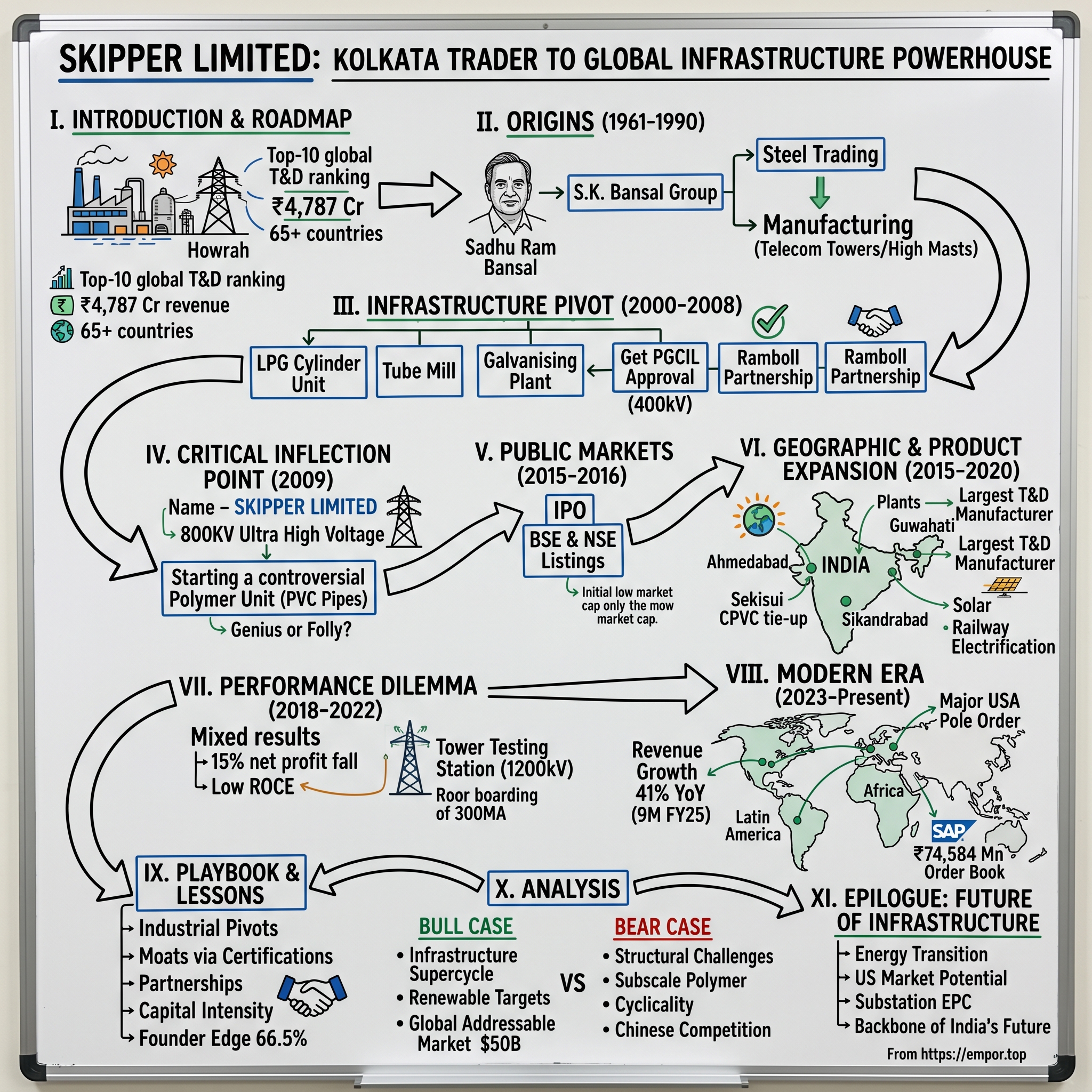

Skipper Limited: From Kolkata Steel Trader to Global Infrastructure Powerhouse

I. Introduction & Episode Roadmap

Picture the sprawling industrial belt of Howrah, just across the Hooghly River from Kolkata. Amid the cacophony of metal grinding against metal, sparks flying from welding torches, and the rhythmic hammering of steel structures, stands one of India's most unlikely success stories. Skipper Limited is a leading manufacturer of Transmission and Distribution (T&D) structures, ranking among the top 10 worldwide, with a Market Cap of ₹5,775-5,791 Crore and Revenue of ₹4,787 Cr.

But this wasn't always the destiny written for Skipper. How does a company that started as a small investment vehicle in the early 1980s—during India's pre-liberalization era of the License Raj—transform into a critical player powering India's electrical grid and now breaking into the lucrative American market?

The answer lies in three pivotal transformations that would have killed most companies: a complete shift from finance to manufacturing, a controversial diversification that analysts still debate, and a global expansion strategy executed from the unlikely headquarters of Kolkata—a city better known for its colonial trading houses than modern manufacturing prowess.

Today's story isn't just about transmission towers and polymer pipes. It's about how a traditional Marwari business family from Kolkata read the tea leaves of India's infrastructure boom decades before it happened, made bold bets that defied conventional wisdom, and built a company that now spans across continents such as Latin America, Europe, and Africa and is spread across 65+ countries.

This is the untold story of Skipper Limited—a masterclass in industrial pivots, timing market cycles, and the delicate art of balancing diversification with focus. Along the way, we'll unpack why entering the PVC pipes business in 2009 was either genius or folly (depending on who you ask), how securing Power Grid approvals became their moat, and what their recent breakthrough order from the United States signals about the next chapter of this remarkable journey.

II. Origins: The S.K. Bansal Story & Early Foundation (1961–1990)

The monsoons of 1961 had just receded from Kolkata when Sadhu Ram Bansal, a young trader with an eye for opportunity, decided to formalize what had been a small trading operation. He founded the S K Bansal Group in 1961, and over the decades, he helped shape the transformation of the Group from a small trading business to a large Market conglomerate. This was Kolkata in its prime—still the commercial capital of India, where fortunes were made in jute, tea, and coal.

But Sadhu Ram wasn't interested in the traditional Marwari businesses that dominated Burrabazar. He saw opportunity in steel—not the glamorous integrated steel plants that Nehru called the "temples of modern India," but the unglamorous business of trading steel products, understanding specifications, building relationships with both producers and consumers. It was a business built on trust, where your word was your bond, and a handshake sealed deals worth lakhs of rupees.

For two decades, the S.K. Bansal Group operated in this ecosystem, learning the rhythms of the steel market, understanding the cyclical nature of infrastructure spending, and most importantly, building relationships that would prove invaluable decades later. By the late 1970s, as India inched toward economic reforms, the younger generation of the Bansal family began pushing for something more ambitious than trading.

The company was incorporated as Skipper Investments Limited in 1981. The name itself was aspirational—a 'skipper' leads the ship, charts the course. Initially, it functioned as an investment vehicle, a common structure for business families to park surplus funds and explore new ventures. But the 1980s were a time of change. The old certainties of the License Raj were crumbling, and whispers of liberalization were in the air.

The transformation began in earnest in 1990. It was renamed Skipper Steels Limited in 1990 and diversified to manufacture Telecom Towers and High Masts. This wasn't a random pivot. The family had spent three decades in steel trading; they understood the material, the suppliers, the quality parameters. More importantly, they saw what others missed—India's telecom revolution was about to begin.

Think about the audacity of this move. Here was a Kolkata-based trading family, deciding to enter manufacturing—not of simple steel products, but of specialized telecom towers. This was 1990, a year before economic liberalization, when getting an industrial license was still a Kafkaesque nightmare, when importing machinery required navigating multiple ministries, when the waiting list for a telephone connection stretched for years.

But the Bansals had done their homework. They knew that whether India liberalized or not, communication infrastructure would be critical. Every telephone connection would need towers, every expansion of the network would require steel structures. They were betting on India's future before that future was even clearly defined.

The early days of Skipper Steels Limited were far from glamorous. The first manufacturing facility was modest—a few rolling mills, basic fabrication equipment, a small team of workers who had to be trained from scratch because telecom tower manufacturing was virtually unknown in India. Quality was inconsistent, orders were sporadic, and the technology was basic.

Yet, what the company lacked in sophistication, it made up for in timing. The telecom sector reforms of 1994 were just around the corner. Private players would soon enter the market. The demand for telecom infrastructure was about to explode. Skipper Steels had positioned itself at exactly the right place, at exactly the right time.

III. The Infrastructure Pivot: Power Transmission Towers (2000–2008)

The new millennium brought with it a different India. The Y2K boom had put Indian technology on the global map, GDP growth was accelerating, and electricity demand was surging. But there was a problem—India's power transmission infrastructure was woefully inadequate. Power generated in coal-rich Chhattisgarh couldn't efficiently reach energy-hungry Mumbai. Hydroelectric power from the Northeast was stranded without transmission lines.

Skipper's management, now increasingly influenced by the second generation of the Bansal family, saw an opportunity larger than telecom towers. The math was simple but compelling: India's peak power deficit was touching 13%, industrial growth was being constrained by power shortages, and the government was finally getting serious about transmission infrastructure. The Power Grid Corporation of India (PGCIL) was ramping up investments.

But first, Skipper needed to build credibility in adjacencies. It set up an LPG Gas Cylinder unit in 2001, followed by establishing its first tube mill in 2003. These might seem like random diversifications, but they were calculated moves. The LPG cylinder unit gave them experience with pressure vessels and quality certifications. The tube mill provided backward integration for their tower business—they could now produce their own raw materials.

In 2005, the company set up its first Galvanising plant. This was crucial. Galvanizing—the process of applying a protective zinc coating to steel—is what gives transmission towers their 50-year life in harsh weather conditions. Most tower manufacturers outsourced this critical process, leading to quality inconsistencies and delays. By bringing it in-house, Skipper could control quality and timelines.

The breakthrough came in 2006. Skipper received Power grid approval for the Tower unit and got an order for 400kV towers in 2006. Getting PGCIL approval was like receiving a knighthood in the transmission tower industry. The qualification process was grueling—prototype testing, factory inspections, financial scrutiny, technical capability assessments. Many companies tried and failed. Skipper passed.

But they didn't go it alone. In a masterstroke of strategic thinking, Skipper Limited tied up with Ramboll, a Danish Engineering company as a manufacturing partner, in the year 2006. Ramboll brought 60 years of transmission line design expertise, sophisticated software for structural analysis, and most importantly, credibility with international clients. The partnership was structured cleverly—Ramboll provided technology and design support, Skipper handled manufacturing and local execution.

Meanwhile, they continued to expand capabilities. In 2007, it forayed into the value addition of Steel Tubes as scaffolding. Again, this wasn't random. The construction boom was underway, infrastructure projects needed scaffolding, and Skipper's steel tubes could serve dual markets—transmission towers and construction.

By 2008, Skipper had transformed from a telecom tower manufacturer to a diversified engineering products company. They could take steel from raw material to finished transmission towers, complete with galvanizing and testing. They had PGCIL approvals, international technology partnerships, and a growing order book.

But the global financial crisis was looming. Credit markets were freezing. Infrastructure spending was about to plummet. What Skipper did next would define its trajectory for the next decade.

IV. The Critical Inflection Point: 2009 Transformation

The year 2009 marked a watershed moment in Skipper's history, though few recognized it at the time. While the world grappled with the aftermath of the Lehman Brothers collapse, Skipper's management made three decisions that would fundamentally alter the company's DNA.

First, the rebranding: It changed its name to Skipper Limited in 2009. Dropping "Steels" from the name wasn't just cosmetic—it signaled ambitions beyond metal. The company was reimagining itself as an infrastructure solutions provider, not just a steel products manufacturer.

The second decision was the one that would make them a true force in power transmission. In 2009, Skipper Limited received an order for 800KV transmission tower from Power Grid Corporation of India Limited. To understand the significance, consider this: 800KV ultra-high voltage transmission is the superhighway of electricity transmission, capable of carrying massive amounts of power across thousands of kilometers with minimal losses. Only a handful of companies globally could manufacture these towers. The technical requirements were extreme—towers standing 150 feet tall, carrying lines with 6,000 MW capacity, withstanding 260 km/hour wind speeds.

But the third decision was the most controversial, one that would divide analysts and investors for years to come. It also commissioned a Polymer production manufacturing Unit in Uluberia, West Bengal and a double side Tube GI Plant in 2009. Simultaneously, Skipper Pipes was started in 2009-2010.

Why would a company that had just cracked the code on high-voltage transmission towers suddenly venture into PVC pipes? The board meetings must have been intense. Here's a company with limited capital, entering a business with completely different dynamics—branded consumer products versus industrial B2B, distributed retail networks versus concentrated government customers, working capital-intensive operations versus project-based cash flows.

The bear case was obvious: loss of focus, management distraction, capital allocation away from the core business where they were gaining momentum. The PVC pipe industry was already crowded with established players like Supreme Industries and Finolex. What could Skipper bring to the table?

But the bull case, as articulated by management, had its own logic. India's agriculture was modernizing, drip irrigation was being subsidized, urban water infrastructure needed upgrading. More importantly, Skipper's existing relationships with electrical contractors could be leveraged—the same contractors installing transmission towers also laid conduit pipes for electrical cables. The dealer network could sell both products. The brand equity in infrastructure could transfer.

The execution strategy was cautious initially. The company mainly focused on the eastern and northeastern markets until 2015-2016. This was Skipper's backyard—West Bengal, Assam, the seven sisters. Competition was less intense here, brand loyalty was still being formed, and Skipper's local reputation carried weight.

The numbers from this period tell an interesting story. While the polymer business was finding its feet, the engineering division was soaring. The 800KV certification opened doors to the most lucrative transmission projects. The government's push for regional grid integration meant more ultra-high voltage lines. Skipper was one of the few qualified suppliers.

V. The Public Markets Journey: IPO and Capital Markets (2015–2016)

By 2015, Skipper had reached an inflection point that many family-owned businesses face: the need for serious capital to fuel the next phase of growth. The transmission tower order book was swelling, the polymer business needed geographic expansion, and working capital requirements were stretching the balance sheet. It was time to tap public markets.

In 2015, Skipper Limited was listed at Bombay Stock Exchange with a market capitalization of over ₹15,000 million (as of March 2015 ending). The IPO process itself was a revelation for a company that had operated in relative obscurity. Road shows in Mumbai's Nariman Point, presentations to mutual fund managers who had never heard of transmission towers, explanations of why a Kolkata-based manufacturing company deserved a premium valuation.

The initial market reception was tepid. Infrastructure stocks were out of favor—the ghosts of the 2010-2013 infrastructure bust still haunted investors. Leverage ratios across the sector were concerning. The polymer diversification confused the equity story—was this an engineering company or a pipes company?

But management persisted. Within months, they secured another crucial listing. The company announced that with effect from 27 May 2015, it has received approval for Listing of equity shares at National Stock Exchange of India. The NSE listing brought liquidity, institutional participation, and importantly, analyst coverage.

In 2016, it was listed in the National Stock Exchange of India with a capital of ₹13,634 million (as of 31 March 2016). The market cap had actually declined from the initial listing—a sobering reminder that public markets can be unforgiving.

But what the public listing did provide was currency for expansion and credibility for large orders. International customers were more comfortable dealing with a listed entity with quarterly disclosures. Banks were willing to extend larger working capital facilities. The company could now offer stock options to attract talent.

The capital raised was immediately deployed. The polymer expansion accelerated—new plants, new geographies, new product lines. The engineering division added specialized capabilities. Most importantly, the company could now bid for larger EPC (Engineering, Procurement, Construction) projects that required significant upfront capital.

VI. Geographic & Product Expansion Era (2015–2020)

Armed with public capital and growing credibility, Skipper embarked on one of the most aggressive expansion phases in its history. The strategy was two-pronged: dominate the domestic transmission tower market while building a pan-India presence in polymer pipes.

The polymer expansion was particularly ambitious. In April 2015, Skipper Limited set up a PVC manufacturing facility in Ahmedabad, Gujarat, with a capacity of 10,000 metric tonnes. The Ahmedabad plant was commissioned with an investment of ₹50 crores. Gujarat was strategic—a large agricultural market, progressive farmers adopting micro-irrigation, and proximity to raw material sources.

By December, they were pushing into India's frontier markets. Skipper entered the Northeast India by commissioning its manufacturing plant in Guwahati, Assam with a capacity to manufacture 4000 MTPA of plumbing and agricultural pipes. The Northeast was virgin territory for organized players—difficult logistics, fragmented markets, but also limited competition and growing construction demand.

The engineering division wasn't standing still. In January 2016, the company set up one of India's largest galvanizing plants in Uluberia, West Bengal. The plant is meant for structures that are 2.5m in diameter and 12m in length. The total galvanizing capacity of the plant is 8000 tonnes per month. This wasn't just about capacity—it was about capability. The ability to galvanize massive structures gave Skipper an edge in bidding for complex projects like river crossings and special towers.

The expansion continued relentlessly. It set up a PVC products plant in Sikandrabad, Uttar Pradesh in 2016, which has a capacity of about 8,000 metric tonnes. UP represented the largest pipes market in India—intensive agriculture, massive rural housing programs, and the government's push for piped water supply.

On the technology front, Skipper was forging crucial partnerships. In 2015, it entered into a partnership with global giant Japan-based Sekisui Chemical as a technology tie-up for manufacturing CPVC Pipes in India. CPVC pipes for hot water plumbing were a premium segment, and Sekisui's technology provided differentiation.

The company's capacity expansion was staggering. The Company increased its T&D manufacturing capacity from 100,000 MTPA to 230,000 MTPA in FY2017. It emerged as the largest manufacturer of T&D Structures in India. Being the largest domestic manufacturer was more than a vanity metric—it meant economies of scale, negotiating power with raw material suppliers, and preferred vendor status with major customers.

In March 2017, the company invested ₹70 crores and set up a new plant in Palasbari, Guwahati, which has a capacity to manufacture 30,000 tonnes of engineering products and 7000 tonnes of polymer products annually. This integrated facility was a template for future expansion—both divisions under one roof, shared overhead costs, operational synergies.

In 2017, Skipper Limited formed a joint venture with Israel-based Metzerplas, a manufacturer of irrigation equipment. Israel's expertise in water management was legendary, and this JV targeted the nascent but fast-growing micro-irrigation market in India.

The company also diversified its engineering portfolio, venturing into Solar Mounting Structure and Railway Electrification Sector. These weren't random diversifications—solar was booming with ambitious government targets, and railway electrification was a national priority with thousands of route kilometers to be converted from diesel.

By 2020, Skipper had transformed from a regional player to a national presence. But the aggressive expansion came at a cost. Working capital was stretched, debt had ballooned, and then COVID-19 struck.

VII. The Performance Dilemma & Mixed Results (2018–2022)

The cracks began showing in June 2018. The company reported a fall of 15% in net profit for the last quarter, with analysts blaming the drop on the decision to diversify into PVC pipes. The criticism was sharp—the polymer business was generating revenues but bleeding margins. The branded play in pipes required continuous advertising spending, the working capital cycle was longer than anticipated, and competition was intensifying.

The numbers painted a mixed picture. In the financial year 2019-20, the company recorded total revenue of ₹1,392.47 crores. This was respectable but not spectacular, especially given the capital employed. The return ratios that investors obsessed over—ROE, ROCE—were underwhelming.

Then came 2020, bringing with it a pandemic that nobody had planned for. Construction sites shut down, transmission line projects were halted, and the pipes market collapsed as real estate and infrastructure spending froze. But Skipper used the crisis to make a strategic investment that would pay dividends later. It commissioned the largest Tower & Monopole Load Testing Station in India in 2020, also one of the largest in the world.

This testing station was a masterstroke. It allowed Skipper to test towers up to 1200kV—specifications that didn't even exist commercially yet. It positioned them for the next generation of transmission infrastructure. International customers were impressed; it demonstrated serious technical capability.

The recovery from COVID was swift. The company reported total revenue of ₹1,711.09 crores in March 2022, while it had registered ₹1,585.53 crores in March 2021. The engineering division was firing on all cylinders, driven by the government's massive push for renewable energy integration, which required extensive transmission infrastructure.

Skipper Pipes has a turnover of ₹330 crores in 2022, contributing to around 19 percent of Skipper's total revenues. After years of investments and struggles, the polymer business was finally gaining traction, though margins remained a concern.

Recognition also came from unexpected quarters. In 2022, it was ranked #61 on Fortune Next 500 list under the iron and steel category, by Fortune India. For a company that had operated in relative obscurity for decades, this was validation of their transformation into a serious player in India Inc.

VIII. Modern Era & Global Ambitions (2023–Present)

The year 2025 would prove to be Skipper's most triumphant yet. The company produces transmission towers, monopoles, power distribution poles, telecom towers, railway structures, and solar mounting structures. It is a leading manufacturer of Transmission and Distribution (T&D) structures, ranking among the top 10 worldwide. The segment's revenue increased by 69% YoY in 9M FY25.

The numbers were staggering. Revenue increased to Rs 46,245 million against Rs 32,820 million, registering a stupendous growth of 41%. This wasn't just organic growth—it was the result of years of capability building finally meeting a massive market opportunity.

But the headline that sent the stock soaring was buried in the management commentary. I'm especially proud to announce our first major pole supply order from the USA, which is a significant breakthrough and opens new growth avenues in North America—a priority geography under our global expansion strategy, announced Devesh Bansal, Director of Skipper Limited.

Breaking into the US market was the holy grail for Indian transmission tower companies. The market was massive, quality standards were stringent, and competition included global giants. That Skipper had cracked this code from their base in Kolkata was remarkable.

The digital transformation was equally impressive. The implementation of SAP S/4HANA RISE is progressing well. This upgrade will bring end-to-end visibility, operational agility, and scalability to support our ambitious growth journey. For a company that had started with handwritten ledgers, this was a complete metamorphosis.

Another strategic milestone was achieved: A particularly exciting development this year is our entry into the Substation EPC segment, marked by the receipt of our first order. Substations are where transmission lines converge and power is transformed—complex projects requiring sophisticated project management. This diversification into EPC was moving Skipper up the value chain.

The order book told its own story of success. Our closing order book at ₹74,584 million reflects our continued market dominance and customer trust. The visibility this provided was crucial—investors could see revenue for the next 18-24 months, lending confidence to the growth story.

The global footprint had expanded dramatically. The company now exports across continents such as Latin America, Europe, and Africa and is spread across 65+ countries. From Kolkata to Colombia, from Bengal to Brazil—Skipper's towers were carrying electricity across the world.

IX. Playbook: Business & Investing Lessons

Skipper's journey from a steel trading firm to a global infrastructure player offers a masterclass in industrial transformation. But what are the replicable lessons from this four-decade saga?

The Art of Industrial Pivots

Skipper executed not one but three major pivots—from trading to manufacturing, from telecom to power transmission, and from pure B2B to partial B2C with polymer pipes. Each pivot was timed to catch a sectoral upturn but executed while the core business was still strong. They never abandoned the previous business while building the new one, creating a portfolio effect that cushioned downturns.

Building Moats Through Certifications

In infrastructure, approvals are everything. PGCIL certification, international quality standards, testing capabilities—these aren't just operational requirements but competitive moats. Once Skipper was approved for 800kV towers, new entrants faced years of qualification processes to compete. The massive testing station built in 2020 extended this moat to 1200kV specifications.

The Partnership Paradox

Rather than going alone, Skipper consistently partnered with global leaders—Ramboll for design, Sekisui for CPVC technology, Metzerplas for irrigation. These partnerships provided instant credibility, technology transfer, and market access. Yet Skipper retained manufacturing and execution control, preventing partners from forward-integrating into their market.

Capital Intensity as Competitive Advantage

The massive galvanizing facility, the testing station, multiple manufacturing plants—these required hundreds of crores in investment. But in infrastructure, capital intensity creates barriers to entry. Customers prefer vendors who have already made these investments, creating a virtuous cycle where scale begets scale.

Balancing Focus vs. Diversification

The polymer pipes diversification remains controversial. Company has low interest coverage ratio. Company has a low return on equity of 9.72% over last 3 years. These metrics partially reflect the capital allocated to the polymer business that hasn't generated adequate returns. Yet, the diversification also provided stability during transmission sector downturns and is now contributing meaningful revenues.

Timing Market Cycles

Every major expansion coincided with a government infrastructure push—telecom liberalization in the 1990s, Power Grid expansion in the 2000s, renewable energy integration in the 2020s. This wasn't luck but pattern recognition, understanding that infrastructure is inherently cyclical and positioning ahead of the curve.

The Promoter Edge

Promoter Holding: 66.5%. This high promoter stake aligned long-term thinking with execution. The family could make decade-long bets on sectors, accept lower returns during building phases, and resist quarterly earnings pressure that might have forced premature exits from investments.

X. Analysis & Bear vs. Bull Case

Bull Case: The Infrastructure Supercycle

The optimists see Skipper at the beginning of a multi-decade infrastructure supercycle. India's ambitious renewable energy targets—500GW by 2030—require massive transmission infrastructure. The CEA projecting Rs 9.15 lakh crore of investments in transmission infrastructure by 2032. Skipper, as India's largest manufacturer, is perfectly positioned.

The US breakthrough changes the narrative completely. If Skipper can compete in the world's most demanding market, it validates their quality and cost competitiveness globally. The addressable market expands from $5 billion domestically to $50 billion globally.

We secured Rs 15,920 million in new orders during the quarter, bringing our FY25 order inflow to Rs 53,353 million, up 24% YoY. Our order book now stands at Rs 74,584 million, an all-time high. This order book provides visibility and confidence in sustained growth.

The digital transformation through SAP S/4HANA will improve margins through better working capital management, optimized procurement, and enhanced project execution. As operations become more efficient, the ROE concerns should ameliorate.

Bear Case: Structural Challenges Persist

The skeptics point to persistent financial metrics that concern investors. The low interest coverage ratio suggests vulnerability to rate cycles. The low return on equity of 9.72% over last 3 years indicates capital allocation challenges.

The polymer business, despite years of investment, remains subscale. In a branded consumer business, Skipper lacks the marketing muscle of established players. The economics of competing with Supreme Industries or Finolex in their strongholds remains questionable.

Infrastructure spending is inherently cyclical and politically driven. A change in government priorities, fiscal constraints, or global economic slowdown could quickly dry up orders. The high fixed cost base makes Skipper vulnerable during downturns.

Chinese competition looms large. While currently focused on their domestic market, Chinese manufacturers have massive scale advantages. If they turn attention to India or global markets where Skipper operates, pricing pressure could intensify.

The working capital intensity of the business model remains a challenge. Large projects require significant upfront investment, payments are often delayed, and any execution hiccup impacts cash flows disproportionately.

XI. Epilogue: The Future of Infrastructure

Standing at their Uluberia facility today, watching massive towers being galvanized for shipment to America, one wonders what Sadhu Ram Bansal would make of his legacy. The small trading firm he started in 1961 now powers electrical grids across continents.

India's energy transition presents an unprecedented opportunity. Renewable energy sources are inherently distributed—solar farms in Rajasthan, wind mills in Tamil Nadu, hydro projects in the Northeast. Connecting these to consumption centers requires exactly what Skipper manufactures: high-voltage transmission infrastructure. The grid of 2040 will look nothing like today's, and Skipper is positioning to build it.

The US entry could be transformative if executed well. The American grid needs massive upgrades—decades-old infrastructure, renewable integration challenges, resilience concerns from extreme weather events. An Indian company competing successfully here would shatter stereotypes about emerging market manufacturers.

Yet challenges remain real. The polymer business needs strategic clarity—double down with massive investment or exit to focus on the core. The balance sheet needs strengthening to fund the next phase of growth. The organization needs to evolve from a family-run enterprise to a professionally managed corporation while retaining entrepreneurial agility.

The recent announcement of substation EPC capabilities suggests management is thinking beyond products to solutions. The future Skipper might not just manufacture towers but design, build, and maintain entire transmission networks—a far more valuable proposition.

As India pursues its ambitious goal of net-zero emissions by 2070, companies like Skipper will be critical enablers. Every solar panel installed, every wind turbine erected, every electric vehicle charged will depend on transmission infrastructure. In that sense, Skipper isn't just building towers and poles—they're building the backbone of India's energy future.

The journey from Kolkata steel trader to global infrastructure player is remarkable. But perhaps the most remarkable chapter is yet to be written. With the US market opening up, digital transformation underway, and India's infrastructure spending accelerating, Skipper Limited stands at another inflection point. The choices made now will determine whether this becomes a $10 billion company powering the global energy transition or remains a solid but subscale player in a commoditizing industry.

The skipper has charted the course. The question is: how far can this ship sail?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube