellation's fleet consistently operates at 94%+ capacity factors versus 90% industry average. That 4% difference translates to $400 million in additional annual revenue with minimal incremental cost.

This operational edge comes from thousands of small improvements: shorter refueling outages (25 days versus industry average of 30), better preventive maintenance schedules, optimized fuel loading patterns, and superior workforce training. In commodity businesses where you can't differentiate the product, operational excellence becomes the only sustainable competitive advantage.

Policy as Strategy: How Constellation Shaped Its Own Market

Rather than accepting market conditions as given, Constellation actively shaped the policy environment. The company spent years lobbying for Zero Emission Credits in state capitals, making the economic case that nuclear plants provided grid reliability and carbon-free power worth subsidizing. They helped design the nuclear production tax credits in the Inflation Reduction Act.

This wasn't just lobbying—it was strategic market creation. By quantifying nuclear's value beyond just electrons (reliability, carbon reduction, jobs), Constellation created new revenue streams that didn't previously exist. The lesson: In regulated or policy-adjacent industries, the ability to shape the rules can be more valuable than playing by them.

Capital Allocation: When to Hold, When to Fold, When to Restart

Constellation's capital allocation reveals clear priorities. During the dark years (2012-2020), they minimized capital expenditure, focusing only on safety and essential maintenance. As markets improved, they pivoted to optimization—spending on turbine upgrades and efficiency improvements with quick paybacks. Now, with long-term contracts from tech giants, they're willing to invest $1.6 billion to restart Three Mile Island.

The discipline is remarkable. The company estimates the Three Mile Island restart project will require approximately $1.6 billion of cash from operations for capital expenditures necessary to restart the plant. They're not building new reactors from scratch ($10+ billion ventures). They're not chasing small modular reactor technology that won't be commercial for a decade. They're investing in proven assets where they have operational expertise and contracted revenue.

Platform Power: Why Scale and Expertise Compound

Constellation isn't just a collection of power plants—it's an integrated platform spanning generation, trading, and retail supply. This creates powerful synergies. The trading desk optimizes output across the entire fleet, capturing price spikes and managing risk. The retail business provides stable cash flow and customer relationships. The nuclear expertise allows them to operate plants others can't.

This platform approach creates compounding advantages. The company achieved a nuclear operating capacity factor of 94.6% and 94.4% for the twelve months ended December 31, 2024 and 2023, respectively. Each additional nuclear plant benefits from shared expertise, standardized procedures, and centralized support functions. A new entrant would need to replicate not just the physical assets but decades of accumulated knowledge and systems.

The Contrarian Bet: Sticking with Nuclear When Everyone Else Ran

The biggest lesson may be the simplest: sometimes the best investments are in unfashionable assets that solve real problems. When Constellation was accumulating nuclear plants in the 2000s, the consensus view was that nuclear was dying. Natural gas was the future. Renewables would dominate. Nuclear was too expensive, too risky, too politically toxic.

Constellation's leaders understood something the market missed: nuclear's unique attributes (24/7 operation, massive scale, zero emissions) would eventually be valued appropriately. They couldn't predict ChatGPT or the AI boom, but they understood that a developed economy needs reliable, clean baseload power. They positioned for that future and waited.

The wait required conviction. During 2014-2016, when gas prices stayed below $3 and nuclear plants were closing monthly, it would have been easy to give up. Many did. Entergy exited merchant nuclear. FirstEnergy tried to. But Constellation held on, improved operations, fought for policy support, and positioned for the turn.

When the turn came—climate urgency, AI explosion, grid reliability concerns—Constellation was the last man standing with the assets everyone suddenly needed. As of August 2025 Constellation Energy has a market cap of $105.43 Billion USD. This makes Constellation Energy the world's 181th most valuable company according to our data. The contrarian bet paid off spectacularly.

X. Analysis & Bull vs. Bear Case

Bull Case: The Structural Winner in a Power-Short World

The bull case for Constellation rests on three pillars, each reinforcing the others. First, the demand picture is unlike anything in modern history. The IEA projects that electricity demand from data centres worldwide is set to more than double by 2030 to around 945 terawatt-hours (TWh), slightly more than the entire electricity consumption of Japan today. AI will be the most significant driver of this increase, with electricity demand from AI-optimised data centres projected to more than quadruple by 2030. This isn't speculative—Microsoft, Amazon, Google, and Oracle have already committed hundreds of billions to AI infrastructure that requires power.

Second, nuclear is the only scalable solution for 24/7 carbon-free power. Solar and wind, even with batteries, can't guarantee 99.999% reliability that data centers require. Natural gas works but produces emissions that violate tech companies' carbon commitments. Nuclear provides baseload power with zero emissions—there's simply no substitute at scale.

Third, Constellation has already won. They control the largest nuclear fleet, have the operational expertise, and are signing long-term contracts at rates well above market prices. The Microsoft deal to restart Three Mile Island validates the thesis. "For the second consecutive year since forming our new company, Constellation has outperformed the top end of its guidance range – a testament to the combined value of our commercial and generation businesses, which were firing on all cylinders in 2024," said Dan Eggers, chief financial officer.

The financial algorithm is compelling. Base earnings grow with inflation and power demand. The nuclear production tax credit adds $2.7 billion annually through 2032. New tech contracts provide step-function margin expansion. The company's guidance for 13% annual earnings growth through 2030 (up from 10% previously) may prove conservative.

Barriers to entry are essentially insurmountable. Building new nuclear plants takes 10-15 years and $10+ billion. The regulatory expertise alone takes decades to develop. The workforce—nuclear engineers, operators, technicians—can't be created quickly. Constellation's assets are irreplaceable in any timeframe relevant to investors.

Bear Case: The Regulatory Sword of Damocles

The bear case starts with regulatory risk—the sword hanging over every nuclear operator. One significant accident anywhere globally could shut down plants or impose costly new requirements. The Nuclear Regulatory Commission could change standards, extend outage requirements, or deny license extensions. State or federal politics could shift against nuclear despite current bipartisan support.

Capital intensity remains daunting. The Three Mile Island restart requires $1.6 billion—and that's for a plant that's already built. Life extensions, upgrades, and eventual decommissioning require massive capital investments with uncertain returns. Rising interest rates make these investments less attractive and could pressure valuations.

Competition from alternative technologies poses a long-term threat. Small modular reactors, while not commercial today, could democratize nuclear power in the 2030s. Fusion, perpetually 20 years away, might finally arrive. More realistically, the combination of renewables, batteries, and demand response could provide the reliability that currently requires nuclear.

Customer concentration risk is real and growing. If Microsoft, Amazon, and a handful of tech giants represent an increasing share of earnings, Constellation becomes vulnerable to their financial health and strategic pivots. What happens if AI advancement slows, if new algorithms require less compute, if tech companies face antitrust breakups?

Political risk around nuclear subsidies looms large. The production tax credits expire in 2032. State zero-emission credits face ongoing legal challenges. A change in federal administration could eliminate support programs. Without subsidies, many nuclear plants return to marginal economics.

The valuation already prices in significant success. Constellation Energy has a market cap or net worth of $105.44 billion as of August 7, 2025. Its market cap has increased by 75.65% in one year. At over $100 billion market cap, Constellation trades at premium multiples assuming flawless execution and continued policy support. Any disappointment—operational issues, regulatory changes, customer delays—could trigger significant multiple compression.

The Verdict: A Generational Position with Known Risks

On balance, Constellation appears positioned to be one of the great infrastructure winners of the AI age. The demand surge is real and accelerating. The competitive moat is genuine and widening. The management team has proven execution capability through multiple cycles.

The risks are serious but known and manageable. Regulatory oversight, while strict, provides stability—the NRC won't allow unsafe operations but also won't arbitrarily shut down compliant plants. Capital intensity is offset by long-term contracts and federal support. Technology disruption is possible but not imminent.

The key insight: Constellation isn't really in the electricity business—they're in the reliability business. As the economy digitizes and artificial intelligence proliferates, the value of 24/7 reliable power only increases. In a world where a microsecond of downtime can cost millions, Constellation's nuclear fleet isn't just valuable—it's irreplaceable.

For long-term investors, the question isn't whether Constellation will face challenges—they will. It's whether the structural tailwinds (AI power demand, climate urgency, grid constraints) overwhelm the headwinds. The bet is that atoms splitting in concrete containment vessels, a 1950s technology, will power the 2030s digital revolution. It's an unlikely marriage of old and new, but perhaps that's exactly what makes it powerful.

XI. Epilogue: The Future of Energy

Standing at the renamed Crane Clean Energy Center in 2028, when Unit 1 comes back online after nearly a decade of silence, will mark more than just a plant restart. It will symbolize American energy policy coming full circle—from nuclear optimism in the 1950s, through Three Mile Island's trauma in 1979, to nuclear's resurrection as the foundation of the AI age.

Constellation Energy committed to achieving 100% carbon-free electricity generation by 2040, a goal that seemed aspirational when announced but now appears conservative. The company is planning to upgrade other existing reactor plants to provide more power, squeezing every possible megawatt from the existing fleet through turbine upgrades, efficiency improvements, and advanced fuel designs. The next frontier presents both opportunity and threat. Small modular reactors, promised for deployment in the late 2020s to early 2030s according to the Department of Energy, could democratize nuclear power. Companies like NuScale, TerraPower, and Kairos Power are racing to commercialize designs that would be factory-built and deployable at smaller scale. If successful, they could undermine Constellation's scarcity value—but they're still years from commercial reality, with the most optimistic estimates placing widespread deployment in the early 2030s.

More immediately, Constellation faces a generational opportunity. Dozens of shuttered nuclear plants across America could theoretically be restarted. Palisades in Michigan, Indian Point in New York, Duane Arnold in Iowa—each represents billions in potential value if the economics align. The Three Mile Island precedent shows it's possible, but each restart requires a creditworthy customer, regulatory approval, and massive capital investment.

The company is also planning to upgrade other existing reactor plants to provide more power. Through advanced fuel designs, turbine upgrades, and operational improvements, Constellation believes it can add thousands of megawatts without building new plants—capital-light growth that drops straight to the bottom line.

What the Microsoft deal really means extends beyond one contract or one plant. It represents the rehabilitation of nuclear power in American consciousness. The facility that symbolized nuclear disaster for two generations will now power the technology defining the next generation. It's a narrative reversal so complete it seems scripted.

For founders and builders, the Constellation story offers profound lessons. Sometimes the biggest opportunities come from assets everyone else has abandoned. Sometimes old technology solves new problems better than cutting-edge innovation. Sometimes the key to the future is hidden in the infrastructure of the past.

The company that began lighting Baltimore's streets with gas in 1816 now powers the algorithms shaping human knowledge. The plants built during the Cold War now enable the AI revolution. The industry Three Mile Island nearly destroyed has been resurrected by that very site.

As Dominguez said on the February 2025 earnings call, "There has never been a more exciting time for our country and for the energy industry. We are privileged to be at the heart of it all." He's not wrong. In the race to power the AI age, the winner won't be the company with the newest technology or the boldest vision. It will be the one with atoms splitting in concrete containment vessels, technology from the 1950s, operated with excellence honed over decades.

Nuclear power is dead. Long live nuclear power.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube