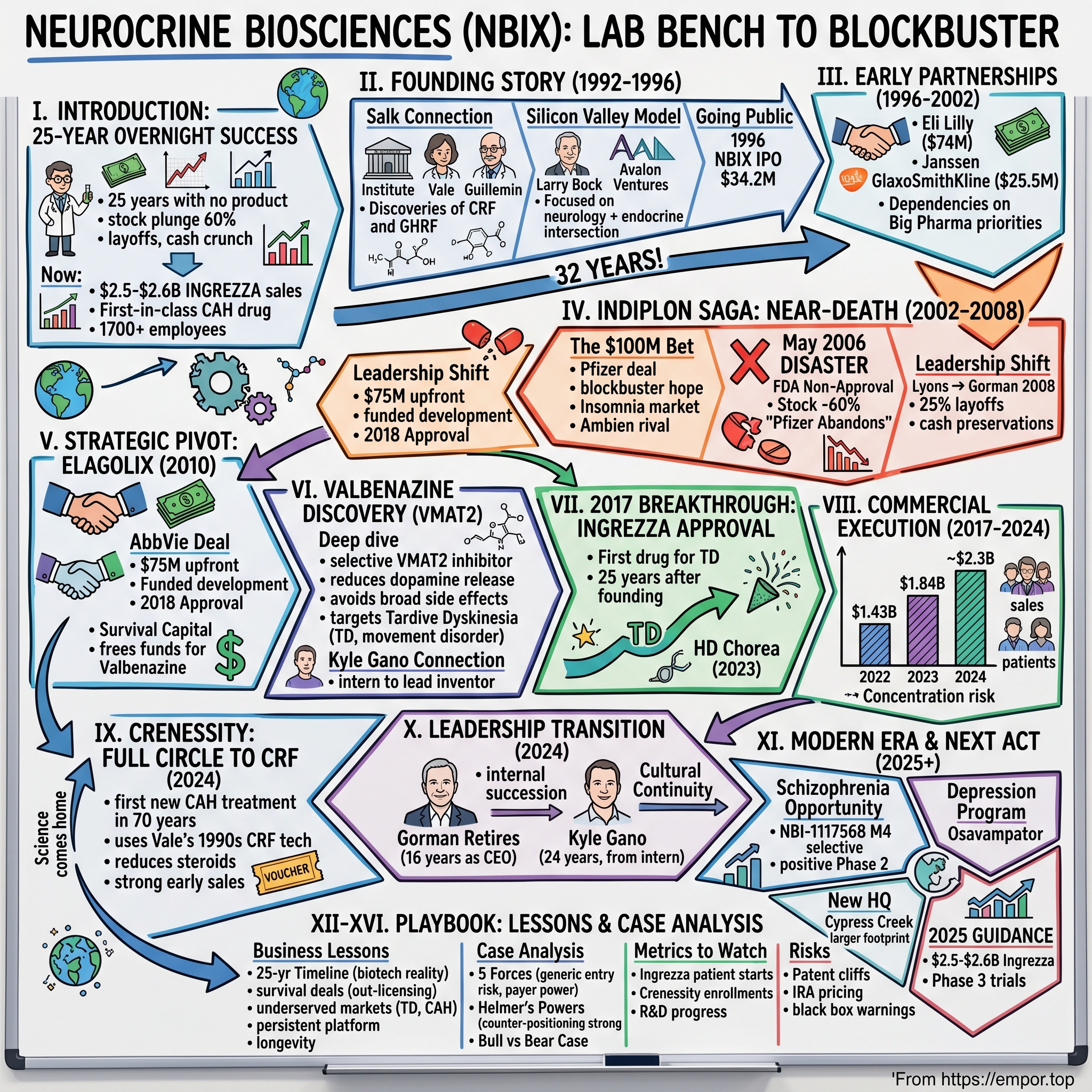

Neurocrine Biosciences: From Lab Bench to Blockbuster

I. Introduction: The 25-Year Overnight Success

The biotech industry loves its comeback stories, but few rival the arc of Neurocrine Biosciences. This is a company that existed for 25 years without a commercial product, survived multiple near-death experiences, watched its stock plunge 60% in a single day, laid off a quarter of its workforce, and came within sight of running out of cash. And yet, by late 2025, it stands as one of the most successful neuroscience companies in America—with 2025 INGREZZA net product sales guidance of $2.5 to $2.6 billion, plus a newly launched first-in-class treatment for congenital adrenal hyperplasia.

From two people to a company of more than 1,700, Neurocrine's journey is a masterclass in what biotech really means: patient capital, patient science, and—most crucially—patient patients who wait decades for treatments that never existed before.

The central question investors must grapple with is this: Is Neurocrine a one-drug wonder that got extraordinarily lucky with Ingrezza, or is it a durable platform company built to generate therapies for generations? With CRENESSITY net product sales through the first nine months of 2025 at $166 million and 1,617 total new patient enrollment forms, the answer is beginning to crystallize. But understanding where this company is going requires understanding the extraordinary path it took to get here.

This story touches on nearly every theme that matters in modern biopharmaceuticals: the commercialization of academic science, the fragile economics of drug development, the role of strategic partnerships, the importance of underserved patient populations, and the remarkable patience required to turn molecular insights into approved medicines.

II. The Founding Story: From Nobel Science to Startup (1992-1996)

The Salk Connection

In the hills of La Jolla, California, overlooking the Pacific Ocean, sits one of the world's most architecturally striking research institutions. The Salk Institute for Biological Studies, founded by polio vaccine pioneer Jonas Salk, has produced some of the most important discoveries in modern biology. It was here that Wylie Vale joined in 1970 and collaborated with his advisor and mentor Roger Guillemin, contributing to the discovery, isolation and identification of thyrotropin releasing hormone and gonadotropin-releasing hormone in the 1970s—work that led to the Nobel Prize for Guillemin.

But Vale wasn't done. At the Salk Institute, Vale led efforts in identifying the group of hormones involved in human growth, reproduction and temperature. His group discovered, isolated and identified corticotropin-releasing hormone (CRF/CRH) in 1981 and growth hormone releasing factor (GHRF) in 1982.

"He cracked one of the most challenging problems of our era: He discovered the brain hormone that serves as the on-off switch to the body's stress response, sometimes called the fight-or-flight response," said Ronald M. Evans, a professor and hormone expert at the Salk Institute. "This has been the subject of speculation and investigation for more than a hundred years," he added, noting that Dr. Vale worked on it for about 15 years.

This discovery—CRF—would become the intellectual foundation for Neurocrine Biosciences. Neurocrine was founded in 1992 by Wylie Vale, Ph.D., of the Salk Institute for Biological Studies, where he contributed to Nobel Prize–winning work in endocrinology, and award-winning Stanford University neurologist Lawrence Steinman, Ph.D.

The Silicon Valley Model Applied to Biotech

Neurocrine Biosciences was founded in 1992 in San Diego, California. The company's establishment was supported by initial seed investment from biotech entrepreneur Larry Bock, who also served as its first chief executive officer.

Larry Bock was a serial biotech entrepreneur who understood that academic science needed commercial infrastructure to become medicine. The company was backed and organized by Larry Bock of Avalon Ventures among others.

The name itself—a portmanteau of "neurological" and "endocrine"—signaled the company's unique thesis. The company was founded in 1992 to treat neurological and endocrine disorders. The company's name is a portmanteau of neurological and endocrine. This wasn't going to be a pure neurology play or a pure endocrinology company; Neurocrine believed the intersection of these fields held untapped therapeutic potential.

The company's foundational work began in neuroendocrine disorders with co-founder Dr. Vale's discovery and study of corticotropin-releasing factor (CRF), an important stress hormone that regulates the release of adrenocorticotropic hormone (ACTH) from the pituitary gland. This work led to the understanding of key biological pathways involved in congenital adrenal hyperplasia (CAH), a rare, genetic, life-long and life-threatening disorder caused by an enzyme deficiency.

Here's the remarkable thing: the science that Vale developed in the 1980s and brought into Neurocrine in 1992 would not produce an approved drug until December 2024—one of the compounds was crinecerfont, an investigational CRF1 receptor antagonist that was approved by the FDA in 2024 and brought innovation to a patient community that has not seen advancements in care in more than 70 years. Thirty-two years from founding to approval. That timeline is almost unimaginable outside of biopharmaceuticals.

Going Public

The company underwent an IPO in May 1996, listing on the NASDAQ exchange under the symbol NBIX and raising $34.2 million. For a company with no products and no revenue, this was a remarkable vote of confidence in the potential of CRF science to become medicine.

The real question was whether the company could survive long enough to see that science mature.

III. Early Partnerships & The Biotech Business Model (1996-2002)

Learning to Dance with Giants

The biotechnology business model of the 1990s and early 2000s depended heavily on partnerships with large pharmaceutical companies. Small biotech firms had the science and innovation; big pharma had the clinical development expertise, regulatory experience, manufacturing capacity, and sales forces needed to bring drugs to market.

Neurocrine quickly learned this dance. In October 1996, Eli Lilly and Company agreed to pay Neurocrine $74 million over five years to develop drugs for obesity and Alzheimer's disease based on its research of CRF-binding protein-ligand inhibitors.

That $74 million deal was transformative for a company that had just raised $34 million in its IPO. It provided non-dilutive capital to pursue research while validating the scientific thesis that CRF-related compounds could become medicines.

Key partnerships shaped this formative period, beginning with a 1995 collaboration with Janssen Pharmaceutica to identify non-peptide CRF1 receptor antagonists for psychiatric indications, which provided upfront payments and milestones.

In July 2001, Neurocrine and GlaxoSmithKline entered into a worldwide research, development and commercialization agreement, including a collaborative research program for up to five years to identify and develop CRF-R antagonist compounds. The collaboration also included worldwide development and commercialization of NBI-34041 as well as potential backup candidates resulting from the research program. Neurocrine received upfront fees and early milestone payments totaling $25.5 million.

The Hidden Risk of Partnership Dependency

These partnerships allowed Neurocrine to build scientific capabilities and stay alive, but they came with strings attached. When you out-license your science to big pharma, you become dependent on their priorities. If they decide to kill a program—for strategic reasons having nothing to do with the science—you lose.

This would become painfully clear with what happened next.

IV. The Indiplon Saga: A Near-Death Experience (2002-2008)

The $100 Million Bet

In December 2002, Neurocrine reached an agreement with Pfizer for the rights to its experimental insomnia drug, indiplon. The deal paid Neurocrine $100 million initially with a possible $300 million more if the drug met regulatory and sales goals.

Indiplon represented a major strategic shift. Here was a drug that could potentially be a blockbuster—equity analysts had been predicting that Indiplon could be a $1 billion seller. Earlier that year, Standard & Poor's credit-rating unit put Indiplon on its Top Ten list of drugs that should achieve $1 billion or more in sales.

The insomnia market was huge. Sanofi-Aventis's Ambien was printing money. And Neurocrine, with Pfizer's marketing muscle behind it, seemed poised to capture a significant share of this multi-billion dollar market.

The May 2006 Disaster

What happened next nearly destroyed the company.

In May 2006, the FDA issued a non-approvable letter for a modified-release 15 mg formulation of indiplon and an approvable letter with stipulations for 5 mg and 10 mg immediate-release formulations. As a result, Pfizer terminated its agreement with Neurocrine.

Neurocrine's stock price dropped 60% on the news.

The market reaction was brutal but rational. Indiplon XR was seen by many industry observers as the only way for the firm to compete in the $3.0 billion a year US sleeping pill market. The extended-release formulation was the differentiated product; the immediate-release versions would compete head-on with generics.

"It's a local tragedy," said analyst Bud Leedom. "It was a very well regarded biotech. It just shows how incredibly risky biotechs are without a product approved."

Abandoned by Pfizer

Neurocrine announced that Neurocrine and Pfizer had agreed to terminate the collaboration agreement to develop and co-promote indiplon. As a result, Neurocrine would reacquire all worldwide rights for indiplon capsules and tablets and would independently develop indiplon for approval and commercialization.

On the day of the news, June 22, shares in San Diego-based Neurocrine plunged 29% to close at $9.85, after hitting a 52-week low of $8.61.

Neurocrine tried to salvage indiplon independently. Following a resubmission of the 5 mg and 10 mg formulations in December 2007, Neurocrine's new drug application was deemed 'approvable' but the FDA requested additional studies. The company discontinued development of the drug in the United States.

In 2007, Neurocrine partnered with Dainippon Sumitomo Pharma to develop and commercialize indiplon in Japan. The deal paid Neurocrine $20 million up front with the ability to receive milestone payments and royalties based on the commercialization of indiplon in Japan.

But the damage was done. Indiplon was dead in the US market—the only market that really mattered.

Leadership Transition

Kevin Gorman replaced Gary Lyons as CEO of the company in January 2008. Lyons was CEO and president of the company since its founding and maintained a role on the company's board of directors.

Dr. Gorman founded Neurocrine in 1992 and held numerous positions across the Company, including Chief Operating Officer, Chief Business Officer, and Senior Vice President of Business Development, before being appointed CEO in 2008. Under Dr. Gorman's three decades of leadership, Neurocrine has emerged as a fully integrated biopharmaceutical enterprise with a broad, mature pipeline, strong financial position, and highly successful commercial product, INGREZZA.

The transition from Lyons to Gorman wasn't just a personnel change—it was a philosophical shift. Gorman had been with the company since its founding, serving at Avalon Medical Partners from 1990 until 1993, where he was responsible for the early-stage founding of Neurocrine and several other biotechnology companies such as Onyx Pharmaceuticals, Metra Biosystems, IDUN and ARIAD Pharmaceuticals.

He knew the company inside and out. And he knew that survival required radical action.

Funding struggles and clinical disappointments culminated in multiple workforce reductions, including a 2010 restructuring that cut approximately 25% of staff to about 90 employees, preserving cash reserves amid a narrowing pipeline and reliance on partnership revenues.

At one point, Neurocrine was left with just 67 people and a building for sale.

V. Strategic Pivot: The AbbVie Deal & Elagolix (2010)

The Decision to Out-License

By 2010, Neurocrine faced an existential choice. The company had developed elagolix, a promising GnRH antagonist for endometriosis, through Phase 2 studies. It could try to develop and commercialize the drug itself—but that would require resources it didn't have. Or it could out-license the asset to a larger partner, trading potential future upside for survival capital.

After discovering and developing elagolix through Phase 2 studies in endometriosis, Neurocrine out-licensed the global rights to elagolix to AbbVie in 2010. AbbVie is responsible for all development and commercialization costs of elagolix.

The deal structure was substantial: Neurocrine granted AbbVie the worldwide rights to develop and commercialize elagolix, an oral gonadotropin-releasing hormone (GnRH) antagonist to treat endometriosis and uterine fibroids. The deal paid Neurocrine $75 million up front.

Under the terms, Neurocrine received an upfront payment of $75 million from AbbVie, which also committed to funding all development costs, with Neurocrine eligible for up to $500 million in development, regulatory, and commercial milestones plus royalties.

Strategic Rationale

"We are pleased to have one of the world's most admired companies as our partner in developing our entire GnRH portfolio for both women's and men's health indications," said Kevin Gorman, president and chief executive officer, Neurocrine Biosciences. "Abbott shares our long-term vision for elagolix, and, together, we look forward to bringing this important new treatment option to endometriosis and uterine fibroid sufferers."

What Gorman didn't say publicly, but what was obvious from the company's financial position, was that this deal kept Neurocrine alive. The $75 million upfront payment, combined with the removal of development costs, freed up capital and resources to focus on what would become the company's breakthrough: valbenazine.

The AbbVie deal also validated Neurocrine's science. Elagolix 150 mg and 200 mg tablets were approved by the US FDA on 23 July 2018 for the management of moderate to severe pain associated with endometriosis. Elagolix is the first oral treatment for moderate to severe endometriosis-associated pain to receive FDA approval in over a decade.

Neurocrine would collect royalties on sales of a drug it discovered and developed through Phase 2—without having to spend the hundreds of millions required to complete Phase 3 trials and commercialization.

VI. The Valbenazine Discovery: Science Behind the Breakthrough

Understanding VMAT2

While the world was focused on Neurocrine's struggles with indiplon and its strategic out-licensing of elagolix, a small team of scientists at the company was working on something different: a selective VMAT2 inhibitor.

VMAT2—vesicular monoamine transporter 2—is a protein that packages neurotransmitters like dopamine into vesicles for storage and release. Valbenazine is thought to function as a highly selective inhibitor of the VMAT2 vesicular monoamine transporter resulting in decreased availability of dopamine in the presynaptic cleft. This leads to decreased dopaminergic activation of the striatal motor pathway. The FDA approved Valbenazine in 2017 to treat tardive dyskinesia in adults.

Valbenazine is known to cause reversible reduction of dopamine release by selectively inhibiting pre-synaptic human vesicular monoamine transporter type 2 (VMAT2). In vitro, valbenazine shows great selectivity for VMAT2 and little to no affinity for VMAT1 or other monoamine receptors.

The selectivity was crucial. Earlier VMAT inhibitors like reserpine were too broad, causing serious psychiatric side effects including depression. Before the currently used antipsychotic medications came into play, reserpine was an irreversible VMAT inhibitor that depletes the brain of dopamine. Patients undergoing treatment with reserpine no longer experience TD, but they also don't experience drive, motivation, or a sense of reward. Instead, they experience depression, parkinsonism, and akathisia. As a result of this, VMAT inhibitors were put aside for decades.

Targeting Tardive Dyskinesia

Tardive dyskinesia (TD) is a devastating movement disorder caused by long-term use of antipsychotic medications. TD occurs in 32.4 percent of patients who receive typical antipsychotics and in 13.1 percent of patients who receive atypical antipsychotics.

It's the first drug approved for the movement disorder, which can be caused by psychiatric medicines. Tardive dyskinesia is an especially feared complication, because it can persist even after stopping the medications. And while the U.S. patient population of about 500,000 is relatively small, the lack of therapies made the launch of Ingrezza a big deal.

There are some 800,000 tardive dyskinesia patients in the U.S., but only around 10% currently take Ingrezza or another medicine inhibiting the same protein, vesicular monoamine transporter 2 (VMAT2), to treat the disorder.

Here was a market with real unmet need. Patients were suffering from a condition with no FDA-approved treatments for over 60 years. Psychiatrists and neurologists had been using off-label treatments with limited efficacy and problematic side effects.

The Kyle Gano Connection

One of the remarkable aspects of the valbenazine story is the role played by Kyle Gano—who in 2024 would become CEO. Gano has led numerous high-impact operational and business priorities. These include having been the lead inventor on the patent to the valbenazine molecule, having served as Team Lead for both the elagolix development program and VMAT2 Franchise Team.

CEO Kyle Gano began his career at Neurocrine as an intern in 2001. From intern to lead inventor to CEO—a 24-year journey within a single company. That kind of institutional continuity is rare in biotech.

VII. The 2017 Breakthrough: INGREZZA Approval

Twenty-Five Years in the Making

On April 11, 2017, Neurocrine achieved what had seemed impossible during the dark days of 2008-2010: the U.S. Food and Drug Administration (FDA) approved INGREZZA (valbenazine) capsules for the treatment of adults with tardive dyskinesia (TD).

In April 2017, the FDA approved valbenazine for the treatment of TD. At the time of approval, it was the first and only drug approved for adults with TD.

"[TD] can be disabling and can further stigmatize patients with mental illness," Mitchell Mathis, MD, director of the Division of Psychiatry Products in the FDA's Center for Drug Evaluation and Research, said in the release. "Approving the first drug for the treatment of [TD] is an important advance for patients suffering with this condition."

"The FDA's approval of INGREZZA represents the culmination of over ten years of dedicated effort from the Neurocrine research and development teams."

Clinical Evidence

The approval was based on robust clinical data. The approval of INGREZZA was based on data from the Kinect 3 study, a Phase III, randomized, double-blind, placebo-controlled, parallel-group, fixed-dose study comparing once-daily INGREZZA 80mg and 40mg to placebo over six weeks in patients with underlying schizophrenia, schizoaffective disorder or mood disorder. INGREZZA met the primary endpoint in this study with a mean change from baseline to week six in the AIMS dyskinesia total score of -3.2 for the 80mg once-daily group as compared to -0.1 in the placebo group (p<0.0001).

INGREZZA has been studied in over 1,000 individuals and more than 20 clinical trials.

First-Mover Advantage

Being first to market in an underserved indication with no approved treatments for 60+ years created a powerful commercial position. Psychiatrists and neurologists had been watching patients suffer from TD for decades with nothing to offer except off-label treatments of uncertain efficacy.

"Until now, one of the few options for physicians when managing TD was to stop, change, or lower the dose of antipsychotic medication, potentially jeopardizing patients' psychiatric stability," Christoph U. Correll, MD, from Hofstra Northwell School of Medicine said in a release. However, the clinical trials showed that the drug reduced involuntary movements "without compromising underlying psychiatric care."

For Neurocrine, the approval represented something even more profound: 25 years from founding to first FDA approval. The company had finally proven that it could bring a drug to market.

VIII. Commercial Execution & Growth (2017-2024)

Building a Commercial Organization from Scratch

Neurocrine had spent its entire existence as a research and development company. In 2017, it had to become something it had never been: a commercial pharmaceutical company.

This required building a sales force, establishing relationships with payers, creating patient access programs, and executing a launch strategy. Ingrezza revenue reached $168 million in the first six months of 2018. (Revenue was less than $10 million for the same period a year ago, when Ingrezza had just started selling).

The growth trajectory was remarkable. Each year brought new sales records: - Last year (2022), the med brought home $1.43 billion in sales for Neurocrine. - In 2023, the drug brought in $1.84 billion, accounting for almost all of the biotech's overall revenue of nearly $1.89 billion. - INGREZZA fourth quarter and fiscal 2024 net product sales were $615 million and $2.3 billion, respectively.

Expanding the Label: Huntington's Disease

In August 2023, Neurocrine achieved a significant label expansion. The U.S. Food and Drug Administration approved INGREZZA capsules for the treatment of adults with chorea associated with Huntington's disease (HD). INGREZZA is the only selective vesicular monoamine transporter 2 (VMAT2) inhibitor that offers an effective starting dosage that can be adjusted by a patient's healthcare provider based on response and tolerability, with no complex titration.

Neurocrine presented data to the FDA in December of 2022, and on August 18th 2023, Neurocrine announced that INGREZZA had been FDA approved, meaning that it can now be officially prescribed to people in the USA to treat HD chorea.

Ingrezza should help address an unmet need in the treatment of Huntington's-associated chorea, according to Charles Duncan, an analyst who covers Neurocrine for the investment firm Cantor Fitzgerald. In a note to clients, Duncan wrote that in the U.S. there are about 30,000 Huntington's patients, of which roughly 90% experience chorea. And among that group, approximately 70% have moderate-to-severe forms of the disorder.

This label expansion brought Ingrezza into direct competition with Teva's Austedo—the medication's label now largely stacks up to Teva Pharmaceutical Industries' rival vesicular monoamine transporter 2 inhibitor Austedo, which picked up its own Huntington's disease chorea nod in 2017.

The Concentration Risk

Through all of this success, however, lurked a significant concern: The blockbuster generated sales of $613 million in the third quarter and is expected to rack up revenue of $2.3 billion in 2024. Ingrezza wasn't just Neurocrine's most important product—it was essentially its only product.

IX. The Crenessity Story: Full Circle to CRF (2024)

Thirty-Two Years Later

In December 2024, something remarkable happened. The science that Wylie Vale brought to Neurocrine in 1992—the CRF research that defined the company's founding thesis—finally produced an approved drug.

CRENESSITY, the first new treatment available in 70 years to the classic congenital adrenal hyperplasia (CAH) community, offers a paradigm-shifting treatment approach. FDA approval supported by data from the largest-ever clinical trial program in pediatric and adult patients with classic CAH.

CRENESSITY, a potent and selective oral corticotropin-releasing factor type 1 receptor (CRF1) antagonist, is the first and only classic CAH treatment that directly reduces excess adrenocorticotropic hormone (ACTH) and downstream adrenal androgen production, allowing for glucocorticoid dose reduction. It is a breakthrough in the treatment landscape for classic CAH.

"For the last three decades, Neurocrine Biosciences, together with our late founder, Wylie W. Vale, has conducted groundbreaking research uncovering the critical role of corticotropin-releasing factor and its receptor, CRF1, in the pathophysiology of congenital adrenal hyperplasia," said Kyle W. Gano, Ph.D., Chief Executive Officer, Neurocrine Biosciences.

The Science Coming Home

Some 20,000 to 30,000 patients in the U.S. have CAH and have historically been prescribed large amounts of steroid hormones like hydrocortisone or a glucocorticoid to regulate their body's adrenal system. Crenessity, according to Gano, uses pharmaceutical technology the company originally licensed from the Salk Institute around the time of the company's 1992 founding to better regulate the body's hypothalamic-pituitary-adrenal axis, in turn necessitating significantly lower doses of hydrocortisone or a glucocorticoid.

Mentored by Dr. Vale, Dimitri E. Grigoriadis, Ph.D., first served as Neurocrine's Director of Pharmacology and Drug Discovery and led the development efforts of several CRF receptor antagonists for neuropsychiatric and neuroendocrine disorders. One of the compounds was crinecerfont, an investigational CRF1 receptor antagonist that was approved by the FDA in 2024 and brought innovation to a patient community that has not seen advancements in care in more than 70 years.

Clinical Evidence and Market Potential

Crenessity's approval is based on two randomized, double-blind, placebo-controlled trials in 182 adults and 103 children with classic CAH. In the first trial, 122 adults received Crenessity twice daily and 60 received placebo twice daily for 24 weeks. The group that received Crenessity reduced their daily glucocorticoid dose by 27% while maintaining control of androstenedione levels, compared to a 10% daily glucocorticoid dose reduction in the group that received placebo.

The launch exceeded expectations. The launch of Crenessity, Neurocrine's treatment for congenital adrenal hyperplasia (CAH), has exceeded expectations with first-quarter sales of $15 million, significantly outperforming the consensus estimate of $4 million.

CRENESSITY net product sales through the first nine months of 2025 were $166 million and included 1,617 total new patient enrollment forms.

Analysts project peak U.S. sales potential for Crenessity could realistically reach between $800 million to $1 billion, underscoring its importance to the company's future growth.

The Priority Review Voucher

The nod is accompanied by a valuable rare pediatric disease priority review voucher, which can be used to expedite the FDA's assessment of another application. These vouchers can be sold to other pharmaceutical companies for substantial sums—providing additional value beyond the commercial potential of the drug itself.

X. Leadership Transition: The Kevin Gorman Era Ends (2024)

Sixteen Years at the Helm

Gorman served as the President and CEO of the Company from January 2008 through October 2024, after having served as Executive Vice President and Chief Operating Officer beginning in 2006.

Kevin Gorman's tenure as CEO spanned the company's darkest hours and its greatest triumphs. "When I took on the role of CEO in 2008, Neurocrine was a clinical stage company with a limited pipeline and no approved products. Together, we have built a diverse pipeline and a leading R&D innovation engine designed to rapidly deliver up to four INDs per year. We successfully launched INGREZZA, which has driven strong financial results while improving the treatment of tardive dyskinesia and chorea associated with Huntington's disease."

Gorman, who has been Neurocrine's CEO since 2008, worked the company to the commercial stage in 2017 with the FDA approval of Ingrezza. With indications in tardive dyskinesia and involuntary movements in Huntington's disease, Ingrezza is today a fast-growing blockbuster with sales expected to surpass $2 billion this year.

Internal Succession

Effective October 11, 2024, the biotech's current chief business development and strategy officer, Kyle Gano, Ph.D., took over the reins as the new CEO. More than three decades after founding Neurocrine in 1992, Kevin Gorman, Ph.D., retired as the neuroscience specialist's CEO.

The choice of Gano reflected Neurocrine's commitment to internal succession and cultural continuity. "We have worked closely together for more than 20 years. He has been instrumental in Neurocrine's success and is an exceptional leader of the organization."

Beyond his business development and strategy portfolio, Dr. Gano has led numerous high-impact operational and business priorities. These include having been the lead inventor on the patent to the valbenazine molecule, having served as Team Lead for both the elagolix development program and VMAT2 Franchise Team, and currently holding oversight responsibility for all muscarinic development teams and activities. He also played key leadership roles in the development of three FDA-approved medicines.

From intern in 2001 to CEO in 2024—Gano's journey embodies the patient capital and patient science that defines Neurocrine.

XI. Modern Era: Pipeline, Diversification & The Next Act (2025 and Beyond)

The Schizophrenia Opportunity

Neurocrine's pipeline reflects an aggressive push into neuropsychiatry. Neurocrine Biosciences announced the initiation of a Phase 3 registrational program to evaluate the efficacy, safety and tolerability of NBI-1117568, the company's investigational oral muscarinic M4 selective orthosteric agonist, as a potential treatment for schizophrenia. Positive top-line data for the Phase 2 clinical study in adults with schizophrenia were reported in August 2024.

Neurocrine is initiating the Phase 3 study supported by positive top-line data from the Phase 2 clinical study, which met its primary endpoint for the once-daily 20 mg dose. The study found a clinically meaningful and statistically significant reduction from baseline in the PANSS total score at Week 6 with a placebo-adjusted mean reduction of 7.5 points (p=0.011 and effect size of 0.61) and an 18.2-point reduction from baseline. A statistically significant improvement across several secondary endpoints.

NBI-1117568 is the first and only investigational oral muscarinic M4 selective orthosteric agonist in clinical development for the treatment of schizophrenia. There are five muscarinic acetylcholine receptors involved in neurotransmission. Muscarinic receptors are central to brain function and validated as drug targets in psychosis and cognitive disorders. As an M4 selective orthosteric agonist, NBI-1117568 offers the potential for a novel mechanism with an improved safety profile.

The Depression Program

Neurocrine announced amendment to strategic collaboration with Takeda to develop and commercialize osavampator. Under the amended agreement, Neurocrine will obtain exclusive rights for all indications to develop and commercialize osavampator in all territories worldwide except Japan, where Takeda will acquire exclusive rights.

Osavampator represents Neurocrine's entry into the massive major depressive disorder market—a condition affecting tens of millions of patients where treatment response remains inadequate.

New Headquarters for a New Era

For much of the last two decades, Neurocrine was headquartered on El Camino Real near Del Mar. The company still leases a couple buildings there, but Neurocrine finally opened its new home in Carmel Valley in 2024 and finished moving its roughly 1,000 San Diego-based employees to the facility earlier this year. The four-building complex along state Route 56 includes some 500,000 square feet of office space and an additional 250,000 square feet of laboratory space.

The sprawling campus, more than double the footprint of Neurocrine's previous headquarters, is an apt representation of the company's recent growth and expansion of its portfolio of neuroscience-focused pharmaceutical drugs.

Financial Guidance

INGREZZA Full Year 2025 Net Product Sales Guidance of $2.5 - $2.6 Billion. CRENESSITY, a First-in-Class Treatment for Children and Adults with Classic Congenital Adrenal Hyperplasia, Approved and Launched in the United States. Phase 3 Programs for Osavampator in Major Depressive Disorder and NBI-'568 in Schizophrenia Initiating in the First Half of 2025.

XII. Playbook: Business & Investing Lessons

The 25-Year Overnight Success

Neurocrine's story demolishes the notion that biotech is about fast returns. From founding in 1992 to first commercial product in 2017 represents a quarter-century of research, clinical trials, failures, near-bankruptcies, and persistence. Investors who bought at the IPO in 1996 and held through the indiplon disaster of 2006, through the workforce reductions of 2010, and through years of clinical trials for valbenazine were rewarded—eventually.

This timeline is not unusual in biotech. It is, in fact, the norm. The lesson for investors is that biotech requires either exceptional patience or exceptional market timing. Position sizing matters enormously when holding companies through multi-year development cycles with binary outcomes.

Strategic Out-Licensing as Survival Strategy

The AbbVie deal for elagolix in 2010 was not a choice—it was a necessity. Neurocrine traded potential upside on a promising drug for immediate survival capital. Critics might argue the company left money on the table when elagolix was eventually approved and launched as Orilissa. But the counterfactual is that without the $75 million upfront payment and the removal of development costs, Neurocrine might not have survived long enough to develop valbenazine.

The lesson: sometimes the best deal is the one that keeps you alive. Option value has no worth if the company goes bankrupt.

First-Mover in Neglected Indications

Neurocrine's strategy of targeting underserved patient populations with no approved treatments proved enormously valuable. Tardive dyskinesia had 500,000-800,000 patients in the US with no FDA-approved treatment for 60+ years. Congenital adrenal hyperplasia had seen no new treatments in 70 years.

In both cases, Neurocrine wasn't competing against entrenched competitors with established sales forces and physician relationships. It was creating markets that didn't exist. This approach requires scientific insight into diseases that have been overlooked, but it reduces commercial risk significantly.

Platform Persistence

The CRF science that Wylie Vale brought to Neurocrine in 1992 didn't produce an approved drug until 2024. Thirty-two years. Most companies would have abandoned that research platform entirely. Neurocrine's persistence—maintaining institutional knowledge, continuing basic research, and eventually developing crinecerfont—demonstrates the value of scientific platforms when properly nurtured over time.

Leadership Longevity

Kevin Gorman's 16-year CEO tenure and Kyle Gano's 24 years at the company (including 7+ years working closely with Gorman) represent unusual continuity for the biotech industry. This continuity appears to have benefited Neurocrine through institutional knowledge preservation, consistent strategic execution, and cultural stability.

XIII. Bull Case & Bear Case Analysis

Porter's Five Forces Assessment

Threat of New Entrants: MODERATE The neuroscience drug development space requires enormous capital, specialized expertise, and 10-15 year development timelines. These represent significant barriers to entry. However, large pharmaceutical companies can enter through acquisition, as Bristol-Myers Squibb demonstrated with Karuna Therapeutics (Cobenfy). The threat is less from de novo startups and more from well-capitalized acquirers.

Bargaining Power of Suppliers: LOW Neurocrine's small molecule drugs don't require complex biological manufacturing. Generic API suppliers are abundant. The company has not disclosed supply concentration risks that would give individual suppliers pricing power.

Bargaining Power of Buyers: MODERATE-HIGH US healthcare payers—pharmacy benefit managers, Medicare, Medicaid—have significant negotiating power. The Inflation Reduction Act introduces new pricing dynamics. The Inflation Reduction Act introduces new pricing dynamics that could affect Neurocrine's revenue growth, particularly for established products like Ingrezza.

However, Neurocrine received Centers for Medicare and Medicaid Services (CMS) notification in January that INGREZZA qualifies for the small biotech exemption under the Medicare Drug Price Negotiation Program.

Threat of Substitutes: MODERATE Neurocrine's drug will now compete more directly with Austedo, a Teva Pharmaceutical medicine that, like Ingrezza, is approved to treat chorea as well as another neurological condition called tardive dyskinesia. Teva represents meaningful competition, though Ingrezza maintains dosing and titration advantages.

Industry Rivalry: MODERATE The VMAT2 inhibitor market is essentially a duopoly between Neurocrine and Teva. Neurocrine operates in a competitive market, with companies like Teva Pharmaceutical Industries and Lundbeck offering competing products in the movement disorder space. The launch of Bristol Myers Squibb's Cobenfy is also being closely watched, as it may provide context for Neurocrine's own M4 targeting agonist in development.

Hamilton Helmer's 7 Powers Framework

Scale Economies: LIMITED As a specialty pharmaceutical company, Neurocrine doesn't benefit from significant scale economies in manufacturing or distribution. Its competitive advantages lie elsewhere.

Network Effects: NONE Pharmaceutical products don't exhibit network effects.

Cornered Resource: MODERATE Neurocrine's patent portfolio on valbenazine and its institutional expertise in VMAT2 biology represent cornered resources. The companies that filed Abbreviated New Drug Applications (ANDA) to the FDA seeking approval to market generic versions of INGREZZA have the right to sell generic versions of INGREZZA in the U.S. beginning March 2038, or earlier under certain circumstances.

Counter-Positioning: STRONG Neurocrine's focus on underserved neurological conditions that large pharma companies overlooked represents strong counter-positioning. Big pharma historically pursued larger market indications; Neurocrine built expertise in neglected conditions.

Switching Costs: MODERATE Physicians who have successfully treated patients with Ingrezza and are comfortable with its dosing and titration would face switching costs in terms of learning new drugs and managing potential transition issues.

Process Power: MODERATE Neurocrine's internal R&D capabilities in neuroscience represent accumulated process power. Neurocrine emphasized its R&D transformation strategy aimed at delivering a new medicine every two years.

Branding: LIMITED In specialty pharmaceuticals, branding matters less than clinical evidence and physician relationships.

Bull Case

-

Ingrezza's long runway: With only 10% of TD patients treated, significant market penetration opportunity remains. Patent protection through 2038 provides extended exclusivity.

-

Crenessity as a second blockbuster: The launch of Crenessity represents a new chapter for Neurocrine, potentially diversifying its revenue streams and addressing an unmet medical need. Analysts project peak U.S. sales potential for Crenessity could realistically reach between $800 million to $1 billion.

-

Deep pipeline in large markets: Phase 3 programs in schizophrenia and major depressive disorder represent substantially larger market opportunities than current indications.

-

Strong balance sheet: As of March 31, 2025, Neurocrine Biosciences had approximately $1.8 billion in cash, cash equivalents, and marketable securities.

-

Proven commercial execution: The successful launches of Ingrezza and Crenessity demonstrate organizational capability to convert science into sales.

Bear Case

-

Revenue concentration: Ingrezza, Neurocrine's primary revenue driver, has shown consistent performance. In Q1 2025, Ingrezza sales reached $545 million, aligning with consensus estimates. But this concentration means any setback to Ingrezza—competitive pressure, pricing erosion, safety signal—would be devastating.

-

Pipeline execution risk: The Phase 3 study of valbenazine for the adjunctive treatment of schizophrenia did not meet the primary endpoint. Consistent trends favoring valbenazine were observed across key study measures, including a statistically significant effect in the positive symptom domain of the Positive and Negative Symptoms Scale (PANSS). This represents a setback in extending the valbenazine franchise.

-

IRA pricing pressure: Government intervention in drug pricing could accelerate and expand beyond current exemptions.

-

Competition intensifying: Teva's Austedo continues to compete in TD and HD chorea. Bristol-Myers Squibb's entry into the muscarinic agonist space with Cobenfy creates competitive pressure for Neurocrine's own muscarinic programs.

-

Crenessity adoption uncertainty: The drug's black box warning requires careful supervision for any changes to glucocorticoid therapy, and it has complicated dosing instructions. Additionally, broad commercial access is not anticipated until the second half of 2025, and only about 15% of patients are located near centers of excellence.

XIV. Key Metrics to Watch

For investors tracking Neurocrine's ongoing performance, three metrics matter most:

1. Ingrezza New Patient Starts

"We delivered a record number of new patient starts for INGREZZA, which is especially impressive given the typically challenging first quarter. This strong performance gives us good momentum heading into the rest of the year."

New patient starts indicate market penetration velocity. With only 10% of the estimated 800,000 TD patients currently treated, the runway for growth depends on reaching new patients. Quarterly disclosure of new patient starts (or proxy metrics like prescription growth) reveals whether Neurocrine is successfully expanding the treated population or merely retaining existing patients.

2. Crenessity Patient Enrollment Forms

CRENESSITY net product sales through the first nine months of 2025 were $166 million and included 1,617 total new patient enrollment forms.

For a rare disease drug with an estimated 20,000-30,000 US patients, patient enrollment velocity is the key leading indicator. The metric captures both physician adoption and patient access. Revenue will follow enrollment with a lag as reimbursement and dosing stabilize.

3. R&D Pipeline Progression

With Phase 3 programs underway in schizophrenia and major depressive disorder, the binary outcomes of these trials will substantially impact Neurocrine's long-term value. Track clinical trial enrollment pace, expected readout dates, and any interim announcements about trial conduct.

XV. Regulatory and Legal Overhangs

Patent Cliff

Generic companies have the right to sell generic versions of INGREZZA in the U.S. beginning March 2038, or earlier under certain circumstances. This provides substantial runway, but the "earlier under certain circumstances" language reflects ongoing patent challenges and potential at-risk generic launches.

Inflation Reduction Act

While Neurocrine has received a small biotech exemption for the current round of Medicare price negotiations, the political and regulatory landscape around drug pricing remains uncertain. Any expansion of government pricing authority or removal of exemptions would create revenue headwinds.

Black Box Warnings

Like Austedo, Ingrezza's label will be updated with a black box warning for depression and suicidal thoughts and behavior in patients with Huntington's. These warnings, while appropriate given the patient population, can limit prescribing and require careful risk management communications.

XVI. Conclusion: Science, Persistence, and the Art of Survival

Neurocrine Biosciences represents something rare in the corporate world: a 33-year story of scientific persistence culminating in transformative medicines for patients who had no options. "Everyone wanted to jump on board because Wylie Vale was the founder," Gorman said in an interview shortly after Vale's death in 2012. "We got some of the best scientists and management talent into the company because of Wylie's involvement."

The company survived the indiplon disaster by making hard choices—out-licensing elagolix to AbbVie, cutting staff to 67 people, focusing resources on the VMAT2 program that would eventually become Ingrezza. It built commercial capabilities from scratch and executed one of biotech's more impressive launches. And it maintained the CRF research platform from its founding long enough to finally see that science approved as Crenessity.

"As we begin our transition into a new chapter of growth and diversification for Neurocrine, we're pleased with our second quarter commercial performance across tardive dyskinesia, Huntington's chorea, and now, classic congenital adrenal hyperplasia," said Kyle W. Gano, Ph.D., Chief Executive Officer of Neurocrine Biosciences. "Although still early in our launch, the demand for CRENESSITY remains robust, underscoring the significant unmet need for a novel treatment option for patients with CAH."

The question for investors remains whether Neurocrine is a two-drug company with a pipeline of uncertain value, or whether the institutional capabilities that created Ingrezza and Crenessity can be replicated across schizophrenia, major depressive disorder, and beyond.

The 33-year overnight success continues to unfold.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube