Natural Grocers: The Three-Generation Health Food Revolution

I. Introduction & Episode Roadmap

The sliding glass doors of a Natural Grocers store open to reveal something unusual in American retail: a family business that chose principles over profits, refused to sell bestsellers that didn't meet their standards, and somehow survived—even thrived—against giants with 500+ locations and billions in backing.

Over the previous five years, the company has grown net sales by 37%, and diluted earnings per share have more than tripled. During this period, Natural Grocers returned $108 million in capital to stockholders through $4.76 of cumulative cash dividends per common share. Standing at $1.24 billion in revenue for fiscal 2024 with just 169 stores, this Colorado-based chain presents a paradox: How does a grocer with strict rules—100% organic produce, no artificial anything, yanking popular products that violate their standards—compete against Whole Foods' empire?

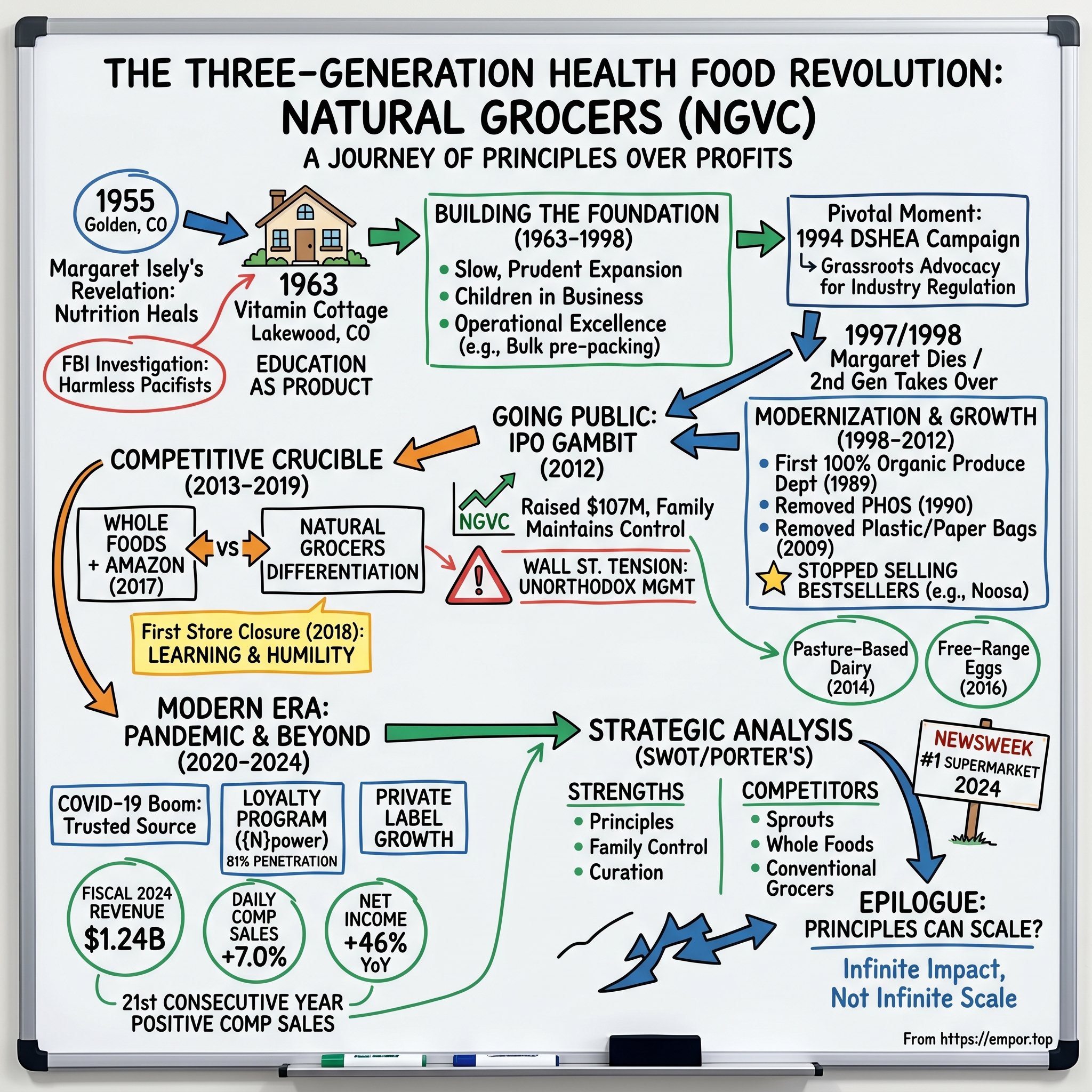

The answer lies in a story that begins with a sick mother in 1955 Golden, Colorado, armed with nothing but a $200 loan and an unshakeable belief that nutrition could heal. Margaret and Philip Isely didn't just start a grocery store. They ignited a movement that would help shape American dietary supplement legislation, pioneer organic retail standards decades before the USDA caught up, and build a three-generation dynasty that refuses to compromise—even when Wall Street demands it.

This is not merely a David versus Goliath retail tale. It's the story of how unwavering principles can become the ultimate business moat, how a family's stubbornness created competitive advantages that billion-dollar competitors can't replicate, and why sometimes the best growth strategy is knowing when to say no.

II. The Origin Story: Margaret's Revelation (1955-1963)

In the foothills of Colorado's Rocky Mountains, a waitress named Margaret Isely falls ill after giving birth to her second child. She develops a chronic infection and feels sluggish for months. Doctors don't have any answers, but she finds a book that advises restricting her diet to organic fruits and vegetables, meat and dairy from naturally raised animals, and fish oil and other supplements. Soon after she embraces the regimen, she begins to feel well again.

The year was 1955. Eisenhower was president, Rosa Parks had just refused to give up her bus seat, and American kitchens were celebrating the miracle of TV dinners and Wonder Bread. Into this world of processed convenience, Margaret began incorporating an organic diet consisting of fruits, vegetables, naturally raised meat and dairy, and supplements, like fish oil. Embracing this regimen, her health improved significantly.

What happened next would seem quaint if it weren't so revolutionary. Borrowing $200 to help feed the family and put gas in the car, Margaret and Philip went door-to-door in Golden, Colorado, lending out books on nutrition and giving out samples of whole grain bread. They weren't selling products—they were evangelizing a philosophy that food could be medicine, decades before that became a Silicon Valley mantra.

The political climate added drama to their mission. Their home was picketed after a local newspaper, the Jefferson Sentinel, accused them of being communists. "One of our neighbors had us investigated because we passed out literature for the Peoples World Parliament," said Margaret, "but the FBI gave us a clean slate as harmless pacifists". Imagine running a business where the FBI investigates you not for financial fraud but for distributing health food literature.

By 1958, they formalized their mission, opening their first brick-and-mortar location called "The Builder's Foundation" in Denver. But the real turning point came in 1963 when the Iselys converted a cottage-style house into a store, inspiring the name Vitamin Cottage. The store opened in Lakewood, Colorado, in 1963.

This wasn't just another health food store. The Iselys embedded education into the business model from day one—lending books, hosting informal nutrition talks, creating what would become a defining characteristic: education as product. While competitors sold vitamins, the Iselys sold knowledge with vitamins on the side.

III. Building the Foundation: The Slow Burn Years (1963-1998)

Growth came at a pace that would horrify modern venture capitalists. The second Vitamin Cottage opened in 1974 in Denver's Cherry Creek neighborhood—eleven years after the first store. By modern startup standards, this was failure. By the Iselys' standards, it was prudent expansion.

The family dynamics added complexity to the business narrative. Margaret's love of all things natural was reflected in her children's names: Zephyr, Kemper, Heather, Lark, and La Rock. Two of the seven Isely children died young, a tragedy that deepened the family's commitment to health and nutrition.

The children grew up in the stores, living the business rather than just working in it. The kids grew up in the business, stocking vitamins, bagging bulk ingredients, and ringing up customers at the registers. Kemper and Heather, our Co-President and Executive Vice President, respectively, both started by filling bulk bags and running the cash register.

The 1990s brought a pivotal moment in both family and industry history. Heather and Margaret led a grassroots letter writing campaign to achieve passage of the Dietary Supplement Health and Education Act of 1994 (DSHEA) which provided the legal framework that regulates the natural products industry today. This wasn't just lobbying—it was existential. Without DSHEA, the FDA could have regulated vitamins and supplements as drugs, potentially destroying the entire industry.

Innovation came through operational excellence rather than flashy marketing. Natural Grocers was a trendsetter in supplements—organizing them by type, rather than by brand, making it easier to find what you needed. Other retailers eventually adopted the same set up. In the 1960s, they started pre-packing all bulk foods and refrigerating select bulk (nuts, seeds, and flours) to ensure quality, cleanliness, and freshness.

When Margaret died in 1997 at age 75, she left behind more than just stores. Margaret Isely died in 1997, and the Iselys' children took over the business the following year. The inheritance: eleven stores and an uncompromising commitment to quality that would soon be tested in ways Margaret never imagined.

IV. Second Generation Takes Charge: Modernization (1998-2012)

The second Isely generation officially took over the business in 1998, a year after Margaret died. Kemper, Zephyr, Heather, and their siblings inherited not just a business but a mission—and they were about to supercharge it.

The first major inflection point had actually occurred in 1989, establishing a precedent that would define the company for decades. In 1989, when Michael Keaton's Batman was the hero of movie theatres everywhere, Natural Grocers made organic the hero of their brand-new produce departments. With their very first bunch of spinach, they decided to do something no other large chain has done before or since – sell only organic produce. This was thirteen years before the USDA even established organic certification standards in 2002.

The 1990s and 2000s saw the company systematically raising its standards while competitors were lowering theirs for scale. In 1990, Natural Grocers took all products with partially hydrogenated oils off their shelves, because of compelling evidence about the associated health risks. In 2015 the FDA finally caught up and took them off the GRAS (generally recognized as safe) list. Twenty-five years ahead of federal regulators—that's not just prescient; it's principled.

The decision-making process revealed the family's priorities. Natural Grocers decided to stop selling "confinement dairy products," such as milk from cows that aren't allowed to graze. That meant yanking Noosa, a best-selling yogurt brand. "You can't compromise your standards just to generate sales," says Kemper.

By 2009, they eliminated all plastic and paper bags from checkouts—not because it was trendy but because it aligned with their environmental values. Every decision reinforced the same message: principles first, profits second.

The expansion accelerated but remained measured. From those eleven stores in 1998, they grew to 53 stores by March 2012. The family was building something substantial, but they faced a crossroads. To achieve their vision of making healthy food accessible nationwide, they needed capital. The solution would test everything they stood for.

V. Going Public: The IPO Gambit (2012)

On Wednesday July 25, 2012 executives and guests of Natural Grocers by Vitamin Cottage, a specialty retailer of natural and organic groceries and dietary supplements, visited the New York Stock Exchange (NYSE) to celebrate the company's initial public offering.

The IPO priced at $15.00 per share, with the stock opening for trading at $18 and closing the first day around $17.94—a 20% pop that signaled market appetite for the company's unique positioning. The company raised $107 million through the offering, with the Iselys selling some shares but crucially maintaining control.

The decision to go public wasn't unanimous or easy. There were obvious concerns, including the onerous reporting requirements for public companies and the scrutiny external shareholders would have about the Iselys' unorthodox management style. Before the IPO, "there was a lot of pressure on us to identify someone as the chief executive officer," Heather says.

But the masterstroke was the ownership structure. Natural Grocers by Vitamin Cottage, Inc. (NGVC) has a dual-class ownership structure, which concentrates voting power with the founding family, even though their economic stake might be smaller than their control. With 57 percent of the shares, the family still owns the majority of the business.

Wall Street met Boulder values, and it was awkward. The company had ambitious projections—management suggested potential for 1,100 stores in the US market. Analysts did the math: 53 stores to 1,100? The skepticism was palpable. Yet the timing was fortuitous. Natural and organic grocery sales jumped from $81 billion in 2012–the year that Natural Grocers went public–to $91 billion in 2013.

The IPO transformed Natural Grocers from a regional player to a company with national ambitions, but it also introduced new tensions. Quarterly earnings calls, analyst expectations, and the relentless pressure for growth—could a company built on saying "no" survive in a world that only wanted to hear "yes"?

VI. The Competitive Crucible (2013-2019)

The post-IPO honeymoon ended quickly. By 2016, Natural Grocers faced its first real crisis—and it was self-inflicted. The company's aggressive expansion led to something they hadn't anticipated: stores cannibalizing each other's sales. Combined with the oil market collapse affecting key states like Colorado and Texas where many stores operated, comparable store sales growth turned negative for the first time in company history.

Meanwhile, the competitive landscape shifted tectonically. In 2017, Amazon acquired Whole Foods for $13.7 billion, sending shockwaves through the industry. Suddenly, Natural Grocers' largest competitor had the backing of the world's most powerful e-commerce platform and effectively unlimited capital. The existential question loomed: How does a 100-store chain compete against Amazon?

The answer came through differentiation, not scale. In 2014, before the Amazon threat materialized, Natural Grocers had already introduced another industry-first standard. Natural Grocers introduced their pasture based dairy standard. It means every milk-based product in their dairy case comes from cows that are 100% pasture based. While Whole Foods was preparing to be acquired, Natural Grocers was raising the bar on product quality.

The company also pioneered standards that competitors couldn't or wouldn't match. In 2016 when the National Park Service turned 100, Natural Grocers was introducing their free-range egg standard, so that chickens could roam and do whatever it is that chickens do. These weren't marketing gimmicks—they were operational commitments that required restructuring entire supply chains.

A critical turning point came in 2018 with Natural Grocers' first-ever store closure in Tulsa. "There was an acknowledgement that it wasn't the best site, and that maybe Tulsa didn't need two stores," recalls Isely. "It was an insight into different parts of the country and how we should approach some of that site learning". The humility to admit mistakes and learn from them—a rarity in public company narratives—became a competitive strength.

During this period, third-generation family members began joining the business, bringing fresh perspectives while maintaining founding principles. The challenge wasn't just competing against Whole Foods and Sprouts; it was ensuring the family's values survived the transition to the next generation.

VII. The Modern Era: Pandemic Boom & Beyond (2020-2024)

When COVID-19 struck in March 2020, Natural Grocers was uniquely positioned. While larger chains struggled with supply chain disruptions, the company's long-standing relationships with smaller, regional suppliers—built over decades of principled partnership—paid dividends. Stores remained stocked when competitors' shelves went bare.

The pandemic accelerated trends Natural Grocers had been cultivating for years. Suddenly, everyone cared about immune health, organic foods, and shopping at stores they could trust. The company's education-first approach, which might have seemed quaint in 2019, became essential as consumers desperately sought reliable health information.

The loyalty program emerged as an unexpected growth driver. {N}power penetration was 81% in the fourth quarter, up from 77% a year ago. This wasn't just a discount card—it was a community membership, providing exclusive access to nutrition education, personalized health coaching, and member-only shopping hours during the pandemic.

Private label transformation accelerated the company's evolution. Natural Grocers' private-label line accounted for 8.4% of total sales, up from 7.8% a year ago. The company launched 19 new products in the fourth quarter, and for the year, it introduced 80 new private-label products. These weren't generic knock-offs but carefully crafted products meeting the company's exacting standards—often exceeding the quality of national brands.

The financial results validated the strategy. This marked the 21st consecutive year of positive comparable-store sales growth. In fiscal 2024, daily average comparable store sales increased 7.0%, comprised of a 3.8% increase in daily average transaction count and a 3.1% increase in daily average transaction size.

Most remarkably, profitability soared. The company achieved a net income of $33.9 million, or $1.47 diluted EPS, marking a substantial improvement from fiscal 2023—a 46.0% increase in net income year-over-year. The board's confidence showed in their actions: announcing a 20% dividend increase to $0.12 per share in November 2024.

VIII. Strategic Analysis: Porter's Five Forces

Supplier Power (Medium)

Natural Grocers faces an interesting supplier dynamic. Their strict quality requirements—100% organic produce, pasture-raised dairy, no artificial ingredients—significantly limit their supplier base. Yet this constraint has become a strength. Decades-long relationships with smaller, mission-aligned suppliers create mutual dependence. These suppliers need Natural Grocers as much as the company needs them, especially as one of the few retailers willing to pay premiums for true quality.

Buyer Power (Medium-High)

The health-conscious consumer is both Natural Grocers' greatest asset and biggest challenge. These shoppers are informed, price-aware, and have increasing alternatives. Mainstream retailers, from Albertsons to Walmart and Aldi, started elbowing their way into the space. Nowadays, shoppers can find not only organic name brands but organic private label products, as well. Yet Natural Grocers maintains pricing power through trust—customers know that everything in the store meets rigorous standards, eliminating decision fatigue.

Threat of Substitutes (High)

The substitutes aren't just other grocers—they're Amazon Fresh, Thrive Market, local farmers' markets, and direct-to-consumer organic brands. Each offers a piece of what Natural Grocers provides. The company's defense? Physical stores that serve as community hubs, immediate gratification, and the ability to see, touch, and smell products—experiences that digital can't replicate.

New Entrants (Medium)

While the capital requirements for opening organic grocery stores are substantial, the real barrier is time. Natural Grocers' 70-year reputation, established supplier relationships, and prime retail locations in secondary markets create advantages that money alone can't buy. New entrants like Erewhon can capture luxury segments, but replicating Natural Grocers' middle-market positioning requires decades of trust-building.

Competitive Rivalry (Very High)

The numbers tell the story. Sprouts has over 380 stores spread across 23 states. Whole Foods operates 500+ locations with Amazon's backing. Then there's everyone else: Kroger with its Simple Truth brand, Walmart's organic expansion, Target's Good & Gather line. Yet when Newsweek readers voted in 2024, Natural Grocers secured the number one spot among supermarkets, beating Harris Teeter, Aldi, Wegmans, Trader Joe's, and notably, placing ahead of both Sprouts (8th) and Whole Foods (9th).

IX. Hamilton's 7 Powers Framework

Counter-Positioning

This is Natural Grocers' strongest power. By maintaining standards that larger competitors won't adopt—100% organic produce when others mix conventional, refusing to sell products with artificial ingredients regardless of popularity—they've created a position that others can't attack without destroying their own business models. Whole Foods can't match these standards without eliminating half their SKUs and raising prices further.

Cornered Resource

The Isely family's continued control through the dual-class structure represents an uncopyable asset. Isely Family Group is the largest shareholder with 15% of shares outstanding. With 15% and 14% of the shares outstanding respectively, Kemper Isely and Zephyr Isely are the second and third largest shareholders. This isn't just about voting rights—it's about 70 years of accumulated trust, relationships, and institutional knowledge that can't be purchased or replicated.

Process Power

The nine-month store opening process, refined over decades, enables Natural Grocers to enter secondary markets that larger competitors ignore. Their ability to make 15,000-square-foot stores profitable where competitors need 40,000+ square feet creates unique expansion opportunities. The nutrition education program, with coaches in every store, requires operational capabilities that Pure digital players can't match and conventional grocers won't invest in.

Branding

"The Original good4u Grocers" positioning resonates with multi-generational customers who remember shopping with their parents at Natural Grocers. Margaret was inducted into the Natural Products Industry Hall of Legends in 2015, cementing the company's place in industry history. This heritage branding becomes more valuable as venture-backed "authentic" brands proliferate.

Scale Economies

Limited compared to giants but meaningful in their niche. Natural Grocers' concentrated presence in specific regions allows for efficient distribution and marketing. Their small-box format means lower occupancy costs—a significant advantage as retail rents rise.

Network Economies

Weak in traditional terms—retail doesn't exhibit strong network effects. However, the {N}power program creates micro-networks within communities, where members share recipes, attend classes together, and create social bonds around health—a soft network effect competitors struggle to replicate.

Switching Costs

Financially minimal but emotionally significant. Customers who've spent years learning to trust Natural Grocers' curation—knowing everything meets strict standards—face high psychological switching costs. Why research every product at Whole Foods when Natural Grocers has already done the work?

X. Bear vs. Bull Case

Bear Case:

The numbers don't lie: 169 stores versus Whole Foods' 500+, Sprouts' 400+, and Kroger's 2,700+. In retail, scale typically wins, and Natural Grocers lacks it. Geographic concentration in western states limits growth potential and increases vulnerability to regional economic downturns. The strict standards that define the company also constrain it—refusing to sell popular products limits revenue potential.

Amazon's entry via Whole Foods changed the game permanently. With unlimited capital, sophisticated logistics, and Prime integration, Amazon can offer convenience and pricing that Natural Grocers can't match. Meanwhile, every conventional grocer now has an organic section. Walmart, with its massive scale, can undercut Natural Grocers on organic basics.

The family control structure, while preserving values, might deter institutional investment and limit access to growth capital. The stock trades at a significant multiple premium to larger, more diversified grocers without the growth rate to justify it.

Bull Case:

Net income increased by 53.2% to $9 million in Q4, and adjusted EBITDA reached $22.6 million—these aren't the numbers of a declining business. The 21-year streak of positive comparable store sales growth demonstrates remarkable consistency through multiple economic cycles.

The differentiated positioning becomes more valuable as the organic market commoditizes. While competitors race to the bottom on price, Natural Grocers maintains premium positioning through trust. The small-box format—averaging 11,000 square feet versus 40,000 for conventional grocers—enables profitable operations in secondary markets that competitors can't serve economically.

{N}power has nearly two million members, creating a loyal customer base that drives 81% penetration of sales, focused, cost-effective marketing. The family control ensures long-term thinking in a short-term market, enabling decisions that public company CEOs couldn't make.

XI. Playbook: Key Lessons

The Power of Principles: Natural Grocers demonstrates that unwavering commitment to standards can become the ultimate differentiator. By refusing to compromise—yanking bestsellers, maintaining 100% organic produce despite cost pressures—they've created a trust moat that money can't buy. The lesson: In commoditizing markets, principles become premium.

Family Business Dynamics: The successful transition from founders to second generation to emerging third generation offers a masterclass in succession planning. Key elements: dual-class structures to maintain control, involving children from childhood, and accepting family quirks as features, not bugs. The absence of a single CEO—having co-presidents instead—violates conventional wisdom but works.

David vs. Goliath Strategy: Competing through differentiation, not scale, requires discipline. Natural Grocers chose depth over breadth—better to dominate Des Moines than struggle in Los Angeles. They turned constraints (small stores, limited selection) into advantages (convenient shopping, curated quality). The lesson: Define the game you're playing, not the one competitors want you to play.

The Education Play: Making customers smarter creates loyalty beyond price. Natural Grocers' nutrition coaches, free classes, and education-first approach build emotional bonds that transcription discounts can't break. In an information-abundant world, curation and trust become invaluable. Smart customers become loyal customers.

Going Public While Staying Private: The dual-class structure enabled growth capital while preserving mission. The lesson for founders: Structure matters more than valuation. Better to own 57% of something aligned with your values than 10% of something that isn't.

XII. Epilogue: Looking Forward

Standing in a Natural Grocers store in late 2025, you can feel the tension between past and future. Third-generation family members walk the aisles their grandparents built, smartphones in hand, discussing TikTok strategies while maintaining standards established before their parents were born.

The challenges ahead are substantial. E-commerce penetration in groceries continues climbing, threatening the physical store model Natural Grocers depends on. Climate change makes sourcing 100% organic produce increasingly difficult and expensive. Labor shortages hit customer-service-intensive models hardest. The company plans four to six new stores annually—modest growth in a winner-take-all economy.

Yet the tailwinds are equally powerful. The regenerative agriculture movement aligns perfectly with Natural Grocers' values—they were sustainable before it had a hashtag. Natural organic products outpaced conventional groceries by nearly two percentage points in 2024, up 6.89% versus conventional growth. Gen Z's obsession with health, authenticity, and transparency plays to every Natural Grocers strength.

The existential question isn't whether Natural Grocers can survive—their financials suggest they're thriving. It's whether principles can scale infinitely. Can you maintain standards at 500 stores that you held at five? Can the fourth generation maintain what the first generation started?

Perhaps that's the wrong question. Natural Grocers' story suggests that infinite scale isn't the goal—sustainable impact is. In a world of venture-backed "mission-driven" brands that compromise at the first sign of pressure, Natural Grocers remains defiantly itself: A three-generation testament to the radical idea that business can be about more than business.

The Iselys started with $200 and a belief that food could heal. Seventy years later, their descendants run a billion-dollar company that still believes the same thing. In American retail, where everything is for sale, Natural Grocers' principles remain priceless. That might be the greatest inheritance of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube