The Manitowoc Company: From Lake Michigan Shipyards to Global Crane Dominance

Introduction & Episode Roadmap

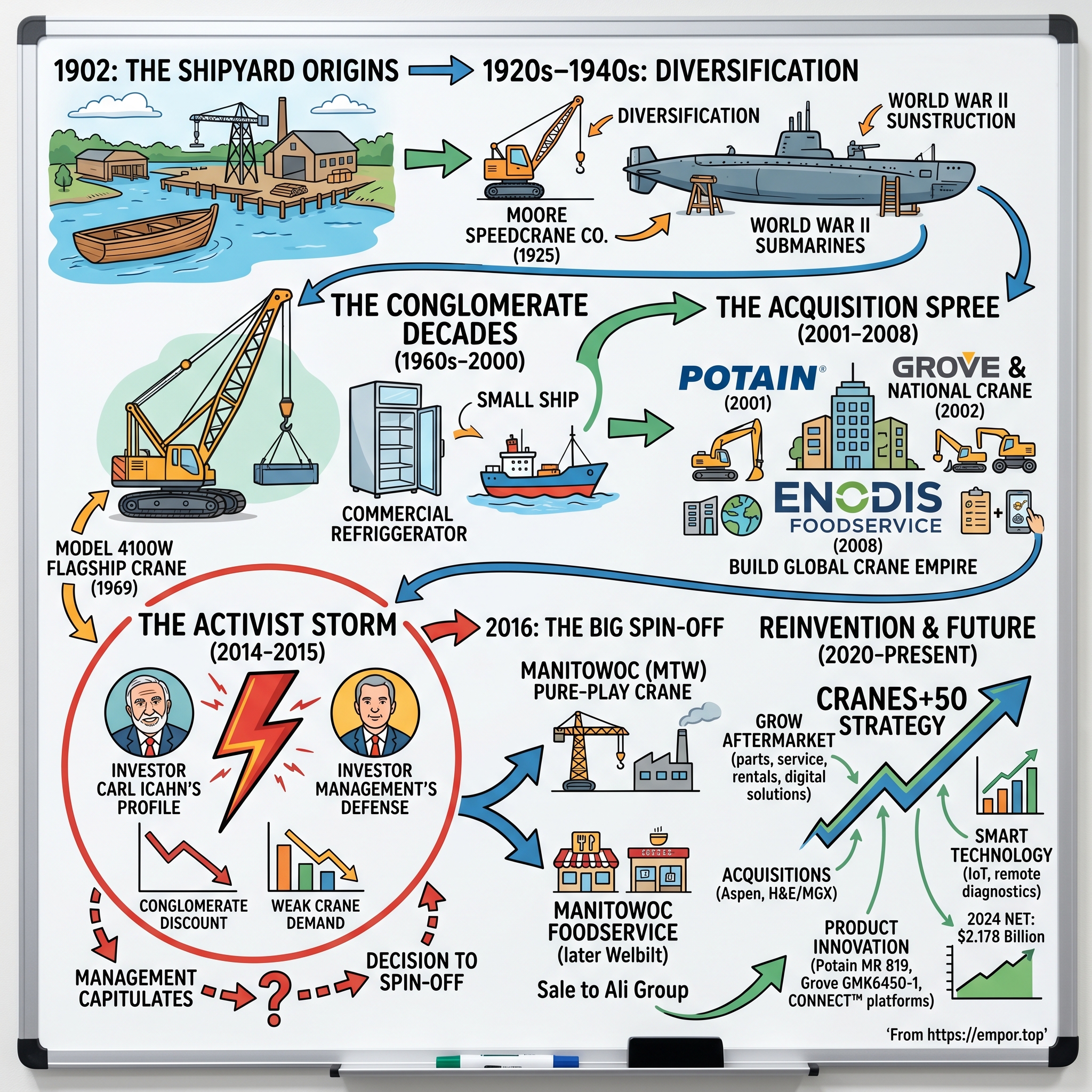

Picture a scene along the frigid shores of Lake Michigan in 1902. Two entrepreneurs, Charles West and Elias Gunnell, stand outside a modest wooden shipyard, surveying their newly acquired property. They had just paid $110,000 for the Burger & Burger Shipyard and Drydock—a sum that would define the next 122 years of industrial American history. Neither man could have imagined that their small ship-repair operation would one day become synonymous with lifting the heaviest loads on Earth.

The Manitowoc Company, founded in 1902, has over a 120-year tradition of providing high-quality, customer-focused products and support services to its markets. Manitowoc is one of the world's leading providers of engineered lifting solutions.

This is the story of The Manitowoc Company (NYSE: MTW)—a narrative of remarkable transformation, wartime heroism, aggressive acquisition, activist investor pressure, and ultimately, corporate reinvention. How does a Great Lakes shipbuilder transform into one of the world's premier crane manufacturers? And what happens when Carl Icahn shows up demanding you split your company in half?

In 2024, The Manitowoc Company reported full-year net sales of $2.178 billion. This figure represents a company that has navigated more pivots than most businesses will see in a century. From building steel ferries to crafting submarines for the U.S. Navy, from manufacturing ice machines to dominating the global tower crane market, Manitowoc's journey illuminates fundamental truths about industrial adaptation, capital allocation, and the art of the corporate spin-off.

The themes running through this story are timeless: How do conglomerates create or destroy value? When does diversification become dilution? And in the heavy equipment business—one of the most cyclical industries on the planet—how does a company build durable competitive advantage?

Origins: Shipbuilding on Lake Michigan (1902-1924)

The city of Manitowoc, Wisconsin sits roughly 80 miles north of Milwaukee, positioned strategically where the Manitowoc River empties into Lake Michigan. In the early twentieth century, this geography was destiny. The Great Lakes represented America's internal ocean—a vast commercial highway connecting Midwestern industry to Eastern markets. Whoever controlled shipbuilding along these shores controlled a critical piece of American commerce.

The only shipyard for sale on the shores of Lake Michigan was located in Manitowoc, Wisconsin. Owned by brothers Henry and George Burger, the Manitowoc operation had grown large and lucrative from its extensive wooden ship repair business. Having found an acquisition that ideally suited their purposes, West and Gunnell bought the Burger and Burger shipyard in 1902 for $110,000.

Gunnell assumed the position of president and West became the general manager of the new Manitowoc Dry Dock Company. The first vessel launched by Manitowoc Dry Dock was the Cheguamegon, a wooden passenger steamer already under construction at the time of the purchase.

Charles West was a detail-obsessed engineer who understood that survival in shipbuilding demanded constant technical improvement. By 1903, however, the company had contracted its first steel ship repair job, and by 1905 the firm had launched the passenger steamer Maywood, the first steel vessel built in the Manitowoc shipyard. The transition from wood to steel was not merely technical—it represented a fundamental bet on the future of American industry.

The company's early decades established the DNA that would carry Manitowoc through multiple reinventions. By World War I, the shipyard employed around 2,500 workers, primarily men skilled in welding, riveting, and joinery, and had grown to include six major buildings capable of producing 18 ships annually. To accommodate the influx of laborers, the company facilitated the construction of over 100 worker homes and even converted a steamer into a floating hotel, enhancing community stability and positioning Manitowoc as a key maritime hub. These developments not only boosted employment but also stimulated related commerce, such as suppliers and services, contributing significantly to the region's prosperity through the 1910s.

But the most extraordinary chapter came with World War II. When America needed submarines—and needed them quickly—the Navy turned to an unlikely source: a freshwater shipyard that had never built a military vessel.

The Manitowoc Shipbuilding Company, headed by Charles West, petitioned the Navy to build destroyers but was asked instead to build submarines—the most sophisticated technological platforms at the time. Due to the availability of skilled craftsmen in the area the company was able to produce a total of twenty-eight Gato and Balao Class submarines between 1941-1945.

Manitowoc had never built a submarine before, but the first was completed 228 days before the contract delivery date. Contracts were awarded for additional submarines, and the last submarine was completed by the date scheduled for the 10th submarine of the original contract.

The logistical challenge was immense. How do you get a submarine from Wisconsin to the Pacific Ocean? Initial sea trials were done in Lake Michigan. Later the submarines were sent down the Mississippi River to New Orleans for final completion and fitting out.

Manitowoc had never built a submarine before, but the first was completed 228 days before the contract delivery date. Contracts were awarded for additional submarines, and the last submarine was completed by the date scheduled for the 10th submarine of the original contract. Total production of 28 submarines was completed for $5,190,681 less than the contract price.

This performance—under budget, ahead of schedule—established a reputation for engineering excellence that would serve Manitowoc for decades. The submarines themselves compiled a remarkable combat record. The submarine USS Rasher (SS-269) was at test depth in the Bering Sea—one of the Manitowoc boats—became the second-highest tonnage sinker among U.S. submarines during the war.

During World War II, the Manitowoc Shipbuilding Company built 28 submarines for the United States Navy. More than 7,000 men and women worked around the clock, 365 days a year to build some of the best submarines in the Navy.

The wartime experience demonstrated something crucial about Manitowoc's character: this was a company that could master complexity, execute under pressure, and adapt its engineering capabilities to radically different products. That entrepreneurial DNA would prove essential for what came next.

The Crane Pivot: A New Business Is Born (1925-1960s)

After World War I, Charles West faced a classic entrepreneur's dilemma. Shipbuilding was cyclical, dependent on government contracts and merchant fleet renewal cycles. The machine shops that had built submarines sat partially idle. West needed a second act.

After World War I, The Manitowoc Shipbuilding Company was looking to diversify their business. After observing the Moore Speedcrane, manufactured in Fort Wayne, Indiana, Charles West thought cranes were a way to expand the business and use his shipyard's machine shops. In 1925, The Moore Speedcrane Company was in debt, and Charles West was willing to help them build cranes to help provide cash for the struggling company.

The Moore Speedcrane Company was teetering on bankruptcy—a perfect opportunity for a cash-rich shipbuilder looking for diversification. West recognized that crane manufacturing shared much with shipbuilding: heavy steel fabrication, precision engineering, and the need to lift enormous weights safely. The skills were transferable; only the end product differed.

All patents were signed over to Manitowoc as a liability; however, they would not sell any machines under the Manitowoc name. The Speedcrane in 1925 was a steam-driven, 15-ton capacity crane that sat on four wheels. Ten models were built by Manitowoc from this basic model.

Eventually, after listening to customer feedback, Moore redesigned the crane and installed a gasoline engine. Another major change was the replacement of the wheels with a crawler base that allowed for better traction. The first model from the redesigned Speedcrane was a Model 100. The Moore Speedcrane Company continued to introduce new models with innovative features; however, this put them deeper into debt. In 1928, when it was apparent that Moore was not going to be able to pay back the debts owed to Manitowoc, they began to manufacture and sell Speedcranes with its own sales force.

By taking control of production in 1928, Manitowoc made its decisive entry into crane manufacturing. The timing proved fortuitous: America's construction boom demanded lifting equipment for buildings, bridges, and highways. Manitowoc started off in the early 20th century in shipbuilding, branched out into crane manufacturing in the 1920s, and in the 1940s entered the foodservice sector through the launch of freezer manufacturing.

Following World War II, the construction and infrastructure boom significantly expanded Manitowoc's crane operations, transitioning from shipbuilding roots to a key player in heavy lifting equipment, with crane sales reaching $146.5 million by 1977.

In 1969, Manitowoc introduced its flagship crane, the Model 4100W. This crane became an industry icon, establishing Manitowoc as the premier name in lattice-boom crawler cranes. The company had found its identity: not just a shipbuilder that made cranes, but a crane manufacturer with deep roots in American heavy industry.

The triple diversification strategy—ships, cranes, and foodservice equipment—represented a deliberate attempt to buffer against cyclicality. The U.S. Navy contracted the company to build ten submarines in 1940. Foodservice equipment entered the mix when Manitowoc began manufacturing freezers in 1945.

By mid-century, Manitowoc had become something unusual: a Wisconsin-based conglomerate touching three unrelated industries. Whether this created or destroyed value would become the central question of the company's next fifty years.

Becoming a Diversified Industrial: Three Legs of the Stool (1970s-2000)

Through the 1970s, 1980s, and 1990s, Manitowoc evolved into a textbook diversified industrial. The company's more recent history is marked by several landmark acquisitions including Sturgeon Bay Shipbuilding and Dry Dock Company in 1968, The Shannon Group (commercial refrigerators and freezers) in 1995, and Marinette Marine Corporation in 2000.

Each leg of the stool served a strategic purpose:

Cranes: The high-margin, high-cyclicality business. When construction boomed, crane profits soared. When construction collapsed, so did crane revenues.

Foodservice: A steadier business selling ice machines and refrigeration equipment to restaurants, hotels, and hospitals. Growth was slower but more predictable.

Marine: Government shipbuilding contracts for the Navy and Coast Guard. Manitowoc Marine was a subdivision of the Manitowoc Company, which builds and repairs commercial and military ships at yards in Marinette, Wisconsin; Sturgeon Bay, Wisconsin; and Cleveland, Ohio. The Marinette shipyard, Marinette Marine, built the first Freedom class littoral combat ship for the United States Navy, and the United States Coast Guard Cutter Mackinaw.

The logic was appealing: when cranes slumped, foodservice kept the lights on. When commercial shipbuilding contracted, Navy contracts provided backlog. Management argued that shared engineering expertise created synergies across divisions.

In 2000, Manitowoc demonstrated its continued prowess in product development with a crane that would become legendary. Manitowoc unveiled the 250-ton lattice boom crawler crane, Model 999, during 2000 Intermat in Paris, one of the world's largest construction equipment trade shows. Model 999 is a 250 tonnes (275 US ton) capacity class crawler crane, which was one of the industry's popular size range.

"The Model 999 has been a firm favorite with contractors in the heavy construction and energy sectors for 20 years, providing enough reach and capacity to tackle virtually any job," says Manitowoc Cranes Product Manager Brennan Seeliger. The crane became so successful that Manitowoc eventually modernized and rebranded it as the MLC250.

But even as Manitowoc celebrated its centennial in 2002, a transformation was underway. The company's leadership saw an opportunity to become something far larger—a global crane powerhouse built through aggressive acquisition. The quiet Wisconsin conglomerate was about to go shopping.

The Acquisition Spree: Building a Crane Empire (2001-2008)

Glen Tellock joined Manitowoc as CFO in 1995 and became CEO in 2005. But even before taking the top job, Tellock was the architect of Manitowoc's most ambitious expansion. His vision: transform Manitowoc from a regional player into a global crane leader through acquisition of the industry's premier brands.

The Potain Acquisition (2001)

The first major move came in 2001 with the acquisition of Potain, the French tower crane manufacturer.

In May 2001 the firm laid out about $307 million in cash and assumed $138.8 million in debt for Potain S.A. (later renamed Potain SAS). At the time a subsidiary of Groupe Legris Industries SA, Potain was headquartered near Lyon, France, and was a global leader in tower cranes for the building and construction industry. With annual sales of about $300 million, Potain operated eight manufacturing facilities in France, Germany, Italy, Portugal, and China, and distributed its cranes to more than 50 nations.

The strategic logic was compelling. Manitowoc dominated crawler cranes—the behemoths used for heavy industrial lifts. But tower cranes—the tall, fixed structures that dot urban construction sites—represented a massive market segment where Manitowoc had no presence. Potain filled that gap instantly.

The addition of Potain helped push Manitowoc's revenues past the $1 billion mark for the first time in 2001.

The Grove Acquisition (2002)

Just one year later, Manitowoc made an even bolder move. Manitowoc acquired the Potain brand in 2001, followed by Grove and National Crane in 2002. The announcement to acquire Grove Worldwide was made in March 2002 at CONEXPO in Las Vegas, Nevada. Manitowoc purchased Grove for $271 million.

In August 2002 Manitowoc acquired Grove Worldwide for about $278 million. Grove, which had just emerged from bankruptcy, was one of the world's leading makers of mobile telescopic cranes.

Grove was a crown jewel—the premier brand in mobile telescopic cranes. In fiscal year 2001, Grove reported revenues of more than $700 million. By acquiring a company fresh from bankruptcy, Manitowoc obtained one of the industry's most recognized names at a distressed price.

"The Grove acquisition, combined with last year's acquisition of Potain, the worldwide leader in tower cranes, gives Manitowoc the broadest product line in the business," said Rob Giebel, president of Manitowoc's Crane Group.

The two Crane purchases significantly expanded Manitowoc's presence overseas, with sales outside North America increasing from less than 6 percent in 2000 to more than 21 percent two years later. Nevertheless, this acquisition spree did not come without a price. Manitowoc posted a net loss of $20.5 million in 2002 thanks to $74 million in special charges, including costs incurred restructuring some of the crane and foodservice operations. The substantial expansion of the crane business, which now generated more than 60 percent of overall revenues, left Manitowoc dependent once again on a more cyclical business just as the global economy was struggling mightily.

Building the Brand Portfolio

Within 18 months, Manitowoc had assembled a portfolio of premier crane brands. Its diversified portfolio of five premier brands—Grove, Manitowoc, National Crane, Potain, and Shuttlelift—addresses a broad spectrum of customer needs, from urban development to large-scale industrial projects. This brand ecosystem, developed through strategic historical acquisitions, supports Manitowoc's role as a key supplier in the estimated USD 35.58 billion global crane market as of 2023.

The Enodis Foodservice Acquisition (2008)

Even as Manitowoc built its crane empire, Tellock wasn't done. In 2008, he made a massive bet on the foodservice side.

The $2.7-billion acquisition will establish Manitowoc among the world's top manufacturers of commercial foodservice equipment. Manitowoc also is one of the world's leading producers of cranes and innovative lifting solutions for the global construction industry.

Listed in London and operationally headquartered in Tampa, Fla., Enodis, a global provider of commercial foodservice equipment with a variety of brands, reported revenues of 0.8 billion pounds Sterling (US $1.7 billion) for the 12 months ended March 29, 2008. Enodis is a major supplier of foodservice equipment, with products on the "cold" and "hot" sides of the industry. To date, Manitowoc Foodservice's focus has been on "cold" equipment. A combination with Enodis will allow Manitowoc to enter two major new market segments, hot foodservice and food retail equipment, as well as expand its cold-side businesses.

The acquisition was transformational—but it came with complications. In 2008, the company acquired Enodis PLC, a UK-based supplier of restaurant equipment, including fryers, ovens, and ice machines. Manitowoc Foodservice was required to sell off the ice division of Enodis, including the Ice-O-Matic, Scotsman, Simag, and Barline brands, to address antitrust concerns.

Tellock's vision was clear: build a diversified industrial with two giant legs—cranes and foodservice—each capable of supporting the company through the other's cyclical troughs. But this very diversification would become the target of activist investors who saw the structure as value destruction rather than value creation.

The Activist Storm (2014-2015)

By 2013, the strategic logic that had guided Manitowoc for decades was coming under attack. Manitowoc's crane business has been hampered by weak demand. The crane business accounted for nearly 62 percent of Manitowoc's total revenue of about $4 billion in 2013.

The poor performance for the cranes business has hurt Manitowoc's stock performance so far this year. Shares are down about 11% in 2014, while the Dow Jones Industrial Average has risen by nearly 10%.

Relational Investors Opens the Attack

In June 2014, the first activist appeared at the gates.

Relational Investors LLC was co-founded by Ralph Whitworth and David Batchelder. It filed a 13D with the SEC last week and said it acquired 11.5 million shares, or an 8.52% stake, in Manitowoc (MTW). The activist investor has urged for a spinoff Manitowoc's Foodservice business.

In the middle of 2014, Relational Investors was busy notching another activist victory, this time at Timken (TKR), while also building up the case on its newest target, The Manitowoc Company (MTW). In short, the firm argued that a foodservice business selling machinery to restaurants didn't have any reason to be paired with a crane equipment business.

Relational's argument was straightforward: Manitowoc was suffering a classic "conglomerate discount." Investors who wanted exposure to construction equipment were forced to also own foodservice manufacturing. Investors interested in restaurant equipment had to accept crane cyclicality. The result was neither fish nor fowl—and a stock price that undervalued both businesses.

The activist fund further said it has "direct and recent experience engaging companies suffering similar discounts" at the Timken Company (TKR), B/E Aerospace, Inc. (BEAV), ITT Corporation (ITT), Ingersoll-Rand Public Limited Company (IR), and Agilent Technologies, Inc. (A). For these companies, separation incongruent businesses led to significant value creation. "This experience gives us confidence in our analysis of the potential value creation available to the company (Manitowoc)," Relational added.

In response, Manitowoc's chairman and chief executive officer, Glen E. Tellock, said in a press release that the company "will continue to consider and review Relational Investors' suggestions."

Management pushed back, publishing slides in September 2014 defending the combined structure. While Relational Investors was attempting to split Manitowoc, management pushed back, publishing slides in September explaining why its Crane and Foodservice businesses share some synergies. Their arguments included diversifying the company's portfolio and improving procurement, scale, and back-office functions.

Then fate intervened. Ralph Whitworth, Relational's legendary co-founder, fell ill. The activist campaign appeared to stall. But nature, in markets, abhors a vacuum.

Carl Icahn Picks Up the Baton

On December 29, 2014, a new player entered the arena. Carl Icahn—the corporate raider who had terrorized boardrooms since the 1980s—disclosed a position in Manitowoc.

Activist investor Carl Icahn has acquired a 7.77-percent ownership stake in Manitowoc and plans to influence the crane and food-services equipment manufacturer to break up into two separate companies, according to an SEC filing.

The decision to split comes roughly a month after Carl Icahn on Dec. 29 joined an activist campaign at Manitowoc. Icahn essentially took the lead on a 6-month-old investor insurgency previously launched by Relational Investors in June. Both high-profile activists had been pressing Manitowoc to separate the cranes business from the foodservice operations, but how big a role Relational played lately was unclear because the activist fund recently began winding down its $6 billion portfolio after its co-founder Ralph Whitworth took a leave from the firm in July for health reasons. Icahn owns 7.8% of Manitowoc, and Relational has an 8.5% stake, so their combined investment represented a formidable obstacle to anyone at Manitowoc who might have wanted to go against them.

Icahn's business model is to take large stakes in companies that he believes will appreciate from changes to corporate policy; Icahn then pressures management to make the changes that he believes will benefit shareholders, and him. Widely regarded as one of the most successful hedge fund managers of all time and one of the greatest investors on Wall Street, he was one of the first activist shareholders and is credited with making that investment strategy mainstream for hedge funds.

Manitowoc's defenses were significant. Wall Street sources have said Icahn would find it challenging to gain support of a majority of board members because directors' terms are staggered so that only a few directors stand for election annually. Manitowoc also has an anti-takeover "poison pill" in place to block individual investors from gaining more than 20 percent of the company's stock.

But governance defenses could only delay, not prevent, the inevitable when two major activists controlled roughly 16% of outstanding shares.

Management Capitulates

The speed of capitulation surprised even seasoned observers. In late January, Manitowoc announced it would pursue separating the company's two business segments, and less than two weeks later announced that it had reached an agreement with Icahn, which would allow him to appoint a person to the board of both Manitowoc, and the new company when it is formally spun off in 2016.

Under intense pressure from high-profile activists Carl Icahn and Relational Investors LLC, Manitowoc Co. (MTW) announced Thursday afternoon that it is splitting into two publicly traded companies — one for its construction cranes business and the other for its foodservice equipment operation. "The plan for separation is the next logical step in Manitowoc's evolution," Glen E. Tellock, president of Manitowoc, told analysts and reporters on a conference call. "The two companies will attract long-term shareholders that are appropriate for their business profiles and will help investors value each company separately." Manitowoc said it plans to complete the separation through a tax-free spinoff of its foodservice business, a transaction it expects to be completed in the first quarter of 2016. The spinoff was announced as Manitowoc reported slightly lower revenue and operating earnings in the fourth quarter of 2014 than in the same period a year earlier.

"After a comprehensive evaluation, including a thorough review of the current and projected operating environments for the two segments, we have determined that the Cranes and Foodservice businesses are best-suited to realize their full potential on a standalone basis," said Glen E. Tellock, Manitowoc chairman and CEO.

It was a complete reversal. The same CEO who had argued for conglomerate synergies was now echoing the activists' talking points. Analysts had argued when the Relational campaign was announced in June that Tellock might fight to keep the two businesses together after he helped create a combined crane and foodservice business based on the argument that the steadier cash flow generated by the foodservice business and its steady growth would act as a buffer that supports the highly volatile and cyclical crane business, which needs seasonal working capital, through more difficult times. Nevertheless, on Thursday in the conference call, Tellock made many of the same arguments that Relational Investors managers have offered up as a justification for the separation: namely that the parting allows each company to attract their own set of long-term shareholders that match up better for each unique business profile.

In 2015, Manitowoc Foodservice, Inc. budged into Icahn activism, agreeing to separate its Cranes and Foodservice businesses. The investor also got his way by gaining a seat on the board.

The activist campaign had succeeded in roughly seven months. One hundred years of corporate history was being unwound in a matter of weeks.

The 2016 Spin-Off

Executing the Split

On March 4, 2016, Manitowoc's board executed the separation that activists had demanded.

The spin-off was achieved through a tax-free distribution to Manitowoc shareholders of one share of Manitowoc Foodservice stock for every share of Manitowoc stock held at the close of business on the record date of February 22, 2016. Beginning today, MFS shares will commence "regular-way" trading on the NYSE.

"We are extremely pleased to complete the spin-off of Manitowoc Foodservice. Under the leadership of Barry Pennypacker and Hubertus Muehlhaeuser, both Manitowoc Cranes and Manitowoc Foodservice are well positioned as independent, public companies to generate sustainable growth and value creation for their respective shareholders," said Kenneth W. Krueger, Manitowoc's chairman and interim chief executive officer.

Two Distinct Companies Emerge

The separation created two very different businesses:

Manitowoc (MTW): A pure-play crane company continuing to trade on NYSE. Founded in 1902, The Manitowoc Company, Inc. is a leading global manufacturer of cranes and lift solutions with 49 manufacturing, distribution, and service facilities in 20 countries.

Manitowoc Foodservice (MFS): Manitowoc Foodservice, Inc. designs, manufactures and supplies best-in-class food and beverage equipment for the global commercial foodservice market, offering customers unparalleled operator and patron insights, collaborative kitchen solutions, culinary expertise and world-class implementation support and service. Headquartered in Tampa, Florida, and operating 20 facilities throughout the Americas, Europe and Asia, the company sells through a global network of over 3,000 distributors and dealers in over 100 countries. The company has more than 5,000 employees and generated sales of $1.5 billion in 2015.

The spin-off of the Foodservice business will lead to enhanced capital allocation policies, strategic flexibility, and distinct business profiles that will appeal to investors. Manitowoc will be able to focus on its growth strategy as market conditions improve.

What Happened to Foodservice?

The story of the spun-off foodservice business provides a coda to this corporate drama.

On March 4, 2016, The Manitowoc Company completed a one for one common share split and created Manitowoc Foodservice. As of March 7, 2016 the newly created company began standard stock offerings on the NYSE under the symbol "MFS" Manitowoc Foodservice rebranded itself as Welbilt, Inc. and traded under the symbol "WBT".

Manitowoc Foodservice consisted of 23 global brands that include 12 holding either #1 or #2 position in their respected global markets. In 2022 Welbilt was acquired by the Italian Ali Group. As part of the acquisition, Manitowoc Ice was sold off to British-American firm Pentair to address antitrust concerns.

The foodservice business ultimately found its home with a strategic acquirer, validating the activists' argument that the parts were worth more separately than together. But for Manitowoc's remaining shareholders, the question was now: Could a pure-play crane company survive the industry's brutal cyclicality without the foodservice cushion?

Life as a Pure-Play Crane Company (2016-2020)

The years immediately following the spin-off proved difficult. Manitowoc was now fully exposed to construction cyclicality without the diversification buffer that management had long argued was essential.

In 2016, we spun off our foodservice business. At that point, it was a real battle to become a sustainable standalone crane company. So we spent the next four or five years really focused on repositioning our manufacturing footprint and our cost position removed well more than $100,000,000 during that time.

The company underwent painful restructuring. Factories were consolidated. Headcount was reduced. Product lines were rationalized. Manitowoc has reduced costs by over $100 million since 2016 and is implementing the Cranes+50 strategy to double non-new machine sales.

Manitowoc produces several lines of cranes to serve the construction, energy, and numerous other industries. The company produces high-capacity lattice-boom crawler cranes, tower cranes, and mobile telescopic cranes for heavy construction, commercial construction, residential construction, energy-related uses, wind farm, infrastructure, duty-cycle, crane-rental applications, among others.

Manitowoc's products are prominently used in infrastructure development, renewable energy initiatives like wind farm installations, and urban construction projects.

End markets diversified—wind energy, infrastructure spending, petrochemical construction—but the fundamental cyclicality remained. When COVID-19 struck in 2020, construction projects halted worldwide. Manitowoc's revenues contracted. The critics who had warned that a standalone crane company couldn't weather downturns appeared vindicated.

But crisis often catalyzes strategic clarity. In the depths of 2020, Manitowoc's leadership made a decision that would reshape the company's trajectory.

CRANES+50 Strategy (2021-Present)

Strategic Pivot to Aftermarket

Aaron Ravenscroft became Manitowoc's CEO in 2018, inheriting a company still finding its footing as a standalone crane manufacturer. By 2021, he unveiled a strategic transformation that would address the company's fundamental challenge: cyclicality.

Adding a little more clarity and focus to our strategy, I am pleased to announce our vision for aftermarket, which we call Cranes+50. Our goal is to increase our aftermarket or non-new machine sales by 50% over the next five years. Historically, our business model has been highly product focus. Our objective is to grow beyond machines and products and to sell more aftermarket parts, field service, lifting solutions, RPOs, rentals for fleet management, used sales, remanufactured cranes, and digital solutions that provide greater customer connectivity.

And then to 2020, which happened to coincide with COVID is when we really started to turn the corner, become aftermarket focused and launched our Cranes plus 50 strategy, which has been to double our non new machine sales starting in that low 400s.

The insight was profound: crane manufacturers live or die by new machine sales, which collapse during downturns. But the installed base of cranes requires parts, service, and support regardless of economic conditions. A crane sitting idle still needs maintenance. An aging fleet still needs renovation.

"On the back of our four strategic initiatives, we are introducing Cranes+50, which codifies our ambition to increase our non-new machine sales by 50 % over the next five years. Growing our aftermarket business is critical to reducing our cyclicality and expanding our margins long-term," concluded Ravenscroft.

Manitowoc's 'CRANES+50 strategy', launched in 2021, focuses on diversifying revenue beyond new machine sales. This includes growing aftermarket parts, services, rentals, used cranes, and digital solutions to create more stable revenue streams.

Recent Acquisitions and Distribution Expansion

To execute the CRANES+50 strategy, Manitowoc needed to get closer to customers. That meant building out direct distribution and service capabilities.

The Manitowoc Company, Inc. has completed the acquisition of substantially all the assets of Aspen Equipment Company ("Aspen"), a diversified crane dealer and a leading final-stage, purpose-built work truck upfitter for approximately $51 million. "We are pleased to welcome the Aspen team to the Manitowoc family. Our combined businesses provide unique synergies to accelerate our growth in the coming years. From a new machine perspective, Aspen's upfitting business fits nicely with our National Crane boom truck business and will enable us to better serve key end markets, such as utility and telecommunications customers. Additionally, Aspen's aftermarket business will complement our previously announced acquisition of H&E's Crane business."

The acquisition of Aspen will expand Manitowoc's direct-to-customer footprint in Iowa, Nebraska, and Minnesota with new sales, used sales, parts, and service to a variety of end markets. Aspen's field support team brings industry-leading technical competencies and exceptional customer support. In addition, Aspen's specialized crane and truck equipment upfitting capabilities provide greater depth of product offerings to a wider base of customers including loyal Manitowoc customers.

In 2021, Manitowoc completed the acquisition of substantially all of the assets of Aspen Equipment Company, a diversified crane dealer and a leading final stage purpose-built work truck upfitter, and substantially all of the assets and liabilities of the crane business of H&E Equipment Services, Inc. ("H&E"), one of the largest rental equipment companies in the U.S.

Manitowoc Cranes produces five brands of cranes: Grove, National Crane, Shuttlelift, Manitowoc, and Potain. In addition, Manitowoc has two distribution businesses based in the U.S.: Aspen Equipment and MGX Equipment Services (formerly H&E Equipment Services' crane business).

Current Financial Position

The CRANES+50 strategy has delivered measurable results.

"Our 2024 results highlight the strength of our aftermarket business which generated a record $629.1 million of revenue. Comparing to 2020, the year before the launch of our CRANES+50 strategy, non-new machine sales have increased by over 67%."

In the latest financial report, Manitowoc reported flat year-over-year net sales of $596.0 million for the fourth quarter of 2024, with a notable net income of $56.7 million. For the full year, net sales slightly decreased by 2.2% to $2,178.0 million, while non-new machine sales saw a modest increase. Despite challenges in the market, the company showed resilience with strong cash flow generation and maintained its strategic focus on the aftermarket business. Key financial highlights include a fourth-quarter adjusted EBITDA of $34.9 million, a slight decrease from the previous year, and significant improvements in net cash provided by operating activities, which increased by $71.0 million. The company achieved a record revenue of $629.1 million from its aftermarket business, demonstrating the success of its CRANES+50 strategy and the growing demand for non-new machine sales.

"In early February, we acquired the distribution rights for the Carolinas and Georgia which expands our aftermarket footprint in the U.S. In addition, we are excited to showcase our new innovative products as well as a variety of aftermarket services at bauma 2025 in April."

Trailing twelve-month revenue reached $2.13 billion as of the third quarter of 2025, reflecting improved market conditions in mobile and tower cranes following the spin-off restructuring. In terms of profitability, the third quarter of 2025 marked a strong performance, with net sales of $553.4 million, representing a 5.4% increase year-over-year, supported by favorable product mix and aftermarket contributions. Orders for the same period totaled $491.4 million, up 15.7% from the prior year, leading to a backlog of $666.5 million. Adjusted EBITDA rose 30.2% to $34.1 million, while net income improved to $5.0 million. The company has actively managed its balance sheet, with total debt standing at $500.4 million as of September 30, 2025, down from higher levels in prior years amid ongoing deleveraging efforts.

Product Innovation & Technology

Recent Innovations

Manitowoc has maintained its reputation for engineering excellence through continuous product development.

Manitowoc used bauma 2025 to reveal details of its largest Potain luffing jib crane for the European and North American markets. The MR 819 has up to 70 m of jib available and a maximum capacity of 64 t – double that of the current largest Potain luffing jib tower cranes, the 32 t capacity MR 608B and MR 618. Manitowoc's Voice of the Customer (VOC) program was crucial to developing the latest flagship model, which addresses the demand for large luffing jib tower cranes to handle heavy precast elements and support infrastructure projects such as bridges and nuclear power plants.

With a maximum capacity of 64 tonnes and up to 70 metres of jib, the MR 819 significantly surpasses its predecessors—the MR 608B and MR 618—which offer a 32-tonne capacity. The development of this high-capacity crane was heavily influenced by Manitowoc's Voice of the Customer (VOC) program, which identified a growing need for larger luffing jib cranes to handle substantial precast components and support critical infrastructure developments like bridge and nuclear facility construction.

Smart Technology

Grove and Potain will highlight smart technology with the Grove CONNECT™ and Potain CONNECT™ platforms. These enable real-time fleet management and crane performance tracking, as well as remote crane diagnostics, which lets users diagnose faults or prep for service and repairs remotely.

Technological advancements are driving the evolution of cranes towards becoming smarter, safer, and more sustainable. This includes greater integration of the Internet of Things (IoT), enabling real-time data collection, remote diagnostics, and predictive maintenance. Automation and remote operation are becoming more common, especially in hazardous environments, and there's a growing emphasis on energy efficiency, with increasing demand for hybrid and battery-powered cranes. Enhanced safety features, such as anti-collision systems and VR training modules, are also becoming standard.

The GMK6450-1 is the strongest heavy-duty 6 axle crane on the market with a self-rigging MegaWingLift™ (rigging time < 20 min). Able to take on jobs that would usually require a seven- or eight-axle model, this outstanding 450 t all-terrain crane features an improved hydraulic system with faster flow to provide quicker operating speeds and even smoother movements.

Competitive Landscape Deep Dive

Major Competitors

The top participants in the mobile crane market are Liebherr (Switzerland), Terex (USA), Tadano (Japan), XCMG (China), Sany (China), Manitowoc (USA), Zoomlion (China), Konecranes (Finland), Kobelco (Japan), Demag (Germany).

Liebherr stands out with its extensive product range and innovative engineering solutions, enabling it to maintain a strong presence globally. Terex, known for its diverse portfolio, leverages its expertise in manufacturing to cater to various sectors, enhancing its market influence. Tadano emphasizes reliability and performance, particularly in the Asian markets, while XCMG and Sany represent significant growth in the Chinese sector, combining technological advancements with competitive pricing. Manitowoc, with its focus on high-capacity cranes, appeals to heavy-lift projects, whereas Zoomlion continues to expand its footprint through strategic investments in R&D. Konecranes, recognized for its advanced automation solutions, and Kobelco, with its strong reputation in hydraulic cranes, further enrich the competitive landscape.

Competitive Dynamics

A major global competitor, Liebherr is recognized for its strong emphasis on engineering innovation and advanced technology in its crane offerings. This Chinese manufacturer leverages substantial production capacities and competitive pricing, particularly impacting emerging markets. Terex competes across various equipment categories, including lifting and material handling, in addition to cranes. Tadano is known for introducing new models with enhanced lifting capacities and operational efficiencies, driven by technological advancements.

The competition extends beyond new equipment sales into the critical aftermarket segment, encompassing parts, service, and rentals. Manitowoc's strategic focus on growing non-new machine sales directly engages with rivals who also prioritize aftermarket support. The industry faces cyclical pressures; for instance, a slowdown in the European tower crane market in 2024 impacted Manitowoc, illustrating the intense competitive environment. Furthermore, factors like U.S. dealer reluctance to commit to orders due to tariff uncertainties can shift market dynamics among global players. Emerging competitors focusing on automation and electrification also present potential disruptions to the traditional competitive landscape, highlighting the need for continuous innovation and adaptation in the Manitowoc Company competitive landscape. Engineering innovation and advanced technology are key differentiators for competitors like Liebherr and Tadano.

Market Size and Position

The company is a key player in the global mobile crane market, which was valued at USD 17.2 billion in 2024. Manitowoc is also a significant competitor in the global tower crane market, valued at USD 7.7 billion in 2024. The company's 'CRANES+50 strategy' is designed to enhance its market position by diversifying revenue.

Strategic Analysis: Bull and Bear Cases

The Bull Case

Aftermarket Transformation Creating Durable Value: The CRANES+50 strategy represents a fundamental shift from a cyclical equipment manufacturer to a recurring-revenue service business. Aftermarket revenue—parts, service, training, digital solutions—is higher margin and less cyclical than new machine sales. With non-new machine revenue up 67% since 2020, Manitowoc is demonstrating that this transformation is real, not aspirational.

Brand Portfolio Creates Switching Costs: Manitowoc's five premier brands—Grove, Manitowoc, Potain, National Crane, Shuttlelift—represent the accumulated expertise of decades. Crane operators train on specific platforms. Fleet owners standardize on specific brands. Parts availability, service expertise, and operator familiarity create meaningful switching costs.

Infrastructure Spending Tailwinds: Government infrastructure programs globally—from the U.S. Infrastructure Investment and Jobs Act to European green energy investments—create sustained demand for lifting equipment. Wind turbine installation, bridge construction, and port modernization all require cranes.

Direct Distribution Building Relationship Assets: The acquisitions of Aspen Equipment and H&E's crane business bring Manitowoc closer to end customers. Direct relationships enable better pricing, faster service response, and deeper customer insights that inform product development.

The Bear Case

Cyclicality Remains Fundamental: Despite aftermarket growth, new crane sales still constitute the majority of revenue. When construction collapses, Manitowoc's revenues contract sharply. No amount of aftermarket revenue can fully offset the brutal cyclicality of heavy equipment.

Chinese Competition Intensifying: XCMG, Sany, and Zoomlion are expanding globally with competitive products at aggressive price points. Chinese manufacturers have captured dominant positions in emerging markets and are increasingly targeting developed markets. This threatens Manitowoc's market share, particularly in price-sensitive segments.

Technology Disruption Risk: Electrification and autonomous operation could reshape the crane industry. Established players with massive installed bases of diesel-powered equipment face stranded asset risk if the transition accelerates. Manufacturers who lead the electrification transition could capture disproportionate market share.

Scale Disadvantages: As a ~$2 billion revenue company, Manitowoc lacks the scale of larger competitors like Liebherr or the Chinese majors. This limits R&D investment capacity, manufacturing efficiency, and purchasing power.

Porter's Five Forces Analysis

Threat of New Entrants (Low): Crane manufacturing requires substantial capital investment, engineering expertise, and brand reputation built over decades. The regulatory environment for lifting equipment is demanding. New entrants face years of effort before achieving competitive credibility.

Supplier Bargaining Power (Moderate): Steel and componentry suppliers have some power given commodity volatility, but Manitowoc's scale provides meaningful purchasing leverage. Vertical integration in key components reduces supplier dependency.

Buyer Bargaining Power (Moderate to High): Large rental companies and construction contractors can demand volume discounts. However, brand loyalty, parts availability, and service proximity create switching costs that limit buyer power.

Threat of Substitutes (Low): For heavy lifting applications, there are few alternatives to cranes. Helicopters can perform some lifting tasks but at vastly higher cost. The installed base of lifting equipment worldwide ensures sustained crane demand.

Competitive Rivalry (High): The global crane market features intense competition among established players, compounded by Chinese competitors expanding internationally. Product differentiation is challenging given functional similarity across brands. Cyclical demand exacerbates competitive pressure during downturns.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Moderate. Manitowoc benefits from manufacturing scale but lacks the overwhelming size advantages of larger competitors.

Network Economies: Weak. Crane markets do not exhibit traditional network effects.

Counter-Positioning: Emerging. The CRANES+50 strategy potentially creates counter-positioning if traditional competitors remain focused exclusively on new equipment sales and fail to invest in aftermarket capabilities.

Switching Costs: Moderate to Strong. Operator training, parts standardization, and service relationships create meaningful switching costs, particularly for fleet customers.

Branding: Strong. Grove, Potain, and Manitowoc represent decades of accumulated brand equity in their respective segments. Brand matters in an industry where equipment failure can cause catastrophic accidents.

Cornered Resource: Weak. Engineering talent is broadly available. No unique resources provide durable competitive advantage.

Process Power: Moderate. Lean manufacturing and Voice of Customer product development processes represent accumulated organizational knowledge, but these are replicable given time and investment.

Key Performance Indicators to Track

For long-term fundamental investors monitoring Manitowoc, two KPIs stand out as essential:

1. Non-New Machine Revenue Growth

This metric captures the success of the CRANES+50 strategy. Starting from a base of approximately $376 million in 2020, the company targeted a 50% increase over five years. With $629 million achieved in 2024 (67% growth), monitoring whether this trajectory continues reveals whether the aftermarket transformation is sustainable or cyclically-driven.

2. Orders-to-Backlog Ratio

Given the cyclical nature of crane demand, the relationship between new orders and backlog provides forward visibility. Strong orders relative to backlog indicate expanding demand; weakness signals approaching headwinds. This metric provides earlier indication of business trajectory than reported revenue.

Conclusion: Lessons from 122 Years

The Manitowoc Company's journey from Lake Michigan shipyard to global crane manufacturer illuminates timeless principles of business transformation:

First, diversification is a double-edged sword. The conglomerate structure that protected Manitowoc through decades of cyclicality also created the "conglomerate discount" that invited activist attack. Whether combined structures create or destroy value depends on execution and investor preferences—not inherent logic.

Second, activists aren't always wrong. Carl Icahn's intervention forced a split that management had resisted for years. The subsequent success of Welbilt (the spun-off foodservice business) suggests that the parts truly were worth more separately. But this doesn't mean all activist campaigns create value—only that management's resistance to change isn't always justified.

Third, cyclicality demands strategic response. The CRANES+50 strategy represents Manitowoc's attempt to build a more resilient business model. Whether aftermarket revenue can truly cushion cyclical equipment sales remains the central question for the company's next chapter.

Fourth, brand portfolios compound over decades. The acquisitions of Potain, Grove, and National Crane created a brand ecosystem that continues to generate value. This argues for patience in evaluating acquisition strategies—what looks expensive today may prove cheap over twenty years.

Manitowoc historically operated as a product-focused company, enduring the difficulties of the volatile market cycles for new cranes. To achieve sustainable growth, however, in both our sales and earnings, we are placing greater emphasis on growing non-new machine sales (i.e., aftermarket parts, services, rentals, used cranes, and digital solutions). Growing this part of our business will provide us with more annuity-like revenue streams to lessen the impact of the crane market cyclicality.

From Charles West's submarine shipyard to Aaron Ravenscroft's aftermarket transformation, The Manitowoc Company has demonstrated remarkable adaptability. Whether that adaptability will prove sufficient in an era of Chinese competition, technological disruption, and persistent cyclicality remains to be seen. But after 122 years of reinvention, betting against Manitowoc's ability to adapt would be unwise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube