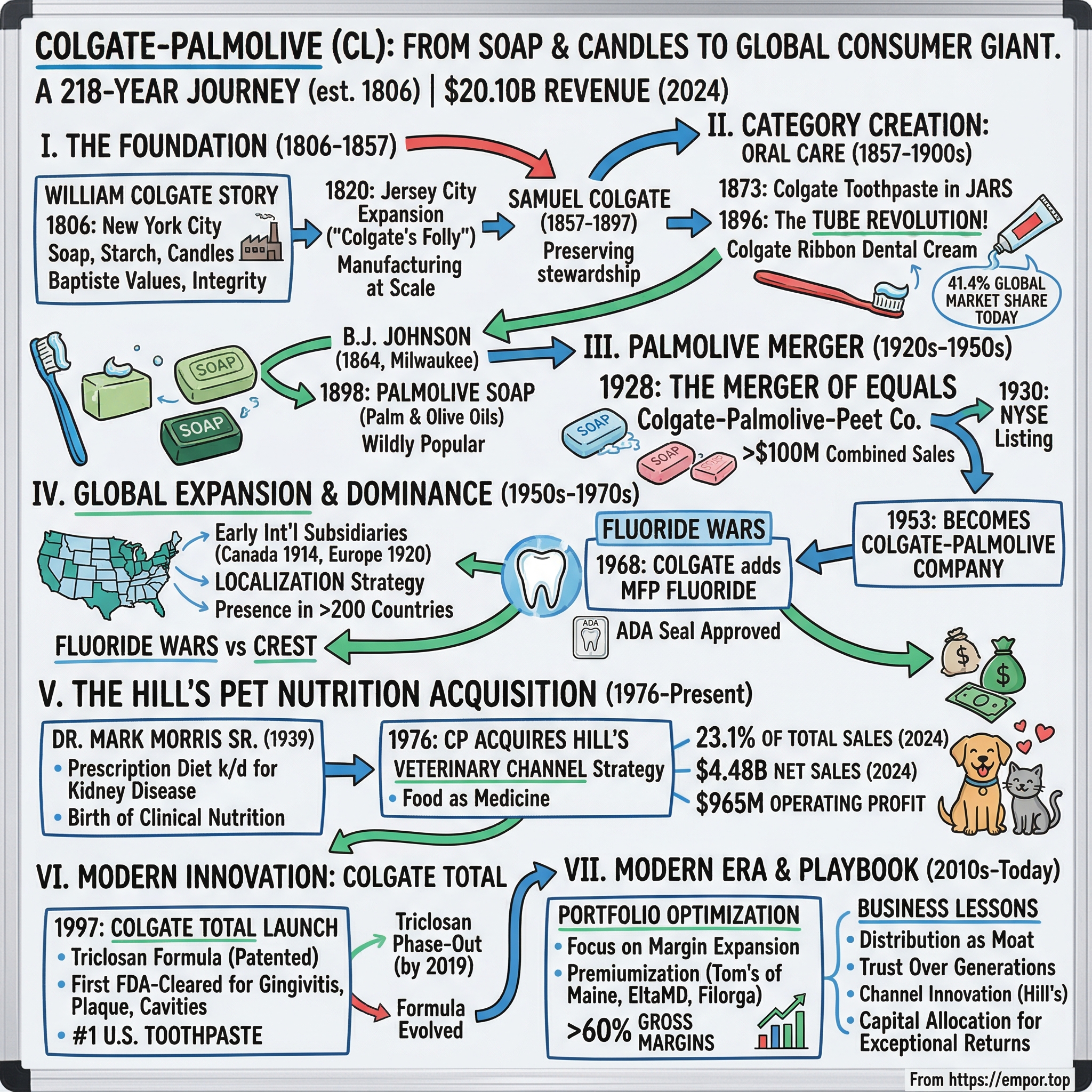

Colgate-Palmolive: From Soap & Candles to Global Consumer Giant

I. Introduction & Episode Roadmap

Picture this: You wake up, stumble to the bathroom, and squeeze toothpaste onto your brush. Later, you wash dishes after breakfast, then feed your dog. In those three mundane moments, you've likely touched products from a 218-year-old company that generates $20.10 billion in annual revenue with gross margins north of 60%. That company is Colgate-Palmolive.

Here's the paradox that should fascinate any serious investor: How does a company selling what are essentially commodities—toothpaste, soap, pet food—maintain pricing power that would make a luxury brand jealous? How does a business founded when Thomas Jefferson was president stay relevant in the age of TikTok and direct-to-consumer disruption?

The answer isn't just about brand strength, though Colgate commands 41.4% global market share in toothpaste. It's about something more fundamental: the systematic construction of competitive moats across distribution, innovation, and consumer trust that compound over centuries. This is the story of how William Colgate's modest soap and candle factory on Dutch Street became a global empire that touches 5 billion people daily.

We'll trace this journey from pre-Civil War America through the creation of entirely new product categories, examine how religious values shaped corporate culture, dissect the strategic genius of the Hill's Pet Nutrition acquisition, and understand why this "boring" consumer products company has delivered returns that would make Silicon Valley envious. Along the way, we'll uncover the playbook for building enduring value in consumer markets—lessons that apply whether you're analyzing CPG giants or the next generation of consumer brands.

The structure ahead: We'll start with William Colgate's immigrant story and the Baptist ethos that shaped early company culture. Then we'll explore the pivot from soap to oral care that created an entire category. We'll dissect the three-way merger that formed modern Colgate-Palmolive, track the global expansion that preceded most multinationals by decades, and examine how smart acquisitions like Hill's created billion-dollar profit centers. Finally, we'll analyze the modern playbook of portfolio optimization and premiumization that keeps this two-century-old company growing.

II. The William Colgate Story & Early Foundation (1806–1857)

The year is 1783. A young William Colgate watches his father Robert lose everything. The elder Colgate, a farmer and political activist in Kent, England, had backed the wrong side—supporting the American Revolution and radical political reform. Facing financial ruin and political persecution, the family makes a desperate choice: emigrate to America. They settle first in Maryland, where William learns soap-making as an apprentice, a skill that would define not just his life but the next two centuries of American consumer products. By 1806, twenty-three-year-old William arrives in New York City with his soap-making skills and a determination forged by family hardship. In 1806 William set up a starch, soap and candle business on Dutch Street in Manhattan. But this wasn't just any random location. The young entrepreneur displayed remarkable business acumen: the Mayor of New York lived on Dutch Street, and in the immediate vicinity of his little factory were the homes of many other prominent men of the day. Every influential citizen passing by would see Colgate's factory—an early lesson in the power of location and proximity to power.

The initial partnership with Francis Smith gave Colgate the capital to start, but it was his brother Bowles who would become his long-term partner after Colgate bought out Smith in 1813. After buying Smith out in 1813, Colgate then partnered with his brother, Bowles Colgate [1789-1845] from 1813 to 1844, with the business now named William Colgate & Company. This wasn't just a business partnership—it was a family enterprise built on shared Baptist values that would permeate company culture for generations.

The Jersey City expansion of 1820 reveals Colgate's willingness to take calculated risks. When Colgate moved his company to Jersey City in 1820 to produce starch, it was called "Colgate's Folly." Critics thought he was insane to build manufacturing capacity across the Hudson River, away from Manhattan's commercial center. But Colgate understood something his contemporaries missed: manufacturing at scale required space and access to raw materials that Manhattan couldn't provide. By 1847, the "folly" had become a sprawling complex that would anchor Colgate's manufacturing for the next century. The Baptist ethos wasn't just window dressing—it fundamentally shaped how the Colgates ran their business. Colgate was a tither to his faith throughout his long and successful business career, giving at minimum 10% of his income to religious causes. But this went beyond simple charity. Beside serving the Bible societies, Colgate also supported Hamilton Literary and Theological Institution (later Madison University and Theological Seminary). Likewise, he regularly gave to the Baptist Missionary Union, and he even fully funded a foreign missionary on his own. The home itself became a center of Baptist social life, with his home was known as an especially pleasant and welcoming place to be.

When William Colgate died on March 25, 1857, the transition to his son Samuel revealed something profound about company culture and values. When William Colgate died in 1857, Samuel took over the business (he did not want to continue the business but thought it would be the right thing to do), reorganizing it as Colgate & Company. This detail—that Samuel felt duty-bound despite personal reluctance—speaks volumes about the sense of stewardship that would define Colgate leadership for generations. This wasn't about personal ambition; it was about preserving and growing something larger than oneself.

Samuel's 40-year reign (1857-1897) would transform a successful soap business into the foundation of a consumer products empire. He brought the same religious fervor to business as his father, serving as president of the Society for the Suppression of Vice, to which he was a friend and ally of Anthony Comstock. He was also a member of the executive committee of the American Baptist Missionary Union and of the American Tract Society. Perhaps most remarkably, he assembled 30,000 volumes of reports (now at the American Baptist Historical Society), comprising the documentary records of the Baptist denomination—showing the same systematic approach to religious history that he would bring to business operations.

The Baptist values created an unusual corporate culture: ethical business practices weren't just good PR, they were religious imperatives. This manifested in product quality (no shortcuts), fair dealing with suppliers and retailers, and a paternalistic but genuine concern for worker welfare. In an era of robber barons and exploitative labor practices, Colgate stood apart. The company's reputation for integrity became a competitive advantage, especially as they moved into products that required consumer trust—like those that would go into people's mouths.

III. From Soap to Toothpaste: The Category Creation (1857–1900s)

Samuel Colgate stared at the ledgers in 1872. The soap business was solid, profitable even, but commoditizing rapidly. Competitors could make soap just as well as Colgate could. What the company needed wasn't just another product—it needed to create an entirely new category where first-mover advantage could compound for decades. The answer would come from an unlikely source: the emerging science of oral hygiene.

In 1872, Samuel introduced Cashmere Bouquet, the world's first milled perfumed toilet soap. Then in 1873, Colgate introduced its first Colgate Toothpaste, an aromatic toothpaste sold in jars. This wasn't simply product line extension—it was strategic genius. Colgate recognized that oral care represented a massive untapped market. Most Americans in the 1870s cleaned their teeth (if at all) with rough powders, salt, or homemade concoctions. The idea of a commercially produced, consistently formulated toothpaste was revolutionary.

The jar format seems quaint now, but it solved real problems. It protected the product from contamination, allowed for attractive packaging that could sit on a bathroom shelf, and most importantly, signaled that this was a premium product worth paying for. Colgate wasn't just selling toothpaste; they were selling the idea that oral hygiene was part of modern, civilized life.

But the real breakthrough—the innovation that would define not just Colgate but the entire oral care industry—came in 1896. In 1896, the company sold its first toothpaste in a collapsible tube (which had recently been invented by dentist Washington Sheffield), named Colgate Ribbon Dental Cream. The tube wasn't Colgate's invention, but they were the first to recognize its transformative potential at scale. This wasn't just a packaging innovation; it was a user experience revolution. The tube made toothpaste portable, hygienic, and easy to dispense. It turned tooth-brushing from a messy chore into a convenient daily ritual. Colgate introduces toothpaste in a collapsible tube in 1896, revolutionizing not just packaging but the entire user experience. This innovative packaging also helped to keep the toothpaste fresh and protected it from contamination, while cutting down the cost of producing toothpaste significantly and eliminating the unhygienic practice of scooping the paste from shared jars onto a toothbrush.

Consider the marketing genius of the moment. The tube allowed Colgate to brand every morning ritual. Unlike soap, which disappeared with use, the tube sat on bathroom shelves as a permanent advertisement. It created what we now call "share of mind"—every squeeze reinforced the Colgate name. The company understood something fundamental about consumer products: convenience drives adoption, but habit drives lifetime value.

In 1911, Colgate distributed two million tubes of toothpaste and toothbrushes to schools and hygienists to demonstrate tooth brushing. This wasn't charity—it was strategic market development. By teaching children to brush with Colgate products, they created customers for life. The educational component also positioned Colgate as the authority on oral health, not just a product manufacturer. This playbook—education as marketing—would be copied by consumer companies for the next century.

The research lab established in 1896 deserves special attention. Also in 1896, Colgate hired Martin Ittner and under his direction founded one of the first applied research labs. While competitors treated soap and toothpaste as commodity products, Colgate invested in scientific innovation. This wasn't Silicon Valley-style disruption; it was methodical, incremental improvement that compounded over decades. The lab would become the source of countless innovations that maintained Colgate's edge even as the basic product remained unchanged.

By 1906, when the five sons of Samuel Colgate incorporated the company, Colgate had achieved something remarkable: they had transformed tooth-brushing from an occasional practice of the wealthy into a daily ritual for the middle class. Colgate is incorporated by the five sons of Samuel Colgate in 1906, and by 1908, when Colgate & Company celebrates its 100th anniversary, their product line includes over 800 different products. The company wasn't just selling toothpaste anymore—they were selling the promise of modern hygiene, social acceptability, and health.

The transition from soap-maker to oral care innovator reveals a deeper truth about successful pivots: they're rarely about abandoning the past but rather applying existing capabilities to new opportunities. Colgate's expertise in chemistry, manufacturing, and distribution—built over decades in soap—transferred perfectly to oral care. The Baptist values of cleanliness and purity resonated even more strongly with products that went into people's mouths. What looked like diversification was actually doubling down on core competencies.

IV. The Palmolive Merger: Creating a CPG Powerhouse (1920s–1950s)

The roaring twenties brought a new challenge to American business: scale. Regional champions were becoming national players, and the consumer products industry was consolidating rapidly. In Milwaukee, a parallel story to Colgate's had been unfolding—one that would soon intersect in one of the era's most significant mergers.B.J. Johnson's story begins in 1864 Milwaukee, where this New York native established what would become a soap empire. Benedict Johnson arrived in the city from Buffalo, where he had been working for the Beard Soap Works. With an advance from his old boss, Johnson established B. J. Johnson & Company to manufacture soap and related products. But Johnson's real breakthrough came in 1898 with a product that would change everything: In 1898, the company introduced the soap that would become one of Milwaukee's most famous native products. Using palm and olive oils as well as cocoa butter, the result was a distinctive light green bar the company called Palmolive. The product proved wildly popular, thanks in large part to an advertising campaign that promoted it as an exotic cleanser that would have been favored in the age of the Pharaohs.

The marketing genius behind Palmolive deserves scrutiny. By the early 1900s, Palmolive was the world's best-selling soap—surpassing even established players like Colgate. The exotic Egyptian theme wasn't just clever advertising; it was strategic positioning. In an era when most soaps were marketed on utilitarian benefits, Palmolive sold aspiration and luxury to the emerging middle class. The green color, derived from the olive oil, became an instant visual differentiator on store shelves.

The path to merger began with consolidation in the soap industry. In 1926 Charles S. Pierce, then president of Palmolive Soap Co. announced "tentative plans for the consolidation" of the Milwaukee-based Palmolive Soap company and the Peet Brothers Soap Company of Kansas City. It was said at the time the combined company assets would exceed US$45,000,000. The Peet Brothers brought their own strengths—strong distribution in the Midwest and West, plus established brands like Crystal White soap.

Then came the blockbuster announcement. In June 1928, rumors started within the investment community that "officials of the Palmolive-Peet Co. are negotiating to purchase the Colgate Co." privately held by the Colgate family. This wasn't just another acquisition—it was a transformative merger of equals. The merger combined the three oldest and largest soap and perfumery companies in the US and was effective July 1, 1928. The combined company was named the "Colgate Palmolive Peet Company. The combined pre-merger sales in 1927 of the three companies exceeded $100,000,000.

The numbers tell the story of scale: The newly combined company had seven US manufacturing facilities as well as factories in 14 foreign countries. This wasn't just about domestic consolidation—it was about building a global platform before "globalization" was even a concept. The merger created synergies that went beyond cost savings: Colgate's strength in oral care, Palmolive's dominance in beauty soap, and Peet's distribution network created a consumer products powerhouse.

The timing was both brilliant and precarious. The merger closed on July 1, 1928—just 15 months before the Wall Street Crash of 1929. In fact, management had even more ambitious plans: On October 25, 1929, management signed an agreement to merge the company with Kraft Phenix Cheese Corporation (forerunner of Kraft Foods) and Hershey Chocolate Company. The crash killed that deal, which in retrospect was fortunate—the focused consumer products company that emerged would prove more valuable than a sprawling conglomerate.

The integration wasn't without challenges. Palmolive-Peet's management initially assumed control of the combined organization. This created tensions as three distinct corporate cultures—Colgate's East Coast Baptist conservatism, Palmolive's Midwest marketing innovation, and Peet's Western entrepreneurialism—had to mesh. The solution was pragmatic: keep the best of each culture while standardizing operations and eliminating redundancies.

On March 13th, 1930, Colgate is first listed on the New York Stock Exchange. This public listing was crucial—it provided liquidity for the founding families while giving the company currency for future acquisitions. The Depression years that followed would test the newly merged company, but the diversified product portfolio provided resilience. When consumers couldn't afford luxury items, they still needed soap and toothpaste.

By 1953, the companies became a joint venture, known as the Colgate-Palmolive Company. The "Peet" was finally dropped from the name, signaling complete integration. The company that emerged from this decades-long merger process was fundamentally different from its predecessors: a professionally managed, publicly traded corporation with global ambitions and the scale to realize them.

V. Global Expansion & Category Dominance (1950s–1970s)

The post-war era presented an unprecedented opportunity. Europe needed rebuilding, emerging markets were modernizing, and American consumer culture was becoming the global aspiration. Colgate-Palmolive's international expansion wasn't accidental—it was systematic and decades ahead of most American companies. The story begins earlier than most realize. Colgate establishes its first international subsidiary in Canada in 1914, and by 1920, Colgate begins establishing operations in Europe, Asia, Latin America and Africa. This timing is crucial—while most American companies were still figuring out their domestic markets, Colgate was planting flags globally. The First World War had created both need and opportunity: devastated European markets needed rebuilding, colonial territories were opening to trade, and American products carried the aura of modernity.

The genius wasn't just in being early—it was in the approach. Rather than exporting American products unchanged, Colgate adapted to local markets from the beginning. In Latin America, they discovered consumers preferred stronger fragrances. In Asia, smaller package sizes matched different purchasing patterns. This localization strategy, revolutionary for its time, would become the template for global CPG expansion. The fluoride wars of the 1960s represent one of the most consequential battles in consumer products history. In 1955 Colgate-Palmolive lost its number-one ranking in the toothpaste market when the rival consumer-goods manufacturer Procter & Gamble Co. began selling Crest, the first toothpaste with fluoride. This wasn't just a market share loss—it was an existential threat. P&G had secured the American Dental Association's seal of approval, turning Crest into the "scientific" choice while Colgate looked outdated.

Colgate's response was brilliant and revealing of corporate strategy under pressure. Although developed by a chemist at Procter and Gamble, its use in toothpaste (Colgate toothpaste and Ultra Brite) was patented by Colgate-Palmolive, as Procter and Gamble was engaged in the marketing of Crest toothpaste (containing stannous fluoride, marketed as "Fluoristan"). In 1968: Colgate toothpaste adds MFP Fluoride, clinically proven to reduce cavities. The MFP formulation allowed Colgate to circumvent P&G's patents while delivering similar cavity-fighting benefits.

The clinical data was impressive: Clinical data from studies that included the use of a placebo control group indicated reductions in dental caries of approximately 17% to 34% with use of this dentifrice. By 1969, Colgate toothpaste with MFP has been classified in Group A and the appropriate use of the Council's seal of acceptance has been authorized. This ADA approval was crucial—it put Colgate back on equal scientific footing with Crest.

The diversification attempts of this era tell a different story—one of strategic missteps that would ultimately lead to greater focus. Ajax cleanser is launched in 1947, establishing a powerful now-global brand equity for cleaning products. By 1966, Palmolive dishwashing liquid is introduced, and 1972 saw the launch of Irish Spring. These seemed like natural extensions—if consumers trusted Colgate to clean their teeth, why not their dishes and laundry?

But the company also ventured into stranger territory. Tennis equipment, golf products, and even a failed attempt at frozen lasagna in 1980 revealed the dangers of brand extension. The cosmetics push through the Helena Rubinstein acquisition similarly struggled. Consumers had clear mental categories: Colgate meant oral care and basic household products. Stretching beyond that confused the brand message and diluted management focus.

George Henry Lesch, president, CEO, and chairman of the board of Colgate-Palmolive in the 1960s and 1970s, transformed the firm into a modern company with major restructuring. His focus on international markets proved prescient. Between 1914 and 1933 the company began establishing international operations, with subsidiaries in Canada, Australia, Europe, and Latin America. But it was the systematic expansion of the 1960s and 1970s that created true global scale.

The numbers tell the story: by the late 1970s, international operations were generating more profit than the U.S. business. This wasn't just about exporting American products—it was about building local manufacturing, adapting to local preferences, and often being the first major CPG company in emerging markets. When competitors finally arrived, Colgate had already built distribution networks and consumer loyalty that proved nearly impossible to dislodge.

VI. The Hill's Pet Nutrition Acquisition & Transformation (1976–Present)

In 1976, Colgate made what seemed like an odd acquisition: a specialty pet food company called Hill's Pet Nutrition. Wall Street was puzzled. Why would a toothpaste company buy a dog food business? The answer would reveal itself as one of the most brilliant strategic moves in CPG history, creating a business that today generates over $4.5 billion in revenue with margins that make even luxury brands envious. The origin story reads like veterinary mythology. The year was 1939 when a young blind man named Morris Frank was traveling the country with his dog, Buddy. Buddy was suffering from kidney failure, and Mr. Frank asked Dr. Mark Morris Sr. for help. Dr. Morris believed he could find a nutritional solution to Buddy's issues, so he developed a new pet food with his wife, Louise Morris, in their kitchen. This wasn't just pet food innovation—it was the birth of veterinary clinical nutrition as a discipline.

Dr. Morris's insight was revolutionary: pet diseases could be managed through precisely formulated nutrition. He wasn't just making better pet food; he was creating therapeutic nutrition—food as medicine. Morris contracted with Burton Hill of the Hill Packing Company in Topeka, Kansas, to can the food with a new name, Canine k/d, and licensed Hill to produce his pet food formulas. Prescription Diet k/d becomes the world's first veterinarian-prepared food for the management of a canine disease.

When Colgate acquired Hill's in 1976—Colgate-Palmolive acquires Hill's Pet Nutrition. Today, Hill's is the global leader in pet nutrition and veterinary recommendations—they weren't just buying a pet food company. They were acquiring a unique business model: the veterinary channel strategy. Hill's products weren't sold in grocery stores alongside Alpo and Purina. They were sold through veterinarians, creating a powerful moat that competitors couldn't easily cross.

The veterinary channel was genius for multiple reasons. First, it positioned Hill's as medicine, not commodity pet food, justifying premium pricing. Second, veterinarians became the sales force—their recommendations carried more weight than any advertising campaign. Third, it created switching costs: once a veterinarian recommended Hill's for a pet's specific condition, owners rarely changed brands. Fourth, it provided invaluable data and feedback loops from veterinary professionals that improved product development.

The expansion beyond prescription diets into Science Diet for healthy pets multiplied the opportunity. Pet owners who used Hill's prescription food for sick pets naturally gravitated to Science Diet for prevention. The lifetime value of a customer wasn't just one pet's lifespan—it was multiple pets over multiple decades, with veterinary recommendations reinforcing brand loyalty at every checkup.

The science behind Hill's created another moat. Over 200 scientists and 900+ dogs and cats dedicate their time to ensuring each Hill's product provides optimal nutrition. The 180-acre Hill's Global Pet Nutrition Center in Topeka, Kansas isn't just a research facility—it's a competitive advantage that would take competitors decades and hundreds of millions to replicate. The research isn't just about creating new products; it's about building scientific credibility that veterinarians trust. The modern results validate the strategy. Hill's Pet Nutrition played a crucial role in Colgate-Palmolive's financial performance, contributing 23.1% of total sales in 2024. For the whole of 2024, Colgate-Palmolive's pet business brought in US$4,483 million in net sales. Operating profits in 2024 were US$965 million—margin levels that would make most businesses envious. This isn't just a pet food business; it's a profit engine generating nearly $1 billion in operating income.

The recent expansion tells a story of a business hitting its stride. Colgate-Palmolive Company plans to purchase three dry pet food manufacturing plants in the U.S. from Red Collar Pet Foods for $700 million to support the global growth of its Hill's Pet Nutrition business. Hill's is currently building a new canned pet food manufacturing facility in Tonganoxie, Kansas. These aren't defensive investments—they're aggressive capacity expansions betting on continued growth.

The social impact creates another layer of moat. Since 2002, we've provided nearly $300 million in food to support shelter animals through the Hill's Food, Shelter & Love® program. To date, 14 million pets have found new homes. This isn't just corporate social responsibility—it's brilliant marketing. Every shelter pet eating Hill's food is a future customer relationship, as new pet parents often continue with the food their adopted pet was eating.

The innovation pipeline remains robust. Coming full circle back to the work of Dr. Morris, Hill's relaunched its Prescription Diet k/d in 2023 with a blend of prebiotics that supports kidney health. The company employs Over 200 scientists and 900+ dogs and cats dedicate their time to ensuring each Hill's product provides optimal nutrition. This R&D intensity creates a continuous stream of new products that competitors struggle to match.

What's most remarkable about Hill's is how it transformed Colgate-Palmolive's business model. While toothpaste and soap are purchased intermittently, pet food creates recurring revenue streams. A dog eating Hill's Prescription Diet for kidney disease might consume $2,000+ of product annually for a decade. The lifetime value of a pet owner dwarfs that of a toothpaste buyer. And the veterinary recommendation creates switching costs that are nearly insurmountable—few pet owners will risk their pet's health by switching from veterinarian-recommended food to save a few dollars.

VII. The Colgate Total Revolution & Innovation Strategy (1990s–2000s)

The 1990s brought a new challenge: how to differentiate in mature categories where innovation seemed exhausted. Toothpaste had fluoride. It cleaned teeth. What more could consumers want? The answer would come in the form of Colgate Total, a product that would redefine not just Colgate's fortunes but the entire oral care category. The development of Colgate Total represents one of the most consequential product launches in consumer products history. Colgate Total is the first toothpaste ever that can legitimately claim that it helps prevent gingivitis, plaque and cavities -- the most common dental problems that people face today. The unique formula of Colgate Total, containing fluoride and the antimicrobial ingredient, Triclosan, has been demonstrated clinically to help prevent gingivitis, plaque and cavities.

The FDA approval process was unprecedented. No other toothpaste manufactured in the United States contains Triclosan or has been cleared to make claims for gingivitis and plaque reduction. It is also the first and only toothpaste that has earned the American Dental Association (ADA) Seal of Acceptance for gingivitis, plaque, cavities and tartar benefits. This wasn't just a new product—it was a new category of therapeutic toothpaste that blurred the line between medicine and consumer product.

The clinical backing was crucial. Dr. Sigmund S. Socransky, Associate Professor of Oral Biology, Harvard School of Dental Medicine, said, "The Colgate Total triclosan co-polymer formulation is one of the most remarkable oral therapeutic achievements in the last 20 years." This wasn't marketing hyperbole—it was peer-reviewed science giving Colgate a competitive advantage that competitors couldn't match without their own lengthy FDA approval process.

The patent protection was equally important. In addition, its formula (patented until 2008), also contains a co-polymer, Gantrez, which continues to work between brushings. This "12-hour protection" claim became the marketing hook that differentiated Total from every other toothpaste. While competitors could clean teeth, only Total could protect them all day.

The global rollout strategy was masterful. First introduced internationally in 1992, Colgate Total is now used by consumers in 103 countries who have purchased nearly half a billion tubes by 1997. By testing in international markets first, Colgate refined the formula and marketing before the crucial U.S. launch. When Total finally hit American shelves in December 1997, it was a proven winner.

The market impact was immediate and lasting. It was introduced in the United States in December 1997 and is today the #1 U.S. toothpaste in dollar sales. Within a year, Total had captured market leadership, and variants like Fresh Stripe expanded the franchise. In the United Kingdom, Colgate Total Fresh Stripe helped lift the Colgate market share to 35%, the highest it's been in many years. And in Canada, Colgate recently achieved a record 43% of the toothpaste market.

The triclosan controversy that emerged years later actually demonstrates the depth of Colgate's competitive moat. Despite concerns raised about triclosan as an endocrine disruptor, Colgate Total maintained market leadership because the clinical benefits were so compelling. The original FDA submission for Colgate Total included more than 100 toxicology studies. When competitors and activists challenged the product, both the FDA and dental professionals continued to support it based on the evidence.

The eventual reformulation tells another story about innovation and adaptation. Due to health and environmental concerns, triclosan was phased out, and by 2019 it is no longer used. But rather than losing market share, Colgate reformulated Total with new active ingredients while maintaining the 12-hour protection claim. This ability to evolve while maintaining brand equity is the hallmark of great consumer products companies.

VIII. Modern Era: Portfolio Optimization & Margin Expansion (2010s–Today)

The 2010s brought a new challenge: how to grow in mature markets with increasingly sophisticated consumers and aggressive private label competition. The answer would come through ruthless portfolio optimization, premiumization, and operational excellence that would push gross margins above 60%—levels typically associated with software companies, not toothpaste makers. The margin story is remarkable. GAAP Gross profit margin and Base Business Gross profit margin* both increased 70 basis points to 60.3% in Q4 2024. For the full year, the company achieved gross margins that most software companies would envy—all while selling physical products that require raw materials, manufacturing, and distribution. The first quarter of 2024 saw Colgate-Palmolive achieving a gross profit margin of 60.0%, a substantial improvement from the previous year's 56.9%.

This isn't just cost-cutting. It's the result of systematic portfolio optimization, premiumization, and pricing power that comes from brand strength. The company has shed low-margin businesses while doubling down on categories where it has pricing power. The exit from private label pet food manufacturing—including a 0.5% negative impact from lower private label pet volume—shows the discipline to walk away from revenue that doesn't meet margin thresholds.

The premiumization strategy has been executed through strategic acquisitions. Tom's of Maine brought natural positioning. EltaMD and Filorga added prestige skincare. These aren't just brand additions—they're margin enhancers. Premium products carry higher margins and create a halo effect that allows the company to raise prices across the portfolio.

The innovation pipeline supports premium pricing. EltaMD's new sunscreen introduction tackles a long-standing market gap with its Invisible Blend Technology. This patent-pending formulation specifically addresses the needs of consumers with deeper skin tones. This isn't generic product development—it's targeted innovation that commands premium pricing by solving specific consumer problems.

Digital transformation has improved both margins and market reach. The company's e-commerce capabilities, accelerated during COVID-19, allow direct-to-consumer sales that capture retail margins. Digital marketing is more efficient than traditional advertising, allowing the company to maintain brand strength while improving marketing ROI. The company increased advertising investment by 16% year-over-year while still expanding margins—evidence of improved efficiency.

The sustainability initiatives create another lever for margin expansion. Colgate launches the first-of-its-kind recyclable toothpaste tube—an innovation that required years of R&D but now provides differentiation that supports premium pricing. Consumers increasingly pay more for sustainable products, and Colgate's innovations in this area support both margins and brand equity.

The geographic mix continues to evolve favorably. Emerging markets, where Colgate often has dominant market positions, are growing faster than developed markets. In these markets, Colgate products are aspirational purchases, commanding premium pricing relative to local competitors. The company's early entry into these markets—decades before most multinationals—created distribution and brand advantages that translate directly to pricing power.

The results speak for themselves: For the full year, we grew net sales 3.3% and organic sales 7.4%, with organic sales growth in every division and in all four of our categories. This isn't just growth—it's profitable growth. GAAP EPS increased 27% to $3.51; Base Business EPS* increased 11% to $3.60. The company is generating earnings growth well above revenue growth, the hallmark of a business with expanding margins and improving capital efficiency.

IX. Playbook: Business & Investing Lessons

After two centuries of compounding, what can investors and operators learn from Colgate-Palmolive's playbook? The lessons go beyond CPG and reveal fundamental truths about building enduring business value.

The Power of Distribution as Competitive Moat

Distribution in consumer products isn't just logistics—it's a nearly insurmountable competitive advantage when done right. Colgate's products are in over 200 countries and territories. This isn't just about shipping products; it's about relationships with millions of retailers, understanding of local regulations, and logistics networks that took decades to build. A startup with a better toothpaste formula faces not a product problem but a distribution problem. By the time they've built distribution in one country, Colgate has launched three new products globally.

The shelf space mathematics are brutal for new entrants. Retailers allocate space based on turnover and reliability. Colgate's products turn quickly and consistently, earning them premium shelf placement. This creates a virtuous cycle: better placement drives higher sales, which earns better placement. Breaking this cycle requires either massive capital (to buy shelf space) or genuine innovation that retailers can't ignore—and even then, success is far from guaranteed.

Brand Building Over Centuries: Trust, Consistency, and Evolution

Colgate's brand value isn't measured in quarters or years but in generations. Parents who used Colgate teach their children to brush with Colgate, who teach their children. This intergenerational trust is nearly impossible to replicate quickly. It's built on millions of positive experiences compounded over time.

But longevity alone doesn't create value—ask Sears or Kodak. Colgate has mastered the balance between consistency (the brand promise never changes) and evolution (the products constantly improve). Colgate Total in 2024 has different ingredients than in 1997, but the promise—comprehensive oral protection—remains constant. This allows the brand to feel both familiar and modern, trusted and innovative.

The Veterinary Channel Innovation

Hill's Pet Nutrition reveals a masterclass in channel strategy. Rather than competing in grocery stores against Purina and Iams, Hill's built an entirely different go-to-market: the veterinary channel. This wasn't just differentiation—it was category creation. Veterinary-recommended pet food became its own category with different economics, different competition, and different consumer psychology.

The genius is in the alignment of incentives. Veterinarians want healthy pets and trusted products they can confidently recommend. Pet owners want what's best for their pets and trust their veterinarian's expertise. Hill's provides products that deliver clinical outcomes, creating a three-way win. Competitors trying to replicate this face a chicken-and-egg problem: veterinarians won't recommend without clinical proof, but generating clinical proof requires resources that are hard to justify without veterinary support.

Capital Allocation: Why Boring Businesses Generate Exceptional Returns

Colgate's capital allocation over decades reveals why "boring" businesses often outperform "exciting" ones. The company generates enormous cash flow with minimal capital requirements. A toothpaste factory, once built, can run for decades with modest maintenance capex. This creates enormous free cash flow that can be returned to shareholders or reinvested at high returns.

Compare this to capital-intensive or technology businesses that require constant reinvestment just to maintain position. Colgate's R&D spending is meaningful but modest—they're not trying to cure cancer or build autonomous vehicles. They're making incremental improvements to proven products. This allows them to return substantial capital to shareholders while still investing for growth. $3.4 billion returned to shareholders in 2024 through dividends and buybacks isn't an anomaly—it's the natural result of a business model with exceptional cash conversion.

Managing Complexity: 200+ Countries, Thousands of SKUs

The operational complexity of Colgate's business is staggering. Different formulations for different markets, different regulations, different consumer preferences, different competitive dynamics. Managing this without drowning in complexity requires systems and processes that have been refined over decades.

The key insight is that complexity, properly managed, becomes a moat. New entrants look at the need to develop products for dozens of markets, navigate different regulatory regimes, and manage thousands of SKUs, and they're overwhelmed. But for Colgate, this is business as usual. They have the systems, the expertise, and the scale to make complexity profitable. What's a barrier for others is a competency for them.

The Advertising ROI Equation and Marketing Efficiency

Colgate's marketing efficiency demonstrates the compounding value of brand awareness. When everyone knows Colgate, advertising doesn't need to build awareness—it just needs to remind and reinforce. This is fundamentally more efficient than building awareness from zero. A Colgate ad showing white teeth and a smile works globally with minor localization. A new brand needs to explain who they are, why they exist, and why consumers should trust them—expensive propositions.

The company's ability to increase advertising spend by 16% while expanding margins shows this efficiency in action. They're not buying awareness; they're buying reminder and reinforcement at the margin. The base of awareness, built over centuries, does most of the work. This is why challenging incumbent CPG brands is so expensive—you're not just competing on product or price, but on generations of accumulated marketing investment.

X. Analysis & Bear vs. Bull Case

Bull Case: The Compounding Machine Continues

The bull case for Colgate rests on multiple pillars that reinforce each other. Start with pricing power. In an inflationary environment, Colgate has demonstrated the ability to pass through costs and then some. Organic sales growth of 7.4% in 2024 despite economic headwinds shows that consumers will pay more for trusted brands. This pricing power isn't temporary—it's structural, based on brand equity that competitors can't quickly replicate.

Emerging market growth provides a multi-decade runway. As billions of consumers in Asia, Africa, and Latin America enter the middle class, their first purchase isn't luxury goods—it's branded consumer products that signal they've "made it." Colgate is already there, already distributed, already trusted. The company generates about 70% of revenue from international markets, with emerging markets growing faster than developed ones. This geographic mix shift naturally drives organic growth.

The pet humanization trend is a secular growth driver that's still early innings. Pet owners increasingly treat pets as family members, willing to pay premium prices for perceived health benefits. Hill's Science Diet and Prescription Diet are perfectly positioned for this trend. With veterinary recommendation and scientific backing, Hill's can charge prices that would seem absurd for "dog food" but make perfect sense for "therapeutic nutrition." This business could double over the next decade as pet ownership grows and spending per pet increases.

The subscription and D2C potential remains largely untapped. While Colgate has been slower than startups to embrace subscription models, they have the brand trust to make it work at scale. Imagine the lifetime value of a consumer who subscribes to toothpaste, pet food, and dish soap delivery. The data from these direct relationships would improve product development and marketing efficiency. The margin improvement from capturing retail markup could add several hundred basis points to gross margins.

Operational leverage continues to expand. The company's gross margins have expanded from the mid-50s to over 60% through mix shift, pricing, and efficiency. There's no reason this can't continue. As the portfolio shifts toward premium products, as manufacturing becomes more efficient, and as digital marketing replaces traditional advertising, margins should continue expanding. A path to 65% gross margins over the next five years isn't unrealistic.

Bear Case: The Slow-Motion Disruption Risk

The bear case isn't about sudden collapse but slow-motion disruption that's hard to see until it's too late. Private label threats are real and growing. Retailers like Amazon, Costco, and Target are investing heavily in private label products that are "good enough" at 30% lower prices. While Colgate has maintained share so far, each recession makes consumers more willing to try private label. Once they realize the private label toothpaste works fine, winning them back requires promotional spending that hurts margins.

Category growth is slowing in developed markets. People only brush their teeth twice a day, only wash dishes after meals, only feed their pets prescribed amounts. In developed markets, volume growth is essentially flat. Growth must come from price increases or mix shift to premium products. But there's a limit to how premium toothpaste can get before consumers rebel. The easy growth from penetration increase is over in mature markets.

Amazon and e-commerce disruption changes the game in subtle but important ways. Online, shelf space is infinite, search rankings matter more than shelf placement, and consumer reviews can trump decades of advertising. Startup brands can build awareness through social media and influencer marketing at a fraction of traditional advertising costs. While Colgate is adapting, they're playing defense in a game where the rules increasingly favor attackers.

ESG pressures are mounting. Plastic packaging, palm oil sourcing, animal testing for new products—these issues won't go away. Solutions are expensive and often hurt product performance or consumer experience. The recyclable tube is great PR but costs more to produce. Removing controversial ingredients requires reformulation that risks product efficacy. These pressures create a tax on the business that didn't exist decades ago.

Competitive positioning versus P&G, Unilever, and Church & Dwight remains challenging. These aren't startups—they're sophisticated competitors with their own scale advantages. P&G's Crest remains formidable in oral care. Unilever competes across categories. Church & Dwight's Arm & Hammer leverages a different but equally powerful brand equity. In every category, Colgate faces credible competitors who prevent them from exercising monopoly pricing power.

Valuation and What the Market is Missing

At current valuations, the market seems to be pricing Colgate as a slow-growth, mature business with limited upside. But this misses several key points. First, the quality of growth matters. Colgate's growth comes with expanding margins and minimal capital requirements—a rare combination. Second, the durability of the business model is underappreciated. This company survived two world wars, the Great Depression, and countless recessions. In an uncertain world, that durability has value.

The hidden growth options are undervalued. The company's ventures into skin care through EltaMD and Filorga could become billion-dollar businesses. The pet nutrition business could double in size. The sustainability innovations could command premium pricing that the market isn't modeling. These aren't pie-in-the-sky ventures—they're logical extensions leveraging existing capabilities.

XI. Epilogue & Reflections

Standing back and viewing Colgate-Palmolive's 218-year journey, several profound insights emerge about business, capitalism, and value creation. This isn't just a story about toothpaste and soap—it's a masterclass in compound growth and the power of patience.

The Remarkable Staying Power of Consumer Brands

In an age where software companies worth billions can disappear in years, Colgate's durability seems almost anachronistic. Yet that durability is precisely the point. Human needs for cleanliness, health, and care for their pets aren't disrupted by technology—they're fundamental. Colgate has tied itself to these fundamental needs and built trust over generations. That trust, once earned, becomes incredibly sticky. It's not nostalgia that keeps people buying Colgate—it's the accumulated weight of millions of positive experiences.

What Colgate Teaches Us About Compound Growth and Patience

The Colgate story is ultimately about compound growth over very long periods. Not the explosive growth of tech companies, but steady, reliable growth that compounds into something extraordinary. A business growing at 5-7% annually doesn't seem exciting compared to software companies growing at 50%. But maintain that growth for decades, add expanding margins and dividends, and the returns are exceptional.

This requires a different kind of patience than most investors possess. It's not about waiting for a catalyst or a turnaround. It's about owning a business that incrementally improves year after year, decade after decade. The improvements are often too small to notice quarter to quarter, but compound into transformation over time. Colgate Total took five years of international testing before U.S. launch. The recyclable tube took years to develop. Hill's took decades to build into a $4 billion business. This patience is cultural and structural—public market pressure makes it hard, but family influence and long-term oriented shareholders make it possible.

Can 200-Year-Old Companies Still Innovate?

The conventional wisdom says old companies can't innovate—they're too bureaucratic, too risk-averse, too wedded to the past. Colgate challenges this narrative. The recyclable tube required genuine innovation. The veterinary channel strategy for Hill's was revolutionary. The premiumization through acquisition shows strategic flexibility.

But Colgate's innovation is different from Silicon Valley's. It's not about disrupting industries or creating new categories from nothing. It's about incremental improvements that compound, about solving real consumer problems, about using science to make better products. It's innovation in service of the core mission rather than innovation for its own sake. This type of innovation is less visible but often more valuable—it builds on existing strengths rather than abandoning them for the next new thing.

The Next Chapter: AI, Personalization, and the Future of CPG

Looking forward, Colgate faces new opportunities and challenges. AI and machine learning could revolutionize product development, allowing personalized formulations based on individual needs. Imagine toothpaste optimized for your specific oral microbiome, or pet food tailored to your dog's genetics. Colgate has the data, the distribution, and the trust to make this work—if they can execute.

The direct-to-consumer revolution is still early for CPG giants. Colgate could build deeper relationships with consumers, gathering data that improves products and marketing while capturing retail margins. Subscription models for everyday products could lock in customer lifetime value in ways that shelf placement never could.

Sustainability will shift from nice-to-have to must-have. Consumers, particularly younger ones, increasingly make purchase decisions based on environmental impact. Colgate's innovations in recyclable packaging and sustainable sourcing could become major competitive advantages—or table stakes, depending on how fast competitors move.

The geographic shift continues. As developed markets mature and emerging markets grow, Colgate's early investments in global distribution become increasingly valuable. The next billion middle-class consumers will come from Asia and Africa. Colgate is already there, already trusted, already distributed. That positioning is almost impossible to replicate.

Final Thoughts

The Colgate-Palmolive story is many things: a testament to American entrepreneurship, a case study in brand building, a playbook for global expansion. But most fundamentally, it's proof that in business, as in life, consistency and patience often triumph over brilliance and speed.

In a world obsessed with disruption, Colgate reminds us that some things endure precisely because they're mundane. Everyone needs to brush their teeth. That simple fact, leveraged with operational excellence and compounded over centuries, created one of the world's great consumer products companies.

For investors, the lesson is clear: don't overlook the boring businesses. The next two centuries might look very different from the last two, but people will still need clean teeth, clean dishes, and healthy pets. Companies that serve these fundamental needs with excellence, efficiency, and trust will continue creating value long after today's hot tech stocks are forgotten.

The margin of safety in owning a business that has survived 218 years isn't just financial—it's existential. Whatever the future brings, Colgate will likely adapt, survive, and thrive. In an uncertain world, that's worth more than any spreadsheet can capture.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube