V-Guard Industries: From a Kerala Stabilizer Workshop to India's Electrical Empire

Introduction & Thesis Statement

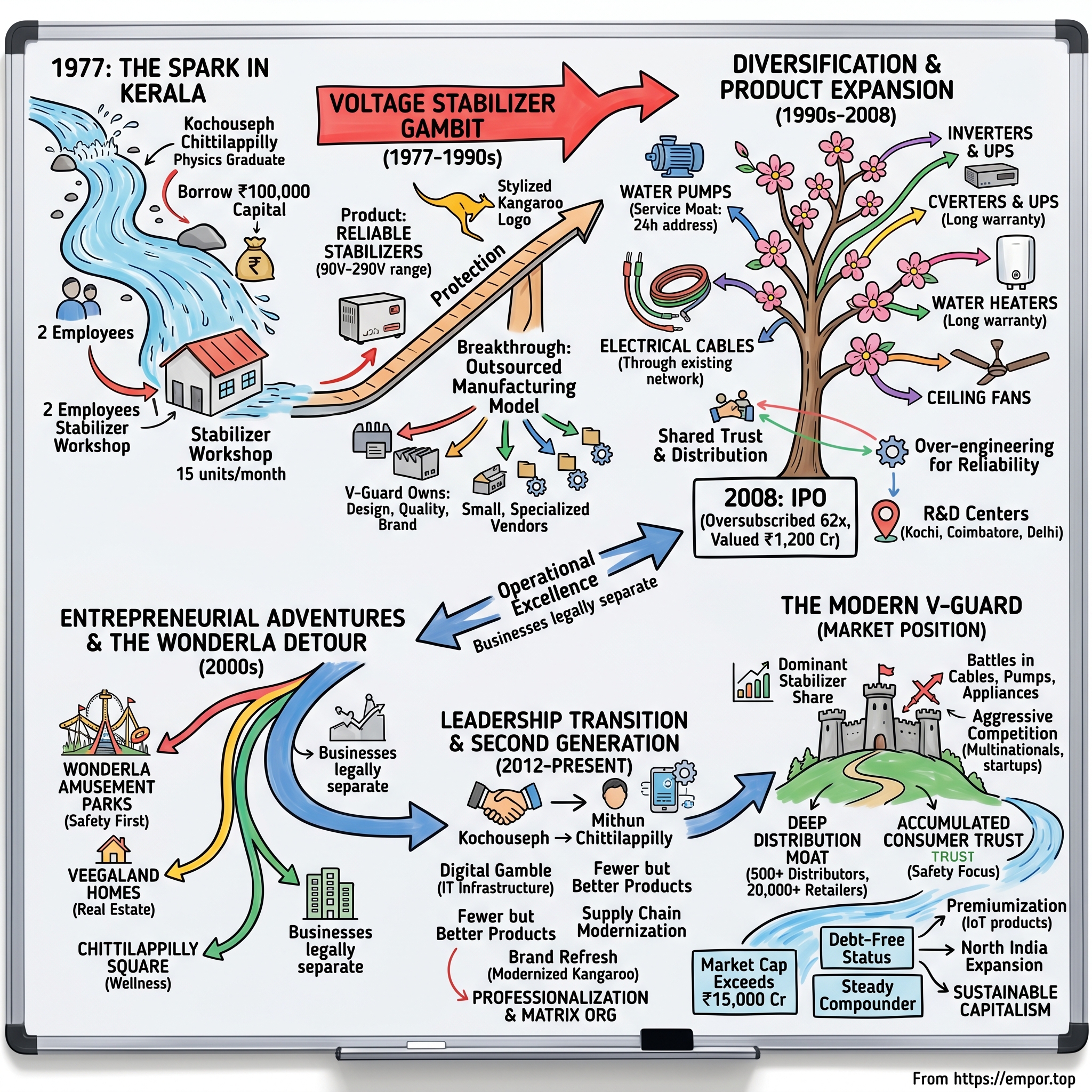

Picture this: It's 1977 in Kerala, and the monsoons have just begun. Power cuts are as predictable as the rain itself. In homes across the state, televisions flicker and die, refrigerators groan to a halt, and the newly purchased mixer-grinder—bought with months of savings—sits vulnerable to the next voltage surge. Into this chaos steps a 27-year-old physics graduate named Kochouseph Chittilappilly, armed with ₹100,000 in borrowed capital and an audacious dream: to protect every Indian home from the vagaries of an unreliable power grid.

Today, V-Guard Industries commands a market capitalization exceeding ₹15,000 crore, with products in over 20 million Indian homes. The company that started with two employees making 15 voltage stabilizers a month now manufactures everything from solar water heaters to modular switches, employing thousands and competing toe-to-toe with multinational giants. This is not just another rags-to-riches story—it's a masterclass in understanding customer pain points, building trust in safety-critical products, and creating distribution moats in one of the world's most complex markets.

The core question that drives this narrative isn't simply how a small workshop became an electrical empire. It's this: In a market where global giants like Schneider and Siemens had every advantage, how did a Kerala-based entrepreneur build one of India's most trusted electrical brands? And perhaps more intriguingly—why did this same entrepreneur, at the peak of his success, decide to build amusement parks and donate his kidney to a complete stranger?

What follows is the unlikely story of V-Guard—a company that shouldn't have succeeded by conventional metrics but did so by rewriting the rules of Indian manufacturing. It's a story about physics meeting commerce, about turning India's infrastructure problems into business opportunities, and about building a ₹5,500 crore revenue business while remaining virtually debt-free. Most importantly, it's about how understanding the anxieties of middle-class India—that moment when the lights flicker during a cricket match, that fear when a water pump fails during summer—can be transformed into an enduring business empire.

This is the V-Guard story, and like the best business stories, it begins not in a boardroom, but in a moment of defiance between a father and son.

The Kochouseph Chittilappilly Origin Story

The year is 1976, and in the Chittilappilly house in Parappur, Thrissur, an argument is brewing over dinner. C.O. Thomas, a traditional agriculturalist who had worked his land for decades, cannot understand why his son Kochouseph—armed with a master's degree in physics from St. Thomas College—wants to throw away a stable future for what seems like a foolish gamble. "You could be a college lecturer," Thomas insists, his voice carrying the weight of generational wisdom. "Or join a bank. Why this... this business nonsense?"

Kochouseph, then 26, had spent the previous three years at Telics, a Thiruvananthapuram-based electronics company, starting as a supervisor overseeing the production of voltage stabilizers and emergency lamps. It wasn't glamorous work—the factory floor was hot, the hours long, and the pay modest. But something about the process fascinated him. He watched customers arrive with burnt-out appliances, their faces etched with frustration. He studied the stabilizer circuits, understanding not just the physics of voltage regulation but the economics of protection. Each damaged television represented months of savings lost; each failed refrigerator meant spoiled food and family stress.

Born in December 1950, Kochouseph was the product of two worlds colliding. His father represented old Kerala—agricultural, conservative, skeptical of risk. But young Kochouseph had come of age in a different India, one where the License Raj was slowly loosening its grip, where entrepreneurs like Dhirubhai Ambani were beginning to capture imaginations. His physics education from Christ College, Irinjalakuda, had taught him to see the world through equations and experiments, but his time at Telics had shown him something textbooks couldn't: the massive gap between what Indian consumers needed and what the market offered.

The breaking point came in early 1977. Kochouseph approached his father with a specific request: ₹100,000 to start his own voltage stabilizer company. In today's money, adjusted for inflation, that's roughly ₹25 lakhs—not a small sum for a middle-class Kerala family. Thomas was incredulous. "One lakh rupees? To compete with established companies? With your physics degree?" The argument that followed would become family legend, lasting late into the night, with Kochouseph's mother attempting to mediate between her traditional husband and her ambitious son.

What finally swayed Thomas wasn't logic but emotion. Kochouseph didn't talk about market opportunities or profit margins. Instead, he spoke about the families he'd met at Telics—the newlyweds whose wedding-gift television had blown within weeks, the small shop owner whose refrigerator failure had cost him his entire inventory. "I understand the science," he told his father, "but more importantly, I understand the problem."

The physics-to-business transformation wasn't as unlikely as it seemed. Voltage stabilization is fundamentally about understanding electromagnetic induction, transformer design, and circuit protection—all concepts central to his academic training. But Kochouseph brought something more: an obsessive attention to reliability. At Telics, he'd noticed that most stabilizer failures weren't due to design flaws but to cost-cutting in components. Companies would use cheaper capacitors that couldn't handle Kerala's humidity, or transformers that overheated in India's summer temperatures.

By March 1977, with his father's reluctant blessing and borrowed capital in hand, Kochouseph rented a small 2000-square-foot shed in Kochi. He hired two employees—one, an experienced technician from Telics who believed in his vision; the other, a young diploma holder eager for opportunity. The workshop was sparse: a few workbenches, basic testing equipment, and a hand-painted sign that read "V-Guard Industries"—the 'V' standing for voltage, though Kochouseph would later enjoy the confusion when people assumed it stood for his name.

The first month, they produced exactly 15 stabilizers. Each one was personally tested by Kochouseph, who would simulate voltage fluctuations far beyond normal parameters. His employees thought he was paranoid, testing each unit for hours. But Kochouseph knew something they didn't: in a market where trust was everything, one failure could destroy a brand before it even began. Those first 15 customers weren't just buying stabilizers; they were the foundation of what would become one of India's most trusted electrical brands.

The Voltage Stabilizer Gambit (1977–1990s)

The workshop in Kochi, summer of 1978. The air hangs thick with humidity and the acrid smell of soldering flux. Kochouseph stands before a returned stabilizer, its casing cracked, internals fried. The customer, a middle-aged banker from Ernakulam, watches expectantly. This is the moment that would define V-Guard's trajectory. Instead of offering excuses or partial refunds—standard practice then—Kochouseph does something unprecedented: he hands the customer a brand-new unit, no questions asked, and asks permission to visit his home to check the electrical conditions. "Your satisfaction," he tells the surprised banker, "is worth more than this stabilizer."

This wasn't just customer service; it was strategic genius. That banker would tell his colleagues, who would tell their neighbors, creating a word-of-mouth network more powerful than any advertisement. But first, V-Guard needed a symbol, something that would stick in consumers' minds. Enter V.A. Sreekandan, known as Mani, a local artist who Kochouseph commissioned to create a logo. The brief was unusual: "I want something that suggests protection, reliability, but also... energy, movement."

Mani's creation—a stylized kangaroo—seemed bizarre at first. What did an Australian marsupial have to do with voltage stabilizers? But Kochouseph saw the genius: a kangaroo protects its young in its pouch, leaps over obstacles, and most importantly, was completely unique in the Indian electrical market. While competitors used lightning bolts and technical diagrams, V-Guard had a kangaroo. It was memorable, approachable, and subtly communicated the core promise: we'll protect what's precious to you.

The real innovation, however, came in the 1980s during a period that nearly destroyed the company. Kerala's powerful trade unions had begun organizing strikes at manufacturing units across the state. Kochouseph watched competitors' factories shut down for weeks, their supply chains crippled. One particularly bitter strike at a nearby electronics factory lasted 47 days, bankrupting the owner. The writing was on the wall: traditional manufacturing in Kerala was becoming untenable.

Instead of fighting the unions or relocating, Kochouseph invented something radical: a completely outsourced manufacturing model where V-Guard would own the design, quality control, and brand, but actual production would happen across dozens of small units. Each unit would specialize in specific components—one making transformers, another winding coils, a third assembling casings. V-Guard's core team would focus solely on design, quality testing, and final assembly.

This wasn't just outsourcing; it was orchestration. Kochouseph created detailed quality manuals for each vendor, instituted surprise inspections, and most crucially, helped finance equipment upgrades for his suppliers. When vendors met quality standards consistently, they got more orders and better payment terms. When they failed, they were given training, not immediately terminated. It was a ecosystem, not just a supply chain.

By 1982, V-Guard was selling 200 stabilizers per month, but the real breakthrough came from understanding South India's unique power problem. Unlike North India, where power cuts were the main issue, South India suffered from violent voltage fluctuations. The State Electricity Boards, struggling with demand-supply mismatches, would routinely allow voltage to swing from 150V to 280V (normal being 230V). Kochouseph redesigned V-Guard stabilizers to handle 90V to 290V—a range that seemed excessive but perfectly matched reality.

The distribution strategy was equally unconventional. Instead of focusing on large electronics retailers in cities, Kochouseph targeted small electrical shops in tier-2 and tier-3 towns. His logic was simple: when power problems struck, people didn't go to fancy showrooms; they rushed to the nearest electrical shop. By 1985, V-Guard had 300 dealers across Kerala and Tamil Nadu, each one trained not just to sell but to educate customers about voltage protection.

The numbers tell the story of exponential growth. From 15 stabilizers per month in 1977, V-Guard reached:

- 1980: 50 units/month

- 1985: 500 units/month

- 1990: 2,000 units/month

- 1995: 10,000 units/month

But raw numbers don't capture the trust being built. In 1987, when a batch of 200 stabilizers failed due to a supplier's faulty capacitors, Kochouseph didn't wait for complaints. He tracked down every customer through dealer records and proactively replaced their units, even visiting homes personally in Kochi. The incident cost V-Guard ₹8 lakhs—nearly wiping out that quarter's profits—but it cemented a reputation: V-Guard stands behind its products, always.

The 1990s brought new challenges. Multinational companies began eyeing India's growing electrical market. Companies like Krykay and Premier were spending heavily on advertising, and Chinese imports were beginning to appear. But V-Guard had something money couldn't buy quickly: thousands of small electrical contractors who recommended V-Guard by default, customers who trusted the kangaroo logo, and a distribution network that reached into India's heartland.

By the decade's end, V-Guard was the largest-selling stabilizer brand in India, with over 500 distributors and 20,000 retail touchpoints. The boy who borrowed ₹1 lakh had built a ₹50 crore business. But Kochouseph knew that depending on one product—even a successful one—was dangerous. The real growth, and the real test of V-Guard's model, would come from expansion into new categories.

Diversification & Product Portfolio Expansion (1990s–2008)

The meeting room at V-Guard's Kochi headquarters, 1992. Kochouseph faces his senior managers, a blueprint spread across the table. But it's not for a new stabilizer—it's for a water pump. His sales head, a veteran who'd been with the company since 1985, is skeptical: "Sir, we're electronics people. Pumps are mechanical. Completely different technology, different dealers, different customer expectations." Kochouseph's response would become company folklore: "When a family's water tank runs dry in summer, do they care if we're electronics people or mechanical people? They just want water."

This exchange crystallized V-Guard's diversification philosophy: enter categories where electrical problems intersect with daily anxieties. Water pumps weren't just mechanical devices; they were lifelines in a country where municipal water supply was erratic. More importantly, pump failures often stemmed from the same voltage fluctuations that V-Guard had built its reputation on solving.

The pump project began with six months of field research. Kochouseph personally visited 200 homes across Kerala and Tamil Nadu, watching how families used pumps, when they failed, and what frustrated users most. The insights were revealing: pumps typically failed not from mechanical wear but from electrical issues—dry running when water levels dropped, motor burnout from voltage fluctuations, and starting problems during low voltage conditions. V-Guard's pumps would address each of these, incorporating voltage protection and dry-run prevention as standard features, not expensive add-ons.

By 1994, V-Guard launched its pump range with a radical service promise: any breakdown would be addressed within 24 hours. The company recruited and trained 500 service technicians across South India, equipping them with motorcycles and spare parts. This service network—unheard of in the pump industry then—became V-Guard's secret weapon. Competitors sold pumps; V-Guard sold peace of mind.

The next category expansion came from an unexpected source: customer complaint data. V-Guard's service centers noticed a pattern—during every monsoon, they received hundreds of calls about electrical accidents from exposed wiring. In 1996, Kochouseph decided to enter the electrical cables market, but with a twist. While competitors focused on industrial cables, V-Guard would target home wiring with cables specifically designed for Indian conditions: extra insulation for humidity, rodent-repellent coating, and fire-retardant properties.

The cable venture nearly failed initially. Established players like Havells and Finolex had locked up traditional distribution channels. V-Guard's solution was audacious: bypass traditional cable dealers entirely and sell through their existing stabilizer network. Electrical shops that had never stocked cables before suddenly had a trusted brand offering them attractive margins and marketing support. Within three years, V-Guard cables reached ₹30 crore in annual sales.

The year 2001 marked a pivotal strategic shift. Analysis of customer purchase patterns revealed something interesting: families buying V-Guard stabilizers often bought water heaters within the same year. The connection was logical—both were essential appliances, both were vulnerable to electrical issues, and both required trust in safety. V-Guard entered the water heater market with innovations that seemed minor but mattered: a thermal cutout that prevented overheating, a pressure release valve tested for Indian water conditions, and critically, a five-year warranty when competitors offered two.

The expansion accelerated through the 2000s: - 2002: Solar water heaters (targeting eco-conscious consumers and hotels) - 2003: Inverters and UPS systems (leveraging battery management expertise) - 2005: Switch gears and modular switches - 2007: Ceiling fans and kitchen appliances

Each category entry followed the same playbook: identify an electrical pain point, over-engineer for reliability, provide superior service, and leverage the existing distribution network. By 2007, V-Guard's revenue had crossed ₹500 crore, with non-stabilizer products contributing 60% of sales.

The company structure evolved to match this complexity. Three distinct divisions emerged:

Electronics Division (30% of revenue): Stabilizers, inverters, UPS systems, solar solutions

Electrical Division (35% of revenue): Cables, pumps, switchgears, modular switches

Consumer Durables (35% of revenue): Water heaters, fans, kitchen appliances

But growth brought challenges. Manufacturing complexity had exploded—V-Guard now managed 300+ SKUs across categories. The outsourced model that worked for stabilizers struggled with pumps requiring precision engineering. Quality control became increasingly difficult as vendor networks expanded to over 200 suppliers.

The solution came through technology and systems. V-Guard implemented SAP in 2004 (among the first mid-sized Indian companies to do so), created vendor quality scorecards with real-time tracking, and established three centers of excellence for R&D in Kochi, Coimbatore, and Delhi. The company also began selective backward integration, acquiring critical component manufacturers to ensure quality while maintaining flexibility.

The 2008 IPO prospectus revealed remarkable numbers: ₹650 crore revenue, ₹45 crore profit, zero debt, and presence in 15 states. The IPO, oversubscribed 62 times, raised ₹150 crore, valuing the company at ₹1,200 crore. But hidden in those numbers was a more interesting story: V-Guard had achieved 30% CAGR over a decade while maintaining 7% net margins in categories where Chinese imports had destroyed profitability for many players.

The secret wasn't just operational excellence—it was trust arbitrage. In categories where product failure meant inconvenience (like fans), cheap imports thrived. But in categories where failure meant danger or significant loss (water heaters, pumps, cables), Indian consumers paid premiums for trust. V-Guard had positioned itself perfectly in this trust zone, commanding 15-20% price premiums over unbranded products while remaining 10-15% cheaper than multinationals.

The Wonderla Detour & Entrepreneurial Adventures

October 2000, and Kochouseph Chittilappilly stands in a muddy field outside Kochi, watching his 12-year-old son Arun's face light up as he describes his recent trip to Disneyland. "Papa, why doesn't India have anything like this?" It's a simple question that would lead to one of Indian business's most unusual diversifications: an electrical goods manufacturer building amusement parks.

The conventional wisdom would have called this insane. V-Guard was hitting its stride in electrical products, revenue was growing 30% annually, and here was the founder wanting to invest ₹30 crores—nearly a year's profit—into roller coasters and water slides. His board was skeptical, investors were confused, and competitors were amused. But Kochouseph saw something others missed: the same middle-class families buying V-Guard stabilizers were desperate for quality entertainment options.

The insight came from data, not emotion. V-Guard's customer research showed that Indian middle-class disposable income was growing 15% annually, but entertainment infrastructure hadn't kept pace. Families would save for months for a vacation, only to find overcrowded, poorly maintained destinations. The amusement park industry in India was dominated by small, unsafe operations or temporary carnival setups. There was a gap for a premium, safe, family entertainment destination—essentially, the V-Guard of amusement parks.

Veegaland (later renamed Wonderla) opened in Kochi in 2000 with 25 rides spread across 30 acres. But this wasn't just about installing imported rides. Kochouseph applied the same obsessive attention to safety that defined V-Guard. Every ride underwent daily 127-point safety checks. Water quality was tested hourly. Staff underwent six months of training—unprecedented in Indian amusement parks. The tagline wasn't about thrills but trust: "Where safety comes first."

The numbers initially looked disastrous. Year one saw just 3 lakh visitors against a projected 5 lakh. The park was bleeding ₹2 crore monthly. Critics pointed out that Kochouseph had violated his own business philosophy—this had nothing to do with electrical products, leveraged none of V-Guard's competencies, and targeted a completely different customer mindset (entertainment vs. necessity).

But Kochouseph saw synergies others missed. The same project management skills that built distribution networks could build theme parks. The same quality obsession that made reliable stabilizers could ensure safe rides. Most importantly, the same middle-class trust that chose V-Guard products would choose Wonderla for their annual family outing.

By 2004, Wonderla Kochi turned profitable, drawing 6 lakh visitors annually. The success prompted expansion to Bangalore in 2005—a ₹120 crore investment that was India's largest amusement park. This wasn't replication but evolution. Bangalore featured India's first reverse looping roller coaster, a musical fountain synchronized to Bollywood songs, and critically, dynamic pricing that matched IT city paydays and school holidays.

The Wonderla model was fascinating: high capital investment (₹100+ crore per park) but exceptional returns once operational. By 2010, Wonderla Bangalore was generating ₹50 crore revenue with 40% EBITDA margins—better than many five-star hotels. The parks weren't just profitable; they were creating a moat. While anyone could import Chinese stabilizers, nobody could replicate a 50-acre amusement park with established brand recognition.

The diversification didn't stop there. In 2005, Kochouseph launched Veegaland Homes, a real estate venture focusing on premium apartments in Kochi. Again, the logic seemed tangential until you understood the insight: the same families buying V-Guard products and visiting Wonderla wanted quality housing. The company's reputation for reliability translated into real estate—apartments sold out off blueprints because buyers trusted the V-Guard name.

Then came Chittilappilly Square in 2012, a wellness park combining naturopathy, ayurveda, and modern medicine. This seemed even more bizarre—what did electrical goods have to do with healthcare? But Kochouseph's philosophy was consistent: identify underserved needs of India's middle class and deliver with uncompromising quality.

The management structure for these ventures was clever. While Kochouseph remained Chairman of V-Guard, his son Arun took operational control of Wonderla, allowing focused leadership while maintaining strategic oversight. The businesses were kept legally separate—Wonderla went public independently in 2014—preventing any drag on V-Guard's core operations.

Critics questioned capital allocation. Between 2000-2010, Kochouseph invested over ₹300 crore in non-electrical ventures while V-Guard's competitors were aggressively expanding market share. Havells spent heavily on advertising, Crompton modernized manufacturing, and Chinese brands flooded the market. Wasn't this dangerous distraction?

The numbers suggest otherwise. During the same period, V-Guard's revenue grew from ₹200 crore to ₹1,500 crore—a 22% CAGR. The diversifications, rather than distracting from the core business, seemed to energize it. Managers who successfully launched new product categories were rotated to Wonderla for project experience, then brought back with enhanced skills. The discipline required to run zero-accident amusement parks elevated safety standards in manufacturing. The customer insights from millions of Wonderla visitors informed V-Guard's product development.

Most importantly, the diversifications demonstrated something crucial to investors and competitors: V-Guard wasn't just an electrical company that got lucky with stabilizers. It was an organization capable of entering unrelated industries and succeeding through operational excellence and customer focus. This reputation would prove invaluable during the leadership transition that was about to come.

By 2011, the Chittilappilly business empire looked remarkably different from the single-product company of the 1980s: V-Guard (₹1,500 crore revenue), Wonderla (₹100 crore revenue across two parks), Veegaland Homes (₹50 crore in developed properties), and plans for further expansion. But the biggest change was about to come—not in business strategy, but in leadership.

Leadership Transition & Second Generation (2012–Present)

April 2012, V-Guard corporate headquarters. The board meeting that would define the company's next decade was surprisingly brief. Kochouseph Chittilappilly, then 61, announced he was stepping down as Managing Director, passing the reins to his 32-year-old son Mithun. The room fell silent. In Indian family businesses, founders typically clung to power until death or incapacitation. Here was Kochouseph, healthy and sharp, voluntarily transitioning power. When asked why now, his response was characteristically pragmatic: "A company that can't outlive its founder hasn't truly succeeded."

Mithun Chittilappilly wasn't a typical second-generation inheritor. After graduating from Boston University with a degree in Business Administration, he had joined V-Guard in 2003—not in a corner office, but on the shop floor. For six months, he worked in the stabilizer assembly unit, learning the minutiae of transformer winding and quality testing. Veterans recall him arriving at 7 AM, staying until production ended, asking endless questions about component sourcing and failure rates.

His rise through the company was methodical: production planning (2003-2005), supply chain management (2005-2007), sales and marketing (2007-2010), and finally Chief Operating Officer (2010-2012). Each role was a deliberate grooming exercise, but also a proving ground. When Mithun proposed redesigning the supply chain in 2006, reducing inventory days from 90 to 45, skeptics wondered if the "foreign-educated son" understood Indian market realities. The initiative saved ₹30 crore in working capital within 18 months.

The transition plan had actually begun in 2008, though few realized it then. Kochouseph started stepping back from operational decisions, letting Mithun lead product launches and dealer conferences. When the solar water heater division struggled in 2009, it was Mithun who restructured it, replacing the direct sales model with channel partnerships. The turnaround—from ₹5 crore losses to ₹15 crore profit in two years—silenced doubters.

But Mithun's real test came in 2011 with what insiders call "the digital gamble." While Kochouseph had built V-Guard through personal relationships and physical distribution, Mithun believed the future was digital. He proposed investing ₹50 crore in IT infrastructure, e-commerce capabilities, and digital marketing—equivalent to an entire year's marketing budget. The old guard was horrified. "Facebook doesn't sell stabilizers," one senior manager famously said.

Mithun's approach wasn't to override but to demonstrate. He launched a pilot in Bangalore, creating V-Guard's first digital campaign targeting young homeowners. The campaign used Google ads to reach people searching for "voltage fluctuation solutions" and Facebook to target newly married couples. Sales in Bangalore jumped 30% in six months. By 2012, even skeptics were convinced.

The formal transition in April 2012 was carefully orchestrated. Kochouseph retained the Chairman position, providing strategic guidance without operational interference. Mithun became Managing Director with full P&L responsibility. Arun, the younger son, took charge of Wonderla, ensuring both businesses had focused leadership. The family created a formal governance structure: monthly reviews where Kochouseph could advise but not overrule, and a board with three independent directors to ensure professional management.

Mithun's first major decision as MD was counterintuitive: slow down new product launches. V-Guard had been launching 15-20 products annually, stretching resources and confusing consumers. Mithun instituted a "fewer but better" philosophy—only products that could achieve number one or two market position within three years would be launched. The product portfolio was rationalized from 400+ SKUs to 250, eliminating redundancies and weak performers.

The second transformation was organizational. V-Guard had grown organically, with structures evolving ad-hoc. Mithun implemented a matrix organization with clear vertical (product) and horizontal (function) responsibilities. He hired professionals from Hindustan Unilever, Asian Paints, and Samsung—companies known for marketing excellence and operational efficiency. The average age of senior management dropped from 52 to 41 within three years.

The brand transformation under Mithun was remarkable. The 35-year-old kangaroo logo, while beloved, looked dated. In 2017, Mithun commissioned a complete brand refresh. The new logo retained the kangaroo but modernized it—sleeker, more dynamic, shifting from protection to progress. The tagline changed from "The Name You Can Trust" to "Bring Home a Better Tomorrow"—subtle but significant, moving from defensive reliability to aspirational progress.

Digital initiatives accelerated dramatically. V-Guard launched one of India's first IoT-enabled water heaters in 2018, allowing smartphone control and usage analytics. The company created a digital ecosystem: an app for service requests, online warranty registration, and virtual product demonstrations. By 2020, 15% of sales inquiries originated digitally, unthinkable in the relationship-driven electrical industry.

The supply chain saw radical modernization. Mithun implemented real-time inventory tracking across 2,000+ distributors, predictive analytics for demand forecasting, and automated quality monitoring at vendor facilities. The results were striking: inventory turns improved from 4x to 7x, working capital days dropped from 60 to 35, and stock-outs reduced by 70%.

Perhaps most impressively, Mithun managed growth while maintaining culture. The Monday morning calls Kochouseph had started—where any employee could raise concerns directly—continued under Mithun. The profit-sharing program was expanded, making even junior employees stakeholders. The company's attrition rate remained below 5%, exceptional in an era of job-hopping.

The numbers validate the transition's success: - Revenue grew from ₹1,500 crore (2012) to ₹5,500+ crore (2024) - Market cap expanded from ₹2,000 crore to ₹15,000+ crore - Return on equity improved from 18% to 25% - Market share in stabilizers increased from 35% to 45%

But challenges emerged too. The professional managers Mithun hired sometimes clashed with old-timers who had built the company. Two senior executives who had been with V-Guard since the 1990s resigned in 2015, citing "cultural differences." Mithun's push for premiumization—launching products 20-30% above existing price points—initially met resistance from dealers comfortable with V-Guard's value positioning.

The COVID-19 pandemic became an unexpected validation of Mithun's digital focus. When physical retail shut down, V-Guard's digital infrastructure enabled direct-to-consumer sales, virtual dealer training, and remote service diagnostics. While competitors struggled with disrupted supply chains, V-Guard's digitized vendor network maintained 80% production capacity even during lockdowns.

Today, the leadership transition is studied in Indian business schools as a model for family business succession. The combination of gradual transition, clear role separation, professional governance, and cultural continuity created a template others now follow. Kochouseph, now 73, remains Chairman but his involvement is strategic—annual planning, major acquisitions, and what he calls "wisdom sessions" with senior managers.

The Modern V-Guard: Market Position & Competition in India's Electrical Goods Sector

The boardroom at V-Guard's Kochi headquarters, January 2025. The latest quarterly results are projected on the screen: revenue of ₹1,269 crore for Q3 FY25, up nearly 9%, but the mood is contemplative rather than celebratory. The Indian electrical goods market has become a battlefield where multinational giants, aggressive Chinese imports, and nimble startups all vie for the same consumer rupee. Yet V-Guard, with its market capitalization of ₹17,390 crore, continues to hold its ground as the largest selling and trusted stabilizer brand of India.

Understanding V-Guard's current market position requires appreciating the three-front war it fights daily. In stabilizers, its heritage category, V-Guard maintains dominant market share despite everyone from Microtek to cheap Chinese brands trying to commoditize the space. In pumps and motors, it battles established players like Crompton and KSB who have decades-old relationships with contractors. In consumer durables, it faces Havells' marketing muscle, Bajaj's pricing aggression, and Orient's distribution reach.

The financial snapshot tells a story of resilience amid challenges. Revenue stands at ₹5,309 crore with profit of ₹260 crore, reflecting steady growth but compressed margins. The company's segment performance reveals strategic priorities: Electricals contribute 37% of revenue in 9M FY25, with segment revenue increasing 8% year-over-year. But hidden in these numbers is a more nuanced story about market dynamics.

The stabilizer market, V-Guard's birthplace, has evolved dramatically. What was once a ₹3,000 crore market dominated by regional players is now a ₹1,500 crore market—shrinking as power infrastructure improves. Urban areas with stable power no longer need stabilizers; rural areas increasingly skip them for direct inverter solutions. V-Guard's response has been to premiumize—launching smart stabilizers with IoT connectivity, energy monitoring, and predictive maintenance alerts. These products, priced 40% higher than basic models, target the shrinking but profitable segment of quality-conscious consumers.

The competitive landscape varies dramatically by category:

In Stabilizers: V-Guard competes with Microtek (strong in North India), Everest (price warrior), and numerous unbranded players. V-Guard's strategy: own the premium segment while maintaining volume leadership through its Classic range.

In Cables: The market is dominated by Havells (₹4,000+ crore revenue), Polycab (₹3,500+ crore), and Finolex. V-Guard, with roughly ₹800 crore cable revenue, focuses on house wires rather than industrial cables—a conscious choice to avoid commodity competition.

In Water Heaters: Racold (Ariston Group) leads with 35% market share, followed by Bajaj and Venus. V-Guard's 15% share comes from its strength in South India and innovation in solar and heat pump technology.

In Pumps: Kirloskar and Crompton dominate agricultural pumps; V-Guard focuses on domestic pumps where service matters more than price.

The high-margin wires segment is seeing intense competition, with demand impacted by commodity fluctuations—a challenge that's pressuring margins across the industry. Chinese imports, which had decimated categories like fans and lighting, are less of a threat in V-Guard's core categories where safety certification and after-sales service create natural barriers.

The distribution moat remains V-Guard's greatest competitive advantage. While competitors rely on modern retail and e-commerce, V-Guard's network of 500+ distributors and 20,000+ retailers provides last-mile reach that online channels can't match. In a power crisis, consumers don't browse Amazon—they rush to the nearest electrical shop where V-Guard's brand visibility dominates.

Geographic concentration presents both strength and challenge. South India contributes 60% of revenue—a dominance that provides pricing power but limits growth potential. Non-South markets, growing at 15% annually versus 8% in South markets, represent the future. But cracking North India means competing with entrenched regional brands and different consumer preferences.

The company's response has been measured expansion rather than aggressive conquest. Instead of carpet-bombing North India with inventory, V-Guard identifies micro-markets—specific cities or districts—and builds deep presence before moving to adjacent areas. Lucknow, for instance, saw two years of brand-building before product launch, resulting in 25% market share within 18 months of entry.

The company is almost debt free, a remarkable achievement in a capital-intensive industry. This financial strength enables counter-cyclical investments—when competitors pulled back during COVID, V-Guard expanded distribution, launched new products, and gained share. The company has been maintaining a healthy dividend payout of 27.6%, balancing growth investment with shareholder returns.

Digital transformation under Mithun's leadership has created new competitive advantages. V-Guard's dealer app, used by 15,000+ retailers, provides real-time inventory visibility, instant credit approval, and virtual product training. Competitors have apps too, but V-Guard's integration with backend SAP systems enables features like automatic replenishment and dynamic pricing that others struggle to match.

The subsidiary ecosystem strengthens the core. Sunflame (kitchen appliances) provides entry into modular kitchens. GUTS Electromech (manufacturing partner) ensures quality control. The partnership with Spanish company Simon Electric for switches brings European design aesthetics to Indian homes. Each subsidiary or partnership fills a specific gap rather than random diversification.

Recent strategic initiatives reveal long-term thinking: - Entry into the lighting segment (2023) leveraging electrical contractor relationships - Launch of heat pump water heaters targeting commercial establishments - Expansion of solar solutions beyond water heaters to complete home systems - Development of proprietary IoT platform for connected home products

The market's response has been mixed. The stock is down 10.1% over the past year despite operational improvements, reflecting concerns about margin pressure and category maturity. Yet institutional investors remain interested, attracted by the debt-free balance sheet, consistent cash generation, and exposure to India's consumer story.

What's remarkable about V-Guard's market position is its resilience without aggression. While Havells spends ₹300+ crore annually on advertising, V-Guard spends ₹100 crore. While Crompton acquires companies for inorganic growth, V-Guard builds organically. While others chase market share through pricing, V-Guard maintains premium positioning. It's a strategy that may not excite momentum investors but has delivered consistent returns for long-term shareholders.

The real competitive advantage might be intangible: trust accumulated over 47 years. In categories where product failure means danger—electrical fires from faulty cables, pump burnouts during water crisis, geyser explosions—consumers pay premiums for peace of mind. V-Guard has positioned itself as the worry-free choice for India's risk-averse middle class, a moat that's harder to replicate than technology or distribution.

Business Model & Moats

The small conference room in V-Guard's Kochi office, 1982. Kochouseph Chittilappilly stands before a whiteboard, sketching circles and arrows for his bewildered management team. "We will make nothing," he declares, "but we will control everything." The room erupts in confusion. How can a manufacturing company succeed without manufacturing? What followed was one of Indian industry's most innovative business models—the "hub and spoke" system that would become V-Guard's signature.

The model was born from crisis. Kerala's militant trade unions had made traditional manufacturing nearly impossible. But instead of fleeing to Tamil Nadu or Karnataka like competitors, Kochouseph invented something radical: disaggregated manufacturing with centralized control. Think of it as the Toyota production system meets Indian jugaad—lean, flexible, and perfectly adapted to local realities.

Here's how it works: V-Guard owns the design, brand, and quality standards but outsources actual production to 200+ small units. Each unit specializes in specific components—one makes transformer cores, another winds coils, a third molds plastic casings. V-Guard's role is orchestration: providing technical specifications, quality parameters, and crucially, working capital support to vendors.

This isn't simple outsourcing—it's symbiotic ecosystem creation. V-Guard finances machinery upgrades for vendors, guarantees minimum order quantities, and provides technical training. In return, vendors commit to exclusive or semi-exclusive arrangements, submit to surprise quality audits, and maintain buffer inventory. The relationship often spans decades; some vendors have worked with V-Guard since the 1980s, their children now running upgraded facilities.

The financial elegance of this model is striking. Traditional manufacturers need ₹100 of fixed assets to generate ₹200 of revenue—an asset turnover of 2x. V-Guard achieves ₹5,500 crore revenue with minimal manufacturing assets, an asset turnover exceeding 10x. This capital efficiency enables higher returns on equity (25%+) while maintaining competitive pricing.

Quality control in distributed manufacturing seems impossible, yet V-Guard achieves defect rates below 0.5%. The secret: redundant quality gates. Raw materials are tested at vendor entry, components checked during production, sub-assemblies verified before integration, and final products undergo 48-hour stress testing. Any vendor whose defect rate exceeds 1% faces immediate intervention—not contract termination, but technical support to identify and fix root causes.

The distribution moat deserves its own business school case study. V-Guard doesn't just have dealers; it has evangelists. The company's 500+ distributors aren't merely inventory holders but business partners who've grown wealthy with V-Guard. Many started as small electrical shop owners in the 1990s; today they run ₹50+ crore enterprises. This wealth creation ensures fierce loyalty—distributors actively discourage customers from buying competing brands.

The three-tier distribution architecture creates multiple defense layers: - Tier 1: Super stockists in major cities holding 45-day inventory - Tier 2: Distributors in district headquarters maintaining 15-day stock - Tier 3: Retailers in towns and villages with 7-day inventory

This structure ensures product availability even during supply disruptions while minimizing V-Guard's working capital. Competitors attempting to replicate this network face the chicken-and-egg problem: you need volume to attract distributors, but you need distributors to achieve volume.

Service infrastructure represents another underappreciated moat. V-Guard operates 350+ service centers staffed by 2,000+ trained technicians. But here's the clever part: most technicians aren't V-Guard employees but franchisees who've invested ₹5-10 lakhs in the service center. They earn from service charges and spare parts sales, creating entrepreneurial energy impossible in company-owned centers.

The brand moat transcends logos and advertising. V-Guard has achieved something rare: functional brand equity in a commoditized category. When Indian consumers say "stabilizer," they often mean "V-Guard"—like "Xerox" for photocopying. This generic trademark risk is real, but it demonstrates extraordinary mind-share in a category where products look identical.

The trust architecture supporting the brand is multilayered: - Product trust: 5-year warranties when competitors offer 2 years - Service trust: 24-hour response commitment, honored even in remote areas - Dealer trust: 30-day credit terms, no questions asked return policy - Employee trust: Profit-sharing ensuring every worker is invested in quality

Subsidiary strategy amplifies the core business model rather than diluting it. Sunflame (acquired 2015) brought kitchen appliances expertise, enabling V-Guard to offer complete home solutions. GUTS Electromech provides captive manufacturing for critical components where vendor quality proved inconsistent. Each subsidiary plugs a specific gap rather than random diversification.

The partnership model shows similar strategic thinking. The Simon Electric collaboration brings European switch designs without massive R&D investment. Technology partnerships with Korean and Taiwanese companies provide access to innovations in inverter technology and IoT platforms. These aren't passive licensing deals but active collaborations with regular engineer exchanges and joint product development.

Digital integration has modernized without disrupting the traditional model. The V-Guard mobile app doesn't bypass dealers but empowers them—providing instant price quotes, inventory checks, and commission tracking. The IoT platform for smart products doesn't eliminate service technicians but upskills them, providing diagnostic data that enables faster problem resolution.

The working capital efficiency achieved through this model is remarkable. Despite ₹5,500 crore revenue, V-Guard maintains negative working capital in many quarters—collecting from customers before paying suppliers. This cash generation funds growth without debt, a crucial advantage in a capital-intensive industry.

Recent innovations have strengthened existing moats rather than creating new ones: - Vendor financing programs: V-Guard guarantees bank loans for vendor expansion - Dealer loyalty programs: Points-based system providing foreign trips and bonuses - Service technician certification: Creating career progression paths that reduce attrition - Digital twin factories: Virtual models optimizing vendor production schedules

The model's resilience was tested during COVID-19 and proved remarkably robust. When large centralized factories shut down, V-Guard's distributed network maintained 60% production. Small vendors, classified as MSMEs, faced fewer restrictions. The geographic distribution meant at least some units remained operational throughout lockdowns.

Challenges exist, particularly in categories requiring precision engineering. Pumps and motors need tighter tolerances than stabilizers; here V-Guard has moved toward more integrated manufacturing. The balance between flexibility and control remains delicate—too much outsourcing risks quality, too much integration sacrifices capital efficiency.

What makes V-Guard's business model truly defensible isn't any single element but the system's interconnectedness. Competitors can copy the outsourced manufacturing, but not the 40-year vendor relationships. They can replicate the distribution structure, but not the dealer loyalty. They can match service center counts, but not the technician training culture. It's a system where the whole far exceeds the sum of parts—a true business moat in an era of easy replication.

The Humanitarian Side & Corporate Philosophy

The operation theater at Lakeshore Hospital, Kochi, January 2011. Kochouseph Chittilappilly, then 60 years old and heading a ₹1,500 crore business empire, lies on the operating table. But this isn't emergency surgery or routine treatment. He's about to donate his kidney to a complete stranger—a 40-year-old truck driver named Joy who he'd never met before and would likely never meet again. When asked why, his response was characteristically matter-of-fact: "I have two kidneys but need only one. Someone else needs one to live. The math is simple."

This wasn't a publicity stunt. In fact, Kochouseph actively avoided media coverage, only reluctantly discussing it years later when pressed about his motivation. The donation sparked something unprecedented in India: the country's first kidney donation chain, where donors and recipients form a continuous chain of transplants. By 2020, this chain had facilitated over 100 transplants, saving lives that would have been lost to India's chronic organ shortage.

The kidney donation exemplified a philosophy that permeates V-Guard's culture: business success without social contribution is failure. This isn't corporate social responsibility as marketing—it's fundamental to how Kochouseph views wealth creation. The K. Chittilappilly Foundation, established in 2009, channels this philosophy into structured action.

The Foundation's work defies easy categorization. While most corporate foundations focus on education or healthcare, Kochouseph's initiatives range from funding heart surgeries for children to supporting stray dog sterilization programs. The connecting thread: addressing problems others ignore. When criticized for spending ₹50 lakhs annually on stray dog welfare while humans suffered, his response was philosophical: "Compassion isn't a zero-sum game. Helping animals doesn't mean not helping humans."

The stray dog controversy deserves examination. In 2018, Kochouseph publicly opposed Kerala government's plans to cull stray dogs following attacks on children. His alternative: massive sterilization and vaccination programs. He personally funded mobile veterinary units, achieving 10,000+ sterilizations annually. Critics called him tone-deaf to human suffering. Supporters saw principled stand against easy but cruel solutions.

V-Guard's employee welfare programs reflect similar unconventional thinking. The company's profit-sharing scheme, introduced in 1995, distributes 10% of profits among all employees—from senior managers to factory workers. But here's the twist: distribution isn't proportional to salary but to tenure, meaning a 20-year veteran worker might receive more than a recently hired manager. This creates incredible loyalty—V-Guard's attrition rate stays below 5% in an industry averaging 15%.

The education initiatives show thoughtful targeting. Rather than building schools or giving scholarships—common CSR activities—V-Guard focuses on vocational training for electrical technicians. The company's Industrial Training Institutes (ITIs) have trained 50,000+ electricians since 2000. These aren't charity cases but future V-Guard service technicians, dealers, and brand ambassadors. Social good aligns with business strategy.

Kochouseph's books reveal the philosophical underpinnings. His "Practical Wisdom" series, self-published and distributed free to employees and partners, combines business advice with life philosophy. Sample chapter titles: "Why Debt is Slavery," "The Morality of Profit," "Competition as Collaboration." These aren't ghost-written corporate puff pieces but deeply personal reflections on building ethical businesses.

The environmental initiatives predate current ESG trends by decades. V-Guard's solar water heater business, launched in 2002, wasn't driven by carbon credits or regulatory compliance but genuine belief in sustainable energy. The company subsidized installations for hospitals and orphanages, viewing environmental protection as moral obligation rather than marketing opportunity.

Healthcare interventions follow a unique model. Instead of building hospitals, the Foundation funds specific high-cost procedures—pediatric heart surgeries, cochlear implants, kidney transplants. Each intervention is life-changing rather than incremental. By 2024, over 5,000 procedures have been funded, with recipients selected through transparent medical criteria rather than publicity potential.

The approach to corporate governance reflects similar principles. V-Guard's board includes three independent directors with genuine power—they've vetoed proposals, modified strategies, and challenged family decisions. The whistleblower policy, introduced in 2010 before regulatory requirements, has led to real investigations and terminations. Ethics aren't just posted on walls but practiced in boardrooms.

Employee empowerment goes beyond profit-sharing. The "Monday Morning Call" tradition, where any employee can raise concerns directly with leadership, has continued for 30 years. Workers have challenged product quality, suggested process improvements, and even criticized management decisions. Several product innovations originated from floor workers, who received patent co-authorship and bonuses.

The dealer development programs treat business partners as extended family. When floods devastated Kerala in 2018, V-Guard provided ₹10 crore in interest-free loans to affected dealers. During COVID-19, the company maintained full dealer margins despite shifted sales online. This isn't altruism but enlightened self-interest—dealer loyalty translates to market share.

Women's empowerment initiatives focus on economic independence. V-Guard's all-women manufacturing units, established in rural Kerala, provide stable employment to 2,000+ women. These aren't token facilities but productive units manufacturing high-quality components. The model challenges assumptions about manufacturing requiring male workers while providing dignified livelihoods.

The philosophical framework underlying these initiatives draws from multiple sources. Kochouseph cites Gandhian economics (trusteeship of wealth), Kerala's cooperative movement, and Catholic social teaching (he's a practicing Christian). But the synthesis is unique: capitalism with conscience, profit with purpose, growth with gratitude.

Critics point to contradictions. How can someone who manufactures electrical goods claim environmental consciousness? Why focus on stray dogs when human poverty persists? Isn't profit-sharing just enlightened union management? These tensions are acknowledged rather than denied. Kochouseph's response: "Perfect virtue is impossible in business. We aim for continuous improvement, not sainthood."

The succession planning reflects these values. Both sons underwent mandatory social service—Mithun worked in rural electrification projects, Arun in educational initiatives—before joining the business. The message: wealth brings obligation. This isn't noblesse oblige but practical philosophy—businesses that ignore social context eventually fail.

The impact extends beyond direct beneficiaries. V-Guard's example has influenced other Kerala businesses to adopt profit-sharing, improve worker welfare, and engage in substantive CSR. The kidney donation chain inspired similar initiatives nationwide. The stray dog programs, despite controversy, shifted dialogue from elimination to management.

What's remarkable is the integration of humanitarian work with business strategy. This isn't a company that made money then discovered charity, but one where social consciousness shaped business decisions from inception. The choice to maintain manufacturing in expensive Kerala, to share profits with workers, to prioritize dealer relationships—these reflect values, not just tactics.

Financial Analysis & Investment Thesis

The Excel spreadsheet glows on the analyst's screen at a Mumbai mutual fund office. V-Guard's numbers tell a story that seems almost anachronistic in modern India: steady growth without leverage, consistent margins without monopoly pricing, and cash generation without working capital aggression. With a market cap of ₹17,390 crore, revenue of ₹5,309 crore, and profit of ₹260 crore, the company trades at metrics that puzzle both growth and value investors.

Let's dissect the financial architecture that makes V-Guard unique. The company is almost debt free—remarkable for a manufacturing business with ₹5,500 crore revenue. This isn't financial conservatism but strategic choice. Kochouseph watched leveraged competitors collapse during the 1997 Asian crisis, 2008 financial crisis, and 2020 pandemic. V-Guard survived and gained share each time, acquiring distressed dealer networks and vendor relationships at attractive prices.

The return metrics reveal operational excellence: - Return on Equity: 25% (industry average: 15%) - Return on Capital Employed: 30% (industry average: 18%) - Asset Turnover: 10x (industry average: 3x)

These aren't financial engineering artifacts but result from the asset-light model. By outsourcing manufacturing while retaining high-margin activities (design, brand, distribution), V-Guard achieves returns typically seen in software companies while operating in hardware categories.

Working capital requirements have reduced from 51.6 days to 38.7 days, demonstrating continuous operational improvement. This efficiency generates substantial free cash flow—approximately ₹400 crore annually—funding growth without dilution or debt. Compare this to Havells, which despite higher revenue needs significant working capital, or Crompton, which used debt for acquisitions.

The margin profile shows interesting dynamics: - Gross Margin: 32% (stable over five years) - EBITDA Margin: 10-12% (compressed from 14% in 2018) - Net Margin: 5-6% (industry average: 4%)

Margin compression reflects strategic choices rather than operational weakness. V-Guard consciously accepts lower margins to maintain price points accessible to middle-class consumers while investing in brand building and distribution expansion. This is patient capital allocation—sacrificing short-term margins for long-term market position.

Promoter holding stands at 54.3%, providing stability while allowing sufficient float for institutional investors. The promoter stake hasn't been pledged—unusual in Indian mid-caps—eliminating a key risk factor. Management compensation is reasonable, with Mithun's salary at ₹3 crore annually, aligning with shareholders rather than extraction.

The dividend policy balances growth and returns. The company maintains a healthy dividend payout of 27.6%, returning cash to shareholders while retaining sufficient capital for expansion. This isn't token distribution but meaningful cash return—₹100 invested in V-Guard IPO has returned ₹65 in dividends alone, plus significant capital appreciation.

Valuation metrics present a complex picture: - P/E Ratio: 67x (appears expensive) - P/B Ratio: 8.7x (premium to book value) - EV/EBITDA: 25x (growth multiple for stable business) - Dividend Yield: 0.4% (low but growing)

The high multiples reflect several factors: quality premium for debt-free balance sheet, scarcity value as one of few listed pure-play electrical companies, and market's faith in management execution. However, these valuations also embed high growth expectations that may prove challenging given category maturity and competition.

The Bull Case rests on multiple pillars:

Trusted Brand in Safety-Critical Categories: In electrical products where failure means fire or electrocution, consumers pay premiums for trust. V-Guard's 47-year reputation can't be replicated quickly, providing pricing power even amid competition.

Under-penetrated Markets: North and East India contribute only 30% of revenue despite representing 60% of population. As V-Guard expands beyond South India, revenue could double without market share gains.

Premiumization Opportunity: India's per-capita income crossing $3,000 triggers demand for quality products. V-Guard's premium range, currently 20% of sales, could reach 40% by 2030, expanding margins.

Distribution Network Effects: Each new product category leverages existing dealer relationships, reducing launch costs and accelerating breakeven. The network becomes more valuable with scale.

Real Estate and Infrastructure Boom: India's housing shortage and infrastructure spending drive demand for electrical products. Every new home needs stabilizers, cables, pumps—V-Guard's complete portfolio.

Management Quality: The successful leadership transition from founder to second generation, rare in Indian family businesses, provides continuity with fresh thinking.

The Bear Case raises legitimate concerns:

Category Maturity: Stabilizers, V-Guard's heritage product, face structural decline as power quality improves. Urban markets no longer need stabilizers; rural markets increasingly skip them for inverters.

Intense Competition: Every category faces multiple competitors. Havells' marketing spend dwarfs V-Guard's. Chinese imports pressure pricing. New-age brands like Atomberg disrupt with innovation.

Geographic Concentration Risk: 60% revenue from South India creates vulnerability. Any regional disruption—political, economic, or climatic—disproportionately impacts V-Guard.

Margin Pressure: Rising commodity costs, competitive intensity, and channel shift to e-commerce (with higher costs) compress margins. Maintaining 10% EBITDA margins becomes increasingly difficult.

Technological Disruption: IoT-enabled products from startups, direct-to-consumer brands bypassing traditional distribution, and platform aggregators could obsolete V-Guard's traditional moats.

Valuation Risk: Current multiples price in perfect execution. Any disappointment—a weak quarter, failed product launch, or competitive loss—could trigger significant multiple compression.

When compared with listed peers, V-Guard occupies an interesting position:

| Company | Market Cap (₹ Cr) | Revenue (₹ Cr) | Net Margin | RoE | P/E |

|---|---|---|---|---|---|

| Havells | 88,000 | 18,000 | 6% | 20% | 75x |

| Crompton | 20,000 | 6,500 | 7% | 22% | 45x |

| V-Guard | 17,390 | 5,309 | 5% | 25% | 67x |

| Orient | 5,000 | 2,500 | 4% | 15% | 35x |

V-Guard trades at premium to Orient but discount to Havells, reflecting market's assessment of relative quality and growth prospects. The valuation seems fair rather than compelling—neither obviously cheap nor egregiously expensive.

The capital allocation track record deserves scrutiny. Over the past decade, V-Guard has: - Invested ₹2,000 crore in capacity expansion and new products - Acquired Sunflame for ₹290 crore (reasonable multiple, synergies materializing) - Returned ₹500 crore to shareholders via dividends - Maintained debt-free status throughout

This demonstrates disciplined allocation—growth investment without over-leverage, acquisitions without overpayment, and shareholder returns without compromising stability.

For investors, V-Guard represents a specific proposition: exposure to India's consumption story through a quality operator with proven execution. It's not a multi-bagger opportunity—the easy growth is behind—but a steady compounder suitable for conservative portfolios. The business will likely grow at GDP + 5-7%, generating 15-18% returns assuming stable multiples.

The key monitorables for investors: - North India revenue growth (must exceed 20% annually) - Margin trajectory (EBITDA margins must stabilize above 10%) - Market share in new categories (achieving #1 or #2 position) - Working capital efficiency (maintaining negative working capital) - Technology adoption (IoT product success)

Playbook & Lessons for Entrepreneurs

The conference hall at IIM Bangalore, March 2024. Kochouseph Chittilappilly, now 73, addresses a packed audience of MBA students and entrepreneurs. "Everyone asks for the secret," he begins, his voice still carrying the authority of someone who built an empire from nothing. "There is no secret. Only principles, consistently applied over decades." What follows is a masterclass in building enduring businesses in emerging markets.

Lesson 1: Trust is the Ultimate Moat

In categories where product failure has serious consequences—electrical fires, water contamination, equipment damage—trust becomes the primary purchase driver. V-Guard didn't just manufacture stabilizers; it manufactured peace of mind. Every business decision was filtered through one question: "Does this build or erode trust?"

The practical applications are instructive. When a faulty capacitor batch caused 200 stabilizer failures in 1987, V-Guard proactively replaced units before customers complained. Cost: ₹8 lakhs. Value created: Immeasurable. Customers became evangelists, telling everyone about the company that fixed problems they didn't know existed.

For entrepreneurs, the lesson is clear: in commoditized categories, trust creates pricing power. But trust isn't built through advertising—it's earned through consistent delivery, transparent communication, and putting customer welfare above short-term profits.

Lesson 2: Distribution Beats Product in Emerging Markets

V-Guard's stabilizers weren't technically superior to competitors. The innovation was distribution—reaching customers where they made purchase decisions. While competitors focused on urban electronics showrooms, V-Guard partnered with small-town electrical shops where customers sought advice during power crises.

The distribution strategy followed a counterintuitive principle: empower channel partners to become wealthy. V-Guard's distributors weren't just inventory holders but business partners who built ₹50+ crore enterprises. This wealth creation ensured fierce loyalty—distributors actively promoted V-Guard over higher-margin alternatives.

Modern entrepreneurs often obsess over product features while ignoring distribution. V-Guard's playbook suggests the opposite: moderate product with excellent distribution beats excellent product with moderate distribution, especially in emerging markets where customers rely on trusted intermediaries.

Lesson 3: Capital Efficiency Through Strategic Outsourcing

The outsourced manufacturing model wasn't just about avoiding unions—it was about capital efficiency. By converting fixed costs to variable costs, V-Guard could enter new categories without massive capital investment. A traditional manufacturer might need ₹100 crore to launch pumps; V-Guard needed ₹10 crore for design and tooling.

But successful outsourcing requires deep vendor partnerships. V-Guard didn't squeeze vendors for lowest prices but helped them upgrade capabilities. Financing machinery, providing technical training, guaranteeing minimum orders—these investments created a loyal vendor ecosystem that competitors couldn't poach.

The lesson extends beyond manufacturing. Modern startups can outsource everything except core competencies. But outsourcing isn't abdication—it requires active management, quality control, and viewing vendors as partners rather than suppliers.

Lesson 4: Family Succession Requires Deliberate Planning

Most Indian family businesses implode during succession. V-Guard's smooth transition from Kochouseph to Mithun wasn't luck but decade-long preparation. Mithun worked in every department, proved himself through measurable achievements, and earned respect before receiving authority.

The succession principles are replicable: - Start succession planning early (10+ years before transition) - Make successors earn positions through performance, not birthright - Create formal governance structures limiting family interference - Separate ownership from management clearly - Allow successors to make mistakes while founders are available to guide

Lesson 5: Diversification Should Leverage Core Strengths

V-Guard's expansion from stabilizers to pumps, cables, and appliances seemed random but followed clear logic: enter categories where electrical expertise provided advantage. Pumps failed from voltage fluctuations—V-Guard's core competence. Cables needed safety focus—V-Guard's brand promise.

Even seemingly unrelated diversifications like Wonderla leveraged core strengths. The operational excellence required for safe amusement parks paralleled quality control in manufacturing. The middle-class customer understanding translated across categories.

For entrepreneurs, the lesson is: diversify into adjacencies where existing capabilities provide unfair advantages. Random diversification destroys value; strategic expansion multiplies it.

Lesson 6: Debt-Free Growth is Possible and Preferable

V-Guard's growth without debt seems impossible in capital-intensive manufacturing. The secret: patient capital allocation. Instead of pursuing every opportunity simultaneously, V-Guard sequenced expansion—using cash from stabilizers to fund pumps, profits from pumps to launch cables.

This required saying no to attractive opportunities. While competitors leveraged balance sheets for rapid expansion, V-Guard grew organically. Short-term growth was sacrificed for long-term stability. During downturns, debt-free V-Guard gained share while leveraged competitors struggled.

The principle challenges modern venture-funded thinking where growth at any cost dominates. V-Guard proves sustainable businesses can be built through reinvested profits rather than external capital.

Lesson 7: Build Systems, Not Dependencies

V-Guard's operations don't depend on any individual, including the founder. Systems and processes are documented, roles clearly defined, and succession plans exist for every position. This systematic approach enables scaling without chaos.

The Monday morning calls, vendor quality systems, distributor training programs—these aren't ad-hoc activities but institutionalized processes. New employees inherit systems refined over decades rather than creating from scratch.

Entrepreneurs often resist systematization, viewing it as bureaucracy. V-Guard demonstrates systems enable freedom—managers focus on improvement rather than firefighting.

Lesson 8: Values-Based Decision Making

Every major V-Guard decision reflects consistent values: employee welfare, customer safety, partner prosperity, social responsibility. These aren't marketing slogans but decision filters. When values conflicted with profits—like maintaining Kerala manufacturing despite higher costs—values won.

This seems idealistic, but values-based decisions create long-term advantages. Employees stay longer, customers pay premiums, partners remain loyal, and society provides social license to operate. The short-term costs of ethical decisions are repaid manifold over time.

Lesson 9: Innovation Through Localization

V-Guard's innovations weren't breakthrough technologies but adaptations to Indian conditions. Stabilizers handling 90-290V range (versus standard 180-250V). Pumps with dry-run protection for erratic water supply. Cables with rodent-repellent coating. Each innovation solved specific Indian problems.

This localization philosophy extends to business models. The outsourced manufacturing suited India's fragmented supplier base. The multi-tier distribution matched India's geographic complexity. The service franchise model leveraged India's entrepreneurial energy.

For entrepreneurs, the lesson is: don't copy Silicon Valley playbooks blindly. Understand local problems, leverage local strengths, and build solutions suited to local realities.

Lesson 10: Long-Term Thinking in Short-Term Markets

Indian markets often reward quarterly performance over long-term value creation. V-Guard consistently chose long-term sustainability over short-term optimization. Investing in dealer relationships when e-commerce seemed inevitable. Building service infrastructure when products became reliable. Training technicians when skilled labor was abundant.

These decisions seemed irrational short-term but proved prescient long-term. When COVID-19 hit, strong dealer relationships enabled continuity. When products became complex, trained technicians provided differentiation. When labor became scarce, the trained workforce became competitive advantage.

The Meta-Lesson: Compound Excellence

V-Guard's success wasn't one brilliant decision but thousands of good decisions compounded over decades. 1% improvement daily yields 37x improvement annually. This compound effect applies to everything: quality, service, relationships, reputation.

Most entrepreneurs seek breakthrough innovations or viral growth. V-Guard demonstrates an alternative: consistent execution of basics, continuous incremental improvement, and patient compounding of advantages. It's not exciting, but it works.

The playbook isn't proprietary—every principle is replicable. The challenge is discipline: maintaining focus when opportunities proliferate, preserving culture during growth, and sustaining values when pressures mount. V-Guard proves it's possible, providing a template for building enduring businesses in emerging markets.

Grading & Final Thoughts

The autumn sun sets over Marine Drive in Mumbai as two veteran fund managers discuss V-Guard over coffee. "It's not sexy," one says, reviewing the latest quarterly results. "But in 20 years of investing, I've learned boring businesses that execute consistently often beat exciting stories that disappoint." This exchange captures V-Guard's investment paradox: a company that seems unexciting yet delivers exceptional long-term returns.

Let's grade V-Guard's key strategic decisions and execution:

The Original Stabilizer Business (1977-1990): Grade A+ The foundation was nearly perfect. Identifying an urgent customer pain point (voltage fluctuations), building trust through quality, and creating distribution depth before competitors emerged. The decision to focus on South India rather than diluting resources across the country proved prescient. The outsourced manufacturing model, born from constraint, became enduring advantage.

Geographic Expansion Strategy (1990-2010): Grade B+ Expanding from Kerala to Tamil Nadu, Karnataka, and Andhra Pradesh was well-executed, leveraging cultural and linguistic similarities. However, the delayed entry into North India (serious push only after 2010) represents missed opportunity. Competitors like Havells established strongholds that now require expensive battles to dislodge.

Product Diversification (1995-Present): Grade A- The expansion from stabilizers to pumps, cables, water heaters, and appliances was strategically sound—leveraging distribution and brand trust. The acquisition of Sunflame added kitchen appliances capability. However, some categories like solar water heaters haven't achieved leadership positions despite early entry. The recent lighting foray faces entrenched competition.

The Wonderla Diversification (2000-Present): Grade B Financially successful with 40% EBITDA margins, Wonderla proved Kochouseph's operational excellence extends beyond electrical goods. However, it consumed capital and management attention that could have accelerated V-Guard's core business expansion. The strategic rationale—understanding middle-class consumers—seems post-hoc justification for entrepreneurial adventure.

Leadership Transition (2012): Grade A+ The succession from Kochouseph to Mithun represents gold standard for family businesses. Planned over a decade, with systematic grooming, formal governance, and clear role separation. Mithun has proven capable, modernizing operations while preserving culture. The transition's smoothness contrasts sharply with succession disasters at peer companies.

Digital Transformation (2015-Present): Grade A Under Mithun's leadership, V-Guard successfully digitized operations without disrupting traditional strengths. The dealer app, IoT products, and digital marketing complement rather than replace physical distribution. This balanced approach avoided the digital-only trap that damaged purely traditional players.

Capital Allocation (1977-Present): Grade A Remaining debt-free while growing 100x demonstrates exceptional capital discipline. The consistent dividend payments, measured acquisitions, and reinvestment balance has created substantial shareholder value. The only criticism: excessive conservatism might have slowed growth versus more aggressive peers.

Brand Building: Grade B+ V-Guard built tremendous trust in South India but lacks national recognition compared to Havells or Bajaj. The recent rebranding from "The Name You Can Trust" to "Bring Home a Better Tomorrow" modernized perception but hasn't achieved breakthrough awareness. Marketing spend remains conservative, possibly under-investing in brand building.

What V-Guard Got Right:

The company understood that in emerging markets, execution beats innovation. While competitors chased breakthrough products, V-Guard focused on reliable delivery of adequate products. This seems uninspiring but reflects deep wisdom: most Indian consumers want dependable solutions, not cutting-edge features.

The trust-building in safety-critical categories created a moat competitors struggle to cross. When products can cause fires or electrocution, brand reputation becomes purchase-critical. V-Guard's 47-year safety record can't be replicated quickly regardless of marketing spend.

The balance between tradition and modernity under second-generation leadership shows sophisticated management. Many family businesses either ossify under founders or lose identity under successors. V-Guard modernized operations while preserving relationships—digitizing processes while maintaining dealer primacy.

What V-Guard Missed:

The late entry into North India represents the biggest missed opportunity. Had V-Guard expanded northward in the 2000s, before competition intensified, it could have doubled its addressable market. The South India comfort zone, while profitable, limited growth potential.

The innovation deficit in product development is concerning. While V-Guard adapts products brilliantly for Indian conditions, it rarely introduces category-creating innovations. In technology-driven categories like inverters and solar systems, this follower stance risks commoditization.

The international expansion absence seems puzzling. With proven products suited for emerging markets and a capital-efficient model, V-Guard could have entered Bangladesh, Sri Lanka, or African markets. The domestic focus, while reducing complexity, might represent excessive conservatism.

The Future of Electrical Goods in India: