Marriott International: From Root Beer Stand to Global Hospitality Empire

I. Introduction & Cold Open

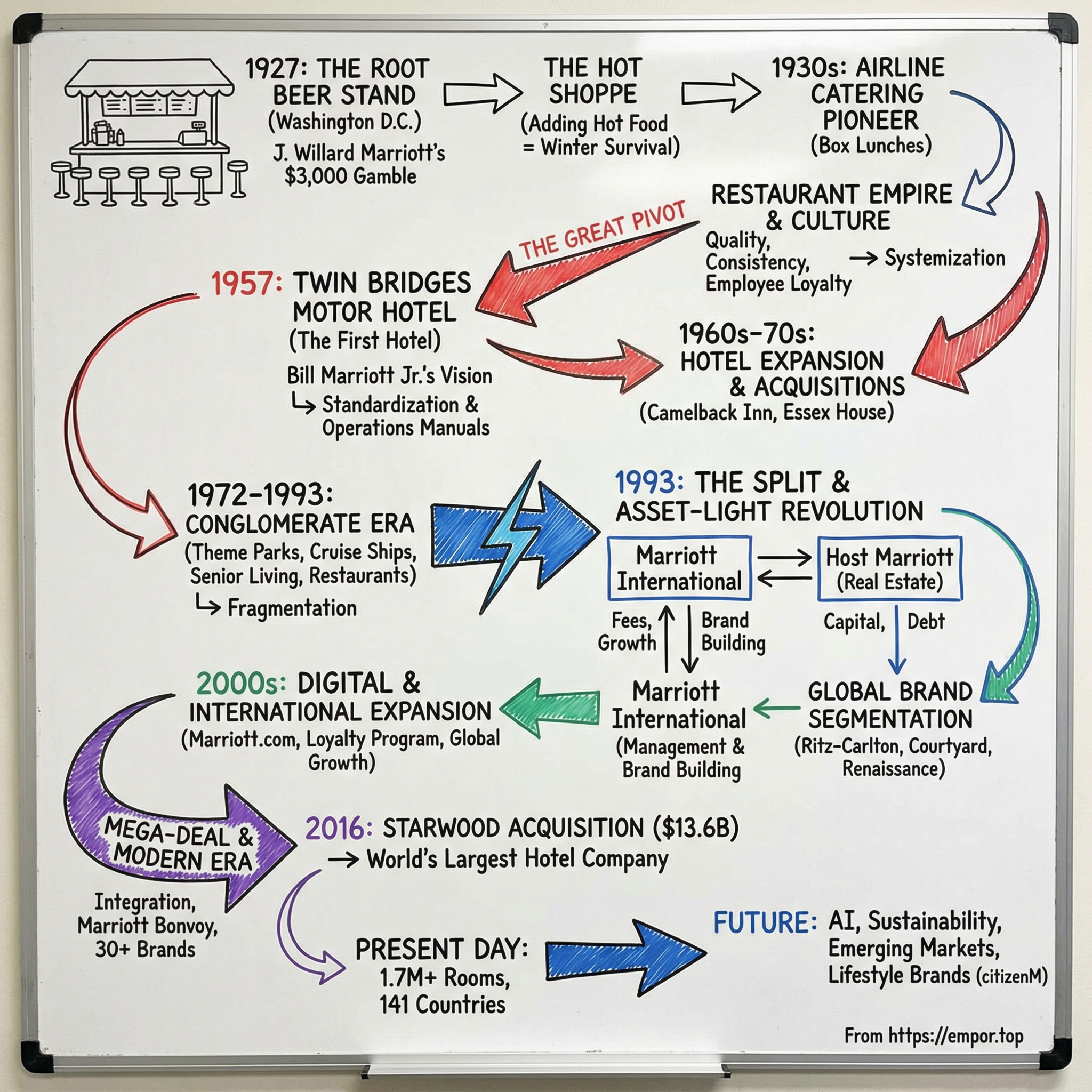

The morning of May 20, 1927, held two moments that would reshape American ambition in vastly different ways. As Charles Lindbergh's Spirit of St. Louis lifted off from Roosevelt Field on Long Island, beginning humanity's first solo transatlantic flight, a far humbler venture was unfolding 200 miles south. At 3128 14th Street NW in Washington, D.C., a young Mormon entrepreneur named J. Willard Marriott was nervously adjusting nine wobbly stools in front of his brand-new root beer stand. One journey would capture the world's imagination for a week; the other would quietly build an empire that would touch millions of lives for a century.

Marriott couldn't have imagined that his $3,000 investment—half borrowed, half scraped together from savings—would evolve into the world's largest hotel company. Today, Marriott International commands a market capitalization of $74.91 billion, operates over 1.7 million rooms across 141 countries, and generated $25.1 billion in revenue in 2024. The company's full-year global RevPAR rose 4.3 percent last year, with record gross room additions exceeding 123,000 rooms. Behind these staggering numbers lies one of American business's most remarkable transformations: from serving root beer floats to Washington office workers to managing luxury resorts in the Maldives, from a single-family operation to a publicly-traded behemoth with 37 brands.

What makes Marriott's story particularly compelling isn't just its scale—it's the deliberate, methodical way the company evolved. Unlike tech unicorns that explode overnight, Marriott's growth spans nearly a century of careful pivots, each building on the last. The company mastered restaurants before entering hotels. It dominated domestic markets before going international. It perfected ownership before pioneering the asset-light model that would revolutionize hospitality. Each transition carried enormous risk, yet each was executed with the precision of a Swiss watch.

The Marriott saga is fundamentally a story about three transformations. First, how a sheepherder's son from rural Utah built a values-driven culture that would outlast him by generations. Second, how a restaurant company recognized that its future lay in beds, not burgers. And third, how a real estate-heavy operation engineered one of business history's most successful pivots to an asset-light, fee-based model that would become the envy of the industry.

This is also a uniquely American story—one of Mormon work ethic meeting Washington power brokers, of family businesses professionalizing without losing their soul, of service industries scaling through systemization. It's about timing markets perfectly (entering hotels just as interstate highways transformed travel) and surviving disasters (from the Depression to COVID-19). Most importantly, it's about building something that endures: a business model so robust that it thrives whether the economy booms or busts, whether travelers seek luxury or economy, whether they're crossing oceans or driving to the next town.

As we trace this journey from nine stools to 9,300 properties, we'll discover that Marriott's real innovation wasn't in hospitality—it was in creating a machine for turning other people's real estate into predictable, high-margin fee streams. We'll see how a company that once prided itself on owning everything became more valuable by owning almost nothing. And we'll understand why, in an industry plagued by cyclicality and capital intensity, Marriott figured out how to print money in good times and bad.

II. J. Willard Marriott: The Founder's Story

The boy who would build a hospitality empire spent his childhood in the high desert of Utah, where winter temperatures plunged to 30 below zero and summer brought scorching heat that cracked the earth. John Willard Marriott—he'd drop the "John" as soon as he could—was born in 1900 in Marriott Settlement, a Mormon community named for his grandfather who'd traveled west with Brigham Young. His father, Hyrum, was a sheepherder who owned little more than rocky land and stubborn livestock. By age eight, young Willard was riding alone into the hills to tend sheep, learning lessons about self-reliance that would shape everything that followed.

The work was brutal. At fourteen, Willard was loading sheep onto railroad cars in Ogden, accompanying them on journeys to markets in San Francisco and Omaha. He'd sleep in the livestock cars, the smell of wool and manure filling his nostrils, counting every nickel earned. Years later, when Marriott executives complained about difficult business conditions, J.W. (as he became known) would remind them about sleeping with sheep in freezing boxcars. "When they were sick, he went to see them. When they were in trouble, he got them help," an early biographer noted—but J.W. wasn't talking about sheep. He was describing the management philosophy he'd carry from those Utah hills to corporate boardrooms.

The transformation from shepherd to entrepreneur began with his Mormon mission. At nineteen, the Church of Jesus Christ of Latter-day Saints sent him to New England, where he spent two years knocking on doors, facing rejection, and learning the art of persuasion. But it was what happened after his mission that changed everything. In 1921, he enrolled at Weber College in Ogden, then transferred to the University of Utah. To pay tuition, he sold woolen underwear to lumberjacks—another exercise in convincing skeptical customers to part with hard-earned money.

The pivotal moment came in 1922 when a cousin, Hugh Colton, convinced him that Washington, D.C. held more opportunity than Utah ever could. Colton had been selling A&W root beer franchises and painted a picture of the nation's capital as a goldmine of government workers with steady paychecks and few places to spend them. J.W. bought a one-way train ticket east, arriving with little more than ambition and a Mormon's abstention from alcohol—ironically perfect for selling root beer.

For five years, Marriott and Colton saved every penny, working various jobs while scouting locations and studying the capital's eating habits. They noticed patterns others missed: government workers had short lunch breaks and predictable schedules. The city sweltered in summer but had few places serving cold drinks. The growing ranks of female secretaries wanted quick, respectable places to eat. By 1927, they'd saved $1,500 each—enough to secure an A&W franchise and lease a small storefront on 14th Street, in the heart of D.C.'s business district.

The timing seemed perfect. America was riding high in the Roaring Twenties. Prosperity was spreading beyond the wealthy to create a new middle class of office workers. But J.W.'s masterstroke wasn't opening in spring—it was what he did when winter arrived. As temperatures dropped, root beer sales plummeted. Most operators would have closed for the season. Instead, Marriott convinced A&W to let him add hot food to the menu, a radical departure from their cold-drinks-only model.

Here's where Marriott's genius for relationships paid off. His wife, Alice Sheets—a University of Utah graduate he'd married just weeks after opening the root beer stand—had befriended the chef at the Mexican Embassy. When J.W. explained their predicament, the chef shared recipes for chili, tamales, and barbecue beef sandwiches. Alice cooked in the tiny back kitchen while J.W. served customers up front. They called it "The Hot Shoppe," and within weeks, lines stretched down 14th Street.

The formula was deceptively simple: quality food, served fast, at prices government clerks could afford. But the execution required fanatical attention to detail. J.W. would arrive at 5 AM to check deliveries, taste-test every batch of chili, and ensure the root beer was perfectly carbonated. He'd stay until midnight, counting receipts and planning the next day. When employees called in sick—which happened often in those days before modern healthcare—J.W. would work their shifts himself.

This hands-on approach created something unusual in 1920s food service: genuine employee loyalty. While other restaurants faced constant turnover, Hot Shoppe workers stayed for years. J.W. knew their names, their families, their problems. When a cook's child needed medical care, J.W. paid the bills. When a waitress's husband lost his job, J.W. found him work. This wasn't charity—it was investment. Loyal employees meant consistent food, which meant repeat customers, which meant predictable profits.

By 1928, the single Hot Shoppe had proven the concept. But J.W. saw bigger opportunity. Automobiles were transforming American life, yet few restaurants catered to this new mobile population. Working with a local architect, Marriott designed the East Coast's first drive-in restaurant, where customers could eat in their cars, served by "running boys" who'd sprint orders from kitchen to automobile. It was an instant sensation, combining America's love affair with cars with its growing appetite for convenience.

The boy from Marriott Settlement had discovered something profound: success came not from revolutionary ideas but from perfect execution of simple concepts. Quality, consistency, value, and treating employees like family—these weren't breakthrough innovations. But nobody else combined them with such relentless discipline. As the 1920s roared to a close, J. Willard Marriott had built the foundation for an empire. He just didn't know it yet.

III. Building the Restaurant Empire (1927–1957)

The stock market crash of October 1929 should have destroyed the Hot Shoppes. All around Washington, restaurants shuttered as government budgets shrank and federal workers lost their jobs. Yet somehow, Marriott's little chain survived—and then thrived. By 1932, while America sank deeper into Depression, J.W. was operating seven locations, serving hot meals to government workers who still had jobs and offering five-cent coffee to those who didn't. The secret wasn't generosity—it was arithmetic. Marriott had figured out that keeping customers coming during bad times, even at tiny margins, preserved the habits that would pay off when prosperity returned.

The 1930s revealed J.W.'s particular genius for reading America's changing appetites. As the federal government expanded under Roosevelt's New Deal, Washington's population exploded with young bureaucrats far from home. They craved comfort food but had neither kitchens nor wives to cook it. Hot Shoppes became their surrogate dining rooms, serving pot roast on Sundays and turkey on Thursdays, maintaining the rhythms of home cooking at restaurant scale. J.W. personally tested every new menu item, often sending dishes back to the kitchen dozens of times until they matched his exacting standards.

The real breakthrough came in 1934 when Marriott noticed something odd: Hot Shoppe sales spiked whenever a new airline route launched from Washington's Hoover Airport. Investigating further, he discovered passengers were buying food to take on flights, where no meals were served. Within months, J.W. had negotiated the world's first airline catering contract with Eastern Air Transport, preparing box lunches in Hot Shoppe kitchens for $0.35 each. It seemed like a small sideline. It would eventually become a billion-dollar business.

The perfectionist culture that would define Marriott for generations crystallized during these years. J.W. became legendary for surprise inspections, showing up at 2 AM to check coffee freshness or hiding in parking lots to time service speed. "His managers never knew what time of day or night he'd show up," recalled an early employee. One night, he found a cook smoking near food preparation—the man was fired on the spot, despite being the nephew of a city councilman. Word spread: Marriott standards were non-negotiable.

This obsession with quality control might have seemed excessive for a restaurant chain, but J.W. understood something his competitors didn't. In a business with tiny margins and fierce competition, the only sustainable advantage was flawless execution. While rivals competed on price or gimmicks, Marriott competed on reliability. A Hot Shoppe meal in 1937 tasted exactly like one in 1934, whether ordered in Georgetown or Silver Spring. This consistency bred the kind of customer loyalty that would survive wars and recessions.

World War II tested this model like nothing before. By 1942, Marriott juggled 24 Hot Shoppes across Washington, Philadelphia, and Baltimore, but wartime rationing made everything complicated. Sugar vanished. Meat required ration stamps. Young male employees enlisted en masse. Revenue plummeted as gas rationing kept customers home. Most restaurant chains retreated, closing locations and waiting for peace. J.W. saw opportunity.

The war had created two massive new markets: defense workers who needed feeding and government buildings that needed cafeteria management. Marriott bid aggressively for contracts to run dining facilities at the Pentagon, Navy yards, and defense plants. The margins were terrible—often just 1-2%—but the volume was enormous. More importantly, these contracts provided steady cash flow when traditional restaurant revenue was unpredictable. By 1945, Marriott was serving 50,000 defense workers daily, learning lessons about high-volume food service that would prove invaluable decades later.

The post-war boom transformed everything. Returning GIs married, had children, and moved to new suburbs sprouting around every American city. They bought cars, took road trips, and ate out more than any generation in history. Hot Shoppes rode this wave perfectly, opening locations along the new highways connecting suburbs to cities. The menu evolved too—adding fried chicken, hamburgers, and milkshakes to appeal to young families. Drive-in service, suspended during gas rationing, returned with carhops on roller skates and neon signs visible from half a mile away.

But J.W.'s shrewdest move was recognizing that Hot Shoppes had become more than restaurants—they were community gathering places. Teen-agers held first dates in the parking lots. Families celebrated birthdays in the dining rooms. Business deals were struck over coffee and pie at the counters. This social function meant Hot Shoppes could charge slightly more than pure fast-food competitors. Parents would pay extra for a "respectable" place where their daughters could work or eat safely.

By 1953, the nine-stool root beer stand had multiplied into 56 restaurants serving 30 million customers annually. Sales topped $20 million. The company had gone public in 1953, though J.W. retained iron control through super-voting shares. Hot Shoppes had become one of America's largest restaurant chains, mentioned in the same breath as Howard Johnson's and Big Boy. Yet J.W. was growing restless.

The restaurant business, he'd learned, had fundamental limitations. Growth required constant capital for new locations. Managing far-flung sites was increasingly difficult as the chain spread beyond J.W.'s ability to personally inspect. Most troubling, margins were stuck in single digits no matter how efficiently they operated. After a quarter-century building the perfect restaurant company, J. Willard Marriott began wondering if he was in the wrong business entirely.

The answer would come from an unexpected source: his son, Bill Jr., fresh from Navy service and University of Utah business school, who saw something his father initially missed. Those same highways filling Hot Shoppes parking lots were creating demand for something else—places to sleep. The American road trip needed more than food; it needed lodging. And nobody was providing it with Marriott-level consistency. The stage was set for the company's most dramatic pivot.

IV. The Hotel Pivot: Twin Bridges and Beyond (1957–1972)

J.W. Marriott stood on a muddy construction site in Arlington, Virginia, watching steel beams rise into the gray January sky of 1956. At 56, after three decades building a restaurant empire, he was gambling everything on a business he barely understood. The Twin Bridges Motor Hotel, under construction just minutes from National Airport, would cost $9 million—more than the combined investment in every Hot Shoppe ever built. Board members called it reckless. Competitors whispered about "Marriott's Folly." Even Alice, his usually supportive wife, wondered if success had finally gone to her husband's head.

The idea had actually been percolating since 1953, when J.W. purchased eight acres near Hot Shoppe No. 8, sensing something others missed. National Airport was about to enter the jet age. Boeing's 707 would soon shrink cross-country flights from eight hours to four. Business travel would explode. These travelers would need places to stay—not the downtown hotels charging $30 a night, not the seedy motor courts renting rooms by the hour, but something in between: clean, consistent, affordable lodging aimed at the emerging middle-market business traveler.

Bill Marriott Jr. had been pushing the hotel concept since returning from the Navy in 1954. At 22, armed with fresh University of Utah business degree, he saw what his father initially resisted: restaurants were a tough, low-margin grind, while hotels could generate returns that made food service look like charity work. A Hot Shoppe might net 5% on a good day. A well-run hotel could clear 20%. More intriguingly, hotels created multiple revenue streams—rooms, restaurants, bars, meeting spaces—from a single piece of real estate.

The generational tension was palpable. J.W. had built his identity around feeding America; Bill Jr. wanted to house it. "We know food, not beds," J.W. would growl during heated family discussions. But Bill Jr. had done his homework, studying every motor hotel from California to Florida, timing check-ins, measuring rooms, interviewing travelers about their frustrations. He discovered something profound: while America had plenty of hotels, nobody was applying the systemization that made Hot Shoppes successful. Every Holiday Inn was different. Howard Johnson's focused more on restaurants than rooms. Quality varied wildly even within chains.

The Twin Bridges Motor Hotel that opened on January 16, 1957, was revolutionary precisely because it wasn't. No swimming pools shaped like guitars, no themed rooms, no gimmicks—just 365 rooms that were clean, comfortable, and identical. Every bed was firm. Every shower had strong pressure. Every room had air conditioning (still rare in 1957), a television, and a telephone. The attached Hot Shoppe restaurant meant guests never had to leave the property. Pricing at $8-12 per night split the difference between downtown luxury and roadside motels.

Opening week was a disaster. A snowstorm kept travelers away. Pipes froze. The accounting system crashed. Occupancy hovered at 30%. J.W., who'd been checking registration cards personally each morning, grew increasingly agitated. Six weeks in, board members suggested cutting losses. Then, as spring arrived and business travel resumed, something magical happened. Word spread among the government contractors and corporate salesmen who frequented National Airport: the new Marriott motor hotel was different. By summer, occupancy hit 90%. By year-end, Twin Bridges had generated more profit than five Hot Shoppes combined.

The lessons came fast and hard. Hotels were infinitely more complex than restaurants—hundreds of employees instead of dozens, thousands of moving parts instead of hundreds. But they were also more forgiving. A bad meal ruined one customer experience; a bad night's stay could be salvaged with free breakfast or late checkout. Hotels generated revenue 24 hours a day, not just at meal times. Most remarkably, while restaurant customers might visit weekly, business travelers needed rooms nightly when traveling. The frequency and ticket size were game-changing.

Bill Jr., now officially executive vice president, pushed for rapid expansion. The Key Bridge Motor Hotel opened in 1959, just two miles from Twin Bridges but capturing different traffic patterns. Dallas followed in 1960, chosen because American Airlines was establishing a hub there. Philadelphia in 1961, Atlanta in 1965—each location selected through careful analysis of airline routes, business growth, and competitor weaknesses. This wasn't the scatter-shot expansion of Holiday Inn. Every Marriott hotel was a calculated bet on specific travel patterns.

The systemization that J.W. had perfected in restaurants proved even more powerful in hotels. Marriott created the industry's first detailed operations manual—a phone-book-thick document specifying everything from the thread count of sheets (200 minimum) to the greeting desk clerks should use ("Good morning, welcome to Marriott" never just "Next"). Housekeepers followed 66-point checklists. Kitchen staff prepared food according to Hot Shoppe recipes. Nothing was left to chance or individual interpretation.

This standardization enabled something competitors couldn't match: predictable quality at scale. A business traveler checking into the Atlanta Marriott in 1966 knew exactly what to expect because it was identical to the Philadelphia Marriott he'd stayed at the previous month. This reliability became Marriott's calling card, worth premium pricing in a market where consistency was rare. While Holiday Inn competed on ubiquity and Howard Johnson's on familiarity, Marriott competed on excellence.

The international expansion began almost accidentally. In 1966, Marriott acquired an airline catering kitchen in Caracas, Venezuela, to service the growing Latin American routes. Local businessmen, familiar with Marriott's reputation, begged them to build a hotel. J.W. resisted—managing properties thousands of miles away seemed impossible. But Bill Jr. saw opportunity. The same American business travelers filling domestic Marriotts were increasingly flying internationally. They'd pay premium prices for familiar quality in foreign cities.

The acquisition strategy that would define Marriott's next phase began with the 1967 purchase of the Camelback Inn in Scottsdale, Arizona. Rather than build from scratch, Marriott bought an existing luxury resort with established clientele and immediately applied their operational discipline. Occupancy jumped 20% within a year. The model was proven: acquire underperforming properties, apply Marriott systems, and watch profits soar. The Essex House overlooking Central Park, purchased in 1969, validated this approach in the luxury segment.

By 1972, when Bill Jr. officially succeeded his father as CEO (though J.W. remained chairman, unable to fully let go), Marriott operated 27 hotels generating more revenue than their 75 Hot Shoppes. The transformation was complete: a restaurant company that happened to own hotels had become a hotel company that happened to run restaurants. But this was just the beginning. Bill Jr. had bigger plans—diversification into every corner of American consumer spending. The conglomerate era was about to begin.

V. Conglomerate Era & Diversification (1972–1993)

Bill Marriott Jr. took the CEO reins in 1972 with the confidence of a man who'd already proven his skeptics wrong once. The hotel business had validated his vision, but why stop there? American corporations were embracing conglomerate fever—ITT owned rent-a-cars and insurance companies, Gulf+Western produced movies and manufactured auto parts. If Marriott could systemize restaurants and hotels, why not cruise ships, theme parks, and retirement homes? The next two decades would test whether operational excellence could transcend industry boundaries, or whether hubris had finally infected the house that J.W. built.

The diversification started logically enough. In 1967, shortly before becoming CEO, Bill Jr. had convinced the board to acquire Big Boy Restaurants, seeing synergy with Hot Shoppes' expertise. By 1973, he'd launched Roy Rogers Roast Beef, aimed directly at McDonald's growing dominance. The logic seemed impeccable: Marriott understood food service better than anyone, and fast food was exploding. Within five years, Roy Rogers had 100 locations generating solid returns. But something subtle was happening—management attention was fragmenting. Every hour spent perfecting roast beef sandwiches was an hour not spent on hotel expansion.

The real departure from core competency came with Sun Line Cruises, launched in 1974. Bill Jr. saw cruising as "floating hotels," a natural extension of hospitality. He hired Norwegian executives, bought Greek ships, and targeted middle-American customers who'd never considered ocean voyages. The first sailing of the Stella Solaris from Miami was a triumph—full occupancy, rave reviews. But ships, Marriott discovered, were nothing like hotels. Maritime regulations, international crews, weather dependencies, and mechanical complexity created operational nightmares that no amount of systemization could solve.

The theme park adventure was even more audacious. In 1976, Marriott paid $250 million for three Great America parks in California, Illinois, and Maryland—massive entertainment complexes with roller coasters, concerts, and seasonal workforces of thousands. Bill Jr. believed Marriott's service culture could differentiate them from Disney and Six Flags. The parks were gorgeous, impeccably maintained, with the cleanest bathrooms in the amusement industry. They also hemorrhaged money. Entertainment required skills Marriott didn't possess: show production, ride design, teenage workforce management. By 1984, they'd sold the parks for less than invested, taking their first major write-down.

Yet even as these adventures foundered, the core hotel business was evolving in fascinating ways. The masterstroke came in 1983 with Courtyard by Marriott, a brand invented through unprecedented market research. Bill Jr. assembled teams of business travelers—the road warriors filling regular Marriotts—and had them design their ideal hotel. The result was revolutionary: smaller lobbies (business travelers didn't socialize), bigger rooms (they worked in them), better desks and lighting, limited food service but excellent coffee. Courtyard wasn't just another brand; it was customer-centric design before Silicon Valley made it fashionable.

The success of Courtyard—100 hotels within seven years—proved Marriott could innovate within hospitality even while struggling outside it. Fairfield Inn followed in 1987, targeting budget-conscious business travelers. Residence Inn, acquired in 1987, served extended-stay guests. Each brand targeted specific customer segments with surgical precision. This portfolio approach was brilliant: Marriott could capture a business traveler at every price point and trip purpose without cannibalizing existing properties.

The senior living venture, launched in 1984, seemed to combine Marriott's hospitality expertise with demographic inevitability. America was aging, and wealthy retirees wanted alternatives to traditional nursing homes. Marriott Senior Living Services offered apartment-style residences with hotel-like amenities—dining rooms, concierge services, housekeeping. The facilities were beautiful, the care exceptional. But healthcare regulations, insurance complexities, and the emotional intensity of eldercare created challenges that blindsided Marriott's operators. This wasn't hospitality; it was healthcare with hospitality characteristics.

The financial engineering of this era deserves special attention. Marriott had discovered something powerful: they could build hotels, operate them until stabilized, then sell the real estate while retaining long-term management contracts. This recycled capital for new development while keeping the predictable management fees. By 1985, Marriott was one of America's largest real estate developers, but their balance sheet was increasingly strained. Interest rates were rising, construction costs soaring, and Wall Street was growing nervous about leverage.

The 1985 death of J.W. Marriott at age 84 marked a symbolic transition. The founder had watched his son's diversification with increasing skepticism, occasionally emerging from semi-retirement to voice displeasure. "Why are we running roller coasters?" he'd ask at board meetings. His death removed the last restraint on Bill Jr.'s ambitions, but also eliminated the institutional memory of what made Marriott special: focus, discipline, and doing ordinary things extraordinarily well.

The November 1989 restructuring announcement shocked Wall Street. Marriott would sell its airline catering division (the business that started it all) to Caterair for $570 million. The restaurant division, including Hot Shoppes, Big Boy, and Roy Rogers, went to Hardee's for $365 million in 1990. The symbolism was profound: Marriott was exiting the food service business that created it. But the logic was irrefutable. Airline catering had become a commodity business with tiny margins. Restaurants faced saturation and changing consumer preferences. Meanwhile, hotels were generating returns that made everything else look like charity work.

The early 1990s recession exposed the fatal flaw in Marriott's model: owning real estate during downturns was brutal. Occupancy plummeted, property values collapsed, and debt service remained fixed. By 1992, Marriott's stock had fallen 70% from its peak. Bond holders were revolting. Something dramatic was needed. Bill Jr. and CFO Stephen Bollenbach hatched perhaps the boldest financial restructuring in American corporate history: split the company in two.

The plan was elegant and controversial. Marriott International would keep the "good" assets—management contracts, franchise agreements, and the valuable brand names. Host Marriott (later Host Hotels & Resorts) would inherit the "bad" assets—real estate, debt, and the capital-intensive ownership model. It was financial engineering at its most aggressive, essentially stuffing all the problems into one entity while keeping all the value in another. Bondholders sued, claiming fraudulent conveyance. Shareholders initially rebelled.

But Bill Jr. pushed through, completing the split in October 1993. Critics called it financial manipulation. Supporters saw genius—Marriott had invented the asset-light hospitality model that would define the industry's next generation. The new Marriott International would own almost no real estate, instead collecting fees for managing properties others owned. It was a complete repudiation of the build-and-own model J.W. had created, yet somehow perfectly aligned with his philosophy of doing what you do best and nothing more.

VI. The Split & Asset-Light Revolution (1993–2016)

The lawyers gathered in Marriott's Bethesda boardroom on October 8, 1993, to sign papers that would fundamentally rewire American hospitality. The split creating Marriott International and Host Marriott wasn't just financial engineering—it was philosophical revolution. For 66 years, the Marriott way meant owning what you operated. Now, Bill Jr. was betting everything on the opposite: operational excellence divorced from capital intensity. The old Marriott built hotels; the new Marriott would build brands.

Wall Street initially hated it. The stock dropped 20% on announcement day. Bondholders, stuck with Host Marriott's overleveraged real estate, filed lawsuits claiming fraudulent transfer. Corporate governance advocates called it the worst example of shareholder abuse in modern history. But Bill Jr. understood something critics missed: the hotel business was actually two businesses awkwardly combined. Real estate investment required massive capital, cyclical returns, and tolerance for leverage. Hotel management required operational expertise, brand building, and human capital. Trying to excel at both was like being a world-class chef who also had to own the farm.

The numbers told the story. Pre-split Marriott generated roughly 8% returns on assets, dragged down by billions in real estate carrying costs. Post-split Marriott International, freed from property ownership, would generate 40%+ returns on its minimal asset base. Management fees—typically 3% of revenue plus incentives—came with 70% margins. Franchise fees were nearly pure profit. The capital that once built a single hotel could now fund management contracts for dozens. It wasn't just a better model; it was a different business entirely.

The transformation required rewiring Marriott's DNA. For decades, the company had hired construction managers, real estate lawyers, and development executives. Now it needed brand marketers, franchise sales teams, and contract negotiators. The culture shift was jarring. Old-timers who'd spent careers selecting carpet for lobbies suddenly had to think about brand positioning for Asian business travelers. But Bill Jr. moved decisively, hiring Procter & Gamble marketers and McDonald's franchising experts. Marriott would become a brand management company that happened to focus on hotels.

The Ritz-Carlton acquisition in 1995 demonstrated the new model's power. The legendary luxury chain was hemorrhaging money, with beautiful properties but inconsistent operations. The old Marriott would have needed billions to buy the real estate. The new Marriott paid just $200 million for 49% of the management company, then another $131 million for full control in 1998. They didn't buy buildings; they bought the right to manage them. Within three years, Ritz-Carlton was solidly profitable, its operational chaos replaced by Marriott's systematic excellence while maintaining its luxury positioning.

This period saw Marriott perfect the art of brand segmentation. Each brand targeted specific psychographics with scientific precision. Ritz-Carlton for luxury traditionalists. Renaissance (acquired in 1997) for boutique-seeking sophisticates. SpringHill Suites for families needing space. TownePlace Suites for extended stays. The genius wasn't just having multiple brands but ensuring they never cannibalized each other. A city might have six Marriott properties, each serving different segments, maximizing market capture without internal competition.

The international expansion strategy reflected asset-light advantages. In China, India, and the Middle East, Marriott could partner with local developers who provided capital while Marriott provided expertise. A Saudi prince wanting a luxury hotel in Riyadh didn't need Marriott's money—he needed their systems, training, and reservation network. Marriott could expand globally without currency risk, political exposure, or capital requirements. By 2005, international properties generated 20% of fees with minimal investment.

The digital transformation starting in 1995 with Marriott.com perfectly complemented the asset-light model. Online reservations reduced distribution costs from 10% (through travel agents) to essentially zero for direct bookings. Customer data enabled targeted marketing impossible in the analog era. The Marriott Rewards program, launched in 1997, created switching costs that locked in high-value travelers. Technology wasn't just operational efficiency; it was competitive moat-building.

The 2008 financial crisis validated the model brutally. Competitors with heavy real estate exposure faced bankruptcy. Lehman Brothers' collapse vaporized hotel financing globally. Property values crashed 40%. But Marriott International barely flinched. Yes, revenues dropped as occupancy plummeted, but without debt service on owned properties, the company remained profitable throughout. They actually accelerated development, signing management contracts for distressed properties at favorable terms. The crisis that destroyed capital-intensive competitors became Marriott's opportunity.

By 2010, the transformation was complete. Marriott International managed $13 billion in revenue but generated it through others' assets. The company employed 300,000 people but most worked for property owners, not Marriott. They controlled 3,500 properties without owning them. Return on invested capital exceeded 50%. The stock price had increased 10-fold since the split. Bill Jr.'s gamble had paid off spectacularly.

The competitive dynamics had also shifted. Hilton, Marriott's eternal rival, had gone private in 2007 in a leveraged buyout that left it saddled with debt. Hyatt remained family-controlled and conservative. InterContinental Hotels Group had followed Marriott's asset-light model but lacked their operational excellence. Starwood Hotels had great brands but subscale distribution. The industry was ripe for consolidation, and Marriott had the currency—a high-valued stock and proven integration capabilities—to be the acquirer.

Yet challenges emerged. The asset-light model's very success created new problems. Without ownership leverage, Marriott had less control over property quality. Franchise hotels might cut corners, damaging brand reputation. Management contracts typically ran 20-30 years, but if properties changed hands, new owners might terminate early. The company was increasingly dependent on development partners who might favor competitors. Most concerning, Airbnb had launched in 2008, offering travelers alternatives Marriott couldn't match—unique properties, local experiences, and prices that undercut hotels.

Bill Jr., now in his eighties but still firmly in control, faced a classic innovator's dilemma. Marriott had perfected the asset-light hotel model just as technology threatened to disrupt hotels entirely. Online travel agencies controlled distribution. Google controlled discovery. Airbnb offered differentiation. Chinese chains were scaling rapidly. The company needed something transformational, not incremental. It needed scale that would make it indispensable to property owners, travelers, and distribution partners.

The answer would come through the largest acquisition in lodging history—a deal so complex it would take two years to complete, face regulatory scrutiny across continents, and ultimately reshape global hospitality. Marriott's pursuit of Starwood Hotels & Resorts would test whether operational excellence could successfully integrate competing cultures, whether scale still mattered in the digital age, and whether Bill Jr. had one more transformation left in him.

VII. The Starwood Mega-Deal & Modern Era (2016–Present)

The phones wouldn't stop ringing in Arne Sorenson's Bethesda office on November 16, 2015. After months of secret negotiations, Marriott had just announced its intention to acquire Starwood Hotels & Resorts for $13.3 billion, creating the world's largest hotel company. Investment bankers were calling to congratulate. Competitors were calling to probe. But Sorenson, Marriott's first non-family CEO since taking over from Bill Jr. in 2012, knew the real work hadn't even started. This wasn't just an acquisition—it was an attempt to consolidate an industry while digital disruption threatened its very foundation.

The pursuit of Starwood had begun eighteen months earlier, when whispers emerged that the Stamford-based company was exploring strategic options. Starwood put itself up for sale in April 2015, frustrated by its inability to match rivals' growth, particularly in limited-service segments. For Marriott, this was the opportunity of a generation. Starwood's portfolio included some of hospitality's most coveted brands: St. Regis for old-money luxury, W for hip urbanites, Westin for wellness-focused travelers, and Sheraton, despite its challenges, remained one of the world's most recognized hotel names.

But the real prize was Starwood Preferred Guest—a loyalty program whose members were deeply loyal, had generally higher incomes and tended to spend many nights on the road. SPG members were the Navy SEALs of business travelers—influential, demanding, and fanatically devoted. They chose hotels based on SPG availability, influenced corporate travel policies, and evangelized the program with religious fervor. Marriott Rewards had more members, but SPG had more passion. Combining them would create an unassailable moat.

The deal structure reflected lessons from decades of M&A experience. Each stockholder would receive $21 cash and 0.8 shares of Marriott International Class A common stock for each of their existing Starwood stocks. This mix of cash and stock aligned incentives—Starwood shareholders would benefit from future synergies while receiving immediate value. The $250 million in projected annual cost synergies seemed conservative, focused on eliminating duplicate corporate functions, combining procurement, and integrating technology platforms.

The integration planning revealed Starwood's operational challenges. While its brands were aspirational, execution was inconsistent. W Hotels in New York delivered cutting-edge experiences; W Hotels in secondary markets felt dated. Sheraton, once Starwood's flagship, had suffered from years of underinvestment. Property owners complained about weak RevPAR growth and limited renovation support. The sales force was fragmented, with different teams calling on the same corporate accounts. Technology systems were a patchwork of acquisitions never fully integrated.

Then came the plot twist. In March 2016, just as shareholders prepared to vote, a consortium led by China's Anbang Insurance Group submitted a $78 per share all-cash offer, trumping Marriott's bid. The financial media went wild—a Chinese insurance company nobody had heard of was trying to buy one of America's iconic hotel companies. Marriott's board faced a dilemma: match the offer and destroy their returns, or walk away and miss the transformational opportunity.

Sorenson's response was masterful. Rather than panic, Marriott raised its bid to $13.6 billion but kept the cash-stock structure. They emphasized what Anbang couldn't offer: operational expertise, distribution power, and certainty of closing. The Chinese consortium, facing regulatory scrutiny and financing questions, withdrew three days later. Marriott had won, but the drama had cost them $300 million extra and revealed how desperately they needed this deal.

On September 23, 2016, the acquisition officially closed. The numbers were staggering: 30 brands, 5,700 properties, 1.1 million rooms across 110 countries. More than 1 out of every 15 hotel rooms globally now flew a Marriott flag. The company's distribution footprint had doubled in Asia, tripled in the Middle East, and added luxury properties in markets where Marriott had been weak. But numbers only told part of the story.

The real challenge was cultural integration. Starwood employees saw themselves as innovators in a stodgy industry—they'd invented category-defining brands, pioneered lifestyle hotels, and built the world's most passionate loyalty program. Marriott employees saw themselves as operational excellence personified—they ran hotels profitably, consistently, and at scale. Starwood was jazz; Marriott was symphony. The question was whether they could play together.

The loyalty program integration became the public test of merger success. Members could link accounts and transfer points immediately, with each Starwood point worth three Marriott Rewards points. But the full integration would take two years, as teams wrestled with incompatible IT systems, different elite tier structures, and divergent redemption philosophies. SPG members scrutinized every change, ready to revolt if their beloved program was diminished.

Behind the scenes, Marriott applied its integration playbook with military precision. Every Starwood property received a 500-point inspection, identifying gaps in Marriott standards. Underperforming general managers were replaced. Procurement contracts were renegotiated, saving millions on everything from mattresses to mini-bar supplies. Sales teams were reorganized around global accounts. The reservation systems, after enormous investment, were finally integrated in 2018.

The creation of Marriott Bonvoy in February 2019 marked the merger's symbolic completion. The unified loyalty program boasted 140 million members, offering benefits across all 30 brands. Points became currency accepted everywhere from Courtyard to St. Regis. Elite members gained reciprocal benefits across portfolios. The program's scale created a gravitational pull—hotels wanted to join for the customer flow, customers joined for the choice, creating a virtuous cycle competitors couldn't match.

COVID-19 arrived just as integration benefits were materializing. The pandemic decimated hospitality—occupancy rates fell below 20%, thousands of hotels closed temporarily, revenue evaporated overnight. But Marriott's scale proved decisive. They could negotiate with lenders on behalf of franchisees, provide operational guidance based on data from 141 countries, and maintain marketing presence when smaller chains went dark. The asset-light model meant Marriott's survival was never in question, even as property owners struggled.

The recovery revealed the merger's strategic brilliance. As travel resumed, Marriott captured outsized share. Business travelers, seeking consistency after chaotic years, defaulted to the safety of Marriott's portfolio. Leisure travelers, armed with saved points and pent-up demand, found options from budget to luxury. The company's leverage with corporate travel departments who often look for one giant chain to house all of their employees proved decisive as companies consolidated vendors post-pandemic. The most recent chapter in Marriott's expansion story arrived in April 2025 with the $355 million acquisition of citizenM, a Netherlands-based lifestyle brand known for its tech-savvy, design-forward approach to the select-service segment. By July 2025, Marriott had completed the acquisition, adding 37 open hotels comprising 8,789 rooms across more than 20 cities in the U.S., Europe, and Asia Pacific. The deal represents Marriott's continued evolution—no longer just aggregating traditional hotel brands but actively seeking innovative concepts that appeal to younger, tech-native travelers who prioritize experience over square footage.

CitizenM's model—compact rooms with smart design, vibrant communal spaces, and self-service technology—offers Marriott a laboratory for innovation without risking established brands. It's a hedge against disruption, bringing in-house the kind of experimentation that might otherwise emerge as competition. The integration strategy mirrors the Starwood playbook: maintain brand independence while leveraging Marriott's distribution muscle and operational excellence.

Today's Marriott International stands as testament to the power of patient capital allocation and strategic evolution. From a nine-stool root beer stand to managing 1.7 million rooms, from owning everything to owning almost nothing, from domestic focus to global dominance—each transformation built on the last, creating compound advantages competitors struggle to replicate.

VIII. Business Model & Strategy Deep Dive

The genius of Marriott's business model lies not in what it owns but in what it controls. After decades of evolution, the company has engineered one of capitalism's most elegant machines: turning other people's real estate investments into predictable, high-margin fee streams while bearing minimal capital risk. Understanding how this machine works—its gears, lubricants, and outputs—reveals why Marriott trades at premium multiples despite operating in a commoditized industry.

The fee structure forms the engine's core. Base management fees, typically 3% of gross revenues, provide the steady heartbeat—collected whether properties are profitable or not. These fees flow through even during downturns, as owners must pay Marriott before their own returns. Incentive fees, usually 20-50% of profits above specified thresholds, create upside during good times without downside exposure during bad times. Franchise fees, ranging from 4-6% of room revenue, require even less involvement—Marriott provides the brand and systems while franchisees handle everything else.

Consider the unit economics of a typical 200-room Marriott-branded hotel generating $15 million in annual revenue. Marriott collects roughly $450,000 in base fees (3% of revenue) plus perhaps $200,000 in incentive fees if the property performs well. For this $650,000, Marriott provides brand power, reservation systems, loyalty program access, operational standards, and management expertise. The property owner bears all capital costs—land, construction, maintenance, renovations—typically investing $30-40 million. Marriott's investment? Essentially zero beyond initial business development costs.

This asymmetry becomes more powerful at scale. Marriott expects to achieve $250 million in annual corporate cost synergies from the Starwood acquisition alone. Technology platforms that cost hundreds of millions to build serve thousands of properties, making per-property costs negligible. Global sales teams calling on Fortune 500 accounts benefit all properties simultaneously. The loyalty program, with 140+ million members, drives direct bookings that reduce distribution costs while increasing property revenues—benefiting both owners and Marriott's incentive fees.

The brand segmentation strategy represents sophisticated market segmentation rarely seen outside consumer packaged goods. Marriott's 37+ brands aren't random accumulation—they're carefully positioned to capture every conceivable travel occasion and price point without cannibalization. Ritz-Carlton and St. Regis compete for ultra-luxury travelers who'd never consider other options. Courtyard and Fairfield Inn serve different business traveler psychographics despite similar prices. Moxy and Aloft target millennials seeking experience over space. Each brand has distinct design standards, service levels, and personality, allowing Marriott to capture maximum market share in any given city.

The power of this portfolio approach compounds in corporate negotiations. When Marriott pitches Microsoft or JPMorgan for their global travel programs, they're not selling individual hotels—they're selling comprehensive solutions. Need luxury hotels for executives? Check. Extended stay for consultants on long projects? Check. Budget options for junior staff? Check. Resort properties for company retreats? Check. This one-stop shopping creates switching costs that lock in corporate accounts for years.

International expansion leverages the asset-light model's inherent advantages. In China, India, or the Middle East, Marriott partners with local developers who understand regulations, have government relationships, and access cheap capital. These partners want Marriott's operational expertise and global distribution, not their money. A Saudi prince building a hotel in Riyadh gains more from Marriott's brand and systems than from any capital they might invest. This allows rapid expansion without foreign exchange risk, political exposure, or capital requirements.

The technology platform has evolved from operational necessity to competitive moat. Marriott.com and the mobile app drive over $20 billion in annual bookings, with direct bookings saving 10-15% versus OTA commissions. The property management systems standardize operations across thousands of hotels, enabling consistent service while reducing training costs. Revenue management algorithms optimize pricing across the portfolio, increasing RevPAR and thus incentive fees. Data from hundreds of millions of stays enables personalization that smaller chains can't match.

Marriott Bonvoy, the merged loyalty program, deserves special attention as a value-creation machine. Members generate 50% higher RevPAR than non-members and book directly 70% of the time, drastically reducing distribution costs. The program's 140+ million members represent a captive audience for credit card partnerships (generating hundreds of millions in annual fees), promotional partnerships, and experiences beyond traditional lodging. Points create float—money collected today for services delivered later—while breakage (points never redeemed) provides pure profit.

The capital allocation framework reflects this model's inherent advantages. Without significant capital requirements for growth, Marriott generates enormous free cash flow relative to its asset base. In 2024, the company generated over $3 billion in operating cash flow on minimal tangible assets. This cash funds three priorities: strategic brand acquisitions (like citizenM), technology investments that enhance the platform, and massive shareholder returns through dividends and buybacks. Since 2014, Marriott has returned over $15 billion to shareholders while simultaneously growing rooms by 50%.

The franchise versus management decision for each property involves complex tradeoffs. Management contracts provide more control and higher fees but require more oversight. Franchise agreements generate lower fees but need minimal involvement, making them perfect for experienced operators in stable markets. Marriott increasingly prefers franchising in North America where standards are established, while using management contracts in emerging markets requiring hands-on development. This hybrid approach maximizes fees while minimizing operational complexity.

Risk management in this model focuses on brand protection rather than asset preservation. A poorly run franchise can damage brand equity affecting thousands of properties. Hence Marriott's 500-point brand standards, regular inspections, and willingness to terminate agreements with non-compliant owners. The company spends hundreds of millions annually on quality assurance—not to protect assets they own, but to protect the intangible brand value that drives their fees.

The bear case for this model centers on its dependence on travel demand and economic cycles. When recession hits or pandemics strike, revenues evaporate quickly. Base fees provide some cushion, but incentive fees disappear entirely. The asset-light model means less downside but also less control—Marriott can't force owners to renovate or maintain standards during tough times. Competition for management contracts has intensified, compressing fees. And the model's success has attracted imitators, with every major chain now pursuing similar strategies.

Yet the bull case remains compelling. The model's scalability is nearly infinite—adding another thousand hotels requires minimal incremental corporate investment. Network effects grow stronger with scale as more properties make the loyalty program more valuable, which attracts more members, which makes properties more profitable, which attracts more owners seeking Marriott brands. The fee-based model provides inflation protection as fees rise with room rates. And global travel's long-term growth trajectory—driven by emerging market wealth creation, demographic shifts, and experiential spending preferences—provides a powerful tailwind.

The strategic brilliance lies in transforming a capital-intensive, cyclical, commodity business into a capital-light, recession-resistant, brand-driven platform. Marriott doesn't sell rooms—they sell the system that enables others to sell rooms profitably. It's the difference between owning gold mines and selling pickaxes during a gold rush. And after nearly a century of refinement, Marriott has built the world's best pickaxe.

IX. Competitive Analysis & Industry Dynamics

The global hotel industry resembles a chess match played across continents, with each major player pursuing distinct strategies while responding to common threats. Marriott's position as the world's largest operator provides advantages, but size alone doesn't guarantee victory in an industry where local execution matters as much as global scale. Understanding the competitive dynamics requires examining both traditional rivals and emerging disruptors who challenge the industry's fundamental assumptions.

Hilton remains Marriott's most direct competitor and eternal rival, their competition stretching back to the 1950s when Conrad Hilton and J. Willard Marriott would occasionally share drinks while secretly plotting each other's destruction. Today's rivalry is less personal but equally intense. Hilton's portfolio of 7,500+ properties across 18 brands mirrors Marriott's approach—asset-light, fee-based, globally distributed. But subtle differences matter. Hilton Honors generates higher revenue per member than Marriott Bonvoy, suggesting superior customer engagement. Hilton's Hampton Inn dominates the limited-service segment where Marriott's Fairfield Inn struggles. Yet Marriott's luxury portfolio far exceeds Hilton's, with Ritz-Carlton and St. Regis commanding price premiums Waldorf Astoria can't match.

The real battle occurs in development pipelines and owner relationships. Both companies court the same developers, often pitching competing brands for identical sites. A developer building a 200-room select-service hotel in Dallas might choose between Marriott's Courtyard and Hilton's Hampton Inn based on marginal differences in fee structures, territory protection, or corporate support. These micro-battles, repeated thousands of times globally, determine long-term market share. Marriott's pipeline includes three under-construction hotels totaling over 600 rooms that are anticipated to open by mid-2026 for citizenM alone, but Hilton's development team matches them deal for deal.

InterContinental Hotels Group (IHG) represents a different competitive model—even more asset-light than Marriott, with 90% of properties franchised versus Marriott's 70%. This ultra-light approach generates industry-leading margins but sacrifices quality control. Holiday Inn, despite being the world's most recognized hotel brand, suffers from inconsistent standards that damage its premium pricing power. IHG's recent acquisition of Six Senses luxury resorts signals recognition that pure franchising has limitations, especially in luxury segments where experience matters more than efficiency.

Hyatt occupies a unique position—smaller scale but superior positioning. With just 1,350 properties, Hyatt can't match Marriott's distribution advantages. But their portfolio skews heavily toward luxury and lifestyle brands that generate outsized RevPAR premiums. Park Hyatt, Andaz, and the recently acquired Thompson Hotels appeal to affluent travelers who actively avoid "chain" hotels. Hyatt's World of Hyatt loyalty program, despite having fewer members, generates higher engagement rates and credit card spending per member. It's a reminder that in hospitality, bigger isn't always better if you're serving the wrong customers.

Accor, Europe's largest hotel operator, demonstrates the challenges of geographic concentration. While dominant in France and strong across Europe, Accor struggles to gain traction in North America where business travel drives industry profits. Their 2016 acquisition of Fairmont, Raffles, and Swissôtel added luxury capability, but integration has proven difficult across different cultures and operating models. Accor's attempt to build a "lifestyle" division through acquisitions of boutique brands like 25hours and Mama Shelter shows everyone is chasing the same millennial traveler, but execution varies wildly.

The Chinese giants—Jin Jiang, Huazhu, and BTG Homeinns—represent tomorrow's competition. Jin Jiang, already the world's second-largest hotel company by room count, operates 10,000+ properties primarily in China. Their acquisition of Louvre Hotels and strategic partnership with Accor signals global ambitions. Huazhu's licensing agreement with Accor brings Western brands to China while preparing Chinese brands for international expansion. These companies benefit from a massive domestic market, government support, and capital access that Western chains can't match. When Chinese outbound travel fully recovers, these chains will follow their customers globally.

Airbnb stands as the industry's most significant disruptor, fundamentally challenging the assumption that travelers need traditional hotels. With 7+ million listings globally, Airbnb offers variety, authenticity, and often better value than hotels. For leisure travelers seeking unique experiences, a Tuscan villa or Tokyo apartment provides something no Marriott property can match. Airbnb's asset-lighter-than-light model—they don't even franchise, just facilitate—generates 80%+ gross margins that make Marriott's 20% operating margins look pedestrian.

Yet Airbnb's threat may be overstated for Marriott's core business. Business travelers, who generate 60% of industry profits, need consistency, corporate billing, and loyalty programs that Airbnb struggles to provide. Group travel for conferences and events requires infrastructure homes can't offer. And luxury travelers increasingly want both—hotels for reliability and Airbnb for authenticity—suggesting complementary rather than substitutional relationships. Marriott's response, launching "Homes & Villas by Marriott International" in 2019, acknowledges Airbnb's innovation while leveraging Marriott's distribution advantages.

Online Travel Agencies (OTAs) like Booking.com and Expedia represent frenemies—essential distribution partners who also pose existential threats. OTAs control customer relationships, charging hotels 15-25% commissions while commoditizing their product. Marriott's scale provides negotiating leverage smaller chains lack, but even they pay billions in OTA commissions annually. The battle for direct bookings has become existential, with Marriott offering member-only rates, mobile check-in, and room selection to incentivize direct relationships. Yet OTAs continue innovating, with Booking.com's "connected trip" vision threatening to intermediate the entire travel experience.

Labor dynamics increasingly shape competitive positioning. Marriott employs over 300,000 people globally, most working for property owners rather than corporate. Rising minimum wages, especially in urban markets, pressure operating margins and thus incentive fees. Union organizing efforts, particularly among housekeeping staff, create operational complexity. The post-COVID labor shortage has forced wage increases that fundamentally alter hotel economics. Marriott's reputation as a relatively worker-friendly employer—dating back to J.W.'s paternalistic approach—provides advantages in tight labor markets, but costs are rising industry-wide.

Environmental, Social, and Governance (ESG) pressures create new competitive dimensions. Marriott has committed to carbon neutrality by 2050, requiring massive investments in energy efficiency, renewable power, and sustainable operations. Younger travelers increasingly consider environmental impact when choosing hotels. Corporate clients demand sustainability reporting for their travel programs. These requirements favor large chains with resources to invest in sustainability over independents who can't afford solar panels or sophisticated recycling systems. But they also create vulnerabilities—Marriott's environmental footprint across 9,300 properties dwarfs boutique competitors who can claim authentic sustainability.

Technology disruption extends beyond OTAs and Airbnb. Google's travel products increasingly influence booking decisions, with 60% of travelers starting their research on Google. Meta-search engines like Trivago and Kayak commoditize pricing. Artificial intelligence promises to revolutionize revenue management, customer service, and personalization. Startups like Sonder are trying to combine Airbnb's apartment inventory with hotel-like consistency and technology. Each innovation threatens to disrupt existing competitive advantages.

The competitive landscape reveals an industry in transition. Traditional boundaries between hotels, homes, and experiences are blurring. Technology is both enabling new competitors and providing tools for incumbents to defend their positions. Scale advantages remain powerful but insufficient without innovation and execution. Marriott's competitive position—largest scale, broadest portfolio, proven execution—provides enormous advantages. But in an industry where a pandemic can eliminate 70% of revenue overnight, where a startup can achieve billion-dollar valuations without owning a single room, where Chinese companies can leverage home market scale to go global, competitive advantages feel increasingly temporary.

The winners will be those who successfully navigate multiple transitions simultaneously: from physical to digital distribution, from standardization to personalization, from Western to Asian demand centers, from business to leisure travel, from ownership to access. Marriott's track record suggests they're well-positioned for these transitions. But past performance, as they say in finance, doesn't guarantee future results.

X. Financial Analysis & Valuation

The numbers tell a story of remarkable financial engineering married to operational excellence. In 2024, Marriott achieved full year global RevPAR growth of 4.3 percent and, with record gross room additions of over 123,000, net rooms grew 6.8 percent to over 1.7 million rooms worldwide at year-end. The company made revenue of US$6.62 billion (up 5.0% from the previous year) in 2024, though the full revenue figure including cost reimbursements reaches $25.1 billion as noted earlier. Base management and franchise fees totaled $1,128 million in the 2024 fourth quarter, a 10 percent increase compared to base management and franchise fees of $1,026 million in the year-ago quarter.

The beauty of Marriott's financial model lies in its simplicity. Revenue flows from three primary streams: base management fees (typically 3% of hotel revenues), incentive fees (20-50% of profits above hurdles), and franchise fees (4-6% of room revenue). These fees require virtually no capital investment yet generate operating margins exceeding 20%. Compare this to traditional hotel ownership, where margins rarely exceed 10% and require massive capital deployment.

Adjusted EBITDA totaled $1,286 million in the 2024 fourth quarter, a 7 percent increase compared to fourth quarter 2023 adjusted EBITDA of $1,197 million. This EBITDA generation on minimal tangible assets produces returns on invested capital that would make Silicon Valley jealous. The asset-light model means that growth requires minimal capital—signing a management contract costs little beyond business development expenses, yet generates fees for decades.

The unit economics demonstrate the model's power. Consider a typical 250-room full-service Marriott generating $20 million in annual revenue. Marriott collects roughly $600,000 in base fees plus potentially $300,000 in incentive fees—$900,000 total. The property owner invested $50-60 million in land and construction. Marriott's investment? Perhaps $100,000 in pre-opening support and training. That's a 900% return in year one, repeating for the 20-30 year contract length.

The increase in fees is primarily attributable to RevPAR increases and unit growth, as well as higher residential and co-branded credit card fees. The credit card partnerships deserve special attention—these generate hundreds of millions in pure profit annually, as banks pay for access to Marriott's customer base. Members earn points for spending, driving loyalty without Marriott bearing any credit risk.

The shareholder return story is equally impressive. For full-year 2024, Marriott repurchased 15.4 million shares for $3.7 billion. Year to date through October 31, the company has returned $3.9 billion to shareholders through dividends and share repurchases. This massive capital return is possible precisely because the business requires so little capital for growth. While competitors reinvest in real estate, Marriott returns cash to shareholders.

The pipeline provides visibility into future growth. The company's worldwide development pipeline totaled 3,766 properties with over 577,000 rooms. The year-end pipeline included 1,381 properties with over 229,000 rooms under construction. These aren't speculative projects—properties under construction have committed capital and will open within 18-24 months. At current fee rates, this pipeline represents roughly $2 billion in additional annual fee revenue once operational.

Geographic mix increasingly favors international markets, which offer higher growth and often better fee structures. Fifty-five percent of rooms in the year-end pipeline are in international markets. Managed hotels in international markets contributed roughly 70 percent of the incentive fees earned in the quarter. International properties often require management rather than franchising, generating higher fees, and face less competition from domestic chains.

The valuation framework for Marriott requires thinking differently than traditional asset-heavy businesses. With minimal tangible assets, traditional price-to-book metrics are meaningless. Instead, investors focus on price-to-earnings, EV/EBITDA, and price-to-free-cash-flow multiples. At current prices around $250 per share and a market cap of $74.91 billion, Marriott trades at approximately 25x forward earnings—a premium to the market but justified by superior growth and returns.

The bear case centers on several vulnerabilities. Economic sensitivity remains high—when GDP contracts, business travel evaporates first. The incentive fee structure means earnings volatility exceeds revenue volatility. Competition for new management contracts has intensified, potentially compressing future fee rates. Labor cost inflation, particularly in developed markets, pressures hotel profitability and thus incentive fees. Technology disruption from OTAs, Google, and alternative accommodations threatens distribution control. Chinese competitors with government backing could undercut fee structures to gain global share.

Environmental regulations and sustainability requirements create new costs without clear revenue benefits. The asset-light model means less control during downturns—Marriott can't force owners to maintain standards or invest in renovations. Brand proliferation risks confusing consumers and diluting the core Marriott identity. Integration challenges from acquisitions could destroy value if mismanaged. And perhaps most concerning, the next generation of travelers might not value traditional hotels as previous generations did.

The bull case remains compelling despite these risks. Global travel demand grows steadily at GDP-plus rates, driven by emerging market wealth creation. The asset-light model provides downside protection—Marriott survived COVID-19 while leveraged competitors nearly collapsed. Network effects strengthen with scale, as larger loyalty programs attract more members who drive more direct bookings. Technology investments in revenue management, personalization, and distribution create competitive advantages smaller chains can't match.

The replacement cost of Marriott's platform—brands, technology, loyalty program, global sales force—would be tens of billions, creating a massive barrier to entry. Management has proven ability to integrate acquisitions, from Starwood to citizenM. The culture of operational excellence, dating back to J.W.'s perfectionism, creates execution advantages competitors struggle to replicate. Geographic and brand diversification provides resilience against localized downturns or segment-specific challenges.

Looking ahead, revenue is forecast to grow 24% p.a. on average during the next 3 years, compared to a 9.6% growth forecast for the Hospitality industry in the US. This outperformance reflects both market share gains and the compounding benefits of scale in a network-effects business.

The financial story ultimately reflects a business model transformation as profound as any in American corporate history. From capital-intensive real estate ownership to capital-light brand management. From cyclical commodity provider to recession-resistant fee collector. From domestic restaurant chain to global hospitality platform. The numbers—20%+ margins, 50%+ ROIC, billions in free cash flow—are just outcomes. The real achievement is building a machine that turns other people's capital into predictable, high-margin fees while bearing minimal risk.

For investors, Marriott represents a rare combination: growth company economics in a mature industry, technology-like margins in a service business, global scale with local execution. The valuation reflects these advantages, but given the durability of the model and runway for growth, the premium seems justified. As long as humans travel—for business, leisure, or necessity—and value consistency, quality, and rewards, Marriott's fee machine will keep printing money.

XI. Playbook: Key Lessons

After nearly a century of evolution, Marriott's journey from root beer stand to global hospitality giant offers a masterclass in strategic business building. The lessons transcend industry boundaries, providing insights applicable to any enterprise seeking sustainable competitive advantage. These aren't theoretical frameworks but battle-tested principles, refined through depressions, wars, booms, busts, and pandemics.

Start Small, Think Big: The Power of Humble Beginnings

J. Willard Marriott didn't set out to build a global empire. He wanted to sell root beer in Washington D.C. But from day one, he operated that nine-stool stand as if it were the Plaza Hotel. This paradox—modest ambitions coupled with exceptional execution—created the foundation for everything that followed. The lesson isn't to limit vision but to perfect execution at whatever scale you operate. Excellence in small things creates the capability for big things. Marriott spent 30 years perfecting restaurants before attempting hotels, building operational muscle memory that would prove invaluable when stakes increased.

Culture as Competitive Advantage: "Take Care of Associates, They'll Take Care of Customers"

J.W.'s philosophy sounds like corporate propaganda, but Marriott weaponized it into sustainable advantage. When competitors faced 100% annual turnover, Marriott retained employees for decades. This wasn't altruism—it was arithmetic. Experienced employees provide better service, make fewer mistakes, and require less training. Better service drives customer loyalty, which drives profitability, which funds better employee benefits, creating a virtuous cycle. The culture survived generational transitions because it was embedded in systems, not just sentiment. Every Marriott manager still learns the story of J.W. paying for employees' medical bills, creating institutional memory that shapes behavior decades after his death.

The Power of Asset-Light Business Models

The 1993 split creating Marriott International represented one of history's great business model innovations, though few recognized it at the time. By separating asset ownership from operational excellence, Marriott discovered you could scale expertise infinitely without capital constraints. This wasn't just financial engineering—it was philosophical revolution. The company that once prided itself on owning everything realized ownership was a burden, not a blessing. The lesson extends beyond hospitality: identify what truly creates value in your business, then structure to maximize that while minimizing everything else.

Brand Portfolio Strategy: Something for Everyone

Marriott's 37+ brands aren't random accumulation but deliberate market segmentation. Each brand targets specific psychographics with surgical precision, allowing complete market coverage without cannibalization. The insight: customers aren't monolithic, and neither should offerings be. A business traveler choosing Courtyard on Tuesday might pick Ritz-Carlton on Saturday. By offering both, Marriott captures the entire wallet share rather than fighting for fragments. This portfolio approach also provides resilience—when luxury suffers, economy thrives; when business travel declines, leisure compensates.

Family Business Succession Done Right

The transition from J.W. to Bill Jr. to professional management under Arne Sorenson represents a rarity: successful multi-generational leadership evolution. Most family businesses implode by the third generation, victims of nepotism, complacency, or family dynamics. Marriott succeeded through deliberate process. Bill Jr. had to prove himself, starting at the bottom despite his surname. The culture emphasized meritocracy over birthright. When time came for Bill Jr.'s succession, he chose the best executive (Sorenson) over family members. The lesson: family businesses succeed when they act like public companies; public companies succeed when they maintain family business values.

When to Pivot: From Restaurants to Hotels

The 1957 decision to enter hotels wasn't obvious. Hot Shoppes were thriving, generating steady profits. But J.W. recognized a fundamental truth: restaurants had inherent limitations—low margins, high labor intensity, limited scalability. Hotels offered superior economics despite higher capital requirements. The pivot required courage to abandon proven success for unproven opportunity. But it was calculated courage, based on careful analysis of travel trends, competitive dynamics, and economic shifts. The lesson: pivot not when forced but when opportunity appears, not from weakness but from strength.

The Art of M&A: Discipline Over Drama

From Ritz-Carlton to Renaissance to Starwood to citizenM, Marriott's acquisition strategy follows consistent principles. Never overpay for ego or headlines. Focus on operational improvement potential rather than financial engineering. Maintain cultural compatibility while respecting acquired brand identity. Integrate systems and back-office functions quickly but preserve customer-facing distinctiveness. The Starwood acquisition, despite its complexity and competition, succeeded because Marriott had practiced on smaller deals for decades. They knew what to integrate immediately (procurement, technology), what to maintain separately (brand identity, loyalty programs initially), and what to eliminate (redundant corporate functions).

Building Enduring Competitive Moats