Procore Technologies: Building the Operating System for Construction

The Central Question: From Carpenter's Frustration to $10 Billion Empire

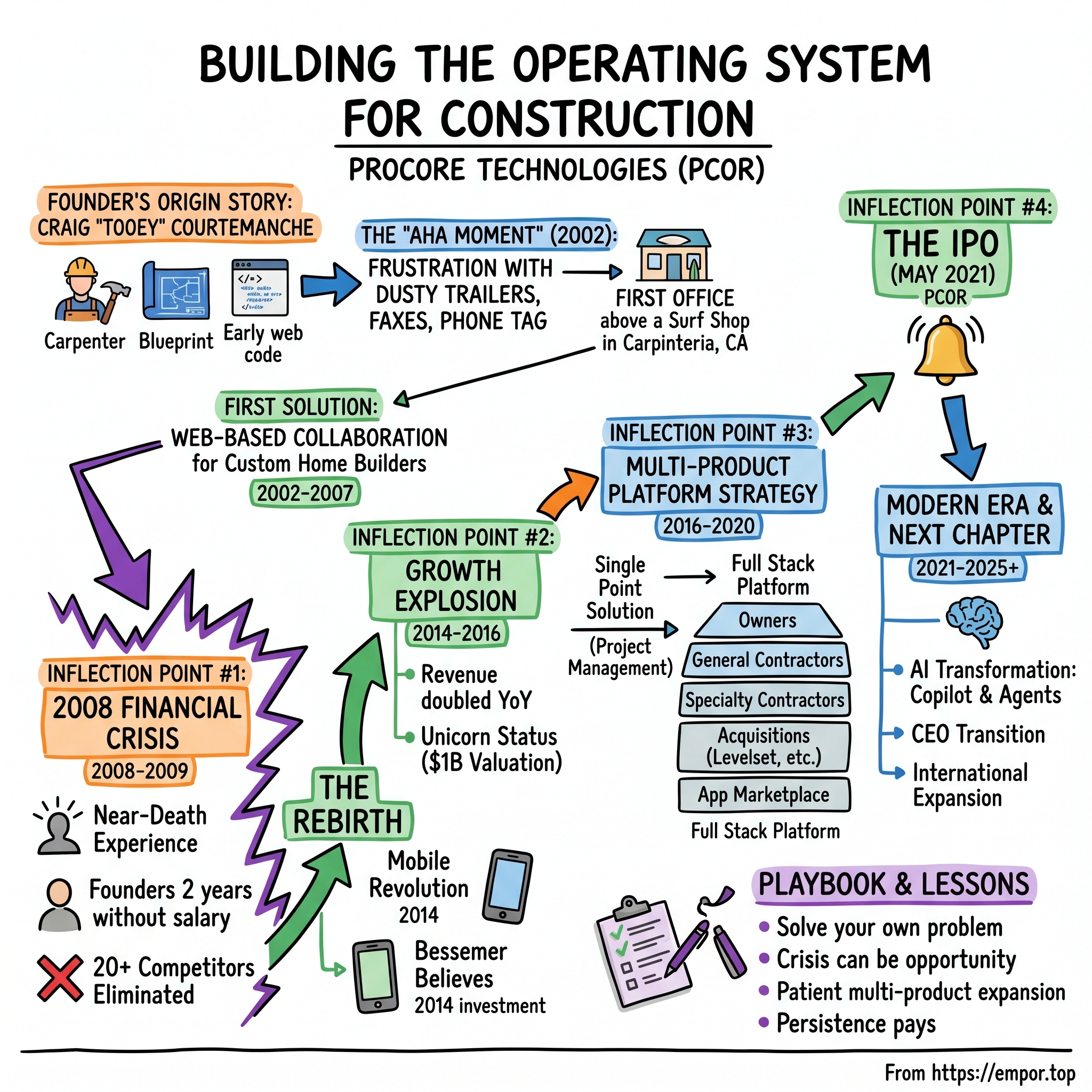

Picture a dusty construction trailer in Santa Barbara, 2002. A frustrated homeowner is drowning in fax transmissions, playing telephone tag with contractors, and watching his dream home project slip into chaos. That homeowner wasn't just any disgruntled client—he was Craig "Tooey" Courtemanche, a veteran of Silicon Valley's dot-com boom, and he was about to channel that frustration into building one of the most consequential vertical SaaS companies of the modern era.

Under his leadership, Procore grew from $9.6M in revenue after 13 years to over $890M in revenue 8 years later, expanding its user base to over 2 million across 150+ countries. That trajectory—the patient first act followed by explosive growth—makes Procore one of the most fascinating case studies in enterprise software.

The company describes itself as "helping transform one of the oldest, largest and least digitized industries in the world," focusing exclusively on construction, connecting and empowering the industry's key stakeholders, such as owners, general contractors, specialty contractors, architects, and engineers.

But the numbers alone don't capture the drama. This is a story of near-death experiences during the 2008 financial crisis, of founders going without salary for two years, of competitors being wiped out while Procore somehow survived. It's a masterclass in patient capital deployment, multi-product expansion, and the unique challenges of bringing technology to an industry that had barely progressed beyond clipboards and carbon copies.

Procore's annual revenue for 2024 reached $1.152B, a 21.23% increase from 2023. As of December 2024, the company had 17,088 organic customers and achieved a gross revenue retention rate of 94%. The path from a small office above a Santa Barbara surf shop to a $10+ billion public company spans over two decades of persistence, pivots, and a founder who simply refused to quit.

II. The Founder's Origin Story: Tooey Courtemanche

The Builder at Heart

Long before software, before venture capital, before construction technology became a recognized category, there was a young man fascinated by the physical act of creation. Founder and CEO Craig "Tooey" Courtemanche started his career as a carpenter and served as a real estate developer, before starting a tech company in Silicon Valley.

Courtemanche, nicknamed "Tooey" because he shared the same first name as his father, wasn't born into the technology world—he arrived there circuitously, through sawdust and blueprints. He grew up with exposure to the construction industry through family connections. This early exposure would later influence his understanding of the industry's needs when founding Procore.

Tooey Courtemanche attended the University of Arizona from 1986 to 1987. Although specific details about his major or degree are not available, this educational experience likely contributed to his diverse background and the development of his skills in both construction and software. His path was unconventional—neither a Stanford computer science graduate nor a McKinsey consultant, but someone who had actually swung hammers and understood the chaos of a job site.

The Silicon Valley Detour

The 1990s transformed Courtemanche from a builder of physical structures into a builder of digital ones. His path into entrepreneurship was unorthodox. He was a veteran of the first dot-com bubble, living in Santa Barbara, and had spent a decade struggling to get widespread adoption of Procore. A few times in those early years, the company even struggled to make payroll.

During the tech boom, Courtemanche learned to code and solve engineering challenges, eventually starting his own software development company focused on web applications in 1996. This dual expertise—understanding construction from the inside out while possessing the technical skills to build software—would prove to be his ultimate competitive advantage.

Before settling on construction software, Courtemanche experimented with several other business ideas, including ventures unrelated to construction technology. In the early days of Procore, he personally coded parts of the initial software despite not having formal training as a software developer.

What made Courtemanche different from other tech founders was his intimate understanding of the customer. He didn't need to commission focus groups or run design thinking workshops. He knew the frustrations firsthand because he had lived them—both as a carpenter on job sites and as an owner trying to manage a complex construction project.

III. The "Aha Moment" & Founding (2002)

When Personal Pain Becomes Business Opportunity

The genesis of Procore came not from market research but from genuine frustration. When building his home in Santa Barbara, Tooey realized that he could apply his technology background in the field of construction. The app he built served to better manage the construction process.

Courtemanche founded Procore in 2002 after seeing how disconnected the construction process could be on a family building project. He developed the first versions of what would become Procore's construction management platform to allow users to see all critical path activities in a single platform.

Phone calls and fax machines were the default communication modes with contractors. When Courtemanche looked at the sheer complexity of coordination—dozens of subcontractors, hundreds of documents, thousands of decisions—and the lack of any streamlined communication system, he saw both a massive problem and a massive opportunity.

The First Solution

The initial step was deceptively simple: build a web-based collaboration tool around Microsoft Project schedules. This tool made it possible to gather feedback from team members about what was actually going to happen against the plan. By just getting everyone on the same page, the team began avoiding mistakes on the job site.

He founded Procore in 2002 with a mission to connect everyone in construction on a global platform and is passionate about bringing together two often disparate worlds: construction and software.

Starting Small—Very Small

Procore's first office was located above a surf shop in Carpinteria, California – a small beach town near Santa Barbara. This unconventional starting point is quite different from the typical Silicon Valley or major tech hub origin story of most successful software companies.

In 2002, Courtemanche founded Procore in Carpinteria, California. The initial years were challenging – he bootstrapped the company and worked to convince an industry traditionally resistant to technological change to adopt cloud-based solutions.

This choice of location would prove significant. Being based in a beach town rather than Silicon Valley meant lower costs but also less access to venture capital networks—a trade-off that would shape the company's slow, methodical early growth.

IV. The Early Struggles & Finding Product-Market Fit (2002-2007)

Learning Construction From the Inside

Courtemanche took a deliberate approach to understanding his market. He visited job sites constantly, learning about the inefficiencies that project managers faced daily. The result was a suite of tools built for actual construction workflows: a daily job log, a two-week look-ahead, a system for managing RFIs (Requests for Information), and a way to share project schedules.

The Celebrity Home Builder Niche

Procore first started as a niche tool for high-net-worth residential builders in places like Aspen and Beverly Hills. "Our first customers were building homes for Eddie Murphy, Barbara Streisand, and Ben Stiller," Tooey recalls. For Procore's early customers, it was a combination of a homeowner who was on the road a lot and a distributed builder team. There was complexity around each home project as most of these homes were built like commercial buildings. Procore quickly found early product-market fit by being narrowly focused and doubling down on its customer profile of custom home builders serving high-net-worth individuals.

This initial focus on luxury residential construction was clever positioning. These projects had commercial-level complexity but were managed by small teams that could adopt new technology quickly. The wealthy homeowners were often tech-savvy themselves and frustrated by the industry's primitive communication methods.

The Resistance Problem

The construction industry's resistance to technology cannot be overstated. This was—and remains—an industry that relied on paper, fax machines, phone calls, and relationships built over decades. Many construction professionals had never used computers on job sites. Internet connectivity at construction sites was rare to nonexistent in the early 2000s.

The $12 trillion architecture, engineering, and construction (AEC) industry has been among the slowest to digitize and innovate.

Steve Zahm, founder of the e-learning company DigitalThink, joined Procore as president in 2004. Procore's revenue in 2012 was $4.8 million. After ten years of effort, the company was still tiny by venture capital standards—barely a viable small business.

The Funding Foundation

Procore Technologies raised nearly $500 million in venture capital funding prior to its initial public offering (IPO) in June 2021, across multiple rounds spanning from 2007 to 2020. The company's funding journey began with a Series B round of $4 million in January 2007, led by Great Pacific Capital.

With the benefit of its first institutional round (true believers like Kevin O'Connor had personally supported the company prior to our investment), Procore had the money to start building a scalable and methodical outbound sales engine.

But the timing of this early funding could not have been worse. Within eighteen months of closing that round, the world would change dramatically.

V. Inflection Point #1: The 2008 Financial Crisis—Near-Death and Rebirth

When the World Stopped Building

The 2008 financial crisis didn't just hurt Procore—it nearly killed it. Almost overnight, residential construction came to a halt, and Procore's customer base evaporated.

It took a while to take off, and almost died during the Great Financial Crisis. But then as mobile took off and more, it accelerated and grew to become the #1 U.S. player in construction SaaS.

Construction ground to a halt in 2008-2009, and so did Procore. The founders never quit. But one seed investor had to write a bridge check for them to make it. And almost all their competitors went belly up.

The numbers tell the story starkly. Companies that had been Procore's customers simply stopped building. Projects were cancelled or indefinitely delayed. General contractors laid off workers and shut down offices. The construction software market—never large to begin with—virtually disappeared.

The Survival Strategy

The founders went without salary for two years. Let that sink in: for twenty-four months, Courtemanche and his team worked without pay, burning through personal savings to keep the company alive. This wasn't the glamorous sacrifice of a founder who knows a big funding round is coming—this was genuine uncertainty about whether the company would exist next month.

The company pivoted toward commercial projects, which were slightly more resilient than the residential sector. But even that was a desperate gamble in an industry that had essentially frozen.

The Accidental Competitive Advantage

The Great Financial Crisis was actually a massive competitive advantage. Most SaaS founders think economic downturns are purely negative, but for Procore, the 2008 crisis was an "extinction level event" that wiped out 20+ competitors. While painful (the founders went without salary for 2 years), emerging as one of the few survivors gave them an almost unbeatable market position.

This is one of the most counter-intuitive lessons from Procore's story. The crisis that nearly destroyed them also eliminated their competition. When the construction industry finally recovered, Procore was one of the few construction software companies left standing. They had earned market share through sheer survival.

The SaaS Pivot

During this period, Procore made another critical decision: pivoting from a traditional licensing model to a subscription-based SaaS model. This shift was radical for enterprise software at the time—Salesforce had pioneered the approach, but it was far from universally accepted. For a construction software company selling to an industry skeptical of technology, asking customers to pay ongoing subscription fees rather than one-time license costs was a bold bet.

The decision proved prescient. The subscription model created predictable recurring revenue and aligned Procore's incentives with customer success—if customers stopped finding value, they could simply not renew.

VI. Inflection Point #2: Mobile Revolution & Venture Capital (2014-2016)

The Smartphone Changes Everything

The single greatest technology shift for construction software wasn't cloud computing or artificial intelligence—it was the smartphone. For the first time in history, construction workers could access software on job sites.

With the birth of the mobile era, construction finally had internet connectivity on the job site through smartphones and tablets. Procore could take advantage of its cloud and mobile platform to help teams involved in complex construction projects to collaborate. Procore's business took off.

Think about what this meant in practice. Before smartphones, any construction software required workers to return to the office trailer or home office to enter data. By the time information was logged, it was already outdated. Real-time collaboration was impossible.

Smartphones and tablets changed the fundamental economics of construction software. Suddenly, a superintendent could photograph a defect, tag it to a specific location on a blueprint, and immediately notify the responsible subcontractor—all from the job site. This wasn't incremental improvement; it was category-creating capability.

Bessemer Believes

In 2014, Bessemer Venture Partners led a $15 million investment round. In 2015, the company raised an additional $30 million in a round led by Bessemer and Iconiq Capital.

When Tooey and I started talking back in 2014, there was an immediate meeting of minds. At Bessemer, we had long been convinced of the power of purpose-built "vertical" software to transform industries. And there were few industries as large and as underserved by software as construction. Tooey's passion for the construction industry was magnetic. His vision for Procore—a platform where the entire construction industry could collaborate—was exactly what we were looking for. Tooey's tenacity, his charisma, his obsession with his customers were the intangible qualities we often find in great CEOs that go on to have a lasting impact on the industries they serve.

The Growth Explosion

With the benefit of Dennis Lyandres, a phenomenal new sales leader (now the CRO), Procore invested intelligently and aggressively behind the "sales and marketing learning curve". The approach proved key to building a powerful sales and customer success organization that could tackle different market segments, from small and mid-sized builders to large companies. In the first year of our investment, Procore more than doubled its ARR growth rate—a rate of acceleration that we have never seen in the Bessemer portfolio.

When Lyandres first joined the company's sales department in 2014 revenue was in the "$10 million" range. Throughout his tenure as head of sales, Procore nearly doubled revenue year-over-year, ending 2017 with over $100 million in revenue.

The growth was staggering. From $9.6 million after thirteen years to over $100 million in revenue within three more years—this wasn't gradual improvement; it was exponential acceleration.

Unicorn Status

In 2015, the Wall Street Journal reported the company to be worth "$500 million post-money." In 2016, the company raised $50 million in a round led by Iconiq, reaching a $1 billion valuation.

Procore had become a unicorn—a company valued at over $1 billion—after more than a decade of patient building. Unlike many unicorns of the 2010s that achieved massive valuations within a few years of founding, Procore's valuation reflected years of accumulated domain expertise, customer relationships, and proven execution.

VII. Inflection Point #3: The Multi-Product Platform Strategy (2016-2020)

From Point Solution to Platform

One of the most consequential strategic decisions in Procore's history was the deliberate, patient expansion from a single product to a comprehensive platform. Procore provides end-to-end construction management software for owners, general contractors, and specialty contractors. It has a unified platform with solutions for various phases of work—including preconstruction, project management, workforce management, and financial management—as well as analytics. Procore also connects to third-party integrations through its App Marketplace.

Today, the average Procore customer uses three to four products, with large enterprises using five to six. "The era of point solutions is over," Tooey states. Customers expect an all-in-one platform and vertical SaaS founders must deliver from day one.

But here's the crucial insight: Procore didn't start implementing their multi-product strategy until years 14-15 of the company's existence. This was intentional—they waited until customers specifically asked for new products.

Building the Ecosystem

Procore integrates with over 500 tools, ensuring it fits into any tech stack. This ecosystem approach reflected a key strategic insight: construction companies use dozens of different software tools, and any platform that required wholesale replacement of existing systems would face massive resistance.

Instead, Procore positioned itself as the central nervous system for construction data, connecting to accounting systems like Sage, design tools from Autodesk, and hundreds of specialized applications through its marketplace.

Funding the Expansion

Procore Technologies Inc, a provider of cloud-based construction management applications, announced today it has raised a $75 million Series H round from Tiger Global Management, bringing its valuation to $3 billion.

In 2018, the company raised an additional $75 million, and in 2020, it raised over $150 million. In total, the company raised nearly $500 million from 2007 through its IPO in 2021.

The capital allowed Procore to pursue an aggressive product development agenda while also funding acquisitions that would fill gaps in their platform.

VIII. Acquisition Strategy & Building the Full Stack

Strategic M&A

Procore has pursued acquisitions strategically to fill specific gaps in its platform capabilities. In July 2019, Procore acquired US project management software group Honest Buildings. In October 2020, it acquired US estimating software provider Esticom. Procore acquired construction artificial intelligence companies Avata Intelligence in 2020, and INDUS.AI in 2021.

The Levelset Deal: Procore's Largest Acquisition

Procore Technologies, Inc. (NYSE: PCOR), has completed its acquisition of Levelset, strengthening its position as a leading provider of construction management software. This acquisition will add lien rights management to the Procore platform, enabling Procore to manage complex compliance workflows and improve the payment process in construction.

The acquisition is its largest ever and comes months after its $635-million IPO. Procore is acquiring lien management and construction payments technology company Levelset for $500 million. The acquisition includes roughly $425 million in cash and $75 million in Procore common stock. The deal would be Procore's largest acquisition ever.

Levelset CEO Scott Wolfe, Jr. said, "Over 250,000 users have deployed Levelset on more than 6.5 million construction projects. This activity generates highly reliable payment and relationship data."

The Levelset acquisition was particularly strategic because it addressed one of construction's most vexing problems: getting paid. The construction industry has the slowest payment cycles of any major sector, with projects typically experiencing 90 days sales outstanding and 74 days payable outstanding. Lien rights management is complex, varies by state, and creates enormous administrative burden.

Recent Acquisitions

The company has continued acquiring capabilities in 2023 and 2024, including Intelliwave Technologies for workforce tracking and Unearth Technologies for geographic information systems (GIS). Most recently, in May 2025, Procore acquired Novorender, a provider of cloud-based 3D visualization tools.

IX. Inflection Point #4: The IPO (May 2021)

Ringing the Opening Bell

Construction management software firm Procore Inc. sold 9.47 million shares for $67 each in a May 20 initial public offering on the New York Stock Exchange. The technology startup and its bankers had marketed shares for $60 to $65 before its IPO, an exchange filing showed. Listed under the ticker symbol PCOR, the stock outperformed its target and ended the trading day at $88 per share, giving the company a market value of more than $8.5 billion.

The initial public offering raised $634.5 million. Following the IPO, the company was valued at nearly $11 billion.

"Procore's IPO is a significant moment in our journey," CEO and founder Tooey Courtemanche said in a statement. "Even though I founded Procore nearly twenty years ago, it feels like we're just getting started. The construction industry is in the early stages of massive digital transformation. We are proud to be at the forefront of this shift."

The Long Road to Public Markets

As of May 2021, the company has over 10,000 customers, and over 2 million users of its products in more than 150 countries.

Courtemanche told TechCrunch: "We went into this IPO not needing the cash. We actually had lots of cash on hand so this is just an additional ability for us to have more resources because more resources means more flexibility and opportunity to execute when opportunities arise. We're just getting started." The company had initially planned to go public early last year, but Procore's IPO was caught up in the onset of COVID-19, leading to its delay.

The IPO was validation not just of Procore but of the entire construction technology category. Here was proof that a vertical SaaS company focused exclusively on construction could achieve massive scale and command premium valuations.

X. Modern Era: AI, International Expansion & The Next Chapter (2021-2025)

The AI Transformation

Procore uses AI in its platform. Two of the ways Procore is using AI are through Procore Copilot and Agents. Copilot is a generative AI tool that allows users to retrieve information from and summarize project documents. Procore Agents streamlines processes such as managing RFIs, scheduling, and submittals to automate tasks and reduce manual data entry. These AI tools support workflows across the full project lifecycle.

Procore announced a series of new product innovations, including the launches of Procore Artificial Intelligence and AI Agents, Resource Management, Safety, and Scheduling at Groundbreak 2024.

CEO Tully Cordemanche emphasized the importance of innovation, stating, "2025 is the year of agents."

CEO Craig Courtemanche highlighted positive feedback from customers using Copilot, which provides intelligent answers rather than just search results. He discussed the potential of Agents to monitor projects 24/7, improving schedule and budget management, and emphasized the unique advantage Procore has with its unified platform and data set.

CEO Transition

In March 2025, Procore announced a major leadership transition. After two decades since founding Carpinteria-based Procore and serving as the company's only CEO, Craig "Tooey" Courtemanche announced that he is planning to transition to executive chairman as soon as the company appoints a new chief executive. Courtemanche first founded Procore in 2002 and is currently the founder, president and CEO of the company. He led the company through many key milestones, including going public in 2021 and being valued at nearly $11 billion.

Procore announced the appointment of Ajei Gopal as Chief Executive Officer Designate, and a member of the company's Board of Directors. Gopal will succeed Procore's Founder, President, and CEO Tooey Courtemanche following the public announcement of the company's Q3 financial results, with an anticipated start date of November 10, 2025. Courtemanche will then transition out of operational responsibilities and focus on his role as Chair of the Board of Directors. Gopal has over 35 years of proven experience leading global technology companies at scale, most recently serving as the President and CEO of Ansys, Inc. from 2017 to 2025. Under Gopal's leadership, Ansys more than tripled its revenue, nearly quadrupled its market value, and became the global leader in engineering simulation.

Financial Performance

In the fourth quarter of 2024, Procore achieved a revenue of $302 million, marking a 16% increase compared to the previous year. For the full year, Procore's revenue reached $1.152 billion, a 21% increase year-over-year, with a non-GAAP operating margin of 10%.

Looking ahead, Procore is optimistic about its growth trajectory for 2025. The company anticipates revenue growth in the range of 12% for both the first quarter and the full year of 2025. Additionally, Procore aims to further improve its non-GAAP operating margins, targeting between 7% to 8% for Q1 2025 and 13% to 13.5% for the entire year.

XI. The Product & Business Model Deep Dive

How Procore Makes Money

Procore's business model is elegantly designed to grow with its customers. The company sells its products on a subscription basis with pricing generally based on the number and mix of products a customer subscribes to and the fixed aggregate dollar volume of construction work contracted to run on the platform annually—what Procore calls "annual construction volume."

As customers subscribe to additional products or increase their annual construction volume, Procore generates more revenue. Importantly, the company does not provide refunds for unused construction volume or charge customers based on consumption or on a per-project basis.

This pricing model creates interesting dynamics: successful construction companies that grow their business naturally become larger Procore customers without any additional sales effort required.

Platform Scale and Data Advantages

By 2023, Procore's platform had been used to manage over 1 million construction projects worldwide, processing hundreds of billions of dollars in construction volume annually. The platform handles an enormous amount of data, including millions of daily photos, documents, and communications from construction sites globally.

With over three million projects delivered in more than 150 countries, the company's platform supports teams from preconstruction through closeout.

Multi-Product Adoption

As of December 31, 2024, 75% of total annual recurring revenue was generated from customers using four or more products. As of December 31, 2024, 48% of total annual recurring revenue was generated from customers using six or more products.

This multi-product adoption is the key to Procore's unit economics. It can take 3-4 years to fully sell customers on the entire Procore suite, and it took 7 years for one of its biggest customers to hit $4.5m in ARR.

Key Customer Metrics

Number of organic customers contributing more than $100,000 of annual recurring revenue totaled 2,333 as of December 31, 2024, an increase of 16% year-over-year. Number of organic customers contributing more than $1,000,000 of annual recurring revenue totaled 86 as of December 31, 2024, an increase of 39% year-over-year. Added 113 net new organic customers in the fourth quarter, ending with a total of 17,088 organic customers. Achieved a gross revenue retention rate of 94% for 2024. Achieved a net revenue retention rate of 106% for 2024.

XII. Playbook: Business & Investing Lessons

Lesson 1: Solve Your Own Problem

Tooey Courtemanche didn't build Procore because market research suggested it was a good idea. He built it because he was genuinely frustrated by the chaos of managing his own construction project. This authenticity—understanding customer pain from firsthand experience—created product-market fit that no amount of user research could replicate.

Lesson 2: Crisis Can Be Opportunity

The 2008 financial crisis was genuinely existential for Procore. But it also eliminated 20+ competitors. Emerging as one of the few survivors gave them an almost unbeatable market position. Sometimes the best competitive strategy isn't brilliant marketing or superior features—it's simply surviving when others don't.

Lesson 3: Hire Salespeople, Not Industry Veterans

Surprisingly, Procore learned that hiring people directly from construction to do sales usually fails. Instead, they found success doing the opposite: hiring great salespeople and teaching them construction. The domain experts are brought in as sales engineers instead. This insight reflects the unique challenge of selling to an industry that historically distrusted technology.

Lesson 4: Patient Multi-Product Expansion

The Procore team understood better than most that a single product would only get Procore so far. Tooey and his team developed a customer-centric product organization centered on the mission of connecting everyone in construction on a global platform. The company evolved from a company with a single product (project management) serving a single market (General Contractors) in the US to an industry-wide platform with 13 different products.

But critically, Procore waited until years 14-15 to implement this multi-product strategy seriously—they let customers pull them into new products rather than pushing products onto customers.

Lesson 5: Maintain Small Features at Scale

Even at $1.2B+ ARR and hundreds of millions in R&D spend, Procore still ships 3-4 "lighthouse features" in every release—just like they did as a small startup. They didn't abandon small, focused improvements even while building massive enterprise functionality.

Lesson 6: Persistence Pays

Thirteen years to $9.6M revenue. Then exponential growth. This is not a story of overnight success—it's a story of two decades of building, surviving, learning, and eventually dominating a massive market.

XIII. Competitive Analysis & Industry Position

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE-LOW

According to McKinsey, the architecture, engineering, and construction (AEC) industry has been among the slowest to digitize and innovate. This creates both opportunity and barrier: the market is large but winning it requires deep domain expertise that takes years to develop. Procore spent 20+ years learning construction workflows—new entrants would need to replicate that knowledge.

Network effects from platform integrations create additional barriers. Procore integrates with over 500 tools. Each integration makes the platform stickier and harder to displace.

Bargaining Power of Suppliers: LOW

As a software company, Procore's primary "suppliers" are cloud infrastructure providers (AWS, Azure) and talent. Cloud infrastructure is commoditized with multiple alternatives. Talent competition is real but not unique to Procore.

Bargaining Power of Buyers: MODERATE

Construction companies can and do switch platforms, but the switching costs are meaningful—all that project data, training, integrations, and workflows need to be migrated. Procore maintains a 94% gross retention rate, demonstrating customer satisfaction and platform stickiness.

Threat of Substitutes: MODERATE

The primary substitute isn't another software platform—it's the status quo of spreadsheets, email, and paper processes. Many construction companies still operate without dedicated construction management software.

Competitive Rivalry: MODERATE-HIGH

The main Procore competitors in 2025 include Mastt, Autodesk Construction Cloud, e-Builder, Oracle Primavera, and several others. These platforms offer specialized construction project management features that address different construction roles.

Procore has a market share of about 9.08% compared to leading competitors Sage Construction and Real Estate, Autodesk Navisworks and Graphisoft.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Procore benefits from economies of scale in R&D—the cost of building features is spread across a growing customer base—and in sales/marketing through brand recognition in a specialized industry.

Network Effects: Indirect network effects exist through the partner ecosystem. As more tools integrate with Procore, the platform becomes more valuable to all users.

Switching Costs: Significant. Construction companies invest substantial time configuring projects, training employees, and integrating with other systems. Migration is painful.

Counter-Positioning: Procore's exclusive focus on construction (versus horizontal project management tools) makes it difficult for generalist competitors to match their domain depth without cannibalizing their own broader businesses.

Cornered Resource: Two decades of accumulated construction workflow knowledge and customer relationships represent a cornered resource that competitors cannot easily replicate.

Process Power: Procore's methodology for understanding customer needs—sitting in job trailers, learning from frontline workers—has become embedded in how the company develops products.

Branding: In U.S. construction, Procore has achieved significant brand recognition. "In the U.S., everyone in construction knows Procore. But when we enter a new country, we have to start from scratch."

XIV. Bull Case & Bear Case

The Bull Case

Massive Underpenetrated Market: The CEO emphasized the significant opportunity in the owner segment, which is currently only 2% penetrated. He noted that while there was strength across all stakeholders, the owner segment presents a substantial opportunity for growth, demonstrating the vast potential ahead for Procore.

The global construction technology market is projected to reach a staggering $26.7 billion by 2027, reflecting a compound annual growth rate (CAGR) of 12.4%.

AI as Accelerant: Procore's massive dataset—millions of projects, billions of data points—positions the company to deliver AI-powered insights that competitors cannot match. The construction industry's unique challenges in scheduling, cost estimation, and risk management are well-suited to AI optimization.

Strong Retention and Expansion: Customers contributing >$100K ARR grew 16% YoY, now 63% of total ARR. Customers >$1M ARR surged 39% YoY, now 17% of total ARR, indicating strong enterprise adoption.

Improving Profitability: Procore raised its full-year revenue guidance to $1.285-$1.290 billion, reflecting a 12% growth. The company also increased its non-GAAP operating margin guidance to 13-13.5%, indicating a 300-350 basis point expansion.

The Bear Case

CEO Transition Risk: The upcoming leadership change introduces execution risk. Courtemanche's relationships, domain expertise, and cultural influence have been central to Procore's success.

Growth Deceleration: Revenue growth has slowed from 30%+ to the low teens. While this is partly by choice (focusing on profitability over growth), it reflects increasing market saturation and competitive pressure.

NRR Decline: Net revenue retention rate decreased to 106% from 114% in the prior year, although management suggests NRR is less relevant due to pooled volume contracts.

Macroeconomic Sensitivity: Business is sensitive to construction industry cycles and macroeconomic conditions. Uncertain economic outlook and potential construction slowdown could negatively impact revenue and customer spending.

Competitive Intensity: Autodesk, Oracle, and numerous well-funded startups are competing aggressively for the construction software market.

XV. Key KPIs for Investors to Track

For long-term fundamental investors evaluating Procore, three metrics stand out as essential to monitor:

1. Number of Customers Contributing >$100K ARR

This metric captures Procore's success in landing and expanding enterprise accounts—the segment driving most net new revenue growth. $100k+ customers are growing 18% overall. Overall customer count is fairly flat. Growth in this cohort indicates the company's ability to move upmarket and expand wallet share with existing customers.

2. Gross Revenue Retention Rate

At 94%, this metric demonstrates platform stickiness. Any deterioration here would signal product or competitive issues. Because construction projects are long-term and switching costs are high, retention should remain elevated—significant decline would be a red flag.

3. Multi-Product Adoption (% of ARR from 4+ and 6+ products)

75% of ARR comes from customers using four or more products; 48% from those using six or more. Increasing penetration indicates successful platform strategy and creates durable competitive advantage through integration depth.

XVI. Regulatory and Accounting Considerations

Revenue Recognition: Procore's subscription model with annual contracts creates straightforward revenue recognition under ASC 606. The company recognizes revenue ratably over the contract term, with no unusual contingencies or performance obligations.

Stock-Based Compensation: Like most growth software companies, Procore has significant stock-based compensation expense. Investors should note that GAAP losses are substantially larger than non-GAAP operating metrics due to this expense.

Accumulated Deficit: Procore has accumulated deficit of $1.2 billion. While concerning from a traditional accounting perspective, this reflects the company's growth investments and is typical for SaaS companies of similar scale and trajectory.

No Material Legal/Regulatory Overhangs: Procore operates in a relatively unregulated software market. The primary regulatory exposure is standard for technology companies—data privacy, employment law, and general corporate compliance.

XVII. Conclusion: The Operating System for Construction

What makes Procore's story compelling isn't just the financial trajectory—it's the demonstration that vertical SaaS, done right, can transform even the most technology-resistant industries.

In ensuing years, Courtemanche and his leadership team built Procore into a $9.78-billion publicly traded company with more than 2 million customers in about 150 nations.

The company sits at an interesting inflection point. After two decades of building, it has achieved category leadership in the United States. The construction industry presents unique challenges, operating on remarkably thin margins of just 2-3% while dealing with high liability and complex stakeholder relationships. Procore's platform addresses these challenges in ways that generate measurable ROI for customers.

The question for investors is whether Procore can maintain its leadership position while expanding internationally, successfully integrate AI capabilities, and navigate a CEO transition—all while the construction industry continues its slow but accelerating digital transformation.

"We are in the early innings of transforming one of the largest and least digitized industries in the world," said Tooey Courtemanche.

If that's true—and the data suggests it is—then Procore's story is far from over. The carpenter's frustration that sparked a software company in 2002 has grown into a platform that processes hundreds of billions of dollars in construction volume annually. The question isn't whether construction will digitize—it's whether Procore will remain the operating system that powers that transformation.

Myth vs. Reality Box

| Consensus Narrative | Reality |

|---|---|

| "Procore is a pure growth story with no path to profitability" | The company expanded non-GAAP operating margins by 800 basis points in 2024 and generated $128M in free cash flow. Profitability path is clearer than many assume. |

| "The 2008 crisis nearly killed Procore" | True, but it also eliminated 20+ competitors, creating an unexpected competitive moat through survival. |

| "Construction technology is a crowded market" | While competitors exist, Procore's 9% market share in a $12+ trillion industry suggests significant white space remains. Most construction companies still use spreadsheets. |

| "Procore's growth is decelerating problematically" | Growth slowdown to ~12-15% is partly strategic—the company is prioritizing margin expansion while maintaining market position. NRR decline bears monitoring. |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube