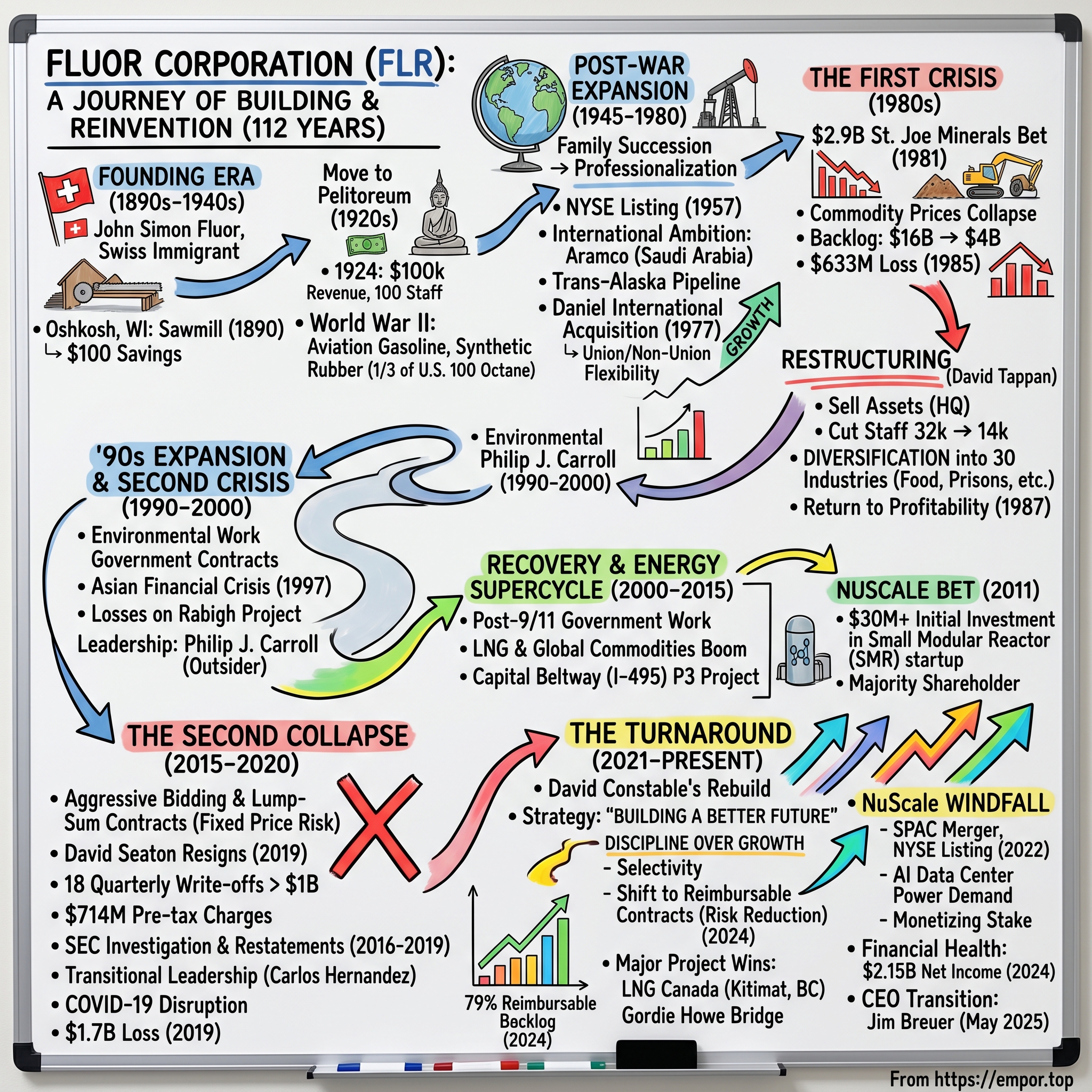

Fluor Corporation: Building the World's Megaprojects

Introduction: The Paradox of Permanence in a Volatile Industry

In July 2025, the LNG tanker Gaslog Glasgow pulled away from Kitimat, British Columbia, carrying Canada's first-ever export cargo of liquefied natural gas. Fluor Corporation announced that LNG Canada had successfully shipped the first liquefied natural gas export cargo from its newly-constructed facility. Since 2018, Fluor, and its joint venture partner, JGC Corporation, had provided critical engineering, procurement, fabrication management, construction and commissioning services to build the facility. The moment represented far more than a shipping milestone—it was validation for a company that, just five years earlier, had been trading below $4 per share and facing existential questions about its survival.

What does it take to survive 112 years in one of the most cyclical, risky, and capital-intensive businesses on earth—and how did this company nearly collapse twice, only to reinvent itself each time?

Fluor had revenue of $16.3 billion in 2024 and is ranked 257 among the Fortune 500 companies. With headquarters in Irving, Texas, Fluor has provided engineering, procurement and construction services for more than 110 years. The company stands as the largest publicly traded engineering and construction company in the Fortune 500 rankings, a survivor across world wars, oil shocks, financial crises, and an industry transformation that has bankrupted many of its peers.

Revenue for 2024 was $16.3 billion and net income attributable to Fluor was $2.1 billion, or $12.30 per diluted share, reflecting the deconsolidation and subsequent remeasurement of Fluor's investment in NuScale. But those numbers tell only part of the story. Full year new awards reached $15.1 billion, with 85% reimbursable. Ending backlog stood at $28.5 billion, 79% reimbursable. The company generated operating cash flow for 2024 of $828 million—the highest OCF generation since 2015.

The engineering, procurement, and construction (EPC) business model presents a fundamental paradox: it requires enormous capital, technical expertise, and organizational capability to execute projects that can stretch for a decade, yet operates on razor-thin margins where a single troubled project can wipe out years of profits. Fluor's journey through this paradox offers a masterclass in cyclical industry survival, capital allocation discipline, and the critical importance of knowing when to say no to attractive-looking work.

This is the story of a Swiss immigrant's garage workshop that became a global infrastructure titan, nearly destroyed itself twice through strategic overreach, and emerged from its latest crisis by fundamentally rethinking its approach to risk. Along the way, we'll examine how a $30 million investment in a small nuclear startup became worth billions—and why that hidden asset now represents one of the most intriguing value creation opportunities in industrial America.

The Immigrant Dream: Founding Era (1890–1940s)

From Wisconsin Sawmill to California Petroleum

In the 1880s, a young Swiss carpenter named John Simon Fluor arrived in America knowing only one English word: "Hello." Born in 1867, Fluor had gained engineering experience serving in the Swiss army, and like millions of immigrants in that era, he came pursuing a dream of opportunity in the New World.

Fluor Corporation's predecessor, Rudolph Fluor & Brother, was founded in 1890 by John Simon Fluor and his two brothers in Oshkosh, Wisconsin as a saw and paper mill. John Fluor acted as its president and contributed $100 in personal savings to help the business get started. The company was renamed Fluor Bros. Construction Co. in 1903.

Those $100 in personal savings—roughly $3,500 in today's dollars—represented the entire capital base for what would become a Fortune 500 enterprise. The early years in Wisconsin taught the Fluor brothers the fundamentals of industrial construction: precision engineering, material procurement, workforce management, and the relentless attention to cost control that separates profitable contractors from bankrupt ones.

In 1912 John Fluor moved to Santa Ana, California for health reasons without his brothers and founded Fluor Corporation out of his garage under the name Fluor Construction Company. The move to Southern California would prove transformative—not because of the region's pleasant climate, but because John Fluor arrived just as California was emerging as the center of American petroleum production.

Pivoting to Petroleum

The timing was remarkable. California's oil boom was accelerating, with the Signal Hill and Los Angeles Basin fields transforming the region into one of the world's leading oil producers. Fluor recognized that this emerging petroleum industry held enormous potential, so in 1921 he began to tailor his engineering and construction work to meet the demands of the field.

Fluor's first projects were in constructing and grading roads, but by the 1920s it was known for building public facilities, industrial complexes and serving a growing California oil and gas industry. It started building office and meter manufacturing facilities for the Southern California Gas Company in 1915, as well as a compressor station for the Industrial Fuel Supply Company in 1919. Fluor built the first "Buddha Tower" in 1921 in Signal Hill, California, for the Industrial Fuel Supply Company.

The "Buddha Tower"—an innovative oil processing structure—marked Fluor's transition from general contractor to specialized energy infrastructure builder. This early specialization established a pattern that would define the company for the next century: identifying emerging industrial needs, developing technical expertise ahead of competitors, and building deep relationships with major energy companies.

By 1924, the business had grown from that $100 garage operation to annual revenues of $100,000 ($1.56 million in 2021 dollars) and a staff of 100 employees. In 1929, the company re-incorporated as Fluor Corporation, establishing the corporate structure that would carry it through the Great Depression.

Wartime Transformation

The Depression years nearly destroyed Fluor, as construction activity across California collapsed. But the company survived by maintaining its technical capabilities and client relationships, positioning itself for the wartime industrial mobilization that would transform American manufacturing.

The outbreak of World War II presented both unprecedented challenges and opportunities. The Allied war effort required massive quantities of high-octane aviation gasoline and synthetic rubber—materials that required sophisticated refinery and chemical plant construction. Early in the war years, Fluor had only a few months to develop facilities and personnel capable of producing these strategic materials.

Fluor rose to the challenge spectacularly. Between 1940 and 1943, Fluor facilities produced more than a third of all 100 percent octane gasoline in the United States—fuel that powered the Allied bomber fleets that would ultimately win the air war over Europe and the Pacific. Sinclair Oil Company selected Fluor to design and build a sulfuric alkylation plant at its California refinery, demonstrating the company's growing reputation for technical excellence in complex chemical processes.

The war years established Fluor as far more than a regional contractor. The company had proven it could mobilize rapidly, execute complex projects under extreme time pressure, and deliver mission-critical infrastructure at scale. When the war ended, Fluor emerged with enhanced capabilities, expanded client relationships, and a reputation that would fuel decades of growth.

Building the Hydrocarbon Age: Post-War Expansion (1945–1980)

Family Succession and International Ambition

John Simon Fluor died in 1944, having transformed his $100 garage workshop into a significant engineering enterprise. He was succeeded by his son Peter Fluor, who died just three years later. Peter was followed by Shirley Meserve (1947) and Donald Darnell (1949), then John Simon "Si" Fluor Jr.

The rapid succession of leadership highlighted both the challenges of family business continuity and the strength of the organization Fluor had built. Despite the turnover at the top, the company's technical capabilities and client relationships remained intact, enabling continued growth through the post-war boom.

In 1946 a contract for a grassroots refinery in Montana solidified Fluor's reputation as a refinery engineering firm and helped lead to an assignment to expand the Aramco facilities in Saudi Arabia.

That Aramco assignment marked Fluor's entry into international markets—a transformation that would define the company's next four decades. The Middle East was becoming the center of global oil production, and Fluor positioned itself as the engineering partner of choice for the American oil majors developing the region's vast reserves.

Professionalization and Stock Market Listing

By the 1950s, the marketplace was short of workers with the skills Fluor demanded. The company responded by establishing in-house training and college tuition reimbursement programs—both of which remain in use today. This investment in human capital reflected a sophisticated understanding that engineering and construction firms ultimately sell expertise, and that expertise resides in people.

The company's stock began trading over the counter in 1950, and in 1957, Fluor's stock began trading on the New York and Pacific exchanges. The public listing provided capital for expansion and created liquidity for family shareholders, while imposing the discipline of public market scrutiny.

Diversification into New Markets

Fluor diversified its business more extensively in 1967, when five companies were merged into a division called Coral Drilling and it started a deep-water oil exploration business in Houston called Deep Oil Technology. In 1968 the company created Fluor Ocean Services, an umbrella management company headquartered in Houston. Fluor's largest offshore drilling acquisition occurred in 1969, when the company took over the Pike Corporation of America. Fluor's involvement with the mining and metals industry also began in 1969.

Building on a record of innovation in oil and gas, Fluor diversified into offshore drilling in 1967. The company then went on to achieve a number of industry milestones, including the design and production of the first tension leg platform, the first deepwater port in the U.S., and the world's largest offshore crude oil and LPG terminals at Ju'aymah in Saudi Arabia.

The Trans-Alaska Pipeline and Middle East Dominance

The 1970s represented Fluor's golden age. The Arab oil embargo of 1973 triggered a massive wave of energy infrastructure investment as Western nations sought to develop domestic supplies and diversify away from Middle Eastern dependence. Fluor was perfectly positioned to capture this demand.

To support the Trans-Alaska Pipeline—one of the largest private construction projects in American history—Fluor designed the world's largest floating berth at the time and the largest single prefabricated component of the pipeline system. The company's innovative floating deck design for supertankers showcased its engineering capabilities at the cutting edge of what was technically possible.

In 1977, Fluor acquired Daniel International Corporation. Daniel was an industrial contractor with revenues over $1 billion a year that in many ways complemented the Fluor portfolio. Daniel's operations were primarily based in the United States, whereas Fluor worked largely overseas. The two had different client lists and were involved in different kinds of projects. Most Fluor employees were members of labor unions, but most of Daniel's employees were not. Despite, and in some cases because of, their differences, the two companies integrated efficiently.

The Daniel acquisition was strategically brilliant. Fluor's business had become predominantly international, while Daniel International's $1 billion construction business was mostly domestic. The acquisition allowed the company to use union labor at Fluor, or non-union labor at Daniel, for each client—providing flexibility that competitors couldn't match. By the end of the decade, Fluor was being named by Engineering News as the largest construction and engineering company in the United States.

The First Crisis: Boom, Bust & Reinvention (1980s)

The Fateful Diversification Bet

The Fluor Corporation entered the 1980's as one of the world's premier builders of large and complex projects. However, the company's $2.2 billion purchase of St. Joe Minerals in 1981 proved to be a devastatingly costly move. Combined with a highly volatile energy market and falling oil prices, the acquisition brought Fluor serious financial trouble.

Fluor made a $2.9 billion acquisition of a zinc, gold, lead and coal mining operation, St. Joe Minerals, in 1981 after a bidding competition for the business with Seagram. By the 1980s, Fluor's primary business was building large refineries, petrochemical plants, oil pipelines and other facilities for the gas and oil industry, especially in the Middle East. By 1981, Fluor's staff had grown to 29,000 and revenue, backlog, and profits had each increased more than 30 percent over the prior year.

St. Joe Minerals Corporation was an American mining company. It was the United States largest producer of lead and zinc at the time of its merger with Fluor Corporation in 1981.

The logic seemed sound: Fluor had extensive experience building mining infrastructure, commodity prices were near historic highs, and vertical integration into natural resources would provide a hedge against the cyclicality of the construction business. The bidding war with Seagram pushed the price to $2.73-2.9 billion—a premium that assumed commodity prices would remain elevated indefinitely.

In 1981 with metal prices running high Fluor Corporation outbid Seagrams to acquire the company. Shortly after the acquisition metal prices collapsed.

The Spectacular Collapse

The timing couldn't have been worse. Within months of closing the St. Joe acquisition, metal prices collapsed. Simultaneously, the oil and gas industry that Fluor served entered a worldwide recession as oil prices declined from their post-1979 peaks.

However, by 1984 the mining operation was causing heavy losses and the oil and gas industry Fluor served was in a worldwide recession due to declining oil prices. From 1981 to 1984, Fluor's backlog went from $16 billion to $4 billion. In 1985 it reported $633 million in losses.

The numbers were staggering. In just three years, Fluor's backlog—the forward indicator of future work—collapsed by 75%. The 1985 loss of $633 million represented a complete reversal from the profitable growth trajectory of the late 1970s. The company was staring at potential bankruptcy.

Restructuring Under David Tappan

David Tappan took Bob Fluor's place as CEO in 1984 after Bob died from cancer and led a difficult restructuring. The company sold $750 million in assets, including Fluor's headquarters in Irvine, in order to pay $1 billion in debt. Staff were reduced from 32,000 to 14,000.

Selling the headquarters—a decision that would have been unthinkable just years earlier—signaled the severity of the crisis and management's willingness to take radical action. The workforce cuts, reducing staff by more than half, were brutal but necessary to right-size the organization for the dramatically reduced demand environment.

In order to lessen its dependence on the oil market and to develop a more diversified clientele, Tappan decided in 1986 to merge Daniel International with Fluor Engineers and Constructors to create Fluor Daniel Inc.

During the restructuring, Fluor's core construction and engineering work was diversified into 30 industries including food, paper manufacturers, prisons and others to reduce its vulnerability to market changes in the oil and gas market. Fluor Engineers, Inc. and Daniel International were merged, forming Fluor Daniel. By 1987, Fluor had returned to profitability with $26.6 million in profits and $108.5 million by 1989. By the end of the restructuring, Fluor had three major divisions: Fluor Daniel, Fluor Construction International and St. Joe Minerals Corp.

The lessons from the 1980s crisis were clear: commodity diversification is dangerous for a services firm, the construction business is inherently cyclical and requires capital discipline, and concentration in any single end market creates existential risk. These lessons would be tested—and partially forgotten—in the decades to come.

The '90s Expansion & Second Crisis (1990–2000)

Service Diversification and Environmental Work

The 1990s brought both recovery and new challenges. In the 1990s, Fluor introduced new services like equipment rentals and staffing. Nuclear waste cleanup projects and other environmental work became a significant portion of Fluor's revenues, reflecting both new regulatory requirements and Fluor's ability to apply its technical capabilities to emerging markets.

The company also did projects related to the Manhattan Project legacy sites, rebuilding after the Iraq War, recovering from Hurricane Katrina and building the Trans-Alaska Pipeline System. These government and crisis-response contracts provided more stable revenue streams than purely commercial construction work.

That same year, IT Group purchased a 54 percent interest in Fluor Daniel GTI, Fluor's environmental division, for $36.3 million. Two years later, the coal mining operation under the A.T. Massey Coal Co. name (part of St. Joe) was spun off into its own business.

The gradual exit from the St. Joe mining assets represented a tacit acknowledgment that the 1981 diversification had been a strategic error. The Massey Coal spinoff would eventually become a significant independent coal producer before its own troubled history.

The Asian Financial Crisis Blow

In 1997, Fluor's revenues fell almost 50 percent, in part due to the Asian financial crisis and a decrease in overseas business. The crisis also exposed execution problems that had been masked by favorable market conditions.

Additionally, Fluor suffered losses from an over-budget power plant project in Rabigh, Saudi Arabia. Fluor was a sub-contractor to General Electric for the project. Fluor's subsidiaries sued GE alleging that it misrepresented the complexity of the project. The litigation highlighted a recurring challenge in the EPC industry: the difficulty of accurately estimating costs and schedules for first-of-a-kind or highly complex projects.

Leadership Transition

In January 1998 McCraw (age 63) resigned after being diagnosed with bladder cancer and was replaced by former Shell President, Philip J. Carroll.

Carroll's appointment was notable as the first outsider named chairman in company history. The decision to break from tradition signaled the board's recognition that the company needed fresh perspective after years of underperformance. In 1999, nearly 5,000 workers were laid off from Fluor Daniel and 15 offices were closed. Fluor Daniel was restructured into four business groups.

In 2001, Fluor's four primary subsidiaries were consolidated into a single Fluor Corporation. In 2002 Alan Boeckmann was appointed as the CEO, followed by David Seaton in 2011.

Recovery & Rise: The Energy Supercycle (2000–2015)

Government Work Expansion Post-9/11

The September 11 attacks and subsequent U.S. military operations in Afghanistan and Iraq created significant demand for Fluor's government services capabilities. The company's experience with Department of Energy sites, military base construction, and logistics support positioned it well to capture contracts supporting the global war on terror.

The LNG and Global Commodities Boom

The 2000s brought what many analysts called the "super-cycle" in commodities—a sustained period of elevated prices driven by China's industrialization and urbanization. For Fluor, this meant a resurgence in demand for the large-scale energy and mining infrastructure projects that represented its core capabilities.

For over 50 years, Fluor has designed, built and validated more than 1,000 life sciences projects, ranging from pilot plants and labs to critical commercial manufacturing facilities. Clients include developers and producers of drugs, biotherapeutics, vaccines and supplements for humans and animals. Fluor's extensive experience in CGMP facility design has resulted in a success rate of 100% in compliant design and construction.

Transportation Infrastructure Push

The mid-2000s marked Fluor's aggressive expansion into transportation infrastructure through innovative public-private partnerships.

Capital Beltway Express (CBE) LLC, a concession formed by Fluor and Transurban (USA), signed a Comprehensive Development Agreement with Virginia Department of Transportation (VDOT) in 2007 to design, construct, finance and operate a new EXPRESS Lanes system along a 14-mile segment of I-495 (Capital Beltway.) The project was a public-private partnership (P3) between VDOT and Fluor-Transurban. The Virginia Department of Rail and Public Transportation (DRPT) played an active role in the project that expanded public transportation in the corridor. CBE contracted the Fluor-Lane team for the design-build portion of the project. The Fluor-Lane design-build team opened 11 major interchanges and bridges along the 14-mile project footprint. The 1,100 member Fluor-Lane and subcontractor teams worked two shifts, often seven days a week replacing bridges, overpasses and adding four new lanes to the Beltway.

The Capital Beltway (I-495) EXPRESS lanes expansion completed ahead of schedule in November 2012. The project was recognized for creating business opportunities for minority subcontractors. The National Association of Minority Contractors Washington Area Chapter cited Fluor-Lane's "vigorous outreach" and noteworthy engagement of more than 185 minority contractors on this important project. Fluor-Lane had a significant impact in developing local transportation contractors to take on future work in the region. The I-495 EXPRESS Lanes project achieved 5 million safe work hours without a lost-time incident in September 2012.

The NuScale Bet—Planting Seeds for the Future

In 2011, Fluor made what appeared to be a modest investment that would eventually prove transformational.

Fluor Corporation announced that the company had committed to making an investment exceeding $30 million in NuScale Power LLC., an Oregon-based small modular reactor (SMR) technology company. The announcement was made in Washington D.C. at the National Press Club by Fluor and NuScale executives with key members of the U.S. House of Representatives along with industry and regulatory leaders in attendance. As part of its investment, Fluor has purchased the company's shares that had previously been in U.S. Securities & Exchange Commission receivership and has become NuScale's majority shareholder. Going forward, NuScale will continue to operate as an independent company. Additionally, Fluor and NuScale have entered into a separate contractual arrangement whereby Fluor will provide certain services to NuScale as well as have exclusive rights to provide engineering and construction services for future NuScale SMR facilities.

In October 2011, Fluor Corporation acquired a majority interest in NuScale for $3.5 million and promised almost $30 million in working capital. According to The Energy Daily, Fluor's investment saved the company, which had been "financially marooned" by its prior investor.

The investment thesis was compelling but speculative: small modular reactors could revolutionize nuclear power by reducing construction risk, enabling factory fabrication, and opening nuclear energy to a broader range of customers. But in 2011, with natural gas prices collapsing due to the shale revolution, nuclear power of any kind seemed uneconomic.

In December 2021, the Fluor Corporation reported that it had invested over $600 million in NuScale since 2011, and that NuScale was expected to go public in 2022 with Fluor owning about 60% of the stock.

The NuScale investment demonstrated patient capital allocation—a willingness to fund long-term technology development that might not pay off for decades, if ever. It was precisely the kind of strategic bet that public companies often struggle to make under quarterly earnings pressure.

The Second Collapse: 2015–2020 Crisis

The Industry-Wide Problem: Aggressive Bidding and Lump-Sum Contracts

The seeds of Fluor's second existential crisis were planted during the good times. Historically, the EPC market was a highly competitive landscape that led to heavy risk taking, where growth was often prioritized over discipline and profitability. For Fluor, as well as much of the industry, this led to management aggressively increasing their backlog of higher-risk lump-sum and guaranteed minimum contracts, leading to execution risks, thin margins and cost overruns.

The fundamental problem was contract structure. In cost-reimbursable contracts, the contractor is paid for actual costs plus a fee—if costs overrun, the client bears most of the risk. In lump-sum contracts, the contractor commits to a fixed price and absorbs all cost overruns. When projects go well, lump-sum contracts can be highly profitable. When they go poorly, losses can be catastrophic.

During the energy supercycle, competitive pressure pushed contractors to accept lump-sum terms on increasingly complex projects. The implicit assumption was that careful estimation, experienced project managers, and robust processes would contain execution risk. That assumption proved dangerously optimistic.

The Fall of David Seaton

In what company insiders and observers say was unexpected, Fluor Corp. CEO David Seaton resigned on May 1 and left the company board of directors, just before the firm's release of first-quarter results that included a $58-million loss, compared with an $18-million loss for the same period a year ago. Three-month revenue for the firm fell 13% to $4.19 billion, below analysts' expectation of $4.81 billion, with all of Fluor's corporate segments also missing consensus expectations on revenue.

In short, poor execution -- years of it. Cost overruns and bad estimates have been building since 2016, and in the past three years, Fluor has taken 18 quarterly write-offs totaling more than $1 billion.

Seaton, 57, is a 34-year Fluor veteran who had been CEO since 2011. Stepping down now "was not what he wanted," according to one industry executive.

The pattern of write-offs was particularly damaging to investor confidence. Quarter after quarter, management would announce charges on troubled projects, eroding the credibility of their forecasts and raising questions about what other problems lurked in the backlog.

"These are two projects out of 1,000 that we're doing, that we are performing miserably on," Seaton told analysts at the time. "I'm really distraught over the fact we've had these two projects deliver this kind of performance, because it overshadows all the good stuff that's out there." The company was doing "a lot of soul searching," he said, and the recent spate of disappointing analyst calls "have taken years off my life."

Shares fell 28% early on May 2 to $29.60, the biggest decline since at least December 2000, before recovering. Fluor lowered its 2019 earnings outlook by $1 per share. With charges taken on several problem energy projects not identified, Fluor's board named former CEO Alan Boeckmann, 70, as executive chairman.

SEC Investigation and Federal Scrutiny

The financial problems attracted regulatory attention.

In disclosing fiscal year 2019 and Q4 2019 financial results, Fluor Corp. announced that the SEC is conducting an investigation of its past accounting and financial reporting, and has requested documents and information related to projects for which the company recorded charges in the second quarter of 2019. Due to the investigation, the company did not expect to file conclusive full-year financial statements until the end of the month.

According to the SEC's order, the accounting errors on one project caused Fluor to materially overstate its net earnings by as much as 37 percent from the company's fiscal year 2016 through the first quarter of its fiscal year 2019. In addition, the delayed loss recognition on the second project caused Fluor to overstate its net earnings by 22 percent in the second quarter of 2018. As a result, Fluor materially misstated the financial statements included in its periodic filings with the Commission.

In August 2019, Fluor announced $714 million in pre-tax charges stemming from an "operational and strategic review" of sixteen projects. These included a project requiring Fluor to validate and complete the design and to build a one-of-a-kind U.S. Army facility for manufacturing nitrocellulose, an ammunition propellant ("Radford" or the "Radford Project"), and a project requiring Fluor to design and build a Floating Production Storage and Offloading ("FPSO") facility for delivery to the Penguins oil and gas field located in the North Sea.

Prompted by the SEC staff's investigation, Fluor undertook an internal investigation in 2020 that identified material weaknesses in its internal control over financial reporting and material errors in its financial statements, and resulted in Fluor restating its annual and quarterly financial statements for its fiscal year 2016 through the third quarter of 2019. The material weaknesses identified in the Restatement were attributable to control failures associated with the Radford and Penguins projects, which resulted in material errors.

The SEC investigation was eventually resolved in September 2023. The Securities and Exchange Commission announced that Irving, Texas-based Fluor Corporation would pay $14.5 million to settle charges stemming from the company's improper accounting on two large-scale, fixed-price construction projects. Without admitting or denying the SEC's findings, Fluor consented to cease and desist from committing or causing future violations and to pay a civil money penalty of $14.5 million. Per the order, Fluor's remedial acts and cooperation factored into the SEC's settlement decision.

Carlos Hernandez's Transitional Leadership

Fluor Corporation announced that David T. Seaton had stepped down as CEO and would no longer serve as a member of the board of directors, effective May 1, 2019. He would remain with the company through the transition and to assist management as requested. Alan L. Boeckmann was named executive chairman of the board. Carlos M. Hernandez, previously responsible for law, risk and compliance, would serve as the interim CEO until a permanent replacement was identified.

Mr. Hernandez had been chief legal officer and secretary of Fluor Corporation since 2007. Prior to joining the company, he was general counsel and secretary of ArcelorMittal USA, Inc. from 2005 to 2007. He holds a bachelor of science degree in civil engineering from Purdue University and a juris doctorate from the University of Miami School of Law.

Hernandez's unusual background—a civil engineer who became a corporate lawyer—proved valuable in navigating the legal and regulatory challenges facing the company. Boeckmann lauded Hernandez for "setting Fluor on the path to restore confidence in our financial reporting." He guided the 2019 strategic review, focusing on strengthening the company's balance sheet and establishing a more transparent culture.

COVID-19 Adds Insult to Injury

Just as Fluor was beginning to stabilize from its operational crisis, the COVID-19 pandemic struck. Construction projects worldwide faced shutdowns, supply chain disruptions, and labor shortages. Then in September 2020, Fluor announced that it had suspended its guidance for 2020, due to "a significant shift in end markets in 2020 driven by volatility in commodity prices and the global disruption from the COVID-19 pandemic."

For the full year of 2019, Fluor lost $1.7 billion.

The combination of operational failures, regulatory scrutiny, and pandemic disruption pushed Fluor's stock to historic lows. For investors who had bought into Fluor during the energy supercycle at prices above $80 per share, the decline to below $4 represented a 95%+ loss—a near-total destruction of value.

The Turnaround: David Constable's Rebuild (2021–Present)

The Third CEO in Two Years

It had been a troubled two years for one of the largest engineering and construction firms in the country. In May 2019, CEO David Seaton abruptly resigned after presiding over 18 quarterly write-offs totaling more than $1 billion.

David E. Constable is Executive Chairman of Fluor Corporation and has been a member of the Board of Directors since 2019. He was appointed Chairman of the Board in May 2022 and also chairs the Executive Committee. David is a versatile executive with significant international experience and a proven track record of driving growth and value creation across multiple industries. He served as Fluor's Chief Executive Officer from January 2021 through April 2025. He is also former Chief Executive Officer of Sasol Ltd from May 2011 to July 2016, where he executed a comprehensive change program and implemented a new operating model focused on enhancing growth across the organization. He brings 43 years of insight to Fluor's business, strategy and operations, having held a variety of leadership roles within Fluor from 1982 to 2011, including group president roles leading Fluor's Project Operations, Power and Operations and Maintenance businesses.

Constable's appointment represented an unusual executive journey—a Fluor lifer who had left to run another company and then returned to rescue his former employer. His deep knowledge of Fluor's operations, combined with his external experience at Sasol, positioned him uniquely to diagnose and address the company's problems.

The New Strategy: Discipline Over Growth

When Constable introduced the 'building a better future' strategy in January 2021, Fluor was at a turning point. Facing uncertainty, the company was determined to rebuild a stronger company by reinforcing financial discipline, lowering its risk profile, being selective with its project pursuits and rebuilding trust with its clients, shareholders and employees.

The strategic shift was fundamental: rather than pursuing backlog growth at any cost, Fluor would prioritize project selection discipline, contract structure quality, and execution excellence. The company announced intent to shift revenue by 2024 to about 70% in non-oil-and-gas sectors, with more push into life sciences, advanced manufacturing and technology, and government security.

"In 2023, we not only reached but surpassed a critical inflection point on our journey to solidifying our position as a technical solutions leader in the global engineering and construction industry," said David Constable, chairman and chief executive officer of Fluor.

The most critical metric was the shift to reimbursable contracts. Full year 2024 new awards reached $15.1 billion, with 85% reimbursable. Ending backlog stood at $28.5 billion, 79% reimbursable. This shift fundamentally reduced Fluor's risk profile—rather than betting on its ability to estimate costs accurately, the company would be paid for actual costs plus a fee.

Major Project Wins and Execution

The turnaround required more than financial engineering—it required demonstrating execution excellence on major projects.

Located on Canada's west coast, the LNG Canada facility benefits from access to abundant, low-cost natural gas and an ice-free harbor. The plant is the first-of-its-kind in Canada with an annual production capacity of up to 14 million tonnes of LNG. It positions Canada as a major supplier of lower carbon natural gas to global markets and will operate under a 40-year license. "This facility establishes the global benchmark for responsible LNG development," said Pierre Bechelany, President of Fluor's LNG & Power business. "Its design enables LNG Canada to produce LNG with some of the lowest emissions of any large-scale LNG facility in the world." JGC Fluor used an innovative modular fabrication approach to achieve significant schedule efficiencies.

In October 2018, LNG Canada made a final investment decision to build its liquefied natural gas (LNG) export facility in Kitimat, British Columbia, Canada. The project represented the largest energy investment in Canadian history.

More than 215 modules were delivered and set into place at the site from January 2022 to July 2023. The largest modules measured approximately 45 meters wide, 75 meters deep and 47 meters in height. The project also included the construction of the second largest LNG storage tank in the world, standing 56 meters high and 75 meters in diameter with a volume of more than 225,000 cubic meters. "Congratulations to our project team and the more than 35,000 workers who helped build the first phase of this facility meeting some of the world's most stringent standards for safety, sustainability and environmental protection."

On the infrastructure front, Fluor reported steady progress on several major projects, including the 94%-complete Gordie Howe International Bridge and the LAX Automated People Mover, both of which are on track for substantial completion in late 2025.

The Gordie Howe International Bridge project team confirmed a new completion and opening timeline. Construction completion is planned for September 2025 with the first vehicles expected to travel across the bridge that fall.

The NuScale Windfall

The 2011 NuScale investment—made during Fluor's darkest hours and maintained through the turnaround crisis—became one of the most valuable assets on Fluor's balance sheet.

In May 2022, NuScale completed a merger with the special-purpose acquisition company (SPAC), Spring Valley Acquisition Corp, raising $380 million of investment. NuScale Power Corporation then listed on the New York Stock Exchange.

The company's VOYGR power plant, which uses 50 MWe modules and scales to 12 modules (600 MWe), was the first SMR to be certified by the US Nuclear Regulatory Commission (2022). The newer 77 MWe module designs were submitted for NRC review on January 1, 2023, and approved May 29, 2025. As of 2025, NuScale Power Corporation is the only manufacturer in America to offer an NRC-approved SMR.

The surge in AI-related data center construction—and the massive power requirements those facilities demand—has driven extraordinary interest in small modular reactors as a carbon-free baseload power source. "The numbers are just astronomical for power demand for data centers," said Constable. "We've got 26,000 megawatts installed in the U.S. right now. They say 92,000 megawatts is required by the end of the decade. So, a big focus here on data centers, combined with power generation."

2024 quarter and full year results include equity method earnings of $2,105 million which include $2,221 million for deconsolidation and remeasurement of our investment in NuScale.

The NuScale stake has attracted activist investor attention. Activist investor Starboard sees a chance to unlock the value of Fluor's 39% stake in NuScale Power. On Oct. 21, 2025, Starboard announced a nearly 5% position in Fluor and stated their intention to unlock value from the company's approximately 39% holding in NuScale Power, which represents more than 60% of the company's market capitalization. As a result, Fluor's investment in NuScale has been highly lucrative – valued at approximately $4.3 billion ($3.4 billion post tax). That's more than half Fluor's current enterprise value. If you were to back out the NuScale stake from Fluor's valuation, then Fluor's enterprise value would drop to $3.3 billion, implying an extremely depressed discount.

In November 2025, Fluor Corporation and NuScale Power Corporation announced that they have reached an agreement regarding the conversion and monetization of Fluor's remaining stake in NuScale. Under the terms of the agreement, Fluor will convert its remaining Class B units into shares of Class A common stock and will promptly begin a structured monetization of shares. Fluor expects to complete the monetization of its stake by the end of the second quarter of 2026.

Current Financial Health and Leadership Transition

For the full year in 2024, Fluor earned $2.15 billion, a significant increase from $139 million in profits in 2023. Its revenue for 2024 hit $16.32 billion, up about 5% from $15.47 billion in 2023. The company's backlog fell to $28.48 billion in 2024, around a 3% drop from $29.44 billion a year ago.

General and administrative expenses for 2024 were $203 million compared to $232 million a year ago. This decrease is due to a reduction in performance-based compensation. Fluor's cash and marketable securities at the end of the year were $3.0 billion, up 14% from 2023.

David E. Constable was Chairman and Chief Executive Officer. Effective May 1, 2025, David transitioned to Executive Chairman of the Board. He first joined the company in 1982. James (Jim) Breuer has been Chief Operating Officer since August 2024.

COO Jim Breuer stepped into the CEO role effective May 1, taking over for David Constable.

Competitive Landscape and Industry Dynamics

The EPC Giants

Fluor's main competitors include KBR, Bechtel, Balfour Beatty, BrandSafway, Worley, McDermott International, STRABAG, Quanta Services, EMCOR Group, AECOM and Jacobs.

Fluor revenue is $16.3B. Among its competitors, the company with the highest revenue is Bechtel Corporation, $17.6B. The company with the lowest revenue is Black & Veatch, $3.2B.

Bechtel is a privately held construction and project management company with a strong presence in infrastructure, oil and gas, and nuclear sectors. Bechtel's extensive experience and global reach make it a formidable competitor for Fluor.

The competitive dynamics in EPC are shaped by several structural factors:

Scale and Technical Expertise: Major projects require contractors with the engineering depth, project management capability, and financial strength to execute work spanning many years and billions of dollars. Only a handful of firms globally can credibly bid on the largest projects.

Client Relationships: Long-term relationships with major energy companies, governments, and industrial clients provide competitive advantages through repeat business and preferential access to new opportunities.

Geographic Presence: Global operations require local capabilities, regulatory knowledge, and supply chain relationships across multiple continents.

Labor Arbitrage: The ability to mobilize workforces across geographies—using lower-cost labor for appropriate tasks while maintaining quality—provides cost advantages.

Risk Management: The ability to structure contracts appropriately and execute projects within budget and schedule separates winners from losers in this industry.

Porter's Five Forces Analysis

Threat of New Entrants (Low): The EPC industry has high barriers to entry including technical expertise requirements, client relationship development, and capital needs for bonding and insurance.

Bargaining Power of Suppliers (Moderate): Specialized equipment suppliers and skilled trades have some leverage, but large contractors can substitute and have significant purchasing power.

Bargaining Power of Buyers (Moderate to High): Major energy companies and governments represent concentrated buying power and can extract competitive pricing, particularly during industry downturns.

Threat of Substitutes (Low): There is no real substitute for engineering, procurement, and construction services for major industrial projects.

Industry Rivalry (High): Competition among major contractors is intense, particularly for marquee projects that enhance reputation and fill backlog.

Hamilton Helmer's 7 Powers Framework

Analyzing Fluor through Helmer's framework reveals both competitive strengths and vulnerabilities:

Scale Economies: Fluor benefits from scale in engineering resources, procurement leverage, and geographic coverage, though these advantages are shared with major competitors.

Network Effects: Limited in EPC, though relationships create some lock-in with long-term clients.

Counter-Positioning: Fluor's shift to reimbursable contracts and selective bidding represents a counter-positioning strategy against competitors still pursuing growth at any cost.

Switching Costs: Moderate for clients with ongoing programs, as switching contractors mid-project or mid-program involves significant costs and risks.

Branding: Strong reputation in energy and chemicals, with growing presence in life sciences and advanced manufacturing.

Cornered Resource: Deep technical expertise in LNG, nuclear services, and complex industrial projects provides differentiated capabilities.

Process Power: Superior project execution processes—if sustainable—would provide meaningful competitive advantage, though this has been Fluor's historical weakness.

Investment Considerations and Key Metrics

Bull Case

Strategic Transformation Success: The shift to reimbursable contracts has fundamentally de-risked the business model. With 79% of backlog now reimbursable, cost overruns no longer pose existential threats.

NuScale Optionality: The NuScale stake represents significant hidden value with potential upside if small modular reactors achieve commercial success in the data center and power generation markets.

Energy Transition Positioning: Fluor's capabilities in LNG, hydrogen, carbon capture, and nuclear position it to benefit from the energy transition regardless of which technologies ultimately prevail.

Data Center Opportunity: The explosive growth in AI-related data center construction creates demand for Fluor's engineering and construction capabilities, potentially at premium margins.

Execution Track Record Rebuilding: Successful completion of LNG Canada, Gordie Howe Bridge, and other major projects demonstrates restored execution capability.

Bear Case

Cyclical Exposure: The EPC industry remains deeply cyclical, and any sustained downturn in energy or industrial capital spending would pressure Fluor's revenues and margins.

Project Risk: Despite the shift to reimbursable contracts, execution risk remains inherent in the business. Fluor Corporation reported Q2 2025 results with significant challenges, leading to revised guidance. Revenue declined 6% year-over-year to $4.0 billion. The company's operational performance faced headwinds with adjusted EBITDA falling 42% to $96 million, impacted by $54 million in cost growth from three infrastructure projects. Q2 new awards totaled $1.8 billion, down 43% year-over-year, with backlog decreasing 13% to $28.2 billion. Due to client hesitation and economic uncertainty, Fluor revised its 2025 guidance downward.

NuScale Uncertainty: While NuScale represents significant value, SMR technology remains commercially unproven, and the path to profitability is uncertain.

Tariff and Trade Policy Risk: The global engineering and construction industry is currently facing significant challenges due to macroeconomic uncertainty and trade policy ambiguity. These factors are causing delays in decision-making for large capital projects, which could impact Fluor's ability to secure new contracts and maintain a robust project pipeline.

Competition: Bechtel, Jacobs, AECOM, and other major players compete aggressively for the same projects and clients.

Key Performance Indicators to Track

Backlog Quality (Reimbursable %): This metric captures the fundamental risk profile shift. Current target is 75%+ reimbursable; higher is better.

Book-to-Burn Ratio: New awards divided by revenue recognized. Ratios above 1.0x indicate growing backlog; ratios sustained above 1.0x signal healthy demand.

Consolidated Segment Margin: Operating profit as a percentage of revenue by segment. Improvements here indicate execution discipline and favorable contract mix.

Conclusion: Lessons from 112 Years of Survival

Fluor's journey from a Swiss immigrant's $100 investment to a Fortune 500 enterprise offers enduring lessons about business survival, capital allocation, and strategic discipline.

Lesson One: Diversification Is Not Always Diversification. The St. Joe Minerals acquisition of 1981 seemed like prudent diversification—extending from services into commodity ownership. In reality, it concentrated risk by creating exposure to commodity price cycles while distracting management from core competencies. True diversification comes from serving diverse end markets with consistent capabilities, not from acquiring fundamentally different businesses.

Lesson Two: Contract Structure Is Strategy. Fluor's near-death experience in 2019-2020 resulted directly from accumulating lump-sum contract risk during favorable market conditions. The shift to reimbursable contracts represents a fundamental strategic repositioning—accepting lower peak returns in exchange for dramatically reduced downside risk.

Lesson Three: Patient Capital Can Create Enormous Value. The NuScale investment—$30 million initially, grown to over $600 million in cumulative investment, now worth billions—demonstrates the power of patient capital allocation in supporting long-duration technology development.

Lesson Four: Crisis Creates Opportunity for Transformation. Both the 1980s crisis and the 2019-2020 crisis forced strategic reassessments that ultimately strengthened the company. Absent the pressure of near-collapse, neither the diversification into 30 industries under Tappan nor the shift to reimbursable contracts under Constable would likely have occurred.

"I could not be more pleased with the progress we have made over the past few years under our building a better future strategy," said David E. Constable. "As we wrap up the first chapter of this strategy, it's time to develop plans for the next chapter, including maximizing opportunities in growth markets, remaining laser focused on execution, generating consistent operating cash flow and continuing to develop the company's most important resource, our people."

For investors evaluating Fluor today, the key question is whether the strategic transformation is durable. The evidence suggests significant progress: the contract mix has shifted decisively toward reimbursable work, major projects are completing successfully, cash generation has improved, and the NuScale stake provides significant optionality. But the construction business remains inherently challenging, execution risk never disappears entirely, and cyclical pressures will eventually test the company's discipline.

What survives across 112 years is not any particular strategy or structure, but rather the organizational capability to recognize when change is necessary and execute that change effectively. John Simon Fluor built that capability when he pivoted from Wisconsin sawmills to California petroleum. David Tappan demonstrated it when he sold the headquarters and diversified into 30 industries. David Constable showed it when he returned to transform contract structures and rebuild execution discipline.

The next chapter of Fluor's story will be written by Jim Breuer and his team. If history is any guide, that chapter will include both opportunities and crises—and the company's survival will depend on the same adaptability that has carried it through the previous 112 years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube