Ionis Pharmaceuticals: The 35-Year Bet on RNA Medicine

I. Introduction & Episode Roadmap

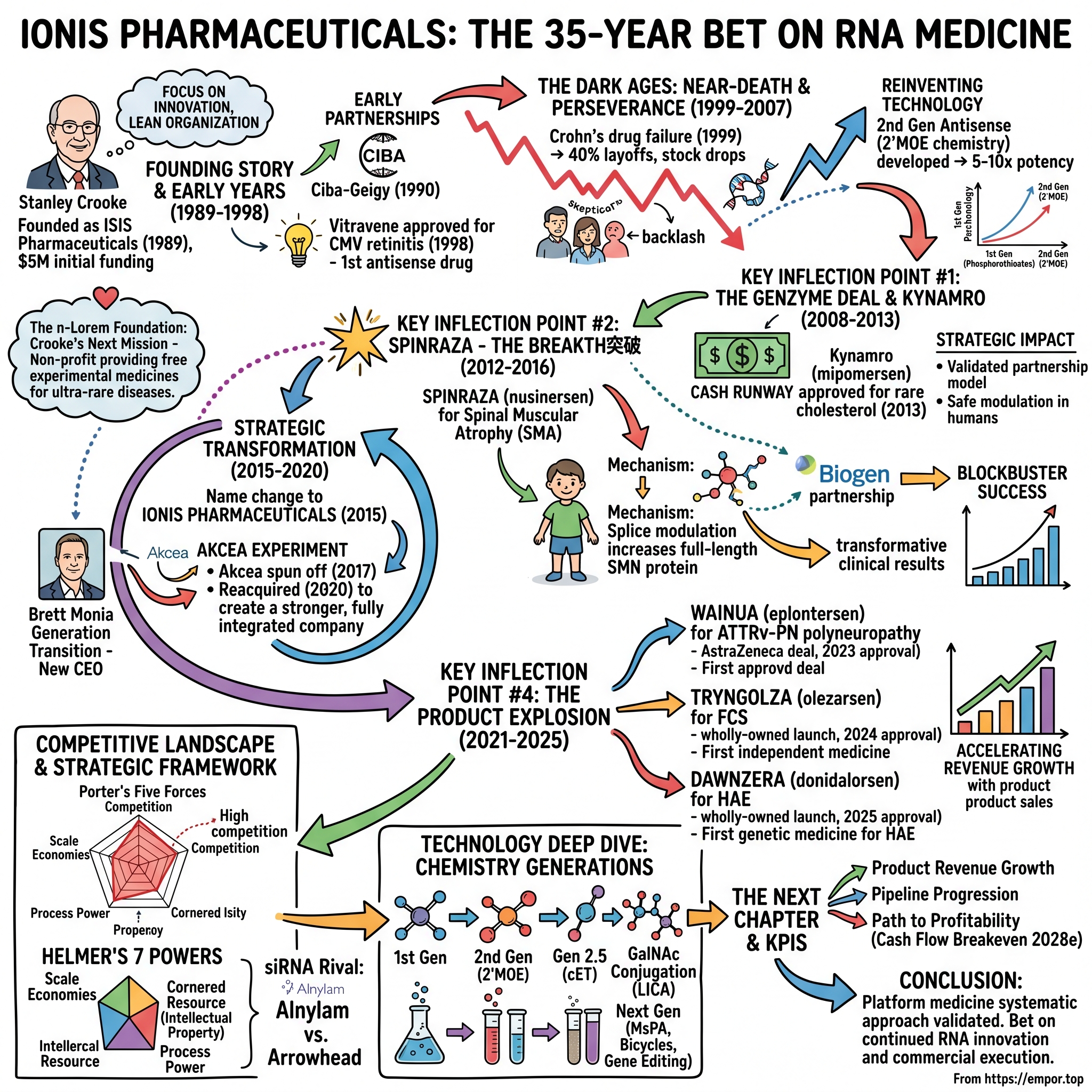

In the winter of 1999, Stanley Crooke stood at the precipice of ruin. His antisense drug for Crohn's disease—the one that was supposed to prove RNA medicines could work—had just failed to outperform a sugar pill in a 300-patient trial. Within days, Ionis's shares fell, and Crooke had to lay off 40% of his employees. The scientific community, which had already grown skeptical of antisense technology, seemed vindicated. Investment banks walked away. Competitors abandoned the field entirely.

Twenty-five years later, that same company sits at the center of a revolution in medicine. Ionis currently has six marketed medicines and a leading pipeline in neurology, cardiology, and other areas of high patient need. With a market capitalization of approximately $11.4 billion and trailing twelve-month revenue approaching $1 billion, Ionis has become one of the most prolific drug discovery engines in biotechnology history—having invented treatments for diseases once considered untouchable by traditional pharmaceuticals.

The central question this story demands is both simple and profound: How did a company survive 27 years of skepticism and clinical failures to pioneer an entirely new class of medicines?

Stanley Crooke founded Ionis Pharmaceuticals—a biotech company that helped pioneer the now successful technology of antisense oligonucleotides (ASO) despite overwhelming challenges and widespread disbelief. What he built was not merely a company but a platform—a systematic approach to drug discovery that could theoretically target any disease with a genetic basis.

The themes that emerge from Ionis's journey are ones that any student of business history will recognize: science versus skepticism (can you persevere when the world thinks you're wrong?), platform versus products (is it better to build a drug-discovery engine or a portfolio of individual treatments?), partnership dependency versus independence (when should you let others commercialize your innovations versus doing it yourself?), and the brutally long road from laboratory concept to patient bedside.

"TRYNGOLZA is the first of four independent Ionis product launches anticipated over the next three years," said Brett P. Monia, Ionis's CEO. "We also expect four key launches from important partnered programs within this timeframe."

The company stands at an inflection point. After three decades of primarily licensing its discoveries to pharmaceutical giants who handled the commercialization, Ionis has declared it will go it alone—building out commercial infrastructure to launch its own drugs and capture more of the value it creates. Ionis's accelerating revenue growth opportunity is fueled by its recent launches and late-stage medicines that provide greater than $5 billion in potential annual peak revenue. With accelerating growth within reach, Ionis has a clear path to achieve sustained positive cash flow and is expected to reach cash flow breakeven in 2028.

To understand whether this bet will pay off, we need to understand the science, the history, and the strategic choices that brought Ionis to this moment.

II. The Science of Antisense: Understanding the Technology

Before diving into corporate history, we must understand what makes Ionis's technology revolutionary—and why it took so long to work.

The central dogma of molecular biology states that DNA encodes RNA, which is then translated into proteins. Every drug you've ever taken—from aspirin to antibody therapies—works by targeting proteins after they've already been made. This approach has obvious limitations: proteins are complex three-dimensional structures, and only a fraction of them have surfaces amenable to small molecules or antibodies. The pharmaceutical industry calls the others "undruggable."

Antisense oligonucleotides (ASOs) are short, synthetic, single-stranded oligodeoxynucleotides that can alter RNA and reduce, restore, or modify protein expression through several distinct mechanisms. By targeting the source of the pathogenesis, ASO-mediated therapies have a higher chance of success than therapies targeting downstream pathways.

The elegance of antisense lies in its simplicity: if you can't drug the protein, drug the messenger. ASOs can bind to their target RNA transcript in a sequence-specific manner via Watson-Crick base pairing. They can thus be designed to target distinct sequences or specific genetic variants. In theory, any gene whose sequence is known can be targeted. Rather than hunting for the molecular equivalent of a keyhole on a protein's surface, you can simply design a complementary sequence that binds to the RNA and prevents it from ever making the problematic protein.

Antisense therapy is a form of treatment that uses antisense oligonucleotides to target messenger RNA. ASOs are capable of altering mRNA expression through a variety of mechanisms, including ribonuclease H mediated decay of the pre-mRNA, direct steric blockage, and exon content modulation through splicing site binding on pre-mRNA.

The mechanism works through multiple pathways. In RNase H-mediated cleavage, when an ASO binds to its target mRNA, it creates a DNA-RNA hybrid that the cell's own machinery recognizes as foreign and destroys. In splice modulation—the mechanism behind Spinraza—the ASO alters how the cell processes pre-mRNA, potentially restoring production of a functional protein. The goal of the antisense approach is the downregulation of a molecular target, usually achieved by induction of RNase H endonuclease activity that cleaves the RNA-DNA heteroduplex with a significant reduction of the target gene translation. Other ASO-driven mechanisms include inhibition of 5′ cap formation, alteration of splicing process (splice-switching), and steric hindrance of ribosomal activity.

What distinguishes single-stranded antisense from its cousin technology, RNA interference (siRNA), reveals much about Ionis's strategic positioning. siRNA uses double-stranded RNA to engage a cellular complex called RISC, which then finds and destroys target mRNA. Alnylam Pharmaceuticals, Ionis's primary competitor, has built its empire on this approach. Each technology has trade-offs: ASOs generally have better cellular penetration properties and can reach tissues that siRNA cannot easily access, while siRNA tends to be more potent once inside the cell.

Why was this approach revolutionary compared to small molecules and antibodies? Consider the arithmetic of drug discovery. Traditional small molecule programs might screen millions of compounds to find one that binds a protein target—a process that can take years and cost hundreds of millions of dollars, with no guarantee of success. The principle of Watson-Crick molecular recognition provides the antisense field more flexibility in RNA-based drug design and expedites its development, which is imperative for targeting a myriad of rare and genetic diseases.

With antisense, once you have a validated platform chemistry, designing a new drug becomes almost algorithmic: identify the RNA sequence you want to target, design a complementary oligonucleotide, and begin testing. This explains Ionis's prolific pipeline—the platform nature of the technology allows for systematic exploration of disease targets rather than one-off drug hunts.

The strategic implication for investors is profound: As of 2020 more than 50 antisense oligonucleotides were in clinical trials, including over 25 in advanced clinical trials (phase II or III). A follow-on drug to Inotersen is being developed by Ionis Pharmaceuticals and under license to Akcea Therapeutics for hereditary transthyretin-mediated amyloidosis.

III. Founding Story & Early Years (1989-1998)

Stanley Crooke is not the sort of person who stumbles into things. Before founding Ionis, he had already helped build oncology research at Bristol Laboratories and risen to lead R&D at SmithKline Beckman—a predecessor of pharmaceutical giant GlaxoSmithKline. After helping build oncology research at Bristol Laboratories, he was hired to lead R&D at SmithKline, which through a series of mergers would become today's GlaxoSmithKline. He arrived in Philadelphia in 1980, a time when SmithKline was enjoying the early spoils of what would become the industry's first blockbuster drug, the ulcer treatment Tagamet. His mandate was to help build a research engine that could produce more big sellers.

But Crooke grew disillusioned. While at SmithKline, Crooke became convinced the drug industry's model was broken. His observation, one that would shape the next 30 years of his career, was that tethering research to a commercial operation was harmful to innovation. To develop and market their drugs, companies "built this enormous infrastructure and it was a tremendous ballast. Just dead weight," he says.

He advocated a leaner organization that would focus on innovation and let a partner company take on selling whatever drugs came out of its efforts. To test the model, he needed a technology that could generate a steady pipeline of therapies. A lot of new ideas were floating around at the time—gene therapy, combinatorial chemistry, lipid-based therapeutics. But after hearing a lecture at SmithKline by two pioneers, Crooke was hooked on antisense.

Ionis Pharmaceuticals was founded in 1989 by Stanley Crooke, under the name ISIS Pharmaceuticals, in order to develop antisense therapy. The company started with $5 million in initial funding.

That initial capital came amid what one researcher described as "incredible optimism and excitement—one might say euphoria—at the time that this was rational drug design" for the most challenging targets and diseases. "The idea is it was going to be God's gift to drug development," says Art Krieg, who was a postdoctoral researcher at the NIH at the time. That euphoria, stoked in no small part by Crooke, led to a pact with Ciba-Geigy worth $30 million, forged while Ionis was still operating out of makeshift labs.

The company made a series of partnerships with pharmaceutical and biotech businesses early on. Its first major contract was a $30 million drug development agreement with Swiss pharmaceutical company Ciba-Geigy, who also invested in Ionis. At first, the company developed antisense methodologies in general, without targeting a specific drug or disease.

The culture Crooke established was deliberately intense. Those who worked with him describe someone who "operates at an intellectual pace, as both a scientist and a leader, that makes him something of a force of nature." Ask anyone to describe Stanley Crooke, CEO of Ionis Pharmaceuticals, and a single word comes up again and again: intense. Friends and adversaries alike say he operates at an intellectual pace, as both a scientist and a leader, that makes him something of a force of nature. Keep up, or be swept aside. It took a force of nature to tunnel through the mountain of challenges that defined antisense oligonucleotides.

The mission statement Crooke crafted captured this urgency: "The first line in our culture statement is one I have thought about on most days of my career: 'sick people depend on us.' That simple statement is an extraordinary motivator when coupled to a demanding culture committed to innovation and the practice of rigorous scientific inquiry and the growth of every individual in the organization."

The first validation came in 1997 and 1998. In 1997, ISIS 2302 became the first antisense medication to be effective when injected, rather than applying it directly to the affected area. The following year, Ionis' fomivirsen (Vitravene) became the first antisense therapy drug approved by the FDA.

Vitravene treated cytomegalovirus retinitis in AIDS patients—a narrow indication that proved the technology could work in humans. But commercial reality was harsh: the drug required injection directly into the eye, the patient population was small, and sales were negligible. The therapy was eventually discontinued in 2004.

Still, the milestone mattered. Ionis had taken a concept from laboratory curiosity to FDA approval. The question was whether this proof of concept could be extended to diseases that actually had commercial markets.

IV. The Dark Ages: Near-Death Experience & Perseverance (1999-2007)

The Crohn's disease disaster of 1999 nearly killed the company. In 1999, a drug that Ionis developed for Crohn's disease, a severe intestinal disorder, failed to outperform a sugar pill in a test with 300 patients. Within days, Ionis's shares fell, and Crooke had to lay off 40% of his employees. "Many investors were very critical and didn't believe that we had made progress and that there was evidence that antisense was working. And so we were all very defensive," he said.

The timing could not have been worse. In 1998, competitor Gilead Sciences abandoned antisense research and sold its patents to Ionis. In 2000, one of Ionis' largest backers, Novartis Pharmaceuticals, ended their partnership with Ionis. Many of the larger pharma and biotech companies abandoned research for antisense methodologies. By this time, Ionis was one of the only companies still developing antisense compounds.

Academic research on the topic was discredited, accompanied by "severe backlash" when people realized the early papers were incorrect, said Karl-Heinz Altmann, who led chemistry at Ciba-Geigy during the Ionis collaboration. Crooke was criticized for exaggerating the capabilities of antisense while minimizing its limitations. The souring attitude toward antisense drew the research team at Ionis closer, and they became more determined, united by the scientific community's dismissal of their work.

This period revealed something fundamental about Crooke's leadership and the culture he had built. Rather than pivot to a different technology or sell the company, he doubled down. In his recent paper, Crooke articulated that creating and advancing a new drug technology required consistent commitment to innovation and innovators, investment in research, and perseverance through many challenges, disappointments, failures, and outright mistakes. "Ionis certainly experienced all those types of events. To persevere, our mission needed to be compelling and clearly articulated, the culture coherent and cohesive."

The breakthrough came from understanding why the first-generation drugs were failing. In the mid-1990s, Ionis and its research partner Ciba-Geigy discovered one of the main reasons first-generation antisense medications had potency and duration issues. The phosphorothioates that replace an oxygen molecule in a DNA strand with a sulfur molecule was decreasing effectiveness. Ionis changed its approach by modifying the ribose ring of the DNA strands instead. Second generation antisense used a methoxyethyl modification and had five-to-ten times the potency of Ionis' first-generation antisense.

This wasn't just an incremental improvement—it was a paradigm shift. The 2′-O-methoxyethyl (2'MOE) chemistry would become the foundation of nearly every successful Ionis drug. The improvement in potency and duration meant drugs could be dosed less frequently and reach therapeutic concentrations that first-generation compounds never achieved.

In the mid-1990s, Ionis and its research partner Ciba-Geigy discovered one of the main reasons first-generation antisense medications had potency and duration issues. The phosphorothioates that replace an oxygen molecule in a DNA strand with a sulfur molecule to prompt genetic modification was decreasing the effectiveness of the RNA to bind to cells. Ionis changed its approach by modifying the ribose ring of the DNA strands instead, eliminating the introduction of sulfur. Second generation antisense used a methoxyethyl modification and had five-to-ten times the potency of Ionis' first-generation antisense.

By the early 2000s, Crooke accepted that his company would survive; Ionis's second-generation antisense drugs had made their way to the clinic. It became clear to him that although having a common enemy brought the team together, it would ultimately become detrimental. Crooke wanted the internal culture to be less defensive. The doubters had disappeared, and it was time the company reflected this.

For investors, this period illustrates a crucial lesson: technological revolutions rarely happen on schedule. Two decades after antisense oligonucleotides were initially identified as agents capable of modulating RNA processing and protein expression, the first antisense oligonucleotide therapies have now been approved for the treatment of neurological disease. Over the years, novel chemical modifications of ASOs have been employed to address these issues. These modifications, in combination with elucidation of the mechanism of action of ASOs and improved clinical trial design, have provided momentum for translation.

V. Key Inflection Point #1: The Genzyme Deal & Kynamro (2008-2013)

After nearly two decades of losses and skepticism, the partnership with Genzyme represented the first major validation that the new chemistry could produce commercially viable drugs.

In 2008, Ionis won a $175 million contract to develop a cholesterol drug then-called mipomersen and later branded as Kynamro, in partnership with Genzyme Corporation. Genzyme paid $325 million in a stock and cash deal, plus a $175 million licensing fee and 30-50% royalty on sales. It was Ionis' first "notable success." Mipomersen was rejected by the European Medicines Agency in 2012, but approved by the FDA in 2013.

The drug targeted a form of severely elevated cholesterol called homozygous familial hypercholesterolemia—a rare genetic condition where patients inherit two defective copies of the gene responsible for clearing LDL cholesterol. These patients often have heart attacks in their twenties or thirties despite maximum medical therapy.

By this time, Ionis had 26 drugs under development and had just opened a new research and development center in 2011. Ionis earned $325 million from Kynamro that year, which was enough to keep the company solvent. This was followed by a series of more profitable deals.

The strategic importance of Kynamro extended far beyond its modest commercial performance. First, it validated the partnership model: a major pharmaceutical company had staked hundreds of millions on Ionis's technology. Second, it demonstrated that second-generation antisense chemistry could safely and effectively modulate disease-relevant targets in humans. Third, it provided the cash runway Ionis needed to pursue more ambitious programs.

The European rejection highlighted a persistent challenge: regulatory agencies remained cautious about new therapeutic modalities, demanding extraordinary safety data before approval. This caution would delay or complicate several subsequent Ionis programs.

VI. Key Inflection Point #2: Spinraza — The Breakthrough (2012-2016)

Every technology company has a "killer app"—the product that proves the platform's potential to the world. For Ionis, that product was Spinraza.

The FDA approved SPINRAZA (nusinersen) under Priority Review for the treatment of spinal muscular atrophy (SMA) in pediatric and adult patients. SPINRAZA is the first and only treatment approved in the U.S. for SMA, a leading genetic cause of death in infants and toddlers that is marked by progressive, debilitating muscle weakness.

Spinal muscular atrophy is a devastating genetic disease. Spinal muscular atrophy refers to a group of inherited neurological disorders that begin in infancy or childhood and lead to the degeneration of spinal motor neurons, the neurons that control skeletal muscles. This degeneration results in weakness, muscle wasting, and in the most severe cases, paralysis and death before two years of age. SMA affects approximately 1 in 10,000 newborns and is a leading genetic cause of death in infants and toddlers.

The science behind Spinraza is elegant. SPINRAZA is an antisense oligonucleotide (ASO) that is designed to treat SMA caused by mutations in the chromosome 5q that leads to SMN protein deficiency. It was discovered and co-developed by Ionis Pharmaceuticals and Biogen. SPINRAZA is designed to selectively bind to and alter the splicing of a single RNA from the SMN2 gene, a gene that is nearly identical to SMN1, in order to increase production of full length SMN protein. ASOs are short synthetic strings of nucleotides designed to selectively bind to target RNA and regulate gene expression. Through use of this technology, SPINRAZA has the potential to increase the amount of functional SMN protein in infants and children with SMA.

Rather than reducing production of a harmful protein—the typical antisense approach—Spinraza uses splice modulation to increase production of a beneficial one. Patients with SMA have a defective SMN1 gene but carry backup copies of a nearly identical gene called SMN2. Unfortunately, SMN2 produces mostly truncated, non-functional protein due to alternative splicing. Spinraza forces the cell to include an exon that's usually skipped, restoring production of full-length, functional SMN protein.

The partnership with Biogen structured the economics. Biogen and Ionis conducted an innovative clinical development program that moved SPINRAZA from its first dose in humans in 2011 to its first regulatory approval in five years. Based on the FDA approval of SPINRAZA, Ionis received a $60 million milestone payment.

Biogen exercised its option to worldwide rights to SPINRAZA in August 2016. Ionis retained tiered royalties on sales up to a percentage in the mid-teens—a structure that would generate hundreds of millions in annual revenue.

The clinical results were transformative. In ENDEAR, a pivotal controlled clinical study, infantile-onset SMA patients treated with SPINRAZA achieved and sustained clinically meaningful improvement in motor function compared to untreated study participants. In addition, a greater percentage of patients on SPINRAZA survived compared to untreated patients.

At a planned interim analysis of ENDEAR, a greater percentage of infants treated with SPINRAZA achieved a motor milestone response compared to those who did not receive treatment (40% versus 0%; p<0.0001) as measured by the Hammersmith Infant Neurological Examination. Additionally, a smaller percentage of patients on SPINRAZA died (23%) compared to untreated patients (43%).

Spinraza became a blockbuster almost immediately. The drug peaked at approximately $2 billion in annual sales in 2019. While sales have since declined due to competition from gene therapy (Novartis's Zolgensma) and newer treatments, Spinraza continues to generate substantial revenue. SPINRAZA (nusinersen) 12mg/5 mL injection is approved in more than 71 countries to treat infants, children and adults with spinal muscular atrophy. As a foundation of care in SMA, more than 14,000 individuals have been treated with SPINRAZA worldwide.

For Ionis, Spinraza accomplished several strategic objectives. It demonstrated that antisense could transform a fatal disease into a manageable condition. It validated the partnership model, generating substantial royalty revenue. And it proved to the broader pharmaceutical industry that RNA medicines were a legitimate therapeutic modality worth investing in.

Ionis's top source of commercial revenue is royalties from Spinraza, the spinal muscular atrophy drug that is marketed by partner Biogen. Ionis reported $216 million in Spinraza royalty revenue in 2024.

VII. Key Inflection Point #3: Strategic Transformation (2015-2020)

In December 2015, the company made a change that seemed trivial but symbolized something profound: it changed its name from ISIS Pharmaceuticals to Ionis Pharmaceuticals. In 2015, the company changed its name from "ISIS" to "IONIS" to avoid confusion with the terrorist group Islamic State of Iraq and the Levant (ISIS).

The rebranding reflected a desire to distance the company from negative associations, but more importantly, it coincided with a period of strategic reinvention.

The cardiovascular division of Ionis was spun-off into a separate company called Akcea in 2017, to help fund Ionis' own research and development.

With a growing list of experimental drugs in the works, Ionis created Akcea as a subsidiary in late 2014 to help with the effort. It was formed specifically to advance the piece of Akcea's pipeline that specifically focused on rare lipid disorders, and sell them once they got to market. By 2017, Ionis had decided Akcea would be more valuable as a standalone company. It conducted an initial public offering that summer, ultimately recording $144 million in gross proceeds.

The Akcea experiment produced mixed results. On one hand, the company was able to notch its first U.S. approval in 2018 with Tegsedi, a drug for peripheral nerve damage caused by an uncommon inherited disease. Then, in 2019, European regulators allowed Akcea to start marketing another drug, Waylivra, as an adjunctive treatment for patients with a metabolic illness known as FCS.

But sales disappointed. Sales of the two totaled $42 million combined in 2019, the last full year of Akcea's independence, and climbed to $70 million in 2020 as they were launched in additional countries. By comparison, Onpattro, a rival therapy to Tegsedi, generated $306 million for its developer, Alnylam Pharmaceuticals.

This underperformance prompted a strategic reversal. In August 2020, Ionis and Akcea entered into a definitive agreement under which Ionis will acquire all of the outstanding shares of Akcea common stock it does not already own, approximately 24%, for $18.15 per share in cash. This corresponds to a total transaction value of approximately $500 million on a fully diluted basis. The transaction has been approved by the Ionis and Akcea Boards of Directors.

On October 12, 2020, Ionis announced the successful completion of its transaction to acquire 100% ownership of Akcea Therapeutics. The combination of Ionis and Akcea accelerates the next phase of Ionis' growth and positions it to better deliver more medicines to patients while maximizing value to all stakeholders.

"This acquisition is another step forward in Ionis' evolution and creates a stronger, more efficient organization," Ionis CEO Brett Monia said in an August 2020 statement. "We believe becoming one company—with one vision and one set of strategic priorities, led by one team—will deliver significant strategic value."

Brett Monia's elevation to CEO marked a generational transition. Brett Monia, Ionis' chief operating officer and new CEO, said that although Crooke challenges his employees at every turn, he also considers them family.

Monia had been with Ionis since 1997 and understood both the science and the strategic opportunity. Under his leadership, the company made the bold decision that would define its next chapter: Ionis would become a fully integrated commercial company, launching its own drugs rather than licensing everything to partners.

VIII. Key Inflection Point #4: The Product Explosion (2021-2025)

The years since 2021 have witnessed an extraordinary acceleration in Ionis's commercial trajectory.

The AstraZeneca deal in 2021 established the template for major partnerships. In December 2021, AstraZeneca bought the right to jointly develop and commercialize eplontersen in the U.S. for $200 million upfront and the promise of up to $485 million once it won FDA approval. AstraZeneca also pledged as much as $2.9 billion in sales-related milestones, plus royalties.

AstraZeneca will pay Ionis an upfront payment of $200 million and additional conditional payments of up to $485 million following regulatory approvals. It will also pay up to $2.9 billion of sales-related milestones based on sales thresholds between $500 million and $6 billion, plus royalties in the range of low double-digit to mid-twenties percentage depending on the region.

That partnership bore fruit in December 2023. The U.S. Food and Drug Administration approved Ionis and AstraZeneca's WAINUA (eplontersen) for the treatment of the polyneuropathy of hereditary transthyretin-mediated amyloidosis in adults. WAINUA is the only approved medicine for the treatment of ATTRv-PN that can be self-administered via an auto-injector.

But the real transformation came with Ionis's wholly-owned drugs.

In December 2024, Ionis Pharmaceuticals secured FDA approval for Tryngolza (olezarsen), a treatment for familial chylomicronemia syndrome (FCS), a rare and life-threatening genetic condition that prevents the body from properly breaking down fats. Tryngolza marked the first time Ionis brought the drug to market itself, rather than relying on a partner. Ionis intends to eventually get approval to use the drug for a wider range of patients.

This was a corporate milestone: "With the recent launch of our first independent medicine, TRYNGOLZA for familial chylomicronemia syndrome, Ionis has begun a new chapter as a fully integrated commercial-stage biotechnology company," said Brett P. Monia. "Over the next three years, we expect three more independent launches, including donidalorsen later this year for hereditary angioedema and olezarsen for severe hypertriglyceridemia in 2026, pending Phase 3 results."

In 2025, the FDA approved Dawnzera, a prophylaxis for treating hereditary angioedema, a rare genetic disease that causes unusual swelling.

The FDA approved Ionis Pharmaceuticals' Dawnzera for preventing swelling attacks caused by the rare disease hereditary angioedema. A Takeda Pharmaceutical product dominates this market, but Ionis has clinical data showing patients had better outcomes after switching to Dawnzera from Takeda's drug and other currently available HAE medications. As with most rare diseases, the market for hereditary angioedema drugs is small. It's also relatively crowded, served by several well-established products. An injection from Ionis Pharmaceuticals is joining the list, and while the biotech company plans to capture new patients, it also aims to grow sales by getting patients to switch over from other products. The FDA's approval of donidalorsen, brand name Dawnzera, makes this Ionis drug the first genetic medicine for hereditary angioedema.

In a 24-week Phase 3 trial, dosing of the study drug every four weeks led to an average 81% reduction in HAE attacks compared to placebo. In the one-year open-label extension study, Dawnzera reduced attacks by an average of 94% across both four-week and eight-week dosing. In this study, Ionis reported that 93% of participants achieved well-controlled disease.

The financial results reflect this commercial momentum. For the third quarter ended September 30, 2025, Ionis reported a total revenue of $157 million, a 17% increase compared to the same period in 2024. The company's net product sales for TRYNGOLZA reached $32 million, contributing significantly to the revenue growth.

Ionis raised its 2025 revenue guidance to $875-$900 million and increased TRYNGOLZA guidance to $85-$95 million, citing quarterly revenue growth and strong product uptake. Management reported strong TRYNGOLZA growth, early DAWNZERA adoption, plans for olezarsen market expansion, and projected peak sales exceeding $500M for DAWNZERA and $1B for olezarsen.

IX. The n-Lorem Foundation: Crooke's Next Mission

When Stanley Crooke retired from Ionis in 2021, he didn't stop working. Instead, he redirected his energy toward a problem that traditional pharmaceutical economics could never solve: diseases so rare that only a handful of people in the world have them.

The n-Lorem Foundation announced its official launch as a nonprofit organization established to provide advanced, experimental RNA-targeted medicines free of charge for life to patients living with ultra-rare diseases. The n-Lorem Foundation is being established with an initial investment by founders Drs. Stanley and Rosanne Crooke. Ionis Pharmaceuticals and Biogen are providing additional funding as the first corporate donors. The Foundation will be headed by Stanley T. Crooke, former chairman and CEO and current executive chairman of the board at Ionis Pharmaceuticals. Dr. Crooke founded Ionis Pharmaceuticals in 1989 and, through his vision and leadership, established the company as the leader in RNA-targeted therapeutics.

The concept is remarkable. n-Lorem Foundation is a non-profit organization established to apply the efficiency, versatility and specificity of antisense technology to charitably provide experimental antisense oligonucleotide medicines to treat nano-rare patients diagnosed with diseases that are the result of a single genetic defect unique to only one or very few individuals. Nano-rare patients describe a very small group of patients (1-30 worldwide) who, because of their small numbers, have few if any treatment options. n-Lorem Foundation was created to provide hope to these nano-rare patients by developing individualized ASO medicines. The advantage of experimental ASO medicines is that they can be developed rapidly, inexpensively and are highly specific.

As the CEO of n-Lorem Foundation, his mission is to provide personalized treatments to ultra-rare disease patients for free as long as they live, no questions asked. Thanks to his humility, coupled with the generosity of other individuals and companies, ultra-rare disease patients have a renewed hope to get the treatments others may not be able to provide. Join Dr. Crooke as he reflects on his humble beginnings at Ionis.

The scale of impact has grown rapidly. n-Lorem's ASOs have been administered to more than 30 patients to date. Nearly all evaluable patients have achieved clinically significant benefit, despite the fact that many nano-rare patients are severely affected by their disease. Importantly, the safety and tolerability profile of n-Lorem ASOs is pristine in all treated patients. "I am proud that, through n-Lorem, we have been able to bring hope and treatment to nano-rare patients today. The benefits we are observing in multiple organs and in multiple genes illustrate the power of antisense and the effectiveness of a mutation-directed therapeutic approach," said Stanley T. Crooke. n-Lorem has received more than 330 applications and accepted more than 160 patients for potential treatment.

The n-Lorem Foundation represents the logical endpoint of platform medicine: if you can design a drug for any genetic target, and if manufacturing becomes cheap enough, why shouldn't every patient have access to a treatment designed specifically for their mutation?

Where did the concept for n-Lorem originate? Stan: It came from a commitment to patients, and my realization about five years ago that the antisense oligonucleotide technology we created at Ionis could be harnessed to meet the needs of ultra-rare disease patients. But I also knew that to reach some of the most isolated patients, technology alone would not be sufficient—we needed a new approach and significant public-private partnerships.

X. Technology Deep Dive: Chemistry Generations

Understanding Ionis's competitive position requires understanding the evolution of its chemistry platform.

First Generation (Phosphorothioates): The original antisense drugs substituted sulfur for oxygen in the DNA backbone, which protected the oligonucleotides from degradation. But this modification also reduced potency and caused side effects. Vitravene, the first FDA-approved antisense drug, used this chemistry.

Second Generation (2'MOE): The breakthrough. Second generation antisense used a methoxyethyl modification and had five-to-ten times the potency of Ionis' first-generation antisense. This also prompted a shift from focusing on cancer treatments in first-generation antisense to things like heart disease and metabolism issues and allowed patients to take antisense pharmaceuticals in higher doses. Most of Ionis's marketed drugs—including Spinraza, Tegsedi, and Wainua—use 2'MOE chemistry.

Generation 2.5 (cET): Constrained ethyl chemistry provides enhanced potency and broader tissue distribution, enabling targeting of organs beyond the liver.

GalNAc Conjugation (LICA): A game-changer for liver-targeted drugs. By linking a GalNAc (N-acetylgalactosamine) molecule to the antisense oligonucleotide, Ionis achieved dramatically improved uptake in liver cells. This technology underlies Wainua and enables subcutaneous administration with a simple auto-injector—a massive convenience improvement over earlier drugs.

Next Generation Technologies:

The company continues advancing its platform. The MsPA (mesyl phosphoramidate) backbone increases biological stability and duration of effect, potentially enabling less frequent dosing. Bicycles—small peptide-based ligands that bind to transferrin receptor 1—may enable improved delivery to muscle tissue, including cardiac muscle, and potentially crossing the blood-brain barrier.

In September 2024, Ionis Pharmaceuticals entered into an agreement with Roche for two early-stage studies. These projects prioritize the development of investigational drugs that target RNA and are intended to treat Alzheimer's disease and Huntington's disease.

Gene editing represents Ionis's newest frontier. The company entered this field through a 2022 partnership with Metagenomi, paying $80 million to work together on four gene editing projects.

XI. Competitive Landscape: The RNA Therapeutics Race

Ionis operates in an increasingly crowded field. The RNA therapeutics market sits at a moderate concentration level where early vaccine titans coexist with a long tail of modality specialists. Moderna and BioNTech continue to dominate revenue through pandemic legacy assets and oncology pipeline breadth, while Alnylam and Ionis leverage rare-disease franchises that deliver predictable cash flows.

Alnylam — The siRNA Rival:

Alnylam Pharmaceuticals has been Ionis's most consistent competitor. The two companies pioneered different approaches to RNA medicine—Ionis with single-stranded antisense, Alnylam with double-stranded siRNA—and have competed directly in several indications.

The approval of Wainua opens up a new front in a long-running battle between Ionis and Alnylam. The two companies are pioneers in different forms of RNA drug making, and each of them has used their respective approaches to bring several rare disease drugs to market. Yet their ambitions have overlapped in transthyretin amyloidosis, an inherited or acquired condition in which a misfolded protein accumulates in the body. For years, Alnylam has had the upper hand. Its first drug for people with transthyretin amyloidosis polyneuropathy, Onpattro, had a dominant market position compared to Ionis' rival Tegsedi. Alnylam also beat Ionis to market with a newer, more convenient version now sold as Amvuttra. Those two drugs generated about $650 million for Alnylam in 2022 and currently comprise a roughly $900 million franchise.

The relationship between Ionis and Alnylam is complex. Under an agreement formed in 2004, certain Ionis patents are licensed exclusively to Alnylam for double-stranded RNAi therapeutics. The two companies also formed Regulus Therapeutics in 2007 as a 50/50 joint venture focused on micro-RNA targets.

Arrowhead — Direct Competition:

Arrowhead Pharmaceuticals represents newer competition, particularly in metabolic diseases. The company has developed its own RNAi platform and is pursuing indications that overlap with Ionis's pipeline.

Arrowhead Pharmaceuticals is making its mark with its innovative RNAi platform, and its Plozasiran therapy shows significant promise for cardiovascular applications, adding to the company's increasing market share.

HAE Competition:

In hereditary angioedema, Ionis faces established players. Takeda Pharmaceutical's lanadelumab, brand name Takhzyro, dominates the HAE prophylaxis market. This antibody kallikrein inhibitor is approved for patients age 2 and older, administered as a subcutaneous injection every two weeks. BioCryst Pharmaceuticals markets Orladeyo, a once-daily oral small molecule kallikrein inhibitor approved for HAE prophylaxis in patients age 12 and older.

Market Growth:

The broader market context favors all RNA therapeutics players. The RNA therapeutics market size stood at USD 15.1 billion in 2025 and is forecast to reach USD 23.5 billion in 2030, translating into a 9.2% CAGR during the assessment period. Venture funding that accelerated after the pandemic has remained buoyant.

The intensity of competition in the RNA Therapeutics Market is very high due to the fast development of technologies and a soaring increase in the funds invested in R&D. Moderna, BioNTech, Alnylam, and Ionis Pharmaceuticals are the key players that dominate the market and have strong RNA pipelines, own platforms, and approved therapies by the FDA. The competition focuses on the innovation in the RNA modalities (mRNA, siRNA, ASOs) and sophisticated delivery systems such as lipid nanoparticles. It is strategic alliances, mergers, and acquisitions as firms seek to either reinforce their RNA abilities or global accessibility. New biotech companies are also getting into the field with specialized technologies for rare and genetic diseases. The mRNA vaccine success has led to traditional pharma giants such as Pfizer, Sanofi, and Eli Lilly to bet billions on RNA-based pipelines.

XII. Porter's Five Forces Analysis & Strategic Framework

1. Threat of New Entrants: MODERATE-LOW

The barriers to entry in RNA therapeutics are formidable. Ionis controls a broad intellectual property estate of more than 1,600 issued patents worldwide that covers RNA-based drug discovery and development. The patent portfolio covers the use of antisense inhibitors as drugs, including chemistries, antisense inhibitor designs called "motifs," methods of use of antisense inhibitors, and mechanisms of action.

Beyond intellectual property, 35+ years of accumulated know-how in chemistry, delivery, and manufacturing create substantial barriers. Two decades after antisense oligonucleotides were initially identified as agents capable of modulating RNA processing and protein expression, progress translating these agents into the clinic has been hampered by inadequate target engagement, insufficient biological activity, and off-target toxic effects.

It took two decades for RNAi research to yield an approved drug as developers wrestled with delivery challenges. New entrants face similar learning curves.

2. Bargaining Power of Suppliers: LOW

Ionis has internalized most critical capabilities, including drug discovery, development, and increasingly manufacturing. The raw materials for oligonucleotide synthesis are available from multiple suppliers.

3. Bargaining Power of Buyers: MODERATE

For rare disease drugs, payers have limited alternatives and significant pressure to cover life-saving treatments. In the HAE space, Dawnzera enters a competitive landscape with several established treatments. Its pricing strategy aligns with competitors, ranging from approximately $345,000 to $690,000 per year. However, as more RNA therapeutics reach market for common conditions, buyer power will increase.

4. Threat of Substitutes: MODERATE

Gene therapy represents the most significant potential substitute—a single treatment that could cure rather than chronically manage genetic diseases. Spinraza's sales decline following Novartis's gene therapy Zolgensma illustrates this dynamic. However, gene therapies face their own challenges: extremely high upfront costs, manufacturing complexity, and uncertain long-term durability.

5. Competitive Rivalry: HIGH AND INCREASING

The intensity of competition in the RNA Therapeutics Market is very high due to the fast development of technologies and a soaring increase in the funds invested in R&D.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Ionis benefits from platform economics—each new drug candidate leverages the same chemistry, manufacturing, and regulatory expertise. However, scale economies in biotech differ from consumer businesses; clinical development remains expensive regardless of company size.

Network Effects: Limited direct network effects, though the company's extensive partnership network creates ecosystem value.

Cornered Resource: Ionis's most defensible position lies in its intellectual property estate and accumulated scientific knowledge. The tacit knowledge developed over 35 years of antisense research—understanding which targets are tractable, which chemistries work in which tissues, how to design clinical trials for RNA drugs—cannot easily be replicated.

Counter-Positioning: Ionis has historically focused on rare diseases where small patient populations deter larger competitors. This strategy is evolving as the company pursues larger indications like severe hypertriglyceridemia.

Switching Costs: For patients on chronic therapy, switching costs are significant—new titration, potential safety monitoring, and physician familiarity all create inertia.

Process Power: Ionis's systematic approach to drug discovery—validated chemistry platforms, established regulatory pathways, proven clinical development capabilities—represents genuine process advantages.

Branding: In the rare disease space, physician and patient advocacy relationships matter significantly. Ionis has built these over decades.

XIII. What to Watch: Key Performance Indicators

For investors tracking Ionis's evolution from partnership-dependent R&D company to integrated commercial entity, three KPIs matter most:

1. Product Revenue Growth (both wholly-owned and royalties)

This is the single most important metric as Ionis transitions to commercial-stage operations. Commercial revenues, which include sales of wholly owned drugs and royalties on partnered drugs, surged 53% year over year to $116 million during the quarter. This growth was primarily driven by Tryngolza product sales and Wainua royalties.

The breakdown between wholly-owned product revenue (TRYNGOLZA, DAWNZERA) and royalty revenue (Spinraza, Wainua, Qalsody) reveals the progress of the independence strategy. Higher wholly-owned revenue means more captured economics per dollar of sales.

2. Pipeline Progression Rate (Phase 3 starts and regulatory submissions)

Ionis's platform thesis depends on consistent conversion of discovery into clinical programs. The company expects Phase 3 trial start in first half of 2025 for ION582 for Angelman syndrome, Phase 3 data for zilganersen in Alexander disease, and Phase 2 data for ION464 in multiple system atrophy.

3. Cash Burn and Path to Profitability

Ionis has approximately $2B in cash and short-term investments per 2025 financial guidance, efficient capital structure and a strong history of disciplined capital management. With accelerating growth within reach, Ionis has a clear path to achieve sustained positive cash flow and is expected to reach cash flow breakeven in 2028.

XIV. Bull Case and Bear Case

The Bull Case

Platform Leverage: Ionis has demonstrated that its technology can address a wide range of diseases—from rare pediatric conditions to prevalent cardiovascular disorders. Each new successful drug validates the platform and creates optionality. Ionis' accelerating revenue growth opportunity is fueled by its recent launches and late-stage medicines that provide greater than $5B in potential annual peak revenue.

Independence Timing: The shift to independent commercialization comes at precisely the right moment—after establishing platform credibility through partnerships but before competition intensifies. Ionis captures more economics per drug at a time when it has the cash reserves and organizational capability to execute.

Pipeline Depth: Ionis has been at the forefront of discovering and developing leading neurological disease medicines, including SPINRAZA for spinal muscular atrophy, WAINUA for hereditary transthyretin-mediated amyloid polyneuropathy, and QALSODY for SOD1-ALS. The clinical-stage portfolio includes 13 therapies, of which eight are wholly owned by Ionis. Ionis' investigational portfolio includes medicines for which there are few or no disease modifying treatments, such as rare diseases including Angelman syndrome, Prion disease and Alexander disease and more common conditions such as Alzheimer's and Parkinson's.

Market Expansion: Early drugs focused on rare diseases with limited markets. Olezarsen's expansion into severe hypertriglyceridemia—affecting hundreds of thousands of patients—represents a much larger commercial opportunity. Last month, Ionis reported positive results from two phase III studies—CORE and CORE2—which evaluated Tryngolza for severe hypertriglyceridemia, which involves a much larger patient population. Both studies met their primary endpoint, with Tryngolza-treated participants showing a statistically significant reduction in triglyceride levels. Like FCS, Ionis also has a first-mover advantage in the sHTG indication.

The Bear Case

Competition Intensification: The RNA therapeutics space that Ionis pioneered is now crowded. For years, Alnylam has had the upper hand. Its first drug for people with transthyretin amyloidosis polyneuropathy, Onpattro, had a dominant market position compared to Ionis' rival Tegsedi. Alnylam also beat Ionis to market with a newer, more convenient version now sold as Amvuttra.

Execution Risk on Independence: Ionis has limited commercial infrastructure experience. The Akcea spinoff and reacquisition revealed the challenges of building sales and marketing capabilities. The company must now execute multiple simultaneous launches across different therapeutic areas.

Royalty Revenue Pressure: Spinraza, historically Ionis's largest revenue source, faces generic competition and market share loss to gene therapy alternatives. Ionis reported $216 million in Spinraza royalty revenue in 2024. This royalty stream may decline faster than new product revenue can replace it.

Clinical Risk: Despite platform validation, individual programs still fail. The Huntington's disease program with Roche was discontinued in 2021 after failing to demonstrate efficacy. Similar setbacks could materially impact the pipeline.

Financial Profile: The debt-to-equity ratio stands at 2.25, which may indicate a higher reliance on debt financing. Warning signs include an Altman Z-Score of 2.71, placing the company in the grey area of financial stress.

XV. Conclusion: The Next Chapter

Ionis Pharmaceuticals stands at a pivotal moment in its 35-year history. The company has achieved what many thought impossible: transforming antisense oligonucleotides from a scientific curiosity into a proven therapeutic modality with six marketed drugs and a deep pipeline.

The transition from R&D platform to integrated commercial company represents both the greatest opportunity and the greatest risk in Ionis's evolution. Success would validate a model where biotechnology companies can capture more of the value they create. Failure would suggest that the partnership model—letting pharmaceutical giants handle commercialization—remains the optimal structure.

"In less than nine months, we achieved two independent launches, marking significant progress toward our goal of transforming human health by bringing RNA-targeted medicines to people with serious diseases," said Brett P. Monia. "Our accelerating growth is driven by an industry-leading pipeline, with two more independent launches planned for 2026, four partner launches by the end of 2027."

Stanley Crooke's original insight—that a platform approach to drug discovery could systematically address diseases once thought undruggable—has been vindicated. The question now is whether the commercial execution can match the scientific achievement.

"The brilliance of Stan's vision isn't just represented by the founding and success of Ionis, but it is also reflected in his creation of an entirely new chemical class of medicines, antisense oligonucleotides," said Joseph Loscalzo, M.D., Ph.D., of Harvard Medical School. "His scientific contributions will no doubt continue to provide extraordinary benefit to the healthcare industry and the many patients who once were" unable to receive treatment.

For long-term investors, Ionis represents a bet on continued RNA medicine innovation, successful commercial execution, and the durability of intellectual property advantages in an increasingly competitive field. The scientific foundation is proven. The platform is validated. The pipeline is deep. The execution chapter is just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube