Northern Trust: The Quiet Giant of American Finance

I. Introduction & Episode Roadmap

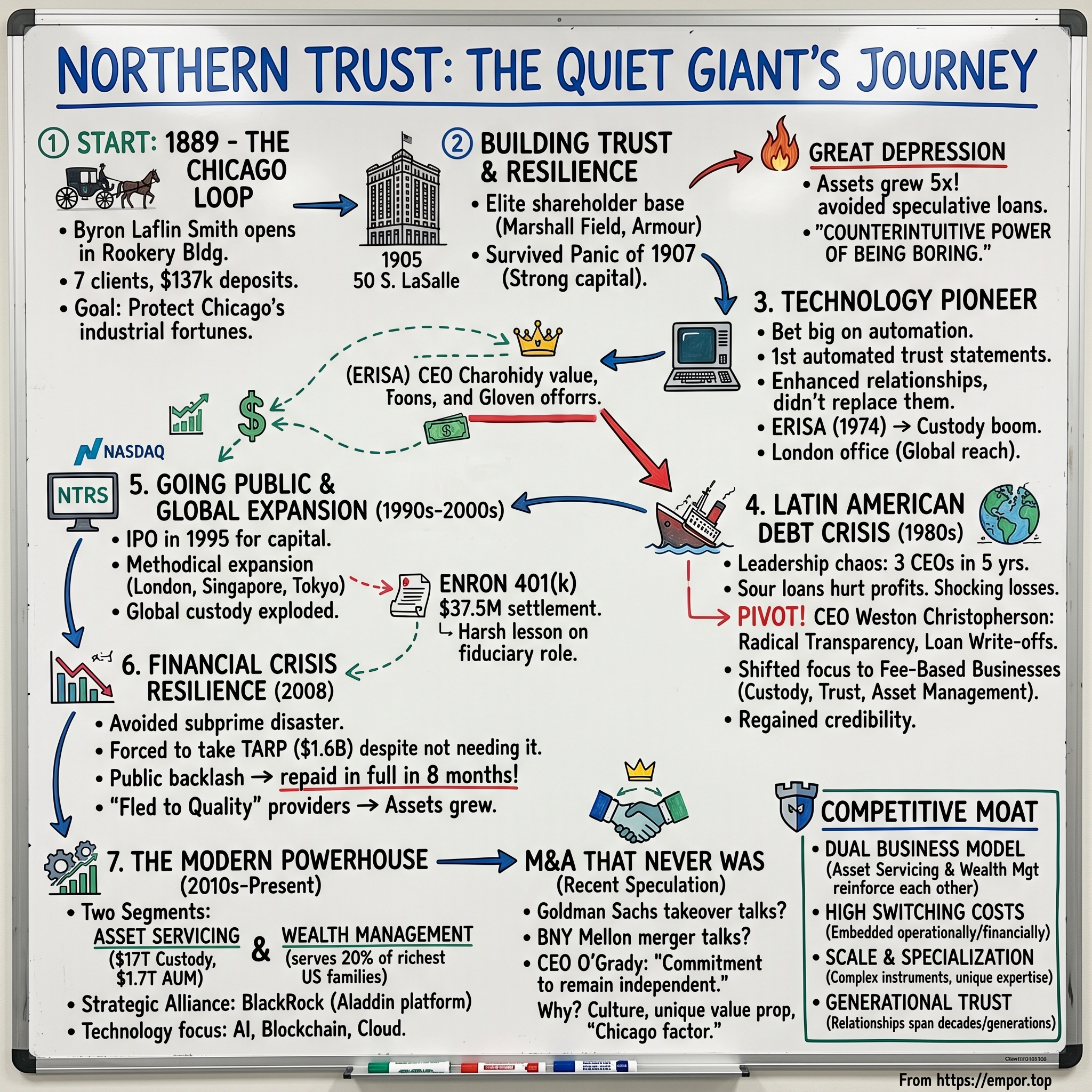

Picture this: It's a sweltering August day in 1889. Chicago's Loop district bustles with horse-drawn carriages and the clanging of streetcars. In a single room of the Rookery Building—that architectural marvel designed by Burnham and Root—a 40-year-old banker named Byron Laflin Smith opens the doors to Northern Trust Company. Seven customers walk through that day. Total deposits: $137,981.25. Smith probably couldn't have imagined that his modest trust company would one day safeguard $17 trillion in assets and manage wealth for over 20% of America's richest families.

Northern Trust today stands as one of those peculiar American financial institutions—massive yet understated, powerful yet rarely in headlines. With $1.7 trillion under management and $17 trillion under custody as of June 2022, it operates in that rarefied air alongside State Street and Bank of New York Mellon. Yet unlike its flashier peers on Wall Street, Northern Trust has remained stubbornly, almost defiantly, Chicago through and through.

The paradox at the heart of this story: How did a conservative Midwestern trust company—one that still maintains its original 1905 headquarters at 50 South LaSalle Street—become one of the world's largest custodians? How did it survive the Panic of 1907, the Great Depression, the Latin American debt crisis, and 2008's financial meltdown while competitors collapsed or merged away their independence?

This is a story about trust—not just the legal instrument, but the actual human quality. It's about technology investments made decades before Silicon Valley taught banks about "digital transformation." It's about serving the ultra-wealthy so well that family relationships span five generations. And perhaps most intriguingly, it's about staying independent in an era of relentless consolidation, even as suitors from Goldman Sachs to Bank of New York Mellon come knocking with multi-billion dollar offers.

The themes we'll explore cut to the heart of American capitalism: the evolution of trust banking from a genteel service for railroad barons to a technology-driven custody powerhouse; the tension between family control and public markets; the art of conservative banking that somehow produces aggressive returns; and the counterintuitive power of being boring in finance.

What makes Northern Trust particularly fascinating for students of business history is its ability to reinvent itself while appearing unchanged. The company that once managed fortunes for Marshall Field and Philip Armour now processes trillions in securities transactions using artificial intelligence. The firm that pioneered automated trust statements in the 1950s now partners with BlackRock on its Aladdin platform. Yet walk into their offices, and you'll still feel that old-school Chicago banking culture—measured, relationship-focused, built for the long haul.

As we'll discover, Northern Trust's story offers profound lessons about building enduring competitive advantages in financial services. In an industry where trust is the ultimate currency, they've figured out how to mint it consistently for 135 years. That's not just longevity—that's a masterclass in institutional memory, risk management, and the compound value of reputation.

II. The Byron Smith Era & Chicago Origins (1889-1930s)

The Great Chicago Fire of 1871 had reduced the city to ash and rubble, but from those ashes rose something extraordinary—a new Chicago, rebuilt with ambition and steel, destined to become America's second city. By 1889, Chicago pulsed with industrial energy. The stockyards processed the nation's meat, the Board of Trade set global grain prices, and fortunes accumulated faster than anywhere outside New York. Into this maelstrom stepped Byron Laflin Smith with a radical proposition: Chicago's new money needed something more sophisticated than a simple bank vault.

Smith wasn't your typical banker. Born into a prominent family—his father was a successful businessman and his mother came from the wealthy Laflin gunpowder dynasty—he understood wealth from the inside. After graduating from high school in Chicago, he'd worked his way up through various financial institutions, including a stint at the Merchants' Loan and Trust Company. But Smith saw a gap in the market that others missed: Chicago's industrialists needed someone to manage their estates, protect their children's inheritances, and handle the complex financial engineering that great wealth demanded. The genius of Smith's timing cannot be overstated. Illinois had just passed new banking legislation in 1887 that finally allowed state-chartered trust companies. Ever cautious, Smith didn't rush in—instead, he had his lawyer file a test lawsuit to clarify the law's provisions. When the Illinois Supreme Court ruled favorably in April 1889, Smith pounced. The court's ruling in Dupee, et al. v. Swigert cleared the way for the launch of Smith's new enterprise: The Northern Trust Company.

What truly set Northern Trust apart from day one was its shareholder base—a who's who of Chicago's gilded age elite. Smith provided 40% of the bank's original $1 million capitalization, but his 27 co-investors read like a directory of American industrial power. There was Marshall Field, the dry goods magnate whose department store empire would define retail for generations. Philip D. Armour, whose meatpacking fortune literally fed the nation. Martin A. Ryerson, the lumber baron turned philanthropist whose name would grace the Art Institute of Chicago.

These weren't passive investors—they were clients, ambassadors, and walking advertisements for Smith's vision of sophisticated wealth management. When a Ryerson or Field entrusted their fortune to Northern Trust, every other wealthy family in Chicago took notice. The company's headquarters building at 50 South LaSalle Street in the Financial District of Chicago dates from 1905 and was designed by Frost and Granger. This wasn't just any building—it represented a statement of permanence and prosperity. Situated strategically between the Chicago Stock Exchange and the Board of Trade, the location announced Northern Trust's arrival as a major financial institution. The building, designed to accommodate future expansion, embodied Smith's vision: build for the long term, plan for growth, but never overreach.

Smith worked without pay for the first six years Northern Trust was in business—a detail that reveals much about both his personal wealth and his commitment to the institution. This wasn't a get-rich-quick scheme but a legacy project. Smith understood that trust, especially in finance, compounds slowly but powerfully.

The early years weren't without challenges. The Panic of 1907—triggered by a failed attempt to corner the copper market—saw runs on banks across America. While the Knickerbocker Trust Company collapsed in New York, sparking nationwide panic, Northern Trust's conservative approach and strong capital base allowed it to weather the storm. Smith's insistence on maintaining high liquidity ratios, which some board members had questioned as overly cautious, suddenly looked prescient.

When Byron Laflin Smith died in March 1914, his son Solomon Albert Smith inherited not just leadership of the bank but a philosophy: conservatism in lending, innovation in service, and an almost religious devotion to client relationships. Solomon Albert Smith took over the bank at just 37 years old, becoming Chicago's youngest bank president.

The younger Smith faced his first major test almost immediately: World War I. While other banks scrambled to adjust, Northern Trust had already begun expanding its commercial banking operations beyond Chicago's borders. By 1941, nearly half of all the bank's commercial accounts were drawn from outside the Chicago metropolitan area.

But it was during the Great Depression that Northern Trust's conservative DNA truly proved its worth. The company's conservative policies served it well during the 1920s and the company's assets actually grew during the Great Depression, while many other banks suffered from bank failure. As banks failed by the thousands—over 9,000 between 1930 and 1933—Northern Trust not only survived but thrived. Assets grew fivefold during the Depression years, a staggering achievement that cemented the bank's reputation as a safe harbor in financial storms.

The secret wasn't complex: Northern Trust had avoided the speculative lending that destroyed so many competitors. No risky real estate plays in Florida. No margin loans to stock speculators. Just careful, relationship-based banking with clients they knew intimately. When FDR declared a bank holiday in 1933, Northern Trust was among the first banks approved to reopen, a validation of its fundamental soundness.

This period also saw Northern Trust pioneer services that seem quaint today but were revolutionary then. They established a Women's Department in 1920, recognizing that the 19th Amendment had created a new class of financial decision-makers. They offered free group life insurance and pension plans to employees—radical benefits that helped them attract and retain Chicago's best banking talent.

By the late 1930s, Northern Trust had evolved from a single-room startup to one of Chicago's most respected financial institutions. The foundation was set: a culture of conservatism that paradoxically enabled innovation, a client base of America's wealthiest families, and a reputation for surviving crises that destroyed competitors. The stage was set for the next act in this remarkable story.

III. The Technology Pioneer Years (1950s-1970s)

The year was 1955. IBM had just introduced its first commercial computer for business use—a room-sized behemoth that cost millions. Most banks viewed these machines as expensive curiosities. But in a conference room at 50 South LaSalle, Northern Trust's leadership made a decision that would define the company's next half-century: they would bet big on automation, bigger than any trust company had dared before.

During the 1950s, Northern Trust spent heavily to develop automated banking services, including the first fully automated financial statements for trust clients. Think about what this meant in practice. While competitors were still hand-calculating interest and manually preparing statements—a process that took armies of clerks weeks to complete—Northern Trust could generate accurate, detailed reports in hours. For wealthy clients managing complex estates across multiple asset classes, this wasn't just convenient; it was transformative.

The man overseeing this technological revolution was Solomon Byron Smith, grandson of the founder, who had assumed leadership alongside his brother Edward Byron Smith after their father Solomon Albert Smith's death in 1963. The brothers represented different but complementary visions: Solomon Byron Smith became chairman of the executive committee and his brother, Edward Byron Smith, became chairman.

The Smith brothers understood something their Wall Street competitors missed: technology wasn't about replacing relationship banking—it was about enhancing it. By automating the mundane, their trust officers could focus on what mattered: understanding clients' needs, structuring complex estates, navigating tax implications. A Northern Trust advisor in 1965 spent time strategizing, not calculating.

This technological edge created a fascinating competitive dynamic. Large New York banks had more capital, but Northern Trust could offer superior service through automation. When a client needed to know their exact position across dozens of holdings, Northern Trust could provide that information in days, not weeks. When tax laws changed—as they frequently did in the 1960s—Northern Trust could recalculate implications across thousands of accounts simultaneously. The 1970s brought a perfect storm of challenges and opportunities. Deregulation transformed American banking—suddenly, financial institutions could pay competitive interest rates, but they also faced new competition from money market funds and investment banks. The Employee Retirement Income Security Act (ERISA) of 1974 created massive new demand for custody services as pension funds needed qualified custodians. Northern Trust, with its technology infrastructure already in place, was perfectly positioned.

Consider what custody meant in the 1970s: physically holding stock certificates in vaults, processing corporate actions, collecting dividends, managing proxy voting. Each transaction required paperwork, verification, settlement. Northern Trust's early investments in automation meant they could handle volumes that would have crushed competitors still relying on manual processes.

The bank also made a prescient geographic move. Near the end of the 1960s, Northern became the first state-chartered bank from Illinois to open an office outside the United States, establishing a London office that helped expand services to European customers. This wasn't just international expansion—it was recognition that wealth management and custody were becoming global businesses. The Northern Trust International Banking Corporation, a New York subsidiary created to handle currency transactions for financial institutions abroad, followed soon after.

By the time Edward Byron Smith retired as chief executive officer in 1979, Northern Trust had transformed from a regional trust company to a technology-enabled financial services powerhouse. Assets had grown from $1 billion in 1963 to multiple billions by decade's end. More importantly, the infrastructure was in place for what would become one of the world's largest custody operations.

The technological foundation laid during these decades would prove crucial. While other banks would scramble to digitize in the 1980s and 1990s, Northern Trust had already done the heavy lifting. They had automated trust accounting when automation meant punch cards. They had built global custody infrastructure when "global" meant having a telex machine. They had created scalable systems when scale meant handling hundreds of accounts, not knowing they would one day handle millions.

This period established a pattern that would define Northern Trust's strategy for decades: invest ahead of the curve in unglamorous but essential infrastructure, use technology to enhance rather than replace relationship banking, and build capabilities that create compound advantages over time. It was conservative banking with a radical twist—conservative in risk-taking, radical in operational innovation.

The stage was now set for Northern Trust's next transformation. The quiet technology pioneer was about to face its greatest test.

IV. Crisis and Transformation: The Latin American Debt Crisis (1980s)

August 1982. Mexico's finance minister picks up a phone and delivers news that will shake the global financial system: Mexico cannot service its $80 billion in foreign debt. Within months, Brazil, Argentina, and virtually every Latin American country follows suit. American banks, drunk on petrodollar recycling and the assumption that countries don't go bankrupt, suddenly face existential crisis. At Northern Trust's Chicago headquarters, new CEO Weston Christopherson—a retail executive who'd never run a bank before—inherits a nightmare.

The story of how Northern Trust navigated the Latin American debt crisis is really three stories: a succession crisis, a credit catastrophe, and ultimately, a masterclass in crisis management that would define the institution's modern character.

First, the succession drama. Edward Byron Smith retired as chief executive officer in 1979. He was succeeded by E. Norman "Bud" Staub. A few years later, Philip W. K. Sweet took over but he resigned in 1984. In 1984, Weston Christopherson, former CEO of Jewel, took the helm. Three CEOs in five years—for a company that had been run by the same family for nearly a century, this leadership chaos couldn't have come at a worse time.

Christopherson was an unusual choice. The former Jewel Companies CEO knew supermarkets, not banking. Critics questioned whether a retailer could navigate complex international finance. But the board saw something others missed: Christopherson understood operations, efficiency, and most critically, how to manage through crisis. At Jewel, he'd modernized a sleepy grocery chain into a retail powerhouse. Northern Trust needed similar transformation.

He is credited with guiding the bank through a difficult period when sour loans to Latin American countries were hurting profits. When oil prices dropped suddenly in the early 1980s, many South American nations realized they could not repay their enormous bank loans. The bank suffered uncharacteristically high losses—a shocking development for an institution that had sailed through the Great Depression.

The numbers were brutal. Northern Trust's Latin American exposure, while smaller than money center banks like Citibank or Chase, still represented a significant portion of capital. When countries stopped paying, Northern Trust faced a choice: extend and pretend (rolling over bad loans and hoping for recovery) or take the pain immediately.

Christopherson chose radical transparency. Aggressive management, loan reserves, and write-offs enabled the bank to restore its asset quality. During Christopherson's six years at Northern Trust, profits rose from $34 million to $113 million. At the time of his retirement in 1990, the company was the 11th most profitable of the 100 largest banks in the United States.

The strategy was painful but effective. Northern Trust took massive provisions against Latin American loans, effectively writing off much of the portfolio. Earnings crashed in the short term. But while competitors played games with their balance sheets—creating off-balance-sheet vehicles, manipulating loan loss reserves—Northern Trust's conservative approach restored credibility with regulators and investors.

Christopherson didn't just manage the crisis; he used it to transform Northern Trust's business model. Recognizing that international lending was both risky and outside Northern Trust's core competency, he pivoted hard toward fee-based businesses: custody, trust, and asset management. These businesses required little capital, generated predictable revenues, and leveraged Northern Trust's technological advantages.

The 1986 acquisition of First Lake Forest Corporation for $61 million in cash exemplified this strategy. First Lake Forest brought wealthy suburban Chicago clients and trust assets—exactly the kind of stable, fee-generating business Christopherson wanted. While other banks chased the next hot lending market, Northern Trust doubled down on boring, profitable services for the wealthy.

This pivot had profound implications. Fee income, which had been a nice supplement to lending profits, became the main event. Custody services, powered by the technology investments of previous decades, scaled beautifully. Trust and estate services, Northern Trust's original business, generated steady returns without credit risk.

By 1990, Northern Trust had emerged from the Latin American debt crisis stronger than before. The company that had entered the 1980s as a traditional commercial bank with a trust department had transformed into something new: a processing powerhouse that happened to have a bank attached. This wasn't just survival—it was metamorphosis.

The crisis also cemented cultural values that persist today. Risk management became religion. Transparency became doctrine. The willingness to take short-term pain for long-term gain became institutional muscle memory. When the next crisis arrived—the S&L collapse, the Asian financial crisis, the dot-com bust—Northern Trust would face them with the confidence of an institution that had stared into the abyss and emerged stronger.

Christopherson's unlikely success—a grocer who saved a bank—became Northern Trust legend. But the real lesson was deeper: sometimes outsiders see what insiders cannot. Christopherson saw that Northern Trust's future lay not in competing with money center banks in lending, but in dominating specialized services where technology, trust, and expertise mattered more than balance sheet size.

V. The Modern Era: Going Public & Global Expansion (1990s-2000s)

The morning of November 17, 1995, marked a watershed moment in Northern Trust history. After 106 years as a closely held institution, the company's shares began trading on NASDAQ under the symbol NTRS. The opening price: $33.50. For an institution that had prided itself on privacy and long-term thinking, going public was almost heretical. Yet it was also inevitable—Northern Trust needed capital to compete globally, and public markets offered the fuel for expansion.

In 1990, company veteran David W. Fox became the seventh CEO of the company. William A. Osborn was named president and chief operating officer in 1993 and became chairman and chief executive officer, in addition to president, in 1995. Fox and Osborn represented continuity—both were Northern Trust lifers who understood the culture. But they also recognized that the financial services landscape was shifting dramatically. Consolidation was accelerating, technology costs were soaring, and clients increasingly demanded global capabilities.

The IPO raised $275 million, but money was only part of the equation. Going public forced Northern Trust to articulate its strategy clearly, report results quarterly, and compete for investor attention. For a company accustomed to measuring success in decades, this was cultural shock therapy.

The late 1990s became a period of aggressive but disciplined expansion. Northern Trust didn't chase headline-grabbing acquisitions. Instead, they built or bought specific capabilities in key markets. London, Singapore, Tokyo—Northern Trust methodically established custody and wealth management operations in financial centers worldwide. The company has offices in 20 US states and locations across 23 countries in Canada, Europe, the Middle East, and the Asia-Pacific region.

The global custody business exploded during this period. As American pension funds and mutual funds invested internationally, they needed custodians who could handle multi-currency settlements, navigate local regulations, and provide consolidated reporting. Northern Trust's technology platform, continuously upgraded since the 1950s, provided competitive advantage. While competitors struggled to integrate acquisitions and harmonize systems, Northern Trust offered a single, global platform. But expansion brought unexpected risks. In 2005, Northern Trust and Enron reached a $365 million settlement with 20,000 employees of Enron after the energy company's collapse. Northern Trust had managed the 401k plan for Enron's employees, who alleged mismanagement and breach of fiduciary duty. The Enron debacle was a harsh reminder: even fee-based businesses carried reputational and legal risks.

The settlement negotiations revealed the complexity of modern fiduciary responsibility. Northern Trust hadn't engaged in fraud—they'd simply administered a plan where employees held too much company stock. But in the post-Enron environment, that wasn't enough. Fiduciaries were expected to protect participants from themselves. The initial settlement amount was later reduced to $37.5 million in an agreement by Federal judge Melinda Harmon, with Northern Trust neither admitting or denying wrongdoing.

Despite setbacks like Enron, the global expansion strategy paid dividends. By the mid-2000s, Northern Trust had become one of the world's top ten custody banks. Assets under custody soared from billions to trillions. The wealth management business, leveraging global capabilities, attracted international ultra-high net worth clients who needed sophisticated cross-border planning.

The technology investments continued to compound. While competitors struggled with legacy systems and acquisition integration, Northern Trust offered unified global reporting, real-time settlement tracking, and sophisticated risk analytics. For institutional clients managing complex portfolios across dozens of markets, this was invaluable.

Cultural challenges emerged as Northern Trust globalized. The conservative Chicago culture didn't always translate to London's aggressive trading floors or Singapore's relationship-driven markets. Northern Trust had to learn when to adapt and when to insist on its values. The answer, generally, was to be flexible on style but inflexible on ethics and risk management.

The 2000s also saw Northern Trust deepen its specialization. Rather than trying to be all things to all clients, they focused on specific niches: corporate and public pension funds, foundations, endowments, sovereign wealth funds. Each segment required deep expertise, customized technology, and dedicated service teams. This specialization created barriers to entry—competitors couldn't easily replicate decades of accumulated knowledge.

By 2007, Northern Trust seemed perfectly positioned. Public markets had provided capital for expansion. Global operations generated diversified revenue streams. Technology investments created scalable platforms. The wealth management and custody businesses produced steady fee income. What could go wrong?

Everything, as it turned out. The global financial crisis was about to test every assumption about risk, liquidity, and trust. Northern Trust would survive—even thrive—but not without controversy.

VI. The Financial Crisis: TARP and Resilience (2008-2010)

October 14, 2008. Nine bank CEOs sit around a conference table at the Treasury Department in Washington. Treasury Secretary Hank Paulson slides a one-page document across the table. The message is clear: take the government's money, whether you need it or not. Among those CEOs is Northern Trust's Frederick Waddell, watching his institution get swept into a political maelstrom it never sought.

Northern Trust didn't need TARP money. Unlike Citigroup teetering on collapse or Bank of America choking on Merrill Lynch's toxic assets, Northern Trust had avoided the subprime mortgage disaster entirely. No CDOs, no synthetic derivatives, no off-balance-sheet vehicles hiding losses. Their boring focus on custody and wealth management suddenly looked brilliant. Yet here was Waddell, being told to take $1.6 billion in government funds to maintain the fiction that all major banks were equally healthy.

The decision tormented Northern Trust's leadership. Accepting TARP funds meant accepting government oversight, compensation restrictions, and public scrutiny. Refusing meant breaking ranks with other major banks and potentially signaling that those who took the money were weak. Waddell chose solidarity—and immediately regretted it. The public backlash came swiftly. In February 2009, Northern Trust hosted its annual client event at the Northern Trust Open golf tournament, featuring concerts by Sheryl Crow and Earth, Wind & Fire. The optics were catastrophic—a TARP recipient throwing lavish parties while the economy burned. Congress erupted. Representative Barney Frank demanded immediate TARP repayment. The media painted Northern Trust as tone-deaf plutocrats partying on taxpayer dollars.

The criticism stung because it was fundamentally unfair. The client events had been planned and paid for long before TARP. Northern Trust sponsored the golf tournament as part of a multi-year contract. The hospitality events were marketing investments, not executive bonuses. But in the toxic political environment of 2009, facts didn't matter. Northern Trust had become a symbol of Wall Street excess.

Northern Trust Corporation announced in June 2009 that it had repaid in full the $1.576 billion preferred share investment made by the U.S. Department of the Treasury under the TARP Capital Purchase Program. "The TARP Capital Purchase Program played a necessary role in helping to stabilize the financial system during a period of crisis, and Northern Trust was proud to participate in the program as a strong, well-capitalized bank," said Northern Trust President and Chief Executive Officer Frederick H. Waddell. "With today's action, the government has realized a positive return on its investment in Northern Trust. We would like to take this opportunity to once again acknowledge the taxpayers' support of the financial system during these difficult times."

Northern Trust was one of 10 big U.S. banks exiting the TARP program on June 17, 2009. The speed of repayment—just eight months after receiving the funds—demonstrated Northern Trust's fundamental strength. They raised capital through public markets, proving investor confidence remained strong.

But the TARP episode left scars. Northern Trust learned that in modern finance, perception matters as much as reality. Being lumped with troubled banks damaged their carefully cultivated reputation for conservatism. The political circus around client entertainment highlighted how quickly public opinion could turn toxic.

The crisis period also revealed Northern Trust's resilience. While competitors wrote down billions in toxic assets, Northern Trust's boring focus on custody and wealth management generated steady profits. Assets under custody actually grew during the crisis as investors fled to quality providers. The wealth management business, serving ultra-conservative wealthy families, remained stable.

More importantly, the crisis accelerated trends that benefited Northern Trust. New regulations like Dodd-Frank increased demand for custody services. Basel III capital requirements made lending less attractive, validating Northern Trust's shift to capital-light businesses. The complexity of post-crisis compliance created opportunities for sophisticated service providers.

Northern Trust emerged from the financial crisis with its reputation bruised but its business model validated. The company that had been forced to take unwanted government funds had repaid them faster than almost anyone. The institution that avoided subprime mortgages and complex derivatives looked prescient, not boring.

The crisis also catalyzed strategic clarity. Northern Trust would double down on what it did best: serving institutional investors and the ultra-wealthy with technology-enabled services requiring minimal capital. Let others chase hot markets and complex products. Northern Trust would remain boring—and profitable.

By 2010, with TARP repaid and the economy stabilizing, Northern Trust stood at an inflection point. The next decade would bring unprecedented growth in assets under custody and management. But it would also bring new challenges: fee compression, technology disruption, and eventually, acquisition interest from larger competitors.

VII. The Asset Servicing & Wealth Management Powerhouse (2010s-Present)

May 2020. The world is in lockdown, markets are in freefall, and Northern Trust quietly announces something that would have been unthinkable a decade earlier: a strategic alliance with BlackRock, the world's largest asset manager. At the end of May 2020, Northern Trust Corporation entered into a strategic alliance with BlackRock. This alliance entails working with BlackRock on its platform called Aladdin with mutual clients. The partnership represented more than a technology deal—it was Northern Trust's acknowledgment that the future of asset servicing required scale, sophistication, and strategic partnerships that would have seemed heretical to Byron Smith.

The 2010s transformed Northern Trust from a successful regional trust company with global operations into a genuine powerhouse in asset servicing and wealth management. Northern Trust Corporation is an American financial services company headquartered in Chicago, Illinois, that caters to corporations, institutional investors, and ultra high net worth individuals. Northern Trust is one of the largest banking institutions in the United States and one of the oldest banks in continuous operation. As of June 30, 2022, it had $1.7 trillion in assets under management and $17 trillion in assets under custody.

The numbers tell only part of the story. Behind those trillions lies a fundamental transformation in how institutional investors and wealthy families manage assets. Northern Trust positioned itself at the nexus of several powerful trends: the institutionalization of investment management, the globalization of capital markets, and the digitization of financial services.

The company operates in two segments, Asset Servicing and Wealth Management. Asset Servicing is a global provider of custodian bank, fund administration, investment operations outsourcing, investment management, investment risk and analytical services, employee benefits services, securities lending, foreign exchange market, treasury management, brokerage firm services, transition management services, banking, and cash management services to corporate and public pension funds, foundations, financial endowments, fund managers, insurance companies, sovereign wealth funds, and other institutional investors. The company's appointment by Aristotle Capital Management for middle office outsourcing services, impacting $40 billion in assets, highlighted Northern Trust's competitive position in the evolving asset servicing landscape. As of June 30, 2025, Northern Trust's IOO capability supports more than 85 clients with approximately $2.63 trillion in assets under administration.

The wealth management segment tells an equally impressive story. Over 20% of the wealthiest families in the United States are clients of the company's wealth management division. The segment provides personal trust, investment management, custodian bank, and philanthropic services, financial consulting, guardianship and estate administration. What's remarkable is the stickiness of these relationships—many span multiple generations, with Northern Trust managing wealth for the great-grandchildren of original clients.

The secret sauce in wealth management isn't just investment performance—it's the ecosystem Northern Trust has built around wealthy families. Estate planning, philanthropic advisory, family office services, art advisory, even concierge services for travel and lifestyle management. When you're managing billions for a family, you become more than a banker—you become a trusted advisor across every aspect of financial life. The expansion of Northern Trust's long-standing relationship with the North Dakota Retirement and Investment Office to include outsourced trading services demonstrates another key competitive advantage. NDRIO manages investments for more than two dozen SIB client funds, the largest being the $12 billion North Dakota Legacy Fund, Public Employees Retirement System, Teachers' Fund for Retirement, and Workforce Safety & Insurance Fund. "We've had the privilege of working with NDRIO for more than 35 years and we are honored to be an extension of their team, providing an efficient and scalable outsourced trading and operations platform to support their investment strategy."

This 35-year relationship exemplifies Northern Trust's approach: start with basic services, prove value over decades, then expand into more sophisticated offerings as clients' needs evolve. It's a compound trust model—each year of successful service makes the next mandate more likely.

The BlackRock alliance deserves special attention. Rather than viewing BlackRock as competition, Northern Trust recognized that partnering with the world's largest asset manager on technology could create mutual benefits. BlackRock's Aladdin platform provides sophisticated risk analytics; Northern Trust provides custody and operational infrastructure. Together, they offer institutional clients an integrated solution neither could provide alone.

Technology investments continue to accelerate. Northern Trust isn't trying to be a fintech company—they're using technology to enhance their core strengths. Artificial intelligence improves transaction monitoring. Blockchain experiments streamline settlement. Cloud computing enables global scale. But unlike Silicon Valley disruptors promising to revolutionize finance, Northern Trust uses technology to do traditional things better, faster, cheaper.

The wealth management business has evolved beyond recognition from Byron Smith's era, yet the core principle remains: serve wealthy families so well they never leave. Modern wealth management at Northern Trust includes impact investing advisory, helping families align investments with values. It includes next-generation education, preparing heirs for wealth responsibility. It includes family governance consulting, helping dynasties avoid the "shirtsleeves to shirtsleeves in three generations" curse.

The numbers validate the strategy. Revenue has grown consistently, driven by both market appreciation and new business wins. Operating leverage has improved as technology investments pay off. Return on equity remains strong despite the capital-light business model. Most importantly, client retention rates in both segments exceed 95%—once clients come to Northern Trust, they rarely leave.

But challenges loom. Fee compression continues as passive investing grows and clients demand lower costs. Competition intensifies from both traditional competitors like State Street and new entrants like technology companies. Regulatory requirements keep increasing, raising compliance costs. The need for continuous technology investment never ends.

Northern Trust's response has been strategic focus. Rather than trying to compete everywhere, they've identified specific niches where their capabilities provide genuine competitive advantage. In asset servicing, that means complex instruments requiring sophisticated operational expertise. In wealth management, that means ultra-high net worth families needing comprehensive solutions.

The announcement of an expanded share buyback program, with authorization for up to $2.5 billion, signals management's confidence in the business model. When you generate more cash than you need for organic growth and your stock trades below intrinsic value, returning capital to shareholders makes sense.

Looking at Northern Trust today, you see an institution that has successfully navigated the transition from traditional banking to modern financial services. The company that once held physical stock certificates in vaults now processes trillions in electronic transactions. The trust officers who once knew every client personally now leverage data analytics to provide personalized service at scale. Yet somehow, the essential character remains: conservative, client-focused, built for the long term.

VIII. The M&A That Never Was: Recent Acquisition Speculation

The conference room at Goldman Sachs' 200 West Street headquarters buzzed with anticipation in early 2024. CEO David Solomon had just outlined his vision: acquire Northern Trust, instantly catapult Goldman into the top tier of custody banks, and capture $1.3 trillion in client assets. The PowerPoint was compelling, the synergies obvious, the strategic rationale clear. Yet as we know today, no deal materialized. The story of why Northern Trust remains independent—despite persistent suitor interest—reveals much about both the company's value and its stubborn commitment to independence. In the past year, CEO David Solomon discussed a potential takeover with Northern Trust and nearly secured a $6 billion deal with Cliffwater, according to people familiar with the matter. Discussions with Northern Trust were more preliminary, but could heat up now that the company is in play. Northern Trust would bring Goldman $1.3 trillion in client money, boosting its total by 40%, and a mundane but giant asset-servicing business that serves as a ledger for much of Wall Street.

The strategic logic for Goldman was compelling. Solomon's disastrous foray into consumer banking with Marcus had cost billions and damaged his credibility. Acquiring Northern Trust would instantly transform Goldman's narrative from investment bank struggling to diversify into a diversified financial services powerhouse. The custody business would provide stable, predictable fee income to offset volatile trading revenues. The wealth management franchise would give Goldman access to ultra-high net worth relationships it had struggled to capture organically. But Northern Trust wasn't playing along. A recent Wall Street Journal report indicated that Bank of New York Mellon has also approached Northern Trust for a potential merger. Discussions for a potential merger of Bank of New York Mellon Corp. and Northern Trust Corp. have been ongoing for more than a year, according to one senior industry executive with knowledge of the talks. "The two have had discussions for a while, but whether the Northern Trust shareholders agree to BNY Mellon's offer is a different story," said the executive.

BNY's interest made even more strategic sense than Goldman's. Combining the world's largest custodian with Northern Trust would create an asset servicing colossus with over $35 trillion under custody. The cost synergies would be enormous—redundant technology platforms, overlapping operations centers, duplicative regulatory infrastructure. Analysts estimated $500 million in annual savings, possibly more.

Yet CEO Michael O'Grady's response was unequivocal. "I want to reaffirm our commitment to remain independent," O'Grady said during a conference call with analysts. "Contrary to recent speculation, during my tenure as CEO, we have never entertained discussions regarding the sale of the company with any financial institution, nor do we intend to."

Why would Northern Trust reject such lucrative offers? The answer reveals much about the company's culture and competitive position. First, independence allows Northern Trust to maintain its unique culture—that conservative, client-first approach that has defined it since 1889. In a merged entity, whether with Goldman or BNY, Northern Trust would inevitably become subordinate to a different culture, different priorities.

Second, Northern Trust's management believes they're just beginning to realize the benefits of decades of investment. The technology platform is finally scaled. The global footprint is established. The client relationships span generations. Why sell just as the compound returns are accelerating?

Third, there's the Chicago factor. Northern Trust isn't just based in Chicago—it IS Chicago finance. A sale to New York-based institutions would represent the final capitulation of Midwest banking to Wall Street. For a company whose identity is intertwined with its hometown, that's not just a business decision—it's existential.

The client perspective matters too. "We've heard from a lot of our clients who have said, 'We chose Northern Trust because it's a different value proposition. It's one where you are focused on trying to provide a higher level of client service, where you do have very targeted expertise in just certain segments of the market where you compete,'" O'Grady noted. Many ultra-wealthy families specifically chose Northern Trust because it wasn't Goldman Sachs or Bank of New York Mellon.

Market dynamics also favor independence, at least for now. Northern Trust's stock has performed well, reducing the premium any acquirer could offer. The company generates strong cash flows and returns capital to shareholders efficiently. Management has credibility after navigating recent challenges successfully.

But the acquisition speculation won't disappear. Northern Trust's market capitalization of $23 billion makes it digestible for larger institutions. The strategic logic—whether for Goldman seeking diversification or BNY seeking scale—remains compelling. As fee compression continues and technology costs escalate, the pressure to consolidate will only intensify.

The deeper question is whether Northern Trust can remain independent indefinitely. History suggests that every financial institution eventually faces a moment where selling becomes inevitable—whether due to crisis, succession issues, or simply an offer too good to refuse. Northern Trust has survived 135 years by adapting to change while maintaining core principles. But in modern finance, where scale increasingly determines success, principled independence may be a luxury even Northern Trust cannot afford forever.

For now, Northern Trust remains defiantly independent, a rare breed in American finance—large enough to compete globally, small enough to maintain its culture, successful enough to reject multi-billion dollar suitors. It's a precarious balance, but one Northern Trust has maintained for over a century. The question isn't whether they can continue—it's for how long.

IX. Business Model & Competitive Moat Analysis

Stand outside Northern Trust's headquarters at 50 South LaSalle and watch the foot traffic. You'll see pension fund executives, family office principals, foundation trustees—the people who control trillions in institutional and private wealth. They're not there for the marble lobbies or free coffee. They're there because Northern Trust has built something remarkably difficult to replicate: a business model that gets stronger with time, not weaker.

The dual business model—Asset Servicing versus Wealth Management—isn't just diversification for its own sake. These businesses reinforce each other in ways competitors struggle to match. When Northern Trust services a corporate pension plan, they often manage assets for the company's executives. When they provide custody for a private equity fund, they frequently serve the fund's partners' personal wealth. It's an ecosystem where every relationship creates potential for another.

Asset Servicing is the invisible infrastructure of global finance. Northern Trust doesn't just hold securities—they process corporate actions, manage collateral, handle foreign exchange, calculate NAVs, produce regulatory reports, manage securities lending programs. For a large institutional investor, Northern Trust might touch every transaction, every position, every report. The switching costs aren't just financial—they're operational. Changing custodians means rewiring hundreds of processes, retraining staff, risking operational disruptions that could cost millions.

The numbers tell the story of scale: $17 trillion under custody, thousands of clients, millions of transactions daily. But scale alone doesn't create a moat—State Street and BNY Mellon have scale too. Northern Trust's advantage lies in specialization. They don't try to custody everything. Instead, they focus on complex instruments requiring sophisticated operational expertise: alternatives, private markets, complex derivatives. When a sovereign wealth fund needs to custody private equity investments across 50 countries with different tax treaties, they turn to Northern Trust. The Wealth Management segment operates in an even more rarified atmosphere. Wealth Management focuses on high-net-worth individuals and families, business owners, executives, professionals, retirees, and established privately held businesses in its target markets with assets typically exceeding $75 million. This isn't mass affluent or even merely wealthy—this is generational wealth, the kind that requires dedicated family offices, sophisticated estate planning, and multi-generational thinking.

The moat in wealth management isn't built on performance—anyone can have a good year. It's built on trust accumulated over decades, expertise in complex situations, and the ability to serve as a true partner across generations. When Northern Trust manages a family's wealth through births, deaths, divorces, business sales, and charitable endeavors, they become embedded in the family's financial DNA. These relationships don't move for 10 basis points of fee savings.

Technology amplifies these advantages rather than threatening them. Northern Trust's Wealth Passport platform provides ultra-high net worth families with consolidated reporting across all assets—not just those held at Northern Trust. It's a loss leader that creates switching costs: once a family relies on Northern Trust's reporting infrastructure, moving becomes operationally painful.

The network effects are subtle but powerful. The more ultra-wealthy families Northern Trust serves, the more expertise they develop in specific challenges: cross-border estate planning, concentrated stock positions, private business transitions. This expertise attracts more similar clients, creating a virtuous cycle. When a tech founder needs to diversify a billion-dollar position, they want advisors who've done it before.

Geographic focus creates local network effects. In Chicago, Northern Trust is THE wealth manager for established families. In Florida, they dominate certain wealthy enclaves. These local networks—where Northern Trust advisors serve multiple members of country clubs, charity boards, and business communities—create referral engines that no amount of advertising can replicate.

The regulatory moat deserves attention. Post-2008 regulations made custody and fiduciary services more complex and expensive. Basel III capital requirements, Dodd-Frank compliance, GDPR in Europe—each new rule raises the bar for competitors. Northern Trust's scale allows them to spread these costs across trillions in assets. A startup custodian would need massive investment just to achieve regulatory compliance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube