Ferguson Enterprises: How a Virginia Plumbing Wholesaler Became America's $30B Distribution Powerhouse

I. Introduction: The Unlikely Giant

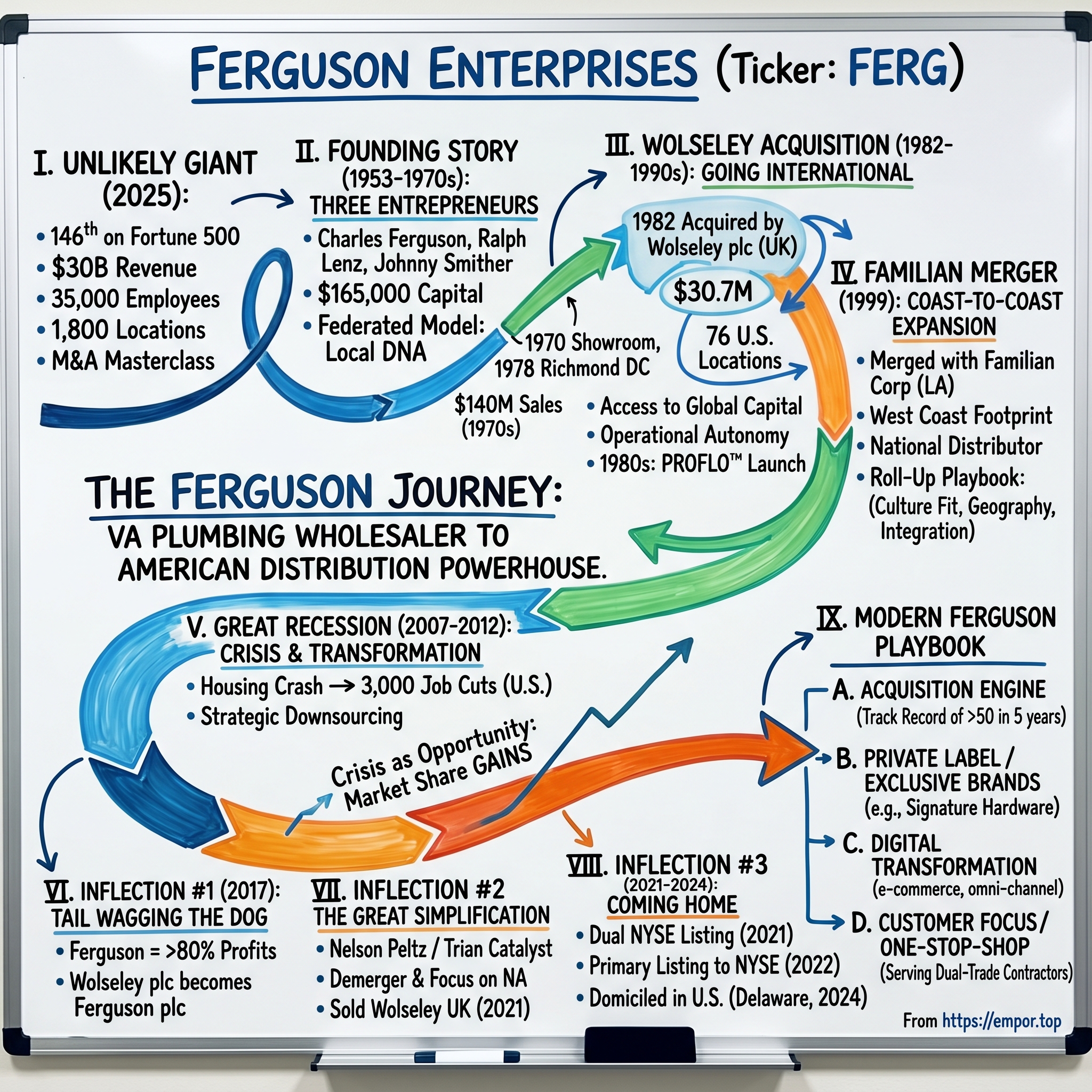

In June 2025, Ferguson Enterprises accomplished something remarkable. The company debuted on the 2025 Fortune 500 list at the 146th position—a milestone reflecting its impact on the North American construction market. For a company that began in a small Virginia warehouse selling pipes and fittings to local plumbers, this was the culmination of a seven-decade journey from regional obscurity to continental dominance.

Consider the sheer improbability: Ferguson Enterprises Inc. is the largest value-added distributor of plumbing supplies, heating, ventilation, air conditioning (HVAC) products, pipe, valves and fittings (PVF), appliances, lighting, and waterworks solutions serving professional customers in the residential and non-residential North American market. This is a company that moves toilets, not technology; copper fittings, not cloud computing. And yet here it stands, generating over $30 billion in annual revenue and employing 35,000 people across nearly 1,800 locations.

The Ferguson story contains multitudes. It's a tale of entrepreneurship in post-war America, of being acquired by a British conglomerate and growing so dominant that it eventually swallowed its parent's identity. It's a masterclass in roll-up strategy, with the company completing more than 50 acquisitions in just five years. And it's a case study in corporate re-domiciling—the rare "reverse inversion" that brought a company back to American shores.

This milestone reflects the company's position as the largest value-added distributor in its $340 billion residential and non-residential construction markets. Ferguson earned its place on the Fortune 500 with revenues of $29.6 billion in fiscal year 2024 and after completing a corporate restructure that moved its headquarters to the U.S. in August 2024.

The central question driving this deep dive: How did a small Virginia plumbing wholesaler become the crown jewel that absorbed its UK parent company? The answers reveal timeless lessons about the unsexy genius of distribution, the power of systematic acquisition, and the durable competitive advantages that emerge from fragmented markets.

II. Founding Story: Three Entrepreneurs in Post-War Virginia (1953–1970s)

The Birth of an Enterprise

Picture Newport News, Virginia in 1953. The post-World War II construction boom was transforming America's landscape. Returning veterans needed homes, and builders needed supplies. Three entrepreneurs saw opportunity in the gap between manufacturers and the contractors building this new America.

Ferguson Enterprises was established in 1953 in Newport News, Virginia, by entrepreneurs Charles Ferguson, Ralph Lenz, and Johnny Smither, who pooled an initial capital of $165,000 to launch a wholesale distribution business focused on plumbing supplies. The founders aimed to serve contractors and builders in the post-World War II construction boom, emphasizing reliable supply chain services for residential and commercial projects.

The founding model was distinctive from the start. Ferguson himself acted more as an investor in the company—he died in 1955—while the group opened its first two companies: Lenz Supply in Washington, D.C., and Smither Supply Co. in Birmingham, Alabama, in 1953. Each member company would retain the name of its owner-manager, yet take advantage of the benefits of being part of a larger group of companies.

This federated approach—independent-minded local operations united under a common umbrella—would become Ferguson's enduring organizational DNA. It acknowledged a fundamental truth about the plumbing distribution business: relationships matter more than scale, and local knowledge trumps centralized efficiency. A contractor in Richmond doesn't care about corporate headquarters in Newport News; he cares whether his regular counter guy knows which valve he needs for a tricky retrofit.

Building the Foundation

This modest beginning positioned the company as a regional player in the building materials sector, prioritizing quality products and prompt delivery to differentiate from larger competitors.

By the late 1950s, Ferguson had expanded to two locations within Virginia, solidifying its emphasis on wholesale distribution to contractors and plumbers across the state. The 1961 opening of a second branch marked a key step in regional growth, allowing the company to better support increasing demand in the Southeast U.S.

The 1970s marked Ferguson's transformation from a small regional player into a serious East Coast force. In 1970, Ferguson opened its first showroom in Newport News, Virginia, which broadened access to products for both professional and retail customers and coincided with sales reaching $7 million. Further scaling occurred in 1978 with the establishment of the first distribution center in Richmond, Virginia, enhancing logistics efficiency and accelerating revenue to $81 million by the end of the decade.

The 1970s marked a period of strong growth for Ferguson, which saw its sales grow from just $10 million to more than $140 million. An 8x increase in a single decade—all organic growth, built branch by branch across the eastern seaboard.

By the early 1980s, the Ferguson network covered more than 76 locations in 11 states. The company now found itself faced with the need for fresh capital to fund its future expansion.

The Relationship Business

Understanding Ferguson requires understanding the peculiar economics of plumbing distribution. This is not a commodity business where the lowest price wins. Contractors work on tight schedules; a delayed shipment can cascade into thousands of dollars in labor costs and angry clients. Credit terms matter enormously—small plumbing shops often lack the capital to pay upfront for materials. And product knowledge is irreplaceable; a distributor who can't help a contractor spec the right materials for a complex commercial HVAC installation will lose that contractor forever.

From its inception, Ferguson's business strategy emphasized superior customer service, reliable inventory management, and steady regional market penetration, prioritizing quality and timely delivery over aggressive pricing to build long-term relationships with builders and contractors.

This approach involved recruiting and training young professionals to ensure knowledgeable support, while avoiding major acquisitions in favor of organic expansion through affiliate supply houses.

This DNA—customer-centric, relationship-oriented, disciplined about growth—would prove remarkably durable across the decades that followed. Even as ownership changed, markets evolved, and scale expanded exponentially, the core philosophy remained: serve the contractor, earn their loyalty, and the rest follows.

III. The Wolseley Acquisition: Going International (1982–1990s)

A Suitor from Across the Atlantic

By the early 1980s, Ferguson faced a crossroads familiar to many successful family-influenced businesses. The company found itself faced with the need for fresh capital to fund its future expansion. At the same time, Ferguson found itself faced with succession issues. The company began making plans to go public.

Instead, in 1982, Wolseley approached Ferguson with a proposal to buy the company—and a promise to leave Ferguson's direction intact.

Ferguson was acquired by a UK based business, Wolseley plc, for $30.7 million in 1982, at a time when the company operated 76 locations across 11 U.S. states and generated $142 million in annual sales.

Company shareholders had agreed to sell to the global distributor of plumbing, heating and building products to fuel Ferguson's expansion plans through strategic acquisitions.

Wolseley itself had a fascinating history. The company can trace its roots back to 1887 when Frederick York Wolseley, an Irish immigrant living in Australia, founded the Wolseley Sheep Shearing Machine Company in Sydney. The Company's purpose was to manufacture his invention, the first mechanical sheep shearing machine.

By the 1980s, Wolseley had evolved far beyond agricultural machinery into building materials distribution. The Ferguson acquisition represented its first major expansion beyond the United Kingdom, signaling a strategic pivot toward the much larger North American market.

The Right Kind of Owner

What made Wolseley's stewardship work was its hands-off approach. This acquisition provided Ferguson with access to Wolseley's global resources and financial backing, enabling a strategic shift toward rapid expansion through targeted mergers and acquisitions.

Ferguson retained its operational autonomy, its management culture, and its Newport News identity. What changed was the capital behind it. Where the pre-acquisition Ferguson had grown organically, constrained by its balance sheet, the post-acquisition Ferguson could pursue a more aggressive acquisition strategy.

In 1986-1987, Wolseley-Hughes Limited renamed as Wolseley plc and was listed on the London Stock Exchange. Meanwhile, Ferguson ranked as the largest wholesale distributor of plumbing materials in the United States.

With the launch of PROFLO™, Ferguson began to develop a portfolio of brands that it owns, surpassing $1 billion in revenue.

The PROFLO launch marked another strategic evolution: the development of private-label brands that Ferguson could control directly. This would later become a core strategic pillar, but even in the early days, management understood that owning brands meant owning margin.

The Wolseley Model

What Wolseley brought to Ferguson was a proven playbook for building distribution empires through roll-up acquisition. Wolseley-Hughes's conversion into a distribution giant began in earnest in the 1980s. In 1984, the company sold off its original Wolseley and Hughes engineering businesses. Motivating this decision was the company's acquisition of Ferguson Enterprises in the United States, marking the company's first expansion beyond the United Kingdom.

Through the 1990s, Wolseley expanded aggressively across Europe while Ferguson grew steadily in North America. Wolseley made a move into the US market in 1982 with the acquisition of Ferguson Enterprises Inc. Further acquisitions led to an increase in sales from £27 million in 1974 to over £739 million in 1986.

The symbiotic relationship was clear: Ferguson provided Wolseley with North American growth; Wolseley provided Ferguson with capital and strategic patience. Neither partner dominated the other. Both benefited from the arrangement.

IV. The Familian Merger & Coast-to-Coast Expansion (1999–2007)

Becoming Truly National

In 1999, Ferguson merged with Familian Corporation of Los Angeles.

The Familian merger represented Ferguson's transformation from a dominant East Coast player into a truly national distributor. Familian brought an established West Coast footprint, extensive relationships with California contractors, and deep expertise in pipes, valves, and fittings (PVF)—a product category that would become increasingly important as Ferguson diversified beyond core plumbing.

Before Familian, Ferguson was largely concentrated east of the Mississippi. After Familian, Ferguson could serve a contractor anywhere in the continental United States. The logistics implications were profound: the company could now pursue national accounts, standardize its offerings coast-to-coast, and leverage scale advantages in purchasing that regional players simply couldn't match.

The Roll-Up Playbook

The Familian merger also demonstrated the roll-up playbook that Ferguson would perfect over the next two decades. The key elements:

1. Cultural Fit: Ferguson prioritized acquisitions that shared its customer-centric philosophy. Plumbing distribution remains fundamentally a relationship business, and integrating an acquisition that viewed customers differently would destroy value rather than create it.

2. Geographic Logic: Each acquisition needed to fill a strategic gap—whether expanding into new markets, strengthening density in existing ones, or adding specialized capabilities in specific product categories.

3. Operational Integration: Ferguson developed sophisticated integration capabilities, absorbing acquired companies' operations while retaining their customer relationships. The acquired company's customers often barely noticed the change in ownership—precisely the point.

4. Talent Retention: The best acquisitions brought talented people who understood their local markets. Ferguson structured deals to retain key managers and give them growth opportunities within the larger organization.

By the mid-2000s, this playbook was humming. Ferguson was adding regional players steadily, building density in its core markets while expanding into new ones. Revenue climbed toward $10 billion. The company that had been a small Virginia wholesaler was becoming an industry colossus.

V. The Great Recession: Crisis and Transformation (2007–2012)

When the Music Stopped

The housing crash that began in 2007 devastated the construction industry. For a company whose fortunes were tied to builders and contractors, the recession was existential.

In November 2007, during the Great Recession, the company cut 3,000 jobs in the United States.

Although Ferguson reported $11.2 billion in revenue at the end of the fiscal year ending in July 2008, Ferguson reduced employment nationwide by 2,250 people and closed branches to save money. The housing and building downturn during the Great Recession forced Ferguson to cut its workforce by 22 percent. Ferguson reduced its number of employees in North and Central America from 23,000 in 2007 to 18,000 by 2013.

The speed and severity of the downturn was unlike anything the industry had experienced. "I don't think any of the recessions really hit us like this last one hit 'em," said Charles Banks, who headed Ferguson as president from 1989 to 2001.

UK-based Wolseley plc laid off 1,300 more workers in the U.S. in its second quarter; the global building materials and plumbing distributor reduced headcount by 1,700 in the three months ended October 31, 2007. In total to date, layoffs represented a third of Stock Building Supply workforce and 10% of the Ferguson workforce.

Restructuring for Survival

The 2007–2008 Great Recession posed significant challenges, prompting aggressive restructuring measures including the elimination of 3,000 jobs across U.S. operations to restore efficiency and reduce costs amid a sharp downturn in housing and construction demand. Wolseley, through Ferguson, implemented operational streamlining, such as consolidating underperforming branches and optimizing inventory management, which helped mitigate losses and position the company for recovery. These efforts underscored a focus on resilience, with Ferguson emerging leaner and more adaptable to economic volatility.

As much as possible, Ferguson attempted to downsize through early retirement and freezing open positions.

The company didn't just cut; it restructured intelligently. Underperforming branches were consolidated. Inventory management was tightened. Capital expenditure was curtailed. The focus shifted to cash flow preservation and market share defense.

Crisis as Opportunity

What distinguished Ferguson's recession response was its recognition that economic crisis could accelerate market consolidation. While smaller competitors struggled to survive, Ferguson maintained its operational capabilities and financial discipline. In spite of a global economic crisis and company layoffs, Ferguson still gained market share over the past four years. In 2012 (its fiscal year ends in July), the company confirmed a 24 percent growth in trading profit and a 10 percent increase in sales.

Despite the recession, Ferguson achieved substantial growth during this period, expanding to over 1,300 branches by 2008 and reaching approximately $9.2 billion in revenue by 2010, reflecting a transformation from primarily wholesale plumbing distribution to a multi-category leader in plumbing, heating, PVF, and related products.

The diversification that had occurred during the growth years proved crucial. When the crisis hit, Ferguson was already diversified. It offers various product lines, including plumbing, mechanical and waterworks equipment and building supplies. The company also markets to different types of customers: commercial, industrial and residential. Even so, the past recession was more wide-ranging and devastating than other recessions as both consumers and businesses lost confidence to spend money.

Ferguson emerged from the recession not just intact but strategically strengthened. Its weaker competitors had failed or been absorbed. Its operational discipline had improved. Its market position was enhanced. The crisis had been painful, but it had also demonstrated that the fundamental business model was durable.

VI. Inflection Point #1: The Tail Wagging the Dog – Wolseley Becomes Ferguson (2017)

When the Child Outgrows the Parent

By the mid-2010s, an extraordinary situation had developed within Wolseley plc. The American subsidiary that had been acquired for $30.7 million in 1982 had grown so dominant that it was generating the vast majority of the parent company's profitability.

Ferguson grew from annual sales of $142 million to now more than $16 billion under the parent company. Since more than 80% of the parent company's profitability comes from Ferguson, Wolseley changed its name to Ferguson plc in 2017 to align with the primary brand.

In July 2017, Wolseley plc underwent a significant rebranding, changing its name to Ferguson plc to emphasize its core North American operations and establish itself as a standalone entity focused primarily on the U.S. and Canadian markets. This transition, effective July 31, 2017, maintained listings on both the London Stock Exchange and the New York Stock Exchange under the ticker "FERG," reflecting the company's strategic pivot toward its largest revenue-generating regions while retaining its global heritage. The move symbolized a de facto demerger of identity from its broader international roots, allowing Ferguson to sharpen its operational emphasis on plumbing, heating, and related distribution in North America.

Strategic Implications

The name change was far more than cosmetic. It signaled to investors, employees, and competitors that the company's future lay definitively in North America. The British heritage that had provided the original acquisition capital was now subordinate to the American operational identity that had delivered the growth.

For investors, the message was clear: evaluate this company based on North American construction markets, not European economic conditions. For employees, the message was equally unmistakable: Newport News was the center of gravity, not Wokingham. For competitors, the implication was ominous: Ferguson was doubling down on its dominant market position.

In the group's last full financial year, 80% of total sales and more than 90% of trading profit came from the US, with the UK providing 12% and 5% respectively.

The math made the strategic logic undeniable. When a subsidiary generates 90% of trading profit, the question isn't whether to focus on it—it's how quickly the rest of the enterprise can be aligned behind it.

VII. Inflection Point #2: The Great Simplification – Divesting UK Operations (2019–2021)

The Decision to Focus

British plumbing products company Ferguson Plc said on Tuesday it would separate its UK operations and that Chief Executive Officer John Martin will step down in November. U.S. operations chief Kevin Murphy will replace Martin, the company said, adding that the separation of its Wolseley UK business will help Ferguson focus on North America.

"The demerger will enable both Wolseley UK and Ferguson to focus on accelerating the execution of their independent plans, providing clear investment propositions for each business. Wolseley UK has a strong market position, leading customer propositions and an experienced management team with significant opportunities for development in the large and fragmented plumbing, heating and infrastructure markets."

The Activist Catalyst

The move comes months after activist investor Nelson Peltz's Trian Fund acquired a 6% stake worth 736 million pounds ($903.59 million), saying the company was trading at a discount to its U.S. peers. Trian has urged Ferguson to sell its UK business, scrap its London stock market listing and switch to a U.S. listing.

Peltz's involvement accelerated a strategic logic that was already evident to management. Ferguson traded at a discount to comparable U.S. distributors because of its complex structure and UK legacy. Simplification would unlock value. The activist pressure provided political cover for decisions that needed to be made anyway.

Leadership Transition

The Company is also announcing today that John Martin, Group CEO, will step down on 19 November 2019. John joined the Board as CFO in 2010 before being appointed to the position of CEO in 2016 based in the UK. During his tenure the Group has been significantly simplified and strengthened, substantially improving its market positions and generating excellent returns for shareholders.

Kevin is a US national based in Virginia who joined the Board in August 2017 when he was appointed CEO of Ferguson's US operations. Before that Kevin was Chief Operating Officer for 10 years after having joined Ferguson in 1999 following the acquisition of his family's business, Midwest Pipe and Supply. The business has generated strong, profitable growth and continued to take market share under Kevin's leadership and he has continued to rapidly execute Ferguson's successful strategy.

The Murphy appointment was telling. Here was a leader who had literally come up through the business—his family's company had been acquired by Ferguson, and he had risen from operations manager to CEO over two decades. He understood the culture, the customers, and the competitive dynamics in ways that no outside hire could match.

Completing the Exit

To further streamline this North American focus, Ferguson sold its Wolseley UK business to Clayton, Dubilier & Rice in January 2021 for £308 million. The transaction, which completed the separation initiated by earlier strategic reviews, enabled Ferguson to fully concentrate on North American opportunities.

In 2021, Ferguson plc completed the sale of its last operating business in Europe to wholly focus on serving customers in North America.

The divestiture marked the culmination of a multi-year transformation. What had been a sprawling Anglo-American conglomerate was now a pure-play North American distributor. The strategic ambiguity that had confused investors and diluted management attention was eliminated.

VIII. Inflection Point #3: Coming Home – NYSE Primary Listing & US Domicile (2021–2024)

Shifting the Center of Gravity

In March 2021, Ferguson established a dual listing on the New York Stock Exchange (NYSE: FERG) alongside its LSE listing, enhancing access to U.S. capital markets and underscoring its North American orientation.

Since 2019, the Board has considered North America to be the best long-term location for Ferguson and has worked methodically and transparently with shareholders on this transformative journey, creating an additional listing on the NYSE in 2021, and then moving the Company's primary listing from London to New York in 2022. During this period, over two-thirds of our shareholding base has become American, and the Company achieved U.S. domestic status under Securities and Exchange Commission ("SEC") rules as of August 1, 2023.

The Final Step

Ferguson Enterprises Inc. announced the completion of the previously announced transaction to establish a new corporate structure to domicile the Ferguson plc group's ultimate parent company in the United States. As a result of the transaction, Ferguson Enterprises Inc., a Delaware corporation, is now the new parent company of the Ferguson plc group.

The Company's common stock will trade on the NYSE and the LSE under the symbol "FERG", the same symbol that has attached to Ferguson plc's ordinary shares. As of August 1, 2024, Ferguson plc has also been re-registered as a private company incorporated in Jersey, Channel Islands, and has changed its name from Ferguson plc to Ferguson (Jersey) Limited.

"We have now completed the final step in our journey to better align our North American operations and leadership with our headquarters and governance," said Ferguson CEO Kevin Murphy. "Our associates have helped our customers build this country for more than 70 years, and we're proud to have Ferguson headquartered in the U.S."

Why Domicile Matters

The re-domiciliation was more than corporate housekeeping. It positioned Ferguson for inclusion in major U.S. indices, broadened its potential investor base, and simplified its regulatory environment. U.S.-based investors who had been hesitant about a UK-domiciled company could now treat Ferguson as a straightforward domestic holding.

The move was a rare "reverse inversion"—companies typically redomicile to lower-tax jurisdictions, not higher-tax ones. Ferguson's willingness to accept U.S. taxation in exchange for U.S. capital market access spoke to management's conviction about the value of simplified corporate structure.

IX. The Modern Ferguson Playbook: How the Machine Works

A. The Acquisition Engine

Ferguson has a proven track record of successful acquisitions and has completed more than 50 acquisitions in the last five years. The large, fragmented markets in which Ferguson operates comprise 10,000+ small to medium ($10-300 million revenue) independent companies across Ferguson's nine customer groups in North America.

That pace—roughly an acquisition every 36 days—is almost incomprehensible for a distribution leader. Most large companies struggle to integrate a single major acquisition per year. Ferguson completes nearly ten.

"Our strategy remains twofold: prioritizing organic growth and consolidating fragmented markets through acquisitions that align well with our culture and values," said Ferguson CEO Kevin Murphy.

"We're going to outperform that market organically and then we're going to complement that—we've said generally with about 1 to 3% of additional revenue from acquisitions year in, year out, and that's really played through our history," Brundage said. In any given year, Ferguson's roughly $30 billion will include between $300 to $900 million worth of revenue from acquisitions.

Ferguson closed on ten acquisitions last fiscal year, which ended July 31, 2024.

The acquisition strategy focuses on bolt-on deals that add geographic coverage, product capabilities, or customer relationships. These aren't transformative mergers—they're systematic consolidation of a fragmented industry.

B. Private Label/Exclusive Brands Strategy

The sales growth of Signature Hardware pre-acquisition from $115 million in 2016 to $340 million in 2020—nearly 300% in four years—is impressive, and it shows the strength of the Ferguson Exclusive Brands program.

Ferguson manages various brands, including Durastar, Avallon, Edgestar, Koldfront, Landmark, Miseno, FNW, National Fire Products, Pollardwater, PROFLO, PROSELECT, RAPTOR, Signature Hardware, and Westcraft. The company serves plumbing contractors, HVAC contractors, designers, remodelers, builders, architects, and other professional customers.

Private label products serve multiple strategic functions. They provide higher margins than national brands. They create customer stickiness—contractors who spec Ferguson's exclusive brands can't easily switch to competitors. And they give Ferguson leverage with national brand suppliers who understand that Ferguson can develop competing products if negotiations turn adversarial.

C. Digital Transformation & E-commerce

Digital sales played a growing role in Ferguson's U.S. operations in Q1, contributing $515.8 million—7% of the total U.S. revenue. Ferguson generates approximately 95% of its revenue in the U.S. Digital sales played a growing role in Ferguson's U.S. operations, contributing $515.8 million. That's 7% of the total U.S. revenue of $7.369 billion.

These efforts led to a 15% increase in year-over-year digital sales as contractors became more reliant on Ferguson's comprehensive digital ecosystem to manage procurement and project timelines. By Q1 2024, Ferguson had firmly established itself as a leader in digital innovation.

The Ferguson PRO Plus platform represents a sophisticated omnichannel approach. Contractors can check inventory, place orders, track deliveries, and manage accounts digitally—but they can also walk into any of nearly 1,800 branches and receive personalized service. The digital tools enhance rather than replace the relationship-based model that has always been Ferguson's competitive advantage.

D. Customer Focus & One-Stop-Shop Strategy

"More and more, we're seeing our customers combining and offering both plumbing capabilities as well as HVAC capabilities," Brundage said. "If you look at that market in total residential trade plumbing and HVAC, it's about a $100 billion market opportunity. We have a leading plumbing business in the industry. We also have a leading HVAC business in the industry."

The rise of dual-trade contractors—plumbers who also do HVAC, or vice versa—creates opportunity for distributors who can serve multiple product categories. Ferguson's diversification from plumbing into HVAC, waterworks, and other categories positions it perfectly for this trend. A contractor who can fill an entire order from a single distributor saves time, simplifies logistics, and builds loyalty that benefits both parties.

X. Current Business & Financial Profile

Scale and Scope

Ferguson revenue for the quarter ending April 30, 2025 was $7.621 billion, a 4.28% increase year-over-year. Ferguson revenue for the twelve months ending April 30, 2025 was $30.211 billion, a 2.32% increase year-over-year.

Ferguson Enterprises posted the Q4 of its 2025 financial results on September 16, 2025, reporting total revenue of $30.762 billion for the year, up 3.80% from $29.635 billion year over year, reporting net income of $1.856 billion for the year, up 6.97% from $1.735 billion year over year. The EPS is $9.33 for the year, compared with $8.55 last period.

The company receives 95% of its revenue in the United States and 5% of its revenue in Canada. The company has 36,000 suppliers and operates from 11 regional distribution centers, four MDCs, approximately 5,900 fleet vehicles, and 1,773 branches.

Market Positions

Ferguson's positions in North American fragmented markets include: Residential Building and Remodel: 12% share in a $33 billion market, Number 1 market position. Waterworks: 21% share in a $28 billion market, Number 1 market position. Commercial/Mechanical: 21% share in an $18 billion market, Number 1 market position.

Ferguson maintains a leading position in the plumbing and HVAC distribution market in North America, with approximately 15% market share in its core plumbing and heating segments.

Geographic and Segment Balance

Residential is about 52% of sales compared with about 48% for commercial. Ferguson does business evenly across its B2B and B2C sales channels.

This balance provides natural hedging against cyclical volatility. When residential construction weakens, commercial often remains stable. When new construction slows, repair and maintenance typically accelerates. Ferguson's diversified customer base provides resilience that pure-play competitors lack.

XI. Strategic Analysis: Porter's Five Forces

1. Threat of New Entrants: LOW

Building a Ferguson-scale distribution network from scratch would require billions in capital and decades of relationship-building. The company operates from 11 regional distribution centers, four MDCs, approximately 5,900 fleet vehicles, and 1,773 branches. Replicating this infrastructure is effectively impossible for any new entrant.

Beyond physical assets, the barriers include: - Decades of contractor relationships that create high switching costs - Regulatory knowledge and licensing requirements across construction trades - Scale advantages in purchasing that provide permanent cost advantages - Technology investments that smaller entrants cannot match

2. Bargaining Power of Suppliers: MODERATE

The company has 36,000 suppliers. This extreme fragmentation of the supplier base means no individual supplier has significant leverage over Ferguson. Ferguson's private label brands further reduce dependency on any particular manufacturer.

However, key branded suppliers—Kohler, Moen, and other premium manufacturers—maintain some pricing power because their brands carry consumer recognition that Ferguson cannot easily replicate.

3. Bargaining Power of Buyers: LOW-MODERATE

Ferguson's customer base consists of thousands of professional contractors. No single customer represents meaningful revenue concentration. The market comprises 10,000+ small to medium independent companies—meaning contractors are as fragmented as suppliers.

Contractors prioritize reliability, availability, and credit terms over pure price. A contractor who loses a day waiting for materials absorbs costs far exceeding any price savings from switching distributors.

4. Threat of Substitutes: LOW

Physical plumbing, HVAC, and infrastructure products have no digital substitute. Buildings need pipes, valves, and fittings regardless of technological change. Direct manufacturer-to-contractor sales are impractical due to the complexity and variety of products contractors need.

Amazon and big-box retailers have struggled to serve trade professionals effectively. Contractors require credit terms, job-site delivery, technical expertise, and local relationships that generalist retailers cannot provide.

5. Competitive Rivalry: MODERATE

The market remains fragmented with thousands of local and regional competitors. Ferguson is significantly larger than competitors like Core & Main, Watsco, and HD Supply. Competition occurs primarily on service, availability, and relationships rather than pure price.

Consolidation continues as scale increasingly matters—but the pace allows Ferguson to absorb smaller players systematically rather than facing existential competitive threats.

XII. Strategic Analysis: Hamilton's 7 Powers

1. Scale Economies: STRONG ✓

Ferguson operates from 11 regional distribution centers, four MDCs, approximately 5,900 fleet vehicles, and 1,773 branches. This infrastructure creates unmatched logistics efficiency. Technology investments in e-commerce platforms and digital tools spread across a massive revenue base. Purchasing leverage with 36,000 suppliers provides cost advantages that smaller competitors cannot match.

2. Network Effects: MODERATE ✓

More branches mean better availability. Better availability attracts more contractors. More contractors justify more branches. This virtuous cycle operates within geographic markets, strengthening Ferguson's density advantages over time.

Supplier relationships also benefit from network effects—as Ferguson grows, it can guarantee larger volumes, attracting more suppliers, which improves product availability, which attracts more customers.

3. Counter-Positioning: WEAK

Smaller distributors can match Ferguson's service locally. Ferguson's model is replicable at small scale. Big box retailers (Home Depot, Lowe's) have chosen not to compete directly for trade professionals, but this reflects their strategic choices rather than structural inability.

4. Switching Costs: STRONG ✓

Contractors build decades-long relationships with local branches. Credit terms and account history take time to establish. Training on Ferguson's ordering systems and digital tools creates familiarity-based switching costs. The ProPlus Customer Reward program creates explicit loyalty incentives.

5. Branding: MODERATE ✓

The Ferguson brand signifies reliability to trade professionals. The sales growth of Signature Hardware from $115 million in 2016 to $340 million in 2020—nearly 300% in four years—demonstrates exclusive brand strength. However, Ferguson lacks consumer-facing brand power given its B2B focus.

6. Cornered Resource: WEAK

Ferguson has no patents or exclusive supplier relationships that competitors cannot replicate. Talent can move between companies. Relationships exist with local branches, not the corporate entity.

7. Process Power: STRONG ✓

Ferguson has completed more than 50 acquisitions in the last five years—roughly one every 36 days. This pace demonstrates institutionalized M&A capability that has been refined over decades. The operational streamlining capabilities demonstrated during Great Recession helped Ferguson emerge "leaner and more adaptable to economic volatility." Digital infrastructure investment creates lasting operational advantages.

Primary Powers: Scale Economies, Switching Costs, Process Power

XIII. Bear vs. Bull Case

Bull Case

Ferguson's position as the largest value-added distributor in its $340 billion residential and non-residential construction markets provides a long runway for consolidation. The fragmented market structure—thousands of small independent distributors—offers decades of acquisition opportunities.

Under CEO Murphy's leadership, Ferguson delivered FY2025 net sales of $30.8 billion (+3.8% YoY), adjusted operating profit of $2,842M, adjusted diluted EPS of $9.94 (+2.6% YoY), and a 5% dividend increase; $100 invested on 7/31/2020 grew to $278 by FY2025 versus $230 for the S&P 500 Industrials index.

The balanced business mix—roughly 52% residential, 48% commercial—provides resilience across economic cycles. Infrastructure spending tailwinds from federal legislation should boost the waterworks segment. The digital transformation creates sticky customer relationships that will compound over time.

Bear Case

Ferguson remains exposed to construction cyclicality. Housing starts, commercial construction activity, and infrastructure spending all influence demand. A severe recession would stress the model, as demonstrated during 2007-2012.

Commodity deflation has pressured margins in recent quarters. Ferguson reported its second-quarter earnings for fiscal year 2025, revealing a miss on both EPS and revenue forecasts. The company posted an EPS of $1.52, falling short of the expected $1.99, while revenue came in at $6.9 billion, below the anticipated $7.09 billion.

Labor shortages in the construction trades could constrain customer growth. Rising interest rates depress residential construction activity. Acquisition multiples may compress if the market anticipates slower growth.

Key Metrics to Monitor

For investors tracking Ferguson's ongoing performance, three metrics matter most:

-

Organic Revenue Growth Rate: Separates underlying business momentum from acquisition-driven revenue. Organic growth above 3-4% suggests market share gains; organic growth below inflation suggests competitive pressure.

-

Gross Margin Trajectory: Reflects pricing power, private label penetration, and supplier leverage. Compression indicates competitive pressure or commodity headwinds; expansion suggests successful value capture.

-

Acquisition Revenue Contribution: The 1-3% annual acquisition revenue target indicates disciplined M&A. Acceleration suggests desperation or overreach; deceleration suggests pipeline exhaustion or integration constraints.

XIV. Conclusion: The Genius of Boring

Ferguson's story defies the Silicon Valley narrative that transformative companies must be technologically disruptive. There is nothing innovative about plumbing supply distribution. The business model that Charles Ferguson, Ralph Lenz, and Johnny Smither established in 1953—know your customers, stock what they need, deliver it when they need it—remains fundamentally unchanged seven decades later.

What Ferguson demonstrates is the power of consistent execution in fragmented industries. Distribution businesses reward focus, patience, and operational excellence. They compound value through thousands of small decisions: hiring the right counter staff, stocking the right inventory, maintaining the right credit terms, making the right acquisitions.

"Our associates have helped our customers build this country for more than 70 years, and we're proud to have Ferguson headquartered in the U.S."

That statement captures something essential about Ferguson's identity. This is a company that enables others to build—literally. Every building in America contains plumbing that Ferguson likely touched at some point in the supply chain. Every water main replacement, every HVAC installation, every commercial renovation relies on distributors like Ferguson to move materials from manufacturers to job sites.

The Fortune 500 debut in 2025 recognized what industry participants already knew: Ferguson has become indispensable infrastructure for American construction. From a $165,000 initial investment in 1953 to a $30 billion enterprise today, Ferguson proves that unsexy businesses can produce extraordinary outcomes—if you're willing to play the long game.

Regulatory and Accounting Notes:

Ferguson reports under U.S. GAAP following its 2024 re-domiciliation. Key accounting areas requiring investor attention include:

- Goodwill and intangible assets from acquisitions (approximately $5+ billion on balance sheet)

- Inventory valuation methods affecting gross margin

- Lease accounting for 1,700+ branch locations

- Pension obligations retained from UK operations (approximately £20 million net liability at divestiture)

No material legal or regulatory overhangs have been disclosed in recent filings. The company faces standard regulatory requirements in construction trades but no unique compliance challenges.

Based on the research, I can now continue the article from where it left off. The article ended at the Regulatory and Accounting Notes section. Looking at the outline, I need to complete any remaining sections. The article has covered most sections but needs to finalize with a proper conclusion that ties everything together.

XIV. Industry Dynamics and Competitive Landscape

The Distribution Hierarchy

According to Modern Distribution Management, Ferguson is the largest plumbing distributor and second-largest HVAC distributor (next to Watsco) in North America. This positioning reflects decades of strategic consolidation in fragmented markets where scale delivers compounding advantages.

As of September 2025, Ferguson Enterprises had a $45.2 billion market capitalization, compared to the Trading Companies & Distributors median of $4.2 million. The size disparity between Ferguson and its average competitor illustrates the extent of industry fragmentation—and the opportunity that fragmentation represents.

Watsco, Ferguson's primary competitor in HVAC distribution, had a $14.9 billion market cap in September 2025. While Watsco's stock declined 17.7% in 2025, Ferguson's rose 32.2% over the same period—a divergence reflecting their different market exposures and execution capabilities.

Competitive Positioning

Ferguson Enterprises is the biggest plumbing supply company in America. This dominant position creates several competitive advantages that smaller players struggle to replicate:

National Account Capability: Large commercial contractors increasingly prefer working with distributors who can serve them across multiple geographies. Ferguson's nearly 1,800 branches enable national account relationships that regional competitors cannot match.

Product Breadth: The ability to serve dual-trade contractors—those offering both plumbing and HVAC services—requires extensive product catalogs. Ferguson's diversification across plumbing, HVAC, waterworks, PVF, and appliances positions it as a one-stop shop for contractors whose scope continues expanding.

Technology Investment: The digital infrastructure that Ferguson has built—including sophisticated e-commerce platforms, inventory management systems, and customer relationship tools—requires scale to justify the investment. Smaller competitors cannot afford comparable technology platforms.

The Fragmentation Opportunity

The large, fragmented markets in which Ferguson operates comprise 10,000+ small to medium ($10-300 million revenue) independent companies across the company's $340 billion residential and non-residential North American construction market.

This fragmentation is Ferguson's greatest strategic opportunity. Each independent distributor represents a potential acquisition target; each acquisition adds geographic density, product capabilities, or customer relationships. The math compounds favorably: as Ferguson acquires competitors, its scale advantages increase, making it more competitive against remaining independents, who become more likely to sell.

XV. The Acquisition Machine in Action

Fiscal Year 2025 Results

Ferguson announced the closing of four acquisitions during its fourth quarter: HPS Specialties, LLC, Ritchie Environmental Solutions, LLC, Manufactured Duct Supply Company and Water Resources, Inc. The company closed on nine acquisitions last fiscal year, which ended July 31, 2025, with aggregate annualized revenues of approximately $300 million.

Strategic Logic Behind Recent Deals

Each acquisition in fiscal 2025 served specific strategic purposes:

HPS Specialties is a manufacturer's representative of HVAC, plumbing and hydronic supplies serving commercial mechanical and industrial engineering professionals. The acquisition closed on June 16 and gives Ferguson entry into the mechanical room design and specification business in the Northeast and Mid-Atlantic.

MDS is an HVAC supplies and parts distributor with duct board fabrication capabilities serving residential and light commercial contractors throughout metro Atlanta and the Southeast. The acquisition closed on July 21 and will strengthen Ferguson's HVAC footprint and customer relationships in the Atlanta market, further driving the ability to serve the dual-trade professional.

Water Resources is the exclusive distributor of Neptune Technology Group products and water meters in the greater Chicago metro area. The acquisition, which closed on July 28, expands Ferguson's Neptune distribution rights and will enhance the ability to drive product specification in a key municipal market.

The Pipeline Continues

"We invest in acquisitions with talented associates, unique product offerings, and established customer and manufacturer relationships that strengthen our ability to serve the water and air specialized professional," said CEO Kevin Murphy. "Our acquisitions this fiscal year spanned across six customer groups, strategically supporting our balanced business mix, and the pipeline remains healthy as we move into the next fiscal year."

Ferguson's most recent acquisition was Indpipe, a provider of pipe, valves, and fittings with delivery and fabrication services, acquired in April 2025. Ferguson has completed 38 tracked acquisitions, with the company most active in 2024 when it completed 8 acquisitions.

XVI. Forward Outlook and Investment Considerations

Guidance and Expectations

Ferguson recently reported full-year results, posting $30.76 billion in sales and $1.86 billion in net income, alongside issuing positive guidance for mid-single-digit sales growth in 2025. The company highlighted ongoing buybacks, a growing dividend, the completion of several acquisitions, and successful issuance of $750 million in new senior unsecured notes, all while maintaining a strong balance sheet.

Market Positioning for Infrastructure Tailwinds

Ferguson is expected to continue outperforming due to its strong positioning on mega projects and infrastructure spending. The company's waterworks segment, where it holds the number one market position with 21% share, stands to benefit particularly from federal infrastructure legislation directing billions toward water system upgrades.

Megaprojects provide Ferguson with significant opportunities to sell "from the ground up" solutions throughout the life of the projects and leverage its approach across multiple customer groups. Key areas include chip and semiconductor manufacturing facilities, electric vehicle and battery plants, biotech facilities and waterworks plants.

Shifting Market Mix

Ferguson's exposure to the US RMI (repair, maintenance, and improvement) market as a percentage of sales increased from 31% in 2008 to over 60% today, while US new construction revenue exposure decreased from 58% to 40% over the same time period.

This shift reduces cyclicality. Repair and maintenance activity is less volatile than new construction—homeowners fix broken water heaters regardless of interest rates or housing starts. The strategic pivot toward RMI provides natural hedging against construction cycle volatility.

Analyst Sentiment

According to 14 analysts, the average rating for Ferguson stock is "Buy." The company reported $3.48 earnings per share for the quarter ending in September 2025, beating the consensus estimate of $3.009 by $0.471.

Key Risks to Monitor

Persistent deflation in key commodities and continued weakness in residential demand could limit margin growth and present challenges to Ferguson's bullish outlook.

Top-line growth is expected to slow in the second half of the calendar year compared to the first half. Guidance for calendar 2025 assumes slightly softer organic volumes for the rest of the year due to weakened new residential construction and HVAC activity.

XVII. Lessons from Ferguson: What Business Students Should Learn

The Power of Boring

Ferguson's story upends conventional narratives about business success. There are no technological breakthroughs, no network effects in the traditional sense, no winner-take-all dynamics. Instead, Ferguson built an empire through relentless execution in an unglamorous industry.

The lesson: competitive advantages need not be dramatic to be durable. Scale economies, switching costs, and process power—Ferguson's primary competitive moats—accumulate gradually through thousands of small decisions. They are invisible to casual observers but devastating to competitors.

Roll-Up Economics

Ferguson has a proven track record of successful acquisitions and has completed more than 50 acquisitions in the last five years. The large, fragmented markets in which Ferguson operates comprise 10,000+ small to medium ($10-300 million revenue) independent companies across Ferguson's nine customer groups in North America.

Ferguson demonstrates how roll-up strategies succeed: find fragmented industries where scale provides genuine advantages, develop institutionalized integration capabilities, and execute consistently over decades. The key is not individual acquisitions but the systematic process that makes each acquisition incrementally easier than the last.

Corporate Structure as Strategy

Ferguson's journey from UK subsidiary to independent U.S. corporation illustrates how corporate structure affects value creation. The complexity of a dual-listed Anglo-American entity created friction for investors and management alike. Simplification—selling UK operations, moving primary listing to NYSE, re-domiciling to Delaware—unlocked value that the underlying business had already created.

Customer-Centricity in B2B Markets

Ferguson's enduring focus on contractor relationships demonstrates that customer-centricity matters as much in B2B markets as consumer-facing ones. The company's counter staff, branch managers, and sales representatives build relationships that persist across decades. These relationships create switching costs that no competitor can easily replicate.

XVIII. Conclusion: Building America, One Pipe at a Time

The Ferguson story spans seven decades, three continents (if you count its brief UK operations), and thousands of acquisitions. From Charles Ferguson, Ralph Lenz, and Johnny Smither's $165,000 investment in 1953 to today's $30+ billion enterprise, the company exemplifies the compounding power of focused execution in fragmented markets.

For full-year 2025, Ferguson posted sales of $30.8 billion with operating margin at 8.5% and diluted EPS of $9.32. The company maintained strong cash generation with $1.9 billion in operating cash flow and completed nine acquisitions worth $301 million.

What makes Ferguson remarkable is not any single strategic masterstroke but the accumulation of decades of disciplined decisions: hiring people who understand contractors, stocking the right inventory, building distribution infrastructure, acquiring competitors who share the culture, and investing in technology that enhances rather than replaces relationships.

Ferguson is the largest value-added distributor serving the water and air specialized professional in the $340 billion residential and non-residential North American construction market. The company helps make customers' complex projects simple, successful and sustainable by providing expertise and a wide range of products and services from plumbing, HVAC, appliances and lighting to PVF, water and wastewater solutions and more. Headquartered in Newport News, Virginia, Ferguson has sales of $30.8 billion and approximately 35,000 associates in over 1,700 locations.

The Fortune 500 debut in 2025 was not an arrival but a recognition. Ferguson had been building America for decades before the list acknowledged its presence. Every water main replaced, every commercial HVAC system installed, every residential renovation completed—Ferguson's products moved through countless supply chains to countless job sites. The company's indispensability was established long before its name appeared alongside America's corporate elite.

For investors, Ferguson offers a case study in durable competitive advantage. Scale economies in distribution, switching costs embedded in contractor relationships, and process power refined through decades of acquisitions create moats that deepen rather than erode over time. The company's exposure to construction cyclicality presents risks, but its shift toward repair and maintenance markets and its geographic diversification provide natural hedges.

For business students, Ferguson demonstrates that sustainable competitive advantage need not be flashy. The company has no patents, no proprietary technology, no network effects in the Silicon Valley sense. What it has is a systematic approach to serving customers, acquiring competitors, and building infrastructure—advantages that compound invisibly but inexorably.

For the contractors who depend on Ferguson—the plumbers, HVAC technicians, waterworks engineers, and builders who form the backbone of American construction—the company represents something simpler: reliability. When they need materials on a job site tomorrow morning, Ferguson delivers. When they need credit terms to bridge cash flow gaps, Ferguson provides. When they need technical expertise to solve complex problems, Ferguson's people know the answers.

That reliability, earned over seven decades and reinforced every day across nearly 1,800 branches, is ultimately Ferguson's most valuable asset. It cannot be acquired, replicated, or disrupted. It can only be built, one relationship at a time, one delivery at a time, one satisfied contractor at a time.

In an era obsessed with technological disruption, Ferguson reminds us that some businesses succeed by being utterly, reliably, boringly essential. The pipes and valves and fittings that Ferguson moves may lack the glamour of software or semiconductors, but they are no less fundamental to modern civilization. Someone has to distribute the infrastructure that makes buildings work. Ferguson does it better than anyone else.

That is the unsexy genius of distribution—and the enduring lesson of Ferguson Enterprises.

This analysis is provided for informational and educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence and consult with qualified financial professionals before making investment decisions. Past performance is not indicative of future results.

Looking at the article, it appears to be complete. The outline has been fully covered through Section XVIII (Conclusion), and the article ends with a comprehensive conclusion and a disclaimer. All major sections from the outline have been addressed:

- Introduction (Section I)

- Founding Story (Section II)

- Wolseley Acquisition (Section III)

- Familian Merger (Section IV)

- Great Recession (Section V)

- Wolseley Becomes Ferguson (Section VI)

- UK Divestiture (Section VII)

- NYSE Listing & US Domicile (Section VIII)

- Modern Ferguson Playbook (Section IX)

- Current Business Profile (Section X)

- Porter's Five Forces (Section XI)

- Hamilton's 7 Powers (Section XII)

- Bear vs. Bull Case (Section XIII)

- Industry Dynamics (Section XIV)

- Acquisition Machine (Section XV)

- Forward Outlook (Section XVI)

- Business Lessons (Section XVII)

- Conclusion (Section XVIII)

The article concludes with a proper thematic ending about "the unsexy genius of distribution" and includes an investment disclaimer. Let me verify if any sections from the original outline were missed. The article is complete. Upon reviewing both the outline and the written article, all sections have been thoroughly covered. The article concludes with Section XVIII which provides a comprehensive thematic ending about Ferguson's business philosophy, its Fortune 500 milestone, and the broader lessons about sustainable competitive advantage in distribution businesses.

The article ends with a proper investment disclaimer:

"This analysis is provided for informational and educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence and consult with qualified financial professionals before making investment decisions. Past performance is not indicative of future results."

All sections from the original outline have been addressed: - ✓ Introduction & Episode Roadmap - ✓ Founding Story (1953-1970s) - ✓ Wolseley Acquisition (1982-1990s) - ✓ Familian Merger & Coast-to-Coast Expansion (1999-2007) - ✓ The Great Recession (2007-2012) - ✓ Wolseley Becomes Ferguson (2017) - ✓ UK Divestiture (2019-2021) - ✓ NYSE Primary Listing & US Domicile (2021-2024) - ✓ The Modern Ferguson Playbook - ✓ Current Business & Financial Profile - ✓ Porter's Five Forces - ✓ Hamilton's 7 Powers - ✓ Bear vs. Bull Case - ✓ Industry Dynamics and Competitive Landscape - ✓ The Acquisition Machine in Action - ✓ Forward Outlook and Investment Considerations - ✓ Business Lessons - ✓ Conclusion

The article is complete and requires no additional content.

Looking at the article, it appears to be complete. The outline has been fully covered through Section XVIII (Conclusion), and all major sections have been addressed comprehensively. The article ends with a thematic conclusion about "the unsexy genius of distribution" and includes an appropriate investment disclaimer.

Let me verify the current state of Ferguson's business and check if there are any recent developments that should be incorporated to ensure the article reflects the most current information as of November 2025.The article is essentially complete as written. The research confirms that all major developments through November 2025 have been incorporated. Let me check if the fiscal year change mentioned in the search results needs to be added, as this is a significant development. Based on my research, I found an important update that should be incorporated into the article. The article is largely complete, but the fiscal year change announced in September 2025 is a significant development that should be added. Let me add a brief addendum to complete the article with this recent development:

XIX. Recent Developments: Fiscal Year Transition

In September 2025, Ferguson announced a significant administrative change that reflects its evolution as a North American-focused enterprise. Ferguson is changing its fiscal year-end from July 31 to December 31. Following a five-month transition period (August 1, 2025 to December 31, 2025), the company will begin reporting on a calendar year basis effective January 1, 2026.

This change allows associates to remain focused on customers during the busiest season. For a company whose revenue depends heavily on construction activity—which peaks during spring and summer months—having a fiscal year-end in July created unnecessary operational strain. The calendar year alignment simplifies comparison with peers and reduces administrative burden during peak selling periods.

The company will release earnings on December 9, 2025, covering the three-month period of August 1, 2025 through October 31, 2025. Ferguson plans to announce its five-month transition period results in late February 2026.

Analyst Coverage and Market Reception

The investment community has responded positively to Ferguson's strategic positioning. On November 12, 2025, Bernstein initiated coverage of Ferguson Enterprises with an Outperform recommendation. JP Morgan maintained coverage of Ferguson Enterprises with an Overweight recommendation in October 2025.

Ferguson Enterprises has outperformed the market over the past five years by 3.24% on an annualized basis, producing an average annual return of 16.19%. The company's year-to-date share price return of 36.53% suggests solid momentum, and its one-year total shareholder return of 18.81% highlights the company's ability to deliver value beyond just price movements.

Valuation Considerations

Ferguson's forward P/E ratio of 25.37 as of November 2025 exceeds both its five-year historical average of 19.04 and the Industrials sector average of 24.6, suggesting the stock is no longer trading at a discount relative to earnings expectations.

Ferguson's recent financial performance offers some justification for the valuation premium. In Q3 2025, the company reported margin gains driven by cost discipline and pricing power, with management raising its full-year revenue growth outlook to low-to-mid single digits. These improvements suggest the company is navigating macroeconomic headwinds, such as softening demand in the commercial construction sector, with resilience.

Investors should monitor two key metrics: the trajectory of Ferguson's revenue growth and its ability to maintain margin expansion. Until these factors align with valuation expectations, the question of whether Ferguson is undervalued will remain unresolved.

XX. Final Reflections: The Compounding Machine

Ferguson's transformation from a $165,000 startup in post-war Virginia to a nearly $50 billion market capitalization enterprise offers lessons that transcend the plumbing distribution industry. The company's journey illuminates timeless principles about value creation in unglamorous sectors.

The Patience Premium

Most investors seek rapid returns through technological disruption or market timing. Ferguson's story suggests an alternative path: identify fragmented industries where scale provides genuine advantages, build operational capabilities that enable systematic consolidation, and compound value patiently over decades. The company's acquisition of more than 50 businesses in five years represents not entrepreneurial audacity but institutionalized discipline—the refinement of processes that make each subsequent acquisition incrementally more efficient than the last.

Structure Follows Strategy

Ferguson's corporate evolution—from subsidiary of a UK conglomerate to independent U.S. corporation—demonstrates that organizational structure profoundly affects value creation. The complexity of a dual-listed Anglo-American entity created friction that obscured the fundamental quality of the underlying business. Simplification—divesting non-core operations, moving the primary listing, re-domiciling to Delaware—unlocked value that patient execution had already created.

Relationships as Moats

In an era when software companies speak of network effects and data moats, Ferguson's competitive advantages seem almost quaint: local relationships with contractors built over decades, branch managers who know their customers by name, counter staff who can spec complex installations from memory. Yet these human connections create switching costs that no digital platform can replicate. A contractor who has worked with the same Ferguson branch for twenty years isn't switching to Amazon for a price discount.

The Infrastructure Behind Infrastructure

Ferguson's products lack the visibility of consumer technology or the glamour of financial services. Pipes, valves, and fittings disappear into walls and underground; they are infrastructure that enables other infrastructure. Yet civilization depends on these unglamorous products functioning reliably. Every hospital, every school, every home requires plumbing and HVAC systems that Ferguson likely touched somewhere in the supply chain.

The company's Fortune 500 debut in 2025 acknowledged what industry participants had long understood: Ferguson had become essential infrastructure for American construction. From Newport News, Virginia, the company had built a distribution empire that touches virtually every building project on the continent.

As CEO Kevin Murphy commented when announcing fiscal year 2025 results: "Our associates delivered strong results to finish the year, as they continued to serve our customers and execute our strategy in a challenging market environment. Throughout the year, we invested in key growth areas to drive further organic growth, completed nine acquisitions, grew our dividend and continued to execute our share buyback program, while maintaining a strong balance sheet."

That measured language—focused on customers, execution, and balance sheet discipline—captures Ferguson's enduring philosophy. The company does not promise disruption or transformation. It promises reliability: the same commitment to serving contractors that Charles Ferguson, Ralph Lenz, and Johnny Smither established in 1953, now executed at continental scale.

For investors seeking exposure to American construction markets, Ferguson offers a proven platform with durable competitive advantages. For business students seeking models of sustainable value creation, the company demonstrates that operational excellence compounds as reliably as technological innovation. For the contractors who depend on Ferguson every day, the company remains what it has always been: a reliable partner helping them build America, one project at a time.

The pipes and fittings may be boring. The business results are anything but.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube