Almirall: From Spanish Pharmacy to European Dermatology Champion

I. Introduction: The Audacious Bet on Skin

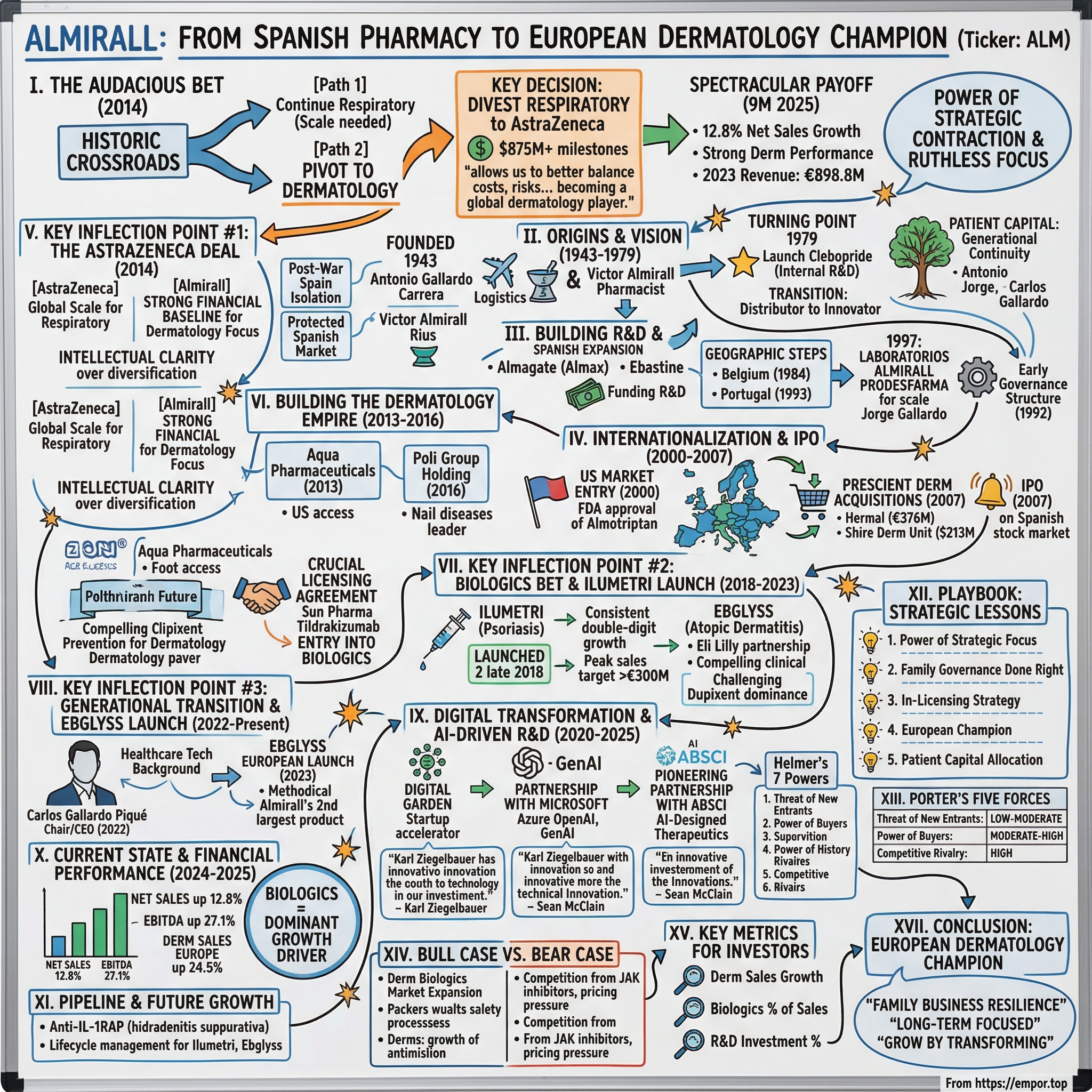

Picture Barcelona in the autumn of 2014. Inside the modernist headquarters near Tibidabo, Jorge Gallardo Ballart—second-generation scion of a pharmaceutical dynasty stretching back to the Franco era—faced the defining decision of his career. The company his father founded seventy years earlier stood at a crossroads: continue building respiratory assets that required the scale of pharmaceutical giants to commercialize globally, or make a counter-intuitive leap into dermatology, a specialty few in pharma then considered glamorous.

Jorge Gallardo made the call: Almirall would divest its entire respiratory franchise to AstraZeneca. In explaining the rationale, he stated that the deal "allows us to better balance the costs, risks and returns of the respiratory business while retaining an important economic interest in its future success. All this constitutes a very solid baseline to move more aggressively in specialty areas and particularly towards becoming a global dermatology player."

Today, that bet has paid off spectacularly. Almirall continues its sustained growth trajectory in 9M 2025, delivering 12.8% net sales growth, strong dermatology performance, solid commercial execution in Europe, and further pipeline progress. In 2023, the company generated total revenues of €898.8 million and was the leading European company in medical dermatology.

The Almirall story illuminates something rarely discussed in business school case studies: the power of strategic contraction. While most pharmaceutical executives chase scale through endless diversification, the Gallardo family did the opposite. They sold their most valuable asset to focus ruthlessly on a single therapeutic area. The results speak for themselves.

Given these dynamics, Almirall can reach increasing numbers of patients with the psoriasis and atopic dermatitis biologics, and therefore the potential peak sales of the biologics portfolio was recently updated to above €800 MM by 2030. What began as a post-war Spanish pharmacy has become Europe's preeminent pure-play dermatology company—a transformation spanning eight decades, three family generations, and one of the boldest strategic pivots in specialty pharma history.

This is a story of patient capital, generational continuity, and the courage to bet everything on a vision. It is also a story about what European pharmaceutical companies can achieve when they resist the temptation to become poor imitations of American giants and instead embrace focused excellence in specialty medicine.

II. Origins: The Gallardo Vision & Post-War Spain (1943-1979)

In the bombed-out aftermath of the Spanish Civil War, Barcelona in 1943 was hardly an obvious cradle for pharmaceutical innovation. Francisco Franco's autarkic economic policies meant Spain was isolated from international trade, its economy shattered, its scientific institutions decimated by exile and repression. Yet it was precisely these conditions that created opportunity for a young businessman named Antonio Gallardo Carrera.

Antonio Gallardo Carrera was born on June 20, 1908. He studied at the school of Commerce of Barcelona and later he joined the former Compagnie Aéropostale (currently, Air France). He worked for 25 years for the Compagnie Aéropostale as Regional Delegate. His position allowed him to foster relationships between France and Spain, receiving the highest French distinction, the Officer of the Legion of Honor.

It was an unconventional background for a pharmaceutical founder. Gallardo Carrera was not a chemist or physician—he was a logistics specialist who understood supply chains and international commerce at a time when Spain desperately needed both. Antonio Gallardo Carrera founded the pharmaceutical company Almirall in 1943, with the support of the pharmacist Victor Almirall Rius.

The partnership was elegant in its complementarity: Gallardo brought capital, commercial acumen, and international relationships; Almirall contributed the technical expertise and the name. The company began operations in 1944, initially focused on local manufacturing and distribution in the protected Spanish market—a necessity given the country's isolation from global pharmaceutical supply chains.

For three decades, Almirall operated as a quintessential family enterprise: profitable, conservative, growing slowly through the Spanish economic miracle of the 1960s. The turning point came in 1979, marking a transition from commercial operations to genuine innovation. In 1979, the company launched gastroprokinetic clebopride in Spain, the first product from the company's internal R&D team.

This milestone deserves emphasis. In an era when most Spanish pharmaceutical companies survived by licensing products from foreign multinationals, Almirall had built the capability to discover and develop its own molecules. The achievement represented years of patient investment in scientific infrastructure—investment that could easily have been distributed to shareholders but was instead reinvested in the business.

Over time, his sons, Antonio and Jorge Gallardo Ballart, joined the company and years later, after the passing of their father, took over the business and prepared the six members of the third generation to take up the reins. The succession was carefully planned. Antonio Gallardo Ballart was born on March 12, 1936. In 1952 he joined Almirall, at the age of 16 years, with a solid international education in Commerce. He held different executive positions at the Company such as Sales and Marketing Manager, being responsible for the launch of key products resulting from Almirall's research: Almax, Cleboril and Ebastel, as well as various licensed products.

What strikes the observer about the Gallardo family's approach is the long time horizons. Antonio Gallardo Carrera founded the company in his mid-thirties; his sons joined as teenagers and spent their entire careers building the enterprise. The family operated with multi-generational patience at a time when most businesses were optimizing for quarterly returns.

For investors, this early history establishes a crucial pattern: Almirall's competitive advantage has never been speed or scale but rather persistence and focus. The clebopride launch in 1979 came after more than a decade of R&D investment—an eternity by modern pharmaceutical timelines. This willingness to make long-duration bets without immediate payoff would prove essential to everything that followed.

III. Building R&D Capabilities & Spanish Expansion (1980s-1997)

The 1980s transformed Almirall from a regional distributor into a genuine innovator. Spain's transition to democracy and its 1986 accession to the European Economic Community opened new markets while intensifying competition. The company responded not by retreating to protected niches but by doubling down on proprietary drug development.

In 1984, the business launched antacid product, almagate, in Spain, as well as anti-inflammatory piketoprofen in 1985 and antihistamine ebastine and cinitapride in 1985. The product cadence reflected a company that had cracked the code of pharmaceutical development—rare for a European mid-cap at the time.

Almagate, marketed as Almax, deserves particular attention. The antacid became a commercial success in Spain, generating the cash flows that would fund subsequent R&D investments. More importantly, it established Almirall's credibility with Spanish physicians and pharmacists. The company was no longer merely distributing foreign products; it was creating medicines that patients and doctors trusted.

In the same year, Almirall opened its first subsidiary, based in Belgium. The international expansion was modest but symbolically significant. Belgium's position as a gateway to European markets made it a logical first step beyond Iberia. In 1992 the company launched aceclofenac and a year later opened its second foreign subsidiary, in Portugal.

The pattern was methodical: develop products domestically, prove their commercial viability, then expand geographically through carefully selected subsidiaries. There were no acquisition sprees or aggressive international campaigns. Each step built on the previous one, creating organizational capabilities before testing them in new markets.

After his father's passing in 1988, he and his brother, Jorge, took the reins of the business, fostering the modernization and internationalization of the Company. The generational transition coincided with Spain's deeper European integration, creating both opportunity and competitive pressure.

The culmination of this era came in 1997. In 1997 came the creation of Laboratorios Almirall Prodesfarma S.A., as a result of the merger between the Grupo Pharmaceutics Almirall, S.A. and the Grupo Prodesfarma. The merger created scale in the Spanish market while maintaining the family's controlling interest. Jorge Gallardo assumed the roles of Chairman and CEO, consolidating leadership for the internationalization push to come.

In 1992 Jorge and Antonio started the development of the Family Governance structure, which achieved the transition to the Third Generation in 2022. This early attention to governance is striking. While many family enterprises defer succession planning until crisis forces the issue, the Gallardo brothers began systematizing governance three decades before the next transition would occur.

The 1980s and 1990s thus established the institutional foundations that would support Almirall's later transformation. The company emerged with proprietary products, international capabilities, consolidated ownership, and—critically—a culture of patient investment in R&D. These were the assets that would enable the strategic pivot to dermatology.

IV. The Internationalization Era & IPO (2000-2007)

The new millennium arrived with Almirall poised to make its most ambitious leap yet: breaking into the American market. In 2000 the FDA approved anti-migraine agent almotriptan. The regulatory milestone opened the world's largest pharmaceutical market to Almirall products for the first time.

A year later the company opened its Mexican subsidiary as well as acquiring its French affiliate. Beginning in 2002, Almirall opened a series of European based subsidiaries; Italy (2002), Germany (2003), Austria, Poland, the United Kingdom, Ireland and Switzerland (2008), Nordic Countries (2010) and Netherlands (2013).

The subsidiary expansion reflected a deliberate strategy: build direct commercial capabilities in key markets rather than relying on licensing partners. Each new affiliate required management attention, capital investment, and local expertise. But the approach allowed Almirall to capture full economic value from its products while learning how to operate in diverse regulatory and commercial environments.

In 2005, Almirall made a prescient acquisition that hinted at its dermatological future. In 2005 the business acquired the commercial rights for Sativex in Europe for the treatment of spasticity associated to multiple sclerosis. While Sativex was a neurological product, the transaction demonstrated Almirall's emerging capabilities in specialty medicine commercialization.

In 2006, the company opened its new R&D Centre based in Sant Feliu de Llobregat as well as the acquisition of the Centre of Excellence for Inhalation Technology. The Sant Feliu facility, spanning 22,000 square meters, was inaugurated as the largest pharmaceutical laboratory in Spain—a physical manifestation of Almirall's R&D ambitions.

The respiratory strategy was in full swing. Almirall had developed aclidinium bromide, a novel muscarinic antagonist for COPD, using a proprietary dry powder inhaler platform called Genuair. The asset would become central to the company's respiratory franchise—and later, to the transformational deal with AstraZeneca.

Then came the IPO. Almirall, S.A. completed its initial public offering (IPO) on June 20, 2007. In 2007, the company floated on the Spanish stock market, as well as acquiring European dermatology specialist, Hermal. The company also acquired a portfolio of eight products from Shire plc.

The timing was ambitious. Spanish equity markets were near cyclical highs, and the pharmaceutical sector commanded premium valuations. The IPO provided capital for the aggressive acquisition strategy that followed while maintaining the Gallardo family's controlling stake.

Two paneuropean acquisitions after IPO in 2007, four new affiliates created in 2008. The company emerged from its first year as a public company with expanded geographic reach and—crucially—its first significant dermatology assets through the Hermal acquisition.

The Hermal deal deserves particular attention. The German company specialized in topical dermatology products, giving Almirall immediate capabilities and credibility in a therapeutic area it would later make its singular focus. The acquisition of Hermal GmbH (€376M) and a the Dermatology Business Unit from Shire Pharmaceuticals ($213M) were significant transactions that laid the groundwork for what would become Almirall's defining strategic direction.

By 2007, Almirall had transformed from a Spanish pharmaceutical company into a pan-European player with meaningful positions in respiratory and dermatology. The company was generating over €800 million in annual revenue, investing heavily in R&D, and pursuing partnerships with global pharmaceutical giants. The stage was set for the defining chapter.

V. KEY INFLECTION POINT #1: The AstraZeneca Deal & Strategic Pivot (2014)

Every company has moments where decisions compound for decades. For Almirall, that moment arrived on July 30, 2014.

AstraZeneca today announced that it has entered an agreement to transfer to the company the rights to Almirall's respiratory franchise for an initial consideration of $875 million on completion, and up to $1.22 billion in development, launch, and sales-related milestones.

Following the completion of the transaction, AstraZeneca will pay Almirall approximately $875 million of initial consideration, subject to adjustment for working capital, and up to $1.22 billion in development, launch and sales-related milestones.

The decision was counterintuitive to the point of appearing reckless. Almirall was selling its most valuable asset—a respiratory franchise that included the recently launched Eklira Genuair and multiple late-stage pipeline assets—to pursue a therapeutic area where it had relatively modest presence. The respiratory business was generating meaningful revenue with blockbuster potential. Why abandon it?

The answer lies in understanding competitive dynamics and capital requirements in respiratory medicine. By 2014, the COPD and asthma markets were dominated by pharmaceutical giants: GlaxoSmithKline, AstraZeneca, Boehringer Ingelheim. Competing required not just excellent science but massive commercial infrastructure spanning dozens of countries, sophisticated relationships with pulmonologists, and marketing budgets in the hundreds of millions.

Jorge Gallardo, President of Almirall said: "This global collaboration will allow us to maximize the potential value of our exciting respiratory franchise and AstraZeneca is the perfect partner to do this. Moreover, the deal has given us a strong financial baseline to accelerate our strategy and to start focusing our resources in becoming a top Dermatology global player with an additional interest in other specialist driven areas."

The strategic logic was sophisticated: Almirall lacked the scale to commercialize respiratory assets globally, but it could capture full value by selling those assets to a company that possessed such scale, while retaining milestone and royalty participation. The proceeds would then fund a more focused strategy where Almirall's size was an advantage rather than a liability.

AstraZeneca today announced that it has completed the strategic transaction to transfer the rights to Almirall's respiratory franchise to the company. Almirall today announced that, effective November 1st, it has completed the transaction to transfer to AstraZeneca the rights of Almirall's respiratory franchise after all closing conditions have been satisfied.

The transaction closed on schedule, and Almirall suddenly possessed a war chest and a mandate. The company had explicitly committed to becoming "a top global Dermatology player"—a declaration that would guide every subsequent strategic decision.

What makes this transaction remarkable is not just the financial terms but the intellectual clarity it represented. Most pharmaceutical executives respond to competitive pressure by seeking diversification: if one therapeutic area is challenging, expand into others. The Gallardo family chose the opposite path. They diagnosed their competitive disadvantage as excessive diversification and corrected it through radical focus.

For investors, the AstraZeneca deal illustrates a profound truth about capital allocation: sometimes the highest-return use of assets is selling them to someone better positioned to maximize their value. The $875 million upfront payment, properly reinvested, would generate far better returns in dermatology than the respiratory assets would have generated under Almirall's constrained capabilities.

VI. Building the Dermatology Empire: The Acquisition Spree (2013-2016)

With cash on hand and strategic clarity established, Almirall embarked on the most aggressive acquisition campaign in its history. The goal was specific: build scale in medical dermatology through targeted acquisitions that added either geographic reach, therapeutic capabilities, or pipeline assets.

Almirall began a concentrated focus on medical dermatology in 2013, following the acquisition of another specialist dermatology company, Aqua Pharmaceuticals.

The transaction implies a cash acquisition of 100% of Aqua Pharmaceuticals for an upfront of $305m plus potential additional earn outs of up to $75m. Provides additional geographic and business diversification and gives access to the largest dermatology market globally.

The Aqua deal marked Almirall's entry into the American dermatology market. With its nation-wide infrastructure and experienced management team, it is dedicated to marketing high-quality products. For the calendar year 2013, the company was expected to report sales of $127 million. Aqua brought established relationships with American dermatologists and a portfolio of topical products spanning acne, steroid-responsive dermatoses, and actinic keratosis.

Then came the decisive year. In 2014 Almirall divested its rights to its respiratory franchise to Astrazeneca focussing on dermatology, later in 2015 declaring its strategic intention to become a leading pharmaceutical company in the field of dermatology and continuing with its expansion by acquiring Poli Group Holding and ThermiGen LLC in 2016.

Spanish pharmaceutical firm Almirall has agreed to acquire 100% of the share capital of Poli Group Holding for €365m, boosting its presence in dermatology. Founded in Italy in 1946 by Dr. Piero Poli, Poli Group is an international niche pharmaceutical company that develops registers and sells mainly proprietary products. With a portfolio of 8 marketed products, Dermatology is the key focus area of the company, being the world leader in nail diseases and treating disorders such as onychomicosis, nail psoriasis and nail dystrophies, skin mycosis, rosacea and acne, among others.

This acquisition is the next step in the strategic evolution of Almirall, moving further into a Specialty Pharma model focused on Dermatology. Through the acquisition Almirall will: Grow its revenues in the Dermatology market globally. Expand its existing Dermatology portfolio with recognized and growing international brands for nail psoriasis and onychomycosis treatment.

Jorge Gallardo, President of Almirall, commented: "This important transaction is the result of our continued focus on growing our presence in the global Dermatology market. The products of Poli Group will provide Almirall with leading market positions in key geographies in which we want to increase our footprint."

But the most consequential strategic move of this period was not an acquisition—it was a licensing agreement that would define Almirall's future. In 2016 Almirall and Sun Pharmaceutical Industries Ltd. sign a licensing agreement for the development and commercialization of tildrakizumab within Europe, a novel biologic treatment for patients with moderate-to-severe plaque psoriasis.

Under terms of the license agreement, Almirall will pay Sun Pharma an initial upfront payment of US $50 million. "This agreement with Sun Pharma allows us to add a novel biologic for treatment of psoriasis to our extensive dermatology portfolio," said Jorge Gallardo, President of Almirall. "This is an exciting time for the treatment of psoriasis, a disease which can take both a physical and emotional toll on patients' lives. Emerging new investigational drugs, like tildrakizumab, are increasingly targeted and will potentially offer patients and physicians another alternative."

The tildrakizumab agreement marked Almirall's entry into biologics—the most innovative and fastest-growing segment of dermatology therapeutics. Rather than attempt to build biologic capabilities de novo, Almirall licensed a late-stage asset from a partner that had already invested in development. The approach was capital-efficient and risk-aware: pay for proven clinical results rather than speculative early-stage science.

By the end of 2016, Almirall had assembled the pieces for its dermatology empire: American commercial infrastructure through Aqua, European branded products through Poli Group, a proprietary dermatology R&D center in Reinbek (inherited from Hermal), and—crucially—a path to biologics through the Sun Pharma partnership. The transformation from diversified pharmaceutical company to focused dermatology specialist was essentially complete.

VII. KEY INFLECTION POINT #2: The Biologics Bet & Ilumetri Launch (2018-2023)

The biologic revolution transformed dermatology from a backwater of pharmaceutical innovation into one of the industry's fastest-growing therapeutic areas. For decades, dermatologists had limited options for severe skin diseases: topical steroids with side effect concerns, systemic immunosuppressants borrowed from transplant medicine, or the older TNF-alpha inhibitors. The arrival of targeted biologics changed everything.

Tildrakizumab, sold under the brand name Ilumya among others, is a monoclonal antibody designed for the treatment of immunologically mediated inflammatory disorders. It is approved for the treatment of adults with moderate-to-severe plaque psoriasis in the United States and in the European Union. Tildrakizumab was designed to block interleukin-23 (IL-23), a cytokine that plays a key role in managing the immune system and autoimmune disease. Tildrakizumab was approved by the Food and Drug Administration in March 2018, and the European Medicines Agency in September 2018, for the treatment of moderate-to-severe plaque psoriasis in adults who are candidates for systemic therapy.

Almirall launched tildrakizumab in Europe as Ilumetri in late 2018. The product targeted a specific segment of the psoriasis market: patients who had failed traditional therapies but were seeking alternatives to the dominant TNF-alpha biologics. Since its 2018 European launch, Ilumetri has consistently delivered double-digit growth and is on track for peak sales exceeding €300 million.

Ilumetri®, for the treatment of psoriasis, grew steadily in 9M 2025, with net sales increasing 12% YoY, to a total of €170.9 MM and remaining on track to meet the €300 MM peak sales target. Anti-IL 23 antibodies remain the leading class in advanced psoriasis treatment, where Ilumetri® is well positioned to further substantiate its market position.

The Ilumetri success validated Almirall's in-licensing model. But the company wasn't resting on a single product. In parallel, Almirall was working with Eli Lilly on an even more significant opportunity: lebrikizumab for atopic dermatitis.

Almirall has the exclusive rights to develop and commercialize lebrikizumab for the treatment of dermatology indications, including eczema, in Europe. Almirall's partner Lilly has the rights for development and commercialization of this biologic in the U.S. and the rest of the world outside Europe.

Lebrikizumab is a monoclonal antibody that selectively targets and neutralizes IL-13 with high binding affinity and a slow dissociation rate. It binds to the IL-13 cytokine at an area that overlaps with the binding site of the IL-4Rα subunit of the IL-13Rα1/IL-4Rα heterodimer, preventing formation of this receptor complex and inhibiting IL-13 signaling.

More than 80 percent of adults and adolescents with moderate-to-severe atopic dermatitis who responded to lebrikizumab treatment at Week 16 in the ADvocate 1 and 2 monotherapy trials and continued treatment for up to three years experienced sustained skin clearance with monthly maintenance dosing.

The clinical profile was compelling. Lebrikizumab offered monthly maintenance dosing—a potential differentiation versus competitors requiring more frequent injections—combined with strong efficacy data. With the atopic dermatitis market emerging as a major field for advanced therapies, it is expected to grow through products with new mechanisms of action. It is anticipated that the atopic dermatitis market will mirror the trajectory seen in the psoriasis market in recent years.

The European Commission approved Ebglyss (lebrikizumab) in 2023, launching Almirall into one of dermatology's most competitive and potentially lucrative markets. The timing was strategic: the atopic dermatitis biologic market was expanding rapidly, but Sanofi/Regeneron's Dupixent had established near-monopolistic dominance.

One of those targeted agents that has taken the market by storm is Regeneron and Sanofi's jointly developed Dupixent (dupilumab), first approved in the US in 2017. The blockbuster monoclonal antibody has seen its sales increase year-over-year amid high uptake from AD – reaching $14.9bn in sales in 2024.

Almirall was entering a market dominated by a competitor with nearly $15 billion in annual sales. But the company had identified a defensible position: European market focus with differentiated dosing convenience.

VIII. KEY INFLECTION POINT #3: Generational Transition & Ebglyss Launch (2022-Present)

Every family business faces the succession question. How do you transfer leadership across generations without destroying the enterprise? How do you balance family continuity with professional excellence? The Gallardo family had been preparing for this moment for thirty years.

In May 2022, a new generational change took place within the founding family, with the replacement of Jorge Gallardo Ballart by his son Carlos Gallardo Piqué at the head of the non-executive presidency of the company. Six months later, Carlos Gallardo also assumed the executive management.

An Almirall and healthcare industry veteran for more than 20 years, with experience in sales, licensing, M&A and international operations. I was elected Chair of the Board of Directors in May 2022 and become CEO in November 2022.

Before joining the pharmaceutical industry, I worked as an engineer in the automotive industry in logistics and supply chain. I hold a MS in industrial engineering from the Universitat Politècnica de Catalunya and an MBA from Stanford Graduate School of Business.

Carlos Gallardo is the Chief Executive Officer (CEO) of Almirall, a global biopharmaceutical company specializing in medical dermatology. He has been with Almirall since 2004 and has held various leadership roles, including Chairman of the Board of Directors. Gallardo's extensive experience in the pharmaceutical industry spans over 20 years, beginning with his tenure at Pfizer in New York.

The succession was deliberately graduated. Carlos first assumed the non-executive chairman role, allowing him to understand board-level governance before taking operational responsibility. In November 2022, he was appointed interim CEO and in light of the very positive evolution and performance, in February 2023 he was appointed CEO. Additionally, Carlos has established a successful career in innovative healthcare technology.

The governance philosophy Jorge Gallardo instilled is instructive for any family enterprise: "At a family business, it is more important to ensure governance than to maintain full ownership," explained Jorge Gallardo. In Gallardo's view, the key to the success of this pharmaceutical company, which has been publicly listed since 2007, is "the professionalisation of the family." "Our board has a high proportion of independent directors, many of them international. Only those family members who add value are allowed to sit on it."

"Our business model is based on internal research and development and access to new products from other international companies," he explained. "This allows us to operate in more than 70 countries through 13 affiliates and a strategic partnership network."

Carlos took the helm at a pivotal moment: Ebglyss was launching across Europe, Ilumetri continued its growth trajectory, and the company needed to execute flawlessly on its biologics commercial strategy.

Ebglyss (lebrikizumab), its flagship atopic dermatitis biologic, delivered €25 million in Q2 sales—a 31% quarter-over-quarter increase—and became the company's second-largest product just 18 months post-launch. Cumulative sales reached €79 million by H1 2025, with reimbursement secured in 14 European countries, including France (added in April 2025).

Including the launches in Q1 2025, Ebglyss is now available in 13 markets (Germany, Norway, UK, Spain, Denmark, Czechia, The Netherlands, Italy, Austria, Belgium, Sweden, Switzerland, and France in Q1) and the launch plans are on track with availability in all countries per plan expected to be achieved by end of 2025 (Portugal, Ireland, and Poland).

The launch execution has been methodical: secure reimbursement, build dermatologist awareness, expand country by country. Ebglyss®, for the treatment of moderate to severe atopic dermatitis, generated €75.5 MM of sales during 9M 2025 – representing more than a 3x increase YoY, as European markets are ramping up after launch. Performance continues to be primarily driven by the biologics portfolio, with Ilumetri® net sales increasing 12.1% YoY (total of €170.9 MM), and Ebglyss® net sales of €75.5 MM – reflecting a more than 3x increase YoY as European markets are ramping up after launch.

The third-generation leadership has inherited an organization in growth mode. But Carlos Gallardo also brought fresh perspectives from his healthcare technology investments. I'm also a Board Member of the European Federation of Pharmaceutical Industries and Associations (EFPIA) and a Member of IFPMA's Biopharmaceutical CEOs Roundtable (BCR). In 2014 I founded CG Health Ventures to invest in and support early-stage technology enabled healthcare companies globally.

Carlos Gallardo, presidente y CEO de Almirall, ha sido elegido vicepresidente segundo de la Federación Europea de Asociaciones de la Industria Farmacéutica (EFPIA, por sus siglas en inglés), uniéndose al nuevo equipo de presidencia para el mandato de los próximos dos años.

The EFPIA leadership role positions Carlos Gallardo—and by extension Almirall—at the center of European pharmaceutical policy discussions. For a mid-cap company, this visibility is valuable for navigating the complex European reimbursement landscape.

IX. Digital Transformation & AI-Driven R&D (2020-2025)

Carlos Gallardo's background in healthcare technology proved immediately relevant. Under his leadership, Almirall accelerated digital initiatives that had been nascent under his father's tenure.

Almirall launched its dermatology digital health accelerator, Digital Garden, in 2020 to support startups that are focused on developing technology-based services and solutions for various dermatological diseases.

The Digital Garden, powered by Almirall, will allow startups focused on developing innovative technology-based services and solutions to play a relevant role in tackling dermatology challenges. Five start-ups have been chosen for the first cohort of this 9-month acceleration program to be based in the Barcelona Health Hub.

In less than two years, Almirall's digital accelerator program has graduated more than 70 employees and established partnerships with 10 startup companies. Wuttke established Almirall's digital accelerator program, or Digital Garden, in 2020.

Almirall has started to embrace digitalisation across many aspects of its business, including the development of digital therapeutics (DTx) such as Claro, an app designed to reduce anxiety and improve wellbeing in people with psoriasis.

The more significant digital bet came in 2024. Almirall has announced today a strategic collaboration with Microsoft aimed at advancing digitalization and technological innovation in the field. The 3-year partnership seeks to advance medical dermatology research, develop next-generation personalized drugs, and accelerate Almirall's overall digital transformation.

Under the agreement, Almirall and Microsoft Industry Solutions, in collaboration with select Microsoft partners, will establish a joint Digital Office. This initiative will capitalize on Almirall's unified data platform, employing generative artificial intelligence (genAI) and advanced analytics technologies to drive digital innovation in drug discovery and development.

"At Almirall, we believe that leading innovation is enabled by collaborating with experts and being at the forefront of science and technology," said Carlos Gallardo, CEO of Almirall. "This agreement with Microsoft is a significant advancement in our digital transformation to achieve our goal of delivering novel treatment options for patients. It will empower us to apply latest technologies to transform our ways of working, and accelerate drug discovery."

Almirall built a custom assistant, using Microsoft Azure OpenAI in Foundry Models, Azure AI Search, and Azure Databricks to help researchers quickly find answers across 400,000 documents in English, Spanish, and Catalan.

But the most ambitious AI initiative came through a pioneering partnership with Absci Corporation. Absci Corporation, a generative AI drug creation company, and Almirall S.A., a global biopharmaceutical company focused on medical dermatology, today announced a drug discovery partnership aimed to develop and commercialize AI-designed therapeutics to fight chronic and debilitating dermatological diseases. The partnership combines Absci's Integrated Drug Creation™ platform with Almirall's dermatological expertise with the goal of delivering life-changing medicines to patients.

The partnership represents Almirall's first de novo AI drug collaboration, and it comes only months after Absci announced it could design and validate de novo therapeutic antibodies using its 'zero-shot' generative AI.

Under the terms of the partnership, Absci will apply its de novo generative AI technology to create and commercialize therapeutic candidates for two dermatological targets. In addition to product royalties, Absci is eligible to receive up to approximately $650 million in upfront fees, R&D, and post-approval milestone payments across the two programs if all milestones are successfully completed.

The partnership yielded early validation. The expansion of the collaboration follows the successful delivery of AI-designed, functional antibody leads against a difficult-to-drug target—the first target addressed within the initial collaboration between Almirall and Absci.

"Using advanced AI capabilities to design therapeutic candidates against historically challenging disease targets is a highly promising approach and Absci´s de-novo AI platform capabilities have already demonstrated early success" said Dr. Karl Ziegelbauer, Chief Scientific Officer at Almirall.

"The progress in our collaboration is a testament that AI de novo drug design is a successful approach to unlock novel biology where traditional drug discovery approaches have failed," said Sean McClain, Founder and CEO of Absci.

The AI-driven R&D strategy reflects Almirall's broader approach: partner with technology leaders rather than attempt to build capabilities de novo. Just as Almirall licensed biologics from Sun Pharma and Eli Lilly rather than developing them internally, the company is accessing AI drug discovery capabilities through Absci rather than investing in its own AI infrastructure.

For investors, the digital initiatives demonstrate that third-generation leadership is not simply maintaining the status quo but actively positioning the company for the next wave of pharmaceutical innovation.

X. Current State & Financial Performance (2024-2025)

The financial results tell the story of a transformation reaching fruition.

Net Sales increased by 12.8% YoY to a total of €820.7 MM, EBITDA reached €180.7 MM (increase of 27.1% YoY) driven by incremental sales across the broad dermatology portfolio, and reduced SG&A in Q3, with a gross margin of 64,9%.

Dermatology sales in Europe continued to grow double digit – increasing 24.5% YoY to a total of €442.4 MM – demonstrating Almirall's leadership in medical dermatology and its relevance to patients and physicians.

Almirall is on track to meet its 2025 guidance of double-digit net sales growth of 10 – 13%, and total EBITDA between €220 MM and €240 MM.

Europe remains Almirall's core growth engine, with the dermatology segment accounting for 56.8% of total H1 2025 net sales.

Almirall delivers a strong start to 2025: growing Q1 overall sales by 15%, and 23.4% in its European Dermatology business YoY, aligned with the company's sustained growth trajectory. EBITDA increase of 35.0% YoY in line with expectations to a total of €70.9 MM driven by continued strong operational execution including out-licensing income realized in Q1 2025.

The biologics portfolio is becoming the dominant growth driver. Almirall's Q2 2025 results highlight 24.2% dermatology sales growth driven by biologics Ebglyss (€25M Q2) and Ilumetri (€58M Q2), now accounting for 70% of segment revenue.

R&D investment remains a priority. In the YTD Almirall invested 12.5% of Net Sales in R&D, representing a total of 102.4 MM. Almirall's long-term success is underpinned by its aggressive R&D investment, which rose 27% year-on-year in H1 2025 to €71.9 million (12.8% of net sales).

The balance sheet provides strategic flexibility. The company finished 2024 at 0.2x Net Debt to EBITDA—essentially no leverage—providing capacity for opportunistic acquisitions or accelerated R&D investment without dilution.

The broader dermatology portfolio continues to perform. In 9M 2025 Wynzora® grew 32.3% YoY to a total of €25.4 MM, and Klisyri® grew 22.6% YoY to a total of €20.1 MM.

The company has achieved what few mid-cap pharmaceutical companies manage: sustained double-digit growth driven by differentiated products in a focused therapeutic area. The strategic pivot that began with the AstraZeneca deal a decade ago has delivered compounding returns.

XI. The Pipeline & Future Growth Catalysts

The current product portfolio drives near-term results, but the pipeline determines long-term value.

Major achievements in Q3 2025 include the approval of Efinaconazole in Germany, and the advancement of our developmental asset LAD191 (Anti-IL-RAP mAb) to phase II. Additional pipeline programs are expected to progress into phase II PoC studies in the next 9 to 12 months including an IL-2muFc fusion protein targeting Alopecia areata, and an anti-IL-21 monoclonal antibody.

The company's pipeline includes: Anti-IL-1RAP monoclonal antibody completed Phase I trials with favorable safety data, now advancing to Phase II for hidradenitis suppurativa, a high-unmet-need indication.

Hidradenitis suppurativa represents a significant commercial opportunity. The chronic inflammatory skin condition affects millions globally, causes severe quality-of-life impairment, and has limited treatment options. Success in Phase II trials could position Almirall to capture meaningful share in an underserved market.

Collaborations with Simcere and Sun Pharma expanding access to Chinese R&D capabilities and lifecycle management for key products.

The established biologics also have pipeline value through lifecycle management. Sun Pharma is running two Phase III studies to assess the efficacy and safety of tildrakizumab in patients suffering from psoriatic arthritis. First results are expected in the second half of 2025.

Almirall, together with its collaborator Eli Lilly, are running a comprehensive program of clinical trials with the aim of further expanding the indications for Lebrikizumab. This includes a Phase III study run by Lilly which explores its safety and efficacy in patients from 6 months to under 18 years to make the benefits of lebrikizumab accessible to the pediatric population.

Expanding existing biologics into new indications represents lower-risk pipeline value: the molecules are already approved with established safety profiles, so incremental indications primarily require demonstrating efficacy in new patient populations.

Several ongoing clinical studies supporting Ebglyss® and Ilumetri® will increase the body of evidence for these important biologics. These lifecycle management activities are aimed at enabling more patients to get access to the benefits of these advanced treatments.

XII. Playbook: Business & Strategic Lessons

The Almirall story yields several lessons applicable beyond pharmaceutical investing.

Lesson 1: The Power of Strategic Focus

Almirall's decision to sell its respiratory franchise appears counterintuitive until you understand competitive positioning. In respiratory medicine, the company faced giants with vastly superior commercial capabilities. In dermatology, Almirall's size became an advantage: nimble enough to focus exclusively on skin disease while large enough to achieve meaningful commercial scale. The lesson: sometimes selling your best asset to buy focus is the highest-return strategy.

Lesson 2: Family Governance Done Right

"At a family business, it is more important to ensure governance than to maintain full ownership." The Gallardo family maintained control while professionalizing operations. Independent board directors brought outside perspective; family members earned their positions rather than inheriting them by right. The 30-year succession planning process ensured generational transitions occurred smoothly.

Lesson 3: In-Licensing as Competitive Strategy

Rather than attempt to build biologic R&D capabilities from scratch—an endeavor requiring billions in investment with uncertain outcomes—Almirall licensed late-stage assets from partners. The approach is capital-efficient, risk-aware, and allows the company to focus its internal capabilities on what it does best: European commercial execution in dermatology.

Lesson 4: European Champion Strategy

Almirall has deliberately concentrated on European market leadership rather than pursuing global scale. The strategy acknowledges that European reimbursement systems favor companies with deep local relationships, regulatory expertise, and established presence. Rather than compete as a small player in the U.S. market, Almirall dominates its home turf.

Lesson 5: Patient Capital Allocation

The AstraZeneca proceeds could have funded dividends or share repurchases. Instead, Almirall reinvested in acquisitions and R&D. The 10+ year time horizon between strategic decision (selling respiratory) and full payoff (biologics reaching scale) would test most public company shareholders. Family control enabled long-term thinking.

XIII. Porter's Five Forces Analysis

Threat of New Entrants: LOW-MODERATE

High barriers protect established players in medical dermatology. Regulatory approval processes (FDA, EMA) require years of clinical trials and hundreds of millions in investment. Established relationships with dermatologists create switching costs. However, biotech startups with novel biologics can disrupt incumbent positions, as demonstrated by the rapid adoption of IL-23 inhibitors in psoriasis.

Almirall's R&D investment of 12-13% of revenue represents a meaningful barrier. The R&D centre in Sant Feliu de Llobregat (Barcelona), houses the departments involved in all stages of R&D, as well as the development of new chemical entities. The Reinbek Centre of Excellence for Dermatology specializes in the development of new formulas for the treatment of skin diseases.

Bargaining Power of Suppliers: LOW

The company also has three production centres: two in Spain, the pharmaceutical plant in Sant Andreu de la Barca (Barcelona) and the pharmaceutical and chemical plant in Sant Celoni (Barcelona); and a pharmaceutical plant in Germany (Reinbek).

Vertical integration in manufacturing reduces dependence on external suppliers. Multiple potential API suppliers globally provide sourcing flexibility.

Bargaining Power of Buyers: MODERATE-HIGH

European healthcare systems negotiate aggressively on pharmaceutical pricing. National reimbursement decisions determine market access in key countries. While Almirall faces competition from giants like Sanofi/Regeneron (Dupixent) and Pfizer (Cibinqo) in atopic dermatitis, its strategic focus on therapeutic differentiation and commercial execution provides a buffer.

Dermatologists have multiple treatment options for psoriasis and atopic dermatitis, creating competitive pressure on pricing and positioning.

Threat of Substitutes: MODERATE

Generics threaten older topical treatments as patents expire. However, biologics enjoy longer exclusivity periods and are difficult to replicate as biosimilars. However, Dupixent now faces competition from JAK inhibitors like abrocitinib (Cibinqo), and upadacitinib (Rinvoq), as well as biologics like tralokinumab (Adbry/Adtralza).

JAK inhibitors represent the most significant substitution threat: oral medications that compete with injectable biologics by offering convenience advantages.

Competitive Rivalry: HIGH

Regeneron and Sanofi's blockbuster Dupixent has transformed the atopic dermatitis market. The global atopic dermatitis (AD) market is poised to reach $22.4bn in drug sales within the decade, buoyed by the availability of targeted therapies.

Almirall competes against pharmaceutical giants with vastly greater resources. The blockbuster monoclonal antibody has seen its sales increase year-over-year amid high uptake from AD – reaching $14.9bn in sales in 2024. Ebglyss must compete for market share against an entrenched incumbent with near-$15 billion in annual sales.

Hamilton Helmer's 7 Powers Assessment

Counter-Positioning: Almirall's pure-play dermatology focus creates counter-positioning versus diversified pharmaceutical companies that cannot justify the same intensity of attention to skin disease.

Scale Economies: Limited due to company size, but present in European commercial operations where fixed costs (sales force, regulatory affairs) spread across larger revenue base.

Switching Costs: Moderate for prescribing physicians who build familiarity with specific biologics. Patient switching costs are higher once stabilized on effective therapy.

Network Effects: Minimal in pharmaceutical commercialization.

Process Power: Deep dermatology expertise accumulated over decades creates process advantages in clinical development and commercial execution.

Branding: Strong brand recognition among European dermatologists through decades of focused presence and investment in medical education.

Cornered Resource: European commercial rights to lebrikizumab (via Eli Lilly partnership) and tildrakizumab (via Sun Pharma) represent valuable resources secured through early partnership commitment.

XIV. Bull Case vs. Bear Case

The Bull Case

The dermatology biologics market continues rapid expansion as diagnosis rates increase and patients move to advanced therapies. A 2025 report published by GlobalData forecasts sector sales will reach the $22.4bn figure by 2033, up from $8.5bn in 2023, reflecting a compound annual growth rate (CAGR) of 10.2%.

Ebglyss captures meaningful European market share as reimbursement expands. Monthly dosing convenience differentiates versus competitors. Almirall's deep dermatologist relationships—cultivated over decades—drive prescription share.

The potential peak sales of the biologics portfolio was recently updated to above €800 MM by 2030. If achieved, biologics alone would nearly double current company revenue.

Pipeline assets advance successfully: the anti-IL-1RAP antibody shows efficacy in hidradenitis suppurativa; lifecycle management expands Ilumetri into psoriatic arthritis; pediatric lebrikizumab approval unlocks new patient populations.

AI partnerships with Absci and Microsoft accelerate drug discovery, compressing timelines and reducing costs. First AI-designed candidates enter clinical development.

The company maintains capital discipline, uses cash flows to fund R&D expansion, and potentially pursues tuck-in acquisitions that enhance the dermatology portfolio.

The Bear Case

Ebglyss struggles to gain share against entrenched Dupixent. European reimbursement negotiations prove difficult as healthcare systems pressure biologic pricing. Almirall faces competition from giants like Sanofi/Regeneron (Dupixent) and Pfizer (Cibinqo) in atopic dermatitis.

JAK inhibitors erode biologic market share by offering oral convenience. Patients and physicians prefer pills to injections, and safety concerns that initially limited JAK inhibitor adoption prove manageable.

Pipeline setbacks occur: Phase II trials fail to demonstrate efficacy; development partners terminate agreements; AI drug discovery partnerships fail to produce viable candidates.

European pharmaceutical pricing pressure intensifies. Healthcare systems demand deeper discounts on biologics, compressing margins across the industry.

Family governance creates complications: third-generation leadership proves less capable than predecessors; family shareholders demand distributions rather than reinvestment; succession to the fourth generation (currently 19 family members) becomes contentious.

Currency fluctuations disadvantage a European-focused company as dollar-denominated competitors gain pricing flexibility.

XV. Key Metrics for Investors

For long-term fundamental investors tracking Almirall, three KPIs deserve particular attention:

1. European Dermatology Sales Growth Rate

This metric captures the core of Almirall's strategy. Sustained double-digit growth indicates successful execution of the biologics launch and maintenance of portfolio strength. Deceleration would signal competitive pressure or reimbursement challenges. Current trajectory: 24.5% YoY growth in 9M 2025.

2. Biologics Revenue as Percentage of Total Sales

The shift from legacy products to biologics drives margin expansion and competitive positioning. As biologics approach 70% of dermatology segment revenue, Almirall becomes increasingly differentiated versus topical/generic competitors. Track quarterly progression toward the €800M+ peak sales target.

3. R&D Investment as Percentage of Sales

Almirall's sustained 12-13% R&D investment ratio signals commitment to innovation. Significant reductions would suggest management prioritizing near-term profitability over long-term competitive position. Increases toward 15%+ would indicate accelerating pipeline investment—potentially value-creating if Phase II assets advance successfully.

XVI. Regulatory & Legal Considerations

European pharmaceutical pricing remains the most significant regulatory overhang. Healthcare systems across the EU face budget pressures that translate into aggressive negotiations with biologic manufacturers. France's recent reimbursement approval for Ebglyss was a positive signal, but each country requires separate negotiation.

The EU Pharmaceutical Strategy adopted in 2020 explicitly seeks to improve access while ensuring affordability. For innovative manufacturers like Almirall, this creates tension: incentives for innovation must coexist with pricing restraint.

No material legal overhangs appear in public disclosures. The company operates in a heavily regulated industry with standard pharmaceutical litigation risks, but no unusual exposures are apparent.

Accounting considerations are standard for pharmaceutical companies: revenue recognition timing around product launches, contingent milestone obligations to licensing partners, and intangible asset amortization from acquisitions all require monitoring but present no unusual concerns.

XVII. Conclusion: The European Dermatology Champion

Almirall's journey from a post-war Spanish pharmacy to Europe's leading pure-play dermatology company spans eight decades and three family generations. The story illuminates what patient capital, strategic focus, and disciplined execution can achieve when aligned across generational time horizons.

The 2014 AstraZeneca deal represents the pivotal moment: selling crown jewels to fund a focused strategy that most observers found questionable. A decade later, the results validate the decision. Almirall commands European leadership in medical dermatology, operates a portfolio of innovative biologics, and generates double-digit growth with strong profitability.

"We are a family business, which makes us more resilient and more focused on the long term. Our system is based on proximity and is key to attracting talent."

The third-generation leadership under Carlos Gallardo maintains the family's commitment to focused excellence while adding capabilities in digital health and AI-driven drug discovery. The succession appears well-executed, governance structures are robust, and strategy remains coherent.

Challenges persist. Competing against Sanofi/Regeneron's Dupixent requires flawless commercial execution. European pricing pressure constrains margins. Pipeline assets face the usual clinical development risks.

But the fundamental investment thesis is clear: Almirall offers exposure to the high-growth medical dermatology market through a focused, well-managed, family-controlled enterprise with proven capital allocation discipline.

For investors seeking European pharmaceutical exposure beyond the mega-caps, Almirall represents a differentiated opportunity. The company demonstrates that mid-size specialty pharma can not only survive but thrive—by knowing exactly what it wants to be and executing relentlessly against that vision.

As Jorge Gallardo once observed, the pharmaceutical industry offers three paths: disappear, survive, or grow by transforming the environment to get stronger. Almirall chose transformation. The results speak for themselves.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube