Ascendis Pharma: Platform Innovation in Rare Disease

I. Introduction & Episode Roadmap

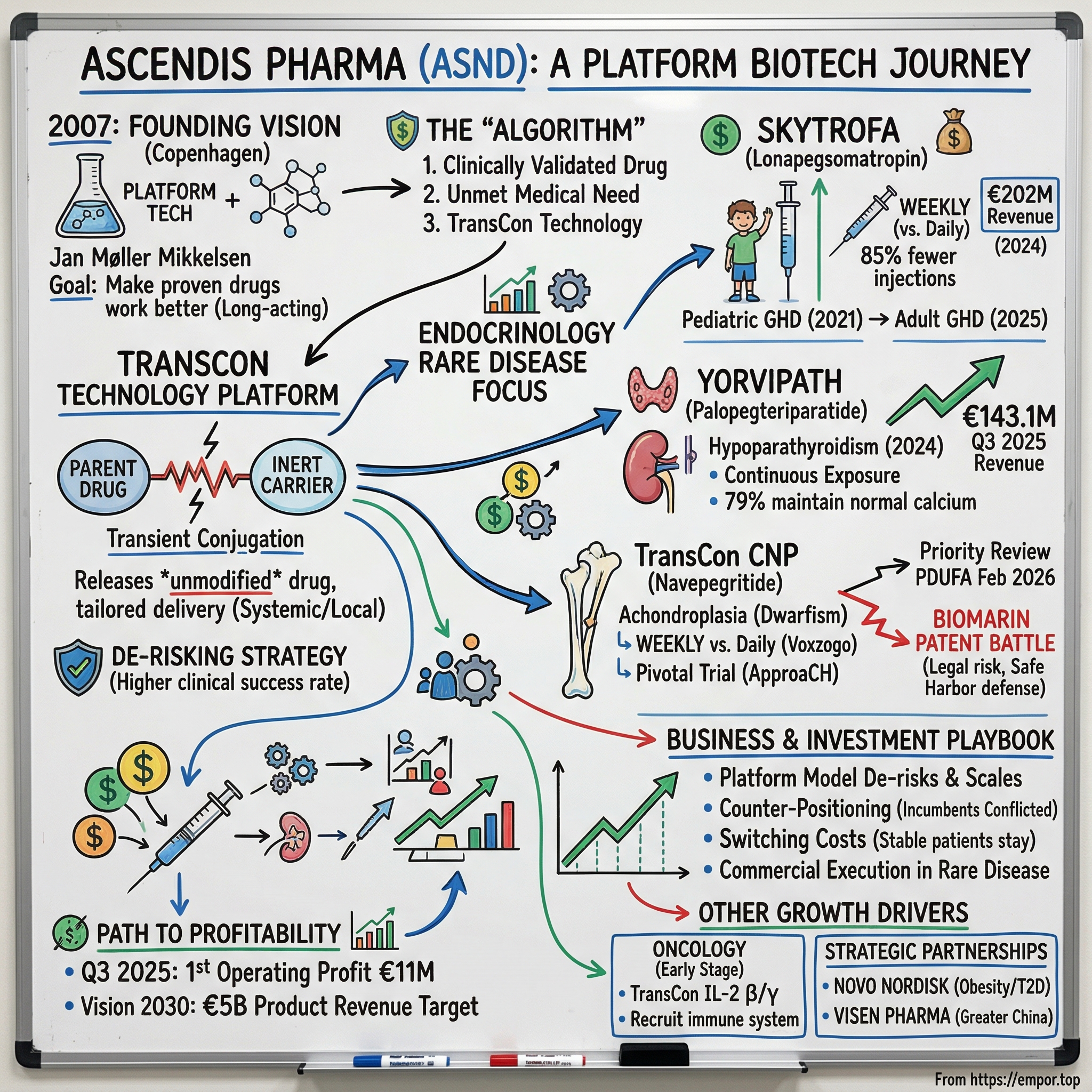

Picture a Copenhagen boardroom in late 2007. Outside, the Scandinavian winter grips the city, but inside, a biochemist with sharp features and even sharper ambition is sketching molecules on a whiteboard. Jan Møller Mikkelsen, fresh off running a drug delivery company, has an idea that seems almost too simple: What if you could take drugs that already work and make them work better—longer-lasting, more convenient, potentially more effective?

Ascendis Pharma was founded in 2007 based on the innovative TransCon technology platform and is headquartered in Copenhagen, Denmark. The company went public following an initial public offering in 2015 on Nasdaq, trading under the symbol ASND.

The central question that makes Ascendis Pharma one of the most fascinating biotech stories of the past decade is this: How did a Danish company with no marketed drugs turn a single technology platform into a rare disease powerhouse, now on the verge of having three potentially blockbuster products—with a fourth therapeutic area just beginning to take shape?

Today, Ascendis Pharma is a global biopharmaceutical company committed to making a meaningful difference in patients' lives. Guided by core values of Patients, Science, and Passion, the company applies its innovative TransCon technology platform to develop new therapies that demonstrate best-in-class potential to improve treatment safety, efficacy, tolerability, and convenience. With headquarters in Denmark, research facilities in Germany, and offices across Europe and the United States, Ascendis is advancing programs in Endocrinology Rare Disease and Oncology.

The numbers tell a story of rapid transformation. In Q3 2025, Ascendis Pharma reported total revenue of €213.6 million compared to just €57.8 million in the same period of 2024—a near-quadrupling driven by commercial product sales. The company achieved Q3 2025 operating profit of €11.0 million—a milestone for a company that had been burning cash for years building its pipeline.

What follows is the story of how Jan Mikkelsen and his team built this company—starting with a technology platform in a Copenhagen laboratory, navigating the brutal regulatory journey from bench to bedside, executing commercially in competitive rare disease markets, and positioning for what could be their biggest opportunity yet. Along the way, we'll extract the business and investing lessons that make Ascendis a case study in platform biotech done right.

II. Founding Vision & The TransCon Technology Platform

Origins: The Danish Biotech Mafia

To understand Ascendis, you first need to understand its founder. Jan Møller Mikkelsen founded Ascendis Pharma and has served as President and Chief Executive Officer, as well as Board member, since December 2007. From 2002 to 2006, Mikkelsen was President and Chief Executive Officer of LifeCycle Pharma A/S. From 2000 to 2002, he was President of the Pharmaceutical Division of Maxygen, Inc. Prior to that, Mikkelsen co-founded ProFound Pharma A/S, a biopharmaceutical company acquired by Maxygen, where he served as Co-Chief Executive Officer from 1999 to 2000. From 1988 to 1999, Mikkelsen held various positions at Novo Nordisk A/S, including Vice President of Protein Discovery.

That Novo Nordisk pedigree matters enormously. Novo Nordisk, the insulin giant, gave Mikkelsen something invaluable: deep expertise in protein therapeutics, an understanding of chronic disease management where patients inject themselves daily for years, and a network throughout the Danish biotech ecosystem. When he founded Ascendis, he wasn't starting from scratch—he was deploying a career's worth of accumulated knowledge about what makes drug delivery work.

Early funding came from venture capital sources, including Sofinnova Partners and NEA, setting the stage for later public financing. The venture backers saw what Mikkelsen saw: a platform that could, if it worked, be applied across many therapeutic areas, creating a pipeline factory rather than a one-drug company.

The TransCon Platform: Elegant Chemistry, Profound Implications

At its core, TransCon is deceptively simple. TransCon refers to "transient conjugation," or the company's unique ability to temporarily (transiently) link an inert carrier to a parent drug with known biology. TransCon is widely applicable to proteins, peptides, or small molecules in multiple therapeutic areas. Whether using systemic or localized release, TransCon works by a simple and elegant mechanism designed to enable a therapeutic to maintain its original mechanism of action.

Let's unpack that. TransCon molecules comprise three integral elements: a parent drug, an inert protective carrier, and a linker that temporarily connects them. When joined together, this carrier effectively deactivates and shields the parent drug from being cleared by the body. Once administered, under specific physiological conditions such as pH and temperature, these molecules initiate the controlled release of the unaltered active parent drug predictably and gradually. Depending on the specific TransCon carrier utilized, TransCon prodrugs can be tailored for either prolonged localized or systemic delivery.

Why does this matter? The magic is in the phrase "unaltered active parent drug." Unlike other long-acting technologies that permanently modify a drug molecule—potentially changing its safety profile or efficacy—TransCon releases the exact same parent drug that physicians have been using for decades. TransCon transforms existing therapeutic molecules into long‐acting prodrugs by transiently binding an unmodified parent drug to an inert carrier via a linker. This design protects the active molecule from rapid clearance, allowing for the controlled, predictable release of the unmodified drug under physiological conditions. By ensuring that the released drug maintains its original mode of action, Ascendis Pharma not only preserves the desired therapeutic effect but also improves patient compliance by reducing dosing frequency.

This is what makes TransCon a de-risking strategy, not just a drug delivery technology. When you're developing a new drug, roughly 90% fail in clinical trials. But when you're taking a clinically validated drug—something that already works—and simply changing how it's delivered, you've eliminated the biggest risk factor in drug development: does the biology work?

The Algorithm: Ascendis's Repeatable Playbook

Ascendis's unique approach to product innovation focuses on identifying unmet medical needs where a clinically validated parent drug or pathway is suitable to TransCon technologies. They call this their "algorithm"—it helps select and advance product candidates. Leveraging this strategic approach, the company currently has a pipeline of three independent endocrinology rare disease product candidates in clinical development and is advancing oncology as a second therapeutic area of focus.

The algorithm essentially asks: Is there a proven drug where the only problem is how it's given to patients? Where daily injections create compliance problems, or where peaks and troughs in drug levels cause side effects? If yes, TransCon can potentially create a once-weekly or even once-monthly version that solves those problems while keeping all the benefits of the original molecule.

For investors, this represents something rare in biotech: a repeatable playbook. Most biotechs are one-trick ponies—they have a single drug candidate, and everything rides on that bet. Ascendis, by contrast, has a technology platform that can generate candidate after candidate, each with a higher probability of success than a typical new drug. That's the moat.

III. From Platform to Pipeline: Building the Rare Disease Focus (2007-2015)

The Strategic Bet on Endocrinology

Ascendis's historical focus on rare endocrine diseases has served as a launching pad for broader therapeutic exploration. The question is: why endocrinology, and specifically why rare diseases?

The answer reveals sophisticated strategic thinking. Endocrine diseases involve hormones—chemical messengers that the body produces in small quantities but that have profound effects. When hormone levels are deficient, replacement therapy is the logical treatment. But hormones are proteins, which means they can't be taken as pills—they get destroyed in the gut. Injection is the only option.

Now consider the patient experience: a child with growth hormone deficiency typically needs daily injections, administered by a parent, for years. That's over 2,000 needle sticks before they finish treatment. Children with growth hormone deficiency are not only characterized by short stature, but they also experience metabolic abnormalities, psychosocial challenges, cognitive deficiencies and reduced quality of life. For decades, the standard of care for GHD has been a daily subcutaneous injection of hGH, which improves growth and metabolic effects. For caregivers and patients, the treatment burden with daily injections is high, which leads to poor adherence and reduced overall treatment outcomes.

The opportunity was clear: take growth hormone—a well-understood, clinically validated therapy—and use TransCon to make it once-weekly instead of daily. Same drug, same efficacy, 85% fewer injections. If it worked, you'd have a clearly superior product that physicians would prescribe and parents would demand.

Why Rare Diseases?

The rare disease focus was equally strategic. Rare (or "orphan") diseases offer several advantages for a clinical-stage biotech:

- Smaller trials: With fewer patients available, regulators accept smaller studies—meaning faster and cheaper development

- Orphan drug designation: This provides seven years of market exclusivity in the US, regardless of patent status

- Clear endpoints: In conditions like growth hormone deficiency, you can measure height velocity directly—no ambiguity about whether the drug works

- Less competition: Large pharma historically avoided rare diseases because the patient populations were too small; that's changing, but pioneers had first-mover advantages

- Premium pricing: Payers accept higher prices for rare disease drugs because the overall budget impact is limited

The 2015 IPO: Going Public Pre-Revenue

Ascendis Pharma raised $108 million by offering 6 million shares at $18 per share—at the high end of the expected range. The IPO raised approximately $108 million, providing significant capital to advance the clinical pipeline based on its TransCon technology.

The company floated in 2015 on Nasdaq at a $373 million valuation, rising to a market cap of almost $5 billion by 2022. Ascendis had previously raised $156 million in VC funding rounds.

Going public as a clinical-stage company with no revenue is standard in biotech, but it's worth pausing to appreciate what Ascendis was selling to public market investors: a bet on a technology platform that had shown promise in preclinical and early clinical studies, but hadn't yet proven itself in a pivotal trial. The conviction was in the platform's elegance and the team's track record—pure venture capital logic translated to public markets.

The 2015 IPO was just the beginning of what would become a capital-intensive journey from laboratory to commercial operations.

IV. Key Inflection Point #1: SKYTROFA and the Transformation to Commercial Company (2021)

The Long Road to Approval

On August 25, 2021, Ascendis Pharma announced that the U.S. Food and Drug Administration (FDA) approved SKYTROFA (lonapegsomatropin-tcgd) for the treatment of pediatric patients one year and older who weigh at least 11.5 kg and have growth failure due to inadequate secretion of endogenous growth hormone. As a once-weekly injection, SKYTROFA is the first FDA approved product that delivers somatropin (growth hormone) by sustained release over one week.

This approval—the culmination of years of clinical development—was transformational. It validated the entire TransCon platform: the chemistry worked, the regulatory pathway worked, and Ascendis could make the transition from development-stage company to commercial operation.

"Today's approval represents an important new choice for children with GHD and their families, who will now have a once-weekly treatment option. In the pivotal head-to-head clinical trial, once-weekly SKYTROFA demonstrated higher annualized height velocity at week 52 compared to somatropin," noted clinical investigators. "This once-weekly treatment could reduce treatment burden and potentially replace the daily somatropin therapies, which have been the standard of care for over 30 years."

Why This Approval Mattered

The data was compelling: SKYTROFA wasn't just non-inferior to daily growth hormone—it was actually better. In head-to-head trials, children on SKYTROFA grew faster than those on daily injections. This is unusual; typically, long-acting formulations trade efficacy for convenience. Ascendis achieved both.

The approval includes the SKYTROFA Auto-Injector and cartridges which, after first removed from a refrigerator, allow families to store the medicine at room temperature for up to six months. With a weekly injection, patients switching from injections every day can experience up to 86 percent fewer injection days per year.

The room-temperature storage is an underappreciated feature. Most biologic drugs require refrigeration, which complicates travel, school trips, and summer camp. SKYTROFA's stability made it not just medically superior but practically superior in ways that matter to real families.

"SKYTROFA offers patients, caregivers, and physicians the potential to replace daily somatropin injections that have been the standard of care for more than 30 years," said Jan Mikkelsen. "As the first and only FDA-approved once-weekly therapy for pediatric growth hormone deficiency, SKYTROFA represents one of the most important innovations for these patients in decades."

Commercial Execution: Building from Scratch

Approval is one thing; selling is another. Ascendis had to build an entire commercial organization—field sales force, medical affairs, market access, patient support programs—essentially from zero.

SKYTROFA generated approximately €202 million in full-year 2024 revenue, excluding prior year adjustments. SKYTROFA achieved approximately €202 million in full-year 2024 revenue, with an 84% year-over-year volume increase and 6.5% U.S. market share.

That market share number—6.5% of the total U.S. growth hormone market—might seem small, but it's remarkable for several reasons. First, SKYTROFA is competing against entrenched daily injections from giants like Novo Nordisk and Pfizer. Second, changing prescriber behavior in pediatric endocrinology is notoriously slow—physicians who've been writing scripts for daily growth hormone for decades don't switch easily. Third, insurance coverage and reimbursement pathways had to be established from scratch.

"Our market research shows SKYTROFA is the treatment of choice for pediatric GHD among patients and physicians," said Jan Mikkelsen. When you're the treatment of choice but still at 6.5% market share, that speaks to both the opportunity ahead and the time required to penetrate established markets.

The Label Expansion: Adult Growth Hormone Deficiency

On July 28, 2025, Ascendis Pharma announced that the FDA approved SKYTROFA for the replacement of endogenous growth hormone in adults with growth hormone deficiency (GHD), a rare disorder resulting from decreased or total loss of growth hormone production. Lonapegsomatropin (approved by the FDA in 2021 for the treatment of pediatric GHD) is a prodrug of somatropin administered once weekly, providing sustained release of active, unmodified somatropin. The FDA's approval of SKYTROFA for adult GHD was based on results from foresiGHt, a Phase 3 randomized trial.

"This important milestone is the first of many planned label expansions supporting our goal to become the leading endocrinology rare disease company."

This label expansion is classic life-cycle management. The same drug, same manufacturing, same sales force—but a new patient population. Adult GHD is a different commercial proposition than pediatric (adults make their own treatment decisions, don't need parental involvement, face different compliance challenges), but the incremental investment is minimal. This is the beauty of platform companies: each new indication leverages the existing infrastructure.

V. Key Inflection Point #2: YORVIPATH and Multi-Product Validation (2023-2024)

The Hypoparathyroidism Opportunity

Hypoparathyroidism is a rare endocrine disease caused by insufficient levels of parathyroid hormone that impact multiple organs and affects an estimated 70,000 to 90,000 people in the United States. YORVIPATH is a prodrug of parathyroid hormone (PTH[1-34]), administered once daily, designed to provide continuous exposure to released PTH over the 24-hour dosing period.

Unlike growth hormone deficiency, hypoparathyroidism had no FDA-approved hormone replacement therapy. Patients were managing their condition with calcium supplements and active vitamin D—treating the symptoms (low calcium) rather than the underlying cause (insufficient parathyroid hormone). It was a market essentially waiting for someone to develop a proper solution.

The only previous FDA-approved PTH replacement, Takeda's Natpara, was discontinued in late 2024 due to manufacturing challenges with the device component. This left a patient population with no approved treatment options—exactly the kind of unmet need where Ascendis could make a difference.

The Regulatory Rollercoaster

After the initial NDA submission in August 2022, Ascendis received a Complete Response Letter (CRL) from the FDA in May 2023, citing concerns related to the manufacturing control strategy for variability of delivered dose in the TransCon PTH drug/device combination product, but not the submitted clinical data. The company resubmitted the NDA in December 2023, and the FDA considered it a complete class 2 response, setting a PDUFA goal of May 2024. In May 2024, the review period was extended by 3 months to August 2024.

Before this approval, the FDA had rejected Yorvipath in May 2023 due to concerns about the consistency of dosage delivery from the TransCon PTH device.

This regulatory journey—rejection, reformulation, delay, then approval—is worth examining closely. The FDA didn't reject YORVIPATH because of safety concerns or efficacy doubts. The clinical data was solid. The problem was manufacturing: ensuring that every dose from the pen device delivered exactly the right amount of drug, consistently, across production batches.

This is an underappreciated risk in biologics development. You can have a miracle drug with perfect clinical trials, but if you can't manufacture it reproducibly, you won't get approval. Ascendis had to go back, work with the FDA, develop a new manufacturing control strategy, and demonstrate consistency. It cost them over a year of delay—but they got it done.

The Approval and Launch

On August 12, 2024, the FDA approved YORVIPATH (palopegteriparatide; developed as TransCon PTH) for the treatment of hypoparathyroidism in adults.

"FDA approval of our second TransCon product, YORVIPATH, reflects our values and dedication to following the science to help patients, as well as our unwavering commitment these past years to addressing the significant unmet medical needs of the hypoparathyroidism community in the United States," said Jan Mikkelsen.

Results showed that 78.7% of patients treated with YORVIPATH maintained normal blood calcium levels without conventional treatments, compared to just 4.8% in the placebo group.

That 79% versus 5% difference is what biostatisticians call "highly statistically significant"—there's no ambiguity about whether the drug works. Patients who couldn't normalize their calcium levels on supplements and vitamin D could do so with YORVIPATH.

The launch trajectory has been remarkable. YORVIPATH achieved 908 prescriptions by February 7, 2025, with full-year 2024 revenue of €28.7 million. Given that the drug was only commercially available for a portion of 2024, this represents strong early uptake.

YORVIPATH revenue for the third quarter of 2025 totaled €143.1 million. "The ongoing strong global launch of YORVIPATH is transforming our financial profile and, based on positive feedback from physicians and patients, we expect to continue to build on this momentum," said Jan Mikkelsen.

The trajectory from €28.7 million in full-year 2024 to €143.1 million in just Q3 2025 represents explosive growth—this is what a successful rare disease launch looks like when you have the right product for an unmet need.

Multi-Product Validation

YORVIPATH's approval and commercial success proved something important: TransCon wasn't a one-hit wonder. The platform could generate multiple successful products across different conditions. This transforms how investors should think about the company—not as a single-product biotech with binary risk, but as a platform company with diversified revenue streams and a pipeline of additional opportunities.

VI. Key Inflection Point #3: TransCon CNP and the Achondroplasia Race (2025)

The Achondroplasia Market

Achondroplasia is a rare genetic condition arising from a systemic fibroblast growth factor receptor 3 (FGFR3) variant that leads to an imbalance in the effects of the FGFR3 and CNP signaling pathways, estimated to affect more than 250,000 people worldwide. While historically considered a bone growth disorder, the FGFR3 variant seen in achondroplasia is expressed in tissues throughout the body, causing serious muscular, neurological, and cardiorespiratory complications in addition to skeletal dysplasia.

Throughout infancy and childhood, observed complications include spinal deformities, enlarged brain ventricles, impaired muscle strength and stamina, hearing deficits and chronic ear infections, upper airway obstructions, sleep-disordered breathing, hip problems, leg bowing, and chronic pain; many of these persist or worsen in adulthood. These medical complications can have detrimental effects on quality of life, physical functioning, and psychosocial function. Individuals with achondroplasia often require multiple surgeries and procedures to alleviate the condition's complications.

The achondroplasia market has an established player: BioMarin's Voxzogo (vosoritide), which requires daily injections. TransCon CNP, if approved, would offer weekly dosing—the same convenience advantage that made SKYTROFA successful in growth hormone deficiency.

Pipeline Progress and the FDA Journey

On June 2, 2025, Ascendis announced that the FDA accepted for priority review its New Drug Application (NDA) for TransCon CNP (navepegritide) for the treatment of children with achondroplasia and set a PDUFA goal date of November 30, 2025 to complete its review. The FDA also informed Ascendis that they are not currently planning to hold an advisory committee meeting to discuss this application.

The absence of an advisory committee meeting is typically a positive signal—it suggests the FDA doesn't see substantial unresolved questions requiring external expert input.

Pivotal Week 52 results from the randomized, double-blind, placebo-controlled ApproaCH Trial of once-weekly TransCon CNP in children with achondroplasia showed key findings: TransCon CNP produced a statistically higher annualized growth velocity at Week 52 versus placebo, improved lower-limb alignment and body proportionality, and showed numerical gains in health-related quality of life with a safety and tolerability profile similar to placebo.

However, regulatory timelines rarely proceed without hiccups. On November 25, 2025, Ascendis announced that the FDA notified the Company that information submitted on November 5, 2025, related to the post-marketing requirement, in response to the FDA's ongoing review constituted a major amendment to the NDA. Accordingly, the FDA extended the PDUFA target action date by three months to February 28, 2026. "We have responded to all outstanding requests from the FDA, including the request for a revised protocol for the post-marketing study, which we received as the lone item for discussion at our late-cycle meeting," said Jan Mikkelsen.

This extension—while disappointing for investors hoping for a November approval—appears to be procedural rather than substantive. The issue is the post-marketing study protocol, not the clinical data or safety profile. Ascendis sounds confident: "We are committed to working diligently with the FDA to finalize elements of the post-marketing requirement, with the goal of bringing this innovative therapy to patients as soon as possible."

The BioMarin Patent Battle

The achondroplasia opportunity comes with a significant complication: BioMarin is aggressively defending its territory.

BioMarin Pharmaceutical initiated a legal action against Ascendis Pharma A/S for infringement of European patent EP 3 175 863 B1 at the Unified Patent Court in Munich, Germany. The patent covers long-acting variants of C-Type Natriuretic Peptide (CNP). The legal action, which would result in a decision in the next 12-15 months, is based on BioMarin's belief that Ascendis' TransCon CNP investigational product and its development program in Germany and elsewhere in Europe infringe BioMarin's patent. The BioMarin patent was confirmed by the European Patent Office's Opposition Division in 2024.

BioMarin has launched an ITC case seeking to block Ascendis from importing its drug into the US. For now, Ascendis is relying upon a safe harbor defense. On April 1, 2025, the day after Ascendis filed with the FDA for TransCon CNP, BioMarin commenced an action at the International Trade Commission to block Ascendis from importing "certain drug products containing C-type natriuretic peptide" that infringe BioMarin's patent. Ascendis purchases TransCon CNP from its supplier, Wacker, which is located in Europe. Accordingly, BioMarin was essentially using the ITC case to stifle Ascendis' development of its competing drug for achondroplasia.

This patent dispute represents a material risk. The bigger problem for Ascendis—and its investors—is that at some point, it will have to reckon with BioMarin's patent. Right now, Ascendis has a "safe harbor" defense to BioMarin's patent, but that is only because Ascendis has yet to commercially launch its drug.

The safe harbor defense protects companies importing drugs for FDA approval purposes—you can bring in a drug to get it approved without patent infringement liability. But once you start selling commercially, that protection evaporates. If BioMarin's patents are upheld and found to cover TransCon CNP, Ascendis could face injunctions blocking sales, substantial damages, or be forced to negotiate a licensing agreement.

For investors, this is the most important risk to monitor around TransCon CNP. The drug could be approved, the clinical data could be excellent, and commercial execution could be flawless—but patent litigation could still significantly impair the opportunity.

VII. Strategic Partnerships & Geographic Expansion

VISEN Pharmaceuticals and the China Strategy

In 2018, VISEN Pharmaceuticals was formed by Ascendis Pharma with an investor syndicate led by Vivo Capital. Focusing on endocrinology, VISEN has received exclusive rights to develop and commercialize Ascendis Pharma's endocrinology rare disease therapies, including TransCon hGH, TransCon PTH, and TransCon CNP in Greater China.

On March 20, 2025, VISEN Pharmaceuticals announced the pricing of its initial public offering on the Hong Kong Stock Exchange. The shares offered in the IPO are priced at HKD 68.80 per share and expected to result in gross proceeds of approximately USD 100 million plus a potential greenshoe of up to approximately USD 15 million. The IPO closed on March 21, 2025, and VISEN's shares trade under the ticker symbol 2561.HK.

Ascendis Pharma holds 41,136,364 shares in VISEN.

The VISEN structure is worth understanding. Rather than building a China operation itself—with all the regulatory complexity, capital requirements, and execution risk that entails—Ascendis spun out an independent company with dedicated Chinese partners and investors. Ascendis retains a significant ownership stake and receives milestone payments and royalties, but VISEN bears the burden of local development and commercialization.

This is increasingly common in biotech: partner locally where you lack expertise, rather than trying to do everything yourself. The China pharmaceutical market is the world's second-largest, but navigating it requires deep local knowledge that most Western biotechs simply don't have.

The Novo Nordisk Partnership

In November 2024, Ascendis Pharma announced that it granted Novo Nordisk A/S an exclusive worldwide license to the TransCon technology platform to develop, manufacture and commercialize Novo Nordisk proprietary products in metabolic diseases (including obesity and type 2 diabetes) and a product-by-product exclusive license in cardiovascular diseases. The lead program in the collaboration is a once-monthly GLP-1 receptor agonist product candidate that will initially target obesity and type 2 diabetes.

The company's total revenue for 2024 reached €363.6 million, up from €266.7 million in 2023, driven by the €91.3 million ($100 million) upfront payment from Novo Nordisk and increased commercial product sales.

The Novo Nordisk deal is strategically brilliant. GLP-1 drugs—Ozempic, Wegovy, Mounjaro—are the hottest space in pharma right now, with a multi-hundred-billion-dollar market opportunity in obesity. But Ascendis has zero capability in metabolic disease. By licensing TransCon to Novo Nordisk—the world leader in the space—Ascendis gets:

- Validation: Novo Nordisk, with all its internal capabilities, chose to license TransCon rather than develop their own long-acting technology

- Revenue: The $100 million upfront plus milestones and royalties

- Focus: Ascendis can concentrate on rare disease while capturing value in metabolic disease through partnership

"We are pleased to collaborate with Novo Nordisk, an established expert in metabolic diseases, to maximize the potential of TransCon products for helping patients," said Jan Mikkelsen. "The agreement with Novo Nordisk reflects our Vision 2030 to create value in additional large therapeutic areas outside endocrinology rare disease through collaborations with established global leaders."

A once-monthly GLP-1 could be transformational in obesity—imagine compliance rates when patients only need to inject once per month instead of once per week. If successful, this partnership alone could be worth billions to Ascendis in royalties.

VIII. Oncology: The Second Therapeutic Area

Applying the Platform to Cancer

With TransCon, Ascendis aims to go one step further in oncology by creating therapies with better efficacy without increasing toxicity—solving the limitations of current treatments to help improve patient outcomes. The company believes TransCon is well-suited for oncology applications given the large number of validated targets with known limitations. TransCon technologies—sustained systemic release and localized (intratumoral) release—can be applied to clinically validated targets and pathways from diverse drug classes, including small molecules, peptides and proteins, targeting different aspects of the cancer immunity cycle.

The company has one oncology candidate in clinical development, TransCon IL-2β/γ, designed for prolonged exposure of an interleukin-2 (IL-2) variant that selectively activates the IL-2 receptor beta/gamma (IL-2Rβ/γ) with minimal binding to the IL-2 receptor alpha (IL-2Rα), offering potential to provide potent anti-tumor effects with reduced risk of toxicity.

The oncology approach is different from endocrinology. In rare endocrine diseases, Ascendis is replacing missing hormones—relatively straightforward biology. In oncology, they're trying to harness the immune system to fight cancer—far more complex and unpredictable.

In trials, TransCon IL-2 β⁄γ alone or in combination with pembrolizumab or TransCon TLR7/8 Agonist was generally well tolerated with no new safety signals. "We are very encouraged by the clinical response and safety profile for TransCon IL-2 β⁄γ and are pleased to see it working as designed to recruit and amplify the body's immune response with sustained immune activation without a corresponding increase in markers of toxicity."

Both oncology candidates are designed to recruit innate and adaptive components of the immune system to maximize anti-cancer activity while reducing dose-limiting toxicities. "TransCon IL-2 β/γ was designed by applying the TransCon technology together with protein bioscience to solve problems with aldesleukin that have eluded industry for many decades—to create a well-tolerated IL-2 therapy that has the potential to effectively activate the immune system to drive anti-cancer activity without dosing complexity."

The oncology pipeline is earlier-stage and higher-risk than endocrinology. But it represents optionality: if the platform works in immuno-oncology, it opens up a vast new market. The read-through from endocrinology success (TransCon chemistry works, the company can execute clinically and commercially) provides some confidence, but oncology remains a bet on the future rather than a current contributor to value.

IX. Playbook: Business & Investing Lessons

The Platform Model in Biotech

Ascendis exemplifies the platform approach done right. The TransCon technology creates value in three ways:

- De-risking: Using validated biology dramatically increases clinical success rates

- Repeatability: The same core technology generates multiple pipeline candidates

- Capital efficiency: Shared infrastructure (manufacturing expertise, regulatory know-how, commercial capabilities) serves multiple products

For investors, platform companies offer a different risk-reward profile than single-product biotechs. You're less likely to see a total wipeout from one failed trial, but you also need to evaluate whether the platform actually generates differentiated products.

Commercial Execution in Rare Disease

YORVIPATH achieved 908 prescriptions by February 7, 2025, with full-year 2024 revenue of €28.7 million—early launch metrics that matter.

Rare disease commercialization is specialized. Patient populations are small, so you can't rely on volume. Instead, success depends on:

- Disease education: Many patients with rare diseases are undiagnosed or misdiagnosed

- Physician targeting: A small number of specialists see most patients

- Patient support: Helping patients navigate insurance, administration, and adherence

- Premium pricing: Per-patient economics must support the commercial model

Ascendis has built this capability. The fact that SKYTROFA reached €202 million in annual revenue with 6.5% market share, and YORVIPATH exploded to €143 million in a single quarter, demonstrates commercial execution ability.

Capital Allocation

As of December 31, 2024, Ascendis Pharma had cash, cash equivalents, and marketable securities totaling €559.5 million. As of September 30, 2025, cash and cash equivalents totaled €539 million.

For the full year 2024, Ascendis Pharma reported a net loss of €378.1 million, or €6.53 per share, compared to a net loss of €481.4 million in 2023.

The improving loss profile tells the story of a company transitioning from R&D-heavy cash burn to commercial-stage profitability. The company achieved an operating profit of €11.0 million in Q3 2025, driven by the successful global launch of YORVIPATH and the continued uptake of SKYTROFA.

Operating profitability—achieved for the first time—is a significant milestone. It demonstrates that the commercial business model works, that YORVIPATH economics are strong, and that continued revenue growth should drive improving cash generation.

Regulatory Navigation

The YORVIPATH Complete Response Letter experience offers lessons. When the FDA raised manufacturing concerns in May 2023, Ascendis didn't panic or pivot—they worked through it systematically, developed a new control strategy, resubmitted, and ultimately received approval 15 months later.

Regulatory risk is inherent to biotech. What matters is management's ability to navigate setbacks constructively. Ascendis's track record—SKYTROFA approved, YORVIPATH approved after a CRL, TransCon CNP under priority review with a new PDUFA date after amendment—suggests competent regulatory execution.

X. Financial Performance & Trajectory

Revenue Ramp

The financial story is one of acceleration:

For Q3 2025, Ascendis reported a net loss of €61 million compared to a net loss of €99.2 million in Q3 2024. Despite the loss, the company showed an increase in revenue to €213.6 million from €57.8 million in the previous year—a significant growth in sales.

The Q3 2025 revenue breakdown: YORVIPATH revenue was €143.1 million (over 4,250 unique patients enrolled, over 2,000 prescribers) and SKYTROFA revenue was €50.7 million.

What's striking is the speed of the YORVIPATH ramp. The drug was approved in August 2024, launched in early 2025, and by Q3 2025 was generating nearly €150 million in quarterly revenue. This is exceptional for a rare disease launch and reflects pent-up demand from an underserved patient population.

Path to Profitability

Looking ahead, Ascendis Pharma expects continued revenue growth in Q4 2025 and is targeting 5 billion euros in annual product revenue by 2030.

Ascendis Pharma's narrative projects €2.2 billion in revenue and €826.6 million in earnings by 2028. This requires 63.9% yearly revenue growth and an earnings increase of €1.10 billion from the current level.

These projections assume successful execution across multiple products, including TransCon CNP approval and launch. The Vision 2030 target of €5 billion in product revenue would imply blockbuster status for multiple products—SKYTROFA across multiple indications, YORVIPATH globally, and TransCon CNP in achondroplasia.

Is this achievable? The trajectory through Q3 2025 supports optimism, but execution risk remains substantial. TransCon CNP faces patent litigation. SKYTROFA needs to continue gaining market share against entrenched competitors. YORVIPATH needs to maintain its launch trajectory as it expands globally. Nothing is guaranteed.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

Barriers to entry in rare disease biotech are substantial. FDA approval requires years of clinical development and hundreds of millions in investment. Orphan drug designations provide 7-year market exclusivity. Ascendis's TransCon patents add additional protection. However, large pharmaceutical companies could acquire smaller players or develop competing long-acting technologies—as evidenced by BioMarin's investment in its own long-acting CNP (BMN 333).

2. Bargaining Power of Suppliers: MEDIUM

Ascendis purchases TransCon CNP from its supplier, Wacker, which is located in Europe. The company relies on third-party contract development and manufacturing organizations (CDMOs) for drug and device components. Manufacturing complexity for biologics creates supplier dependency—the YORVIPATH CRL demonstrated that manufacturing challenges can delay approvals. However, multiple qualified biologics manufacturers exist globally, limiting any single supplier's leverage.

3. Bargaining Power of Buyers: LOW-MEDIUM

Rare disease patients have limited treatment options, which reduces buyer power. However, payers (insurance companies, PBMs) have significant negotiating leverage—specialty drug prices are scrutinized, and access can be restricted. Patient advocacy groups influence adoption but don't set prices. Positive feedback from physicians and the drug's potential renal protection benefits create high barriers to switching for competitors.

4. Threat of Substitutes: LOW

"Despite this, adherence to daily somatropin injections, which have been the standard of care for more than 25 years, remains a problem." Weekly dosing offers significant patient benefit versus daily injections. For hypoparathyroidism, YORVIPATH is the first FDA-approved hormone replacement—there is no direct substitute. For growth hormone deficiency, daily injections remain available but are clinically inferior in terms of adherence.

5. Competitive Rivalry: MEDIUM-HIGH

In growth hormone, SKYTROFA competes against established daily therapies from Novo Nordisk, Pfizer, and others. Market share gains have been steady but gradual. In achondroplasia, BioMarin's Voxzogo is established and the company is defending aggressively through patent litigation. In hypoparathyroidism, potential competitors include MBX developing canvuparatide and BridgeBio advancing encaleret for a broader patient population—though neither directly competes with YORVIPATH's mechanism of action.

Hamilton's 7 Powers Analysis

1. Scale Economies: EMERGING

Commercial infrastructure is being leveraged across multiple products—the same field sales force that promotes SKYTROFA can promote YORVIPATH to overlapping specialists. R&D platform allows efficient development of new candidates. However, Ascendis is not yet at scale compared to big pharma, and fixed cost leverage is still building.

2. Network Economies: LIMITED

This is not a traditional network effects business—patients don't benefit from other patients using the drug. However, physician relationships and patient advocacy connections compound over time. As more physicians gain experience with SKYTROFA, comfort increases and referrals grow. Similarly, relationships with patient advocacy groups (like the HypoPARAthyroidism Association) create informational advantages.

3. Counter-Positioning: STRONG ✓

This is perhaps Ascendis's most important strategic advantage. Established growth hormone players—particularly Novo Nordisk—have enormous daily injection franchises they would cannibalize by promoting a once-weekly competitor. They are structurally conflicted: pushing weekly growth hormone would undermine their existing revenue base. Ascendis, with nothing to protect, can focus entirely on capturing the long-acting opportunity.

This biopharmaceutical company stands out with its unique approach to creating potentially best-in-class treatments for unmet medical needs.

4. Switching Costs: MODERATE-HIGH ✓

Patients stable on therapy are unlikely to switch—growth hormone treatment typically continues for years, and changing medications introduces uncertainty. Physician familiarity with dosing and monitoring creates stickiness. Patient support programs (like Ascendis Signature Access Program) create administrative friction that discourages switching. Device training on the auto-injector creates learning curves.

5. Branding: BUILDING

Ascendis is becoming known as the rare endocrine disease leader. "This important milestone is the first of many planned label expansions supporting our goal to become the leading endocrinology rare disease company." Patient advocacy relationships strengthen brand in small but influential communities. Over time, being "the TransCon company" could become an asset in itself—signaling long-acting, patient-friendly formulations.

6. Cornered Resource: STRONG ✓

The TransCon technology platform, protected by patents, is a cornered resource. It cannot be replicated by competitors without infringing intellectual property. The accumulated know-how in TransCon chemistry—how to select linkers, design carriers, control release kinetics—represents proprietary expertise built over 17 years. Management stability (Mikkelsen has led the company since founding) preserves institutional knowledge.

7. Process Power: MODERATE

Ascendis has developed organizational capabilities in rare disease drug development and commercialization. The "algorithm" for product selection represents codified process knowledge. However, these processes are not yet so embedded that they would be difficult for a well-funded competitor to replicate with time and investment.

XII. Key Risks and Regulatory Overhangs

Patent Litigation

The BioMarin patent dispute represents the most significant near-term risk. An adverse ruling could result in injunctions blocking TransCon CNP sales in Europe (UPC case) or the U.S. (ITC case), substantial damages, or forced licensing arrangements. Resolution is expected within 12-15 months for the European case; U.S. timing is less certain.

Regulatory Execution

The TransCon CNP PDUFA date extension to February 28, 2026, while likely procedural, reminds investors that regulatory timelines are never certain. Future label expansions for SKYTROFA (Turner syndrome, idiopathic short stature, SGA) and international filings introduce additional regulatory risk.

Manufacturing

The YORVIPATH CRL demonstrated that device/drug combination products have unique manufacturing challenges. As production scales across multiple products, maintaining quality and consistency becomes increasingly complex. Any manufacturing disruption could impact supply and revenue.

Competitive Response

Established players are not standing still. BioMarin is developing BMN 333, its own long-acting CNP. Other companies may enter the long-acting growth hormone space. Success attracts competition.

Pipeline Concentration

Despite the platform, Ascendis's near-term value remains concentrated in three endocrinology products. The oncology pipeline is early-stage with uncertain outcomes. Heavy reliance on rare endocrine diseases creates concentration risk if any major product disappoints.

XIII. Key Metrics to Monitor

For long-term investors following Ascendis, three KPIs deserve particular attention:

1. YORVIPATH Quarterly Revenue and Patient Enrollment

YORVIPATH is the current growth driver. The trajectory from €28.7 million (full-year 2024) to €143.1 million (Q3 2025 alone) demonstrates explosive adoption. Watch quarterly revenue progression and the number of unique patients enrolled—these metrics indicate whether the launch momentum is sustained or fading. A slowdown would suggest market saturation or competitive pressure; continued acceleration supports the blockbuster thesis.

2. TransCon CNP Regulatory and Legal Milestones

The February 28, 2026 PDUFA date and ongoing patent litigation outcomes will determine whether TransCon CNP becomes a third blockbuster product. Any FDA action (approval, CRL, or further delay), court rulings in the BioMarin cases, or settlement announcements will materially impact the investment thesis.

3. Operating Margin Progression

Q3 2025's €11 million operating profit marked the first quarter of profitability. As YORVIPATH scales and SKYTROFA matures, operating leverage should improve. Track the progression from current single-digit margins toward the company's long-term profitability targets—this will reveal whether the commercial model is truly working or whether expenses are growing faster than revenue.

XIV. The Bull Case

Multi-Product Blockbuster Potential: SKYTROFA in pediatric and adult GHD, YORVIPATH in hypoparathyroidism, and TransCon CNP in achondroplasia each have blockbuster potential. Success across all three, plus label expansions and geographic rollout, could support the €5 billion revenue target by 2030.

Platform Validation Creates Future Optionality: The Novo Nordisk partnership validates TransCon's applicability beyond rare disease. If monthly GLP-1s become reality, royalties could be substantial. Oncology pipeline, while early, represents additional upside.

Operating Leverage Ahead: With commercial infrastructure largely built, incremental revenue should drop to the bottom line at attractive rates. First operating profit achieved in Q3 2025; profitability should accelerate with growth.

Favorable Competitive Dynamics: Counter-positioning against incumbents who can't cannibalize their own franchises, combined with first-mover advantages in YORVIPATH (no approved competitors) and potential best-in-class profile in CNP (weekly vs. daily), creates durable competitive positions.

XV. The Bear Case

Patent Litigation Overhang: An adverse ruling in the BioMarin cases could significantly impair the TransCon CNP opportunity—potentially the largest value driver in the current pipeline. Uncertainty alone may weigh on valuation until resolution.

Execution Risk at Scale: Building from one commercial product to three requires flawless execution across sales, manufacturing, and market access. Any stumbles—supply disruptions, payer pushback, slower-than-expected market penetration—could derail the trajectory.

Competition Intensifying: BioMarin is developing its own long-acting CNP. Large pharma increasingly interested in rare disease. First-mover advantages are never permanent.

Valuation Assumes Success: At current market capitalization, the stock prices in successful execution across multiple products. If any major assumption proves wrong—CNP patent issues, YORVIPATH plateau, SKYTROFA share losses—downside could be significant.

Cash Requirements: While cash position is solid and operating profitability emerging, the company may need additional capital for label expansion trials, international launches, or unforeseen circumstances. Dilution risk exists.

XVI. Conclusion: Platform Innovation in Action

Ascendis Pharma represents one of the cleaner examples of platform biotech done right. The TransCon technology—elegant in conception, validated in practice—has generated multiple clinical and commercial successes. The strategic focus on rare endocrine diseases provided the foothold; execution in SKYTROFA demonstrated commercial capability; YORVIPATH's explosive launch proves the model is repeatable.

The company sits at an inflection point. Operating profitability has been achieved. Two products are generating substantial revenue. A third is under FDA review (pending patent resolution). Partnership validation from Novo Nordisk suggests the platform has applications beyond rare disease. The Vision 2030 target of €5 billion in product revenue is ambitious but not implausible given the trajectory.

Yet risks are real. The BioMarin litigation creates binary uncertainty around TransCon CNP. Competitive dynamics will intensify as the company succeeds. Execution must remain flawless across an expanding operation.

For long-term investors, Ascendis offers exposure to the rare disease megatrend with platform economics that traditional single-product biotechs lack. The question is whether today's valuation adequately reflects both the opportunity and the risks. What's clear is that Jan Mikkelsen's whiteboard sketch from 2007—the vision of making proven drugs work better—has become commercial reality. The next chapter, featuring multiple blockbuster products and expansion into new therapeutic areas, is being written in real time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube