Dalmia Bharat: Building India, One Cement Bag at a Time

I. Introduction & Episode Roadmap

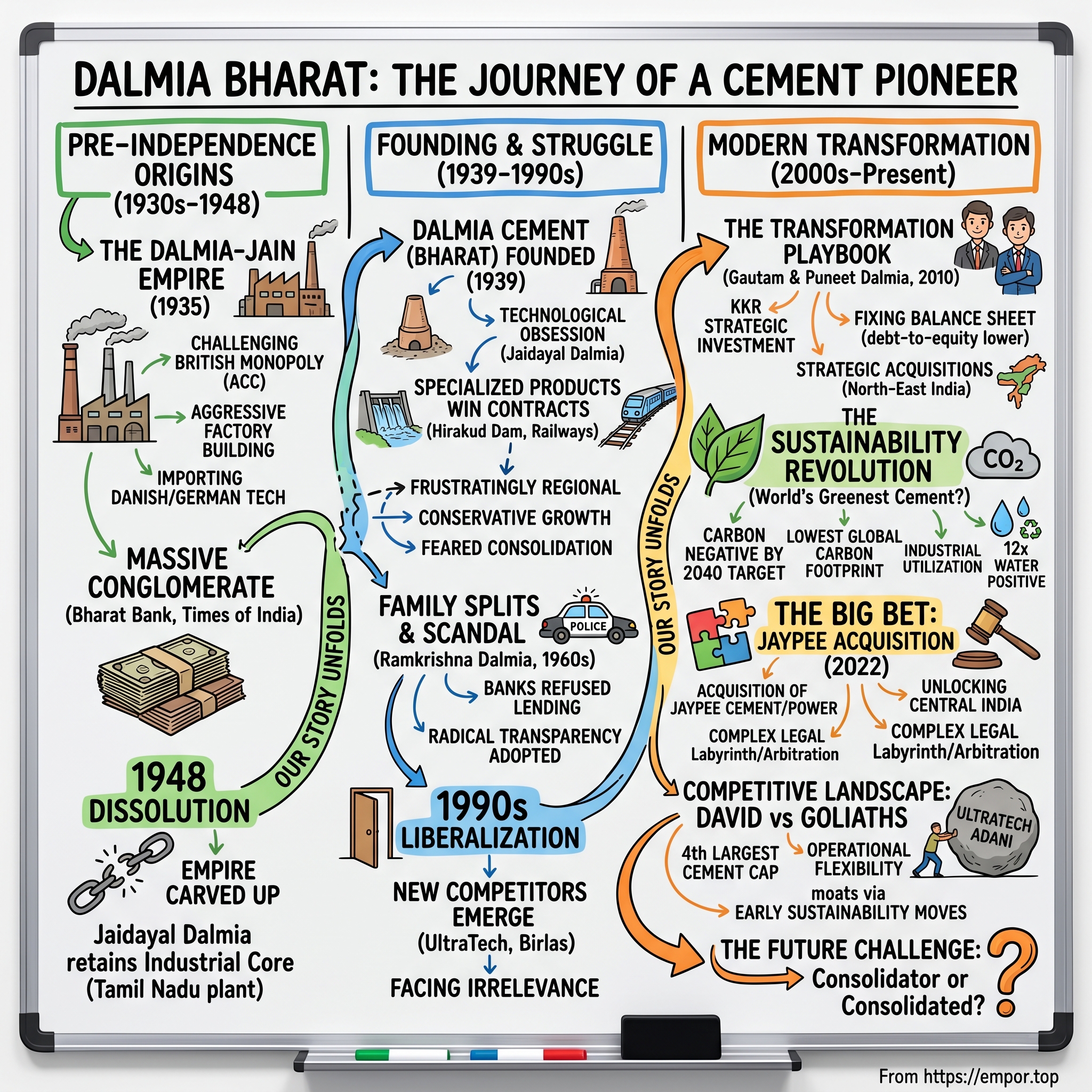

Picture this: A humid August morning in 1947. As India awakens to independence, cement kilns across the subcontinent burn through the night—some in what would become Pakistan, others in the new India. Among them, the Dalmia family's factories, built to challenge British monopolies, now faced a choice that would split empires, brothers, and destinies. This is the story of how one branch of that fractured dynasty transformed from a pre-independence industrial rebel into India's greenest cement company, worth over ₹42,000 crores today.

Dalmia Bharat stands as India's fourth-largest cement manufacturer by installed capacity, generating approximately ₹14,000 crores in revenue. Yet beneath these numbers lies a saga spanning nine decades—of family feuds that would make succession drama pale, of betting against colonial monopolies, of surviving government inquiries and imprisonment, and ultimately, of a third-generation transformation that turned a regional player into a sustainability pioneer.

The question isn't just how a cement company survived partition, family splits, and decades of stagnation. It's how the same company that once symbolized old-economy excess became the world's lowest carbon footprint cement producer, committed to becoming carbon negative by 2040. This journey from family empire to modern corporation reveals lessons about resilience, reinvention, and the unexpected competitive advantages of going green in the grittiest of industries.

Our story unfolds in three acts: the empire builders who challenged British monopolies, the lost decades of splits and survival, and the modern transformation that's rewriting what a cement company can be. Along the way, we'll decode how Dalmia navigates an industry where scale is survival, where Goliaths like UltraTech and Adani tower overhead, and where the next decade will determine whether this 85-year-old company becomes a consolidator or consolidated.

II. The Dalmia-Jain Empire: Pre-Independence Origins (1930s–1948)

The year was 1935, and Ramkrishna Dalmia had a problem. The Associated Cement Companies (ACC), backed by British capital and political favor, controlled India's cement market with an iron grip. Prices were fixed high, supply was restricted, and Indian industrialists were effectively locked out. Where others saw an impenetrable monopoly, the Dalmia brothers—Ramkrishna and Jaidayal—saw opportunity.

The brothers had already built a trading empire in eastern India, dealing in everything from jute to sugar. But cement was different. It wasn't just another commodity; it was literally the foundation of a nation waiting to be built. The Dalmias' strategy was audacious: build factories faster than ACC could respond, in locations they wouldn't expect, using technology they couldn't match.

The masterstroke came through an unlikely alliance. The Jain family, led by Sahu Shanti Prasad Jain, controlled significant capital but lacked the Dalmias' operational expertise. In the 1930s, these families merged operations to form the Dalmia-Jain Group—a conglomerate that would soon span from Lahore (now Pakistan) to Tamil Nadu, challenging British commercial hegemony at every turn.

By 1946, the empire had grown beyond anyone's imagination. The group controlled Bharat Bank with 110 branches, Bharat Fire and General Insurance Company, Lahore Electric Supply Company, the prestigious Govan group of companies, cotton mills in Delhi and Rajputana, dairy operations, and jute mills across Bengal. But Ramkrishna's most audacious acquisition came that year: Bennett, Coleman & Co. Ltd., publisher of The Times of India. An Indian industrialist now controlled the voice of British India's establishment press.

The Dalmia-Jain model was revolutionary for its time. While British companies focused on extracting profits for shareholders in London, the Dalmias reinvested aggressively, built local supply chains, and—crucially—imported the latest cement technology from Denmark and Germany. When Danish suppliers quoted excessive prices for their wet process technology, Jaidayal personally negotiated, playing suppliers against each other until prices dropped by 40%. This wasn't just business; it was economic warfare against colonial monopolies.

Their cement plants sprouted across undivided India like monuments to indigenous enterprise. Each location was chosen strategically—near limestone deposits, yes, but also along planned railway routes and future industrial corridors that the British had ignored. The Dalmiapuram plant in Tamil Nadu, established in 1939 with a modest 250 tonnes per day capacity, would become the cornerstone of what survived the coming storm.

But empires built on family bonds carry their own vulnerabilities. By early 1948, with India newly independent and Pakistan carved out, tensions between the Dalmia and Jain families reached a breaking point. The trigger wasn't just business—it was a fundamental disagreement about the future. The Jains wanted consolidation and careful growth; the Dalmias pushed for aggressive expansion into the new India's industrial vacuum.

The dissolution meeting at the Jains' Mussoorie hill station house in May 1948 was described by attendees as "civilized on the surface, volcanic underneath." Over three days, an empire built over two decades was carved up with the precision of Partition itself. The Jains took the insurance and finance businesses, forming what would become the Sahu Jain Group. Jaidayal Dalmia retained Dalmia Cement (Bharat) Ltd. and Orissa Cement Ltd.—the industrial core that would define the family's next chapter. Ramkrishna kept his media empire and various other interests, setting the stage for a spectacular rise and fall that would shake Indian business.

III. Jaidayal's Legacy: Founding Dalmia Cement (1939–1990s)

While his brother Ramkrishna captured headlines with media acquisitions and financial engineering, Jaidayal Dalmia was a different breed of industrialist. Engineers who worked with him in the 1950s described a man who could identify limestone quality by taste, who spent nights on factory floors debugging kilns, and who treated cement not as a commodity but as a craft requiring constant innovation.

The Dalmiapuram plant, founded in 1939, became Jaidayal's laboratory. Starting with just 250 tonnes per day capacity, he obsessed over every aspect of production. When European suppliers quoted standard technology packages, Jaidayal demanded modifications—higher heat recovery, lower coal consumption, adaptations for Indian limestone's unique mineral content. "Why should we burn coal the British way when Tamil Nadu limestone behaves differently?" he famously asked Danish engineers, forcing them to customize their designs.

This technical obsession paid dividends when independent India launched its infrastructure ambitions. The Hirakud Dam project in Odisha, billed as the world's longest earthen dam, required cement that could withstand massive hydraulic pressures and temperature variations. ACC, the established player, bid with standard Portland cement. Jaidayal's team developed a specialized slag cement with higher sulfate resistance and lower heat of hydration—technical specifications that meant nothing to politicians but everything to engineers. Dalmia won the contract.

The railway modernization program of the 1960s brought another opportunity. Concrete sleepers were replacing wooden ones, but standard cement cracked under the constant vibration of Indian Railways' heavy freight trains. Jaidayal's son, Jai Hari Dalmia, who had joined the business after studying chemical engineering in Germany, developed a pre-stressed concrete mix that could handle 25% more load cycles. By 1975, Dalmia Cement was supplying 30% of Indian Railways' concrete sleeper requirements.

The oil exploration boom of the 1970s and 80s revealed another niche. Oil well cement required extreme properties—it had to remain liquid while being pumped thousands of feet underground, then set rapidly under pressure and temperature conditions that would destroy normal cement. Most Indian companies imported this specialty cement. Yadu Hari Dalmia, Jaidayal's younger son, partnered with Halliburton to develop an indigenous alternative. The first successful batch in 1982 saved ONGC 60% on procurement costs.

Yet for all their technical prowess, the Dalmias remained frustratingly regional. While competitors consolidated—ACC merging with smaller players, the Birlas building UltraTech through acquisitions—Dalmia Cement seemed content with its southern stronghold. Part of this was strategic caution; Jaidayal had witnessed his brother Ramkrishna's empire crumble under aggressive expansion. Part was the family's engineering DNA—they preferred perfecting existing operations over managing far-flung acquisitions.

By the 1990s, this conservatism looked like a fatal flaw. Liberalization had unleashed new competitors with access to foreign capital and technology. The company's 3 million tonnes annual capacity, impressive in 1970, looked quaint compared to ACC's 20 million tonnes or Grasim's aggressive expansion plans. When Jaidayal passed away in 1992, leaving the company to his sons, industry observers wondered if Dalmia Cement would survive the coming consolidation or become another family business absorbed by larger rivals.

The next generation faced a stark choice: remain a profitable but shrinking regional player, or risk everything on national expansion. The answer would come from an unexpected source—Jaidayal's grandsons, educated at Wharton and Harvard, who saw opportunity where their fathers saw only risk.

IV. The Lost Decades: Family Splits & Survival Mode (1960s–2000s)

The Government of India's Commission of Inquiry report, released on a monsoon morning in 1956, read like a financial thriller. Ramkrishna Dalmia, the flamboyant half of the original Dalmia brothers, stood accused of siphoning funds from publicly listed companies, manipulating stock prices, and using Bharat Bank as a personal treasury. The investigation revealed byzantine financial structures—106 companies cross-holding shares, circular loans that led nowhere, and paper profits that existed only in creative accounting.

For Jaidayal's cement business, the scandal was both a crisis and an opportunity. The crisis was immediate: banks refused to lend to anything with "Dalmia" in its name, suppliers demanded cash upfront, and talented managers fled to competitors. The opportunity was subtler: with Ramkrishna's financial engineering discredited, Jaidayal's emphasis on operational excellence suddenly looked prescient.

Ramkrishna's imprisonment in 1962 for tax evasion and misappropriation sent shockwaves through Indian business. Here was a man who had owned The Times of India, who had dined with Nehru, now in Tihar Jail. But for Jaidayal's sons, Jai Hari and Yadu Hari, the real challenge was preventing their uncle's disgrace from destroying their own ambitions.

The family's solution was surgical separation. By 1965, all financial connections between Ramkrishna's entities and Dalmia Cement were severed. The company adopted what Jai Hari called "radical transparency"—publishing detailed quarterly accounts when regulations only required annual statements, inviting institutional investors to factory visits, and maintaining debt-to-equity ratios below 0.5 when industry average exceeded 2.0.

Yet even as they rebuilt credibility, new fractures emerged within Jaidayal's branch. The Orissa Cement Limited (OCL) became a flashpoint between brothers. Jai Hari wanted to merge it with Dalmia Cement for operational synergies; Yadu Hari saw it as his independent legacy. By 1989, the brothers formally split the businesses—a "velvet divorce" compared to their father's acrimonious separation from the Jains, but a split nonetheless.

The 1990s brought liberalization, and with it, a harsh reality. While the Dalmias had been managing family disputes, competitors had been building scale. ACC, backed by Holcim, expanded from 20 to 30 million tonnes capacity. The Birlas consolidated their cement operations under Grasim, then launched UltraTech. New entrants like Jaypee Group leveraged political connections to secure limestone leases and environmental clearances that took the Dalmias years to obtain.

A telling moment came in 1997. Lafarge, the French cement giant, was shopping for an Indian partner. They evaluated Dalmia Cement but chose to partner with the Birlas instead. The reason, according to a former Lafarge executive, was simple: "The Dalmias had excellent plants but no vision for national scale. They were perfecting the past while others were building the future."

By 1999, facing irrelevance, Yadu Hari's son Gautam Dalmia and Jai Hari's son Puneet Dalmia made a radical decision. Despite their fathers' split, the cousins would work together, bringing complementary skills—Gautam's financial engineering learned at Wharton, Puneet's operational expertise from running plants. They incorporated Renaissance Group as their investment vehicle, signaling both continuity with family legacy and a break from its limitations.

The young Dalmias inherited a company ranked 20th in Indian cement, with 9 million tonnes capacity concentrated in South India. UltraTech had 50 million tonnes. The gap seemed insurmountable. But Gautam saw opportunity in the industry's coming disruption: environmental regulations were tightening, coal costs were rising, and the old game of who-could-build-capacity-fastest was ending. The new game would be about efficiency, sustainability, and financial engineering. It was a game the Dalmias had been unconsciously preparing for through their decades of cautious, technical operations.

V. The Transformation Playbook: From #20 to #4 (2010–2020)

The boardroom at Mumbai's Oberoi Hotel fell silent when Gautam Dalmia finished his presentation in March 2010. Across the table sat Henry Kravis himself, flanked by KKR partners who had flown in from Hong Kong. The ask was audacious: ₹750 crores for 15% of a cement company ranked 20th in India, with most of its 9 million tonnes capacity trapped in Tamil Nadu. "Your EBITDA per tonne is impressive," Kravis finally said, "but how do you compete with UltraTech's 50 million tonnes?" Gautam's response would define the next decade: "We don't compete on size. We compete on cost. And we're about to show you how a David can dance with Goliaths."

KKR's investment of approximately 15% stake in Dalmia Cement Bharat Ltd. for a period of 5 years wasn't just capital—it was validation. The private equity giant had evaluated every major cement player in India and chose the smallest. Their thesis was counterintuitive: in a commodity business defined by scale, they bet on operational excellence and strategic acquisitions rather than blind capacity addition.

The transformation blueprint was elegantly simple yet brutally hard to execute. Step one: fix the balance sheet. The company's debt-to-equity ratio stood at 1.8x in 2010, reasonable by industry standards but crippling for ambitious M&A. Within eighteen months, through asset sales and operational improvements, they brought it down to 0.8x, creating dry powder for acquisitions.

Step two arrived faster than expected. The company expanded into North-East India with the acquisition of Calcom Cement India Limited and Adhunik Cements Limited. The Northeast was India's forgotten frontier—massive infrastructure needs, zero local capacity, and logistics nightmares that scared away larger players. Where others saw problems, Dalmia saw pricing power. Calcom's Assam plant, acquired for ₹420 crores, was generating ₹180 crores EBITDA within two years.

The masterstroke came in 2015. The company acquired 74.6% stake in OCL India Limited with a capacity of 6.7 MnTPA—ironically, the same Orissa Cement that Gautam's grandfather had built and his father had lost in the family split. The ₹3,200 crore acquisition wasn't just about capacity; it was about redemption. OCL brought three integrated plants in eastern India, the country's highest-growth cement market, plus something invaluable: relationships with eastern India's industrial ecosystem built over six decades.

But Puneet Dalmia, the operational brain to Gautam's financial acumen, knew that acquisitions without integration were just expensive distractions. He implemented what insiders called the "Toyota system for cement"—standardizing processes across plants, creating centralized procurement that leveraged combined volumes for 15% cost savings, and most critically, building India's first integrated logistics command center that optimized rail-road mix in real-time.

The numbers told the story: capacity and revenue growth pegged at almost 14% and 17% CAGR respectively through the decade. By 2020, installed capacity had expanded from 9 to over 30 million tonnes. But the real achievement was maintaining margins while growing—EBITDA per tonne actually increased from ₹780 to ₹1,050, defying the industry norm where rapid expansion destroyed profitability.

Dalmia Bharat Limited received Rs 588 cr from successful equity exit of the global private equity firm KKR in 2020, delivering them a 3.5x return. But KKR's exit was less an ending than a validation—the transformation was complete, the platform was built. The company that couldn't get meetings with investment bankers in 2009 was now fielding calls from global funds. The question was no longer whether Dalmia could survive among giants, but whether it could become one itself.

VI. The Sustainability Revolution: World's Greenest Cement?

The September 2019 announcement stopped cement industry executives cold. Dalmia Cement had been invited to speak at the Climate Action Summit of UN Secretary-General on 23rd September, 2019 to share their commitment to being carbon negative by 2040—the only cement company in the world on that stage. In an industry where reducing emissions by 20% was considered heroic, Dalmia was promising to absorb more carbon than it emitted. Either they had lost their minds, or they knew something others didn't.

The answer lay in Mahendra Singhi's office whiteboard, covered with equations that would make a climate scientist weep with joy. Singhi, poached from rival Shree Cement in 2013, wasn't a typical cement executive. He had spent fifteen years with the Cement Sustainability Initiative, developing roadmaps that most CEOs filed away unread. At Dalmia, he found believers.

Today, the company's carbon footprint is 40% lower than the global average for a cement company, which is the lowest carbon footprint in the global cement sector. This wasn't achieved through one moonshot technology but through hundreds of incremental innovations that compounded into revolution. The company reduced electricity consumption to 72 kWh per tonne of cement as compared to global average of 90 to 100 kWh per tonne of cement—a 20% advantage that translated directly to the bottom line.

The real breakthrough was recognizing that sustainability wasn't a cost center but a profit driver. Based on the circular economy concept and to conserve mineral resources, the company produces high blended cements with the best available technology. In this process, we utilise various industrial wastes such as BF slag (waste from steel industry) and fly ash (waste from thermal power plants). What others saw as waste disposal problems, Dalmia saw as free raw materials. Steel plants paid them to take slag; thermal plants begged them to remove fly ash. These "wastes" replaced expensive clinker while actually improving cement quality.

Considering the corporate responsibility of living in harmony with local communities by minimising the competing use of water, Dalmia Cement undertook the target to become water positive by 2017. It created various check dams, farm ponds, rehabilitation of village ponds, etc. The company achieved 12 times water positive status, meaning they returned twelve times more water to communities than they consumed—turning regulatory compliance into community goodwill.

The boldest move came with carbon capture. Dalmia Cement (Bharat) Limited, today announced it will build a large scale facility of 500,000 tonne per year carbon capture at its cement plant at Tamil Nadu, India. The partnership with UK's Carbon Clean Solutions wasn't just about technology—it was about reimagining cement plants as carbon sinks rather than carbon sources.

Dalmia Cement (Bharat) Limited, joined RE 100 – an ambitious campaign of leading conglomerates of the world. It was the only one from the global cement sector to commit to a long term transition to renewable energy. By 2020, Dalmia is first triple joiner globally of RE 100, EP 100 and EV 100 initiatives—committing to 100% renewable electricity, doubling energy productivity, and transitioning to electric vehicles.

The economics were counterintuitive but compelling. "We have been able to achieve about 20 per cent reduction in carbon intensity in five years. At the same time, our profitability has increased manifold. This proves our philosophy that clean and green is profitable and sustainable," Singhi added. Lower energy costs, premium pricing for green cement, carbon credits, and operational excellence created a virtuous cycle where sustainability drove profitability.

Critics argued it was greenwashing—that cement could never truly be green. But European construction giants, facing their own carbon commitments, began specifying Dalmia's low-carbon cement for projects. When a single wind farm project in Tamil Nadu chose Dalmia over competitors due to carbon specifications, generating ₹120 crores in revenue, the industry took notice.

According to the CDP (formerly Carbon Disclosure Project) cement sector report in April, Dalmia Bharat has achieved the first rank in CDP's low carbon transition league. For a company that couldn't compete on scale, sustainability had become the ultimate differentiator. The question wasn't whether green cement was real, but whether competitors could catch up before carbon pricing made high-emission cement economically obsolete.

VII. The Big Bet: Jaypee Acquisition Drama (2022–Present)

The conference room at Mumbai's Trident Hotel erupted in December 2022. Lawyers from three firms shouted across mahogany tables while investment bankers frantically recalculated spreadsheets. At the center sat Puneet Dalmia, calm as the eye of a hurricane, signing what would become Indian cement's most complex acquisition: Jaiprakash Associates' cement and power businesses for Rs 5,666 crore, including debt.

The deal was audacious in its complexity. The deal includes cement capacity of 9.4 million tonnes in Madhya Pradesh, Uttar Pradesh and Chhattisgarh, clinker capacity of 6.7 million tonnes (MT) and thermal power plants of 280 MW. For Dalmia, ranked fourth with 37 million tonnes capacity, this represented a 25% expansion overnight. More critically, it unlocked Central India—the one region where Dalmia had zero presence while competitors dominated.

But the real drama lay in what the press releases didn't mention. The closure of the Dalmia-Jaypee deal is being held up by ongoing discussions between lenders to the Jaypee group and the National Asset Reconstruction Company Limited (NARCL), as well as a separate arbitration between Jaiprakash Associates and UltraTech Cement. UltraTech, which had acquired over 20 million tonnes from Jaypee between 2014-2017, claimed right of first refusal on any future Jaypee sales—a clause buried in decade-old agreements.

From its inception, the deal has been fraught with concerns, possibly leading Dalmia Cement to structure it in three parts. One tranche of the deal includes JP Super Cement with an enterprise value of Rs 1,500 crore, and costs and expenses up to Rs 190 crore. This surgical approach wasn't just legal maneuvering—it was financial chess. By breaking the acquisition into tranches, Dalmia could close portions even if others got stuck in litigation, maintaining momentum while competitors tangled in courts.

The strategic rationale went beyond capacity addition. Jaypee's plants sat on the Madhya Pradesh-Uttar Pradesh border, perfectly positioned to serve India's largest construction market—the National Capital Region—while also accessing the infrastructure boom in Central India. The 280 MW captive power capacity meant energy security in a region plagued by grid instability. The limestone reserves, enough for 30 years, were located in politically stable states with mining-friendly policies.

Yet industry watchers questioned the price. At ₹600 per tonne of capacity, Dalmia was paying nearly double the replacement cost. The plants, averaging 15 years old, needed modernization. Environmental clearances were due for renewal. Labor unions at Jaypee facilities had a reputation for militancy. The integration challenges seemed insurmountable.

Gautam Dalmia's response revealed the deeper strategy: "We're not buying plants; we're buying time." In an industry where getting environmental clearance for a greenfield plant took 5-7 years, acquiring operational assets—even troubled ones—offered immediate market access. While Adani and UltraTech fought over mega-acquisitions, Dalmia could consolidate Central India before anyone noticed.

Dalmia said the deal was a significant step towards reaching 110 MT to 130 MT capacity by fiscal year 2031, with its capacity currently pegged at 37 MT. This wasn't just expansion—it was transformation from regional champion to national contender. The path to 75 million tonnes by FY27 now seemed achievable, not through one blockbuster deal but through strategic accumulation.

As the arbitration has been underway since December 2022, the remaining two tranches of Dalmia's deal with Jaypee are now awaiting clarity from lenders, according to people in the know. Media reports suggest that lenders to the Jaypee group have been in discussions with NARCL to sell their entire debt exposure of various Jaiprakash Associates businesses, including cement. If a successful deal is reached, it remains to be seen whether NARCL will follow through with the agreement signed between Jaiprakash Associates and Dalmia Cement.

The waiting game continues, but Dalmia has already begun preparing integration teams, negotiating coal linkages, and identifying synergies. The acquisition, if completed, won't just add capacity—it will complete Dalmia's transformation from a South Indian cement company to a pan-India player, finally competing on equal geographic footing with the giants. The question isn't whether they can digest this acquisition, but whether the legal labyrinth will let them try.

VIII. Competitive Landscape: David Among Goliaths

The numbers told a stark story at the Cement Manufacturers Association's 2024 annual meeting. UltraTech Cement, the undisputed king, commanded 140+ million tonnes capacity—nearly four times Dalmia's size. Adani Cement, through its audacious acquisition of ACC and Ambuja from Holcim, had overnight become India's second-largest player with 70 million tonnes. Shree Cement, the operational excellence machine from Rajasthan, generated EBITDA margins that made CFOs weep with envy. And there stood Dalmia, fourth place with 49.5 million tonnes, impressive by any measure except when compared to the titans surrounding it.

"Scale is destiny in cement," Kumar Mangalam Birla had declared after UltraTech's latest acquisition spree. The economics seemed irrefutable: larger players secured better freight rates, negotiated superior coal linkages, and spread fixed costs over massive volumes. They could weather price wars that would bankrupt smaller players. They had the balance sheets to snap up distressed assets during downturns.

Yet Puneet Dalmia saw the landscape differently. "The game isn't about being the biggest," he told investors in early 2024. "It's about being the most profitable per tonne." While UltraTech spread across 22 plants trying to maintain uniform quality, Dalmia's 15 plants operated like a Swiss watch. While Adani integrated two massive, culturally different organizations, Dalmia ran lean with decision-making centralized among family members who could approve a ₹100 crore investment over WhatsApp.

The market dynamics were shifting in subtle ways that favored the focused over the bloated. Environmental regulations were tightening—plants needed expensive upgrades to meet new emission norms. Coal prices had tripled since 2020. Railway freight rates increased annually. In this environment, operational efficiency mattered more than raw scale. Dalmia's kiln fuel consumption of 725 kcal/kg of clinker beat industry average by 8%. Their logistics cost per tonne, optimized through algorithm-driven routing, undercut UltraTech's by ₹40 in overlapping markets.

The regional strategy also had hidden advantages. While UltraTech and Adani fought brutal price wars in Western and Northern markets, Dalmia quietly dominated pockets—Northeastern states where they controlled 35% market share, specific districts in Tamil Nadu where brand loyalty ran three generations deep. In these micro-markets, Dalmia commanded premium pricing that would be impossible in competitive zones.

The company has delivered a poor sales growth of 7.64% over past five years. Company has a low return on equity of 5.28% over last 3 years. These metrics looked weak against Shree Cement's 15% ROE or UltraTech's consistent double-digit growth. But they missed the transformation underway. The poor historical returns reflected the digestion period of massive acquisitions. The real test would come as these assets reached optimal utilization.

The competitive dynamics were also changing with customer preferences. Government infrastructure projects, traditionally price-focused, now included sustainability criteria in tenders. Real estate developers, facing pressure from international investors, sought low-carbon cement for green building certifications. In these emerging segments, Dalmia's environmental credentials trumped UltraTech's scale.

Yet challenges remained acute. Dalmia's 46.2x P/E ratio suggested markets expected perfection—any execution stumble would trigger savage correction. The 0.40% dividend yield indicated cash was being hoarded for expansion rather than returned to shareholders, testing investor patience. In a commodity business where switching costs were nil, customer loyalty remained fragile.

The financing disadvantage was particularly painful. When UltraTech raised debt, banks competed to lend at MCLR plus 20 basis points. Dalmia paid 75 basis points higher, a seemingly small difference that translated to ₹50 crores additional interest annually. In acquisition battles, UltraTech could offer all-cash deals while Dalmia structured complex earn-outs and contingent payments.

The talent war was equally challenging. IIT graduates dreamed of joining Birla Group or Adani's rocket ship, not a fourth-place cement company. Dalmia competed by offering faster progression—a 30-year-old could run a plant, impossible at UltraTech's hierarchical structure. They recruited from tier-2 engineering colleges, finding hungry talent overlooked by giants. The head of their digital initiatives was a dropout from a Ranchi engineering college who had built logistics software in his hostel room.

The next five years would determine whether Dalmia's David could genuinely compete with the Goliaths or would itself become an acquisition target. The cement industry's history littered with regional champions absorbed by nationals—Gujarat Ambuja by Holcim, Binani by UltraTech. As consolidation accelerated, standing still meant becoming prey. Dalmia's challenge wasn't just growing to 110 million tonnes by 2031 but doing so while maintaining the operational excellence and sustainability leadership that justified its existence as an independent player.

IX. Playbook: Business & Investing Lessons

The January 2019 board meeting lasted fourteen hours. Three generations of Dalmias sat around the table—the family patriarch's portrait watching from the wall, current leaders debating strategy, and next-generation MBAs challenging every assumption. The question was deceptively simple: Should Dalmia remain a cement pure-play or diversify like the conglomerates of old? The answer would define whether family businesses could survive in modern India.

The first lesson emerged from their painful history: family unity is a competitive advantage only when coupled with professional governance. The Dalmias had watched the Modis, Singhanias, and their own relatives destroy empires through succession battles. Their solution was elegant—family members could join only after external experience and board positions rotated between branches. Emotional decisions were confined to family councils; business decisions required independent director approval. When Gautam and Puneet disagreed on the Jaypee acquisition's pricing, they brought in McKinsey to arbitrate—unthinkable in traditional family businesses.

The second insight challenged conventional wisdom: in commodity businesses, the lowest-cost producer doesn't always win—the most flexible one does. Shree Cement had lower costs through operational excellence, but their model required running plants at 95%+ utilization. Dalmia deliberately maintained 80-85% utilization, sacrificing efficiency for agility. When sand shortages hit Tamil Nadu construction in 2019, Dalmia could redirect capacity to Karnataka overnight while Shree's optimized supply chains took weeks to adjust. Flexibility had value that spreadsheets couldn't capture.

The sustainability transformation revealed a third principle: regulatory shifts create moats for early movers. While competitors treated environmental compliance as a cost center, Dalmia recognized that carbon taxes were inevitable. Every tonne of CO2 saved today would be worth ₹2,000-3,000 in carbon credits by 2030. The ₹500 crore invested in carbon capture technology looked expensive against today's profits but cheap against tomorrow's carbon prices. First-movers would lock in green premiums before they became table stakes.

The capital allocation framework defied textbook finance: in consolidating industries, overpay for strategic assets, underpay for everything else. The Jaypee acquisition at ₹600 per tonne looked expensive, but Central India access was worth the premium. Conversely, when buying limestone mines or logistics assets, Dalmia waited for distress, acquiring assets at 30-40% of replacement cost. The discipline was knowing which assets were strategic versus commoditized.

The organizational lesson was counterintuitive: remain subscale in corporate functions while scaling operations. UltraTech's Mumbai headquarters housed 500+ executives; Dalmia's Delhi office had 80. This wasn't frugality but focus—decisions happened at plants, not boardrooms. The head of manufacturing could approve ₹10 crore capital expenditure without corporate sign-off. This radical decentralization enabled plant managers to experiment with everything from alternative fuels to worker incentive schemes, creating innovation labs across locations.

The technology adoption strategy offered another insight: in traditional industries, be second-wave adopters, not pioneers. Let competitors debug new technologies. When UltraTech installed Germany's first-generation waste heat recovery systems, they suffered 18 months of downtime. Dalmia installed second-generation Chinese systems two years later at half the cost with twice the reliability. The same pattern repeated with automation, alternative fuels, and now artificial intelligence—let others pay the pioneer tax.

The stakeholder management approach was particularly nuanced: treat different stakeholders as option holders, not equity holders. Employees received performance bonuses but limited equity—their upside came from skill development and career progression. Communities near plants got profit-sharing through trusts, aligning their interests without diluting control. Minority shareholders received growth, not dividends. Only family members held permanent equity, ensuring long-term thinking survived quarterly pressures.

The geographic expansion strategy embodied patient capital: build density before diversity. While Adani spread across India simultaneously, Dalmia saturated regions sequentially. They wouldn't enter a new state until they had 20%+ market share in existing ones. This concentration created local economies of scale—dedicated rail sidings, distributor loyalty, brand recognition—that translated to 15-20% EBITDA margins versus 10-12% for subscale players.

The acquisition integration playbook was surgical: preserve what works, standardize what scales. When Dalmia acquired OCL, they retained the entire sales team who knew Odisha's market intimately. But procurement, finance, and technology were centralized within six months. Local market knowledge stayed local; scalable functions scaled. This selective integration maintained entrepreneurial energy while capturing synergies.

The ultimate lesson transcended business school frameworks: in capital-intensive industries, culture eats strategy and operations eats culture. Dalmia's culture emphasized technical excellence—plant heads were engineers, not MBAs. Strategy meetings discussed kiln temperatures and limestone chemistry, not just market share. This operational obsession created a culture where a 1% improvement in fuel efficiency was celebrated more than a ₹100 crore contract. In commodity businesses where products are identical, operational excellence becomes the only sustainable differentiation.

X. Bear vs. Bull Case

Bear Case: The Uncomfortable Truths

The bearish argument against Dalmia Bharat starts with simple arithmetic. At 46.2x P/E ratio, the market prices Dalmia like a technology company, not a cement manufacturer grinding limestone. UltraTech trades at 28x, Shree Cement at 32x. This premium assumes flawless execution in an industry where a single monsoon failure can destroy quarterly earnings. The valuation implies Dalmia will grow faster, operate better, and face fewer challenges than larger, better-resourced competitors—a fantasy that ignores cement's brutal realities.

The scale disadvantage becomes more pronounced as consolidation accelerates. UltraTech's 140 million tonnes capacity secures coal linkages at prices Dalmia can't match. When Coal India auctions blocks, UltraTech bids aggressively knowing they can spread costs across massive volumes. Dalmia must buy expensive imported coal or e-auction coal at 30% premiums. This input cost disadvantage—₹200-300 per tonne—is structural, not operational.

The Jaypee acquisition, if it closes, could become an integration nightmare. The plants average 15 years old, requiring ₹1,000+ crores in modernization. The workforce, accustomed to Jaypee's financially distressed environment, may resist Dalmia's efficiency drives. Environmental clearances need renewal by 2025—any delays would strand assets. The ₹5,666 crore price tag assumes everything goes right; history suggests otherwise.

The sustainability narrative, while admirable, may prove economically suicidal. Carbon capture technology remains unproven at scale—the ₹500 crore investment might never generate returns. Green cement commands just 2-3% premiums in select markets, insufficient to justify higher production costs. When recession hits and customers prioritize price over planet, Dalmia's green investments become stranded assets while competitors using dirty-but-cheap processes undercut them.

Geographic concentration poses hidden risks. Dalmia derives 40% of revenues from South India, where real estate—cement's largest consumer—faces structural headwinds. IT companies are reducing office space, residential inventory remains unsold, and infrastructure spending shifts to Northern states. Unlike diversified players, Dalmia can't offset regional weakness with strength elsewhere.

The promoter holding at 55.8% seems aligned but creates other problems. Family control limits institutional ownership, reducing liquidity and analyst coverage. Stock prices remain volatile—a 20% single-day swing isn't unusual. The concentrated ownership also raises succession risks. What happens when the current generation retires? Will the fourth generation maintain operational focus or seek financial engineering?

The commodity trap remains inescapable. Cement is cement—customers switch suppliers for ₹10 per bag savings. Brand building in commodities is largely futile; even UltraTech's massive advertising generates minimal pricing power. As industry capacity additions of 40 million tonnes annually come online through 2025, pricing power evaporates. EBITDA margins will compress from current 18% to historical 12-14%, destroying returns.

Bull Case: The Hidden Strengths

The bullish thesis rests on a fundamental misunderstanding the market makes: Dalmia isn't competing on scale but on return on capital. While giants chase volumes, Dalmia optimizes returns. Their EBITDA per tonne of ₹1,050 exceeds UltraTech's ₹950 despite the scale disadvantage. This efficiency gap widens as environmental regulations favor Dalmia's modern, green plants over competitors' aging, polluting assets.

The valuation premium reflects transformation, not steady-state operations. Over the last decade, Dalmia Bharat has emerged as one of the fastest growing cement companies with its capacity and revenue growth pegged at almost 14% and 17% CAGR respectively. As recent acquisitions reach optimal utilization by FY26, EBITDA could surge 40-50%. The market prices tomorrow's earnings, not yesterday's struggles.

Infrastructure spending, India's economic priority, directly benefits cement demand. The government's ₹100 trillion infrastructure pipeline through 2030 requires 450 million tonnes of cement annually versus current consumption of 380 million tonnes. This structural deficit means pricing power returns despite capacity additions. Dalmia's strategic locations near infrastructure projects position them to capture disproportionate value.

The sustainability leadership creates tangible competitive advantages. European construction giants like LafargeHolcim specify low-carbon cement for Indian projects to meet their global carbon commitments. Dalmia wins these contracts by default—competitors can't match their carbon footprint. As carbon border taxes proliferate globally, Dalmia's green cement could access export markets closed to high-emission producers.

The capital allocation track record suggests management excellence. The 2015 OCL acquisition, initially questioned, now generates 25% ROE. The Belgian refractories sale at 24x EBITDA demonstrated timing prowess. Management thinks in decades, not quarters—rare in Indian corporations. Their conservative balance sheet (debt-to-equity below 1x) provides flexibility to acquire distressed assets during downturns.

Regional dominance trumps national presence in cement's local market dynamics. In Northeast India, Dalmia controls distribution, relationships, and logistics—new entrants would need years to challenge this position. These regional monopolies generate 25%+ EBITDA margins, subsidizing expansion elsewhere. UltraTech might be bigger nationally, but Dalmia rules its kingdoms.

The organization's technical DNA creates sustainable advantages. With three R&D centers developing proprietary cement variants, Dalmia isn't just manufacturing commodity cement but engineered solutions. Their oil well cement, railway sleeper concrete, and marine-grade variants command 30-40% premiums. This specialization focus, impossible for diversified giants, generates superior returns.

The hidden asset lies in distribution. With 49,300 channel partners, Dalmia has deeper penetration in its markets than apparent from capacity statistics. This distribution network, built over decades, would cost ₹5,000+ crores to replicate. As rural construction booms, this last-mile connectivity becomes invaluable. New entrants might build plants but can't build relationships overnight.

The family ownership, rather than weakness, provides strategic patience. While listed competitors face quarterly pressures, Dalmia can accept lower returns during transformation years. The family's 55.8% stake aligns interests—they profit only when minority shareholders do. This long-term orientation enables contrarian bets like carbon capture that public companies couldn't justify.

The ultimate bull case rests on India's economic transformation. As per-capita cement consumption rises from 250 kg to the global average of 500 kg, demand doubles. In this scenario, everyone wins, but efficient producers win more. Dalmia's low-cost position, sustainability leadership, and operational excellence position them to capture disproportionate value from India's building boom. The question isn't whether demand materializes but whether Dalmia can execute its expansion without stumbling.

XI. Epilogue & "What Would We Do?"

Standing at the crossroads of 2024, Dalmia Bharat faces choices that will determine whether it remains an independent force or becomes another chapter in India's consolidation story. The path to 110-130 million tonnes by 2031 seems clear on paper—complete the Jaypee acquisition, add 15 million tonnes annually through brownfield expansion, perhaps another strategic acquisition. But execution is where strategy goes to die.

If we were advising the Dalmia family, our first prescription would be uncomfortable: slow down the capacity race and double down on differentiation. The industry adds 40 million tonnes annually; fighting this tsunami with more capacity is futile. Instead, convert 50% of capacity to specialty products—oil well cement, railway concrete, marine-grade variants—where Dalmia's technical expertise commands premiums. Let UltraTech and Adani slug it out in commodity Portland cement while Dalmia becomes India's Holcim, not its biggest but its best.

The international expansion opportunity deserves serious consideration, but not in the conventional way. Rather than building plants overseas, become India's cement technology exporter. Dalmia's carbon capture expertise, waste heat recovery systems, and alternative fuel capabilities have global demand. License technology to African and Southeast Asian cement companies for royalties. Build an engineering services division that generates 15-20% EBITDA margins without capital investment. This asset-light international strategy sidesteps capital constraints while leveraging intellectual property.

The sustainability narrative needs evolution from cost to revenue. Create a separate green cement brand commanding 10-15% premiums, marketed directly to environmentally conscious consumers and corporations. Partner with real estate developers to create "carbon-neutral buildings" using Dalmia's negative-emission cement. Turn sustainability from corporate responsibility to profit center. The premium segment might remain small—10% of volumes—but could contribute 25% of profits.

Technology investments should focus on disruption, not optimization. While competitors digitize existing processes, Dalmia should explore 3D printing concrete for construction, self-healing cement that extends building life, or carbon-negative concrete that actively absorbs CO2. Partner with IITs and international universities to incubate breakthrough technologies. Even one success could transform industry economics.

The organizational structure needs radical surgery. Split into three divisions: commodity cement (volume game), specialty products (margin game), and sustainability solutions (technology game). Give each division separate P&L responsibility, capital allocation authority, and performance metrics. The commodity division focuses on cost; specialty on innovation; sustainability on disruption. This prevents commodity thinking from contaminating higher-value businesses.

Capital structure optimization could unlock immediate value. The current dividend yield of 0.40% satisfies neither growth nor income investors. Implement a formulaic capital allocation policy: 50% of free cash flow for growth capex, 30% for dividends, 20% for buybacks when stock trades below intrinsic value. This transparency would reduce the holding company discount while maintaining growth flexibility.

The succession planning needs attention before it becomes urgent. Professionalize management by bringing in external CEOs for operating divisions while family retains board control. Create a family council separate from business operations, handling wealth management and philanthropy. Establish clear rules for next-generation entry—mandatory external experience, performance-based progression, rotation across businesses. This prevents the succession battles that destroyed other family empires.

Brand building requires a different approach in commodities. Instead of advertising cement, sponsor infrastructure. Fund engineering scholarships, establish construction worker training institutes, create affordable housing foundations. Build brand equity through social infrastructure, not television commercials. When customers choose Dalmia, they support community development, not just buy cement.

The M&A strategy needs discipline. Avoid bidding wars with UltraTech or Adani—they have deeper pockets. Instead, focus on stressed assets, international technology companies, or adjacent businesses like ready-mix concrete. The next acquisition should strengthen capabilities, not just add capacity. Pay cash for distressed assets, stock for strategic mergers, maintaining balance sheet flexibility.

Risk management must evolve beyond financial metrics. Climate risk is business risk—floods affecting plants, water scarcity constraining production, carbon taxes destroying margins. Invest in climate adaptation—flood defenses, water recycling, renewable energy—not as ESG initiatives but as business continuity. The company that survives climate change wins by default.

The ultimate strategic choice is existential: remain independent or find a strategic partner. Independence requires achieving 75+ million tonnes capacity to remain relevant, demanding ₹15,000+ crores investment. Alternatively, merge with an international player seeking Indian exposure—LafargeHolcim, HeidelbergCement, or Cemex. Dalmia's sustainability leadership and local knowledge complement their global capabilities. A merger of equals, rather than acquisition, preserves family legacy while accessing global resources.

The next five years will test whether third-generation transformation can overcome first-generation habits. The cement industry offers no prizes for second place—you either consolidate or get consolidated. Dalmia's choice isn't just about capacity or geography but about identity: remain a cement company that happens to be sustainable, or become a sustainability company that happens to make cement. That choice will determine whether Dalmia Bharat builds India's future or becomes part of its past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube