Ametek: The Industrial Conglomerate That Nobody Knows

I. Introduction & Episode Roadmap

Picture this: You're reading the components list on a semiconductor fabrication machine that costs more than a Manhattan apartment. Or examining the sensors inside the Mars Perseverance rover. Maybe you're looking at the precision instruments measuring jet engine performance on a Boeing 787. Behind each of these technologies, there's a 94-year-old company you've probably never heard of—Ametek.

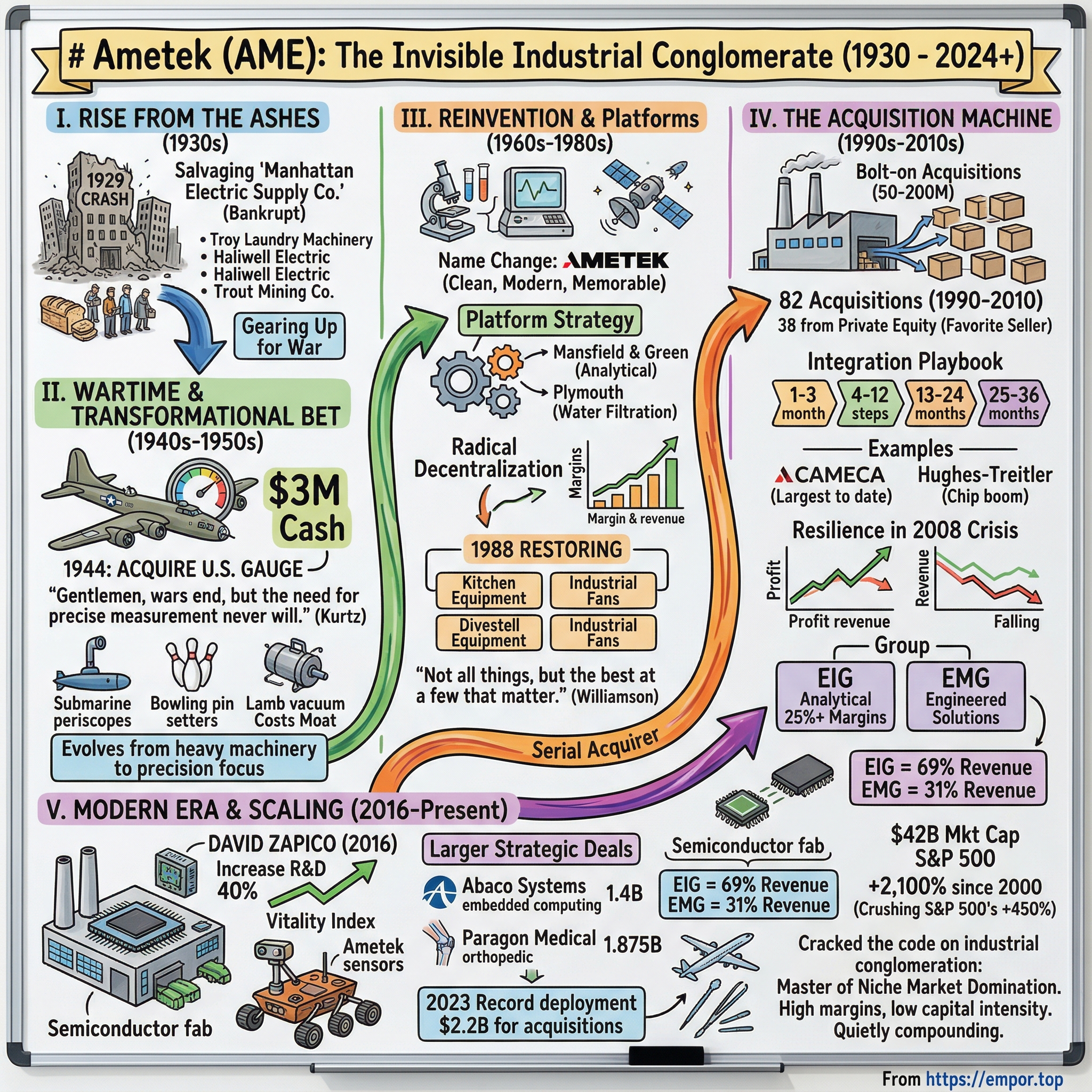

With a $42 billion market cap, Ametek sits comfortably in the S&P 500, larger than household names like Snap, Roku, or Peloton combined. Yet while those companies dominate headlines, Ametek operates in the shadows, quietly compounding wealth for shareholders at rates that would make most tech investors jealous. Since 2000, the stock has returned over 2,100%, crushing the S&P 500's 450% return over the same period.

The company's origin story reads like industrial fiction: In March 1930, as breadlines formed across America and the Dow Jones had lost half its value from its 1929 peak, a group of stockholders gathered to salvage the bankrupt Manhattan Electric Supply Company. What emerged was American Machine and Metals—a hodgepodge of industrial assets that nobody else wanted. Troy Laundry Machinery. Haliwell Electric. The wonderfully named Trout Mining Company. Assets that seemed destined for the scrapheap of the Great Depression.

Today, that collection of industrial castoffs has transformed into a precision instrument powerhouse with over 40 businesses operating across 30 countries. The company's Electronic Instruments Group generates nearly 70% of revenue, producing everything from ultra-high vacuum pumps for semiconductor manufacturing to mass spectrometers that detect chemical weapons. The Electromechanical Group, responsible for the remaining 31%, makes the motors that power surgical tools and the specialty metals used in next-generation aircraft engines.

But here's what makes Ametek truly fascinating: In an era obsessed with disruption and "moving fast and breaking things," this company has perfected the art of moving deliberately and fixing everything. They've completed 82 acquisitions without a single major write-down. They've expanded operating margins for 15 consecutive years. They generate returns on invested capital that routinely exceed 20%.

The thesis for today's deep dive is simple yet profound: Ametek has cracked the code on industrial conglomeration by becoming the master of niche market domination. While everyone else was chasing scale and market share in commodity businesses, Ametek was quietly buying the companies that make the one component nobody else can manufacture—then making it better, cheaper, and more essential than ever before.

What follows is the story of how a Depression-era salvage operation became one of the most successful serial acquirers in American business history. We'll explore the pivotal moments—from the transformative U.S. Gauge acquisition in 1944 that saved the company, to the radical 1988 restructuring that set the template for modern Ametek, to the acceleration under current CEO David Zapico that saw the company deploy $2.2 billion on acquisitions in 2023 alone.

We'll decode their four-pillar growth model that targets double-digit earnings growth through every business cycle. We'll examine why private equity firms have become their favorite sellers, providing 38 of their 82 acquisitions. And we'll answer the question that matters most to investors: In a world where industrial conglomerates have largely fallen out of favor, why does Ametek's model not just survive but thrive?

II. Origins: Rising from the Ashes of the Great Depression

The Woolworth Building's marble lobby echoed with nervous whispers on that March morning in 1930. Manhattan Electric Supply Company—once a thriving electrical equipment distributor—had collapsed into bankruptcy, another casualty of the unfolding economic catastrophe. But while most saw only wreckage, a group of stockholders led by industrialist S.L. Daniels saw opportunity. They weren't looking to liquidate; they were looking to build.

What Daniels and his associates cobbled together from the bankruptcy proceedings was, charitably speaking, an eclectic portfolio. The crown jewel was Troy Laundry Machinery Company of Chicago, which manufactured commercial washing equipment for hotels and hospitals. There was Haliwell Electric Corporation, producing specialty switches for the nascent aviation industry. And then there was Trout Mining Company—yes, a mining operation named after a fish—which owned mineral rights in the Southwest that nobody quite knew what to do with.

The new entity, christened American Machine and Metals, incorporated in Delaware with $5 million in assets and a strategy that could generously be called "opportunistic." While U.S. industrial production plummeted 45% between 1929 and 1932, AME somehow scraped together slight profits. Not because of brilliant strategy or operational excellence, but through sheer stubbornness and the fact that even in the depths of the Depression, hospitals still needed laundry equipment and planes still needed switches.

The company's early annual reports, typed on thin wartime paper that's now yellowed and brittle in corporate archives, reveal a management philosophy that would seem quaint today: "We seek to manufacture products of genuine utility at prices that reflect fair value." No mention of disruption, no talk of total addressable markets. Just products, utility, fair value.

By 1939, as Wehrmacht tanks rolled into Poland and the world descended into war, AME's fortunes shifted dramatically. The U.S. government, scrambling to prepare for a conflict it could no longer avoid, desperately needed manufacturers who could produce precision instruments and specialized equipment. AME's scattered collection of industrial businesses suddenly became strategic assets. Orders poured in for aircraft components, military washing facilities, and precision gauges for weapons manufacturing.

But the truly transformative moment came in 1944, as Allied forces stormed the beaches of Normandy. AME's board made what seemed like an enormous gamble: acquiring U.S. Gauge Company for $3 million in cash—equivalent to 60% of the company's total assets at the time. U.S. Gauge manufactured precision pressure and temperature instruments critical for everything from submarine depth measurements to bomber altitude readings.

The acquisition nearly broke the company. Board minutes from July 1944 reveal heated debates, with one director warning that "this purchase could prove our undoing should peace arrive sooner than expected." But CEO William Kurtz, a former U.S. Navy engineer who understood the importance of precision measurement, pushed it through with an argument that would define Ametek's future: "Gentlemen, wars end, but the need for precise measurement never will."

Kurtz was more right than he could have imagined. U.S. Gauge didn't just survive the post-war transition; it thrived. As American industry retooled for peacetime production, every oil refinery, chemical plant, and power station needed pressure gauges. Every commercial aircraft required altimeters. Every industrial process demanded precise measurement. By 1950, U.S. Gauge products generated nearly half of AME's total revenue.

The post-war years brought a parade of small acquisitions—Westchester Automatic Devices in 1946, Philadelphia Gear Works in 1948, Lamb Electric in 1950. Each added a new capability, a new market, a new group of customers. But more importantly, management was learning something crucial: the power of owning the critical component that nobody else could make.

Consider Lamb Electric, acquired for just $1.2 million. The company made specialized vacuum motors for industrial applications—not sexy, not revolutionary, but absolutely essential for dozens of manufacturing processes. Once customers designed their equipment around a Lamb motor, switching to another supplier meant redesigning the entire system. It was a moat built not on patents or technology, but on the simple physics of integration costs.

By 1955, AME had grown to $25 million in annual sales across seventeen different product lines. The hodgepodge of Depression-era assets had evolved into something more coherent—though calling it focused would be generous. The company made everything from automatic bowling pin setters (the Troy division's unexpected post-war pivot) to submarine periscopes (a classified contract that executives couldn't discuss for decades).

But beneath this seemingly random collection of businesses, a pattern was emerging. Whether by design or accident, AME had stumbled onto a powerful insight: In the industrial world, the most valuable businesses weren't necessarily the biggest or most visible. They were the ones that solved specific, critical problems for customers who had no alternative suppliers. A submarine needs a periscope that won't leak at 500 feet underwater. A refinery needs pressure gauges that won't fail in extreme heat. A hospital needs washing equipment that ensures complete sterilization.

As the 1950s drew to a close, American Machine and Metals stood at a crossroads. The company had survived the Depression, thrived during the war, and successfully navigated the peacetime transition. But it remained a small player in the vast American industrial landscape, with competitors like General Electric and Westinghouse commanding thousand times its market value. The next phase of the company's evolution would require more than opportunistic acquisitions and steady execution. It would require a complete reimagining of what an industrial company could be.

III. The Reinvention: From Heavy Machinery to Precision Instruments (1960s–1980s)

The mahogany-paneled boardroom at 410 Park Avenue was thick with cigarette smoke when the decision was made. It was early 1960, and American Machine and Metals faced an identity crisis. The company name—clunky, industrial, redolent of the Depression era—no longer fit what they were becoming. After hours of debate, someone suggested simply using the company's stock ticker: AMETEK. Clean, modern, memorable. The board voted unanimously.

But changing the name was the easy part. The real transformation was happening on factory floors from Pennsylvania to California, driven by a new generation of engineers who saw opportunity where others saw obsolescence. The industrial landscape was shifting beneath their feet. The Space Race had begun. Electronics were replacing mechanical systems. Precision mattered more than power. And AMETEK was perfectly positioned to ride this wave—if it could shed its heavy machinery past.

The pivotal acquisition came in 1965: Mansfield and Green, a small Massachusetts company that made laboratory instruments for chemical analysis. The price tag of $8 million raised eyebrows—it was AMETEK's largest acquisition to date. But what Mansfield and Green represented was worth far more than its assets. It was AMETEK's entry into the world of analytical instruments, where margins were measured in the 30-40% range rather than the 10-15% typical of heavy machinery.

The integration of Mansfield and Green revealed something remarkable. When AMETEK's engineers applied their precision manufacturing techniques to laboratory instruments, they could produce equipment that was not just cheaper but actually better than the competition. They reduced failure rates by 60%. They cut production time in half. They turned a good business into a great one.

Enter Dr. John Lux, appointed president in 1966. A chemical engineer by training with a PhD from MIT, Lux was unlike any leader AMETEK had seen. Where previous executives managed from Manhattan offices, Lux spent his first year visiting every single AMETEK facility—all 23 of them. He ate in factory cafeterias, worked night shifts with maintenance crews, and held impromptu engineering sessions on factory floors.

"Dr. Lux would show up at 6 AM with his slide rule and start asking questions," recalled Tom Patterson, a retired AMETEK engineer, in a company oral history. "Not gotcha questions, but genuine curiosity. 'Why do we do it this way? What if we tried this instead?' By lunch, we'd have three new ideas to test."

Lux's management philosophy was radical for its time: radical decentralization coupled with rigorous measurement. Each business unit operated as its own profit center, with its own P&L responsibility. But every unit had to report the same metrics, measured the same way, every single month. Revenue per employee. Gross margin. Return on assets. Days sales outstanding. The numbers told the story, and Lux read them like a novel.

In 1967, AMETEK made another seemingly odd acquisition: Plymouth Products, a water filtration company. What did water filters have to do with precision instruments? Everything, it turned out. The same technologies that measured chemical composition could be adapted to analyze water quality. The same customers who bought laboratory instruments needed water purification systems. The same sales force could sell both.

This was the beginning of AMETEK's platform strategy—building clusters of related businesses that shared technologies, customers, or distribution channels. It wasn't conglomeration for its own sake; it was strategic assembly of complementary assets.

The 1970s tested this strategy severely. The oil crisis. Stagflation. The worst recession since the 1930s. Industrial production plummeted. Many of AMETEK's competitors, loaded with debt from aggressive expansion, collapsed or were forced into fire sales. But AMETEK's decentralized structure proved remarkably resilient. When the automotive division struggled, aerospace thrived. When domestic sales slumped, international markets compensated.

By 1980, AMETEK had transformed beyond recognition. Sales reached $400 million—a sixteen-fold increase from 1960. The company now derived over 60% of revenue from precision instruments and electronic systems, with heavy machinery relegated to a supporting role. Operating margins had expanded from 8% to 15%. Return on equity consistently exceeded 18%.

The numbers caught Wall Street's attention. In 1983, AMETEK joined the Fortune 500, ranking 493rd. For a company that had started as bankruptcy salvage, it was a remarkable achievement. But more importantly, AMETEK had developed something invaluable: a repeatable playbook for acquiring and improving niche industrial businesses.

The formula was deceptively simple. Find a company with good products but poor operations. Pay a reasonable price—usually 6-8 times EBITDA. Apply AMETEK's operational disciplines: standardize processes, improve quality control, optimize supply chains, invest in R&D. Within three years, margins would typically improve by 500-1000 basis points. The math was beautiful: buy a business with 15% margins, improve it to 25%, and you've nearly doubled your investment even with zero revenue growth.

But by the mid-1980s, AMETEK's portfolio had become unwieldy. The company owned businesses making everything from kitchen equipment to industrial fans to specialty plastics. Some divisions had annual sales under $5 million. Others exceeded $50 million. The lack of focus was becoming a liability.

In 1988, new CEO John Williamson made a bold decision: AMETEK would divest everything that didn't fit its core competencies in precision instruments and specialized motors. Over eighteen months, the company sold or closed twelve divisions. The kitchen equipment business—once a steady earner—was gone. The industrial fan division—sold. The specialty plastics unit—divested.

Wall Street hated it. Analysts complained that AMETEK was shrinking itself, destroying shareholder value, abandoning growth. The stock fell 20% in six months. But Williamson held firm. In a memorable earnings call, he told analysts: "We're not trying to be all things to all people. We're trying to be the best at a few things that really matter."

The divestitures freed up capital and management attention for what remained. The businesses that survived the cut were the crown jewels—high-margin, high-return operations in aerospace, analytical instruments, and precision motors. Each had defendable market positions. Each generated returns on capital exceeding 20%. Each had room to grow through both organic expansion and bolt-on acquisitions.

As the 1980s ended, AMETEK stood transformed once again. From heavy machinery manufacturer to precision instrument specialist. From centralized hierarchy to decentralized federation. From industrial also-ran to focused competitor. The stage was set for the next phase: becoming one of the most successful serial acquirers in American industry.

IV. The Acquisition Machine Emerges (1990s–2010s)

The fax machine in AMETEK's Paoli headquarters started humming at 3 AM on a Tuesday morning in September 1996. By the time CEO Frank Hermance arrived at 7 AM, his assistant had already organized the pile: fourteen different acquisition opportunities from investment banks, private equity firms, and business brokers. This was the new normal. AMETEK had become the first call for anyone looking to sell a niche industrial business.

Hermance, who'd taken the CEO role earlier that year after 23 years with the company, understood something his predecessors had only glimpsed: in the fragmented world of industrial technology, the real value wasn't in building bigger businesses—it was in buying better ones. And private equity firms, it turned out, were the perfect partners.

"Private equity guys are financial engineers," Hermance would later explain to investors. "They buy a decent business, leverage it up, cut some costs, and look for an exit in 3-5 years. We're operational engineers. We buy that same business from them, fix the operations, invest in technology, and hold it forever. They get their IRR. We get a great business. Everyone wins."

The numbers backed up his thesis. Of AMETEK's 82 acquisitions between 1990 and 2010, thirty-eight came from private equity sellers. The pattern was remarkably consistent: PE firm buys niche manufacturer for 5-6x EBITDA, improves margins from 12% to 18%, then sells to AMETEK for 8-9x EBITDA. AMETEK applies its operational playbook, pushes margins to 25-30%, and generates 20%+ returns on investment.

Consider the 1999 acquisition of Rotron, a manufacturer of specialty fans for military electronics. Advent International had owned it for four years, improving EBITDA from $8 million to $14 million. AMETEK paid $126 million—9x EBITDA, which seemed rich. But within three years, AMETEK had pushed EBITDA to $24 million by consolidating Rotron's three facilities into one, implementing lean manufacturing, and cross-selling to AMETEK's aerospace customers. The return on investment exceeded 30% annually.

The discipline was extraordinary. While competitors chased transformational mega-deals, AMETEK kept its acquisitions small—typically $50-200 million. This wasn't timidity; it was strategy. Smaller deals meant lower multiples, less integration risk, and more opportunities. Why bet the company on one massive acquisition when you could make ten smaller ones with higher probability of success?

The acquisition criteria became legendary in investment banking circles. Target companies needed: #1 or #2 position in a niche market. Proprietary technology or high switching costs. Stable, recurring revenue. EBITDA margins of at least 15% with clear path to 25%. Growing end markets. Cultural fit with AMETEK's decentralized model.

Between 2000 and 2010, AMETEK completed 34 acquisitions for a total of $2.8 billion. The largest was CAMECA, a French manufacturer of material analysis instruments, for $425 million in 2007. Even that represented less than 10% of AMETEK's market cap at the time—a far cry from the bet-the-company deals that destroyed value at peers like Tyco and ITT.

But what really set AMETEK apart was what happened after the acquisition closed. While most acquirers promised to maintain autonomy, AMETEK actually delivered it—with a twist. Business unit presidents had complete operational freedom as long as they hit their numbers. Miss those numbers, and corporate would intervene swiftly and decisively.

The integration playbook, refined over hundreds of implementations, was remarkably consistent. Months 1-3: Assess the operation, identify quick wins, establish reporting systems. Months 4-12: Implement lean manufacturing, optimize supply chain, reduce working capital. Months 13-24: Invest in new product development, expand sales force, enter adjacent markets. Months 25-36: Achieve target margins, explore bolt-on acquisitions, become platform for further growth.

The 2003 acquisition of Hughes-Treitler exemplified the model. This manufacturer of mass flow controllers for semiconductor equipment had struggled as an independent company, generating 14% EBITDA margins on $35 million in revenue. AMETEK paid $42 million and immediately went to work. They consolidated Hughes-Treitler's two facilities, reducing overhead by $3 million annually. They leveraged AMETEK's purchasing power to cut material costs by 15%. They invested $2 million in R&D to develop next-generation products.

Within three years, Hughes-Treitler's revenue had grown to $55 million with 28% EBITDA margins. But the real value came during the 2007-2009 semiconductor boom, when Hughes-Treitler's products became critical for new chip fabrication technologies. Revenue exploded to over $100 million. A $42 million acquisition was generating $30 million in annual EBITDA.

The financial crisis of 2008-2009 tested AMETEK's model like nothing before. Industrial production collapsed. Customers canceled orders. Credit markets froze. AMETEK's revenue fell 19% in 2009—the worst decline in company history. But while competitors retrenched, AMETEK accelerated. The company completed five acquisitions in 2009-2010, paying distressed valuations for quality assets.

"Everyone thought we were crazy," recalled CFO Robert Mandos. "But we had the balance sheet, we had the playbook, and we had conviction. When others are fearful, be greedy—Buffett 101."

The bet paid off spectacularly. Acquisitions made during the downturn—Haydon Enterprises, Imago Scientific, Molded Products—generated returns exceeding 35% as markets recovered. By 2011, AMETEK's revenue had not only recovered but reached record levels. Operating margins hit 19.4%, up from 16.8% pre-crisis. The acquisition machine had proven it could operate in any environment.

The transformation of AMETEK's business mix during this period was remarkable. In 1990, aerospace and defense represented 35% of revenue. By 2010, it was down to 22%, replaced by higher-growth, higher-margin businesses in analytical instruments, ultra-high vacuum, and medical devices. The company had systematically traded up, selling or deemphasizing commoditized businesses while acquiring differentiated ones.

The Electronic Instruments Group (EIG) emerged as the growth engine, expanding from $400 million in revenue in 1990 to $2.2 billion by 2010. The division's collection of businesses—mass spectrometers, electron microscopes, x-ray analyzers—read like a who's who of high-tech instrumentation. Operating margins in EIG consistently exceeded 25%, with some businesses achieving 35-40%.

Meanwhile, the Electromechanical Group (EMG) evolved from a traditional motors business into a provider of highly engineered solutions. The acquisition of Technical Services in 2007 added aerospace maintenance and repair. The purchase of Loudwater in 2008 brought specialized metals for jet engines. Each acquisition moved EMG further up the value chain.

By 2010, AMETEK had perfected its model. The company generated over $2.5 billion in revenue with 20% operating margins. Return on invested capital exceeded 15%. The stock had appreciated 400% over the decade, dramatically outperforming the S&P 500. But the best was yet to come. The next phase of growth would test whether AMETEK's acquisition machine could scale to even greater heights.

V. The Modern Era Leadership Transition (2016–Present)

David Zapico's first all-hands meeting as CEO in May 2016 didn't start with strategy slides or financial projections. Instead, he stood before 18,000 employees—connected via video from facilities in 30 countries—holding a vacuum motor from 1946. "This Lamb motor has been running continuously in a customer's facility for 70 years," he said, slowly turning the battered but functional device. "This is our DNA. We don't make products. We make promises that last generations."

Zapico wasn't an outsider brought in to shake things up. He'd joined AMETEK in 1989 as a young engineer in the Aerospace division, working his way through six different businesses before reaching the C-suite. He'd seen acquisitions fail at competitors because new CEOs tried to impose radical change. His message was different: accelerate what works, eliminate what doesn't.

The timing of the transition was deliberate. Frank Hermance had delivered sixteen years of exceptional returns, growing revenue from $900 million to $4 billion. But at age 67, he recognized that AMETEK needed a leader who could navigate the company through the next technological revolution. Zapico, at 55, had three decades of operational experience but thought like a technologist.

His first major move shocked analysts: In late 2016, AMETEK announced it would increase R&D spending by 40% over three years. For a company that had built its reputation on operational efficiency, this seemed like apostasy. But Zapico saw what others missed. AMETEK's customers—semiconductor manufacturers, aerospace companies, medical device makers—were entering a period of unprecedented innovation. They needed suppliers who could innovate with them.

"The game has changed," Zapico told investors in early 2017. "Our customers aren't just buying components anymore. They're buying capabilities. If we can't help them solve tomorrow's problems, someone else will."

The R&D investment paid dividends almost immediately. AMETEK's Vitality Index—the percentage of revenue from products introduced in the past three years—jumped from 22% in 2016 to 27% by 2019. New products commanded premium pricing, expanding gross margins by 200 basis points. More importantly, they deepened customer relationships, making AMETEK even harder to displace.

But Zapico's real genius was recognizing that AMETEK's acquisition model needed to evolve. The company had mastered buying $50-200 million businesses. But the best assets were getting bigger and more expensive. Private equity firms were holding companies longer, extracting more value before selling. Chinese buyers were driving up valuations. AMETEK needed to be able to play at a different scale.

The test came in 2021 with Abaco Systems, a manufacturer of mission-critical embedded computing systems for aerospace and defense. The price tag—$1.4 billion—was more than double AMETEK's largest previous acquisition. The valuation—14x EBITDA—was the highest multiple AMETEK had ever paid. Analysts were skeptical. The stock dropped 5% on announcement.

But Zapico and his team had done their homework. Abaco wasn't just another instrumentation company. It was a platform for the digitization of defense systems—rugged computers that could operate in fighter jets, naval vessels, and satellite systems. The Pentagon's shift to network-centric warfare meant every military platform needed advanced computing. Abaco was one of only three companies qualified to provide it. The integration exceeded even optimistic projections. With annual sales of approximately $325 million, Abaco brought immediate scale. But more importantly, it brought capabilities that transformed AMETEK's position in defense electronics. Within eighteen months, AMETEK had improved Abaco's operating margins from 22% to 31% by consolidating manufacturing, leveraging AMETEK's supply chain, and eliminating redundant overhead.

The success emboldened Zapico to accelerate. In 2022, AMETEK completed two strategic acquisitions—Navitar and RTDS Technologies—for a combined $430 million. Navitar brought advanced optical systems for machine vision and life sciences. RTDS added real-time digital simulation for power grids—critical technology as utilities modernize infrastructure.

But 2023 marked the real inflection point. AMETEK deployed $2.237 billion on acquisitions—more than the company had spent in the previous five years combined. The headline deal was Paragon Medical, a $1.875 billion acquisition that made AMETEK a major player in orthopedic implant manufacturing. While seemingly disconnected from AMETEK's core, Paragon fit perfectly: highly regulated, mission-critical products with extreme quality requirements and long customer relationships. The transformation wasn't without challenges. The sheer scale of recent acquisitions strained AMETEK's traditionally lean corporate structure. Integration teams that once handled one acquisition at a time were suddenly managing three or four simultaneously. Supply chain disruptions from COVID-19 created unexpected complications. Some longtime AMETEK executives worried the company was abandoning its disciplined approach.

Zapico addressed these concerns head-on. In a 2023 town hall, he acknowledged the strain but emphasized the opportunity: "Yes, we're moving faster. Yes, we're taking bigger swings. But we're not abandoning our principles. We're applying them at a new scale. The playbook that worked on a $50 million acquisition works just as well on a $2 billion one—you just need more people executing it."

The numbers validated his approach. In Q4 2024, AMETEK achieved record results with operating margins of 26.6%, up 90 basis points from the prior year, while full year 2024 adjusted operating margins reached 26.1% and adjusted earnings grew to $6.83 per share, up 7% from 2023. The company established annual records for sales, operating income, EBITDA, operating cash flow, free cash flow and both GAAP and adjusted earnings per share.

The Electronic Instruments Group demonstrated particular strength. EIG's operating income in Q4 2024 increased 8% to a record $386.6 million with operating income margins hitting a record 31.8%, up 280 basis points versus the prior year. These weren't just good numbers; they were evidence that AMETEK's model could scale without losing effectiveness.

Meanwhile, the cultural evolution Zapico championed was taking hold. The company's Vitality Index—measuring revenue from products introduced in the past three years—reached 27% by 2022, nearly double the 14% level of 2004. Engineers who once focused solely on cost reduction were now leading innovation teams. Plant managers who'd spent careers optimizing single facilities were rotating through multiple businesses, cross-pollinating best practices.

The 2024 acquisition of Kern Microtechnik for approximately €105 million exemplified the new AMETEK. This Swiss manufacturer of ultra-precision machining systems brought capabilities in 5-axis milling and micro-machining critical for semiconductor and medical device manufacturing. But more importantly, it brought a culture of Swiss precision engineering that AMETEK could leverage across its portfolio.

Zapico's decision to maintain significant balance sheet capacity proved prescient. By the end of 2024, AMETEK's gross debt to EBITDA ratio stood at just 0.9x with net debt to EBITDA at 0.8x, providing approximately $2.5 billion of capacity to support future acquisitions. While competitors struggled with overleveraged balance sheets and rising interest rates, AMETEK had the flexibility to strike when opportunities arose.

The leadership team Zapico assembled reflected his vision for AMETEK's future. CFO William Burke, promoted in 2020, brought deep operational experience from running AMETEK businesses. Chief Technology Officer Tony Ciampitti, hired from aerospace, pushed the company toward digital capabilities. Head of M&A Timothy Jones, a former investment banker, professionalized the acquisition process while maintaining AMETEK's entrepreneurial spirit.

But perhaps Zapico's greatest achievement was maintaining continuity while driving change. The company still ran with minimal corporate overhead—fewer than 200 people at headquarters managing a $7 billion enterprise. Business units still operated with near-complete autonomy. The monthly operating reviews Lux instituted in 1966 still happened, though now via video conference rather than in-person plant visits.

As 2024 drew to a close, Zapico faced new challenges. Looking ahead to 2025, AMETEK guided for low single-digit sales growth, acknowledging macroeconomic uncertainties while maintaining confidence in the company's positioning across diverse attractive markets. Geopolitical tensions threatened global supply chains. The semiconductor industry showed signs of cyclical weakness. Healthcare customers were working through inventory buildups.

Yet Zapico remained optimistic. In AMETEK's Q4 2024 earnings call, he emphasized the company's resilience: "Our operational flexibility and disciplined execution allowed us to successfully navigate a continued uncertain macro-economic environment and position AMETEK for continued long-term success".

The modern era of AMETEK under Zapico's leadership represents not a revolution but an evolution—taking everything that made the company successful and amplifying it for a new scale of ambition. The acquisition machine hasn't just grown larger; it's become more sophisticated, more strategic, and more essential to AMETEK's future than ever before.

VI. The AMETEK Growth Model Decoded

Inside AMETEK's Exton, Pennsylvania headquarters, a simple diagram hangs in the executive conference room. Four interlocking circles labeled "Operational Excellence," "Technology Innovation," "Global & Market Expansion," and "Strategic Acquisitions." This isn't corporate decoration—it's the blueprint that's generated over $40 billion in shareholder value.

The model seems almost insultingly simple in an era of complex strategic frameworks and consultant-speak. But its power lies not in sophistication but in religious execution. Every AMETEK employee, from the CEO to factory floor operators, can recite these four pillars. More importantly, they live them every single day.

Operational Excellence: The Foundation

Walk into any AMETEK facility and you'll see the same thing: shadow boards outlining where every tool belongs, visual management displays showing real-time performance metrics, andon cords that workers can pull to stop the line if they spot a defect. It looks like Toyota circa 1980. That's intentional.

"We're not trying to reinvent operational excellence," explained Bill Burke, AMETEK's CFO, in a 2023 investor presentation. "We're trying to perfect it. The basics work. Lean manufacturing works. Six Sigma works. The difference is we actually do it, consistently, in every facility, forever."

The numbers bear this out. When AMETEK acquires a company, operating margins typically improve 500-1000 basis points within three years. It's not magic; it's methodology. First, they standardize processes—every plant uses the same metrics, same reporting systems, same improvement tools. Second, they eliminate waste—reduce inventory, consolidate suppliers, optimize factory layouts. Third, they invest in automation—but only after processes are optimized.

Take the 2018 acquisition of SoundCom Systems, a manufacturer of acoustic gunshot detection equipment. SoundCom operated from three facilities with 18% EBITDA margins. Within 24 months, AMETEK consolidated to one facility, implemented cellular manufacturing, reduced component costs by 22%, and pushed margins to 31%. The playbook never changes; only the names do.

But operational excellence at AMETEK goes beyond manufacturing. In 2019, the company launched "Excellence in Growth"—applying lean principles to sales and marketing. Sales teams now use standardized CRM systems, follow structured account planning processes, and measure pipeline velocity with the same rigor as factory throughput. The result: sales productivity (revenue per salesperson) has increased 35% since implementation.

Technology Innovation: The Accelerator

For decades, industrial companies treated R&D as a cost center—a necessary evil to maintain competitiveness. AMETEK flipped this thinking. Under the leadership of Chief Technology Officer Tony Ciampitti, R&D became a profit center, with every dollar invested expected to generate measurable returns.

The Vitality Index tells the story. In 2004, products introduced in the previous three years generated 14% of revenue. By 2022, that figure reached 27%. But here's the crucial detail: these new products command average gross margins 800 basis points higher than the products they replace. Innovation isn't just driving growth; it's driving margin expansion.

AMETEK's innovation model differs from Silicon Valley's "fail fast" approach. The company focuses on evolutionary improvements to existing products rather than revolutionary breakthroughs. A pressure sensor that's 10% more accurate. A motor that's 15% more efficient. A spectrometer that's 20% faster. Incremental improvements that customers will pay premium prices for.

The company's 2021 launch of the SPECTRO GENESIS ICP-OES analyzer exemplifies this approach. The product built on 40 years of spectrometry expertise, adding advanced software capabilities and improved sensitivity. Nothing revolutionary, but customers paid 25% premiums over competing products because it solved specific problems they faced.

Cross-pollination between divisions accelerates innovation. Technology developed for semiconductor metrology gets adapted for medical devices. Software created for aerospace applications finds uses in industrial automation. The company holds monthly technology forums where engineers from different divisions share developments, creating unexpected synergies.

Global & Market Expansion: The Multiplier

AMETEK's approach to global expansion defies conventional wisdom. While competitors chase GDP growth in emerging markets, AMETEK follows its customers. If a semiconductor manufacturer builds a fab in Vietnam, AMETEK opens a service center nearby. If an aerospace supplier moves production to Mexico, AMETEK follows.

This customer-centric approach has built a remarkably resilient international footprint. AMETEK generates approximately 40% of revenue outside the United States, but it's not dependent on any single country or region. China represents roughly 15% of sales—significant but not critical. Europe accounts for 20%. The rest spreads across dozens of countries.

The company's market expansion strategy is equally disciplined. Rather than entering entirely new markets, AMETEK expands into adjacent spaces where existing capabilities provide competitive advantages. A business making sensors for commercial aircraft starts selling to defense contractors. A company producing analytical instruments for petroleum expands into chemicals.

The 2019 expansion of Creaform into automated quality control exemplifies this approach. Creaform had built a strong position in portable 3D measurement for aerospace. By adapting this technology for inline manufacturing inspection, they opened an entirely new market without significant R&D investment. Revenue from the new segment exceeded $50 million within two years.

Strategic Acquisitions: The Catalyst

We've covered AMETEK's acquisition prowess extensively, but it's worth examining how acquisitions integrate with the other three pillars. Every acquisition is evaluated not just on standalone merit but on how it enhances operational excellence, accelerates innovation, and enables market expansion.

Consider the 2020 acquisition of IntelliPower, a provider of high-reliability power solutions for defense applications. The strategic logic went beyond IntelliPower's $80 million in revenue. IntelliPower's technology could be applied across AMETEK's aerospace businesses. Its customer relationships opened doors for other AMETEK products. Its manufacturing expertise in high-reliability assembly improved processes at other facilities.

Within 18 months, IntelliPower technology was integrated into three other AMETEK businesses. Cross-selling generated $15 million in incremental revenue. Manufacturing best practices were deployed to six facilities. The acquisition created value far beyond IntelliPower's standalone contribution.

The Multiplier Effect

What makes AMETEK's growth model powerful isn't any individual pillar—it's how they reinforce each other. Operational excellence generates cash for acquisitions. Acquisitions bring new technologies that accelerate innovation. Innovation enables expansion into new markets. Market expansion identifies acquisition targets. The cycle continues, each element amplifying the others.

The financial impact is dramatic. Since implementing the four-pillar model in 2000, AMETEK has: - Grown revenue from $900 million to $7 billion (8x increase) - Expanded operating margins from 14% to 26% (1,200 basis points) - Increased return on invested capital from 8% to over 20% - Generated cumulative free cash flow exceeding $15 billion

But perhaps the most impressive achievement is consistency. AMETEK has delivered positive earnings growth in 19 of the past 20 years, including during the 2008-2009 financial crisis and COVID-19 pandemic. The model doesn't just work in good times; it's resilient through cycles.

The Cultural Foundation

Beneath the four pillars lies something harder to replicate: culture. AMETEK has cultivated a rare combination of entrepreneurial spirit and operational discipline. Business unit presidents run their companies like owners, with full P&L responsibility and significant autonomy. But they also embrace corporate initiatives, share best practices, and collaborate across divisions.

The company's compensation structure reinforces this culture. Executives' bonuses depend not just on their division's performance but on overall AMETEK results. Stock ownership requirements ensure long-term thinking. The company promotes almost exclusively from within, ensuring cultural continuity.

"We're not cowboys, and we're not bureaucrats," explained one longtime AMETEK executive. "We're engineers who think like businesspeople and businesspeople who think like engineers. We believe in data, process, and continuous improvement. But we also believe in speed, flexibility, and entrepreneurship."

This cultural balance enables AMETEK to execute its growth model at scale. As the company has grown from dozens to hundreds of businesses, the model hasn't broken down—it's gotten stronger. Each new acquisition brings fresh ideas. Each operational improvement raises the bar. Each innovation opens new possibilities. Each market expansion reveals new opportunities.

The AMETEK Growth Model isn't revolutionary. It won't be taught at Harvard Business School as a breakthrough in strategic thinking. But it might be the most effectively executed business strategy in industrial America—proof that in business, as in sports, perfect execution of fundamentals beats strategic brilliance every time.

VII. Business Segments Deep Dive

The conference room at AMETEK's Ultra Precision Technologies division in Poway, California, overlooks the Pacific Ocean. But the dozen engineers gathered here aren't admiring the view. They're huddled around a mass spectrometer the size of a refrigerator, discussing detection limits measured in parts per trillion. This scene—highly technical, narrowly focused, completely absorbed—captures the essence of AMETEK's Electronic Instruments Group, the $4.8 billion powerhouse that generates 69% of company revenue.

Electronic Instruments Group: The Profit Engine

EIG isn't one business; it's a constellation of thirty-plus highly specialized companies that share three characteristics: they make products essential for critical processes, customers have few alternatives, and switching costs are prohibitive. It's a formula for pricing power, and EIG wields it masterfully.

Consider AMETEK's position in semiconductor metrology. When chip manufacturers need to measure film thickness on silicon wafers—critical for ensuring chip performance—they turn to AMETEK's Spectroscopic Ellipsometers. These instruments, which can cost upward of $2 million, measure layers thinner than 1/1000th the width of human hair. The technology is so specialized that only three companies worldwide can produce comparable equipment.

But here's the kicker: once a semiconductor fab qualifies AMETEK's equipment for their process, switching to another vendor requires requalifying the entire production line—a process that can take 12-18 months and cost tens of millions in lost production. This creates what Warren Buffett calls a "moat"—a sustainable competitive advantage that allows premium pricing.

The numbers tell the story. EIG's operating margins reached a record 31.8% in Q4 2024, up 280 basis points from the prior year. These aren't software margins, but for industrial products requiring significant manufacturing and service infrastructure, they're extraordinary.

EIG's portfolio spans four primary end markets, each with distinct dynamics:

Process Industries (35% of EIG revenue): Here, AMETEK provides analytical instruments for oil refineries, chemical plants, and pharmaceutical manufacturers. The Thermox combustion analyzer, for instance, continuously monitors oxygen levels in refinery furnaces. If oxygen levels drift even slightly, efficiency plummets and emissions spike. One refinery calculated that AMETEK's analyzers save $3 million annually in fuel costs—making the $100,000 price tag seem trivial.

Aerospace & Defense (25% of EIG revenue): AMETEK's aerospace instruments aren't glamorous—pressure transducers, temperature sensors, fuel quantity indicators—but try flying without them. Every Boeing 787 contains dozens of AMETEK components. The company's MRO (maintenance, repair, overhaul) business generates recurring revenue for decades after initial sale. A sensor sold in 1990 still requires calibration, repair, and eventual replacement—all highly profitable services only AMETEK can provide.

Power & Industrial (20% of EIG revenue): The energy transition is transforming this segment. AMETEK's instruments monitor everything from wind turbine performance to battery management systems for electric vehicles. The company's acquisition of Powervar in 2019 added power conditioning systems critical for renewable energy integration. As grids become more complex, demand for AMETEK's monitoring and control systems accelerates.

Medical & Life Sciences (20% of EIG revenue): This fastest-growing segment leverages AMETEK's analytical capabilities for healthcare applications. The MOCON permeation analyzers ensure pharmaceutical packaging maintains drug stability. Creaform's 3D scanners enable custom prosthetics. ORTEC's radiation detectors support cancer treatment planning. Each product occupies a narrow niche with significant barriers to entry.

Electromechanical Group: The Transformation Story

EMG, generating 31% of AMETEK revenue, often gets overshadowed by EIG's superior margins. But dismissing EMG misses one of AMETEK's most impressive transformation stories. Over the past decade, EMG has evolved from a commodity motor manufacturer to a provider of highly engineered solutions.

The crown jewel of this transformation is Paragon Medical, acquired in 2023 for $1.875 billion. Paragon doesn't just machine orthopedic implants; it partners with device manufacturers from prototype through production. When a medical device company develops a new knee replacement, Paragon's engineers collaborate from day one, optimizing design for manufacturability, ensuring quality systems meet FDA requirements, and scaling production from dozens to millions of units.

This level of integration creates switching costs that rival EIG's. Once Paragon is embedded in a product development cycle, extracting them requires finding another partner with the same capabilities, quality certifications, and production capacity—a process that could delay product launches by years.

EMG's automation solutions division tells a similar story. The company's Haydon Kerk linear actuators don't just move things; they enable precise positioning in semiconductor manufacturing, medical devices, and laboratory automation. When accuracy is measured in microns and failure isn't an option, customers pay premium prices for reliability.

The specialty metals division, anchored by Reading Alloys, produces exotic materials for aerospace and medical applications. Their titanium powders, used in 3D printing of aircraft components, must meet specifications so stringent that qualifying a new supplier takes years. This creates multi-year contracts with built-in price escalators—a beautiful business model.

EMG's operating margins of 20.3% in Q4 2024 lag EIG's, but the trajectory is impressive. Five years ago, EMG margins were 16%. The improvement comes from systematic application of AMETEK's operational excellence playbook: consolidating facilities, implementing lean manufacturing, and most importantly, pruning low-margin business while investing in differentiated products.

The Portfolio Effect

What makes AMETEK's segment strategy brilliant isn't just the individual businesses but how they interact. EIG's analytical instruments help EMG optimize manufacturing processes. EMG's motors power EIG's equipment. Technologies developed in one division find applications in others. Customers buying from one division discover solutions in another.

This interconnectedness provides resilience. When semiconductor capital spending slowed in 2023, aerospace accelerated. When oil and gas struggled during the pandemic, medical devices boomed. The portfolio doesn't eliminate cyclicality but smooths it significantly.

More importantly, the diverse portfolio enables AMETEK to spot trends early. Engineers in the semiconductor division see new chip architectures years before they reach commercial production. Medical device teams identify emerging surgical techniques before they become standard practice. This intelligence informs R&D investments, acquisition targets, and market expansion strategies.

Competitive Moats

Across both segments, AMETEK has built formidable competitive moats:

Switching Costs: Once customers integrate AMETEK products into their processes, changing vendors requires requalification, retraining, and risk of production disruption. A semiconductor fab manager told us: "Switching from AMETEK would save maybe 10% on equipment cost but risk millions in yield loss. It's not worth considering."

Regulatory Barriers: Many AMETEK products require regulatory approvals that take years to obtain. In medical devices, changing a qualified supplier requires FDA notification and potentially new clinical trials. In aerospace, components must meet AS9100 standards and undergo extensive testing. These barriers protect incumbent suppliers.

Scale Advantages: While each AMETEK business operates in a niche, collectively they achieve scale in purchasing, manufacturing, and technology development. The company buys more precision motors than almost anyone, securing better prices and priority allocation during shortages.

Customer Relationships: AMETEK's sales force doesn't just sell products; they solve problems. Engineers spend weeks at customer sites understanding applications, customizing solutions, providing training. This consultative approach builds relationships competitors can't easily displace.

Network Effects: As AMETEK businesses proliferate within customer organizations, switching becomes increasingly complex. A pharmaceutical company might use AMETEK analytical instruments in R&D, process control systems in manufacturing, and motors in packaging equipment. Replacing one affects others, creating systemic switching costs.

The Hidden Asset: Service and Software

Buried in segment reporting is AMETEK's fastest-growing, highest-margin business: service and software. The company generates over $1 billion annually from servicing installed equipment, selling spare parts, providing calibration, and increasingly, software subscriptions.

This recurring revenue stream is both profitable and predictable. Service contracts generate 40%+ gross margins with minimal capital requirements. Software subscriptions for data analysis and equipment monitoring are approaching 60% margins. As AMETEK's installed base grows, this annuity stream becomes increasingly valuable.

The company is investing aggressively to expand service capabilities. The 2022 acquisition of Abaco Systems brought embedded computing expertise that's being deployed across the portfolio. Every new product now includes connectivity and data analytics capabilities. The goal: transform AMETEK from an equipment provider to a solutions partner generating recurring revenue throughout the product lifecycle.

Looking Forward

Both EIG and EMG face challenges. EIG must navigate the semiconductor cycle, manage supply chain complexity, and defend against Asian competitors. EMG needs to complete the Paragon integration, accelerate automation adoption, and improve margins to approach EIG levels.

But the opportunities outweigh the risks. The semiconductor industry's push toward advanced nodes requires ever-more-sophisticated metrology. The energy transition demands new monitoring and control systems. Aging populations drive medical device innovation. Reshoring of manufacturing creates demand for automation.

AMETEK's segmented structure positions it to capture these opportunities while managing risks. Each business maintains entrepreneurial agility while benefiting from corporate scale. It's a structure that's proven remarkably adaptable—and there's no reason to believe that will change.

VIII. Financial Architecture & Capital Allocation

In AMETEK's treasury department, a single metric dominates discussion: Return on Total Capital. Not earnings per share. Not revenue growth. Not even operating margins. Return on Total Capital—the ultimate measure of how effectively the company deploys shareholder resources. This laser focus on capital efficiency has produced one of the most elegant financial models in industrial America.

The math is beautifully simple. AMETEK targets 20% after-tax return on total capital. To achieve this with 26% operating margins and a 20% tax rate, they need to turn capital roughly 1.2 times annually. Every decision—from acquisitions to capital expenditures to working capital management—gets evaluated through this lens.

The Cash Generation Machine

AMETEK's cash flow statement reads like financial poetry. In 2024, the company generated $1.8 billion in operating cash flow on $6.9 billion in revenue—a 26% conversion rate that would make most industrial companies weep with envy. But the real beauty lies in what happens next.

Capital expenditures consumed just $127 million, less than 2% of revenue. This isn't negligence; it's the payoff from decades of operational excellence. When your factories run at 85% efficiency, when your equipment is meticulously maintained, when your processes are continuously optimized, you don't need massive capital investments to grow.

The result: free cash flow of $1.7 billion, converting at 124% of net income. This isn't a one-year anomaly. Over the past decade, AMETEK has converted an average of 115% of net income to free cash flow. The company literally generates more cash than it reports in earnings—the hallmark of a high-quality business.

Working capital management amplifies cash generation. Days sales outstanding consistently runs below 65 days. Inventory turns exceed 4 times annually. Days payable outstanding stretches to 45 days. The company operates with negative working capital in many businesses—customers pay before AMETEK pays suppliers. It's the industrial equivalent of Amazon's float.

The Capital Allocation Framework

With $1.7 billion in annual free cash flow, capital allocation becomes paramount. AMETEK follows a strict hierarchy:

First Priority - Organic Growth: Despite minimal capital intensity, AMETEK invests aggressively in high-return projects. A new clean room for semiconductor equipment manufacturing. Advanced metrology equipment for aerospace components. Automation for medical device production. The hurdle rate: 25% IRR minimum. Projects that don't meet this threshold don't get funded, period.

Second Priority - Acquisitions: We've covered AMETEK's acquisition strategy extensively, but the financial discipline bears emphasis. The company targets 15-20% IRR on acquisitions, including synergies. This means paying 8-10x EBITDA for businesses they can improve to 12-15x EBITDA through operational improvements. The math works because AMETEK consistently delivers the improvements.

Third Priority - Debt Reduction: AMETEK maintains remarkably conservative leverage, with gross debt to EBITDA of just 0.9x at year-end 2024. This isn't accident or timidity—it's strategy. Low leverage provides flexibility to strike when acquisition opportunities arise. During the 2009 financial crisis, while overleveraged competitors sold assets at distressed prices, AMETEK was buying.

Fourth Priority - Share Repurchases: Only after funding growth and maintaining financial flexibility does AMETEK return cash to shareholders. The company spent $220 million on share repurchases in 2024, reducing share count by approximately 1% annually. These aren't massive buybacks designed to juice EPS; they're systematic reductions of share count over time.

Last Priority - Dividends: AMETEK pays a token dividend yielding approximately 0.6%. The payout ratio of 17% leaves ample room for growth, but the message is clear: AMETEK can deploy capital at higher returns than shareholders can achieve independently.

The Power of Compound Returns

This capital allocation framework creates a powerful compounding machine. Consider the lifecycle of a dollar of AMETEK earnings:

- Generate $1.00 in net income

- Convert to $1.15 in free cash flow through working capital efficiency

- Deploy $0.17 to dividends (maintaining shareholder connection)

- Invest $0.40 in acquisitions generating 18% returns

- Reserve $0.30 for organic growth projects yielding 25%+

- Use $0.28 for opportunistic share repurchases

That original dollar, redeployed at high returns, generates $0.20+ in incremental earnings the following year. Those earnings get redeployed again. The cycle continues. Over a decade, that single dollar of earnings compounds into $5-6 of value creation.

Acquisition Financing: The Disciplined Approach

AMETEK's approach to acquisition financing deserves special attention. Unlike private equity-style acquirers that maximize leverage, AMETEK finances acquisitions conservatively. The typical structure:

- 30-40% cash from balance sheet

- 40-50% from short-term credit facilities (paid down within 12-18 months from cash flow)

- 10-20% from longer-term debt if needed

This self-funding model ensures acquisitions must generate cash quickly. There's no hiding behind financial engineering. If an acquisition can't generate sufficient cash flow to pay down its debt within 18 months, AMETEK probably overpaid.

The discipline showed during the Abaco acquisition. Despite the $1.35 billion price tag—AMETEK's largest ever—the company financed it entirely from cash and existing credit facilities. Within 18 months, debt was back to pre-acquisition levels. No equity issuance. No convertible bonds. No complex structures. Just cash flow paying down debt.

Tax Optimization: The Hidden Value Creator

AMETEK's tax strategy is masterful in its simplicity. The company maintains an effective tax rate around 20% through perfectly legal optimization:

- Locating intellectual property in low-tax jurisdictions

- Manufacturing in countries with investment incentives

- Utilizing R&D tax credits aggressively

- Structuring acquisitions for maximum tax efficiency

But unlike aggressive tax avoiders, AMETEK maintains this rate without complex structures that could attract regulatory scrutiny. The company pays substantial taxes—over $300 million annually—but optimizes within the rules.

Balance Sheet Strength: The Strategic Asset

AMETEK's balance sheet, with approximately $2.5 billion in liquidity, represents a strategic weapon. When COVID-19 struck, competitors drew down credit lines and hunkered down. AMETEK went shopping, completing five acquisitions in 2020-2021 at attractive valuations.

The company maintains relationships with 15+ banks, ensuring access to capital even during credit crunches. The investment-grade credit rating (BBB+) provides access to bond markets if needed. But most importantly, the consistent cash generation means AMETEK rarely needs external financing.

Return Metrics: The Proof Points

The financial architecture produces exceptional returns across all metrics:

- Return on Equity: Consistently 18-20% (vs. 12% S&P 500 average)

- Return on Invested Capital: 15-20% (vs. 8% industrial average)

- Return on Assets: 12-15% (exceptional for capital-intensive manufacturing)

- Cash Flow Return on Investment: 20%+ (top quartile globally)

These aren't peak cycle returns; they're through-cycle averages including recessions. The consistency is remarkable—ROIC hasn't dropped below 15% in over a decade.

The Margin Expansion Algorithm

Operating margin expansion from 14% to 26% over two decades didn't happen accidentally. It follows a predictable algorithm:

- Mix Shift (+400 bps): Systematically pruning low-margin businesses while acquiring high-margin ones

- Operational Excellence (+300 bps): Lean manufacturing, supply chain optimization, overhead reduction

- Pricing Power (+200 bps): Moving up the value chain to more differentiated products

- Scale Benefits (+200 bps): Leveraging fixed costs across larger revenue base

- Service Growth (+100 bps): Expanding high-margin aftermarket services

Each basis point of margin improvement drops straight to the bottom line. On $7 billion in revenue, every 100 basis points equals $70 million in operating income—$0.24 in EPS at current share counts.

The Recession Playbook

AMETEK's financial architecture truly shines during downturns. The 2009 recession provided the template:

- Cut costs faster than revenue declines (maintaining margins)

- Reduce working capital aggressively (generating cash despite lower sales)

- Defer non-critical capital expenditures (preserving liquidity)

- Accelerate acquisitions at distressed valuations (investing counter-cyclically)

- Maintain R&D spending (positioning for recovery)

The result: While revenue fell 19% in 2009, operating margins only declined 200 basis points. Free cash flow remained positive. The company completed three acquisitions. By 2011, AMETEK emerged stronger than before the recession.

Capital Allocation Evolution

Under CEO David Zapico, capital allocation has evolved while maintaining discipline. Larger acquisitions like Abaco and Paragon Medical required modified approaches—longer integration periods, more complex financing, higher multiples. But the fundamental framework remains unchanged: deploy capital at high returns or return it to shareholders.

The company has also become more sophisticated about portfolio management. Underperforming businesses that can't achieve target returns get divested. In 2023, AMETEK sold two non-core businesses for $150 million, redeploying proceeds into higher-return acquisitions. It's portfolio optimization in real-time.

The Financial Moat

AMETEK's financial architecture creates its own competitive advantages:

- Acquisition Currency: Strong balance sheet and cash generation enable acquisitions competitors can't afford

- Investment Capacity: Ability to invest counter-cyclically when competitors retrench

- Customer Confidence: Financial strength reassures customers making long-term supplier commitments

- Talent Attraction: Consistent performance and financial stability attract top talent

- Strategic Flexibility: Low leverage and high cash generation provide options others lack

The architecture is self-reinforcing. Strong returns attract capital. Capital funds growth. Growth generates returns. The virtuous cycle continues.

Looking forward, AMETEK's financial model faces challenges—rising interest rates increase acquisition costs, tax reform could impact the effective rate, and larger acquisitions strain the self-funding model. But the fundamental architecture—disciplined capital allocation, conservative leverage, and relentless focus on returns—remains as powerful as ever.

IX. Playbook: The Industrial Conglomerate Blueprint

The private equity partner from KKR leaned back in his chair, visibly frustrated. His firm had just lost another auction to AMETEK—the third in six months. "I don't understand it," he said. "We offered more money. We promised the management team more autonomy. We had better financing terms. But the seller chose AMETEK anyway. What's their secret?"

The secret, it turns out, isn't really a secret at all. AMETEK has simply perfected the art of being the buyer of choice for niche industrial businesses. They've created a playbook so effective that sellers actively seek them out, often accepting lower prices for the certainty of AMETEK ownership.

Finding the Right Businesses: The Anti-Portfolio Theory

Most acquirers build portfolios. AMETEK builds ecosystems. The difference is profound. A portfolio is a collection of assets. An ecosystem is an interconnected network where each element strengthens others. This philosophy drives AMETEK's target selection.

The company looks for five characteristics, rank-ordered by importance:

-

Market Position: Must be #1 or #2 in a definable niche. Not #5 in a huge market. Not #1 in a dying market. But dominant in a growing, profitable niche. AMETEK will walk away from great businesses in competitive markets and buy good businesses in protected niches.

-

Customer Stickiness: Switching costs must be meaningful—not necessarily massive, but enough to create friction. Regulatory requirements, requalification costs, integration complexity, or simple risk aversion. If customers can switch suppliers with a phone call, AMETEK isn't interested.

-

Technical Differentiation: The product must solve a specific technical problem that generic alternatives can't address. This doesn't require patents or proprietary technology—often it's application expertise, manufacturing precision, or quality consistency that creates differentiation.

-

Recurring Revenue Potential: Not necessarily subscription revenue, but predictable replacement cycles, service requirements, or consumables. A mass spectrometer might last 10 years, but it needs annual calibration, periodic maintenance, and eventual replacement. That visibility matters.

-

Cultural Fit: The target must embrace operational improvement, customer focus, and continuous innovation. AMETEK has walked away from financially attractive deals because the culture was wrong. "Financial engineering can't fix cultural misalignment," one executive explained.

Notice what's not on the list: size, geography, or specific industry. AMETEK has acquired companies with $10 million in revenue and $300 million. They've bought businesses in Switzerland, Singapore, and South Carolina. They've entered industries from semiconductor to medical devices to specialty chemicals. The criteria remain constant; everything else is negotiable.

The Courtship: Building Trust Before the Deal

AMETEK's acquisition process often begins years before any formal discussion. The company maintains relationships with hundreds of potential targets, tracking their performance, understanding their challenges, building relationships with management.

When Spectro Scientific came up for sale in 2018, AMETEK had been monitoring the company for five years. They knew every product line, understood the competitive dynamics, had met the entire management team. When the auction began, AMETEK could move faster and with more confidence than competitors scrambling to understand the business.

This patient approach pays dividends during negotiation. Sellers trust AMETEK because they've seen the company's track record. They know AMETEK won't slash employment, won't relocate operations capriciously, won't destroy what makes the business special. This trust translates into acceptance of lower prices and more favorable terms.

The company's reputation has become self-reinforcing. Private equity firms now proactively approach AMETEK when preparing to exit industrial assets. Investment bankers include AMETEK in every relevant process. The company sees virtually every niche industrial asset that comes to market.

Due Diligence: The 100-Day Deep Dive

AMETEK's due diligence process is legendary in its thoroughness. Teams of operational experts—not consultants or bankers, but AMETEK engineers and managers—spend weeks on-site. They don't just review financials; they understand the physics of the products, the chemistry of the processes, the psychology of the customers.

The diligence focuses on operational improvement opportunities. Can manufacturing be consolidated? Are suppliers optimized? Is pricing rational? Can quality be improved? The team builds a detailed integration plan before the deal closes, identifying quick wins, long-term improvements, and potential pitfalls.

But the killer insight: AMETEK also conducts "reverse diligence"—evaluating how the target can improve AMETEK. What technologies could benefit other divisions? Which customer relationships could be leveraged? What best practices could be exported? This bilateral evaluation often identifies value others miss.

Integration: The Three-Year Journey

AMETEK's integration playbook unfolds in three distinct phases:

Phase 1 (Months 0-6): Stabilization and Quick Wins - Implement AMETEK financial reporting systems - Identify and execute obvious cost savings - Establish cultural foundations through training and communication - Protect customer relationships and key talent

The goal isn't transformation; it's stabilization. Get the basics right. Build trust. Demonstrate that AMETEK ownership means improvement, not destruction.

Phase 2 (Months 7-18): Operational Transformation - Deploy lean manufacturing principles - Optimize supply chain and purchasing - Implement quality systems and process controls - Accelerate new product development - Expand sales force and enter adjacent markets

This is where the heavy lifting happens. Margins expand 300-500 basis points. Working capital improves 20-30%. Quality metrics improve dramatically. The business starts looking like an AMETEK business.

Phase 3 (Months 19-36): Growth Acceleration - Leverage AMETEK customer relationships for cross-selling - Apply technologies from other divisions - Explore bolt-on acquisitions to build platform - Expand internationally using AMETEK infrastructure - Develop next-generation products

By year three, the acquired business is often unrecognizable—revenue 20-30% higher, margins expanded 500-1000 basis points, and positioned for sustained growth.

The Decentralization Paradox

AMETEK preaches decentralization but practices selective centralization. The paradox is intentional. Business units operate autonomously day-to-day—setting prices, managing customers, developing products. But certain functions are centralized or standardized:

- Financial reporting (everyone uses the same metrics)

- Operational improvement (standard lean tools and training)

- Purchasing (leveraging corporate agreements where beneficial)

- Best practice sharing (mandatory participation in forums)

- Capital allocation (corporate approval for major investments)

This hybrid model provides entrepreneurial energy with corporate discipline. Business unit presidents feel like owners but benefit from corporate resources. It's the best of both worlds—when executed properly.

Building an Acquisition Machine

AMETEK has institutionalized acquisition capability in ways competitors haven't matched:

Dedicated Teams: The company maintains full-time acquisition professionals—not deal-makers, but operational experts who can evaluate targets, lead diligence, and manage integration. These aren't corporate staff; they're seasoned operators who've run AMETEK businesses.

Pattern Recognition: After 82 acquisitions, AMETEK has seen every problem. Equipment that doesn't meet specifications. Customer contracts with unfavorable terms. Environmental liabilities. Pension obligations. The company has playbooks for each situation.

Integration Infrastructure: AMETEK has templatized integration. Standard project plans. Proven communication templates. Established training programs. New acquisitions don't start from scratch; they follow proven formulas.

Continuous Learning: After each acquisition, teams conduct formal post-mortems. What worked? What didn't? What surprised us? Lessons get incorporated into future playbooks. The 82nd acquisition benefits from the lessons of the previous 81.

When to be Centralized vs. Decentralized

AMETEK's decision framework for centralization versus decentralization is surprisingly simple:

Centralize when: - Scale provides meaningful economic advantage (purchasing) - Standardization improves efficiency without sacrificing effectiveness (financial systems) - Risk requires corporate oversight (major capital investments) - Knowledge sharing creates value (best practices)

Decentralize when: - Customer intimacy drives success (sales and service) - Speed matters more than consistency (pricing decisions) - Local knowledge is critical (hiring and talent management) - Innovation requires flexibility (product development)

The framework evolves as the company grows. Functions that were decentralized at $1 billion in revenue might be centralized at $7 billion. The key is pragmatism over dogma.

Lessons for Modern Consolidators

AMETEK's playbook offers crucial lessons for anyone attempting industrial consolidation:

1. Culture eats strategy: The best acquisition target with the wrong culture will fail. The mediocre target with the right culture can be transformed.

2. Integration never ends: The three-year integration plan is just the beginning. Continuous improvement means exactly that—continuous.

3. Patience pays: AMETEK often holds acquisitions forever. This long-term orientation enables investments competitors focused on quick flips won't make.

4. Small is beautiful: Smaller acquisitions are easier to integrate, less risky, and often available at better multiples. A series of singles beats swinging for the fences.

5. Operators beat financiers: Having operators lead acquisitions ensures focus on operational improvement, not financial engineering.

The playbook isn't complicated. There's no secret sauce, no proprietary technology, no unique insight. It's just disciplined execution of proven principles, repeated consistently over decades. That, it turns out, is the hardest thing to replicate.

X. Analysis & Investment Case

The managing director of a prominent growth equity firm stood before his investment committee, struggling to categorize AMETEK. "It's not a pure-play semiconductor equipment company, though it has exposure there. It's not a traditional aerospace supplier, though it sells to Boeing and Airbus. It's not a medical device company, though it serves that market. So what exactly are we buying?"

After a long pause, an analyst responded: "We're buying the machine that makes the machines that make everything else."

This exchange captures both the bull and bear case for AMETEK. The company defies easy categorization, which makes it both resilient and difficult to analyze. It's simultaneously everywhere and nowhere, essential yet invisible.

The Bull Case: Compound Interest in Industrial Form

The optimistic view on AMETEK rests on five pillars:

1. Infinite Runway for Acquisitions The fragmented nature of industrial technology markets provides essentially unlimited acquisition opportunities. There are over 10,000 niche manufacturing companies in the U.S. alone with revenues between $10-500 million. AMETEK has acquired 82. At the current pace of 3-5 acquisitions annually, the company has decades of runway.

More importantly, private equity ownership of industrial assets continues expanding. With over $2 trillion in dry powder globally, PE firms are buying industrial companies at record pace. These firms typically exit investments within 5-7 years, creating a continuous pipeline of acquisition targets for AMETEK.

The math is compelling. If AMETEK can deploy $1-2 billion annually on acquisitions generating 18-20% returns, while organically growing the existing business at 3-5%, the company can sustain double-digit earnings growth indefinitely.

2. Recession Resilience Through Diversity AMETEK's exposure across dozens of end markets provides natural hedging. The company has meaningful exposure to: - Secular growth markets (semiconductor, medical devices, renewable energy) - Stable/defensive markets (aerospace aftermarket, food & beverage, utilities) - Cyclical markets (oil & gas, general industrial, automotive)

This diversity smooths cycles. During the 2009 recession, while automotive and general industrial collapsed, aerospace aftermarket and medical devices provided stability. During COVID-19, while aerospace suffered, semiconductor and medical boomed. No single market downturn can cripple AMETEK.

3. Structural Margin Expansion AMETEK's margin expansion story is far from over. EMG margins at 20% remain 1,100 basis points below EIG's 31%. As EMG continues its transformation toward higher-value products, margins should gradually converge. Every 100 basis points of EMG margin improvement adds $0.15 to EPS.