NextEra Energy: The Clean Energy Colossus

I. Introduction & Episode Roadmap

Picture this: It's 2012, and Jim Robo stands before Wall Street analysts as the newly minted CEO of NextEra Energy. The company's market cap hovers around $29 billion—respectable for a utility, unremarkable for the broader market. Fast forward to October 2024, and that same company commands a $170 billion valuation, making it the world's largest electric utility holding company by market capitalization. The transformation that unfolded between those two moments represents one of the most audacious strategic pivots in American corporate history.

NextEra Energy today operates 58 gigawatts of generating capacity and pulls in over $25 billion in annual revenue. But here's what makes this story remarkable: while tech giants were disrupting industries through software and network effects, NextEra built its empire in the most capital-intensive, regulated, and seemingly boring sector imaginable—electric utilities. They didn't just adapt to the energy transition; they architected it.

The central question we're exploring isn't just how a Florida utility founded in 1925 became the world's largest renewable energy developer. It's how they turned the disadvantages of their legacy business—massive capital requirements, regulatory oversight, geographic constraints—into the very foundations of their competitive moat. This is a story about seeing around corners when everyone else is looking straight ahead.

What unfolds is a masterclass in three critical business themes. First, the transformation from regulated monopoly to competitive clean energy giant—a Jekyll and Hyde act that shouldn't work but does. Second, capital allocation mastery in an industry where a single wrong bet can destroy decades of value. And third, the counterintuitive art of building competitive advantages in what appears to be a commodity business.

By the end of this journey, you'll understand how to build scale in capital-intensive industries when Silicon Valley wisdom says asset-light is the only way. You'll see the power of long-term vision in an era obsessed with quarterly earnings. And perhaps most importantly, you'll learn how navigating the byzantine world of regulated markets can become your greatest strategic asset rather than your biggest burden.

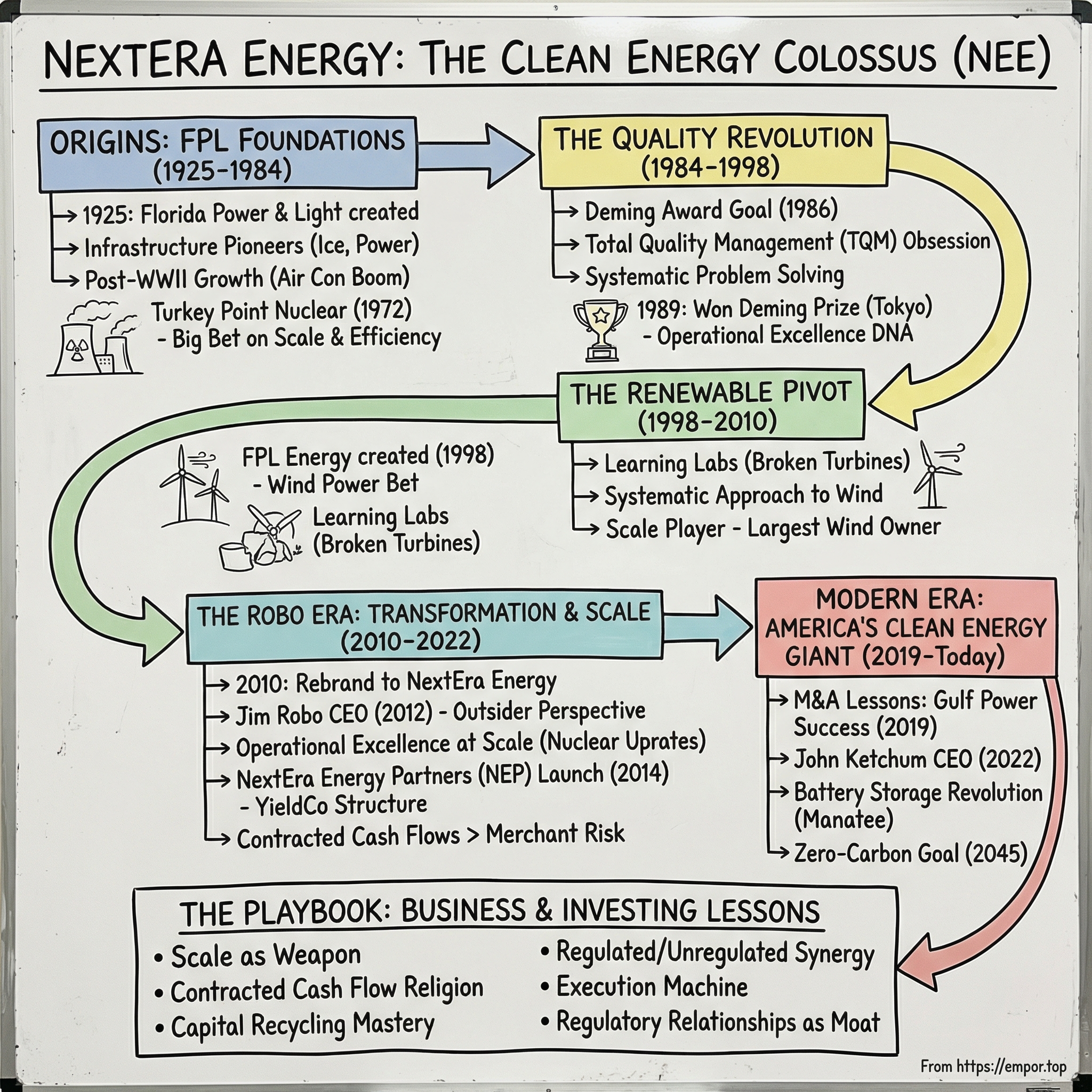

II. Origins: Florida Power & Light Foundations (1925–1984)

The story begins not in a garage or dorm room, but in the swamps and settlements of 1920s Florida. On December 28, 1925, Florida Power & Light Company emerged from the consolidation of dozens of small utilities scattered across the state. The initial entity was less power company and more conglomerate of necessity—owning not just power plants but water facilities, gas plants, ice companies, laundry services, and even an ice cream business. With 76,000 customers across 58 communities, FPL was stitching together the infrastructure of a frontier state that barely resembled the Florida we know today.

This wasn't the methodical expansion of a master plan. It was entrepreneurial chaos meeting desperate need. In pre-air-conditioning Florida, ice wasn't a luxury—it was survival. Electric power wasn't about charging phones; it was about keeping food from spoiling in subtropical heat. The company's early leaders weren't utility executives; they were infrastructure pioneers building civilization from scratch.

The real transformation began after World War II. During the war years, FPL had sent 569 employees—a quarter of its workforce—to the armed forces. The company responded by hiring women for positions previously considered men's work: meter reading, truck driving, mechanical repairs. This wartime flexibility would prove prophetic. When those soldiers returned to a Florida experiencing its first major population boom, FPL had already learned to adapt quickly to dramatic change.

The numbers tell the story of explosive growth. Florida's population doubled from 2.8 million in 1950 to 5.8 million by 1965. FPL's customer base grew even faster. Air conditioning transformed from luxury to necessity, and with it came insatiable demand for electricity. The company was adding new power plants as fast as they could pour concrete, but it wasn't enough. They needed something bigger, more efficient, more scalable.

Enter the nuclear age. In 1972, FPL's Turkey Point Nuclear Generating Station came online—Florida's first nuclear reactor and a $195 million bet on the future. This wasn't just about adding capacity; it was about fundamentally reimagining what a utility could be. While other Florida utilities stayed small and regional, FPL was thinking in terms of baseload power for millions.

The decision to go nuclear revealed something crucial about FPL's DNA: they were willing to make massive, irreversible bets on technologies others feared. Nuclear power in the 1970s was controversial, expensive, and fraught with regulatory risk. But FPL's leadership saw what others missed—that scale and efficiency would ultimately matter more than flexibility in the utility business.

By 1984, FPL had grown so large and complex that it reorganized into FPL Group, a holding company structure that would allow for diversification beyond the regulated utility. The stated goal was to leverage their operational expertise into adjacent markets. The unstated goal was to escape the suffocating embrace of utility regulation. They had built an impressive Florida franchise, but the question loomed: was being a well-run regional utility enough? The answer would drive the next phase of their evolution.

III. The Quality Revolution & Deming Award (1984–1998)

The transformation that would set NextEra apart began not with a strategic acquisition or technological breakthrough, but with an obsession that bordered on the religious: quality improvement. In 1986, FPL's chairman Marshall McDonald returned from Japan with what seemed like an impossible dream—to become the first non-Japanese company to win the prestigious Deming Award for quality management.

To understand the audacity of this goal, consider the context. The Deming Award was Japan's highest honor for operational excellence, created to recognize companies that achieved breakthrough improvements through Total Quality Management. No American company had ever won it. No utility had even attempted it. McDonald was essentially declaring that a Florida power company would out-Japanese the Japanese at their own game.

The pursuit consumed the company. FPL invested millions of dollars and countless hours training every single employee in statistical process control, root cause analysis, and continuous improvement methodologies. They created 1,800 quality improvement teams. Employees learned to map processes with the precision of Swiss watchmakers. They tracked everything—from the time to answer customer calls to the number of minutes of power interruption per customer per year.

The cultural transformation was jarring. Utility companies in the 1980s operated like government bureaucracies—slow, hierarchical, risk-averse. FPL was asking linemen to think like management consultants, customer service reps to act like process engineers. The resistance was fierce. Many longtime employees saw it as Japanese corporate imperialism, an abandonment of American management traditions.

But something remarkable happened. As teams began solving problems systematically rather than reactively, performance metrics started moving in ways nobody expected. Customer complaints dropped by 60%. The average service unavailability fell from 75 minutes per customer per year to 48 minutes. Operating costs per kilowatt-hour generated decreased even as service quality improved. The impossible was becoming inevitable.

Meanwhile, FPL Group was learning hard lessons about diversification. In 1985, they acquired Colonial Penn Insurance for $566 million, convinced they could apply utility-style operational excellence to insurance. The logic seemed sound: both were regulated industries with predictable cash flows and large customer bases. The reality was brutal. Insurance required completely different capabilities—actuarial expertise, sales culture, risk assessment. By 1991, they sold Colonial Penn at a loss, admitting what should have been obvious: being good at running power plants doesn't make you good at assessing mortality risk.

November 14, 1989, marked FPL's finest hour. In Tokyo, they were awarded the Deming Prize, the first company outside Japan to achieve this recognition. The Japanese judges were stunned by the transformation—here was an American utility that had internalized quality principles more thoroughly than many Japanese companies. The award ceremony was broadcast on Japanese television. Florida linemen had become celebrities in Tokyo.

But the real prize wasn't the trophy. The quality revolution had fundamentally rewired FPL's organizational DNA. They now had 15,000 employees who thought in terms of continuous improvement, who saw problems as opportunities for systematic solutions. This cultural transformation would prove invaluable when the company later pivoted to renewable energy—a business that rewards operational excellence and continuous cost reduction above all else.

By 1998, FPL Group was ready for its next act. They created FPL Energy as a subsidiary to pursue opportunities outside their regulated Florida territory. They attempted to acquire 37 power stations across Maine, Massachusetts, and New Jersey. The quality revolution had given them operational confidence. Now they needed strategic direction. The stage was set for their renewable energy transformation.

IV. The Renewable Energy Pivot (1998–2010)

The year 1998 marked a curious moment in energy history. Oil traded at $12 a barrel. Natural gas was cheap and plentiful. Climate change was still debated in op-ed pages rather than boardrooms. Against this backdrop, FPL Group made a decision that seemed either visionary or foolish: they would bet big on wind power through their newly created subsidiary, FPL Energy.

The origin of this pivot wasn't some grand environmental awakening. It was opportunistic pattern recognition. The Public Utility Regulatory Policies Act of 1978 had created requirements for utilities to buy power from renewable sources. The Energy Policy Act of 1992 had opened wholesale power markets. Production tax credits made wind economics suddenly interesting. FPL Energy's leadership saw these policy tailwinds and asked: what if we became the scale player in a fragmented market?

Their early wind projects were learning laboratories. The company's first major wind farms in Iowa and Texas revealed brutal realities. Wind turbines broke down constantly. Gearboxes failed. Blades cracked. Availability rates—the percentage of time turbines actually generated power—hovered around 75%, making economics marginal at best. One executive later recalled counting dead turbines across West Texas and wondering if they'd made a terrible mistake.

But FPL Energy approached these problems with the systematic rigor inherited from their Deming days. They created failure databases, tracking every component breakdown across their fleet. They negotiated volume agreements with turbine manufacturers, demanding improved warranties and performance guarantees. They developed proprietary operating procedures that pushed availability rates above 95%. What others saw as inherent limitations of wind power, FPL Energy treated as engineering problems to be solved.

The Stateline Wind Energy Center, which came online in 2001 spanning Oregon and Washington, showcased their emerging playbook. At 300 megawatts, it was the world's largest wind farm when completed. But size wasn't the innovation. FPL Energy had figured out how to develop, finance, construct, and operate wind farms at a scale and efficiency nobody else could match. They were becoming the McDonald's of wind power—standardized, systematic, relentlessly efficient. The competitive landscape in the early 2000s was fragmented and amateurish. Wind developers were mostly small, venture-backed companies or European firms testing American markets. Between 2002 and 2003, the company built or acquired 17 different wind farms across the country, including in Texas, Iowa, Pennsylvania, South Dakota, California, New Mexico, Oklahoma, North Dakota and Minnesota. This aggressive expansion wasn't just about adding megawatts—it was about achieving critical mass before competitors realized what was happening.

The merger discussions that peppered this period reveal the strategic tensions within FPL Group. Through the early 2000s, FPL Group was the subject of multiple merger discussions, including with Iberdrola, Entergy, and Constellation Energy. Each potential deal represented a different vision for the company's future. Iberdrola would have meant doubling down on renewables with a European partner. Entergy or Constellation would have created a traditional utility giant. That none of these deals closed proved fortuitous—FPL Energy was better off building than buying.

In 2005, FPL Group acquired Gexa Energy. This retail electricity provider in Texas represented a different kind of bet—on deregulated markets and customer relationships. While Gexa never became central to the NextEra story, it showed the company's willingness to experiment with business models beyond pure generation.

By 2007, the renewable strategy was generating internal tensions. That year, Florida regulators rejected FPL's plan to build a coal plant near the Everglades, a reminder that the regulated utility and competitive renewable businesses were increasingly at odds strategically. Coal made sense for baseload power in Florida. Wind made sense for the future. The company was trying to ride two horses heading in different directions.

The financial crisis of 2008-2009 proved to be FPL Energy's opportunity. While competitors retreated, they accelerated. Credit markets froze, but FPL Energy had the balance sheet of a regulated utility behind them. They could finance projects when pure-play renewable developers couldn't. They bought distressed assets at fire-sale prices. They locked in turbine orders when manufacturers were desperate for customers. FPL Energy became the largest owner and operator of wind power in the world.

What started as an opportunistic diversification play had become a transformational strategy. FPL Energy wasn't just participating in the renewable energy market—they were defining it. Their systematic approach to development, construction, and operations had created a playbook others would spend the next decade trying to copy. The renewable pivot was complete.

V. The Robo Era: Transformation & Scale (2010–2022)

The corporate name change in 2010 from FPL Group to NextEra Energy might seem like typical rebranding fluff, but it marked a fundamental shift in identity. The following year, FPL Group rebranded as NextEra Energy. At the time, it provided power in 28 states and Canada. This wasn't a Florida utility with side businesses anymore. This was an energy company that happened to own a Florida utility.

Jim Robo's ascension to CEO in 2012 brought a new kind of leadership to the utility sector. Robo hadn't climbed through utility operations like most industry CEOs. He'd joined as VP of corporate development in 2002 from General Electric, where he'd learned Jack Welch's playbook of operational excellence and aggressive capital deployment. His background was Harvard MBA and Wall Street, not engineering and grid operations. To the old guard, he was an outsider. To investors, he was exactly what the industry needed.

The numbers from Robo's tenure tell a story of unprecedented value creation. The company grew from a $29 billion market cap when he became CEO to over $150 billion by his retirement—a more than 5x increase while the S&P 500 merely doubled. But raw appreciation understates the transformation. Robo didn't just grow NextEra; he reinvented what a utility could be.

The company celebrated the commissioning of its 10,000th MW of wind energy. To put that in perspective, 10,000 megawatts could power roughly 7.5 million homes. NextEra had built more wind capacity than most countries. But Robo understood that scale alone wasn't enough. The real advantage came from operational excellence at that scale.

The nuclear operations showcased this perfectly. NextEra Energy completed the largest multi-state nuclear uprate project in U.S. history. The multi-billion dollar expansion at St. Lucie, Turkey Point and Point Beach involved six separate nuclear units. These weren't new plants—they were efficiency improvements to existing assets, squeezing more megawatts from the same infrastructure. It was the Deming philosophy applied to nuclear physics.

The masterstroke of the Robo era was the 2014 launch of NextEra Energy Partners (NEP). The company launched NextEra Energy Partners, a growth-oriented limited partnership to acquire, manage and own contracted clean energy projects with stable, long-term cash flows. At the time, it was the most successful IPO of its kind.

The YieldCo structure was financial engineering at its finest. NextEra Energy Resources would develop projects, then "drop down" completed assets to NEP at attractive valuations. NEP would pay cash, which NextEra would recycle into new development. Meanwhile, public investors got access to stable, contracted renewable cash flows with high distribution yields. It was a perpetual motion machine for capital recycling.

But NEP was more than clever finance. It solved a fundamental problem in renewable development: the mismatch between development risk and operating risk. Developing wind and solar projects requires expertise, relationships, and risk tolerance. Operating them requires patient capital seeking steady returns. By separating these functions into different vehicles, NextEra could optimize for both.

The strategic focus during this period was relentless: contracted cash flows over merchant risk. While competitors built projects hoping to sell power at favorable spot prices, NextEra insisted on long-term power purchase agreements (PPAs) with creditworthy utilities. This meant lower returns but also lower risk. In an industry where a single bad project could destroy years of value creation, boring was beautiful.

Under Robo as NEER CEO, the company executed its largest three-year capital investment program in history, deployed tens of billions in renewable projects, and nearly doubled its development backlog. They pioneered $5 billion in capital recycling—selling operational assets to fund new development. Every dollar was working harder than the last.

The culture Robo built was unique in the utility sector. He recruited talent from investment banks, consulting firms, and tech companies. He paid for performance, not tenure. He pushed decision-making down the organization while maintaining strict financial discipline. One former executive described it as "Goldman Sachs meets Toyota Production System meets Florida utility"—a combination that shouldn't work but did.

By 2022, when Robo handed the reins to John Ketchum, NextEra Energy had become something unprecedented: a regulated utility that was also the world's largest renewable developer, a capital-intensive infrastructure company that traded at tech-like multiples, a 97-year-old firm that operated like a growth startup. The transformation was complete, but the story was far from over.

VI. Failed M&A Attempts & The Gulf Power Success (2015–2019)

The string of failed acquisitions from 2015 to 2019 reads like a comedy of errors, but each failure taught NextEra valuable lessons about the limits of their expansion strategy. The attempted deals—Hawaiian Electric, Oncor, SCANA, Santee Cooper—represented billions in proposed investments and years of management attention. The 2010s saw additional merger and acquisition attempts by NEE, including with Hawaiian Electric Industries, Oncor Electric Delivery, SCANA, Santee Cooper, and Gulf Power Company. Of these, only the Gulf Power acquisition was successful.

The Hawaiian Electric saga was particularly revealing. NextEra announced the $4.3 billion deal in December 2014, promising to accelerate Hawaii's transition to renewable energy. They offered to reduce customer bills, increase rooftop solar adoption, and help Hawaii achieve its 100% renewable goal. On paper, it was perfect—an isolated island grid desperately needing renewable expertise meeting the world's best renewable developer.

But NextEra had misread the room. Hawaii regulators saw a mainland corporation trying to colonize their energy system. Local stakeholders worried about job losses and decision-making moving to Florida. The application NextEra submitted lacked the detail regulators expected, suggesting arrogance or incompetence. After 18 months of hearings, Hawaii killed the deal. NextEra had spent millions and had nothing to show for it.

The Oncor pursuit in 2017 was even more ambitious—a $12 billion bid for Texas's largest transmission and distribution utility. Oncor owned 140,000 miles of power lines serving 10 million Texans. For NextEra, it represented a platform for renewable development across Texas, America's largest wind market. They structured a complex deal involving Oncor's bankruptcy and a special ownership structure to satisfy Texas regulators who wanted local control.

Texas officials, however, took issue with the financial engineering. They worried NextEra would strip cash from Oncor to fund renewable development elsewhere. They questioned whether Florida executives understood Texas's unique market structure. When Sempra Energy swooped in with a simpler, more Texas-friendly offer, NextEra was outmaneuvered. Another year wasted, another deal dead.

The SCANA debacle in 2018 involved a utility crippled by a failed nuclear project in South Carolina. NextEra offered $15 billion, promising to clean up the nuclear mess and reduce customer rates. But Dominion Energy's competing bid was marginally higher and faced less regulatory resistance. NextEra walked away rather than overpay.

Each failed deal revealed the same pattern: NextEra's financial and operational superiority meant nothing if they couldn't navigate local politics and regulatory preferences. They were playing chess while regulators wanted checkers. Their sophisticated proposals confused rather than convinced. Their Florida success story didn't translate to other states' contexts.

But then came Gulf Power, and everything clicked. The acquisition was completed in January 2019 and NEE merged Gulf Power with FPL in January 2022. This wasn't a hostile takeover of a troubled utility or a complex cross-border merger. It was a friendly acquisition of a neighboring Florida utility from Southern Company, which needed cash for its own troubled nuclear project in Georgia.

Gulf Power served 450,000 customers in northwest Florida—small by NextEra standards but strategically vital. It gave FPL coverage across nearly all of Florida, creating operational synergies in storm response, procurement, and grid management. The cultures were similar, the regulators familiar, the integration straightforward.

The $6.5 billion price tag included not just Gulf Power but also Florida City Gas and ownership stakes in two natural gas plants. NextEra projected $500 million in operational savings over five years—conservative by their standards but achievable. Florida regulators approved the deal with minimal conditions. It was boring, logical, and successful—everything the failed deals weren't.

The lesson from this period wasn't that M&A didn't work for NextEra. It was that successful M&A required humility, local knowledge, and regulatory alignment. You couldn't simply show up with superior operations and expect gratitude. You had to earn the right to operate in each jurisdiction. The Gulf Power success proved NextEra could do deals when they played to their strengths. The failures proved those strengths had limits.

VII. Modern Era: America's Clean Energy Giant (2019–Today)

The scale of NextEra's modern operations defies easy comprehension. Florida Power & Light Company serves more than 6 million accounts, providing electricity to around 12 million people in Florida. NEER, together with its affiliated entities, is the world's largest generator of renewable energy from wind and solar. These aren't just impressive statistics—they represent a complete reimagining of what an American utility can be.

John Ketchum's appointment as CEO in 2022 brought fresh energy to an already ambitious company. Unlike the financial engineering focus of the Robo era, Ketchum emphasized operational excellence and strategic partnerships. His background running NextEra Energy Resources gave him deep understanding of the renewable development business. He knew where the bodies were buried and where the opportunities lay hidden.

The battery storage revolution exemplifies NextEra's ability to ride technology curves. Battery component installation began on the Manatee Energy Storage Center in Florida by its subsidiary Florida Power & Light, which at 409MW / 900MWh is thought to be the largest battery system paired with an existing solar PV power plant under construction to date in the world. This wasn't just adding batteries to the grid—it was fundamentally rethinking how electricity systems operate.

The strategic pivot to storage solved multiple problems simultaneously. It addressed the intermittency of renewables, turning solar farms into dispatchable power plants. It provided grid services that commanded premium prices. Most importantly, it created a new growth vector just as wind and solar were becoming commoditized. NextEra wasn't just participating in the storage boom—they were defining it.

NextEra Energy sets goal to achieve zero-carbon emissions by no later than 2045. This commitment sounds like standard corporate greenwashing until you realize NextEra has the scale and capabilities to actually achieve it. They're not making promises about purchasing offsets or creative accounting. They're building the physical infrastructure to eliminate carbon from their generation fleet.

The company's development pipeline reveals the magnitude of their ambition. NextEra Energy Partners is planning to have a renewables and energy storage portfolio of 81GW by 2027. The figure would more than a doubling of its present renewables and energy storage portfolio, which stood at 38GW as of the end of September. To contextualize this growth: they're planning to add more renewable capacity in three years than most utilities own in total.

Strategic partnerships have become central to NextEra's growth strategy. In June 2024, Entergy and NextEra Energy Resources announced a joint development agreement that will accelerate the development of up to 4.5 gigawatts (GW) of new solar generation and energy storage projects. Rather than competing with other utilities, NextEra positions itself as their partner in the energy transition. They provide the expertise and scale; utilities provide the customers and regulatory relationships.

The financial metrics tell a story of disciplined execution. NextEra Energy, Inc. (NYSE: NEE) has posted its first-quarter 2025 financial results. With trailing twelve-month revenue of $25.26 billion and 2024 revenue of $24.75 billion, the company maintains steady growth even as it deploys tens of billions in capital. This isn't the boom-bust cycle typical of commodity businesses—it's predictable, contracted growth.

FPL's Florida operations showcase how the regulated utility business funds the renewable growth engine. The subsidiary is on track to install 30 million solar panels by 2025, transforming Florida into one of America's leading solar states despite lacking renewable mandates. They're proving that clean energy can win on economics alone, without policy support.

The operational statistics boggle the mind. NextEra operates 35,052 MW of generating capacity across their fleet. They maintain 91,000 circuit miles of transmission and distribution lines. NextEra Energy Resources has 119 wind projects in the United States and Canada. Each number represents thousands of individual assets, each requiring maintenance, optimization, and careful management.

But perhaps the most impressive achievement is cultural. NextEra has maintained entrepreneurial energy while operating at massive scale. They've attracted talent from across industries—tech workers seeking climate impact, financiers wanting to build rather than just model, engineers drawn to solving real-world problems. In 2025, NextEra Energy was once again ranked #1 in the electric and gas utilities industry on Fortune's list of World's Most Admired Companies. We have earned this recognition 17 times in the last 19 years.

The modern NextEra Energy stands as proof that incumbent advantages—capital, scale, expertise, relationships—still matter in the 21st century economy. While Silicon Valley preaches disruption, NextEra demonstrates the power of transformation from within. They didn't destroy the old utility model; they transcended it.

VIII. Playbook: Business & Investing Lessons

The NextEra playbook reads like a masterclass in turning supposed disadvantages into moats. While Silicon Valley preaches asset-light business models, NextEra proved that in energy, scale is destiny. Their fundamental insight: renewable energy development isn't a technology business—it's an industrialization business where the winners achieve manufacturing-like efficiencies at massive scale.

Scale as Competitive Weapon

That scale is increasingly giving it a competitive advantage over smaller developers. It can get equipment at lower prices while locking in lower capital costs. That's enabling it to win more business and earn higher returns. When NextEra negotiates with turbine manufacturers, they're not buying dozens of units—they're buying thousands. This purchasing power translates directly to project economics that competitors can't match.

The numbers tell the story. We are one of the largest purchasers of major energy-related equipment and other supplies. This provides economies of scale that provide buying power and result in cost efficiencies that benefit our customers. A 10% cost advantage on equipment might seem modest, but in a business where returns are measured in single digits, it's the difference between winning and losing.

The Contracted Cash Flow Religion

NextEra's most important strategic choice was refusing to play the merchant power game. While competitors built projects hoping to sell power at favorable spot prices, NextEra insisted on 20-year power purchase agreements with investment-grade utilities. This meant accepting lower returns—perhaps 7-9% instead of potential 15%—but it also meant predictable, bankable cash flows that could support massive capital deployment.

The size and diversity of this backlog offer several advantages. First, it provides revenue visibility, allowing the company to plan and allocate resources effectively. Second, it demonstrates NextEra's strong market position and ability to secure large-scale projects in a competitive landscape. Lastly, the backlog's scale allows for economies of scale in procurement and development, potentially improving project economics and profitability.

Capital Recycling Mastery

The YieldCo structure through NextEra Energy Partners created a perpetual capital recycling machine. Develop projects at 10-12% unlevered returns, sell them to NEP at 7-8% yields, reinvest the proceeds at 10-12%. Rinse and repeat. It's financial engineering, but grounded in real asset development rather than paper shuffling.

This recycling strategy solved the fundamental problem of renewable development: you need massive capital to build projects, but once operational, they're boring, stable assets better suited for yield-seeking investors. By separating development from ownership, NextEra could optimize for both.

The Regulated/Unregulated Synergy

Most see regulated utilities and competitive generation as fundamentally different businesses. NextEra saw them as complementary. The regulated utility provides stable cash flows and a strong credit rating—One of the biggest scale advantages NextEra Energy has is its strong balance sheet backed by an A bond rating. Ketchum noted the company's strong credit rating gives it a cost of capital advantage—while the competitive business provides growth. Together, they create a self-reinforcing cycle.

Long-Term Thinking in Short-Term Markets

Energy markets are notoriously cyclical, with boom-bust patterns that destroy capital and companies alike. NextEra's approach: ignore the cycles and focus on secular trends. When natural gas prices crashed in 2014-2016, making renewable economics challenging, NextEra kept building. They understood that renewable costs would continue declining while fossil fuel costs would remain volatile.

According to the company's analysis, new onshore wind ($25-$50/MWh) and solar ($35-$75/MWh) are significantly more cost-effective than new natural gas combined cycle ($90-$115/MWh) and small modular nuclear reactors ($130-$150/MWh). This cost advantage isn't temporary—it's structural and widening.

Technology Platform Approach

The company's scale and experience in developing and operating renewable energy projects give it a significant edge in terms of efficiency and cost-effectiveness. Its use of proprietary big data and AI technologies further enhances its ability to optimize project development and operations. NextEra treats renewable development like a technology platform business—standardized processes, data-driven optimization, continuous improvement.

They've built proprietary systems for everything from wind resource assessment to construction scheduling to operational optimization. These aren't one-off projects; they're iterations of a constantly improving template.

Leadership Philosophy

The company operates on four key pillars that permeate every decision: teamwork, execution, innovation, and disciplined capital management. These aren't just corporate buzzwords—they're observable in how NextEra operates. Teamwork means breaking down silos between regulated and competitive businesses. Execution means hitting development targets quarter after quarter. Innovation means being first to battery storage at scale. Disciplined capital management means walking away from deals that don't meet return hurdles.

The Network Effects Nobody Sees

While renewable energy lacks traditional network effects, NextEra has created pseudo-network effects through scale. Our in-house team of professionals has the capability to take projects from site evaluation to commercial operation. Our team includes individuals with expertise in site development and permitting; legal and environmental compliance; interconnection analysis, engineering and construction; operations and maintenance; and project finance.

Every project makes the next one easier. Every relationship with a landowner creates opportunities for adjacent development. Every utility PPA establishes credibility for the next negotiation. Every operational improvement can be deployed across thousands of assets.

The lesson for investors and operators: in capital-intensive industries, competitive advantages come not from disruption but from patient accumulation of capabilities, relationships, and scale. NextEra didn't revolutionize energy; they industrialized it.

IX. Power Dynamics & Analysis

The competitive landscape in American energy reveals NextEra's unique position—neither pure utility nor pure renewable developer, but something more powerful than either. Traditional analysis frameworks fail to capture the strategic dynamics at play. This isn't about market share percentages or competitive matrices. It's about who controls the infrastructure for America's energy transition.

The Regulated Utility Comparison

Against traditional utilities like Duke Energy, Southern Company, and Dominion, NextEra operates in a different dimension. NextEra Energy's ROE stood at 11.6% for Q4 2024, reflecting a strong ability to generate profits from shareholders' equity. In comparison, the company's ROI was 7.4%, indicating efficient use of its investments to generate earnings. These metrics exceed most regulated utility peers who struggle to achieve double-digit ROEs in today's regulatory environment.

But the real differentiation isn't in financial metrics—it's in strategic positioning. While Duke and Southern Company defend aging coal fleets and navigate stranded asset risks, NextEra has already pivoted to the future. Their Florida franchise generates cash to fund renewable development, while competitors' regulated businesses constrain their strategic options.

The Renewable Pure-Play Challenge

Companies like Ørsted, Brookfield Renewable Partners, and Pattern Energy represent a different competitive vector. These renewable pure-plays often boast higher growth rates and trade at premium multiples. But they lack NextEra's fundamental advantages: access to low-cost capital through the regulated utility, operational expertise at massive scale, and the ability to weather commodity cycles.

The recent financial performance tells the story. NextEra Energy had strong operational and financial performance in 2024, delivering full year adjusted earnings per share of $3.43, up over 8% from 2023, once again at the high end of our adjusted EPS expectations range. Since 2021, we have delivered compound annual growth in adjusted EPS of over 10%, which is the highest among all top 10 power companies. In fact, if you look over the last five, 10, 15 and 20 years, you will see the same absolute and relative performance.

The Cost Advantage Moat

NextEra's true competitive advantage lies in their ability to deliver renewable energy at costs competitors can't match. They've achieved what seemed impossible: making renewables cheaper than fossil fuels without subsidies. According to the company's analysis, new onshore wind ($25-$50/MWh) and solar ($35-$75/MWh) are significantly more cost-effective than new natural gas combined cycle ($90-$115/MWh) and small modular nuclear reactors ($130-$150/MWh).

This cost leadership stems from multiple reinforcing factors. Scale enables better equipment pricing. Operational excellence drives higher capacity factors. Financial strength secures lower cost of capital. Experienced development teams navigate permitting and interconnection faster. Each advantage reinforces the others, creating a widening moat.

The Execution Machine

While competitors talk about ambitious renewable targets, NextEra delivers consistent execution. Energy Resources Adjusted Earnings Growth: More than 13% year-over-year for full year 2024. Energy Resources New Investments Contribution: Increased by $0.48 per share in 2024. Energy Resources Renewables Backlog: More than 25 gigawatts. This isn't promise—it's performance.

The consistency matters more than the magnitude. In an industry plagued by project delays, cost overruns, and development failures, NextEra's predictability becomes its own competitive advantage. Utilities choosing development partners know NextEra will deliver on time and on budget. That reliability commands premium pricing and preferred partner status.

Capital Markets Positioning

NextEra has achieved something remarkable in capital markets: utility-like stability with growth company multiples. NextEra Energy reported an EPS of $1.45 for Q4 2024, which compared favorably to the $1.30 EPS reported in Q3 2024. This represents a +11.5% quarter-over-quarter (QoQ) growth, signifying a healthy profitability trend. The company's total revenue for Q4 2024 stood at $5.3 billion, demonstrating consistent operational momentum.

The company's financial engineering sophistication sets them apart. Interest Rate Hedges: $28.5 billion in place. While competitors scramble to manage interest rate exposure, NextEra locked in favorable rates years ago. This foresight translates directly to competitive advantage in project economics.

The Technology Integration Play

Unlike pure utilities or renewable developers, NextEra has positioned itself at the intersection of multiple technology curves—solar, wind, batteries, hydrogen, grid software. They're not betting on a single technology winner; they're building the platform that integrates them all.

This positioning becomes crucial as the energy system grows more complex. Data centers need 24/7 clean power—NextEra can provide solar plus batteries. Industrial customers want green hydrogen—NextEra has the renewable capacity to produce it. Grid operators need flexibility—NextEra offers virtual power plants. No competitor matches this solution breadth.

Regulatory Relationships as Competitive Advantage

After decades of operation, NextEra has built regulatory relationships that newer entrants can't replicate. FPL Reported ROE: Approximately 11.4% for full year 2024. FPL Reserve Amortization: $328 million used in 2024, with a year-end balance of $895 million. FPL Capital Expenditures: Approximately $8.2 billion for full year 2024. FPL Retail Sales Growth: 1.9% increase for full year 2024 on a weather-normalized basis. These metrics reflect not just operational excellence but regulatory trust.

The Talent Arbitrage

NextEra has become the employer of choice for energy sector talent. They attract utility executives seeking growth, renewable developers wanting scale, and financial professionals drawn to complex capital structures. This talent concentration creates a virtuous cycle—the best people deliver the best results, attracting more top talent.

Competitive Threats on the Horizon

The greatest threats to NextEra don't come from traditional competitors but from adjacent industries. Tech giants like Amazon, Google, and Microsoft are increasingly entering energy markets directly. Oil majors like Shell and BP bring massive balance sheets to renewable development. Private equity firms deploy unprecedented capital into energy infrastructure.

But NextEra's response reveals confidence: they partner rather than compete with these new entrants. They provide renewable power to tech companies' data centers. They co-develop projects with oil majors. They sell assets to infrastructure funds. By positioning as the essential partner rather than competitor, they turn threats into opportunities.

The power dynamics reveal an inescapable conclusion: NextEra has achieved escape velocity from traditional utility competition while building barriers that pure renewable players can't surmount. They occupy a unique strategic position that becomes more valuable as the energy transition accelerates.

X. Bear vs. Bull Case

The investment case for NextEra Energy presents a fascinating study in contrasts—a company that has defied utility sector gravity for over a decade yet faces mounting challenges that could constrain future performance. Both bears and bulls make compelling arguments grounded in fundamental realities rather than speculation.

Bear Case: The Limits of Growth

The bearish perspective starts with a mathematical reality: trees don't grow to the sky, especially in capital-intensive industries. NextEra's success has created its own constraints. At a $170 billion market capitalization, generating meaningful growth requires deploying tens of billions in capital annually at attractive returns. The law of large numbers becomes an inexorable headwind.

Interest rate sensitivity poses an existential challenge. While management touts their hedging prowess—John Ketchum mentioned that NextEra has $32 billion of interest rate swaps in place with an average coupon of around 3.9%. The sensitivity to interest rate changes is minimal, with an EPS impact of $0.01 to $0.03 for 2025 and 2026, and $0.03 to $0.05 for 2027—these hedges eventually roll off. In a sustained high-rate environment, NextEra's capital-intensive model faces severe pressure. Every 100 basis point increase in borrowing costs translates to billions in additional interest expense.

Regulatory risks loom larger as NextEra's influence grows. The company's aggressive lobbying against rooftop solar and net metering has generated significant backlash. Critics argue NextEra fights to preserve utility monopolies while claiming to champion clean energy. This reputational risk could manifest in adverse regulatory decisions, particularly as populist sentiment grows against large corporations.

The technological disruption threat is real and accelerating. Distributed energy resources—rooftop solar, home batteries, microgrids—directly challenge the centralized utility model. While NextEra participates in utility-scale renewables, they're structurally disadvantaged in distributed generation. If the future is truly distributed, NextEra's massive centralized assets could become stranded.

Execution risk scales with ambition. NextEra plans to deploy $50-55 billion in capital over the coming years. Each project carries development risk, construction risk, operational risk. While their track record is strong, the sheer volume of projects increases the probability of material failures. One major project disaster—a wind farm that doesn't perform, a nuclear incident, a transmission failure—could destroy billions in value.

The competitive landscape is intensifying. The cost of gas-fired generation has more than doubled over the last five years due to limited supply of gas turbines and higher EPC costs. There are uncertainties and risks associated with nuclear energy, with new nuclear projects unlikely to contribute significantly to the grid over the next decade. As renewable development becomes mainstream, NextEra's first-mover advantages erode. Oil majors bring larger balance sheets. Tech companies offer higher margins. Private equity deploys patient capital. NextEra's competitive moat may be narrower than it appears.

Political risks have escalated dramatically. Renewable energy has become politically polarized, with federal policy swinging wildly between administrations. State-level policies vary dramatically—Texas welcomes wind farms while other states impose moratoriums. NextEra must navigate this fractured landscape while making 30-year investment decisions.

Bull Case: The Unstoppable Force

The bullish thesis rests on a fundamental observation: NextEra has consistently exceeded expectations for two decades, and the drivers of their success are strengthening, not weakening. Our consistent financial outperformance is due, first and foremost, to the efforts and execution by our team. I couldn't be more proud of how our team has continued to deliver, and I firmly believe that our track record of execution positions us to lead the build out of energy infrastructure across the country in the coming years.

The energy transition represents a multi-trillion-dollar opportunity, and NextEra is perfectly positioned to capture disproportionate value. Electricity demand is inflecting higher after decades of stagnation. Data centers, electric vehicles, industrial electrification, and AI computing drive insatiable power demand. NextEra doesn't need to capture market share; the market is expanding faster than anyone can build.

Cost advantages are structural and widening. NextEra's scale enables procurement savings, operational efficiencies, and financing advantages that compound over time. Smaller competitors face dis-economies of scale. Larger competitors lack NextEra's specialized expertise. This sweet spot is nearly impossible to replicate.

The contracted cash flow model provides remarkable visibility. Energy Resources Renewables Backlog: More than 25 gigawatts. Cash Flow from Operations Growth: More than 17% increase for full year 2024. Unlike merchant generators exposed to volatile power prices, NextEra's long-term PPAs provide predictable revenue streams. This visibility enables aggressive capital deployment with confidence.

Capital recycling creates a perpetual growth engine. Through NextEra Energy Partners and asset sales, the company continuously harvests value from operational assets to fund new development. This model is self-reinforcing—success begets capital begets success.

Regulatory relationships represent an underappreciated moat. After decades of reliable service in Florida, NextEra has earned regulatory trust that translates to favorable rate treatments. Florida Power and Light (FPL) continues to deliver high reliability and outstanding customer service while keeping bills 40% below the national average. The company has a strong balance sheet and has been successful in maintaining a high return on equity, with FPL's reported ROE for regulatory purposes at approximately 11.4% for 2024.

The technology optionality is immense. Battery storage is still early innings. Hydrogen represents a massive future market. Carbon capture could extend fossil asset lives. Grid optimization software commands premium valuations. NextEra doesn't need all of these to succeed—any one could drive another decade of growth.

Management quality stands out in a mediocre sector. While utility executives typically rise through operational ranks, NextEra's leadership brings financial sophistication, strategic vision, and execution discipline rare in the industry. They've consistently allocated capital better than peers, creating enormous shareholder value.

The dividend growth commitment provides downside protection. NextEra targets 10% annual dividend growth through at least 2026, backed by visible cash flow growth. This commitment attracts income investors who provide stable demand for the stock, reducing volatility.

Climate momentum is irreversible regardless of policy volatility. Corporations have committed to net-zero targets. States have enacted renewable mandates. Economics increasingly favor clean energy. These secular forces transcend political cycles.

The Verdict

Both cases have merit, but the weight of evidence favors the bulls with important caveats. NextEra's competitive position is stronger than bears acknowledge, but not as impregnable as bulls assume. The company will likely continue outperforming utility peers while potentially underperforming high-growth technology companies.

The key insight: NextEra is transitioning from a growth story to a value story, from a disruptor to an incumbent. This isn't bearish—many of history's best investments came from companies making this transition successfully. But it requires adjusting expectations from the explosive growth of the past to the steady compounding of the future.

For investors, the question isn't whether NextEra is a good company—it clearly is. The question is whether it's a good investment at current valuations. With the stock trading at premium multiples to both utilities and renewable pure-plays, the market has priced in significant execution. Any stumble could trigger material multiple compression.

The ultimate bull case may be the bear case's weakness: every challenge facing NextEra faces other energy companies worse. In a sector plagued by disruption, transition, and uncertainty, NextEra's relative advantages may matter more than absolute performance. Sometimes the winner isn't the fastest runner but the last one standing.

XI. Epilogue & "If We Were CEOs"

Standing at the intersection of NextEra's first century and its second, we see a company that has transcended its origins so thoroughly that its founders wouldn't recognize it. From ice delivery in 1920s Florida to managing the world's largest renewable energy portfolio—the transformation seems almost mythical. Yet the next chapter may require an even more dramatic reinvention.

If we were sitting in John Ketchum's chair today, staring at the strategic chessboard, several moves would dominate our thinking.

The Data Center Imperative

The AI revolution has created an unprecedented electricity demand shock. Data centers are being announced faster than transmission lines can be built. If we were CEO, we'd create "NextEra Digital"—a dedicated division offering turnkey clean energy solutions for hyperscalers. Not just power purchase agreements, but fully integrated campuses combining renewable generation, battery storage, grid connections, and even cooling systems.

Amazon, Microsoft, and Google are spending hundreds of billions on AI infrastructure. They need partners who can deliver gigawatts, not megawatts. NextEra could become the exclusive energy platform for the AI age, capturing value far beyond commodity electricity sales.

The International Expansion Paradox

NextEra has remained stubbornly American while peers like Iberdrola and Enel built global empires. If we were CEO, we'd selectively enter international markets—but not through traditional expansion. We'd export the NextEra model through management contracts and technical services agreements. Teach others to build renewable energy at scale, take a fee plus upside, minimize capital deployment.

India, Southeast Asia, and Africa need hundreds of gigawatts of clean energy. They don't need another foreign owner; they need expertise. NextEra could become the McKinsey of energy transition—selling knowledge, not kilowatts.

The Virtual Power Plant Revolution

The grid's biggest challenge isn't generation—it's orchestration. If we were CEO, we'd acquire or build a world-class virtual power plant platform. Aggregate millions of distributed resources—solar panels, batteries, EVs, smart thermostats—into grid-scale assets. This isn't about competing with rooftop solar; it's about becoming the operating system that makes distributed resources valuable.

Imagine controlling 50 GW of distributed assets without owning any of them. Pure software margins on top of NextEra's physical infrastructure. This platform could be worth more than the entire utility.

The Hydrogen Hedge

While others debate hydrogen's viability, we'd make asymmetric bets on the infrastructure regardless of which production method wins. If we were CEO, we'd partner with industrial gas companies to build hydrogen pipelines and storage connected to our renewable sites. If green hydrogen succeeds, we're the supplier. If it fails, we've spent relatively little. Optionality with limited downside.

The Regulatory Revolution

The current regulatory model—cost-plus pricing, rate cases, allowed returns—is dying. If we were CEO, we'd proactively propose performance-based rates tied to carbon reduction, reliability, and customer satisfaction. Get ahead of the disruption rather than fighting it. Transform FPL into the model for 21st-century utility regulation, then export that model nationwide.

Strategic Surprises from the Story

The biggest surprise from studying NextEra's history isn't their success in renewables—many predicted that transition. It's their ability to maintain utility-style stability while executing growth-company strategies. They've violated the supposed iron law that you can't be both safe and aggressive.

The second surprise is how little technology mattered compared to execution. NextEra doesn't manufacture solar panels or wind turbines. They don't own breakthrough patents. Their advantage comes from doing ordinary things extraordinarily well, repeatedly, at scale. In an era obsessed with disruption, they've proven that operational excellence still wins.

The third surprise is the power of patient capital in impatient markets. While competitors chased hot trends—fuel cells, clean coal, small modular reactors—NextEra stayed boringly focused on wind and solar. They resisted the siren song of diversification, and that discipline created extraordinary value.

Lessons for Founders

For entrepreneurs studying NextEra's playbook, several lessons emerge:

1. Scale is a strategy, not an outcome. NextEra didn't get big and then gain advantages. They pursued scale deliberately because they understood it would create competitive moats. In capital-intensive industries, subscale equals suboptimal.

2. Boring businesses can create exciting returns. Utilities are the antithesis of sexy Silicon Valley startups. Yet NextEra has generated tech-like returns from utility assets. The lesson: execution matters more than industry selection.

3. Regulatory capture is a two-way street. NextEra shaped regulations as much as regulations shaped them. Rather than viewing government as an obstacle, they made it a partner. This requires long-term thinking and relationship investment most startups avoid.

4. Financial engineering without operational excellence is worthless. NextEra's complex structures—YieldCos, tax equity, project finance—only work because the underlying assets perform. Financial creativity amplifies operational success; it doesn't replace it.

5. Culture eats strategy, but strategy guides culture. NextEra's culture of execution didn't happen accidentally. Leadership deliberately built systems, incentives, and processes that rewarded performance. Strategy shaped culture, which then executed strategy.

The Ultimate Question

As we close this examination, one question lingers: Is NextEra's success replicable, or was it a unique product of time, place, and circumstance? Could another company follow their playbook today?

The honest answer is both yes and no. The specific path—Florida utility becomes renewable giant—is closed. But the meta-strategy remains valid: identify a massive industry transition, build capabilities before competitors recognize the opportunity, scale aggressively when the window opens, then defend with operational excellence.

The energy transition is perhaps one-third complete. Transportation, heating, industrial processes, agriculture—entire sectors await electrification and decarbonization. The NextEra of tomorrow might not be in energy at all. It might be in carbon removal, sustainable agriculture, or climate adaptation.

What matters isn't the industry but the approach: patient capital, operational excellence, strategic focus, and the courage to build at scale when others hesitate. These principles transcend sectors and cycles.

NextEra's story isn't finished. At 100 years old, they're really just beginning. The next century will bring challenges we can't imagine—fusion power, climate catastrophes, technologies not yet invented. But if history is any guide, NextEra will adapt, evolve, and likely thrive.

For investors, operators, and students of business, NextEra offers a masterclass in building enduring value in the real economy. While the digital world captures headlines, companies like NextEra quietly power civilization. Their story reminds us that sometimes the most important businesses are the ones we take for granted—until the lights go out.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube