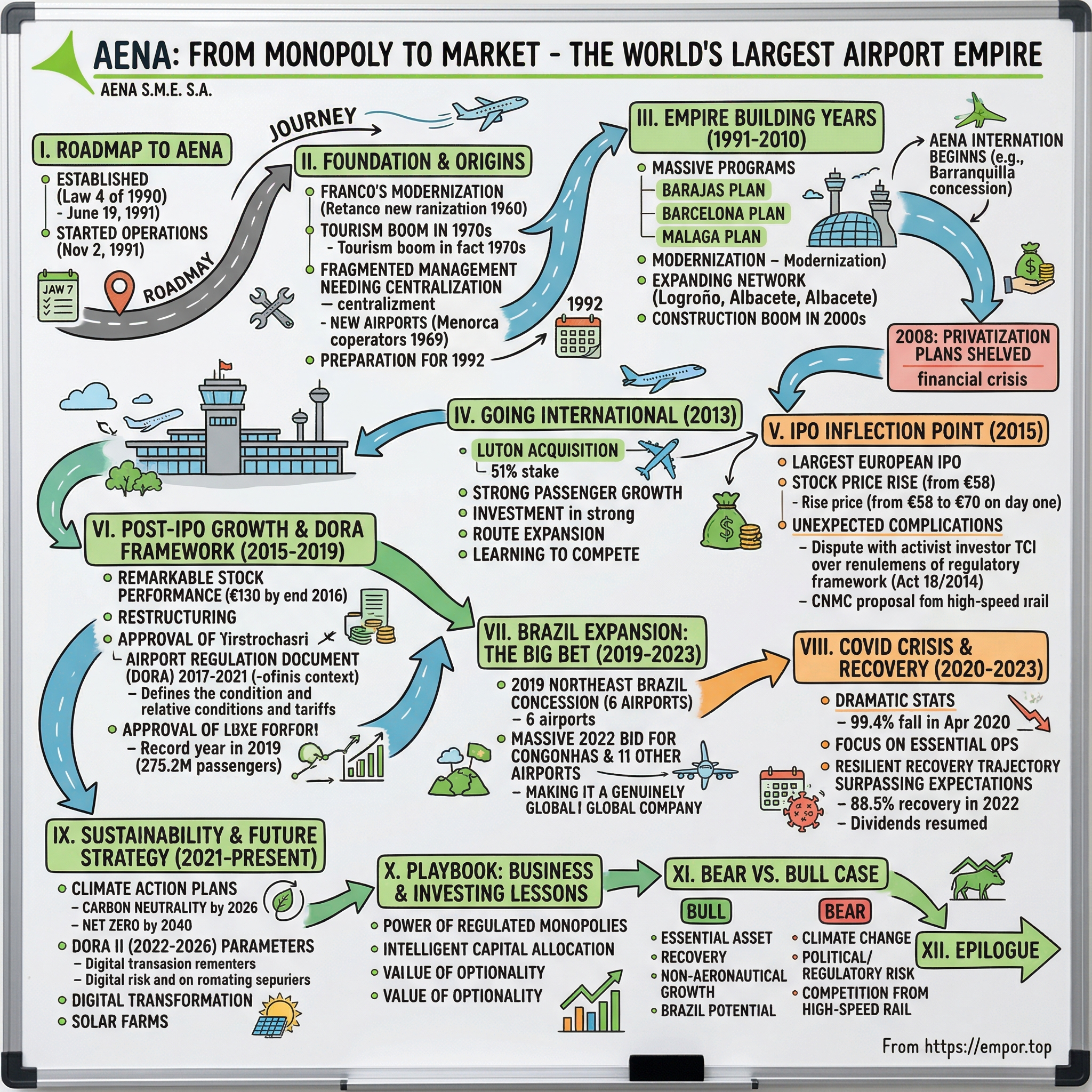

Aena: From Monopoly to Market - The World's Largest Airport Empire

I. Introduction & Episode Roadmap

Picture this scene: it's February 11, 2015, and the trading floor at the Madrid Stock Exchange erupts in a frenzy of activity. Spain's airport operator Aena, a company that just months earlier many thought would never see the public markets, is making its debut. The IPO closed with a share price increase of approximately 21% in the first day of trading from €58 to €70, transforming a sleepy state monopoly into Europe's hottest stock.

How did a Spanish government entity, born from the bureaucratic machinery of a post-Franco state, become the world's largest airport operator? This is the story of Aena—a company that manages more passengers annually than any other airport operator on the planet, controls Europe's most extensive airport network, and somehow maintains profitability while operating remote airfields in Spain's smallest towns.

The narrative ahead takes us from the dying days of Francisco Franco's dictatorship through Spain's democratic transition, into the country's construction boom, through a devastating financial crisis, and ultimately to one of Europe's most successful privatizations. We'll explore how Aena built its empire brick by brick, from its birth under Article 82 of Law 4 of 1990 on the General State Budget, effectively established on June 19, 1991, and beginning operations at airports on November 2, 1991, to managing a network that today spans continents.

Along the way, we'll uncover the tensions between public service and private profit, the battle with activist investors over regulatory frameworks, and the audacious international expansion that saw a Spanish operator take control of London's fifth-busiest airport and Brazil's second-largest air hub. This is a story of transformation, ambition, and the delicate dance between government control and market forces.

II. Foundation & Origins: Building Modern Spain (1927-1991)

The roots of Spain's modern aviation infrastructure stretch back to a very different era. Madrid's Barajas Airport was constructed in 1927, opening to domestic and international air traffic on April 22, 1931, just as Spain's Second Republic was finding its feet. But the real transformation of Spanish aviation would come decades later, shaped by two powerful forces: Franco's authoritarian modernization efforts and the explosion of mass tourism.

During the Franco years, Spanish aviation existed in a peculiar state—simultaneously isolated from much of Europe yet increasingly vital to the regime's economic survival. By the 1970s, large jets were landing at Barajas, and the growth of traffic mainly as a result of tourism exceeded forecasts. At the beginning of the decade, the airport reached 1.2 million passengers, double that envisaged in the Plan of Airports of 1957. In the 1970s, with the boom in tourism and the arrival of the Boeing 747, the airport reached 4 million passengers.

The transformation wasn't limited to Madrid. Across Spain's Mediterranean coast and island territories, a parallel revolution was underway. On March 24, 1969, the new Menorca Airport was inaugurated in its current location. The opening of the new airport marked the start of a real tourist boom for the island. The number of passengers that passed through the Menorca aerodrome doubled in two years. While in 1968, 112,000 travellers used the old San Luis Aerodrome, in 1970 a total of 239,000 passed through the new facilities. The rise in tourism in the 70s made it necessary to carry out improvements to the terminal.

The fragmented nature of Spanish airport management—with different airports operating under various authorities and standards—was becoming increasingly untenable. By the late 1980s, as Spain prepared for its grand coming-out party with the 1992 Barcelona Olympics and Seville Expo, the need for centralized, professional airport management was undeniable.

The creation of Aena is associated with the process of liberalisation and market access that took place at the end of the 1980s in European international air transport. In the first decade since it began to provide airport services, on November 2, 1991, Aena began an extensive and complete modernisation of Spanish airport and air navigation facilities, placing the airports at the forefront of neighbouring countries.

The formal establishment of Aena represented more than administrative tidying—it was a recognition that airports had become too important to Spain's economy to be managed as afterthoughts. Tourism was no longer a pleasant bonus but the lifeblood of entire regions. The company inherited a mixed bag: gleaming international gateways in Madrid and Barcelona, bustling tourist airports along the coasts, and numerous small regional facilities that would never turn a profit but were deemed essential for territorial cohesion.

Aena International was created as Aena's vehicle for its business development objectives outside Spain. A year earlier, it made its first foray into the international arena by starting international activity directly with the concession contract for the Barranquilla airport (Colombia). Even in its infancy, the organization was thinking beyond Spain's borders.

III. The Empire Building Years (1991-2010)

The newly formed Aena faced an immediate test: preparing Spain's airports for the dual showcase events of 1992—the Barcelona Olympics and Seville's Universal Exposition. These weren't just sporting and cultural events; they were Spain's declaration that it had arrived as a modern European nation. The airports would be the first impression for millions of visitors.

From 1990, Barcelona-El Prat Airport faced the challenge of absorbing all of the traffic expected for 1992, the year the Olympic Games were held in Barcelona. In 1990, the new service building was inaugurated; in 1992, the passenger terminal extension began providing service (terminal B), along with the new terminals A and C, which included the first 24 positions with direct access to the aircraft through airbridges. That year there were over 10 million passengers.

But the real transformation came with three massive infrastructure programs that would reshape Spanish aviation: the Barajas Plan, Barcelona Plan & Malaga Plan. These weren't mere expansions—they were complete reimaginings of what Spanish airports could be.

The scale of ambition was staggering. Barajas would gain a new terminal designed by Richard Rogers and Antonio Lamela that would become one of the world's architectural marvels. Barcelona would be transformed into a hub capable of competing with Europe's giants. Málaga would be positioned as the gateway to the Costa del Sol's tourism empire.

In the same decade, the airports of Logroño, Albacete, Burgos and Huesca-Pirineos and the heliports of Ceuta and Algeciras were opened to air traffic, making up the most important network of airports in the international sphere. This expansion reflected a uniquely Spanish challenge: maintaining connectivity to remote regions regardless of economic viability.

After the completion of the liberalisation process of intra-European air transport, promoted by the EU, Aena fostered effective competition in ground handling, with the incorporation of several handling agents, facilitated the entry into the market of numerous airlines and watched how new low-cost companies in Europe emerged first-hand. And both generated rates of growth in air traffic in Europe that lasted until the middle of the first decade of the 21st century and for which Aena's structure was prepared.

The 2000s brought Spain's construction boom, and airports weren't immune to the fever. Regional politicians lobbied for their own airports as symbols of progress and modernity. Some, like Ciudad Real's ghost airport (built privately, not by Aena), would become infamous white elephants. But Aena's network expansion, while ambitious, remained mostly grounded in operational logic rather than political vanity.

By 2008, discussions about privatization were already underway. The Spanish Cabinet had approved a partial privatization plan that would have seen private investors take up to 30% of the company. But then came Lehman Brothers' collapse, and with it, Spain's economic miracle turned into a nightmare. The privatization plans were shelved as the country entered its deepest recession in decades.

IV. The Luton Acquisition: Going International (2013)

As Spain remained mired in economic crisis in 2013, Aena made a move that surprised many observers: On November 27, 2013, Aena Internacional and Aerofi SàRL ("Aerofi"), subsidiary of Ardian (formerly AXA Private Equity), acquired the concessionaire of London-Luton Airport in the United Kingdom. Aena Internacional currently has a 51% stake in the company's capital.

The acquisition of London Luton Airport wasn't just about adding another facility to the portfolio. The consortium of Aena (51%) and Ardian (49%) reached financial close on its acquisition of London Luton Airport for a consideration of £394.4 million ($647 million). This was Aena's first controlled international asset, a crucial testing ground for whether the Spanish operator could succeed outside its home market.

The new owners were attracted to the airport because of its strong growth in passenger numbers, which increased from 3.4 million in 1998 to the current ten million. The passenger numbers are expected to further increase following the implementation of a plan submitted to the Luton Borough Council to expand and improve the airport.

The timing seemed counterintuitive. Spain was still reeling from its economic crisis, youth unemployment exceeded 50%, and Aena itself was undergoing painful restructuring. Yet here was the Spanish operator, partnering with a French private equity firm to buy a British airport. The strategic logic, however, was compelling. Luton offered something Aena desperately needed: proof that it could operate successfully in a competitive, deregulated market.

Under Aena and Ardian's ownership, Luton underwent a remarkable transformation. Since 2013, Ardian together with leading airport operator Aena invested heavily in developing the airport, committing over £160 million in total. As a result, the airport has been transformed and passenger numbers increased from 9.7 million in 2013 to 15.8 million in 2017, making LLA one of the UK's fastest growing airports.

The Luton experience taught Aena valuable lessons about operating in a market where airports actually compete for passengers and airlines. Unlike in Spain, where Aena controlled virtually every commercial airport, in London it had to fight for market share against Heathrow, Gatwick, Stansted, and London City. The company learned to be more commercially aggressive, more responsive to airline needs, and more innovative in its retail offerings.

The airport's route network substantially increased since Ardian and Aena invested in 2013, now serving over 140 destinations across Europe, Asia and Africa. The strong performance of the airport over the last four and a half years has seen the creation of 3,000 direct and indirect jobs.

V. The IPO Inflection Point (2015)

The road to Aena's IPO was paved with political calculation, financial necessity, and more than a little drama. Spain's economy in 2014 was slowly emerging from its deepest recession in decades. The government needed to signal that Spain was open for business again, that international investors could trust Spanish assets.

Aena was hit hard by Spain's economic downturn and underwent a massive overhaul, which included firing 20% of its workers and a rise in airport taxes that helped restore it back to financial health. The company reported a net profit of 596.7 million euros for 2013, emerging from a net loss of 63.5 million euros the previous year.

The privatization process itself became a masterclass in expectation management—or perhaps mismanagement. The government set a minimum price for the IPO of €22 per share, the institutional investors who were acting as anchors offered prices in the range of €50-55, and the final IPO price was approximately €60 per share. This extraordinary spread between the government's floor price and what investors were actually willing to pay raised eyebrows across European capital markets.

The Spanish government actively encouraged foreign investment through this process, and because of the support of TCI and other international investors, the IPO of Aena in February 2015 was a major success. It was the largest IPO in Spain since the financial crisis, and signaled that Spain was able to attract foreign investment to drive economic growth.

Aena was partially privatized through an initial public offering in February 2015. This IPO was the largest in Europe and the fourth largest worldwide that year. The first day of trading set the tone for what was to come—explosive growth that would confound skeptics and enrich early investors.

But the IPO brought unexpected complications. According to the existing framework (Act 18/2014), the tariff charges paid by airlines to Aena to reimburse Aena for the airline's share of airport costs, will be frozen for the next 10 years. This regulatory framework, which had been a selling point for the IPO, would soon become a battlefield.

Enter Chris Hohn and The Children's Investment Fund (TCI), one of the world's most successful activist investors. TCI had taken a significant stake during the IPO, becoming Aena's largest private shareholder with 7.7% of the company. What followed was a regulatory drama that would test the boundaries of Spain's commitment to private investors.

On Monday (May 18, 2015) the Children's Investment Fund (TCI) filed an administrative appeal against Spain's National Commission for Markets and Competition (CNMC) before the National High Court. After filing its action against the supervisor, TCI said that 'the CNMC proposal poses very serious economic effects for both Aena and its shareholders'.

The dispute centered on how airport costs should be allocated between Aena and airlines. Should the CNMC succeed in its efforts, Aena and its shareholders, including the Spanish government which owns 51% of Aena, would suffer material damages that could exceed €1 billion. The CNMC's proposed methodology would boost airline profits at the expense of Aena.

This wasn't just a technical regulatory dispute—it was a test case for whether Spain could be trusted to maintain stable rules for privatized companies. TCI's very public fight, unusual for Spanish capital markets, sent a clear message: international investors wouldn't quietly accept regulatory changes that undermined their investments.

VI. Post-IPO Growth & DORA Framework (2015-2019)

The post-IPO years saw Aena's transformation from a sleepy quasi-governmental entity into a stock market darling. At the end of 2016, the price increased to €130 per share, more than doubling from the IPO price in less than two years. Since TCI entered Aena in February 2015, both 2015 and 2016 had been extraordinary years. The stock price had increased from €58 (at the IPO date) to nearly €130 at 2016 year-end.

This remarkable performance wasn't just financial engineering or market exuberance. Aena was fundamentally restructuring how it operated, squeezing more revenue from every passenger while keeping costs under tight control. The company discovered that Spanish airports had been dramatically under-monetized compared to international peers, particularly in retail and commercial activities.

On January 27, 2017, the Council of Ministers approved the Airport Regulation Document (DORA), which sets out the conditions to be met by airports on the Aena network for the period 2017-2021. This document would become the cornerstone of Aena's regulatory framework, providing the stability investors craved while ensuring airports met minimum service standards.

The DORA establishes the minimum conditions necessary to ensure the accessibility, sufficiency and suitability of airport infrastructures and the adequate provision of the basic services of the airport network, fixing the path of variation of the maximum annual revenues per passenger allowed to the operator, ensuring economic sufficiency in the provision of the service and a continuous improvement in the competitiveness of airport tariffs.

The beauty of the DORA framework, from an investor perspective, was its predictability. The new framework, named Document for Airport Regulations (DORA), establishes the tariffs will not increase at least until 2025. While this might seem like a constraint, it actually provided Aena with a clear incentive structure: since aeronautical charges were frozen, the only way to grow revenue per passenger was through commercial activities—shops, restaurants, parking, and other services.

In 2019, Aena managed the highest traffic, a record year with the network handling 275.2 million passengers. The company had perfected its model: use the monopoly position in Spain to generate stable cash flows, reinvest in commercial infrastructure to boost non-aeronautical revenues, and carefully expand internationally in markets with growth potential.

The numbers told a story of operational excellence. Aena was generating returns on invested capital that made other airport operators envious, all while operating under a tariff freeze. The company had turned regulatory constraints into competitive advantages, using the predictability of the Spanish framework to plan long-term investments that would pay off over decades.

VII. Brazil Expansion: The Big Bet (2019-2023)

While Aena's Spanish operations hummed along profitably, the company's leadership knew that real growth would have to come from international expansion. Brazil, with its vast geography, growing middle class, and underdeveloped airport infrastructure, presented an irresistible opportunity.

The first move came in 2019 when Aena Internacional was awarded the 30-year concession, with the possibility of an additional 5-year extension, of the Northeast Brazil airport group, comprising six airports (Recife, Maceió, Joao Pessoa-Bayeux, Aracajú, Juazeiro do Norte and Campina Grande). This wasn't just about adding airports to the portfolio; it was about proving Aena could operate in emerging markets with very different economic and regulatory dynamics than Europe.

ANB - Aeroportos do Nordeste do Brasil in operation since 2020 became Aena's laboratory for understanding Brazilian aviation. The Northeast region, while less wealthy than São Paulo or Rio de Janeiro, was experiencing rapid growth in domestic tourism and business travel. Aena applied lessons learned from managing regional Spanish airports—how to maximize revenue from limited traffic, how to work with local stakeholders, how to upgrade infrastructure efficiently.

But the real prize came in August 2022. The price of the concession, as a result of the public auction, was R$2.450 billion—about €468 million. Congonhas Airport, with 22.8 million passengers per year, is the group's busiest airport and the second busiest in Brazil. The acquisition of eleven airports, including São Paulo's downtown Congonhas Airport, represented Aena's largest international investment ever.

The Spanish company had been awarded the management after making a bid of 2.450 million reais (478 million euros), with the agreement stipulating management for a period of thirty years, with the possibility of extending for a further five years. Investments of 5.89 billion reais (1.05 billion euros) are expected, 73% of this total until 2028.

Congonhas wasn't just another airport—it was Brazil's premiere business aviation hub, the preferred airport for São Paulo's financial elite, constrained by its urban location but blessed with unbeatable convenience. Think of it as Brazil's London City Airport, but handling ten times the passengers. São Paulo/Congonhas closed 2023 with more than 22 million passengers. Aena Brasil started operating the eleven new BOAB airports between October and November 2023.

Aena Brazil leads the largest network of franchised airports in Brazil with 17 facilities spread across nine states, handling over 41 million passengers in 2023, which is equal to 20% of the country's air traffic. The scale of the Brazilian operation fundamentally changed Aena's international profile. No longer was it a Spanish operator with some international assets; it was becoming a genuinely global airport company.

VIII. COVID Crisis & Recovery (2020-2023)

March 2020 brought the aviation industry to its knees. The airports in Aena's network closed April at 141,014 passengers, a fall of 99.4% compared to the same month last year. The figures show how the movement of people has been halted to prevent the spread of coronavirus. Out of the total number of passengers, 126,066 were commercial passengers with 72,233 on domestic flights, 99% less than in April 2019.

The numbers were apocalyptic. The number of air passengers reduced by 60.2% compared to 2019. International and domestic air travel demand dropped by 75.6% and 48.8%, respectively. For a company whose entire business model depended on moving people through terminals, this was an existential crisis.

Aena went from facilitating the mobility of more than 300 million passengers on almost 3 million flights to focusing on the minimum essential and exceptional repatriation and health operations, and then adjusting to traffic demand in a progressive and safe manner, preserving the safety and health of passengers and workers at all times.

Yet Aena's response revealed the hidden strengths of its model. Unlike airlines, which hemorrhaged cash as planes sat grounded, airports still had to maintain essential infrastructure. The Spanish government, as majority owner, provided implicit backing that assured creditors. The regulated nature of the business, often criticized by investors, now provided stability.

The airports in the Aena network closed out 2021 with 119,959,671 passengers, which is 56.4% less passenger traffic than for the same period in 2019, or equivalent to 43.6% of the pre-pandemic volume. With respect to 2020, a year that was already affected by the COVID-19 crisis, 2021 closed out with an increase in passenger traffic of 57.7%.

The recovery trajectory was better than many predicted. Spanish airport operator Aena expects its passenger traffic in 2022 to reach 68% of pre-pandemic levels. The number of passengers flying through Aena's airports in 2021 was about 44% the pre-pandemic level.

By 2022, something remarkable was happening. The airports in the Aena network closed 2022 with a total of 243,681,775 passengers, representing an 88.5% recovery in passenger traffic compared to 2019. For the month of December, the recovery was close to 100%, standing at 98.1% compared to the same month in 2019.

The Spanish tourism machine, written off by many during the pandemic's darkest days, roared back to life. Aena expects to recover the pre-pandemic traffic levels in 2024 (about 275 million passengers), ahead of initial estimates. This recovery is taking place across the Aena network without the operational problems severely impacting other European airports. "This growing traffic will be managed at quality levels that have successfully been delivered through the challenging summer 2022".

Unlike the chaos that engulfed airports in Amsterdam, London, and Frankfurt during the summer of 2022—with hours-long security lines and thousands of cancelled flights—Aena's airports operated relatively smoothly. The company had maintained its workforce through the crisis, resisting the deep cuts that other operators made. When demand snapped back, Aena was ready.

Aena's board will propose to the Shareholders' meeting a dividend payment based on an 80% pay-out over the entire period of the Strategic Plan. Thus, the dividend proposed for 2022 will be increased by an additional €1.37 per share over the resulting profit at the end of the fiscal year. The resumption of dividends sent a powerful signal: Aena hadn't just survived the crisis; it had emerged stronger.

IX. Sustainability & Future Strategy (2021-Present)

As Aena emerged from the pandemic, it faced a new challenge: reconciling its business model—fundamentally based on increasing air travel—with mounting pressure to address climate change. The company's response has been ambitious, perhaps surprisingly so for an organization still majority-owned by a government.

This real concern for environmental sustainability has been reflected in the Airport Regulation Document for the next 5 years, from 2022 to 2026 (DORA II), which includes rigorous environmental parameters to guarantee airport sustainability.

The centerpiece of Aena's environmental strategy is its Climate Action Plan. The company has committed to investing €550 million from 2021-2030, targeting carbon neutrality by 2026 and net zero emissions by 2040. The government is ploughing an environmental strategy furrow by which Aena commits to self-powering all its airports with solar power, with €350 million specifically allocated for solar farms across the airport network.

These aren't just token gestures. Aena is transforming vast expanses of unused airport land into solar farms, turning liability into asset. The economic logic is compelling: Spain enjoys abundant sunshine, electricity costs are a significant operational expense, and the regulated framework allows Aena to earn returns on environmental investments.

DORA II establishes a stable and adequate framework for the growth of Aena's activity until 2026, with a rate freeze and a level of investment that will make it possible to reach the appropriate level of quality in the provision of airport services, especially in terms of sustainability and digitisation.

The digital transformation agenda is equally ambitious. Aena is deploying biometric technology to speed passenger processing, artificial intelligence to optimize airport operations, and advanced analytics to maximize commercial revenues. The goal is to handle more passengers with existing infrastructure, extracting maximum value from every square meter of terminal space.

The sustainability push has also become a differentiator in international competitions. When bidding for new concessions, Aena can point to concrete achievements in reducing emissions and implementing renewable energy, not just vague commitments. In Brazil, where environmental concerns are increasingly shaping infrastructure development, this has proven particularly valuable.

Yet tensions remain. TCI and other investors continue to push for climate action, but they also want returns. Airlines demand lower charges and better service while resisting environmental fees. The Spanish government wants Aena to maintain unprofitable regional airports while also maximizing the value of its 51% stake. Managing these competing demands requires delicate balancing.

X. Playbook: Business & Investing Lessons

The Aena story offers a masterclass in several key business principles that transcend the airport industry. First and foremost is the power of regulated monopolies when properly managed. While investors often shy away from heavily regulated businesses, Aena demonstrates that predictable regulation can actually be an asset. The DORA framework, with its transparent rules and long-term visibility, allows for strategic planning that would be impossible in more volatile competitive markets.

The company's approach to capital allocation deserves particular attention. During the pre-IPO restructuring, Aena ruthlessly cut costs, reducing headcount by 20% and renegotiating supplier contracts. But once public, the company pivoted to intelligent growth investments. Every euro spent on commercial infrastructure—from luxury retail spaces to automated parking systems—generated returns far exceeding the cost of capital. This discipline extended to international expansion, where Aena only pursued opportunities where it could gain control and implement its operating model.

The handling of the activist investor situation with TCI provides lessons in stakeholder management. Rather than engaging in a public battle, Aena's management worked behind the scenes to address legitimate concerns while maintaining government support. The company learned to speak the language of public markets while never forgetting that its majority shareholder had political as well as financial objectives.

The international expansion strategy reveals another crucial insight: the value of optionality. The Luton acquisition, while small relative to Aena's Spanish operations, provided invaluable experience operating in competitive markets. This knowledge proved essential when pursuing larger opportunities in Brazil. Each international venture built capabilities that opened doors to the next opportunity.

Perhaps most instructive is how Aena turned regulatory constraints into competitive advantages. The tariff freeze, initially seen as limiting, forced the company to innovate in commercial revenues. The obligation to maintain unprofitable regional airports became a barrier to entry that no private competitor could match. The requirement for environmental investments positioned Aena as a sustainability leader just as ESG considerations became paramount for investors.

The COVID crisis response highlighted the importance of financial conservatism during good times. Aena's strong balance sheet entering the pandemic, combined with government backing, allowed it to maintain operations and workforce when others were making desperate cuts. This positioned the company to capture the recovery faster than competitors who had to rebuild capabilities.

XI. Analysis & Bear vs. Bull Case

The bull case for Aena rests on several powerful foundations. The company operates what Warren Buffett would call a "toll bridge"—an essential infrastructure asset with no practical alternatives. Aena is the world's leading airport operator, with 63 airports, 48 of which in Spain, and the world's leading operator by number of passengers. In Spain, if you want to fly commercially, you almost certainly pass through an Aena airport.

The recovery trajectory post-COVID has exceeded expectations, with Spanish tourism showing remarkable resilience. The regulatory framework, while constraining aeronautical charges, provides unprecedented visibility through 2026 and likely beyond. Commercial revenues per passenger continue to grow as Aena becomes more sophisticated in retail partnerships and digital services. The Brazilian expansion opens a massive growth market where Aena's operational expertise commands premium valuations.

The bear case, however, cannot be dismissed. Climate change poses an existential challenge to an industry predicated on growth in air travel. While Aena is investing in sustainability, the fundamental tension between environmental goals and business growth remains unresolved. Flight shaming, carbon taxes, and potential regulation could structurally reduce demand, particularly for the short-haul flights that constitute much of Aena's Spanish traffic.

The regulatory risk that crystallized with the CNMC dispute in 2015 hasn't disappeared. The Spanish government's 51% stake means political considerations will always influence strategic decisions. A change in government could bring pressure to reduce charges, increase investments in unprofitable airports, or limit international expansion. The next DORA negotiation in 2026 could see airlines successfully lobbying for charge reductions, especially if traffic has fully recovered.

Competition from high-speed rail presents a growing threat. Spain's extensive AVE network already connects major cities faster than flying when considering airport processing time. Further rail expansion could erode domestic aviation, particularly on routes like Madrid-Barcelona, one of Europe's busiest air corridors. The European Union's push for modal shift from air to rail adds regulatory backing to this competitive threat.

Brazilian operations, while promising, carry execution risk. Operating in an emerging market with different regulatory frameworks, currency exposure, and political volatility adds complexity. The massive investment requirements for Brazilian airport upgrades must be funded while maintaining dividends to shareholders, creating potential capital allocation tensions.

The specter of another black swan event—whether pandemic, financial crisis, or geopolitical shock—looms over any aviation investment. While Aena proved resilient during COVID, its high operational leverage means any significant traffic reduction immediately impacts profitability.

XII. Epilogue & Looking Forward

As we look toward Aena's future, the company stands at a fascinating inflection point. The successful navigation of the COVID crisis has proven the resilience of its model, but new challenges are emerging that will test its adaptability.

The question of further privatization remains open. While the Spanish government has shown no immediate interest in reducing its stake, fiscal pressures and the success of the partial privatization could eventually lead to further sell-downs. Conversely, a left-wing government might seek to increase state control, especially if Aena's profitability is seen as coming at the expense of airlines or passengers.

The international expansion story is far from over. With operations now established in Brazil, Aena is well-positioned to pursue other Latin American opportunities. The company's proven ability to manage diverse airport portfolios, from congested urban hubs to remote regional facilities, is a capability few competitors can match. Yet each new market brings its own complexities and risks.

Technology will reshape the airport experience in ways we're only beginning to understand. Biometric processing, autonomous vehicles, and artificial intelligence could dramatically reduce the labor intensity of airport operations. Aena's scale provides both the resources to invest in these technologies and the platform to deploy them profitably. But technology also enables new forms of competition, from virtual meetings reducing business travel to autonomous vehicles potentially changing ground transportation dynamics.

The environmental transition presents both the greatest risk and potentially the greatest opportunity. Aena's commitment to renewable energy could transform it from carbon villain to sustainability hero. The vast land holdings around airports are ideal for solar farms, potentially making Aena a significant renewable energy producer. But if air travel becomes socially unacceptable or economically unviable due to carbon pricing, no amount of solar panels will save the business model.

The regulatory framework will continue evolving. The next DORA negotiation in 2026 will be crucial, setting the economic parameters for the rest of the decade. Aena must balance the demands of airlines seeking lower charges, investors wanting returns, and governments pursuing environmental and social objectives. The company's track record suggests it can navigate these tensions, but past performance doesn't guarantee future success.

What makes Aena unique in the global airport landscape isn't just its scale or profitability—it's the successful fusion of public service obligations with private market disciplines. The company proves that privatization doesn't require full private ownership, that monopolies can be managed efficiently, and that seemingly contradictory objectives can be reconciled through careful structuring and governance.

The Spanish airport operator that emerged from the bureaucratic structures of a post-dictatorship state has become a sophisticated global infrastructure company. Its journey from monopoly to market isn't complete—in many ways, Aena remains both monopoly and market participant, public and private, domestic and international. These contradictions aren't weaknesses to be resolved but strengths to be managed.

For investors, Aena offers a rare combination: the stability of regulated infrastructure with the growth potential of emerging markets expansion. For governments, it provides a template for privatization that maintains public control while accessing private capital and expertise. For the aviation industry, it demonstrates that airports can be more than passive infrastructure—they can be active participants in shaping travel patterns and passenger experiences.

As Aena approaches its fourth decade, the company that began as a Spanish state monopoly has evolved into something unprecedented: a global airport empire that remains majority government-owned, a regulated monopoly that competes internationally, a traditional infrastructure company embracing radical sustainability goals. The tensions inherent in this model—between public and private, stability and growth, tradition and innovation—will continue to define its trajectory.

The story of Aena is ultimately a story about transformation—of companies, industries, and countries. It reminds us that the most interesting businesses often exist at the intersection of seemingly incompatible ideas, that the best investments sometimes come wrapped in complexity, and that even the most traditional industries can reinvent themselves when necessity demands and opportunity allows.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube