NVR: The Land-Light Homebuilding Revolution

I. Cold Open & Episode Roadmap

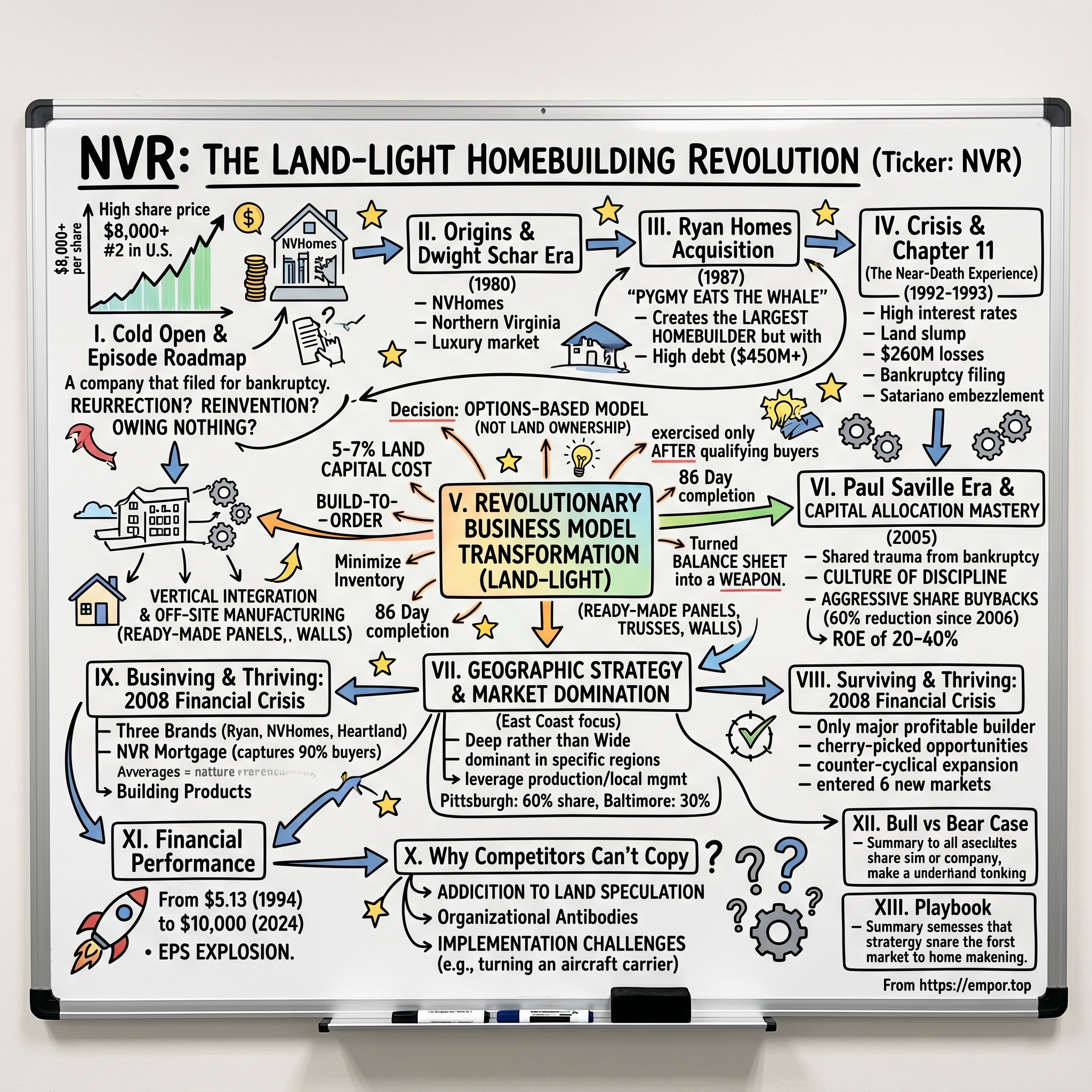

Picture this: A stock trading at over $8,000 per share, making it the second most expensive on all U.S. exchanges, trailing only Warren Buffett's Berkshire Hathaway Class A shares. Now imagine that same company filed for bankruptcy just three decades ago, wiping out nearly all shareholder value. This isn't a Silicon Valley unicorn or a biotech miracle—it's a homebuilder. A homebuilder that builds fewer homes than its competitors, owns virtually no land, and operates in just 14 states plus Washington D.C.Welcome to the tale of NVR, Inc., a company that as of today trades at $8,212.81, having reached an all-time high of $9,964.77 on October 18, 2024. That astronomical share price makes it the second most expensive stock on U.S. exchanges, a rarefied air it shares only with Warren Buffett's Berkshire Hathaway Class A shares. Yet this isn't a story about steady, predictable growth. It's about resurrection, reinvention, and the counterintuitive power of owning nothing in an industry built on owning everything.

As of 2023, NVR stands as the fourth-largest home construction company in the United States by homes closed. But here's the twist: they achieve this while owning virtually no land, maintaining minimal inventory, and operating with a fraction of the capital their competitors deploy. The central question isn't just how a company that filed for bankruptcy in 1992 became one of the greatest compounders in stock market history—it's how they discovered that sometimes the best way to win is to play an entirely different game.

This is a masterclass in crisis-driven innovation. It's a testament to capital allocation excellence that would make even the most disciplined private equity partners envious. And perhaps most importantly, it's proof that in business, as in investing, being contrarian isn't just about betting against the crowd—it's about reimagining the rules entirely.

What you're about to discover challenges everything conventional wisdom teaches about homebuilding. You'll learn why a company that refuses to speculate on land consistently outperforms those that do. Why building fewer homes can create more value. And why sometimes the most important competitive advantage isn't what you own, but what you choose not to own.

The themes we'll explore—crisis as catalyst, capital discipline as strategy, and the paradox of constraints breeding innovation—aren't just relevant to homebuilding. They're universal lessons about how great businesses are forged in the crucible of near-death experiences and how the scars of failure can become the blueprint for extraordinary success.

II. Origins & the Dwight Schar Era

The year was 1980, and in the affluent suburbs of Northern Virginia, a former schoolteacher turned homebuilding executive was about to launch a company that would one day trade at nearly $10,000 per share. But Dwight Schar's journey to founding NVHomes didn't begin in a boardroom—it started in a junior high school classroom in rural Ohio, where he taught during the week and sold homes on weekends to make ends meet.

Born and raised in rural northeast Ohio, Schar graduated from Ashland University in 1964 with a degree in education. After graduating, he began teaching, but on weekends took a job selling homes. He soon left teaching to pursue a career in homebuilding. It was this weekend side hustle that would change everything. The young teacher discovered he had a gift for understanding what homebuyers wanted, and more importantly, how to deliver it profitably.

In 1968, Schar joined Ryan Homes, where he headed the company's land acquisition and development efforts in Ohio, Kentucky, and Indiana until 1973. He was then appointed vice-president and group manager of Ryan Homes' Washington D.C. operations from 1973 to 1977. During these formative years at Ryan Homes, Schar absorbed every lesson the homebuilding industry had to offer—from land acquisition strategies to construction management, from customer psychology to capital allocation. But perhaps more importantly, he observed what he believed the industry was doing wrong: tying up enormous amounts of capital in land speculation.

When Schar decided to strike out on his own in 1977, he faced an unexpected obstacle: a two-year non-compete agreement with Ryan Homes that forced him to leave the homebuilding industry entirely. He finally launched Northern Virginia Land and Homes Company in 1980. Those two years of forced exile proved invaluable. While his competitors continued building through the late 1970s recession, Schar watched from the sidelines, studying market cycles, analyzing failures, and formulating a vision for what would become NVHomes.

The Washington D.C. metro area in 1980 was the perfect laboratory for Schar's experiment. Federal government employment provided economic stability, the region's educated workforce demanded quality homes, and the sprawling suburbs of Northern Virginia offered endless growth opportunities. Schar positioned NVHomes as a luxury builder, targeting move-up buyers who wanted more than just four walls and a roof—they wanted a statement of success.

The company's early growth was nothing short of spectacular. Under Schar's leadership, Northern Virginia Land and Homes Company experienced significant success in its first decade, with a mortgage service entity added in 1984 and a debut on the public trading floor in 1986. By 1986, the company had doubled its net income each year, reaching nearly $14 million. The formula seemed simple: buy land in the path of development, build quality homes, sell them at premium prices, repeat.

But this go-go growth strategy had a dark side. NVR's approach during the 1980s was fundamentally a leveraged bet on ever-rising land prices. The company borrowed heavily to acquire massive land positions, believing that Washington's continued growth would bail out any mistakes. Under Schar's leadership, NVR grew rapidly, expanding into mortgage services in 1984 and going public in 1986. Land prices were indeed skyrocketing throughout the eighties, making the strategy look brilliant—at least on paper.

The cultural DNA established during these early years would prove both a blessing and a curse. On one hand, NVHomes developed a reputation for quality and customer service that commanded premium prices. The company understood that in the D.C. market, where government workers and contractors formed a stable, affluent customer base, buyers would pay more for perceived value. On the other hand, the aggressive expansion mindset and appetite for leverage that characterized the 1980s would soon lead the company to the brink of disaster.

By 1986, NVHomes had conquered Northern Virginia. But Schar's ambitions extended far beyond the Beltway. He saw an opportunity to roll up the fragmented homebuilding industry, creating a multi-regional powerhouse. The vehicle for this transformation would be an audacious acquisition—one that would reunite him with his former employer in a twist worthy of a business thriller.

III. The Ryan Homes Acquisition & Building an Empire

The boardroom at Ryan Homes' Pittsburgh headquarters must have been electric with disbelief when the acquisition terms were announced in 1986. Here was NVHomes, a six-year-old company with annual revenues under $100 million, proposing to acquire Ryan Homes—a venerable institution founded in 1948 that had built homes for America's expanding post-war economy and generated five times NVHomes' revenue. This was especially remarkable considering the latter had generated 5x more revenue than NVHomes the previous year. Industry observers called it "a case of the pygmy eating the whale".

In 1986, the company acquired Ryan Homes, founded in 1948 in Pittsburgh, Pennsylvania, to provide housing in the expanding post-war economy. But Schar saw something others missed. Ryan Homes wasn't just a homebuilder—it was a brand with four decades of trust, a manufacturing system that could build homes at scale, and most importantly, a complementary market position. While NVHomes targeted luxury move-up buyers in the Washington area, Ryan Homes had perfected the art of building for first-time homebuyers and blue-collar families across multiple states.

The strategic logic was compelling: combine NVHomes' high-margin luxury expertise with Ryan Homes' volume-based entry-level mastery. Create a portfolio of brands that could capture customers at every price point and life stage. Leverage Ryan Homes' manufacturing capabilities and established supply chains. And perhaps most ambitiously, use the combined entity's scale to dominate entire metropolitan markets rather than competing for scraps.

A few months after becoming a limited partnership, NVH acquired a controlling interest in Ryan Homes, Inc. Before the end of 1987 NVH had acquired all of Ryan, making it a subsidiary of the newly formed NVRyan L.P. The acquisition was structured through multiple stages, first gaining control, then completing the full takeover. In 1987, NVR, Inc. acquired Ryan Homes for a reported $312 million, culminating in the creation of the largest homebuilding company in the whole of the United States.

But here's where Schar's ambition collided with financial reality. The Ryan Homes deal was also a leveraged buyout. The company financed the acquisition with over $450 million in debt, provided by a consortium of banks and subordinated debt securities. This wasn't just leverage—it was leverage on top of leverage, as NVHomes had already borrowed heavily to fund its rapid expansion and land accumulation strategy throughout the mid-1980s.

The newly christened NVR (dropping "yan" from NVRyan) now operated three distinct brands. Ryan Homes would continue serving first-time buyers with affordable, standardized homes. NVHomes would focus on the luxury segment with custom features and premium locations. And the company's land development arm would feed both operations with a steady pipeline of buildable lots. The company structure seemed perfectly designed for the go-go real estate market of the late 1980s.

By 1987, the combined entity was firing on all cylinders. In 1987, NVRyan sold about 3,800 homes in the Washington area for a total value of nearly $500 million. The company had successfully created a vertically integrated homebuilding machine, controlling everything from land development to mortgage origination. Wall Street loved the story—here was a company that had cracked the code on consolidating the fragmented homebuilding industry.

The multi-brand strategy allowed NVR to segment the market with surgical precision. Ryan Homes could compete on price and efficiency, churning out standardized floor plans in suburban developments. NVHomes could command premium prices by offering architectural details and customization options that justified higher margins. And both brands could share back-office functions, construction expertise, and purchasing power.

But beneath the surface, warning signs were already emerging. The company's debt load was staggering—nearly half a billion dollars borrowed at a time when interest rates were beginning to creep higher. The land inventory on NVR's balance sheet had ballooned to dangerous levels. And most ominously, the company's entire business model depended on two assumptions that would soon prove catastrophic: that land prices would continue rising, and that the housing market would keep expanding.

As 1987 turned to 1988, and then to 1989, NVR continued its aggressive expansion, opening new markets and accumulating more land. A big part of that growth was funded with leverage, where Schar borrowed a ton of money to "buy vast swaths of land and hold it" for use in future homebuilding. The company seemed unstoppable, a juggernaut rolling through the Eastern United States, transforming farmland into subdivisions and booking ever-higher profits.

But in the distance, storm clouds were gathering. The savings and loan crisis was beginning to unfold. Credit markets were tightening. And somewhere in NVR's sprawling land holdings—parcels bought at peak prices with borrowed money—lay the seeds of the company's near-destruction.

IV. Crisis & Chapter 11: The Near-Death Experience

The spring of 1992 should have been a time of renewal in the homebuilding industry. Interest rates were finally beginning to ease from their early-1990s peaks. The economy was showing tentative signs of recovery. But in NVR's McLean, Virginia headquarters, the atmosphere was funereal. After months of desperate negotiations with banks and bondholders, the inevitable had arrived.

The company's growth ended two years ago when debt-laden NVR crashed in the real estate slump. In 1991, the company lost $36.7 million and had revenue of $818.9 million. In 1990, NVR lost $260 million and had revenue of $1.1 billion. The numbers told a story of catastrophic decline—from over a billion in revenue to bankruptcy in just two years.

The early 1990s recession had exposed the fatal flaw in NVR's business model: leverage piled upon leverage in a cyclical industry. In the early 1990's "interest rates rose sharply into double digits, home sales dropped precipitously, and Schar was left with loans on land he suddenly did not need". Industry-wide completions fell by more than 50%. What had looked like shrewd expansion now revealed itself as reckless speculation.

On April 6, 1992, NVR and some of its homebuilding subsidiaries filed for Chapter 11 bankruptcy. The filing wasn't a surprise to insiders—negotiations with creditors had been ongoing for months—but it still represented a stunning fall from grace for a company that just five years earlier had been the acquirer, not the acquired.

The restructuring drama that unfolded over the next 17 months would transform not just NVR's balance sheet, but its entire philosophy of business. The Chapter 11 bankruptcy (aka 'reorganization' bankruptcy) allowed NVR to restructure its debts and operations while continuing its core functions. This was crucial—unlike a liquidation, NVR could keep building and selling homes while negotiating with creditors.

The bondholders, owed $206 million, held all the cards. Bondholders to whom NVR owed $206 million have received a 91.1 percent stake in the new corporation, while former holders of partnership unit have seen their equity reduced to 6 percent. The bondholders agreed to trade their debt claims for equity in the reorganized company, a classic debt-for-equity swap that would wipe out nearly all existing shareholder value but give the company a fighting chance at survival.

Remarkably, throughout this corporate near-death experience, the operational side of the business continued functioning. During the bankruptcy proceedings, the company continued to have healthy revenue from its NVHomes and Ryan Homes subsidiaries, and from NVR Mortgage, which filed separately for Chapter 11 protection in December 1992. Since the bankruptcy court protected customers' deposits from creditors as long as NVR kept building, the proceedings had virtually no effect on buyers.

The firm built 4,228 housing units last year. Dwight Schar, who might have been expected to be shown the door, somehow maintained his position. Even though control of NVR likely will shift to the bondholders, Schar said he expects to continue as chairman. His survival would prove crucial to what came next.

The bankruptcy wasn't just a financial restructuring—it was a philosophical awakening. Looking back on the experience, one of Schar's close developer friends noted that "Schar discovered the hard way that you don't want to hold a whole lot of land" in this business. This lesson, learned at enormous cost, would become the foundation of NVR's revolutionary business model.

To add insult to injury during this period, Anthony Satariano, CFO of NVR's finance business, embezzled $763,000 and fled to Malta. Schar's ex-wife sued him for $1.3 million. It seemed everything that could go wrong did go wrong.

But from this crucible of crisis emerged clarity. Dwight Schar was still at the helm and appears to have taken a solemn oath to never again use leverage, never again own land or empty lots on NVR's balance sheet, and never again blow the lid on large M&A. The company that would emerge from bankruptcy in September 1993 would bear the same name but would operate on fundamentally different principles.

From April 6, 1992, the petition date, until September 30, 1993, the date NVR eventually emerged from bankruptcy, NVR made 5,571 transfers of real property and paid $8,349,103 in transfer and recordation taxes to state and local taxing authorities. The company had maintained its operations through the entire bankruptcy period—a remarkable achievement that preserved both its workforce and its reputation.

In September 1993, the company emerged from bankruptcy protection and once again became a public company. But this wasn't the same NVR that had entered bankruptcy 17 months earlier. The near-death experience had forced a complete reimagining of what a homebuilding company could be.

V. The Revolutionary Business Model Transformation

The bankruptcy courtroom in September 1993 was a somber place. But as NVR emerged from Chapter 11 protection, something remarkable had happened. From the ashes of near-total failure, a revolutionary business model was born—one that would transform NVR from industry laughingstock to the envy of every homebuilder in America.

The revolutionary idea that indefinitely changed NVR was the decision to switch to an options-based business model, where NVR would write options on land rather than spending capital on it. At only 5-7% of the land capital cost, NVR's options were only exercised after home buyers were qualified for their mortgages. This wasn't just a tweak to the old model—it was a complete philosophical inversion of everything the homebuilding industry believed to be true.

Think about the audacity of this approach. For decades, homebuilders had operated on a simple premise: buy land cheap, develop it, build homes, sell them for more. Land ownership was the foundation of the entire business. But NVR's bankruptcy had taught them a brutal lesson—in a cyclical industry, owning land was like playing Russian roulette with five bullets in the chamber.

Unlike its competitors, NVR avoids buying speculative land in favor of land purchase agreements. These land purchase agreements are options bought by NVR that can be exercised to purchase land. By using these contracts, NVR can buy land close to the time when it will be used. The genius was in the timing—NVR would only pull the trigger on land purchases after customers had already committed to buying homes and secured financing.

The operational revolution went even deeper. Instead, after its reorganization, NVR purchased individual options to buy land that were exercised only after home buyers qualified for their mortgages. After the customer qualified, NVR would construct the house using on-site contractors. This build-to-order approach eliminated speculation entirely. No more building homes hoping buyers would materialize. No more carrying unsold inventory through downturns.

The numbers tell the story of this transformation's immediate impact. NVR will only exercise a land option contract when it has a buyer for the house and that buyer has received mortgage financing. This allows NVR to lock in pricing from its suppliers (using fixed-price contracts) before it locks in a sales price. It also allows NVR to partially finance its balance sheet with customer deposits.

As a result, NVR boasted an average 86 day home completion rate in 1992—less than three months from breaking ground to handing over keys. Some homebuilders take five or six months to complete a house. NVR often does it in three or four. This wasn't just about speed—it was about capital efficiency. Every day a home sat unfinished was a day capital was tied up earning nothing.

The manufacturing revolution complemented the land-light strategy perfectly. NVR was able to minimize costs, increase quality, and speed product delivery through its subsidiaries that premanufactured segments of the home in off-site facilities. The ready-made panels were delivered to the site where contractors, under the supervision of NVR representatives, assembled and finished the home.

Basically, they build the home off-site. The four walls of the home, all built off-site. Staircases, all built off-site. Interior walls, built off-site, brought there on a truck and then just stood up and nailed together. It's vertically integrated prefab stuff. This wasn't just construction—it was manufacturing, with all the efficiencies that implied.

The cultural transformation was perhaps even more profound than the operational one. NVR famously eschews owning and developing land, which is unique among homebuilders. In fact NVR avoids owning much of anything, preferring to lease its offices, manufacturing facilities, and even employee laptops. All of this adds up to make NVR one of the most capital-efficient businesses out there. The company is truly fanatical about this, and its industry-leading ROE shows.

But here's what made this model truly revolutionary: it turned NVR's balance sheet from a liability into a competitive weapon. After paying the option to acquire the finished building lot from land developers the company goes out and markets a new home. "In addition to our focus on liquidity, another key aspect of our business model is emphasizing local market concentration.

The option contracts themselves became a form of insurance. In good times, NVR could exercise options and build homes for eager buyers. In bad times, they could simply walk away, losing only the option payment—typically 5-7% of the land value—rather than being stuck with depreciating land assets worth millions.

One industry expert captured the essence of the transformation: NVR doesn't exercise lot option contracts until the commitment is received, and even then, they wait to exercise until "3-4 days prior to actually going and digging a hole, breaking ground". Something like 90 days after the lot option is exercised and cash starts going out the door, the house is complete and remaining balances are paid.

The skeptics were numerous and vocal. How could a homebuilder succeed without owning land? How could you guarantee supply without controlling the raw material? Wouldn't land developers demand higher prices knowing NVR had no alternative?

But NVR had discovered something profound: in a world of abundant capital and scarce discipline, being the disciplined buyer with ready cash was more valuable than being the speculative landowner with illiquid assets. Land developers, often stretched thin themselves, valued NVR's certainty of execution and quick payment terms. The company became the buyer of choice for developers who needed reliable takeout for their projects.

This model also fundamentally changed NVR's relationship with risk. With NVR, the risk of unsold properties is much smaller, and it can walk away from land if market prices turn sour before construction starts. Consider that in 2008, the housing crash clobbered anyone with a hefty land inventory. Some builders had to discount homes drastically, while others faced crippling write-offs. NVR had challenges too, but on a relative basis, it emerged in better shape.

The transformation wasn't immediate or easy. It required retraining an entire organization, convincing suppliers to work differently, and most challengingly, resisting the temptation to return to the old ways when markets got hot and competitors seemed to be printing money through land speculation. But Dwight Schar and his team held firm, understanding that surviving the next downturn was more important than maximizing the current upturn.

VI. The Paul Saville Era & Capital Allocation Mastery

In the summer of 2005, as Dwight Schar stepped back from day-to-day operations, a numbers man who had been with the company since 1981 assumed the CEO role. Paul Saville was appointed to his position as President and CEO in 2005, but his influence on NVR's capital allocation philosophy had been building for decades. Executive Chairman Paul Saville has been with the company since 1981, fostering a culture and discipline supportive of the company's unique strategy.

After receiving his M.B.A. from the University of Pittsburgh, Saville joined Ryan Homes, predecessor of NVR, working in various financial positions within the company. His backgrounds in finance and strategic planning/oversight prepared him to serve as Vice President of Business Planning, then CFO and effectively chief operating officer. This wasn't just a succession—it was a deliberate passing of the torch to someone who had lived through the bankruptcy, understood the lessons, and would protect the culture at all costs.

The post-bankruptcy culture Saville inherited and reinforced was unlike anything else in homebuilding. As Saville experienced the near collapse of the company back in the 1992 bankruptcy alongside Schar, management learned from its past. This shared trauma created an almost religious devotion to capital discipline. Where other homebuilders saw opportunity in leverage, NVR saw danger. Where competitors accumulated land, NVR accumulated cash.

The share buyback machine that Saville would oversee represents one of the most aggressive and successful capital return programs in corporate America. The numbers are staggering: they bought back 60% of shares since the last peak in 2006 and compounded free cash flow (FCF) per share by 12% CAGR whilst housing starts barely improved and input costs (labor and construction materials) increased for everyone.

Think about the mathematical beauty of this approach. While competitors were building more homes to grow earnings, NVR was shrinking its share count to grow earnings per share. Every buyback at reasonable prices created value for remaining shareholders. And because the business model generated such consistent cash flow, the buyback program could continue through cycles, not just in good times.

NVR has had a return on invested capital of over 50% for the last 10 years despite the subprime mortgage crisis. This wasn't luck—it was the systematic result of a business model that required minimal capital to grow. When you can generate 50% returns on capital and your stock trades at reasonable multiples, the math of buybacks becomes compelling.

The decision to eschew dividends was equally strategic. Why pay out cash that would be taxed as ordinary income when you could use that same cash to buy back shares, creating tax-deferred value for long-term shareholders? This wasn't financial engineering—it was owner-oriented thinking at its finest.

Under Saville's watch, operational excellence became an obsession. The company didn't just want to avoid owning land; it wanted to minimize owning anything. Office spaces were leased. Manufacturing facilities were leased. Even employee laptops were leased. Every dollar not tied up in fixed assets was a dollar available for homebuilding or buybacks.

The compensation structure Saville championed reinforced these priorities. Unlike competitors who compensated executives based on revenue growth or units built, NVR tied compensation to return on capital. This seemingly small detail had profound implications. It meant executives were incentivized to grow profitably, not just grow. To be selective about opportunities, not chase every deal. To think like owners, not empire builders.

Mr. Saville has been CEO of NVR since July 1, 2005. From 2006 to 2020, Mr. Saville realized $382,935,083 in total compensation. But this compensation was heavily weighted toward long-term equity grants that aligned his interests with shareholders. The latest proxy statement states that he owns 210,378 shares of NVR, or 6.3%. Saville has deferred compensation valued at $488,393,808. This wasn't just skin in the game—it was his entire financial future tied to NVR's success.

The capital efficiency metrics under Saville's leadership defied industry norms. By avoiding the capital intensive and multi-year process of land development, NVR has been able to generate returns-on-equity (ROE) of 20 to 40% over the long term, 2x to 3x better than most of its large homebuilder competitors. These weren't peak cycle numbers—these were through-cycle averages that included the devastating 2008 financial crisis.

The discipline extended to growth opportunities. While competitors rushed into new markets during booms, NVR expanded methodically, only entering markets where it could achieve dominant share over time. The philosophy was simple: better to be the biggest fish in a smaller pond than a minnow in the ocean.

Risk aversion became a competitive advantage. In an industry notorious for blow-ups and bankruptcies, NVR's conservative approach attracted the best land developers as partners, the most creditworthy customers, and the most patient shareholders. The company's bonds traded at spreads typically associated with investment-grade industrials, not cyclical homebuilders.

But perhaps Saville's greatest achievement was institutionalizing the culture beyond any single individual. On May 4, 2022, Eugene J. Bredow will assume the role of Chief Executive Officer. Mr. Bredow currently serves as the President of NVR Mortgage. The succession planning ensured that the next generation of leadership had been steeped in NVR's unique approach, understanding not just the what but the why behind every decision.

Saville joined the company in 1981 and was President and CEO from 2005 to 2022. He assumed the position of executive chair in 2022. His transition to Executive Chairman wasn't retirement—it was a deliberate move to preserve institutional memory while allowing new leadership to operate. The culture and discipline he helped build had become NVR's true moat.

VII. Geographic Strategy & Market Domination

If you fly over the Eastern United States at night, the lights below tell a story of concentrated population and economic activity. From Boston to Washington, from Pittsburgh to Charlotte, a continuous corridor of illumination marks one of the world's most prosperous regions. This is NVR country—and the company's geographic strategy represents a masterclass in the power of regional dominance over national presence.

In 2021, 22% of the company's revenue was from the Washington metropolitan area. The company primarily operates on the East Coast of the United States, but its operations encompass 14 states as well as Washington, D.C. But these numbers obscure a more profound truth: NVR isn't trying to be everywhere. It's trying to be everything in the places it chooses to be.

The Eastern seaboard focus wasn't accidental—it was genius. This region offers stable employment anchored by government jobs, high household incomes, limited land supply that creates pricing power, and dense population centers that maximize operational efficiency. While competitors spread themselves thin trying to capture market share nationally, NVR went deep rather than wide.

The company has grown from its core Washington D.C. market, where it has an estimated 20% market share, into the adjacent markets of Baltimore and Richmond, where it now commands a similar or even higher market share. In Pittsburgh, PA, NVR has a 60% market share of the new home market, in Baltimore, MD, 30%, and in Washington D.C., 20%, as of 2013. These aren't just impressive numbers—they represent market positions so dominant that NVR effectively sets the terms for land developers, subcontractors, and even competitors in these regions.

The market share strategy is about more than just bragging rights. NVR's strategy of establishing itself as the dominant builder in each geography allows the company to leverage its regional production facilities, leverage local management, foster strong relationships with subcontractors, and obtain access to quality land deals. When you're building 20-30% of all new homes in a market, you become the buyer every land developer wants to work with, the employer every subcontractor depends on, and the brand every real estate agent knows to recommend.

The top 9 metros collectively represented roughly 50% of NVR's total completions in 2021, while Philadelphia, Baltimore, and Washington, DC represented nearly 30% of total completions. That's a significant concentration of activity in just a ~200-mile corridor. This concentration would terrify most investors—what about diversification? What about spreading risk? But NVR understood something crucial: in homebuilding, density creates efficiency, and efficiency creates profitability.

The company's growth pattern over the past two decades reveals the methodical nature of its expansion. NVR's market share in both metros has actually increased considerably over time (for example, Washington, DC was just 8.2% in 2004 and sat at 25.0% in 2021, and Baltimore was at 16.4% in 2004 but 26.6% in 2021). So, the real reason for the steadily declining concentration is that NVR has successfully expanded in other markets, notably Philadelphia, Richmond, Cincinnati, Charlotte, Nashville, Greenville, Chicago, and multiple cities in Florida.

For example, in Philadelphia they went from 6.4% share in 2004 to 27.5% in 2021, in Nashville they went from roughly 2% share in the early-2000's to 7.4% in 2021, and in Chicago they went from sub-1% share to 5.3% in 2021. This isn't expansion—it's conquest. NVR enters a market quietly, learns the local dynamics, builds relationships, and then systematically takes share year after year until it achieves a dominant position.

The density advantage manifests in countless operational benefits. When you're building hundreds of homes within a 50-mile radius rather than dozens scattered across a state, everything becomes more efficient. Construction supervisors can visit multiple sites in a day. Subcontractors can move crews between projects without long commutes. Materials can be delivered from central facilities without excessive transportation costs. Marketing dollars go further when concentrated in specific media markets.

The company's relatively standardized floor plans have helped reduce design complexity and achieve a best-in-class "cycle time,"—the time to construct a finished home—nearly one-third better than competitors Additionally, by utilizing offsite manufacturing and assembly for its components, NVR can reduce waste and enhance construction quality. This operational leverage is only possible with geographic concentration.

The secondary and tertiary market strategy adds another layer of sophistication. In newer locations, such as Pittsburgh and Charlotte, NVR has an estimated 5-10% market share, but they are steadily gaining as the company leverages its existing infrastructure and industry relationships. Rather than competing in the most expensive, most competitive markets like California or Texas, NVR finds value in overlooked metros where it can achieve dominance without battling national giants.

Unlike most homebuilders, NVR broadly avoids competing in top metro areas, instead opting for promising secondary and tertiary metro areas like Richmond, Virginia and Greenville, South Carolina. These markets offer better economics—land is cheaper, competition is less intense, and local governments are often more accommodating to development. Yet they still offer the population growth and economic stability necessary for a healthy housing market.

The manufacturing and supply chain advantages of geographic concentration cannot be overstated. With manufacturing facilities in Maryland, Pennsylvania, New York, New Jersey, North Carolina, Ohio, Virginia and Tennessee, this division supplies structural building components that are produced to exacting standards in a controlled environment, and then delivered to the job site to reduce waste and improve efficiency. These facilities are strategically located to serve NVR's concentrated markets, minimizing transportation costs and delivery times.

The brand portfolio strategy also aligns with geographic concentration. NVR has three trade names that focus on different parts of the market: Ryan Homes, which primarily targets first-time and first-time move-up buyers (I estimate 90%+ of total revenue); and, NVHomes and Heartland Homes which both target luxury buyers, but only operate in 4 cities (Washington, Baltimore, Philadelphia, and Pittsburgh). By operating multiple brands in the same markets, NVR can capture customers across the entire price spectrum without the complexity of managing operations across disparate geographies.

That kind of superior market share is key to NVR's "land-light" strategy. It's the leading builder in most markets where it operates (others include Pittsburgh and Philadelphia), which gives it the leverage to get developers to accept options rather than outright purchases. This reveals the symbiotic relationship between geographic dominance and the land-light model—you need market power to negotiate favorable option contracts, and concentrated operations to make those options economically viable.

NVR's growth strategy over the last twenty years has been focused on achieving leading share in existing and adjacent markets. This patient, methodical approach stands in stark contrast to competitors who chase hot markets, enter and exit regions based on short-term opportunities, and never achieve the scale necessary for true operational efficiency.

The risk of geographic concentration is real—a regional recession, regulatory changes, or demographic shifts could disproportionately impact NVR. But the company has managed this risk through diversification within its regions, serving multiple customer segments, price points, and housing types within each market. And the operational advantages of concentration have proven more valuable than the theoretical benefits of geographic diversification, especially during downturns when efficiency matters most.

VIII. Surviving & Thriving Through the Great Financial Crisis

The autumn of 2008 was when the American dream turned into a nightmare. Lehman Brothers had collapsed. Credit markets were frozen. And for homebuilders, it was apocalypse now. Housing starts plummeted from 2.3 million units at the 2006 peak to just 550,000 by 2009. Home prices crashed 30% nationally. Builders who had gorged on land during the boom now faced write-downs that would wipe out years of profits—or worse, their entire companies.

At NVR's headquarters in Reston, Virginia, there was tension but not panic. The company had seen this movie before—in 1992. And this time, they had a script for survival. NVR also posited a really impressive feat throughout the Great Financial Crisis – out of its subgroup of companies including Toll Brothers, Dr. Horton, Lennar, and PulteGroup, NVR was the only homebuilder that remained profitable over the period. This could be attributed to its options-based business model as it helped maintain higher margins and keep the balance sheet relatively cleaner.

During the housing crisis a decade ago, NVR was the only major homebuilder to make a profit every year. Think about the magnitude of that achievement. While competitors posted billions in losses, laid off thousands of employees, and in some cases filed for bankruptcy, NVR remained profitable. Not hugely profitable—earnings fell from their 2005 peak of $697 million—but profitable nonetheless.

How did the land-light model protect NVR during 2008? The answer lay in what they didn't own. While competitors sat on billions of dollars of land bought at peak prices, now worth a fraction of what they paid, NVR's exposure was limited to option deposits—typically just 5-7% of land value. When markets turned, they could walk away from options on overpriced land, losing only the deposit rather than the entire land value.

"They're the only builder that never lost money throughout the whole downturn," notes Alex Barron, founder and senior research analyst of the Housing Research Center. The competitive dynamics during the crisis were almost surreal. While peers struggled for survival, NVR was cherry-picking opportunities. NVR in the global financial crisis, in the housing crisis, they entered six new markets, and they bought back unbelievable amounts of cheap stock.

Its return on invested capital never dipped below 12 percent in the worst of the global financial crisis. That's more than the home industry builder average today. Their lowest of their low is higher than the industry average today. This wasn't just resilience—it was dominance. While competitors were playing defense, NVR was on offense.

The debt paydown story during the crisis reveals management's priorities. For instance, as Saville experienced the near collapse of the company back in the 1992 bankruptcy alongside Schar, management learned from its past and NVR strategically used its resources to pay off its debt. In 2006, NVR had $350 million in notes and loans payable; this was decreased down to $90 million by 2010. While the Federal Reserve was flooding markets with liquidity and encouraging borrowing, NVR was doing the opposite—strengthening its balance sheet for the next battle.

The operational adjustments during the crisis were surgical rather than panicked. NVR didn't engage in mass layoffs or shut down operations. Instead, they modestly reduced construction pace, negotiated better terms with suppliers who were desperate for business, maintained relationships with subcontractors who would remember their loyalty, and most importantly, continued taking market share from weakened competitors.

The contrast between 1992 and 2008 is instructive. In 1992, NVR was the distressed company, overwhelmed by debt and forced into bankruptcy. In 2008, they were the predator, using their strong balance sheet and consistent cash flow to expand while others contracted. The lessons from the first crisis had been internalized so thoroughly that the second crisis became an opportunity rather than a threat.

When everyone else in the industry is struggling literally to survive, they enter new markets. This counter-cyclical expansion strategy is only possible with a business model that generates cash even in downturns. While competitors were selling assets to raise cash, NVR was deploying cash to gain strategic advantages that would pay dividends for years.

The psychological impact on the organization was profound. Surviving and thriving through 2008 validated everything NVR had built since 1993. The discipline, the conservative approach, the resistance to industry norms—all of it had been vindicated. Employees who lived through 2008 became true believers in the NVR way. The crisis didn't create the culture; it crystallized it.

But perhaps the most important lesson from 2008 was what NVR didn't do. They didn't abandon their model to chase the recovery. As markets began recovering in 2010 and 2011, as land prices bottomed and began rising again, as competitors started speculating once more, NVR stuck to its discipline. They didn't suddenly start buying land because it was "cheap." They didn't leverage up to accelerate growth. They didn't acquire struggling competitors.

The share buyback activity during and after the crisis deserves special attention. With the stock trading at depressed valuations—falling from over $900 in 2005 to under $400 in early 2009—NVR accelerated buybacks. They were buying dollars for fifty cents, and they knew it. This wasn't market timing; it was value recognition by insiders who understood their business better than panicked markets.

Despite NVR's land-light strategy success, the industry's use of land options remains lower than it was during the housing boom in 2004-2006. They're not moving toward NVR's land-light, asset-light business model. The industry is sticking to the asset-heavy own the land and pray model. Even after watching NVR's outperformance through the crisis, competitors couldn't or wouldn't change their ways.

Of all the industries to get hit hard by the financial crisis, America's homebuilders may have been dealt the most crippling blow. Builders are still wrestling with the financial consequences of their decisions during the housing bubble, including the debt they amassed while gobbling up land. But the nation's fifth-biggest homebuilder sidestepped most of this drama. The crisis that destroyed so many became NVR's finest hour.

IX. The Business Model Deep Dive

IX. The Business Model Deep Dive

To truly understand NVR's revolutionary approach, you need to grasp the mechanics of option contracts—financial instruments that most homebuilders view as exotic but NVR treats as essential. These aren't complex derivatives traded on Wall Street; they're straightforward agreements that fundamentally alter the economics of homebuilding.

One Tegus expert noted that NVR doesn't exercise lot option contracts until the commitment is received, and even then, they wait to exercise until "3-4 days prior to actually going and digging a hole, breaking ground". Something like 90 days after the lot option is exercised and cash starts going out the door, the house is complete and remaining balances are paid. This timing precision transforms the traditional homebuilding cash cycle from years to months.

The option structure typically works like this: NVR identifies a parcel through a land developer, negotiates an option price (usually the full retail value of finished lots), pays a deposit of 5-7% to secure the option, and critically, sets specific contingencies that must be met before exercising. These contingencies include zoning approvals, infrastructure completion, market absorption rates, and even competitive dynamics. If any condition isn't met, NVR can walk away.

The working capital dynamics this creates are extraordinary. It also allows NVR to partially finance its balance sheet with customer deposits. When a buyer signs a purchase agreement, they typically put down 5-10% of the home price. This deposit sits on NVR's balance sheet as a liability, but it's also cash that can fund operations. By the time NVR exercises the land option and begins construction, customer deposits have already provided working capital.

The cash conversion cycle becomes negative—NVR collects money before spending it. While competitors tie up capital for years in land development, NVR's capital is working for mere months. This isn't just efficiency; it's a fundamental reimagining of homebuilding economics.

The three-brand strategy allows precise market segmentation without operational complexity. Ryan Homes' and Fox Ridge Homes' target market is first-time homebuyers and first-time move-up buyers while NVHomes and Heartland Homes focus more on move-up and discretionary buyers. But beneath these different facades lies the same operational engine—the same option contracts, the same build-to-order process, the same manufacturing efficiency.

Ryan Homes, representing roughly 90% of revenue, operates with remarkable standardization. Limited floor plans, predetermined options packages, and streamlined decision-making reduce complexity while maintaining enough customization to satisfy buyers. The average Ryan Homes buyer selects from perhaps 3-5 floor plans with predetermined elevation styles, choosing from a curated selection of finishes that have been pre-negotiated with suppliers.

NVHomes serves the luxury segment but maintains the same disciplined approach. While offering more customization and higher-end finishes, the fundamental model remains unchanged—no speculative building, no land ownership, no deviation from the formula. Even luxury buyers must commit and qualify for financing before construction begins.

The mortgage banking synergies through NVR Mortgage Finance represent another layer of integration without capital intensity. NVR Mortgage captures approximately 90% of NVR's homebuyers, generating fee income while maintaining intimate knowledge of buyer creditworthiness. This isn't just cross-selling; it's risk management. When your mortgage arm underwrites the buyer, you know exactly when to pull the trigger on construction.

NVR Settlement Services, the title and settlement arm, captures additional fee income while ensuring smooth closings. In 2023, these financial services operations generated approximately $150 million in revenue with minimal capital requirements. Pure fee income with strategic value—the perfect complement to the homebuilding operations.

The Building Products division, often overlooked by analysts, represents vertical integration without the traditional capital burden. Manufacturing roof trusses, floor trusses, wall panels, and stairs in controlled environments improves quality, reduces weather delays, and captures additional margin. But crucially, these facilities are leased, not owned, maintaining the asset-light philosophy even in manufacturing.

The pre-manufacturing process deserves deeper examination. Components are built in climate-controlled facilities with precision equipment, reducing defects and waste. Wall panels arrive on-site with electrical and plumbing rough-ins already complete. Stairs are delivered as finished units. This isn't just prefabrication; it's the industrialization of homebuilding, turning a craft business into a manufacturing business.

Quality control in the factories exceeds anything possible on a traditional job site. Lumber is stored in optimal conditions, preventing warping and moisture damage. Cuts are made with computer-controlled precision. Assembly follows standardized procedures with multiple inspection points. The result is higher quality at lower cost—a rare combination in any industry.

The subcontractor relationships in this model differ fundamentally from traditional homebuilding. Instead of maintaining permanent crews with high fixed costs, NVR uses independent subcontractors who are paid per house. This variabilizes what competitors treat as fixed costs. In downturns, NVR doesn't carry excess labor capacity. In upturns, they can scale rapidly by engaging more subcontractors.

But this isn't a purely transactional relationship. NVR's market dominance means steady work for subcontractors who perform. The company's predictable building schedule—enabled by the build-to-order model—allows subcontractors to plan their workforce efficiently. It's a symbiotic relationship where both parties benefit from the other's success.

The technology infrastructure supporting this model, while not flashy, is sophisticated. Real-time systems track option contracts, monitor land developer performance, coordinate manufacturing and delivery schedules, and manage the complex dance of getting the right materials to the right site at the right time. This isn't Silicon Valley-style disruption; it's operational excellence through systematic process improvement.

Customer relationship management starts before the first meeting. NVR's sales process is engineered to qualify buyers quickly, identifying serious purchasers from casual browsers. Sales consultants are trained to guide buyers toward decisions that fit both their needs and NVR's operational parameters. The goal isn't just a sale; it's a profitable sale that will close on schedule.

The pricing strategy embedded in the model provides another advantage. Because NVR locks in costs through option contracts and supplier agreements before setting home prices, they can price with precision. Competitors who own land purchased years earlier struggle to price appropriately in changing markets. NVR's real-time cost basis enables real-time pricing decisions.

X. Why Competitors Can't Copy

The question every investor asks: If NVR's model is so superior, why doesn't everyone copy it? The answer reveals deep truths about organizational psychology, industry culture, and the difficulty of change even when the benefits are obvious.

Like another one of our holdings, First Republic Bank, there's a cultural reason why competitors can't fully replicate NVR's strategy. Homebuilders typically start out as land developers and are therefore used to and drawn to the short-term, leveraged returns that the land speculation business can bring. This isn't just habit; it's identity. Asking a traditional homebuilder to give up land ownership is like asking a chef to give up knives.

The industry's addiction to land speculation runs deeper than economics—it's almost psychological. Land represents control, opportunity, and most seductively, the potential for enormous profits when markets rise. The siren song of buying land at $50,000 per lot and selling homes on that land when it's worth $100,000 per lot is irresistible to most builders. They see NVR paying current market prices for lots and think they're leaving money on the table.

The organizational antibodies against change are powerful. Consider a traditional homebuilder attempting to convert to NVR's model. The land development team—often the most powerful group in the organization—would effectively be eliminated. The executives who built careers on their ability to identify and acquire valuable land parcels would see their expertise devalued. The corporate culture that celebrates big land deals would need complete transformation.

Companies like NVR have long practiced an asset-light model, emerging from near-death financial crises with corporate mandates prohibiting them from holding extensive land inventories. Their success in navigating volatile markets with reduced risk profiles has cemented the asset-light approach as a hallmark of efficiency, productivity, and profitability within the industry. But this wasn't choice; it was necessity. And that origin story matters.

Wall Street's evolving view tells its own story. For years, analysts penalized NVR for its unconventional approach. The company was seen as an oddity, a survivor of bankruptcy that hadn't learned how "real" homebuilding worked. Analysts would discount NVR's multiple relative to peers, arguing that without land assets, the company lacked the upside potential of traditional builders.

But gradually, especially after 2008, the narrative shifted. What was once seen as weird became wise. What was once viewed as constraint became competitive advantage. Today, NVR trades at premium multiples, reflecting the market's recognition that predictable cash flows and high returns on capital are worth more than speculative land gains.

The recent industry shifts toward land-light models represent both validation and competition. Lennar is pivoting toward a long-anticipated shift: the transition to a land-light, asset-light business model through its Millrose spin-off... Lennar's Millrose spin-off strategy, revealed during its Q3 2024 earnings call, represents a profound shift for the company. After decades of operating as a traditional homebuilder, Lennar is attempting to have its cake and eat it too—maintaining a land development capability while moving toward an asset-light model.

D.R. Horton's approach with Forestar represents another variant. Rather than eliminating land development, they've separated it into a distinct entity that sells finished lots to D.R. Horton and other builders. It's a halfway measure that acknowledges the benefits of the land-light model while maintaining some control over land supply.

But these conversions face massive implementation challenges. Lennar and D.R. Horton have decades of organizational muscle memory around land acquisition and development. They have billions in existing land assets that must be worked through. They have relationships with investors who expect them to act like traditional homebuilders. Changing direction is like turning an aircraft carrier—possible, but slow and difficult.

The risk management implications of model change create additional barriers. A traditional homebuilder moving to land-light must essentially abandon its core competency and develop new ones. The transition period is fraught with danger—too fast, and you lack the capabilities to execute the new model; too slow, and you get stuck between two models, executing neither well.

The capital allocation discipline required for NVR's model represents another barrier. Traditional homebuilders are growth-oriented, measuring success by units built and revenue generated. NVR measures success by return on capital and cash generation. This isn't just a different metric; it's a different philosophy that permeates every decision from land acquisition to product design to geographic expansion.

The investor base expectations create their own constraints. NVR's shareholders have self-selected for those who value capital efficiency and risk management. Traditional homebuilder shareholders often want growth and geographic expansion. Changing models means potentially changing your entire shareholder base—a risk many management teams won't take.

Even when competitors attempt to copy elements of NVR's model, execution often falls short. Using options requires discipline to walk away from deals when conditions aren't met. Build-to-order requires resisting the temptation to spec build when markets heat up. Capital return requires saying no to acquisitions that could boost revenues but hurt returns. Every element of the model requires doing less when instinct says do more.

The manufacturing and operational capabilities NVR has built over decades can't be replicated overnight. The relationships with land developers who trust NVR to perform on option contracts took years to establish. The systems and processes that enable 90-day construction cycles were refined through thousands of iterations. These aren't strategies you can copy; they're capabilities you must build.

Perhaps most fundamentally, NVR's model requires accepting lower revenues and fewer units built in exchange for higher returns and lower risk. In an industry where size has traditionally equated to success, this trade-off is culturally unacceptable to many organizations. CEOs want to run bigger companies, not more profitable ones. Investment bankers want to finance larger deals, not more efficient operations.

XI. Financial Performance & Stock Market Returns

The stock chart of NVR from October 1994 to today looks like something from a different universe. NVR reached its all-time high on Oct 18, 2024 with the price of 9,964.77 USD, and its all-time low was 5.13 USD and was reached on Oct 5, 1994. That's not a typo—from $5.13 to nearly $10,000 per share, a return that transforms every $1,000 invested at the low into nearly $2 million today.

But raw stock performance only tells part of the story. The consistency of operational excellence behind those returns reveals the true miracle. By avoiding the capital intensive and multi-year process of land development, NVR has been able to generate returns-on-equity (ROE) of 20 to 40% over the long term, 2x to 3x better than most of its large homebuilder competitors. These aren't cherry-picked numbers from boom years; they're sustained performance through multiple cycles.

The margin stability through cycles defies industry norms. These factors, combined with NVR's use of land purchase agreements, have led to average operating margins of 9.7% over the last five years and operating margins of 10.4% in 2013. While competitors see margins compress in downturns and expand in upturns, NVR maintains remarkable consistency. This predictability allows for better planning, more confident capital allocation, and ultimately, higher multiples from investors who value stability.

The current financial snapshot reveals a business at peak performance. Reporting a remarkable net income of approximately $1.76 billion on revenues nearing $10.55 billion for the fiscal year ending 2023... with a strong market capitalization often exceeding $25 billion in early 2024. Think about the mathematics here: a 16.7% net margin in homebuilding, an industry where 5% is considered good and 10% is exceptional.

The return on equity story deserves deeper examination. In 2023, NVR generated a 45% ROE. To put this in perspective, the average S&P 500 company generates roughly 15% ROE. Warren Buffett has said that a 20% ROE sustained over time is exceptional. NVR has exceeded 20% ROE for most of the past two decades, including during the financial crisis.

The free cash flow generation is perhaps even more impressive than reported earnings. Because NVR requires minimal capital investment to grow, nearly all earnings convert to free cash flow. Over the past decade, NVR has generated cumulative free cash flow of over $10 billion while maintaining and growing its market position. This cash generation funds the buyback machine that has reduced shares outstanding from 7.6 million in 2005 to approximately 3.1 million today.

The balance sheet strength provides the foundation for everything else. As of the latest quarter, NVR has minimal debt, over $2 billion in cash and equivalents, and working capital that often runs negative due to customer deposits. This isn't just a strong balance sheet; it's a fortress balance sheet that can withstand any conceivable housing downturn.

The per-share metrics tell the story of intelligent capital allocation. While revenues have grown modestly—from about $5 billion in 2005 to $10.5 billion in 2023—earnings per share have exploded from roughly $90 to over $550. This five-fold increase in EPS while revenues merely doubled demonstrates the power of combining operational excellence with aggressive share buybacks.

The valuation metrics reflect the market's recognition of quality. NVR trades at approximately 15 times earnings, a premium to most homebuilders but a discount to high-quality industrials with similar returns on capital. The enterprise value to EBITDA ratio of roughly 12 times similarly suggests the market values NVR more like a stable industrial than a cyclical homebuilder.

The dividend policy—or lack thereof—remains controversial but logical. By retaining all earnings for buybacks rather than paying dividends, NVR maximizes tax efficiency for shareholders. A dollar used for buybacks increases the value of remaining shares without creating a taxable event. A dollar paid in dividends is immediately taxable to recipients. For long-term shareholders, the mathematics overwhelmingly favor buybacks.

The geographic revenue mix provides insights into performance drivers. The Washington D.C. metro area, still generating over 20% of revenues, remains the cash cow that funds expansion elsewhere. But growth is coming from newer markets—the Carolinas, Florida, and secondary metros where NVR is gaining share. This diversification within concentration strategy reduces dependence on any single market while maintaining operational efficiency.

The product mix evolution shows adaptation without abandoning discipline. While Ryan Homes still dominates revenues, the average selling price has increased from roughly $250,000 in 2010 to over $450,000 today. This isn't just inflation; it's a deliberate move upmarket as first-time buyers get priced out and move-up buyers become the primary customer base.

The mortgage banking contribution, while small in absolute terms, provides outsized returns on capital. With minimal capital requirements, NVR Mortgage generates roughly $50 million in annual profit—a 100%+ return on invested capital. These financial services provide both strategic value and financial returns that exceed the homebuilding operations.

Comparing NVR's stock performance to peers over various timeframes reveals consistent outperformance. Over the past 20 years, NVR has generated annual returns of approximately 18%, compared to 11% for the broader homebuilding sector and 10% for the S&P 500. But the path to those returns matters—NVR achieved them with lower volatility and smaller drawdowns than competitors.

The institutional ownership structure reflects quality recognition. Major shareholders include Wellington Management, BlackRock, and other blue-chip investment firms that typically avoid cyclical homebuilders. The insider ownership, particularly by long-tenured executives, aligns management with shareholders in pursuing long-term value creation over short-term earnings management.

XII. Bull vs Bear Case & Future Outlook

The Bull Case:

The housing shortage fundamentals in the United States present a generational opportunity for disciplined operators like NVR. Years of underbuilding following the financial crisis have created a structural deficit estimated at 3-5 million homes. Millennial household formation is accelerating just as Baby Boomers age in place rather than downsizing. This supply-demand imbalance isn't a cycle—it's a secular trend that could persist for a decade or more.

Geographic expansion opportunities remain substantial despite NVR's already impressive presence. With only a 2% market share of the U.S home construction industry overall, we believe NVR can more than triple its current size by expanding geographically. The company's methodical market entry strategy—proven in Nashville, Charlotte, and other recent additions—can be replicated in dozens of secondary metros across the South and Midwest.

The market share gains in existing markets show no signs of slowing. In Philadelphia, NVR grew from 6% share to nearly 28% over two decades. Similar stories are playing out in every market they enter. The combination of operational excellence, financial strength, and brand reputation creates a flywheel effect where success breeds more success.

Capital allocation optionality provides multiple paths to value creation. With billions in free cash flow generation ahead, management can choose between accelerating buybacks at attractive prices, making strategic acquisitions if the land-light model spreads and creates targets, or even initiating a dividend if tax laws change to favor income over capital gains. This flexibility is valuable in an uncertain world.

The competitive landscape is actually improving for NVR despite attempts at imitation. As competitors struggle to transition to asset-light models, they're caught between strategies—neither executing their traditional model well nor successfully copying NVR. This transition period creates opportunities for NVR to gain share and acquire talent from struggling competitors.

Interest rate normalization could accelerate demand. After the spike in mortgage rates to over 7% in 2023, any decline toward historical norms of 4-5% would unleash pent-up demand from buyers who've been waiting on the sidelines. NVR's build-to-order model positions them perfectly to capture this demand without taking inventory risk.

The Bear Case:

The geographic concentration risks are real and growing. The company's geographic concentration along the Mid-Atlantic and Eastern U.S. regions leaves it vulnerable to localized economic downturns or regulatory shifts that could disproportionately impact sales volumes and profitability. Climate change impacts, from hurricanes to flooding, disproportionately affect the Eastern seaboard where NVR operates.

Rising mortgage rates and affordability challenges threaten the entire housing market. With median home prices at historic highs relative to median incomes, and mortgage rates well above recent lows, monthly payments have become unaffordable for many buyers. NVR's exposure to first-time buyers through Ryan Homes makes them particularly vulnerable to affordability constraints.

Option contract availability in new markets represents a hidden challenge. NVR's model depends on land developers willing to sell options rather than finished lots. In new markets without established relationships, developers may resist this structure, forcing NVR to either compromise its model or forego expansion opportunities.

Management succession questions loom large. While the transition from Schar to Saville to Bredow has been smooth so far, the cultural DNA that makes NVR special could be diluted over time. The next generation of leadership may not have the scar tissue from 1992 that created the discipline. Success itself could breed complacency.

The competitive response is intensifying. Lennar's Millrose spinoff and D.R. Horton's Forestar represent serious attempts to replicate elements of NVR's model. While execution challenges remain, these competitors have the scale and resources to eventually succeed. If the entire industry moves toward land-light models, NVR's competitive advantage erodes.

Regulatory risks are evolving in concerning ways. Impact fees are rising across NVR's markets. Zoning restrictions are tightening in response to NIMBY pressures. Environmental regulations are adding costs and delays. Labor shortages are driving wage inflation that can't always be passed to buyers. These headwinds affect all builders but could disproportionately impact NVR's concentrated operations.

The macroeconomic environment presents multiple threats. A recession would obviously hurt housing demand, but even continued growth with inflation could be problematic if the Federal Reserve maintains higher rates to combat price pressures. The narrow path between recession and inflation leaves little room for error.

Technology disruption, while often overhyped, could eventually matter. Companies like Icon are 3D printing homes. Modular builders like Boxabl promise radical cost reductions. While these technologies haven't scaled yet, a breakthrough could disrupt traditional builders. NVR's manufacturing capabilities provide some protection, but radical innovation could change the game entirely.

The valuation already reflects significant optimism. At 15 times earnings and with the stock near all-time highs, NVR needs to execute flawlessly to justify current prices. Any operational stumble, market downturn, or competitive pressure could lead to multiple compression that overwhelms operational performance.

XIII. Playbook: Key Business Lessons

The first and perhaps most powerful lesson from NVR's journey is that crisis can be the greatest catalyst for innovation. As an unintended consequence, NVR was forced to deal with an asset-light model 30 years ago. What seemed like catastrophe—bankruptcy that wiped out shareholders and nearly destroyed the company—became the forcing function for reimagining the entire business model. Without the crisis of 1992, NVR would likely be just another leveraged homebuilder today.

The power of saying no emerges as a defining characteristic. What NVR doesn't do is as important as what it does. They don't speculate on land. They don't build spec homes. They don't chase hot markets. They don't make transformative acquisitions. They don't pay dividends. In a world that celebrates activity, NVR has built enormous value through disciplined inactivity.

Capital allocation as competitive advantage transcends industry boundaries. While competitors focus on operational metrics like units built or margins achieved, NVR focuses relentlessly on return on capital. This isn't just measurement; it's philosophy. Every decision—from market entry to product design—is evaluated through the lens of capital efficiency. Over time, this discipline compounds into insurmountable advantage.

Building culture that survives leadership transitions represents organizational alchemy. From Schar to Saville to Bredow, NVR has maintained its core DNA while adapting to new challenges. This isn't accident; it's architecture. The company systematically promotes from within, ensures potential leaders experience multiple functions, and most importantly, selects for cultural fit over pure talent.

Why being different is more important than being better challenges conventional strategy. NVR doesn't build better homes than competitors—they build them differently. The homes themselves are comparable to what Lennar or D.R. Horton produces. But the business model wrapped around those homes is fundamentally different. In competitive markets, differentiation trumps marginal improvement.

The paradox of slow growth creating superior returns confounds traditional thinking. NVR grows revenues slowly, expands geographically methodically, and often builds fewer homes than competitors. Yet they generate superior returns for shareholders. This isn't despite the slow growth—it's because of it. By growing within their capabilities rather than beyond them, NVR maintains the discipline that creates value.

Constraints breed creativity in ways abundance never can. NVR's prohibition on land ownership forced innovation in supplier relationships, customer management, and operational efficiency. Without the option to solve problems with capital, they had to solve them with intelligence. These capability advantages persist even after the constraints that created them are removed.

The value of institutional memory cannot be overstated. Having executives who lived through 1992 created a visceral understanding of risk that no amount of education could provide. This shared experience became shared wisdom, transmitted through stories and embedded in processes. Companies that forget their history are doomed to repeat it.

Simplicity scales better than complexity. NVR's model is sophisticated but not complicated. Option contracts are simple to understand. Build-to-order is a straightforward concept. The power comes from consistent execution rather than clever innovation. While competitors add complexity through financial engineering or elaborate strategies, NVR keeps things simple and does them well.

The customer isn't always right—but the right customer is gold. NVR doesn't try to serve everyone. They explicitly filter for customers who can qualify for mortgages and will follow their process. This selectivity seems restrictive but actually enables the entire model. By saying no to marginal customers, they can say yes to efficiency.

Vertical integration without capital intensity squares the circle. NVR's manufacturing operations provide integration benefits without the typical capital requirements. By leasing facilities and maintaining flexibility, they capture value without capturing risk. This hybrid approach—neither fully integrated nor fully outsourced—optimizes for both efficiency and flexibility.

Trust is the ultimate currency in cyclical industries. NVR's reputation for closing on option contracts, paying suppliers promptly, and treating stakeholders fairly becomes a competitive advantage in downturns when trust is scarce. This reputation took decades to build and would take moments to destroy—a asymmetry that enforces continued good behavior.

The importance of aligned incentives extends beyond executive compensation. From sales consultants compensated on closed homes rather than signed contracts, to subcontractors paid promptly for quality work, to land developers who know NVR will perform—everyone in the ecosystem benefits from NVR's success. This alignment creates a network effect where all participants want NVR to win.

XIV. Epilogue & Reflections

The journey from bankruptcy to blue chip seems almost mythical in its improbability. A company that in 1992 was days away from liquidation now trades at nearly $10,000 per share, making it one of the most expensive stocks in America. But this isn't a story about luck or timing—it's about the transformative power of learning from failure and having the courage to be different.

What NVR teaches us about resilience and reinvention extends far beyond homebuilding. Every industry has its orthodoxies, its "way things are done." NVR's example shows that challenging these assumptions, especially when forced by circumstances, can create extraordinary value. The company didn't succeed despite its bankruptcy—in many ways, it succeeded because of it.

The homebuilding industry's future increasingly looks like NVR's present. The attempted transitions by Lennar and D.R. Horton suggest the land-light model will eventually become table stakes. But first-mover advantages in business model innovation can persist for decades. NVR has a 30-year head start in understanding how to operate without land, manage option contracts, and maintain discipline through cycles.

The greatest surprise from researching NVR isn't the stock performance or the financial metrics—it's the boringness of it all. No breakthrough technology. No charismatic founder with a reality distortion field. No viral marketing campaigns. Just disciplined execution of a simple model, repeated thousands of times, compound over decades. In a world obsessed with disruption, NVR proves that consistency can be revolutionary.

The sustainability of NVR's competitive advantages seems paradoxical—they're both obvious and impossible to copy. Everyone can see what NVR does differently. The playbook is hidden in plain sight in their public filings. Yet three decades after their transformation, they remain the only major builder fully committed to the land-light model. This suggests their advantages stem not from secrets but from discipline, culture, and capabilities that take decades to build.

Looking forward, NVR faces the challenge every successful company eventually confronts: the enemy of great is good. When you're generating 40% returns on equity and your stock is at all-time highs, the temptation to coast is powerful. But markets are dynamic, competitors are adapting, and customer needs are evolving. NVR's continued success will require the same paranoia and discipline that enabled their resurrection.

The broader implications for investors are profound. NVR demonstrates that sector doesn't determine destiny—business model does. A homebuilder can generate software-like returns. A cyclical company can produce stable cash flows. A capital-intensive industry can be operated with minimal capital. These inversions challenge fundamental assumptions about investing and suggest opportunities hide where conventional wisdom says they can't exist.

Perhaps the most enduring lesson is about the nature of competitive advantage itself. NVR's moat isn't technology that can be obsoleted or brand that can be tarnished or scale that can be matched. It's culture, discipline, and learned behavior—intangible assets that compound over time and become stronger with use. In an age of rapid change, these slow-moving advantages might be the most valuable of all.