NiSource: The Regulated Utility's Reinvention

I. Introduction & Episode Roadmap

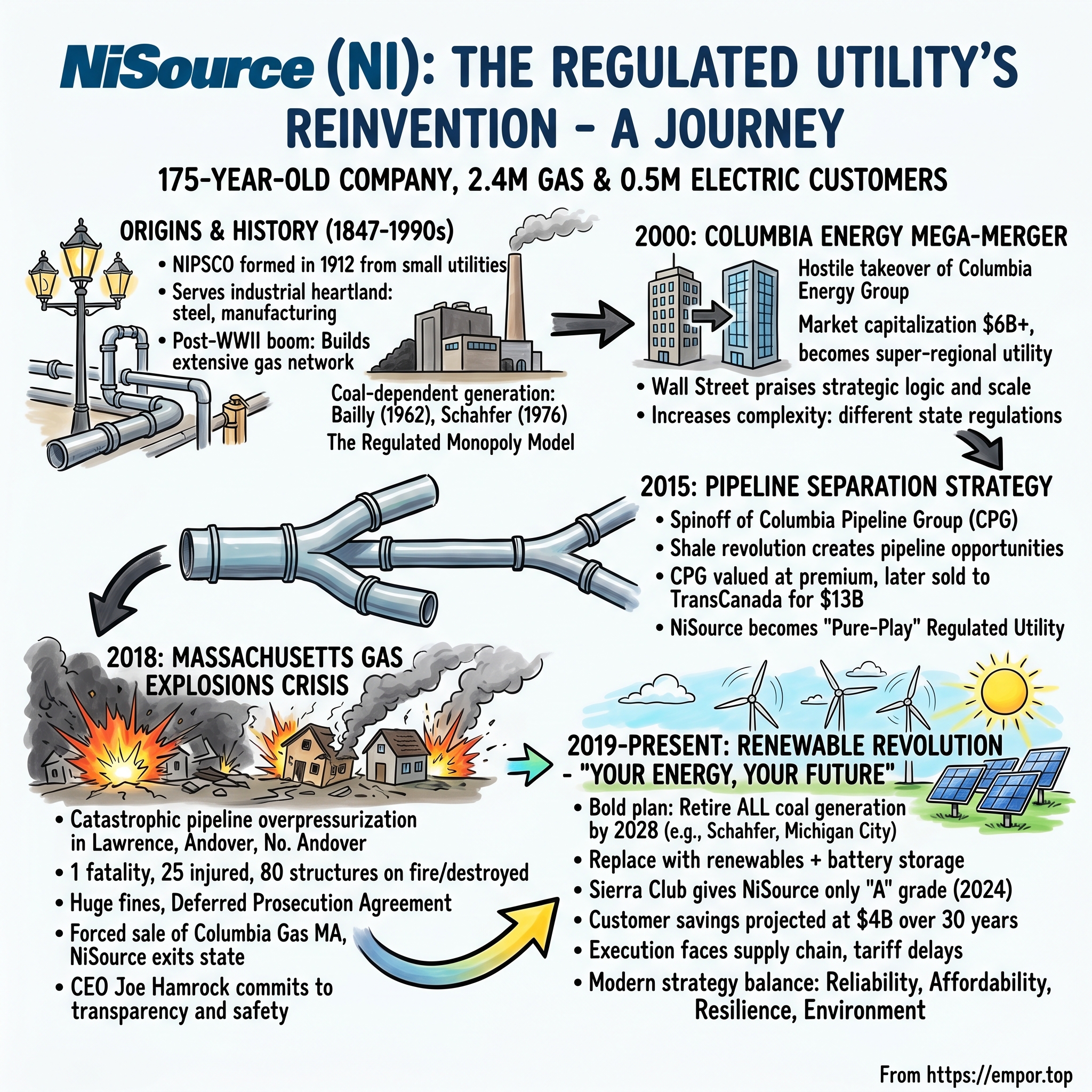

Picture this: In January 2019, while most century-old utilities were still clinging to their coal plants like precious heirlooms, NiSource's CEO Joe Hamrock stood before investors and announced something audacious. The company would retire all its remaining coal generation—over 2,000 megawatts of capacity—and replace it entirely with renewables. Not in 2050. Not in 2040. But by 2028. The kicker? They'd do it while saving customers money.

This wasn't some Silicon Valley startup making bold promises about disrupting energy. This was NiSource—a 175-year-old utility with roots stretching back to 1847, serving 2.4 million natural gas customers through 37,200 miles of pipeline and half a million electric customers in northern Indiana. A company so embedded in America's industrial heartland that its infrastructure literally powered the rise of Gary's steel mills and Chicago's expansion.

How does a utility—perhaps the most change-resistant business model ever invented—transform from coal dependency to renewable energy leadership? How does it navigate existential crises, including gas explosions that killed residents and destroyed entire neighborhoods? And why would the Sierra Club, not exactly known for cozy relationships with fossil fuel companies, give NiSource the only "A" grade among utility parent companies in their 2024 clean energy ranking?

The NiSource story isn't just about energy transition. It's about the fundamental tension at the heart of American capitalism: how monopolies granted by the state balance public service with private profit. It's about engineering both physical infrastructure and financial structures. And it's about how sometimes, the most radical transformations come not from disruption, but from within the most regulated corners of the economy.

Over the next several hours, we'll trace NiSource's evolution from its 19th-century origins through hostile takeovers, strategic spinoffs, devastating accidents, and ultimately to its current position as an unlikely leader in clean energy. We'll examine the regulated utility model—a business structure so unique that even sophisticated investors often misunderstand it. We'll explore how catastrophe can catalyze transformation. And we'll assess whether NiSource's renewable bet represents genuine strategic vision or simply riding regulatory tailwinds.

This is a story about infrastructure, regulation, and energy—but more fundamentally, it's about how established institutions reinvent themselves when survival demands it. Let's begin where all great utility stories start: with the laying of the first pipes.

II. Origins & The Long Arc of History (1847–1990s)

The year is 1847. James K. Polk is president. The California Gold Rush hasn't started yet. And in northern Indiana, a group of businessmen gather to solve a problem that seems quaint today: how to light their streets without whale oil. They form what would become one of NiSource's earliest predecessor companies, beginning a process of laying gas pipes that would continue, almost uninterrupted, for the next 175 years.

But the real story begins in 1912, when Northern Indiana Public Service Company—NIPSCO—was born from the consolidation of smaller utilities. This wasn't unusual; the early 20th century saw massive consolidation in the utility sector as financiers realized the economics of scale in power generation and distribution. What made NIPSCO different was its location: northern Indiana, perfectly positioned between Chicago's insatiable energy appetite and the industrial boom towns sprouting across the Midwest.

The 1920s were the Wild West of utilities. Holding companies stacked on holding companies, creating byzantine corporate structures that would make today's private equity firms blush. Samuel Insull, the Chicago utility magnate who'd learned at Thomas Edison's knee, built an empire of interconnected utilities that stretched across 32 states. NIPSCO, while independent, watched and learned. They understood that in the utility business, bigger meant better returns—more customers to spread fixed costs, more political clout for favorable rate decisions, more capital for expansion.

Then came 1929, and with it, the collapse of Insull's empire and dozens of other utility pyramids. The devastation was so complete that Franklin Roosevelt made utility reform a centerpiece of the New Deal. The Public Utility Holding Company Act of 1935—PUHCA—effectively outlawed the holding company structures that had enabled such spectacular collapses. Utilities were forced to simplify, to focus on geographic regions, to submit to state regulation.

For NIPSCO, PUHCA was both constraint and opportunity. While other utilities spent years unwinding complex structures, NIPSCO's relatively simple organization allowed it to focus on what utilities do best: building infrastructure. Through the 1940s and 1950s, as northern Indiana transformed from agricultural heartland to industrial powerhouse, NIPSCO laid the pipes and strung the wires that made it possible.

The post-war boom brought a new challenge: coal. Northern Indiana sits inconveniently far from Appalachian coal fields but tantalizingly close to Illinois Basin coal—lower quality but abundant. NIPSCO made a fateful decision: they would build their generation fleet around this local coal. The Bailly Generating Station, opened in 1962 on the shores of Lake Michigan, could burn 14,000 tons of coal daily. The R.M. Schahfer Generating Station, completed in 1976, added another 1,600 megawatts of coal-fired capacity.

By the 1980s, NIPSCO had evolved into something uniquely American: a regulated monopoly that was simultaneously incredibly powerful—controlling the energy fate of millions—and completely constrained by public utility commissions that dictated everything from investment decisions to customer rates. The regulatory compact was elegant in its simplicity: the utility got a monopoly and a guaranteed return on investment; in exchange, it had to serve everyone in its territory and submit to price regulation.

Understanding this model is crucial because it explains everything that follows. In a normal business, you make money by selling more product at higher margins. In a regulated utility, you make money by investing capital—building power plants, laying pipes, upgrading substations—and earning a regulated return on that investment. The more you invest (assuming regulators approve), the more you earn. It's capitalism, but not as Silicon Valley knows it.

The 1990s brought deregulation fever. California was unbundling its utilities. Texas was creating competitive power markets. Financial engineers were discovering that utility assets, with their stable cash flows, could be sliced, diced, and securitized in ways that would make investment bankers salivate. NIPSCO watched this transformation and made a crucial decision: rather than resist the financialization of utilities, they would master it.

In April 1999, NIPSCO Industries Inc. changed its name to NiSource Inc. It sounds like corporate rebranding fluff, but it signaled something deeper—a transformation from regional utility to aspiring energy conglomerate. The company that had spent a century laying pipes in Indiana was about to embark on its most ambitious expansion yet. The age of mega-mergers was beginning, and NiSource intended to be a buyer, not a seller.

III. The Columbia Energy Mega-Merger (2000)

February 28, 2000. Gary Neale, NiSource's CEO, picks up the phone to make a call that will either transform his company or destroy it. On the other end: Oliver Richard, chairman of Columbia Energy Group. The message: NiSource is launching a hostile takeover.

Columbia Energy wasn't just any utility—it was a giant, with operations stretching from the Gulf of Mexico to New England, serving 4.4 million customers. Its market cap of $4.5 billion dwarfed NiSource's $1.9 billion. In the genteel world of utilities, where mergers were typically negotiated over bourbon in wood-paneled boardrooms, a hostile takeover was almost unheard of. David was loading his sling to take on Goliath.

The backstory reads like a business school case study in strategic patience. For eight months before going public, NiSource had been quietly approaching Columbia about a friendly merger. Columbia's board, led by Richard, repeatedly rebuffed them. They thought NiSource was too small, too Midwestern, too... unsophisticated. Columbia had bigger dreams—they were in talks with other partners, exploring international expansion, considering ventures beyond traditional utility operations.

But Neale had done his homework. Columbia's stock was trading at $62, well below what NiSource calculated as its intrinsic value. More importantly, Columbia's shareholders were restless. The company's international ventures had disappointed. Its non-regulated businesses were underperforming. The stock had languished while peers soared during the late-1990s bull market.

NiSource's hostile bid was brilliantly structured: $64 per share in cash and stock, valuing Columbia at $6 billion including debt. But here's where it gets interesting—NiSource didn't have $6 billion. They had commitments from banks, contingent on due diligence. They had a stock component that required Columbia shareholders to bet on the combined company's future. It was financial engineering at its finest, or most reckless, depending on your perspective.

Columbia's board initially resisted, deploying the standard takeover defenses. They questioned NiSource's financing. They raised regulatory concerns—would officials in Massachusetts, Ohio, Pennsylvania, Virginia, and Maryland really approve being controlled by an Indiana company? They even explored white knight alternatives.

But NiSource had an ace: the shareholders. Institutional investors who owned Columbia stock saw the immediate premium and the strategic logic. A combined NiSource-Columbia would create the fourth-largest gas utility in America, with economies of scale that could drive hundreds of millions in synergies. More importantly, it would create a "super-regional" utility with diversified regulatory exposure—if one state commission got difficult, others might compensate.

The turning point came in July 2000. After five months of public warfare, Columbia's board blinked. But not without extracting concessions: the price rose to $72 per share, valuing Columbia at $7.9 billion including debt. NiSource also agreed to governance provisions that gave Columbia board members significant representation in the combined company.

The integration that followed was a masterclass in utility consolidation. Unlike tech mergers where cultures clash over ping-pong tables and stock options, utility integration is about systems—billing systems, dispatch systems, emergency response protocols. NiSource kept Columbia's brand in markets where it had strong recognition while centralizing back-office functions. They identified $150 million in annual synergies, mostly from eliminating duplicate corporate functions and optimizing gas procurement.

But the real genius of the merger wasn't operational—it was regulatory. By maintaining separate utility subsidiaries in each state while centralizing holding company functions, NiSource could optimize its regulatory strategy. When Ohio was offering favorable rate treatment for infrastructure investment, they could accelerate spending there. When Massachusetts tightened regulations, they could slow investment while maintaining service.

The combined company now served 3.7 million gas and electric customers across nine states. Annual revenues exceeded $7 billion. The transformation from regional utility to national player was complete. Or so it seemed.

What Neale and his team didn't fully appreciate was that they hadn't just acquired assets and customers—they'd acquired complexity. Each state had different regulations, different politics, different energy mixes. Columbia's gas distribution network in Massachusetts, built in the 19th century, required different management than NIPSCO's relatively modern Indiana infrastructure. The company that had mastered the regulatory compact in Indiana now had to master it in eight additional jurisdictions, each with its own quirks and requirements.

The merger closed in November 2000, just eight months after the hostile bid was launched—lightning speed for a utility transaction of this size. Wall Street loved it. The stock rose 15% on the closing announcement. Analysts praised the strategic vision and execution. But within the combined company, the real work was just beginning. Integrating two utilities is like performing surgery on a patient who can't stop running—the lights must stay on, the gas must keep flowing, even as you're rewiring the entire nervous system.

As we'll see, this complexity would eventually lead NiSource to a radical strategic reversal. But in 2000, the future looked bright. Natural gas was the bridge fuel to a cleaner energy future. Deregulation was creating new opportunities. And NiSource had just become one of America's energy giants. The question was: could they manage what they'd bought?

IV. The Pipeline Separation Strategy (2015)

September 28, 2014. Robert Skaggs Jr., NiSource's CEO, stands before the board with a radical proposal that would have seemed insane just years earlier: break up the company. Specifically, separate Columbia Pipeline Group—the interstate pipeline business that moved gas from production fields to local distribution systems—from the rest of NiSource. Undo part of what the Columbia merger had built.

To understand why this made sense, you need to understand how the utility business had evolved since 2000. The shale revolution—horizontal drilling plus hydraulic fracturing—had transformed America from gas importer to gas exporter. The Marcellus and Utica shales, sitting right in Columbia Pipeline's backyard, had become the Saudi Arabia of natural gas. Pipeline companies were printing money moving gas from these fields to markets.

But here's the catch: pipeline companies and local distribution companies (LDCs) are fundamentally different businesses, even though both move natural gas. Pipelines are like toll roads—you charge for capacity and flow, with limited regulatory oversight from FERC (Federal Energy Regulatory Commission). LDCs are classic utilities—heavily regulated by state commissions, earning returns on invested capital, obligated to serve all customers.

Wall Street valued these businesses differently. Pipeline companies, with their growth potential and fee-based models, traded at 15-20x EBITDA. Integrated utilities like NiSource traded at 8-10x. The math was simple: Columbia Pipeline Group was worth more outside NiSource than inside it.

But Skaggs had a deeper insight. The regulatory compact that governed utilities was becoming increasingly complex. States wanted cleaner energy, infrastructure investment, and lower rates—simultaneously. Managing this while also running interstate pipelines created conflicts. When NiSource negotiated gas transportation rates with Columbia Pipeline, regulators wondered if they were getting fair deals. When Columbia Pipeline wanted to build new capacity, regulators questioned whether it benefited local ratepayers.

The separation, announced in September 2014, was structured as a tax-free spinoff. Each NiSource shareholder would receive one share of Columbia Pipeline Group (CPG) for each share of NiSource they owned. No cash changed hands. No investment bankers got rich (well, not that rich). It was corporate simplification at its finest.

The details were fascinating. CPG would get Columbia Pipeline Partners (their master limited partnership), Columbia Gulf (their major pipeline system), and Columbia Midstream (their gathering operations). NiSource would keep the local gas distribution operations and NIPSCO's electric business. Debt would be allocated proportionally. Both companies would be investment-grade rated.

Wall Street's reaction was euphoric. The day of the announcement, NiSource stock jumped 8%. Analysts who had been pushing for a breakup for years finally got their wish. The sum of the parts was indeed greater than the whole—immediately after separation on July 1, 2015, the combined market value of NiSource and CPG exceeded the pre-announcement value by $2 billion.

But the real winner emerged six months later. In March 2016, TransCanada (now TC Energy) announced it would acquire CPG for $13 billion including debt—a 32% premium to CPG's trading price. For NiSource shareholders who held onto their CPG shares, the spinoff had created extraordinary value. A shareholder who owned $100 of NiSource before the separation announcement ended up with roughly $180 of value by the time TransCanada closed.

The strategic implications were profound. Post-separation, NiSource was now a "pure-play" regulated utility—no commodity exposure, no complex pipeline economics, just the steady business of delivering gas and electricity to customers under state regulation. This simplification allowed management to focus on what really mattered: the energy transition that was about to reshape their entire business model.

Skaggs, in his final analyst call as CEO (he retired in 2015, succeeded by Joe Hamrock), put it simply: "We've created two companies that can each pursue their optimal strategies without compromise." CPG could chase pipeline growth opportunities. NiSource could focus on modernizing its distribution infrastructure and generation fleet.

The separation also freed NiSource from a hidden burden: the capital intensity of pipeline expansion. CPG had been planning billions in growth projects to serve Marcellus producers. While potentially lucrative, these projects would have consumed capital that NiSource needed for its own infrastructure. Post-separation, NiSource could allocate capital purely based on regulated utility returns.

There was one more benefit, though management didn't emphasize it at the time: the separation removed NiSource from the increasingly contentious world of interstate pipelines. Environmental opposition to new pipelines was growing. Permitting was becoming nightmarish. By 2020, when TC Energy would write off $2.8 billion on the canceled Keystone XL pipeline, NiSource could watch from the sidelines, grateful to be out of that business.

The pipeline separation marked the end of NiSource's empire-building phase. No more acquisitions, no more complex corporate structures, no more trying to be all things to all stakeholders. Just a regulated utility, serving customers, earning allowed returns. Simple, boring, predictable.

Of course, nothing in the utility business stays simple for long. Even as NiSource was simplifying its corporate structure, a crisis was brewing in its Massachusetts operations that would test everything the company thought it knew about risk management.

V. The Massachusetts Gas Explosions Crisis (2018)

September 13, 2018, 4:11 PM. A Columbia Gas technician in Lawrence, Massachusetts, notices something wrong on his monitoring screen. Gas pressure in the south Lawrence distribution system is spiking—not gradually, but exponentially. Within minutes, pressure that should be 0.5 PSI hits 75 PSI. Natural gas, pushed at fire-hose pressure through century-old cast iron pipes designed for a trickle, begins seeking any escape.

At 4:20 PM, the first explosion rocks a home on Chickering Road in Lawrence. Then another on Springfield Street. Then another. And another. Within an hour, 80 structures across Lawrence, Andover, and North Andover are on fire or have exploded. Residents describe the scene as apocalyptic—houses launching into the air, flames shooting from basement foundations, the smell of gas everywhere.

Leonel Rondon, 18, is sitting in his car in a Lawrence driveway when a house chimney, blown off by an explosion, crashes through his windshield. He dies instantly—the disaster's only fatality, though it could have been far worse. Twenty-five others are injured, some with severe burns. Eight thousand six hundred customers lose gas service. The Merrimack Valley has become a war zone.

The cause, investigators would later determine, was almost laughably preventable. Columbia Gas was replacing cast iron pipes—routine work for any gas utility. But when they relocated pressure sensors, nobody updated the distribution maps. When workers increased pressure in the new pipes, the system thought pressure was too low in the old ones and opened regulators wide, creating the deadly overpressure. Joe Hamrock, NiSource's CEO, immediately flew to Massachusetts. What he found was a company utterly unprepared for crisis. Columbia Gas had no unified command structure, no clear communication protocols, no rapid response capability. While fires still burned, politicians were on TV demanding Columbia Gas leave the state forever. Customers who'd lost everything were sleeping in high school gymnasiums. The company's reputation, built over a century, was destroyed in an afternoon.

The financial toll mounted quickly. Columbia Gas agreed to pay a criminal fine of $53 million, the largest criminal fine ever imposed under the Pipeline Safety Act. The company reached a $143 million settlement with residents and businesses affected by the explosions. An $80 million agreement with the three communities. State fines. Federal monitoring costs. Emergency response expenses. All told, NiSource would eventually report disaster-related costs exceeding $1.6 billion.

But the real cost was strategic. As part of a deferred prosecution agreement, NiSource agreed to undertake their best reasonable efforts to sell Columbia Gas Massachusetts, after which NiSource and Columbia Gas would stop all gas pipeline operations in Massachusetts. The company wasn't just being fined—it was being exiled.

The sale to Eversource, announced the same day as the guilty plea, was both humiliation and relief. Eversource agreed to buy Columbia Gas's Massachusetts assets for $1.1 billion—a price that, after accounting for all the disaster-related liabilities NiSource retained, represented a massive loss on assets they'd owned for decades.

The safety failures were damning. By at least 2015, according to an internal company notice, Columbia Gas knew that the failure to properly account for control lines in construction projects could lead to a "catastrophic event," including fires and explosions. They knew the risk. They had identified the danger. Yet throughout the project, Columbia Gas disregarded the known safety risks related to control lines, and instead focused on the timely completion of construction projects to maximize earnings.

For a utility, whose entire business model depends on public trust and regulatory approval, the Massachusetts disaster was existential. How do you convince regulators in Indiana, Ohio, Pennsylvania, Virginia, Maryland, and Kentucky that you can be trusted when you've just killed someone and destroyed a community through negligence?

Hamrock's response was radical transparency. NiSource didn't fight the investigations, didn't minimize responsibility, didn't hide behind lawyers. They accepted guilt, paid the fines, implemented every safety recommendation from the National Transportation Safety Board across all their operations—not just in Massachusetts. They brought in external safety experts, created new oversight positions, implemented technology that would have prevented the Massachusetts disaster.

More fundamentally, the crisis forced a cultural transformation. The utility industry had always moved slowly, carefully, incrementally. Safety was important, but so was cost control, schedule adherence, and avoiding regulatory attention. Massachusetts changed that calculus. Safety became the only priority that mattered. Every procedure was reviewed. Every project was reassessed. Every employee was retrained.

The irony is that this safety obsession, born from tragedy, would become essential to NiSource's next transformation. Because when you're asking communities to let you build thousands of megawatts of wind turbines and solar panels—infrastructure that many still view with suspicion—your safety record matters. Your reputation for competence matters. Your ability to execute complex projects without killing people really, really matters.

The Massachusetts disaster could have destroyed NiSource. Instead, it became the crucible that forged the company's future. The utility that emerged from the crisis was leaner (having lost Massachusetts), more focused (pure-play regulated utility in friendly jurisdictions), and paradoxically more ambitious. If you could survive having your name synonymous with disaster, if you could rebuild from that level of reputational destruction, what else could you transform?

VI. The Renewable Revolution: "Your Energy, Your Future" (2018–Present)

January 2019. Four months after the Massachusetts explosions. NiSource's stock is still recovering. Trust is at an all-time low. And Joe Hamrock stands up at an investor conference to announce that NiSource will retire all its coal plants and replace them with renewables. The timing seems insane. The ambition seems impossible. The market's reaction? The stock jumps 5%.

To understand why this announcement landed differently than you'd expect, you need to understand what had been happening in the boardrooms and planning departments of NiSource for the preceding eighteen months. While the public saw a traditional utility clinging to coal, inside the company a revolution was brewing—driven not by environmental activism but by spreadsheets.

The math had changed. In 2010, building a megawatt of wind capacity cost $2,500. By 2018, it was under $1,200. Solar had fallen even more dramatically—from $4,000 per megawatt to under $1,000. Battery storage, once a fantasy, was becoming economically viable. Meanwhile, coal plants required constant maintenance, environmental compliance costs kept rising, and capacity factors were falling as natural gas plants undercut them in wholesale markets. NiSource's 2018 Integrated Resource Plan—filed months after the Massachusetts disaster—had already identified the economic case for renewables. The effort detailed in the company's 2018 integrated resource plan (IRP) lays out a blueprint to transition northern Indiana's energy generation away from coal and toward renewable energy sources. But it was the January 2019 announcement that crystallized the vision: the company announced that it would accelerate retirement of its five coal-fired units, and focus on "renewable energy resources, such as solar and wind energy, along with battery storage technology," as part of an initiative titled "Your Energy, Your Future", with a goal of "reducing carbon emissions by more than 90 percent by 2028."

The plan was breathtaking in scope. The company will retire Units 14, 15, 17 and 18 at the R.M. Schahfer Generating Station in Wheatfield, Ind., no later than 2023 and Unit 12 at the Michigan City Generating station in Michigan City, Ind., by 2028. To replace the coal-fired plants, NIPSCO anticipates pursuing largely renewable energy resources – solar and wind energy – combined with battery storage.

This wasn't greenwashing. The numbers were compelling. NIPSCO's analysis showed that customers would save $4 billion over 30 years by moving to renewables versus continuing with coal. The utility could retire debt-heavy coal plants, reduce operations and maintenance costs, and invest in assets that qualified for federal tax credits. Regulators loved it because it meant cleaner air and economic development—solar and wind projects bring construction jobs and property tax revenues to rural counties.

But execution proved harder than planning. In 2022, the U.S. Commerce Department launched an investigation into whether solar manufacturers were using factories in Southeast Asia to circumvent American tariffs on Chinese panels. The company's plans to retire its coal units by 2023 could be postponed, according to its quarterly earnings filing on Wednesday, as it foresees up to 18 months of delays in new solar deployments.

Solar projects originally scheduled for completion in 2022 and 2023 could experience six to 18 months of delays, NiSource said. The Indiana Crossroads Solar Park and Dunns Bridge Solar I project, representing about $440 million of investment, saw their in-service dates shift from the end of 2022 to the middle of 2023. The two units of the Schahfer plant total 847 MW and were initially meant to be retired by May 2023, replaced with solar projects in 2022 and 2023, according to NiSource's utility subsidiary, Northern Indiana Public Service (NIPSCO). The company expects to remain on track with retiring the single unit at Michigan City Generating Station by 2028.

Despite these setbacks, NiSource pressed forward. By July 2023, they announced that their first two solar projects—Indiana Crossroads and Dunns Bridge I—were online and operating. These Indiana-based solar projects are online and operating, producing more cost-effective, cleaner energy for homes and businesses across Indiana. NIPSCO's in-service wind projects are performing well, and 100 percent of the excess power sales and renewable energy credit (REC) sales from these existing renewable projects and our existing generation fleet currently goes back to customers, which is nearly $60 million since 2021.

The transformation wasn't just about swapping coal for solar panels. NiSource previously laid out plans to invest up to $10.6 billion from 2021 through 2024 in its electric and gas operations, with $2 billion earmarked for renewable energy investments. This represented one of the most aggressive utility transformation programs in America.

The results speak for themselves. In October 2024, the Sierra Club—not exactly known for praising utilities—released their "Dirty Truth" report card. NiSource was the only parent utility company to receive an A grade in the Sierra Club's ranking. Think about that: a company that five years earlier was running coal plants, that had just caused deadly explosions through negligence, was now the environmental movement's favorite utility.

The strategic logic was impeccable. By moving first and fastest on renewables, NiSource locked in the best sites, the best developers, and the best terms. They secured federal tax credits before they potentially expired. They pleased regulators who were under pressure to address climate change. They attracted ESG-focused investors who had been avoiding utilities. And perhaps most importantly, they gave their battered reputation a compelling redemption narrative.

VII. The Modern Utility Business Model

Walk into NiSource's investor relations presentation today and you'll see a business that would be unrecognizable to utility executives from even a decade ago. Gone are the complex corporate structures, the commodity trading desks, the international ventures. What remains is almost monastically simple: regulated utility operations in six states, serving 3.7 million customers, earning allowed returns on invested capital.

The beauty of the modern regulated utility model, as NiSource has refined it, lies in its predictability. Regulators set the rules: you can earn, say, a 9.8% return on equity for investments in electric infrastructure, 9.6% for gas distribution. You propose investments—a new substation here, pipeline replacement there, renewable generation over there. Regulators approve (or modify) your plans. You build. You earn. Rinse and repeat.

But here's where it gets interesting. The transition to renewable energy sources must balance multiple factors - including reliability, affordability, resilience, and environmental impact - that affect current and future customers and communities. That means we must continue to provide customers with access to a reliable supply of energy at an affordable cost as we bring solar, wind and other cleaner energy sources online.

NiSource's modern strategy threads this needle through what they call "constructive regulatory environments"—utility-speak for states where regulators understand that utilities need to earn reasonable returns to attract capital. Indiana, Ohio, Pennsylvania, Virginia, Maryland, Kentucky—these aren't California or New York with their aggressive climate mandates and contentious rate cases. These are states where utilities and regulators have developed decades-long working relationships.

The company targets 6-8% annual growth in rate base—the value of assets on which they earn regulated returns. This isn't Silicon Valley hockey-stick growth, but for a utility, it's aggressive. Every dollar of approved investment becomes part of the rate base. Every dollar in the rate base earns that regulated return, year after year, until the asset is retired.

The infrastructure modernization opportunity is massive. Much of America's gas distribution system dates to the post-WWII boom or earlier. Cast iron pipes installed when Eisenhower was president need replacement. Electronic sensors and automated shut-offs that could have prevented the Massachusetts disaster need installation. The Infrastructure Investment and Jobs Act of 2021 provided federal support for exactly these kinds of projects.

But the real growth driver is the energy transition itself. Replacing a coal plant with wind and solar plus battery storage doesn't just reduce emissions—it creates rate base growth. A 500 MW solar farm might cost $500 million. Add battery storage, transmission upgrades, and grid integration, and you're talking about a billion-dollar investment opportunity that will earn regulated returns for decades.

The gas distribution business presents a different challenge. NiSource is fortunate to have access to a plentiful supply of low-cost natural gas to include as part of our evolving energy mix. Natural gas not only supports the transition by serving as a feedstock to help satisfy demand as we deploy new energy technologies, but also provides the infrastructure to support the distribution of other fuels such as hydrogen, renewable natural gas and greener fuels blended with natural gas.

This is delicate positioning. Environmental advocates want gas eliminated entirely. But NiSource argues—and many regulators agree—that gas remains essential for reliability, especially during polar vortexes when renewable generation can't meet peak heating demand. The company is hedging by experimenting with hydrogen blending and renewable natural gas, trying to future-proof their gas infrastructure.

NiSource is conducting a multi-phase hydrogen blending project as a potential way to enhance our customers' sustainability and provide a safe, reliable and renewable energy source for years to come. Phase 1 is being conducted at NiSource's Columbia Gas of Pennsylvania Training Center's Safety Town in Monaca, Pa., to determine the optimal blend percent that could be introduced into the natural gas distribution system. Columbia Gas of Pennsylvania partnered with EN Engineering to build a hydrogen blending skid that mixes hydrogen with natural gas into Safety Town's distribution system at various percentages, ranging from 2 to 20 percent.

The financial engineering is as important as the physical engineering. NiSource maintains investment-grade credit ratings—crucial for accessing capital markets at reasonable rates. They've structured their business to generate steady cash flows that cover dividends and fund growth investments. They've eliminated commodity exposure, weather normalization smooths out seasonal variations, and regulatory mechanisms allow for timely recovery of costs.

This model creates a virtuous cycle. Stable returns attract capital. Capital funds infrastructure investment. Infrastructure investment improves service and reliability. Better service pleases regulators. Happy regulators approve rate increases. Rate increases generate returns. Returns attract more capital.

The challenge is execution. Every project must come in on budget—cost overruns often can't be recovered from ratepayers. Every rate case must be carefully managed—ask for too much and regulators push back, ask for too little and you leave money on the table. Every safety incident risks not just lives but the regulatory compact itself.

NiSource has also discovered an unexpected benefit of their renewable transformation: customer satisfaction. Solar and wind projects are visible symbols of progress. Customers who might resist rate increases for maintaining old coal plants are more accepting when they see wind turbines spinning and solar panels gleaming. The company that was literally run out of Massachusetts has become a model for utility transformation.

The numbers tell the story. From 2021 to 2024, NiSource invested over $8 billion in infrastructure. Rate base grew from $11 billion to over $16 billion. Regulated returns remained stable. The stock price nearly doubled. For a business model that many consider obsolete, the regulated utility framework—properly executed—continues to generate impressive returns.

VIII. Playbook: Lessons in Regulated Returns

If you want to understand how to run a regulated utility in the 21st century, study NiSource's playbook from 2015 to present. Not because they got everything right—Massachusetts proves otherwise—but because they've demonstrated how to transform crisis into opportunity within one of capitalism's most constrained business models.

Lesson One: Master the Regulatory Game

Utilities don't compete in markets; they perform in regulatory theaters. Each state public utility commission has its own culture, priorities, and politics. Indiana values economic development and industrial competitiveness. Ohio focuses on reliability and gradual modernization. Pennsylvania emphasizes safety after years of pipeline incidents. Virginia balances environmental goals with affordability concerns.

NiSource maintains separate regulatory teams for each state, staffed with locals who understand the nuances. They file rate cases strategically—never too many at once, always with compelling narratives about safety and modernization. They settle rather than litigate when possible, understanding that today's adversary in a rate case is tomorrow's partner in a infrastructure program.

The company has learned to speak different languages to different audiences. To environmentalists: "We're retiring coal and building renewables." To industrial customers: "We're maintaining reliability and controlling costs." To regulators: "We're modernizing infrastructure and enhancing safety." All true, all part of the same strategy, but emphasized differently depending on the audience.

Lesson Two: Capital Allocation as Competitive Advantage

In a normal business, you allocate capital to the highest return opportunities. In a regulated utility, returns are fixed—so you allocate capital to the opportunities most likely to be approved and included in rate base. This requires deep understanding of regulatory priorities and political winds.

NiSource's capital allocation framework is elegant. Priority one: safety and compliance investments that prevent another Massachusetts. These are almost always approved. Priority two: renewable generation that replaces retiring coal plants. Regulators want clean energy, and replacement generation is essential. Priority three: grid modernization that enables distributed resources and improves reliability. Priority four: growth investments to serve new load.

They've also mastered the art of capital recycling. The Columbia Pipeline spinoff generated billions in value that could be redeployed into regulated investments. Asset sales, like the forced sale of Massachusetts gas operations, free up capital for higher-return opportunities elsewhere. Even disaster settlements can be structured to minimize cash impact while addressing stakeholder concerns.

Lesson Three: Crisis Response Determines Survival

The Massachusetts explosions could have destroyed NiSource. Other utilities have been broken up or bankrupted by similar disasters—think Pacific Gas & Electric and California wildfires. NiSource survived because they responded with radical transparency and accountability.

They didn't hide behind lawyers or public relations firms. CEO Joe Hamrock personally went to Massachusetts, met with victims, accepted responsibility. They agreed to sell the business and leave the state—unprecedented for a utility. They implemented every safety recommendation across all operations, not just where required.

This response transformed potential existential threat into reputation rehabilitation. Regulators in other states saw a company that took responsibility and fixed problems. Investors saw management that could handle crisis. Communities saw a utility that put safety first, even at enormous cost.

Lesson Four: Long-term Thinking in Short-term Markets

Wall Street wants quarterly earnings growth. Utilities plan in decades. NiSource has bridged this gap by providing clear, long-term strategic frameworks while delivering consistent near-term results.

Their 2018 announcement of coal retirement by 2028 gave a ten-year runway. Investors could model the transformation. Regulators could plan for transition. Communities could prepare for change. Employees could retrain or retire. By telegraphing moves years in advance, NiSource eliminated surprise and built consensus.

They've also learned to use market volatility to their advantage. When natural gas prices spike, their regulated model means they pass costs through to customers—no commodity risk. When renewable costs plummet, they lock in long-term contracts and power purchase agreements. When interest rates rise, their regulated returns adjust upward through rate cases.

Lesson Five: ESG as Core Strategy, Not Marketing

Environmental, Social, and Governance (ESG) considerations have become central to NiSource's strategy—not because they're fashionable, but because they align with the regulatory compact. Environmental improvements please regulators and communities. Social programs—workforce development, supplier diversity, community investment—build political capital. Governance improvements reduce regulatory risk.

The renewable transformation exemplifies this integration. It's simultaneously an environmental win (reduced emissions), social benefit (clean air for communities), and governance improvement (alignment with state policy goals). The fact that it also happens to be economically optimal makes it irresistible to all stakeholders.

Lesson Six: The Power of Predictability

In a world of disruption, NiSource sells stability. Regulated returns. Essential services. Inflation-protected revenues. Dividend growth. This predictability attracts a specific investor base—pension funds, insurance companies, retirees—who value consistency over excitement.

Management has learned to under-promise and over-deliver. Guidance is conservative. Surprises are positive. Dividends grow steadily but not aggressively. This predictability creates a virtuous cycle: stable stock price reduces cost of capital, which improves returns, which attracts more conservative investors, which further stabilizes the stock price.

Lesson Seven: Technology as Enabler, Not Disruptor

While tech companies talk about disrupting utilities, NiSource quietly deploys technology to enhance their regulated model. Smart meters enable time-of-use pricing and demand response. Grid sensors prevent outages and improve reliability. Renewable generation and battery storage reduce costs while meeting environmental goals.

But they've learned from Massachusetts that technology without process is dangerous. Every new system requires training, procedures, and fail-safes. Innovation happens incrementally, not revolutionarily. The goal isn't to be cutting-edge but to be competently modern.

The NiSource playbook isn't revolutionary. It's evolutionary refinement of a business model that's existed for a century. But in an era of disruption, sometimes the best strategy is to perfect what already works rather than chase what might work. For investors seeking regulated returns in an unregulated world, NiSource offers a masterclass in execution within constraints.

IX. Bear vs. Bull Case & Valuation

The Bull Case: Infrastructure Renaissance Meets Energy Transition

Bulls see NiSource as perfectly positioned for the next decade. Start with the math: $40 billion in long-term infrastructure investment opportunities over 20 years. Not hoped-for, might-happen investments, but necessary replacements and upgrades that regulators must approve because the alternative is system failure.

The energy transition isn't a risk—it's an accelerant. Every coal plant retired creates opportunity to build renewables. Every renewable project needs transmission upgrades, grid stabilization, and backup resources. Battery storage is moving from experiment to essential. The Infrastructure Investment and Jobs Act provides federal support. The Inflation Reduction Act extends renewable tax credits. State mandates require clean energy. NiSource is surfing a tsunami of supportive policy.

Their regulatory relationships are sterling (Massachusetts notwithstanding). Six states provide diversification—a bad decision in one jurisdiction won't sink the company. The territories are constructive: Midwest industrial states that understand utilities need returns to attract capital. No California-style politics. No New York-style activism.

The competitive position is actually strengthening. Scale matters more as complexity increases. Small municipal utilities can't manage renewable integration, hydrogen experiments, and cybersecurity simultaneously. Consolidation opportunities will emerge. NiSource, with its simplified structure and strong balance sheet, can be an acquirer.

Customer growth is accelerating after decades of stagnation. Data centers need massive power for AI computing. Electric vehicles need charging infrastructure. Building electrification shifts heating from gas to electric. Renewable manufacturing—solar panels, batteries, wind turbines—requires reliable power. The Midwest's manufacturing renaissance drives industrial demand.

Valuation remains reasonable. Utilities trade at 16-18x forward earnings, in line with historical averages despite dramatically improved growth prospects. NiSource's premium to peers reflects superior execution but remains modest. Dividend yield of 3-4% provides cushion while waiting for growth.

The hidden option value is enormous. Hydrogen could transform gas infrastructure from stranded asset to essential bridge. Carbon capture could extend gas plant life. Small modular reactors could provide baseload clean power. NiSource doesn't need any of these to work, but if even one does, the upside is substantial.

The Bear Case: Regulatory Roulette in a Decarbonizing World

Bears see existential threats everywhere. Start with the fundamental contradiction: NiSource operates gas distribution networks in a world moving toward electrification. Those 37,200 miles of pipeline could become stranded assets. Recovery might be denied. Write-offs could be massive.

Regulatory risk is real and growing. Public utility commissions are political bodies. Populist backlash against rate increases is building as inflation persists. Every polar vortex that drives bills higher creates pressure for regulatory intervention. The Massachusetts disaster proves that one incident can destroy decades of relationships.

Execution risk on the renewable transition is substantial. The company's plans to retire its coal units by 2023 could be postponed, as it foresees up to 18 months of delays in new solar deployments. Solar projects originally scheduled for completion in 2022 and 2023 could experience six to 18 months of delays. Supply chain disruptions continue. Interconnection queues stretch for years. Transmission constraints limit renewable deployment. Cost overruns can't always be recovered.

Competition is evolving in dangerous ways. Distributed energy resources—rooftop solar, home batteries, microgrids—let customers defect from the grid. Community solar programs socialize benefits while utilities bear costs. Tech companies are building their own power resources. The utility monopoly isn't what it used to be.

Capital intensity is reaching dangerous levels. NiSource previously laid out plans to invest up to $10.6 billion from 2021 through 2024. That's real money that must be raised in capital markets. Interest rates have risen. Credit spreads have widened. If capital markets close, even temporarily, utilities can't function.

The renewable economics that drove transformation are deteriorating. Solar panel costs are rising due to trade disputes. Wind turbine availability is constrained. Battery costs aren't falling as fast as projected. Grid integration costs are higher than modeled. The easy renewable wins have been captured.

Climate adaptation costs aren't fully recognized. Polar vortexes stress gas systems. Derechos destroy transmission lines. Floods threaten generation stations. Droughts reduce hydro output. The infrastructure built for yesterday's climate won't survive tomorrow's extremes.

Technology disruption remains a threat. Fusion power could make current infrastructure obsolete. Solid-state batteries could enable complete grid defection. Quantum computing could revolutionize grid management in ways incumbents can't match. Utilities are always one breakthrough away from obsolescence.

Valuation: Priced for Perfection or Reasonably Valued?

At current levels, NiSource trades at approximately 17x forward earnings, a 10% premium to the utility sector average. The dividend yield of 3.5% is slightly below the sector's 3.8% average, reflecting higher growth expectations. Price-to-book ratio of 1.8x suggests the market values the regulatory franchises above replacement cost.

The key question: does successful execution of the renewable transition justify premium valuation? Bulls argue yes—NiSource has proven it can transform its business model while maintaining regulatory relationships. Bears argue no—the easy gains have been captured and future growth requires flawless execution in an increasingly complex environment.

Discounted cash flow models suggest fair value depends entirely on assumptions about allowed returns, capital deployment, and regulatory recovery. A 50-basis-point change in allowed ROE swings valuation by 15%. A one-year delay in renewable deployment reduces value by 5%. A adverse regulatory decision in any major jurisdiction could cut value by 10-20%.

Relative valuation provides little clarity. Compared to pure-play renewable developers, NiSource looks cheap. Compared to traditional utilities, it looks expensive. Compared to pipeline companies (its former business), it looks fairly valued. The company defies easy categorization.

Perhaps the most honest assessment: NiSource is a bet on American infrastructure renewal and energy transition, executed through the regulated utility model. If you believe America will modernize its energy infrastructure, decarbonize responsibly, and maintain the regulatory compact, NiSource is attractively valued. If you believe any of those assumptions will break, the stock is priced for disappointment.

For long-term fundamental investors, the question isn't whether NiSource can navigate the energy transition—they're already doing it. The question is whether the regulated utility model itself survives the transition. NiSource is betting it not only survives but thrives. The next decade will determine if they're right.

X. Looking Forward: The Next Energy Era

The year is 2035. A NiSource customer in Fort Wayne, Indiana, wakes up in a home heated by an electric heat pump powered by wind energy from turbines in Benton County. Their electric vehicle charges overnight using battery-stored solar power. Their stove runs on a blend of renewable natural gas and green hydrogen flowing through pipes first laid in 1962. Their electricity bill is lower, in inflation-adjusted terms, than it was in 2024. This isn't science fiction—it's NiSource's strategic plan.

The utility industry stands at an inflection point more dramatic than any since Edison and Westinghouse battled over AC versus DC power. The next decade will determine whether incumbent utilities lead the energy transition or become casualties of it. NiSource's positioning—post-coal, post-pipeline, post-crisis—makes it a fascinating laboratory for utility transformation.

Start with hydrogen, the most hyped and least understood opportunity. NiSource is exploring hydrogen as a potential source in a future energy mix through participation in several federal funding opportunities within the Department of Energy's Hydrogen Hub program and other company-initiated pilot programs. NiSource is conducting a multi-phase hydrogen blending project as a potential way to enhance our customers' sustainability and provide a safe, reliable and renewable energy source for years to come.

The physics are compelling: hydrogen can be produced from renewable electricity through electrolysis, stored indefinitely, and burned without carbon emissions. The economics are challenging: green hydrogen costs 3-5x more than natural gas. The infrastructure questions are existential: can existing pipelines handle hydrogen's different properties? NiSource's experiments will help answer these questions.

Grid modernization presents more immediate opportunities. The traditional grid was designed for one-way power flow from large generators to passive consumers. Tomorrow's grid must handle two-way flows, with every rooftop solar panel a potential generator, every electric vehicle a potential battery, every smart appliance a potential demand response resource.

NiSource is investing billions in grid intelligence—sensors that detect problems before they cause outages, software that optimizes power flows in real-time, automation that reroutes power around damaged sections. This isn't sexy technology, but it's essential for renewable integration. When clouds suddenly cover a solar farm, the grid must instantly compensate. When wind dies at sunset just as EV charging peaks, something must fill the gap.

Data centers represent a wild card opportunity. AI computation requires massive, reliable, always-on power—exactly what utilities provide. A single large data center can consume as much electricity as a small city. Microsoft, Google, and Amazon are building data centers across the Midwest, drawn by cheap land, cool climate, and distance from coastal climate risks. Each facility represents hundreds of millions in rate base investment for interconnection and transmission upgrades.

The electrification megatrend could revive load growth after decades of stagnation. Electric vehicles are just the beginning. Industrial processes are electrifying—steel production using electric arc furnaces, chemical production using electric heating, even cement production using electric kilns. Buildings are electrifying—heat pumps replacing gas furnaces, induction stoves replacing gas ranges, electric water heaters replacing gas boilers.

But electrification creates a paradox for NiSource: growing electric demand while potentially stranding gas assets. Their response is pragmatic—embrace electrification where it makes sense while positioning gas infrastructure for molecular energy carriers like hydrogen and renewable natural gas. Natural gas provides the infrastructure to support the distribution of other fuels such as hydrogen, renewable natural gas and greener fuels blended with natural gas.

Climate adaptation will require massive investment regardless of mitigation success. The infrastructure built for Indiana's historical climate—moderate summers, cold but not extreme winters—must be hardened for weather volatility. Transmission lines must withstand derechos. Substations must survive flooding. Gas systems must maintain pressure during polar vortexes. Each upgrade creates rate base opportunity.

The regulatory compact itself is evolving. Performance-based ratemaking rewards outcomes (reliability, customer satisfaction, emission reductions) rather than just investment. Revenue decoupling breaks the link between sales volume and profits, enabling utilities to promote efficiency. Regulatory innovation could accelerate or constrain NiSource's transformation.

What would we do if we were running NiSource? Double down on the energy transition while hedging bets. Accelerate renewable deployment to lock in tax credits and leading competitive positions. Modernize gas infrastructure for hydrogen compatibility while acknowledging some assets will be stranded. Build optionality through strategic partnerships with tech companies, renewable developers, and industrial customers. Maintain financial flexibility for opportunistic acquisitions as smaller utilities struggle with transition costs.

Most importantly, we'd recognize that utilities are ultimately political entities operating social contracts. The path forward requires not just technical execution but social legitimacy. Every rate increase must be justified. Every investment must benefit communities. Every decision must balance competing stakeholder interests.

The next decade will test whether NiSource's transformation from coal-dependent laggard to renewable leader was a one-time pivot or the beginning of continuous adaptation. The company that survived Massachusetts explosions and thrived through coal retirement faces new challenges: accelerating electrification, emerging technologies, evolving regulations, and changing customer expectations.

But NiSource has advantages. They've proven they can transform. They've simplified their structure. They've strengthened their balance sheet. They've rebuilt their reputation. They operate in states that need economic development and will support reasonable utility investment. They serve regions where renewable resources are abundant and interconnection is feasible.

The bear case is that utilities are dinosaurs awaiting extinction by distributed resources and technological disruption. The bull case is that society needs someone to orchestrate the energy transition, maintain reliability during transformation, and ensure universal service regardless of economics. NiSource is betting that "someone" remains the regulated utility, evolved for a new era but still essential.

XI. Recent News

The most recent developments at NiSource demonstrate a company hitting its operational stride while navigating an increasingly complex energy landscape. NiSource reported full-year 2024 non-GAAP adjusted net income available to common shareholders of $798.6 million, or $1.75 of adjusted EPS compared to non-GAAP adjusted net income available to common shareholders of $716.3 million, or $1.60 of adjusted EPS, for the same period of 2023. This represents a 9.4% year-over-year increase, exceeding the top end of guidance ranges.

Looking forward, NiSource is raising 2025 non-GAAP adjusted EPS guidance to $1.85-$1.89. The base capital expenditure plan is increased to $19.4 billion, a $100 million increase versus the prior $19.3 billion. This is expected to result in 8%-10% rate base growth and non-GAAP adjusted EPS growth of 6%-8% annually for the 2025-2029 period.

CEO Lloyd Yates emphasized the company's execution track record: "We continue our track record of strong financial growth achieving 2024 non-GAAP EPS of $1.75, delivering an 8.5% 3-year compound annualized growth rate." This performance is particularly notable given the challenges of managing a massive infrastructure transformation while maintaining service reliability.

The renewable transition continues to progress. "During the second quarter NiSource placed the Cavalry Solar & Storage project into service and reported strong earnings results, executing our investment plan and delivering consistent shareholder returns." This 200 MW solar facility with 45 MW of battery storage represents another milestone in the company's coal-to-renewables transformation.

Regulatory progress remains steady across jurisdictions. "We are making progress in our rate cases, advanced NIPSCO Integrated Resource Plan (IRP) dialogue and received approvals for several Indiana investments that will improve reliability and lower costs to customers." The constructive regulatory environment continues to support the company's aggressive investment plans.

Perhaps most significantly, NiSource is positioning itself for potential hypergrowth from data centers and AI-driven electricity demand. Management's comments during recent earnings calls reveal careful preparation for what could be transformative load growth, with enhanced balance sheet flexibility and regulatory mechanisms designed to accommodate rapid infrastructure expansion.

The company's operational excellence is reflected in customer satisfaction metrics, with four of our operating companies were rated "easiest to do business with" in Escalent's 2025 Trusted Brand & Customer Engagement: Residential report. This represents a remarkable turnaround for a company that just six years ago was synonymous with disaster in Massachusetts.

Financial strength continues to improve, with over $2 billion in balance sheet improvements through 2023-2024, positioning the company to fund its ambitious capital program while maintaining investment-grade ratings. The dividend remains secure with modest growth, currently yielding approximately 3.5%.

XII. Outro & Links

The NiSource story is ultimately about transformation within constraints—how a 175-year-old utility reinvented itself not by abandoning its core business model but by perfecting it for a new era. From the gas-lit streets of 1847 Indiana to today's wind turbines and solar farms, from the Massachusetts disaster to industry-leading safety scores, from coal dependency to renewable leadership, NiSource has demonstrated that even the most traditional businesses can evolve.

What makes this transformation remarkable isn't its speed—utilities don't do anything quickly—but its thoroughness. NiSource didn't just swap coal for solar; they reimagined what a utility could be. They simplified complex corporate structures, divested non-core assets, doubled down on safety, and aligned their business model with societal goals around climate change.

The investment thesis remains compelling for patient capital. The regulatory compact, often seen as a constraint, provides NiSource with something increasingly rare in modern capitalism: predictability. In a world of disruption, NiSource offers the radical proposition that some things—delivering energy, maintaining infrastructure, serving communities—remain essential and valuable.

The risks are real. Stranded gas assets, regulatory backlash, execution challenges on renewable deployment, and technological disruption all threaten the traditional utility model. But NiSource has proven remarkably adaptive, turning crisis into opportunity, constraints into competitive advantages.

For investors seeking exposure to the energy transition without the volatility of pure-play renewable developers or the obsolescence risk of fossil fuel companies, NiSource offers a middle path. It's a bet that America will need massive infrastructure investment, that the energy transition will happen gradually rather than suddenly, and that somebody needs to keep the lights on during the transformation.

The next decade will test whether NiSource's transformation was the beginning of continuous adaptation or a one-time pivot. Data center demand, hydrogen economics, regulatory evolution, and climate adaptation will all shape the company's trajectory. But if the past decade is any guide, NiSource will continue doing what utilities do best: slowly, steadily, reliably delivering essential services while earning regulated returns.

In the end, NiSource proves that sometimes the most revolutionary act isn't disruption but evolution—taking a business model perfected over centuries and adapting it for centuries more. For a company that began laying pipes when gas lights were cutting-edge technology, leading America's renewable energy transition is just another chapter in a very long story.

For Further Research:

- NiSource Investor Relations: nisource.com/investors

- NIPSCO "Your Energy, Your Future" Initiative: nipsco.com/future

- Sierra Club "Dirty Truth" Report (2024): Analysis of utility clean energy transitions

- Columbia Gas Massachusetts Incident Investigation: National Transportation Safety Board Report

- Indiana Utility Regulatory Commission: Integrated Resource Plan filings and rate case dockets

- EIA State Energy Profiles: Energy infrastructure and consumption data for NiSource service territories

- S&P Global Market Intelligence: Utility sector analysis and regulatory tracking

- Edison Electric Institute: Industry statistics and utility transformation case studies

Key Regulatory Filings:

- NiSource 10-K Annual Reports (2019-2024)

- NIPSCO Integrated Resource Plans (2018, 2021, 2024)

- Rate case testimonies across six state jurisdictions

- Columbia Pipeline Group separation documents (2015)

- Massachusetts Department of Public Utilities settlement agreements (2020)

Books for Context:

- "The Grid" by Gretchen Bakke - Understanding America's electricity infrastructure

- "Natural Gas and Geopolitics" edited by David G. Victor et al. - Pipeline economics and energy security

- "The Quest" by Daniel Yergin - Energy transitions throughout history

- "Confessions of a Radical Industrialist" by Ray Anderson - Corporate transformation and sustainability

This story continues to unfold. Every rate case decision, every renewable project completion, every quarterly earnings call adds another data point to understanding whether NiSource's transformation represents the future of utilities or a successful but ultimately unique adaptation. For investors, regulators, and communities across the Midwest, the answer matters enormously.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube