Oracle: The Database Empire That Conquered Enterprise Computing

I. Introduction & Cold Open

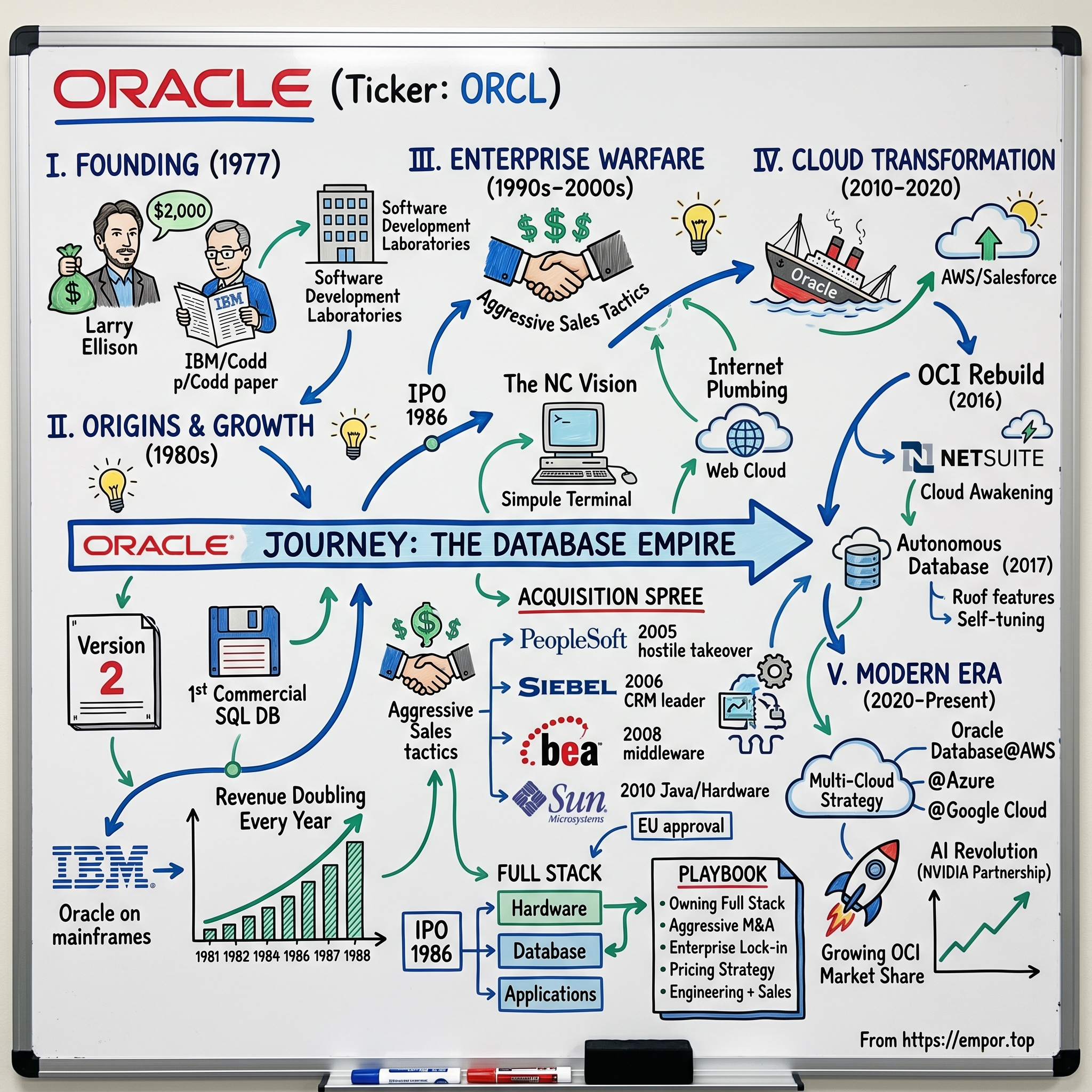

Picture this: It's 1977, and a college dropout with $1,200 to his name is reading a technical paper from IBM researcher Edgar F. Codd about something called "relational databases." The paper is dense, academic, revolutionary—and IBM has no plans to commercialize it anytime soon. That dropout, Larry Ellison, sees what IBM doesn't: the future of how every corporation on Earth will store and manage information. He names his company after a CIA project he'd worked on—"Oracle"—and sets out to beat IBM at its own game.

Fast forward to today: Oracle is worth over $520 billion, making it one of the most valuable software companies in history. Every time you check your bank balance, book a flight, or order from a major retailer, there's a good chance an Oracle database is humming away in the background, processing your transaction with the reliability of a Swiss watch. The company that started with three engineers and a borrowed idea has become so embedded in the world's digital infrastructure that removing it would be like trying to extract rebar from concrete—theoretically possible, but practically catastrophic.

But Oracle isn't just a database company anymore. It's a sprawling empire that spans applications, hardware, and cloud computing. It's the company that perfected the art of the hostile takeover in Silicon Valley, swallowing competitors like PeopleSoft and Sun Microsystems. It's the last major enterprise software company still controlled by its founder, with Larry Ellison—now worth over $200 billion—still calling the shots as Executive Chairman and CTO at age 80.

This is the story of how a relentless founder built a company that enterprise IT departments simultaneously depend on and complain about. It's about technical brilliance married to aggressive sales tactics, about being late to the cloud revolution but refusing to surrender, about building switching costs so high that customers joke about being held hostage—while renewing their contracts year after year.

The journey from that CIA project to today's multi-cloud strategy reveals fundamental truths about enterprise software: why boring beats sexy, why lock-in creates value, and why in the world of mission-critical systems, nobody ever got fired for buying Oracle. Even when they wanted to.

II. Origins: Larry Ellison & The Founding Story (1944-1977)

The man who would build one of technology's great empires began life as Lawrence Joseph Ellison in the Bronx, born to a 19-year-old unwed mother in August 1944. When pneumonia nearly killed him at nine months old, his mother gave him to her aunt and uncle in Chicago—Lillian and Louis Ellison—who raised him as their own. Louis, a Russian-Jewish immigrant who'd lost his fortune in the Great Depression, worked as a government employee and made clear his adopted son would never amount to much. "You'll never be successful," he'd tell young Larry. "You don't have it in you."

Larry proved him wrong by dropping out—twice. First from the University of Illinois after his sophomore year when his adoptive mother died, then from the University of Chicago after just one term. But in that single Chicago term, he discovered something that would shape his destiny: computer programming. It was 1964, and while his classmates saw computers as glorified calculators, Ellison saw liberation—a world where logic ruled and code was power.

He packed his Ford Thunderbird and drove to California in 1966, age 22, with a few hundred dollars and no plan beyond escaping the Midwest. Silicon Valley wasn't Silicon Valley yet—it was orange groves and defense contractors. Ellison bounced between programming jobs: Wells Fargo, Amdahl Corporation, and finally Ampex, where fate intervened in the form of a classified project. At Ampex, Ellison worked on a database project for the Central Intelligence Agency—code-named "Oracle". He managed to secure a $50,000 contract from the CIA to build a database program that was meant to be able to answer any question about anything. But the real revelation came when his colleague Ed Oates handed him an IBM Research Journal containing Edgar F. Codd's 1970 paper, "A Relational Model of Data for Large Shared Data Banks."

To understand what Ellison saw that others didn't, you need to understand the database world of 1977. Data was stored in hierarchical or network databases—rigid, inflexible structures that required programmers to navigate complex paths to retrieve information. Codd proposed representing data as simple tables with rows and columns, where each column represents a domain and each row contains related values. It was elegant, powerful, and IBM—Codd's employer—saw it as an intellectual curiosity that might cannibalize their existing products.

IBM was initially reluctant to implement Codd's relational database model primarily to protect their revenue from their existing hierarchical database product called IMS Database. IBM viewed Codd's concept as merely an "intellectual curiosity" that could potentially undermine their existing products. While IBM dithered, Ellison acted.

In June 1977, Ellison co-founded Software Development Laboratories with Bob Miner and Ed Oates with just $2,000 in capital—$1,200 was Ellison's contribution. The division of labor was brutally honest: The three founders decided that Ellison was the worst programmer so he became the salesman. Miner, the technical genius, would build the product. Oates would handle development. Ellison would sell the future.

They kept the CIA project codename for their database: Oracle. The company received permission to use the name, perhaps the first of many aggressive moves that would define Oracle's culture. While IBM kept their System R database secret, treating it like the Manhattan Project, Ellison's team was building a commercial version in a cramped office, racing to beat the giant to market.

The irony was delicious: three guys with $2,000 were about to beat IBM—then the most powerful technology company on Earth—at their own game, using research IBM had commissioned but refused to commercialize. It was the beginning of a pattern that would define Oracle's entire history: see the future before the incumbents do, then move faster and more aggressively than anyone thinks possible.

III. The Database Wars & Going Public (1977-1990)

In 1979, Oracle released their first version of Database. Ellison believed that customers would be skeptical about purchasing a Version 1 product since first versions are often perceived as untested or incomplete. By starting with "Version 2", Oracle positioned their database as a more mature and reliable solution. It was classic Ellison—part marketing genius, part confidence trick, all results. Oracle Version 2 became the first commercial SQL-based relational database to hit the market, beating IBM's SQL/DS by two years.

The early product was, by all accounts, barely functional. It crashed frequently, corrupted data, and required constant patches. But Ellison understood something fundamental about enterprise software: being first mattered more than being perfect. While competitors refined their products in laboratories, Oracle was in the field, learning from real customers, iterating in production. Understanding both customers and technology, Ellison designed database tables that he used to demonstrate the power of SQL to customers.

Then came the breakthrough that would transform Oracle from a startup to a rocket ship. In 1981, IBM—the very company whose research Oracle had commercialized—adopted Oracle for their mainframe systems. The irony was extraordinary: IBM needed a SQL database for their customers, their own System R wasn't ready, and Oracle was the only game in town. It was like Coca-Cola buying syrup from a lemonade stand.

The IBM endorsement triggered a seven-year run that remains one of the most spectacular growth stories in business history. Revenue doubled every single year from 1981 to 1988—from roughly $2 million to over $280 million. By February 1983 the Rosen Electronics Letter said that Oracle was "the most comprehensive offering we've seen" among databases, with good marketing and substantial installed base. The newsletter said that revenue in fiscal 1983 would be about $8 million and would double in 1984.

On March 12, 1986, the company had its initial public offering. By 1987, Oracle had become the largest database management company in the world, surpassing Cullinet, Cincom, and even challenging IBM in certain segments. The company that started with $2,000 was now worth hundreds of millions.

But Oracle's sales culture was becoming legendary for all the wrong reasons. Ellison had built a compensation system that rewarded booking future revenue today—sales reps could claim commissions on multi-year deals upfront, even if the customer might never pay. The incentive was to close deals at any cost, promise anything, book the revenue, collect the commission, and let someone else worry about delivery.

Oracle's "up-front" marketing strategy urged potential customers to buy the largest possible amount of software all at once. The sales people then booked the value of future license sales in the current quarter, thereby increasing their bonuses. This became a problem when the future sales subsequently failed to materialize.

The bill came due in 1990. An internal audit revealed the house of cards: earnings had been dramatically overstated, customers were defaulting, and the company was running out of cash despite showing profits on paper. Oracle's stock price crashed 80% in a single day. Oracle laid off 10% of its workforce (about 400 people) because it was losing money. The company teetered on the edge of bankruptcy.

Oracle eventually had to restate its earnings twice, and had to settle class-action lawsuits arising from its having overstated its earnings. But Ellison, displaying the resilience that would define his career, engineered one of tech's great turnarounds. He brought in disciplined executives like Ray Lane to clean up sales practices, implemented strict revenue recognition rules, and refocused on product quality.

The near-death experience taught Oracle—and Ellison—a crucial lesson: aggressive was good, reckless was fatal. The company emerged from the crisis leaner, meaner, and ready for the next war. The database battles were won, but the enterprise software wars were just beginning.

IV. The Internet Era & Failed NC Computer (1990s)

By 1995, Larry Ellison had a new enemy and a radical vision. The enemy was Microsoft and its Windows monopoly. The vision was the Network Computer (NC)—a $500 device that would destroy the personal computer industry as everyone knew it. "The PC is a ridiculous device," Ellison declared at conference after conference. "Why does everyone need a full computer on their desk when all they really need is a window to the network?"

The NC was breathtakingly ahead of its time—essentially a Chromebook conceived 15 years before Google existed. No hard drive, no complex operating system, no Microsoft tax. Just a screen, keyboard, and connection to servers where all the applications and data would live. It was cloud computing before anyone called it that, Software-as-a-Service when software still came in boxes.

Ellison evangelized the NC with religious fervor, positioning it as liberation from the "Microsoft monopoly." He formed alliances with IBM, Sun, Apple, and Netscape—an anti-Microsoft coalition united more by shared antipathy than shared vision. Oracle would provide the database backend, Sun the servers, IBM the credibility. The PC was dead, Ellison proclaimed. The network was the computer.

But reality bit hard. The NC's promised $500 price point proved impossible to hit—early models cost nearly as much as PCs. Meanwhile, PC prices were plummeting exactly as Ellison predicted they wouldn't. A decent Windows machine dropped from $2,000 to under $1,000 while Oracle was still trying to ship its first NC. Worse, the devices that did ship were sluggish, buggy, and required IT infrastructure that most companies didn't have. The broadband needed to make NCs viable barely existed outside Silicon Valley.

By 1999, the NC was dead, but Ellison had already moved on. While publicly pushing network computers, Oracle had quietly been rebuilding itself for the Internet age. The company developed web-enabled versions of its database, embraced Java (despite it being Sun's technology), and began building a suite of enterprise applications that could run in web browsers. The NC failed as a product but succeeded as a vision—it forced Oracle to think beyond databases, to imagine software delivered as a service rather than shipped in boxes.

The real transformation of the 1990s wasn't the NC; it was Oracle's evolution from a database company to an enterprise software giant. The company launched Oracle Applications—ERP systems that competed with SAP—and began its first serious acquisitions. The failed NC battle had taught Ellison a crucial lesson: you couldn't beat monopolies with clever hardware. You beat them by becoming a monopoly yourself, by owning every layer of enterprise software from the database up.

The dot-com boom was beginning, and while everyone else was funding pet food delivery services, Oracle was quietly becoming the plumbing of the Internet economy. Every e-commerce transaction, every online bank transfer, every web application needed a database. And increasingly, that database was Oracle. The company that failed to kill the PC was about to become indispensable to the Internet age.

V. The Acquisition Spree: Building Through M&A (2000-2010)

The opening shot of Oracle's acquisition wars came in June 2003, stunning Silicon Valley with its audacity. Oracle announced a hostile takeover bid for PeopleSoft, its rival in enterprise applications, for $5.1 billion. PeopleSoft's CEO, Craig Conway—a former Oracle executive who Ellison had personally fired—called it "atrociously bad behavior from a company with a history of atrociously bad behavior." The business world hadn't seen anything yet.

The PeopleSoft battle would rage for 18 months, becoming the most dramatic hostile takeover in software history. Conway compared Ellison to Genghis Khan, took out full-page newspaper ads denouncing Oracle, and implemented a "poison pill" that would refund customers' money if PeopleSoft was acquired. Oracle raised its bid four times, eventually paying $10.3 billion in January 2005—double its initial offer. Within months, Oracle laid off 5,000 PeopleSoft employees. Conway's fears of pillaging proved prophetic.

But Ellison was just warming up. In 2006, Oracle swallowed Siebel Systems for $5.8 billion. Tom Siebel, the company's founder, had also once worked for Ellison before leaving to build the world's leading CRM company. The acquisition announcement included a telling quote from Ellison: "In a single step, Oracle becomes the number one CRM applications company in the world." Not through innovation, not through better products, but through the simple act of buying the competition.

The 2008 acquisition of BEA Systems for $8.5 billion gave Oracle the middleware layer—the software that connects applications to databases. Then came the masterstroke: Sun Microsystems in 2010 for $7.4 billion. Sun wasn't just another software company; it built hardware, operated the Java programming language, and owned MySQL, the open-source database that many saw as Oracle's biggest long-term threat. The European Commission delayed the acquisition for several months over questions about Oracle's plans for MySQL, Sun's open-source database that competed directly with Oracle's cash cow. But Ellison played hardball, refusing to divest MySQL and threatening to shut it down entirely if regulators blocked the deal. On January 21, 2010, EU Competition Commissioner Neelie Kroes announced unconditional approval of the deal. On January 27, 2010, Oracle announced that it had completed the acquisition.

The Sun acquisition was transformative on multiple levels. Oracle President Safra Catz declared it would be "more profitable in per share contribution in the first year than we had planned for the acquisitions of BEA, PeopleSoft and Siebel combined." More importantly, Oracle, only a software vendor prior to the merger, owned Sun's hardware product lines, such as SPARC Enterprise, as well as Sun's software product lines, including the Java programming language.

An Oracle executive would later explain the strategic value: "It gave us a whole stack, a credible stack. And we could now sell at a higher point into the companies, into the board room." Oracle wasn't just selling databases anymore; it was selling complete systems—hardware, operating system, middleware, database, applications. Everything a company needed from one vendor, with one throat to choke when things went wrong.

The human cost was predictable and brutal. Several notable engineers resigned following the acquisition, including James Gosling, the creator of Java (resigned April 2010); Tim Bray, the creator of XML (resigned February 2010); Kohsuke Kawaguchi, lead developer of Hudson (resigned April 2010); and Bryan Cantrill, the co-creator of DTrace (resigned July 2010). Thousands more were laid off as Oracle integrated operations and eliminated redundancies.

But from Ellison's perspective, the acquisition spree of the 2000s had been a masterclass in empire building. In less than a decade, Oracle had spent over $40 billion to transform itself from a database company into an enterprise software conglomerate that touched every aspect of corporate computing. The strategy was simple: if you can't out-innovate them, buy them. If they won't sell, destroy them. And if regulators complain, outlast them.

The acquisitions also revealed a deeper truth about enterprise software: consolidation was inevitable. Customers didn't want to integrate products from dozens of vendors; they wanted solutions that worked together. By buying the competition, Oracle wasn't just eliminating rivals—it was simplifying the technology stack for enterprises. The fact that this simplification came with vendor lock-in and price increases was, from Oracle's perspective, a feature, not a bug.

VI. The Cloud Transformation (2010-2020)

In 2011, Marc Benioff, the CEO of Salesforce and former Oracle executive, took the stage at his company's Dreamforce conference wearing a life jacket. Behind him, a massive screen showed a sinking yacht with "Oracle" painted on its hull. "We're witnessing the end of software," Benioff declared. "Cloud computing is here, and the old guard doesn't get it." Larry Ellison, watching from Redwood Shores, must have been seething. His former protégé wasn't just competing; he was publicly declaring Oracle obsolete.

The truth hurt because it was partially true. While Oracle had been busy buying enterprise software companies, Amazon Web Services had been quietly building the future. Launched in 2006, AWS had turned computing infrastructure into a utility—spin up servers with a credit card, pay only for what you use, scale instantly. By 2011, AWS was generating over $1 billion in revenue while Oracle was still selling software that required months to install and armies of consultants to configure.

Oracle's first attempt at cloud computing was embarrassing. Fusion Applications, launched in 2010, was supposed to be Oracle's cloud-first suite combining the best features from E-Business Suite, JD Edwards, PeopleSoft, and Siebel. But Fusion wasn't originally engineered for multi-tenancy—the ability to serve multiple customers from a single instance of software. Instead, Oracle was essentially hosting traditional applications and calling it "cloud." Customers weren't fooled. The performance was poor, the pricing confusing, and the migration path from on-premises systems tortuous.

Ellison's initial response to the cloud revolution was denial mixed with derision. "What is cloud computing?" he asked at a 2010 conference. "It's just computers, databases and networks. If I'm missing something, please tell me now!" He claimed Oracle had been doing cloud computing for 15 years—a statement that revealed either profound misunderstanding or deliberate obfuscation.

But by 2012, even Ellison couldn't ignore reality. AWS was growing at 50% annually. Microsoft was pivoting hard to Azure. Google was entering the market. Oracle's stock price was stagnant while cloud companies soared. In a rare moment of humility, Ellison admitted Oracle was late to the cloud party and announced a complete rebuild of Oracle's cloud infrastructure from scratch.

The result was Oracle Cloud Infrastructure (OCI), launched in 2016 as a ground-up reconstruction designed to compete directly with AWS. Unlike Fusion's half-hearted attempt, OCI was genuinely built for the cloud era—with bare metal servers, autonomous services, and aggressive pricing. Oracle hired away top engineers from AWS and Google, essentially buying the expertise it couldn't develop internally. The acquisition that signaled Oracle's genuine cloud awakening was the $9.3 billion purchase of NetSuite in 2016. The transaction was valued at $109.00 per share in cash, or approximately $9.3 billion. NetSuite wasn't just another enterprise application—it was the very first cloud company, founded in 1998 by Evan Goldberg with backing from Larry Ellison himself. The company was seeded with start-up money from Oracle CEO Larry Ellison, who provided approximately $125 million in initial financial backing through his venture capital entity Tako Ventures.

The deal was controversial—Oracle founder Larry Ellison owned nearly 40% of NetSuite, creating obvious conflicts of interest. But it gave Oracle something crucial: a genuinely cloud-native ERP system for mid-market companies, the customers Oracle had always struggled to reach. "Oracle and NetSuite cloud applications are complementary, and will coexist in the marketplace forever," said Mark Hurd, Chief Executive Officer, Oracle.

But the real innovation came with Oracle's Autonomous Database, announced in 2017. This wasn't just a database in the cloud; it was a database that managed itself—automatically tuning performance, patching security vulnerabilities, and backing up data without human intervention. Ellison called it "the most important thing we've done in a long, long time." For once, the hyperbole might have been justified. The Autonomous Database addressed the biggest pain point of Oracle deployments: the armies of database administrators required to keep them running.

By 2020, Oracle had built something credible in the cloud, but the numbers told a sobering story. AWS had over 30% of the cloud infrastructure market. Microsoft Azure had 20%. Google Cloud had 10%. Oracle? Less than 2%. The company that dominated enterprise databases was a rounding error in cloud computing.

The transformation had been expensive, painful, and incomplete. But it had also been necessary. The alternative was watching customers slowly migrate to cloud-native competitors, taking their data—and Oracle's future—with them. The cloud transformation wasn't just about technology; it was about survival.

VII. Modern Era: Multi-Cloud Strategy & AI Revolution (2020-Present)

The pandemic changed everything for Oracle—not because of remote work or digital transformation, but because of a single video call in April 2020. Larry Ellison was on Zoom with President Trump's COVID task force, and someone mentioned that states couldn't track vaccine distribution. "We can build that," Ellison said. Within weeks, Oracle had created the National Electronic Health Records system, processing millions of vaccination records. It was a proof point that Oracle could still move fast when it mattered, but more importantly, it revealed the company's new strategy: go where Amazon couldn't follow. Oracle's response was counterintuitive but brilliant: instead of trying to catch up with AWS's massive scale, they would go smaller and everywhere. By 2024, Oracle Cloud spans 50 interconnected geographic commercial and government cloud regions, while Azure operates in 60+ regions and AWS and Google have fewer. But the real innovation wasn't the number—it was the strategy. Oracle would put cloud regions where others couldn't or wouldn't: inside customer data centers, in government facilities, even in countries with data sovereignty requirements that made AWS uncomfortable.

The aggressive pricing strategy was classic Oracle—turned on its head. Oracle's standard compute shapes are 57% cheaper than equivalent AWS EC2 instances, block storage is 78% cheaper than AWS EBS, and data egress is 13X cheaper than AWS data egress. For a company that built its fortune on premium pricing, this was heretical. But Ellison understood that in infrastructure, you had to buy market share before you could extract value.

Then came the masterstroke: the multi-cloud partnerships. In September 2024, Oracle announced Oracle Database@AWS, Oracle Database@Azure, and Oracle Database@Google Cloud give customers direct access to Oracle Database services running on Oracle Cloud Infrastructure (OCI) and deployed in AWS, Google Cloud, and Microsoft Azure data centers, respectively. Instead of forcing customers to choose, Oracle would run its databases inside its competitors' clouds. It was surrender and victory combined—acknowledging that customers would use AWS and Azure while ensuring Oracle databases remained indispensable.

The strategy revealed a fundamental shift in Oracle's thinking. For decades, the company had believed in the walled garden—use Oracle everything or suffer the consequences. But the cloud era demanded coexistence. Customers wanted best-of-breed solutions, not monolithic stacks. By making Oracle Database available everywhere, the company ensured its most profitable product would survive regardless of which cloud won.

The AI revolution provided another opportunity. While everyone focused on large language models and chatbots, Oracle quietly built massive GPU clusters for enterprise AI workloads. The company's partnership with NVIDIA gave it access to the latest chips, and its lower pricing made it attractive for companies wanting to experiment with AI without AWS's costs. Oracle wasn't trying to compete with OpenAI or Google's AI research; it was providing the infrastructure for enterprises to build their own AI applications.

By 2024, the transformation was complete. Oracle had evolved from a company fighting the cloud to one embracing it on its own terms. The multi-cloud strategy meant Oracle databases could run anywhere. The autonomous features reduced the complexity that had plagued Oracle deployments. The aggressive pricing removed the cost barrier. And Larry Ellison, now 80, remained as combative as ever, declaring at conferences that Oracle would eventually overtake AWS in cloud infrastructure.

The numbers suggested otherwise—Amazon is the leader with a 31% market share, followed by Microsoft with 20% and Google with 12%. According to the statistics, OCI's market share amounted to 3%. But market share wasn't the only metric that mattered. Oracle had successfully protected its database franchise, expanded into new markets with cloud applications, and built a credible infrastructure business. For a company that was supposed to be disrupted by the cloud, it had done remarkably well.

VIII. Playbook: The Oracle Way

To understand Oracle's enduring success, you need to understand its playbook—a set of strategies so consistent over five decades that they've become as predictable as they are effective. This isn't the Silicon Valley playbook of "move fast and break things" or "disrupt yourself before someone else does." This is enterprise software warfare, where battles are won in procurement departments and victories are measured in decades-long contracts.

The Power of Owning the Full Stack

Oracle's fundamental insight was that complexity creates value. While competitors specialized—SAP in applications, Microsoft in operating systems, IBM in services—Oracle systematically acquired or built every layer of the enterprise technology stack. Database, middleware, applications, hardware, even the chips in some cases. This wasn't just about cross-selling opportunities, though those were lucrative. It was about creating a trap.

When everything comes from one vendor, integration is smoother, support is simpler, and finger-pointing disappears. But more importantly, once a company runs Oracle databases with Oracle applications on Oracle hardware, the switching costs become astronomical. Not just in money, but in risk. Who wants to be the CTO who tried to migrate off Oracle and brought the company to its knees?

Aggressive M&A as a Growth Strategy

Between 2005 and 2020, Oracle acquired over 100 companies for more than $100 billion. But these weren't the acqui-hires beloved by Silicon Valley, where you buy a company for its talent. Oracle bought companies for their customers. The pattern was ruthlessly consistent: identify a competitor with a substantial installed base, acquire them, migrate their customers to Oracle products, and eliminate redundant development.

The brilliance was in the execution. Oracle would promise to support acquired products indefinitely, calming customer nerves. Then, over years, support would become more expensive while migration paths to Oracle products would become suspiciously attractive. Eventually, most customers would "choose" to standardize on Oracle. The few who resisted paid increasingly exorbitant support fees that made them wonderfully profitable.

The Enterprise Lock-in Model

Oracle perfected the roach motel business model: customers check in, but they don't check out. It starts innocently enough—a departmental database here, a financial application there. But Oracle's software is designed to expand. The database needs middleware. The middleware works best with Oracle applications. The applications run optimally on Oracle hardware.

Before long, Oracle isn't just a vendor; it's woven into the fabric of the enterprise. The company's data lives in Oracle databases. Its business processes run on Oracle applications. Its IT staff is trained on Oracle technologies. Leaving Oracle doesn't just mean changing software—it means re-engineering the entire business. The fact that this lock-in frustrates customers is irrelevant. As Ellison once said, "It's not enough that we win; everyone else must lose."

Pricing Strategy: Start High, Negotiate Hard

Oracle's pricing strategy is psychological warfare. List prices are astronomical—sometimes 10x what customers eventually pay. But this isn't arbitrary. High list prices serve multiple purposes: they anchor negotiations at a high level, they make discounts feel like victories, and they allow sales reps enormous flexibility in closing deals.

The real genius is in the structure. Oracle doesn't just charge for software; it charges for everything. Licenses, support, upgrades, patches, consulting, training. And the pricing is deliberately opaque—processor-based licensing, named user licensing, perpetual licenses, term licenses. No two customers pay the same price for the same thing. This complexity isn't a bug; it's a feature. It makes comparison shopping nearly impossible and gives Oracle's sales force maximum leverage.

Engineering Excellence Married with Aggressive Sales

This might be Oracle's most underappreciated strategy. While the company is famous (or infamous) for its aggressive sales culture, its engineering is genuinely world-class. Oracle Database isn't the market leader just because of lock-in; it's technically superior in many ways. The company invests billions in R&D, holds thousands of patents, and employs some of the industry's best engineers.

This combination is powerful. The engineering excellence gives the sales force credibility. The aggressive sales culture ensures the engineering excellence gets monetized. Many tech companies struggle with this balance—great products that don't sell, or mediocre products sold brilliantly. Oracle manages both.

The Multi-Cloud Pivot

The newest addition to the playbook represents Oracle's biggest strategic shift in decades. Instead of forcing customers into Oracle's cloud, the company now runs its databases in competitors' clouds. This seems like capitulation, but it's actually brilliant jujitsu. Oracle recognized that the infrastructure battle was largely lost—AWS, Azure, and Google had too much scale. But the database battle? That was still winnable.

By making Oracle Database available everywhere, the company ensures its most profitable product remains relevant regardless of where customers deploy their applications. It's the admission that in the cloud era, being indispensable matters more than being dominant.

Lessons on Founder-Led Companies

Larry Ellison's continued involvement—as Executive Chairman and CTO at age 80—provides a unique case study in founder leadership. Unlike Jobs, Gates, or Page and Brin, Ellison never really left. This has advantages: consistent vision, quick decision-making, long-term thinking unconstrained by quarterly pressures. But it also has disadvantages: succession uncertainty, cultural stagnation, and the inability to move past strategies that worked in the past but may not work in the future.

The Oracle playbook has generated enormous value—over $500 billion in market cap, decades of profitability, and a seemingly unassailable position in enterprise databases. But playbooks eventually become predictable. Customers know Oracle will be expensive. Competitors know Oracle will try to buy them. Regulators know Oracle will push the boundaries.

The question isn't whether the Oracle playbook still works—clearly it does. The question is whether it will continue working in a world of open source, cloud computing, and customers increasingly unwilling to accept vendor lock-in. Oracle's bet is that enterprises will always value integration, support, and stability over freedom and flexibility. So far, they've been right.

IX. Power Analysis & Competitive Dynamics

Sources of Power: The Database Moat

Oracle's core power comes from what Hamilton Helmer would call "switching costs"—but that term undersells the reality. When a bank runs its core transaction systems on Oracle Database, switching isn't just costly; it's existential. One migration error and millions of transactions could fail. One compatibility issue and decades of stored procedures become worthless. The risk isn't measured in dollars but in careers ended and companies destroyed.

This creates what economists call a "host-parasite" relationship, though Oracle would prefer "symbiotic." The customer (host) depends on Oracle for survival, while Oracle (parasite) extracts maximum value without quite killing the host. The genius is in the calibration—Oracle pushes prices to the point of pain but not rebellion, complexity to the point of frustration but not abandonment.

The network effects are subtle but real. Every Oracle-trained DBA increases the ecosystem's value. Every application written for Oracle Database reinforces the standard. Every enterprise that chooses Oracle validates the choice for peers. It's not the consumer-style network effect of Facebook or Instagram, but the enterprise network effect of "nobody ever got fired for buying Oracle."

Scale economies complete the triad. Oracle spends over $7 billion annually on R&D—more than most competitors' total revenue. This creates a virtuous cycle: more investment leads to better products, which justify higher prices, which fund more investment. Competitors can't match the spending without the customer base, but can't build the customer base without the product quality that spending enables.

Competition Landscape: The Four-Front War

Oracle fights on four fronts simultaneously, each requiring different strategies:

Against Microsoft ($3 trillion market cap), it's David vs. Goliath—if David had $500 billion and a mean streak. Microsoft's SQL Server competes directly with Oracle Database, Azure competes with OCI, and Dynamics competes with Oracle's applications. The rivalry is personal—Ellison has called Microsoft's technology "mediocre" for decades. Yet pragmatism prevails: Oracle Database now runs in Azure data centers because customers demanded it.

Against AWS, Oracle faces an existential challenge. Amazon built AWS partially to get away from Oracle's expensive databases, then turned that internal project into the world's largest cloud platform. AWS offers multiple database options—Aurora, RDS, DynamoDB—all designed to help customers escape Oracle. The response? Make Oracle Database available on AWS while simultaneously claiming OCI is superior and cheaper.

Against Salesforce, it's teacher vs. student. Marc Benioff learned at Oracle, then built Salesforce as the anti-Oracle—cloud-native, subscription-based, user-friendly. Oracle's response was typically aggressive: build competing products, acquire complementary ones (NetSuite), and constantly remind everyone that Salesforce itself runs on Oracle databases.

Against open source (PostgreSQL, MySQL, MongoDB), Oracle faces death by a thousand cuts. These databases are free, increasingly capable, and beloved by developers. Oracle's strategy? Embrace and extend—acquire MySQL through Sun, offer Oracle Database Free Edition, and constantly emphasize that when your data absolutely, positively cannot be lost, you need commercial-grade software.

The Database Moat: Why Oracle Database Remains Irreplaceable

The numbers tell the story: Oracle Database generates over $10 billion in annual revenue with margins estimated above 90%. But why can't someone just build a better database? The answer reveals the depth of Oracle's moat.

First, compatibility. Millions of applications are written specifically for Oracle Database, using Oracle-specific SQL extensions, PL/SQL procedures, and optimization techniques. Migrating means rewriting code that's been refined over decades. It's not impossible, but it's expensive, risky, and offers no business value beyond vendor change.

Second, features. Oracle Database has capabilities—Real Application Clusters, Partitioning, Advanced Security—that competitors either lack or implement differently. These aren't nice-to-haves for enterprises; they're mission-critical requirements refined over 40 years of real-world usage.

Third, ecosystem. An entire industry exists around Oracle Database—consultants, tools, training, books. Every Fortune 500 company has Oracle experts on staff. This human infrastructure represents billions in investment that would be stranded by migration.

Fourth, trust. When you're processing millions of financial transactions daily, "good enough" isn't good enough. Oracle Database has proven itself in the most demanding environments on Earth. That track record can't be replicated quickly, no matter how much venture capital you raise.

Cloud Infrastructure: The Disadvantage of Being Late

In cloud infrastructure, Oracle faces the innovator's dilemma in reverse. The company has the technology and capital to compete but lacks the scale and ecosystem. AWS launched in 2006; Oracle's serious cloud efforts began a decade later. In technology, a decade is geological time.

The disadvantages compound. Fewer regions mean higher latency for some customers. Smaller scale means less aggressive pricing on commodity services. Limited ecosystem means fewer third-party tools and integrations. It's a vicious cycle—customers choose AWS because everyone uses AWS, reinforcing AWS's dominance.

Oracle's response—the multi-cloud strategy—is either brilliant adaptation or slow-motion surrender, depending on your perspective. By running Oracle databases in competitors' clouds, Oracle ensures relevance but potentially accelerates infrastructure commoditization. If databases can run anywhere, why does the underlying cloud matter?

Enterprise vs. Consumer: The Road Not Taken

Oracle's focus on enterprise customers was a deliberate choice with profound implications. Enterprise software is lucrative—multi-million dollar deals, multi-year contracts, 90%+ gross margins. But it's also slow, complex, and resistant to change. Consumer software is the opposite—fast-moving, simple, winner-take-all.

This choice shaped everything: Oracle's products (powerful but complex), sales model (relationship-based, high-touch), and culture (aggressive, competitive, profit-focused). It also meant Oracle missed entire revolutions—social media, mobile apps, consumer cloud services. While Facebook and Google were defining the modern internet, Oracle was selling databases to banks.

Was this a mistake? Financially, no. Oracle's enterprise focus generated enormous profits and built a defensible moat. Strategically, maybe. The consumer internet companies now have the scale, talent, and capital to challenge Oracle in enterprise markets. Google Cloud, built on consumer-scale infrastructure, can offer services Oracle can't match. Amazon, which learned logistics from e-commerce, applies those lessons to cloud computing.

The Innovator's Dilemma: Protecting Legacy While Building Future

Oracle faces the classic innovator's dilemma: how to embrace cloud computing without cannibalizing its lucrative on-premises business. Every customer that moves to the cloud potentially pays less than they did for perpetual licenses. Every autonomous database deployment potentially eliminates database administrator positions—and the associated consulting revenue.

The company's solution is to have it both ways—claim cloud leadership while keeping on-premises customers locked in. This works financially (revenue continues growing) but creates strategic confusion. Is Oracle a cloud company or a legacy vendor? The answer "both" satisfies no one.

The deeper challenge is cultural. Oracle succeeded by being expensive, complex, and indispensable. The cloud era rewards the opposite: cheap, simple, and replaceable. Can a company built on lock-in truly embrace openness? Can a sales culture that celebrates million-dollar deals adapt to self-service sign-ups? Oracle is betting it can transform without losing what made it successful. The jury is still out.

X. Bear vs. Bull Case

Bull Case: The Fortress of Enterprise Computing

The bull case for Oracle starts with a simple observation: enterprises aren't startups. While Silicon Valley obsesses over the latest JavaScript framework or serverless architecture, the Fortune 500 runs on systems that were designed when Mark Zuckerberg was in elementary school. These aren't legacy systems because companies are lazy; they're legacy because they work, processing trillions in transactions annually with five-nines reliability.

Oracle's unassailable position in mission-critical databases represents one of the most durable competitive advantages in technology. When JPMorgan processes your wire transfer, when United Airlines books your flight, when Walmart tracks its inventory—there's an Oracle database underneath, humming along with the reliability of a Swiss watch. The replacement cost isn't just the software; it's the risk of being the executive who broke something that worked. In enterprise IT, that's career suicide.

The multi-cloud strategy that seemed like capitulation is actually expansion of the addressable market. By making Oracle Database available on AWS, Azure, and Google Cloud, Oracle just multiplied its potential customer base. Companies that would never consider OCI will happily run Oracle Database on their preferred cloud. It's not about winning the infrastructure war; it's about making the database layer cloud-agnostic and indispensable.

The AI revolution plays to Oracle's strengths in ways that aren't immediately obvious. While OpenAI and Anthropic capture headlines, enterprises need somewhere to run their AI workloads, store their vectors, and manage their data pipelines. Oracle's Autonomous Database, with built-in machine learning and automatic optimization, is perfectly positioned for enterprises that want AI capabilities without AI complexity.

Financially, the numbers are compelling. Oracle generates over $50 billion in annual revenue with operating margins above 40%. Free cash flow exceeds $8 billion annually. The company returns billions to shareholders through buybacks while still investing heavily in R&D. This isn't a company managing decline; it's a profit machine with decades of runway.

The alignment with Larry Ellison, who owns approximately 42% of the company, ensures long-term thinking. When your founder's net worth of $200+ billion is tied to the stock price, you can bet he's motivated. Unlike hired CEOs optimizing for their five-year vest, Ellison thinks in decades. His continued involvement at 80 might seem like a governance risk, but it's also strategic continuity.

The Oracle customer base represents an almost insurmountable switching moat. These aren't consumers who can switch from iPhone to Android on a whim. These are enterprises with decades of data, custom applications, and business processes built around Oracle. The lifetime value of these customers, especially as they modernize with Oracle's cloud offerings, could exceed current market expectations.

Bear Case: The Slow-Motion Disruption

The bear case for Oracle isn't about sudden collapse—it's about gradual irrelevance. Like IBM before it, Oracle risks becoming a highly profitable but strategically marginalized company, managing decline while the industry moves on.

Being late to cloud isn't just a timing issue—it's a structural disadvantage that compounds over time. While Oracle claims its cloud is superior, the market has spoken: AWS, Microsoft, and Google dominate with no signs of ceding ground. Oracle's cloud market share isn't just small; it's strategically insufficient to achieve the scale economies that make cloud profitable. Every quarter that passes widens the gap.

The legacy technology debt is massive and growing. Oracle maintains dozens of acquired products, each with its own codebase, customer base, and technical debt. The promise of integration remains largely unfulfilled—PeopleSoft customers still run PeopleSoft, Siebel customers still run Siebel. This isn't a unified platform; it's a holding company of enterprise software assets.

Customer satisfaction remains Oracle's Achilles heel. The company consistently ranks at the bottom of vendor satisfaction surveys. The aggressive sales tactics that built Oracle now create resentment. Every customer forced into an audit, every unexpected price increase, every failed implementation creates an enemy waiting for alternatives. In the age of social media and developer advocacy, reputation matters more than ever.

The dependence on aggressive sales tactics becomes less effective as buyers become more sophisticated. The old playbook—FUD (fear, uncertainty, doubt), vendor lock-in, audit threats—works on the current generation of IT leaders who grew up with Oracle. But the next generation, raised on open source and cloud, sees these tactics as archaic. They'd rather build on PostgreSQL than deal with Oracle's licensing complexity.

The innovator's dilemma is real and unsolved. Every autonomous database sale potentially eliminates multiple DBA positions and consulting opportunities. Every cloud migration reduces the total contract value. Oracle is essentially forced to disrupt its own business model, but doing so too quickly would devastate near-term financials. The result is strategic paralysis disguised as transformation.

The open-source threat grows stronger every year. PostgreSQL has become enterprise-ready. MongoDB dominates in modern applications. MySQL, despite Oracle's ownership, remains freely available. The price differential—free versus tens of thousands per core—becomes harder to justify as open-source databases become more capable.

The Verdict: Profitable Decline or Renaissance?

The truth likely lies between the extremes. Oracle is neither doomed nor dominant. It's a highly profitable company managing a transition from legacy leader to cloud competitor, from monopolist to participant, from feared to merely respected.

The bull case assumes enterprises value stability over innovation, that switching costs remain prohibitive, and that Oracle's cloud investments eventually pay off. This is essentially a bet that enterprise IT remains conservative, that digital transformation is slower than expected, and that Oracle's database dominance translates into cloud relevance.

The bear case assumes the opposite: that enterprises increasingly embrace change, that cloud-native competitors offer compelling alternatives, and that Oracle's cultural DNA prevents true transformation. This is a bet that technical debt eventually overwhelms, that customer resentment eventually matters, and that being late to cloud is ultimately fatal.

For investors, the question isn't whether Oracle survives—it will. The question is whether it thrives. Can a company built on complexity embrace simplicity? Can a culture of aggression adapt to collaboration? Can a legacy vendor become a cloud leader? The answer determines whether Oracle is a value trap or an undervalued transformation story.

The numbers suggest caution: growing but slowly, profitable but not explosively, transitioning but not transformed. The stock price reflects this ambiguity—neither cheap enough for value investors nor exciting enough for growth investors. Oracle exists in valuation purgatory, too successful to be dismissed but not successful enough to be celebrated.

XI. Epilogue: Legacy & Future

Larry Ellison stands at the podium at Oracle CloudWorld 2024, age 80, still commanding the stage with the energy of someone half his age. Behind him, slides show Oracle's cloud regions expanding across the globe like a time-lapse of empire building. "We're not done," he declares. "We're just getting started." It's the same message he's been delivering for five decades, and somehow, it still doesn't sound like hyperbole.

Ellison's place in technology history is secure but complicated. He's not the beloved visionary like Jobs, the philanthropist like Gates, or the innovator like Page and Brin. He's the warrior, the competitor, the man who built a fortune by being tougher than everyone else. In Silicon Valley's mythology of garage startups and world-changing idealism, Ellison is the antihero—proof that nice guys don't always finish first.

Yet his impact is undeniable. Oracle didn't just build databases; it built the infrastructure for global commerce. Every credit card swipe, every online purchase, every supply chain transaction—Oracle is there, invisible but essential. The company processes trillions of dollars in transactions annually, stores exabytes of the world's most critical data, and runs systems that literally cannot fail. If Oracle disappeared tomorrow, the global economy would grind to a halt.

The database that ate the world started as a consulting project for the CIA and became the foundation of enterprise computing. It's a testament to the power of being early (first commercial SQL database), being aggressive (outmaneuvering IBM), and being relentless (forty years of execution). Oracle Database isn't just software; it's infrastructure as fundamental as roads or power grids.

But what happens after Ellison? It's the question that hangs over Oracle like a cloud. Safra Catz, CEO since 2014, is competent but not visionary. The bench of potential successors is thin. The culture is so shaped by Ellison's personality that it's hard to imagine Oracle without him. Some companies transcend their founders—Apple after Jobs, Microsoft after Gates. Others don't—Digital Equipment Corporation, Wang Laboratories, companies that dominated their eras but couldn't survive leadership transition.

The next battleground is clear: AI and sovereign clouds. As nations demand data sovereignty and enterprises seek AI capabilities, Oracle is positioning itself as the trusted provider—not the coolest or cheapest, but the most reliable. The company's partnership with NVIDIA for AI infrastructure, its expansion into government clouds, and its focus on autonomous operations all point to a strategy of being indispensable rather than innovative.

The sovereign cloud opportunity is particularly intriguing. As governments realize data is strategic, they want it stored domestically, managed by trusted providers, and subject to local laws. Oracle, with its history of government contracts and enterprise security, is uniquely positioned. While AWS and Google face scrutiny over data privacy and Chinese ownership concerns limit Alibaba Cloud's expansion, Oracle can position itself as the safe choice.

Yet the fundamental tension remains: Can Oracle transform while remaining Oracle? The company's strength—its complexity, integration, and lock-in—is also its weakness in an era that values simplicity, modularity, and freedom. Every autonomous feature that simplifies management reduces the need for Oracle consultants. Every cloud migration that succeeds makes the next one easier. Every open-source database that matures makes Oracle's premium harder to justify.

The final reflection on building a $500+ billion company is that it required a unique combination of timing, talent, and tenacity. Ellison saw the future (relational databases) before others, executed better than anyone thought possible, and simply outlasted the competition. He didn't build Oracle by being liked; he built it by being necessary.

Oracle's story is ultimately about power—the power of owning critical infrastructure, the power of making yourself indispensable, the power of surviving long enough to see competitors fade. It's not the Silicon Valley story we like to tell—of innovation and disruption and changing the world. It's a different story: of execution and persistence and winning ugly.

As the tech industry enters the AI era, Oracle remains what it's always been: essential but unloved, powerful but resented, successful but somehow still underestimated. The company that everyone predicts will decline but never does. The database that ate the world and is still hungry.

Whether Oracle thrives or merely survives in the next decade depends on its ability to resolve the contradiction at its heart: How do you disrupt yourself without destroying yourself? How do you embrace the future without abandoning what made you successful? How do you transform a culture built on conflict into one built on collaboration?

The answer will determine whether Oracle's next chapter is renewal or decline, whether it becomes the enterprise AI platform or the next IBM, whether Larry Ellison's legacy is building a company that lasted 50 years or one that lasts 100.

The one certainty? Oracle will fight. It's what they do. It's who they are. And in enterprise software, sometimes that's enough.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube