PNC Financial Services: From Pittsburgh Trust to National Banking Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's October 24, 2008, the darkest days of the financial crisis. Lehman Brothers collapsed five weeks ago. Markets are in freefall. Banks are failing weekly. In Pittsburgh, PNC's leadership team gathers in their boardroom overlooking the three rivers. They've just received $7.7 billion in TARP funds from the Treasury—money meant to shore up their balance sheet and prevent systemic collapse. Within hours, they'll deploy $5.2 billion of it to acquire Cleveland's National City Corp, a wounded giant with $150 billion in assets. The audacity is breathtaking. While others hoard cash, PNC goes shopping.

That moment encapsulates everything about PNC Financial Services Group—strategic patience erupting into decisive action, crisis as opportunity, and the methodical construction of an American banking powerhouse through forty years of disciplined acquisitions. Today, PNC stands as America's fifth-largest bank with over $560 billion in assets, operating across 27 states and Washington D.C., with 2,629 branches and 9,523 ATMs. But this isn't a story about size—it's about strategy.

How does a post-Civil War Pittsburgh savings bank transform into a coast-to-coast financial giant? Through what might be the most disciplined M&A playbook in American banking. While JPMorgan and Bank of America grew through massive, transformative deals, PNC perfected the art of the strategic bolt-on—over 40 acquisitions since 1983, each one expanding territory, capabilities, or market share with surgical precision.

The themes that emerge are fascinating: geographic patience (waiting decades for the right southeastern expansion), technology foresight (consolidating platforms in 1990 when peers ran dozens), and crisis opportunism (the National City and BBVA USA deals both came during market turmoil). There's also a darker thread—the TARP controversy that still shadows the company's reputation in Cleveland, where using government bailout funds to eliminate a hometown bank left lasting scars.

What makes PNC particularly relevant today? In an era of fintech disruption and digital-first banking, PNC represents something different—a Main Street banking model that's proven remarkably resilient. While Citigroup and Wells Fargo stumbled through scandals, while regional peers like Silicon Valley Bank and First Republic imploded, PNC kept grinding out consistent returns through disciplined underwriting and diversified revenue streams.

This is ultimately a story about compound advantages—how forty years of smart acquisitions, technology investments, and geographic expansion create a moat that's wider than it appears. It's about understanding when banking consolidation creates value versus when it destroys it. And it's about CEO William Demchak's vision to challenge the Big Four banks not through size alone, but through focused execution in the markets that matter most.

We'll trace this journey from two nineteenth-century Pennsylvania banks through the landmark 1983 merger that created PNC, the acquisition spree that followed, the controversial National City deal, and finally the 2021 BBVA USA acquisition that completed the coast-to-coast footprint. Along the way, we'll examine what PNC's playbook teaches about serial acquisition, why regional banking economics still matter, and whether this Pittsburgh powerhouse can truly compete with the Wall Street giants.

II. Origins & The Two Pennsylvania Banks

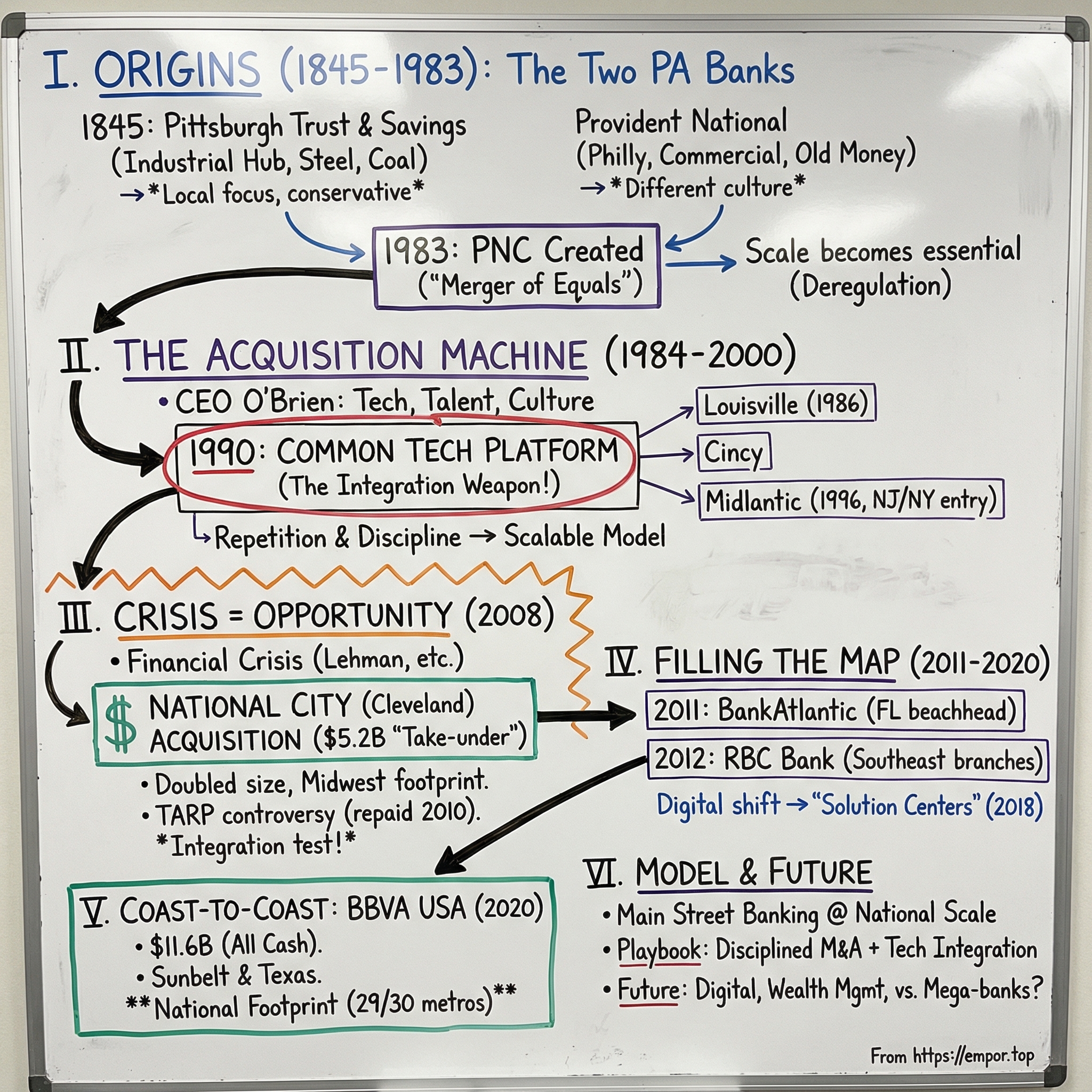

The story begins not in gleaming corporate towers but in the soot and smoke of industrial Pennsylvania. On April 10, 1845, a group of Pittsburgh merchants and industrialists gathered to charter the Pittsburgh Trust and Savings Company. Their timing proved catastrophic. Before the bank could open its doors, the Great Fire of Pittsburgh swept through the city on April 10, 1845—the very day of their charter—destroying a third of the city and delaying operations for seven years. When the bank finally opened on January 28, 1852, it embodied Pittsburgh's industrial resilience: rebuilt from ashes, ready to finance the steel mills and railroads that would forge modern America.

Pittsburgh in the 1850s was transforming from river trading post to industrial powerhouse. Andrew Carnegie hadn't yet built his steel empire, but the ingredients were assembling—coal from nearby mines, iron ore floating down from Lake Superior, and ambitious immigrants flooding in for factory work. Pittsburgh Trust and Savings positioned itself as the banker to this transformation, financing everything from bridge construction to steel mill expansion. The bank's early ledgers read like an industrial revolution roster: loans to foundries, coal operators, railroad companies.

Meanwhile, 300 miles east in Philadelphia, a different banking culture was emerging. The City of Brotherly Love had been America's financial capital before New York's ascendance, and its banks reflected old-money conservatism mixed with Quaker prudence. Provident Trust Company, formed in 1957 from the merger of the original Provident Trust Company and Provident Tradesmens Bank and Trust Company, embodied this Philadelphia ethos—steady, conservative, focused on wealth preservation for the city's established families rather than financing risky industrial ventures.

The contrast between these two banking cultures would later prove complementary. Pittsburgh banks learned to evaluate industrial risk, understanding cash flows from steel production and manufacturing cycles. Philadelphia banks mastered trust services, estate planning, and the steady accumulation of deposits from a more diversified economy. One chased growth through industrial lending; the other built stability through diversified services.

The 1930s brought these differences into sharp relief. As the Depression strangled credit nationwide, Pittsburgh's First National Bank didn't retreat but instead partnered with Peoples-Pittsburgh Trust Company to finance municipal improvements. While other banks called in loans, these Pittsburgh institutions funded public works projects, understanding that keeping the steel mills running and workers employed would ultimately protect their loan portfolios. It was counter-cyclical thinking that would echo through PNC's later crisis strategies.

By the 1970s, both Pittsburgh National Corporation and Provident National Corporation had grown into regional powerhouses through local acquisitions. Pittsburgh National had assembled a network across western Pennsylvania's industrial corridor. Provident National dominated southeastern Pennsylvania's more diversified economy. But state banking laws kept them caged—Pennsylvania banks couldn't branch freely even within state borders until 1982, creating a patchwork of local fiefdoms rather than statewide institutions.

The industrial context matters here. Pennsylvania's dual-city structure—Pittsburgh's heavy industry versus Philadelphia's diversified commerce—created two distinct banking ecosystems. Pittsburgh banks became experts at riding commodity cycles, understanding that steel demand drove everything from real estate values to retail sales. Philadelphia banks developed broader expertise—healthcare, education, professional services. Neither could claim statewide dominance, but together they covered Pennsylvania's economic spectrum.

This geographic and cultural divide might have persisted indefinitely. But 1982's banking deregulation changed everything. Suddenly, Pennsylvania banks could operate statewide. The race was on to build scale before out-of-state competitors arrived. For Pittsburgh National and Provident National, the logic was inescapable: merge or be acquired. Their combination would create not just Pennsylvania's largest bank but a platform for national expansion. The industrial age of Pennsylvania banking was ending; the acquisition age was about to begin.

III. The Historic 1983 Merger: Birth of PNC

The regulatory dam burst in 1982. Pennsylvania's new banking legislation didn't just permit statewide branching—it signaled that interstate banking was coming. Bank executives across America understood the implications: consolidate or die. In Pittsburgh and Philadelphia boardrooms, strategic planners ran the same calculations: who could we buy, who might buy us, and how quickly could out-of-state giants like Citigroup or Bank of America move in?

Thomas O'Brien, then president of Pittsburgh National Corporation, saw opportunity where others saw threat. At 46, O'Brien was young for a bank president, ambitious, and convinced that Pennsylvania needed a champion bank before New York and Charlotte giants carved up the territory. His counterpart at Provident National, William Adams, shared the vision but from a different angle—he wanted to preserve Philadelphia's banking independence while gaining scale to compete.

The first meeting between the two banks happened in neutral territory—a Harrisburg hotel, halfway between the cities, in March 1983. O'Brien brought maps showing Pittsburgh National's western Pennsylvania dominance; Adams countered with Provident's southeastern strength. Together, they controlled complementary halves of America's second-largest state. The strategic fit was obvious, but cultural differences loomed. Pittsburgh bankers wore steel-toed boots to mill visits; Philadelphia bankers attended orchestra galas. Could these cultures merge?

The numbers made cultural concerns secondary. Combined, they would create a $10.3 billion institution—the largest bank merger in American history at that time. The deal terms reflected careful balance: technically a merger of equals with shared governance, though Pittsburgh National was slightly larger. The name itself became a diplomatic masterstroke—PNC Financial Corp, taking the shared initials of both holding companies. Neither city could claim victory; both could claim ownership.

But the real brilliance lay in the integration strategy. Rather than force one culture onto the other, they created a federated model—centralized technology and risk management, but localized decision-making. Pittsburgh branches kept lending to steel companies; Philadelphia branches maintained their trust business. The first joint board meeting revealed the wisdom: when Pittsburgh directors worried about industrial loan exposure, Philadelphia's diversified portfolio provided comfort. When Philadelphia directors questioned expansion costs, Pittsburgh's growth trajectory justified investment.

Leadership succession proved trickier. Merle Gilliand became the first CEO, but the arrangement felt transitional. The real power dynamics emerged in 1985 when Thomas O'Brien took over at age 48, becoming the youngest CEO of any major U.S. bank. O'Brien brought a different energy—less banker, more strategist. He'd studied every major bank merger of the previous decade, cataloguing what worked and what didn't. His conclusion: successful consolidation required three things—technology standardization, cultural patience, and geographic discipline.

The technology piece came first. While competitors ran separate systems for each acquired bank—Chemical Bank famously operated 17 different platforms—O'Brien insisted on immediate consolidation. Every PNC customer would use the same systems, see the same products, experience the same service. It cost millions upfront but would save hundreds of millions over time. More importantly, it sent a message: PNC wasn't assembling banks, it was building one bank.

The cultural patience manifested in retention strategies. Rather than wholesale layoffs, PNC identified top performers from both legacy banks and gave them expanded roles. A Philadelphia trust officer might suddenly oversee western Pennsylvania wealth management. A Pittsburgh commercial lender could run mid-Atlantic corporate banking. This cross-pollination broke down tribal boundaries while preserving institutional knowledge.

Geographic discipline meant resisting empire-building temptations. When Florida banks came up for sale, O'Brien passed—too far from the core footprint. When New York institutions beckoned, he demurred—too expensive, too competitive. Instead, PNC would expand in concentric circles from Pennsylvania, building density before seeking distance. It wasn't sexy, but it was smart.

The first year's results validated the strategy. Cost savings hit 15% faster than projected. Cross-selling between commercial and trust divisions exceeded targets. Credit losses stayed below peer averages despite industrial Pennsylvania's struggles. Wall Street noticed—PNC's stock outperformed money center banks despite being a regional player. The template was set: disciplined acquisition, patient integration, strategic focus. Over the next two decades, PNC would execute this playbook dozens of times, building America's most successful serial acquirer. But first, they had to prove the model could work beyond Pennsylvania.

IV. The Acquisition Machine: 1984–2000

Thomas O'Brien's first acquisition as CEO wasn't supposed to happen. In 1986, federal regulators had just begun allowing interstate banking through regional compacts, and Citizens Fidelity Corporation of Louisville, Kentucky, was being courted by larger suitors. Fifth Third Bank seemed the logical buyer—already dominant in Ohio, expanding south. But O'Brien saw something others missed: Citizens Fidelity's trust business perfectly complemented PNC's commercial lending, and Louisville's position as a distribution hub for the upper South created geographic optionality.

The pursuit of Citizens Fidelity revealed O'Brien's acquisition methodology. While competitors focused on size and immediate cost synergies, PNC evaluated three criteria: does it strengthen our competitive position in existing markets or give us platform value in new ones? Can we integrate it within 18 months without disrupting customer relationships? Will it be accretive to earnings within two years without excessive cost-cutting? If any answer was no, they walked away. O'Brien famously killed deals on conference calls when due diligence revealed integration complexities, earning a reputation for discipline that sometimes frustrated investment bankers but delighted shareholders.

Between 1986 and 1990, PNC executed a series of surgical strikes—Central Bancorporation of Cincinnati, expanding their Ohio presence; Bank of Delaware Corporation, providing mid-Atlantic density; Marine Bancorp of Erie, filling a geographic gap between Pittsburgh and Buffalo. None were transformative individually, but collectively they created something powerful: a true super-regional footprint from Kentucky to New York's southern tier.

The 1990 decision to consolidate technology platforms across all acquisitions proved prescient. While NationsBank (later Bank of America) struggled with systems integration through the decade, PNC could absorb new banks in months, not years. A single platform meant single training programs, unified product sets, consistent risk management. When they acquired a bank on Friday, customers saw PNC products by Monday. The efficiency was staggering—integration costs ran 40% below industry averages.

Then came the deal that changed everything: Midlantic Corporation in 1996. At $30 billion in assets, Midlantic was PNC's largest acquisition yet, with dominant positions from southern New Jersey through the Washington D.C. suburbs. But Midlantic was struggling—bad real estate loans, bloated costs, regulatory scrutiny. Other bidders saw a fixer-upper requiring massive restructuring. O'Brien saw opportunity.

The Midlantic integration became PNC's masterpiece. Rather than slash costs immediately, they first stabilized the credit portfolio, working through problem loans methodically. They retained Midlantic's best commercial bankers but imported PNC's credit culture. Within 18 months, they'd cut operating expenses by 35% while actually growing revenues through cross-selling PNC products to Midlantic's customer base. The New York metro presence—Midlantic's northern New Jersey branches—gave PNC access to America's largest banking market without paying Manhattan prices.

Between 1991 and 1996, PNC acquired more than ten smaller banks, but these weren't random purchases. Each filled a specific gap—First Eastern in northeastern Pennsylvania, Northeastern Bancorp in western New York, Chemical Banking's Massachusetts branches. O'Brien called it "string of pearls" strategy—each acquisition small enough to digest easily but positioned to create continuous market presence. By 1996, you could drive from Louisville to Albany and never leave PNC's footprint.

The discipline extended to what PNC didn't buy. When CoreStates went on the block in 1997—a massive Philadelphia bank that would have doubled PNC's size—O'Brien passed despite board pressure. His analysis: too much overlap with existing Pennsylvania operations, too many problem assets, integration complexity off the charts. First Union bought CoreStates instead and spent five years struggling with integration. O'Brien's restraint looked like genius.

By 2000, PNC had transformed from a Pennsylvania bank into a Mid-Atlantic powerhouse with $70 billion in assets. But O'Brien recognized that banking itself was transforming. Customers wanted investment services, insurance products, sophisticated treasury management. Pure commercial banking wasn't enough. The company's name change to PNC Financial Services Group in 2000 signaled this evolution—no longer just a bank but a diversified financial services company.

The acquisition machine had created something unique: a bank with national scale but regional focus, sophisticated capabilities but Main Street sensibilities, aggressive growth but conservative underwriting. While Citigroup chased global ambitions and Bank of America pursued nationwide retail dominance, PNC carved out a different niche—the premier financial institution for mid-sized businesses and affluent individuals in America's industrial heartland. It was profitable, defensible, and about to be tested by the greatest financial crisis since the Depression.

V. The National City Acquisition: Crisis Creates Opportunity (2008)

By summer 2007, National City CEO Peter Raskind still believed his bank could weather the subprime storm. Headquartered in Cleveland's historic National City Center, the 163-year-old institution had survived the Depression, the S&L crisis, and the Rust Belt's deindustrialization. With $150 billion in assets across Ohio, Michigan, Indiana, and Illinois, National City ranked as America's eighth-largest bank. But Raskind had made a fatal bet: aggressive expansion into Florida real estate just as the housing bubble peaked. By March 2008, with mortgage defaults cascading through their $40 billion residential portfolio, National City's stock had fallen 80%.

Jim Rohr, who'd succeeded O'Brien as PNC's CEO in 2000, watched National City's deterioration with keen interest. Rohr was different from his predecessor—an accountant by training, methodical where O'Brien was visionary, but equally disciplined about acquisition criteria. For years, he'd wanted entry into the Midwest's industrial markets. National City's footprint was perfect; their balance sheet was toxic. The question wasn't whether National City would sell, but to whom and when.

The courtship began quietly in July 2008. Wells Fargo expressed interest first, seeing National City as their entry to the Midwest. Fifth Third Bank, based in Cincinnati, offered to move their headquarters to Cleveland to win political support. KeyBank, Cleveland's other major bank, explored a hometown merger. But each potential buyer faced the same problem: how to absorb $15 billion in projected loan losses without destroying their own capital ratios?

Then came September 15, 2008: Lehman Brothers collapsed. The financial system froze. Credit markets shut down. Within weeks, Washington Mutual failed, Wachovia teetered, and Morgan Stanley nearly fell. Treasury Secretary Hank Paulson and Federal Reserve Chairman Ben Bernanke scrambled to prevent systemic collapse. Their solution: the Troubled Asset Relief Program (TARP), injecting capital directly into banks to shore up balance sheets.

On October 13, Paulson summoned nine major bank CEOs to Treasury, including Rohr. The message was stark: take TARP funds whether you need them or not. System stability required universal participation. PNC received $7.7 billion—money Rohr hadn't requested and didn't particularly need given PNC's conservative underwriting. But within hours of leaving Treasury, Rohr called his board with a radical proposal: use the TARP funds to acquire National City.

The speed was breathtaking. On October 23, National City's board met in emergency session. Their stock had fallen below $2; the FDIC was preparing seizure plans. Raskind had personally petitioned for TARP funds but been rejected—regulators deemed National City too weak to save. At 4 PM, PNC's offer arrived: $5.2 billion in stock, roughly $2.23 per share. Fifth Third's competing bid had collapsed. Wells Fargo wanted more time. PNC demanded an answer by midnight.

The Cleveland Plain Dealer would later call it a "take-under"—a price below even National City's depleted market value. But National City's board had no alternative. Bankruptcy meant shareholders got zero; at least PNC offered something. At 11:47 PM, they voted to accept. The announcement came Friday morning, October 24: PNC would acquire National City, creating America's fifth-largest bank with $290 billion in assets.

The public reaction was explosive. How could PNC use taxpayer TARP funds—money meant to increase lending—to eliminate a competitor? Representative Dennis Kucinich of Cleveland called for Congressional hearings. National City employees protested outside PNC branches. Editorial pages condemned "disaster capitalism" and "corporate welfare." The optics were terrible: Pittsburgh bank uses government money to destroy Cleveland rival.

Rohr's defense was purely economic. Without acquisition, National City would fail, devastating the Midwest's credit markets. PNC's purchase preserved customer relationships, maintained lending capacity, and saved the FDIC billions in resolution costs. Yes, they'd cut costs—14,000 jobs ultimately—but they'd also inject capital, stabilize operations, and maintain branches that would otherwise close. It was creative destruction at massive scale.

The integration challenges dwarfed anything PNC had previously attempted. National City wasn't just bigger than prior acquisitions; it was broken. Their loan portfolio required line-by-line review. Their technology systems were antiquated. Their culture, after months of crisis, was demoralized. PNC deployed 500 managers to Cleveland, Detroit, and Chicago, conducting triage on everything from commercial relationships to branch leases.

The proximity of Cleveland to Pittsburgh created unique tensions. These weren't distant markets where redundancy was minimal. Cleveland and Pittsburgh branches sometimes sat blocks apart. Corporate clients often had relationships with both banks. The cuts were surgical but brutal—downtown Cleveland lost 2,000 finance jobs, Pittsburgh saw 1,200 positions eliminated. Entire departments vanished. National City's mortgage division, once 5,000 strong, essentially disappeared.

But Rohr also made strategic investments. PNC kept National City's middle-market commercial banking team largely intact, recognizing their Midwest relationships were irreplaceable. They maintained the Cleveland headquarters as a major operational hub. They honored all customer deposits and most commercial credit lines. By 2010, when PNC repaid their TARP funds—using proceeds from selling their Global Investment Servicing division to BNY Mellon—the combined institution was solidly profitable.

The National City acquisition transformed PNC from super-regional to quasi-national. Suddenly they had top-three market share in Pittsburgh, Cleveland, Cincinnati, Columbus, Detroit, and Indianapolis. Their commercial banking footprint stretched from the Atlantic to Lake Michigan. The deal's $2.5 billion in annual cost savings exceeded projections. By any financial metric, it was spectacularly successful.

Yet the reputational shadow lingered, especially in Cleveland where National City had been synonymous with civic leadership for 163 years. The acquisition became a case study in crisis opportunism—legally sound, financially brilliant, but ethically complicated. Had PNC saved the Midwest banking system or exploited taxpayer funds for corporate gain? The answer depended on your zip code. In Pittsburgh, Rohr was a strategic genius. In Cleveland, he remained the man who killed National City.

That duality would inform PNC's next decade. They'd proven they could execute massive, complex acquisitions under extreme pressure. They'd demonstrated balance sheet strength when peers were fragile. But they'd also learned that financial engineering without social license creates lasting resentment. As they looked toward future expansion, particularly in the Southeast and West, the National City lessons loomed large: sometimes the best deal isn't worth the reputational cost. Sometimes it is.

VI. Geographic Expansion: Building a National Footprint (2010–2020)

The National City integration was barely complete when Jim Rohr made a counterintuitive decision: sell PNC's crown jewel. Global Investment Servicing (GIS), their custody and fund administration business, generated steady fees serving $2.3 trillion in assets. But in July 2010, Rohr sold GIS to Bank of New York Mellon for $2.3 billion. Wall Street was puzzled—why divest a high-margin, low-risk business? Rohr's answer was strategic clarity: PNC would be a Main Street bank, not a Wall Street one. The sale proceeds repaid TARP obligations while funding geographic expansion.

Bill Demchak, who succeeded Rohr as CEO in 2013, brought a different perspective. A former JPMorgan investment banker who'd joined PNC in 2002, Demchak understood capital markets but believed regional banking's future lay in technology and geographic density. His strategic vision was precise: dominate the Eastern seaboard from Maine to Florida, then push selectively westward. Not nationwide ubiquity like Bank of America, but strategic depth in America's most economically dynamic regions.

The Southeast beckoned first. While PNC dominated the Rust Belt, they had minimal presence below the Mason-Dixon line. The 2011 acquisition of BankAtlantic's Tampa Bay branches was a toe in the water—19 locations for $42 million, barely a rounding error. But it gave PNC eyes on Florida's commercial real estate recovery and relationships with Northeast transplants wintering in St. Petersburg. Small deal, big intelligence value.

Then came the RBC opportunity. Royal Bank of Canada had spent a decade trying to crack U.S. retail banking, accumulating 426 branches across North Carolina, South Carolina, Georgia, Alabama, Florida, and Virginia. By 2011, they'd given up—too subscale, too expensive, wrong strategic fit. Demchak saw what others missed: RBC's branches were predominantly in high-growth suburban markets, their customers skewed affluent, and their commercial relationships included emerging Southeast manufacturers.

The $3.45 billion purchase price in 2012 was substantial but strategic. Unlike National City's distressed assets, RBC's portfolio was clean. Integration would be straightforward—PNC's proven playbook, no crisis conditions. More importantly, it transformed PNC's geographic profile. Suddenly they were a legitimate Southeast player with critical mass in Charlotte, Raleigh, Atlanta, and Orlando. The cultural fit proved surprising—Southern business owners appreciated PNC's commercial banking depth, while coastal retirees recognized the brand from their Northern roots.

Technology investment accelerated in parallel. Between 2012 and 2015, PNC spent $3 billion on digital infrastructure—mobile banking apps, online account opening, algorithmic underwriting. Demchak's insight: geographic expansion without physical density required digital excellence. A business in Birmingham might not have a PNC branch nearby, but they could access full treasury management services online. Retail customers in suburban Atlanta might visit branches rarely but engage daily through mobile apps.

The 2015 opening of PNC's new Pittsburgh headquarters—The Tower at PNC Plaza—sent a symbolic message. The 33-story LEED Platinum skyscraper wasn't just environmentally innovative with its double-skin facade and natural ventilation; it was a statement of permanence. While other banks shed real estate and embraced remote work, PNC doubled down on physical presence. The building's advanced workspace design—collaborative zones, client entertainment spaces, training facilities—reflected Demchak's belief that banking remained fundamentally a relationship business.

But the real innovation came at branch level. In 2018, PNC began deploying "Solution Centers"—a hybrid between traditional branches and digital kiosks. Customers could conduct routine transactions through advanced ATMs, schedule video conferences with specialists, or meet in-person for complex needs. Each Solution Center required 40% less space and 50% fewer staff than traditional branches while handling 90% of customer needs. It was automated efficiency with human availability—Amazon convenience with community presence.

The geographic expansion wasn't random. PNC's strategic planning team had identified 30 high-growth metro areas where they wanted material presence. By 2019, they operated in 19 of them. The gaps were glaring—Texas, California, Colorado, Arizona. These Western markets were dominated by different players—Wells Fargo, JPMorgan Chase, regional specialists. Breaking in would require either massive organic investment or a transformative acquisition.

Behind the expansion lay sophisticated analytics. PNC's economists tracked migration patterns, identifying corridors where their existing customers were relocating. They analyzed industry clusters, focusing on markets with diversified economies rather than single-sector dependence. They studied demographic trends, prioritizing areas with growing millennial populations and rising household formation. It wasn't just about planting flags; it was about strategic density in markets that mattered.

By 2020, PNC had quietly assembled something remarkable: the only bank with top-five market share in both the Midwest and Mid-Atlantic, growing presence across the Southeast, and technological capabilities matching money-center banks. Revenue had diversified—fee income now matched net interest income, unlike traditional regional banks dependent on rate spreads. Commercial banking relationships spanned middle-market manufacturers to Fortune 500 treasury management.

Yet Demchak knew the footprint remained incomplete. The Southwest and West Coast represented 40% of U.S. economic activity but 0% of PNC's presence. Texas alone had an economy larger than Canada. California's tech ecosystem dwarfed Pittsburgh's emerging innovation economy. To truly compete with JPMorgan and Bank of America, PNC needed Western exposure. The question was how—organic expansion would take decades and billions in investment. Acquisition seemed the only path, but what Western bank would fit PNC's disciplined criteria?

The answer would come from an unexpected source: a Spanish bank looking to exit America just as a global pandemic created the perfect conditions for transformative M&A.

VII. The BBVA USA Acquisition: Coast-to-Coast at Last (2020–2021)

The Zoom call on November 15, 2020, connected Pittsburgh, Houston, and Madrid. Bill Demchak sat in PNC's executive conference room, masked and socially distanced from his team. In Houston, BBVA USA CEO Javier Rodriguez participated from an empty office tower. From Madrid, BBVA Group Chairman Carlos Torres Vila joined at midnight local time. The conversation that would create America's first new coast-to-coast bank in a generation lasted exactly 47 minutes.

BBVA's American adventure had begun in 2004 when they acquired Alabama's Compass Bank for $9.6 billion. The Spanish banking giant spent the next fifteen years pouring capital into U.S. expansion—buying Texas State Bank, Guaranty Bank, and Simple Finance, rebranding everything as BBVA USA. By 2020, they'd assembled 637 branches across Texas, Alabama, Arizona, California, Colorado, Florida, and New Mexico with $104 billion in assets. Yet after sixteen years and billions in investment, they commanded less than 2% market share in most markets. Torres Vila had reached a stark conclusion: without massive additional investment, BBVA USA would remain subscale indefinitely.

Demchak had tracked BBVA USA for years. Their footprint was PNC's photo negative—strong where PNC was absent, particularly in Texas's booming metros and California's wealth centers. Their customer base skewed younger and more diverse than PNC's Rust Belt core. Their digital capabilities, inherited from fintech acquisition Simple, were surprisingly advanced. When COVID-19 crashed bank valuations in March 2020, Demchak sensed opportunity.

The pandemic context was crucial. Traditional M&A due diligence—site visits, in-person meetings, systematic review—was impossible. But it also meant sellers were motivated and valuations depressed. More importantly, the Federal Reserve had signaled unlimited support for bank consolidation that strengthened system stability. Interest rates near zero made financing cheap, while PNC's excess capital from years of conservative underwriting meant they could pay cash without dilution.

The negotiation was unlike any major bank deal in history. Teams never met in person. Due diligence happened through virtual data rooms and video conferences. Integration planning occurred through shared digital workspaces. When Demchak and Torres Vila needed to discuss price, they used encrypted messaging apps. The entire $11.6 billion transaction—one of banking's largest ever—was negotiated entirely remotely.

The price—19.7 times BBVA USA's 2019 earnings—raised eyebrows. In a pandemic, with credit losses looming, why pay a premium? Demchak's math was different. First, BBVA USA's loan book was surprisingly clean—conservative underwriting in Texas, minimal commercial real estate exposure, strong capital ratios. Second, the strategic value transcended financials. PNC would instantly become a top-10 bank in the fourth, fifth, and tenth largest U.S. states. Third, expected cost savings of $900 million annually—35% of BBVA USA's expense base—would make the math work even at premium pricing.

The announcement on November 16, 2020, stunned the banking world. While everyone focused on pandemic survival, PNC had engineered the largest bank acquisition since the financial crisis. The combined institution would have $560 billion in assets, presence in 29 of America's 30 largest markets, and true coast-to-coast coverage. Geography that took Bank of America three decades to assemble, PNC achieved in one deal.

But execution complexity dwarfed even National City. BBVA USA operated on completely different technology infrastructure—core banking systems from Spain, digital platforms from Portland, risk management from Houston. Converting 2.6 million customers, 9,000 employees, and 600 branches across seven states would require military precision. PNC created Project Synergy—2,000 employees working full-time on integration, supported by every major consulting firm and systems integrator.

The cultural challenges were equally daunting. BBVA USA employees had experienced three ownership changes in fifteen years. Texas bankers accustomed to BBVA's European management style now reported to Pittsburgh. California technologists from Simple worried about East Coast banking conservatism. Alabama branches that had been Compass Bank for a century faced their fourth rebrand. Demchak personally visited every major BBVA market, conducting town halls and emphasizing continuity—local leadership would remain, community relationships would strengthen, employees who performed would thrive.

October 2021's conversion weekend was banking's equivalent of D-Day. From Friday evening to Monday morning, PNC migrated every account, moved every transaction record, and converted every system. Eight thousand employees worked through the weekend. Temporary command centers operated in Pittsburgh, Houston, Phoenix, and Birmingham. By Monday morning, October 18, every BBVA USA customer was a PNC customer. ATMs dispensed cash with PNC branding. Mobile apps showed PNC interfaces. The largest bank systems conversion in U.S. history executed flawlessly.

The strategic implications were transformative. PNC now competed directly with JPMorgan Chase in Texas, Bank of America in California, Wells Fargo in Colorado. Their commercial banking could serve companies expanding nationally without switching banks. Wealth management could follow snowbirds from Pittsburgh to Phoenix. Treasury management could integrate East Coast headquarters with West Coast operations. True network effects emerged—each market strengthening others through customer relationships and operational efficiency.

Demchak also announced an $88 billion Community Benefits Plan over four years, targeting low-and-moderate-income communities across the expanded footprint. Unlike performative corporate social responsibility, this was strategic—BBVA USA's diverse customer base in Houston, Phoenix, and Los Angeles required authentic community engagement. PNC would finance affordable housing, support minority-owned businesses, and expand access to banking services in underserved communities. It was both good business and good politics.

By mid-2022, the acquisition's success was undeniable. Cost synergies exceeded targets. Customer retention hit 94%. Texas commercial lending grew 20% annually. California wealth management assets rose 30%. The feared culture clash never materialized—instead, PNC's commercial banking strength complemented BBVA's retail innovation. The combined institution generated record earnings while maintaining credit discipline.

The BBVA acquisition completed PNC's 40-year transformation. From two Pennsylvania banks to America's only true super-regional, present in every major economic region but focused on Main Street banking. While JPMorgan chased investment banking and Bank of America pursued global ambitions, PNC had methodically built something different—a coast-to-coast commercial bank serving the real economy. The footprint was complete. The question now: what would they do with it?

VIII. Business Model & Competitive Advantages

Walk into a PNC branch in Houston, Pittsburgh, or Phoenix, and you'll notice something different from JPMorgan or Bank of America locations. The wealth advisor sits next to the small business specialist. The commercial banker's office connects to the retail floor. This physical layout reflects PNC's strategic differentiation—while money-center banks segment customers into silos, PNC builds ecosystems around client relationships. A successful entrepreneur banks personally at PNC, their business uses PNC treasury management, their wealth sits with PNC advisors, and their company's employees use PNC retail services. It's the community bank model scaled to $560 billion.

The Main Street focus isn't nostalgic—it's economically strategic. Consider the revenue mix: 52% comes from net interest income, 48% from fees. Compare that to regional peers like Regions (70% net interest) or Citizens (75% net interest). PNC's fee diversity—asset management, treasury services, card processing, capital markets—provides stability when interest rates shift. During 2023's rate volatility, while Silicon Valley Bank and First Republic collapsed from duration mismatches, PNC's diversified revenue barely fluctuated.

The commercial banking franchise forms PNC's competitive moat. With 45% of revenues from corporate and institutional banking, PNC dominates the middle market—companies with $5 million to $2 billion in revenue. These aren't JPMorgan's Fortune 500 clients or community banks' local businesses. They're regional manufacturers, healthcare systems, universities, municipalities—complex enough to need sophisticated services but not large enough to access capital markets directly. PNC's average commercial relationship generates $2.8 million in annual revenue across multiple products: lending, cash management, foreign exchange, interest rate hedging, 401(k) administration.

This middle-market focus creates powerful economics. These clients rarely switch banks—relationship tenure averages 14 years. They're less price-sensitive than large corporates who bid out every service. They need advice, not just products, creating consulting-like relationships. And they're surprisingly resilient—during the 2008 crisis, PNC's middle-market losses were 60% lower than large corporate defaults. The boring middle of American business turns out to be highly profitable.

Technology infrastructure represents an hidden advantage. That 1990 decision to maintain a single platform means PNC operates one core banking system while Bank of America manages six and Wells Fargo runs four. This translates to massive operational efficiency—PNC's efficiency ratio of 57% beats most peers despite their smaller scale. More importantly, unified technology enables rapid innovation. When PNC launches a new product, it's available instantly across all channels and markets. When they acquire a bank, integration happens in months, not years.

The asset management business—$187 billion under administration—deserves special attention. Unlike pure-play investment banks, PNC's wealth management grows organically from commercial banking relationships. The business owner who sells their company becomes a wealth client. The doctor whose practice PNC finances moves their personal assets over. This captive origination model produces 15% annual asset growth without expensive advisor recruitment. It also creates stickiness—clients with both banking and investment relationships rarely leave.

Risk management philosophy differentiates PNC from aggressive regional peers. They've never chased yields into exotic securities, maintained strict commercial real estate limits (18% of loans versus 30%+ at failed banks), and avoided crypto speculation entirely. The conservative culture traces to Pittsburgh's industrial heritage—when your borrowers are steel mills and coal companies, you learn to model downside scenarios. This discipline costs growth in boom times but preserves capital during busts. PNC has been profitable every year since 1983 except 1987, including 2008-2009.

The branch network itself is surprisingly strategic. While digital banks abandon physical presence and money-centers shrink footprints, PNC's 2,600 locations provide competitive advantage. But these aren't your grandfather's branches. The Solution Center model—60% of new locations—combines digital convenience with human expertise. Routine transactions happen through machines; complex problems get solved by specialists. It's more Apple Store than traditional bank—experiential, educational, efficient. Branches become customer acquisition centers, not transaction processing facilities.

Treasury management capabilities rival money-center banks. PNC processes $2.7 trillion in annual payment volume, manages 80,000 corporate accounts, and provides working capital to 40% of Fortune 500 companies. Their PINACLE platform combines cash management, payments, trade finance, and supply chain finance in one interface. For middle-market CFOs, it's JPMorgan-quality infrastructure at regional bank pricing. The business generates $2.3 billion in annual fees with 70% EBITDA margins—software economics in banking wrapper.

Geographic diversification now provides natural hedging. When Midwest manufacturing slows, Southeast services grow. When California technology struggles, Texas energy thrives. This wasn't true before BBVA—PNC was overexposed to Rust Belt industrials. Now they're balanced across regions and industries. The loan portfolio reflects this: 22% commercial real estate, 15% consumer, 38% commercial and industrial, 25% residential mortgage. No concentration threatens systemic risk.

Capital allocation remains distinctly conservative. While peers leveraged up during the zero-rate years, PNC maintained 9.5% CET1 ratios, well above regulatory minimums. They've returned $30 billion to shareholders through dividends and buybacks since 2010 while still funding growth. The dividend—yielding 3.8%—has increased annually since 2011. This balance—growth plus return—attracts both value and growth investors, broadening the shareholder base.

The competitive moat comes from combining these elements. A Texas manufacturer can get a loan from many banks, but PNC provides the loan, manages cash, processes payments, hedges currencies, administers the 401(k), and handles the owner's wealth. A Florida healthcare system might bank with SunTrust, but PNC offers integrated solutions from equipment finance to physician wealth management. It's not one killer product but an ecosystem of services that creates switching costs and pricing power.

This model faces challenges. Fintechs unbundle each service—Stripe for payments, Brex for corporate cards, Mercury for startup banking. Large corporates increasingly bypass banks for direct capital markets access. Digital natives expect experiences PNC's technology can't yet deliver. But for the vast middle of American business—too large for community banks, too small for Wall Street—PNC's integrated model remains compelling. They're not trying to be everything to everyone, just everything to the customers that matter most to their strategy.

IX. Playbook: M&A Excellence & Integration

Study PNC's 40-plus acquisitions since 1983, and a pattern emerges that reads like a military field manual. Every deal follows the same sequence: strategic assessment, valuation discipline, systematic integration, cultural absorption, and value realization. While other banks approach M&A opportunistically, PNC executes with manufacturing precision. The playbook, refined over four decades, explains why PNC's acquisitions consistently exceed synergy targets while peers struggle with integration failures.

The strategic assessment phase begins years before any deal. PNC maintains a "strategic map" of 200+ potential targets, updated quarterly with financial performance, market position, and management changes. They know which banks have commercial lending strength, who owns attractive branch networks, where technology platforms excel. When BBVA USA became available, PNC had already modeled the acquisition five different ways. This preparation enables speed—they can evaluate and bid on opportunities in days while competitors need weeks.

Valuation discipline separates PNC from empire builders. The iron rule: pay no more than what you can earn back through synergies within three years. This means walking away from auctions where emotional bidding inflates prices. In 2019, PNC passed on SunTrust's merger with BB&T despite board pressure to respond. The analysis was clear: too expensive, too much overlap, integration complexity off the charts. That discipline preserved capital for BBVA USA two years later at better economics.

The integration methodology reads like Toyota's production system. Day One: announce retention decisions for senior management. Day 30: complete technology assessment and choose platform. Day 60: finalize branch consolidation plans. Day 90: launch customer communication campaign. Day 180: complete systems conversion. Day 365: achieve 50% of targeted cost saves. Day 730: full integration complete. This timeline never varies. Every employee knows their role. Every milestone has accountable owners. It's banking M&A as assembly line.

Technology integration showcases the playbook's sophistication. PNC maintains a 400-person integration team permanently staffed, not consultants hired for each deal. They've converted 40+ different core banking systems onto PNC's platform. They maintain a "data lake" with translation protocols for every major banking system. When acquiring a bank, they can predict integration costs within 5% based on system complexity. The BBVA conversion—600 branches across seven states—went flawlessly because PNC had practiced the moves hundreds of times.

Cultural integration reveals unexpected sophistication. PNC doesn't impose Pittsburgh culture on acquired banks; instead, they identify cultural strengths to preserve. National City's middle-market commercial expertise was maintained. RBC's wealth management approach continued. BBVA's digital innovation got expanded. The key: separate cultural identity from operational efficiency. Local market presence and customer relationships reflect acquired banks' heritage; back-office operations conform to PNC standards. Customers see continuity; shareholders see synergies.

The talent retention strategy is surgical. Within days of announcement, PNC identifies "critical talent"—top 20% of performers essential to value preservation. These employees receive retention bonuses, expanded roles, and clear career paths. The next 60% get standard packages. The bottom 20% face elimination. This clarity reduces uncertainty and exodus. During BBVA integration, PNC retained 94% of identified critical talent, compared to 60% industry average. They turned potential brain drain into competitive advantage.

Cost synergy realization follows proven formulas. Branch consolidation uses algorithmic modeling—customer overlap, traffic patterns, lease costs, competitive dynamics. Back-office consolidation happens in waves—first, eliminate duplicate corporate functions; second, combine operations centers; third, optimize vendor contracts. Technology spending gets centralized immediately. Marketing budgets merge but maintain local flexibility. The precision is remarkable: PNC projected $900 million in BBVA synergies and achieved $950 million.

Revenue synergies—historically harder to achieve—get equal attention. PNC maps product gaps: which acquired customers lack wealth management, who needs treasury services, where lending relationships can expand. They deploy specialist teams to high-value segments. Commercial bankers visit every significant business client within 90 days. Wealth advisors contact every affluent household. The cross-sell happens systematically, not hopefully. BBVA USA customers increased products-per-relationship from 3.2 to 4.7 within eighteen months.

Risk management during integration is paranoid. PNC assumes Murphy's Law: everything that can go wrong will. They maintain double staff during conversions. They run parallel systems for critical functions. They keep manual backup processes. During the National City weekend conversion, PNC had 500 IT specialists on standby for problems that never materialized. This redundancy costs millions but prevents billions in potential losses. No PNC acquisition has ever suffered a major operational failure.

Regulatory management throughout M&A is equally sophisticated. PNC maintains continuous dialogue with the Fed, OCC, and FDIC. They submit integration plans before deal announcement. They invite regulatory observers to integration meetings. They over-communicate on progress and problems. This transparency builds trust. When PNC sought approval for BBVA acquisition during a pandemic, regulators approved in record time because PNC's track record spoke for itself.

The learning system compounds advantages over time. After each acquisition, PNC conducts systematic post-mortems: what worked, what didn't, what to improve. These lessons get codified into the playbook. The National City integration taught them about managing cultural sensitivity in proximate markets. RBC revealed the importance of maintaining local commercial banking expertise. BBVA demonstrated remote integration possibilities. Each deal makes the next one better.

Comparing PNC's playbook to peers reveals stark contrasts. Bank of America's NationsBank-BankAmerica merger took five years to fully integrate. Wells Fargo still struggles with Wachovia systems issues fifteen years later. First Union's CoreStates acquisition destroyed billions in value. Meanwhile, PNC consistently hits integration targets, retains customers, and realizes synergies. The difference isn't luck—it's systematic excellence refined over decades.

The playbook's principles extend beyond banking. Any serial acquirer can learn from PNC's discipline: prepare extensively before opportunities arise, maintain valuation discipline despite competitive pressure, invest in permanent integration capabilities, respect acquired cultures while driving operational conformity, and systematically capture lessons for continuous improvement. It's not sexy—no dramatic headlines or transformative vision—just relentless execution of proven processes.

For investors, the playbook represents sustainable competitive advantage. While any bank can make acquisitions, few can integrate them profitably. PNC's methodology reduces execution risk, accelerates synergy capture, and enables larger, more complex deals. The BBVA acquisition—$11.6 billion during a pandemic—would terrify most banks. For PNC, it was just the playbook at scale. This capability creates optionality: when the next banking crisis triggers consolidation, PNC will be buyer, not seller, and their integration machine will turn disruption into value.

X. Analysis & Investment Case

The investment case for PNC starts with a simple observation: among America's ten largest banks, PNC trades at the lowest multiple to book value despite superior returns on equity. The market prices PNC like a sleepy regional bank—11x forward earnings versus 13x for JPMorgan—yet PNC's ROE of 13.5% matches money-center performance with lower volatility. This valuation disconnect creates opportunity, but understanding it requires dissecting both the bear and bull narratives.

The bear case begins with rate sensitivity. PNC's asset mix—38% commercial loans, 25% residential mortgages—reprices slowly when rates fall. Their deposit base, concentrated in commercial accounts, demands market pricing. This creates margin compression in falling rate environments. When the Fed cut rates to zero in 2020, PNC's net interest margin compressed 80 basis points, worse than peers. Bears argue this rate sensitivity makes PNC uninvestable during monetary easing cycles.

Geographic concentration concerns persist despite expansion. Yes, PNC now operates coast-to-coast, but 60% of deposits still come from Pennsylvania, Ohio, Michigan, and Illinois—Rust Belt markets with declining populations and struggling industries. Texas and California presence, while growing, remains subscale compared to incumbents. Bears see PNC caught between worlds—too concentrated in declining regions, too weak in growth markets.

Commercial real estate exposure terrifies some investors. At 22% of loans, PNC's CRE concentration sits below regional peers but above money-centers. With office vacancies at record highs and retail struggling, bears project massive losses coming. They point to signature patterns—Pittsburgh office values down 30%, Cleveland retail vacancies at 20%, Detroit industrial struggling. If CRE follows 1990s patterns, PNC could face $20 billion in losses.

Technology disruption represents existential threat. While PNC invested heavily in digital capabilities, they're not Chase with unlimited technology budgets or Capital One with fintech DNA. Young customers choose Chime or Cash App, not regional banks. Small businesses use Square or Stripe, not traditional merchant services. Commercial clients increasingly expect real-time everything—payments, reporting, credit decisions. Bears see PNC fighting tomorrow's war with yesterday's weapons.

The regulatory overhang looms large. At $560 billion in assets, PNC sits in regulatory purgatory—too big to be simple, too small for too-big-to-fail advantages. They face the same compliance costs as JPMorgan without the scale benefits. Stress tests constrain capital returns. Living wills require expensive planning. Anti-money laundering demands massive investment. Bears calculate PNC spends 180 basis points of assets on compliance versus 120 for smaller regionals.

But the bull case starts where bears end—with misunderstood strengths. That rate sensitivity? It cuts both ways. When rates rise, PNC's asset-sensitive balance sheet expands margins faster than peers. From 2022-2023, net interest income grew 45%, beating every large bank. The commercial deposit base, while rate-sensitive, is also sticky—average relationship duration exceeds 14 years. PNC doesn't chase hot money; they cultivate permanent capital.

Geographic diversification is actually optimal. The Rust Belt isn't dying; it's transforming. Pittsburgh has become a robotics hub. Columbus thrives on logistics and insurance. Detroit's automotive industry is electrifying. Meanwhile, PNC's Southeast presence targets the right markets—Raleigh's research triangle, Atlanta's corporate hub, Florida's wealth corridor. The Texas footprint focuses on Houston energy and Dallas commerce, not speculative Austin technology. It's selective density, not scattered presence.

The commercial real estate portfolio is similarly misunderstood. Unlike 1980s S&Ls, PNC's CRE book is granular—average loan size of $3.2 million across 7,000 borrowers. They avoided trophy properties and mega-developments. Their underwriting assumes 40% value declines, not 10% hiccups. Most importantly, 65% of CRE loans are owner-occupied—doctors' offices, manufacturing facilities, warehouses—not speculative developments. When analysts model 1990s-style CRE collapse, they're fighting the last war.

Technology position is strategically sound. PNC doesn't need to be Chime because their customers aren't 22-year-olds living paycheck-to-paycheck. Their sweet spot—affluent households, middle-market businesses, institutional clients—values relationship over application. The billion-dollar technology spend isn't trying to out-innovate Square; it's digitizing complex commercial processes. PNC's PINACLE treasury platform processes more volume than most fintech unicorns combined. Boring competence beats flashy disruption in commercial banking.

Capital flexibility represents hidden value. With 9.5% CET1 ratios versus 7% regulatory minimums, PNC maintains $15 billion in excess capital. They could acquire a $50 billion bank tomorrow, return $10 billion to shareholders, or absorb massive credit losses—optionality worth considering. During the next crisis, while peers rebuild capital, PNC will deploy it. The patient accumulation of capital is strategic preparation, not inefficient allocation.

The valuation math is compelling. At 1.2x tangible book value, PNC trades at a 20% discount to large bank peers despite comparable returns. If PNC simply re-rated to peer multiples, the stock would appreciate 25%. But the real opportunity is earnings growth. Consensus expects 5% annual EPS growth; PNC has delivered 8% over the past decade. The BBVA synergies alone add $0.75 to annual earnings. Rising rates could add another $1.00. Normal credit losses would save $0.50 versus current reserves. The path to $15 EPS by 2025 seems conservative.

Risk-reward favors patient investors. Downside is limited—the dividend yields 3.8%, book value provides support, and excess capital cushions shocks. Upside is substantial—multiple expansion, earnings growth, and strategic optionality. The biggest risk isn't what PNC does wrong but what they might do right—the next transformative acquisition that cements their position among America's banking giants.

For fundamental investors seeking quality at reasonable price, PNC represents rare value. It's a competitively advantaged business (superior ROE), with sustainable moat (middle-market dominance), trading at discount to intrinsic value (low P/B multiple), with multiple paths to appreciation (earnings growth, multiple expansion, capital return). The market sees a boring regional bank. Reality is a disciplined acquirer with national scale, diversified revenue, and patient capital waiting for opportunity. Sometimes the best investments hide in plain sight.

XI. Future Vision & Strategic Options

Bill Demchak's 2024 investor day presentation included an unusual slide: a map of the United States with PNC's footprint in green and "strategic white spaces" in gray. The gray areas—the Pacific Northwest, Mountain West, and New England—represented $8 trillion in deposits where PNC has zero presence. "We're not done," Demchak said simply. "The consolidation of American banking is inevitable, and we intend to lead it." At 61, with a decade likely remaining as CEO, Demchak is positioning PNC for moves that could fundamentally reshape American banking.

The strategic logic for continued expansion is compelling. Scale economics in banking are brutal—technology costs are largely fixed, regulatory compliance doesn't decrease with size, and product development requires massive investment. JPMorgan spends $12 billion annually on technology; PNC spends $3 billion. That 4x difference shows up in product sophistication, customer experience, and operational efficiency. To truly compete with the Big Four, PNC needs scale approaching $1 trillion in assets. They're at $560 billion. The math points toward more acquisitions. The remaining geographic white spaces tell a compelling story. The Pacific Northwest—Seattle's tech economy, Portland's creative class—remains untapped. New England's wealth concentration from Boston to Greenwich offers tantalizing opportunities. The Mountain West's explosive growth in Denver, Salt Lake City, and Boise represents America's new economic frontier. Demchak's strategic planning team has identified specific targets in each region, though regulatory approval timelines and willing sellers remain variables.

Recent smaller acquisitions show PNC's continued appetite—Aqueduct Capital Group, LINGA, and Mellott Company representing tactical capability additions rather than geographic expansion. More significantly, in October 2023, PNC acquired $16.6 billion in capital commitments facilities from Signature Bridge Bank through the FDIC, primarily fund subscription lines to private equity sponsors, immediately accretive at 10 cents per share in Q4 2023. This wasn't geographic expansion but capability deepening—strengthening their already formidable position in private equity banking.

The wealth management expansion strategy deserves particular attention. With $187 billion under management generating 15% annual growth, PNC sees wealth as the connective tissue between commercial and retail banking. Every business owner becomes a wealth client; every wealth client brings commercial relationships. The model works particularly well in markets like Texas and California where entrepreneurial wealth creation happens rapidly. Demchak envisions doubling wealth assets to $400 billion by 2030 through organic growth and selective acquisitions.

Digital transformation accelerates rather than replaces physical expansion. The Solution Center model—now 40% of branches—proves that physical presence matters when combined with digital excellence. Customers want the option of human interaction for complex needs while handling routine transactions digitally. PNC's investment in 200 new Solution Centers over the next three years targets high-growth suburban markets where affluent households and businesses cluster. It's selective density, not ubiquitous coverage.

The most intriguing strategic development is PNC's July 2024 partnership with Coinbase to offer cryptocurrency services—clients can buy, hold, and sell cryptocurrencies through PNC accounts while PNC provides banking services to Coinbase. For conservative PNC to embrace crypto signals strategic evolution. Demchak framed it perfectly: "Partnering with Coinbase accelerates our ability to bring innovative, crypto financial solutions to our clients...to meet growing demand for secure and streamlined access to digital assets on PNC's trusted platform." This isn't speculative trading but responding to client demand for regulated crypto access.

The cryptocurrency move reflects broader strategic thinking. PNC won't lead bleeding-edge innovation—that's for fintechs and tech companies. But once innovations prove durable and clients demand them, PNC provides trusted, regulated access. They were late to mobile banking but now have best-in-class apps. They avoided early blockchain experiments but now use distributed ledger for trade finance. The Coinbase partnership initially targets wealth and asset management clients, allowing crypto trading from PNC accounts—perfect for their affluent customer base seeking portfolio diversification.

Climate finance represents another growth vector. PNC committed $30 billion to sustainable finance by 2030, focusing on renewable energy project finance, green bonds, and ESG-linked loans. This isn't virtue signaling—it's following the money. Their commercial clients increasingly need sustainability financing for regulatory compliance and investor demands. PNC's expertise in project finance from decades of infrastructure lending positions them perfectly for the energy transition. They're already the third-largest renewable energy lender among U.S. banks.

The potential for a transformative merger-of-equals looms large. While PNC has always been acquirer, not acquired, the math for a combination with a peer like U.S. Bank or Truist could be compelling. Combined with U.S. Bank's Midwest dominance, they'd create a true national champion. Merged with Truist's Southeast strength, they'd dominate the Eastern United States. Demchak hasn't ruled out being acquired if the premium and strategic fit align. At the right price—say 1.8x book value—PNC shareholders could see 50% immediate returns.

International expansion remains notably absent from strategic discussions. Unlike JPMorgan's global ambitions or Bank of America's international corporate banking, PNC stays deliberately domestic. The reasoning is sound—international banking requires massive investment for uncertain returns. Better to dominate profitable U.S. markets than chase prestige in London or Tokyo. The only international services PNC provides support U.S. clients' overseas needs—foreign exchange, trade finance, correspondent banking.

Technology partnerships will accelerate capability expansion without massive investment. The Coinbase model—partnering with best-in-class providers rather than building internally—could extend to other areas. Imagine PNC partnering with Stripe for payment processing, Plaid for data aggregation, or Affirm for buy-now-pay-later. These partnerships provide cutting-edge capabilities while PNC focuses on their core strength: relationship banking backed by balance sheet lending.

The strategic optionality is remarkable. PNC could acquire a $100 billion Western bank and complete their nationwide footprint. They could merge with a peer and challenge the Big Four directly. They could stay disciplined, grow organically, and compound returns for shareholders. They could even sell to JPMorgan or Bank of America at massive premiums. Few banks have such strategic flexibility combined with the capital and capability to execute any option.

The next decade will determine whether PNC joins America's banking oligopoly or remains the best of the rest. The pieces are in place—national footprint, diversified revenue, strong capital, proven execution. The question isn't capability but ambition. Does Demchak want to run a trillion-dollar bank with all its complexity and scrutiny? Or does he prefer PNC's current position—large enough to matter, small enough to maneuver, profitable enough to satisfy shareholders, strategic enough to shape the industry?

The answer may come from an unexpected source: the next financial crisis. When credit losses mount and weak banks fail, PNC will be buying, not selling. Their patient accumulation of capital, conservative underwriting, and integration expertise position them perfectly for crisis-driven consolidation. The 2008 playbook—using government support to eliminate competitors—could repeat at even larger scale. When that moment comes, PNC won't just participate in banking consolidation; they'll lead it. The question isn't if but when, and whether the target will be large enough to fundamentally transform American banking's competitive landscape.

XII. Recent News

In July 2024, PNC announced a groundbreaking strategic partnership with Coinbase, leveraging Coinbase's Crypto-as-a-Service platform to allow PNC clients to buy, hold, and sell cryptocurrencies while providing banking services to Coinbase—marking PNC as one of the largest U.S. banks to offer comprehensive crypto services. The move signals PNC's recognition that digital assets have moved from speculation to client necessity, with CEO William Demchak stating the partnership speeds up the bank's ability to bring "crypto financial solutions" to clients amid growing demand for secure digital asset access.

The timing proved prescient. Days after PNC's announcement, President Trump signed the GENIUS Act into law, establishing the first federal framework for stablecoin regulation in the United States. Major bank CEOs including JPMorgan's Jamie Dimon, Citigroup's Jane Fraser, and Bank of America's Brian Moynihan announced plans to get involved in dollar-pegged stablecoins following the legislation's passage. PNC's early mover advantage in crypto infrastructure positions them ahead of money-center peers still evaluating digital asset strategies.

In October 2023, PNC acquired $16.6 billion in capital commitments facilities from Signature Bridge Bank through an FDIC agreement, including $9 billion of funded loans primarily comprising fund subscription lines to private equity sponsors, immediately accretive at 10 cents per share in Q4 2023. The acquisition strengthens PNC's position in private equity banking without geographic expansion, demonstrating their ability to acquire distressed assets profitably even outside traditional bank M&A.

XIII. Links & Resources

Annual Reports & Investor Materials - PNC Investor Relations: investor.pnc.com - SEC Filings: www.sec.gov/edgar (Ticker: PNC) - Quarterly Earnings Presentations - Annual 10-K Reports - Proxy Statements (DEF 14A)

Historical Merger Documentation - National City Merger Proxy (2008) - BBVA USA Acquisition Materials (2020-2021) - RBC Bank Acquisition Documents (2012)

Banking Industry Research - Federal Reserve Economic Data (FRED) - FDIC Quarterly Banking Profile - SNL Financial (S&P Global Market Intelligence) - American Bankers Association Research

Books on Banking History & M&A - "The Great American Bank Robbery" - Paul Sperry - "Too Big to Fail" - Andrew Ross Sorkin - "The Bankers' New Clothes" - Anat Admati - "A History of American Banking" - Murray Rothbard

PNC Leadership Resources - CEO William Demchak Interviews (Bloomberg, CNBC) - Investor Day Presentations - Banking Conference Speeches

Regulatory Resources - Federal Reserve Board: federalreserve.gov - Office of the Comptroller of the Currency: occ.gov - FDIC: fdic.gov - Consumer Financial Protection Bureau: cfpb.gov

M&A and Banking Analysis - KBW Bank Index and Research - Morgan Stanley Banking Research - Goldman Sachs Financial Institutions Group Reports

Technology & Innovation - Finovate Conference Materials - Banking Technology Magazine - American Banker Digital Banking Report

Regional Economic Data - Federal Reserve District Banks Economic Data - Bureau of Labor Statistics Regional Reports - Census Bureau Metropolitan Statistical Areas

Competitive Intelligence - Peer Bank 10-Ks and Investor Presentations - Call Report Data (FFIEC) - Banking Industry Conferences and Panels

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube