Veeva Systems: The Vertical SaaS Champion

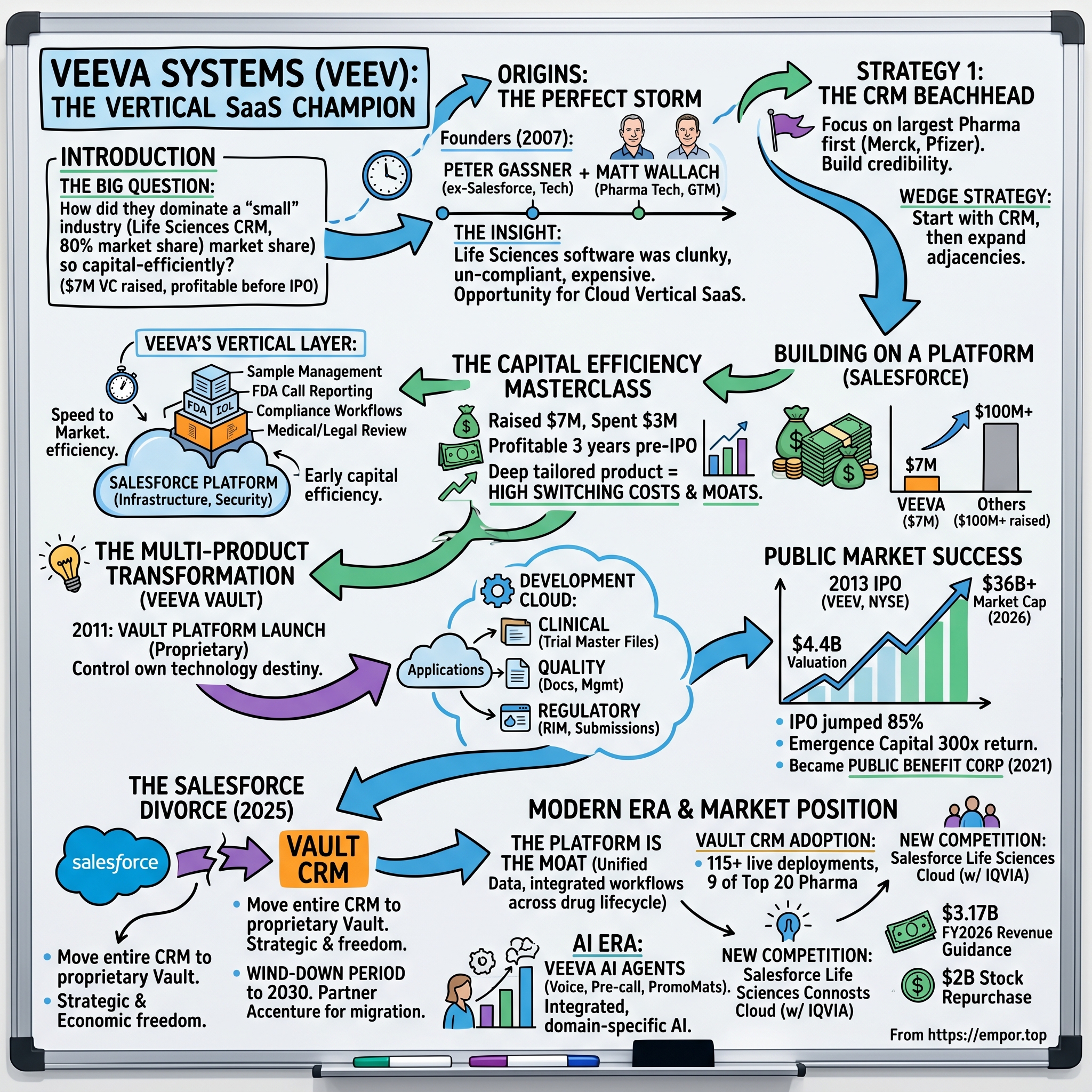

Introduction & The Big Question

Somewhere in the constellation of enterprise software companies—a universe dominated by horizontal giants like Salesforce, Oracle, and SAP—there sits a quiet anomaly. Veeva Systems, a company most people outside the pharmaceutical industry have never heard of, commands a market capitalization north of $36 billion, generates nearly $3.2 billion in annual revenue, and holds roughly 80 percent market share in life sciences customer relationship management software. It serves over 1,500 customers across 150 countries, including virtually every major pharmaceutical and biotech company on the planet.

But the truly remarkable part of the Veeva story is not its current dominance. It is how it got there. Founded in 2007 by two men who had never met before, funded with just $7 million in venture capital—of which only $3 million was actually spent—and profitable for three consecutive years before its 2013 IPO, Veeva may be the most capital-efficient enterprise software company ever built. In an industry where burning through hundreds of millions before going public is considered normal, Veeva's frugality borders on the subversive.

The company went public at a $4.4 billion valuation, and the stock jumped 85 percent on its first day of trading. Its sole venture investor, Emergence Capital Partners, earned a 300-fold return on a $4 million check. That single investment returned Emergence's entire second fund more than seven times over. Numbers like these do not happen in enterprise software. They barely happen anywhere.

The central question of this story is deceptively simple: How did two former enterprise software executives—one from Salesforce, one from the pharmaceutical technology world—build a company this dominant, this profitable, and this durable by focusing on a single industry that most venture capitalists considered too small to bother with? The answer involves a series of counterintuitive bets: building on someone else's platform and then leaving it, refusing to raise money when capital was cheap, choosing depth over breadth, and treating profitability not as a distant aspiration but as a founding principle. This is the story of vertical SaaS done right—and the lessons it holds for anyone trying to build an enduring technology company.

Origins: The Perfect Storm

Peter Gassner grew up in Portland, Oregon, the son of Swiss immigrants. His father owned a machine shop—the kind of small, hands-on business where you learned that margins mattered and waste was the enemy. Peter was the third of six children, and his path to technology was neither obvious nor linear. A high school math teacher suggested he try a computer science class, and something clicked. But Gassner was restless. He kept starting and stopping college, taking extended breaks to surf in Hawaii, backpack through Australia, and work as a trekking guide in Thailand. This was not the biography of a future enterprise software CEO. It was the biography of someone searching for the right problem to solve.

Eventually, Gassner found his way into the software industry, working at PeopleSoft during its formative years and developing deep expertise in building large-scale enterprise applications. But the transformative experience came at Salesforce, where he spent four years in the mid-2000s as a senior technology leader. At Salesforce, Gassner witnessed firsthand the power of cloud computing to displace entrenched on-premise software vendors. He saw how a well-architected platform could scale across thousands of customers with minimal friction. And he noticed something that most people at Salesforce were not paying attention to: the horizontal platform was leaving enormous value on the table by treating all industries the same.

Life sciences, in particular, was a mess. Pharmaceutical companies were spending billions on software systems designed for generic sales teams, then layering on expensive customizations to handle the industry's unique requirements—regulatory compliance, sample tracking, call reporting to the FDA, complex approval workflows for promotional materials. The result was a patchwork of clunky, on-premise solutions that cost a fortune to maintain and did a poor job of serving the industry's actual needs. Gassner saw an opportunity: take the power of cloud computing and build something purpose-built for life sciences. Not a horizontal platform with a pharma skin. A genuine vertical solution.

Three thousand miles away, Matt Wallach was seeing the same opportunity from a completely different angle. Wallach was a Harvard Business School graduate who had spent his career in pharmaceutical technology—first as a management consultant, then as a product manager at several technology firms building software for pharma sales representatives and clinical research associates. He understood the pharmaceutical industry's pain points with an intimacy that few technologists could match. He knew that pharma sales reps needed software designed for their specific workflows—tracking physician interactions, managing drug samples under DEA regulations, navigating complex compliance requirements that generic CRM tools simply could not handle.

The two men had never met. Gassner was in Silicon Valley. Wallach was in Philadelphia. But in January 2007, through mutual connections in the enterprise software world, they found each other—and discovered they shared an almost identical vision: build a cloud-native software company focused exclusively on life sciences. They founded the company under the decidedly unglamorous name "Verticals onDemand, Inc." and divided responsibilities along natural lines. Gassner would design the technology platform and products from California. Wallach would build customer relationships and drive go-to-market strategy from the East Coast, leveraging his deep connections with the big pharmaceutical companies.

The strategic choice to start with CRM was deliberate. Customer relationship management was the beachhead—the most visible, most widely used software category in pharmaceutical commercial operations, and the one where the pain of using generic tools was most acute. Every major pharma company had sales reps in the field visiting physicians, and every one of them was struggling with software that did not understand the fundamental realities of pharmaceutical selling. By solving CRM first, and solving it definitively, Gassner and Wallach could establish credibility with the largest pharmaceutical companies and then expand into adjacent categories. It was a wedge strategy, and it was brilliant.

The founders made another critical early decision: they would target the largest pharmaceutical companies first, not small biotech startups. This was counterintuitive. Most enterprise software startups begin with small customers who are easier to close and more willing to take a risk on unproven technology. But Gassner and Wallach understood that in life sciences, the big companies set the standard. If Pfizer or Merck adopted your platform, the rest of the industry would follow. Landing a top-20 pharma company was not just a revenue win—it was a market signal that could accelerate adoption across the entire industry. The bet paid off spectacularly. Within five years of launch, Veeva CRM had captured over 80 percent of the pharmaceutical CRM market, a dominance that persists to this day.

The Salesforce Platform Play

When Gassner and Wallach sat down to build Veeva's first product, they faced a classic startup dilemma: build the entire technology stack from scratch, which would take years and millions of dollars, or build on top of an existing platform and get to market fast. They chose the latter, and the platform they chose was Salesforce.

This was not an obvious decision at the time. Building on Salesforce meant inheriting its security infrastructure, its scalability, and its ecosystem of developers and administrators—all significant advantages for a startup with limited capital. But it also meant dependency. Veeva would be, in a very real sense, a tenant in Salesforce's house. If Salesforce changed its pricing, its APIs, or its strategic direction, Veeva would be affected. For most startups, this kind of platform risk would be disqualifying. For Gassner, who had spent four years inside Salesforce and understood both its strengths and its limitations, it was a calculated bet. The speed-to-market advantage was worth the dependency risk—at least for now.

The genius of Veeva's approach was in what it built on top of the Salesforce foundation. While the underlying infrastructure handled the plumbing—database management, user authentication, basic CRM functionality—Veeva layered on deeply industry-specific features that Salesforce would never build. Sample management for tracking controlled pharmaceutical samples under DEA regulations. Call reporting that captured the specific data points the FDA required. Compliance workflows that ensured promotional materials were reviewed and approved according to pharmaceutical industry standards. Medical, legal, and regulatory review processes built directly into the software. These were not cosmetic customizations. They were fundamental capabilities that transformed a generic CRM into a purpose-built pharmaceutical operating system.

The early customer wins validated the approach. Pharmaceutical companies that had been spending millions on on-premise CRM implementations—with armies of consultants, lengthy deployment timelines, and painful upgrade cycles—could now switch to Veeva and get a cloud-based solution that actually understood their business. The value proposition was compelling: lower total cost of ownership, faster deployment, automatic updates, and functionality that was designed for their industry from the ground up rather than bolted on as an afterthought.

In June 2008, Veeva raised its Series A round: $4 million from Emergence Capital Partners. It was the only venture round the company would ever need. Emergence, a San Francisco-based firm that had made its name backing enterprise SaaS companies, saw in Veeva something rare—a company with genuine product-market fit, a massive addressable market hiding inside a seemingly narrow vertical, and founders who were obsessed with capital efficiency. The partnership between Veeva and Emergence would prove to be one of the most lucrative in venture capital history.

In 2014, Veeva and Salesforce extended their partnership through 2025, with Veeva becoming Salesforce's preferred worldwide partner for pharmaceutical and biotech CRM. The arrangement was mutually beneficial: Salesforce got a partner that was driving significant platform revenue in a lucrative vertical, and Veeva got the stability of a long-term platform commitment. For nearly a decade, the relationship worked. But even as Veeva was deepening its Salesforce partnership, Gassner was quietly building something else—a proprietary platform that would eventually allow Veeva to stand on its own.

The Capital Efficiency Masterclass

The venture capital industry runs on a simple narrative: raise as much money as you can, grow as fast as possible, worry about profitability later. In the mid-2000s and early 2010s, this narrative was reaching its zenith. Enterprise SaaS companies were raising tens of millions, sometimes hundreds of millions, before generating meaningful revenue. The logic was that market share mattered more than margins, and the winner in each category would be the company that outspent its competitors.

Gassner rejected this logic entirely. When he and Wallach went out to raise their initial funding, most venture capitalists told them the same thing: the market was too small. Life sciences was one industry. The total addressable market for pharmaceutical CRM was a fraction of the broader CRM market that Salesforce was pursuing. Why would you limit yourself to one vertical when you could build a horizontal platform and serve everyone? It was crazy.

Gassner's response was that the VCs had the analysis exactly backward. By focusing on one industry, Veeva could build products that were so deeply tailored to customer needs that switching costs would be enormous. Pharmaceutical companies would not just prefer Veeva—they would depend on it. The industry's complex regulatory requirements meant that any CRM solution needed to be validated, documented, and integrated into compliance workflows. Once a pharmaceutical company was running on Veeva, the cost of switching to a generic alternative was not just financial—it was operational and regulatory. This was not a feature. This was a moat.

The capital efficiency numbers remain staggering by any measure. Veeva raised $7 million total before its IPO. It used only $3 million of that. The company was profitable for three consecutive years before going public—a claim that almost no enterprise SaaS company of that era could make. For context, consider that Salesforce itself had raised over $100 million before its 2004 IPO. Workday raised $185 million. ServiceNow raised $83 million. Veeva raised $7 million and did not even spend all of it.

How was this possible? Three factors converged. First, building on the Salesforce platform dramatically reduced Veeva's infrastructure costs. The company did not need to build and maintain its own data centers, security infrastructure, or basic CRM functionality. Second, the decision to target large pharmaceutical companies meant that Veeva's average contract value was high from the start. Each customer represented significant recurring revenue, which meant the company could grow efficiently without needing thousands of small customers. Third, and perhaps most importantly, Gassner and Wallach were philosophically committed to building a profitable business from day one. This was not a company that viewed profitability as something to figure out later. It was a company that viewed profitability as a competitive advantage.

The decision not to raise more money was itself a strategic choice. In Silicon Valley, raising a large funding round is often treated as a milestone—a signal of success and ambition. Gassner saw it differently. Every dollar of venture capital came with expectations: expectations for growth rates, expectations for exit timelines, expectations that might not align with building a durable, long-term business. By staying capital-efficient, Veeva retained control over its own destiny. The founders could make decisions based on what was right for customers and for the long-term health of the business, not based on what would satisfy venture investors looking for a quick return.

This discipline would prove prescient. When Veeva went public in 2013, the company was not just growing fast—it was growing profitably. That combination of growth and profitability gave the stock an unusual profile in the public markets: a high-growth SaaS company that did not require constant capital infusions to sustain its trajectory. Investors noticed. The IPO was one of the most successful enterprise software debuts of the decade.

The Multi-Product Transformation

In 2010, Peter Gassner faced a decision that would define Veeva's next decade. The company's CRM product had conquered the pharmaceutical sales market with remarkable speed. The temptation was to stay focused on CRM—to deepen its capabilities, expand into adjacent geographies, and extract maximum value from a dominant market position. Some members of the team argued for exactly this approach. CRM was working. Why complicate things?

But Gassner saw a larger opportunity. Pharmaceutical companies did not just need better CRM software. They needed better software across their entire operation—from clinical trials to regulatory submissions to quality management to promotional content review. Each of these functions was served by aging, on-premise systems that were poorly integrated, expensive to maintain, and slow to evolve. If Veeva could build a platform that addressed the full lifecycle of pharmaceutical operations, the company's addressable market would expand by an order of magnitude.

The first step was Veeva Vault, introduced in 2011 as a cloud-based content management system for life sciences. This was not just another product launch. It was a strategic declaration: Veeva was going to build its own proprietary platform, separate from Salesforce, capable of hosting an entire suite of applications. Vault was designed from the ground up for the stringent requirements of regulated industries—document control, audit trails, electronic signatures, version management, and the kind of validated workflows that pharmaceutical regulators demanded. Think of it as a purpose-built operating system for the mountains of documentation that drug development generates.

The Vault platform became the foundation for what Veeva would eventually call its Development Cloud—a suite of applications spanning the entire drug development lifecycle. Vault Clinical handled trial master files, electronic data capture, and clinical trial management. Vault Quality managed quality documents, deviations, corrective actions, and change control processes. Vault RIM, introduced in 2015-2016, provided a unified regulatory information management platform for tracking drug registrations and submissions across global markets. Each of these applications addressed a specific pain point that pharmaceutical companies had been solving with disconnected, on-premise systems from different vendors.

The adoption was swift and deep. By 2023, eighteen of the top twenty pharmaceutical companies were using Veeva's electronic trial master file system. Over 450 companies had adopted Vault for clinical operations. More than 300 used Vault Quality applications. Over 200 relied on Vault RIM for regulatory management. These were not casual adoptions. Each deployment represented a deep integration into the customer's operational workflows—the kind of entrenchment that makes switching costs formidable and customer relationships durable.

The multi-product strategy also created powerful cross-selling dynamics. A pharmaceutical company that started with Veeva CRM for its commercial operations could expand into Vault for content management, then add clinical and regulatory applications as the relationship deepened. Each additional product increased the customer's dependency on the Veeva ecosystem and made the economic relationship more valuable for both sides. This is the classic land-and-expand motion that enterprise software investors love to see, but Veeva executed it with unusual discipline—expanding into categories where it had genuine domain expertise and could deliver differentiated value, rather than chasing adjacencies for the sake of revenue growth.

The decision to build Vault on a proprietary platform rather than extending the Salesforce foundation was perhaps the most consequential architectural choice in Veeva's history. At the time, it seemed like an unnecessary risk. Why build a new platform when you already had a perfectly good one from Salesforce? But Gassner was thinking several moves ahead. A proprietary platform would give Veeva complete control over its technology stack—performance, security, release cycles, and long-term roadmap. It would eliminate the dependency on Salesforce that had enabled Veeva's initial growth but could eventually constrain its evolution. And it would position Veeva to do something that most platform partners never attempt: walk away from the platform entirely.

The IPO and Public Market Success

On October 16, 2013, Veeva Systems debuted on the New York Stock Exchange under the ticker VEEV. The IPO had been one of the most closely watched enterprise software offerings of the year, and the market's reception exceeded even the most optimistic expectations.

The pricing journey told its own story. Veeva initially set a range of $12 to $14 per share, reflecting the caution that accompanies any enterprise software IPO in a market still recovering from the financial crisis. As demand built during the roadshow, the range was raised to $16 to $18. Then, in a final revision that signaled overwhelming institutional interest, the offering was priced at $20 per share. The stock opened at $29.71 and closed the day at $37.16—an 85.8 percent first-day gain that valued the company at $4.4 billion.

For Emergence Capital Partners, the moment was transformative. The firm's $4 million Series A investment was now worth over $1.2 billion. Emergence held 31.6 percent of the company after the offering, a stake valued at $1.4 billion—roughly seven times the entire size of the $200 million fund that had backed Veeva. In venture capital, a fund-returning investment is considered exceptional. Emergence's Veeva bet returned the fund seven times over. It remains one of the most successful venture investments in the history of enterprise software.

Veeva raised approximately $217 million in the offering, capital that the company hardly needed given its already-profitable operations. The IPO was less about raising money and more about providing liquidity for early investors and establishing the public market currency that would support Veeva's continued growth through acquisitions and talent recruitment.

What followed in the public markets was a decade-long compounding story. From its IPO valuation of $4.4 billion, Veeva's market capitalization grew to approximately $36 billion by early 2026—representing roughly a nine-fold increase. The stock reached an all-time high of $341 per share in August 2021, during the pandemic-era technology boom, before pulling back as the broader software sector de-rated. As of early 2026, shares trade around $221, reflecting both the company's strong fundamentals and investor concerns about intensifying competition and the complexity of its ongoing platform transition.

Throughout its time as a public company, Veeva demonstrated the kind of long-term thinking that is rare in an era of quarterly earnings obsession. Revenue grew from roughly $210 million in fiscal 2014 to $2.75 billion in fiscal 2025—a thirteen-fold increase over eleven years. The company maintained operating margins that consistently exceeded those of its enterprise software peers, a testament to the capital-efficient DNA that Gassner had embedded from the beginning.

In February 2021, Veeva made corporate history by becoming the first publicly traded company to convert to a Public Benefit Corporation. The conversion, which required shareholder approval, passed with 99 percent of voting shares in favor. As a PBC, Veeva's board and management have a legal obligation to balance the interests of shareholders with those of other stakeholders—customers, employees, and the broader community. It was a philosophical statement about the kind of company Gassner wanted to build: not one optimized purely for short-term shareholder returns, but one designed to create durable value for the entire life sciences ecosystem. In January 2026, the board authorized a $2 billion stock repurchase program, underscoring management's confidence in the company's long-term value.

The Salesforce Divorce

In December 2022, Veeva made an announcement that sent ripples through the enterprise software world: it would not renew its partnership with Salesforce when the agreement expired in September 2025. Instead, Veeva would migrate its entire CRM customer base to Vault CRM, its proprietary platform. After fifteen years of building on Salesforce's foundation, Veeva was leaving home.

The decision had been years in the making. Since the launch of Vault in 2011, Gassner had been quietly building the proprietary infrastructure that would make this moment possible. Vault CRM was not a hastily assembled replacement—it was the culmination of more than a decade of platform development, refined through hundreds of Vault deployments across clinical, regulatory, and quality applications. The technology was ready. The question was whether the customers would follow.

The motivations for the split were both strategic and economic. On the strategic side, running CRM on Salesforce's platform meant that Veeva was constrained by Salesforce's release cycles, API limitations, and architectural decisions. Every feature Veeva wanted to build had to work within the boundaries of what Salesforce's platform allowed. By moving to Vault, Veeva would have complete control over its technology stack—the ability to optimize performance, innovate on its own timeline, and integrate CRM seamlessly with its rapidly growing suite of Vault applications. For customers who were already using Vault for clinical or regulatory work, running CRM on the same platform meant a unified experience and simplified data management.

On the economic side, the math was compelling. Building on Salesforce meant paying platform fees that consumed a meaningful portion of Veeva's CRM revenue. Moving to a proprietary platform would eliminate these fees and expand gross margins over time. For a company generating nearly $3.2 billion in annual revenue, even a modest margin improvement represented significant value.

The transition was designed with characteristic Veeva prudence. Customers would have a five-year wind-down period, extending until September 2030, to migrate from the Salesforce-based CRM to Vault CRM. Veeva would handle the migration of standard data, minimizing disruption for most customers. Companies with extensive custom objects and integrations would need additional planning, and Veeva partnered with Accenture to provide migration support.

The early results have been encouraging. By Q3 of fiscal year 2026, Veeva reported over 115 live Vault CRM deployments, with 23 new customers added in the quarter alone. Nine of the top twenty pharmaceutical companies had committed to Vault CRM, including landmark wins with Merck, Roche, and Novo Nordisk's international operations. The migration was not just proceeding on schedule—it was accelerating.

For Salesforce, the loss was more than financial. Veeva had been a showcase partner—proof that the Salesforce platform could support mission-critical, industry-specific applications at scale. Its departure raised uncomfortable questions about whether other successful platform partners might eventually follow the same path, building on Salesforce to gain initial traction and then migrating to proprietary infrastructure once they achieved sufficient scale and customer lock-in. The risk of "platform graduation"—partners outgrowing the platform—suddenly felt very real.

Salesforce's response was direct: it partnered with IQVIA, Veeva's most significant competitor, to build Salesforce Life Sciences Cloud. Launched in September 2025, the offering combined IQVIA's pharmaceutical domain expertise with Salesforce's AI capabilities and platform infrastructure. By December 2025, Salesforce had signed more than 40 life sciences customers, including major names like Takeda, Pfizer, and Boehringer Ingelheim. The battle for life sciences CRM, long a one-company market, had become a genuine competitive contest.

But the scoreboard in early 2026 favored Veeva. Nine of the top twenty pharma companies had committed to Vault CRM versus three choosing Salesforce Life Sciences Cloud. Veeva's decade-long head start in understanding pharmaceutical workflows, its deep integration across commercial and R&D applications, and the switching costs embedded in its installed base created formidable advantages. The divorce from Salesforce was proving to be not an act of self-destruction but an act of strategic liberation.

Modern Era & Market Position

Veeva Systems in early 2026 is a company operating at a scale and breadth that would have been unimaginable at its founding. With over 1,500 customers, annual revenues approaching $3.2 billion, and more than 7,000 employees operating across 150 countries, the company has evolved from a pharmaceutical CRM startup into the dominant software platform for the global life sciences industry.

The financial trajectory tells a story of consistent, disciplined growth. In fiscal year 2025, total revenues reached $2.75 billion, up 16 percent year-over-year. Subscription services revenue—the recurring, high-margin core of the business—grew 20 percent to $2.28 billion. The most recent quarter, Q3 of fiscal year 2026, showed continued momentum: total revenues of $811 million, up 16 percent, with subscription services of $682 million, up 17 percent. The company exceeded analyst expectations on both revenue and earnings, reporting non-GAAP earnings per share of $2.04 against a consensus estimate of $1.95. For the full fiscal year 2026, management raised guidance to approximately $3.17 billion in revenue.

The AI era presents both opportunity and validation for Veeva's platform strategy. In October 2025, the company announced Veeva AI Agents—agentic AI capabilities embedded directly into the Vault platform. The first agents became available in December 2025 for Vault CRM and PromoMats, including a Voice Agent that helps sales reps capture call notes through natural language, a Pre-call Agent that prepares personalized briefings before physician meetings, a Free Text Agent for flexible data entry, and content review agents for promotional materials compliance. Additional agents for clinical, regulatory, safety, quality, and medical applications are planned throughout 2026.

What makes Veeva's AI approach distinctive is its integration depth. Because Veeva controls the entire platform and has deep domain expertise in life sciences workflows, its AI agents can be purpose-built for specific pharmaceutical use cases rather than offering generic AI capabilities layered on top. The agents understand Veeva application context, have application-specific prompts and safety guardrails, and have direct access to the relevant data and documents within the Vault ecosystem. The technology runs on large language models from Anthropic and Amazon, hosted on Amazon Bedrock—a pragmatic choice that leverages best-in-class AI infrastructure while allowing Veeva to focus on the domain-specific application layer.

The competitive landscape has grown more complex. IQVIA, a data analytics and technology company with deep roots in pharmaceutical services, continues to market its OCE CRM platform through 2029 while collaborating with Salesforce on the Life Sciences Cloud. Salesforce has rebranded its offering as Agentforce Life Sciences, signaling an aggressive push into AI-powered pharmaceutical CRM. The three-way competition between Veeva, Salesforce, and IQVIA represents the first genuine threat to Veeva's CRM dominance in over a decade.

Yet Veeva's competitive position remains formidable for reasons that go beyond CRM. The company's Vault platform now spans the entire drug development lifecycle—from clinical trial management and regulatory submissions to quality management and commercial operations. No competitor offers this breadth of integrated applications purpose-built for life sciences. A pharmaceutical company running on the full Veeva suite benefits from unified data, consistent workflows, and simplified vendor management in a way that assembling point solutions from multiple vendors simply cannot match. This integrated platform strategy is Veeva's deepest competitive moat.

The Veeva Basics initiative, aimed at emerging biotechs, represents a smart play for the next generation of customers. Over 100 biotech companies across 60 organizations have adopted Veeva Basics, with plans to expand the offering to include LIMS and PromoMats in early 2026. By capturing small biotechs early and growing with them as they scale, Veeva is planting seeds for future enterprise relationships—the same wedge strategy that worked so effectively with large pharma a decade ago, now applied to the long tail of the industry.

Playbook: Lessons for Founders & Investors

The Veeva story offers a set of lessons that challenge some of the most deeply held assumptions in technology investing.

The first is the vertical SaaS thesis, validated at a scale that even its proponents did not expect. When Gassner and Wallach founded Veeva, the conventional wisdom in venture capital was that vertical software markets were too small to produce large outcomes. The Total Addressable Market slide in a pitch deck was supposed to show billions of dollars of opportunity, and a company focused on CRM for pharmaceutical sales reps did not clear that bar. What the skeptics missed was the expansion potential. By starting with CRM and expanding into content management, clinical operations, regulatory affairs, and quality management, Veeva grew its addressable market from hundreds of millions to tens of billions without ever leaving the life sciences industry. The lesson is that TAM is not static—it is a function of execution, trust, and the ability to solve adjacent problems for customers who already depend on you.

The second lesson is that capital efficiency is a strategic weapon, not just a financial constraint. Veeva's decision to raise only $7 million was not born of necessity—it was born of conviction. Gassner believed that building a profitable business from day one would create better products, better customer relationships, and better long-term outcomes than the grow-at-all-costs playbook that dominated Silicon Valley. He was right. The discipline of profitability forced Veeva to prioritize features that customers would actually pay for, to build a sales organization that could close enterprise deals efficiently, and to make product decisions based on customer value rather than investor narratives. In an era when dozens of unprofitable SaaS companies have seen their stock prices collapse as interest rates rose and growth decelerated, Veeva's capital efficiency looks less like an anomaly and more like a template.

The third lesson is about platform partnerships—when to leverage them and when to leave. Veeva's Salesforce relationship demonstrates both the power and the peril of building on someone else's platform. The partnership gave Veeva speed to market, credibility, and access to a proven technology infrastructure at a fraction of what it would have cost to build from scratch. But Gassner was never under any illusion that the partnership would last forever. From the moment Vault launched in 2011, Veeva was building the infrastructure for independence. The ten-year gap between Vault's launch and the Salesforce departure announcement gave Veeva time to prove the technology, build customer confidence, and create a migration path that minimized disruption. The lesson for founders: platform partnerships are vehicles, not destinations. Use them to accelerate early growth, but invest in your own infrastructure before you need it.

The fourth lesson is the power of going against the grain. Veeva was contrarian at every turn. It focused on one industry when VCs wanted horizontal platforms. It prioritized profitability when growth at all costs was gospel. It targeted the largest, most demanding customers first when conventional wisdom said to start small. It built a proprietary platform while everyone else was building on Salesforce. It became a Public Benefit Corporation when shareholder primacy was the dominant ideology. Each of these decisions was met with skepticism at the time. Each proved to be correct in hindsight. There is a pattern here: the most durable competitive advantages often come from doing things that the consensus considers irrational.

The fifth lesson is that industry expertise is a moat. Veeva's understanding of pharmaceutical regulations, clinical trial processes, and commercial operations is not something a horizontal software company can replicate by hiring a few industry consultants. It is embedded in the product architecture, the compliance workflows, the data models, and the validation procedures that make Veeva's software suitable for use in a regulated environment. This knowledge accumulates over time and creates a compounding advantage that becomes more difficult to overcome with each passing year.

Analysis & Investment Case

The investment case for Veeva rests on a few key dynamics that investors should understand clearly.

On the bull side, Veeva's competitive position is anchored by what Hamilton Helmer would call "switching costs" and "process power." Once a pharmaceutical company has validated and deployed Veeva's software across its commercial and development operations, the cost of ripping it out and replacing it with an alternative is enormous—not just in licensing fees, but in revalidation, retraining, compliance documentation, and operational risk. This is not ordinary customer stickiness. In a regulated industry where software changes require formal validation protocols and regulatory documentation, switching costs approach the level of structural lock-in. Veeva also benefits from what Helmer calls "cornered resource"—its deep domain expertise in life sciences workflows is a scarce asset that competitors cannot easily replicate.

From a Porter's Five Forces perspective, the picture is nuanced. The threat of new entrants is moderate: Salesforce Life Sciences Cloud is a genuine competitive entry backed by significant resources, but the regulatory expertise and installed base required to compete effectively create meaningful barriers. The bargaining power of buyers is constrained by switching costs—large pharma companies cannot easily move to alternatives without significant disruption. Supplier power is limited given Veeva's shift to a proprietary platform. The threat of substitutes is low in the near term, as no alternative platform offers comparable breadth and depth for life sciences. Competitive rivalry, however, is intensifying. The Salesforce-IQVIA partnership represents the most serious competitive challenge Veeva has faced in its history.

The bear case centers on three concerns. First, the Vault CRM migration is a complex, multi-year undertaking that carries execution risk. While early results are encouraging, migrating hundreds of enterprise customers from one platform to another is inherently fraught with potential delays, cost overruns, and customer dissatisfaction. Second, Salesforce's entry into life sciences CRM with backing from IQVIA introduces genuine competition for the first time. While Veeva holds the early advantage, Salesforce's resources, AI capabilities, and existing enterprise relationships should not be underestimated. Third, Veeva trades at a premium valuation—roughly 43 times trailing earnings—that leaves limited room for error. Any stumble in the migration, any loss of major customers to Salesforce, or any deceleration in growth could trigger a meaningful multiple compression.

The bull case is straightforward: Veeva is the dominant platform in a large, growing, and deeply regulated market with structural switching costs that protect its installed base. The Vault platform migration, if executed successfully, will expand margins and deepen competitive moats by giving Veeva full control over its technology stack. The AI opportunity is substantial, and Veeva's integrated platform position gives it a natural advantage in delivering AI capabilities that are deeply embedded in pharmaceutical workflows rather than bolted on as generic features. The Veeva Basics initiative opens the emerging biotech market, planting the seeds for the next generation of enterprise customers.

For investors tracking this story, two KPIs matter most. The first is subscription revenue growth, which reflects the underlying health of customer adoption and expansion—this metric captures both new customer wins and the deepening of existing relationships across the Vault platform. The second is Vault CRM migration progress, measured by the number of live deployments and committed top-20 pharma customers—this metric directly tracks the most consequential strategic bet the company has made since its founding.

Epilogue & Reflection

In the early days of Veeva, Peter Gassner used to say that the company was thinking ninety days ahead—just far enough to land the next customer and make the next payroll. Two decades later, Gassner talks about building a hundred-year company. The distance between those two time horizons tells the story of what Veeva has become.

The most counterintuitive insight from the Veeva story may be this: the company that everyone said was too narrow, too focused, and too small turned out to be none of those things. By going deep into one industry rather than wide across many, Veeva discovered an addressable market far larger than anyone anticipated and built competitive advantages far more durable than horizontal breadth could have provided. The pharmaceutical industry's complexity, which most technology companies viewed as a deterrent, was precisely what made it so valuable once mastered.

The Salesforce divorce adds a final, clarifying chapter. Veeva spent its first fifteen years building on someone else's platform—a pragmatic choice that enabled rapid growth. Now it is betting its future on a platform it owns entirely. The transition carries real risk, but it also carries the potential for a fundamentally different kind of company: one that controls its destiny completely, from the database layer to the AI agents that sit on top. If the migration succeeds—and the early evidence suggests it will—Veeva will emerge as something rare in enterprise software: a vertically integrated platform company with dominant market share, expanding margins, and no platform dependency.

In an industry obsessed with disruption, Veeva's story is really about something more old-fashioned: discipline. The discipline to focus when everyone urged breadth. The discipline to profit when everyone celebrated losses. The discipline to build for decades when everyone optimized for quarters. These are not glamorous qualities. They do not generate breathless headlines or viral Twitter threads. But they are the qualities that build companies that last—and in the end, that is the only kind of company worth building.

Recent News

In Q3 of fiscal year 2026, ended October 31, 2025, Veeva reported total revenues of $811.2 million, exceeding analyst expectations. Subscription services revenue grew 17 percent year-over-year to $682.5 million. Management raised full-year fiscal 2026 guidance to approximately $3.17 billion in total revenue.

The Vault CRM migration continued to accelerate, with over 115 live deployments and nine of the top twenty pharmaceutical companies committed to the platform. Notable customer wins included Novo Nordisk's international operations in January 2026 and Roche in November 2025.

Veeva AI Agents launched in December 2025 for Vault CRM and PromoMats, with additional agents planned across clinical, regulatory, safety, quality, and medical applications throughout 2026. The AI agents use large language models from Anthropic and Amazon, hosted on Amazon Bedrock.

Salesforce Life Sciences Cloud, developed in partnership with IQVIA, became generally available in September 2025 and had signed over 40 customers by December 2025, including Takeda, Pfizer, and Boehringer Ingelheim.

In January 2026, Veeva's board authorized a $2 billion stock repurchase program. The company's next earnings report is expected on March 4, 2026.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube