Sundaram Finance: The Quiet Giant of Indian NBFCs

I. Introduction & Episode Roadmap

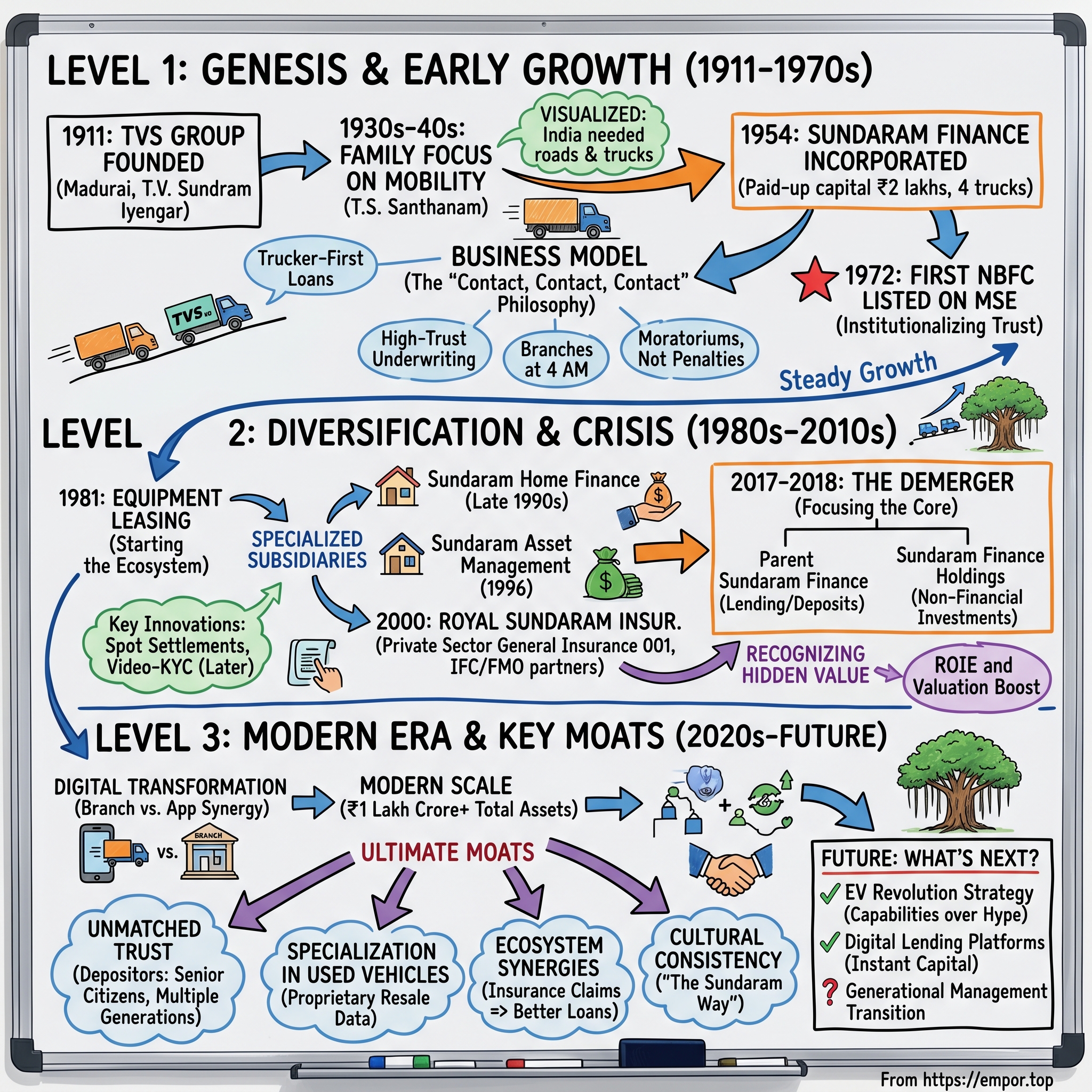

Picture this: It's 2024, and you're walking through the bustling streets of Chennai. Pass by any commercial vehicle depot, and there's a good chance the trucks, buses, and excavators you see were financed by a company most urban Indians have never heard of. Yet this same company manages over ₹1 lakh crore in combined assets, has been trusted by three generations of depositors, and runs India's first private general insurance company. Welcome to the paradox of Sundaram Finance—invisible to many, indispensable to millions.

With a market capitalization hovering around ₹50,000 crore, Sundaram Finance Limited stands as one of India's most valuable non-banking financial companies. But unlike the flashy fintech unicorns or aggressive new-age lenders that dominate business headlines, Sundaram has built its empire through a decidedly old-fashioned approach: deep relationships, conservative underwriting, and an almost religious devotion to trust.

The question that drives this story isn't just how a truck financing company founded in 1954 became a financial services conglomerate. It's how they did it while maintaining the same family values and customer-first philosophy that their founder preached when India was still finding its feet as an independent nation. This is a story about compound trust—how reputation, carefully cultivated over seven decades, becomes an economic moat that no amount of venture capital can replicate.

Our journey begins in pre-independence India with a young lawyer who would plant the seeds of an industrial empire. We'll trace how his son transformed a small vehicle financing operation into a financial powerhouse. We'll examine the strategic chess moves—from becoming India's first private insurer to a complex corporate demerger. And we'll analyze whether this quiet giant can maintain its edge in an era of digital disruption and regulatory flux.

This isn't just the story of Sundaram Finance. It's the story of Indian capitalism itself—from the License Raj to liberalization, from relationship banking to algorithmic lending, from family businesses to professional management. And at its heart lies a simple but profound insight: in a country where trust in institutions runs thin, being boring but reliable might be the greatest competitive advantage of all.

II. TVS Group Genesis & The Founder's Vision

The year was 1877, and in the small town of Thirukkurungudi in Tamil Nadu's deep south, T.V. Sundram Iyengar was born into a traditional Brahmin family. Nobody could have predicted that this lawyer-turned-entrepreneur would lay the foundation for one of India's most enduring business dynasties. But then again, the best origin stories often begin with the most unlikely protagonists.

Young Sundram Iyengar's path to business wasn't linear. After qualifying as a lawyer, he took the steady route—joining the Indian Railways, then moving to banking. These experiences weren't mere career stops; they were his business education. In the railways, he saw how infrastructure could transform commerce. In banking, he understood the power of capital and trust. By 1911, at age 34, he was ready to synthesize these lessons into something bigger.

That year, in Madurai—the ancient temple city that had been a commercial hub for centuries—Sundram Iyengar founded what would become the TVS Group. The name itself was simple: T.V. Sundaram, his initials plus his father's name. But the philosophy he embedded was anything but simple. "Trust, Value, Service"—three words that would later conveniently match the TVS acronym and become the group's eternal mantra.

What made Sundram Iyengar remarkable wasn't just his business acumen but his approach to succession. He had five sons, and rather than create a battle for control, he gave each a distinct territory within the growing empire. It was almost Shakespearean in its elegance—divide the kingdom before conflict could arise. Each son would build his own vertical while maintaining the overarching family values.

Among these five sons, T.S. Santhanam stood out—not for being the eldest or most charismatic, but for his peculiar obsession with mobility. In 1936, while India was still under British rule and most Indians traveled by bullock cart or train, Santhanam moved the family's operations to Madras (now Chennai). He immersed himself in what seemed like disconnected sectors: road transport, automobiles, components, insurance, and banking. To outsiders, it looked scattered. To Santhanam, it was an ecosystem waiting to be born.

The post-independence period of 1947-1950 was India's entrepreneurial crucible. The British had left behind railways but barely any roads. The new nation needed to move goods, connect markets, build infrastructure. Santhanam saw this clearly: India wouldn't industrialize without trucks, and truckers wouldn't buy trucks without financing. The opportunity wasn't just large—it was foundational to the country's economic development.

But here's where the TVS story diverges from typical business narratives. While other business houses rushed to grab licenses for steel plants and textile mills, Santhanam focused on something unglamorous: helping small transport operators buy trucks. His vision wasn't to build an industrial empire but to enable thousands of small entrepreneurs to build theirs. This wasn't just business philosophy; it was almost spiritual—the Brahmanical ideal of enabling others' prosperity.

The cultural context matters here. In 1950s South India, lending money was still viewed through a moral lens. The local Chettiar community had dominated informal lending for centuries, but their high interest rates created more resentment than respect. Santhanam wanted to create something different—lending as service, not exploitation. Finance as enablement, not entrapment.

By the early 1950s, the pieces were in place. The TVS Group had established credibility, Santhanam had identified the opportunity, and India desperately needed vehicle financing. But credibility and opportunity don't automatically translate into a successful financial institution. That transformation would require something more—an almost maniacal focus on understanding customers that would become Sundaram Finance's defining characteristic.

III. The Birth of Sundaram Finance (1954)

The founding moment came in 1954, but not with fanfare or grand announcements. T.S. Santhanam incorporated Sundaram Finance with a paid-up capital of just ₹2 lakhs—roughly $4,000 at the time. To put this in perspective, this was enough to buy perhaps four trucks. The company was promoted by Madras Motor & General Insurance Company, already part of the TVS stable, creating immediate synergies between insurance and financing.

But the real capital Santhanam brought wasn't monetary—it was philosophical. He had spent years traveling across India, and not in first-class railway compartments. He rode in trucks, slept in driver dormitories, ate at roadside dhabas. While other financiers sat in wood-paneled offices waiting for customers to come to them, Santhanam was out on the highways, understanding the economics of transportation from the inside.

His employees still tell stories of Santhanam's travels. He would show up at transport hubs at 4 AM, when drivers were preparing for their journeys. He'd drink chai with them, learning about their routes, their challenges, their dreams. One veteran employee recalled: "Santhanam sir knew the cost of diesel on the Madras-Bombay route better than most transport operators. He knew which stretches had toll taxes, where drivers stopped for meals, how monsoons affected delivery schedules."

This granular understanding translated into revolutionary lending practices. While banks demanded elaborate documentation and collateral, Sundaram Finance developed a system based on understanding cash flows. They knew a transport operator running the Chennai-Bangalore route could make predictable returns. They understood seasonal variations—how harvest seasons meant more cargo, how festivals affected payment schedules.

The "Contact, Contact, Contact" philosophy wasn't just a catchy phrase—it was operational doctrine. Every Sundaram Finance employee was expected to maintain relationships with customers that went beyond transactions. They attended customers' family functions, helped their children with school admissions, provided business advice beyond financing. This wasn't corporate social responsibility; this was relationship banking before anyone coined the term.

The 1960s tested this model severely. India's economy was struggling, the 1962 China war had drained resources, and the 1965 Pakistan war created further uncertainty. Many NBFCs collapsed as borrowers defaulted. But Sundaram Finance's deep relationships paid off. When customers faced difficulties, they came to Sundaram first—not to default, but to restructure. The company's recovery rates stayed above 98% even during the worst periods, a number that seemed almost mythical in Indian lending.

By 1972, Sundaram Finance achieved a milestone that validated Santhanam's vision: it became the first NBFC to list on the Madras Stock Exchange. This wasn't just about raising capital—the company was already profitable and cash-rich. It was about institutionalizing trust. By opening ownership to the public, Santhanam was saying: "We're not just asking you to trust us with your loans; we're inviting you to own part of this institution."

The IPO was priced at ₹10 per share, and it was oversubscribed 3x despite minimal marketing. What's remarkable is that this would be the company's only public offering ever. Unlike modern companies that tap capital markets repeatedly, Sundaram Finance would fund its entire growth trajectory through internal accruals and deposits. This wasn't capital efficiency; it was capital discipline.

The early customer relationships became legendary within the industry. There's the story of K. Raghavan, a transport operator who bought his first truck in 1958 with Sundaram financing. By 1975, he owned a fleet of 50 trucks, all financed by Sundaram. When asked why he never explored other lenders offering lower rates, he said: "When my father died in 1962, I couldn't pay EMIs for three months. Sundaram's manager attended the funeral, gave me six months moratorium, and never charged penalty. You think I care about half a percent interest rate?"

These weren't isolated incidents but systematic relationship building. Sundaram Finance maintained detailed records not just of payment histories but of customer families. Branch managers knew when customers' children were getting married, when they faced medical emergencies, when they were expanding operations. This information wasn't used for cross-selling but for deepening trust.

The transformation was remarkable: from ₹2 lakhs in 1954 to ₹10 crores in assets by 1975. But more importantly, Sundaram Finance had created a template for Indian NBFCs—that you could be profitable while being ethical, that relationships were assets more valuable than collateral, and that in a low-trust society, being boringly reliable was revolutionary.

IV. Diversification & Building the Financial Empire (1980s–2000s)

The 1980s marked an inflection point for Sundaram Finance. Under the leadership of T.S. Santhanam's chosen successors, the company faced a strategic crossroads: remain a specialized vehicle financier or evolve into a comprehensive financial services provider. The answer came not from strategy consultants or market research, but from listening to customers who were asking, "You've helped us buy trucks, can you help us buy homes? Lease equipment? Manage our surplus funds?"

The diversification began in 1981 with equipment leasing—a natural extension from vehicle financing. But this wasn't random expansion. The same transport operators who bought trucks also needed trailers, containers, and material handling equipment. The same construction companies that bought excavators needed concrete mixers and cranes. Sundaram Finance wasn't entering new markets; it was serving existing customers more comprehensively.

The real strategic masterstroke came post-1989 when Sundaram began creating specialized subsidiaries rather than divisions. India Equipment Leasing Ltd. for specialized leasing, Sundaram Home Finance Ltd. for housing loans—each entity had its own management, capital structure, and regulatory compliance. This wasn't bureaucratic complexity; it was risk management through structural design. If one vertical faced regulatory challenges, others remained insulated.

The housing finance venture deserves special attention. In the early 1990s, housing finance in India was dominated by HDFC and LIC Housing Finance. Sundaram's entry seemed late and unnecessary. But they brought a unique angle: financing homes for the same commercial vehicle drivers and small transport operators they'd served for decades. These customers had irregular but substantial incomes that traditional housing financiers couldn't underwrite. Sundaram could because they had 40 years of cash flow data.

The international partnerships revealed sophisticated thinking. Rather than going alone, Sundaram brought in the International Finance Corporation (IFC) Washington and FMO Netherlands as partners in the housing finance venture. This wasn't just about capital—both institutions brought global best practices in mortgage underwriting and risk management. More importantly, their presence signaled to regulators and markets that Sundaram operated at international standards.

The 1996 joint venture with Newton Management Limited UK for asset management was particularly prescient. India's mutual fund industry was nascent, dominated by Unit Trust of India. But Sundaram saw that rising incomes would create demand for professional wealth management. The timing seemed early—India's GDP per capita was still under $400. But this was exactly the point: build capabilities before the market explodes, not after.

Between 1999 and 2000, Sundaram executed a complex series of amalgamations that would make investment bankers proud. India Equipment Leasing, Aparajita Finance, Balika Finance, and Paramjyothi Finance were all merged into the parent entity. The total consideration of ₹20.10 crores seemed modest, but the strategic value was immense. These companies brought geographic presence, customer relationships, and specialized expertise that would have taken years to build organically.

What made this diversification successful wasn't financial engineering but cultural consistency. Every new venture followed the same Sundaram playbook: deep customer understanding, conservative underwriting, and relationship-first approach. A customer getting a home loan experienced the same service philosophy as one financing a truck. This consistency created a network effect—satisfied customers in one vertical became ambassadors for other services.

The numbers tell the story: by 2000, Sundaram Finance's assets had grown to ₹3,000 crores from ₹100 crores in 1985. But more importantly, the company had transformed from a monoline vehicle financier to a diversified financial services provider with presence across the customer lifecycle—vehicle loans for business, home loans for security, deposits for savings, mutual funds for wealth creation, insurance for protection.

The ecosystem approach created competitive advantages that went beyond individual products. A transport operator who took a vehicle loan often placed his surplus funds in Sundaram deposits, bought insurance from Royal Sundaram, and invested in Sundaram mutual funds. This wasn't aggressive cross-selling but natural progression of trust. The lifetime value of customers exploded while acquisition costs remained minimal.

By the late 1990s, as India stood on the cusp of financial liberalization, Sundaram Finance had positioned itself perfectly. It had the infrastructure, relationships, and credibility to capitalize on the coming boom. But the biggest opportunity—and challenge—would come from an unexpected quarter: the opening up of India's insurance sector, monopolized by government companies since 1956.

V. The Insurance Revolution: Royal Sundaram Story (2000)

October 2000 should have been a moment of triumph for Sundaram Finance. After years of lobbying, regulatory preparation, and partnership negotiations, Royal Sundaram Alliance Insurance Company received the first private sector general insurance license in independent India's history. Yet T.S. Krishnamurthy, then Managing Director of Sundaram Finance, later recalled feeling "more trepidation than celebration." They were about to compete with the Life Insurance Corporation and General Insurance Corporation—behemoths that had monopolized Indian insurance for 44 years.

The backstory reveals remarkable foresight. As early as 1995, when insurance liberalization was just political speculation, Sundaram Finance began preparing. They studied global insurance markets, sent executives for training abroad, and most crucially, began searching for the right international partner. The choice of Royal & SunAlliance Insurance plc wasn't random—they were the world's second-largest general insurer with 300 years of history. If Sundaram was going to challenge monopolies, they needed heavyweight backing.

The regulatory journey itself was Kafkaesque. The Insurance Regulatory and Development Authority (IRDAI) had just been formed in 1999. Nobody knew exactly what standards would be required. Sundaram's team submitted a license application that ran over 5,000 pages, detailing everything from actuarial models to claim settlement procedures. They were essentially writing the playbook while playing the game.

When the license finally arrived—literally the first one issued, bearing serial number 001—the challenge became execution. How do you sell insurance in a market where the concept itself was associated with government inefficiency and claim rejection? Royal Sundaram's answer was radical for its simplicity: actually pay claims quickly.

The company introduced "Spot Settlement" for motor insurance claims under ₹50,000. While government insurers took months, Royal Sundaram promised settlement in hours. The first such claim was processed in Chennai in December 2000—a small accident, ₹12,000 damage, settled in 3 hours. The customer, a taxi driver named Murugan, became an inadvertent brand ambassador, telling everyone about this "new insurance company that actually pays."

The distribution strategy leveraged Sundaram Finance's existing network brilliantly. Every vehicle finance branch became an insurance point-of-sale. But they went beyond tied selling. Royal Sundaram created India's first dedicated insurance advisors—trained professionals who only sold insurance, not loans or investments. This specialization was expensive but created service differentiation that customers noticed.

By 2005, Royal Sundaram had captured 5% of private general insurance market—impressive given that 15 other private players had entered. But the real validation came from an unexpected source: the Tamil Nadu government chose Royal Sundaram for its pioneering health insurance scheme covering below-poverty-line families. A private insurer managing government welfare—it was unprecedented.

The 2015 buyout of Royal & SunAlliance's 26% stake for ₹732 crores was a defining moment. Sundaram Finance raised its holding to 75.90%, effectively taking control. The timing was perfect—the foreign partner needed capital for global restructuring, while Sundaram wanted greater strategic freedom. The price implied a valuation of ₹2,800 crores for Royal Sundaram, which seemed expensive then but would prove prescient.

The 2019 entry of Ageas Insurance International N.V. as a 40% strategic partner marked another evolution. Ageas brought European expertise in digital insurance and data analytics. The resulting ownership structure—Sundaram Finance 50%, Ageas 40%, other Indian shareholders 10%—created perfect balance between local knowledge and global capability.

What made Royal Sundaram successful wasn't just first-mover advantage but cultural transformation of insurance itself. They published claim settlement ratios monthly (unheard of in the industry), created India's first 24/7 claim hotline, and introduced cashless garage networks for motor repairs. These seem standard today; in 2000, they were revolutionary.

The numbers validate the strategy: Royal Sundaram's gross written premium grew from ₹100 crores in 2001 to ₹4,000 crores by 2020. More importantly, their claim settlement ratio consistently exceeded 85%, compared to industry averages below 70%. In a business built on trust, being trustworthy was competitive advantage.

The insurance venture also created unexpected synergies. Data from insurance claims improved vehicle financing underwriting. Insurance customers became deposit clients. The ecosystem effect compounded—each business strengthened others. By 2020, Royal Sundaram wasn't just a successful subsidiary; it had become integral to Sundaram Finance's identity as a comprehensive financial services provider.

VI. The Demerger Drama & Corporate Restructuring (2017–2018)

The board meeting in March 2017 was unusually tense. Sundaram Finance's directors faced a decision that would fundamentally alter the company's 63-year-old structure. The proposal: demerge all non-financial investments—the automotive components business, training services, shared services, property holdings—into a separate entity. For a company that had never undertaken major restructuring, this was corporate surgery of the highest order.

The catalyst wasn't crisis but clarity. New RBI regulations were increasingly distinguishing between "core" and "non-core" activities of NBFCs. Sundaram Finance owned stakes in TVS Lucas (automotive components), Turbo Energy (wind turbine components), and various real estate holdings. These investments, accumulated over decades, were profitable but created regulatory complexity. More importantly, they obscured the company's true financial services performance from investors.

S. Viji, the CFO who architected the demerger, explained the logic with a simple analogy: "Imagine you're running a restaurant, but you also own the farms that supply vegetables. The farms are profitable, but restaurant investors want to evaluate your cooking, not your farming. We needed to separate the two."

The mechanics were elegant: create Sundaram Finance Holdings Limited (SFHL), transfer all non-core investments to it, and give existing shareholders one SFHL share for every Sundaram Finance share held. No cash changed hands, no shareholder was disadvantaged, but suddenly investors had two pure-play investments instead of one conglomerate.

The market's initial reaction was confused. Sundaram Finance stock fell 8% on announcement day. Analysts scrambled to value the demerged entities separately. Short-sellers bet that the sum of parts would be less than the whole. They were spectacularly wrong.

What happened next validated the strategy brilliantly. Freed from regulatory constraints on non-financial investments, Sundaram Finance could deploy capital more efficiently into its core lending business. Return on equity improved from 14% to 18% within two years. Meanwhile, SFHL could pursue manufacturing opportunities without NBFC restrictions. Both entities became more valuable apart than together.

The demerger also revealed hidden value. The property holdings transferred to SFHL included land parcels in Chennai acquired decades ago for branch offices. Urban expansion had turned these into prime real estate. SFHL's book value exceeded ₹1,000 crores, essentially value that had been invisible within Sundaram Finance's consolidated statements.

The human dimension was equally important. Employees in manufacturing ventures no longer felt like stepchildren in a financial services company. They had their own board, strategy, and growth path. Sundaram Finance employees could focus purely on financial services without distraction. Specialization improved execution in both entities.

The timing proved prescient. By 2018, RBI introduced stricter guidelines on NBFCs' non-financial investments. Companies that hadn't restructured faced forced asset sales at distressed valuations. Sundaram had moved proactively, maintaining control and maximizing value. This wasn't just compliance; it was strategic foresight.

The demerger's success triggered broader introspection. If separating non-core assets created such value, what about the financial services portfolio itself? Should housing finance, insurance, and asset management be listed separately? The board decided against further splits, believing the ecosystem synergies outweighed pure-play premiums. Time would prove them right.

By 2019, the demerger benefits were undeniable. Sundaram Finance's valuation multiples expanded from 2.5x to 3.5x book value. SFHL traded at respectable valuations despite being a holding company. Combined market capitalization of both entities exceeded the pre-demerger value by 40%. Financial engineering had created real economic value.

The demerger also marked a generational transition in thinking. The older generation had built through accumulation—adding businesses, properties, investments. The new leadership understood that in modern capital markets, focus trumps diversification. Less could indeed be more if the "less" was clearly defined and excellently executed.

VII. Modern Era: Digital Transformation & Scale

The WhatsApp message arrived at 11:47 PM on a Sunday in March 2021. A transport operator in Pune needed urgent working capital to bid for a large contract the next morning. By 6 AM Monday, ₹50 lakhs had been credited to his account. No branch visit, no physical documents, no human intervention beyond the initial message. For a company built on high-touch relationships, this seamless digital execution represented a revolution as profound as any in its 67-year history.

The digital transformation journey hadn't been smooth. As late as 2015, Sundaram Finance's technology infrastructure was, charitably speaking, vintage. Core banking ran on AS/400 systems from the 1990s. Loan applications were paper-based. Customer data lived in branch-level silos. For a company with ₹30,000 crores in assets, this wasn't just inefficient—it was existential risk.

The wake-up call came from an unexpected source: customers. The same transport operators who'd been visiting branches for decades suddenly started asking about mobile apps. Their children, now involved in family businesses, expected Instagram-style interfaces for loan applications. The choice was stark: evolve or become irrelevant.

Rather than pursue big-bang transformation, Sundaram chose surgical strikes. First priority: digitize customer-facing processes while keeping backend systems stable. They partnered with niche fintech firms for specific solutions—loan origination, credit scoring, document management—rather than buying expensive enterprise platforms. This "best of breed" approach cost more in integration but delivered faster results.

The numbers tell the transformation story: Digital loan origination grew from 0% in 2016 to 65% by 2023. Customer acquisition cost dropped 40%. Loan processing time reduced from 7 days to 4 hours for existing customers. Yet branch networks expanded from 640 to nearly 1,000 locations. This wasn't digital replacing physical but augmenting it.

The COVID-19 pandemic accelerated changes that might have taken years. When lockdowns prevented branch visits, Sundaram launched video-KYC within three weeks—a process that typically took Indian financial institutions six months. They created "Digital Relationship Managers"—experienced staff who managed customers entirely through video calls, maintaining the high-touch feel through high-tech mediums.

But digital transformation revealed a deeper challenge: data. Sundaram had seven decades of customer information, but it was fragmented across systems, formats, and locations. The data lake project launched in 2020 aimed to create a unified view of every customer interaction since 1954. Early results were remarkable—they discovered that 40% of new customers had family members who were existing clients, enabling relationship-based underwriting that no algorithm could replicate.

The competitive landscape had also transformed dramatically. On one side, banks with unlimited capital were aggressively entering vehicle financing. On another, fintech startups promised instant loans through apps. Traditional NBFCs were getting squeezed from both ends. Sundaram's response was counterintuitive: don't compete on speed or price, double down on specialized knowledge.

Take the used commercial vehicle financing segment. While fintechs relied on generic algorithms, Sundaram developed proprietary models incorporating 50 years of resale data, route economics, and operator profiles. They could price a 2015 Ashok Leyland truck operating on the Chennai-Coimbatore route more accurately than any competitor. This wasn't just data science; it was domain expertise encoded in algorithms.

The scale achieved by 2024 is staggering: ₹50,000+ crores in assets under management, additional ₹56,000 crores in third-party assets managed through subsidiaries. The company serves over 200,000 depositors, 300,000 vehicle finance customers, and millions of insurance policyholders. Yet the average ticket size remains modest—₹15 lakhs for commercial vehicles, ₹6 lakhs for cars. This is financial inclusion at scale.

The human capital transformation paralleled digital changes. Average employee age dropped from 45 to 35 years between 2015 and 2023. New hires included data scientists, UX designers, and cybersecurity experts—roles that didn't exist in Sundaram a decade ago. Yet the company maintained its promote-from-within culture, with 70% of senior management being internal promotions.

The investment in technology—over ₹500 crores between 2018 and 2023—seemed massive for a company that had historically been capital-efficient. But the returns justified the spending. Operating expense ratios improved despite technology investments. Net interest margins expanded as better data enabled superior risk pricing. Most importantly, customer satisfaction scores, measured through Net Promoter Score, reached 70+, exceptional for financial services.

VIII. Business Model & Competitive Advantages

To understand Sundaram Finance's competitive positioning, you need to appreciate the elegant simplicity of its business model. At its core, the company does three things exceptionally well: it takes deposits from retail investors, lends money for productive assets, and provides financial protection through insurance. Everything else—the technology, the branches, the subsidiaries—exists to support these three pillars.

The deposit franchise represents the foundation. With over 2 lakh depositors, Sundaram has built what Warren Buffett would call "float"—low-cost, sticky capital that funds lending operations. What's remarkable is the composition: 60% are senior citizens who've been depositing for over a decade, 30% are second-generation customers whose parents were depositors, and many have never visited a branch in years yet renew automatically. This isn't just capital; it's institutional trust monetized.

The lending portfolio reveals sophisticated risk management. Vehicle finance dominates—60% commercial vehicles, 25% passenger cars, 15% construction equipment and tractors. But within each category lies granular specialization. Sundaram doesn't just finance "trucks"; they understand the economics of specific routes, cargo types, and operator profiles. They know that a refrigerated truck on the Delhi-Mumbai route has different risk characteristics than a cement carrier in Tamil Nadu. This knowledge, accumulated over decades and now encoded in algorithms, enables pricing precision that generalist lenders can't match.

The subsidiary ecosystem creates multiple competitive moats. Royal Sundaram General Insurance doesn't just provide another revenue stream; it generates claims data that improves vehicle financing underwriting. Sundaram Home Finance serves the same customers who take vehicle loans, reducing acquisition costs. Sundaram Asset Management manages surplus funds for the same depositors and borrowers. Each business strengthens others through shared customers, data, and trust.

Consider the economics of customer acquisition. A typical NBFC spends 2-3% of loan value on origination—advertising, sales commissions, documentation. Sundaram's cost: 0.8%. Why? Because 45% of new vehicle loans come from existing customers or referrals. A transport operator who took his first loan in 1990 has introduced his son, nephew, and business partners. Three generations of a family might have relationships across deposits, loans, insurance, and investments. The lifetime value of such relationships is extraordinary.

The cross-selling metrics validate the ecosystem approach. The average customer uses 2.3 Sundaram products. For customers with relationships exceeding five years, this rises to 3.1 products. More importantly, multi-product customers have 90% lower default rates and 40% lower servicing costs. This isn't coincidence—customers who trust you with deposits are more likely to repay loans.

Geographic diversification provides stability. While 35% of business comes from Tamil Nadu (the home state), no single state exceeds 15% of portfolio. This wasn't planned expansion but organic growth following customer migration. As South Indian transport operators expanded nationally, Sundaram followed. Today, a truck financed in Chennai might operate on routes to Guwahati, creating natural geographic hedging.

The competitive landscape has evolved dramatically. Banks, with access to low-cost CASA deposits, can underprice on interest rates. Fintech lenders promise instant approval and minimal documentation. Yet Sundaram's market share in commercial vehicle financing has remained stable at 8-10% for two decades. The reason: specialization trumps generalization in complex lending.

Take the used commercial vehicle segment—a ₹50,000 crore market that banks largely ignore and fintechs can't crack. Valuing a five-year-old truck requires understanding maintenance history, operator reputation, route economics, and resale dynamics. Sundaram's database includes transaction prices for 500,000 used vehicles over 30 years. No algorithm can replicate this institutional knowledge overnight.

The trust advantage manifests in crisis resilience. During the 2008 financial crisis, when other NBFCs faced deposit runs, Sundaram saw deposit inflows increase 15%. During COVID-19, when vehicle utilization plummeted, Sundaram's collection efficiency stayed above 95% while industry averages dropped to 70%. Customers prioritized Sundaram repayments because they valued the long-term relationship more than short-term relief.

The capital efficiency metrics reveal disciplined execution. Return on equity consistently exceeds 15% despite conservative leveraging (debt-to-equity below 5x versus regulatory permission of 10x). Net interest margins of 7-8% seem modest versus fintech lenders claiming 12-15%, but Sundaram's credit costs (loan losses) average 0.5% versus industry norms of 2-3%. The result: consistent profitability through cycles.

The moat isn't impregnable. Digital-native customers might not value relationship banking. Electric vehicles could disrupt financing economics. Regulatory changes could compress margins. But Sundaram's response has been thoughtful evolution rather than dramatic transformation—digitizing processes while maintaining human touchpoints, preparing for EV financing while dominating ICE vehicles, diversifying revenue while maintaining core focus.

IX. Playbook: Leadership & Culture Lessons

The Monday morning ritual at Sundaram Finance headquarters hasn't changed in 40 years. At 8:30 AM sharp, senior management gathers for what they call "customer notes"—a 30-minute session where branch managers share customer stories from the previous week. Not statistics or targets, but actual narratives: the transport operator who expanded his fleet, the driver who became an owner, the family that faced medical emergency. This isn't corporate theater; it's cultural transmission.

The leadership philosophy traces directly to T.S. Santhanam's principles, documented in a slim volume called "The Sundaram Way" that every employee receives on joining. The core insight: in financial services, culture is strategy. You can copy products, poach people, and replicate processes, but you cannot duplicate seven decades of behavioral consistency.

Consider how leadership transitions have been managed. When T.S. Santhanam stepped down in 1985, he didn't anoint a family successor. Instead, R. Thyagarajan, a professional who'd joined as a management trainee, became Managing Director. This set a precedent: competence over bloodline. Yet family members remained on the board, providing continuity of values while allowing professional management to drive operations.

The current leadership structure reflects this balance. Harsha Viji, the current Managing Director (promoted in 2021), joined as a management trainee in 1987. She worked in every department—operations, credit, treasury, strategy—before reaching the top. This isn't just succession planning; it's cultural preservation through lived experience.

The decision-making framework reveals institutional wisdom. Major decisions require what they call "three-generation thinking"—how would the founder view this, how does current leadership assess it, and what legacy does it leave for future leaders? This sounds philosophical, but it drives practical choices. The decision to avoid subprime lending during the 2003-2007 credit boom came from asking: "Would T.S. Santhanam have been comfortable with these customers?"

Employee development follows the "growing banyan tree" model. Like the banyan's aerial roots that become new trunks, senior employees are expected to mentor multiple juniors who eventually become leaders themselves. The company maintains detailed "mentorship trees" showing how knowledge transferred across generations. A branch manager in Coimbatore can trace his training lineage back to executives from the 1960s.

The compensation philosophy defies modern HR trends. No stock options, no variable pay exceeding 30% of total compensation, no massive CEO pay multiples. The highest-paid executive earns roughly 50x the lowest-paid employee—modest by global standards. Yet employee retention exceeds 85% after five years. The trade-off is explicit: moderate financial rewards for exceptional job security and cultural belonging.

Customer-first philosophy isn't a slogan but operational reality. Branch managers have discretionary authority to waive penalties, restructure loans, and make exceptions—powers that algorithm-driven lenders would consider heretical. One branch manager recounted approving a loan renewal for a transport operator whose son had died in an accident, despite missed payments. "The family needed support, not pressure. They've been customers for 20 years. They'll recover and remember."

The risk management culture balances empowerment with accountability. Every credit officer maintains a "relationship book"—a physical ledger of loans they've approved. Even after promotion or transfer, they track these loans' performance. Default isn't just a statistical event but personal responsibility. This creates natural conservatism—you're more careful when your signature follows the loan forever.

Communication patterns reinforce values. The company still publishes a physical newsletter, "Sundaram Samachar," featuring customer success stories, employee achievements, and messages from leadership. Email exists, but important announcements come through traditional channels. The annual general meeting includes a cultural program where employees' children perform classical music—connecting business with broader Tamil cultural traditions.

The approach to technology reveals cultural sophistication. Rather than positioning digital transformation as replacing human judgment, leadership frames it as "giving our people better tools to serve customers." The loan origination system doesn't eliminate credit officers; it frees them from paperwork to spend more time understanding customer needs. This framing prevented the resistance that derailed digital initiatives at other traditional institutions.

Failure handling demonstrates maturity. When a ₹100 crore fraud was discovered in the Bangalore operations in 2015, the response was instructive. No scapegoating, no mass firings. Instead, systematic process improvement, additional training, and most importantly, public acknowledgment that systems failed, not just individuals. The manager who discovered the fraud was promoted, signaling that identifying problems was valued over hiding them.

The paradox of Sundaram's culture: it's simultaneously rigid and flexible. Core values—trust, service, relationships—remain inviolate. But operational practices evolve constantly. The company that once insisted on physical documentation now approves loans via WhatsApp. The institution that promoted only from within now hires data scientists from IITs. This isn't contradiction but sophistication—knowing what to preserve and what to change.

External validation confirms cultural strength. Sundaram regularly appears on "Great Places to Work" lists, but more telling are informal indicators. The children of employees often join the company—not through nepotism but genuine preference. Competitors regularly poach Sundaram employees for senior positions, viewing "Sundaram training" as quality certification. Retired employees often continue unofficial ambassadorship, referring customers decades after leaving.

X. Analysis & Investment Case

The investment thesis for Sundaram Finance requires understanding a fundamental tension: this is simultaneously one of India's most expensive NBFCs and potentially one of its most undervalued financial franchises. Trading at 3.78 times book value when peers average 1.5-2x, the valuation seems demanding. Yet dig deeper, and the premium might be justified—even conservative.

Start with the numbers that matter. Revenue grew 20.75% year-over-year to ₹2,207.35 crores in Q3 2024-25, while net profit increased 6.56% to ₹455.47 crores. The growing gap between revenue and profit growth signals margin pressure—likely from rising funding costs and competitive intensity. Net profit margins compressed to 20.63%, still healthy but trending downward.

The balance sheet reveals both strength and concern. Assets exceed ₹50,000 crores with additional ₹56,000 crores under management, providing scale advantages in technology investments and regulatory compliance. However, the company has low interest coverage ratio, suggesting earnings are sensitive to rate cycles—a vulnerability in the current rising rate environment.

Promoter holding at 37.2% strikes an optimal balance—high enough to ensure aligned interests, low enough to provide market liquidity. The promoter stake has remained stable for years, signaling neither distress selling nor creeping acquisitions. This stability matters in Indian markets where promoter actions often signal more than financial statements.

The competitive positioning appears sustainable despite pressures. In commercial vehicle financing, Sundaram maintains 8-10% market share despite bank aggression. The moat isn't market share but segment selection—focusing on used vehicles, small operators, and specialized equipment where relationship banking matters more than rate competition. This is classic Porter strategy: compete where your advantages matter most.

Regulatory dynamics favor established players. RBI's tightening of NBFC regulations—higher capital requirements, stricter asset classification, enhanced governance standards—creates compliance costs that smaller players cannot bear. Sundaram's size and systems position it to benefit from industry consolidation. The regulatory burden that seems negative actually strengthens competitive position.

The technology transformation, while expensive, is bearing fruit. Digital origination reducing costs, data analytics improving risk selection, and automated operations enhancing productivity. The ₹500 crore technology investment seems large, but spread across ₹50,000 crore assets, it's just 1%—reasonable for capability building that should yield benefits for years.

Geographic and product diversification provides resilience. No state exceeds 15% of portfolio, no product exceeds 35% of revenue. This isn't exciting growth but boring stability—exactly what conservative investors value. During regional disruptions (Kerala floods, Maharashtra lockdowns), portfolio impact remained manageable.

The hidden value lies in subsidiaries. Royal Sundaram, with gross written premiums exceeding ₹4,000 crores, could be worth ₹5,000-7,000 crores independently. Sundaram Home Finance, with its niche positioning, might value at ₹2,000-3,000 crores. The sum-of-parts valuation exceeds current market cap, suggesting either the market misunderstands the structure or sees risks not apparent in numbers.

Risk factors deserve serious consideration. Asset quality, while historically strong, faces challenges from economic slowdowns affecting transport operators. Electric vehicle transition could obsolete existing expertise in ICE vehicle financing. Fintech disruption might erode margins even if market share holds. These aren't immediate threats but secular challenges requiring strategic response.

The interest rate sensitivity cuts both ways. Rising rates increase funding costs, pressuring margins. But they also reduce competition from venture-funded fintechs dependent on cheap capital. Sundaram's deposit franchise provides funding stability that purely wholesale-funded NBFCs lack. In a rate cycle, boring retail deposits become strategic advantage.

The management quality premium seems justified. Conservative accounting, transparent disclosure, and prudent capital allocation create trust that translates to lower funding costs and higher valuations. The decision to avoid aggressive growth during credit booms has cost short-term returns but preserved long-term franchise value.

Relative valuation provides context. Bajaj Finance trades at 5-6x book value with higher growth but more retail exposure. Cholamandalam Investment trades at 2.5-3x with similar business mix but less conservative underwriting. Sundaram's premium to Chola seems justified; discount to Bajaj reflects growth differential.

The investment case ultimately depends on time horizon and philosophy. For momentum investors seeking quarterly beats, Sundaram disappoints—growth is steady, not spectacular. For quality investors valuing franchise strength, the premium valuation seems reasonable for a business that's survived every crisis since 1954. For value investors, the sum-of-parts discount provides margin of safety.

XI. The Future: What's Next for Sundaram?

The electric vehicle revolution isn't coming to India—it's already here, just unevenly distributed. In Sundaram Finance's Mumbai office, loan applications for electric three-wheelers now exceed those for CNG variants. Yet in Bihar branches, customers haven't even inquired about EV financing. This asymmetric transition represents both existential threat and generational opportunity for a company built on internal combustion expertise.

Sundaram's EV strategy reveals characteristic thoughtfulness. Rather than rushing to finance every electric vehicle, they're building expertise systematically. Partnerships with OEMs to understand battery degradation curves. Pilot programs with fleet operators to model total cost of ownership. Specialized training for credit officers on EV economics. This isn't just product development; it's capability building for a fundamentally different asset class.

The challenge goes beyond technology. EV financing requires understanding battery leasing models, charging infrastructure availability, and electricity tariff structures. Residual values—critical for loan recovery—remain unpredictable. A five-year-old diesel truck has established resale markets; a five-year-old electric truck with degraded battery pack is still an unknown. Sundaram is essentially rebuilding decades of knowledge from scratch.

Yet the opportunity is massive. India's commercial EV market could reach ₹500,000 crores by 2030. Early movers who crack the financing model will dominate for decades. Sundaram's advantages—relationships with fleet operators, understanding of route economics, trust for long-term partnerships—remain relevant. The assets change; the underlying business doesn't.

Digital lending platforms represent another transformation vector. While Sundaram has digitized existing processes, the next leap involves entirely digital products. Think instant working capital loans for transporters based on GPS tracking data. Or dynamic pricing that adjusts interest rates based on real-time utilization metrics. The company is piloting such products, but cultural resistance remains—loan officers trained on relationship banking struggle with algorithmic decision-making.

The partnership strategy is evolving. Recent collaborations with fintech startups for specific capabilities—Open Financial for banking APIs, Perfios for bank statement analysis—signal recognition that not everything needs building internally. The challenge: maintaining cultural integrity while absorbing external innovation. Early results seem positive, with fintech partners appreciating Sundaram's domain expertise while providing technological capabilities.

Rural and semi-urban expansion offers organic growth without competitive intensity. India's 6,000+ towns with populations between 20,000-100,000 remain underserved by formal financial services. Sundaram's branch expansion focuses on these markets, leveraging the trust premium that matters more in smaller communities. A branch in Tirunelveli might take three years to break even, but once established, faces minimal competition for decades.

The wealth management opportunity for India's growing affluent class seems natural yet complex. The same business families that took vehicle loans in the 1980s now have second-generation entrepreneurs seeking sophisticated financial planning. Sundaram's mutual fund and portfolio management services target this segment. But transitioning from lending relationship to advisory relationship requires different capabilities—from product pushing to solution designing.

Generational transition poses the ultimate test. The third generation of founding family members now occupies board positions. They bring global education and modern perspectives but must maintain cultural continuity. More critically, the professional management—many nearing retirement—must transfer institutional knowledge to younger leaders who've never experienced pre-liberalization India.

The regulatory landscape continues evolving. RBI's proposed guidelines on digital lending, climate risk disclosure, and operational resilience will require substantial compliance investments. But regulation also creates opportunity. As marginal players exit, market share concentrates among capable institutions. Sundaram's compliance infrastructure positions it to benefit from regulatory tightening.

International expansion remains notably absent from strategic priorities. While Indian companies aggressively pursue global markets, Sundaram remains India-focused. This isn't provincialism but pragmatism—the domestic opportunity remains massive, and international expansion would dilute focus. The company that took 70 years to cover India won't rush into Africa or Southeast Asia.

The biggest question: can Sundaram maintain its cultural DNA while scaling for modern markets? The company now employs over 5,000 people across 1,000 locations. Maintaining consistent service culture at this scale challenges any organization. Early indicators seem positive—customer satisfaction scores remain high, employee engagement stays strong. But cultural dilution happens gradually, then suddenly.

Climate change adds another dimension. Extreme weather events affecting vehicle operations, transition to sustainable finance, and environmental regulations on vehicle emissions all impact business models. Sundaram has begun incorporating climate risk in underwriting, but this remains nascent. The company that understood monsoon impacts on trucking routes must now model unprecedented weather patterns.

The convergence of these trends—electrification, digitalization, regulation, climate change—suggests the next decade will challenge Sundaram more than the previous seven. Success requires balancing preservation with transformation, maintaining what makes Sundaram special while evolving for new realities.

XII. Epilogue & Key Takeaways

Step back from the numbers, strategies, and market dynamics, and Sundaram Finance's story reveals something profound about business building in emerging markets. This isn't just a company that succeeded; it's an institution that helped build modern India's commercial infrastructure, one truck loan at a time.

The compound effect of reputation emerges as the central lesson. Every satisfied customer from 1954 onwards became a node in an expanding trust network. Their children became customers, their business partners took loans, their communities developed confidence in formal financial services. Sundaram didn't just build a loan book; it created social capital that compounds faster than financial returns.

What would T.S. Santhanam think of today's Sundaram? The scale would astound him—₹50,000 crores in assets versus ₹2 lakhs in founding capital. The technology would bewilder him—algorithms approving loans he personally underwrote. But the core would feel familiar: relationships driving transactions, trust determining success, and service defining differentiation. The tools changed; the philosophy endured.

The story matters for Indian financial services because it proves an alternative path exists. While others chase valuation unicorns through aggressive lending and regulatory arbitrage, Sundaram demonstrates that boring excellence creates lasting value. In markets where trust is scarce, being trustworthy becomes the ultimate competitive advantage.

For investors, Sundaram offers a fascinating study in quality versus growth trade-offs. The company will never deliver venture-style returns or fintech-like growth rates. But it also won't implode from aggressive lending or regulatory crackdowns. This is a marathon runner in a market full of sprinters—less exciting to watch but more likely to finish the race.

The sustainability lesson transcends financial services. In an era of blitzscaling and growth-at-all-costs mentality, Sundaram proves that building slowly but soundly creates more durable value. The company that took 20 years to expand beyond Tamil Nadu now operates nationally with minimal credit losses. Patience wasn't constraint but strategy.

The cultural preservation amid scaling provides a template for family businesses professionalizing. By separating ownership from operation while maintaining value transmission, Sundaram avoided both nepotistic decay and cultural dilution. The third generation of family members provides governance while professional managers drive operations—a balance many family businesses fail to achieve.

For entrepreneurs, the Sundaram story offers both inspiration and warning. Inspiration that customer obsession and ethical practice can build hundred-billion-rupee enterprises. Warning that such building takes decades, requires immense patience, and offers few shortcuts. This isn't a get-rich-quick story but a get-rich-slowly-and-surely narrative.

The regulatory relationship model deserves study. By consistently exceeding compliance requirements and maintaining transparent communication, Sundaram earned regulatory trust that translates to business flexibility. While others fight regulations, Sundaram shapes them through demonstrated responsibility. This isn't lobbying but leadership through example.

The ecosystem approach—building multiple related businesses that strengthen each other—provides lessons for platform strategies. But unlike tech platforms that extract value through network effects, Sundaram creates value through service integration. Customers aren't locked in through switching costs but retained through satisfaction. This is platform economics with human face.

As India accelerates toward becoming a $10 trillion economy, institutions like Sundaram Finance become more, not less, important. The country needs financial intermediaries that can channel savings into productive assets, support entrepreneurship without recklessness, and maintain stability through cycles. Sundaram has proven it can do all three.

The ultimate takeaway: in financial services, culture is strategy, reputation is moat, and trust is currency. Sundaram Finance didn't discover these truths; it institutionalized them. For seven decades, through multiple crises and transformations, the company has demonstrated that doing the right thing repeatedly creates more value than any financial engineering.

Whether Sundaram can maintain this trajectory through electric vehicles, digital disruption, and generational transition remains uncertain. But the foundation—deep customer relationships, conservative underwriting, and cultural consistency—provides better odds than any algorithm or innovation. In a world of constant change, being boringly reliable might be the most radical strategy of all.

The quiet giant of Indian NBFCs will likely remain quiet, steadily financing India's growth without fanfare or headlines. And perhaps that's the greatest lesson: sustainable value creation rarely makes noise. It compounds silently, visible only to those patient enough to look beyond quarterly earnings to generational impact.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube