Nationstar Mortgage / Mr. Cooper Group: The Phoenix of American Mortgage Servicing

Introduction: A $14 Billion Question

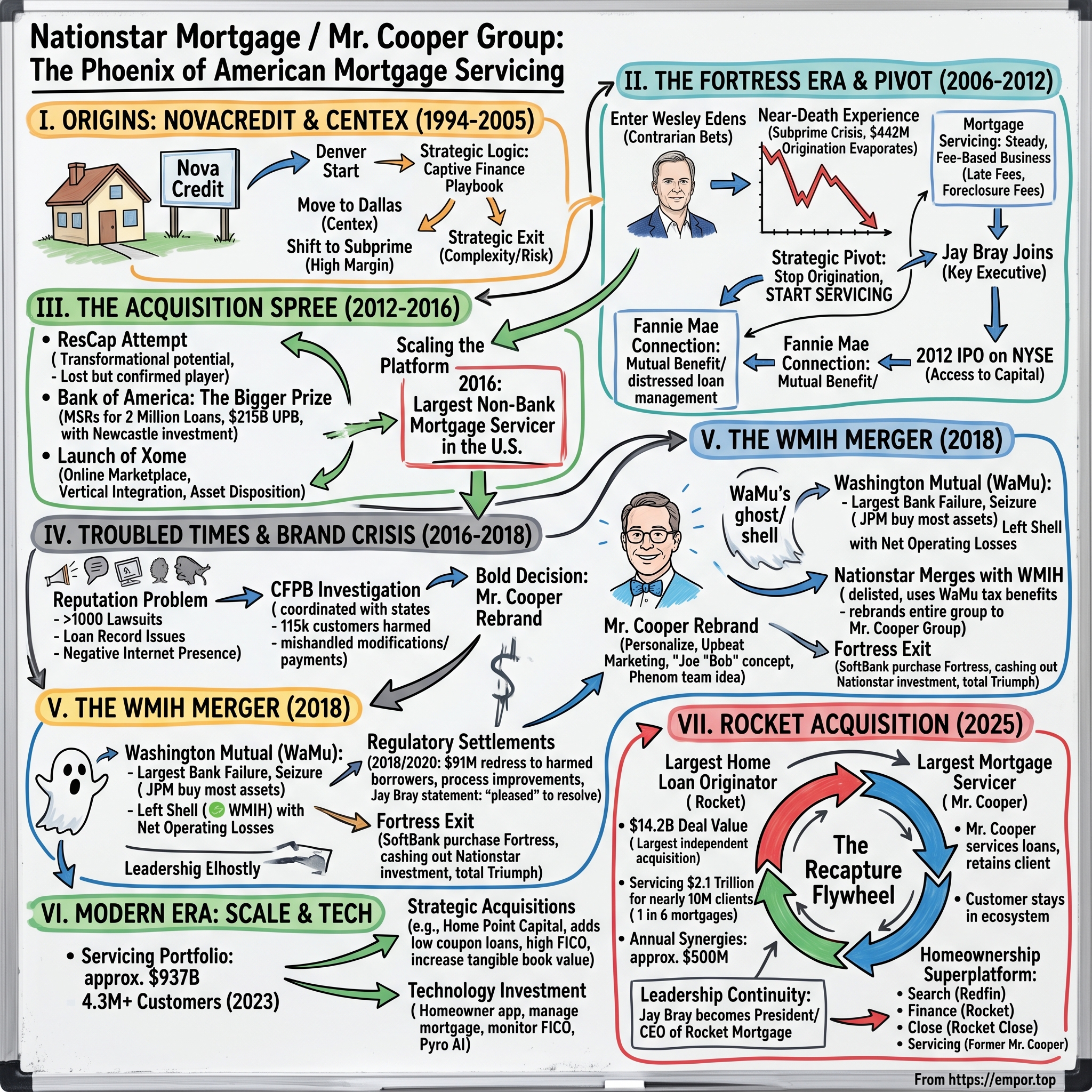

On the morning of October 1, 2025, in boardrooms across America's financial industry, executives watched as Rocket Companies, the Detroit-based homeownership platform, announced the completed acquisition of Mr. Cooper Group—bringing together the country's largest home loan originator and the largest mortgage servicer. This deal marked the largest independent mortgage acquisition in U.S. history.

The combined entity would service more than $2.1 trillion across nearly 10 million clients, representing one in every six mortgages in America. At the closing bell, Rocket Companies valued the deal at $14.2 billion—a staggering sum for a company whose story began three decades earlier as an obscure Denver credit operation that nearly collapsed in the subprime crisis.

How did a small home equity lender morph into America's dominant non-bank mortgage servicer? How did a company slapped with over a thousand customer lawsuits successfully rebrand itself with a cartoon mascot wearing a turquoise bowtie? And why did Rocket founder Dan Gilbert pay $14 billion for what was, at its core, an elaborate payment-processing machine?

Mr. Cooper Group Inc. became an American financial services company specializing in the non-bank servicing of residential mortgage loans, operating as the largest such servicer in the United States with a portfolio exceeding $1 trillion in unpaid principal balance and serving more than 6 million customers. But that clinical description masks one of the most improbable corporate reinvention stories in modern finance—a tale of private equity engineering, distressed asset arbitrage, regulatory warfare, and ultimately, industry consolidation.

This is the story of four reinventions: the subprime origins, the post-crisis pivot, the regulatory reckoning, and the ultimate combination with America's most aggressive mortgage originator. It's a story that reveals everything about how the American housing finance system actually works—and who profits from it.

Part I: Origins—From Nova Credit to Centex (1994–2005)

The Denver Beginning

Nationstar was founded in Denver, Colorado, in 1994 as Nova Credit Corporation. The company began life as a modest mortgage operation at a time when the U.S. housing finance system was undergoing a quiet revolution. Securitization was democratizing credit, and companies across the country were discovering they could originate loans, bundle them, and sell them to Wall Street—capturing fees at every step while offloading the actual risk.

In 1997, the company moved to Dallas, Texas, where home-builder Centex Homes established Nova Credit Corporation as their in-house lender for new construction and changed the company name to Centex Credit Corporation.

The strategic logic was elegant in its simplicity. Centex was one of America's largest homebuilders, constructing thousands of new homes annually across the country. Every home needed financing. By owning their own mortgage operation, Centex could capture the financing profit on each sale while also smoothing the purchase process for buyers—reducing friction and accelerating closings.

The Captive Finance Playbook

Captive finance subsidiaries were nothing new—automakers had pioneered the concept decades earlier. But in housing, the model offered particular advantages. A builder-owned lender could pre-qualify buyers, ensuring that groundbreaking didn't begin until financing was secured. It could also offer promotional rates and terms that independent lenders couldn't match, essentially subsidizing financing to move inventory.

In 2001, Centex Credit Corporation was merged into Centex Home Equity Company, and it operated as the subprime mortgage originator and servicer for Centex until 2005.

The shift into subprime was emblematic of the era. As the housing boom intensified through the early 2000s, the appetite for mortgage credit expanded beyond traditional borrowers. Subprime lending—extending mortgages to borrowers with damaged credit histories at higher interest rates—became a high-margin business that major financial institutions and homebuilders alike rushed to enter.

The Strategic Exit

By 2005, however, Centex's leadership was reading different signals. In 2005, the decision was made to withdraw Centex Homes from non-home-building businesses, including the mortgage business.

The decision proved prescient. Centex's management recognized that mortgage lending was becoming increasingly complex—regulatory burdens were growing, capital requirements were tightening, and the reputational risks of foreclosing on customers who had bought Centex homes created uncomfortable corporate conflicts. Better to sell the operation and focus on core competency: building houses.

Looking for buyers, Centex found a willing taker in one of Wall Street's most aggressive alternative asset managers—a firm that would transform the small Texas mortgage operation into something entirely different.

Part II: The Fortress Era—Private Equity Transformation (2006–2012)

Enter Wesley Edens

Fortress Investment Group LLC was founded in 1998 in New York City as a private equity firm by Wesley R. Edens, a former partner at BlackRock; Rob Kauffman, a managing director at UBS; Randal A. Nardone, also a managing director at UBS; Michael Novogratz, a former partner at Goldman Sachs; and Pete Briger, also a former partner at Goldman Sachs.

Edens' investment style was described in a 2007 Wall Street Journal article as one based on "contrarian bets, creative financing and a knack for building business from investments." He grew up on a rural ranch in Montana, the son of a psychologist father and schoolteacher mother, and earned his finance degree from Oregon State—hardly the pedigreed path of most Wall Street titans. But Edens had a gift for spotting undervalued, complex assets that others couldn't—or wouldn't—touch.

Fortress's investments grew rapidly, with its private equity funds netting 39.7% between 1999 and 2006. Fortress completed its initial public offering on February 8, 2007, with Goldman Sachs and Lehman Brothers underwriting the IPO. When Fortress launched on the NYSE on February 9, 2007, it was the first large private equity firm in the United States to be traded publicly.

The Nationstar Acquisition

Fortress Investment Group acquired Centex Home Equity and renamed it Nationstar Mortgage in 2006. The new corporate identity marked the completion of the sale of Centex Home Equity by Centex Corporation to an affiliate of Fortress Investment Group.

At the time of acquisition, "This name change signifies a new beginning for our company and represents our national scope of services," said Anthony H. Barone, President and CEO of Nationstar Mortgage. "Our Nationstar Mortgage brand is synonymous with our strengths and experience as a leading non-prime mortgage lender."

Nationstar Mortgage currently ranked as the eighth largest retail non-prime lender in the U.S. and was licensed to do business in 47 states. The company had 2,200 employees and a $10.5 billion loan portfolio.

Fortress's timing, however, proved catastrophic.

The Near-Death Experience

Fortress's timing on Nationstar proved awful. The ink was hardly dry on their Champion buyout when the easy money that financed the housing boom dried up. Within six months, Nationstar ceased writing new subprime business, which up until then accounted for the overwhelming majority of its revenue.

Its total losses for 2007 and 2008: $442 million.

The financial crisis wasn't just painful for Nationstar—it was nearly fatal. As the subprime market collapsed, the company's origination business evaporated. The rest of the Wall Street competition—companies including Lehman Brothers' Aurora Loan Services, Morgan Stanley's Saxon Mortgage, Goldman Sachs' Litton Loan Servicing, and Bear Stearns' EMC Mortgage—either backed away from their subprime units or failed.

Fortress itself was reeling. "[I] certainly did not distinguish myself from a performance standpoint as the market went straight down on the resi [residential] side," Edens said during the company's most recent earnings call.

The Strategic Pivot

What happened next would define Nationstar's future. Rather than writing down the investment and moving on, Edens and his partners doubled down—but on an entirely different strategy.

Though Nationstar's underwriting business was a wreck, it had a very sizable advantage in its owner: Even though Edens and his partners had already been burned once by Nationstar, they were willing to underwrite a bid at reinventing the operation.

The pivot was elegant: instead of originating mortgages—a business that had become toxic—Nationstar would service them. Mortgage servicing, the collection of monthly payments and management of escrow accounts, was a steady, fee-based business that actually benefited from distress. When borrowers fell behind, servicers collected late fees. When loans defaulted, servicers managed the foreclosure process—earning fees at every step.

Nationstar Mortgage went from private equity flop to a top servicer of troubled loans, thanks to deft management and a Fannie Mae partnership once hidden even from parts of the government.

The Fannie Mae Connection

The transformation required a crucial partner: Fannie Mae. Bray, who was Nationstar's chief financial officer at the time, said the company also benefited because the former Centex portfolio performed better than those of many other subprime lenders—a fact that caught the attention of Fannie Mae execs. "We continued to originate Fannie Mae product [after halting subprime], and then we started talking with them about how we can help ... on the servicing side," Bray said. Nationstar began inspecting Fannie's portfolios in the summer of 2008 and took on its first servicing work with the GSE later that year.

One other ingredient critical to Nationstar's meteoric rise is a deal it struck with Fannie Mae at the height of the mortgage servicing crisis. Under it, the taxpayer-backed entity agreed to feed Nationstar business on exclusive and favorable terms. In exchange, Nationstar granted Fannie veto power over decisions made by the unit handling its loans and a secret option to buy the division out.

The relationship was symbiotic. Fannie Mae was drowning in distressed loans and needed specialized servicers who could work with troubled borrowers. Major banks were retreating from the business, facing crushing regulatory scrutiny and reputational damage from foreclosing on homeowners. Nationstar offered a solution: specialized expertise in loss mitigation, without the bank-level regulatory spotlight.

Over the next four years, Nationstar outpaced its rivals in a growth spurt that has propelled it into the upper reaches of the servicing business with oversight of more than $200 billion in mortgages and a $3.2 billion market capitalization. Along the way, the Lewisville, Texas company has been lauded for its financial innovation, high-quality service and deep pockets of its majority owner—Fortress Investment Group.

Building the Management Team

The transformation wasn't accidental—it was orchestrated by executives who understood both mortgage finance and government-sponsored enterprise dynamics intimately.

That investment was already a success by the time Fortress acquired Centex Mortgage's subprime home equity division, a deal which brought Bray on board.

Jay Bray would prove indispensable. Jay Bray is a seasoned executive with nearly 25 years of experience in the mortgage servicing and originations industry. As the Chairman and Chief Executive Officer of Mr. Cooper Group, he has been instrumental in driving the company's strategic direction since 2012. Prior to this role, he served as Chief Financial Officer, showcasing his strong financial acumen.

Jay's career began at Arthur Andersen, where he honed his skills in auditing before moving on to leadership roles at Bank of America. His expertise includes asset-backed securitization and secondary market strategies. A Certified Public Accountant, Jay holds a B.A.A. in Accounting from Auburn University.

He served as the President of Nationstar Mortgage Holdings Inc. (formerly, Centex Home Equity) from October 7, 2011 to February 27, 2012 and served as its Chief Financial Officer until February 27, 2012. He managed the Asset Backed Securitization process for NationsCredit and EquiCredit originated products, at Bank of America and his responsibilities included developing and implementing a secondary execution strategy and profitability plan. Additionally, Mr. Bray led the portfolio acquisition (correspondent) pricing and modeling group, acquiring over $9 billion in non-conforming product in 1999—ranked No. 1 in sub-prime acquisition by B&C Lending magazine.

The IPO

In March 2012, Nationstar Mortgage Holdings, Inc. went public with an initial public offering on the New York Stock Exchange.

The timing couldn't have been better. Banks were desperate to shed mortgage servicing assets, and Nationstar had positioned itself as the buyer of choice. The IPO gave the company a public currency to fund acquisitions and provided Fortress a path toward liquidity after years of patient investment.

Jay Bray, Nationstar's chief executive, said his company is uniquely well positioned to maintain its rapid servicing expansion for years to come, and investors seem to agree: shares that have more than doubled since their March listing to a recent $33. Fortress is still in control with a 76% stake.

For investors studying the Nationstar story, the lesson was clear: in financial services, timing and positioning matter more than almost anything else. Fortress had bought a subprime originator at the worst possible moment, suffered massive losses, and then transformed the business into a servicing powerhouse at precisely the moment when distressed mortgage servicing became the hottest trade in housing finance.

Part III: The Acquisition Spree—Becoming a Giant (2012–2016)

The ResCap Deal: Transformational Acquisition

With the IPO complete and access to public equity markets secured, Nationstar embarked on one of the most aggressive acquisition campaigns in mortgage servicing history.

Lewisville, Texas-based Nationstar said in a separate announcement that it would acquire ResCap, with the purchase including $374 billion in mortgage servicing assets, $201 billion in primary residential mortgage servicing rights, and $173 billion in subservicing contracts.

The ResCap deal was transformational. ResCap, the mortgage unit of auto lender Ally Financial Inc, filed for bankruptcy in May in an effort to wipe out legal liabilities from mortgage-backed securities it sold during the housing boom.

Nationstar said that it anticipates adding more than 2.4 million customers from the transaction, as well as $550 billion in servicing and sub-servicing contracts, a move that it said would make it the largest non-bank residential mortgage originator and one of the largest originators in the nation.

"We believe this transaction will cement Nationstar's position as the nation's pre-eminent non-bank mortgage servicer, and it reflects a record of servicing performance that has made us a partner of choice in a transforming industry," said Nationstar CEO Jay Bray.

The Bidding War

The ResCap assets were too valuable to acquire without competition. Ocwen Financial Corp and Walter Investment Management Corp have teamed up to top Nationstar Mortgage Holdings Inc's starting bid for Residential Capital LLC's mortgage business. The consortium offered to buy the mortgage business for $40 million more than Nationstar's $2.45 billion opening bid.

Even Warren Buffett entered the fray. Warren Buffett's Berkshire Hathaway Inc has set the low bid for the loan package at $1.44 billion. Berkshire also argued in bankruptcy court for the right to be the opening bidder for the mortgage business, but failed to unseat Nationstar. It did get Nationstar, majority owned by Fortress Investment Group LLC, to increase the opening bid by $125 million.

Ocwen Financial Corp and Walter Investment Management Corp on Wednesday prevailed in a bankruptcy auction for Residential Capital LLC's mortgage business with a $3 billion bid that topped rival Nationstar Mortgage Holdings Inc. The deal, which needs bankruptcy court approval, is the latest example of non-bank financial companies expanding in the mortgage business in the wake of the financial crisis.

"Obviously we are disappointed in the outcome of the auction, but in the end our judgment was that the price of the assets would not represent a compelling investment opportunity for us," Nationstar Chief Executive Jay Bray said in a statement.

Though Nationstar lost the ResCap auction, the company had demonstrated something important: it was a serious player in the mortgage servicing consolidation game, with the financial backing and operational capability to compete for the largest transactions.

Bank of America: The Bigger Prize

What Nationstar lost in ResCap, it more than made up for with Bank of America.

In addition to the MSRs, Nationstar will also be acquiring approximately $5.8 billion in related servicing advance receivables as the associated portfolios are boarded during 2013.

As part of the settlement, BofA agreed to sell servicing rights on two million home loans—many of which are securitized by Fannie Mae—with an unpaid principal balance of $306 billion. Nationstar Mortgage Holdings confirmed it will buy $215 billion in unpaid principal balance from the BofA MSR pool for $1.3 billion.

Nationstar announced that it has closed the purchase of mortgage servicing rights ("MSR") with an approximate $97 billion unpaid principal balance ("UPB"), based on December 31, 2012 closing balances and certain other assets from Bank of America. The transaction was completed pursuant to the previously announced MSR purchase and sale agreement, dated January 6, 2013. This servicing portfolio consists of rights to service loans that are owned, insured or guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae.

Nationstar is one of the largest servicers in the United States, with a servicing portfolio of over 1.8 million residential mortgages in excess of $300 billion in unpaid principal balance as of February 1, 2013. Nationstar's integrated loan origination business mitigates servicing portfolio run-off and improves credit performance for loan investors.

Why Banks Were Selling

The exodus of banks from mortgage servicing wasn't voluntary—it was driven by post-crisis regulatory changes that made servicing expensive and risky for traditional financial institutions.

Basel III capital requirements treated mortgage servicing rights as risky assets, forcing banks to hold significant capital against them. The Consumer Financial Protection Bureau, created by the Dodd-Frank Act, scrutinized servicer practices with unprecedented intensity. And foreclosing on homeowners—even when legally justified—generated negative headlines that bank marketing departments despised.

Non-bank servicers like Nationstar faced lighter regulatory oversight and no capital requirements. They could operate with higher leverage and lower overhead. And crucially, they didn't have to worry about cross-selling checking accounts or credit cards to the same customers whose homes they might need to foreclose.

The year had barely started when Nationstar and Bank of America announced a $1.3 billion deal involving $215 billion worth of MSRs. Nationstar entered the agreement with backing from Newcastle Investment Corp.; according to a release published at the time, each company retained one-third interest in the MSRs, with Nationstar servicing all the loans. The deal brought Nationstar's customer base up to 1.5 million, and its servicing portfolio grew to an estimated $425 billion.

The Launch of Xome

Following the aggressive servicing acquisitions, Nationstar moved to vertically integrate. Following its IPO, Nationstar Mortgage launched Xome, an online real estate marketplace.

Xome is a leading online real estate marketplace. The company provides mortgage servicers end-to-end asset marketing and disposition strategies, recapture solutions and real estate and data services and enables consumers and investors to buy and sell properties online with a best-in-class auction platform.

The Xome strategy reflected Nationstar's understanding that distressed servicing wasn't just about collecting payments—it was about managing the entire lifecycle of troubled loans, including the eventual sale of foreclosed properties. By owning the real estate auction platform, Nationstar could capture additional fees when properties sold while providing a turnkey solution to investors.

Rising to the Top

By 2016, Nationstar had become the largest non-bank mortgage servicer in the United States.

The transformation was remarkable. In less than a decade, a failed subprime lender had become the dominant player in an entirely different business. The company had grown through a combination of organic expansion and aggressive acquisition, funded by Fortress's deep pockets and creative financial engineering.

But success brought scrutiny, and Nationstar's rapid growth had outpaced its operational capabilities in ways that would soon become painfully apparent.

Part IV: Troubled Times—Regulatory Battles & Brand Crisis (2016–2018)

The Reputation Problem

This tale begins with a company called Nationstar Mortgage. Based in Coppell, Nationstar had a reputation—not a good one. The company was slapped with more than a thousand lawsuits, many from furious customers who claimed their homes were wrongly foreclosed. Nationstar's name became synonymous with mortgage nightmares. It was all over the Internet, and for all the wrong reasons.

The complaints followed a pattern. When Nationstar acquired servicing rights from other institutions, loan records didn't always transfer cleanly. Borrowers who had negotiated loan modifications with their previous servicer found that Nationstar didn't honor the agreements. Payments were misapplied. Escrow accounts were mismanaged. And worst of all, some homeowners found themselves foreclosed upon despite making every payment on time.

The CFPB Investigation

The Consumer Financial Protection Bureau (Bureau) filed a complaint and proposed stipulated judgment and order against Nationstar Mortgage, LLC, which does business as Mr. Cooper (Nationstar). The Bureau's action is part of a coordinated effort between the Bureau, a multistate group of state attorneys general, and state bank regulators. The Bureau alleges that Nationstar violated multiple Federal consumer financial laws, causing substantial harm to the borrowers whose mortgage loans it serviced, including distressed homeowners. Nationstar is one of the nation's largest mortgage servicers and the largest non-bank mortgage servicer in the United States.

Specifically, the CFPB alleged that between Jan. 2012 and Jan. 1, 2016, Nationstar: Failed to identify loans on its systems that had pending loss-mitigation applications or trial-modification plans, and as a result failed to honor borrowers' loan modification agreements.

Mr. Cooper, the nation's largest nonbank servicer of mortgage loans, will refund customers nearly $90 million and pay a civil penalty of more than $6.5 million to settle a lawsuit claiming it violated the rights of over 115,000 customers, some of whom it had illegally foreclosed on. When Mr. Cooper—then known as Nationstar—bought thousands of mortgages through MSR bulk purchases, it frequently failed to identify loans with existing modifications, according to the lawsuit. Those modifications allowed the borrower to make trial payments, which would then require the servicer to permanently modify the loans. But Mr. Cooper often didn't take those mods into account, and then foreclosed on thousands of those borrowers.

The Mr. Cooper Rebrand

Facing a reputational crisis, Nationstar's leadership made a bold decision: a complete corporate rebrand.

In August 2017, Nationstar Mortgages, LLC, announced it was changing its name to Mr. Cooper after releasing its worst financial report to date. The company stated that the name change was meant to "personalize the mortgage experience."

In 2017, after the company released its worst financial report ever, it announced that it would go by the name of Mr. Cooper. The thinking at the time was that you had a friend in Mr. Cooper. He'll take good care of you. That was opposite of what happened to some customers, many of whom believed Mr. Cooper was real.

The cartoonish Mr. Cooper cuts a quirky figure with his headphones, wide-rimmed glasses and turquoise-colored bowtie.

According to Bray, the company is doing more than rebranding, it's actually reimagining how it operates, which meant the transition would take longer than first thought. Back in December, Bray told HousingWire that the company planned to officially transition to Mr. Cooper in the first half of 2017, but earlier this year, the company set the official date of August 2017. As it turns out, Aug. 21, 2017 is D-Day, or Mr. Cooper-Day, as it were.

You spent about $5 million on your rebranding project, and out of that came the idea of this bowtie-wearing avatar representing the Mr. Cooper concept. He would symbolize the new version of Nationstar, the one that cared about people and offered "a more personalized experience."

And the Phenomenon team came up with the idea of referring to every person within the business as another Mr. Cooper. It was quite extensive, which is understandable considering how most Americans still view mortgage providers nearly a decade after the last housing crisis.

There's a peppy video full of upbeat marketing copy that personifies "Mr. Cooper" as a champion of mortgagors who "believes in the solution" and "hates the status quo." Christen Reyenga, Nationstar's AVP of corporate communications, told RMD in a phone interview that the company settled on a personal rebrand after focus groups revealed that the happiest borrowers had latched onto a one-on-one connection at their mortgage firms. "When someone had a positive experience with their mortgage servicer, it was always a person who made it a great experience—it was Joe, it was Bob," Reyenga said.

The Regulatory Settlements

In 2018, Mr. Cooper paid out millions of dollars in settlements in New York and California due to various violations of state banking laws.

In 2020, Mr. Cooper agreed to a $91 million settlement with the CFPB, all 50 states, and three U.S. territories, for mishandling foreclosures and borrowers' payments.

The proposed judgment and order, if entered by the court, would require Nationstar to pay approximately $73 million in redress to more than 40,000 harmed borrowers. It would also require Nationstar to pay a $1.5 million civil penalty to the Bureau.

In a statement following the news of the settlement, Mr. Cooper's Chairman and CEO Jay Bray said the company was "pleased" to resolve the matter. "When these issues were identified several years ago, we immediately made restitution to our impacted customers and invested in process improvements to prevent reoccurrence," he said. "Since then, we have continued to invest in technology, people, and leadership to ensure that our compliance and risk management programs not only meet our regulators' expectations but also support sustainable growth."

The settlements represented a significant cost, but they also drew a line under years of regulatory uncertainty. For investors, the resolution—while expensive—removed a major overhang and allowed the market to focus on Mr. Cooper's fundamental business rather than its legal exposure.

Part V: The WMIH Merger—Washington Mutual's Ghost (2018)

The Unlikely Corporate Parent

The 2018 corporate restructuring that created Mr. Cooper Group involved one of the strangest merger partners in financial history: the corporate shell of Washington Mutual—the largest bank failure in American history.

The seizure of WaMu Bank resulted in the largest bank failure in American financial history, dwarfing the failure of Continental Illinois in 1984. On September 26, 2008, Washington Mutual, Inc. and its remaining subsidiary, WMI Investment Corp., filed for Chapter 11 bankruptcy.

WMI Holdings Corporation was incorporated as the Washington National Building Loan and Investment Association on September 25, 1889, after the Great Seattle Fire destroyed 120 acres of the central business district of Seattle. The newly formed company made its first home mortgage loan on the West Coast on February 10, 1890.

Before the receivership action, it was the sixth-largest bank in the United States. According to WaMu's 2007 SEC filing, the holding company held assets valued at $327.9 billion.

From that date through September 24, 2008, WaMu experienced a bank run whereby customers withdrew $16.7 billion in deposits over those nine days, and in excess of $22 billion in cash outflow since July 2008, both conditions which ultimately led the Office of Thrift Supervision to close the bank. The FDIC then sold most of the bank's assets to JPMorgan Chase for $1.9 billion in cash plus assumption of all secured debt.

The Shell Company

On September 26, 2008, WaMu, Inc., and its remaining subsidiary, WMI Investment Corp., filed for Chapter 11 bankruptcy and after seven plans to reorganize the company finally emerged from Chapter 11 bankruptcy the following month as WMI Holdings Corporation.

In 2012, WMIH emerged from bankruptcy as the successor to Washington Mutual, and is currently the direct parent of WM Mortgage Reinsurance. According to WMIH's website, the company had limited operations since it emerged from bankruptcy. During that time, WMIH mainly oversaw WM Mortgage Reinsurance's legacy business, which has not written any new business since September 2008, and is currently operating in runoff mode.

What remained of Washington Mutual was essentially a corporate shell with tax attributes—specifically, significant net operating losses that could shelter future income from taxation. For a profitable company like Nationstar, merging with WMIH offered substantial tax benefits.

The Deal Structure

In 2018 Nationstar and WMI Holdings Corporation (WMIH), the corporate successor to the defunct Washington Mutual, merged. As a result Nationstar was delisted from the New York Stock Exchange and WMIH changed its name to Mr. Cooper Group.

WMIH Corp. and Nationstar Mortgage Holdings Inc. today announced that the stockholders of both companies approved all proposals relating to the merger of WMIH and Nationstar. Under the Agreement and Plan of Merger, dated February 12, 2018, by and among Nationstar, WMIH Corp. and Wand Merger Corporation, Wand Merger Corporation will merge with and into Nationstar, resulting in Nationstar becoming a wholly-owned subsidiary of WMIH.

The company that holds Washington Mutual's legacy business can move ahead with its plan to buy a controlling interest in Nationstar Mortgage now that both companies' shareholders have approved the deal. Holders of approximately 80% of the shares of WMIH that were entitled to vote approved the proposal and more than 90% of holders of outstanding shares of Nationstar entitled to vote were in favor of the transaction.

The Fortress Exit

As previously disclosed, FIF HE Holdings LLC ("Fortress") agreed to make an election to receive Cash Consideration with respect to no less than 50% of its shares of Nationstar common stock. Fortress elected to receive Cash Consideration for 68,104,736 shares of Nationstar common stock, which constitutes 100% of the shares held by Fortress. It is expected that Fortress will own approximately 5.1% of the shares of common stock of WMIH after applying proration.

On February 14, 2017, SoftBank Group agreed that it would buy Fortress Investment Group LLC for $3.3 billion. The SoftBank acquisition was completed in the last week of December, with Fortress being delisted from the New York Stock Exchange.

For Fortress, the WMIH merger represented the final chapter of a twelve-year investment that had begun as a disaster and ended as a triumph. The firm cashed out at $18 per share for a company it had nearly lost entirely during the financial crisis.

As one of the largest mortgage servicers in the country, operating under its Mr. Cooper® brand, the company is uniquely positioned for growth in a highly addressable and extremely healthy housing market. "We are pleased to complete this merger and begin our next phase of growth as an even stronger company, well-positioned to capitalize on the trends in the housing market and build on our leadership in the industry," said Jay Bray, Chairman and Chief Executive Officer of the combined company.

Part VI: The Modern Era—Scale & Technology (2018–2025)

Building the Dominant Platform

With the regulatory settlements behind it and a new corporate structure in place, Mr. Cooper resumed its growth trajectory.

As of 2023, it was one of the largest mortgage servicers in the United States with a servicing portfolio of approximately $937 billion and more than 4.3 million customers.

In 2020, Mr. Cooper originated over 146,000 mortgages with a total value of over $36 billion.

Strategic Acquisitions Continue

Dallas, Texas-based Mr. Cooper Group has entered into an agreement to acquire struggling Home Point Capital for $324 million in cash, the companies announced on Wednesday. The transaction will ultimately result in the seller shutting down operations.

Mr. Cooper's Chairman and CEO Jay Bray commented, "This acquisition is consistent with our strategy of growing our customer base, deploying our capital with a focus on attractive risk-adjusted returns, and maintaining a very strong balance sheet. Home Point has amassed an impressive servicing portfolio, consisting of conventional loans to borrowers with high FICO scores, low coupons, and strong equity cushions."

In total, Mr. Cooper is acquiring Home Point's $84 billion servicing portfolio, which will contribute to Mr. Cooper's return on equity with an estimated 10% increase to operating earnings in the first year. Mr. Cooper also estimates a tangible book value increase of about $1 per share at closing.

The acquisition involves the company acquiring Home Point's outstanding shares, as well as an $84 billion portfolio of mortgage servicing rights and assuming $500 million in senior notes. "This acquisition adds scale to our platform, bringing us closer to our $1 trillion strategic target, while enhancing returns due to attractive yields and positive operating leverage," Jay Bray, CEO and chairman of Mr. Cooper, said.

Technology Investment

Mr. Cooper invested heavily in technology platforms designed to improve the customer experience while reducing operational costs.

Along with its massive servicing portfolio, Mr. Cooper Group has a homeowner mobile app with more than 500,000 downloads that allows users to manage their mortgage, monitor their FICO score, view home value and equity, and explore refinance options, all from their mobile device, which has helped the company stake a permanent residency in their customers' lives.

Leadership Continuity

Through all the corporate transformations—from Nationstar to Mr. Cooper, through the WMIH merger and beyond—Jay Bray remained at the helm. Mr. Jay Bray has been Chief Executive Officer of Nationstar Mortgage Holdings Inc. since 2012.

Jay Bray is currently 57 years old and serves as the Chief Executive Officer at Mr. Cooper Group Inc. He assumed his role on 07-31-2018, marking the start of his leadership at the company. With extensive experience in the mortgage and financial services industry, he has held several key positions at the company, including a term as President.

The leadership continuity was unusual in an industry marked by executive turnover and spoke to Bray's ability to navigate the company through repeated transformations while maintaining operational execution.

Part VII: The Rocket Acquisition—Industry Consolidation (2025)

The $14 Billion Deal

Rocket Companies, the Detroit-based fintech platform including mortgage, real estate, title and personal finance businesses, announced a definitive agreement to acquire Mr. Cooper Group Inc. in an all-stock transaction for $9.4 billion in equity value, based on an 11.0x exchange ratio.

Under the terms of the agreement, Mr. Cooper shareholders will receive a fixed exchange ratio of 11.0 Rocket shares for each share of Mr. Cooper common stock. This represents a $143.33 per share value based on the closing price as of March 28, 2025, and a premium of 35% over the volume weighted average price (VWAP) of Mr. Cooper.

Rocket Companies, the Detroit-based homeownership platform, announced the completed acquisition of Mr. Cooper Group—bringing together the country's largest home loan originator and the largest mortgage servicer.

Rocket Companies said Wednesday it has completed a mega-deal valued at $14.2 billion to acquire mortgage servicer Mr. Cooper Group.

Strategic Rationale

Combined company to service more than $2.1 trillion in loan volume. Integrating Rocket's originations-servicing recapture flywheel with Mr. Cooper's servicing platform will drive down costs and improve the experience for the companies' nearly 10 million combined clients, representing one in every six mortgages. Transaction is expected to generate annual run-rate revenue and cost synergies of approximately $500 million.

As a result of the acquisition, the combined company is expected to serve nearly 10 million clients, managing a $2.1 trillion unpaid principal balance, which represents roughly one in every six mortgages across the country. The combination unites Mr. Cooper's servicing operations with Rocket's scale in mortgage origination and its growing real estate and technology platform. Together, the companies will create a comprehensive homeownership ecosystem spanning mortgage origination, servicing, real estate search, title and closing.

"Jay Bray and his team have built a technology-driven platform that is the backbone of Mr. Cooper, helping it scale to become the largest servicer in the country. By integrating Mr. Cooper's servicing strength with Rocket's origination capabilities and AI technology and established strong national brand, our goal is to lower costs and make the process easier."

The Recapture Flywheel

The strategic logic centered on recapture—the ability to refinance existing servicing customers into new loans rather than losing them to competitors.

When interest rates fall, mortgage borrowers refinance. Traditional servicers lose the customer when this happens—the new lender captures the servicing rights. But if the servicer is also an originator, they can refinance the customer themselves, maintaining the relationship and capturing origination fees.

Rocket was America's largest mortgage originator but had limited servicing. Mr. Cooper was America's largest servicer but had modest origination capacity. Combined, the companies could create a flywheel where servicing customers became origination customers, who became servicing customers again—an endless loop of fee capture.

Leadership Continuity

Upon closing of the transaction, it is expected that Mr. Cooper Group's Chairman and CEO Jay Bray will become President and CEO of Rocket Mortgage, reporting to Krishna. Dan Gilbert will remain Chairman of Rocket Companies.

"This transaction brings to a close a multi-year journey during which Mr. Cooper grew to become the nation's largest servicer and produced enormous value for our clients, partners, stakeholders and investors," Bray said. "Now, by joining forces with Rocket, we start a new journey, which I believe offers an even bigger opportunity. Through the power of our platform and our people, we will create a more personalized experience that makes owning a home more attainable and easier to navigate. Together, we will deliver the change the housing industry needs."

As part of the acquisition, Mr. Cooper and all of its servicing functions will be rebranded under the Rocket umbrella.

Part VIII: Business Model Deep Dive

What Is Mortgage Servicing?

Finding a home and financing the purchase with a mortgage loan are only the beginning of the homeownership journey. Once the loan closes, the next step is mortgage servicing where servicers manage the borrower's monthly mortgage payments, annual taxes and insurance premiums.

Mortgage servicing occurs after the loan closes and funding is completed. It is the process of collecting monthly loan payments and managing the borrower's annual taxes and insurance premiums using their escrow accounts. Some lenders service the mortgage after closing, but typically the mortgage servicing rights (MSR) are sold to another company.

Revenue Streams

Mortgage servicers generate revenue through multiple streams:

Servicing Fees: The primary revenue source, typically 0.25% to 0.50% of the unpaid principal balance annually, paid by the loan owner (investor, GSE, or bank) to the servicer.

Float Income: Servicers hold borrower payments temporarily before remitting to investors, earning interest on the float. They also hold escrow funds for taxes and insurance, generating additional float income.

Ancillary Fees: Late fees, default-related fees, modification fees, and other charges assessed during the servicing relationship.

Recapture: When servicers also originate loans, they can capture refinancing business from their own servicing portfolio, earning origination fees while retaining servicing.

The Economics of Scale

Mortgage servicing is a scale business, meaning the economics of scale can be achieved with larger servicing portfolio by spreading the fixed costs among more loans being serviced.

Over the years there has been a huge consolidation of servicing because it is such an economy of scale business. The more loans you can service through the pipeline, the more efficient the operation.

The fixed costs of servicing—technology platforms, compliance infrastructure, call centers—don't scale linearly with portfolio size. A servicer managing 5 million loans doesn't need ten times the infrastructure of one managing 500,000. This creates powerful economies of scale that favor consolidation.

Interest Rate Sensitivity

This period was a windfall for servicers. Rising rates typically slow down borrower prepayments, increase the fair value of mortgage servicing rights (MSRs), and enable companies to earn more interest on funds held in escrow accounts.

From an MSR valuation standpoint, prepayments and delinquencies make it a tricky business. MSR valuations have huge implications for liquidity risk. They become sizable assets on the balance sheet and can be a major source of collateral for nonbank financing.

MSR values are inversely correlated with interest rates. When rates fall, borrowers refinance, prepaying their mortgages and terminating the servicer's fee stream. When rates rise, prepayments slow, and MSR values increase. This creates natural hedge characteristics for mortgage originators, whose business declines when rates rise.

Service Offerings

Mr. Cooper's platform encompasses three primary business lines:

Servicing: Processing payments, handling escrow accounts, and managing the day-to-day administration of mortgage loans for institutional investors and GSEs.

Origination: Direct-to-consumer and correspondent lending, allowing the company to refresh its servicing portfolio and capture customers throughout the homeownership lifecycle.

Xome: A leading online real estate marketplace providing mortgage servicers end-to-end asset marketing and disposition strategies, recapture solutions and real estate and data services.

Part IX: Investment Considerations

Myth vs. Reality

| Myth | Reality |

|---|---|

| Mortgage servicing is a boring, low-margin business | Servicing generates 40-50% EBITDA margins at scale with significant float income |

| Non-bank servicers are riskier than bank servicers | Non-banks face lighter capital requirements but greater liquidity risk during stress |

| The Mr. Cooper rebrand was just marketing | The brand transformation accompanied significant operational improvements and technology investment |

| Rocket overpaid for Mr. Cooper | The strategic value of combining origination and servicing creates revenue synergies unavailable to either standalone |

Competitive Landscape: Porter's Five Forces

Threat of New Entrants: LOW - High barriers from regulatory complexity and technology requirements - Scale economies favor incumbents - MSR acquisitions require significant capital

Bargaining Power of Suppliers: MODERATE - Loan sellers (banks, originators) have multiple buyers for MSRs - However, few buyers have capacity for large portfolios

Bargaining Power of Buyers: LOW - Borrowers cannot choose their servicer - Institutional investors value execution and compliance

Threat of Substitutes: LOW - No substitute for mortgage servicing exists - Technology could automate some functions but core service unchanged

Industry Rivalry: MODERATE-HIGH - Competition for MSR acquisitions intense - Pricing pressure on servicing fees from large investors - Technology investment race ongoing

Helmer's 7 Powers Analysis

Scale Economies: STRONG - Fixed costs spread across larger loan base - Technology platform advantages compound with scale

Network Effects: WEAK - No direct network effects in servicing - Modest network effects through Xome real estate platform

Counter-Positioning: PRESENT - Non-bank model allows lighter capital structure than banks - Banks cannot easily replicate non-bank cost structure

Switching Costs: HIGH - Borrowers cannot switch servicers - Institutional clients face high costs from servicer transitions

Cornered Resource: MODERATE - Regulatory relationships and GSE approvals valuable - Experienced management team difficult to replicate

Process Power: PRESENT - Operational excellence in loan boarding and loss mitigation - Technology platform investment creates process advantages

Brand: WEAK - Mr. Cooper brand awareness improved but limited brand power - Borrowers don't choose servicers based on brand

Key Performance Indicators

For investors tracking Mr. Cooper (now Rocket) performance, three KPIs matter most:

-

Servicing Portfolio Growth (UPB): The total unpaid principal balance of serviced loans drives revenue. Portfolio growth through acquisitions and retention indicates market position and scale advantages.

-

Recapture Rate: The percentage of refinancing customers retained within the origination platform. Higher recapture rates demonstrate the value of integrated servicing-origination model and drive origination volume during rate decline cycles.

-

Cost Per Loan: Operating expenses divided by total loans serviced. This metric captures the realization of scale economies and operational efficiency improvements that drive margin expansion.

Regulatory and Accounting Considerations

Material Regulatory Risks: - CFPB oversight remains intense for non-bank servicers - State-level licensing requirements create compliance burden - FHFA market share caps could limit future acquisitions

Accounting Judgments: - MSR valuation requires significant management estimates - Prepayment speed assumptions materially impact MSR fair value - Delinquency and default reserves involve judgment about credit performance

Bull Case Summary

The combined Rocket-Mr. Cooper entity creates a vertically integrated homeownership platform with unmatched scale. The servicing-origination flywheel generates sustainable competitive advantage through customer recapture. Technology investments and AI capabilities position the company for digital transformation of mortgage services. Rising interest rates support MSR values and servicing economics.

Bear Case Summary

Integration risk from combining two large, complex organizations could disrupt operations. Regulatory scrutiny of dominant market position may intensify. Interest rate volatility creates MSR valuation swings that complicate earnings predictability. Non-bank liquidity risk remains during market stress periods. Historical customer service issues could resurface at scale.

Conclusion: The Phoenix Complete

From its founding as Nova Credit in Denver in 1994, through its near-death experience in the financial crisis, to its emergence as America's dominant mortgage servicer and ultimate acquisition by Rocket Companies, the company now known as Mr. Cooper represents one of the most remarkable corporate transformation stories in American financial services.

The narrative arc follows a classic phoenix pattern: origins in one business model (subprime origination), destruction of that model, rebirth in an entirely different business (servicing), growth through aggressive acquisition, crisis and rebranding, and ultimate consolidation into a larger entity.

What makes the story particularly instructive is how it illuminates the hidden machinery of American housing finance. Most homeowners never think about mortgage servicing—they simply make payments to whoever bought their loan. But that anonymous payment processor represents a massive, profitable industry that has consolidated dramatically since the financial crisis.

Jay Bray, then CEO of Mr. Cooper, stated that, "This transaction brings to a close a multi-year journey during which Mr. Cooper grew to become the nation's largest servicer and produced enormous value for our clients, partners, stakeholders and investors." Bray further added, "Now, by joining forces with Rocket, we start a new journey, which I believe offers an even bigger opportunity."

The Mr. Cooper story is ultimately a story about the power of scale, the value of patient capital, and the remarkable ability of well-managed companies to reinvent themselves when their original business model fails. Whether the Rocket combination delivers on its promised synergies remains to be seen, but the journey from Denver startup to $14 billion acquisition provides a masterclass in corporate adaptation and transformation.

Part X: The Broader Industry Context

The Great Migration from Banks to Non-Banks

The rise of Mr. Cooper from distressed subprime lender to industry champion reflects a fundamental restructuring of American mortgage finance that accelerated after the 2008 financial crisis. The transformation in mortgage market structure has been dramatic. Non-bank mortgage companies emerged as the dominant force in home lending, increasing their market share from 44.6% in 2018 to a peak of 60.8% in 2021 before settling at 53.3% in 2024. Non-bank mortgage companies now originate 53.3% of all home loans, while bank market shares have fallen from 42.5% to 30.1%.

Banks significantly reduced their involvement in the mortgage market after the financial crisis, due to regulatory and market changes. Nonbank mortgage companies stepped in to serve consumers. They now service 68% of federal-guaranteed mortgage loans and 53% of all mortgage loans outstanding.

Nonbanks have increased their market share of government-guaranteed mortgages from 13% in 2009 to 90% today, becoming a significant source of mortgage credit for first-time homebuyers, low- and moderate-income consumers, veterans, and communities of color.

Regulatory Evolution

The regulatory framework for non-bank servicers evolved significantly as their market share grew. In 2021, the CSBS Board of Directors approved for state adoption Nonbank Mortgage Servicer Prudential Standards, establishing new capital, liquidity, and corporate governance requirements for nonbank mortgage servicers. Nonbank mortgage servicers licensed in at least one state that has adopted the model prudential standards collectively service 99% of the nonbank mortgage market by loan count.

The tangible shareholders' equity of the top 50 nonbank servicers has increased 155% since 2019. The unrestricted cash of the top 50 nonbank forward mortgage servicers has increased 221% since 2019 and 11% in the past year.

Despite these improvements, concerns remained. A recent report from the Financial Stability Oversight Council (FSOC) highlighted vulnerabilities at nonbank mortgage servicers, warning that these could pose risks to financial stability. The FSOC recommended increased regulation and measures to bolster these companies' liquidity during periods of stress. Additionally, Ginnie Mae's new risk-based capital requirement—effective December 31, 2024—poses a significant challenge for nonbanks.

The Competitive Landscape in 2025

Non-bank financial institutions make up 17 of the top 25 mortgage lenders in the U.S., highlighting their growing influence. United Wholesale Mortgage is the largest U.S. mortgage lender, originating 366,078 mortgages worth $139.7 billion in 2024.

United Wholesale Mortgage, Rocket Mortgage, and CrossCountry Mortgage are the three largest mortgage lenders in the United States by loan originations—and they're all non-bank lenders.

Analysts called Mr. Cooper a servicing "powerhouse," after it acquired Home Point Capital's $84 billion servicing portfolio in May 2023 and Flagstar's $356 billion book in July 2024. As of June 30, 2024, Mr. Cooper had become the largest U.S. primary servicer—those companies with direct consumer interactions, regardless of who owns the servicing rights—with a $1.2 trillion unpaid principal balance.

Part XI: Lessons from the Phoenix

The Private Equity Playbook

The Nationstar/Mr. Cooper story offers a master class in private equity value creation—though not through the conventional playbook. Fortress didn't create value through cost-cutting or financial engineering alone. Instead, the firm demonstrated patience during a near-catastrophic period, pivoted the business model entirely, and then executed an aggressive acquisition strategy when competitors retreated.

The timeline is instructive:

| Year | Event | Lesson |

|---|---|---|

| 2006 | Fortress acquires Centex Home Equity | Entry timing was terrible |

| 2007-2008 | Subprime collapse nearly destroys company | Near-total loss |

| 2008-2011 | Pivot from origination to servicing | Business model flexibility |

| 2012 | IPO creates acquisition currency | Capital markets access |

| 2012-2016 | Aggressive portfolio acquisitions | Scale advantages in servicing |

| 2018 | WMIH merger provides exit | Creative exit structuring |

For Fortress, the Nationstar investment delivered returns despite—not because of—the original investment thesis. The firm entered subprime lending just as the market collapsed. Had Fortress simply written off the investment and moved on, the outcome would have been catastrophic. Instead, the firm's willingness to provide additional capital and support management's strategic pivot transformed disaster into success.

The Importance of Regulatory Arbitrage

Nationstar's rise illustrates how regulatory arbitrage can create competitive advantage. Non-bank servicers operate under different regulatory frameworks than depositories, with different capital requirements, liquidity standards, and supervisory regimes. This created cost structure advantages that allowed Nationstar to acquire servicing portfolios that banks were eager to shed.

The regulatory arbitrage was not permanent, however. As non-bank servicers grew larger and more systemically important, regulatory attention increased. The CFPB settlements, state regulatory actions, and ongoing FSOC scrutiny demonstrated that regulatory advantages erode as scale increases.

Brand Transformation in Financial Services

The Mr. Cooper rebrand offers lessons—both positive and cautionary—for financial services companies considering similar transformations.

The positive lesson: radical brand change is possible. A company associated with foreclosure nightmares successfully repositioned itself as a friendly, approachable servicer. Customer satisfaction scores improved. Regulatory scrutiny, while remaining intense, became manageable.

The cautionary lesson: brand transformation cannot substitute for operational improvement. The Mr. Cooper rebrand succeeded because it accompanied genuine improvements in customer service, technology platforms, and compliance processes. A brand change without underlying operational change would likely have backfired.

The Value of Management Continuity

Jay Bray's tenure as CEO spans from 2012 through the Rocket acquisition—a remarkable run of continuity in an industry marked by executive turnover. His leadership through the post-crisis pivot, the acquisition spree, the regulatory battles, and ultimately the sale to Rocket demonstrates the value of consistent strategic vision.

Bray's background—accounting degree, CPA license, experience at Arthur Andersen and Bank of America—provided the financial acumen necessary to navigate the complex economics of mortgage servicing. His willingness to make bold strategic moves, including the controversial rebrand, demonstrated that operational expertise alone isn't sufficient for transformational leadership.

Part XII: The Combined Entity—Rocket and Mr. Cooper

Creating the Homeownership SuperplatformThe completed acquisition represents the largest independent mortgage deal in U.S. history, creating a new dominant player that combines origination, servicing, and real estate search under one brand.

Together with Mr. Cooper, Rocket's capabilities span the entirety of homeownership—home search, financing, title, closing and servicing. These acquisitions allow Rocket to build on its $500 million investment in data and AI technology.

The Technology and Data Advantage

The acquisition enhances Rocket's data capabilities, adding nearly 7 million new clients and 150 million annual customer interactions. This expanded dataset will improve automation, personalization and overall operational efficiency.

Moreover, the combined companies will benefit from a more balanced business model, allowing them to generate stable earnings across various interest rate environments.

Competitive Response

The industry has already begun to respond. UWM has responded to Rocket's plans to acquire Mr. Cooper by pulling its own loan servicing from the company and signing a long-term agreement with ICE Mortgage Technology to bring servicing in-house.

If Rocket can capture 20 percent of next year's projected $715 billion refi market, that would amount to $143 billion in refinancing business—41 percent more than the company's $101.2 billion in total 2024 loan production.

The Redfin Connection

Rocket also recently closed its acquisition of Redfin in July. Together with Mr. Cooper, Rocket's capabilities span the entirety of homeownership—home search, financing, title, closing and servicing.

Rocket is hoping its acquisition of Redfin, which closed July 1, will boost its share of the purchase loan business. Rocket now offers preferred pricing for borrowers involved in deals where the buyer or seller is represented by a Redfin agent, and is seeing "some awesome early data" from integration of the companies' operations.

Brand Transition

As part of the acquisition, Mr. Cooper and all of its servicing functions will be rebranded under the Rocket name. The company said the integration will deepen lifetime relationships by giving homeowners more opportunities to access lending products, from first purchases to refinances and home equity loans.

For mortgage professionals, the integration signals a major reshaping of the competitive landscape. Rocket gains scale on both ends of the business cycle—new loan production and long-term servicing relationships—while sharpening its ability to market refinances, home equity loans, and future purchase mortgages directly to existing borrowers.

Part XIII: What the Future Holds

The Integrated Homeownership Platform

The Rocket-Mr. Cooper combination represents a fundamental reimagining of the American mortgage business. Rather than operating as discrete, transactional businesses—an originator here, a servicer there, a real estate broker somewhere else—the combined entity aspires to create a seamless platform that serves homeowners throughout their entire lifecycle.

The strategic vision encompasses:

Home Search: Through Redfin, consumers begin their homeownership journey on the Rocket platform, browsing listings and connecting with agents.

Financing: When ready to purchase, Rocket Mortgage provides origination services, converting browsers into borrowers.

Closing: Rocket Close handles title and closing services, keeping the transaction within the ecosystem.

Servicing: The former Mr. Cooper operation processes payments and manages escrow accounts, maintaining the customer relationship for years.

Recapture: When customers are ready to refinance, take equity out, or purchase again, the platform already knows them and can offer competitive rates with minimal friction.

Risks and Challenges

Integration risk looms large. Combining two massive technology platforms, distinct corporate cultures, and overlapping functions presents execution challenges that will take years to fully resolve.

Regulatory scrutiny may intensify as the combined entity's market share approaches levels that concern antitrust authorities and financial stability regulators. Managing relationships with the CFPB, state regulators, and the GSEs becomes more complex as scale increases.

Interest rate volatility remains the fundamental risk for any mortgage business. A sharp decline in rates would trigger a refinancing wave, benefiting origination but potentially causing MSR values to decline. A sharp increase would support servicing economics but crush origination volumes.

The Final Chapter of the Phoenix

For the company that began as Nova Credit Corporation in Denver in 1994, the Rocket acquisition represents both an ending and a continuation. The independent journey from subprime originator to servicing giant to public company has concluded with absorption into a larger platform. But Mr. Cooper's operational engine, technology platform, and customer relationships continue under new ownership.

Jay Bray, the architect of much of the company's post-crisis success, carries the Mr. Cooper legacy forward in his new role. After 25 years driving the expansion and culture of Mr. Cooper, Jay Bray, Mr. Cooper's current CEO, will join Rocket as the new President and CEO of Rocket Mortgage, reporting to Varun Krishna, CEO of Rocket Companies. Bray will also join Rocket's board of directors.

Conclusion: The American Mortgage Machine

The Mr. Cooper story reveals truths about American finance that rarely appear in textbooks or annual reports. It shows how private equity can create value not just through cost-cutting, but through strategic transformation when original investment theses fail. It demonstrates how regulatory change creates winners and losers, transferring massive businesses from banks to non-banks over the span of a decade. And it illustrates how technology, scale, and operational execution can transform a nearly bankrupt subprime lender into the backbone of America's mortgage servicing infrastructure.

The numbers tell part of the story: from a $10.5 billion loan portfolio at the time of the Fortress acquisition to a $1 trillion servicing portfolio at the time of the Rocket deal. From near-bankruptcy in 2008 to a $14.2 billion acquisition valuation in 2025. From a company "slapped with more than a thousand lawsuits" to a platform serving 6 million customers.

But numbers alone miss the narrative arc—the phoenix rising from subprime ashes, rebranded with a cartoon mascot, and ultimately absorbed into the largest mortgage deal in American history.

For students of business strategy, the Mr. Cooper case offers several enduring lessons:

Timing matters less than adaptation. Fortress entered at the worst possible time, but the ability to pivot from origination to servicing transformed disaster into success.

Scale creates defensibility. In servicing, the largest players benefit from cost advantages that smaller competitors cannot match, driving continuous consolidation.

Regulatory arbitrage is temporary. The advantages non-banks enjoyed over depositories attracted growth, but also attracted regulatory attention that eroded those advantages over time.

Brand can be reconstructed. Even companies with terrible reputations can rehabilitate their image through operational improvement and strategic repositioning.

Consolidation is the endgame. In mature, scale-driven industries, independent players eventually combine into larger platforms capable of capturing value across the entire customer lifecycle.

The Mr. Cooper story has concluded, but the dynamics it illustrates continue to reshape American housing finance. As Rocket integrates its acquisitions and competitors respond, the next chapter of mortgage industry consolidation has only begun.

The phoenix has landed. What rises next remains to be written.

Note: This article is intended for educational purposes and does not constitute investment advice. Past performance does not guarantee future results. Investors should conduct their own due diligence before making investment decisions.

Part XIV: The Human Element—Customer Experience Transformation

From Nightmare to Partnership

The transformation of customer experience at Mr. Cooper represents one of the most significant turnarounds in financial services history. Understanding how the company evolved from generating over a thousand lawsuits to achieving industry-leading satisfaction scores requires examining the operational changes implemented alongside the brand transformation.

The Persistent Satisfaction Gap

Despite significant investments in technology and process improvements, Mr. Cooper continued to face challenges in customer satisfaction metrics. The company Rocket acquired, Mr. Cooper, historically did not score well in servicing surveys. In 2025, it ranked 23rd of 31 companies eligible to be scored, at 564. Part of the low score was a result of the large number of financially stressed consumers in its portfolio.

The contrast with Rocket's existing business was stark. While Rocket consistently earned high marks for loan servicing, Mr. Cooper's J.D. Power rankings had been subpar for more than a decade. Rocket Mortgage was named #1 in client satisfaction by J.D. Power in mortgage servicing for the 11th year—the most of any lender.

The industry-wide picture painted a similar story. Homeowner satisfaction with mortgage servicers in general was down 10 points from a year ago. Rising escrow costs such as property taxes and insurance and poor communication were factors driving lower customer satisfaction with loan servicers.

Technology Investments and AI Integration

Mr. Cooper made substantial investments in artificial intelligence to address operational efficiency and customer experience. In reporting a $198 million Q2 profit in 2025, Mr. Cooper President Mike Weinbach said the company could service mortgages for about half the cost of its competitors. That gap was widening as Mr. Cooper continued to "invest in and implement new AI solutions, since this technology is uniquely suited for optimizing large call center operations."

Jay Bray said on the same call that Mr. Cooper was "firing on all cylinders" and intended to "hit the ground running" with an integrated platform when it merged with Rocket Companies.

The Rocket integration promises to apply even more sophisticated technology to customer interactions. At the core of Rocket Mortgage's servicing excellence is innovation. To support more than 3.4 million servicing calls annually, Rocket Mortgage developed Rocket Logic – Synopsis, an AI tool that transcribes and analyzes conversations, allowing team members to focus on building lasting relationships over routine tasks.

The Integration Challenge

The acquisition presented both an opportunity and a risk. Mr. Cooper's servicing scale and expertise was complemented by Rocket's long track record of client satisfaction, recognized by J.D. Power. As one, the companies planned to deepen lifetime relationships by giving homeowners more opportunities to access lending products that fit their needs—from a first purchase to a quick refinance or home equity loan.

Even though Mr. Cooper was at the bottom of the J.D. Power origination list with a 697 score, it was a vast improvement from 2024, when it scored 659. In fact, all but two of the scored companies showed year-over-year improvement.

Part XV: The Cybersecurity Dimension

The 2023 Data BreachIn October 2023, Mr. Cooper experienced one of the largest data breaches in the mortgage industry's history. Mr. Cooper shut down multiple systems after it discovered the cyberattack on October 31, 2023 and started its investigation. The data accessible during the attack included the names, addresses, phone numbers, Social Security numbers, dates of birth, and bank account numbers of Mr. Cooper's customers.

Mortgage lender Mr. Cooper admitted almost 14.7 million people's private information, including addresses and bank account numbers, were stolen in the IT security breach, which was expected to cost the business at least $25 million to clean up.

The breach had immediate operational consequences. Apart from the legal repercussions, Mr. Cooper also faced significant backlash when its customers weren't able to make their mortgage payments online. Those who made payments just before the systems were shut down didn't receive confirmations, leading to consumer angst on social media.

Legal Aftermath

Mr. Cooper Group faced a proposed class action over the October 2023 mortgage cyberattack that potentially exposed the personal information of thousands of people. The suit relayed that the information compromised in the breach included consumers' full names, addresses, dates of birth and Social Security numbers. The case argued that the "massive and preventable" Mr. Cooper data breach was a result of the company's negligence in implementing reasonable cybersecurity protocols to protect the sensitive information in its care.

CEO Jay Bray said in a statement: "We take our role as a mortgage company very seriously, and there is nothing more important to us than maintaining our customers' trust. I want you to know how sorry I am for any concern or frustration this may have caused."

Implications for the Rocket Integration

The cybersecurity incident raises important questions about the technological and data security integration between Rocket and Mr. Cooper. With the combined entity now managing data on nearly 10 million homeowners, the stakes for cybersecurity have never been higher. With details from more than 65 million calls with clients each year, 30 petabytes of data and a mission to Help Everyone Home, Rocket Companies is well positioned to be the destination for AI-fueled homeownership.

Part XVI: The Financial Architecture of Mortgage Servicing

Understanding MSR Economics### The Interest Rate Dynamic

The economics of mortgage servicing rights create a natural hedge for diversified mortgage companies. When interest rates rise, there are fewer prepayments, and the value of mortgage servicing rights increases. However, when interest rates are low, the prepayment speed increases, and the value of mortgage servicing rights decrease.

This inverse relationship with interest rates makes MSR portfolios particularly valuable during periods of rising rates—precisely the environment that crushes origination businesses. The increase in mortgage rates that occurred in 2022 led to a significant increase in the value of mortgage servicing rights. The decline in assumed prepayment speeds drove most of the increase in MSR value, but a lesser-known driver of increased MSR value relates to earnings from float income due to substantially higher earnings rates.

Float Income Mechanics

Interest income from float arises from two sources. The larger component comes from loans that are escrowed (impounded) for property taxes and hazard insurance. The servicer collects the escrow payment monthly, disburses the insurance annually, and disburses the property taxes quarterly, semi-annually, or annually depending on the jurisdiction.

Valuation Complexity

MSR valuation may sound complex, but it essentially comes down to estimating how much net money servicing a loan will bring in over time, and accounting for the fact that loans can end early (prepayment or default) and that money in the future is worth less than money today. Key factors like the servicing fee, expected loan prepayment rates, and prevailing interest rates all play a major role in determining MSR values.

From an MSR valuation standpoint, prepayments and delinquencies make it a tricky business. MSR valuations have huge implications for liquidity risk. They become sizable assets on the balance sheet and can be a major source of collateral for nonbank financing.

The Recapture Value

One of the most significant value drivers in the Rocket-Mr. Cooper combination relates to recapture. When a loan underlying Mortgage Servicing Rights is prepaid, and the loan is refinanced with the servicer and thus "retained," servicing fees lost from the prepaid loan will be recaptured through the economics of the new lending arrangement.

Rocket Mortgage has ranked #1 in J.D. Power's mortgage servicer study for 10 years and #1 in mortgage origination 12 times, driving the company's 83% recapture rate—triple the industry average. This recapture capability, applied to Mr. Cooper's massive servicing portfolio, represents the strategic core of the acquisition thesis.

Part XVII: Epilogue—The New American Mortgage Landscape

Industry Consolidation Accelerates

The Rocket-Mr. Cooper transaction marked the most significant step yet in the ongoing consolidation of American mortgage finance. But the deal's impact extends beyond the two companies involved. Once Mr. Cooper and Rocket are under the same roof, they'll be collecting payments on $2.1 trillion in outstanding loans from nearly 10 million homeowners—about one in six U.S. mortgages. Like other lenders that keep their loan servicing rights, Rocket likes the countercyclical nature of the business. Fees generated by loan servicing can help even out the ups and downs in mortgage lending.

Competitive Response

The industry has already begun to respond to Rocket's aggressive consolidation strategy. UWM has responded to Rocket's plans to acquire Mr. Cooper by pulling its own loan servicing from the company and signing a long-term agreement with ICE Mortgage Technology to bring servicing in-house.

The refinancing opportunity ahead could be substantial. While purchase lending is now the name of the game for mortgage lenders, economists at Fannie Mae expect refinancing volume will rebound to $511 billion this year and hit $761 billion in 2026 as mortgage rates come down. If Rocket can capture 20 percent of next year's projected $761 billion refi market, that would amount to $152 billion in refinancing business—50 percent more than the company's $101.2 billion in total 2024 loan production.

The Integration Journey Ahead

With the acquisition closed on October 1, 2025, the hard work of integration has only begun. The combined entity faces significant operational challenges—merging technology platforms, aligning corporate cultures, and standardizing processes across formerly independent organizations.

"There's definitely a focus, I think, on bringing more of the two experiences together and trying to create more [rather] than handling them separately, which has traditionally been more of the focus" at mortgage lenders, according to J.D. Power's senior director of lending intelligence.

The End of Independence

For Mr. Cooper, the Rocket acquisition marked the end of an extraordinary independent journey. From its founding as Nova Credit Corporation in Denver in 1994, through its transformation under Fortress ownership, its near-death experience in the financial crisis, its aggressive expansion through acquisition, its regulatory troubles and rebrand, and finally its emergence as America's largest non-bank mortgage servicer—the company traveled a path that few could have predicted.

"This transaction brings to a close a multi-year journey during which Mr. Cooper grew to become the nation's largest servicer and produced enormous value for our clients, partners, stakeholders and investors," Bray said. "Now, by joining forces with Rocket, we start a new journey, which I believe offers an even bigger opportunity. Through the power of our platform and our people, we will create a more personalized experience that makes owning a home more attainable and easier to navigate. Together, we will deliver the change the housing industry needs."

Final Reflections: Lessons from the Phoenix

The Mr. Cooper story offers a masterclass in corporate transformation, private equity value creation, and the hidden machinery of American housing finance. Several enduring lessons emerge:

Timing matters less than adaptation. Fortress entered at the worst possible time—acquiring a subprime lender just as the subprime market collapsed. But the firm's willingness to support management through a complete business model pivot transformed disaster into success.

Scale creates defensibility. In mortgage servicing, the largest players benefit from cost advantages that smaller competitors cannot match. The fixed costs of technology, compliance, and operations don't scale linearly with portfolio size, creating powerful economies of scale that favor consolidation.

Regulatory arbitrage is temporary. The advantages non-banks enjoyed over depositories attracted growth, but also attracted regulatory attention. As the CFPB settlements demonstrated, regulatory advantages erode as scale and market importance increase.